taxation of incentive stock options – a case study

TRANSCRIPT

© 2015 Grant Thornton LLP. All rights reserved.

Taxation of stock

options and

restricted stock: The basics and beyond

© 2015 Grant Thornton LLP. All rights reserved. 2

What you'll learn:

Understand the tax rules

surrounding stock options and

restricted stock including:

1. Incentive stock options

[case study]

2. Nonqualified stock options

3. Restricted stock

© 2015 Grant Thornton LLP. All rights reserved. 3

Jane is an executive at Private Company.

Meet Jane Doe --

your new client

Jane is 58 years old and plans

to retire in 5 years.

Jane's stock ownership in

Private Company represents

about 75% of her net worth.

© 2015 Grant Thornton LLP | All rights reserved

– Incentive stock options

– Nonqualified stock options

– Restricted stock

Jane's compensation at Private Company includes:

© 2015 Grant Thornton LLP | All rights reserved

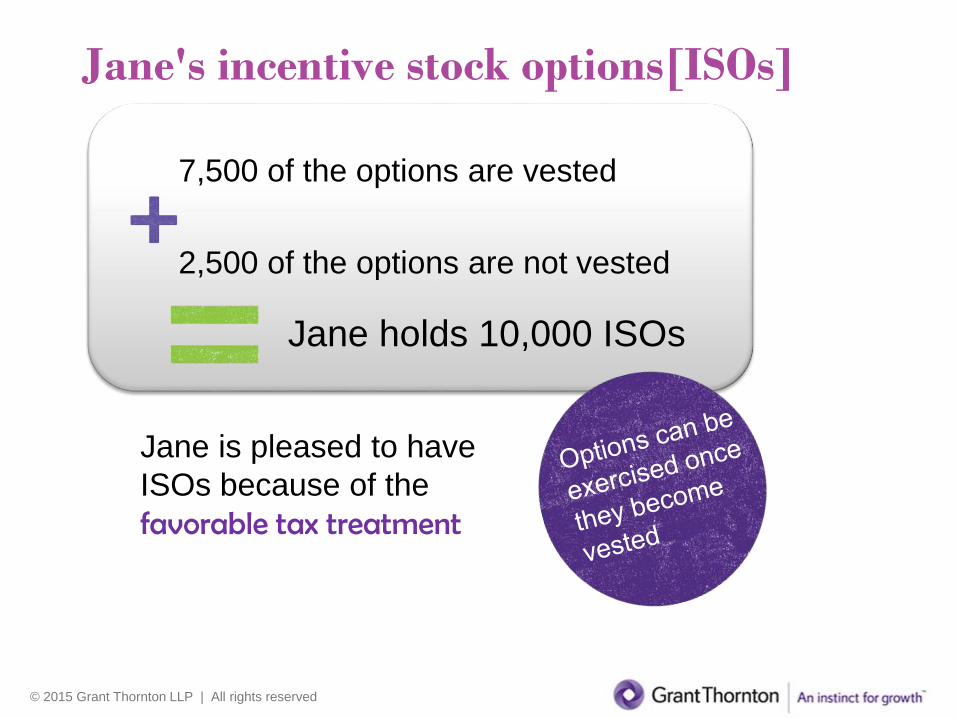

Jane's incentive stock options[ISOs]

7,500 of the options are vested

2,500 of the options are not vested

Jane holds 10,000 ISOs

Jane is pleased to have

ISOs because of the

favorable tax treatment

© 2015 Grant Thornton LLP | All rights reserved

• No income tax upon

grant

• No income tax upon

exercise

Why is Jane

so pleased to

have ISOs?

Sign up for the full webcast!

© 2015 Grant Thornton LLP | All rights reserved

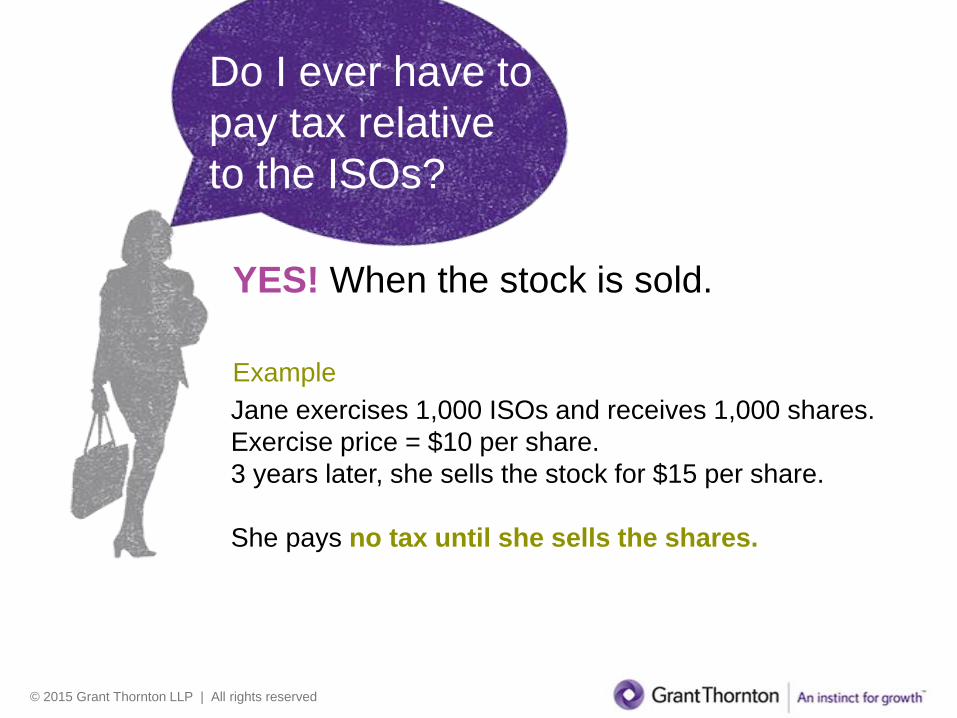

Do I ever have to

pay tax relative

to the ISOs?

YES! When the stock is sold.

Jane exercises 1,000 ISOs and receives 1,000 shares.

Exercise price = $10 per share.

3 years later, she sells the stock for $15 per share.

She pays no tax until she sells the shares.

Example

© 2015 Grant Thornton LLP | All rights reserved

What should Jane be aware of

regarding the stock she acquires

when exercising her ISOs

Disqualifying dispositions!

If stock is sold within

• 2 years after ISO is granted or

• 1 year after ISO is exercised

Learn more about disqualifying dispositions

© 2015 Grant Thornton LLP | All rights reserved

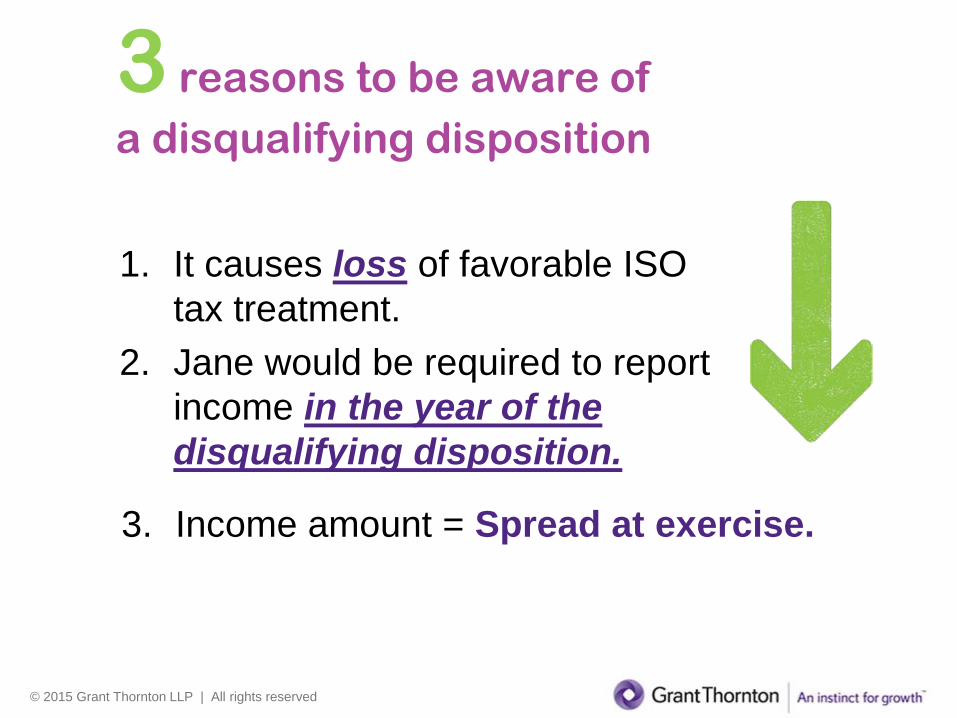

3 reasons to be aware of

a disqualifying disposition

1. It causes loss of favorable ISO

tax treatment.

2. Jane would be required to report

income in the year of the

disqualifying disposition.

3. Income amount = Spread at exercise.

© 2015 Grant Thornton LLP | All rights reserved

What is the tax treatment when

stock value declines after

exercise?

What is the ISO ordinary income calculation?

What may lead to an

alternative minimum tax?

Sign up for our webcast to

learn what happens to

Jane's stock value.

© 2015 Grant Thornton LLP. All rights reserved.

Taxation of stock

options and restricted

stock:

The basics and beyondThursday, Sept. 3, 2015

3 - 4:30 p.m. ET.

CPE credits: 1.5

© 2015 Grant Thornton LLP. All rights reserved. 12

Jeff Martin

Senior Manager

Compensation and Benefits Consulting

Washington National Tax Office

+1 202 521 1526

Eric Myszka

Manager

Compensation and Benefits

Consulting

Chicago

+1 312 602 8297

Rebecca Calvo

Manager

Compensation and Benefits

Consulting

Houston

+1 832 476 3778

Presenters