technology ahead of its time - iis windows...

TRANSCRIPT

Technology ahead of its time

Cytec Industries Inc. (NYSE : CYT)

Investor Day Presentation

Presented by: David Lilley, Chairman, President and CEO

Jim Cronin, Executive Vice President and CFOShane Fleming, President Cytec Specialty ChemicalsSteve Speak, President Cytec Engineered Materials

May 9, 2007

2

Forward Looking Statement and Non-GAAP Measures

During the course of this meeting we may make forward-looking statements. All statements that address expectations or projections about the future are forward-looking statements.

Some of these statements include words such as “expects”, “anticipates,” “plans,” “intends,” “projects,” and “outlook.” Although they reflect our current expectations, these statements are not guarantees of future performance because they involve a number of risks, uncertainties, and assumptions.

Included in this presentation are estimates for full year 2007 sales and earnings. These were included in our April 19, 2007 press release, which was also furnished as an exhibit to a current report on Form 8-K. These estimates set forth the Company’s assumptions and management’s best estimate of the full year 2007 sales and earnings at that time based on various assumptions set forth in the press release. There can be no assurance that sales or earnings will develop in the manner projected. Actual results may differ materially.

We recommend that you review Cytec’s SEC filings for a discussion of some of the factors which could cause actual results to differ materially from its expectations and projections. This and other Cytec information may be accessed at www.cytec.com.

In sections of this presentation certain ‘non-GAAP” measures are provided and identified as such. We believe that the “non-GAAP” measures can more accurately reflect comparisons of year to year trends and is consistent with how we review the information. A reconciliation of all “non-GAAP” measures to the applicable GAAP measure is provided in the appendix at the end of this presentation.

3

49%

22%9%

20%

Sales by SegmentSales by Segment Sales by Geographic RegionSales by Geographic Region

* Excludes sales of divested water treatment chemicals product lines

Cytec Surface Specialties

Building Block Chemicals

Cytec Engineered Materials

Cytec Performance Chemicals*

North America

Europe

Asia

Latin America

The Cytec Profile2006

Sales $3.1B*

38%

14%

6%42%

Cytec Specialty

Chemicals

4

OUR VISIONCytec’s vision is to become a premier specialty chemicals and materials company through:

Customer FocusSuperior TechnologyOperational ExcellenceEmployee Commitment

so that we can take pride in our achievements and our shareholders will enjoy the highest return on their investment.

5

OUR MISSION

Cytec’s mission is to enhanceshareholder value through double-digit percentage annual growth in earnings per share, while achieving a superior return on equity .

6

Cytec’s Growth Strategy

GDP GrowthGrowth With Market

Focus on TechnologyGrow With New ProductIntroductions and ExistingProducts For New Applications

Bolt-On Acquisitions Operational ExcellenceContinue to Enhance productivity

Targeting 5-7% Top-Line Growth&

Double-Digit EPS Growth

TOP LINE

BOTTOM LINE

Geographic ExpansionGrow In Areas Such As: Asia, Latin America

Focus On Creating Sustainable Technology FranchisesFocus On Creating Sustainable Technology Franchises

7

AgendaShane Fleming – President, Cytec Specialty Chemicals

– Cytec Performance Chemicals

– Cytec Surface Specialties

Steve Speak – President, Cytec Engineered Materials

– Cytec Engineered Materials

Jim Cronin – Executive Vice President and Chief Financial Officer

– Building Block Chemicals

– Income Taxes

– Capital Spending

– Balance Sheet

– Cash Flow

– EPS Wrap-Up

David Lilley – Chairman, President and Chief Executive Officer

– Questions

8

Cytec Performance Chemicals

Product lines discussed today:• Mining Chemicals

• Polymer Additives

• Pressure Sensitive Adhesives

Shane Fleming, President Cytec Specialty ChemicalsShane Fleming, President Cytec Specialty Chemicals

9

Cytec Performance Chemicals Profile2006 sales M$678*

#1 in specialty mining chemicals for copper and alumina processing

#1 high purity phosphine and derivative chemicals

A leading global supplier of polymer additives light stabilizers

Niche supplier for adhesives, emulsion polymers, inks, and acrylic monomer stabilization

2006 operating margin 7.9%

Pressure Sensitive Adhesive

Specialty Additives

MiningChemicals

Phosphine Chemicals

Polymer Additives

Urethanes

Asia Latin America

North America Europe

Product Portfolio (% of Sales) By Region (% of Sales)

31%

7%14%

37%

10%18%

20%33%

15%15%

* Excludes sales of divested water treatment chemicals product line

Staying The Course: Focus On Technology And Manufacturing ImprovementsStaying The Course: Focus On Technology And Manufacturing Improvements

10

Mining Chemicals

Proven History• Almost 100-year history in mining industry• World’s largest full-line, full-service supplier of mining reagents

Value Proposition• Use of Cytec reagents results in improved

metallurgy and recoveries, lower operating costs, and production ofhigher value end products

Global Presence• Worldwide manufacturing and

distribution• Technical service available across

the globe

Eco-Friendly• Work with customers to address

environmental concerns and the safety of their employees

Performance• Business focus on maximizing customers’ return on investment• New product introductions that exceed existing performance standards and push the

limits of what was previously thought possible

11

Mining Chemicals - The Only True Global Provider

Industries

Copper GoldComplex Sulfides ZincNickel PGMUranium CobaltMolybdenum AluminaFeldspar PhosphateMica IronGlass Sand BariteCalcium Carbonate Rare Earths

Product Lines

30%

50%

20%

Alumina Processing

Solvent Extraction

Mineral Processing

Flocculants DispersantsAntiscalants FrothersDepressants PromotersDefoamers CollectorsDewatering Aids Filter AidsMaterial Handling AidsSolvent Extraction Reagents

2006 Sales M$200

Market Production Growth:Copper greater than 3.5% p.a.

Alumina greater than 5% p.a.

12

Mineral and MEP Value Chain

Reagents Remain A Small Portion Of Overall Cost Of Mineral ProductionReagents Remain A Small Portion Of Overall Cost Of Mineral Production

SolventExtraction

ExplorationExploration CommunitionCommunition ConcentrationConcentration Smelting & RefiningSmelting & Refining

Flotation

MiningMining

Thickening

Final ProductsFinal Products Metal componentsMetal components Metal FabricationMetal Fabrication

CableElectrical Plumbing

Net Ore Exports

Water & Waste Discharge

CurrentPosition

OxideProcess

SulfideProcess

BlastingMiningHauling

Net concentrate Exports

SmelterAcid Plant

Power

TailingsTreatment

Electro-winning Furnace &

Refining

CrushingGrinding

RollingCastingDrawing

ForgingPresses

Extruding

SurveyingDrilling

Assaying

Leaching

Copper Price $2.65/lbAvg. SX cash cost $0.50/lb

Avg. flotation cash cost $0.80/lb

Copper Price $2.65/lbAvg. SX cash cost $0.50/lb

Avg. flotation cash cost $0.80/lb

FiltrationTransport

H2SO4

13

Alumina Bayer Process Flow Sheet

Alumina Process Provides Many Opportunities For Cytec TechnologyAlumina Process Provides Many Opportunities For Cytec Technology

Alumina Price $250/MTAlumina Price $250/MT

14

Polymer AdditivesInnovative Technology• 50-year history of supplying leading-edge light stabilizers and antioxidants• Business focus on developing innovative new products that change the

industry’s competitive landscape

Product Superiority• Product mix characterized by technically

differentiated products that deliver performance advantages over competing offerings with some older commodity products

• “Total system packages” require lower dosages to achieve the same or better results

Technical Expertise• Up-front product testing confirms efficacy

of additives before customer makes purchasedecision

• Cytec personnel act as consultants for customers, providing technical product recommendations and manufacturing advice

Versatility• Cytec’s polymer additives find use in many different polymer applications

15

Polymer Additives

40%

7%

18%

20%10%

5%

Automotive

Performance FiberOther

RotationalMolding

Agricultural Film

Specialty Film & Sheet (PET)

Product Chemistries

BenzophenonesBenzotriazolesTriazinesBenzoxazinonesHindered BenzoatesHindered AminesPhenolicsPhenolic/Phosphite BlendsThioestersQuaternary Ammonium Compounds

Product Lines

CYASORB® Light StabilizersCYASORB THT® Light StabilizersCYASTAT® Antistatic AgentsCYANOX® Antioxidants

2006 Sales M$ 134

Top CompetitorsCiba, Chemtura, Adeka, Clariant

Market growth 4-6% p.a.

16

Polymer Additives - Applications

Automotive Plastics

Agricultural FilmRotational

Molding

UltravioletEnergy

RadiantIR/Heat

UV stabilizers are light stable chemicals that absorb harmful UV radiation and dissipate it through non-destructive pathways (heat, fluorescence, phosphorescence).

Protecting Against UV Damage Across Multiple Products & IndustriesProtecting Against UV Damage Across Multiple Products & Industries

17

Basic Petrochemical

Feedstock

Basic Petrochemical

Feedstock

FeedstocksFeedstocks

Chemical IntermediatesChemical

Intermediates

PipePipe

Specialty Packaging

Specialty Packaging

AgriculturalFilm

AgriculturalFilmRaw MaterialsRaw Materials IntermediatesIntermediates

MarketsMarkets

AutomotiveAutomotive

Otheradditives

ResinsResins

UVStabilizers,

AO

UVStabilizers,

AO

Current Position

Master Batch

NA EU

AP LA

Rotational Molding

Rotational Molding

Optical FilmsOptical Films

Wire and Cable

Wire and Cable

Cor

e M

arke

ts

CompoundsCompounds SpandexSpandex

Artificial TurfArtificial Turf

Cytec’s Targeted Markets Represent 30% Of Total MarketCytec’s Targeted Markets Represent 30% Of Total Market

Emer

ging

Mar

kets

Polymer Additives Value Chain

18

Polymer Additives - Business Approach

• Continue targeted market approach with differentiated triazine technology

• Focus R&D and technical service on selected market sectors

• Continue active assessment of product line profitability of mature products

• Drive operational excellence initiatives at US plant to improve return on assets

• Limit capex to only fast payback projects

A Turnaround Business – Good Progress Made In Last 12 MonthsA Turnaround Business – Good Progress Made In Last 12 Months

19

Pressure Sensitive AdhesivesInnovative Technology• Technology leader in both emulsion-based and solvent-based systems• Products focused on specialty applications like skin adhesion, high temperatures and

challenging surfaces

Broad Product Portfolio• More than 80 different formulations• Innovative products such as high-performance emulsions, removable adhesives and non-

interfering medical adhesives

Economics• Attractive total systems cost for

end users• Solid cost/performance ratio

Eco-Friendly• In process of developing UV-curable

PSAs

Manufacturing Excellence• cGMP facility allows us to manufacture our line of transdermal PSAs under the stringent

conditions required by both the FDA and pharmaceutical manufacturers

20

Pressure Sensitive Adhesives

34%

Labels

23%

18%8%17%

Tapes

Graphics

MedicalSpecialty

Applications

Product LinesGELVA® Multipolymer EmulsionsGELVA® Multipolymer SolutionsSOLUCRYL® Solvent-based Acrylic

Polymers UCECRYL® Water-based Acrylic

Polymers

Cloth medical tapesFinger bandagesDrug delivery patchesFrozen foods labelsFood and beverage containersIndustrial labels General purpose home, office and

industrial tapes Graphic filmsRemovable decals

2006 Sales M$91

Markets Served

Top CompetitorsAvery, 3M, Ashland, National Starch, Rohm & Haas, BASF

Targeting Innovation To High Value Sub-Segments In Tapes And GraphicsTargeting Innovation To High Value Sub-Segments In Tapes And Graphics

21

Pressure Sensitive Adhesives - Applications

Tapes –Electrical & HVAC

Medical –Transdermal Patches

Graphics –Films & Decals

GELVA GME is the only emulsion PSA capable of meeting the stringent requirements associated with the “No Label Look” for the beverage label market, while maintaining clarity:• Water resistance• High temperature resistance (pasteurizable)• Cold temperature resistance (72 hours in an ice chest)

Beverage Labels

Technology Leader In Emulsion-Based And Solvent-Based SystemsTechnology Leader In Emulsion-Based And Solvent-Based Systems

22

PSA Value Chain

Creating New Technology Platform With Eco-Friendly UV Cure PSACreating New Technology Platform With Eco-Friendly UV Cure PSA

BasicPetrochemical

FeedstockChemical

Intermediates

Solvents

LabelCoaters

Raw MaterialsRaw Materials IntermediatesIntermediates CoaterCoater End UserEnd UserConverterConverter

Current Position

Adhesives BU

Other PSAs

Acrylic Solvent borne PSA

Monomers

Additives

Paper

Film

Other Facestocks

Foam

Release Liners

GraphicCoaters

TapeCoaters

MedicalCoaters

SpecialtyCoaters

Converters

Paper Merchants

Screen Printers

Sign Shops

Digital Houses

Converters

Distributors

Manufacturer

/

Brand Owner

Acrylic Water borne PSA

UV PSA

Target Position

23

Pressure Sensitive Adhesives - Business approach

Already Actioned

• Rationalize to a global organization based on functional lines

• Eliminate duplicate activities e.g. local R&D

• Establish cost effective manufacturing network

Path Forward

• Focus R&D activity on high value niche applications

• Increase market presence and penetration of Asian market

24

Cytec Performance Chemicals - Summary

• Portfolio of technology driven product lines requiring different business approaches– Strong positions in growth markets e.g. Mining

Chemicals and Phosphines (market and technology leadership), PSA (leader in both emulsion and solvent-based technologies)

– Opportunity to improve earnings through productivity, and additional product rationalization / asset restructuring in turnaround product lines, i.e. Polymer Additives and Urethanes

– Operate Specialty Additives for cash

Portfolio Approach Expected To Yield Average Annual +10% EBIT GrowthPortfolio Approach Expected To Yield Average Annual +10% EBIT Growth

25

Cytec Surface Specialties

• The Coatings Market

• Our Product Lines

• Our Earnings Growth

Shane Fleming, President Cytec Specialty ChemicalsShane Fleming, President Cytec Specialty Chemicals

26

Global Coatings Market Overview

Maintenance21%

Automotive6%

Industrial28%

Architecture45%

By Segment

EMEA38%

Americas31%

Asia31%

By Region

WB Industrial9%

Powders5%

Radcure1%

Other2%

WB Architecture

28%

HS Solvent Based

8%

MS Solvent Based47%

By Technology

Projected Coatings Growth Rate:North America 2.1% Asia Pacific 12.5%Latin America 6.0% Japan 0.3%Western Europe 1.5% China 8.0%Eastern Europe 6.0%

Paint technology varies dramatically across regions:• Western Europe, Japan and North America are largely converted to

lower VOC systems. • Higher VOC solvent based systems are still the primary technology in

other regions.

Coatings Growth Rate thru 2009:Architectural +2.0%Industrial +2.5%Automotive -1.0%Maintenance +2.5%

Three key demand trends increasing growth opportunities:1. New VOC regulations coming into effect through 2010 driving

reformulations for lower VOC or environmentally friendly resin systems.

2. Increased performance, e.g. scratch or chemical resistance3. Need to lower overall cost of resin systems

Strong Drivers For Growth Opportunities In NA And EU Despite Overall Growth At ~GDPStrong Drivers For Growth Opportunities In NA And EU Despite Overall Growth At ~GDP

Global Paint Market : B$ 67 of Revenues and 28 million MT of Volume

Source: SRI 2005 Coatings, Skeist Coatings VII

27

The value chain for coatings is comprised of global feedstock producers, a mixture of large commodity companies and specialty chemical companies, paint companies, industrial

distributors, direct sales and retailers in serving end users

BasicPetrochemical

Feedstock

ChemicalIntermediates Monomers

Solvents

FineOrganic

ChemicalsSpecialtyPaints

IndustrialOEM Paints

ArchitecturalPaint

Companies

CompanyStores

PaintDistributors

LargeNationalChains

EndUsers

Distributors andManufacturing Reps

Direct Sales

IndependentStores

Consumer

Raw Materials Intermediates Finished Products End UserDistribution

Coatings Industry Value Chain

Pigments

Resins

Additives

Resins

We Deliver A Broad Range Of Specialty Resins, Crosslinkers And Additives With Technical Service Support To Enable Our Customers To Meet End User Needs

We Deliver A Broad Range Of Specialty Resins, Crosslinkers And Additives With Technical Service Support To Enable Our Customers To Meet End User Needs

Crosslinker

Cytec Technology Positions

28

Our Product lines

• Liquid Coating Resins

• Powder Coating Resins

• Radcure Resins

29

Cytec Surface Specialties

Waterborne

Powder

Radcure

Aminos

Solventborne

North America

Europe

Asia

Latin America2006 Sales M$1,523

2006 Operating Margin 6.3%

Leadership positions in eco-friendly and solventborne technologies

Global presence, including R&D and manufacturing, to service customers

2006 and 2007 transition years for putting in place growth and productivity initiatives leading to

Significant profit improvement potential

16%

22%

28%

3%

25%

55%

17%

17%

17%

LiquidCoatingsResins

30

Liquid Coating ResinsNew Products and System Innovation • Strong presence in waterborne technologies to meet VOC

regulations• Specialty additives as solutions to enable solventborne

conversion into waterborne

Broad Product Portfolio• Present in a variety of technologies serving the needs of almost

all segments of the coating market• Leader in Waterborne alkyd and Waterborne epoxies as growing

technologies to replace solventborne coatings in architecture and industrial coating applications

Global Presence• Manufacturing presence in Europe, North America, Brazil, Japan,

Thailand• R&D and TS&D laboratories in all regions

Technical and Formulation knowledge• Extensive formulation know-how to serve customersKey Raw Materials (all quantities + or -10% in metric tons)

• Formaldehyde 55,000• Methanol 35,000• Methyl Formaldehyde 30,000• Melamine 20,000 (Internal transfer)• Styrene 15,000

31

Liquid Coating Resins

Waterborne

Solventborne Aminos

33%33%

34%

Technology

Market

Automotive

ArchitecturalCompounding &Reinforcement

OthersMaintenanceand Marine

Industrial

10%17%

36%

10%5%

22%

Major Competitors:- DSM- Cray Valley- Hexion- BASF- Ineos

32

Liquid Coating Resins Environmental Drivers

Increasing VOC regulations in Europe, North America & Japan

Waterborne technologies and High solids acrylic as low VOC alternatives

Continue product development in:• Exterior stains• High solids acrylics/ Trim enamels (WB alkyds)• One pack waterborne epoxyMonitor VOC legislation in Asia

Category Aspect/Technology Actions

Increased Environmental Pressure Leading To New Opportunities For Product And System Innovation

Increased Environmental Pressure Leading To New Opportunities For Product And System Innovation

End user pressure to reduce total coatings costs

Lower film build systemsReduce number of coatsLess energy consumption

Develop breakthrough one pack epoxy systems to increase productivity Work on one less bake step for Auto OEM

Reduced HAPS and formaldehyde emissions

Formaldehyde free crosslinker Ambient cure systems

Get products ready when legislation come into full force

• formaldehyde free crosslinker in NA and EU• ambient cure waterborne resins

REACH product registrations

Potentially discontinue select products due to testing costsCoatings customers may discontinue products as a result

Finalize assessment of impacted substances by REACHDevelop action plan for potential product rationalization

33

Priority 2 : Restore profitability and competitive position in product clusters with lower technology differentiation

Liquid Coatings Margin Improvement Actions

Restore Profitability In The Near Term Through Aggressive Portfolio And Cost Rationalization And Deliver Longer Term EBIT Growth Through Globalization Of WB Systems

Restore Profitability In The Near Term Through Aggressive Portfolio And Cost Rationalization And Deliver Longer Term EBIT Growth Through Globalization Of WB Systems

Implement value pricing, product line and asset rationalizationAmino Cluster – Turnaround

• Restructure North America / European manufacturing base• Optimize SG&A and resource deployment• Develop and launch more cost effective offsets for commoditized products• Execute investment plan for high solids eco-friendly products for Japan automotive market

Solventborne Cluster – Rationalize/optimize portfolio• Finalize rationalization plan of alkyds and other commoditizing solvent based products• Based on the above, implement asset base restructuring plan in Europe• Bottom slice solventborne products through aggressive pricing actions

Expand global sales of waterborne technologies • Invest in Wallingford (CT) to secure local sourcing and support growth in NA• Accelerate growth by reallocating technical and commercial resources• Position additives and resins as a synergetic system to drive conversion of current solvent based coatings to lower VOC replacements

• Raise awareness of complete range through marketing communication and technical training

Priority 1 : Drive globalization and growth of WB technologies

34

Conclusion: Liquid Coating Resins A Differentiated Strategy for the Three Clusters

Grow Waterborne, Turnaround Aminos, Harvest SolventborneGrow Waterborne, Turnaround Aminos, Harvest Solventborne

Invest to growFocus on the high endAssess opportunities for growth

Japan

Focus on the high endShift to the high endAssess opportunities for growth

Asia excl Japan

Turn-aroundFocus on the high endHarvest low-end

Invest to growAmericas

Turn-aroundFocus on high-endHarvest low-end

Invest to growEurope

AminosSolventborneWaterborne

35

Powder Coating ResinsHigh Performance Innovation• Global reliable supply of quality polyester resin targeting reduction of total

formulation Costs and Value-Adding Innovative Finishes• A dual innovation strategy implemented to take into account strong market needs

in terms of lowering total applied cost

Broad Product Portfolio• Broad CRYLCOAT® resin portfolio meeting most end-use market needs• Additives and master batches – ADDITOL®, MODAFLOW® and BECKOPOX®• POWDERLINK® cross-linking technology for special finishes• UVECOAT® resins for radiation-curable powder coatings

Market Position• Leader in all segments: Hybrid, Primid(*), TGIC – standard and superdurable• Leader in additive master batches for improved coating performance• Leader in UV powder binders for reaching beyond traditional powder marketsGlobal Presence• Manufacturing plants and technical service laboratories in the North America,

South America, Asia Pacific and Europe• Innovation pipeline serving innovation worldwide from research centers in

Belgium, Italy, U.S. and South KoreaKey Raw Materials (all quantities + or – 10% in metric tons)• NPG (Neo Pentyl Glycol) 60,000• PTA (Purified Terephthalic Acid) 80,000• PIA (Purified Isophthalic Acid) 15,000

36

Powder Coatings End-Uses (excl. functional)

Architectural14%

Furniture11%

Automotive16 %

Gen’l Industrial Outdoor30%

Gen’l Industrial Indoor14%

Appliances16%

Global Market for PE Powder Resins

Powder Coating Resins Markets ServedGlobal Markets Expected to Grow 7% per Annum

EuropeMiddle East

Africa

Americas

Asia Pacific

17 %

35%

48 %

37

Must innovate to survive in a competitive landscape:1. Expand market reach through:

• Entry into non traditional markets• High performing resins for most profitable markets

2. Maintain competitiveness through:• Improve in-process and raw material cost position• Lower total formulation and end-use cost for customers

Powder Coating Resins Competitive Landscape

Cytec And DSM Remain Only Two Truly Global PlayersCytec And DSM Remain Only Two Truly Global Players

Top Competitors- Cytec- DSM- Cray Valley- Nuplex- Hexion- Bayer- Zhongfa- Chanxie

38

Powder Coating Resins Environmental Drivers

Strengthening VOC regulationsfocus Europe/Americas first

Powder as a recognized low VOC option

• Include low VOC in value proposition in segment where powder penetration is low• Review opportunities to promote powder as VOC-free surface finishing option• Priority to Europe and Americas but follow up needed for Asia at later time

Category Aspect/Technology Actions

Polyester Powder – Intrinsically Compliant To Most Stringent Enviro RegulationsPolyester Powder – Intrinsically Compliant To Most Stringent Enviro Regulations

Increasing energy costsLow bake powderUV Powder

Regulations related to health hazard and toxicology concerns

• Reinforce low energy usage in UV powder value proposition• Promote and expand use of low bake technology based on energy efficiency• Assess energy usage of powder vis-à-vis other coating solutions

TGICBisphenol A

• Continue to promote resins for TGIC-free formulations in southern Europe• Develop optimized systems compliant with food contact regulations• Replace liquid and powder systems using epoxy with full polyester solutions

39

Conclusion: Powder Coating Resins

Margin Improvement

Operational Excellence

Product mix optimization and dual innovation strategy focusing on both improving cost position and expanding the

reach of powder into more profitable segments

Continuous capacity stretch to support demand at next-to-zero cost, through lean manufacturing implementation and

process innovation

Global Leadership Position

Maintain global leadership position, growing business and promoting profitable innovation in powder coating with global

key accounts and industry winners

Good Top-Line And Earnings Growth But Margins Held Down By Low End CompetitorsGood Top-Line And Earnings Growth But Margins Held Down By Low End Competitors

40

RADCURE™ Energy Curable Solutions

Innovative Technology• 35+ years experience in radiation curing technology• Pioneer and worldwide leader in UV & EB energy curable Oligomers

and Monomers

Broad Product Portfolio• Portfolio of 500+ efficient and environmentally-friendly coating resins,

additives and servicesEconomics• High production throughput (fast cure rates)• Low energy requirements

Total Solutions Provider• World class technical service and application support expertise

Eco-Friendly• Zero or low solvent emissions

Performance• High gloss/ultra smooth surfaces• Ability to coat heat sensitive substrates

Key Raw Materials (all quantities + or – 10% in metric tons)• Acrylic acid 40,000• Diglycidylether BPA 10,000• TPG (tri propylene glycol) 10,500

41

RADCURE Markets Served

Graphic Arts

Packaging Publishing

Commercial Industrial

Radiation Curing Is An Attractive Solution For Many ApplicationsRadiation Curing Is An Attractive Solution For Many Applications

Industrial Coatings

Wood

Plastics

Opto-Electronics

Metal

Glass Lamination

Electronics

5% Inks

24%

Plastics & Metal

29%

Wood & Paper

19%

OPV

23%

Monomers

33%

Formulations &Additives

10%

Oligomers

57%

42

WOOD

PUTTY

PRIMER

SEALER

TOP COAT

Wood – Parquet Flooring

TFT Glass substrate

Black matrix

Polarizer

Electrode

Liquid crystal

Protective film

ElectrodeAlignment film

Sealant

Anisotropicconductorfilm

TAB

Driver LSI

PCB

SpacerLight diffuser Prism sheet Waveguideplate

Edge light

Reflector

PolarizerColor filter

Electronics (flat panel displays)

Cytec Is A Global Player With Diversified Portfolio In All Major UV ApplicationsCytec Is A Global Player With Diversified Portfolio In All Major UV Applications

UV/EB Curing Resins & Additives Example of Applications

Red=Target Applications

RadcureApplication

43

Radcure Resins Competitive Landscape

Source: Cytec estimate

Leadership Position Within A Fragmented Global Competitive EnvironmentLeadership Position Within A Fragmented Global Competitive Environment

Key Focus Going Forward:

• Technical differentiation (breakthrough

applications, cost effective production)

• Progressive diversification (non-traditional

applications)

• Flexibility and speed critical

Key Competitors:

• Sartomer

• BASF

• Eternal

• AGI

• Cognis

• Bayer

•Toa Gosei

• Regional Players

44

Category

1. Solvent reduction in the Inks and OPV industry

2. VOC/ CO2 reduction for the coil industry

3. VOC/ CO2 reduction for industrial spray applications

4. Heavy metal reduction in electronics

5. Highest energy cost in history

6. Oil based raw materials getting scarce

7. Recycling of coated finished goods

Aspect

Radcure inks for indirect food contact and approval of Radcure systems for direct food contact

Radcure systems for coil

Radiation curable spray coatings for wood, plastics & automotive

Radiation curable alternatives for chromium based technology

Radiation curing is the most energy efficient way to cure inks and coatings

Radiation curable products based on renewable resources

Radiation curable products compatible with the recycling process

Actions

Develop/ market low extractable, low odorrange of products & Food contact Legislation initiative in US

Develop / market UV primer for coil to replace solvent system

Develop / market low viscosity systems for spray applications ( WB UV )

Develop / market UV curable black matrix inks for LCD’s production

Increase emphasis on energy savings in print advertising and push faster curing products

Develop resins based on renewable raw materials and market these in existing and new application areas

Include recycling capability developments for paper & board, plastics for packaging, automotive

Radcure Resins Environmental Drivers & Market Opportunities

Key Drivers; Cost/Productivity – Environmental Legislation – PerformanceKey Drivers; Cost/Productivity – Environmental Legislation – Performance

45

Conclusion: Radcure Resins

Platform BusinessApproach

Invest to SustainGlobal Leadership

Dedicated teams to drive global focus on major growth initiatives. Key platforms include Electronics and Water Borne technologies

Accelerating resource loading in Asia high growth region.Capital expenditures for new capacity/productivity. Acquisitions to fill key technology / market gaps including targets in fast growing electronics market.

Dual Strategy

Intensify efforts to identify and develop breakthroughapplications in and outside the current coatings and ink market as well as drive productivity initiatives to remain competitive in core resin manufacturing

Good Top-Line And Earnings Growth Through Innovation And ProductivityGood Top-Line And Earnings Growth Through Innovation And Productivity

46

Cytec Surface SpecialtiesEarnings Growth

Investment in eco-friendly products and high growth markets

– Wallingford, CT. waterborne resins plant; start-up Q2 ‘08

– China Radcure oligomers plant; start-up Q2 ‘08

– Aminos capacity expansion in Japan mid-2009

Increased productivity from innovation

– Revitalized and balanced product development pipelines – striking the

right mix of “Breakthrough and Incremental” projects

– Disciplined project execution linking R&D, Marketing and Manufacturing

using Cytec Innovation Management System (CIMS) process

Driving Innovation Across Entire OrganizationDriving Innovation Across Entire Organization

47

Product rationalization / Asset restructuring• Product rationalization

– Additional rationalization ongoing of solventborne product lines coupled with asset redeployment to waterborne products (primarily Europe)

– Maximizing asset utilization by bottom slicing lower margin business to optimize mix

• Asset restructuring– Dijon plant shutdown / product transfers complete; now in “clean and

secure” phase

– Additional restructuring investigations ongoing for Liquid Coating Resins

Expect Completion Of Study For Further Restructuring By Q3, 2007Expect Completion Of Study For Further Restructuring By Q3, 2007

Cytec Surface SpecialtiesEarnings Growth

48

Cytec Surface SpecialtiesEarnings Growth

Operational Excellence to Improve Margins• R&D supporting Manufacturing to improve basic process chemistry

and qualify alternate / lower cost raw materials– Savings beginning in 2007

• Lean manufacturing being introduced at all major sites, reducingcosts and adding capacity at low / no capital

– Powders; gained 20% capacity globally, 10% headcount reduction at 2nd largest site

– LCR; Expect 15% capacity gain at largest plant to support LCR growth, and allow other site rationalization.

• Expanded / Integrated Six Sigma programs– In-house training of Black-belts across global manufacturing base

– Six Sigma related yield improvements programs across multiple product lines delivered > $2 million per year in savings in 2006; integrated into other major efforts as a key contributor

Lean Program Delivering Real Value in Lower Costs / Extra CapacityLean Program Delivering Real Value in Lower Costs / Extra Capacity

49

Cytec Surface SpecialtiesEarnings Growth

Operational Excellence continued• Best practice sharing leveraging global “Product Line Cluster” manufacturing

organization– Radcure; sharing monomers recovery work at San Fernando Plant (savings of $1 million) to all

sites will result in > $4-5 million per year savings (Target date for completion: year end 2008)

– LCR; European sites absorbed high value products from Dijon shutdown with virtually no added capital or operating costs

• Dedicated energy / waste reduction teams focused on lowering energy usage and waste generation costs

– 2007 Targets:• Energy savings of >$2 million/year through engineering solutions

• Waste reduction savings of $1.5 – 2.0 million

• On track with implementation of Global ERP system– Real-time access to global data (faster decision making, lower inventory, improved service

levels)

– Increased productivity (and lower maintenance costs)

– Slated for completion by end of 2008

Multi-Pronged Approach Leading to Earnings GrowthMulti-Pronged Approach Leading to Earnings Growth

50

Cytec Surface SpecialtiesPost 2007

• Well aligned with key market trends:– Move to environmentally friendly products

– Presence in high growth Asia markets

• Target for top line growth of 5% per annum

• Target for average earnings growth of 15% per annum which includes benefits of actions to get to 10% operating margin

Innovation And Relentless Focus On Costs Will Drive Improvement In Surface SpecialtiesInnovation And Relentless Focus On Costs Will Drive Improvement In Surface Specialties

51

Presented By: Steve Speak

President, Cytec Engineered Materials

52

CEM Overview

Global Leadership Build From Organic and Acquisition-Based Growth

E M D

Fothergill

NARMCO

Global Leadership Build From Organic and Acquisition-Based Growth

E M D

Fothergill

NARMCO

53

CEM Company OverviewBroad Product Portfolio

And Capabilities

Composites Adhesives

Carbon Fibers

Carbon Weaving

Specialty Products

Material Science

A strong franchise built on technology leadershipA strong franchise built on technology leadership

54

Global Market & Product Leadership

Market Segments Product Familiesand

A Leader in these…

Military AircraftCommercial Aircraft Business and Regional JetsRotorcraftLaunch VehiclesHigh Performance Automotive

Damage tolerant composites Structural Film Adhesives and PrimersHigh Temperature Composites and AdhesivesComposites for Automated ProcessingAblative Materials for Launch Vehicles/MissilesPAN Carbon Fibers for Aerospace

55

With Strong Position in Primary StructuresFF--2222

Cytec Technologies have enabled the Cytec Technologies have enabled the growth of composites in high growth of composites in high

performance primary structural performance primary structural applicationsapplications

PremierPremier

AA--380380

FF--3535

0%

10%

20%

30%

40%

50%

60%

1970 1980 1990 2000 2010

Com

posi

te U

sage

Mirage

F18CD

C17

AV 8B Rafale

F18 E/F

UCAV

F35

F/A 22

B2

A-380A-320 A-340

A-330

F15

787

Premier Horizon

787787

FF--1818

UCAVUCAV

Global HawkGlobal Hawk

56

Global Operations and Research

Oestringen, Germany• Composite prepregs• Film adhesives

Oestringen, Germany• Composite prepregs• Film adhesives

Havre de Grace, MD• Film adhesives• Syntactic foams• Primers• Potting compounds• Sealants• Research

Havre de Grace, MD• Film adhesives• Syntactic foams• Primers• Potting compounds• Sealants• Research

Rock Hill, SC• PAN carbon fibersRock Hill, SC• PAN carbon fibers

Bellevue, WA

Greenville, SC• Carbon fibers - pitch and PAN

Greenville, SC• Carbon fibers - pitch and PAN

Hampton, GA

Sandy, UT

Winona, MN• Ablative composites• Carbon/carbon molding compounds

• Carbon fiber preforms

• Sheet molding compounds

Winona, MN• Ablative composites• Carbon/carbon molding compounds

• Carbon fiber preforms

• Sheet molding compounds

Greenville, TX• Composite prepregs• Prepreg tow and slit tape

• Weaving

Greenville, TX• Composite prepregs• Prepreg tow and slit tape

• Weaving

St. Louis, MO

Wrexham, UK• Composite prepregs • Film adhesives • Potting compounds• Research

Wrexham, UK• Composite prepregs • Film adhesives • Potting compounds• Research

Wilton, UK• ResearchWilton, UK• Research

Naples, Italy

Toulouse, France

Niagara Falls, Canada

■

OperationsRegional Sales OfficesResearch & DevelopmentManufacturing RepsRegional Tech Support Office

Wichita, KS

Tempe, AZ • HeadquartersTempe, AZ • Headquarters

Torino, Italy

St. Germain En Laye, France

Central Village, CT

Bedford, TX

Moenchengladbach, Germany

China ■

Singapore ■

Thailand ■Anaheim, CA• Composite prepregs• Film adhesives • Primers• Research• Silicone sealants (D Aircraft)

Anaheim, CA• Composite prepregs• Film adhesives • Primers• Research• Silicone sealants (D Aircraft)

Malaysia ■

Korea ■

Taiwan ■

Tokyo, Japan ■

Sidney

57

Operating Results

0

100

200

300

400

500

600

700

2002 2003 2004 2005 2006

Sale

s ($

M)

40

60

80

100

120

140

Earn

ings

($M

)

Sales Operating Earnings

Global Sales & Earnings2006: Sales = $602M, Earnings = $106M

58

Sales Distribution

End-Market Sales Distribution -Diversified Aerospace Portfolio

Regional Sales Distribution -Global Reach

North America,63%

Europe30%

Asia7%

Satellite & Launch

2%

Brakes4%

HP & Other15%

Biz/Reg Jet & Comm Rotor

17%

Military 26%

Large Commercial

Transport36%

59

What is a Composite?

• Combination of a reinforcement material and a matrix

• Early examples– Mud and straw– Fiberglass and Resins

• Fibers provide strength and stiffness

• Matrix protects fiber, transfers loads between fibers and imparts other value-added attributes

• “Advanced” composites - Reinforcement = carbon fiber. Typically 65% Fiber / 35% Resin

60

“Prepreg” Manufacturing

Release paper

Resin Applicator

Resin Film Roll

HOT MELT RESIN

Continuous fiber

Or

Woven fabrics

Resin Film

Heat & pressureResin Film

Cooling of

Material

“Prepreg” Fabric or Tape

Resin Film

Heat & pressureResin Film

Cooling of

Material

“Prepreg” Fabric or Tape

61

If the Composites Industry was a Person…What Would it Look Like?

62

Still early in the growth and adoption cycle…but

mature and proved in terms of performance,

reliability and value

Carbon Composites

Aluminum Steel

LowTechnology

Maturity

HighTechnology

Maturity

Technology Learning CurveTechnology Learning Curve

If the Composites Industry was a Person…What Would it Look Like?

63

Why Composites???

Advantages Over Metals

Improvements in materials/manufacturing technology and applicatiImprovements in materials/manufacturing technology and applications ons experience are reducing/eliminating the disadvantages of composiexperience are reducing/eliminating the disadvantages of compositestes

Lighter weight

High strength and stiffness

High corrosion resistance

High fatigue resistance

Ability to fabricate complex and highly integrated components

Ability to reduce or eliminate the need for mechanical fasteners

Historically high cost—driven mostly by part manufacturing cost

Earlier in the learning curve than metals

Earlier generations of technology fell short of impact resistance targets

Disadvantages

64

Typical Composite Applications

F/A-22

= Composites

Including skins not shown

Mili

tary

Larg

e Co

mm

erci

al T

rans

port

Cockpit components

Doors

Interiors: sidewall, ceiling and floor

panels; storage and cargo bins; lavatories

and galleys

Radome

Air conditioning ductwork

Pylonfairings

Leadingedgeslats

Ailerons

Fin boxes and rudders

Engine components and cowlings

Exteriors: Wing to body fairings

Flaps, spoilers and deflectors

Tail planesand elevators

65

Typical Composite Applications

F/A-22

= Composites

Including skins not shown

Roto

rcra

ft

Mili

tary

Larg

e Co

mm

erci

al T

rans

port

High

Per

form

ance

Aut

o

Cockpit components

Doors

Interiors: sidewall, ceiling and floor

panels; storage and cargo bins; lavatories

and galleys

Radome

Air conditioning ductwork

Pylonfairings

Leadingedgeslats

Ailerons

Fin boxes and rudders

Engine components and cowlings

Exteriors: Wing to body fairings

Flaps, spoilers and deflectors

Tail planesand elevators

66

Military Aerospace—Segment Drivers & TrendsDrivers: – Lightweight, high strength &

damage tolerant structures– Higher service temperature – Corrosion and fatigue resistance– Stealth– Affordable performance

Trends: – Steady growth in composite usage– Steady growth in number of

composites containing aircraft – Leveraging proven technologies for

today’s programs—but seeking even greater performance gains for future programs

……Cytec is the clear segment leaderCytec is the clear segment leader……new programs using larger amounts of Compositesnew programs using larger amounts of Composites

0%

10%

20%

30%

40%

50%

60%

MirageF15

F18CD

C17

AV 8B Rafale

F18 E/F

UCAV

EuroFighter

F35

F/A 22

B2

1970 1980 1990 2000 20100%

10%

20%

30%

40%

50%

60%

MirageF15

F18CD

C17

AV 8B Rafale

F18 E/F

UCAV

EuroFighter

F35

F/A 22

B2

0%

10%

20%

30%

40%

50%

60%

MirageF15

F18CD

C17

AV 8B Rafale

F18 E/F

UCAV

EuroFighter

F35

F/A 22

B2

MirageF15

F18CD

C17

AV 8B Rafale

F18 E/F

UCAV

EuroFighter

F35

F/A 22

B2

MirageF15

F18CD

C17

AV 8B Rafale

F18 E/F

UCAV

EuroFighter

F35

F/A 22

B2

1970 1980 1990 2000 2010

Increasing Composite Use in Military Aircraft

67

Commercial Aerospace—Segment Drivers & TrendsDrivers:

– Revenue passenger mile (RPM) growth

– Aircraft obsolescence and replacement

– Customer preferences/improved performance

– Fuel cost escalation

Trends: – Increasing Large Commercial

Transport (LCT) and Business Jet production rates

– Strong order backlog, continuing to build

– Strong secular trend towards adoption of composites to achieve higher aircraft performance value

Production RatesProduction Rates

Orders and BacklogOrders and BacklogBacklogOrders

200

400

600

800

1000

1200

2002 2003 2004 2005 2006 2007 2008 2009

Total CEM Proj Boeing/CEM Proj Airbus/CEM Proj

0250500750

100012501500175020002250

1998 1999 2000 2001 2002 2003 2004 2005 2006-500

1000

2500

4000

5500

Boeing Orders Airbus Orders Backlog

68

% composite by weight of aircraft% composite by weight of aircraft

Step Change In Composite Usage%

Com

posi

te

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

747

757/767A300-600

777A330/340

747-400

A310

High50%

% C

ompo

site

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

747747

757/767757/767A300-600A300-600

777777A330/340A330/340

747-400747-400

A310A310Low 10%

FSA

69

……increasing production rates for current generation aircraft and increasing production rates for current generation aircraft and the secular the secular trend toward increased composites provide long growth potential!trend toward increased composites provide long growth potential!

% composite by weight of aircraft% composite by weight of aircraft

Step Change In Composite Usage%

Com

posi

te

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

747

757/767A300-600

777A330/340

747-400

A310

High50%

% C

ompo

site

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

747747

757/767757/767A300-600A300-600

777777A330/340A330/340

747-400747-400

A310A310Low 10%

A380

Future Single Aisle

787

A380A380

A350

Future Single Aisle

FSA

70

The Challenges For Composite Suppliers

• Affordable Performance

• Developing the Supply Chain

Technology Advancement

Expanding Supply To Meet Demand

Matching Geographic Point of Supply with Customer Demand

=

=

=

71

Technology Mission: First In Technology Solutions

First and foremost a technology company

Strongest competitive discriminator

Primary platform for creating value for our customers

Rich heritage and technology portfolio developed over 65 years of investment

Customer focus and Operations Excellence critical to delivering technology value

72

Technology Mission: First In Technology Solutions

First and foremost a technology company

Strongest competitive discriminator

Primary platform for creating value for our customers

Rich heritage and technology portfolio developed over 65 years of investment

Customer focus and Operations Excellence critical to delivering technology value

The Composites Challenge—Affordable Performance

Material cost is only a small fraction of total part cost

Total Composite Part Cost

CEM Technology Solutions

Out-of-autoclave materials

Integrated Composite Systems

Automated tape & fiber placement

Resin Infusion

Adhesives

……delivering higher performance and value than metalsdelivering higher performance and value than metals

Carbon Fiber

73

Integrated Composite Development Targets• Historical customer requirements

focused on damage tolerance and maximum use temperature

• New programs seeking even higher performance levels

– Higher mechanical performance with equal/greater damage tolerance = weight savings

– Improved manufacturing processability = affordability

• CEM employing a fully integrated R&D approach through our Global Technology Organization

– New carbon fibers– Carbon fiber / matrix interface

optimization– Improved resin matrix

……CEMCEM’’s broad capability and fully integrated material science approacs broad capability and fully integrated material science approach to product h to product development will enable further advances in our composite materidevelopment will enable further advances in our composite material performance al performance

……Carbon fiber technology is becoming more Carbon fiber technology is becoming more critical to meeting future customer needscritical to meeting future customer needs

Strength and Use TemperatureTo

ughn

ess

5276-1

5250-4997

977-2

NextGenerationTechnology

74

CEM—Carbon Fiber Update

• Carbon fiber technology is growing more important for meeting higher customer requirements and demand

• CEM currently supplies about 1/3 of requirements internally—growing to 50%+

• CEM is investing more to ensure strong technology and supply chain position

Carbon Fiber Development Targets

Spec

ific

Tens

ile S

tren

gth

Specific Tensile Modulus

Stronger &

Lighter ComponentsAramid

S Glass

Steel

Aluminum2024-T6

SMGen

1

SMGen

2

IMGen

1

IMGen

2

75

CEM—Carbon Fiber Update

• Carbon fiber technology is growing more important for meeting higher customer requirements and demand

• CEM currently supplies about 1/3 of requirements internally—growing to 50%+

• CEM is investing more to ensure strong technology and supply chain position

2002 2007 2010

3K E

Q c

apac

ity

Carbon Fiber Development Targets

Cytec Carbon Fiber Capacity Growth

Double Capacity

Double Capacity

• Capacity Growth– Doubled capacity since 2001 acquisition

– New carbon fiber capacity in planning phase—will double capacity again

– Targeted strictly for strategic aerospace customers and select aerospace applications

– Site selection complete, preliminary design late-2007, on-line early 2010

Spec

ific

Tens

ile S

tren

gth

Specific Tensile Modulus

Stronger &

Lighter ComponentsAramid

S Glass

Steel

Aluminum2024-T6

SMGen

1

SMGen

2

IMGen

1

IMGen

2

76

Technology—Automated ProcessingAutomated Fiber Placement

Highly automated Manufacturing Process—Developed by Machine Manufacturers

Required Development of New Material Solutions That:

– Meets Demanding Aerospace Performance Requirements

– Adaptable to New Automated Fiber Placement Process

Cytec Developed New “Slit PrepregTape” Product Now Qualified for Several New Applications

77

Technology—Automated Processing

AFP on Raytheon Premier One Business Jet

All Composite Fuselage—600 Lbs.

20% Lighter Than Aluminum Design With Greater Interior Volume

Part Count Reduced From 13,000 to 6,000

Production Costs Reduced 10%

Automated Fiber Placement

Highly automated Manufacturing Process—Developed by Machine Manufacturers

Required Development of New Material Solutions That:

– Meets Demanding Aerospace Performance Requirements

– Adaptable to New Automated Fiber Placement Process

Cytec Developed New “Slit PrepregTape” Product Now Qualified for Several New Applications

78

Technology—Resin Infusion

• Infusion of resin into a dry carbon preform• Several acronyms cover variations of Resin Infusion

– RTM - Resin Transfer Molding– RFI - Resin Film Infusion– VARTM - Vacuum Assisted Resin Transfer Molding

• Benefits– Labor reduction– Net part shape– Complex and integrated structures– Fastener elimination

Pressure

Resin

Heat

VacuumDry carbon preform

…… Challenge Challenge –– Aerospace quality resins are difficult to process via this methAerospace quality resins are difficult to process via this methodod

79

Technology—PRIFORM™ Resin Infusion

Technology Application Technology Application Convert complex, structural, bolted metal spoiler design to a fully integrated, bonded composite structure using resin infusion process

Benefits- 50 kg+ savings per ship- 22 bolts eliminated/part- No complex machining- Reduced assembly hours- Certified and in flight

Old Technology

New PRIFORM Technology

Cytec’s patented PRIFORMTM Technology Combines the Benefits of Engineered Textile Preforms and Resin Infusion Technology to enable customers to overcome these Limitations!

80

Out-of-Autoclave Processing

Traditional Aerospace ThermosetComposites Require High Pressure Autoclave Processing

Cytec “Out-of-autoclave”Technology Delivers Aerospace Performance With Simple Vacuum/Oven Cure process

– Based on Traditional Thermosetting Prepreg Materials or new Resin Infusion Materials

– Eliminates Need for Autoclave

– Opens Door for Manufacture of Much Larger Structures

– Reduces Customer Process Costs

…… Promising Technology for Emerging ApplicationsPromising Technology for Emerging Applications

81

Cosmetic Surfacing AdhesivesCompetitive ProductComposite parts usually require more

extensive “finishing processes” to achieve a high quality paintable surface

Cytec pioneered development of adhesive surfacing film technology to dramatically reduce these finishing costs

Next Generation SurfaceMasterTM

technology delivers step-change improvement in surface quality—further reducing customer processing costs

– Virtually eliminates surface imperfections– 50% improvement in surface quality versus

current generation products

…… SurfaceMasterSurfaceMaster™™ baselinedbaselined for many new programs including Boeing 787 for many new programs including Boeing 787

Cytec Surface Master Film

82

Boeing 787 Technology

Toughened resin-film-infusion material

Superior fatigue performance

Inherent flame/smoke and toxicity compliance

Fuselage Frames—Weight efficient, structure critical components

83

Boeing 787 Technology

Toughened resin-film-infusion material

Superior fatigue performance

Inherent flame/smoke and toxicity compliance

Fuselage Frames—Weight efficient, structure critical components

Rear Pressure Bulkhead—The first out-of-autoclave commercial airplane part for Boeing primary structure

60-80 lbs /ship set weight savings

Significantly Lower non-recurring and non-recurring costs

84

CEM—Supply Chain & Regional Growth• Capacity and capability expansions

– High-volume / best in class process variation prepreg line (EU)

– Best in class slit-tape capacity (U.S.)– Carbon fiber capacity expansions (U.S.) – Carbon Weaving– Key raw material supply

State of the Art Manufacturing CenterÖstringen, Germany

• Significant capital investment planned over the next five years

– Carbon Fiber Capacity– Process capabilities improvement—

focused on product consistency and variation

– Capacity expansion to support future platform growth—prepregs and adhesives

85

CEM—Supply Chain & Regional Growth• Capacity and capability expansions

– High-volume / best in class process variation prepreg line (EU)

– Best in class slit-tape capacity (U.S.)– Carbon fiber capacity expansions (U.S.) – Carbon Weaving– Key raw material supply

State of the Art Manufacturing CenterÖstringen, Germany

• Significant capital investment planned over the next five years

– Carbon Fiber Capacity– Process capabilities improvement—

focused on product consistency and variation

– Capacity expansion to support future platform growth—prepregs and adhesives

• Regional expansion to support a growing global customer base

– Commitment to a China manufacturing facility—site selected, formal project initiated 2007

Future China Manufacturing Site

86

Mission and Business Objectives

Business Objectives• Annual top line growth ~10%• 15% average annual earnings growth• Lay solid foundation for sustained new program growth in

the next decade

Mission

Cytec Engineered Materials will be a premier growth organization continuously creating value by providing innovative engineered material solutions for the most demanding applications.

87

Summary

Technology advancements and demand for “affordable performance” are rapidly accelerating the substitution of composites for metals

Secular trend towards increased composites use is occurring broadly across all high-performance market segments

Carbon fiber is a key material—from both a technology and supply position—Cytec is investing for the future

Cytec Engineered Materials is an industry leader and is well positioned to take advantage of this growth with robust, integrated technology solutions

88

… to create a new future!… to create a new future!

Breaking Through Barriers ...Breaking Through Barriers ...

89

Agenda

Jim Cronin – Executive Vice President and Chief Financial Officer

– Building Block Chemicals

– Income Taxes

– Capital Spending

– Balance Sheet

– Cash Flow

– EPS Wrap-Up

90

Major ProductsMajor ProductsAcrylonitrile Acrylic Fiber, ABS plastic, Kemira

Hydrocyanic Acid Degussa

Melamine Cytec Surface Specialties (1/3 of capacity)Merchant sales

Sulfuric Acid Degussa plus Merchant sales

Input CostsInput CostsPropylene AcrylonitrileAmmonia Acrylonitrile, MelamineNatural gas Energy

Building Block ChemicalsWellWell--run, world scale integrated operations focused on operational exrun, world scale integrated operations focused on operational excellence to take cellence to take advantage of market conditions and be cash positive in all econoadvantage of market conditions and be cash positive in all economic cycles. mic cycles.

2006 Sales M$339Operating Margin 5%

Market DynamicsMarket DynamicsAcrylonitrile Global capacity utilization looks to remain tight over next 2-3 years

Global demand increasing 2.5% per yearMelamine: Reductions in global capacity due to shutdowns in Europe and Asia

Regional demand; No. America and Europe +4%, China +10%, Latin America +6%

91

Income Taxes

2006 2007P

Effective Tax Rate* 26.8% 29.5 - 30.5%

2007 Forecast:

Tax rate for 2007 unfavorably influenced by the following factors -

• Water Treatment Chemicals and Acrylamide divestiture full year impact loss of

earnings in low or zero tax jurisdictions (+1.2%)

• Overall US/International earnings mix: Shift to higher taxed US earnings {approx.

50/50 for 2007 vs. 40/60 for 2006} (+0.9 to +1.6%)

• US law changes: 100% phase out of ETI benefits coupled with gradual phase in

(66%) of less desirable replacement regime (+0.6 to +0.9%)

* ”Normalized” rate

Focus Is On Efficient Cash Repatriation Globally, Simplification And LeveragingFocus Is On Efficient Cash Repatriation Globally, Simplification And Leveraging

92

Capital Spending By Business Segment

CPC - Max HT Mining Chemicals Expansion – Atequiza, MexicoAll-Site Safety Investments

CEM - Composites Plant – Shanghai, ChinaCEM - New Carbon Fiber Plant – Greenville, SCCEM - Refurbish Carbon Fiber Pilot Line – Greenville, SCCSS - Radcure Plant – Shanghai, ChinaCSS - Waterborne Resins – Wallingford, CT

Major Projects:

130-140103

62Other

1512Building Blocks (BB)

43-5334Cytec Engineered Materials (CEM)

4529Cytec Surface Specialties (CSS)

2126Cytec Performance Chemicals (CPC)

2007 Est.

2006 Actual$ Millions

Disciplined Capital Spending Focused On Growth Product LinesDisciplined Capital Spending Focused On Growth Product Lines

93

Leverage*

2.3

5.42.5

12

3.9

9.3

02468

101214

2005 2006 2007P

Total Debt to EBITDAEBITDA to Interest Expense

31%40%

27%18%

45%58%

10%20%30%40%50%60%70%

2005 2006 2007P

Funds from Operations to Total DebtTotal Debt to Capital

*Rating agency methodology.

Quick Improvement, Strong Balance Sheet, Investment Grade RatedQuick Improvement, Strong Balance Sheet, Investment Grade Rated

94

Pensions($ in millions)

$ 83$137Net Liability

(68)(78)Related Deferred Tax Asset

(664)(555)Less: Plan Assets

$815$770Accumulated Benefit Obligation

20062005

• Plans Are Adequately Funded• US Salaried Defined Benefit Plans Frozen As Of 12/31/07

• Plans Are Adequately Funded• US Salaried Defined Benefit Plans Frozen As Of 12/31/07

95

Postretirement Medical Benefits($ in millions)

Cytec Cash Contributions Averaged Approximately M$16 Per Year Over Last Two YearsCytec Cash Contributions Averaged Approximately M$16 Per Year Over Last Two Years

$106$101Net Liability on an Actuarial Basis

(68)(87)Related Deferred Tax Asset

(69)(70)Less: Plan Assets

$243$258Gross Actuarial Liability

20062005

96

Environmental Remediation ($ in millions)

$ 82$ 81Net Liability on Balance Sheet

(21)(22)Related Deferred Tax Asset

$103$103Accrual Balance

20062005

• Cash Outlays Are Stable And Averaging A Modest M$7 Over The Last Two Years• Active Real Estate Divestment Program

• Cash Outlays Are Stable And Averaging A Modest M$7 Over The Last Two Years• Active Real Estate Divestment Program

97

Contingent Liabilities - Update

• Asbestos• 61% decline in the number of claimants in 2006 vs. 2005

• Reserve balance at December 31, 2006 – M$55

– Reserved through the year 2049 (Stallard/Manton Decay Model)

– Detail update completed in 2006

– Insurance receivables equal about 55% of gross reserve

• Lead • Insurance policies expected to cover greater than 50% portion of defense

and indemnity costs, if any, for lead pigment property damage claims.

Pursuing additional coverage with the other carriers

• No reserve balance needed.

Excellent Legal Positions And Good, Stable Insurance Coverage Limits ExposureExcellent Legal Positions And Good, Stable Insurance Coverage Limits Exposure

98

Debt Composition As Of March 31, 2007

90%100%Total

25%2%Other

93%51%Euro Debt*

90%47%Dollar Debt*

Fixed Rate Portion Percent of Total Debt

51Five-year Revolver Due February 15, 2010

(In Millions)

$901Total Debt

50Other

2506.00% Notes Due October 1, 20152004.60% Notes Due July 1, 20132505.50% Notes Due October 1, 2010

$ 1006.75% Notes Due March 15, 2008

Debt after acquisition March 31, 2005

$1,780

* Including the impact of our euro/dollar cross currency swaps

Rapidly Paying Down Debt With Free Cash Flow And Divestiture ProceedsRapidly Paying Down Debt With Free Cash Flow And Divestiture Proceeds

99

0

100

200

300

400

'07 '08 '09 '10 '11 '12 '13 '14 '15 '16Year

Am

ount Outstanding

Long-Term Debt Maturities As of March 31, 2007

Five-yearRevolver -

Public Debt -

Can be prepaid with excess cash any time prior to maturity

Well Distributed Maturity ProfileWell Distributed Maturity Profile

In Millions

$

100

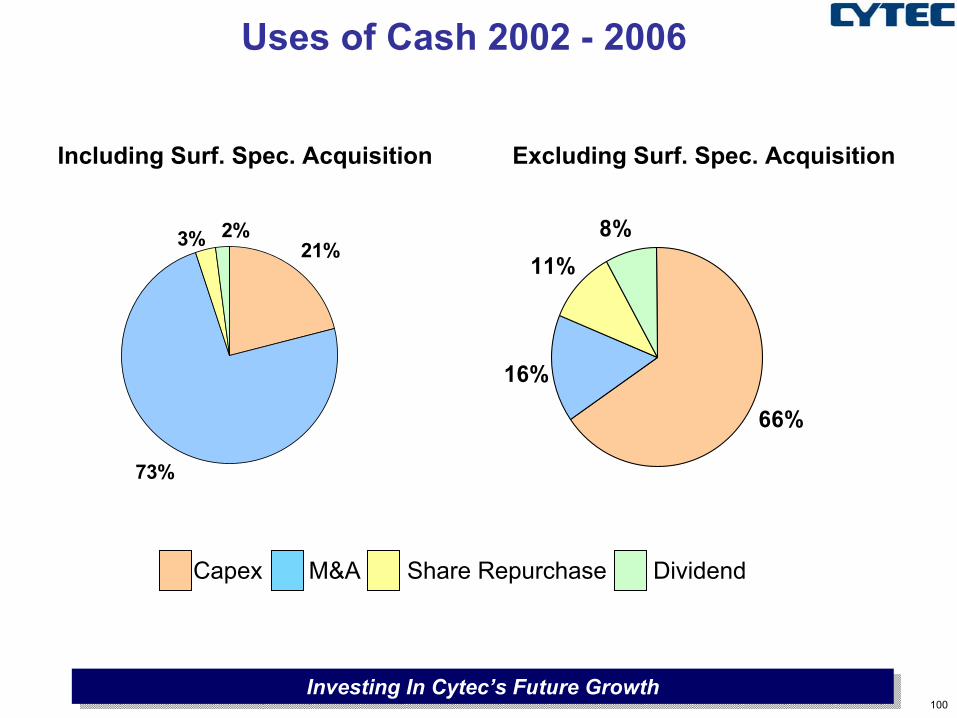

Uses of Cash 2002 - 2006

21%

73%

3% 2%

66%

16%

11%8%

Investing In Cytec’s Future GrowthInvesting In Cytec’s Future Growth

Including Surf. Spec. Acquisition Excluding Surf. Spec. Acquisition

Capex M&A Share Repurchase Dividend

101

Uses of Cash cont’d

Key points:• Good cash flow and balance sheet• Manageable liabilities• Uses of cash going forward:

• Maintenance of business capital• Capital projects to support the growth businesses• Pay down debt• Bolt-on acquisitions (stock buyback hurdle rate)• Stock buyback• Dividends

Our Financial Strength Let’s Us Consider All The Above Uses Of CashOur Financial Strength Let’s Us Consider All The Above Uses Of Cash

102

Cash Flow Statement($ in millions)

*including ($76) gain on sales of assets and ($73) net working capital**including ($16) gain on sale of assets and ($57) net working capital

$116$124Free Cash Flow

3245Options Exercised

(19)(19)Dividends

(130)(103)Capital Expenditures

$233$201Cash Flow from Operations

(107)**(147)*Working Capital and Other

142153Depreciation and Amortization

$198$195Net Income

2007P2006

103

Earnings Per Share 2004-2007

2004 2005 2006 2007P

Reported $2.96 $1.27 $4.01 N/A”Normalized” $3.03 $3.07 $3.45 3.60-3.80% Growth 31% 1% 12% 4%-10%

Successful Achievement of 2007 EPS Target Contingent Upon …..1. Execution of ….

Selling price initiatives exceeding the raw material cost increasesKeeping up with market growth and market share gainsSignificant cost and efficiency improvements at manufacturing locations

2. Keeping people motivated and innovative through turbulent times. Focus on the priorities.

Major Risks to the 2007 Plan ….1. Higher than plan raw material costs and raw material cost volatility caused by

shortages and spikes in oil prices2. Competition failing to raise or giving up price for share3. Regional recession

104

Technology ahead of its time

Cytec Industries Inc. (NYSE : CYT)

Investor Day Presentation

May 9, 2007

105

Reconciliation of “Non-GAAP” Measures to GAAP MeasuresManagement believes that net after-tax earnings and diluted earnings per share before special items, non-GAAP measures, are meaningful to investors because they provide a view of the Company with respect to ongoing operations. Special items represent significant charges or credits that are important to an understanding of the Company’s overall operating results in the periods presented. Such measurements are not recognized in accordance with generally accepted accounting principles (GAAP) and should not be viewed as an alternative to GAAP measures of performance.Full-Year 2004 “Non-GAAP” Diluted EPS $3.03

- Add back Reduction in Income Tax Provision 0.06- Add back Litigation Settlement Charge (0.12)- Add back Premium Paid to Redeem Preferred Stock (0.24)- Add back Settlement of Disputed Matters with Series C Holders (0.04)- Add back Settlements of Carbon Fiber Litigation Matters (0.15)- Add back Gains on anticipatory currency and interest rate hedging 0.42

Full-Year 2004 Reported Diluted EPS $2.96Full Year 2005 “Non-GAAP” Diluted EPS 3.07

- Add back purchase accounting charges for fair value of inventory in excess of normal manufacturing cost (0.33)- Add back write-off of in-process research and development costs of Surface Specialties (0.80)- Add back loss on currency and interest rate derivative transactions (0.60)- Add back anticipated settlement of a certain litigation matter (0.04)- Add back optional redemption of Mandatory Par Put Remarketed Securities (MOPPRS) prior to their maturity (0.30)- Add back income tax benefit reflecting favorable developments on of tax audits with respect to prior years returns 0.61- Add back restructuring costs (0.27)- Add back settlement to resolve a dispute over an environmental matter (0.07)- Add back Integration expenses related to acquired businesses (0.00)

Full Year 2005 Reported Diluted EPS 1.27Full Year 2006 “Non-GAAP” Diluted EPS $3.45

- Add back asset impairment charge 0.51- Add back net restructuring charge 0.33- Add back integration costs related to acquired business 0.03- Add back charge related to UK benefit plan change 0.04- Add back net charge related to contingent liability study/update 0.03- Add back gain relating to a certain legal dispute (0.26)- Add back gain on divestiture (1.23)- Add back income tax benefit related to completion of prior years audits (0.07)- Add back tax on capital reduction at an international subsidiary 0.04- Add back cumulative effect of accounting change 0.02

Full Year 2006 Reported Diluted EPS $4.01

Cytec Industries Inc.