technology - dmia.danareksaonline.com

TRANSCRIPT

Equity Research Technology

See important disclosure at the back of this report www.danareksa.com

Technology Thursday, 19 August 2021

OVERWEIGHT Oiling the flywheel

Foundations are in place with solid GMV in ecommerce despite ups and downs during Covid-19, and the sector is projected to grow due to attractively low penetration and favorable demographics. New start-ups and digital enablers empower merchants to sell more and add velocity to blooming ecosystems. Players venture expansion in new attractive markets to embed on their platforms. GMV growth offers the basis for positive profitability dynamics which can support the new expansion and add spin to one’s ecosystem flying wheel.

A new horizon by hitting capital markets. Internet players like GoTo, Bukalapak and Traveloka have laid the foundations with relatively quick market acquisitions in e-tailing commerce (C2C, B2C, B2B), transport, F&B, Media, and Travel. They hit the capital markets to seek funds and this signals a new horizon in our view, whereby players gather new ammunition, shareholder diversification, and room to forge business alliances. More penetration, digital enablers and new markets. In the new horizon, we expect greater e-tailing penetration from 21% by onboarding merchants and sellers in online platforms to drive larger GMV. Ridehailing and last-mile logistics will seek new geographic coverage in non-tier 1 cities and deeper penetration to support GMV growth. Moreover, logistic improvements will support the growth of e-groceries. We expect BNPL to support ecommerce and greater traction on fintech solutions. We also expect more virtual products and investment products such as mutual funds which are less than 1% in Indonesia. Digital penetration in Healthcare and education offer bundling prospects and tap attractive population segments. Gluing the ecosystem by nurturing brand awareness. Current competition requires an omnichannel presence, making an online marketplace, O2O inseparable at this point. Investments will continue to flow to improve the brand and platform awareness, improve its capabilities and security, drive personalization with Cloud data and AI to safeguard GMV market share. A competitive brand will incentivize merchants & UMKMs to onboard and stay with the platform. All-commerce with a focus on B2B and cost management. Ecommerce players lay more focus on merchants/agents to improve supply and enhance GMV by using O2O schemes. Quick wins can be realized with the supply of chain gains, cutting costs, while a) more same day deliveries b) access to merchants and consumer lending support turnover growth. Cloud computing & analytics, digital engagement and advertising should be more effective with larger penetration and more big data. This elaboration is crucial to drive consumer digital demand, which in return boosts the supply of products/services effectively adding velocity to ecosystem’s flying wheel. The flying wheel is an autonomous function, rendering cash burning less of a priority. GMV expansion with new coverage. GRAB ridehailing in SE Asia projects to soon be positive EBITDA, but we understand e-payments service are a financial drag, including Gojek as well, due to a lack of customer loyalty. But they are important in onboarding users to more sophisticated fintech services. Both injected capital to Linkaja with a view to support their digital campaigns in non tier 1 and ex-Java coverage expansion. We also understand that Covid-19 will offer lasting tailwinds for contactless activities. Lastly, though we believe social commerce has strong roots, more micro business will eventually be enticed to onboard more formal platforms. Initiate with Overweight. We start our coverage with Bukalapak, which addresses supply inefficiencies by empowering the end-seller, expecting to fuel GMV growth from the backbone of Indonesia’s society.

x Niko Margaronis

(62-21) 5091 4100 ext. 3512

2 www.danareksa.com See important disclosure at the back of this report

The low hanging fruits of Data Connectivity with online services saving customers money & precious time. Digital Internet companies offer efficiencies in the procurement and fulfilment of goods/services for the mass population. Marketing, Procurement, fulfilment, Transport/Delivery of goods and services is improved for the supplier while they can be now available on-demand for the consumer.

Ecommerce Mothership. The Ecommerce marketplace is the birthplace and mothership platform for internet companies while adjacent sectors can foster alongside on strong foundations.

Exhibit 2. Diagram: disruption creates value transfer and creation with platform integration

Source: BRI Danareksa Sekuritas

Value Transfer & Creation with platform

integration

Traditional Brick Mortar retail stores

O2O physical stores

Modern convenience stores. Mini markets are nimble for

expansion, sophisticated, penetrating dense areas

Warungs.Smaller than mini

markets, less sophisticated, very attractive footprint

Large brick mortar /Supermarkets

Most impacted from Covid19, adapt to

new economy

Traditional financial intermediaries

Threat from branchless banking, lower cost of funds

Travel agents Tend to be replaced by online

bookings (OTA). Disruption accelerated with Covid19

Transport OwnersPositively disrupted as

business vol grows, monetizing vehicles faster

Healthcare companiesModernization accelerated, more private investments and healthcare availability

Education systemOpportunities for diverse learning, and tap young

demographics

Ecommerce platforms & marketplaces

Fintech Platforms

Entertainment / social Platforms

Media Production houses Competition in Adex from

sophisticated SosMed, digital channels. Room for SVOD for

local content

Media aggregatorsCollect crème de la crème

content, and negotiate favorable terms

Last mile transport platforms

F&B sectorPositive overall impact on consumer experience, with elevation of food delivery

service & awareness

FMCG distributors / Wholesalers

Will continue being disrupted, as ecommerce

players exploit inefficiencies

On-demand food delivery

BRAND DISTRIBUTION CENTRE

BRAND/MANUFACTURER

GT DISTRIBUTOR

WHOLESALER

RETAILER / (Warung)

STREAMLINING DISTRIBUTION

3

www.danareksa.com See important disclosure at the back of this report

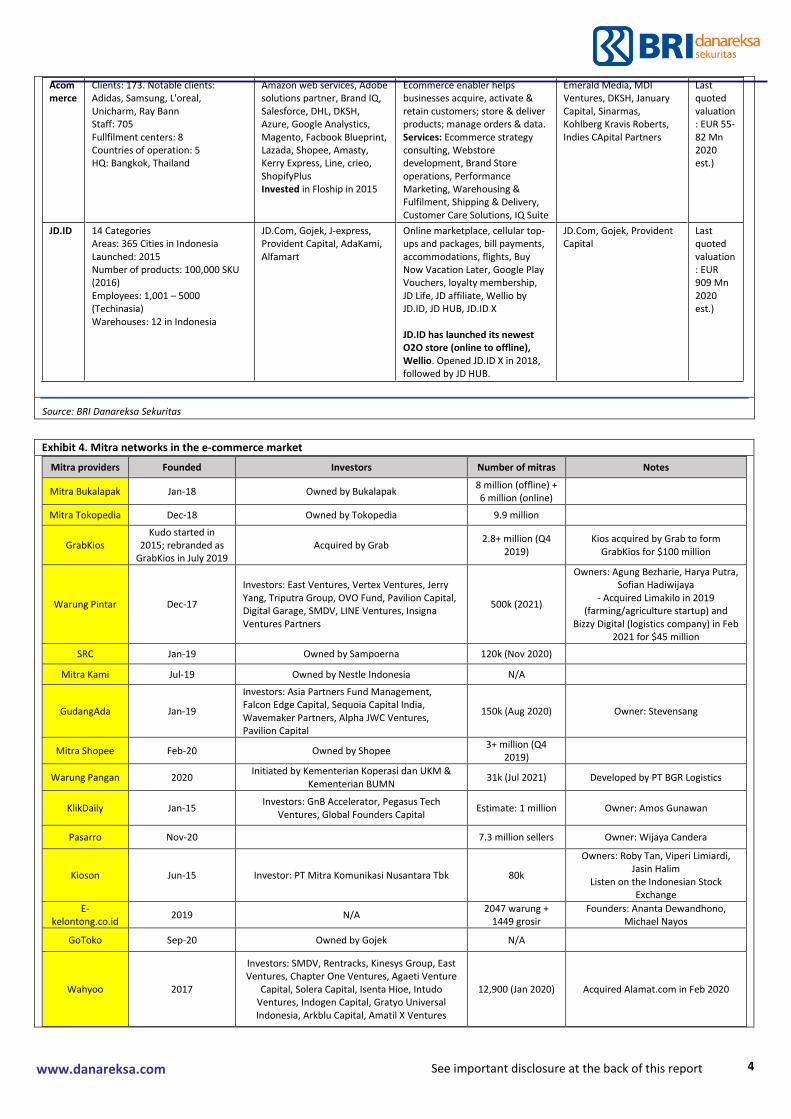

Exhibit 3. E-tailing core players

Comp General Info + Matrix Affiliations Features Key Shareholders Valuatio

n

Bukalapak

90 million users Average daily transactions: 2 million GMV: $4.93 bn (2020) TPV: Rp 4.29 bn (2020) Employees: 2000+ Launched: January 2010

FMCG: Unilever, Danone, CocaCola Amatil, Heinz ABC Indonesia, Garudafood, Suntory Garuda, UltraJaya Gaming: itemku Tech: Microsoft, Google Financial services: Standard Chartered Bank, Bank Mandiri, Bank BRI, Bank Syariah, DBS, Tanamduit Insurance: Igloo Singapore Groceries: HappyFresh Janio 6.9mn Mitra warungs

Online marketplace, blog, Cellular top-ups and packages, bill payments, investments, loans, transportation ticketing, social services. - Bukalapak listed on the Indonesian Stock Exchange on August 6th 2021, at a price of Rp 850 per share, for approx. Rp 21.9 trillion in proceeds.

PT Kreatif Media Karya (23.93%), API 9hong Kong) Investment Limited (13.05%), Archipelago Investment Pte. Ltd. (9.45%), Achmad Zaky Syaifudin (4.32%), Muhammad Fajrin Rasyid (2.64%), New Hope OCA Limited (3.16%). Batavia Incubator Pte. Ltd (2.47%), Mirae Asset-Naver Asia Growth Investment Pte. Ltd (1.80%), UBS AG, London Branch (1.86%), Willix Halim (1.40%), Others (37.32%)

Last quoted valuation: USD 5.95bn

Tokopedia

100 mn users GMV: $14 bn (2020) Employees: 4,700 (2019) Founded: 6 February 2009

Merged with Gojek, Tokio Marine Indonesia GroupM, Semangat Digital Bangsa, Hypermart, Matahari

Online marketplace, fintech and e-payment (digital wallet, investments, virtual credit card, insurance), Mitra Tokopedia virtual goods, Tokopedia Salam

Softbank (35.35%), Alibaba Group (28.25%), Radiant (10.6%), Sequoia India (8.05%), William Tanuwijaya (4.66%), Anderson Investments (3.28%), Leontinus Edison (1.9%), Google (1.64%), East Ventures (1.08%), DreamFund (1%)

Last valuation: USD 7.5 billion (before GoTo) USD 18 billion (after merger)

Blibli Number of users: 18.52 million Founded: 15 August 2011 Owner and founder: Djarum Country: Indonesia

DANA, Maybank Finance, garasi.id, Hypermart, BCA, Galeri Indonesia, Marriott Business Council Indonesia, OVO, Foodcycle, Pertamina, CARRO, Samsung, Monstore, Jangkau, Indodana, Walt Disney, Unilever, Central Department Store,

Online marketplace, Blibli Hasanah, Blibli Paylater, Blibli Mitra. In 2020 starts its 1st offline store Bliblimart Collaborated with BCA Digital to integrate Blibli with the digital banking application "Blu".

Djarum Group, GDP Ventures

N/A

Shopee

users: 93 million (2020) Avg. daily transactions: 2.8 million GMV: $14.2 bn (2020) Employees: 20,000+ Countries: Singapore, Malaysia, Indonesia, Thailand, Taiwan, Vietnam, Philippines, Mexico, Brazil, Chile, Colombia Founded: 5 February 2015

PGN, Pertagas, Badak LNG, Danone, Bank Syariah, Sekolah Ekspor, Snack Video, Kadin, SMESCO, Bank Mandiri, Pegadaian, Unilever, Abbott, Kickfest, Suzuki, Hypermart, Traveloka, JCB, J&T Express

Online marketplace, cellular package top-ups, bill payment, transportation ticketing, Shopee supermarket, Shopee Food - Integration of ShopeePay with QRIS will be beneficial to support MSME Shopee has in-house Logistics: Shopee Express

Subsidiary of Sea Group. Sea Group shareholders is Tencent: 39.7% Blue Dolphins Venture: 15% Forrest Li: 20% Gang Ye: 10%

Last quoted valuation: USD 120 billion - Sea Group

Lazada

Number of users: 30.52 million GMV: $4.5 bn (2020) Countries: Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam Founded: 27 March 2012 Owner: Alibaba Group Founders: Rocket Internet Employees: 10,000+

Grab, OVO, Telkomsel, Lion Parcel, UC Browser, IDexpress, Mastercard, Pakuwon Group Jakarta, Bhinneka, L'Oreal, GoSend, EVOS, Chilibeli, Taobao, JNE

Online marketplace, LazMall key strengths: e-commerce, technology, and logistics. Lazada has also partnered with the government in Kakak Asuh UMKM in attempt to provide a mentoring program for SMEs to digitalise.

Alibaba, Temasek Holdings, Verlinvest, Rocket Internet, Kinnnevik AB, Tesco, Access Industries, HV Capital, TEC Ventures, Summit Partners

Last quoted valuation: USD 3.15 Bn (2017)

GudangAda

Number of users: 300,000 (Jan 2021) GMV: $600 Mn (Jan 2021) NMV: $6 bn Countries: Indonesia (500 cities) Launched: January 2019 Founder: Stevensang Employees: 322 Merchants: 100,000+

Bank OCBC NISP - Online marketplace where wholesale and retail goods, specifically in FMCG, Point-of-sale system, order management, logistic tracking, and payments. - GudangAda partners with banks to provide working capital for SMEs, With their latest $100 million Series B funding to develop AI-based tools that can provide personalised recommendations for merchant customers.

Asia Partners Fund Management, Falcon Edge Capital, Sequoia Capital India, Wavemaker Partners, Pavilion Capital, Alpha JWC Ventures

$135.9 million

4

www.danareksa.com See important disclosure at the back of this report

Acommerce

Clients: 173. Notable clients: Adidas, Samsung, L'oreal, Unicharm, Ray Bann Staff: 705 Fullfilment centers: 8 Countries of operation: 5 HQ: Bangkok, Thailand

Amazon web services, Adobe solutions partner, Brand IQ, Salesforce, DHL, DKSH, Azure, Google Analystics, Magento, Facbook Blueprint, Lazada, Shopee, Amasty, Kerry Express, Line, crieo, ShopifyPlus Invested in Floship in 2015

Ecommerce enabler helps businesses acquire, activate & retain customers; store & deliver products; manage orders & data. Services: Ecommerce strategy consulting, Webstore development, Brand Store operations, Performance Marketing, Warehousing & Fulfilment, Shipping & Delivery, Customer Care Solutions, IQ Suite

Emerald Media, MDI Ventures, DKSH, January Capital, Sinarmas, Kohlberg Kravis Roberts, Indies CApital Partners

Last quoted valuation: EUR 55-82 Mn 2020 est.)

JD.ID 14 Categories Areas: 365 Cities in Indonesia Launched: 2015 Number of products: 100,000 SKU (2016) Employees: 1,001 – 5000 (Techinasia) Warehouses: 12 in Indonesia

JD.Com, Gojek, J-express, Provident Capital, AdaKami, Alfamart

Online marketplace, cellular top-ups and packages, bill payments, accommodations, flights, Buy Now Vacation Later, Google Play Vouchers, loyalty membership, JD Life, JD affiliate, Wellio by JD.ID, JD HUB, JD.ID X JD.ID has launched its newest O2O store (online to offline), Wellio. Opened JD.ID X in 2018, followed by JD HUB.

JD.Com, Gojek, Provident Capital

Last quoted valuation: EUR 909 Mn 2020 est.)

Source: BRI Danareksa Sekuritas

Exhibit 4. Mitra networks in the e-commerce market

Mitra providers Founded Investors Number of mitras Notes

Mitra Bukalapak Jan-18 Owned by Bukalapak 8 million (offline) + 6 million (online)

Mitra Tokopedia Dec-18 Owned by Tokopedia 9.9 million

GrabKios Kudo started in

2015; rebranded as GrabKios in July 2019

Acquired by Grab 2.8+ million (Q4

2019) Kios acquired by Grab to form

GrabKios for $100 million

Warung Pintar Dec-17

Investors: East Ventures, Vertex Ventures, Jerry Yang, Triputra Group, OVO Fund, Pavilion Capital, Digital Garage, SMDV, LINE Ventures, Insigna Ventures Partners

500k (2021)

Owners: Agung Bezharie, Harya Putra, Sofian Hadiwijaya

- Acquired Limakilo in 2019 (farming/agriculture startup) and

Bizzy Digital (logistics company) in Feb 2021 for $45 million

SRC Jan-19 Owned by Sampoerna 120k (Nov 2020)

Mitra Kami Jul-19 Owned by Nestle Indonesia N/A

GudangAda Jan-19

Investors: Asia Partners Fund Management, Falcon Edge Capital, Sequoia Capital India, Wavemaker Partners, Alpha JWC Ventures, Pavilion Capital

150k (Aug 2020) Owner: Stevensang

Mitra Shopee Feb-20 Owned by Shopee 3+ million (Q4

2019)

Warung Pangan 2020 Initiated by Kementerian Koperasi dan UKM &

Kementerian BUMN 31k (Jul 2021) Developed by PT BGR Logistics

KlikDaily Jan-15 Investors: GnB Accelerator, Pegasus Tech

Ventures, Global Founders Capital Estimate: 1 million Owner: Amos Gunawan

Pasarro Nov-20 7.3 million sellers Owner: Wijaya Candera

Kioson Jun-15 Investor: PT Mitra Komunikasi Nusantara Tbk 80k

Owners: Roby Tan, Viperi Limiardi, Jasin Halim

Listen on the Indonesian Stock Exchange

E-kelontong.co.id

2019 N/A 2047 warung +

1449 grosir Founders: Ananta Dewandhono,

Michael Nayos

GoToko Sep-20 Owned by Gojek N/A

Wahyoo 2017

Investors: SMDV, Rentracks, Kinesys Group, East Ventures, Chapter One Ventures, Agaeti Venture

Capital, Solera Capital, Isenta Hioe, Intudo Ventures, Indogen Capital, Gratyo Universal Indonesia, Arkblu Capital, Amatil X Ventures

12,900 (Jan 2020) Acquired Alamat.com in Feb 2020

5

www.danareksa.com See important disclosure at the back of this report

Ula 2019

Investors: Sequoia Capital India, Saison Capital, Quona Capital, Lightspeed India Partners, Willy

Arifin, Vaibhav Gupta, Sujeet Kumar, SMDV, Rohan Monga, Patrick Walujo, Alto Partners

Multi-Family Office, B Capital Group

25,000 (Apr 2021) Founders: Alan Wong, Derry Sakti,

Nipun Mehra, Riky Tenggara

Blibli Mitra 2019 Owned by Blibli 45,000 (Jul 2021)

Ralali.com Aug-13

Owner: Joseph Aditya Investors: East Ventures, Qualgro VC, CyberAgent

Capital, Beenos Partners, SBI Group, Digital Garage, AddVentures, TNB Aura, Arbor Ventures,

Jo Hirao

20k pemasok, 500k pembeli UMKM

(May 2021)

Indotrading.com 2012

Owner: Handy Chang Investors: Rebright Partners, OPT SEA, Golden

Gate, GMO VenturePartners, Convergence Ventures, aucfan Co., Ltd.

85k (Jun 2021)

Other initiatives: Djarum Retail Partnership (partnered with Mitra Blibli), Gudang Garam Strategic Partnership

Source: BRI Danareksa Sekuritas

We understand there will be competition of customers onboarding onto the formal market.

E-commerce has blossomed in Indonesia predominantly based on 2 key pillars. First is the social commerce that grew by riding on the proliferation of the social media. Sales of goods can be conducted with/without the support of sosmed/platform enabler that can save costs for the merchant.

Second, is the growth of horizontal internet players, the e-tailers who can provide online platform to conduct sales on a massive scale, selling volumes of the smallest to the largest value size items.

E-tailers have more localized focus, whilst social media can propagate effects of digital marketing better at this point in our view.

E-tailers have the innate ability to disrupt and raise the efficiency in retailing. This is possible thanks to their key assets of technology and human capital needed to continue innovate and improve their capabilities. In that respect, they appreciate the qualities of omnipresence in consumer experience and therefore seek partnerships via Online to Offline (O2O) with disrupted retailers who have relied on their physical stores as a point of sales to generate turnover till now. One key trait of brick mortars, is their unique prominent locations in dense areas that makes them attractive for showcasing goods. However we think they have also fulfilment capabilities that can be realized.

Most recent example, is when Gojek bought stake in Matahari Prima (MPPA IJ) recently. Moreover, Amazon has ~503 Whole Foods physical stores currently, and Alibaba runs 232 HEMA physical stores, while Americanas (AMER3 BZ) has 2,155 physical stores. Those are some examples that emulate a form of O2O to serve omnipresence objectives. We do not however expect Gojek owning significant stake in MPPA in near future, primarily based on the principles of sharing economy.

Exhibit 5a. E-tailing and Social commerce coexistence Exhibit 5b. Forms of Social Commerce

Source: McKinsey Source: Redseer

6

www.danareksa.com See important disclosure at the back of this report

Exhibit 5c. Traditional retailing moving to forms of e-commerce

Source: BRI Danareksa Sekuritas

The early digital foundations:

➢ Early tangible and quick wins on a mass scale: Internet companies have the upper hand sticking to core principles of sharing economy – light capex models without the commitment of a long capex cycle, making them resilient, adaptive while building sustainable ecosystems. Moreover, they have the ability to empower existing sector structures and practices, and onboarding them into new digital processes.

➢ The technology ecosystem is made possible thanks to improved data connectivity for on-demand services and platforms to flourish. This is a massive disruption in the way business sectors are affected across the board. E-commerce players create value by addressing several fulfilment innovations: a) last mile ridehailing & logistics and b) payment services. Data connectivity was a major factor in democratizing platform benefits to internet users on a mass scale. Moreover, on-demand service creates a new level of competition in the online consumer space.

➢ The sharing economy expands the reach and impact of platform economics. Unbundling the value chain process allows merchants, enterprises and even SMSEs theoretically to address and sell for all ticket size needs and for an unlimited number of users and unlimited use of the platform and interface without uncontrolled IT and marketing spending.

➢ With a sharing economy. IT budgets do not carry long periods of capex cycle either. The velocity to go to market is greater with a tech company. This further expands to entire society as it unlocks more value creation for every economic unit in the market.

Exhibit 6. Cost comparison of cloud computing and traditional hardware

Source: AWS Amazon Indonesia

Warungs, Mom & Pop stores

Distributors / Subdistributors

Supermarkets

Convenience stores:

Minimarkets

Wholesaler

E-commerce

Online Marketplace

Physical stores

Vertical playersE.g. Zalora &

Sephora

General Trade

Modern TradeBrick & mortar

Social CommerceSales made

through Social Media

Wholesale & Retail Trade (~64% of

MSMEs)

Warungs, Mom & Pop stores → O2O

Supermarkets → O2O

Minimarkets → O2O

Direct selling

Backend enablers

Community based selling

Influencer aided selling

7

www.danareksa.com See important disclosure at the back of this report

Transportation and Logistics sector; the key enabling ecosystem sector

Last mile businesses like ride-hailing so far works as a supporting function for ecommerce and other adjacent services. The controlling shareholder of UBER was forced to exit due to intense competition and challenging economics and was acquired by Grab.

We relay here the thoughts of our logistics analyst, Ignatius Prayoga The change of transportation has been rapid since the digitalization era, starting with online motorbike ride hailing. This national trend was started by Gojek followed by other transportation companies such as Grab and Uber. Then, these companies expanded their services to car ride hailing which ran head-to-head with transportation businesses in Indonesia, especially in Jakarta. More expansion to other businesses went more rapidly given integration of payment services to the business which taps more markets such as ecommerce, food and beverages, home services, shopping services and other initiatives, with the goal to be a SuperApp in Indonesia. We believe that vast service coverage of business that relies on transportation and a large number of ecosystem drivers will benefit start-ups.

Exhibit 6. Contribution of Gojek to Indonesia Economy in 2019 Exhibit 7. Gojek business coverage

Source: FE UI, BRIDS Source: Company, BRIDS

Digitalizing the transportation industry. In the past 6 years, we observed that transportation companies are making their way to digitalize their business to better reach their targeted customers, fleet optimalization and find optimum pricing schemes through an App. We see exponential growth of digital transportation use as it is affordable, easy to order and customize. As for the supply side, motorcycles have been a good choice since they are affordable and easy financing for the driver and more agile for short-medium distances. Furthermore, the partnership formed between digital transportation companies and the driver is relatively flexible so that the driver can work at their own pace. Currently, ride hailing services such as Gojek have 2mn partners while Grab has 2mn partners and is available in 167 cities across Indonesia. We think tapping the transportation sector is the key for creating an ecosystem that connects other means of businesses, especially for merchants.

Exhibit 8. Mostly use online transportation Exhibit 9. Gojek demand heatmap

0,0 20,0 40,0 60,0

Gopay SME Partner

Gosend social seller

SME outside Gojek Ecosystem

GoFood SME partner

GoCar

GoRide

IDR tn

51%46%

3%

Grab Gojek Others

8

www.danareksa.com See important disclosure at the back of this report

Source: APJII, BRIDS Source: Nielsen, BRIDS

Creating an ecosystem of customers and drivers. A digital transportation company now aims to be a super app that can serve all customers needs. Therefore, we think the prevailing company can reach customer engagement as much as possible by fulfilling their daily needs to maintain active use through an ecosystem. A digital transportation company is not only building a client base ecosystem but also the drivers. This large group of drivers is a great enabler to deliver many types of services to customers. Moreover, the initiative creates more job alternatives

Exhibit 10. Number of Gojek Drivers Exhibit 11. Gojek partner monthly income average, 2019

Source: FE UI, BRIDS Source: FE UI, BRIDS

Connecting merchants and customers instantly. As ecommerce has been showing rapid transaction growth in the past 5 years, digital transportation companies started to provide instant and same day services that allow customers to obtain purchased goods on the same day. The same initiative is also applied in food and beverage merchants which allows customers to get fresh meals right in front of the door. According to Nielsen Research, more people tend to purchase food from delivery platforms than dining in which indicates a new trend of ordering food, especially in urban areas. Furthermore, we notice a significant amount of new SMEs that operate in the food and beverage business. We think these initiatives improve SME capability to deliver their goods to customers. Besides instant transportation, food and beverage merchants can get more benefits from promotion in the platform which enables SME to grow rapidly, especially during the pandemic. According to research conducted by McKinsey, 34% of respondents used food ordering applications more often during the pandemic. Furthermore, 65% of Gojek respondents use Gofood more frequently compared to before the pandemic. A report from Momentum Works suggests that Food delivery platforms reach GMV of USD 3.7bn in 2020 with 53% of market share dominated by Grab food and the rest by Gojek.

Exhibit 12. Food delivery market share in Indonesia in 2020 Exhibit 13. Food and beverage order method in a week

Source: Momentum Works Source: Nielsen, BRIDS

-

0,50

1,00

1,50

2,00

2,50

3,00

2015 2016 2017 2018 2019 2020

Mn

Dri

vers

0,01,02,03,04,05,06,07,0

No

n-

Jab

od

etab

ek

Jab

od

etab

ek

No

n-

Jab

od

etab

ek

Jab

od

etab

ek

No

n-

Jab

od

etab

ek

Jab

od

etab

ek

Go-Ride Go-Car Go-Life

IDR

Mn

/mo

nth

1,96 1,74

Gojek Grab food

0 0,5 1 1,5 2 2,5 3

Phonecall

Takeaway through restaurant…

Takeaway with phone order

Dining in

Takeaway

F&B app (GoFood, GrabFood, etc)

Times per week (x/week)

9

www.danareksa.com See important disclosure at the back of this report

Ecommerce boom – Logistics sector game changer. As Ecommerce improves rapidly in Indonesia, the demand for fast and cheap delivery service increases significantly. Last year, the total parcels served from digital orders reached ~5mn parcels based on several logistics company estimates and BI digital payment. Furthermore, the pandemic changed the playing field whereby people changed the mode of transaction to online. According to Gojek, ecommerce delivery increased by 42%yoy during Lebaran. Meanwhile, Anteraja’s parcels per day delivered grew by 2x in Jun21 vs Mar21 even in the pandemic. This resilient growth shows a strong correlation between ecommerce growth and expedition growth in the new economy.

Consolidation and alliances are starting to form. As competition gets tougher, more alliances and consolidation are seen in transportation services. For example, Blue Bird put its services on the Gojek platform to boost orders and awareness. On the other hand, Gocar, a car ride hailing business from Gojek, needs more cars to fulfil customers’ orders. Furthermore, Anteraja is now collaborating with Gojek and Grab to improve its last-mile delivery service which involves developing an ecosystem to improve services to customers. Ecommerce platform starts to build its own fulfilment center. To ensure the deliverables of goods and seizing opportunity in the logistics industry, several ecommerce companies are establishing their own delivery services. For example, Shopee formed Shopee express that integrates its automated warehouses and delivery service. We also observed several retailers already utilize this service and third-party fulfilment service which may cut their logistics costs. Several independent fulfilment companies are seen to be operational offering a wide range of additional services such as an order and chat management system, quality control service, inventory and packaging management system, return service and many others. Ecommerce companies can incorporate delivery fees to merchandise prices and state zero delivery fees which might be a threat to other logistics companies. This marks the need to expand to other businesses such as C2C and serve other start-ups.

Exhibit 16. Fulfillment service diagram Exhibit 17. Independent fulfillment company in Indonesia

Exhibit 14. Ecommerce delivery method in Jakarta, 2019 Exhibit 15. Anteraja’s parcels per day growth

Source: BPS DKI Jakarta, BRIDS Source: Company, BRIDS

Online courrier

31%

Post Mail23%

Direct delivery by

seller22%

Pick up in designated

area22%

Others2%

10

www.danareksa.com See important disclosure at the back of this report

Source: BigCommerce Source: Google first page, BRIDS

Light assets and operational excellence are keys with archipelago characteristics in Indonesia. The Indonesian region comprises of scattered islands, although most economic activity is still centralized in Java. The existence of ecommerce and expansion of cellular signals has enabled SME across regions to participate in the market which increased the need for the availability of delivery in particular regions. Therefore, logistics companies should have wide coverage and systems that are reliable enough to meet client expectations. We think that logistics companies that have the lightest assets and can maintain operational excellence will be best placed to seize the opportunities. Price competition can be intensified. Like what we have seen in the telco and transportation industry, services of the same quality will lead to a price war. This may also be the case for logistics companies. Currently, capital is being burned to promote delivery services to build the customer base of logistics companies in ecommerce platforms through free of charge services or discounts. However, we think customers may not be loyal to certain companies as they are elastic to the price changes. As such, we think the logistics company that can survive this imminent challenge is a company that is able to maintain its operation quality such as service punctuality, safety of the goods and reasonable price. According to interviews with several logistics companies, Indonesia still needs more delivery capacity to meet ecommerce’s rapid demand. More coverage expansion and new players are needed to serve this developing new economy. Thus, we think that the price war would not happen in the short term, as the industry is still developing.

Exhibit 19. Delivery fee comparison

Source: Ecommerce platforms, BRIDS

Jakarta utara to Jakarta Selatan Bandung to Jakarta Selatan

Instant Nextday Next day Kargo

Grab Express 74,000 Sicepat 13,000 Sicepat 20,000 Sicepat 30,000

GoSend 71,000 AnterAja 13,000 Anteraja 15,000 Rex 27,500

JNE 18,000 JNE 30,000

Same Day Reguler

Anter aja 15,000 Anteraja 10,000 Reguler Ekonomi

Sicepat 10,000 Anteraja 11,000 JNE 10,000

Lion Parcel 9,000 Sicepat 14,000 Wahana 5,000

J&T 15,000 Sicepat 9,000

JNE 12,000

TIKI 11,000

Pos Indonesia 11,000

*Goods delivered: A box of mask Lion Parcel 10,800

Exhibit 18. Destination of delivery based on island

Source: BPS 2020, BRIDS

11

www.danareksa.com See important disclosure at the back of this report

Exhibit 20. Ride Hailing & Logistic Market

Comp.

General Info Affiliations Features Shareholders Valuatio

n

Gojek On-demand

No. Users: 170 Mn (2021) GMV: USD 12 Bn (2020) Cities: 200+ Founding year: 2010 HQ: Jakarta, Indonesia Drivers: 2 Mn + (2021) GTV: USD 12 Bn (2020, Dailysocial)

Tokopedia, Moka, Midtrans, AirAsia, ARTO, WePay, AirCTO, Coins.ph, LinkAja, SafebvPoda, JD.ID, Escapex, ZULU, T RUMA, Kartuku, LOKET, PasarPolis, KitaBisa, Doogether, alodoc, Pluang, Kumparan, Zenius, MainGame.com, Leftshift Technologies, MOOA, Blue Bird, 900k+ merchants

Transport & logistics: GoRide, GoCar, GoSend, GoBox, GoBlueBird, gosend, GoBox, GoTransit Food delivery and shopping: Gofood, Goshop, Gomart Health: Gomed Payments: GoPulsa, GoNearby, GoTagihan, GoInvestasi, GoPayLater News & Entertainment: GoTix, GoPlay Business: Moka, GoBiz, MidTrans, GoStore - Gojek exited Thailand, enabling Gojek to increase investments in its Vietnam and Singapore operations.

Telkomsel, PayPal, Facebook, Cool Japan Fund, Visa Ventures, Mitsubishi UFJ LEase & Finance, Mitsubishi Motors, Mitsubishi Corporation, AIA Group, SCB 10X, Astra International, Provident Capital Partners, JD.com, Google, Tencent Holdings, Google for Startups Accelerator, Allianz X, Warburg Pincus, BlackRock, Temasek, Samsung Ventures, Blibli.com, Via-AD, Meituan Dianping, KKR, DST GLobal, Farralon Capital, Formation Group, Sequoia Cap. India, Northstar, Capital Group Companies, Rakuten Ventures,

USD 5.3 Bn Last quoted valuation: USD 10.5 Bn (2020)

Grab On-demand

No. Users: 187 Mn (2021) Adjusted Net rev: USD 1.6 Bn (2020) GMV: USD 12.5 Bn (2020); estimated to grow by 40% CAGR to USD 34.2 Bn in 2023 Cities: 400+ Founded year: 2012 HQ: Singapore

OVO, EMTK, LinkAja, NinjaVan, StickEarn, Splyt, OYO, Moca, Bento, iKaaZ, Kudo and 2 Mn merchants

Deliveries: GrabExpress, GrabFood, GrabKitchen, GrabMart Mobility: GrabCar, GrabBike, GrabShare Financial Services: GrabPay (OVO), GrabFinance, GrabInsure, GrabInvest Enterprise and others: GrabAds, GrabDefence Matrix as reported on investor presentation for SPAC listing in the US: Deliveries: USD 5.5 Bn 2020 GMV, 203% CAGR 2018--2020 GMV Mobility: USD 3.2 Bn 2020 GMV, 37% CAGR 2020-2020E GMV Financial Services: USD 8.9 Bn 2020 TPV, 102% CAGR 2018-2020 TPV

Signite Partners, STIC Investments, TIS INTEC Group, Mitsubishi UFJ Financial Group, Invesco, Experian Ventures, Softbank Group, Tokyo Century Corporation, Microsoft, Kaskornbank, Booking Holdings, Kia Motors Company, Hyundai Motor Company, Yamaha Motor Ventures, All-Stars Investment, Lightspeed Venture Partners, Sino-Rock Investment Management, Mirae Asset Financial Group, Macquairie Capital, Oppenheimer Funds, Ping An Capital, Vulcan Capital, Finch Capital, HSBC, Toyota, Uber, SK Group, Didi Chuxing, Emtek Group, Honda Motor Co., China Investment Corporation, Coatue Management, 500 Accelerator, Qunar, Hillhouse Capital management, Vertex Ventures SE Asia, GGV Capital, Tiger Global Management, 500 Startups.

USD 11.856 Bn Last quoted valuation: USD 39.55 Bn (2020)

J&T 3PL

J&T operates in Indonesia, Philippines, Singapore, Cambodia Founded: 2015 HQ: Jak, Indonesia 100 gateway centers 4000 operating points 30,000 Employees 8,000 vehicles, 10,000 collection points

Crewdible, Titipaja, Shipper, This Is April, CuMart, Jet Commerce, PT ACT Technology, Oppo, SHopee, Tokopedia, Bukalapak, Hijabenka, Berrybenka, Datascrip, Sunchila, Janio, ShopeePay, Trigana Air

EZ: 2-3 days delivery Eco: 5-14 days delivery, to Sumatra, Kalimantan, Sulawesi, Bali J&T Super: 1-2 days delivery, covering JABODATABEK - J&T received USD 2 Bn from a private equity round led by Boyu Capital. to have its IPO in the US, potentially raising USD 1 Bn. - Started its airline cargo operations, and is expanding overseas. covid-19 tailwinds. Reported to generate 70% of its business comes from foreign markets.

Private Equity Rounds: Sequoia Capital China, Boyu Capital, Hillhouse Capital Group

USD 2.2Bn Last quoted valuation: USD 7.8 Bn (May 2021, CB Insights)

12

www.danareksa.com See important disclosure at the back of this report

SiCepat 3PL

730 locations in Indonesia Founding year: 2014

Tokopedia, Shopee, Bukalapak, Blibli, Jakmall, Zalora, Zilingo, Heavenlights, Even white, Lights. cio, Macadamia house, Klamby, Mayoutfut, Feulis, Ocla, Vanilla Hijab, Male, Kami., Livehaf, Metamorv, Dompet Dhuafa, Alfamart, Volta Indonesia, DigiResto, MCAS Comments: Launch DigiResto, a food delivery chat system and SiCepat Drop Points with MCAS, a parcel drop point solution system. With 940+ parcel drop points.

SiUntung: 15 hour shipping for JABODATABEK and Bandung BestL 1 day shipping for all big cities in Indonesia Gokil: 1-3 day shipping, min 10 kg, for all big cities in Indonesia Halu: Starting from IDR 5,ooo, 1-3 day shipping, for all big cities in Indonesia COD: Cash on Delivery for E-commerce purchases, 8 hour shipping for JABODATABEK, Bandung, Yogyakarta, Solo, Semarang, Surabaya SiCepat Syariah: 2.5% of of shipping fee is donated through Dompet Dhuafa, for non-marketplace transactions H3LO: 1-3 day shipping, discounted price SiCepat Go!: International shipping from JABODATABEK, Bandung, Yogya, Semarang, Surabaya, Denpasar, Medan, Makassar, Max. 30 Kg SiCepat Klik: Tracking system

SeriesB: Indies Capital Partners, Trihill Capital, Falcon House Partners, Daiwa Securities Group, KFF DEG, Pavilion Capital, Kejora Capital, MDI Ventures Funding rounds: Series B: USD 220 Mn led by Falcon House Partners and MDI Ventures Series A: USD 50 Mn led by Barito Teknologi and Kejora Capital Seed round: USD 3.5 Mn led by Kejora Capital

Last quoted valuation: USD 744 Mn (2021)

Waersix 3PL

Cities: 211 Trucks: 50,339 Warehouses: 418 (available in 34 provinces, 100 cities) Founded: 2017 HQ: Jakarta, Indonesia

Indofood, American Standard, Unilver, Wilmar, Orarg Tua, Nutrifood, Softex Ineondesia, PP Construction, Hexindo, SCG, Suntory Trukita

Transport Warehousing Comments: Waresix expands the first-mile logistic, to complete its mid-mile logistic segment. Waresix opens new transportation routes to improve Indonesian archipelago network. Acquired Trukita along with its 10,000 trucks.

MDI Ventures, EV Growth, Jungle Ventures, East Ventures, Monk’s Hill Ventures, Redbadge Pacific, Softbank Ventures Asia, Pavilion Capital, Emtek Group

USD 129 Mn

Kargo 98% Fulfilment rate. 8,000++ Total shipper 6,000++ trucks 10,000 users 50,000 ++ truck partners

Danone, PT Amerta Indah Otsuka, Metrox Group, Bukuanmurah.id, Coca-Cola Amatil, ABC Heinz, Shopee, Nutrifood, tpsfood, CFC, Bungasari Flour mills, 3PE

Shipping, Financing for vendors (allow vendors to receive payment within 3-5 working days deducted with a facility fee/interest ) .

10100 Fund, Coca-Cola Amatil Indonesia, Sequoia Capital India, Tenaya Capital, Convergence Ventures, Southeast Asian Fund, Alter Global, AC Ventures, January Capital, Agaeti Ventures, Zhen Fund, Innocen Capital, Intudo Ventures, ATM Capital

Last quoted valuation: EUR 113-169 Mn

Purpose of use the funds was altered due to Covid19. funds as a relief fund for its trucking partners so that they can survive financially util company operations return to pre pandemic figures. In addition, the company plans to invest its funds for infrastructure and technology improvement, as well as increasing its workforce with local talents

Shipper

161 warehouses network: 30 cities 25,000 sellers/users (2019) 10 fulfilment centers across Indonesia (2019) Shipper is a shipping & warehousing aggregator

Grab, DPEX, SiCepat Expressm J&T Express, Lion Parcel, GoSend, Indah Lagistic Cargo, SAP Express Center, Alfatrex, Ninja Express, Tiki, Wahana, WooCommerce Plugin, Magento, PORTER, Pakde, JNE, POS Indonesia, Grab Express

Shipping Aggregator (concierge) Warehousing rentals API Integration (Business to shipping/warehousing integration) (2020) series B funding to develop technology and expand its logistics network. Acquired Pakde, - warehousing solutions company, and Porter, local delivery startup so Shipper can process shipping orders themselves.

Prosus Ventures, Insigna Ventures Partners, Floodgate, AC Ventures, DST Global, Y Incubator, Sequoia Capital India, Lightspeed Venture Partners

Last quoted valuation: EUR 229-344 Mn (dealroom Apr 2021)

Ritase 50+ Enterprise Shippers 500+ transporters 6,500+ trucks 7,000+ drivers

Nestlte, Unilever, Japfa, Lotte, NPCT1, Prima Jaya Motor

Transporter, Shipper, Ritshop (trucking marketplace collaboration with Prima Jaya Motor), and retail deliveries. Comments: Expanded to Singapore in 2019. Future expansion plan into ASEAN network, with priority to Malaysia, Philippines or Thailand. Focus on FMCG industry in Singapore. New product, RitSea, to focus on maritime transportation. work together with Tanjung Priok Terminal (NPCT1) to digitize an integrated trucking haulage system with the port.

ZWC Partners, Insignia Ventures Partners, JAFCO Asia, Skystar Capital, Golden Gate, Patrick Cheung, Mitsubishi Corporation, Pegasus Tech Ventures, BEENEXT Funding rounds: Seed Round: USD 3Mn led by Insigna Ventures Partners Corporate round: USD 1.6 Mn Series A: USD 8.5 Mn led by Golden Gate

USD 13.1 Mn Last quoted valuation: EUR 11-16 Mn (Dealroom Sep 2018 est.)

Logisly

40,000+ trucks Focus on B2B 1,000 businesses customers (2020) 300 corporate shippers (2020)

JD.ID, Grab, Unilever, Haier, P&G, KINO, OT, Sinar Meadow, Modena, HERO, J-express, DHL, Tanuhub, Marriott, Kraft Heinz, National Logistic Ecosystem

Transporter and Shipper services. Provides financing to partnered transporters.

Monk's Hill Ventures, SeedPlus, Convergence Ventures, Genesia Ventures

Last valuation: EUR 22-33 Mn (Dealroom Nov 2020)

13

www.danareksa.com See important disclosure at the back of this report

Comments: Aims to optimize efficiency in the trucking industry, as they report that only 40% of trucks are utilized in Indonesia. Plans to increase transporter partners to 1,000 transporters. And expand and acquire 1,000 shipper (customers) partners. - 2019 In 2021, partnered with Bank Jago to provide financing for Logisly vendors. This will help Logisly increase its available capital for working capital purposes and enable the company to receive more orders. Eximku (Andalin)

95% fullfilment rate Connected to 100+ ports worldwide

Clients: Krispy Kreme, Agung Sedayu Group, Hitachi, Calmic, Indah Kiat, Indoexim, Lion, Wings, Dermapack, Electrolux, Indo Kemika Group, Ferro, GD group, etc.

Air Cargo & Air Courier, Ocean FCL & LCL, Project Shipment, customers Clearance, Alibaba Gold Supplier (Alibaba partnerships for businesses) Focuses on import and export activities. To boost its GMV to USD 100 Mn by 2021 (Techinasia).

BRI Ventures, BEENEXT, Access Ventures, ATM Capital, Mountain Partners, Ideabox Ventures

Last valuation: EUR 4-5 Mn (Dealroom oct 2020)

Crewdible Warehousing

Charges 3.5% transaction fee (Rp 10,000 Max), and other fees depending on package 100 warehouses (2019, warta ekonomi) 3,000 SME partners (2020, tribunnews)

Koinworks: partnership to provide financing to customers - GudGadget,

Bangekeles.com, Ealllaluna, Leinsjenkins, - Warehouse (whs)

partners: AGM Fullfiment Center, BEST Whs, Weikenn WHs, Citra Whs, Duri Utara Whs, JB Whs, Junior Persada, Gudang Industries Label, Whs Dutamas, Gravity Whs, etc.

- Integrated storage and warehousing facility: provides inventory mgmt, sales report, packaging, return mgmt - SME inventory and storage mgmt. - Introduced micro cold storage facility, which includes freezers, chillers, and cold room storages to customers. Aims to expand this service into 200 points in Indonesia. - Received a USD 1.5 Mn funding from Global Founders Capital. Funds to be used to expand its presence in big cities in Indonesia. Aims to expand operations to be able to complete 20k to 100k transactions per month.

Global Founders Capital USD 1.5 Mn Last quoted valuation: EUR 508 Mn (dealroom oct 2020 est.)

SAP Express Satria Antaran Prima

204 branches (2020) 600 hubs (2020) Fleet: 138 blind van, 43 CDE, 25 CDD, 120 others (2020) No. couriers: 2010 No. of deliveries: 21,747,557 Shipment volume (kg): 33,291,033 Founded in 2014

notable customers: BBCA, Berry Benka, BBNI, BTPN, Dirjen Bea dan Cukai, DJP, Herbalife Nutrition, HMSP, Indofood, JD.ID, LAzada, Lotte, BMRI, Matahari, Bank Mega, Pertamina Patra Niaga, Sophie, UNVR, Zalora, Zilingo

City and Domestic Couriers, International Express Shipping and Cargo, Waerhouse Management, Mailroom Management Service, Ecommerce, Land transportation, Ocean and Air Cargo, Dedicated Courier, Last mile delivery, retail agent, expeditions, Wood Packaging. First logistic company that Launch COD feature. Payment can be completed with QRIS technology.

In 2018, SAP Express went public. 62% of the funds to pay debt, while 38% working capital. Budiyanto Darmastono (47.76%) Gdex Sea Sdn Bhd (18,00%) Gd Express Carier Bhd (16,50%) Gd Valuegard Sdn Bhd (10,00%) Public (7,74%)

Last quoted valuation: Market Cap IDR 891.666 Bn

PAXEL On-demand

Users: 1.7 Mn+ Completed Deliveries 8.5mn+

1.4 Mn + partnered UMKM (Kontan)

Sameday delivery, PaxelBox, PaxelMarket, PaxelBig, Instant Delivery Targets to expand partnership with UMKM to 2Mn partnerships. Also plans to add more lockets nationwide.

Johari Zein, Susquehanna International (SIG), East Ventures, SMDV, MDI Ventures, Centauri Fund

USD 17 Mn+

Lockets: 230 (2020, katadata) Couriers: 1.5 K couriers (2019, techinasia) Area: JABODETABEK, Cikarang, Cimahi, Bandung, Cirebon, Tasikmalaya, Purwokerto, Yogyakarta, Magelang, Solo, Semarang, Ngawi, Sidoarjo, Jember, Madiun, Kediri, Surabaya, Malang, Banyuwangi, Denpasar, Makassar, Medan

Ninja Express 3PL

Part of Ninja Van (HQ in Singapore) Customers: 88Mn+ Coverage: SouthEast Asia Deliveries: 1.5Mn + deliveries per day

NinjaVan Lazada, Fank.co.th, Bukalpak, Chilindo, Sendo.vn, Shopee, Tokopedia, UNVR, Zalora

Last mile deliveries, COD, pick up at drop-off points. Lite account: up to 125 parcels per month. Prepaid. Pro Account: up to 125 parcels per month. Postpaid service. receive dedicated account manager, API and Webhook management, schedule pick ups. Comments: Focuses on providing last ile delivery services for businesses: Enterprises, small businesses, and social media seller, etc.

DPD Group, Grab, Geopost, Golden Gate, Intouch Holdings PCL, B Capital Group, Carmenta Capital management, Bangkok Bank, Zamrud Sovereign Wealth Fund

Last quoted valuation: EUR 682 Mn - Ninja Van (Dealroom May 2020 Est.)

Anteraja

Founded: 2019 ASSA Same day, Next day, & regular deliveries Adi Sarana Armada (ASSA) N/A

Availability: Java, Bali, Nusa Tenggara, Sumatra, Kalimantan, Sulawesi, Papua Couriers: 5k+ (2020), Locations: 600 points

Lalamove

Drivers: 80K drivers Partners: 5K business partners

Notable customers: Re Juve, EdenFarm, Printerous, MOKA

Courier service, COD, multi stop delivery Sequoia Capital China, Hillhouse Capital Group, Virtruvian Partners, D1 Capital Partners, Boyu Capital, Tiger Fund

Lastvaluation: EUR 9.1 Bn Jan2021

Source: BRI Danareksa Sekuritas

14

www.danareksa.com See important disclosure at the back of this report

Exhibit 21. Ride Hailing market shares in SE Asia

Source: TechinAsia

Exhibit 22. Fare relationship between distance and margin gain

Source: Bloomberg Intelligence

The entertainment sector; creating more attachment

Content and entertainment (OTT, gaming, education) itself sees its own secular online growth, with the sunrise of linear TV inevitably due. Linear TV predominantly focuses on FMCG products advertising. With the use of Short Videos, on-demand content - video, music, gaming, educational content and even OTT - advertising expenditure is more efficient and targeted. The Indonesian population is fairly young with solid millennials & younger generation groups.

Moreover, ecommerce fuels digital advertising resilience. This is a two way street with digital social and search advertising fuelling GMV. Cloud analytics can drive precise targeted advertising and create advantages.

➢ The ability for online content to engage is greater, and able to build distinctively separate ecosystems among viewers. Scale is developed with freemium models and where providers can monetize content based on 2 distinct models; advertising and subscription based. We believe content production costs can be contained, as media houses and apps source more content from uploaders and influencers and look for talent who can enrich the experience of viewers.

15

www.danareksa.com See important disclosure at the back of this report

Exhibit 23. OTT & Gaming Market players

Comp General Info Affiliations Features Key Shareholders Valuation

Vidio.com

No. of users: 1.1 million (subscribed) per Jan 2021. Founded: October 2014. Operating Region: Indonesia. HQ: Jakarta, Indonesia.

PT XL Axiata Tbk Series, Movies & Entertainment Shows, Sports Shows, International TV, Watch Ad-free

PT Surya Citra Media Tbk (SCMA) - 99.99%

N/A

Disney+ Hotstar

No. of users: 2.5 million (subscribed) per Feb 2021. Founded: February 2015, Acquired by Disney in 2019; integrates with Disney+. Launch in Indonesia: September 2020; Telkomsel as Release Partner. Operating Region: India, Indonesia, Malaysia, Thailand. HQ: India

Telkomsel TV Shows and Movies available in English and Regional languages, Seamless Video Playback, Smart Search, Friendly User Interface, Hot Content Catalogue, Accessible on Google Play and Apple App Store.

Novi Digital Entertainment Private Limited

N/A

Amazon Prime

No. of users: 200 million+ (subscribed) as of Jan 2021. Founded: April 2005. HQ: Seattle, Washington, USA. Operating Countries: Austria, Australia, Belgium, Brazil, Canada, China, France, Germany, India, Italy, Japan, Luxembourg, Mexico, Netherlands, Saudi Arabia, Singapore, Spain, Turkey, UK, USA.

SHOWTIME, STARZ, A+E Network, AMC, Gaia, RLJ Entertainment, DramaFever, Tribeca Short List, Cinedigm, Smithsonian, IndieFlix, Curiosity Stream, Qello, FlixFling, BroadbandTV, DEFY Media, Gravitas, Ring TV Boxing.

Prime Early Access, Prime Exclusive Deals, Day Exclusive Deals, Unlimited video streaming of latest movies, award winning Amazon originals and TV shows from India and around the world, Unlimited, ad-free access to playlists, stations, and millions of songs and albums at no additional cost.

Amazon.com Inc: Mutual fund holders (32.33%), Other institutional (26.64%), Individual Stakeholders (10.88%).

N/A

Viu No. of users: 45 million monthly active users (2020). 1.5 million subscribers in Indonesia (2021) CAGR: 26% over next 3 years. Launched: Oct.2015. HQ: Hong Kong. Operates in : Hong Kong, India, Singapore, Malaysia, Thailand, Philippines, UAE, Bahrain, Egypt, Indonesia, Jordan, Kuwait, Oman, Qatar, Saudi Arabia, Myanmar, South Africa.

Mediacorp, GMM Grammy (One 31 Channel, GMM 25)

Unlimited Downloads, Access to all dramas, variety shows, movies and kids animation, TV access via TV app or casting, Full HD (1080p), No video ads.

PCCW Media (Controlling Shareholder). Foxconn Ventures, Hony Capital, Temasek Holdings (18

N/A

HBO No. of users: 41.5 million subscribers in the US (2020) Founded: 1972. HQ: New York City, USA. Operating Region: Licensed in 150 countries.

AT&T, DIRECTV, Spectrum, Hulu, YouTube TV, Apple TV, Google Play

Stream HBO Original Series, Hit Movies, Documentaries, Sports, and Exclusive Comedy Specials.

WarnerMedia Studios & Networks

Undisclosed

Disney Fox

Acquired: March 2019. Type: Full Acquisition. Cost: USD 71.3 Bn

Television Studios The Walt Disney Company

(74%), Fox Corporation (26%)

iQiyi Subscribing Members: 105.3 Mn (Mar 2021). MAU: 479 Mn (2020). Founded: 2010. HQ: Beijing, China.

Media Prima, Celcom Leading internet video streaming service: Highly popular original content, comprehensive library of professionally-produced, professional user generated, and user-generated content. Premium content: user engagement, monetization opportunities.

Other institutional (64.74%), Mutual Fund Holders (14.15%),. Top owners: Baidu (56.2%), Hillhouse Capital Advisors Ltd. (10.21%), Credit Suisse Securities (6.88%), UBS Securities (5.35%).

Last quoted valuation: Market Cap: USD 16.4 Bn (2020)

WeTV 100k users (2019), Launched: 2018. HQ: China. Regions: China, Philippines, Thailand, Indonesia, Malaysia, India.

Xtreme Appliances Video streaming service, supports video-on-demand and television broadcasts

Tencent Video, Tencent

iflix Users: 25 Mn active users (2020). Founded: 2014. HQ: Kuala Lumpur, Malaysia.

TikTok, PT Media Nusantara Citra Tbk (MNC), Viva Communications Inc., Globe Telecom, Telkomsel.

Memberships (iflixFREE, iflixVIP), movie of the day, premium TV series (international and local), ad-free premium access to hundreds of movies and TV shows from local and international studios (iflixVIP membership).

Tencent, Fidelity International, Yoshimoto Investment, Kwese, Hearst Communications, Liberty Global, Zain Group, Sky UK.

USD 348 Mn

16

www.danareksa.com See important disclosure at the back of this report

RCTI+ Founding year: 2019 MNC Group, Global Mediacom (BMTR)

OTT service, stream movies, series; watch live shows and live events; news media platform. Comments: The company is targeting to reach 40Mn MAU in 2021

MNC Group N/A

Mola TV Founding year: 2019 Polytron, Djarum Group Stream movies and series; live events; sports liveb stream Mola recently switched its strategy to include OTT service due to the Covid-19 pandemic, to cope with the cancelation of football matches.

Djarum Group N/A

Goplay Founded: September 2019. HQ: Jakarta, Indonesia.

TVN Movies (South Korea), Astro (Malaysia)

Live streaming feature (Goplay Live) covering concerts, webinars, talk shows and reality shows, Video on Demand Shows, Pay-per-view (PPV) service, cast feature on Android and Airplay on Apple to watch shows on big screen televisions.

PT Aplikasi Karya Anak Bangsa (Gojek) , Cool Japan Fund

Undisclosed

MAXstream

No. of users: 8.2 million monthly active users (2020) Founded: 2016. HQ: Jakarta, Indonesia

beIN Sports, Vidio.com, WarnerMedia Entertainment

Domestic and foreign films, Live TV Channels (Local and International), TV Shows, Subscription Packages, MAXstream Quota

PT Telekomunikasi Seluler (Telkomsel)

N/A

Noice No. of users: 180k active users (March 2021) Launched: June 2018 as radio streaming platform, added music and podcasts in October 2019. HQ: Jakarta, Indonesia.

PT Quatro Kreasi Indonesia

Podcasts, Music, Radio, Content. Multiple Audio and Content in 1 App, Available to Listen Anytime and Anywhere. Comments: MARI is looking to launch Noice 3.0 by the end of 2021 to monetize the business, enable extra content creators to share podcasts in the app and integrate with other platforms.

PT Mahaka Radio Integra (MARI) - 75%, Alpha JWC Ventures and Kinesys Group - 25%

N/A

Garena No. of users: 80 million daily active users globally. Founed: May 2009. HQ: Singapore

Tencent In Game Features (Smart Ping, Colorblind Mode, Chat Commands, Emotes), Ranked Play, Social (Guide to Clubs), Rewards (XP System Breakdown).

Sea Ltd, indirect shareholder Tencent

Dunia Games

No. of users: 4 million monthly active website visitors (Dunia Games Website). Founded: 2013. HQ: Jakarta, Indonesia

Source for All Gaming (Tips, Guides, Reviews), Latest Gaming News Portal, Purchase Game Vouchers Online (Steam Wallet, Garena, Gemscool, Lyto, Megaxus)

PT Telekomunikasi Seluler (Telkomsel)

N/A

Source: BRI Danareksa Sekuritas

➢ Content and Gaming entertainment, nourishing the digital crowd. Relatively high developing costs to produce titles, and royalty fees. The gaming developers in Indonesia are still at the nascent stage. Gaming and music on the other hand rely on the freemium models, which are largely price competitive in our view and thus need to create a large base. A classic example is Tencent creating a large entertainment ecosystem, whilst Garena of SEA still monetizes on the highly popular Freefire with positive EBITDA subsidizing the EBITDA losses in SEA’s ecommerce biz. We believe local players may benefit from gaming/music as supporting services in a larger ecosystem. Gaming aggregators and voucher resellers is the best fit model in Indonesia so far. Gaming is highly adoptive for mobile/smartphone users apart from game consoles and desktops, to become increasingly engaging with increasing data upload/download speeds and lower data latency improving the gaming experience. Moreover, E-sports, gaming events, influencers, and Twitch-like viewership is adopted by millennials and younger age groups, who may have low financial capital but they are the next consumption decision makers in households. Music aggregators, on the other hand, have the power to create their own content with podcasts addressing current trends finding resonance with users, who may also enjoy live taped content on demand vs. linear supply.

17

www.danareksa.com See important disclosure at the back of this report

➢ Social networks and short video drive strong engagement. Their adoption and growth has been rampant and is an essential service. Examples are messaging apps and short video aggregators like YouTube, Facebook & Instagram, TikTok, Vidio.com, MNCN+. SoSMed has the greatest appeal in young age groups. The digital frontrunner China sees unparallel advertising spending on e-commerce as well as on short videos.

➢ Moreover, technology investments such as Facebook Oculus are expected to drive new dimensions on digital content and the gaming experience.

➢ IM messenger services in Indonesia are heavily driven by foreign players such as Whatsapp, Facebook, LINE, Instagram, Viber, Telegram, and Google Duo messengers. Their communication channels can be highly disruptive by introducing fintech and peer-to-peer lending and introducing their own digital wallets and currencies.

➢ WABA whatsapp business accounts also offer support to merchants making available business catalogs and creating shopping carts. DIVA IJ and DMMX IJ of Kresna group adopt and make use of those functionalities to help business traction for their merchants.

➢ OTT will continue to offer paid content services with plenty of room for content differentiation. It is a great supportive service to be part of a larger experience ecosystem to drive engagement. The market is dominated by large deep-pocketed international players: Netflix, HBO, Disney, Amazon Prime, iQiyi, Viu etc. The rise of local champion Vidio.com is an unmistakable bet that relies on local content, sports and taste with own production houses that resonate with local users. MNCN+ and Vision+ are also strong contenders for digital local content with their own production and short videos.

Exhibit 24. Online advertising methods in China: rising of short video share

Source: Bloomberg Intelligence

Travel sector: In anticipation of a rebound. Similarly travel sector saw major disruption easily on a very fragmented market. Despite witnessing major drop in travel turnover, Traveloka itself undertook new directions shifting to food delivery Traveloka Eats and possibly ecommerce.

Exhibit 25. Travel/Ticketing Market

Com General Info + Matrix Affiliations Features Shareholders Quoted Valuation

Traveloka

60 Mn+ app downloads Users: 40 Mn (2021, investor.id) Reach: 8 APAC nations Merchants: 66k+ Accommodations: 60k+ direct-contract accommodations in Southeast Asia, 1 Mn+ worldwide accommodations (including 17k+ villas, 25k+ apartments), available in 100 different

Payment partners: BBCA, BMRI, BBNI, BBRI, Visa, martercards, JCB, ATM Bersama, Alto, Prima, Alfamart, Alfa midi, Indomaret, BCA KlikPay, Mandiri Debit, CIMB Clocks HOtel Partners: L Accor hotels, Aerowsiata, Amazing Hotels & Resorts Indonesia, ARCHIPELAGO, artottelgroup, AZANA, Best Wester, D'primahotel, DHM, Golden Tulip, Horison,

20+ products Transportation: flights, flights + hotel, trains, JR Pass, Bus & Shuttle, Airport transfer, car rental, airport train, flight status, price alert Accommodation: Hotels, Flights + Hotel, Buy Now Stay Later, Villas, Apartments Things to Do: Xperience, Eats, Healthcare Bills (payment): data top up and packages, mobile post-paid, PLN, BPJS Kesehatan, Telkom, PDAM, game voucher, multi finance, cable tv & internet, credit card, PBB, electronic money Others: pay later, gift voucher, insurance, city guides, budget planner, Traveloka Corporates Insights: In April, news that Traveloka is planning to list

EV Growth, Qatar Investment Authority, GIC, Expedia, Hillhouse Capital Group, JD.com, East Ventures, Sequoia Capital, Global Founders

Last quoted valuation: USD 3 Bn (krasia), with potential valiation of USD 5 Bn with SPAC listing. Claimed its near profitable. hotel transaction reached 70-

18

www.danareksa.com See important disclosure at the back of this report

countries. Flights: 200k routes, 150+ airlines, 950 airport destinations worldwide Experience: 18k+ things to do SKU's, 1000+ merchant partners across SEA Loans: 6 million+ loans Founded: 2012

Kahum Hotels, Sheraton, Sahid, Terra Hotels, Omega, Parador, Horsion, IHG, Swiss-nel hotel, red planet, Tauzia, Topotels, W house, Marriott, Initiwhiz, Pesonna hotels, Santika Indonesia, SAS hospitality Investments: Member.id, KiotViet, PouchNATION, PasarPolis, Mytour, Pegipegi, Travel Book TREX Ventures: JV with Siam Commercial Bank Pcl - SCB10X) Others: West Java Provincial Goverment, BBRI and BMRI to create designed credit cards, Lalamove

in the US stock market through SPAC, Bridgetown Holdings Ltd. This deal may potentially boost the company's valuation to USD 5 Bn and raise USD 500-750 Mn. -Set up a JV with Siam Commercial Bank to create TREX Ventures, a fintech company to provide financial products to its 16 Mn users in Thailand. In 2018 Traveloka started Buy Now Pay Later facility and created the Paylater Credit Card - Expands through Traveloka Eats with delivery services partnering with Lalamove (both companies are backed by Hillhouse Capital). It is reported that Traveloka Eats charges a lower fee of 15% of each order, compared to 20% from GoFood and GrabFood.

Capital

75% pre pandemic level.

-Covid 19

effect: lowest business rate, refunds increased by 10x since february (1 Mn flight refund worth USD 100 Mn), 100 employee layoffs (10% of workforce) (Jul. 2020)

Agoda HQ: Singapore Founded: 2005 Owned by Booking Holdings (NASDAQ: BKNG) Focus on APAC region Operation in Thailand Listings: 2.5 Mn+ propoerties in 200+ countries. 200+ Airlines 27 Mn+ reviews Agoda member users: 1 Mn+ (2009)

Booking Holdings (NASDAQ:BKNG); booking.com, Priceline, Opentable, Kayak, and rentalcars.com Other: Viator, Meituan, Trip.com, fareharbor, HotelsCombined, Grab, Didi Chuxing

Accomodations (hotels, homes, private stays, monthly stays), Ground Transportation (airport transfers and car rentals), Flights, Activities, loyalty membership (Agoda Reward and AgodaCash) - Agoda actively improve user experience, lower

acquisition costs, and expand products. Agoda spends USD 4.96 Bn on online marketing annually. Introduced flights aggregator feature in 2019. - In 2021, Agoda sees domestic tourism returning

activity in Thailand, Vietnam, and Taiwan. Waiting for vaccination programs to be completed so international travel recovers. Agoda records higher domestic travel even before pandemic levels.

Owned by Booking Holdings (100%)

N/A

Pegipegi

- 9 Airline partners - 25 k flight routes - 25k+ hotel options - 2.8 k train routes Founded: 2012

Airlines: Citilink, Lion Air, Sriwijaya Air, Garuda Indonesia, Air Asia, Batik Air,, Winfs Air, NAM Air, Scoot Other: BMRI, BBCA, BBNI, BBRI, LG, TLKM, EXCL, LINE, CGV, Samsung, Blibli, Tripadvisor, Wego, Trivago, wonderful Indonesia, etc.

Hotel, Airline, Train, Bus & Travel bookings PegiPegi claims to run its operations independently even after acquired by Traveloka

Acquired by Traveloka

N/A

Tiket.com

- 100k routes - 150 partnered arilines - 950 airport destinations - 1 Mn + accommodations/stays (hotels, villa, apartment) Founding year: 2011

Train: PT KAI Airlines: Air Asia, KLM, ANA, Citilink, expressair, United Arilines, etc Hotels: Marriott, Hilton, IHG, Best Western, etc. Car rentals: Express, TRAC, Tritama, etc. Activities: Funland, Java Jazz, Waterbom, etc.

Airline ticketing, Hotels, Train tickets, car rental, Event ticketing/booking Flexi ticket: purchases can be redeemed/used within 1 year Instalment payment Comments: Plans to go public through SPAC that will value the company at USD 2 Bn and raise USD 200 Mn.

Undisclosed Angel Investor: USD 1 Mn

Last quoted valuation: EUR 4-5 Mn (dealroom oct 2011 est.)

Source: BRI Danareksa Sekuritas

19

www.danareksa.com See important disclosure at the back of this report

GMV latest standings of E-tailers

So far ecommerce customer loyalty is still a working project we believe.

According to GMV data gathered, it appears there is high volatility in market share for Indonesia and the root cause of that is the heavy marketing campaigns run frequently. A great deal of effort is spent on the consumer front to mold stickiness and loyalty of the user.

The rivalry between SE Asia's online retailers has intensified again. According to iPrice, Tokopedia outpaced Shopee in 1Q to be the No.1 e-tail platform in Indonesia, where 40% of ASEAN's digital consumers are located. Tokopedia's monthly web visits jumped to 135.1mn, 6% higher than Shopee's.

Exhibit 26. GMV standings of E-tailers

Source: Various media, disclosures & daily press

E-commerce competition on SE Asia scale. ➢ SEA controls the no. 1 e-tailing commerce player and is armed with a cash-

rich balance sheet. It recently launched its own food-delivery service ShopeeFood with a digital wallet Shopee Pay which is already dominating the peers. This may well challenge Grab and Gojek's food delivery market dominance, particularly in Indonesia, where over 40% of the region's digital consumers reside, according to Google, Temasek and Bain & Co.

➢ U.S. and China have 21% in food delivery penetration, vs. 11% in SE Asia. The sector provides SEA a large opportunity to expand its user base and lastmile logistics network through its ShopeeFood, which in turn could have synergistic effects in adjacent offerings such as e-commerce and financial services. SEA also owns Now, a leading food delivery app in Vietnam.

➢ SEA can keep leveraging its highly lucrative gaming business and prominent e-commerce brand to penetrate the food delivery market.

➢ Gojek exited Thailand’s ride-hailing operations in return for 4.76% of Air Asia shares, as part of a realignment of its SE Asia strategy. Gojek instead increased investment in its Vietnam and Singapore operations, having identified these markets as strong sources of growth for the business going forward. This includes increased driver and merchant acquisition initiatives, enhancements to user experience as well as launching new products and services.

2018 2019 2020

E-commerce GMV

Indonesia E-commerce GMV (Google

Temasek Bain)$12.2bn $21bn $32bn

Indonesia E-commerce GMV by Frost

& Sullivan $11.6 bn $17.9 bn $30.6 bn

Bukalapak $1.81bn $3.73bn $4.93 bn

Shopee $8.2bn $5.6bn $14.2 bn

Tokopedia $5.1 bn $1.3 bn (May) /

$15.6 bn (Q4) $14 bn

Lazada N/A N/A $4.5 bn

MAU

Bukalapak 50mn 70mn 90mn

Shopee 34.5mn 72.9mn 129mn

Tokopedia 80mn 67.9mn 100mn

Lazada 58.2mn 28.3mn 36.2mn

MERCHANTS

Bukalapak - online 4mn 5mn 6mn

Bukalapak - offline 2.5mn 7mn

Shopee 1.6 mn (Q1) 3 mn 3.7+ mn

Tokopedia 5 mn 7 mn (Nov 2019) 9.9 mn

Lazada N/A N/A N/A

20

www.danareksa.com See important disclosure at the back of this report

➢ Tokopedia's merger with Gojek in 2021 to create GoTo, may see Tokopedia expand outside Indonesia for the first time, into Vietnam where Gojek has already rolled out its ride-hailing service. However, Shopee still has the upper hand, given its 64% market share by user traffic, and a highly profitable gaming business Garena that can subsidize Shopee market share expansion.

➢ Shopee continues to be SE Asia’s largest e-tailer with 228mn monthly web visits, more than double Lazada’s 110mn. Tokopedia, Alibaba's Lazada and Amazon may eye Vietnam for its growth potential too, while Shopee is gunning expansion in Latin America to capture opportunities.

Exhibit 27. Actual and forecast SE Asia total GMV by country

Source: Google, Temasek, Bain & Co.

E-payment services is a financial drag but a vital element for fintech and ecosystem adoption.

The Ecommerce, ride-hailing and food delivery biz were the driving forces for e-payments. Thus, epayment services integrated into those forces have the advantage in driving usage and GTV in comparison to diversified players OVO and Dana.

Moreover, we believe epayments are also key to driving financial inclusion in Indonesia, by onboarding users to more sophisticated fintech services.

Even if the Covid19 new daily cases recede, the authorities will promote contactless transactions to avoid spikes in Covid19 new cases, and therefore the use of e-money & digital wallets.

21

www.danareksa.com See important disclosure at the back of this report

Exhibit 28. E-wallets Competition

E-Payment Total Users MAU/MAU Rank GTV Merchants

20

18

DANA 1 million MAU Rank - 4 40 merchants

OVO 115 million MAU Rank - 2 9,000 MSMEs (August)

Link Aja MAU Rank - 3

Shopee Pay

Jenius 700k MAU Rank - 5

Gopay 20 Mn MAU Rank - 1 200k merchants, 20k MSMEs

20

19

DANA 30 million MAU Rank - 3, 35Mn 1.5k merchants, 87.5k MSMEs

OVO 110 Mn MAU rank - 2 180k MSMEs

Link Aja 40 million MAU Rank - 4 250k merchants, 380 e-commerce, 2.5k filling stations (SPBU)

Shopee Pay

Jenius 1.6 million

Gopay 115 Mn MAU Rank - 1

GTV: USD 6.3 Bn/IDR 89.5 T

320k MSMEs

20

20

DANA 50 million 180k merchants, 120 MSMEs

OVO 950k MSMEs, 1.5million merchants

Link Aja 61 million 315k merchants, 5k e-commerce, 5.5k filling stations (SPBU)

Shopee Pay 10 Mn

Jenius 2.5 million 29 Jenius Pay merchants

Gopay 420k merchants in 370 cities

20

21

DANA 70 million (Sem I 2021) 13.5 Mn 3k online merchants

OVO 115 Mn 20.8 Mn 1.5 Mn+ merchants

Link Aja 66 million 7.2 Mn 350k merchants, 680 traditional markets, 6k online marketplace, 1.6k mosque.

Shopee Pay 10 Mn

Jenius 3.1 million

Gopay 900 business partners

Source: BRI Danareksa Sekuritas

Exhibit 28a. Digital Payment Gross Transaction Value (GTV USDbn) in SE Asia

Exhibit 28b. Method of payments

Source: Google, Temasek, Bain & Co Source: Google, Temasek, Bain & Co (A2A are transfers)

22

www.danareksa.com See important disclosure at the back of this report

Exhibit 29. Embedded vs. Independent E-wallet have different focuses

Source: Momentum Works

Pricing, promos, discounts and outlook. The pricing of goods and services is an important aspect, and key determinant for adoption. Start-ups will have to compensate the subsidies for purchasing goods and services with benefits that technology brings and its adoption thereof. Moreover, since we are still in the phase of adoption, stickiness and loyalty is paramount to have clients revisiting the platform and repeat/expand purchases, effectively bringing down cash costs. We have reached 21% ecommerce penetration in retail, and beyond the aforementioned balancing act, internet players would need to defend their market positions and we may see some more discounts, free shipping offers etc. Nonetheless, facilities like 0% instalment payments, cashbacks for future purchases, point rewards to encourage loyalty may be subsidizing payments but have a positive effect for future turnover. Lastly, there is widespread offerings Buy Now Pay Later, which emulates the functionalities of credit cards for users who have limited credit records, that should positively affect business turnover.

Exhibit 30. Payment promotions by Grab

Source: Grab

23

www.danareksa.com See important disclosure at the back of this report

New Horizon: Expansion enabled by big data processes in the cloud. Unconnected pools of big data waiting to be connected and provide insights for consumer behaviour. From now and into the future, several businesses will pass the low hanging fruits of data connectivity and digital platform and accelerate the very process of needs discovery through personalization. .

Internet players have many opportunities in terms of:

a) additional coverage

Internet economic growth is very versatile. When other sectors slow down, others step up and make an impact.

Exhibit 31. Indonesia sectoral GMV projection Exhibit 32. GMV sectoral comparison in SE Asia

Source: Google, Temasek, Bain & Co 2020 Source: Google, Temasek, Bain & Co 2020

Exhibit 33. Number of districts with Tokopedia & Gojek presence Exhibit 34. Metropolitan vs. non Metro ecommerce coverage

Source: LPEM, University of Indonesia Study Source: LPEM, University of Indonesia Study

Exhibit 35. Presence of Tokopedia across Indonesian districts, 2019 Exhibit 36. Presence of Gojek across Indonesian districts, 2019

Source: LPEM, University of Indonesia Study Source: LPEM, University of Indonesia Study

24

www.danareksa.com See important disclosure at the back of this report

Exhibit 37. E-tailing spend was projected beyond tier-1 cities

Source: Mckinsey

Exhibit 38. Indonesian E-commerce GMV projection

Source: Frost and Sullivan, Bukalapak

b) Additional online penetration Covid19 has altered the outlook and consumer behaviour to adjust to new lifestyles in line with mobility restrictions, WFH, SFH. But the core attributes of the demographics remain.

- Indonesian consumers have been the main growth engine for economic growth, with an aspiring middle class for improved lifestyles throughout Indonesian islands. We expect Indonesian consumers to dictate those aspirations through higher purchases online.

- Secondly, we understand the aspiring class has high smartphone adoption at circa 65% smartphone penetration.

- Thirdly, the rate of Indonesian urbanization increases with the population relocating to city centres with higher economic activity.

- Equally important, we expect that precautions for Covid19 will not dissipate. Rather, lifestyles will adapt to include more contactless activities with 3D/hologram communication enabled by 5G, online transactions and e-money/digital currency transactions.

Upside seen at higher digital penetrations The graphs below depict that older cohorts will tend to generate more volume as digital penetration increases. This is because either the ecommerce has become mainstream, or other alternatives to purchase goods are no longer meaningful. We understand that ridehailing companies and e-payment services subsidize fares and offer a great deal of promotions, which along the way, can be removed at a steady state, or when the service becomes mainstream.

25

www.danareksa.com See important disclosure at the back of this report

Exhibit 39a. Grab monthly transacting users split by number of offerings (%). Users are using more offerings

Exhibit 39b. Shopify Canada: Order growth from previous loyal users

Source: Grab 2021 Source: Shopify 2021

c) data cloud enabler Tech companies can help fuel their longer-term growth with Cloud computing supporting services. Users include tech start-ups, financial institutions, telecommunications, enterprises and SOEs who already store and process data in public/hybrid cloud. We expect big data and machine learning across digital internal platforms of entities. They will use AI to identify abnormal behaviour in their value chain, and machine learning for customer profiling to serve consumers more efficiently and create more opportunities to upsell/cross-sell. Early adopters of e-Commerce have matured over the years and tend to demand more differentiated product/service offerings.

Exhibit 40. Cloud spending forecast by functional market

Source: IDC, Bloomberg Intelligence

Internet companies approach from 2 ends, supply & demand: focus on the consumer (Amazon, Alibaba), and focus on the merchant (Shopify way) depending on penetration levels. In an environment where there is stronger online penetration and purchasing power, we expect internet companies to empower consumer experience. In an environment where infrastructure, logistics is still relatively limited and under long development, the focus may shift on empowering the supply side and the merchants.

26

www.danareksa.com See important disclosure at the back of this report

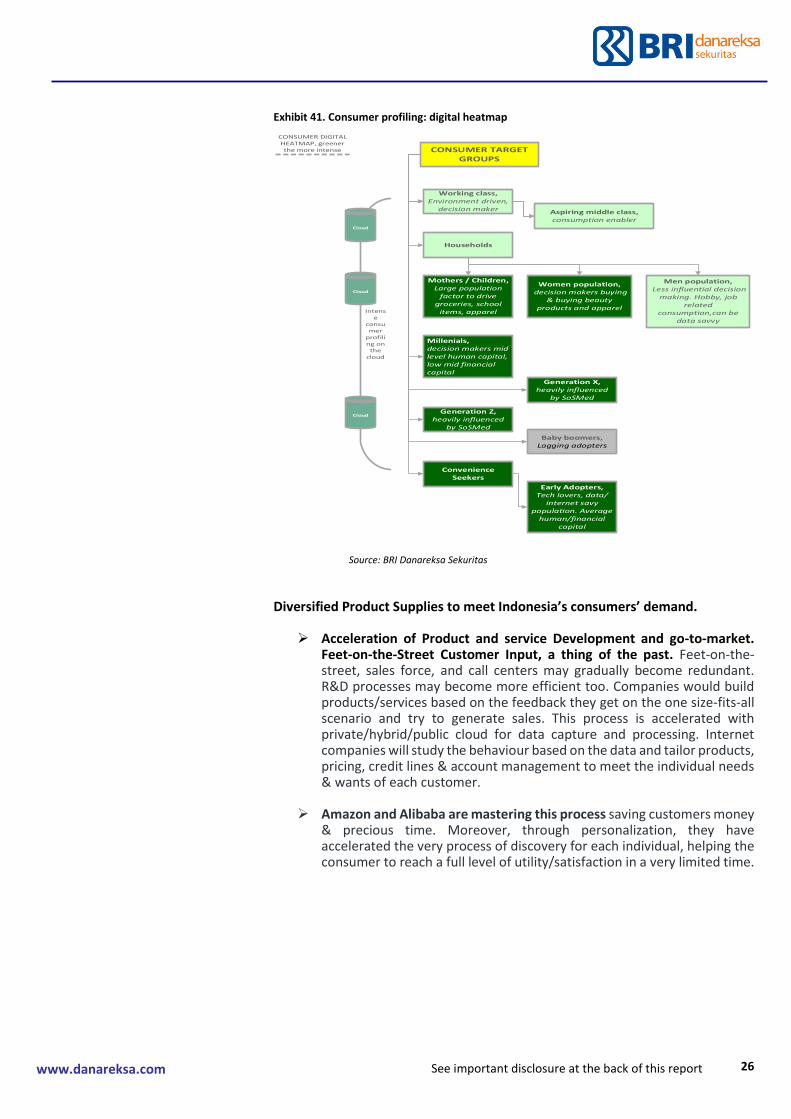

Exhibit 41. Consumer profiling: digital heatmap

Source: BRI Danareksa Sekuritas

Diversified Product Supplies to meet Indonesia’s consumers’ demand.

➢ Acceleration of Product and service Development and go-to-market. Feet-on-the-Street Customer Input, a thing of the past. Feet-on-the-street, sales force, and call centers may gradually become redundant. R&D processes may become more efficient too. Companies would build products/services based on the feedback they get on the one size-fits-all scenario and try to generate sales. This process is accelerated with private/hybrid/public cloud for data capture and processing. Internet companies will study the behaviour based on the data and tailor products, pricing, credit lines & account management to meet the individual needs & wants of each customer.

➢ Amazon and Alibaba are mastering this process saving customers money

& precious time. Moreover, through personalization, they have accelerated the very process of discovery for each individual, helping the consumer to reach a full level of utility/satisfaction in a very limited time.