technology - ambitreports.ambitcapital.com/reports/ambit_technology... · 2017-02-15 · technology...

TRANSCRIPT

TECHNOLOGY

Research Analysts:

Trumped

Sagar [email protected]: +91 22 3043 3291

Sudheer [email protected]: +91 22 3043 3203

TCS INFY TECHM

WPROHCLT

CTSH

February 2017

Technology

February 15, 2017 Ambit Capital Pvt. Ltd. Page 2

CONTENTS

Trumped ………………………………………………………………………………..3

Protectionism will hurt margins, but not revenue growth ……………………….4

Why is this time different? ……………………………………………………………6

Only half of the margin drop will be recovered; not before 3-5 years ………..9

TCS fares the best, Cognizant the worst …………………………………………11

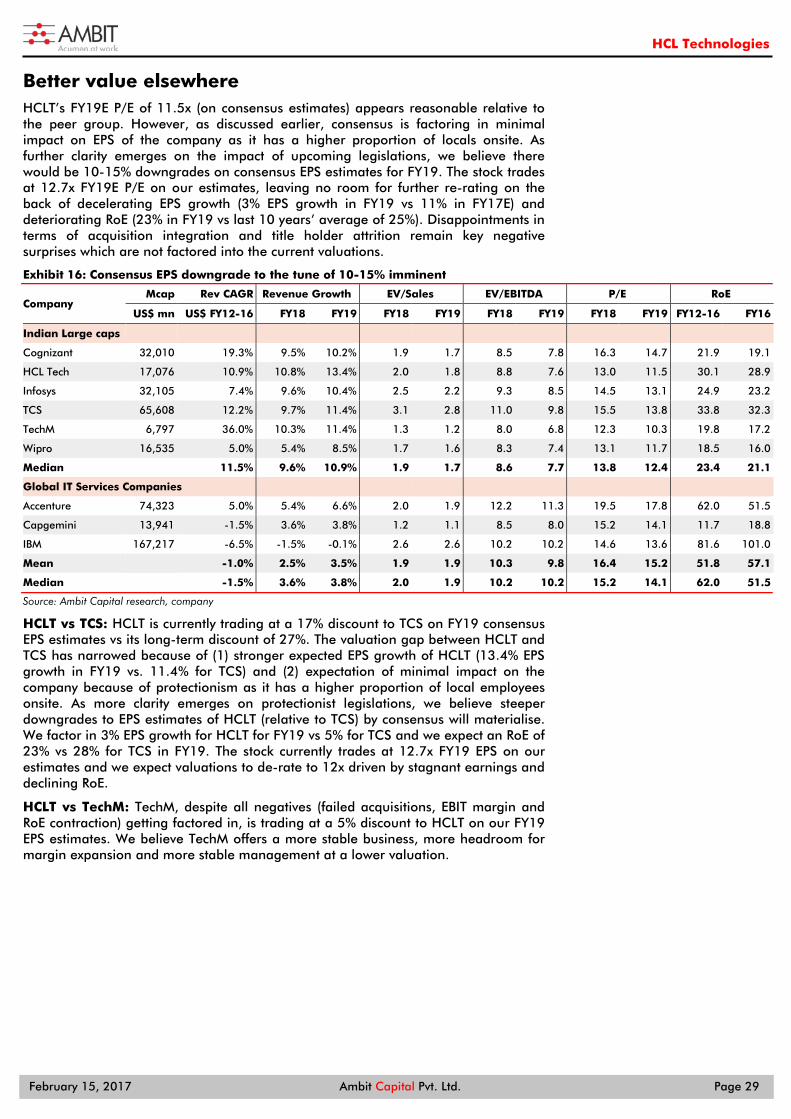

Stick to quality. TCS is our top pick, downgrade HCLT to SELL. ……………….12

COMPANY

HCL Technologies (SELL): Not prepared for the fight …………………………..17

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision.

Trumped

Protectionist measures by the Trump administration will not kill Indian IT but cause grievous bodily harm. Our base case scenario is that the cost of all onsite workers will spike to a minimum of US$100,000 p.a. (2x current minimum). Due to shortage of US-based IT talent, any forced increase in wages of H-1B visa-holders will quickly spread across substitutes including locals. This will hurt aggregate margin of top-6 Indian IT companies by 470bps over FY18-20; high competitive intensity and customer pushback will limit immediate re-pricing. Only half of the damage will be made up, and that too 3-5 years later. Cost of locals will gradually fall as supply increases but full recovery doubtful given stickiness of wages, lower onsite utilisation. Our pecking order is now TCS (top BUY) > Infosys, TechM > HCLT (downgrade to SELL) > Wipro > Cognizant (top SELL).

Protectionism will hurt margins but not revenue growth

Feedback from our US immigration expert and recent actions by the Trump administration make us worry. However, the intent is not to kill Indian IT but to prevent visa abuse. To boost local supply of talent, the Trump administration will likely accept higher costs for all US-based workforce, hurting margins. Indian IT's demand will be unchanged because: (1) technology (including IT services) continues to become more critical to business; (2) unlike manufacturing, offshoring of IT services can be done gradually and quietly; and (3) Indian IT will remain competitive as costs will rise for everyone. Only half of the margin drop will be recovered, but only in 3-5 years

By FY22-24, supply of US local IT workforce should increase in response to higher wages. Indian IT vendors by then will most likely staff locally (85%+) for US operations. Contract renewals beginning FY20 would provide opportunity to Indian vendors to re-price for higher employee cost; a phenomenon shared by the US companies for their own employees. Otherwise considered to be very efficient, Indian IT will have to get more efficient (reduced travel, more offshore delivery) but still stare at lower margins than present levels.

Cognizant to be hurt the most in terms of margin hit, TCS the least

Early investments in non-US markets, stronger processes for more offshore delivery and a place higher up the value chain (already high wages) will lead to more robust margins. Cognizant fares the worst (730bps hit) as we estimate that 21% of its employees are based in the US, of which 91% earn less than US$100K. We estimate only 350bps hit to TCS' margins because it likely has only 11% of its employees in the US, of which 83% earn less than US$100K. Stick to quality; TCS is our top pick; downgrade HCLT to SELL

TCS has the best track record with respect to managing margin shocks (EBIT margin has fluctuated within a 200bps band for 6 of the past 7 years) whereas HCLT/TechM have fluctuated as much as 8-10ppt over this time. TechM's low exposure to the US and scope to improve margins protect it somewhat. Infosys will be hurt due to its high exposure to the US, but at current valuations it is a steal. HCLT is ill-prepared to deal with looming structural challenges as it suffers from non-quantifiable risks from sudden spree of acquisitions, organisation structure and frequent CEO changes; we turn SELLers. We retain SELL stance on Wipro and Cognizant as they too struggle with internal transformations.

THEMATIC IT SERVICES February 15, 2017

Technology

NEGATIVE

Key Recommendations

TCS BUY

Target Price: Rs2670 Upside 11%

TechM BUY

Target Price: Rs560 Upside: 11%

CTSH SELL

Target Price: $37 Downside: 36%

Wipro SELL

Target Price: Rs430 Downside: 10%

HCLT SELL

Target Price: Rs750 Downside: 10%

On our framework, Cognizant fares the worst but TCS fares the best

Source: Ambit Capital research, company; Note: Size of bubble is proportional to the EBIT margin drop over FY18-20E.

80%82%84%86%88%90%92%94%96%98%

100%

10% 15% 20%

%a

ge i

f em

noly

ees

ea

rniu

ng

less

th

an

U

S$100K

%age of employee base in US

Research Analysts

Sagar Rastogi

+91 22 3043 3291

Sudheer Guntupalli

+91 22 3043 3203

TCS

TECHM

WPRO

INFO

HCLT

CTSH

Technology

February 15, 2017 Ambit Capital Pvt. Ltd. Page 4

Protectionism will hurt margins, but not revenue growth It is difficult to forecast the exact legislation, but the intent of the US government appears to be preventing visa abuse not killing Indian IT. So in our base case scenario, we assume that over FY19 and FY20 the cost per onsite worker for an Indian IT company will rise to a minimum of US$100,000 p.a. from ~US$50,000 now. We are different from consensus in that we estimate the cost of all onsite workers to increase instead of only the H-1B visa-holders. We estimate that this would not impact revenue growth of Indian IT but hurt margins by 350-730bps over FY18-20.

Our rationale for picking this base case Why an increase in cost and not an outright ban?

Trump administration intends to prevent abuse not kill Indian IT. Based on our discussions with our US immigration expert and our reading of recent legislation, the intent of the Trump administration is not to break the business model of Indian IT companies, which would hurt the technology competitiveness of American firms. It is to close loopholes for abuse and ensure that technology companies invest adequately in creating a skilled talent pool in the US. We believe that the Trump administration would do this by nudging companies to pay higher wages to visa-holders.

Why increase in costs for all onsite workers and not just H-1B visa-holders?

Because there is a shortage of talent currently and the talent supply is relatively inflexible, any increase in salaries for H-1B visa-holders for Indian IT companies will quickly percolate through the entire labour pool including locals, green card holders, other temporary visa-holders (e.g. L-1, B-1 in lieu of H-1B, H-4), sub-contractors, etc.

For instance, if the cost of an H-1B visa-holder is set at a minimum of US$130,000 p.a., an Indian IT company would opt to hire a local from a client or a competitor, which in turn would increase wages to retain talent.

Similarly, Indian IT companies could apply for green cards for their employees which would likely be exempt from the harsh protectionist measures. A green card, formally known as a US Permanent Resident Card, confers permission to reside and take employment in the United States. This is different from the H-1B and L-1, which are non-immigrant work visas.

What is the evidence of talent shortage?

As per the US Bureau of Labor Statistics, the unemployment rate in the “Information” industry was just 3.1% (Dec-16) vs the overall unemployment rate of 4.5%. Anecdotally as well, we hear of Indian IT workers in the US enjoying much better work-life balance and perks as compared to their peers in India; this also points to better bargaining power.

Why $100,000 p.a. and not US$130,000 p.a. or higher? Why over 2 years?

As discussed above, the Trump administration is business friendly and would not want to prohibitively increase the cost of IT services suddenly for all US businesses. Hence, we expect it to provide a glide-path of increase – perhaps, US$80,000 p.a. in the first year followed by US$100,000 p.a. in the second year.

We estimate that adverse protectionist action would not impact revenue growth of Indian IT but hurt margins by 350-730bps over FY18-20.

Trump administration intends to prevent abuse, not kill Indian IT.

Because there is a shortage of talent and the talent supply is relatively inflexible, any increase in salaries for H-1B visa-holders for Indian IT companies will quickly percolate through the entire IT labour pool.

As per the US Bureau of Labor Statistics, the unemployment rate in the “Information” industry was just 3.1% (Dec-16) vs. overall unemployment rate of 4.5%.

Technology

February 15, 2017 Ambit Capital Pvt. Ltd. Page 5

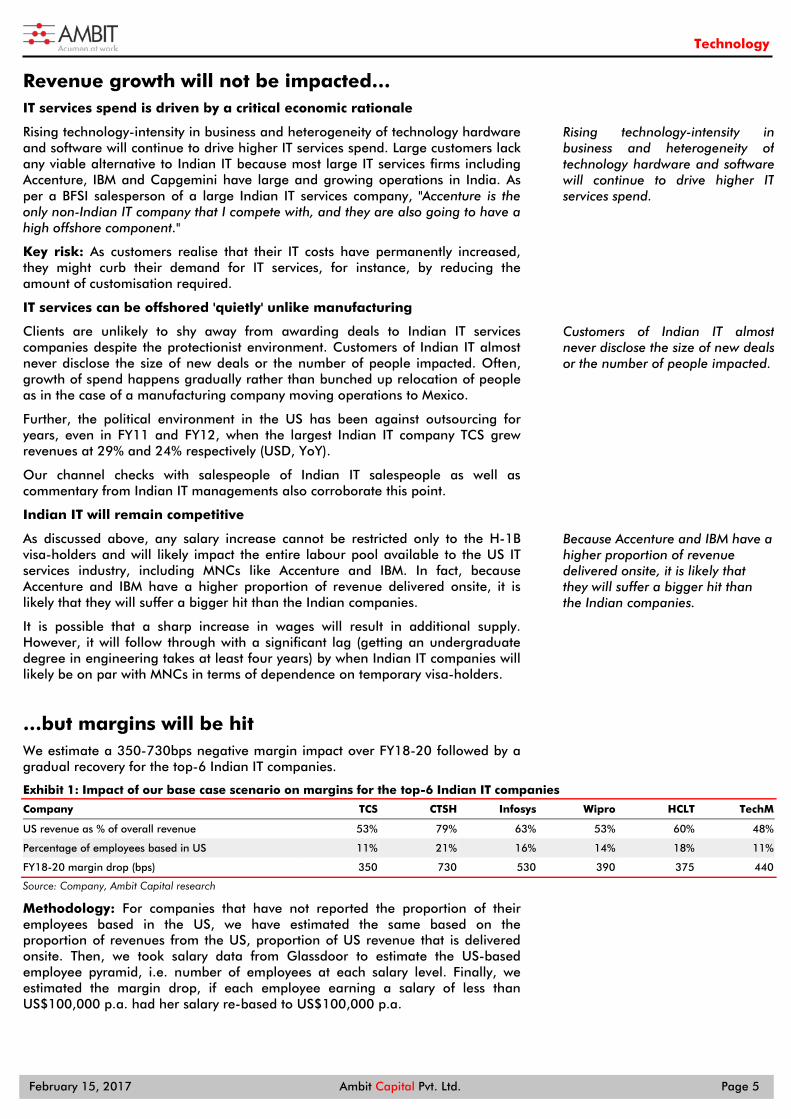

Revenue growth will not be impacted… IT services spend is driven by a critical economic rationale

Rising technology-intensity in business and heterogeneity of technology hardware and software will continue to drive higher IT services spend. Large customers lack any viable alternative to Indian IT because most large IT services firms including Accenture, IBM and Capgemini have large and growing operations in India. As per a BFSI salesperson of a large Indian IT services company, "Accenture is the only non-Indian IT company that I compete with, and they are also going to have a high offshore component."

Key risk: As customers realise that their IT costs have permanently increased, they might curb their demand for IT services, for instance, by reducing the amount of customisation required.

IT services can be offshored 'quietly' unlike manufacturing

Clients are unlikely to shy away from awarding deals to Indian IT services companies despite the protectionist environment. Customers of Indian IT almost never disclose the size of new deals or the number of people impacted. Often, growth of spend happens gradually rather than bunched up relocation of people as in the case of a manufacturing company moving operations to Mexico.

Further, the political environment in the US has been against outsourcing for years, even in FY11 and FY12, when the largest Indian IT company TCS grew revenues at 29% and 24% respectively (USD, YoY).

Our channel checks with salespeople of Indian IT salespeople as well as commentary from Indian IT managements also corroborate this point.

Indian IT will remain competitive

As discussed above, any salary increase cannot be restricted only to the H-1B visa-holders and will likely impact the entire labour pool available to the US IT services industry, including MNCs like Accenture and IBM. In fact, because Accenture and IBM have a higher proportion of revenue delivered onsite, it is likely that they will suffer a bigger hit than the Indian companies.

It is possible that a sharp increase in wages will result in additional supply. However, it will follow through with a significant lag (getting an undergraduate degree in engineering takes at least four years) by when Indian IT companies will likely be on par with MNCs in terms of dependence on temporary visa-holders.

…but margins will be hit We estimate a 350-730bps negative margin impact over FY18-20 followed by a gradual recovery for the top-6 Indian IT companies.

Exhibit 1: Impact of our base case scenario on margins for the top-6 Indian IT companies

Company TCS CTSH Infosys Wipro HCLT TechM

US revenue as % of overall revenue 53% 79% 63% 53% 60% 48%

Percentage of employees based in US 11% 21% 16% 14% 18% 11%

FY18-20 margin drop (bps) 350 730 530 390 375 440

Source: Company, Ambit Capital research

Methodology: For companies that have not reported the proportion of their employees based in the US, we have estimated the same based on the proportion of revenues from the US, proportion of US revenue that is delivered onsite. Then, we took salary data from Glassdoor to estimate the US-based employee pyramid, i.e. number of employees at each salary level. Finally, we estimated the margin drop, if each employee earning a salary of less than US$100,000 p.a. had her salary re-based to US$100,000 p.a.

Rising technology-intensity in business and heterogeneity of technology hardware and software will continue to drive higher IT services spend.

Customers of Indian IT almost never disclose the size of new deals or the number of people impacted.

Because Accenture and IBM have a higher proportion of revenue delivered onsite, it is likely that they will suffer a bigger hit than the Indian companies.

Technology

February 15, 2017 Ambit Capital Pvt. Ltd. Page 6

Why is this time different? We note that the US government has threatened protectionist action in the past and failed to follow through. There is also merit in the argument of Indian IT companies that protectionism would hurt all US businesses by raising the cost of IT, which is an increasingly vital expenditure. However, contrary to popular opinion which expected the Trump administration to tone down its campaign promises once it came to power, we have seen unprecedented steps such as the travel ban. Recent political appointees, the four legislations targeting the H-1B visa programme, and our discussions with Indian IT management indicate that unlike previous years, this time the threat of protectionism is real.

Trump administration is going all out to fulfil campaign promises US President Trump's recent executive orders to start building a US-Mexican border wall and travel ban on immigrants from seven predominantly Muslim countries for three months among others show that the he is willing to take unprecedented steps to fulfil his campaign promises even when he knows that they will provoke national or international outrage. We had highlighted this risk in our note dated 27th September 2016 and 5th January 2017.

H-1B visas are a target Whilst he has personally flip-flopped on the H-1B visa issue, his choice of appointees to important positions indicates a clear stance against Indian IT companies. For instance, US President Trump has nominated Senator Jeff Sessions, who had once proposed eliminating the H-1B visa programme entirely (link), for the position of Attorney General.

Our US immigration expert informs us that "Republicans hate the loopholes in the H-1B visa programme", especially since recent media articles in the New York Times and the Huffington Post have provoked outrage (link, link). For instance, there is currently no numerical limit on the number of 'B-1 in lieu of H-1B' visas that can be issued, which can be used similar to the H-1B visas.

Many adverse legislation have been introduced Two bills introduced in the US House of Representatives in January seek to significantly increase the minimum annual wage criterion for the "exempt H-1B non-immigrant" status from US$60,000 to US$100,000 and US$130,000 respectively. These are the 'Protect and Grow American Jobs Act' introduced by Congressman Issa (Republican) and the 'High-Skilled Integrity and Fairness Act of 2017' introduced by Congresswoman Lofgren (Democrat) respectively.

As per our US immigration expert, in practice, the requirements for non-exempt visa-holders are impossible to comply with. For instance, a US immigration expert that we consulted told us that vendors need to get their clients to attest that they would not displace any US worker 90 days prior or after applying for the US, which clients are not willing to provide.

On 20th January 2017, Senate Judiciary Committee Chairman Chuck Grassley (Republican) and Assistant Democratic Leader Dick Durbin introduced the H-1B and L-1 visa reform act of 2017. The most harmful clauses are: (1) firms employing more than 50 people, with more than 50% of their employees on such visas to not be allowed to apply for more visas and (2) The U.S. Citizenship and Immigration Services to prioritise allocation of the limited (85000 p.a.) H-1B visas based on the applicant's educational profile and salary instead of a random lottery (current practice).

US-Mexican border wall and travel ban are unprecedented steps.

Trump's choice of appointees to important positions indicates a clear stance against Indian IT companies.

Our US immigration expert informs us that "Republicans hate the loopholes in the H-1B visa programme".

Two bills increase the minimum annual wage criterion for the "exempt H-1B non-immigrant" status from US$60,000 to US$100,000 and US$130,000 respectively.

Grassley-Durbin bill could prevent Indian IT companies from getting more visas.

Technology

February 15, 2017 Ambit Capital Pvt. Ltd. Page 7

This would be highly detrimental for Indian IT firms. Most of them have more than 50% of their employees on temporary visas currently. Further, in case allocation is prioritised according to salary, they would not be able to compete with the likes of Google and Microsoft in terms of salaries. For instance, last year, the average salary of new H-1B visa-holder employees for Microsoft was US$129,610, 70% higher than the corresponding number for TCS. If last year's labour condition applicants were sorted in descending order of salaries, Indian IT companies would not have managed to get a single visa.

On 30th January 2017, Senator Joe Donnelly introduced the End Outsourcing Act. Key adverse clauses: (1) Federal contracts, funded by taxpayers, would only go to companies that have not outsourced domestic jobs and (2) Companies that ship jobs to foreign countries would forfeit tax breaks and incentives. This would prevent Indian IT's customers from getting federal contracts.

More on the way Separately, the Trump administration has talked about a border adjustment tax which would be imposed on all imports (link). This would also impose additional costs on Indian vendors.

As per Bloomberg (link), Trump's administration has drafted an executive order aimed at overhauling the work-visa programmes, with one of the provisions being that "businesses would have to try to hire American first and if they recruit foreign workers, priority would be given to the most highly paid."

Indian IT's changed tune is also a worrying signal Indian IT managements used to be dismissive earlier, but now appear to be preparing for adverse protectionist action on a war footing.

In earlier years, an Indian IT management's response to the threat of protectionism was to say that any such legislation would be unviable, pointing to the low unemployment rate in the US tech workforce.

However, recently TCS management said that it is cognizant of a threat to the price and quantity of H-1B visas, and that they were taking steps to counter the same. It also commented that TCS was likely the largest hirer of US locals in the IT industry last year, and that it had applied for only about one-third the visas in 2016 compared to 2015.

The CFO of a leading IT services company told us that this time they do expect some protectionist legislation and that their actions to counter the threat of protectionism have taken on an added urgency.

Even though recent bills could be dodged, we worry about the intent As discussed in our note dated 9th January 2017, the recent bills do not require increasing of wages of all H-1B visa-holders to these levels but only impose additional requirements on H-1B visa-holders that earn less than US$100,000 or US$130,000 (depending on the bill).

Whilst customers might be reluctant to give attestations today, we believe that they might be more flexible if it entails additional cost of US$40,000-70,000 p.a. per onsite worker.

Further, it is a misconception that non-exempt H-1B visa-holders are not allowed to be placed at client worksites.

The relevant clause is in section 1182(n)F of "Title 8 – Aliens and Nationality" in the US constitution. The clause states that outplacement is not allowed for non-exempt H-1B non-immigrants only in the case where two conditions hold: (1) non-immigrant performs duties at client’s location AND (2) there is evidence of employer-employee relationship between the visa-holder and the client.

End Outsourcing Act would prevent Indian IT's customers from getting federal contracts.

Indian IT management used to be dismissive earlier, but now appears to be preparing for adverse protectionist action on a war footing.

Customers might be willing to give attestations if it entails additional cost of US$40,000-70,000 p.a. per onsite worker

Technology

February 15, 2017 Ambit Capital Pvt. Ltd. Page 8

However, as a matter of course, Indian IT companies already take care to ensure that there is no evidence of an employer-employee relationship between the visa-holder and the client. For instance, they submit a client invitation letter (click here for a sample) as part of the visa application. Further, the US Citizenship and Immigration Services has also issued a memo to its staff (link) that offers a favourable interpretation of a typical Indian IT project arrangement. Simply put, it states that as long as the Indian IT company specifies the right to control and also exercises control, it is perceived to be the employer even if the employee is working at the client’s location. It also includes an illustrative example (page 5 – "long-term placement at a third-party work site").

Finally, Indian IT companies can also hire locals at salaries lower than the above mentioned levels and not have to comply with these requirements. This might require a slight increase in wages, lower utilisation, etc. but the margin impact would not be as severe as expected by consensus (e.g. 500bps for TCS).

It is a misconception that non-exempt H-1B visa-holders cannot be outplaced.

Indian IT companies can also hire locals at lower salaries.

Technology

February 15, 2017 Ambit Capital Pvt. Ltd. Page 9

Only half of the margin drop will be recovered; not before 3-5 years Over time, the cost of locals will reduce as supply increases in response to the higher wages and then wages will automatically cool. This will take over 5 years! By then, Indian IT companies will boost local proportion of US-based workforce to the levels of US companies, making further protectionist action redundant. Margin recovery will happen as they (1) extract more flexibility and better prices from their US customers and (2) adjust processes to optimise utilisation despite high proportion of local talent, spend lower on travel and increase proportion of revenue delivered offshore. Only half the margin drop will be recovered because of inherent stickiness of wages and structurally lower onsite utilisation.

We have sanity-checked these ideas with employees of leading Indian IT services companies, industry analysts and clients.

Eventually Indian IT will staff locally The recent as well as earlier draft protectionist legislations target H-1B dependent employers, which are defined in US law as companies in which more than 15% of the employee-base consists of H-1B visa-holders. Hence, Indian IT companies will strive to reduce their dependence on such temporary work visas to below 15% to escape future legislation.

One way to do this quickly is by applying for green cards for some of the H-1B employees. As per our US immigration expert, "The Trump administration is only against people on non-immigrant work visas. The employees on immigrant visas will be treated on par with US citizens." This is subject to a per-country quota, but in earlier draft legislations, even employees who had only applied for the green card were exempt from protectionist measures.

Acquiring companies with large US citizens or green-card holders on their payrolls is another option. However, this cannot be the only reason for acquisition.

Indian IT companies will likely invest in building a large supply of local talent in the US, just as they have in India. A few of them such as TCS and Infosys have already built a large pool of digital learning assets that could be accessed from anywhere on any device. In India, these companies also collaborate with universities to ensure that their education is suited for their requirements, and offer low-paid internships. See our note dated 11th November 2016 for more details. Some of these initiatives could also work in the US. Interestingly, Carrier which recently announced plans to lay off a number of manufacturing employees in the US, promised to provide up to four years of tuition towards a degree in any field including academic fees and books (link). So clearly, there is a push towards re-skilling workers even from outside the IT industry. The increased supply will gradually bring down costs of US-based onsite workers.

Indian vendors would need to temper expectations of their India-based employees with respect to opportunities to work in the US. Because in India there is a lot more supply for Indian IT than demand, wage pressures due to this change can be contained.

Indian IT companies could apply for green cards, and make acquisitions to reduce proportion of H-1B visas to less than 15% of the total US workforce

Indian IT companies will likely invest in building a large supply of local talent.

Technology

February 15, 2017 Ambit Capital Pvt. Ltd. Page 10

Vendors will extract some pricing hikes and flexibility from clients over time Because the increase in cost of visa-holders is likely to be steep and because the top-tier Indian IT vendors have a deep relationship with their customers, it is likely that they will be able to persuade their clients to be more flexible as they adapt to the new regulations. For instance, some clients will likely give the additional attestations for non-exempt H-1B visa-holders if the alternative is to spend an extra US$70,000 p.a. per such person.

Further, as discussed above, clients will be forced to give significant wage hikes to their tech employees and will therefore be understanding to give at least some pricing hikes to their vendors over a sufficient period of time.

We note that Cognizant, which is the second-largest Indian IT services company with ~20% share in its focus segments of BFSI and Healthcare, recently changed its strategy to prioritise profitability over growth. This should help the entire Indian IT industry pass on pricing hikes to customers. See our note dated 10th February 2017 for more details.

Vendors will tweak processes to work with a largely local workforce One of the advantages of using H-1B visa-holders over US locals has been that this improves onsite utilisation and keeps the average employee costs low. Over time, Indian companies will learn to optimise their operating parameters when working with a high proportion of locals.

Why have Indian vendors continued to prefer H-1B visa-holders so far?

First, Indian vendors maintain their bench in India instead of in the US. All IT services vendors need to maintain a bench because there are often time-gaps between projects. An H-1B visa-holder can be sent back to India when there is no requirement of her skill-set in the US, but not a US local.

Second, H-1B visa-holders are likely to be more amenable to move wherever they are required in the US. On the other hand, a US local would be reluctant to work on a project that is far from her home city.

Third, top-tier companies typically churn H-1B visa-holders every 2-3 years, before they leverage their US onsite experience and acquired skills into significantly higher wages. Also, this ensures that more of its employees get a chance to work in the US. This is a powerful motivation factor for Indian employees who are therefore willing to work in India for relatively low wages.

How will they change processes to assuage the negatives?

First, Indian vendors would ensure that they hired just-in-time for requirements. This should be possible by investing in a strong local hiring engine. Their planning processes should already be robust as they anyway apply for H-1B visas months before the actual requirements. For instance, currently Indian IT companies have to apply for visas on 1st April to get them in the year starting 1st October.

Second, using US locals over H-1B visa-holders will result in lower travel costs including cost of visas, airline tickets and hotel stays.

Third, the companies will also strive to increase the proportion of revenue delivered from near-shore (e.g. in Mexico or Canada) or offshore delivery centres. Digital collaborative technologies like video conferencing could also be leveraged to do this.

Clients will likely give the additional attestations for non-exempt H-1B visa-holders.

And some pricing hikes.

Using H-1B visa-holders results in better onsite utilisation and keeps the average employee costs low.

Currently, Indian vendors to maintain their employee bench in India. H-1B visa-holders are more mobile and can be churned to keep employee costs low.

Indian IT will hire just-in-time, spend lower on travel and reduce proportion of revenue delivered in the US.

Technology

February 15, 2017 Ambit Capital Pvt. Ltd. Page 11

TCS fares the best, Cognizant the worst Early investments in non-US markets, stronger processes for more offshore delivery and a place higher up the value chain (already high wages) will lead to more robust margins. Cognizant fares the worst (730bps hit) as we estimate that 21% of its employees are based in the US, of which 91% earn less than US$100K. We estimate only 350bps hit to TCS' margins because it likely has only 11% of its employees in the US, of which 83% earn less than US$100K.

Our framework for margin hit Vendors with early investments in non-US markets, stronger processes for more offshore delivery and higher up the value chain (already high wages) will see a lower hit to margins. We estimate highest margin drop for Cognizant (730bps) due to protectionism and the lowest margin drop for TCS (350bps).

Early investments in non-US markets (Proxy: Proportion of revenues from outside the US)

Vendors that were early to invest in markets outside the US are relatively insulated from protectionist action in the US. TCS is the best placed on this metric and Cognizant is the worst.

Processes that facilitate greater offshore delivery (Proxy: Proportion of revenue delivered offshore)

Vendors that have invested in processes to improve offshore delivery have a low proportion of employees in the US. Again, TCS fares the best and TechM fares the worst.

Higher up the value chain (Proxy: Proportion of US-based employees on a high salary)

If most of its onsite employees are already earning high wages, the vendor will see a lower impact from rising floor of wages. TCS is the best placed on this metric and TechM is the worst.

Exhibit 2: On our framework, Cognizant fares the worst but TCS fares the best

Source: Ambit Capital research, company; Note: Size of bubble is proportional to the EBIT margin drop over FY18-20E.

80%

82%

84%

86%

88%

90%

92%

94%

96%

98%

100%

10% 12% 14% 16% 18% 20% 22%

%a

ge if

em

no

lyees

ea

rniu

ng

less

th

an

U

S$1

00

K

%age of employee base in US

We estimate highest margin drop for Cognizant (730bps) due to protectionism and the lowest margin drop for TCS (350bps).

CTSH

INFO

TCS

HCLT

WPRO

TechM

Technology

February 15, 2017 Ambit Capital Pvt. Ltd. Page 12

Stick to quality. TCS is our top pick, downgrade HCLT to SELL. Our revised pecking order is TCS (top BUY) > TechM, Infosys (BUYs) > HCLT (now SELL) > Wipro (SELL) > Cognizant (top SELL). TCS has the best track record with respect to managing margin shocks (EBIT margin has fluctuated within a 200bps band for 6 out of past 7 years) whereas HCLT/TechM have fluctuated as much as 8-10ppt over this time. TechM's low exposure to the US and scope to improve margins protect it somewhat. Infosys will be hurt due to its high exposure to the US, but at current valuations, it is a steal. HCLT is ill-prepared to deal with looming structural challenges as it suffers from non-quantifiable risks from sudden spree of acquisitions, organisation structure and frequent CEO changes; we turn SELLers. We retain our SELL stance on Wipro and Cognizant as they too struggle with internal transformations.

Our framework for margin recovery Vendors with greater scope to improve profitability from current levels and better adaptability are better equipped to manage the hit from protectionism.

Greater scope to improve profitability (our assessment)

Among the top-6 Indian IT companies, only Cognizant and TechM have significant scope to improve profitability. Please see details in the company-specific sections below.

Better adaptability (Proxy: margin stability)

In tough times, higher quality companies typically do better. So vendors that are closer to their customers will be better able to extract better pricing and more flexibility from them. These also tend to be more agile and will be faster to reduce the number of temporary visa-holders in the US and optimise their metrics for the new operating model. The past track record in terms of margin management is a good proxy for these qualities. On this metric, TCS, Cognizant and Infosys fare better than Wipro, HCLT and TechM.

Changes to estimates and target price Incorporating a 350-730bps hit to margins over FY18-20E, as explained in the previous section, leads to FY19 EPS cut by 6-19% across the top-6 Indian IT companies. However, we take other factors into consideration to arrive at our target price. Please see the company-specific sections for more details.

Exhibit 3: Impact of our base case scenario on EPS estimates and target price

Company TCS CTSH Infosys Wipro HCLT TechM

US revenue as % of overall revenue 53% 79% 63% 53% 60% 48%

Percentage of employees based in US 11% 21% 16% 14% 18% 11%

FY18-20 margin drop (bps) because of protectionism 350 730 530 390 375 440

FY18 EBIT margin 26% 17% 24% 17% 20% 15%

Impact on FY19 EPS because of protectionism -6% -24% -10% -10% -10% -14%

Spread of EBIT margin over FY07-16 (max-min) 5.9% 1.7%* 6.1% 3.5%* 10.0% 13.0%

Years taken for recovery of 50% margin drop 3 3 3 5 5 5

Percentage change in target price -8% -12% -13% -10% -21% -7%

New target price 2670 40 1050 430 750 560

Implied FY19 P/E 17 14 16 12 12 14

Upside 22% -28% 11% -8% -9% 15%

Rating BUY SELL BUY SELL SELL BUY

Source: Company data, Ambit Capital research. *Note: Wipro and Cognizant's spread is under-stated because their margin includes gains/losses from forex hedges. FY18 for Indian companies correspond to CY17 for Cognizant and vice-versa.

Vendors with greater scope to improve profitability from current levels and better adaptability are better equipped to manage the hit from protectionism.

Technology

February 15, 2017 Ambit Capital Pvt. Ltd. Page 13

TCS – the unshakeable Despite its industry leading margins, TCS is likely to see the least margin pressure (in bps) compared to peers due to its relatively low exposure to the US and relatively low proportion of revenues delivered onsite. It also appears to be the first to have anticipated protectionist headwinds and taken corrective actions. For instance, in FY17, it applied for one-third the number of visas it had applied in FY16. We have trimmed FY19 EPS estimates by 6% and reduced target price to Rs2670 (earlier: Rs2900). This implies 17x FY19E EPS. Maintain BUY.

TCS remains well-positioned to gain market share (currently under 3%) in global IT services driven by low cost structure (ingrained in culture, best-in-class), conservative investments in new growth areas (e.g. Japan, automation) and track record of high quality delivery (has best customer references in almost every segment). Its processes and culture are hard to replicate, which ensures high RoE (FY16A: 37%). The business is also highly cash-generative (FY16 pre-tax CFO/EBITDA: 93%, FY16 FCF/Net income: 78%) which management is willing to share with investors (FY16 dividend payout: 57%). In this context, current valuations are attractive at 16x one-year-forward P/E vs 19x which it averaged over the previous 10 years.

The recent CEO change is a negative, but our concerns are assuaged because: (a) the new CEO is a knowledgeable insider, (b) there will be no change in strategy and (c) the old CEO will be available to TCS for critical help in his new role as new group chairman. Senior employee attrition, which could hurt both sales and delivery, remains the biggest risk for TCS.

Exhibit 4: TCS is the least impacted among the Top-6 because of its pyramid structure and lower onsite presence

New Estimates Old Estimates Change

FY17E FY18E FY19E FY17E FY18E FY19E FY17E FY18E FY19E

Revenue (US$ mn) 17,597 19,301 21,511 17,589 19,283 21,490 0% 0% 0%

YoY Growth 6.4% 9.7% 11.4% 6.3% 9.6% 11.4% 10bps 10bps 00bps

EBIT (Rs bn) 308 346 361 307 339 385 1% 2% -6%

EBIT margin 26.0% 26.4% 24.6% 26.0% 26.2% 26.4% 00bps 20bps -170bps

PBT 348 376 394 341 368 418 2% 2% -6%

PAT 265 286 300 259 281 319 2% 2% -6%

EPS 134 145 152 132 143 162 2% 2% -6%

Source: Ambit Capital research, company

Cognizant – most vulnerable to protectionist measures Cognizant has the highest exposure to the US (79% of revenues) compared to peers and is therefore the most vulnerable to protectionist measures. Based on our model, ceteris paribus, increase in minimum cost per onsite worker should hurt its margin by 730bps over CY17-19E.

However, it has recently changed its strategy to prioritise profitability over growth. It also has higher headroom to cut costs, especially SG&A, as compared to peers. So we build CY17-19E margin dip of only 630bps. Because of its low margin base, the CY19 EPS estimate is cut by 34%.

Cognizant has demonstrated a strong track record of maintaining margins in the past despite the volatile currency and business environment. So, we expect a relatively fast recovery in margins (half over 3 years). As a result, our target price cut is less harsh at 18% to US$38 (earlier: US$45). This implies 12x CY18 EPS.

Cognizant leads in its focus verticals (BFSI and Healthcare account for 70% of revenues), delivers industry-leading growth, and is a top-5 global vendor in digital capability. However, low-cost peers (TCS/Infosys) are fast catching up in terms of capabilities and its pricing premium is vulnerable to cuts. Growth differential over peers has fallen to 4ppt in CY14-16E from 16ppt in CY04-06

Technology

February 15, 2017 Ambit Capital Pvt. Ltd. Page 14

even as its margins remain 10-12ppt lower. It has, therefore, rightly decided to change its strategy to focus on profitability over revenue growth. However, this will likely compromise client satisfaction in the medium term, leading to poor revenue growth. In this context, current valuation of 16x one-year-forward P/E is unreasonable though it is at an 11% discount to the past 10-year-average.

A sudden uptick in its revenues driven by rising rate environment (boosts profits for BFSI, which is its largest customer segment) as well as M&A activity at its healthcare clients (leads to integration spend) are the key risks to our SELL stance.

Exhibit 5: Cognizant will be the most impacted because of its higher exposure to the US

New estimates Old estimates % Change

CY17 CY18 CY19 CY17 CY18 CY19 CY17 CY18 CY19

Revenue (US$ mn) 14,105 15,023 16,274 14,105 15,023 16,274 0% 0% 0%

YoY Growth 4% 7% 8% 4% 7% 8% 00bps 00bps 00bps

EBIT (US$ mn) 2,440 2,238 2,034 2,512 2,749 3,057 -3% -19% -33%

EBIT margin 17.3% 14.9% 12.5% 17.8% 18.3% 18.8% -50bps -340bps -630bps

PBT 2,507 2,317 2,136 2,591 2,874 3,227 -3% -19% -34%

PAT 1,855 1,714 1,580 1,918 2,127 2,388 -3% -19% -34%

EPS (US$) 3.0 2.8 2.6 3.2 3.5 3.9 -3% -19% -34%

Source: Ambit Capital research, company

Infosys – Good franchise at compelling valuations Infosys had already burnt its fingers with respect to its visa processes in 2013 (link) when it was forced to pay US$34mn to end a US investigation related to alleged fraud over visas. This is likely why it is more prepared for protectionist headwinds today. As per our US immigration expert, "Infosys now complies with a higher standard with respect to complying with relevant visa-related regulations."

Based on our discussion with a former senior HR manager at Infosys, we understand that it has invested aggressively in a local hiring programme and also pays slightly higher than market salaries to its H-1B staff. Recently, in a media interview, former executive chairman, NRN shared that he had started a programme to reduce the proportion of onsite work to 10% from 30% and to replace all H-1B personnel with local talent.

CEO Vishal Sikka is himself based in Silicon Valley and has a very good reputation in the US technology space. For instance, Glassdoor rated him best CEO. However, its relatively high US exposure (63% of revenue, second only to Cognizant) could hurt it. We build a FY19E EBIT margin hit of 265bps, which results in FY19E EPS cut of 9%. Our target price reduces to Rs1050 (earlier: Rs1200). This implies 16x FY19E EPS.

Infosys’s portfolio has higher exposure to discretionary spending of clients (source: channel checks) and so it could be a beneficiary of a cyclical uptick in the demand environment. Further, it is well-placed to benefit from Digital because of its focus on strategy and design-oriented consulting. Vishal Sikka’s super sales ability is also likely to maintain the momentum of new deal wins as well as revenues from top-10 clients. Total contract value of deals won over CY16 is 54% higher than that in CY13. Revenue from top-10 clients is up 11% over CY13-16. As per channel checks, the management’s initiatives to improve innovation, automation and efficiency also appear to be progressing well.

Title-holder attrition is the key risk to our BUY stance.

Technology

February 15, 2017 Ambit Capital Pvt. Ltd. Page 15

Exhibit 6: Infosys's high exposure to the US (63% of revenue, second only to Cognizant) could hurt

Key Assumptions and Estimates New estimates Old estimates Change

FY17E FY18E FY19E FY17E FY18E FY19E FY17 FY18E FY19E

Revenue (US$ mn) 10,202 10,922 12,071 10,244 11,227 12,393 0% -3% -3%

YoY Growth 7.4% 7.1% 10.5% 7.8% 9.6% 10.4% -40 bps -250 bps 10 bps

EBIT (Rs bn) 169.6 182.0 179.8 169.0 183.0 201.0 0% -1% -11%

EBIT margin 24.7% 24.5% 21.9% 24.6% 24.3% 24.5% 10 bps 20 bps -260 bps

PBT 199.6 211.7 212.6 198.0 211.0 234.0 1% 0% -9%

PAT 142.3 149.3 149.9 140.0 149.0 164.9 2% 0% -9%

EPS (Rs) 62.3 65.3 65.6 61.0 65.3 72.1 2% 0% -9%

Source: Ambit Capital research, company

Wipro – low exposure to the US helps Wipro has also been hiring from US campuses since at least the past 8 years. In a 2009 interview to Rediff, Wipro chairman and largest shareholder, Mr. Premji said that it was hiring from US campuses for its US-based delivery centres. It also benefits because it has a relatively low exposure to the US (53% of revenue). We cut our FY19E EBIT margin estimate by 190bps which leads to FY19E EPS cut of 9%. This pushes down target price to Rs430 (earlier: Rs450). This implies 12x FY19E EPS.

Like Infosys, Wipro’s portfolio is also skewed towards discretionary work but it has relatively low exposure to the US BFSI segment (we estimate ~15%) and is therefore not as leveraged to a cyclical uptick in this segment. Further, its customer-connect remains weak as until recently its relationship managers were rotated every 18 months. To add to its woes, the CEO is also relatively new. Whilst the company is taking the right steps in correcting the organisational structure and focusing on building annuity-like revenues, the problems of portfolio mix and culture (highly silo-ed, does not have the DNA of vertical domain expertise which is crucial today) are hard to change overnight.

A sudden uptick in revenues from the energy and healthcare segments (it has higher exposure compared to peers) is the key risk to our SELL stance.

Exhibit 7: Wipro's low exposure to the US limits the margin hit

Key Assumptions and Estimates New estimates Old estimates Change

FY17E FY18E FY19E FY17E FY18E FY19E FY17E FY18E FY19E

Revenue (IT services) (US$ mn) 7,691 8,058 8,747 7,734 8,148 8,844 -1% -1% -1%

Revenue (Rs bn) 553.1 574.0 620.8 549.0 571.0 618.0 1% 1% 0%

EBIT (Rs bn) 93.7 94.6 94.0 93.0 94.0 105.9 1% 1% -11%

EBIT margin 16.9% 16.5% 15.1% 16.9% 16.5% 17.1% 00bps 00bps -190bps

PBT 110 112 113 109 111 124 1% 1% -9%

PAT 84 86 87 84 85 95 0% 1% -9%

EPS 34.6 35.4 35.8 34.3 35.1 39.6 1% 1% -9%

Source: Ambit Capital research, company

HCLT – low proportion of H-1Bs does not mean it is insulated from protectionism As per HCLT management, only 35% of US-based employees are on temporary visas vs 50%+ for peers. This is likely due to its greater propensity to re-badge employees of clients (more common in infrastructure management services deals and total outsourcing deals). Consensus assumes that it would be least impacted by any adverse protectionist action on H-1B visas. However, as discussed above, the wages of all onsite workers, including locals, would rise if the cost of H-1B visa holders is artificially inflated. HCLT derives 60% of revenue from the US. So, we have reduced our FY19E EBIT margin by 190bps and FY19E EPS by 9%.

Technology

February 15, 2017 Ambit Capital Pvt. Ltd. Page 16

HCLT is ill-prepared to handle this structural challenge as we see rising risks from internal issues: (i) service-line-centric organisation structure which makes it vulnerable in the digital era; (ii) likely another round of senior management attrition and (iii) sudden spree of acquisitions. We have cut our target price to Rs750 (earlier: Rs950), implies 12x FY19E EPS, and downgraded our stance to SELL. We are publishing a detailed report explaining this along with this note.

Exhibit 8: HCLT's low proportion of H-1B staff does not mean it is insulated from protectionism

New Old Change

FY17E FY18E FY19E FY17E FY18E FY19E FY17E FY18E FY18E

Revenue (US$ mn) 6,927 7,640 8,664 6,957 7,711 8,746 0% -1% -1%

Revenue growth (YoY) 11.1% 10.3% 13.4% 11.6% 10.8% 13.4% -50bps -50bps 00bps

EBIT (Rs bn) 94.4 103.5 106.1 93.0 103.5 117.1 1% 0% -9%

EBIT margin 20.2% 19.9% 18.0% 20.2% 19.9% 19.9% 00bps 00bps -190bps

PBT 104 113 116 103 113 128 0% 0% -9%

PAT 82 89 91 81 89 100 0% 0% -9%

Dil Adj EPS 57.8 62.7 64.8 57.6 62.7 70.9 0% 0% -9%

Source: Ambit Capital research, company

TechM – poor capability of handling margin shocks is priced in TechM has relatively low exposure to the US (48% of revenue), but has a high proportion of revenue delivered onsite due to its acquisitive strategy and greater proportion of transformational projects. So, protectionism will likely hit its margins by 440bps over FY18-20E and half of this would be recovered by FY25E.

However, as it has significant scope to improve margins from current levels and is already taking steps to boost the employee pyramid, onsite-offshore ratio etc., we had built a 400bps improvement in margins over FY17-21E and a slight decline thereafter. Please see our note dated 17 Jan 2017 for details.

Combining the impact of the above two drivers on margins, we build a margin drop of only 240bps over FY18-20E to 11.1% and recovery of 170bps by FY23E, post which margins will remain stable. We cut our target price by 7% to Rs560 (earlier: 600). This implies 15x FY19E EPS. We retain our BUY stance.

TechM has strong competitive advantages (global top-3) in the telecom segment, which contributes roughly half of its revenue. It also has the highest scope to improve margins (~400bps from current level) as it corrects inefficiencies that have crept up over time (pyramid, onsite-offshore ratio, loss-making subsidiaries).

TechM has high customer concentration (Top-10 customers contribute ~38% of revenues). Slowdown in spend due to customer-specific issues is a key risk to our BUY stance.

Exhibit 9: We expect a 220bps hit to FY19 margins due to protectionism

New Old Change

FY17E FY18E FY19E FY17E FY18E FY19E FY17E FY18E FY19E

Revenues (US$ mn) 4,361 4,863 5,348 4,361 4,863 5,348 0% 0% 0%

YoY growth 8% 12% 10% 8% 12% 0.1 00bps 00bps 00bps

EBIT (Rs bn) 35.7 44.8 44.8 35.7 44.8 52.9 0% 0% -15%

EBIT margin 12.1% 13.5% 12.3% 12.1% 13.5% 14.5% 00bps 00bps -220bps

PBT 40.2 47.1 47.5 40.2 47.1 55.5 0% 0% -14%

PAT 29.7 35.6 35.9 29.7 35.6 42.0 0% 0% -15%

EPS 34.3 40.1 40.4 34.3 40.1 47.3 0% 0% -15%

Source: Ambit Capital research, company

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision.

Not prepared for the fightWe cede our conviction and turn SELLers given rising risks: (i) service-line-centric structure makes HCLT vulnerable in the digital era; (ii) likely another round of senior management exits; (iii) sudden spree of acquisitions. Unlike Axon which brought in CXO connects, these acquisitions were either unrequired or brought in end-of-life products or easy-to-build capabilities. With added risk of protectionism looming, we do not envy the new CEO’s job. Having fewer H-1B employees will not insulate it from wage inflation pressure, which will act across the US-based workforce. We cut our FY19 EPS by 9% to Rs65 (7% lower than consensus). We cut our TP to Rs750 (Rs930 earlier), implying 12x FY19E EPS (14x earlier), in line with Wipro. Incipient signs of re-organisation and more enticing valuations could make us reconsider our stance.

Competitive position: STRONG Changes to this position: WEAKENING

Unrequired acquisitions can add unknown risks

Of the recent 11 acquisitions, Volvo’s IT captive is synergistic (adds client/regional reach); IBM IP partnerships could have been avoided; Geometric, Butler and Power Objects could have been built organically; for others why not partnerships? Cultural clashes and wasted management bandwidth from acquisitions are plenty (TechM, MTCL, Infosys). Axon was an exception, bringing critical capabilities/relationships and not part of a series.

Organisation structure – HCLT’s Achilles heel

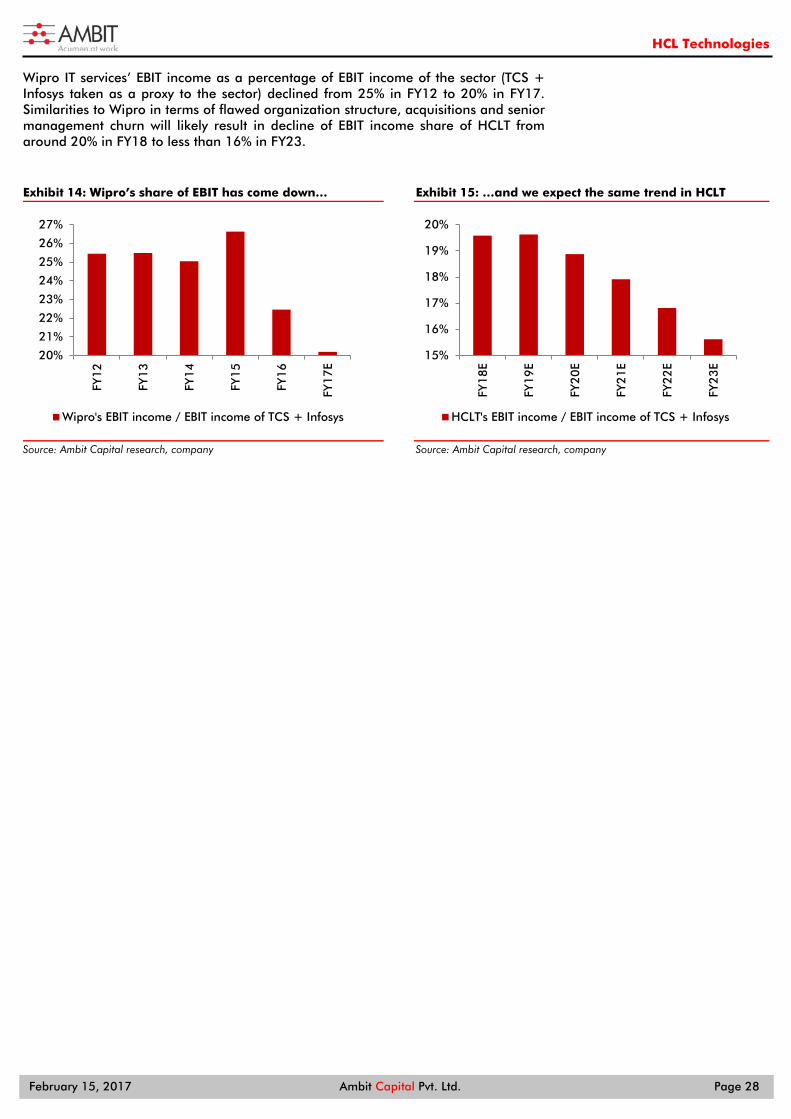

A service-line-led sales force is prone to disruption by changing technology, especially as customers increasingly prefer vendors who can talk the language of their business. Parallel chains of command for sales and delivery make it less able to pull off digital projects that require stitching together multiple service-lines into a holistic solution; Wipro is an example. Also, HCLT has had 3 CEOs in the last 4 years not for business but for ‘fit-with-the-promoter’ reasons.

Not just H-1B, the entire US employee base would re-price

IT talent shortage in the US will raise cost of all substitutes (incl. locals) if H-1B visa gets pricier. Less mature processes (fallout of organisation structure?) have caused poor track record of managing margin shocks (swung 10% in FY06-16 vs 6% for TCS/Infosys). Margins could decline to 16% (drop lower than industry) but we expect only half the loss to be recovered by FY25.

Tailwinds short-lived, similarities to Wipro worrisome

Benefits of better mix (~60% of revenue from IMS/ES) could taper post FY19 and fallout of the above risks (unless addressed) will be visible by then. At a time when investors are worried of first-time structural non-quantifiable risks, we advise staying away from companies with internal issues (Wipro and now HCLT). Risks: positive surprise from large deal wins.

CHANGE IN STANCE HCLT IN EQUITY February 15, 2017

HCL TechnologiesSELL

Technology

Recommendation Mcap (bn): `1,151/US$17 3M ADV (mn): `1,393/US$21 CMP: `832 TP (12 mths): `750 Downside (%): 10%

Flags Accounting: GREEN Predictability: GREEN Earnings Momentum: GREEN

Catalyst

Disappointment in revenue growthor margin in FY18 due to the recentacquisitions.

Performance (%)

Source: Bloomberg, Ambit Capital Research

80

90

100

110

120

Feb-

16

Mar

-16

May

-16

Jun-

16

Aug

-16

Sep-

16

Nov

-16

Dec

-16

Jan-

17

SENSEX HCLT

Research Analysts

Sagar Rastogi

+91 22 3043 3291

Sudheer Guntupalli

+91 22 3043 3203

Key financials

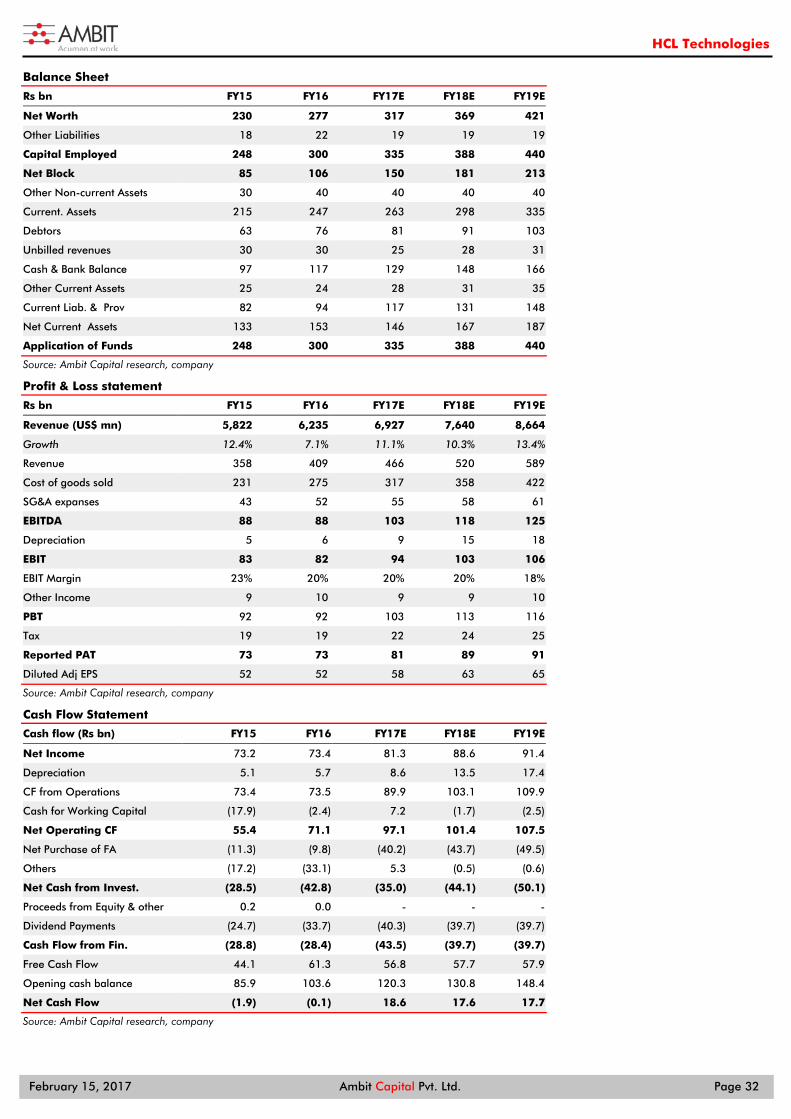

Year to March FY15 FY16 FY17E FY18E FY19E Net Revenues (` bn) 358 409 466 520 589

Operating Profits (` bn) 83 82 94 103 106

Net Profits (` bn) 73 73 81 89 91

RoE (%) 35 29 27 26 23

P/E (x) 16 16 14 13 13

Source: Company, Ambit Capital research

HCL Technologies

February 15, 2017 Ambit Capital Pvt. Ltd. Page 18

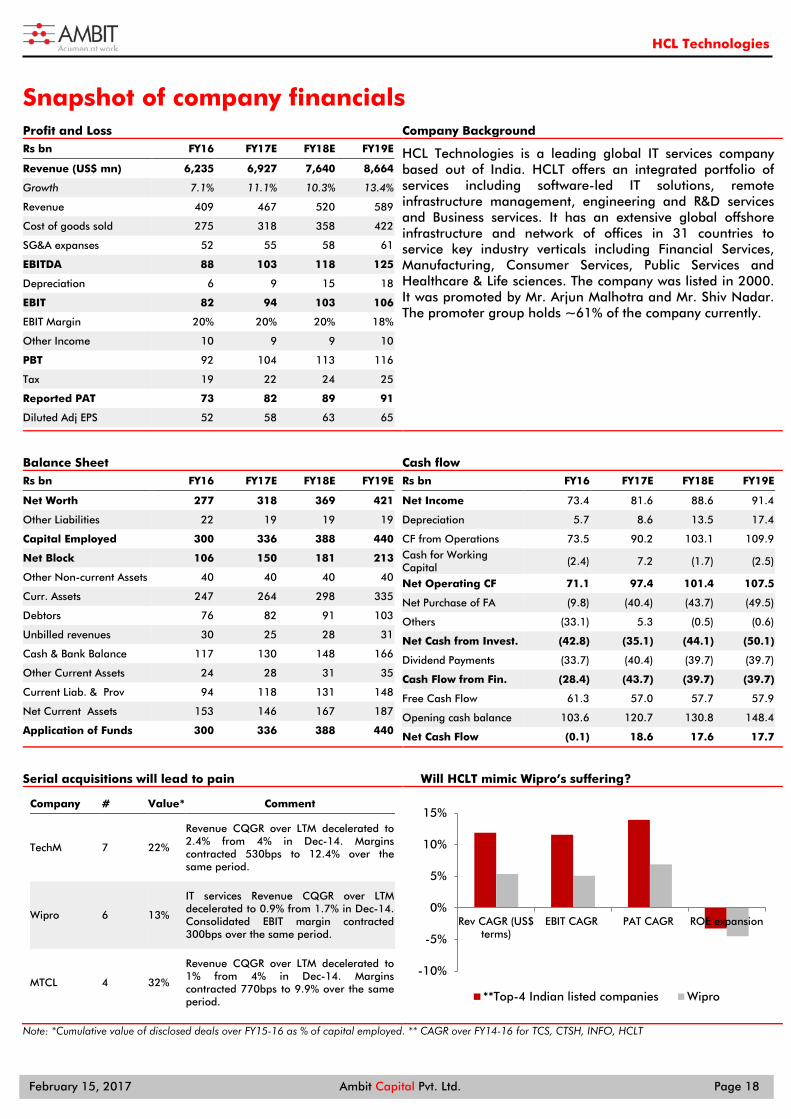

Snapshot of company financials Profit and Loss Company Background Rs bn FY16 FY17E FY18E FY19E

Revenue (US$ mn) 6,235 6,927 7,640 8,664

Growth 7.1% 11.1% 10.3% 13.4%

Revenue 409 467 520 589

Cost of goods sold 275 318 358 422

SG&A expanses 52 55 58 61

EBITDA 88 103 118 125

Depreciation 6 9 15 18

EBIT 82 94 103 106

EBIT Margin 20% 20% 20% 18%

Other Income 10 9 9 10

PBT 92 104 113 116

Tax 19 22 24 25

Reported PAT 73 82 89 91

Diluted Adj EPS 52 58 63 65

HCL Technologies is a leading global IT services company based out of India. HCLT offers an integrated portfolio of services including software-led IT solutions, remote infrastructure management, engineering and R&D services and Business services. It has an extensive global offshore infrastructure and network of offices in 31 countries to service key industry verticals including Financial Services, Manufacturing, Consumer Services, Public Services and Healthcare & Life sciences. The company was listed in 2000. It was promoted by Mr. Arjun Malhotra and Mr. Shiv Nadar. The promoter group holds ~61% of the company currently.

Balance Sheet Cash flow Rs bn FY16 FY17E FY18E FY19E

Net Worth 277 318 369 421

Other Liabilities 22 19 19 19

Capital Employed 300 336 388 440

Net Block 106 150 181 213

Other Non-current Assets 40 40 40 40

Curr. Assets 247 264 298 335

Debtors 76 82 91 103

Unbilled revenues 30 25 28 31

Cash & Bank Balance 117 130 148 166

Other Current Assets 24 28 31 35

Current Liab. & Prov 94 118 131 148

Net Current Assets 153 146 167 187

Application of Funds 300 336 388 440

Rs bn FY16 FY17E FY18E FY19E

Net Income 73.4 81.6 88.6 91.4

Depreciation 5.7 8.6 13.5 17.4

CF from Operations 73.5 90.2 103.1 109.9 Cash for Working Capital (2.4) 7.2 (1.7) (2.5)

Net Operating CF 71.1 97.4 101.4 107.5

Net Purchase of FA (9.8) (40.4) (43.7) (49.5)

Others (33.1) 5.3 (0.5) (0.6)

Net Cash from Invest. (42.8) (35.1) (44.1) (50.1)

Dividend Payments (33.7) (40.4) (39.7) (39.7)

Cash Flow from Fin. (28.4) (43.7) (39.7) (39.7)

Free Cash Flow 61.3 57.0 57.7 57.9

Opening cash balance 103.6 120.7 130.8 148.4

Net Cash Flow (0.1) 18.6 17.6 17.7

Serial acquisitions will lead to pain Will HCLT mimic Wipro’s suffering?

Company # Value* Comment

TechM 7 22%

Revenue CQGR over LTM decelerated to 2.4% from 4% in Dec-14. Margins contracted 530bps to 12.4% over the same period.

Wipro 6 13%

IT services Revenue CQGR over LTM decelerated to 0.9% from 1.7% in Dec-14. Consolidated EBIT margin contracted 300bps over the same period.

MTCL 4 32%

Revenue CQGR over LTM decelerated to 1% from 4% in Dec-14. Margins contracted 770bps to 9.9% over the same period.

Note: *Cumulative value of disclosed deals over FY15-16 as % of capital employed. ** CAGR over FY14-16 for TCS, CTSH, INFO, HCLT

-10%

-5%

0%

5%

10%

15%

Rev CAGR (US$terms)

EBIT CAGR PAT CAGR ROE expansion

**Top-4 Indian listed companies Wipro

HCL Technologies

February 15, 2017 Ambit Capital Pvt. Ltd. Page 19

Unrequired acquisitions could pose unknown risks HCLT acquired Axon in 2009, which gave it critical capabilities in SAP and relationships with CXOs in large organisations. It did not make any acquisition between August 2009 and July 2015. However, it has deployed almost 21% of its total capital on 11 acquisitions (including three IP partnerships) post July 2015. Of these, we find only Volvo’s IT captive synergistic (adds to client/regional reach). The IBM IP partnerships should have been passed. Geometric, Butler and Power Objects added capabilities that could have been built organically; and partnerships would have served well for the others. We have seen a number of IT services companies disappoint massively because they underestimated challenges with respect to integration and overestimated business prospects of the target; TechM, Mindtree and Wipro are examples. Axon was an exception.

HCLT did not make any acquisition between August 2009 and July 2015. Since then, it has made eight acquisitions by investing over $500mn (10% of capital employed, FY17E) and three IP-partnerships with IBM for end-of-life software that require investments of $560mn (11% of capital employed, FY17E). Worryingly, it has indicated that it would make more investments in end-of-life software.

We have seen a number of IT services companies disappoint massively because they underestimated challenges with respect to integration and overestimated business prospects of the target. For instance, TechM acquired Lightbridge Communications in November 2014, paying what appeared to be reasonable valuations of ~13x P/E. Since then, the annual revenue run-rate has dropped from US$430mn to US$280mn (our estimate), profits have swung into losses, and there is still no visibility when it will get back to profitability. TechM's management credibility has taken a permanent beating due to this deal.

Mindtree acquired Bluefin, a provider of SAP implementation services, in June 2015. It was hit by uncertainty around Brexit and sharp depreciation in the GBP against the USD. It consistently underperformed management expectations since then and continues to make losses.

Exhibit 1: Acquisitions made by HCLT in the past 18 months

End-of-life software Capabilities that could have been built in-house

Niche technology where a partnership could have worked Customer captive

App security, data transformation, testing automation, mainframe management tools (US$155mn)

Butler America Aerospace LLC (Defence Engineering services, US$85mn)

Moogsoft (real time analytics, US$30mn*) Volvo AB (US$138mn)

API/web service enablement for mainframes (US$55mn) Geometric (Engineering, US$188mn) Point to Point (Cloud engineer,

US$11mn) Workload automation, DevOps (US$350mn)

PowerObjects (Cloud CRM, US$46mn)

Trygstad Technical services (IoT, M2M)

Concept to Silicon (Engineering services)

Source: Ambit Capital research, Bloomberg; *Note: HCLT and a number of other investors have invested a total of US$30mn in Moogsoft Inc.

End-of-life software: Management aspires to build a product revenue stream…

The management likely expects product revenue stream to be stickier and less prone to the steady pricing pressure like in IT services. It already has strong product engineering capabilities having helped create some of the most successful software in the world. A partnership with IBM, one of the world's top software companies, with a revenue-share agreement helps it offset the handicap of not having expertise and experience of selling software. Further, HCLT could leverage some of this software in the delivery of managed services (60%+ of its FY17E revenues of US$7bn), thereby improving margins.

We have seen a number of IT services companies disappoint massively because they underestimated challenges with respect to integration, and overestimated business prospects of the target.

HCL Technologies

February 15, 2017 Ambit Capital Pvt. Ltd. Page 20

...but we worry about the risks

IBM's higher bargaining power, the 'auction' type process for winning this deal and the threat to HCLT's partnerships with other vendors make us worry.

IBM is 12x the size of HCLT in terms of revenues (FY17E) and understands the prospects of its software much better than HCLT ever could. We wonder why IBM would enter into a revenue-share agreement with its vendor instead of paying it a fee for product engineering services if the software truly had great potential.

Further, this 'sale' of IP has also been in the form of an auction, with multiple vendors evaluating the software and bidding for it. So, HCLT suffers from 'winner's curse'. In fact, a senior employee at one of HCLT's competitors who had also looked at this software told us that HCLT likely paid 2x fair value for this software.

Finally, HCLT's relationships with IBM's competitors like CA and BMC and also with its clients could suffer if it gives the impression that its choice of software for delivery of services is biased.

We had highlighted these risks in our note dated 24th January 2017.

HCLT has acquired companies for capabilities that could have been quickly acquired organically

We do not like such acquisitions because they pose the risk of cultures clashing and resulting in key people quitting. Further, expensive valuations almost always destroy shareholder value.

For instance, HCLT announced acquisition of Geometric at an EV/trailing sales = 1.4x to enhance PLM and manufacturing engineering capabilities (boosts engineering services revenue by 12%). Geometric's portfolio is weak with significant exposure to slow growing and low margin businesses like Product Lifecycle Management implementation, outsourced product development and mechanical engineering outsourcing services (together contribute 88% of revenues of Geometric). Acquiring a slow growth Indian legacy business rather than a next-gen business (like IoT or blockchain related) shows desperation for growth.

This acquisition will be margin dilutive (30bps EBIT margin contraction expected in FY18E) given that EBIT margin (adjusted for consultant fees) of Geometric is ~8% vs 20% EBIT margin for the company. NOPAT margin profile of Geometric is significantly weaker than that of HCLT (16% in FY16), resulting in ~60bps contraction in overall ROCE because of the deal.

HCLT likely already had relationships with ~60 of Geometric’s clients and could have acquired the talent pool (~2600 people) organically at a much lower cost in as little as six months.

We had discussed this in our note dated 4th April 2016.

We applaud interest in niche technologies, but highlight that a partnership would have been a better option than investment

HCLT can learn from start-ups and also embed their cutting edge technology into its offerings to make them more attractive to customers. However, these objectives can be achieved by partnerships without risking financial capital. Further, a growing technology company would want to partner with as many IT services companies as possible without granting exclusive partnership rights to its investor entity.

We had discussed this in our note dated 14th May 2015.

HCL Technologies

February 15, 2017 Ambit Capital Pvt. Ltd. Page 21

Organisation structure – Achilles’ heel HCLT has separate sales teams for large service lines, including Application Services, IMS, enterprise solutions and Engineering Services. The company has industry-specific sales teams as well, but our channel checks indicate that the service-line-specific sales teams are more dominant. Such a sales force is more vulnerable to disruption by changing technology, especially as customers increasingly prefer vendors who can talk their business language. Parallel chains of command for sales and delivery make it less able to pull off digital projects that require stitching together multiple service lines into a holistic solution. Adding to this, HCLT has two power centres which make senior management attrition more likely. It has had 3 CEOs in the last 4 years not for business issues but for ‘fit-with-the-promoter’. This is eerily similar to Wipro, which has had multiple centres of control and four CEOs in last 10 years.

Service-line-driven approach to sales… There are separate sales teams for large service-lines, including infrastructure management services, application development and maintenance, enterprise software implementation, engineering services and business process services. HCLT does have some industry-specific sales teams as well, but our channel checks indicate that the service-line-specific sales teams are more dominant.

This is flawed for three reasons: (1) customers increasingly prefer vendors that speak the business language, (2) HCLT is at risk of disruption from changes in technology, and (3) digital projects require vendors to deliver a holistic solution by stitching together multiple service-lines.

As technology gets more and more integrated into business, IT services spend is increasingly getting driven by outside the CIO's office, including the Chief Marketing Officer, Chief Financial Officer, Business heads and sometimes even the CEO. In this context, the pitch by a salesperson who specialises in an industry segment is likely to gain more traction than the pitch by a salesperson who specialises in technology. For instance, "We understand the recent FATCA regulation, and can build a solution for you to comply with it" is a better pitch to a bank than "We have 100 developers who are trained in Java and can build any IT solution for you."

With a technology-driven approach, the vendor risks getting tied to a specific technology. So, if the customer views HCLT as a SAP specialist and changes its ERP system from SAP to Oracle, HCLT is at risk of being booted out. On the other hand, a competitor which positions itself as a solution provider to manufacturing companies can better navigate such shifts. The pace of changes in technology has accelerated significantly.

Digital projects increasingly require integration of multiple technologies. If the vendor's organisation structure is not geared for different technology teams to work well together, it could hurt customer satisfaction. Further, an industry-segment-driven approach also makes it easier to cross-sell different service lines and thus mine the customer.

Parallel chains of command for sales and delivery… For the large service lines, the sales and delivery reporting lines connect only at the level of CEO.

Each of the 4 large service-lines (IMS, Applications, Engineering Services and BPO) has a head of sales and a head of delivery. The heads of sales report to the CEO. The heads of delivery report into Ajit Kumar, President – Systems Integration and Applications Service Delivery, who reports to the CEO.

This makes decision-making less agile. For instance, sales would like to push through changes in scope without increase in price to keep the customer happy, but delivery would push back to ensure that margin targets are met. Eventually, every such decision would have to pass through several layers of management to be passed.

…could handicap growth in the digital era.

…makes decision-making less agile.

HCL Technologies

February 15, 2017 Ambit Capital Pvt. Ltd. Page 22

Exhibit 2: HCLT' service-line-centric organisation structure

Source: Ambit Capital research, company; Note: Sales guys are primarily focused on revenues and delivery guys are primarily focused on profits.

Exhibit 3: TCS's customer-centric organisation structure

Source: Ambit Capital research, company; Note: Each A/c manager is responsible for both revenue and profits, and co-ordinates with each of the service-lines who play supporting roles.

Exhibit 4: Wipro too had flawed structure in the past

Source: Ambit Capital research, company

Exhibit 5: However, Wipro has changed it recently…

Source: Ambit Capital research, company

HCL Technologies

February 15, 2017 Ambit Capital Pvt. Ltd. Page 23

There are two centres of power in the organisation… Shiv Nadar, the founder who controls 60% of shareholding is the chairman and also the chief strategy officer of the company. He is well-respected not only in the HCL group but across the global IT services industry. For instance, some of his mentees occupy leadership positions across various Indian IT services companies including NIIT Technologies and Tech Mahindra. This creates an alternate power centre to the CEO.

…making senior management attrition likely The arrangement of a separate CEO and an executive chairman by itself is not a problem if the Chairman and CEO are on the same wavelength, believe in the same strategy, agree on the people and methods of execution and have clearly divided responsibilities. However, if one of these presumptions does not hold true, friction starts to develop, which can lead to CEO attrition, which in turn could make other title holders quit.

Senior management attrition is dangerous as it distracts from execution and also hurts sales. IT services is a relatively intangible, but critical service and so it takes time for a salesperson to build trust with a client.

Vineet Nayar resigned as CEO in 2013, which led to a slew of exits Vineet Nayar was the CEO of HCLT from 2007 to 2013. He was an HCL-lifer, having joined in 1985 after earning his MBA from XLRI. In 1993, he founded Comnet, which was the start of HCLT's remote infrastructure management services business. It was also in his tenure that HCLT took the bold bet of acquiring Axon, which gave it entry into a number of large customers.

He is widely considered as one of the best salespeople in Indian IT (helped grow sales 5x during his tenure). As per a senior employee of a competitor, he pioneered the idea of selling directly to CEOs at forums such as the World Economic Forum and hosting gala customer events to drive sales. It is not clear on the reasons for his exit, though media reports have speculated that it was due to friction between him and Shiv Nadar (link). We note that a number of senior title-holders exited soon after this event.

Exhibit 6: A number of senior executives quit HCLT after Vineet Nayar resigned

Person No. of

years at HCLT

Designation at HCLT Year of quitting New Co. Designation at New Co.

R Srikrishna 20 Head-IMS and Healthcare 2014 Hexaware CEO

Vinod Chandran 20 Head-IMS Americas 2014 Hexaware Head-IMS

Vijay Iyer 14 AVP, large strategic projects 2014 Hexaware Head-Travel & Transportation

Amrinder Singh 14 AVP, Retail & CPG 2013 Hexaware Head-Europe

Amalesh Mishra 6 Sales Director, APJ* 2015 Hexaware Head-APJ, ME**, Africa

Milan Bhatt 10 AVP, Life Sciences 2014 Symphony Teleca Head-Healthcare and digital

Sandeep Kishore NA Head-Healthcare 2015 Zensar CEO

Krishnan Chatterjee 12 Chief Customer Officer, BeyonDigital 2015 SAP Head-Marketing, India subcontinent

Source: Ambit Capital research

Anant Gupta resigned as CEO in 2016 Anant Gupta was the CEO of HCLT from 2013 to 2016. He had begun his career with HCL in 1993 and headed the infrastructure management services business. He resigned after just three years at the helm to start his own venture. We are worried that there might be some more senior exits after this change.

…the executive chairman and the CEO

HCL Technologies

February 15, 2017 Ambit Capital Pvt. Ltd. Page 24

There are scary similarities with Wipro Wipro has at least three power centres including the executive chairman, his son who is the chief strategy officer and member of the board, and the CEO. The executive chairman, Azim Premji, holds ~73% stake in Wipro and commands enormous respect within and outside the organisation.

Wipro has seen four CEOs in the past 10 years. This has contributed to churn in both sales and delivery which has hurt customer trust and therefore account mining. Wipro's top10 customers contribute revenue of ~US$130mn p.a. on average (CY16) vs ~US$220mn p.a. for Infosys. HCLT is also low at ~US$150mn p.a. TCS has stopped reporting this information, but it was ~US$300mn in FY13 and has likely only increased since then.

We suspect that the frequent CEO changes at Wipro and resulting pressure on near-term performance have also contributed to a highly acquisitive culture at Wipro, which has in most instances failed to create value.

Wipro has underperformed peers significantly over the past 10 years, e.g. FY06-16 EPS CAGR of 10% vs 25% for HCLT.

However, HCLT differs from Wipro as it has a better portfolio mix and better culture. Further, HCLT's CEOs have been internal promotions rather than external lateral hires.

Wipro has seen four CEOs in the past ten years. This has contributed to churn in both sales and delivery which has hurt customer trust and therefore account mining.

HCL Technologies

February 15, 2017 Ambit Capital Pvt. Ltd. Page 25

Not just H-1B, the entire US employee base re-prices Higher proportion of local employees (60% vs 30-45% for peers) onsite has built up the expectation of lower impact on margins because of protectionism. However, increase in the cost of H-1Bs coupled with shortage of IT talent in the US will result in an increase in the cost of all substitutes (including locals). Less mature processes relative to bigger peers like TCS, Infosys (another fallout of organisation structure?) have led to HCLT’s poor track record of managing margin shocks in the past; its margins swung 10% over FY06-16 vs 6% for TCS and Infosys. We expect an EBIT margin impact of 380bps over FY18-20 (vs 350bps for TCS and 520bps for Infosys) but expect only half of that loss to be recovered by FY25.

HCLT high proportion of local employees is likely because of the greater propensity of the company to re-badge employees of clients. This practice is also likely more prevalent in Infrastructure Management Services deals and total outsourcing deals where HCLT has a stronger proposition than peers.

In this context, consensus expects minimal impact on HCLT due to any harsh protectionist measures by the Trump administration.

However, as discussed in our thematic dated 15 February 2017, the cost of all US-based workers is likely to increase.

Exhibit 7: Higher proportion of local employees onsite raised expectations that company will be least impacted

TCS CTSH Infosys Wipro HCLT TechM

Revenue from US as % of overall revenue 53% 79% 63% 53% 60% 48%

Estimate of number of onsite employees in US 35,231 43,866 28,957 19,484 16,919 8,000

Estimate of number of onsite employees who are local 10,569 19,740 12,944 8,242 10,151 3,200

Estimate of number of visa holders onsite 24,662 24,126 16,013 11,242 6,768 4,800

Estimate of the proportion of L-1 visa holders 10% 10% 5% 10% 10% 16%

Estimate of the number of H-1B visa holders 22,196 21,713 14,659 10,118 6,091 4,020

Number of onsite employees in US who are local - % 30% 45% 45% 42% 60% 40%

Source: Ambit Capital research, company

We have reduced our FY19E EBIT margin by 190bps and FY19E EPS by 9% due to protectionism measures by the Trump administration.

Exhibit 8: HCLT is likely to suffer EBIT margin hit by 190bps in FY19

New Old Change

FY17E FY18E FY19E FY17E FY18E FY19E FY17E FY18E FY18E

Revenue (US$ mn) 6,927 7,640 8,664 6,957 7,711 8,746 0% -1% -1%

Revenue growth (YoY) 11.1% 10.3% 13.4% 11.6% 10.8% 13.4% -50bps -50bps 00bps

EBIT (Rs bn) 94.4 103.5 106.1 93.0 103.5 117.1 1% 0% -9%

EBIT margin 20.2% 19.9% 18.0% 20.2% 19.9% 19.9% 00bps 00bps -190bps

PBT 104 113 116 103 113 128 0% 0% -9%

PAT 82 89 91 81 89 100 0% 0% -9%

Dil Adj EPS 57.8 62.7 64.8 57.6 62.7 70.9 0% 0% -9%

Source: Ambit Capital research, company

Consensus wrongly expects minimal impact on HCLT due to any harsh protectionist measures by the Trump administration.

HCL Technologies

February 15, 2017 Ambit Capital Pvt. Ltd. Page 26

Tailwinds short-lived; similarities to Wipro worrisome Current valuations factor in 10% revenue CAGR (USD terms) over FY16-26. The benefits of better mix (~60% of revenue from IMS/ES) leading to revenue CAGR of 12% over FY17-19E will likely taper post FY19. The fallout of the above risks (unless addressed) will be visible by then. We build in 7% revenue CAGR over FY19-26. At a time when investors are worried of first-time structural non-quantifiable risks, we advise staying away from companies with internal issues (Wipro and now HCLT) even though earnings multiples might appear alluring (13x FY19 EPS). Our DCF-based target price of Rs750 (Rs950 earlier) implies 12x FY19 EPS.

Average positioning on CAPOM framework We use our proprietary CAPOM framework that we introduced in our thematic note “Expect continued divergence” dated 10 July 2014 to form a view on growth and profitability outlook for Indian IT services companies. The CAPOM framework ranks companies on Capital Allocation, Portfolio Mix, Operational Excellence and Management (soft issues). Given the recent aggressive acquisition spree which will be return dilutive in our view, HCLT ranks poorly on Capital Allocation relative to larger peers like TCS. Its flawed organisation structure, multiple power centres and senior management attrition lead to poor ranking on the Management factor (soft issues). Overall, HCLT has an average positioning on our CAPOM framework.