tby talks to dr. riad t. salameh, 2016 governor of banque ... · tby talks to dr. riad t. salameh,...

TRANSCRIPT

LEBANON2016

TBY talks to Dr. Riad T. Salameh, Governor of Banque du Liban, on efforts to ensure confidence in the economy.

The government is working to set into motion the energy program sought both by business and a growing population.

45 71 144 The tourism sector is enjoying a positive rebound despite the many challenges brought about by external factors.

£60

2016LEBANON

6 Year in review • Lebanon

10 DIPLOMACY 10 Standing firm • Review

12 HE Tammam Salam, Prime

Minister of Lebanon • Inside

perspective

14 Let’s be Franc • Focus: Lebanese-

French relations

15 HE François Hollande, President

of France • Guest speaker

16 HE Stéphane Dion, Foreign Affairs

Minister of Canada • Guest speaker

17 Deep pockets • Focus:

International Donors Conference in

London

18 HE Gebran Bassil, Minister of

Foreign Affairs and Emigrants •

Interview

19 Jamal Itani, Mayor of Beirut

• Interview

20 TBY awards • Lebanon

21 ECONOMY 21 Phoenix stirs • Review

22 Ziad Hayek, Secretary General,

Higher Council for Privatization (HCP)

• Column

27 HE Ali Hasan Khalil, Minister of

Finance • Interview

28 Alia Abbas, General Director of

the Ministry of Economy and Trade

• Interview

29 Nabil A. Itani, Chairman &

General Manager of IDAL

• Interview

30 Salim Zeenni, Chairman of the

American-Lebanese Chamber of

Commerce • Interview

32 Better together • B2B

33 Raya Haffar El Hassan,

Chairwoman of the Tripoli Special

Economic Zone (TSEZ) • Interview

34 The Tripoli transformation

• Focus: Tripoli economic free zone

36 Dr. Khater Abi Habib, Chairman of

the Board of Directors of Kafalat

• Interview

37 Mario Saradar, Chairman & CEO of

Saradar Group • Interview

38 New pegs • Focus: Lebanese

Exports

39 Eddy Cherfan, CEO of AC Holding

• Interview

40 Mazen Moussallem, Chairman of

Level 5 Holding • Interview

41 Why Lebanon? • Forum

42 FINANCE 42 About the money • Review:

Banking

44 Dr. Mayada Baydas, Executive

General Manager, Emkan Finance

• Column

45 Dr. Riad T. Salameh, Governor of

Banque du Liban • Interview

46 Dr. Makram Sader, Secretary

General of the Association of Banks

in Lebanon • Interview

47 Dr. Freddie Baz, Vice Chairman &

Group Strategy Director of Bank Audi

• Interview

48 Ghassan T. Assaf, Chairman &

General Manager of BBAC

• Interview

In partnership with:AMCHAM

50 Strength in finance • Forum

51 Anwar Jammal, Chairman & CEO

of Jammal Trust Bank (JTB)

• Interview

52 Islamic finance • B2B

54 Abdul Razzak Achour, Chairman &

General Manager of Fenicia Bank

• Interview

56 Stuck on stable • Focus: The

dollarization of the Lebanese

economy

58 Making a market • Review: Capital

markets

60 Dr. Ghaleb Mahmassani, Vice

President of Beirut Stock Exchange

(BSE) • Interview

61 Firas Safieddine, Vice Chairman of

the Capital Markets Authority (CMA)

• Interview

62 Scaling up • Forum

64 Life is a rollercoaster • Review:

Insurance

66 Max R. Zaccar, Chairman of

Commercial Insurance & President

of the Association of Insurance

Companies• Interview

67 George Matossian, General

Manager & Vice President of Al

Mashrek • Interview

68 Fintech for insurance • Vox populi

70 Nothing too small • Focus:

Microinsurance

45

21

THEBUSINESSYEAR4 LEBANON 2016

71 ENERGY 71 Energetic remedies needed

• Review

75 HE Arthur Nazarian, Minister of

Energy and Water Resources

• Interview

76 HE Mohamad Machnouk, Minister

of Environment • Interview

77 Wissam Zahabi, Chairman of the

Board of the Lebanese Petroleum

Administration (LPA) • Interview

78 Gas pipe dreams • Focus:

Sovereign wealth funds

79 Energy efficiency • B2B

80 Pierre El Khoury, General

Director of the Lebanese Center

for Energy Conservation (LCEC) •

Interview

81 INDUSTRY81 Made to order • Review

85 HE Hussein Hajj Hassan, Minister

of Industry • Interview

86 Dr. Fady Gemayel, President

of the Association of Lebanese

Industrialists (ALI) • Interview

87 Car dealers • Forum

88 George Rbeiz, General Manager

of Diageo Lebanon • Interview

90 Beer & wine producers • Forum

91 Industry • Vox populi

92 Industrial solution • Focus:

Industrial cities

93 ICT & MEDIA 93 Learning curve • Review

96 HE Boutros Harb, Minister of

Telecommunications • Interview

97 Marianne Hoayek, Director of

the Executive Office of Banque du

Liban • Interview

98 Thinking IT through

• Roundtable

102 Venture capital funds • B2B

103 Entrepreneurship • Forum

104 The new star • Focus:

Infrastructure for the startup

ecosystem

105 Software companies • B2B

106 Ibrahim Al Amine, Editor-in-

Chief of Al-Akhbar • Interview

107 Modernizing Lebanon

• Forum

108 TRANSPORT108 Into the grind • Review

111 John Chedid, Country Manager

of DHL • Interview

112 Maritime trade • Forum

113 Bridging the gap • Focus:

Maritime exports bridge

114 Winging it • B2B

115 CONSTRUCTION & REAL ESTATE115 Bricks, despite mortars

• Review: Construction

120 Waddah El-Solh, Country

Head - Levant of Majid Al Futtaim

Properties • Interview

121 Jihad Abou Chacra, Vice

Chairman of Sakr Holding and CEO

of Remax Lebanon • Interview

122 Developers and contractors

• Forum

124 A stimulus for the rest of us

• Focus: Real estate

125 Brokers • B2B

115

110

93

47

73

THEBUSINESSYEAR 5

MANY OF THE INTERVIEWS PUBLISHED HERE HAVE BEEN ABRIDGED.

THE ORIGINAL, FULL-LENGTH INTERVIEWS CAN BE READ AT

THEBUSINESSYEAR.COM

149

126

133 By the book • Review:

Education

134 Stéphane Attali, Director

General, ESA Business School

• Column

135 HE Elias Bou Saab, Minister of

Education and Higher Education

• Interview

136 Irina Bokova, Director General

of UNESCO • Interview

137 Mohamed Harajli, Provost of

the American University of Beirut

(AUB) • Interview

138 High marks • Focus: Programs

to school Syrian refugee children

140 Joseph G. Jabbra, President of

the Lebanese American University

(LAU) • Interview

141 Adnan S. Hussein, President of

Lebanese University • Interview

142 Pan-Lebanon universities

• B2B

143 Mixed educational system

• Vox populi

144 TOURISM 144 Only ancient ruins • Review

146 Roula Korban Khadra, General

Manager, Three O Nine Hotel

• Column

148 Naif Zureikat, Cluster General

Manager of Hilton Hotels & Resorts

• Interview

150 Nightlife • B2B

151 Beirut's beat • Focus: Lebanese

nightlife

152 When in Lebanon... • Life &

leisure

154 EXECUTIVE GUIDE154 Now’s the time • Review: Doing

business

155 Common interests • Review:

Tax enforcement & banking secrecy

158 Ramy Torbey, Managing

Partner at Aziz Torbey Law Firm

• Interview

126 HEALTH & EDUCATION126 In sickness and in health

• Review: Health

129 Armand Pahrés, President

of the Lebanese Pharmaceutical

Importers Association (LPIA)

• Interview

130 Pharma • Forum

131 Children’s cancer center • B2B

132 Pharma land • Focus:

Incentives for pharmaceuticals in

Lebanon

Editor-in-ChiefLeland Rice

Country ManagerFlorencia Solano

Country EditorIrving Argaez

Project AssistantElla Elazkany

Chief Executive OfficerAyşe Hazır Valentin

Chief Operating OfficerLaila Bastati

Senior EditorPeter Howson

Associate EditorTerry Whitlam

Sub-EditorsJared Kimball, Emily Casswell, Kevin Mataraci, Shireen Nisha, Nathan T. Jefferson

Editorial CoordinatorAleksandra Fabia Tugal

Assistant Web EditorBelemir Ece Çolak

ContributorsAidan McMahon, Mark Szawlowski

TranscribersSusan Barrett, Heather Conover, Nikolai Davis, Gillian Docherty, Attila Pelit, Jeffrey Rodgers, Jason Shaw, Deanne de Vries,Pronto Publishing Services

Acting Art DirectorBahar Kara

Senior DesignersCeren Bettemir, Dan Le

Graphic DesignersSérgio Caldeira, Lara Nasifoğlu

Cover ArtistKürşat Ünsal

HR ManagerInés Delgado

PR AssistantBerna Köse

Operations ManagerSemiha Elkıran

Operations ExecutiveÖznur Yıldız

Operations AssistantGamze Zorlu

Finance DirectorSerpil Yaltalıer

Finance ExecutiveJanine Escobar

Circulation & Marketing DirectorAmy Burtin

PublisherPeggy Rosiak

The Business Year is published by The Business Year International, Trident Chambers, P.O. Box 146, Road Town, Tortola, British Virgin Islands. Printed by Apa Uniprint, Hadımköy Mahallesi 434 Street No:6, 34555, Arnavutköy, İstanbul, Türkiye. The Business Year is a registered trademark of The Business Year International, Copyright The Business Year International Inc. 2015. All rights reserved. No part of this publication may be re-produced, stored in a retrievable system, or trans-mitted in any form or by any means, electronic, mechanical, photocopied, recorded, or otherwise without prior permission of The Business Year International Inc. The Business Year Internation-al Inc. has made every effort to ensure that the content of this publication is accurate at the time of printing. The Business Year International Inc. makes no warranty, representation, or undertaking, whether expressed or implied, nor does it assume any legal liability, direct or indirect, or responsibility for the accuracy, completeness, or usefulness of any information contained in this publication.

ISBN 978-1-908180-77-3

www.thebusinessyear.com

120

THEBUSINESSYEAR 21

R E V I E W

Economy

The many chambers of commerce throughout Lebanon are taking proactive steps to better position companies to succeed.

32 Fighting the trade deficit has been a battle Lebanon has been faced with since its independence.

38 TBY talks to Alia Abbas, General Director of the Ministry of Economy and Trade, on maintaining economic growth.

28

Faced with numer-ous economic and social challenges stemming from

spillover effects of the Syri-an civil war and the failure to establish the current presi-dential administration, Leb-anon saw the progression of its development shift gears to a slower pace than in rela-tively recent years, with 2015 GDP reaching an estimated USD47.1 billion, a 1.5% YoY increase in real growth from 2014. Despite posting a resil-ient performance in 2015 in the face of formidable mac-roeconomic and geopolitical headwinds thanks to some of the country’s most reliable pil-lars of its structural economic foundation, last year’s 1.5% annual GDP growth marked a slowdown in the expansion of its economic output from the 1.8% GDP growth registered at the end of 2014.

Mile-high legal and bu-reaucratic barriers have crept through the cracks in a politi-cal system that has since 2014 seen neither the presidential vacancy filled nor the parlia-mentary impasse resolved,

With GDP growth remaining positive in 2015 and projections for 2016 looking even more optimistic, Lebanon has made the best of its trying circumstances in a year of commendable resilience.

Having weathered a storm that could best even the most developed of nations under similar circumstances, Lebanon is showing how its economy can sustain growth despite a political deadlock and a civil war raging in a neighboring state.

PHOENIX STIRSshaking the framework of an increasingly value-adding economy largely dependent on the financial support of foreign direct investments into the country. Respon-dents to the World Economic Forum’s 2015-2016 Global Competitiveness Report cited government instability as the number one barrier to doing business is Lebanon, while the report ranked the country 125th in the world in terms of the business effects of security concerns. The unanimity with which individuals and groups both within Lebanon’s politi-cal sphere and without concur on the handicap that these on-going partisan shortcomings are placing on the country’s realization of its full develop-ment potential have provided a renewed pressure on party leaders to work together to create the social and admin-istrative conditions needed in order to return to the levels of rapid GDP growth it enjoyed in years prior. The ember of optimism is that despite the many major setbacks, Leba-non’s economy has actually performed as well as it has. A

Image: Anna Omelchenko

THEBUSINESSYEAR22 LEBANON 2016

*Rea

d th

e fu

ll in

terv

iew

at t

heb

usi

nes

syea

r.co

m

years-long backlog of much-needed legislative updates is still waiting to be processed and im-plemented once the government is stabilized, furthering optimism over the major benefits the country can expect to enjoy once the seem-ingly achievable task of properly establishing the state administration is accomplished.

The effects of the conflict in Syria have had devastating effects on Lebanon’s economy, but one development that leaders of government and industry are betting on to parry the years of lost productivity is the anticipated massive period of reconstruction throughout the most war-torn regions of Syria. In order to capitalize on the opportunities for social and econom-ic development sure to go hand-in-hand with the all-important end to the regional violence, the Lebanese government and its most signif-icant economic players must still take drastic strides to have in place a state polity capable of meaningfully enacting decisive collective policies and a private sector with the required infrastructure in place for investments to again stimulate renewed growth throughout Leba-non, particularly areas along the border regions with Syria that, in addition to the fall in demand for land transport brought about by the con-flict, have long suffered from insufficient levels of support and underdevelopment. Respon-dents to the Global Competitiveness Report also listed an inadequate supply of infrastruc-ture as the second-most significant obstacle to doing business in Lebanon; the report ranked the quality of Lebanon’s overall infrastructure 138th, though the quality of its port infrastruc-ture was ranked a much better 80th. Having in place within a short timeframe a sufficient lev-el of strategic infrastructure within Lebanon’s border will be vital to not only supporting local economic development, but also enabling Leb-anon-based investments to participate in the

post-conflict Syrian reconstruction boom that waits on the other side of an as-yet elusive end to the five-year civil war.

According to the Global Competitiveness Re-port, Lebanon was the 101st most competitive economy in the world, moving up 12 spots from 113 in the organization’s 2014-2015 edition of the report. Lebanon’s economy is predomi-nantly service-oriented, with services account-ing for 69.7% of GDP in 2015. Within the diverse range of business segments, banking and tour-ism represent primary main growth sectors, as conditions for the removal of current obstacles to growth for a sector like tourism hinge on rela-tively clearly defined, albeit difficult to achieve, strategic developments. With the limited natu-ral resources available on the sovereign lands of what is one of the smallest countries in the MENA region, Lebanon draws largely on its population and strategic location as a Medi-terranean gateway to the Arab world for much of its competitive advantage. Its population of slightly more than 4.5 million makes for a labor force of roughly 1.63 million, not taking into consideration the many foreign workers in the country, which some estimates put at as high as 1 million individuals. Lebanon’s econ-omy is characterized as one in transition from being efficiency-driven to innovation-driven, with a general trend for many years across sec-tors being to develop domestic capabilities in a direction that better positions entities in the public and private sectors to fill the roles of a value-added economic output model. GDP per capita at global purchasing price parity in Leb-anon was more than USD18,200 in 2015, well ahead of the consolidated MENA-Pakistan re-gional average.

Lebanon’s macroeconomic environment was ranked just the 139th most competitive in the world in the Global Competitiveness

ZIAD HAYEKSecretary General, Higher Council for Privatization (HCP)

What do you see for the future of privatizations and PPPs in Lebanon in the upcoming years?We need the right people with the necessary vision and determination to make bold changes in the country, which would prompt among other actions the long-awaited privatization of the telecom sector. I am also optimistic that the ongoing PPP projects can influence the emergence of similar projects in other sectors, and with parliament currently discussing the PPP law this might peak in momentum in the near future. Lebanon will have to use PPPs regardless of preference, as many of the projects needed for the country require levels

of financial support that the government cannot provide. The priority in Lebanon is probably the energy sector, but we also need to use PPPs in transport, water, prisons, schools, and municipal services such as waste water treatment, solid waste management, and underground parking. If we pass the PPP legislation and create a better framework to increase investor confidence, we can solve the country’s chronic unemployment problem by creating over 200,000 jobs in the first five years alone. The potential for these processes to grow is strong, and we are working on moving in that direction.*

THEBUSINESSYEAR24 LEBANON 2016

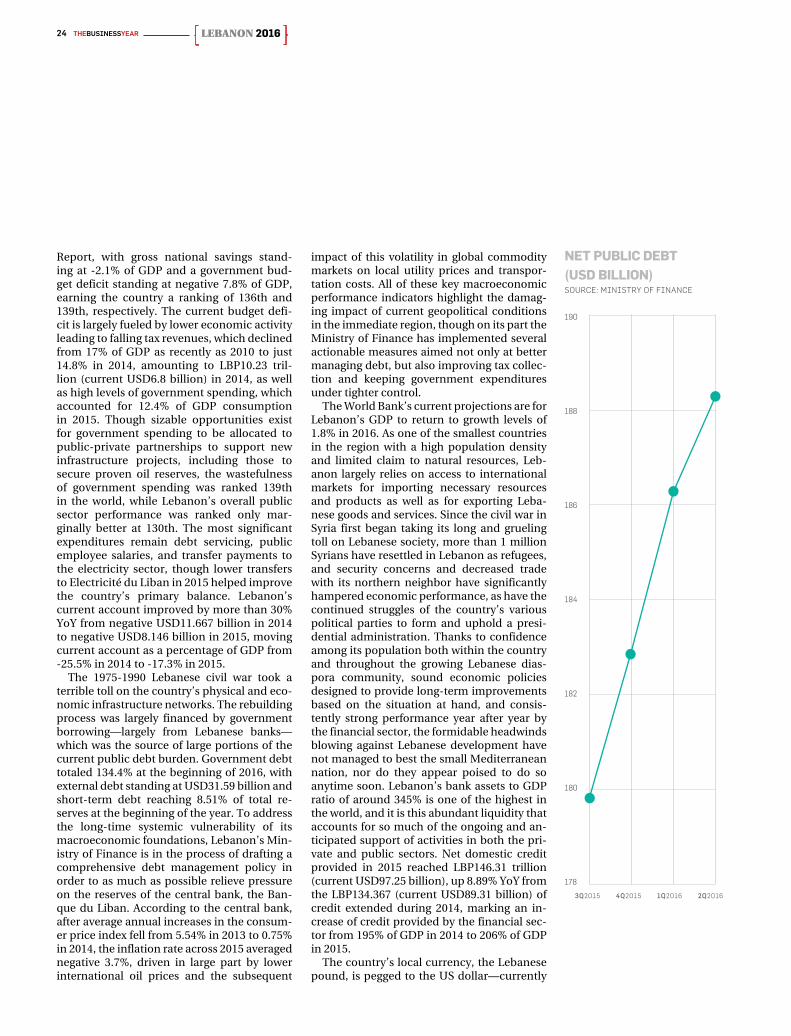

Report, with gross national savings stand-ing at -2.1% of GDP and a government bud-get deficit standing at negative 7.8% of GDP, earning the country a ranking of 136th and 139th, respectively. The current budget defi-cit is largely fueled by lower economic activity leading to falling tax revenues, which declined from 17% of GDP as recently as 2010 to just 14.8% in 2014, amounting to LBP10.23 tril-lion (current USD6.8 billion) in 2014, as well as high levels of government spending, which accounted for 12.4% of GDP consumption in 2015. Though sizable opportunities exist for government spending to be allocated to public-private partnerships to support new infrastructure projects, including those to secure proven oil reserves, the wastefulness of government spending was ranked 139th in the world, while Lebanon’s overall public sector performance was ranked only mar-ginally better at 130th. The most significant expenditures remain debt servicing, public employee salaries, and transfer payments to the electricity sector, though lower transfers to Electricité du Liban in 2015 helped improve the country’s primary balance. Lebanon’s current account improved by more than 30% YoY from negative USD11.667 billion in 2014 to negative USD8.146 billion in 2015, moving current account as a percentage of GDP from -25.5% in 2014 to -17.3% in 2015.

The 1975-1990 Lebanese civil war took a terrible toll on the country’s physical and eco-nomic infrastructure networks. The rebuilding process was largely financed by government borrowing—largely from Lebanese banks—which was the source of large portions of the current public debt burden. Government debt totaled 134.4% at the beginning of 2016, with external debt standing at USD31.59 billion and short-term debt reaching 8.51% of total re-serves at the beginning of the year. To address the long-time systemic vulnerability of its macroeconomic foundations, Lebanon’s Min-istry of Finance is in the process of drafting a comprehensive debt management policy in order to as much as possible relieve pressure on the reserves of the central bank, the Ban-que du Liban. According to the central bank, after average annual increases in the consum-er price index fell from 5.54% in 2013 to 0.75% in 2014, the inflation rate across 2015 averaged negative 3.7%, driven in large part by lower international oil prices and the subsequent

impact of this volatility in global commodity markets on local utility prices and transpor-tation costs. All of these key macroeconomic performance indicators highlight the damag-ing impact of current geopolitical conditions in the immediate region, though on its part the Ministry of Finance has implemented several actionable measures aimed not only at better managing debt, but also improving tax collec-tion and keeping government expenditures under tighter control.

The World Bank’s current projections are for Lebanon’s GDP to return to growth levels of 1.8% in 2016. As one of the smallest countries in the region with a high population density and limited claim to natural resources, Leb-anon largely relies on access to international markets for importing necessary resources and products as well as for exporting Leba-nese goods and services. Since the civil war in Syria first began taking its long and grueling toll on Lebanese society, more than 1 million Syrians have resettled in Lebanon as refugees, and security concerns and decreased trade with its northern neighbor have significantly hampered economic performance, as have the continued struggles of the country’s various political parties to form and uphold a presi-dential administration. Thanks to confidence among its population both within the country and throughout the growing Lebanese dias-pora community, sound economic policies designed to provide long-term improvements based on the situation at hand, and consis-tently strong performance year after year by the financial sector, the formidable headwinds blowing against Lebanese development have not managed to best the small Mediterranean nation, nor do they appear poised to do so anytime soon. Lebanon’s bank assets to GDP ratio of around 345% is one of the highest in the world, and it is this abundant liquidity that accounts for so much of the ongoing and an-ticipated support of activities in both the pri-vate and public sectors. Net domestic credit provided in 2015 reached LBP146.31 trillion (current USD97.25 billion), up 8.89% YoY from the LBP134.367 (current USD89.31 billion) of credit extended during 2014, marking an in-crease of credit provided by the financial sec-tor from 195% of GDP in 2014 to 206% of GDP in 2015.

The country’s local currency, the Lebanese pound, is pegged to the US dollar—currently

190

188

186

184

182

180

178

NET PUBLIC DEBT(USD BILLION)SOURCE: MINISTRY OF FINANCE

3Q2015 4Q2015 1Q2016 2Q2016

THEBUSINESSYEAR26 LEBANON 2016

95 YEARS OF TRADITION AND EXPERTISE

Beirut Stock Exchange

www.bse.com.lb

at an exchange rate of around LBP1,500 to the dollar—providing a welcome column of con-fidence in the security of exposing investor assets to Lebanese risk. Although its capital markets are known for not being particular-ly deep, the soundness of banks in Lebanon is world class, with the country being ranked 23rd for the same measure by the Global Competitiveness Report. Enabling firms in Lebanon, over 90% of which make up the stra-tegically vital SME segment, to contribute to the continued development of a more robust and competitive economy are a vital respon-sibility of leaders among both the political sphere and private sector business interests. To do so, the focus must remain on eliminat-ing those obstacles that currently stunt levels of private investment, and for its part, many key organizers of the interim government have acknowledged unanimously the impor-tance of taking the first steps to removing these roadblocks. By maintaining consistent-ly high levels of liquidity and capitalization, lending institutions will play a major role in

mobilizing capital resources to develop proj-ects both in Lebanon and across the border in Syria when the time for rebuilding arrives. Any improvements to the economy of Lebanon in 2016 will be largely contingent on solidify-ing the country’s political system so urgently needed to restore investor confidence, boost exports and balance trade flows, and attract greater levels of both foreign tourist arrivals as well as FDI. ✖

Having in place within a short timeframe a sufficient level of strategic infrastructure within Lebanon’s borders will be vital not only for supporting local economic development, but also for enabling Lebanon-based investments to participate in the post-conflict Syrian reconstruction boom.

THEBUSINESSYEAR 81

R E V I E W

Industry

90 The region has a long history of beer and winemaking, with many successful brands based in Lebanon.

Car sales, especially luxury vehicles, have not been affected by economic circumstances and are in fact seeing healthy numbers.

87 85 TBY talks to HE Hussein Hajj Hassan, Minister of Industry.

T

Despite declines in the export levels to which the country’s economic performance is so closely tied, operations throughout the industrial sector found new ways of adding generating value at a time when Lebanon needs it most.

With Lebanon’s macroeconomic and geopolitical troubles continuing in 2015, the country’s industrial sector managed to make the best of a challenging situation.

MADE TO ORDERhe industrial sec-tor in Lebanon ac-counts for roughly 7.5% of GDP and

employs around 140,000 peo-ple, which is the equivalent of approximately 25% of the local workforce. Industry is in fact the second-largest employer in the country, be-hind only the public sector. Manufacturing in Lebanon is comprised of more than 15 sub-sectors, which vary greatly in terms of the their contribution to employment and GDP. The food and bev-erage segment accounts for the largest share of industrial output at 26% of 2015 industry totals, followed by metal and metal products at 12%, other non-metallic mineral prod-ucts at 11.7%, and electrical machinery and apparatuses at 11%. Some of Lebanon’s most important industrial exports include chemical products, which accounted for 26% of all industrial exports in 2015, prepared foodstuffs at 24.6%, and base metals and articles of base metal at 19.7%. Volatility in global markets for precious metals evaporated nearly 75%

of the book value of Lebanon’s jewelry exports, dropping rev-enues from jewelry exports from USD1.7 billion in 2012 to just USD434 million in 2015.

Due to the relatively limit-ed size of the Lebanese mar-ket, the country’s growth and prosperity are closely tied to access to key international markets for importing eco-nomic inputs and products as well as for selling Lebanese products. The small Medi-terranean country’s strate-gic position as the historical crossroads between Europe, Asia, and Africa by both land and sea has helped enable Lebanon to grow into a key regional hub business and trade and a well-established mediator between Arab econ-omies and the rest of the world. Trade has long been an important source of both employment and value gener-ation, and it remains a central pillar of the country’s econo-my, accounting for 27.5% of the country’s GDP. According to the Ministry of Economy and Trade, total exports fell by 10.90% YoY from USD3.312 billion in 2014 to USD2.951

Image: Ksara

THEBUSINESSYEAR82 LEBANON 2016

billion in 2015. However, the USD3.150 billion derived from industrial exports in 2014 repre-sented 95.11% of the USD3.312 billion in total exports recorded during the year, up from the 85.98% of total exports accounted for by indus-trial products in 2013. With an end-2015 total of around USD2.77 billion, industrial exports have maintained their central position as the driving force behind Lebanon’s international trade, accounting for nearly 93.87% of total ex-ports last year. One of the competitive advan-tages that industrial firms enjoy by operating in Lebanon is the level of organization and insti-tutional support across the sector. The Associ-ation of Lebanese Industrialists plays an active role in promoting the interests of its many con-stituents, and government facilities provide for a 50% exemption on tariff duties for exported goods, while applying just a 2% customs duty for equipment, machinery, building materials, and spare parts imported into the country for the purposes of developing new industrial ven-tures. Wide access to foreign export markets granted by the many bilateral and multilateral trade agreements that Lebanon has signed is a further advantage for industrial firms looking to use the country as a regional base.

Merchandise trade, which immediately fol-lowing the end of the Lebanese civil war rep-resented the equivalent of 96.3% of the coun-try’s GDP, stood at 47.6% of GDP in 2015, down slightly from 56.2% in 2014. One of the many factors contributing to last year’s drop-off in trade, which during 2015 measured roughly 22% of the total level of Lebanon’s GDP, was heightened concern over ongoing security risks stemming from regional conflict, which among other consequences has led to an in-crease in the cost of land transport. Lebanon’s primary export partners include Syria, which at 15.3% still stands as the largest single import-er of Lebanese products despite the ongoing Syrian civil war. Turkey accounts for 11.9% of Lebanese exports, followed by Saudi Arabia at 8.3%, Egypt at 7.4%, Iraq at 5.7%, and Bangla-desh at 5.1%. The close connection between economic growth and exports—and thus the industrial sector by extension—underlines the potential to expand upon efforts to develop an ever-more specialized production portfolio in Lebanon, increasing the competitiveness of its industry by achieving sector-specific improve-ments to innovation and productivity. The larg-est importers of Lebanese industrial goods and services in 2015 include Syria at 17.8% of total industrial exports from Lebanon in 2015, fol-lowed by Turkey at 16.4%, Bangladesh at 7.2%, Iraq at 6.4%, and Saudi Arabia at 6.2%. Of the

many commodity exports that drive Lebanon’s economic performance, fruits and vegetables represent 22.5% of total commodity exports, while chemicals account for 20.1%, followed by prepared foodstuffs at 19%, base metals at 15.2%, and wood pulp and paper at 6%.

AGRO-INDUSTRYTwo of the most productive staples of industry in Lebanon are its agricultural and agro-indus-trial sectors. Lebanese agriculture is often asso-ciated with its highly sought after produce, par-ticularly olives, tomatoes, citrus fruits, grapes, apples, vegetables, and potatoes. Thanks in large part to the country’s internationally re-nowned culinary traditions and the availability of skilled labor at relatively low-cost to produc-ers, Lebanon’s agro-industrial sector is a sig-nificant contributor to the country’s economy, with the most recent figures showing that in 2011 the agro-industry accounted for approx-imately 26.3% of total industrial output and generated roughly 2.2% of the country’s GDP, while the estimated workforce of 20,607 indi-viduals engaging in agro-industrial activities represents around 25% of all industrial sector employment.

Around 740 of the 970 food and beverage op-erations in Lebanon belong to the agro-indus-trial segment, accounting for the largest share of industrial establishments in the country with about 18% of all industrial enterprises. Exports of agro-food products alone accounted for 20.7% of total exports in 2015. The eurozone, another of the key drivers of the long-term sustainability of Lebanese industry, accounted for 7.8% of Lebanon’s ago-industrial exports in 2015. The total volume of agro-industrial ex-ports increased by 53% from 2012 to 2015, and despite the many serious blows to Lebanon’s economy caused by ongoing violent conflicts in Syria and Iraq, agro-industrial exports to Syr-ia increased by 191% in 2015, giving it a 61.7% share of all agro-industrial exports to non-GCC Arab countries, while exports of agro-industrial products to Iraq increased by 253% last year.

PHARMACEUTICALSThe value of Lebanon’s pharmaceutical mar-ket in 2015 was estimated at roughly USD1.63 billion in 2015, with current projections set at an expected CAGR of 6.2% through 2020, ul-timately driving up the value of the country’s pharmaceutical industry to nearly USD2.20 bil-lion. At 3.15% of GDP in 2015, the pharmaceu-tical industry’s contribution to national output in Lebanon was the largest among all coun-tries in the entire MENA region. The country’s

970 Food and beverage

544 Furniture

502 Paper, paper products, and printing

417 Metal products (excluding transport equipment)

410 Non-mineral mining products

397 Machinery and electrical appliances

379 Chemicals

237 Textiles

237 Wood products

190 Others

NUMBER OF INDUSTRY FIRMS BY SECTORSOURCE: DIRECTORY OF EXPORTS

& INDUSTRIAL FIRMS IN LEBANON

(2015-2016)

THEBUSINESSYEAR84 LEBANON 2016

pharmaceutical sector is currently comprised of 11 manufacturing facilities and 164 import-ers. From 2012 through 2015, exports of phar-maceutical products demonstrated a CAGR of 17.68%, reaching USD55.3 million in 2015. The top destinations abroad for Lebanese pharma-ceutical products are primarily Arab countries, specifically Iraq, which accounted for 18% of pharmaceutical exports in 2015, Saudi Arabia at 17%, and Jordan at 11%. There are a number of underlying factors supporting the strong per-formance of the sector in Lebanon, including a continually restocked pool of qualified local la-bor made possible by the country’s world-class education system, specifically in the all-import-ant fields of math and science, as well as quickly growing regional markets and a well-developed healthcare system.

CHEMICAL INDUSTRYLebanon’s chemical industry stands out as one of the country’s most diversified sectors. The roughly 110 different items produced and ex-ported by the sector include basic chemicals, rubber, cosmetics, soaps and detergents, re-fined oil derivatives, paints and varnishes, and plastic, with the latter forming at least some part of the operations of around 80% of all companies operating in the country’s chemical sector, while 29% of chemical firms had activi-ties in the perfume segment and 26% produced paint products. As of the beginning of 2016, there were 379 factories operating in this sec-tor, accounting for just over 9% of all industri-al firms in Lebanon. Sales of locally produced chemical products abroad accounted for 14% of all Lebanese industrial exports in 2015, mak-ing the segment the third most important in terms of the number of industrial products that it imported last year. Around 2% of total Leba-nese exports in 2015 were accounted for by in-organic chemicals, while fertilizers accounted for an additional 3% of total exports. In 2015, Lebanon’s chemical exports in 2015 were made up mainly of resinoids, essential oils, and cos-metics and toilet preparations, which together accounted for 27% of chemical product exports last year. This sub-sector of Lebanese industry is another of the many local beneficiaries of the country’s affinity for producing highly skilled chemists at the undergraduate, graduate, and post-graduate levels.

PRINTING INDUSTRYPrinting is still a relatively small activity in Leb-anon, accounting for only around 7.5% of total industrial output in 2013 when the latest data for the sector was published. As of the start of 2014, the printing sector provided employment for 3,693 individuals, accounting for 5.2% of the overall industrial workforce. The sub-sector is made up mostly of SMEs, with 45.5% of print-

ing companies employing five to nine workers, and 86.3% of printing companies employing fewer than 35 employees. The sector’s activities are mostly geared toward consumer markets, through products like periodicals and books, and industrial customers who demand printed materials for packaging and distribution. As of the start of 2016, Lebanon is as a net exporter of printed products, with exports of printing out-put accounting for 3% of total exports in 2015.

The limited size of Lebanon both in terms of its territory and its market largely shape the profile of its economic models. With less than 5 million people living in Lebanon, competing with other economies of similar structural com-position but larger populations along the lines of scale will never provide a sustainable way for-ward. Instead, the country’s leaders of govern-ment and private industry have all recognized that the development of the human resources needed to transition fully to a knowledge-based economy is tantamount for the long-term pros-perity for its many economic sectors, industry not least among them. Increasing value-added activities is a key point of the national agenda, and the preliminary results of the initiative can be seen among many other places in its trade statistics; the value per ton of exported goods in 2014 was around USD1,122, more than 35% less than the USD1,522 per ton of goods export-ed in 2015. While overall the volume exports may have declined by 13.2% during 2015, the decline in the value of those exports remaining at just 10.9% is evidence of the successful tran-sition by Lebanon’s economic actors toward creating more value, rather than just creating more. ✖

2015 TOTAL IMPORTS AND EXPORTSSOURCE: MINISTRY OF ECONOMY & TRADE

IMPORTS

USD billion

18.06YoY change

-11.8%

USD billion

-15.116 YoY change

-12%

USD billion

2.952YoY change

-10.9%

USD billion

21.020YoY change

-11.7%

EXPORTS TRADE DEFICITTRADE AGGREGATE

Millions of tons

15.69YoY change

1.6%

Millions of tons

1.940YoY change

-13.2%

Millions of tons

-13.759 YoY change

4.1%

Millions of tons

17.639YoY change

-3%

The value of Lebanon’s pharmaceutical market in 2015 was estimated at roughly USD1.63 billion in 2015, with current projections set at an expected CAGR of 6.2% through 2020, ultimately driving up the value of the country’s pharmaceutical industry to nearly USD2.20 billion.

THEBUSINESSYEAR152 LEBANON 2016

L I F E & L E I S U R E

Azadea Group is a premier lifestyle company with more than 50 leading international franchises across the Middle East and Africa, including many fashion brands as well as offerings in entertain-ment and the food and beverages sectors. The Azadea Group in its current form grew out of a sin-gle clothing store in Beirut called Subway, opened in 1978 in the heart of the city. Just a few years lat-er it won its first international franchise with Max-Mara, and Azadea now employs over 12,000 peo-ple and oversees more than 650 stores across 13 countries. The majority of the group’s employees in Lebanon are Lebanese nationals, an important characteristic of one of the most inspiring exam-ples of entrepreneurs in the country’s lifestyle sec-tor driving the country’s economic development. The impact of Azadea extends far beyond its shop floors, with no more visible an example of this generosity than the landmark 22,000sqm Sanayeh Garden project in central Beirut.

Kidz Holding is a Lebanese success story that has greatly shaped both the entertain-ment and education industries through-out the Middle East. Kidz has leveraged its successful model of "edutainment" parks that it developed in Lebanon as a vehicle for exporting Lebanese leisure offerings to regional neighbors, reshaping the original concept of its content and visual aesthetic to the reflect the different cultures where it operates. This mixed concept of educating through entertainment is also appealing

to parents, who are attracted by the more than 80 activities that Kidz parks offer for both children and parents alike. Building on the success of the original KidzMondo, Kidz Holding has established four new concepts, namely called KidzMondo Vil-lage, Karnavali, Star District, and The Es-cape, all of which are sure to deepen the offerings of Lebanon’s leisure industry and further attract visitors to experience the evolution of culture as it is taking place.

KIDZ HOLDING

Food Kapital was established in 2006 as a pio-neer in the Lebanese market. Always driven by the same craving for delicious and affordable food, Food Kapital Holdings has carved out a niche for its restaurants to the point where it is now a cultural force practically impossible to divorce from the rest of Lebanon’s cultural and lifestyle trends. The best ambassadors for the concept of Lebanese cuisine are the Leba-nese people, who all across the world bring with

them the seeds of the Lebanese culinary tradi-tion in the form of hummus, tabbouleh, falafel, and the many other dishes now commonplace throughout the world. The Mediterranean diet—arguably embodied by traditional Leba-nese cuisine as well—has even been recognized by UNESCO as an intangible heritage. The pas-sion that Food Kapital puts into its food and the diversity and healthiness of its offerings leave no doubt as to why Lebanese food is so beloved.

FKH

AZADEA GROUP

A confluence of time and cultures, and centuries of years of rich Lebanese heritage have given birth to one of the region’s most dynamic life & leisure environments.

DORY DACCACHE CEO, Food Kapital Holding

WHEN IN LEBANON...

THEBUSINESSYEAR 153Tourism

Hilton is one of the world’s most recog-nizable hotel chains, with nearly 750,000 rooms in more than 100 countries, and Lebanon is no exception, where the Hil-ton brand is one the most trusted in hos-pitality and its hotels stand as landmark features of its urban skylines. Though the original Beirut Hilton Hotel was never occupied due to the civil war, Hilton ho-tels are now positioned at the center of Lebanon, both figuratively and literally. In the heart of the city just minutes from

the airport, Hilton Beirut’s Metropolitan Palace and Habtoor Grand hotels are standards of excellence in Lebanon’s hos-pitality sector. The hotels boast a variety of suites, penthouses, a 31st-floor bar that is the city’s highest, and a 2,000-person convention space that is the largest in Lebanon. Hilton hotels offer guests the best of Lebanese hospitality and provide direct access to attractions such as the many notable mosques, museums, and traditional souk markets.

One of the main inspirations to create the Three O Nine hotel was the perceived gap in quali-ty boutique hotels in Beirut. Three O Nine was created as a trendy, urban, and lively idea to bring new life to the surrounding Hamra area. The hotel’s blend of innovative concepts and chic installations has had a major impact on the city’s hospitality sector by visually transform-ing the landscape, attracting more visitors, and improving locals’ perceptions of their own city. The Three O Nine Urban House is situated just 15 minutes away from the airport in the heart of Ras Beirut on the aptly named Bliss Street next to the American University of Beirut. Its prime location offers quick and easy access to the cap-ital’s top downtown destinations, including its world-class restaurants, the seaside Corniche promenade, the Hamra shopping district, and the nearby historic city center.

HILTON

Ichiban restaurants attract attention as some of Beirut’s most widely recognized places to enjoy authentic Japanese cuisine. Through its fusion of innovative and classical culinary concepts, Ichiban has reached a new level of prominence within the capital city’s cuisine scene, serving 25,000 pieces of sushi to the hungry and curious on a daily basis. Against the saturation of Leba-

non’s food and beverage industry by a wide range of high-quality alternatives all vying for a piece of the same highly competitive market, Ichiban has managed in just a few years to more than double its service capacity and has plans to introduce in the near future even more locations to feed the hungry people of Beirut looking to experience the city’s tradition of culinary excellence.

ICHIBAN

THREE O NINE HOTEL

FADY EL KHOURY General Manager, Ichiban Holding