teachers' retirement system of alabama in addition, there are 1,748 employees with annual...

TRANSCRIPT

Teachers' Retirement System of Alabama Report of the Actuary on the Annual Valuation Prepared as of September 30, 2015

June 22, 2016

Board of ControlTeachers’ Retirement System of AlabamaMontgomery, Alabama

Members of the Board:

In this report are submitted the results of the annual valuation of the assets and liabilities of the Teachers'Retirement System of Alabama, prepared as of September 30, 2015 in accordance with Section 16-25-19(q)of the act governing the operation of the System.

The purpose of this report is to provide a summary of the funded status of the System as ofSeptember 30, 2015 and to recommend rates of State contribution. While not verifying the data at the source,the actuary performed tests for consistency and reasonability.

On the basis of the valuation, we have determined employer contribution rates of 12.24% of payroll for Tier Imembers and 11.01% of payroll for Tier II members for the fiscal year ending September 30, 2018.

The promised benefits of the System are included in the actuarially calculated contribution rates which aredeveloped using the Entry Age Normal cost method. Five-year smoothed market value of assets is used foractuarial valuation purposes. Gains and losses are reflected in the unfunded actuarial accrued liability that isbeing amortized by regular annual contributions as a level percentage of payroll, on the assumption thatpayroll will increase by 3.25% annually. The assumptions recommended by the actuary and adopted by theBoard are in the aggregate reasonably related to the experience under the System and to reasonableexpectations of anticipated experience under the System. The assumptions and methods used for fundingpurposes meet the parameters outlined in the Board’s funding policy.

In this report, we provided the following information and supporting schedules in the Actuarial and StatisticalSections of the Comprehensive Annual Financial Report (CAFR):

Summary of Actuarial Assumptions and Methods Actuarial Cost Method Summary of Plan Provisions as Interpreted for Valuation Purposes Schedule of Funding Progress Solvency Test Schedule of Active Member Valuation Data

We also provide the following schedules for the CAFR in a separate supplemental report: Analysis of Actuarial Gains and Losses Schedule of Retirants and Beneficiaries Added and Removed from Rolls Retired Members by Type of Benefit as of September 30, 2015 Ten-Year History of Average Monthly Benefit Payments as of September 30

Off

Cavanaugh Macdonald CC OO NN SS UU LL TT II NN GG,, LL LL CC

The experience and dedication you deserve

3550 Busbee Pkwy, Suite 250, Kennesaw, GA 30144 Phone (678) 388-1700 • Fax (678) 388-1730

www.CavMacConsulting.com Offices in Englewood, CO • Kennesaw, GA • Bellevue, NE

June 22, 2016 Board of Control Page 2

The necessary GASB Statement Nos. 67 and 68 disclosure information is provided in separate supplementalreports.

This is to certify that the independent consulting actuary is a member of the American Academy of Actuariesand has experience in performing valuations for public retirement systems, that the valuation was prepared inaccordance with principles of practice prescribed by the Actuarial Standards Board, and that the actuarialcalculations were performed by qualified actuaries in accordance with accepted actuarial procedures, basedon the current provisions of the retirement system and on actuarial assumptions that are internally consistentand reasonably based on the actual experience of the System.

Future actuarial results may differ significantly from the current results presented in this report due to suchfactors as the following: plan experience differing from that anticipated by the economic or demographicassumptions; changes in economic or demographic assumptions; increases or decreases expected as partof the natural operation of the methodology used for these measurements (such as the end of anamortization period or additional cost or contribution requirements based on the plan’s funded status); and changes in plan provisions or applicable law. Since the potential impact of such factors is outside the scopeof a normal annual actuarial valuation, an analysis of the range of results is not presented herein.

The actuarial computations presented in this report are for purposes of determining the recommendedfunding amounts for the System. Use of these computations for purposes other than meeting theserequirements may not be appropriate.

In our opinion the System is operating on an actuarially sound basis. Assuming that contributions to theSystem are made by the employer from year to year in the future at the rates recommended on the basis ofthe successive actuarial valuations, the continued sufficiency of the retirement fund to provide the benefitscalled for under the System may be safely anticipated.

The Table of Contents, which immediately follows, outlines the material contained in the report.

Respectfully submitted,

Edward A. Macdonald, ASA, FCA, MAAA Cathy TurcotPresident Principal and Managing Director

John J. Garrett, ASA, FCA, MAAAPrincipal and Consulting Actuary

EAM/mjn

TABLE OF CONTENTS

Section Item Page No.

I Summary of Principal Results 1

II Membership 3

III Assets 5

IV Comments on Valuation 7

V Contributions Payable by Employer 9

VI Annual Actuarial Certification 11

VII Analysis of Financial Experience 12

VIII Accounting Information 13

Schedule

A Valuation Balance Sheet and Solvency Test 15

B Development of the Actuarial Value of Assets 17

C Summary of Receipts and Disbursements 18

D Smoothed Valuation Interest Rate 19

E Outline of Actuarial Assumptions and Methods 20

F Actuarial Cost Method 24

G Board Funding Policy 25

H Projection of Transitional UAAL and Amortization of Bases 27

I Summary of Main Plan Provisions as Interpretedfor Valuation Purposes 32

J Schedule of Membership Data 37

Page 1

TEACHERS' RETIREMENT SYSTEM OF ALABAMA REPORT OF THE ACTUARY ON THE ANNUAL VALUATION

PREPARED AS OF SEPTEMBER 30, 2015

SECTION I - SUMMARY OF PRINCIPAL RESULTS

1. For convenience of reference, the principal results of the valuation and a comparison with the

preceding year's results are summarized below:

VALUATION DATE September 30, 2015 September 30, 2014

Active members Number Annual compensation

135,986 $ 6,297,938,621

135,230 $ 6,214,949,700

Retired members and beneficiaries Number Annual allowances

88,633 $ 1,964,212,008

85,209 $ 1,865,549,629

DROP participants Number 699 1,748 Annual compensation $ 52,847,343 $ 120,210,805 Annual allowances 26,937,787 62,162,236 Assets Actuarial value $ 21,740,279,791 $ 20,809,871,128 Market value 21,574,652,720 22,253,817,957 Unfunded actuarial accrued liability $ 10,104,562,691 $ 10,027,958,472

Funded Ratio 68.3% 67.5%

CONTRIBUTIONS FOR FISCAL YEAR ENDING September 30, 2018 September 30, 2017

Tier I (first hired prior to January 1, 2013)

Employer contribution rate Normal 2.43% 2.00% Unfunded actuarial accrued liability 9.45 9.65 Death benefit 0.02 0.02 Term life 0.01 0.01 Administration 0.33 0.33 Total 12.24% 12.01%

Tier II (first hired on or after January 1, 2013)

Employer contribution rate Normal 1.20% 0.81% Unfunded actuarial accrued liability 9.45 9.65 Death benefit 0.02 0.02 Term life 0.01 0.01 Administration 0.33 0.33 Total 11.01% 10.82%

Blended Amortization period 29.5 years 29.8 years

Page 2

2. Comments on the valuation results as of September 30, 2015 are given in Section IV and further

discussion of the contribution levels is set out in Section V.

3. Schedule D of this report shows the development of the smoothed interest rate used for valuation

purposes. Schedule B shows the development of the actuarial value of assets. Schedule E of this

report outlines the full set of actuarial assumptions and methods used in the current valuation. Since

the previous valuation, there was a modification to the programming to remove the 10% reduction

applied to member contribution refunds. This reduction was to account for interest accumulation

adjustments less than 4% paid to members. However, since this interest is transferred from the

assets used for valuation purposes to the Expense Fund, it was more appropriate to reflect the full

liability in the valuation. The Board funding policy is shown in Schedule G.

4. Provisions of the System, as summarized in Schedule I, were taken into account in the current

valuation. There have been no changes since the previous valuation. Section VI of this report shows

the certification of the liquidation period used to determine the accrued liability contribution rate.

5. The funded ratio shown in the Summary of Principal Results is the ratio of the actuarial value of assets

to the actuarial accrued liability. The funded status would be different based on the market value of

assets. The funded ratio is an indication of progress in funding the promised benefits. Since the ratio

is less than 100%, there is a need for additional contributions towards payment of the unfunded

actuarial accrued liability. In addition, this funded ratio does not have any relationship to measuring

sufficiency if the plan had to settle its liabilities.

Page 3

SECTION II - MEMBERSHIP

1. The following table shows the number of active members and their annual compensation as of

September 30, 2015 on the basis of which the valuation was prepared.

TABLE 1

THE NUMBER AND ANNUAL COMPENSATION OF ACTIVE MEMBERS AS OF SEPTEMBER 30, 2015

GROUP NUMBER COMPENSATION

Tier I 113,362 $ 5,501,829,930

Tier II 22,624 796,108,691

Subtotal 135,986 $ 6,297,938,621

DROP 699 52,847,343

Total 136,685 $ 6,350,785,964

The table reflects the active membership for whom complete valuation data were submitted. The results of the valuation include an estimated liability for an additional 15,916 inactive members and contribution balances for 29,071 non-vested inactive members who have not contributed for more than 5 years.

2. The following table shows a six-year history of active member valuation data.

TABLE 2

SCHEDULE OF ACTIVE MEMBER VALUATION DATA

Valuation Date

Number

Annual Payroll

Annual Average Pay

% Increase in Average Pay

9/30/20151 135,986 $ 6,297,938,621 $ 46,313 0.77% 9/30/20142 135,230 6,214,949,700 45,958 1.48 9/30/20133 133,919 6,065,042,345 45,289 2.06 9/30/20124 133,791 5,936,831,043 44,374 3.74 9/30/20115 135,768 5,807,655,862 42,776 (0.12) 9/30/20106 136,290 5,836,902,762 42,827 (0.01)

1 In addition, there are 699 employees with annual compensation of $52,847,343 who are currently participating in the DROP program. Employers of the Retirement System contribute on this payroll.

2 In addition, there are 1,748 employees with annual compensation of $120,210,805 who are currently participating in the DROP program. Employers of the Retirement System contribute on this payroll.

3 In addition, there are 3,029 employees with annual compensation of $198,322,151 who are currently participating in the DROP program. Employers of the Retirement System contribute on this payroll.

3 In addition, there are 4,436 employees with annual compensation of $285,484,977 who are currently participating in the DROP program. Employers of the Retirement System contribute on this payroll.

4 In addition, there are 5,625 employees with annual compensation of $$351,906,404 who are currently participating in the DROP program. Employers of the Retirement System contribute on this payroll.

5 In addition, there are 5,737 employees with annual compensation of 346,301,313 who are currently participating in the DROP program. Employers of the Retirement System contribute on this payroll.

Page 4

3. The following table shows the number and annual retirement allowances payable to retired members

and their beneficiaries on the roll of the Retirement System as of the valuation date.

TABLE 3

THE NUMBER AND ANNUAL RETIREMENT ALLOWANCES OF RETIRED MEMBERS AND BENEFICIARIES ON THE ROLL

AS OF SEPTEMBER 30, 2015

GROUP

NUMBER

ANNUAL RETIREMENT

ALLOWANCES

Service Retirements 78,547 $ 1,833,828,764

Disability Retirements 5,523 62,204,273

Beneficiaries of Deceased Members 4,563 68,178,971

Subtotal 88,633 $ 1,964,212,008

DROP Participants 699 26,937,787

Total 89,332 $ 1,991,149,795 4. Schedule J shows the distribution by age and service of the number and average annual

compensation of active members included in the valuation and a distribution by age of the number

and benefits of retired members and beneficiaries included in the valuation.

Page 5

SECTION III - ASSETS

1. The current retirement law provides for the maintenance of six funds for the purpose of recording the

fiscal transactions of the System, namely, the Annuity Savings Fund, the Pension Accumulation Fund,

the Deferred Retirement Option Plan Fund, the Pre-Retirement Death Benefit Fund, the Life

Insurance Fund and the Expense Fund.

(a) Annuity Savings Fund The Annuity Savings Fund is the fund to which are credited all contributions made by

members together with regular interest thereon. When a member retires or when a survivor allowance becomes payable the amount of the member's accumulated contributions are transferred from the Annuity Savings Fund to the Pension Accumulation Fund. The market value of assets credited to the Annuity Savings Fund on September 30, 2015, which represent the accumulated contributions of active members to that date, including interest, amounted to $4,894,144,912.

(b) Pension Accumulation Fund The Pension Accumulation Fund is the fund to which are credited all contributions made by

the employer, except those contributions made to the Pre-Retirement Death Benefit Fund, the Life Insurance Fund or the Expense Fund. When a member retires or when a survivor allowance becomes payable, the pension is paid from this fund. In addition, the amount of the member’s accumulated contributions is transferred from the Annuity Savings Fund to the Pension Accumulation Fund and the annuity is paid from this fund. On September 30, 2015 the market value of assets credited to this fund amounted to $16,194,523,396.

(c) DROP Fund The DROP Fund is the fund to which are credited deferred retirement benefits on behalf of

members who elect to participate in the DROP, together with regular interest thereon. In addition, member contributions while participating in the DROP, together with regular interest therein, are credited to the Fund. At the end of the DROP deferral period, the member receives the amount of the deferred retirement benefits and contributions plus interest in the member’s DROP account. The DROP is closed to new participants as of June 1, 2011. On September 30, 2015, the market value of assets credited to this Fund amounted to $485,984,412.

(d) Pre-Retirement Death Benefit Fund

The Pre-Retirement Death Benefit Fund is the fund to which are credited contributions made by the employer for the special pre-retirement death benefit which became effective October 1, 1983. On September 30, 2015, the market value of assets credited to this fund amounted to $50,294,645. These assets are not included in the valuation and the liabilities associated with these death benefits are not included in the valuation.

(e) Life Insurance Fund

The Life Insurance Fund is the fund to which are credited contributions made by the employer for life insurance benefits which became effective October 1, 1987. On September 30, 2015, the market value of assets credited to this fund amounted to $15,708,896. These assets are not included in the valuation and the liabilities associated with these life insurance benefits are not included in the valuation.

Page 6

(f) Expense Fund

The Expense Fund is the fund from which the expenses of the administration of the retirement system are paid. Any amounts credited to the accounts of members withdrawing before retirement and not returnable under the provisions of subsection (g) of Section 16-25-14 are credited to the Expense Fund. Additional contributions required to meet the expenses of the retirement system made by the employer are also credited to this fund. On September 30, 2015, the market value of assets credited to this fund amounted to $12,006,561. These assets are not included in the valuation.

2. As of September 30, 2015 the total market value of assets reported exclusive of the Pre-Retirement

Death Benefit Fund, the Life Insurance Fund and the Expense Fund amounted to $21,574,652,720

as shown in the following table.

TABLE 4

MARKET VALUE OF ASSETS BY FUND AS OF SEPTEMBER 30, 2015

FUND MARKET VALUE OF ASSETS

Annuity Savings Fund $ 4,894,144,912 Pension Accumulation Fund 16,194,523,396 DROP Fund 485,984,412 Total Market Value of Assets $ 21,574,652,720

3. The five-year market related actuarial value of assets as of September 30, 2015 was

$21,740,279,791. Schedule B shows the development of the actuarial value of assets as of

September 30, 2015.

4. Schedule C shows the receipts and disbursements of the System for the year preceding the valuation

date and a reconciliation of the fund balances at market value.

Page 7

SECTION IV - COMMENTS ON VALUATION

1. Schedule A of this report contains the valuation balance sheet which shows the present and

prospective assets and liabilities of the System as of September 30, 2015.

2. The valuation balance sheet shows that the System has total prospective liabilities of

$36,506,646,228. Of this amount, $18,621,250,135 is for the prospective benefits payable on

account of present retired members, beneficiaries of deceased members, and DROP participants,

$629,364,544 is for the prospective benefits payable on account of present inactive members and

$17,256,031,549 is for the prospective benefits payable on account of present active members.

Against these liabilities, the System has total actuarial value of assets, exclusive of the Pre-

Retirement Death Benefit Fund, the Life Insurance Fund and the Expense Fund, of $21,740,279,791

as of September 30, 2015. The difference of $14,766,366,437 between the total liabilities and the

total actuarial value of assets represents the present value of contributions to be made in the future.

Of this amount, $3,560,025,802 is the present value of future contributions expected to be made

by members to the Annuity Savings Fund, and the balance of $11,206,340,635 represents the

present value of future contributions payable by the employer.

3. The employer's regular contributions to the System consist of normal contributions and unfunded

actuarial accrued liability (UAAL) contributions. The valuation indicates that employer normal

contributions at the rate of 2.43% of payroll for Tier I members and 1.20% of payroll for Tier II

members are required to provide the benefits of the System.

4. Prospective normal contributions have a present value of $1,101,777,944. When this amount is

subtracted from $11,206,340,635 which is the present value of the total future contributions to be

made by the employer, there remains $10,104,562,691 as the amount of future UAAL contributions.

5. The funding policy adopted by the Board, as shown in Schedule G, provides that one-fifteenth of the

unfunded actuarial liability as of September 30, 2012 (Transitional UAAL) will be amortized as a level

percent of payroll over a closed period. The closed period shall be the amortization period for the

September 30, 2012 valuation, not to exceed 30 years. The remaining Transitional UAAL each year

will be amortized over an open period. The open period shall be the amortization period for the

September 30, 2012 valuation, not to exceed 30 years. After 15 years the entire Transitional UAAL

Page 8

will be closed. In each subsequent valuation all benefit changes, assumption and method changes

and experience gains and/or losses that have occurred since the previous valuation will determine a

New Incremental UAAL. Each New Incremental UAAL will be amortized as a level percent of payroll

over a closed 30–year period from the date it is established.

6. The total UAAL contribution rate is 9.45% of payroll determined in accordance with the Board’s

funding policy. The UAAL contribution rate has been calculated on the assumption that the aggregate

amount of accrued liability contribution will increase by 3.25% each year. Schedule H of this report

shows a projection of the open Transitional UAAL and amortization schedules for all closed bases on

September 30, 2015.

7. The following table shows the components of the total unfunded actuarial accrued liability (UAAL)

and the derivation of the accrued liability contribution rate in accordance with the funding policy.

TABLE 5

TOTAL UAAL AND UAAL CONTRIBUTION

UAAL Amortization

Period Amortization

Payment Open Transitional $ 7,276,833,673 30 $466,722,853 Closed Transitional 9/30/2012 659,423,718 27 44,548,455 Closed Transitional 9/30/2013 660,846,260 28 43,830,581 Closed Transitional 9/30/2014 661,530,334 29 43,124,275 Closed Transitional 9/30/2015 661,530,334 30 42,429,350 New Incremental 9/30/2013 433,527,124 28 28,753,655 New Incremental 9/30/2014 (169,226,658) 29 (11,031,659) New Incremental 9/30/2015 (79,902,094) 30 (5,124,775) Total $10,104,562,691 $653,252,735

Total Amortized Payment Adjusted for Timing $628,592,737 Total Estimated Payroll $6,653,009,015 UAAL Contribution Rate 9.45%

8. A contribution of 0.02% is required to meet the cost of the pre-retirement death benefit program this

year. The assets and liabilities of this program are not included in the valuation. A contribution of

0.01% is required to meet the cost of life insurance premiums. The assets and liabilities of this

program are not included in the valuation.

9. An additional contribution of 0.33% of payroll is required to cover the expenses of administering the

System.

Page 9

SECTION V - CONTRIBUTIONS PAYABLE BY EMPLOYER

1. The retirement law provides that the employer contributions are to be paid from the same source from

which employees’ salaries are paid.

2. On the basis of the actuarial valuation prepared as of September 30, 2015 it is recommended that

the employer make contributions at the following rates beginning October 1, 2017:

TABLE 6

EMPLOYER CONTRIBUTION RATES AS A PERCENTAGE OF MEMBERS' COMPENSATION*

EMPLOYER CONTRIBUTION

FISCAL YEAR ENDING SEPTEMBER 30, 2018

Tier I Tier II

Normal 2.43% 1.20%

Unfunded Actuarial Accrued Liability 9.45 9.45

Death Benefit 0.02 0.02 Term-Life 0.01 0.01 Administration 0.33 0.33 Total 12.24% 11.01%

* All members initially joining the System on and after January 1, 2013 are Tier II members.

Page 10

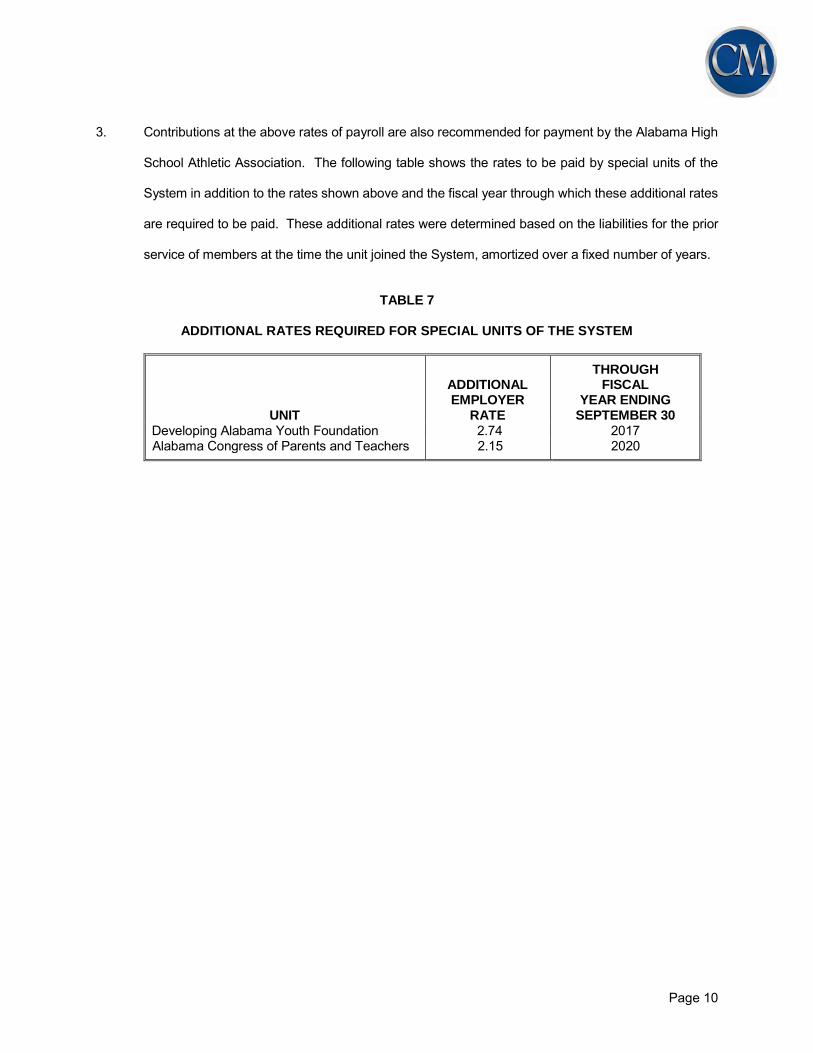

3. Contributions at the above rates of payroll are also recommended for payment by the Alabama High

School Athletic Association. The following table shows the rates to be paid by special units of the

System in addition to the rates shown above and the fiscal year through which these additional rates

are required to be paid. These additional rates were determined based on the liabilities for the prior

service of members at the time the unit joined the System, amortized over a fixed number of years.

TABLE 7

ADDITIONAL RATES REQUIRED FOR SPECIAL UNITS OF THE SYSTEM

UNIT

ADDITIONAL EMPLOYER

RATE

THROUGH FISCAL

YEAR ENDING SEPTEMBER 30

Developing Alabama Youth Foundation 2.74 2017 Alabama Congress of Parents and Teachers 2.15 2020

Page 11

SECTION VI – ANNUAL ACTUARIAL CERTIFICATION

The following is the annual actuarial certification to the Teachers' Retirement System of Alabama required

by Act 2000-732.

1. We hereby certify that there has been a change since the previous valuation in the liquidation period

used to determine the accrued liability contribution rate from 29.8 years to 29.5 years. The unfunded

actuarial accrued liability rate of 9.45% to be paid by employers to the Teachers' Retirement System of

Alabama has been determined in accordance with the Funding Policy adopted by the Board and shown

in Schedule G of this report.

Signed

Edward A. Macdonald, ASA, FCA, MAAA President

Page 12

SECTION VII – ANALYSIS OF FINANCIAL EXPERIENCE

The following table shows the estimated gain or loss from various factors that resulted in an increase of

$76,604,219 in the unfunded actuarial accrued liability from $10,027,958,472 to $10,104,562,691 during the

year ending September 30, 2015.

.

ANALYSIS OF FINANCIAL EXPERIENCE (in millions of dollars)

ITEM

AMOUNT OF INCREASE/

(DECREASE) IN UAAL

Interest (8.15%) added to previous UAAL $ 817.3 Accrued liability contribution* (650.8)

Experience: Valuation asset growth Pensioners' mortality Turnover and retirements New entrants Salary increases Method changes Amendments Interest Smoothing Miscellaneous changes

(212.9) 10.0 (3.1) 39.0 (307.1) 0.0 0.0 385.6 (1.4)

Total Increase/(Decrease) in UAAL

$ 76.6

*Equal to the total contributions made to the System less the normal cost for the year adjusted for interest to September 30, 2015 (($1,192,802,253 x 1.04075) – ($546,136,386 x 1.0815)).

Page 13

SECTION VIII - ACCOUNTING INFORMATION

The information required under Governmental Accounting Standard Board (GASB) Statements No. 67 and

68 will be issued in separate reports. The following information is provided for informational purposes only.

1. The following is a distribution of the number of employees by type of membership.

NUMBER OF ACTIVE AND RETIRED MEMBERS

AS OF SEPTEMBER 30, 2015

GROUP NUMBER

Retirees and beneficiaries currently receiving benefits

88,633

DROP participants 699 Terminated employees entitled to benefits but not yet receiving benefits

15,916

Non-vested inactive members who have not contributed for more than 5 years

29,071

Active members 135,986

Total 270,305

2. The schedule of funding progress is shown below.

SCHEDULE OF FUNDING PROGRESS (Dollar amounts in thousands)

Actuarial Actuarial Accrued Unfunded UAAL as a

Actuarial Value of Liability (AAL) AAL Funded Covered Percentage of Valuation Assets Entry Age (UAAL) Ratio Payroll Covered Payroll

Date ( a ) ( b ) ( b - a ) ( a / b ) ( c ) ( ( b - a ) / c )

9/30/2010 $20,132,779 $28,299,523 $8,166,744 71.1% $6,183,204 132.1% 9/30/20111 19,430,135 28,776,316 9,346,181 67.5 6,159,562 151.7 9/30/20122 18,786,008 28,251,367 9,465,359 66.5 6,222,316 152.1 9/30/2013 19,629,816 29,665,843 10,036,027 66.2 6,263,364 160.2 9/30/2014 20,809,871 30,837,829 10,027,958 67.5 6,335,161 158.3 9/30/2015 21,740,280 31,844,843 10,104,563 68.3 6,350,786 159.1

1Reflects changes in assumptions. 2Reflects changes in methods.

Page 14

3. The information presented above was determined as part of the actuarial valuation at

September 30, 2015. Additional information as of the latest actuarial valuation follows.

Valuation date 09/30/2015

Actuarial cost method Entry Age Normal

Amortization method Level percent closed Single equivalent remaining amortization period 29.5 years

Asset valuation method Five-year market related value Actuarial assumptions:

Ultimate Investment Rate of Return* 8.00%

Projected salary increases* 3.50 - 8.25%

Cost-of-living adjustments None

*Includes price inflation at 3.00%

Page 15

SCHEDULE A

VALUATION BALANCE SHEET SHOWING THE PRESENT AND PROSPECTIVE ASSETS AND LIABILITIES OF

THE TEACHERS' RETIREMENT SYSTEM OF ALABAMA AS OF SEPTEMBER 30, 2015

September 30, 2015

ASSETS

Actuarial Value of Assets $ 21,740,279,791 Present value of future members’ contributions to the

Annuity Savings Fund $ 3,560,025,802

Present value of future employer contributions to the Pension Accumulation Fund

Normal contributions $ 1,101,777,944 Unfunded actuarial accrued liability contributions 10,104,562,691 Total prospective employer contributions $ 11,206,340,635 Total Assets $ 36,506,646,228

LIABILITIES

Present value of benefits payable on account of retired members, beneficiaries of deceased members now drawing retirement allowances, and DROP participants

Service Retirements $ 17,072,238,046 Disability Retirements 528,596,856 Beneficiaries of Deceased Members 534,430,821 DROP Participant Accounts 485,984,412 Total $ 18,621,250,135 Inactive Members $ 585,925,616

Inactive T-Section Accounts $ 43,438,928 Present value of prospective benefits payable on account of present active members:

Service retirement allowances $ 15,507,381,139 Disability retirement allowances 609,644,230 Death Benefits 108,429,768 Termination Benefits 1,030,576,412 Total $ 17,256,031,549 Total Liabilities $ 36,506,646,228

Page 16

SCHEDULE A (continued)

SOLVENCY TEST

($1000’s)

Aggregate Accrued Liabilities For Portion of Accrued Liabilities Covered by Reported Asset

Valuation Date

(1) Active

Member Contributions

(2) Retirants

and Beneficiaries

(3) Active Members

(Employer Financed Portion)

Reported Assets

(1)

(2)

(3)

9/30/2015 $4,894,145 $18,621,250 $8,329,448 $21,740,280 100% 90% 0.0% 9/30/2014 4,589,021 18,104,369 8,144,439 20,809,871 100 90 0.0 9/30/2013 4,261,269 17,666,932 7,737,642 19,629,816 100 87 0.0 9/30/20121 3,921,179 17,085,972 7,244,216 18,786,008 100 87 0.0 9/30/20112 3,620,301 17,245,088 7,910,927 19,430,135 100 92 0.0 9/30/2010 3,498,959 16,083,293 8,717,271 20,132,779 100 100 6.3

1 Reflects changes in methods. 2 Reflects changes in actuarial assumptions.

Page 17

SCHEDULE B

DEVELOPMENT OF SEPTEMBER 30, 2015 ACTUARIAL VALUE OF ASSETS

(1) Actuarial Value of Assets on September 30, 2014 $ 20,809,871,128 (2) Market Value of Assets on September 30, 2015 21,574,652,720 (3) Market Value of Assets on September 30, 2014 22,253,817,957 (4) Net Cash Flow During the Fiscal Year a. Contributions 1,192,802,253 b. Benefit Payments and DROP Distributions 2,075,228,736 c. Refunds to Members 53,133,999 d. Transfer to Expense Fund – Interest Forfeiture 4,625,284 e. Investment Expenses 9,554,122 f. Net Cash Flow: (a. - b. - c. - d. - e.) (949,739,888) (5) Actual Investment Return ((2) - (3) - (4)f.) 270,574,651 (6) Assumed Rate of Return on Assets 8.00% (7) Amount for Immediate Recognition ((3) * (6)) + (((4)a. - (4)b. - (4)c. - (4)d.) * .5 * (6)) + (4)e.

1,752,252,128

(8) Investment Gain/(Loss) for the Fiscal Year ((5) - (7)) (1,481,677,477) (9) Phased-In Recognition of Investment Gain/(Loss) a. Current Fiscal Year: ( .2 * (8)) (296,335,495) b. Prior Fiscal Year 171,251,071 c. Second Prior Fiscal Year 252,980,847 d. Third Prior Fiscal Year 0 e. Fourth Prior Fiscal Year 0 f. Total Recognized Investment Gain/(Loss) for Fiscal Year 127,896,423 (10) Actuarial Value of Assets on September 30, 2015 ((1) + (4)f. + (7) + (9)f.)

$ 21,740,279,791

Date Investment Gain/(Loss)

Amount Recognized

Remaining Balance as of September 30, 2015

9/30/2013 $ 1,264,904,237 $ 758,942,541 $ 505,961,696 9/30/2014 856,255,357 342,502,142 513,753,215 9/30/2015 $ (1,481,677,477) $ (296,335,495) $ (1,185,341,982)

Page 18

SCHEDULE C

SUMMARY OF RECEIPTS AND DISBURSEMENTS FOR THE PERIOD ENDING SEPTEMBER 30, 2015

Receipts for the Period

Contributions: Members Employer

$ 477,917,619 714,884,634

Total $ 1,192,802,253

Investment Income 267,873,704*

TOTAL $ 1,460,675,957

Disbursements for the Period Benefit Payments Refunds to Members DROP Distributions Miscellaneous: Transfers from Plant Fund Transfers to Expense Fund –Interest Forfeiture Transfers to Expense Fund –Investment Expenses Transfers to Pre-retirement Death Benefit Fund

$ (28,027) 4,625,284 6,407,122

474,080

$ 1,862,163,274 53,133,999 213,065,462

Total 11,478,459

TOTAL $ 2,139,841,194

Excess of Receipts over Disbursements $ (679,165,237) Reconciliation of Asset Balances

Market Value of Assets as of September 30, 2014 $ 22,253,817,957

Excess of Receipts over Disbursements (679,165,237)

Market Value of Assets as of September 30, 2015 $ 21,574,652,720

*Net of $3,147,000 in investment expenses.

Page 19

SCHEDULE D

SMOOTHED INTEREST RATE

Actual Rate of Return for 5 Year Look Back Period

Fiscal Year Ending 9/30

Actual Rate of Return for Fiscal Year

2011 1.81 2012 18.30 2013 14.93 2014 12.13 2015 1.04

SMOOTHED INTEREST RATE: The assumed rate of return during the 25 year look forward period beginning on the valuation date. This is the investment rate of return expected to be earned during this period based on the actual rates earned during the five year look back period shown above such that the average rate of return over the combined 30 year period is equivalent to the ultimate investment rate of return (currently 8.00%). On this basis, for the September 30, 2015 valuation, the smoothed interest rate during the 25 year look forward period has been determined to be 7.72%. ULTIMATE INVESTMENT RATE OF RETURN: The assumed investment rate of return used in determining the smoothed interest rate described above. This is also the assumed investment rate of return after the 25 year look forward period and is currently 8.00%. CORRIDOR AROUND SMOOTHED INTEREST RATE: A corridor of 0.50% around the ultimate investment rate of return is applied in determining the smoothed interest rate. In addition, the limited smoothed interest rate may not increase or decrease by more than 1/8% each year. The smoothed interest rate used in the last valuation was 8.15%, therefore the corridor around the smoothed interest rate applied in the current valuation is 8.02% to 8.27%. LIMITED SMOOTHED INTEREST RATE: The assumed rate of return during the 25 year look forward period used for valuation purposes is limited by the application of the corridor above. Since the smoothed interest rate is 7.72%, the assumed rate for the first 25 years after the valuation date is outside the corridor. The smoothed interest rate for valuation purposes is limited to 8.02%

Page 20

SCHEDULE E

OUTLINE OF ACTUARIAL ASSUMPTIONS AND METHODS

The assumptions and methods used in the valuation were selected based on the actuarial experience study prepared as of September 30, 2010, submitted to and adopted by the Board on January 27, 2012. ULTIMATE INVESTMENT RATE OF RETURN: 8.00% per annum, compounded annually, including price inflation at 3%. SALARY INCREASES: Representative values of the assumed annual rates of future salary increases are as follows and include wage inflation at 3.25% per annum:

Service Annual Rate Service Annual Rate

0 8.25 % 6 5.00 % 1 6.50 7 4.75 2 5.75 8 to 13 4.50 3 5.50 14 to 18 4.00 4 5.25 19 & Over 3.50 5 5.00

SEPARATIONS BEFORE SERVICE RETIREMENT: Representative values of the assumed annual rates of death, disability, and withdrawal are as follows:

Annual Rate of Age Death* Disability Withdrawal

Years of Service Years of Service 0-24 25+ 0-4 5-9 10-20 20+

Male

20 25 30 35 40 45 50 55 60 65 69

0.02% 0.02 0.03 0.05 0.07 0.09 0.12 0.20 0.40 0.77 1.20

0.04%

0.10% 0.10 0.10 0.10

30.00% 0.05 15.68 10.00% 0.05 14.25 5.40 5.00% 0.10 14.25 5.40 3.00 0.18 14.00 5.40 2.50 1.00% 0.31 14.00 5.00 2.50 1.00 0.51 12.50 4.50 2.50 1.00 0.96 12.00 4.00 2.50 1.00 0.50 12.00 4.00

12.00 6.00 12.00 6.00

Female

20 25 30 35 40 45 50 55 60 65 69

0.01% 0.01 0.01 0.02 0.03 0.04 0.06 0.11 0.21 0.40 0.62

0.10%

0.15% 0.15 0.15 0.25

28.50% 0.10 14.00 8.00% 0.10 14.00 5.80 4.00% 0.15 14.00 5.00 3.00 0.16 12.00 4.50 2.10 1.10% 0.33 11.50 3.75 2.10 0.75 0.63 11.00 3.75 2.10 0.75 0.99 11.00 3.75 2.50 0.75 0.25 12.00 4.50 14.00 6.00

14.00 6.00 * Rates of pre-retirement mortality are according to the sex distinct RP-2000 Combined Mortality Table Projected with

Scale AA to 2015 set back one year for females with an adjustment of factor of 0.75 for males and 0.50 for females.

Page 21

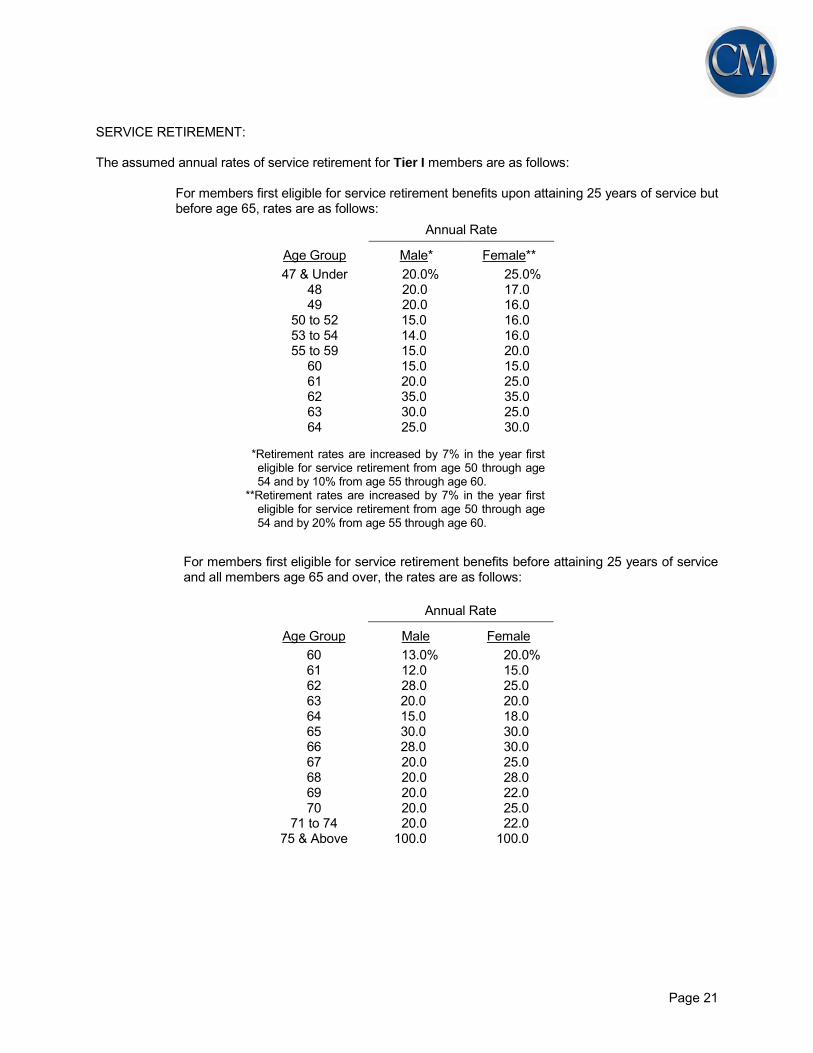

SERVICE RETIREMENT: The assumed annual rates of service retirement for Tier I members are as follows:

For members first eligible for service retirement benefits upon attaining 25 years of service but before age 65, rates are as follows:

Annual Rate

Age Group Male* Female** 47 & Under

48 49

50 to 52 53 to 54 55 to 59

60 61 62 63 64

20.0% 20.0 20.0 15.0 14.0 15.0 15.0 20.0 35.0 30.0 25.0

25.0% 17.0 16.0 16.0 16.0 20.0 15.0 25.0 35.0 25.0 30.0

*Retirement rates are increased by 7% in the year first eligible for service retirement from age 50 through age 54 and by 10% from age 55 through age 60.

**Retirement rates are increased by 7% in the year first eligible for service retirement from age 50 through age 54 and by 20% from age 55 through age 60.

For members first eligible for service retirement benefits before attaining 25 years of service and all members age 65 and over, the rates are as follows:

Annual Rate

Age Group Male Female 60 61 62 63 64 65 66

13.0% 12.0 28.0 20.0 15.0 30.0 28.0

20.0% 15.0 25.0 20.0 18.0 30.0 30.0

67 20.0 25.0 68 20.0 28.0 69 20.0 22.0 70 20.0 25.0

71 to 74 20.0 22.0 75 & Above 100.0 100.0

Page 22

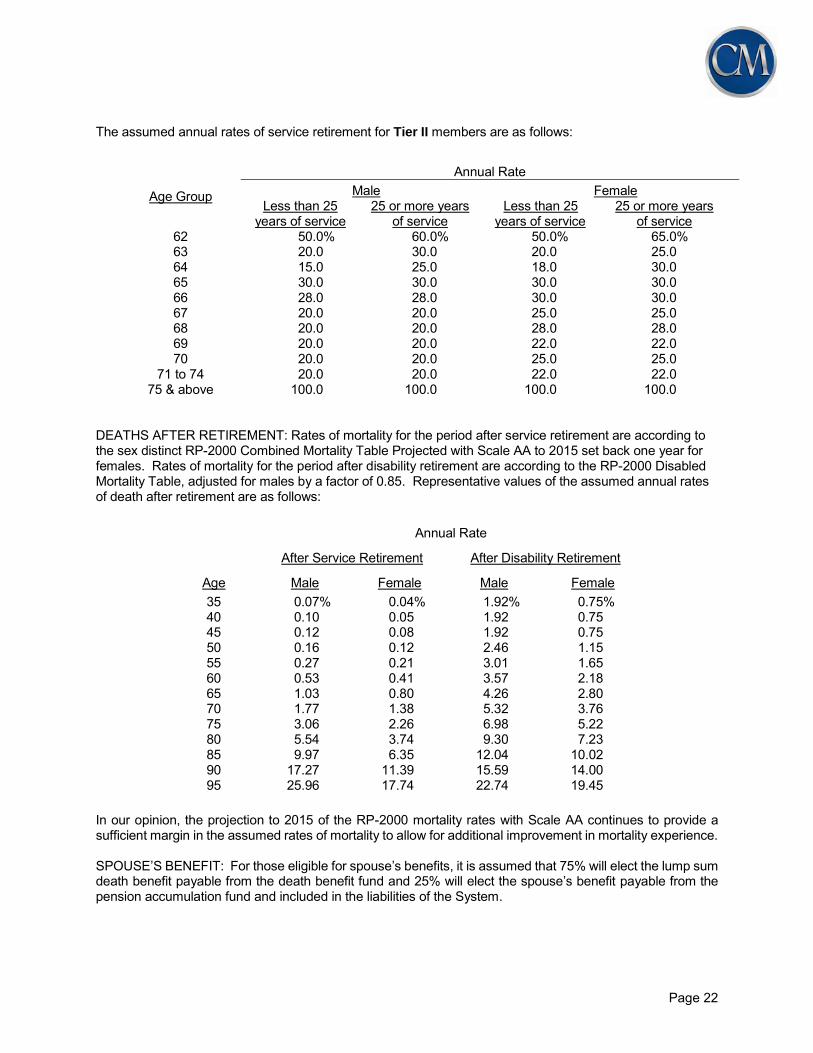

The assumed annual rates of service retirement for Tier II members are as follows:

Age Group

Annual Rate Male Female

Less than 25 years of service

25 or more years of service

Less than 25 years of service

25 or more years of service

62 50.0% 60.0% 50.0% 65.0% 63 20.0 30.0 20.0 25.0 64 15.0 25.0 18.0 30.0 65 30.0 30.0 30.0 30.0 66 28.0 28.0 30.0 30.0 67 20.0 20.0 25.0 25.0 68 20.0 20.0 28.0 28.0 69 20.0 20.0 22.0 22.0 70 20.0 20.0 25.0 25.0

71 to 74 20.0 20.0 22.0 22.0 75 & above 100.0 100.0 100.0 100.0

DEATHS AFTER RETIREMENT: Rates of mortality for the period after service retirement are according to the sex distinct RP-2000 Combined Mortality Table Projected with Scale AA to 2015 set back one year for females. Rates of mortality for the period after disability retirement are according to the RP-2000 Disabled Mortality Table, adjusted for males by a factor of 0.85. Representative values of the assumed annual rates of death after retirement are as follows:

Annual Rate

After Service Retirement After Disability Retirement

Age Male Female Male Female 35 40 45 50 55 60 65 70 75 80 85 90 95

0.07% 0.10 0.12 0.16 0.27 0.53 1.03 1.77 3.06 5.54 9.97 17.27 25.96

0.04% 0.05 0.08 0.12 0.21 0.41 0.80 1.38 2.26 3.74 6.35 11.39 17.74

1.92% 1.92 1.92 2.46 3.01 3.57 4.26 5.32 6.98 9.30 12.04 15.59 22.74

0.75% 0.75 0.75 1.15 1.65 2.18 2.80 3.76 5.22 7.23 10.02 14.00 19.45

In our opinion, the projection to 2015 of the RP-2000 mortality rates with Scale AA continues to provide a sufficient margin in the assumed rates of mortality to allow for additional improvement in mortality experience. SPOUSE’S BENEFIT: For those eligible for spouse’s benefits, it is assumed that 75% will elect the lump sum death benefit payable from the death benefit fund and 25% will elect the spouse’s benefit payable from the pension accumulation fund and included in the liabilities of the System.

Page 23

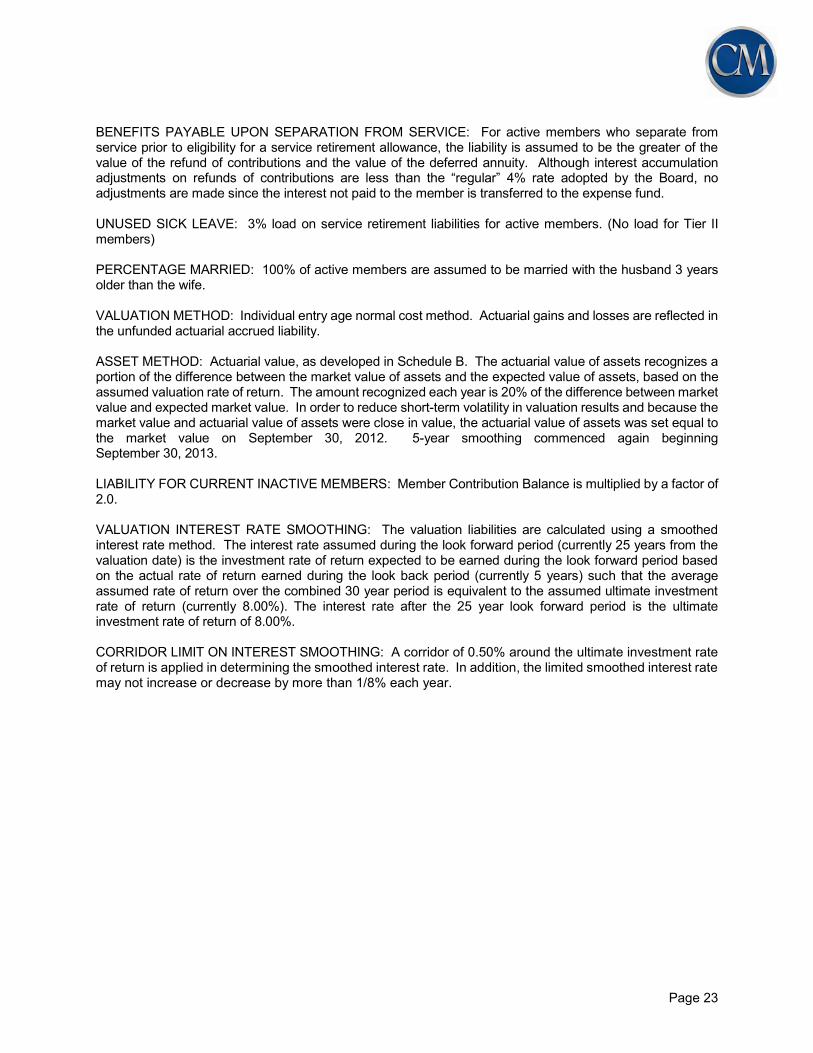

BENEFITS PAYABLE UPON SEPARATION FROM SERVICE: For active members who separate from service prior to eligibility for a service retirement allowance, the liability is assumed to be the greater of the value of the refund of contributions and the value of the deferred annuity. Although interest accumulation adjustments on refunds of contributions are less than the “regular” 4% rate adopted by the Board, no adjustments are made since the interest not paid to the member is transferred to the expense fund. UNUSED SICK LEAVE: 3% load on service retirement liabilities for active members. (No load for Tier II members) PERCENTAGE MARRIED: 100% of active members are assumed to be married with the husband 3 years older than the wife. VALUATION METHOD: Individual entry age normal cost method. Actuarial gains and losses are reflected in the unfunded actuarial accrued liability. ASSET METHOD: Actuarial value, as developed in Schedule B. The actuarial value of assets recognizes a portion of the difference between the market value of assets and the expected value of assets, based on the assumed valuation rate of return. The amount recognized each year is 20% of the difference between market value and expected market value. In order to reduce short-term volatility in valuation results and because the market value and actuarial value of assets were close in value, the actuarial value of assets was set equal to the market value on September 30, 2012. 5-year smoothing commenced again beginning September 30, 2013. LIABILITY FOR CURRENT INACTIVE MEMBERS: Member Contribution Balance is multiplied by a factor of 2.0. VALUATION INTEREST RATE SMOOTHING: The valuation liabilities are calculated using a smoothed interest rate method. The interest rate assumed during the look forward period (currently 25 years from the valuation date) is the investment rate of return expected to be earned during the look forward period based on the actual rate of return earned during the look back period (currently 5 years) such that the average assumed rate of return over the combined 30 year period is equivalent to the assumed ultimate investment rate of return (currently 8.00%). The interest rate after the 25 year look forward period is the ultimate investment rate of return of 8.00%. CORRIDOR LIMIT ON INTEREST SMOOTHING: A corridor of 0.50% around the ultimate investment rate of return is applied in determining the smoothed interest rate. In addition, the limited smoothed interest rate may not increase or decrease by more than 1/8% each year.

Page 24

SCHEDULE F

ACTUARIAL COST METHOD

1. The valuation is prepared on the projected benefit basis, under which the present value, at the interest

rate assumed to be earned in the future (see Schedules D and E for a description of the interest rate

used), of each member's expected benefit payable at retirement or death is determined, based on his

age, service, sex and compensation. The calculations take into account the probability of a member's

death or termination of employment prior to becoming eligible for a benefit, as well as the probability

of his terminating with a service, disability or survivor's benefit. Future salary increases are also

anticipated. The present value of the expected benefits payable on account of the active members

is added to the present value of the expected future payments to retired members and beneficiaries

to obtain the present value of all expected benefits payable from the System on account of the present

group of members and beneficiaries.

2. The employer contributions required to support the benefits of the System are determined following

a level funding approach, and consist of a normal contribution and an accrued liability contribution.

3. The normal contribution is determined using the "individual entry age normal" method. Under this

method, a calculation is made to determine the uniform and constant percentage rate of employer

contribution which, if applied to the compensation of the each new member during the entire period

of his anticipated covered service, would be required in addition to the contributions of the member

to meet the cost of all benefits payable on his behalf.

4. The unfunded actuarial accrued liability contributions are determined by subtracting the present value

of prospective employer normal contributions and member contributions together with the current

assets held from the present value of expected benefits to be paid from the System.

Page 25

SCHEDULE G

BOARD FUNDING POLICY

The purpose of the funding policy is to state the overall funding objectives for the Teachers’ Retirement System of Alabama (System), the benchmarks that will be used to measure progress in achieving those goals, and the methods and assumptions that will be employed to develop the benchmarks. The funding policy reflects the Board’s long-term strategy for stability in funding of the plan. For that reason, it is critical that this funding policy remain unchanged until its objectives are met. I. Funding Objectives The goal in requiring employer and member contributions to the System is to accumulate sufficient assets during a member’s employment to fully finance the benefits the member is expected to receive throughout retirement. In meeting this objective, the System will strive to meet the following funding objectives:

To maintain an increasing funded ratio (ratio of system actuarial value of assets to actuarial accrued liabilities) that reflects a trend of improved actuarial condition. The long-term objective is to attain a funded ratio which is consistent with the fiscal health and long-term stability of the System.

To maintain adequate asset levels to finance the benefits promised to members and monitor the future demands for liquidity.

To develop a pattern of contribution rates expressed as a percentage of member payroll as measured by valuations prepared in accordance with applicable State laws and the principles of practice prescribed by the Actuarial Standards Board. In no event will the employer contribution rate be negative.

To provide intergenerational equity for taxpayers with respect to System costs.

II. Benchmarks To track progress in achieving the previously outlined funding objectives, the following benchmarks will be measured annually as of the valuation date. The valuation date is the date that the annual actuarial valuation of the System’s assets and liabilities is prepared. This date is currently September 30th each year with due recognition that a single year’s results may not be indicative of long-term trends:

Funded ratio – The funded ratio, defined as the actuarial value of assets divided by the actuarial accrued liability, should increase over time, before adjustments for changes in benefits, actuarial methods, and/or actuarial assumptions. An open amortization period is one for which the amortization period is recalculated on a yearly basis and the ending date of the amortization period is a variable with each recalculation. A closed amortization period is one which is calculated over a fixed period and at the end of that period, the amount is fully amortized.

Unfunded Actuarial Accrued Liability (UAAL) Transitional UAAL - The UAAL established as of the initial valuation date for which this

funding policy is adopted shall be known as the Transitional UAAL (applicable only to employers participating in the System as of the adoption date of the funding policy).

New Incremental UAAL - Each subsequent valuation will produce a New Incremental UAAL consisting of all benefit changes, assumption and method changes and experience gains and/or losses that have occurred since the previous valuation.

UAAL Amortization Period and Contribution Rates In each valuation 1/15th of the Transitional UAAL will be amortized over a closed period.

The closed period shall be the amortization period for the valuation preceding the adoption of the funding policy not to exceed 30 years. The remaining Transitional UAAL each year will be amortized over an open period. The open period shall be the amortization period for the valuation preceding the adoption of the funding policy not to exceed 30 years. After 15 years the entire Transitional UAAL will be closed.

Each New Incremental UAAL shall be amortized over a closed 30 year period. Employer Normal Contribution Rate – the contribution rate determined as of the valuation

date each year based on the provisions of Alabama Code Section 16-25-21. In each valuation subsequent to the adoption of this funding policy the required employer

contribution rate will be determined by the summation of the employer Normal Contribution Rate, a contribution rate for administrative expenses, a contribution rate for the

Page 26

pre-retirement death benefit fund, a contribution rate for the term life insurance fund, the individual amortization rate for each of the New Incremental UAAL bases, the individual amortization rate for each of the 15 closed periods for the Transitional UAAL and the amortization of any remaining open portion of the Transitional UAAL.

UAAL Amortization Period for Employers joining the System after the Implementation of this Funding Policy

For Employers joining the System after the implementation of this Funding Policy, the employer contribution rate shall be computed as the sum of the employer Normal Contribution rate, a contribution rate for administrative expenses, a contribution rate for the pre-retirement death benefit fund, a contribution rate for the term life insurance fund, and the initial UAAL contribution rate. The initial UAAL contribution rate shall be determined by amortizing the initial UAAL over a closed period equal to the expected future working lifetime of the active membership. This initial amortization period shall not be less than 10 years nor greater than 30 years.

In subsequent years the UAAL and employer contribution rate shall be determined in accordance with the rules of the Funding Policy described in the previous section.

III. Methods and Assumptions The actuarial funding method used to develop the benchmarks will be the Entry Age Normal (EAN) actuarial cost method. The actuarial methods and assumptions used will be those last adopted by the Board based upon the advice and recommendation of the actuary including the Interest Smoothing methodology. The actuary shall conduct an investigation into the system’s experience at least every five years and utilize the results of the investigation to form the basis for those recommendations which shall include the Interest Smoothing Methodology. IV. Funding Policy Progress The Board will periodically have projections of funded status performed to assess the current and expected future progress towards the overall funding goals of the System.

Page 27

SCHEDULE H

PROJECTION OF TRANSITIONAL UAAL AND AMORTIZATION OF BASES

PROJECTION OF THE OPEN TRANSITIONAL UAAL

Valuation Date

Transitional UAAL

Beginning of Year

Transitional Closed

Transitional Remaining Open 8% Interest

Amortization Payment

Transitional Open UAAL End of Year

(1) (2) (3)=(1)-(2) (4)=(3)*.08 (5) (6)=(3)+(4)-(5)

9/30/2012 $9,465,359,317 $631,023,954 $8,834,335,363 $706,746,829 $566,618,173 $8,974,464,019 9/30/2013 8,974,464,019 641,033,144 8,333,430,875 666,674,470 534,491,072 8,465,614,273 9/30/2014 8,465,614,273 651,201,098 7,814,413,175 625,153,054 501,202,222 7,938,364,007 9/30/2015 7,938,364,007 661,530,334 7,276,833,673 582,146,694 466,722,853 7,392,257,515 9/30/2016 7,392,257,515 672,023,410 6,720,234,104 537,618,728 431,023,570 6,826,829,262 9/30/2017 6,826,829,262 682,682,926 6,144,146,336 491,531,707 394,074,351 6,241,603,692 9/30/2018 6,241,603,692 693,511,521 5,548,092,171 443,847,374 355,844,523 5,636,095,022 9/30/2019 5,636,095,022 704,511,878 4,931,583,144 394,526,652 316,302,757 5,009,807,039 9/30/2020 5,009,807,039 715,686,720 4,294,120,319 343,529,626 275,417,053 4,362,232,892 9/30/2021 4,362,232,892 727,038,815 3,635,194,077 290,815,526 233,154,724 3,692,854,879 9/30/2022 3,692,854,879 738,570,976 2,954,283,903 236,342,712 189,482,386 3,001,144,229 9/30/2023 3,001,144,229 750,286,057 2,250,858,172 180,068,654 144,365,942 2,286,560,884 9/30/2024 2,286,560,884 762,186,961 1,524,373,923 121,949,914 97,770,566 1,548,553,271 9/30/2025 1,548,553,271 774,276,635 774,276,636 61,942,131 49,660,693 786,558,074 9/30/2026 786,558,074 786,558,074 0 0 0 0

Page 28

SCHEDULE H (continued)

AMORTIZATION SCHEDULE FOR BASE CLOSED ON SEPTEMBER 30, 2012

Valuation Date

Balance of Transitional

Closed 9/30/2012

Annual Amortization

Payment

9/30/2012 $631,023,954 $40,472,727 9/30/2013 641,033,144 41,788,090 9/30/2014 650,527,705 43,146,203 9/30/2015 659,423,718 44,548,455 9/30/2016 667,629,161 45,996,280 9/30/2017 675,043,214 47,491,159 9/30/2018 681,555,513 49,034,621 9/30/2019 687,045,333 50,628,246 9/30/2020 691,380,713 52,273,664 9/30/2021 694,417,505 53,972,559 9/30/2022 695,998,347 55,726,667 9/30/2023 695,951,548 57,537,783 9/30/2024 694,089,889 59,407,761 9/30/2025 690,209,318 61,338,514 9/30/2026 684,087,550 63,332,015 9/30/2027 675,482,539 65,390,306 9/30/2028 664,130,836 67,515,491 9/30/2029 649,745,812 69,709,744 9/30/2030 632,015,733 71,975,311 9/30/2031 610,601,681 74,314,508 9/30/2032 585,135,307 76,729,730 9/30/2033 555,216,402 79,223,446 9/30/2034 520,410,267 81,798,208 9/30/2035 480,244,881 84,456,650 9/30/2036 434,207,821 87,201,491 9/30/2037 381,742,956 90,035,540 9/30/2038 322,246,853 92,961,695 9/30/2039 255,064,906 95,982,950 9/30/2040 179,487,149 99,102,396 9/30/2041 94,743,725 102,323,223 9/30/2042 0 0

Page 29

SCHEDULE H (continued)

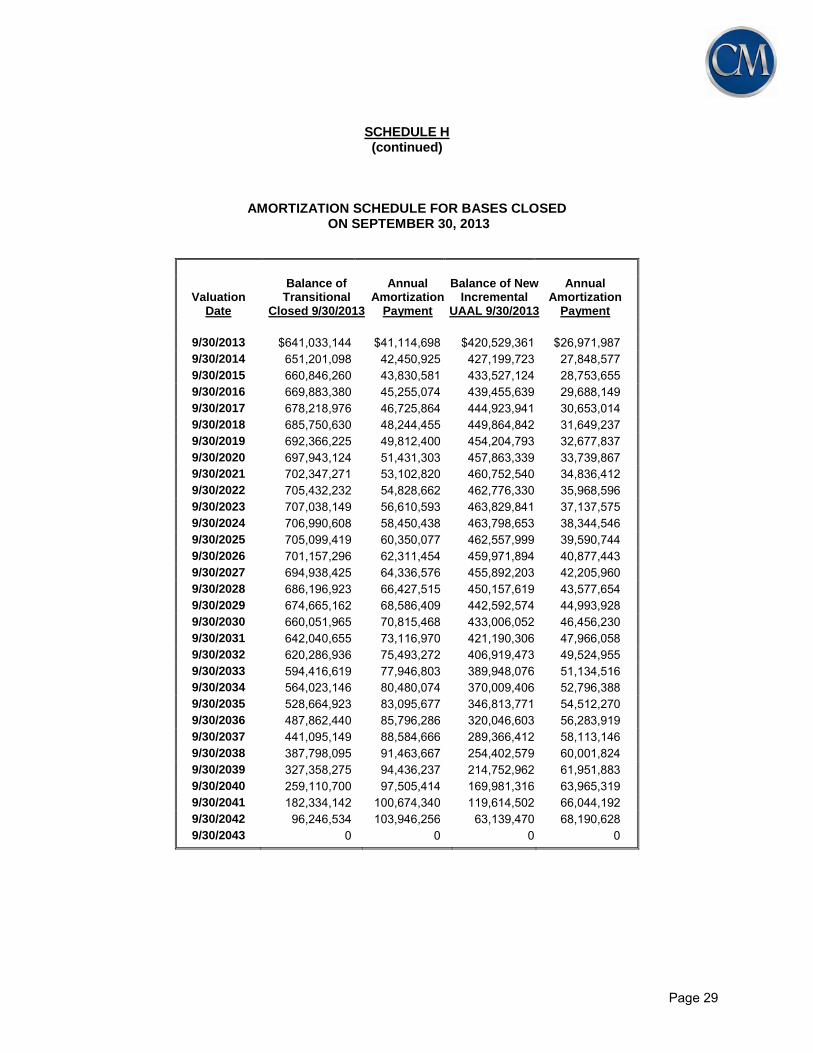

AMORTIZATION SCHEDULE FOR BASES CLOSED ON SEPTEMBER 30, 2013

Valuation Date

Balance of Transitional

Closed 9/30/2013

Annual Amortization

Payment

Balance of New Incremental

UAAL 9/30/2013

Annual Amortization

Payment

9/30/2013 $641,033,144 $41,114,698 $420,529,361 $26,971,987 9/30/2014 651,201,098 42,450,925 427,199,723 27,848,577 9/30/2015 660,846,260 43,830,581 433,527,124 28,753,655 9/30/2016 669,883,380 45,255,074 439,455,639 29,688,149 9/30/2017 678,218,976 46,725,864 444,923,941 30,653,014 9/30/2018 685,750,630 48,244,455 449,864,842 31,649,237 9/30/2019 692,366,225 49,812,400 454,204,793 32,677,837 9/30/2020 697,943,124 51,431,303 457,863,339 33,739,867 9/30/2021 702,347,271 53,102,820 460,752,540 34,836,412 9/30/2022 705,432,232 54,828,662 462,776,330 35,968,596 9/30/2023 707,038,149 56,610,593 463,829,841 37,137,575 9/30/2024 706,990,608 58,450,438 463,798,653 38,344,546 9/30/2025 705,099,419 60,350,077 462,557,999 39,590,744 9/30/2026 701,157,296 62,311,454 459,971,894 40,877,443 9/30/2027 694,938,425 64,336,576 455,892,203 42,205,960 9/30/2028 686,196,923 66,427,515 450,157,619 43,577,654 9/30/2029 674,665,162 68,586,409 442,592,574 44,993,928 9/30/2030 660,051,965 70,815,468 433,006,052 46,456,230 9/30/2031 642,040,655 73,116,970 421,190,306 47,966,058 9/30/2032 620,286,936 75,493,272 406,919,473 49,524,955 9/30/2033 594,416,619 77,946,803 389,948,076 51,134,516 9/30/2034 564,023,146 80,480,074 370,009,406 52,796,388 9/30/2035 528,664,923 83,095,677 346,813,771 54,512,270 9/30/2036 487,862,440 85,796,286 320,046,603 56,283,919 9/30/2037 441,095,149 88,584,666 289,366,412 58,113,146 9/30/2038 387,798,095 91,463,667 254,402,579 60,001,824 9/30/2039 327,358,275 94,436,237 214,752,962 61,951,883 9/30/2040 259,110,700 97,505,414 169,981,316 63,965,319 9/30/2041 182,334,142 100,674,340 119,614,502 66,044,192 9/30/2042 96,246,534 103,946,256 63,139,470 68,190,628 9/30/2043 0 0 0 0

Page 30

SCHEDULE H (continued)

AMORTIZATION SCHEDULE FOR BASES CLOSED ON SEPTEMBER 30, 2014

Valuation Date

Balance of Transitional

Closed 9/30/2014

Annual Amortization

Payment

Balance of New Incremental

UAAL 9/30/2014

Annual Amortization

Payment

9/30/2014 $651,201,098 $41,766,852 $(166,584,327) $(10,684,415) 9/30/2015 661,530,334 43,124,275 (169,226,658) (11,031,659) 9/30/2016 671,328,486 44,525,813 (171,733,132) (11,390,188) 9/30/2017 680,508,952 45,972,902 (174,081,595) (11,760,369) 9/30/2018 688,976,765 47,467,022 (176,247,754) (12,142,581) 9/30/2019 696,627,885 49,009,700 (178,204,993) (12,537,215) 9/30/2020 703,348,416 50,602,515 (179,924,178) (12,944,674) 9/30/2021 709,013,774 52,247,097 (181,373,439) (13,365,376) 9/30/2022 713,487,779 53,945,128 (182,517,938) (13,799,751) 9/30/2023 716,621,673 55,698,344 (183,319,622) (14,248,243) 9/30/2024 718,253,063 57,508,540 (183,736,949) (14,711,310) 9/30/2025 718,204,768 59,377,568 (183,724,595) (15,189,428) 9/30/2026 716,283,581 61,307,339 (183,233,134) (15,683,084) 9/30/2027 712,278,929 63,299,827 (182,208,701) (16,192,785) 9/30/2028 705,961,415 65,357,072 (180,592,612) (16,719,050) 9/30/2029 697,081,257 67,481,177 (178,320,971) (17,262,419) 9/30/2030 685,366,581 69,674,315 (175,324,229) (17,823,448) 9/30/2031 670,521,592 71,938,730 (171,526,720) (18,402,710) 9/30/2032 652,224,589 74,276,739 (166,846,147) (19,000,798) 9/30/2033 630,125,818 76,690,733 (161,193,041) (19,618,324) 9/30/2034 603,845,150 79,183,182 (154,470,160) (20,255,920) 9/30/2035 572,969,581 81,756,635 (146,571,854) (20,914,237) 9/30/2036 537,050,512 84,413,726 (137,383,365) (21,593,950) 9/30/2037 495,600,827 87,157,172 (126,780,085) (22,295,753) 9/30/2038 448,091,721 89,989,780 (114,626,738) (23,020,365) 9/30/2039 393,949,279 92,914,448 (100,776,512) (23,768,527) 9/30/2040 332,550,774 95,934,167 (85,070,107) (24,541,004) 9/30/2041 263,220,668 99,052,028 (67,334,711) (25,338,587) 9/30/2042 185,226,294 102,271,219 (47,382,902) (26,162,091) 9/30/2043 97,773,179 105,595,033 (25,011,443) (27,012,359) 9/30/2044 0 0 0 0

Page 31

SCHEDULE H (continued)

AMORTIZATION SCHEDULE FOR BASES CLOSED ON SEPTEMBER 30, 2015

Valuation Date

Balance of Transitional

Closed 9/30/2015

Annual Amortization

Payment

Balance of New Incremental

UAAL 9/30/2015

Annual Amortization

Payment

9/30/2015 $661,530,334 $42,429,350 $(79,902,094) $(5,124,775) 9/30/2016 672,023,410 43,808,304 (81,169,487) (5,291,330) 9/30/2017 681,976,979 45,232,074 (82,371,716) (5,463,298) 9/30/2018 691,303,064 46,702,116 (83,498,155) (5,640,855) 9/30/2019 699,905,192 48,219,935 (84,537,152) (5,824,183) 9/30/2020 707,677,672 49,787,083 (85,475,941) (6,013,469) 9/30/2021 714,504,803 51,405,163 (86,300,547) (6,208,907) 9/30/2022 720,260,024 53,075,831 (86,995,684) (6,410,696) 9/30/2023 724,804,995 54,800,796 (87,544,643) (6,619,044) 9/30/2024 727,988,599 56,581,821 (87,929,170) (6,834,163) 9/30/2025 729,645,865 58,420,731 (88,129,341) (7,056,273) 9/30/2026 729,596,804 60,319,404 (88,123,415) (7,285,602) 9/30/2027 727,645,144 62,279,785 (87,887,687) (7,522,384) 9/30/2028 723,576,970 64,303,878 (87,396,317) (7,766,862) 9/30/2029 717,159,250 66,393,754 (86,621,161) (8,019,285) 9/30/2030 708,138,236 68,551,551 (85,531,570) (8,279,911) 9/30/2031 696,237,744 70,779,477 (84,094,184) (8,549,008) 9/30/2032 681,157,287 73,079,809 (82,272,710) (8,826,851) 9/30/2033 662,570,060 75,454,903 (80,027,676) (9,113,724) 9/30/2034 640,120,761 77,907,188 (77,316,166) (9,409,920) 9/30/2035 613,423,235 80,439,171 (74,091,540) (9,715,742) 9/30/2036 582,057,922 83,053,444 (70,303,121) (10,031,504) 9/30/2037 545,569,112 85,752,681 (65,895,866) (10,357,528) 9/30/2038 503,461,959 88,539,643 (60,810,008) (10,694,147) 9/30/2039 455,199,273 91,417,182 (54,980,661) (11,041,707) 9/30/2040 400,198,033 94,388,240 (48,337,407) (11,400,563) 9/30/2041 337,825,635 97,455,858 (40,803,837) (11,771,081) 9/30/2042 267,395,828 100,623,173 (32,297,063) (12,153,641) 9/30/2043 188,164,321 103,893,427 (22,727,186) (12,548,634) 9/30/2044 99,324,040 107,269,963 (11,996,727) (12,956,465) 9/30/2045 0 0 0 0

Page 32

SCHEDULE I

SUMMARY OF MAIN PLAN PROVISIONS AS INTERPRETED FOR VALUATION PURPOSES

The Teachers' Retirement System of Alabama was established on September 15, 1939 and went into effect

September 30, 1941. The valuation took into account amendments to the System through the valuation date.

There is a new tier (Tier II) of benefits for all members initially joining the System on and after

January 1, 2013. The following summary describes the main benefit and contribution provisions of the System

as interpreted for the valuation.

1 - DEFINITIONS

Average Final Compensation - the average compensation of a member for:

Tier I – the 3 highest years in the last 10 years of Creditable Service Tier II – the 5 highest years in the last 10 years of Creditable Service

Membership Service – all service rendered while a member of the retirement system and for which contributions are made. Creditable Service – the sum of membership service, prior service, and any other service established as creditable in accordance with the provisions of the retirement law. Annuity – payments for life derived from accumulated contributions of a member. Pension – payments for life derived from employer contributions. Retirement Allowance – the sum of the annuity and pension. 2 - BENEFITS Service Retirement Allowance Condition for Allowance Tier I A retirement allowance is payable upon the request of any

member who has completed 25 years of creditable service or who has attained age 60 and completed at least 10 years of creditable service.

Tier II A retirement allowance is payable upon the request of any

member who has attained age 62 and completed at least 10 years of creditable service (age 56 with 10 years of creditable service for a full-time certified firefighter, police officer or correctional officer).

Page 33

Amount of Allowance Tier I Upon service retirement a member receives a retirement

allowance equal to 2.0125% of the member's average final compensation multiplied by the number of years of creditable service. At retirement, a member receives one additional year of creditable service in determining the retirement allowance for each five years of service as a full-time certified firefighter, police officer or correctional officer.

Tier II Upon service retirement a member receives a retirement

allowance equal to 1.65% of the member's average final compensation multiplied by the number of years of creditable service. The benefit is capped at 80% of the member’s average final compensation.

Both The member may elect to receive a reduced retirement

allowance in order to provide an allowance to a designated beneficiary after the member’s death (see “Special Privileges at Retirement” below).

Disability Retirement Allowance Condition for Allowance A disability retirement allowance may be granted to a

member who has 10 years or more of creditable service who becomes totally and permanently incapacitated for duty before reaching eligibility for a service retirement allowance.

Amount of Allowance Tier I On retirement for disability, a member receives a retirement

allowance equal to 2.0125% of the member's average final compensation multiplied by the number of years of creditable service. At retirement, a member receives one additional year of creditable service in determining the retirement allowance for each five years of service as a full-time certified firefighter, police officer or correctional officer.

Tier II Upon disability retirement a member receives a retirement

allowance equal to 1.65% of the member's average final compensation multiplied by the number of years of creditable service. The benefit is capped at 80% of the member’s average final compensation.

Both The member may elect to receive a reduced retirement

allowance in order to provide an allowance to a designated beneficiary after the member’s death (see “Special Privileges at Retirement” below).

Page 34

Benefits Payable on Separation from Service Any member who withdraws from service is entitled to

receive his or her contributions with allowable interest. A member who has completed 10 years of creditable service may, after separation from service, continue in the membership of the System and file for service retirement after reaching age 60 (age 62 for Tier II members).

Benefits Payable upon Death in Active Service In the event of the death of a member eligible for service

retirement, the designated beneficiary may elect (1) to exercise Option 3 defined below under “Special Privileges at Retirement” or (2) to receive a return of member contributions and total earned interest plus a death benefit payable from the pre-retirement death benefit fund equal to the salary on which the member made retirement contributions for the previous scholastic year (July 1-June 30).*

In the event of the death of a member with more than one

year of service who is not eligible to retire, the designated beneficiary shall receive the return of member contributions and total earned interest. Also, the designated beneficiary shall receive an additional death benefit payable from the pre-retirement death benefit fund equal to the salary on which retirement contributions were made for the previous scholastic year (July 1-June 30).*

In the event of a job-related death of a member with less

than one year of service, the designated beneficiary shall receive the return of member contributions and total earned interest plus a death benefit payable from the pre-retirement death benefit fund equal to the annual earnable compensation of the member at the time of death.*

In the event of the death of a member with less than one

year of service that is not job-related, the designated beneficiary shall receive the return of member contributions and total earned interest plus a matching death benefit which is limited to a $5,000 maximum.

*However, if the death occurred more than 180 calendar

days after the member’s last day in pay status, or if the deceased had applied for a refund of contributions or terminated employment, the lump sum will be the same as if the member had less than one year of service and the death was not job-related.

Page 35

Special Privileges at Retirement In lieu of the full retirement allowance, any member may, at

retirement, elect to receive a reduced retirement allowance equal in value to the full allowance, with the provision that:

Option 1 - If the member dies before annuity payments have

equaled the present value of the annuity at the date of retirement, the balance is paid to a designated beneficiary or to his estate, or

Option 2 - After the member’s death, the member’s allowance

is continued throughout the life of the designated beneficiary, or

Option 3 - After the member’s death, one-half of the

member’s allowance is continued throughout the life of the designated beneficiary, or

Option 4 - Some other benefit is paid either to the member

or to such other person as the member shall designate provided such benefit, together with the reduced retirement allowance, is of equivalent actuarial value to his retirement allowance and is approved by the Board of Control.

Deferred Retirement Option Plan (DROP) Prior to March 25, 2011, a member may elect to participate

in the Deferred Retirement Option Plan (DROP) upon completion of at least 25 years of creditable service (excluding sick leave) and attainment of at least 55 years of age. Under the DROP, the member may defer receipt of a retirement allowance and continue employment for a period not to exceed five years, nor to be less than three years. At the end of this period, the member will withdraw from active service and receive the retirement benefit calculated at the time of enrollment in the DROP, and also receive a payment for the deferred retirement benefits, employee contributions while participating in the DROP and interest earned on DROP deposits.

The effect of Act 2011-27 is that no new participants will be

allowed to enter DROP with an effective participation date after June 1, 2011.

Term Life Insurance Upon the death of a contributing member there is paid a term

life insurance benefit of $15,000 (pro-rated for part-time members)

Page 36

Member Contributions Tier I Prior to October 1, 2011, regular members contributed 5.0%

of salary and certified police officers, firefighters and correctional officers contributed 6.0% of salary. DROP participants continue to contribute during the DROP period, but receive a refund of these contributions and regular interest upon retirement.

Beginning October 1, 2011, the contribution rates were increased to 7.25% for regular members and 8.25% for police officers, firefighters and correctional officers.

Beginning October 1, 2012, the contribution rates were

increased to 7.50% for regular members and 8.50% for police officers, firefighters and correctional officers.

Tier II Regular members contribute 6% of salary and full-time

certified firefighters, police officers and correctional officers contribute 7% of salary

Both If positive investment performance results in a decrease in

the total contribution rate paid by employers and employees participating in the System, the Retirement System of Alabama shall first reduce the employee contribution rate.

“Regular Interest” is 4% which is the rate adopted by the

Board and applied to the balance in each member’s’ account every year; however, if a member receives a refund of contributions, the interest rate applied to the refund is lower than the 4% regular rate (Based on Section 16-25-14-(g)(1)).

Page 37

SCHEDULE J

SCHEDULE OF MEMBERSHIP DATA AS OF SEPTEMBER 30, 2015

NUMBER OF ACTIVE MEMBERS AND THEIR AVERAGE COMPENSATION BY AGE AND YEARS OF SERVICE

Attained

Age Years of Service

Under 1 1 to 4 5 to 9 10 to 14 15 to 19 20 to 24 25 to 29 30 to 34 35 to 39 > 40 Total

Under 25 1,097 1,326 6 2,429

Avg. Pay 30,855 29,678 23,093 30,194

25 to 29 1,540 7,820 1,578 16 10,954

Avg. Pay 32,423 35,071 42,339 27,315 35,735

30 to 34 1,027 5,041 5,945 1,982 13 14,008

Avg. Pay 37,540 38,469 45,983 49,025 47,602 43,092

35 to 39 910 4,319 4,061 6,058 1,495 15 16,858

Avg. Pay 36,028 39,762 47,290 51,277 54,681 44,252 46,839

40 to 44 769 3,771 3,652 4,094 5,390 1,137 11 18,824

Avg. Pay 36,271 37,961 46,733 50,174 56,201 58,625 41,505 48,723

45 to 49 608 3,240 3,463 3,836 4,035 4,325 934 15 20,456

Avg. Pay 33,540 36,120 44,516 46,457 53,788 59,751 59,732 58,729 48,979

50 to 54 430 2,550 2,896 3,640 3,709 2,874 2,308 484 12 18,903

Avg. Pay 34,834 35,912 41,682 43,832 48,344 55,386 59,769 57,511 51,295 47,172

55 to 59 350 1,885 2,311 3,008 3,338 3,024 1,959 1,122 442 5 17,444

Avg. Pay 37,966 36,511 43,687 42,339 46,298 53,136 59,085 62,894 62,665 42,808 48,147

60 to 64 275 1,537 1,569 1,824 1,967 1,887 1,332 165 68 13 10,637

Avg. Pay 50,626 48,432 42,508 42,516 46,341 49,865 59,194 71,179 65,532 56,348 48,287

65 to 69 97 664 857 737 555 460 385 55 25 10 3,845

Avg. Pay 38,387 48,388 51,569 43,309 48,306 52,435 66,292 74,957 65,629 72,531 50,691

70 & up 32 238 425 349 242 152 121 33 18 18 1,628

Avg. Pay 43,310 47,352 52,728 35,699 41,948 58,428 70,389 67,137 79,144 112,150 49,590

Total 7,135 32,391 26,763 25,544 20,744 13,874 7,050 1,874 565 46 135,986

Avg. Pay 35,137 37,593 45,292 47,005 51,306 55,694 59,975 62,629 63,425 80,230 46,313

Average Age: 45.50 Average Service: 10.95

Page 38

SCHEDULE J (continued)

NUMBER OF SERVICE RETIREMENTS AND THEIR BENEFITS BY AGE

Age

Number of Members

Total Annual Benefits

Average Annual Benefits

Under 50 301 $ 8,830,932 $ 29,339 50 – 54 1,843 54,431,488 29,534 55 – 59 5,209 156,446,991 30,034 60 – 64 14,797 378,144,273 25,555 65 – 69 20,212 473,120,093 23,408 70 – 74 14,143 318,599,065 22,527 75 – 79 9,823 210,463,251 21,426 80 – 84 6,459 130,409,672 20,190 85 – 89 3,786 70,377,925 18,589 90 – 94 1,477 25,489,510 17,258

95 & Over 497 7,515,564 15,122

Total 78,547 $ 1,833,828,764 $ 23,347 Average Age: 70.0

NUMBER OF DROP PARTICIPANTS AND THEIR BENEFITS BY AGE

Age Number

of Members Total

Annual Benefits Average

Annual Benefits

55 – 59 2 $ 64,100 $ 32,050 60 – 64 571 21,619,562 37,863 65 – 69 107 4,384,051 40,972 70 – 74 16 725,834 45,365 75 – 79 3 144,240 48,080 80 – 84

85 & Over

Total 699 $ 26,937,787 $ 38,538 Average Age: 62.0

Page 39

SCHEDULE J (continued)

NUMBER OF BENEFICIARIES AND THEIR BENEFITS BY AGE

Age

Number of Members

Total Annual Benefits

Average Annual Benefits

Under 50 343 $ 3,761,277 $ 10,966 50 – 54 172 1,822,786 10,598 55 – 59 265 3,214,308 12,129 60 – 64 414 6,082,694 14,692 65 – 69 571 8,814,881 15,438 70 – 74 660 11,337,262 17,178 75 – 79 670 11,189,114 16,700 80 – 84 635 10,149,089 15,983 85 – 89 488 7,229,998 14,816 90 – 94 273 3,729,613 13,662

95 & Over 72 847,949 11,777

Total 4,563 $ 68,178,971 $ 14,942 Average Age: 71.7

NUMBER OF DISABLED RETIREES

AND THEIR BENEFITS BY AGE

Age Number

of Members Total

Annual Benefits Average

Annual Benefits

Under 50 368 $ 4,290,922 $ 11,660 50 – 54 546 6,289,229 11,519 55 – 59 968 11,208,720 11,579 60 – 64 1,332 15,227,346 11,432 65 – 69 1,119 12,133,454 10,843 70 – 74 661 7,199,326 10,892 75 – 79 295 3,302,745 11,196 80 – 84 156 1,690,114 10,834 85 – 89 58 628,150 10,830 90 – 94 18 215,419 11,968

95 & Over 2 18,848 9,424

Total 5,523 $ 62,204,273 $ 11,263 Average Age: 63.0