taxation of u.s. citizen physicians in canada

TRANSCRIPT

TAXATION OF U.S. CITIZEN PHYSICIANS IN CANADA PLANNING CONSIDERATIONS AND REQUIREMENTS

Presented by Hutcheson and Co. LLP and MD Financial Management

ABOUT US

Hutcheson & Co established in 1987

Full service tax and accounting solutions including cross border tax specialties

5 Partner firm with an excellent team of 23 staff members

Located in Victoria BC –Yates and Cook Street

TOPICS

Phil Hogan - Introduction

Ammo Baines –Canadian Tax Structures for Physicians

Brent England –US Tax Considerations and Requirements

Phil Hogan –Wrap Up and Questions

GENERAL US TAX REQUIREMENTS

US Citizens are required to file US 1040 income tax returns regardless of where they live

Other foreign financial and tax reporting is required

Canada-US tax treaty helps eliminate double taxation

Penalties can be high for non-compliance and late filing of specific tax forms

TAX FILING REQUIREMENTS FOR US PERSONS

Annual Filing Requirements T1

1040

FBAR (foreign bank account reporting – form 114)

Related treaty disclosures

Family Trust 3520-3520A

Private Corporate ownership 5471

Subpart F income (investment income)

COMMON CANADIAN TAX STRUCTURES

Considerations Legal

Health Professions Act

Section 43

College of the Physician and Surgeons of BC Bylaws

Part 6

Financial

Other

COMMON CANADIAN TAX STRUCTURES

Structures Shares held by physician

Add Spouse

Add Family Trust

Add Holding Company

Physician(shareholder)

OPCO

Voting Participating

SHARES HELD BY PHYSICIAN

COMMON CANADIAN TAX STRUCTURES

Add Spouse Voting shares for Physician

Non-voting shares for Spouse

Features participating vs non-participating

Physician(shareholder)

Spouse(shareholder)

OPCO

Non-VotingParticipating

Voting Non-Participating Non-Voting

Participating

ADD SPOUSE

COMMON CANADIAN TAX STRUCTURES

Add Family Trust Structure

Benefits versus “add spouse”

Now or later?

Physician(Shareholder)

OPCO

VotingNon-Participating

Non-VotingParticipating

Trust

Physician(Trustee)

Beneficiaries- Physician- Spouse- Children (over 18)

ADD FAMILY TRUST

COMMON CANADIAN TAX STRUCTURES

Add Holding Company Investment asset growth

Asset protection

Avoid subpart F inclusion (see final structure)

Physician(Trustee)

Trust

HOLDCO

Physician(Shareholder)

OPCO

Non-VotingParticipating

VotingParticipating

Beneficiaries- Physician- Spouse- Children (over 18)

VotingNon-participating

ADD HOLDING COMPANY

Non-VotingParticipating

VotingNon-participating

Physician US Citizen(Shareholder)

Spouse(Shareholder)

Trust

Trustee- 3rd Party- Spouse & 3rd Party- Spouse Only

OPCO HOLDCO

Non-VotingParticipating

VotingNon-participating

Beneficiaries- Spouse- Children (over 18)

ALTERNATIVE FOR US CITIZENS

Non-VotingParticipating

PLANNING CONSIDERATIONS

Corporation – PFIC vs CFC and subpart F PFIC Income

50/50 holding companies may be considered a PFIC

PFIC definition - 50% of inactive assets or 75% of inactive income

Punitive taxation

Controlled Foreign Company (CFC) and Subpart F Income (cannot be a PFIC)

Investment income in excess of dividends paid

Move investment assets to Holdco (not owned by US Citizen)

Income splitting Spouse and children

Ability to use lower marginal rates

PLANNING CONSIDERATIONS (CON’T)

Tax deferral Retain assets in corporation to defer higher personal tax rates

Sale of practice Capital gains exemption below $800,000

May not be easy to sell

AVOID PENALTIES!

Late FBAR (form 114) - $10,000

Late 5471 - $10,000

Late 3520A/3520 –Greater of $10,00 and % of trust property

T1135 - $25 a day to a max of $2,500 plus interest

Penalties on overdue tax payments

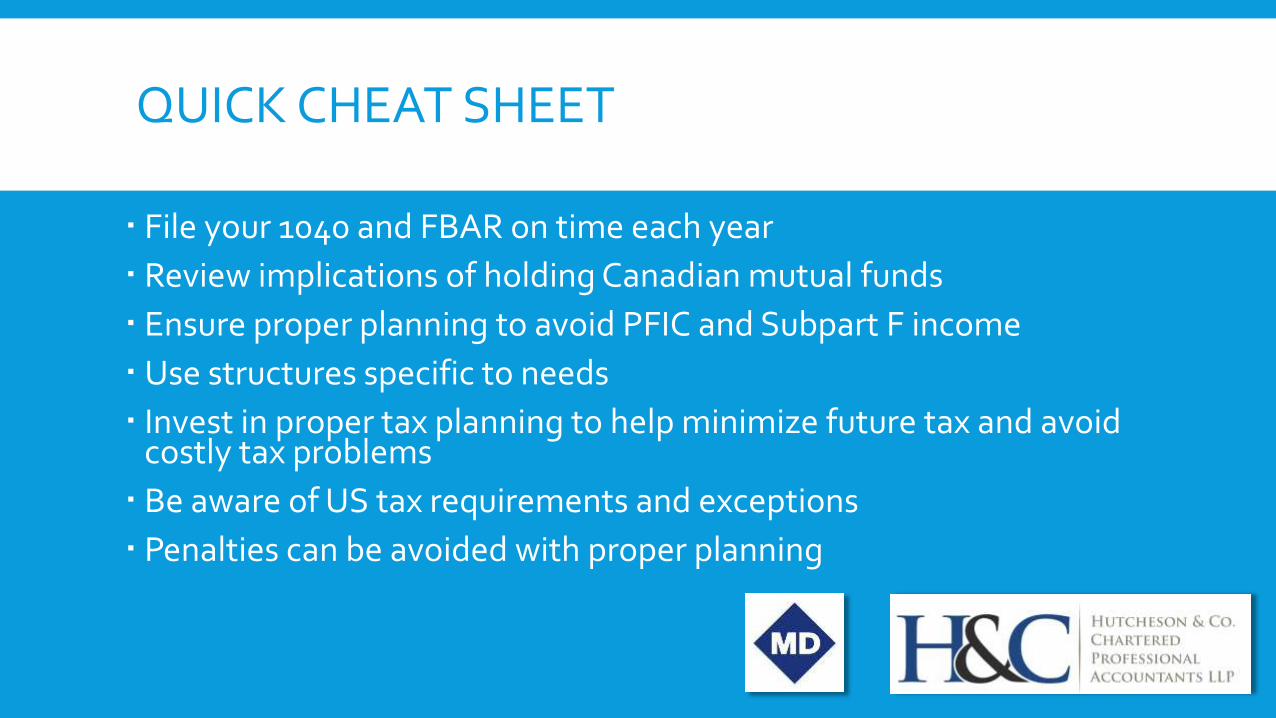

QUICK CHEAT SHEET

File your 1040 and FBAR on time each year

Review implications of holding Canadian mutual funds

Ensure proper planning to avoid PFIC and Subpart F income

Use structures specific to needs

Invest in proper tax planning to help minimize future tax and avoid costly tax problems

Be aware of US tax requirements and exceptions

Penalties can be avoided with proper planning

QUESTIONS?

CONTACT US

Name Email Phone Number

Brent England CPA, CA, CPA (Colorado)

[email protected] 250-381-2400

Phil Hogan CPA, CA, CPA (Colorado)

[email protected] 250-381-2400

Terry Dyer CPA, CA, RTRP [email protected] 250-381-2400

Ammo Baines BBA, CPA, CA [email protected] 250-381-2400