technical assistance to the government of punjab debt

TRANSCRIPT

1

Technical Assistance to the

Government of Punjab

Debt Management Unit

March 12, 2018

This publication was produced for review by the United States

Agency for International Development. It was prepared by USAID

Financial Market Development Activity.

FINANCIAL MARKET DEVELOPMENT ACTIVITY

2

DISCLAIMER

The author’s views expressed in this publication do not necessarily

reflect the views of the United States Agency for International

Development or the United States Government.

Technical Assistance to the

Government of Punjab

Debt Management Unit

FINANCIAL MARKET DEVELOPMENT ACTIVITY

3

Table of Contents

LIST OF ACRONYMS ............................................................................................. 4

MEETING COUNTERPARTIES .............................................................................. 4

INTRODUCTION ..................................................................................................... 5

CURRENT STATUS OF GOPB DEBT MANAGEMENT ......................................... 6

1.1 Responsibilities of DMU ............................................................................................................ 6

1.2 Debt amount outstanding, structure, and type of debt obligations ........................................... 6

1.3 Punjab Provincial Government Debt as of December 2017 ..................................................... 7

BASIC STRUCTURE OF DEBT INSTRUMENTS AND TRANSACTION

RECORDING .......................................................................................................... 8

CURRENT STAGE: TRACKING OF LOANS, DISBURSEMENTS, AND DEBT

SERVICE .............................................................................................................. 10

PROPOSED SOLUTION ....................................................................................... 13

ISSUES REQUIRING FURTHER CLARIFICATION .............................................. 14

PROPOSED ACTION PLAN ................................................................................. 15

ANNEX 1: DEBT REPORT ................................................................................... 16

ANNEX 2: DMFAS VERSION 6 ............................................................................ 17

ANNEX 3: DEBT SECURITY EXAMPLE IN A BASIC DATABASE STRUCTURE 18

ANNEX 4: LOAN AMORTIZATION TABLE ........................................................... 19

4

LIST OF ACRONYMS

AGPR Accountant General Pakistan Revenue

BPC SAP Business Planning and Consolidation tool

CSDRMS Commonwealth Secretariat Debt Recording and Management System

DMFAS Debt Management and Financial Analysis System

DMU Debt Management Unit (of GoPb)

EAD Economic Affairs Division (of GOP)

FABS Financial Accounts and Budget System

GoP Government of Pakistan

GoPb Government of Punjab

NAM New Accounting Model

SAP Nationwide SAP based accounting and budget execution ERP system

MEETING COUNTERPARTIES

FMD team held meetings with following counterparties:

Debt Management Unit, Finance Department, Government of Punjab, Lahore

• Mr. Abdul Rehman Warraich - Head of Debt Management Unit

• Mr. Syed Muntazir Abbas - Financial Analyst

• Mr. Sonia Ata - Financial Analyst

Accountant General Punjab Office, Lahore

• Mr Umar Wasim, Additional AG and team

Treasury Office Punjab, Lahore

• Mr. Halid Mehmud, Treasury officer and team

Financial Accounts and Budget Systems at Accountant General Pakistan

Revenues

• Mr. Ammar Naqvi, Director General FABS and team

5

INTRODUCTION

Through Finance Bill 2015, the Government of Pakistan allowed all provinces to issue

subnational bonds and borrow 0.3% of GDP (subsequently increased to 0.85% of GDP).

Consequently, all provinces have planned to borrow through issuance of provincial

government securities.

The Gov’t Punjab, Debt Management Unit (DMU), plans to enter the debt capital market

through issuance of local government bonds, with other provinces likely to follow. During a

meeting held on 25 October 2017, DMU requested the FMD team’s assistance in the following

areas:

• Technical and advisory services for issuing bonds.

• Assistance on specification and selection of software for both internal and external

debt recording.

• Comprehensive accounting solutions for debt records management.

• Training and capacity building.

The FMD team held a series of meetings between October - December 2017. In addition, the

FMD team delivered a workshop to DMU and Finance Department senior officials on 7th and

8th of November 2017 at GoPb Finance Department / Debt Management Unit, Lahore. The

FMD team delivered a detailed presentation on debt securities issuance techniques and

recommendations regarding the choice of instruments, primary placement techniques, auction

modalities and potential investor base.

Through these engagements, DMU’s requirements for setting up a comprehensive recording,

accounting and reporting framework that should also enable appropriate control of

disbursement events for loans was discussed in detail.

Previous recommendations were summarized in FMD’s Report “Launch of a provincial debt

securities issuance program and proposal for further assistance to GoPb Finance Department

Debt Management Unit” completed in January 2018.

DMU has since requested technical support with the following:

1. Due Diligence of the existing process from loan signing to on-lending to GoPb, a

structured disbursement mechanism, and recording and accounting framework;

identification of gaps in existing recording and accounting system and suggestions of

the best possible method to address those gaps and improvement especially in

recording and accounting aspect.

2. Drafting of a comprehensive lending policy for GoPb for granting loans and issuing

provincial government guarantee to Public Sector Entities owned by GoPb.

6

The current report summarizes initial findings and draft recommendations for the first of the

aforementioned topics. This report is based on discussions with DMU on needs and single

meetings with Punjab Treasury Office, Accountant General Office Punjab and MD and senior

staff of AGPR Financial Accounts and Budget Systems, Islamabad. Prevailing procedures and

issues related to subnational debt management at Government of Punjab were briefly

reviewed. The involved partied are invited to comment on various questions, open issues, and

proposed next steps highlighted in this report to determine the best path forward. To this

end, the report concludes with a preliminary action plan to be discussed and/or modified for

final agreement by stakeholders to provincial debt issuance.

CURRENT STATUS OF GOPB DEBT MANAGEMENT

1.1 Responsibilities of DMU

According to the website of the Finance Department of the Government of the Punjab the

Debt Management Unit (DMU) has been established in Finance Department during FY 2015-

16 for developing and implementing a comprehensive plan for management of sub-national

debt. This entails raising the required amount of borrowing at low cost, diversify the sources

of borrowing and maintain a maturity profile that avoids excessive repayments in any one

year. DMU has been especially assigned following tasks:

1. Preparation and execution of debt management strategy.

2. Developing an automated database of debt and guarantees.

3. Developing and implementing the policies and procedures necessary for sound

administration of debt.

4. Assisting the Government in developing and implementing a legislative framework for

effective debt management.

FMD’s current assistance is related to the second of DMU’ tasks.

1.2 Debt amount outstanding, structure, and type of debt obligations

Currently GoPb debt consists of following items:

• Federally signed external loans for direct payment to provincial project management

units to be repaid by the provincial government through reductions from the monthly

revenue share allocations from the federal to the provincial government.

• Loans, for which proceeds are directly credited to Account 1 of GoPb.

DMU sees a substantial hurdle in getting timely and precise information on the payment of

interest and principal of external loans raised by the Federal Government, which are assigned

to Projects in Punjab, but served by the federal government towards external lenders.

7

DMU claims that the countrywide SAP system for budget execution at federal and provincial

level contains only information on the aggregate level of interest and capital expenditures but

does not allow querying loan by loan.

The Treasury Office of GoPb, claims that a recent change in regulations circumvents their

otherwise desirable endorsement of checks issued to third parties (project management units)

for direct payment loans. That means disbursements can be made for which no budget

allocation is available and disbursements might not necessarily recorded by the Treasury.

However, they seem to be able to enter loan related transactions loan by loan (by account

number and project code into the SAP accounting module).

The Accountant General Office Punjab praised the capabilities of the SAP based

nationwide accounting solution but mentioned also the lack of accessibility of disaggregated

data. They called for a datalink with SBP (which is not part of the system) for daily updated

exchange rates for conversion into PKR of foreign currency denominated receipts and

payment obligations.

The nation-wide SAP-based budget accounting system is maintained by Financial Accounts and

Budget Systems (FABS) at AGPR (Accountant General Pakistan Revenues). FABS comprises

the New Accounting Model(NAM), and a SAP-ERP-based Information Technology platform.

The New Accounting Model(NAM) was introduced in year 2000, through approval by the

Auditor General of Pakistan, to improve the traditional government accounting system by

bringing-in a shift towards modified cash-basis of accounting, double-entry book-keeping,

commitment accounting, fixed asset accounting and a new multi-dimensional Chart of

Accounts. A key objective of FABS (i.e. NAM, along with the SAP-based IT platform) was to

help produce timely, relevant, accurate, reliable and comprehensive financial reports for the

decision makers to enable effective accountability and better financial governance. Objectives

of FABS include effective budgetary management, financial control, cash forecasting, trend

analyses, fiscal administration and debt management.

According to AG Punjab, there is already work in progress to incorporate the debt

management function into FABS and this could be the gate through which DMU’s needs are

met. A centralized solution implies also that other provincial governments will gain access to

a debt management tool that is integrated into FABS. This would help avoid duplicate data

entries and need for frequent reconciliation. Whether the functionality of the envisaged FABS

debt management functionality fully meets the requirements of DMU regarding detailed data

retrieval, analysis, and reporting capabilities need verification.

1.3 Punjab Provincial Government Debt as of December 2017

According to the DMU’s latest debt report, as of December 2017 provincial public debt

consists of PKR 597.2 billion of external loans and PKR 12.5 billion of domestic loans. While

the former is comprised of more than 120 individual loans, it is exclusively from external

funding and on-lending to Punjab by the Federal Government, mainly from multilateral lenders

and bilaterally from China and France. The domestic borrowing, denominated in PKR, are

8

direct loans of the Federal Government to Punjab. Direct domestic borrowing from

commercial banks and/or through issuance of provincial government debt securities have not

yet materialized but are planned to reach PKR 25 billion during FY 2017-18.

DMU faces the challenge of consolidating these debt items into a single database, allowing not

only the regular production of a debt report, but also supporting the fulfillment of all other

tasks assigned to the unit.

BASIC STRUCTURE OF DEBT INSTRUMENTS AND

TRANSACTION RECORDING

A database supporting debt management, meeting reporting and analysis needs, consists of

four basic tables, which include:

1. Table of instruments, for which a unique instrument identifier serves as primary key.

Each record represents a debt instrument (e.g. loan or bond) and the fields describing

the salient features of the instrument.

2. Cash Flow table for each instrument, that defines the repayment schedule of a unit of

each instrument

3. Table of transactions for each instrument. A transaction is modifying the quantity

outstanding for each instrument, thus it comprises of primary placements, including

re-openings and buy-backs of a debt security and disbursements and prepayments of

a loan.

4. Finally, the amortization table shows the repayment schedule (interest or coupon,

principal and other fees) for each instrument at a certain date, taking into account all

transactions completed until that date.

The following entity-relationship diagram shows the basic relations between tables of the debt

database:

9

This basic scheme needs to be augmented with at least two more tables, notably daily

exchange rates, to calculate PKR amounts of foreign currency denominated loans and bonds

and reference interest rates (e.g. KIBOR, LIBOR) for variable interest rate loans.

In a cash accounting environment records of the Transactions and Amortization tables can

be linked to the corresponding accounts in the Chart of Accounts:

• Sale of bonds and disbursements of loans are classified as capital receipts, buy-backs

of bonds, prepayment of loans and final redemption of principal are treated as capital

expenditures.

• Interest, coupon payments and any service fee are classified as current (interest)

expenditures.

• In case of negotiable instruments, which may be sold at discount or premium the latter

would be accounted as interest expenditure, respective interest revenue on the date

the transaction is completed.

Usually, for loans, especially for foreign project loans, the calculation of the amortization

profile is more complex than for most other debt instruments:

• Many loan agreements foresee the loan to be split into tranches and different tranches

with different features, including varying currency denominations, interest, and

10

principal repayment profiles. Therefore, in these cases each loan tranche must be

treated as an individual debt instrument.

• The amount of interest to be paid on the first interest payment date after a

disbursement depends on the interest rate and the number of days between the

disbursement date and the date of the next upcoming interest payment date.

Therefore, the actual amortization profile of a loan requires a consolidation of all

individual disbursements, unlike a bond, where the amortization profile does depend

only on the amount of bonds issued and sold.

• Loans carry a fee structure that may partially also depend on e.g. undrawn amounts.

• Capitalized interest, which is not due until a pre-set date, but added to the principal

amount, may substantially change the amortization profile.

Debt management software like DMFAS or CSDRMS have built in cash flow and amortization

table templates for practically all standard types of loans provided by multilateral finance

institutions and, in addition, allow for an individual, manual parametrization for loans that do

not fall into standard categories.

CURRENT STAGE: TRACKING OF LOANS, DISBURSEMENTS,

AND DEBT SERVICE

The current state of tracking disbursements and debt service at GoPb level is mostly related

to the treatment of external loans, for which DMU has a limited control over the payment

flow. Although GoPb co-signs all external loan agreements that are dedicated to finance

projects in Punjab, DMU must consolidate its debt records with lender databases. This is due

to two information access deficiencies in the current treatment of recording of debt related

payment flows:

• There is no immediate, direct, and automatic access to information about debt service

operations by the Federal Government towards external lenders. GoPb faces debt

service obligations only indirectly through the monthly reduction from revenue share.

It is not clear, how these monthly reductions can be split into principal repayments

(debt reducing capital expenditures), interest or fee payments and, to which of the

outstanding loans the payment can be attributed.

• Disbursements for direct payment loans, although recorded into FABS by the Punjab

Treasury Office are not accessible by DMU on a loan-by-loan basis.

According to information from Accountant General Punjab Office the flow of information and

accounting for receipts, interest and principal payment of foreign loans is the following:

Receipts of foreign loans

1. SBP, Lahore sends credit advice of foreign loan receipt to Treasury Office, Lahore and

copy to AG office.

11

2. Treasury office Lahore enters the credit advice into the SAP system together with

necessary object codes (Loan ID?) to be booked as a capital receipt into account

E03302 – foreign debt received from Federal Government.

3. AG Punjab office prepares, and rand submits monthly reconciliation to the concerned

departments of GoPb and obtains confirmation in respect to the receipts booked.

4. In case of third party payments accounting entries are received from Finance

Department by AG and incorporated as a separate disclosure in the Financial

Statements of the Provincial Government. (FMD’s understanding is that capital

receipts of third parties are also entered into the SAP system by the Treasury office)

Payment of interest and principal of foreign loans

1. Payment of principal and interest on foreign loans is made from GoPb budget in form

of a deduction at source from federal transfers by the Federal Government, intimated

through letter by Finance Division, GoP

2. Classification regarding grant, cost center and detailed object code is communicated

to AG Punjab by Finance Department, GoPb.

3. AG Punjab Account Current Section books this amount in SAP on receiving clearance

memo from SBP head office.

Improvements to the aforementioned process of recording receipts and debt service

suggested by AG are the following:

1. FABS SAP accounting system should provide for entering the Loan ID foreign currency

amount and exchange rate to track loan wise receipt and payments.

2. FABS SAP accounting system should provide for recording of third party payments.

3. Integration of data of existing and future loans into SAP system for booking receipts

and payments against a specific loan number.

FMD suggests following recommendation 1 and 2, but not necessarily 3, for the following

reasons:

1. The FABS SAP accounting system should be extended with a table of external loans,

recording in appropriate fields all salient features of external loan agreements

concluded by the Federal Government. A linked table should capture all

disbursements, identified by loan ID and value date, in the currency of disbursement

and also converted into PKR based a daily mid exchange rates provided by SBP.

Each loan needs to be flagged as federally utilized or assigned to a Provincial

Government project. In the latter case it is local Treasury offices that are obliged to

record disbursements, including those that are done by third parties’ Project

Management Units.

12

2. Spending of third party Project Management Units does not seem to be accounted for

budget expenditure in the currently used Chart of Accounts. However, disbursements

from foreign loans to PMUs are capital receipts that increase the GoPb debt

outstanding. That would require accounting for an increase of the expenditure side of

the provincial budget and this is certainly best done by adding an account for third

party investment expenditures into the Chart of Accounts and FABS SAP accounting

system which would exactly match the amount of those imbursements.

The SAP platform in its implementation for FABS in Pakistan does not have a “Debt

Module” as this has been assumed in previous meetings in Lahore. It is another SAP

module, notably the SAP Business Planning and Consolidation (BPC) tool that

is available to the FABS development staff and intended to be used for the recording

of debt and debt related transactions. This system development tool may provide a

solution for recording and making accessible for authorized users data on individual

loans, including those that incur payments to third parties.

3. As for the proposal of covering full loan amortization schedules and even future loans

for debt and budget planning purposes there are challenges. For the time being,

external loans are recorded federally by EAD in the DMFAS system, and parallel for

transactions into FABS, also by EAD. As already stated, disbursements for loans on-

lent to provincial governments are entered into FABS by the Treasuries of the

respective provincial governments. Repayments to the foreign lender are, again,

recorded at federal level. However, maintaining an up to date database for external

loans in DMFAS requires these disbursements also to be recorded by EAD.

Currently, DMFAS 5.3 is installed at EAD. Version 5.3 is a client server infrastructure

supposed to be used locally at the venue where it is installed. An upgrade to Version

6 is planned for 2018 and this upgrade will result in a complete reshuffle of the IT

infrastructure. Version 6 is web based and authorized users can access it through a

browser remotely through intranet or internet. Version 6 covers far more instruments

for recording, including conventional and Islamic instruments, loans, and debt

securities. It allows for linking with other financial information management systems

(e.g. SAP) and a wide range of role-based user access regulation. It also maintains the

main functionality of debt management software: the tracking of all items of the debt

portfolio, covering all loans, tranches, disbursements, repayments and the generation

the amortization profile of all debt obligations outstanding.

Such would result in a duplication of efforts and of data recorded, if the SAP Business

Planning and Consolidation (BPC) tool is to replicate this functionality of the

already in use DMFAS system. There is already a replication ongoing: EAD enters debt

related transactions in parallel, into DMFAS, and into the SAP accounting system.

13

FMD is recommending and looking for a solution that:

• Ensures a better synchronization between debt data recorded in DMFAS and

in the SAP accounting system, avoiding duplicated manual data entry; and

• Making essential information from the DMFAS database, notably the actual

amortization profiles from DMFAS accessible to provincial DMUs.

PROPOSED SOLUTION

Although there are a range of countries where DMFAS or CSDRMS is installed and used at

subnational levels it doesn’t seem to be an appropriate solution for Pakistan’s current

arrangement for the treatment and management of debt at provincial level. For Punjab, the

current debt profile consists of 98% external loans, originated by the Federal Government

and already tracked in two separate systems. What is supposed to become additional debt,

originated by GoPb will be a few new domestic commercial bank loans and/or publicly offered

debt securities. All transactions for this debt, and access to information thereof, will be fully

under control of GoPb Finance Department. Debt outstanding and amortization profile of all

items can be practically and easily summarized in the above outlined basic structure of a debt

database. Whether the SAP Business Planning and Consolidation (BPC) tool can be

utilized to provide such functionality is yet to be examined. If this tool can be used, then a

solution should be developed that can be utilized separately by all provincial governments.

As for the treatment of external debt the following scheme is suggested:

1. External loan agreements (assigned to Punjab)

• Registered into DMFAS and into FABS SAP by EAD (with the change to DMFAS

version 6 FMD suggests to programmatically generate the input record to SAP by

DMFAS)

2. Disbursements

• Recorded by TO Punjab into SAP, SAP generates and sends disbursement record

to EAD/DMFAS

3. Payment of interest, fees, principal to foreign lender

• Recorded by EAD into DMFAS and SAP

4. Deduction at source of debt service for GoPb

• GoP MoF Finance Division calculates monthly reduction of debt service from

revenue share to GoPb, notifies GoPb about amount and breakdown into interest,

fees, principal, to be entered into SAP at federal level or provincial Treasury office

5. Access to information on external loans for Punjab DMU

• DMU is given read access to SAP tables on registered loan agreements assigned to

Punjab province, disbursements on loan wise (including those that constitute

payments to third parties) and loan wise debt service completed by the federal

Government through SBP

14

• DMU receives monthly an update of amortization tables for all loans registered in

DMFAS database and assigned to Punjab province. After the change to DMFAS

Version 6, DMU may be given direct read access to the DMFAS database for all

loans assigned to GoPb.

6. Coverage of domestic borrowing by GoPb

There are two options:

• DMU sets up a small database with four related tables (instruments, cash flow,

transactions and resulting amortization profiles) for outstanding PKR loans from

the Federal Government (declining amount of PKR 12 billion on December-17)

and to capture newly raised commercial bank loans and publicly issued provincial

debt securities. This can be done with local IT support in Excel, Access or any

standard relational database management system with a simple front end.

• FABS uses the SAP Business Planning and Consolidation (BPC) tool to

develop such functionality. Most likely DMU would register the instruments into

the database provided by BPC, while Treasury Office Punjab would be responsible

for entering sales/drawings and debt service operations. Such a solution is

preferred by FMD, as it offer SAP supported debt management functionality not

just for Punjab, but for all provinces of Pakistan.

7. Consolidation of all debt data

• Provided amortization profile tables of all instruments, for external loans, as well

as for domestically raised loans and debt securities do have a exactly the same

structure, then they can be joined into one single table, allowing the creation of

practically all necessary indicators of provincial debt. This can be done with any

suitable Business Intelligence tool.

ISSUES REQUIRING FURTHER CLARIFICATION

As this report summarizes findings on the current treatment of and potential improvements

to provincial-level debt and debt related transaction recording further issues were uncovered

and need clarification. FMD proposes getting more insight on current procedures regarding

the following:

• Is Treasury Office Lahore supposed to enter all disbursements of loans including third

party direct payments and prospectively disbursements from borrowing from local

commercial banks or issuance of provincial government securities into the SAP

accounting system?

• If this is done on a loan wise basis, with loan ID and project code attached, can this

information, recorded in SAP, made available, through read-only select queries, to

authorized end users, like DMU and AG Punjab?

• What information on loan agreements and interest, fee and principle payments are

stored in SAP and can it be made accessible to authorized end-users, like DMU?

15

• Would it be possible for provincial governments’ DMUs, in this case for Punjab, to

receive a monthly update of amortization tables from the EAD DMFAS database?

• Is the DMFAS database at EAD fully synchronized or reconciled on a regular frequency

with loan data entered into the SAB accounting system?

• Can DMU given access to those disaggregated tables in the SAP accounting system

that contain debt instrument and debt related transaction records for GoPb debt,

including direct payments to third parties?

PROPOSED ACTION PLAN

Next steps to further the development of provincial debt issuance include:

1. FMD develops a detailed flow chart illustrating the current flow of approvals, debt

related payments and residence of disaggregated information upon them within the

current SAP system table/view structure.

• Involved parties: DMU, Treasury Office Punjab, Accountant General Office

Punjab, FABS. LOE: 5 days (3 Lahore, 2 Islamabad).

2. FMD develops a proposal for re-design of the data collection business process that

ensures improved access of DMU to debt data in the SAP system

• Involved parties: same as under 1. LOE 5 days (3 Islamabad, 2 Lahore).

3. FMD works with FABS on the use of the SAP Business Planning and Consolidation

(BPC) tool to cover debt management operations of provincial governments and

provide DMU with the required elementary debt data (i.e. consolidated amortization

profile of all outstanding debt items) suitable for creating required reports, debt

indicators and base data for risk analysis and issuance planning.

• Involved parties: FABS. LOE 5 days (Islamabad).

4. FMD assists DMU on the introduction of a Business Intelligence tool for further

processing of and reporting on consolidated debt data made available under 3.

Activity

• Involved parties GoPb DMU. LOE 5 days (Lahore) + 15 days of a local IT expert.

FMD proposes to postpone enquires about a deeper integration into debt management of

the existing DMFAS installation at EAD until the version upgrade to DMFAS Version 6 is

completed.

16

ANNEX 1: DEBT REPORT

17

ANNEX 2: DMFAS VERSION 6

DMFAS software is designed to help countries manage their external and domestic public

debt. DMFAS manages debt obligations such as government debts, government-guaranteed

debts and on-lending debts, as well as grants and debt reorganizations. It can also be used to

monitor private non-guaranteed external debt. DMFAS fully meets the comprehensive needs

of a debt management office, whether front-office (issuance of debt securities), middle-office

(analysis) or back-office (registration and management of operations) tasks. Usually installed

in the Central Bank and/or Ministry of Finance, it provides accurate and timely information

for debt management. DMFAS enables debt officers to carry out the following operations:

• Record all information concerning loans, grants and debt securities, including their

possible relationship to projects and to different national budget accounts

• Create and update estimated disbursements automatically

• Calculate all amortization tables automatically

• Record real drawings, real subscriptions and debt service operations

• Identify loans where debt service is in arrears and calculate late interest

• Produce a wide range of standard and customized reports, including reports for

validation, control, and statistical bulletins

• Perform analysis of their debt portfolio and build debt strategies

The key benefits of DMFAS 6:

• Robust debt management capabilities: once the database has been filled with

information relating to loans, debt securities and grants DMFAS enhances the

autonomy and management of a debt office. As the system processes huge amounts

of information on debt, more time and energy can be deployed on analytical and

management tasks. For instance, DMFAS allows debt managers to do the following:

• Actively monitor the timing, amounts and terms of a country’s external and or

domestic liabilities

• Test the sensitivity of debt service to changes in interest rates and exchange rates

• Produce drawing requests and payment orders

• DMFAS can be run as a stand-alone system, on an intranet or an extranet, on most

operating and network systems.

• DMFAS offers powerful analytical and managerial tools for portfolio analysis

• and reporting. A robust security system enables managers to assign specific privileges

or restrict rights to users and user groups.

• DMFAS is user friendly: even with minimal training, beginners can build the DMFAS

database and generate reports. With its flexible interface, DMFAS allows for easy

customization; codes and field names can be modified by authorized end-users.

• Extensive documentation is provided on all modules including a contextual online help

system.

18

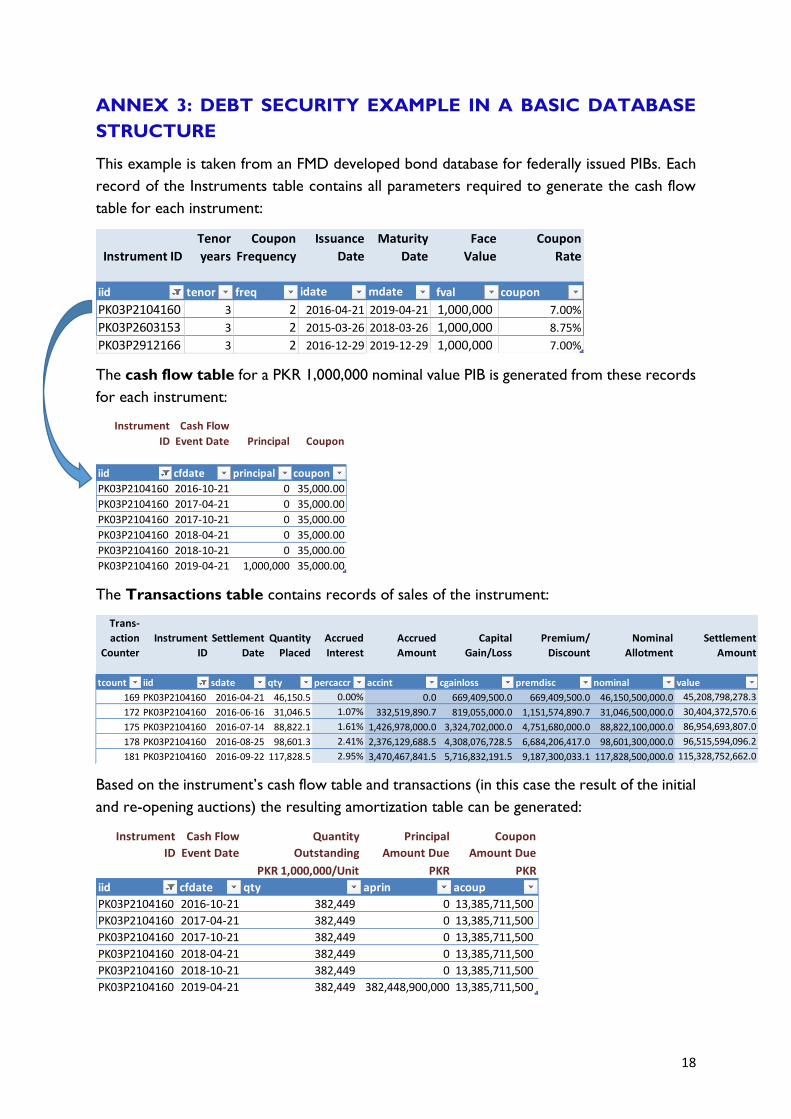

ANNEX 3: DEBT SECURITY EXAMPLE IN A BASIC DATABASE

STRUCTURE

This example is taken from an FMD developed bond database for federally issued PIBs. Each

record of the Instruments table contains all parameters required to generate the cash flow

table for each instrument:

The cash flow table for a PKR 1,000,000 nominal value PIB is generated from these records

for each instrument:

The Transactions table contains records of sales of the instrument:

Based on the instrument’s cash flow table and transactions (in this case the result of the initial

and re-opening auctions) the resulting amortization table can be generated:

Tenor Coupon Issuance Maturity Face Coupon

Instrument ID years Frequency Date Date Value Rate

iid tenor freq idate mdate fval coupon

PK03P2104160 3 2 2016-04-21 2019-04-21 1,000,000 7.00%

PK03P2603153 3 2 2015-03-26 2018-03-26 1,000,000 8.75%

PK03P2912166 3 2 2016-12-29 2019-12-29 1,000,000 7.00%

Instrument Cash Flow

ID Event Date Principal Coupon

iid cfdate principal coupon

PK03P2104160 2016-10-21 0 35,000.00

PK03P2104160 2017-04-21 0 35,000.00

PK03P2104160 2017-10-21 0 35,000.00

PK03P2104160 2018-04-21 0 35,000.00

PK03P2104160 2018-10-21 0 35,000.00

PK03P2104160 2019-04-21 1,000,000 35,000.00

Trans-

action Instrument Settlement Quantity Accrued Accrued Capital Premium/ Nominal Settlement

Counter ID Date Placed Interest Amount Gain/Loss Discount Allotment Amount

tcount iid sdate qty percaccr accint cgainloss premdisc nominal value

169 PK03P2104160 2016-04-21 46,150.5 0.00% 0.0 669,409,500.0 669,409,500.0 46,150,500,000.0 45,208,798,278.3

172 PK03P2104160 2016-06-16 31,046.5 1.07% 332,519,890.7 819,055,000.0 1,151,574,890.7 31,046,500,000.0 30,404,372,570.6

175 PK03P2104160 2016-07-14 88,822.1 1.61% 1,426,978,000.0 3,324,702,000.0 4,751,680,000.0 88,822,100,000.0 86,954,693,807.0

178 PK03P2104160 2016-08-25 98,601.3 2.41% 2,376,129,688.5 4,308,076,728.5 6,684,206,417.0 98,601,300,000.0 96,515,594,096.2

181 PK03P2104160 2016-09-22 117,828.5 2.95% 3,470,467,841.5 5,716,832,191.5 9,187,300,033.1 117,828,500,000.0 115,328,752,662.0

Instrument Cash Flow Quantity Principal Coupon

ID Event Date Outstanding Amount Due Amount Due

PKR 1,000,000/Unit PKR PKR

iid cfdate qty aprin acoup

PK03P2104160 2016-10-21 382,449 0 13,385,711,500

PK03P2104160 2017-04-21 382,449 0 13,385,711,500

PK03P2104160 2017-10-21 382,449 0 13,385,711,500

PK03P2104160 2018-04-21 382,449 0 13,385,711,500

PK03P2104160 2018-10-21 382,449 0 13,385,711,500

PK03P2104160 2019-04-21 382,449 382,448,900,000 13,385,711,500

19

ANNEX 4: LOAN AMORTIZATION TABLE

The treatment of loans differs in three aspects from that of bonds:

• There is no premium or discount due when a disbursement is calculated;

• The amortization schedule for each disbursement may contain a fragmented interest

payment depending on the value date of the disbursement, if in between two interest

payment dates and;

• Additional fees may be imposed by the lender (front-end fee and standby fee for

undrawn balances)

Below an example for the amortization table of a bullet loan with fixed interest and

disbursements of which two fall in between interest payment dates:

* Calculation of interest is based on ACT/360 day count convention in this example

Due to the way interest is calculated for loan disbursements, each tranche has to be treated

like a separate instrument, before the resulting cumulative amortization schedule is calculated.

The same approach needs to be applied for more complex structures, like variable rate loans,

loans with capitalized interest, etc.

6-year loan, 10% interest, paid annually, drawn through 3 disbursements, effective issuance date:

2014-06-15

Unit Disbursement dates and amounts Resulting

Date Cash flow 2014-06-15 2015-09-10 2016-10-10 Cumulative

300 400 300 Amortization

Interest Principal Profile

2015-06-15 100 0 30 9.67 39.67

2016-06-15 100 0 30 40 9.75 79.75

2017-06-15 100 0 30 40 30 100.00

2018-06-15 100 0 30 40 30 100.00

2019-06-15 100 0 30 40 30 100.00

2020-06-15 100 1000 330 440 330 1100.00

Amortization per disbursement