team unicamp - cfa society...

TRANSCRIPT

Team Unicamp

André de Teive ArgolloLara Siqueira OliveiraFelipe Husein

Luiz Henrique Mori SartorMurilo Viana

Target Price: BRL 49.35

Current Price: BRL 35.11

Source: Bloomberg and Team’s Estimates

Recommendation

BUY

Upside: 40.5%

Recommendation

(i) expected Brazilian economy recovery(ii) consolidation of car rental segment (iii) strong competitive advantages

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

15

20

25

30

35

40

45

50

jan-16 fev-16 mar-16 abr-16 mai-16 jun-16 jul-16 ago-16 set-16 out-16 nov-16

RENT3

CompanyOverview

1973: Established in Belo Horizonte by Mattar and

Resende families 2005: IPO (USD 295 mn)

1999: Fleet Management

segment

80’s and 90’s: Franchising and Car Sales segments

1981: leadership RAC segment

2016: 8 countries, 552 agencies, 117k cars. Leader in the market

1981: Expansion Latin America

1997: PE DL&J acquires 33% of shares for USD 50 mn

Company Overwiew

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

Main Shareholder’s

Mattar Family (%) 12.9

Resende Family (%) 15.9

Free Float (%) 72.2

Localiza Rent a Car S.A.

Controlling/Management Shares (%) 27.9

Treasury shares (%) 1.7

Free Float (%) 70.4

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

Source: Company`s Data (2016)

Integrated Business Platform Footprint

Business Description

Consolidation Strategy

Core Business

70% of Total Fleet

EBITDA generation

Support Division

Minimize Costs

Direct Sales Channel

Lowest Depreciation

Supplementary Division

Penetration

Brand Recognition

Broaden Horizons

Outsource Management

Purchase on Demand

High Utilization Rates

Taylor-Made Contracts

Car Sales 52%Car Rental

(RAC) 33.5%

Fleet Rental 15.8%

Franchising 0.45%

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

Source: Company`s Data (2016)

Business Description: Revenue Breakdown per Segment (2015)

Industry and

Competitors

Industry Overview

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

0%

10%

20%

30%

40%

50%

60%

70%

Fleet Prenetation

Source: ABLA

0

100

200

300

400

500

600

700

800

900

0%

10%

20%

30%

40%

50%

60%

2000 2002 2004 2006 2008 2010 2012 2014

Daily fee/Minimum Wage Minimum Wage

Daily Fee/Minimum Wage vs. Minimum Wage

Market Share U.S.

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

Source: BCB, Team’s Estimates, Company’s Estimates

51%

23%

20%

5%

Enterprise Holdings Hertz Avis Others

National Market Share Distribution (Revenue)

13%

3%

4%

5%

75%

Localiza Locamerica Unidas JSL - Movida Others

U.S Market Share Distribution (Revenue)

3 Main Segments: RAC, Fleet and Car Sales

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

Source: Company’s Data (2016)

7.5% 4.3%3.4%

5%

6.5%

73.3%

Localiza UnidasMovida Ouro VerdeLocamerica Others

Market Share Fleet (Fleet Size)Market Share RAC (Fleet Size)

22.40%

6%

9.9%

61.70%

Localiza Unidas Movida Outros

Less Pulverized

Capital Intensive

Entry Barriers

Business

Leisure

More Fragmented

Lower Entry Barriers

Corporations

3 Main Segments: RAC, Fleet and Car Sales

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

8.48.9 9 9.4

10.1 9.9

3.3 3.5 3.6 3.6 3.32.5

0

3

6

9

12

2010 2011 2012 2013 2014 2015

used cars new cars

2.5x 2.5x 2.5x 2.6x 3.1x 4x

Brazilian Market of New Cars vs Used Cars (Millions)

Source: Company’s Data (2016)

7.5%4.3% 3.4%

5%

6.5%

73.3%

Localiza Unidas

Movida Ouro Verde

Locamerica Others

Market Share Fleet (Fleet Size)Market Share RAC (Fleet Size)

22.4%

6%

9.9%

61.7%

Localiza Unidas Movida Outros

Investment Thesis

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

0

1

2

3

4

5

Threat ofSubstituteProducts

Bargain Powerof Suppliers

Threat of NewEntrants

Bargain Powerof Customers

CompetitiveRivalry within

Industry

Localiza Average Competitors

Porter’s Five Forces

Source: BCB, Team’s Estimates

0%

5%

10%

15%

20%

25%

30%

Localiza Unidas

Locamerica Ouro Verde

JSL consolidada

ROIC- Localiza X Competitors (2016) ROE – Localiza X Competitors (2016)

17%

9.3%10.5%

6.5%

8.4%

0%

5%

10%

15%

1

Localiza Unidas

Locamerica Ouro Verde

JSL Consolidada

Fund-raising

Car Purchase

Car Rental

Car Sales

1

2

3

4

Competitive Advantages in Each Business Level

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

Fund-raising Advantages

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

Fund-raising

25%-30% discounts in each car price

Higher

Localiza

1

Bonds - Debt profile (Face value) – Million BRL

Source: Companys Data

brAA+ S&P BB S&P A- (bra) Fitch AA- (bra) Fitch A(bra) Fitch

Aa1.br Moody's AA- (bra) Fitch

AAA (bra) Fitch

Nat

ion

al S

cale

BB+ Fitch Baa1 Moody's B+ S&P Ba3 Moody's

Ba2 Moody's BB- S&P

BB+ S&P

Glo

bal

Sca

le

Ratings

99523

299619 770 672

1169

2016 2017 2018 2019 2020 2021

Debt profile

Cash

921

At 09/30/2016

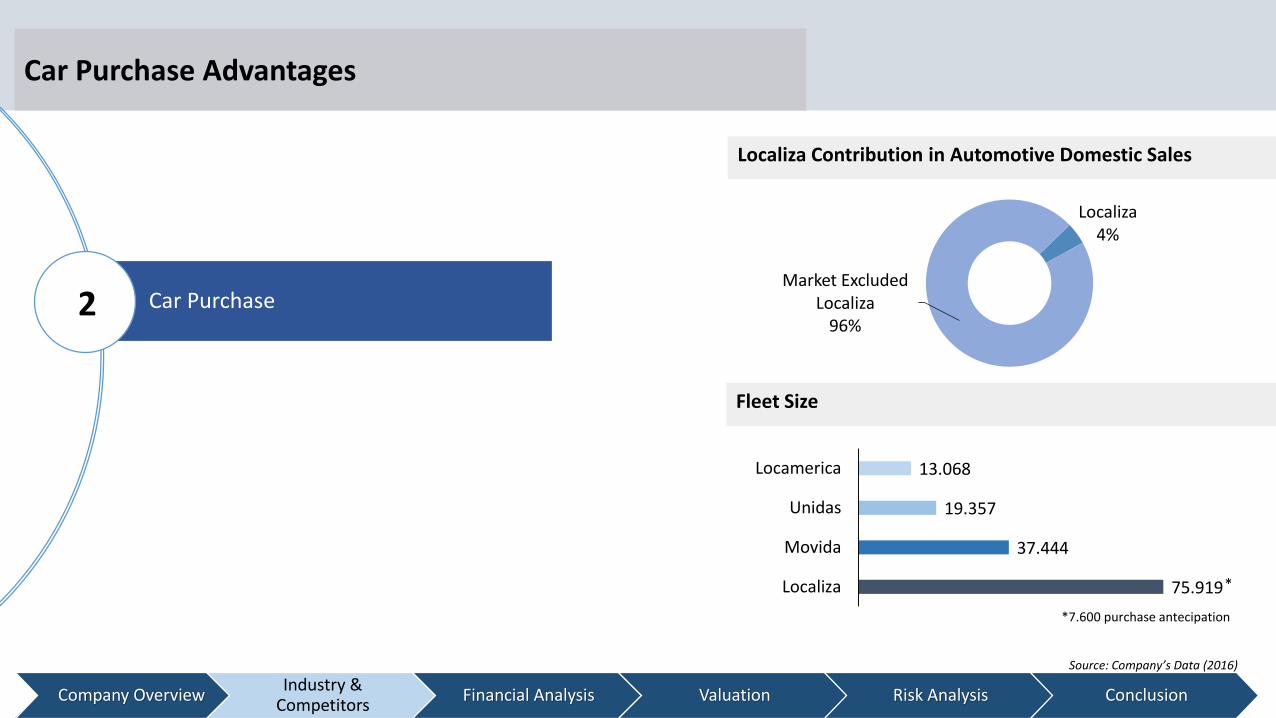

Car Purchase Advantages

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

Car Purchase

rates

2

Localiza4%

Market Excluded Localiza

96%

75.919

37.444

19.357

13.068

Localiza

Movida

Unidas

Locamerica

Localiza Contribution in Automotive Domestic Sales

Fleet Size

Source: Company’s Data (2016)

*

*7.600 purchase antecipation

Car Rental3

Competition Advantages

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

1Movida Unidas Hertz Localiza

494

100

163

204

10650

4644

2420

0 20 40 60 80 100 120

1

Avis Outros HertzUnidas Movida Localiza

388136

7464

26

0 100 200 300 400 500

Avis Hertz Movida

Unidas Localiza

Airport Agencies Off-Airport Agencies

Source: Company’s Data (2016)

49451.342

6.7

Others

Localiza

Hertz

Number of branchesMarket Share by Revenue

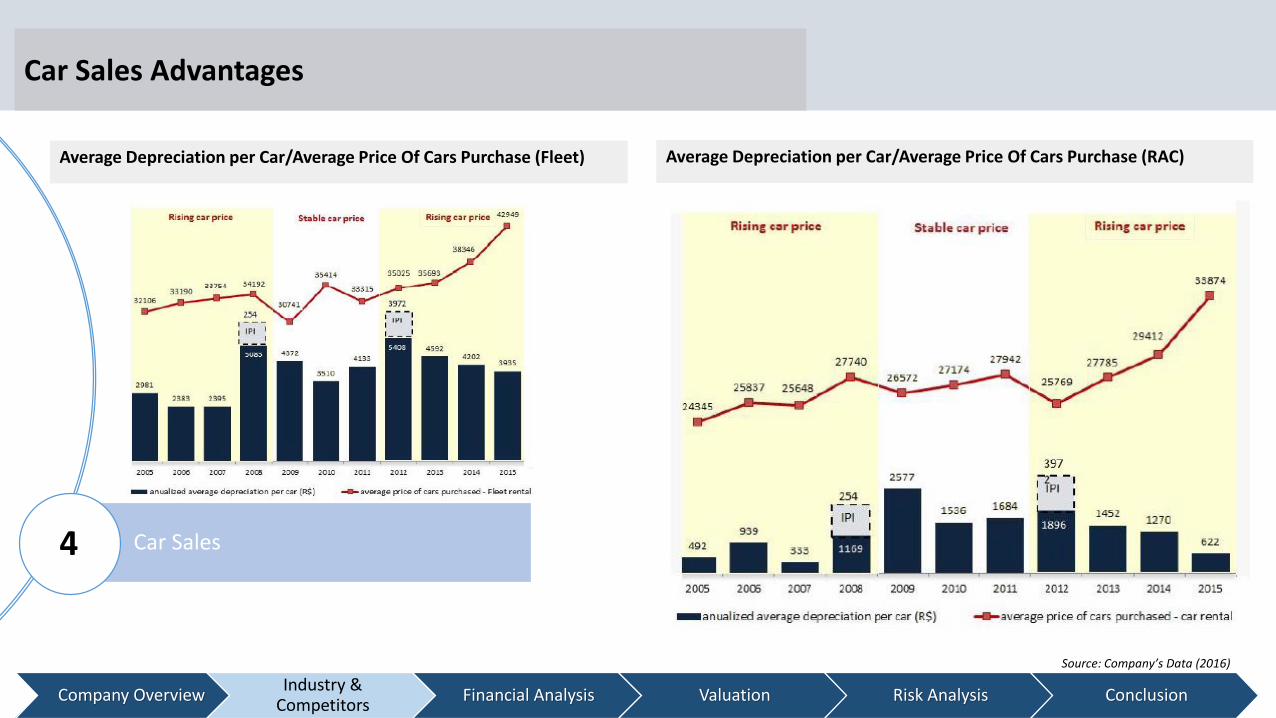

Car Sales Advantages

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

494

100

163

204

204

163

100

Car Sales 4

Average Depreciation per Car/Average Price Of Cars Purchase (RAC)

Source: Company’s Data (2016)

Average Depreciation per Car/Average Price Of Cars Purchase (Fleet)

Car Sales

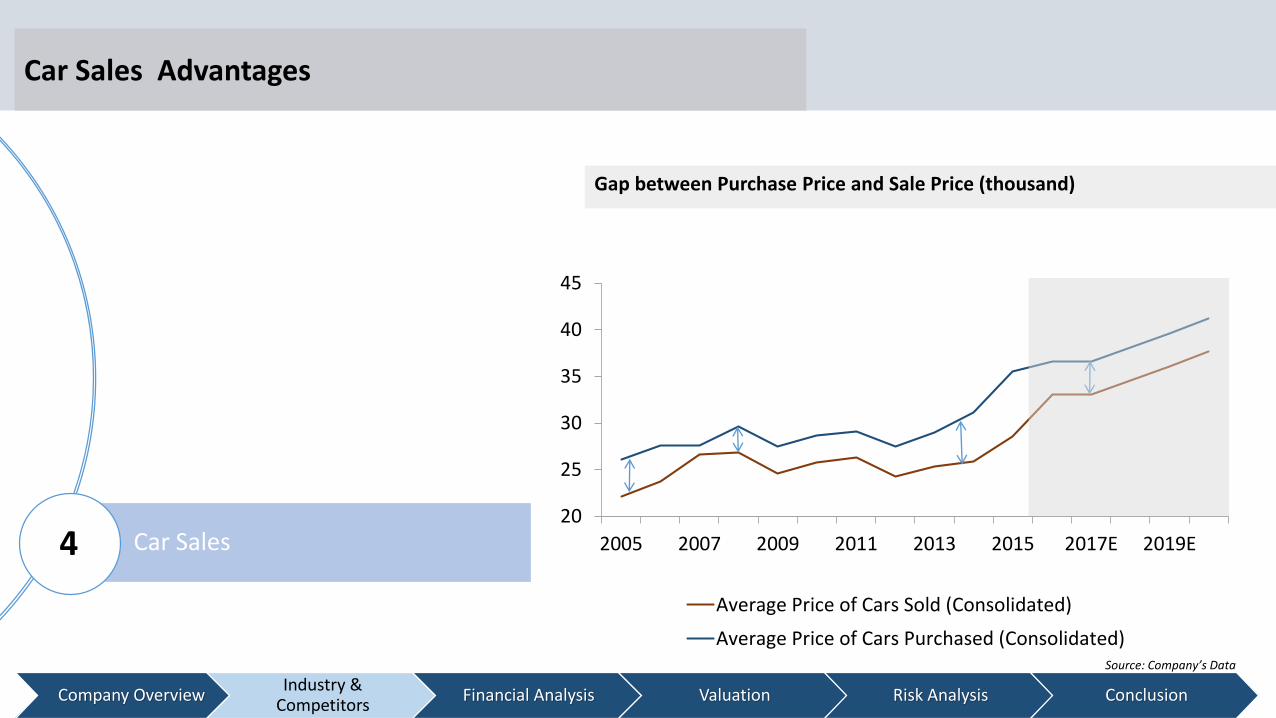

Car Sales Advantages

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

163

204

163

100

4

Source: Company’s Data

Gap between Purchase Price and Sale Price (thousand)

20

25

30

35

40

45

2005 2007 2009 2011 2013 2015 2017E 2019E

Average Price of Cars Sold (Consolidated)

Average Price of Cars Purchased (Consolidated)

Competitors’ Recent Moves

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

494

100

163

204

204

163

100

4% 6%

25% 27%

40%

48% 48%

0%

10%

20%

30%

40%

50%

60%

0

5

10

15

20

25

30

35

40

2012 2013 2014 1Q15 2Q15 3Q15 4Q15

Tho

usa

nd

s

Movida's fleet size

Movida as % of Localiza in RAC

Movida Fleet Growth In RAC segment as % of Localiza’s Fleet (thousands)

Source: Localiza, Movida and Teams’s Estimates

65.170.7

77.671.3 71.5 71.1

76.8

2.6 4.6

19.2 19.628.4

34.3 37.1

10.6 1419.7 18.7 18.2 18.3 19.3

2012 2013 2014 1H15 2H15 3H15 4H15

Localiza Movida Unidas

Largest Players in RAC Segment ( Fleet size in thousands)

Competition Structure

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

494

100

163

204

204

163

100

Source: Company’s Data (2016)

FLEET SEGMENT NICHE RENT A CAR

Financial

Analysis

Revenue Drivers

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

494

100

163

204

204

163

100

-5%

0%

5%

10%

15%

20%

2011 2013 2015 2017 2019 2021

Brazilian GDP Net Revenue

GDP x Net Revenue Volume vs. Tariff

40

50

60

70

80

90

100

0

5

10

15

20

25

30

2005 2008 2011 2014 2017E 2020E

Mill

ion

s

RAC Rentals Fleet RentalsRAC - Daily Rental Fleet - Daily Rental

Source: Company’s Data (2016), Team’s Estimates amd BCB

5%

10%

15%

20%

25%

30%

35%

40%

2010 2012 2014 2016E 2018E

Gross profit Margin EBIT MarginNet profit Margin

Margin (Gross Profit, EBIT, Net Profit)EBITDA Historical Breakdown

Margins

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

Source: Company’s Data, Bloomberg and Team’s Estimates

37.9%

20.07%

10.76%

45% 47%41%

37% 39%32% 32% 33%

68% 69% 66% 66%60% 62% 61% 65%

3% 3% 4% 6% 6% 7% 8% 6%0%

10%

20%

30%

40%

50%

60%

70%

80%

2010 2011 2012 2013 2014 2015 1H15 1H16

Rent a Car Fleet Rental Car Sales

EBTIDA Evolution

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

494

100

163

204

204

163

100

3 34

5 56

8 9 9 10 910

1213

0

2

4

6

8

10

12

14

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E

Hu

nd

red

s o

f M

illio

ns

EBITDA

18%

1%

12%

11%

EBTIDA

Source: Company’s Data (2016) and Team’s Estimates

Profitability

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

494

100

163

204

204

163

100

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

ROIC Kd

6.7%3.8%

491

488

168

0

100

200

300

400

500

2010 2012 2014 Actual 2018E

Localiza Median National Peers Median Global Peers

ROIC vs. Kd Net Income (million)

Source: Company’s Data and Team’s Estimates

Leverage

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

100

163

204

204

163

100

JSL 4.3x

Ouro verde 3.8x

Locamerica 2.9x

Unidas 2.5x

Localiza 1.7x

Ouro Verde 9.7x

JSL 4.6x

Locamerica 2.0x

Unidas 1.1x

Localiza0.8x

Net Debt/EBITDA

Source: Company’s Data (2016) and Bloomberg

Net Debt/Equity

Valuation

EBITDA

Net Used Car Sales Revenue

Depreciation

Income Tax

Working capital

CFO

Capex -Renewals

CFO net of Capex

RenewalsCapex -Fleet

Expansion Capex - HQ

FCF Before Interest

-2050 -1050 -50 950 1950

Industry OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

CAPEX

CAPEX Ratios (million) Free Cash Flow Breakdown (2015)

Source: Company’s Data and Team’s Estimates

91%

54%

33% 33%

64%

74%

97%

40%

21%16%

13%

21% 22%

32%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

50

100

150

200

250

300

350

400

450

500

2010 2011 2012 2013 2014 2015 9M16

Net CAPEX for fleet renewal CAPEX Fleet Expansion

CAPEX (total) / CFO CAPEX (total)/D&A

Depreciation

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

494

100

163

204

204

163

100

Depreciation = Purchase Price – Transaction Costs – Residual Value

Source: Company’s Data and Team’s Estimates

millions

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

50

100

150

200

250

300

350

400

450

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E 2020E

Depreciation Depreciation / Tangible Assets (Cars)

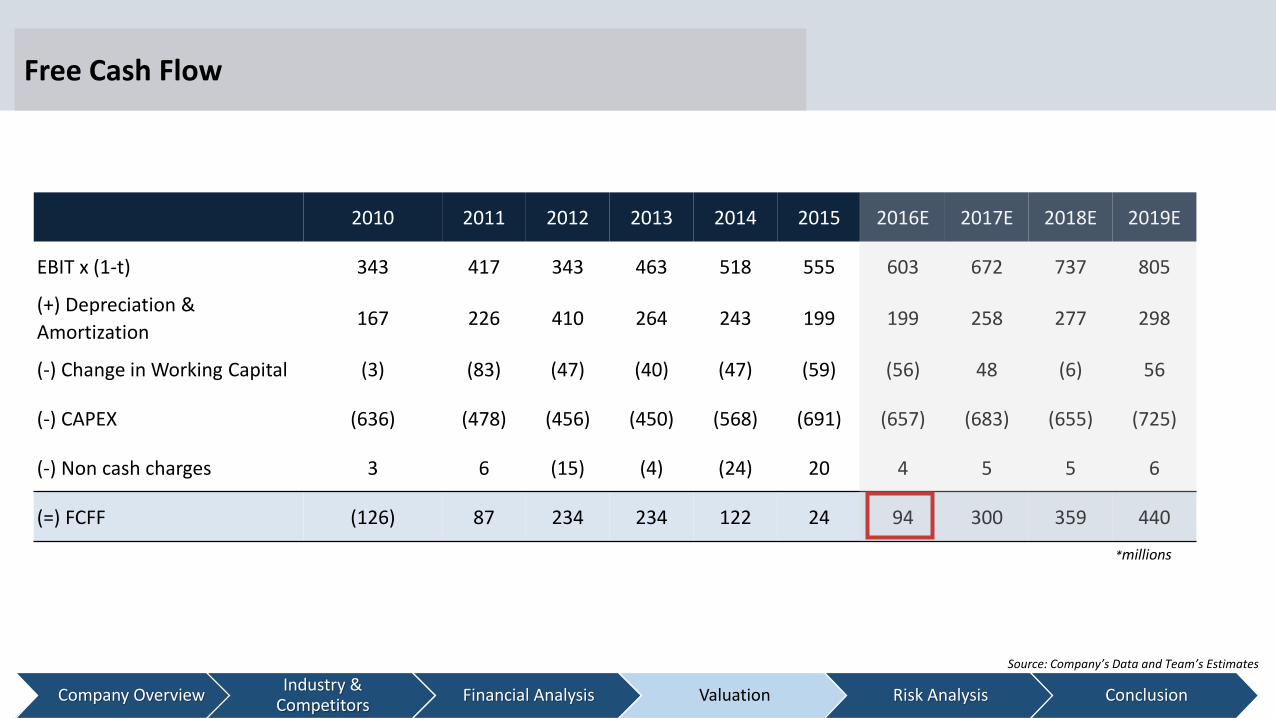

Free Cash Flow

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

494

100

163

204

204

163

100 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E

EBIT x (1-t) 343 417 343 463 518 555 603 672 737 805

(+) Depreciation &

Amortization167 226 410 264 243 199 199 258 277 298

(-) Change in Working Capital (3) (83) (47) (40) (47) (59) (56) 48 (6) 56

(-) CAPEX (636) (478) (456) (450) (568) (691) (657) (683) (655) (725)

(-) Non cash charges 3 6 (15) (4) (24) 20 4 5 5 6

(=) FCFF (126) 87 234 234 122 24 94 300 359 440

Source: Company’s Data and Team’s Estimates

*millions

Weighed Avarege Cost Of Capital

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

494

100

163

204

204

163

100

WACC Assumption

WACC Assumptions (%)

Risk Free Rate 1.8%

Target D/E Ratio 60%

Beta 1.16

Equity Risk Premium 5.52%

Brazil Country Risk Premium 3.94%

Inflation Diferential 3.17%

Cost of Equity 15.33%

Cost of Debt 12.3%

Final WACC 11.83%

WACC

11.0% 11.5% 12% 12.5% 13%

Perp

etu

ity

gro

wth 5% 48.20 44.28 40.91 37.98 35.42

5.5% 53.03 48.38 44.44 41.06 38.12

6% 58.82 53.23 48.56 44.61 41.21

6.5% 65.90 59.05 53.43 48.74 44.77

7% 74.74 66.15 59.27 53.63 48.92

Sensitivity Analysis (WACC)

Source: Company’s Data and Team’s Estimates

Terminal Growth of 6%

Inflation 4.5%

Real GDP Growth 1.5%

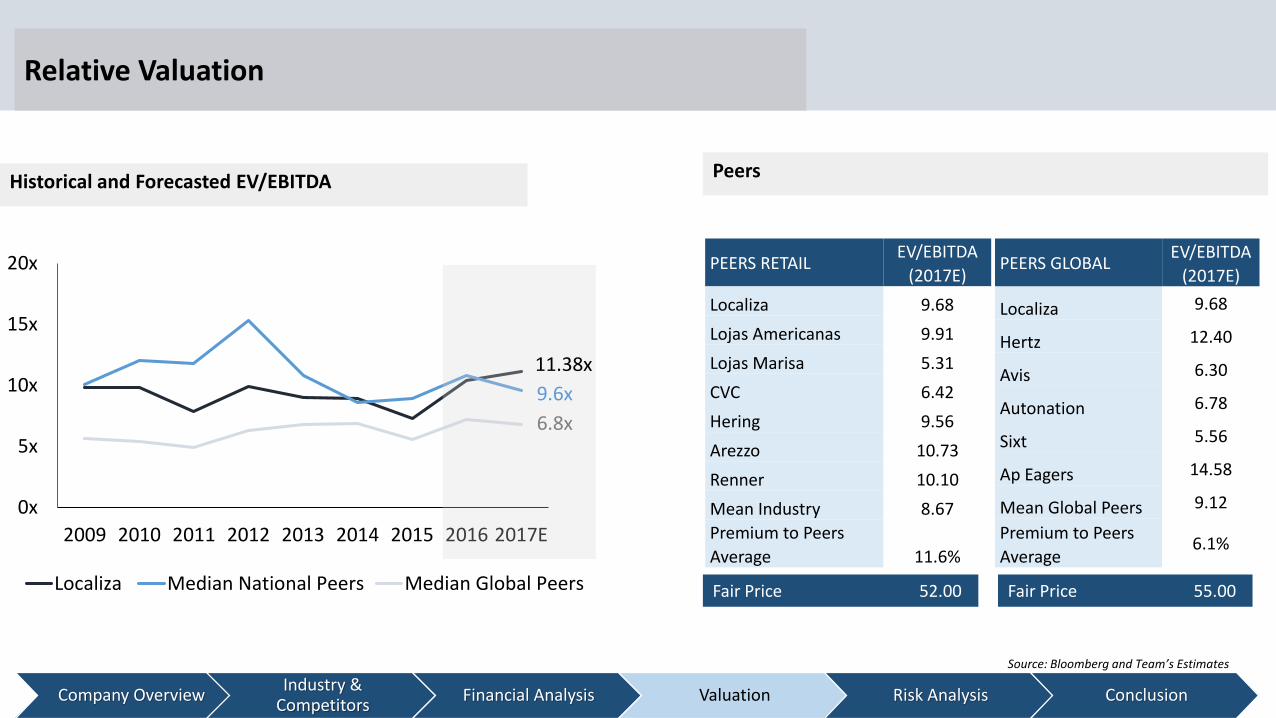

Relative Valuation

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

494

100

163

204

204

163

100

Historical and Forecasted EV/EBITDA

0x

5x

10x

15x

20x

2009 2010 2011 2012 2013 2014 2015 2016 2017E

Localiza Median National Peers Median Global Peers

Peers

11.38x

9.6x

6.8x

Source: Bloomberg and Team’s Estimates

Fair Price 52.00 Fair Price 55.00

PEERS RETAILEV/EBITDA

(2017E)

Localiza 9.68

Lojas Americanas 9.91

Lojas Marisa 5.31

CVC 6.42

Hering 9.56

Arezzo 10.73

Renner 10.10

Mean Industry 8.67

Premium to Peers

Average 11.6%

PEERS GLOBALEV/EBITDA

(2017E)

Localiza 9.68

Hertz 12.40

Avis 6.30

Autonation 6.78

Sixt 5.56

Ap Eagers 14.58

Mean Global Peers 9.12

Premium to Peers

Average6.1%

P/E

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

Multiples Analysis

10

15

20

25

30

35

40

Localiza Mean +2 Standard Deviation -2 Standard Deviation

Price to Earnings and Price to Book Value

2

3

4

5

6

7

8

jan-10 mai-10 set-10 jan-11 mai-11 set-11 jan-12 mai-12 set-12 jan-13 mai-13 set-13 jan-14 mai-14 set-14 jan-15 mai-15 set-15 jan-16 mai-16 set-16

Localiza Mean +2 standard deviation -2 Standard deviationSource: Bloomberg

P/E

P/B

Risks

Analysis

Monte Carlo

Industry OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

494

100

163

204

204

163

100

Monte Carlo Simulation

0

200

400

600

800

1000

1200

30

32

34

36

38

40

42

44

46

48

50

52

54

56

58

60

62

64

66

68

70

Sell: 1.38% Hold: 21.44% Buy: 77.18%

Risk Variable Distribution

Decrease in

RevenuesGDP Real Growth (%) log-normal

Decrease in

RevenuesInfation Rate - IPCA (%) log-normal

Decrease in

MarginsInterest Rate SELIC (%) log-normal

RENT's price simulation46.92 Mean33.68 Minimum66.08 Maximum5.23 Std Dev

Source: Team’s Estimates

Risk Analysis

494

100

163

204

204

163

100

Risk Matrix

Industry OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

Source: Bloomberg and Team’s Estimates

New Generation, Disruptive Ideas, Innovative Companies

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

494

100

163

204

204

163

100

Disruptive Ideas

3.33.12

1.72

4.58

3.27

2.162.281.73

0.891.180.94 0.49

2013 2014 2015

18-21 years 22-30 years 31-40 years 41 or more

11.34

9.05

5.26

2013 2014 2015

-53%

Age Range- In million

Issue of driver’s license – Brazil (million)

Source:Denatran/Citylab

Conclusion

BUYTarget Price:

BRL 49.35Upside: 40.5%Current Price:

BRL 35.11

Qualitative Positives Quantitative Positives

Optimal and sophisticated pricing models

Margins and Clear Earning Visibility

Anti-cyclical free cash flows

Low funding costs

Solid financials

Full exploitation of sectorial imperfections

Synergies among commercial units

Broad geographical coverage

Wrap Up

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

BUYTarget Price:

BRL 49.35Upside: 20%

Current Price:BRL 38

Qualitative Positives Quantitative Positives

Optimal and sophisticated pricing models

Margins and Clear Earning Visibility

Anti-cyclical free cash flows

Low funding costs

Solid financials

Full exploitation of sectorial imperfections

Synergies among commercial units

Broad geographical coverage

Wrap Up

Company OverviewIndustry &

CompetitorsFinancial Analysis Valuation Risk Analysis Conclusion

Q&A

Appendix 1.1: Balance Sheet

494

100

163

204

204

163

100

100

In BR Millions 2012 2013 2014 2015 2016E 2017E 2018E 2019E

Cash and Cash Equivalents 824 1,011 1,390 1,385 1,164 1,576 1,926 2,242

Trade Accounts Receivable 361 408 460 486 555 569 657 684

Other Current Assets 50 58 95 103 81 88 96 105

Decommissioning Cars to Fleet Renewal 13 17 18 32 31 34 37 40

Total Current Assets 1,248 1,493 1,963 2,006 1,831 2,266 2,716 3,071

Derivative Financial Instruments Swap 0 0 0 46 46 46 46 46

Trade Accounts Receivable 4 7 3 5 5 5 5 5

Escrow Deposit 23 38 42 53 53 53 53 53

Deferred Income Tax and Social Contribution 25 32 33 0 0 0 0 0

Cars 2,534 2,781 3,278 3,611 3,975 4,273 4,602 4,973

Other 171 166 204 314 432 559 610 667

Software 36 47 60 67 43 47 51 56

Goodwill on Acquisition of Investments 5 12 22 22 22 22 22 22

Total Non Current Assets 2,798 3,085 3,735 4,117 4,576 5,004 5,388 5,821

TOTAL ASSETS 4,046 4,578 5,698 6,123 6,407 7,270 8,104 8,893

Appendix 1.2: Balance Sheet

494

100

163

204

204

163

100

100

Trade Accounts Payable 356 461 828 691 702 758 827 904

Payroll and Related Charges 53 74 86 86 87 94 103 113

Loans, Financing and Debentures 210 275 301 422 422 500 500 500

Income Tax and Social Contribution 26 35 41 28 28 28 28 28

Dividends and Interest on Own Capital 19 53 59 29 29 29 29 29

Other Current Liabilities 70 79 82 100 88 95 104 114

Total Current Liabilities 734 977 1,398 1,356 1,358 1,505 1,591 1,688

Loans, Financing and Debentures 1,845 2,068 2,412 2,597 2,597 2,997 3,390 3,674

Provisions 35 51 70 68 68 68 68 68

Deferred Income Tax and Social Contribution 77 112 139 142 142 142 142 142

Other Non Current Liabilities 30 30 23 19 19 19 19 19

Total Non Current Liabilities 1.987 2.260 2.644 2.825 2.825 3.225 3.618 3.903

TOTAL LIABILITIES 2,721 3,237 4,042 4,181 4,183 4,730 5,210 5,591

Capital Social 602 977 977 977 977 977 977 977

Retained Earnings 0 30 40 36 36 36 36 36

Reserves 723 334 638 929 1,207 1,519 1,868 2,270

TOTAL SHAREHOLDERS' EQUITY 1,325 1,341 1,656 1,942 2,224 2,540 2,895 3,302

TOTAL LIABILITIES AND SHAREHOLDERS' EQUITY 4,046 4,578 5,698 6,123 6,407 7,270 8,104 8,893

In BR Millions 2012 2013 2014 2015 2016E 2017E 2018E 2019E

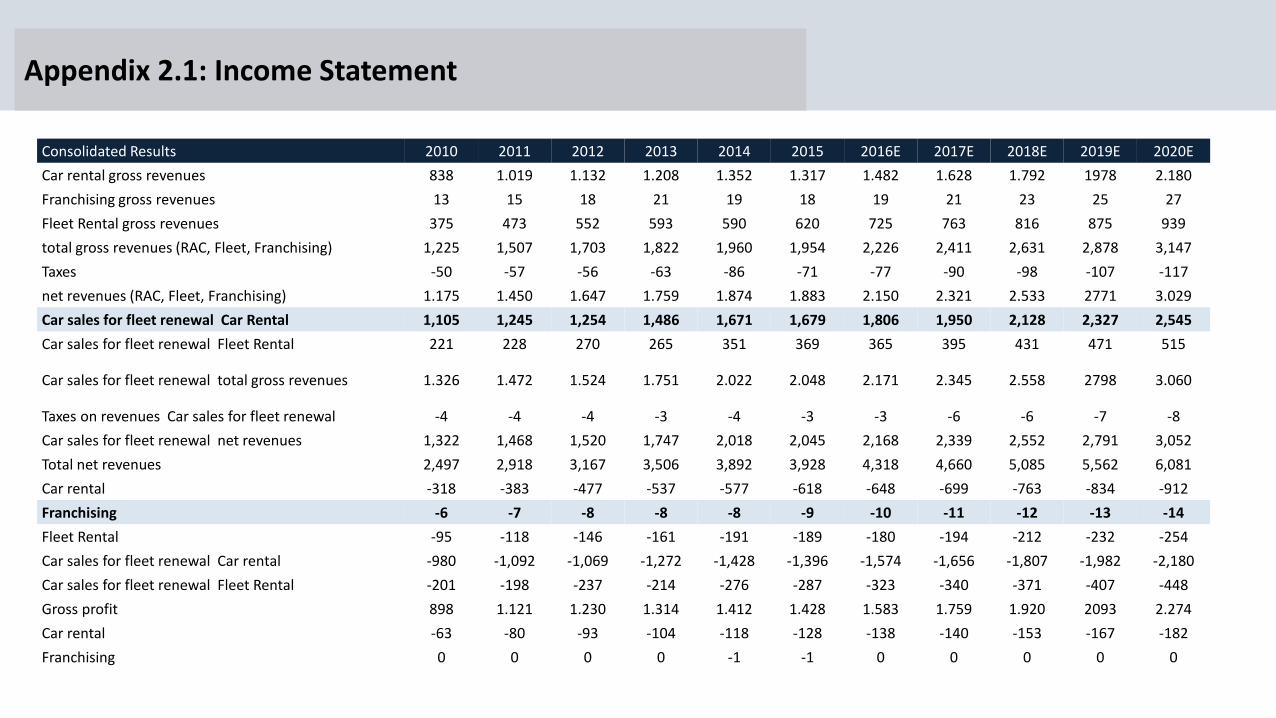

Appendix 2.1: Income Statement

494

100

163

204

204

163

100

100

Consolidated Results 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E 2020E

Car rental gross revenues 838 1.019 1.132 1.208 1.352 1.317 1.482 1.628 1.792 1978 2.180

Franchising gross revenues 13 15 18 21 19 18 19 21 23 25 27

Fleet Rental gross revenues 375 473 552 593 590 620 725 763 816 875 939

total gross revenues (RAC, Fleet, Franchising) 1,225 1,507 1,703 1,822 1,960 1,954 2,226 2,411 2,631 2,878 3,147

Taxes -50 -57 -56 -63 -86 -71 -77 -90 -98 -107 -117

net revenues (RAC, Fleet, Franchising) 1.175 1.450 1.647 1.759 1.874 1.883 2.150 2.321 2.533 2771 3.029

Car sales for fleet renewal Car Rental 1,105 1,245 1,254 1,486 1,671 1,679 1,806 1,950 2,128 2,327 2,545

Car sales for fleet renewal Fleet Rental 221 228 270 265 351 369 365 395 431 471 515

Car sales for fleet renewal total gross revenues 1.326 1.472 1.524 1.751 2.022 2.048 2.171 2.345 2.558 2798 3.060

Taxes on revenues Car sales for fleet renewal -4 -4 -4 -3 -4 -3 -3 -6 -6 -7 -8

Car sales for fleet renewal net revenues 1,322 1,468 1,520 1,747 2,018 2,045 2,168 2,339 2,552 2,791 3,052

Total net revenues 2,497 2,918 3,167 3,506 3,892 3,928 4,318 4,660 5,085 5,562 6,081

Car rental -318 -383 -477 -537 -577 -618 -648 -699 -763 -834 -912

Franchising -6 -7 -8 -8 -8 -9 -10 -11 -12 -13 -14

Fleet Rental -95 -118 -146 -161 -191 -189 -180 -194 -212 -232 -254

Car sales for fleet renewal Car rental -980 -1,092 -1,069 -1,272 -1,428 -1,396 -1,574 -1,656 -1,807 -1,982 -2,180

Car sales for fleet renewal Fleet Rental -201 -198 -237 -214 -276 -287 -323 -340 -371 -407 -448

Gross profit 898 1.121 1.230 1.314 1.412 1.428 1.583 1.759 1.920 2093 2.274

Car rental -63 -80 -93 -104 -118 -128 -138 -140 -153 -167 -182

Franchising 0 0 0 0 -1 -1 0 0 0 0 0

Appendix 2.2: Income Statement

494

100

163

204

204

163

100

100

Fleet Rental -10 -11 -12 -14 -15 -18 -19 -20 -22 -24 -26

Car sales for fleet renewal -98 -129 -151 -162 -172 -191 -217 -234 -256 -280 -306

General, administrative and other expenses -78 -81 -99 -118 -136 -156 -171 -185 -202 -221 -241

Car rental -66 -86 -213 -86 -78 -39 -39 -80 -85 -92 -99

Fleet Rental -80 -115 -164 -143 -129 -125 -125 -139 -150 -161 -174

Other assets depreciation and amortization -21 -24 -33 -35 -36 -36 -36 -40 -43 -46 -50

Operating profit before financial results and taxes 482 596 466 652 727 736 838 921 1.010 1102 1.194

Expense -168 -239 -199 -187 -276 -370 -461 -431 -450 -464 -464

Income 38 60 61 77 125 167 217 175 187 220 250

Income before tax and social contribution 352 417 327 542 576 533 594 666 747 858 980

Income tax and social contribution -102 -125 -86 -157 -165 -130 -166 -186 -209 -240 -274

Net income for the period 251 292 241 384 411 402 428 479 538 618 706

Consolidated Results 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E 2020E

CH-IN

Appendix 3: Beta

494

100

163

204

204

163

100

100

EnterpriseMarket Cap.

(USD)

Enterprise Value

(USD)

Total

Debt/Total

Assets (%)

Gross

Beta

Ajusted

Beta

(2/3*1/3)

Industry

Leverage

Beta (%)

Average

Capital

Structure

(%)

Industry

Tax Rate

(%)

Industry

Unleverage

Beta (%)

Localiza

Leverage

Beta (%)

Average 7,191,356,107 10,890,717,024 49 0.92 0.95

LOCALIZA RENT A CAR 2,523,788,115 3,033,972,159 49 0.93 0.95

AVIS BUDGET GROUP INC 3,121,310,315 17,289,310,315 70 1.72 1.48 0.62 0.3

AUTONATION INC 4,971,744,284 11,427,944,284 64 1.19 1.12 0.31 0.18

SIXT SE 249,886,695 5,105,098,501 50 0.95 0.96 0.12 0.06

EUROPCAR GROUPE SA 1,250,955,724 3,576,522,232 48 0.83 0.89 0.08 0.04

LOCAMERICA 102,794,736 296,367,072 60 0.18 0.45 0 0,00

TOTAL 14,195,473,911 40,944,728,458 370 6 6 1.19 0.61 0.37 0.86 1.16

Appendix 4.1: Key Financials

494

100

163

204

204

163

100

100

2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E

Margins

Gross Margin (%) 38% 39% 37% 36% 36% 37% 38% 38% 38%

Net Profit Margin (%) 10% 8% 11% 11% 10% 10% 10% 11% 11%

EBITDA Margin (%) 28% 28% 26% 25% 24% 24% 25% 25% 25%

EBIT Margin (%) 20% 15% 19% 19% 19% 19% 20% 20% 20%

Profitability

ROA (%) 7% 6% 8% 7% 7% 7% 7% 7% 7%

ROE (%) 26% 18% 29% 25% 21% 19% 19% 19% 19%

ROIC (%) 17% 13% 17% 17% 16% 15% 15% 15% 15%

2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E

Appendix 4.2: Key Financials

494

100

163

204

204

163

100

100

Market Ratios

EV/EBITDA (x) 8x 10x 9x 9x 7x 10x 10x 9x 8x

P/E (x) 17x 31x 18x 18x 13x 21x 18x 16x 14x

P/BV (x) 5x 6x 5x 4x 3x 4x 3x 3x 3x

Dividend Yield (%) 0,02x 0,01x 0,05x 0,01x 0,03x 0,02x 0,02x 0,02x 0,03x

Operational Efficiency

Spread ROIC x Wacc (%) 5.4 2 5.9 6 4.1 3.2 3.3 3.3 3.5

Spread ROIC x Kd (%) 8.7 6.2 11.6 10.4 6.2 3.7 6 6.6 7.1

Capital Structure

Assets/Equity (x) 3.6 3.0 3.4 3.4 3.2 2.9 2.9 2.8 2.7

Market Debt/Equity (X) 1.8 1.5 1.7 1.6 1.5 1.3 1.4 1.3 1.3

2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E

2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E

2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E

Appendix 5: Du Pont Analysis

494

100

163

204

204

163

100

100

Appendix 6: Debt Ratios

494

100

163

204

204

163

100

100

1… 1,3631,231

1,333 1.322

1,589 1,624

2,447

2,6822,548

2,798

3.296

3,6433,784

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

2010 2011 2012 2013 2014 2015 2016

Net debt Fleet value

Appendix 7: Returns

494

100

163

204

204

163

100

100

19%

15.4%

7.1%

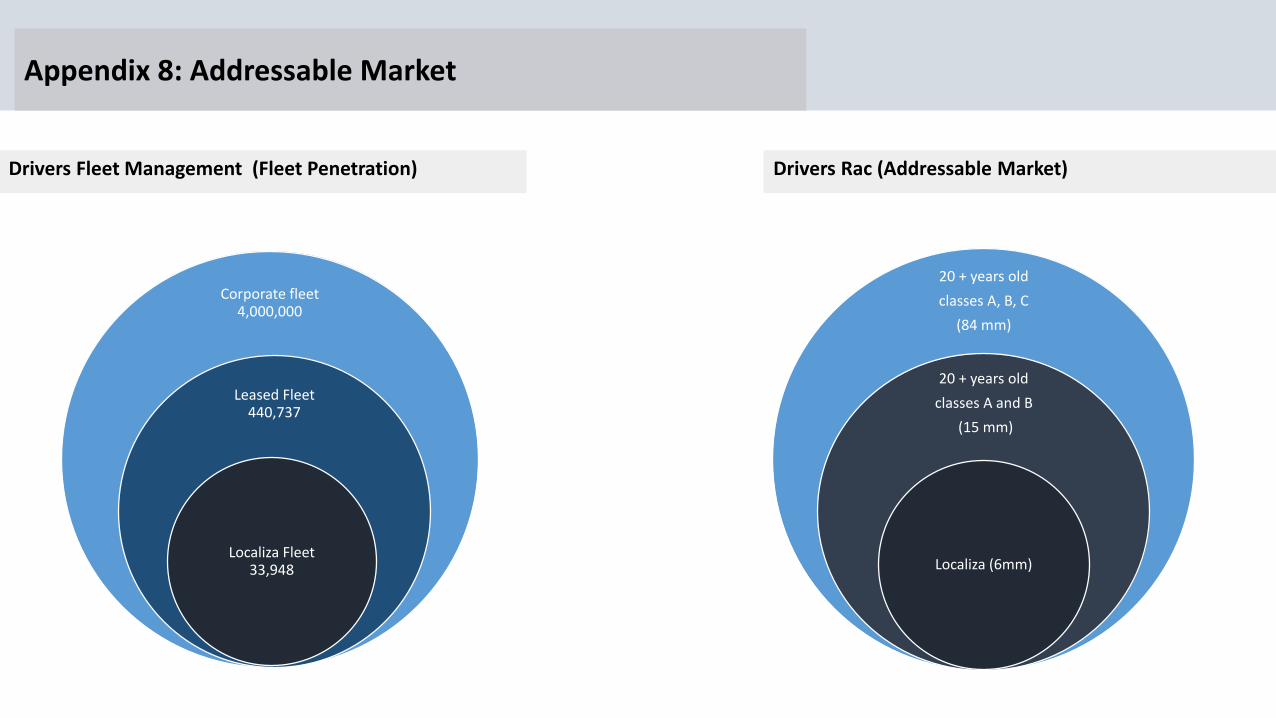

Appendix 8: Addressable Market

494

100

163

204

204

163

100

100

Corporate fleet4,000,000

Leased Fleet440,737

Localiza Fleet33,948

20 + years old

classes A, B, C

(84 mm)

20 + years old

classes A and B

(15 mm)

Localiza (6mm)

Drivers Fleet Management (Fleet Penetration) Drivers Rac (Addressable Market)

Appendix 9: Additional Risks

494

100

163

204

204

163

100

100

0

50

100

150

200

250

Social SecurityClaims Tax Claims Labor Claim Civil Lawsuits

Fin

anci

al L

oss

Remote Possible Probable

2507

241726

3769916208

Chances of Loss

Remote Possible Probable Total

Social Security Claims 4.782 20.288 0 25.070

Tax Claims 194.943 41.630 5.153 241.726

Labor Claim 0 0 37.699 37.699

Civil Lawsuits 0 0 16.208 16.208

Total Financial Impact 199.725 61.918 59.060 320.703

Material Arbitration, Administrative and Court Proceedings Probability of Loss

Appendix 10.1: Risk Analysis (Scenarios Outputs)

494

100

163

204

204

163

100

100

Base case Bear case Bull case

Revenue* 8,6% 8,1% 8,7%

Net Profit* 11,4% 8,8% 12,2%

EBITDA* 10,3% 9,0% 10,7%

Average ROIC** 15,3% 14,6% 15,5%

Average Total Debt / Total Capitalization (Bk. Equity)** 0,56x 0,56x 0,56x

Target Price 49,35 39,27 52,72

Upside/ (Downside) 22,2% -2,8% 30,5%

Appendix 10.2: Risk Analysis (Deterioration Scenarios for CDI rates)

494

100

163

204

204

163

100

100

Scenarios Base case Scenario I : 25% deterioration Scenario II : 50% deterioration

Net debt (dec 2015) 1,588.6 1,588.6 1,588.6

Net detb subject to CDI variation 1,059.2 1,059.2 1,059.2

Effective average rate of CDI in 12 months ended 31.12.15 13.23% 13.23% 13.23%

Estimated average annual rate of CDI, according to scenarios15.38% 19.23% 23.07%

Effect on financial expenses subject to the CDI variation

- According to effective rate (140.1) (140.1) (140.1)

- According to scenarios (162.9) (203.7) (244.4)

(Increase) in annual interest expense (22.8) (63.6) (104.3)

Appendix 11.1: Sensitivy Analysis (USA T-Bond – 10 years)

494

100

163

204

204

163

100

100

Perp

etu

ity

gro

wth

USA T-Bond (10 years)

R$ 49,35 0,0% 0,5% 1,0% 1,5% 2,0% 2,5% 3,0% 3,5%

3% R$ 34,60 R$ 33,60 R$ 32,65 R$ 31,74 R$ 30,88 R$ 30,06 R$ 29,28 R$ 28,53

4% R$ 40,10 R$ 38,80 R$ 37,57 R$ 36,42 R$ 35,32 R$ 34,29 R$ 33,30 R$ 32,37

5% R$ 47,37 R$ 45,62 R$ 43,98 R$ 42,45 R$ 41,01 R$ 39,67 R$ 38,40 R$ 37,20

6% R$ 57,47 R$ 54,97 R$ 52,67 R$ 50,55 R$ 48,58 R$ 46,76 R$ 45,05 R$ 43,46

7% R$ 72,39 R$ 68,58 R$ 65,13 R$ 62,00 R$ 59,14 R$ 56,52 R$ 54,12 R$ 51,90

8% R$ 96,73 R$ 90,19 R$ 84,46 R$ 79,39 R$ 74,88 R$ 70,84 R$ 67,20 R$ 63,90

9% R$ 143,46 R$ 129,84 R$ 118,54 R$ 109,02 R$ 100,89 R$ 93,86 R$ 87,72 R$ 82,31

Appendix 11.2: Sensitivy Analysis (Price Readjustment)

494

100

163

204

204

163

100

100

Pri

ce R

ead

just

men

t (F

leet

)

Price Readjustment as percentage of inflation (RAC)

R$ 49,35 10% 20% 30% 40% 50% 60% 70% 80%

10% R$ 28,25 R$ 34,03 R$ 39,83 R$ 45,66 R$ 51,52 R$ 57,41 R$ 63,33 R$ 69,28

20% R$ 30,64 R$ 36,39 R$ 42,17 R$ 47,98 R$ 53,82 R$ 59,68 R$ 65,58 R$ 71,51

30% R$ 33,06 R$ 38,79 R$ 44,54 R$ 50,32 R$ 56,14 R$ 61,98 R$ 67,86 R$ 73,77

40% R$ 35,50 R$ 41,20 R$ 46,93 R$ 52,69 R$ 58,48 R$ 64,31 R$ 70,16 R$ 76,05

50% R$ 37,97 R$ 43,65 R$ 49,35 R$ 55,09 R$ 60,86 R$ 66,66 R$ 72,49 R$ 78,36

60% R$ 40,46 R$ 46,12 R$ 51,80 R$ 57,51 R$ 63,26 R$ 69,04 R$ 74,85 R$ 80,70

70% R$ 42,98 R$ 48,61 R$ 54,27 R$ 59,96 R$ 65,68 R$ 71,44 R$ 77,23 R$ 83,06

Appendix 12.1: Governance and Management (Bord of Directors)

494

100

163

204

204

163

100

100

Name Position Description

Eugênio Pacelli Mattar President Director

Mr. Eugênio Mattar is one of the founders of the Company. Today, he is

counselor of the Company and executive director President of the Company

(CEO) and it`s affiliates. He holds a bachelor`s degree in Civil Engineering from

UFMG in 1975 and a graduate degree in economics engineering in 1976. Mr.

Mattar studied administration in Fundação Dom Cabral.

Roberto Antônio Mendes CFO and Investor Relations

Mr. Roberto Mendes is Director of Finance and Investor Relations of Localiza

rent a car S.A. where he has been working since 1985. He has a bachelor`s

degree in business administration and accounting sciences from UFMG. He

started his career as external auditor first in Pwc, then KPMG (1971-1979),

Controller of Valep (today, Fosfertil) in the time it was from Grupo Vale (1976-

1979), Mendes Júnior (1979-1985). He has a graduate degree in Executive STC

from Fundação Dom Cabral, in strategy and inovation in business from Wharton

University of Pennsylvania (2011) and also attended to Kellogg Scholl of

Management

Bruno Moreira de Andrade Executive Director

Mr. Bruno it is the Franchising Executive Director of the Company, in which he

joined in 1985. He holds a bachelor`s degree in Civil Engineering from Escola de

Engenharia Kennedy in 1983, also holds a graduate degree in economics

engineering from Fundação Dom Cabral, Marketing (UNA), Franchising

development from St. Thomas University (Minneapolis, USA) and Executive STC

from Fundação Dom Cabral and Kellogg Scholl of management (Chicago/USA).

Eugênia Maria Rafael de Oliveira Executive Director

Mrs. Eugênia Oliveira it is Executive Director of the Company, in which se joined

in 1980. She holds a bachelor`s degree in Business Administraton from PUC-MG

in 1981 and a graduate degree in marketing from UMA in 1985. Mrs. Eugênia

Oliveira was part of 2003 class of management from Kellogg

Appendix 12.2: Governance and Management (Bord of Directors)

494

100

163

204

204

163

100

100

Marco Antônio Guimarães Executive Director

Mr. Marco Antônio is the Company`s executive director, in which he joined in

1990. He holds a degree in business administration from FUMEC in 1978 and

holds a graduate degree in management from Keramik Holding Laufen from

Gstaad in Switerland in 1988 and a portable MBA in management in Brazil -

Santili, Schlouchauer & Jucá in 1994. Mr. Guimarães was part of 2002

management program from Kellogg School of management.

Edmar Vidigal Paiva Executive Director

Mr. Paiva it is Executive Director of Localiza rent a car S.A.. He holds a bachelor`s

degree in Accounting Sciences from PUC-MG in 1998. He holds a graduate

degree in Finance from IBMEC, Executive MBA and Executive Development

Program, both from Fundação Dom Cabral. He was Controller manager of Líder

Aviação e auditor manager of Deloitte Touche Tohmatsu.

Heros di Jorge Executive Director

Mr. Heros di Jorge holds a bachelor degree in Economics and Administration,

and also holds a graduate degree in Financial Mathematics and Executive MBA

from Fundação Dom Cabral. Mr. Heros has been working in the Company since

1987, first in sales of car`s rent in São Paulo, then he was Director os sales of

Lozaliza Gestão de Frotas in São Paulo, he was promoted to regional manager of

Localiza Seminovos in São Paulo and in 2012 took the retail`s car sales position

in the headquarters. He is Executive Director since July, 2016

Name Position Description

Appendix 13.1: Administrative Board

494

100

163

204

204

163

100

100

Name Position Description

Salim Mattar President

Mr. Salim Mattar is the Executive President of the Board of directors. He

founded the Company in 1973 and had been being the President Director of

the Company s until May 2013. Salim Mattar holds a bachelor`s degree in

business administration from FUMEC in 1976. Mr. Salim also is: Director of

Locapar Participações e Administração Ltda; Shareholder and advisor of OMNI

Táxi Aéreo andPottencial Seguradora S.A.

Antônio Cláudio Brandão Resende Vice-President

Mr. Antônio Resende is one of the founders of the Company. He holds a

bachelor`s degree in Business Administration from União de Negócios e

Administração in 1977. Currently, he is vice-president of the Administrative

Board Counsil and he was administrative Vice-President of the Company and

it`s affiliates until 2008.

Eugênio Mattar Advisor

Mr. Eugênio Mattar is one of the founders of the Company. Today, he is

counselor of the Company and executive director President of the Company

(CEO) and it`s affiliates. He holds a bachelor`s degree in Civil Engineering from

UFMG in 1975 and a graduate degree in economics engineering in 1976. Mr.

Mattar studied administration in Fundação Dom Cabral.

Flávio Brandão Resende Advisor

Mr. Flávio Resende is one of the founders of the Company and member of the

Administrative Counsil of the Company. He holds a bachelor`s degree in Civil

Engeneering from Escola de Enhenharia Kennedy in 1980. Mr. Resende also is

Administrative Partner of FBR Participações e Administração LTDA and

Administrative Partner of FRJR Empreendimentos imobiliários LTDA.

Appendix 13.2: Administrative Board

494

100

163

204

204

163

100

100

José Galló Advisor

Mr. José Galló is na independent administrative counsil member. He holds a

bachelor`s degree in Business Administration from Fundação Getúlio Vargas in

1974. He has been being administrative counsil member since 1998. Mr. Galló

also is: President Director and Administrative counsil member of Lojas Renner

S.A. and administrative counsil member of SLC Agrícola S.A.

Oscar Bernardes Advisor

Mr. Oscar Bernardes is na independent administrative counsil member of the

Company since 2007. He was Bunge International CEO (1996-1999). Before

Bunge, he was Senior Partner of Booz-Allen & Hamilton. He was also

administrative counsil member of Alpagartas S.A., Delphi Corporation and

Johnson Eletric.

Stefano Bonfiglio Advisor

Mr. Bonfiglio is na independent advisory member since 2000. He holds a

economics degree from Georgetown University in 1985 and a MBA from

Wharton School in 1992, also he holds a M.A. in International Relations from

the University of Pennsylvania.Mr. Stefano Bonfiglio is founder partner of

Stirling Square Capital Partners, a private equity firm specialized in acquisitions

in Europe and Chairman of Axitea S.p.A.

Letícia Costa Advisor

Mrs. Maria Letícia Costa is na independent advisory of the Company. She holds

a bachelor`s degree in Production Engineering from Escola Politécnica da

Universidade de São Paulo and holds a MBA from Johnson School of Cornell

University. Mrs. Maria Letícia Costa also is Partner at Prada Assessoria and

Graduate director of Instituto Insper in São Paulo.

Name Position Description

Appendix 14: Awareness

494

100

163

204

204

163

100

100

2015 Awards

Franchising excellence seal (Brazilian Franchising Association)

32th most valuable Brazilian Brand (Isto É Magazine – BrandAnalytics)

One of the most admirable Brazilian HR (HR Management Magazine)

Best Investor Relationship programs in Brazil (IR Magazine)

Company with good relationship with journalist (Business Communication Magazine)

Localiza: Among 13 Companies in the World cited for GARTNER as a IT reference

Best CEO, CFO, IR and best IR program in Latam (Institucional Investor Magazine)

Best Companies for consumer (Época Reclame Aqui)

25th most valuable Brazilian Brand

Excellence in Finance Award (IBEF 2015)

Appendix 15: SWOT Analysis

494

100

163

204

204

163

100

100

Forces Weaknesses

1. High performance management, widely recognized by the market, which has

been delivering a better result than others competitors. According with

Institutional Investor Magazine, Localiza has the best CEO, CFO and IR in Latam.

1. Some importante and experienced managers like Marco Antônio Guimarães

(Seminovos) and Daltro Leite are expected to retire in short term. In mid-term,

Eugênio Mattar (CEO) and Roberto Mendes (CFO) also are expected to retire.

2. 25th most valuable brazilian brand (Interbrand ranking) and quality recognized

by customers – best Car Rental Company (Época Reclame Aqui Award).

2. Business strongly dependente on GDP performance. The current recession of

two years and uncertainities about the possible recovery of the economy put in

risk the company`s performance.

3. Largest single purchaser of light vehicles, resulting in better bargaining power

and payment discounts.

3.Financial results largely dependent on the conditions of purchase of new

vehicles and the sale of semi-new

4. Seminovos divisions has the strategic function to sell Localiza`s used cars

directly to the final consumer. Without intermediaries, it is possible to have better

margin on the sale.

Opportunities Threats

1. RAC and Fleet markets are not consolidated yet. Localiza is the best positioned

Company to grow with quality in this scenario

1. Major foreign players such as Hertz and Enterprise can raise the bet in the

Brazilian market, competing with Localiza in industry consolidation.

2. Localiza has been being solid financial results, usually better than the

competitors. In this scenario, it is possible to growth with or without mergers and

acquisitions.

2. Possibility of no concession renewal in airports, which may affect considerably

the company`s operating and financial results.

Appendix 16: Brand Recognition

494

100

163

204

204

163

100

100

50

55

60

65

70

75

80

2012 2013 2014 2015 1Q16

Localiza Unidas -adjusted Movida - adjusted

RAC Utilization Rate (adjusted by Localiza’s Method)

Appendix 18: Utilization Rates

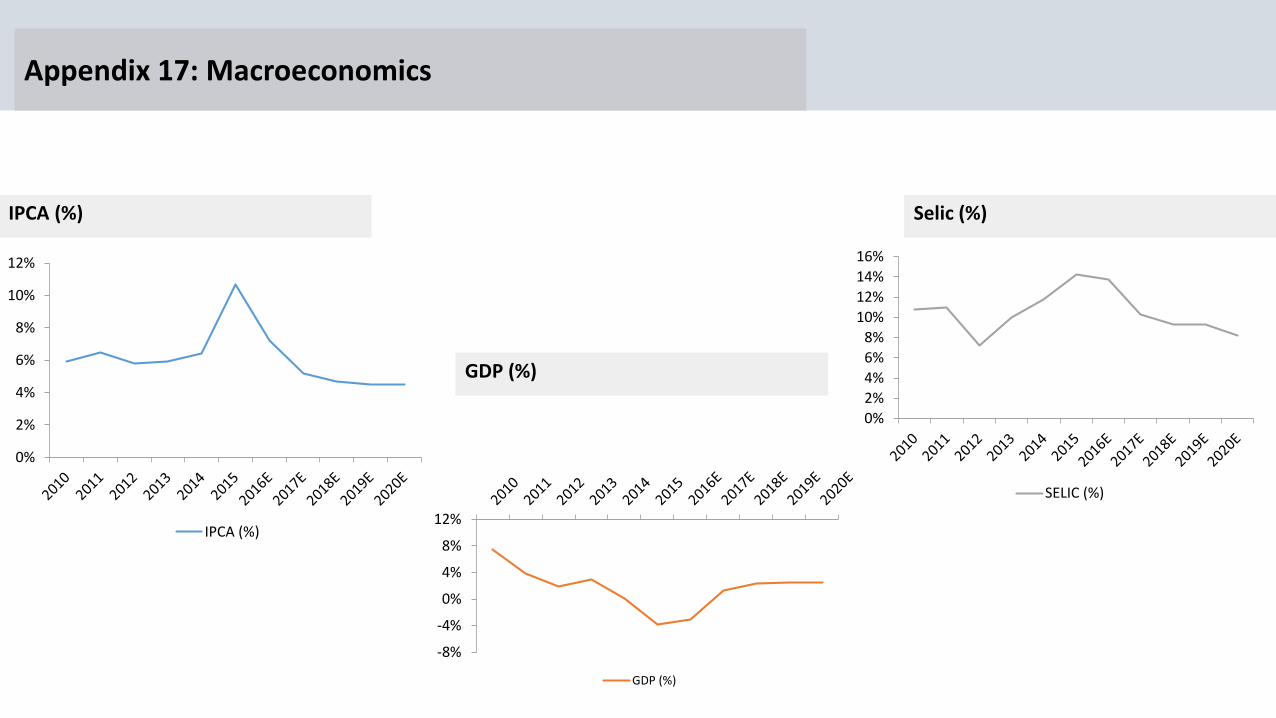

Appendix 17: Macroeconomics

494

100

163

204

204

163

100

100

0%

2%

4%

6%

8%

10%

12%

IPCA (%)

IPCA (%)

0%

2%

4%

6%

8%

10%

12%

14%

16%

SELIC (%)

GDP (%)

-8%

-4%

0%

4%

8%

12%

GDP (%)

Selic (%)

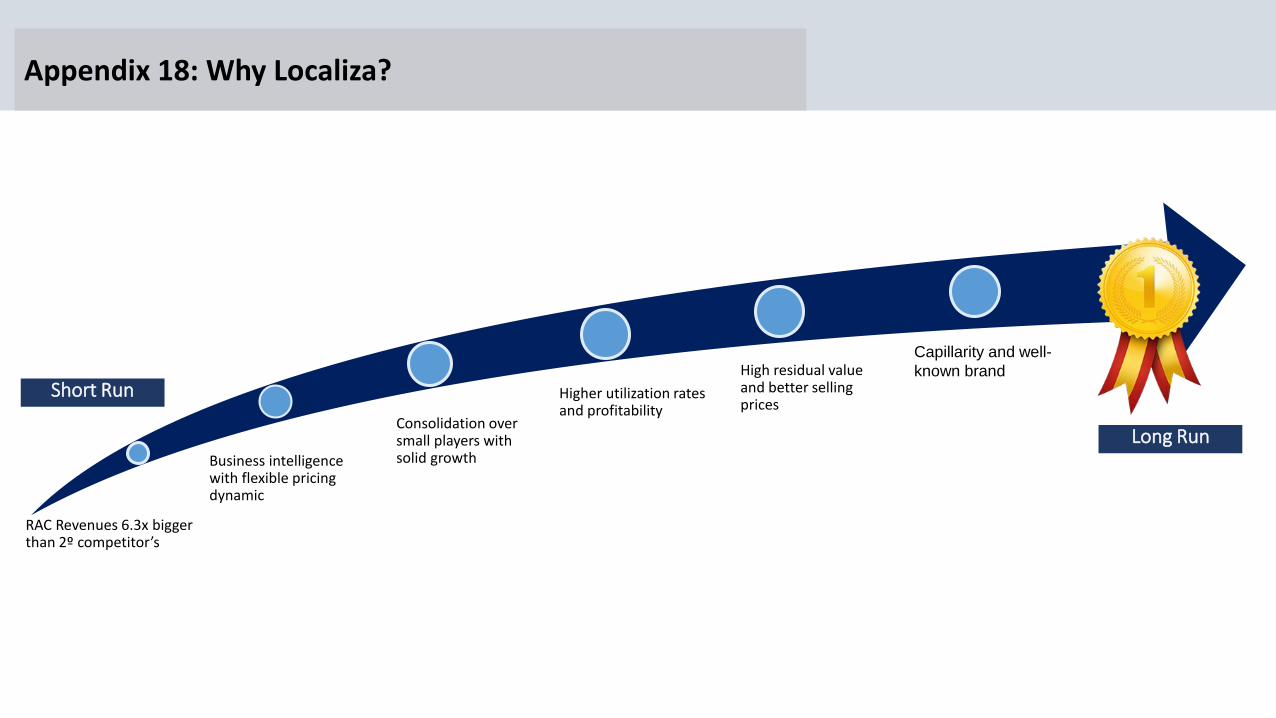

Appendix 18: Why Localiza?

494

100

163

204

204

163

100

RAC Revenues 6.3x bigger than 2º competitor’s

Business intelligence with flexible pricing dynamic

Consolidation over small players with solid growth

Higher utilization rates and profitability

High residual value and better selling prices

Capillarity and well-

known brand

Short Run

Long Run

Appendix 19: Revenue Forecast

494

100

163

204

204

163

100

34% 34% 33% 34% 34% 35% 35%

17% 17%15% 15%

16%16%

16%47%

49%51% 51%

49%49%

49%

0

1

2

3

4

5

6

2012 2013 2014 2015 2016E 2017E 2018E

Car Rental Gross Revenue Fleet Rental Gross Revenue Car Sales Gross Revenue

Revenue Breakdown

Source: Company’s Data

6.0%

6.0%

9.2%

5.8%

Appendix 20: Leverage

100

163

204

204

163

100

Debt Ratios

Source: Company’s Data and Bloomberg

End of period 2010 (*) 2011 2012 2013 2014 2015 9M16

Net debt/Fleet Value 52% 51% 48% 48% 40% 44% 44%

Net debt/Ebitda (**) 2.0x 1.7x 1.4x 1.5x 1.4x 1.7x 1.9x

Net debt/Equity 1.4x 1.2x 0.9x 1.0x 0.8x 0.8x 0.9x

EBITDA/ Net Interest Expenses 5.0x 4.6x 6.3x 8.3x 4.6x 4.6x 4.4x

Appendix 21: Car Sales Advantages

494

100

163

204

204

163

100

Seminovos Stores (78)

Source: Company’s Data