technology & strategy - skynet blogsstatic.skynetblogs.be/media/169675/576596611.pdf · –fit...

TRANSCRIPT

Technology & Strategy

GEST-D-484

Manuel Hensmans

1

Group presentations

• Has everyone sent me their group

presentation?

– Or told me about their blog?

• Please do: [email protected]

2

Last class

• Part III: Setting the strategic direction

– Importance strategic capability

– Analyse internal resources and competences

• VRIN

• Case Dyson

– Quiz

3

This class

• Part III: Setting the strategic direction

– Fit external position + internal capability

• Fit industry profitability & resources/competences

• 5 steps

– Results Quiz 1 & 2

– Creating strategic intent for the future

• 8 steps

4

Fit external position & internal

capabilities

1 Industry profitability

- Positive versus negative drivers profitability

2 Within industry some firms perform better

– Why? Key Success Factors

3 What capabilities do these KSF imply?

- Use value chain analysis for completeness

5

Fit external position & internal

capabilities

4 Appraise resources and competences

– Importance

• What capabilities most likely to confer sust comp adv

– Relative strenghts/weaknesses

• Compared to competitors

• Can benchmark both quantitatively (revenue/cost or

performance) & qualitatively (best practices)

6

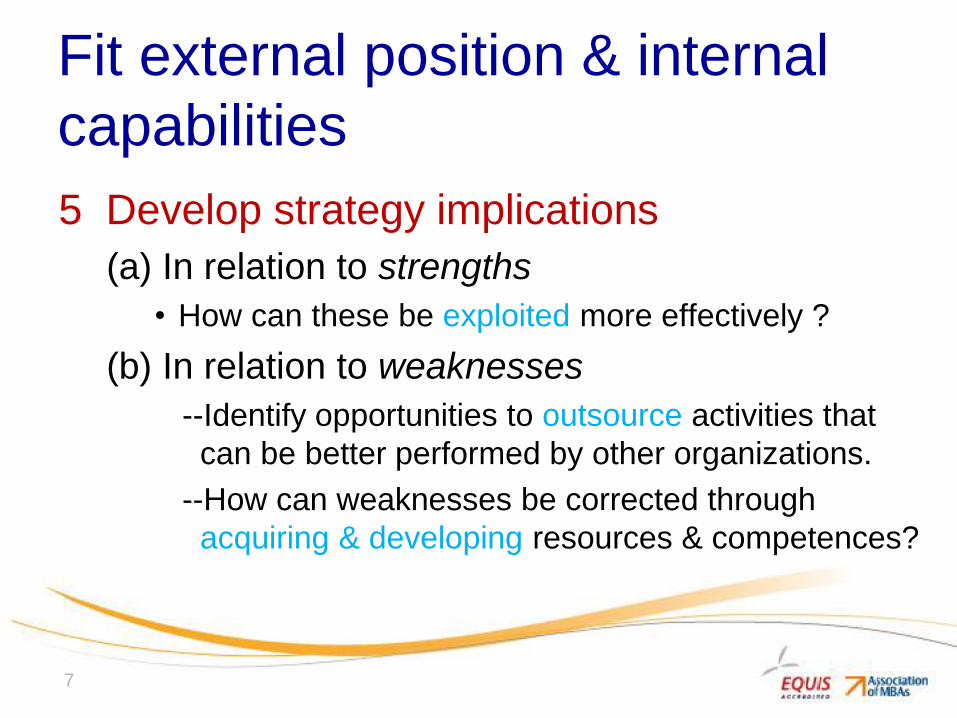

Fit external position & internal

capabilities

5 Develop strategy implications

(a) In relation to strengths

• How can these be exploited more effectively ?

(b) In relation to weaknesses

--Identify opportunities to outsource activities that

can be better performed by other organizations.

--How can weaknesses be corrected through

acquiring & developing resources & competences?

7

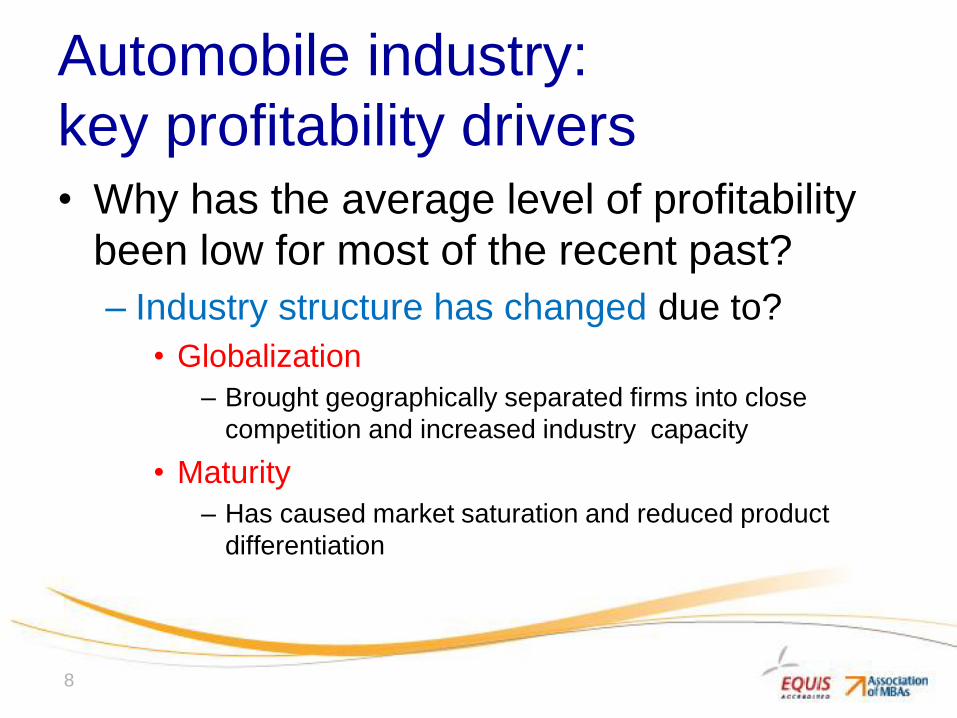

Automobile industry:

key profitability drivers • Why has the average level of profitability

been low for most of the recent past?

– Industry structure has changed due to?

• Globalization

– Brought geographically separated firms into close

competition and increased industry capacity

• Maturity

– Has caused market saturation and reduced product

differentiation

8

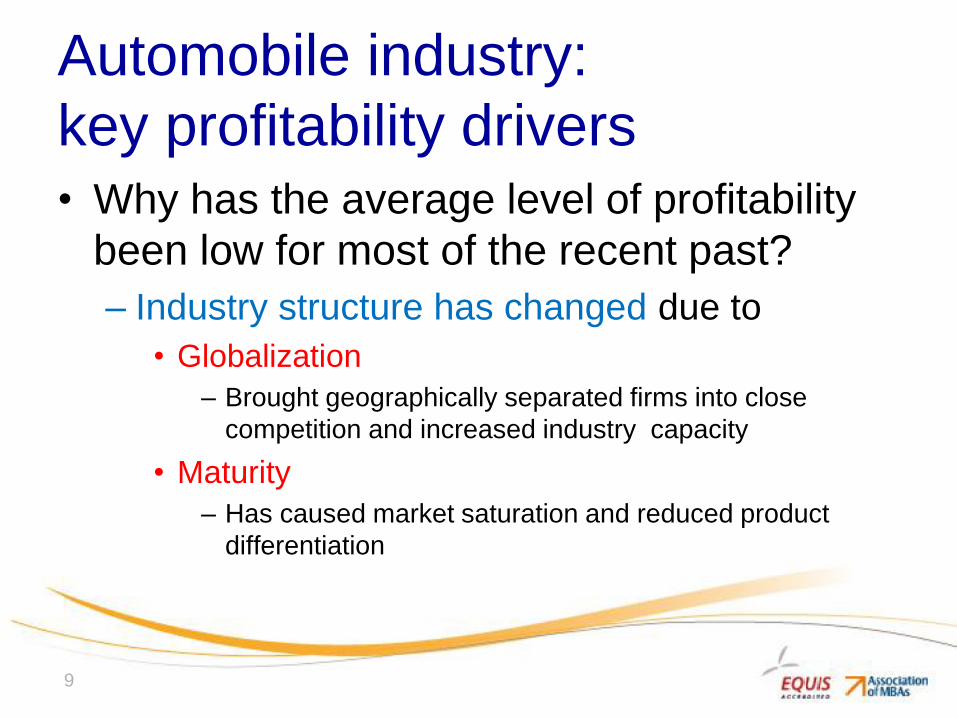

Automobile industry:

key profitability drivers • Why has the average level of profitability

been low for most of the recent past?

– Industry structure has changed due to

• Globalization

– Brought geographically separated firms into close

competition and increased industry capacity

• Maturity

– Has caused market saturation and reduced product

differentiation

9

Some firms perform better:

Key success factors • World automobile industry

– Key success factors

• Low-cost production

• Attractively designed new models

– Embodying latest technologies

• Financial strength

– To weather the heavy investment requirements and

cyclical nature of the industry

11

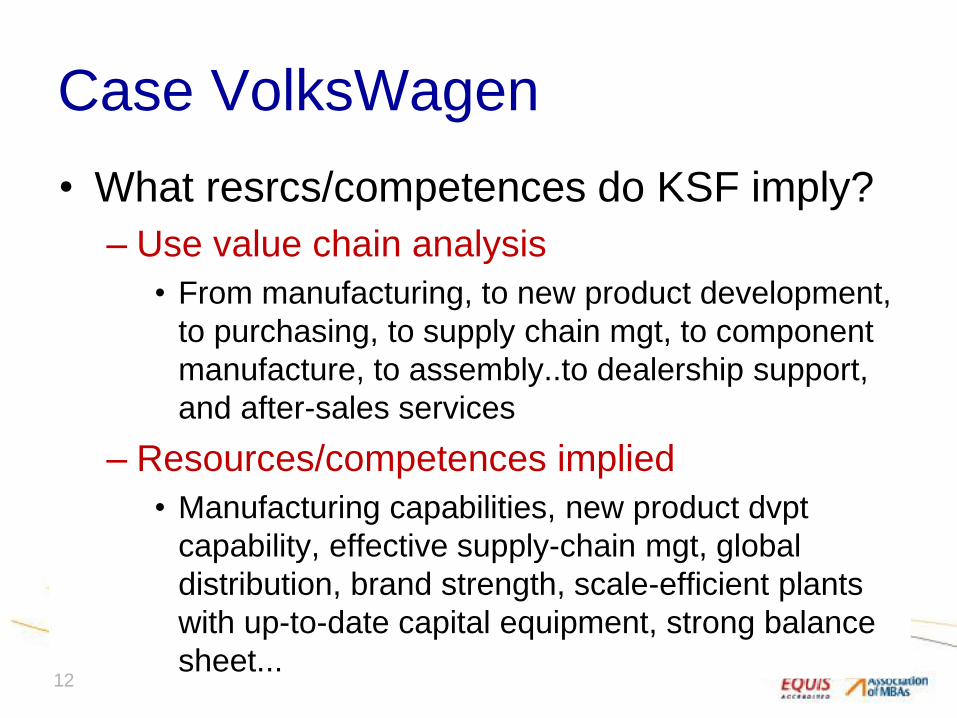

Case VolksWagen

• What resrcs/competences do KSF imply?

– Use value chain analysis

• From manufacturing, to new product development,

to purchasing, to supply chain mgt, to component

manufacture, to assembly..to dealership support,

and after-sales services

– Resources/competences implied

• Manufacturing capabilities, new product dvpt

capability, effective supply-chain mgt, global

distribution, brand strength, scale-efficient plants

with up-to-date capital equipment, strong balance

sheet...

12

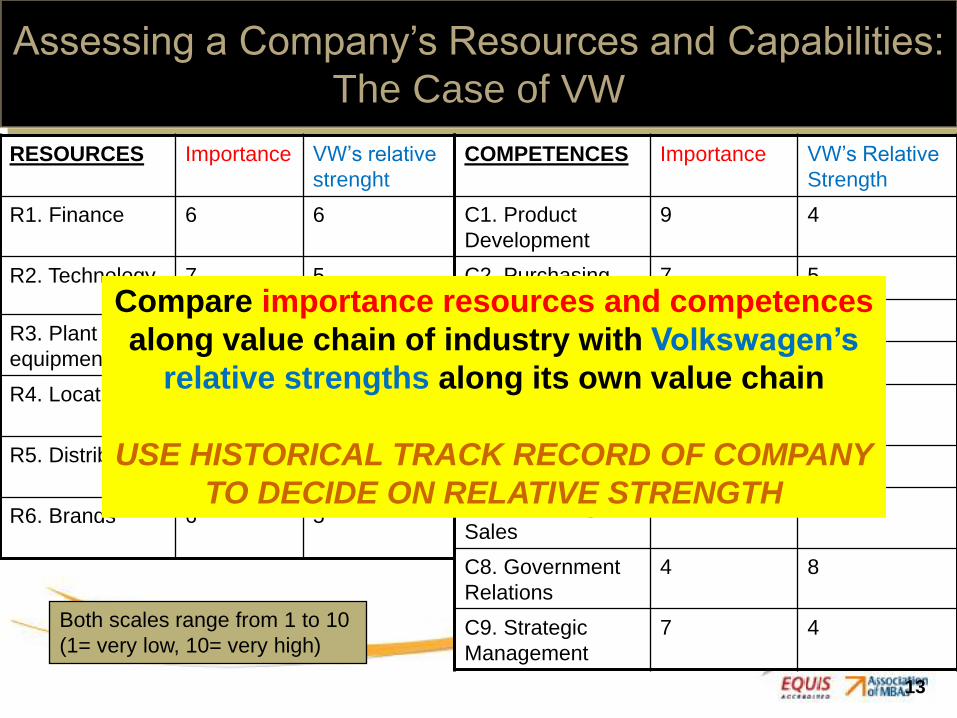

Assessing a Company’s Resources and Capabilities:

The Case of VW

RESOURCES Importance VW’s relative

strenght

R1. Finance 6 6

R2. Technology 7 5

R3. Plant and

equipment

8 8

R4. Location 4 4

R5. Distribution 8 5

R6. Brands 6 5

COMPETENCES Importance VW’s Relative

Strength

C1. Product

Development

9 4

C2. Purchasing 7 5

C3. Engineering 7 9

C4. Manufacturing 8 4

C5. Financial

Management

6 4

C6. R&D 5 4

C7. Marketing and

Sales

9 4

C8. Government

Relations

4 8

C9. Strategic

Management

7 4 Both scales range from 1 to 10

(1= very low, 10= very high)

13

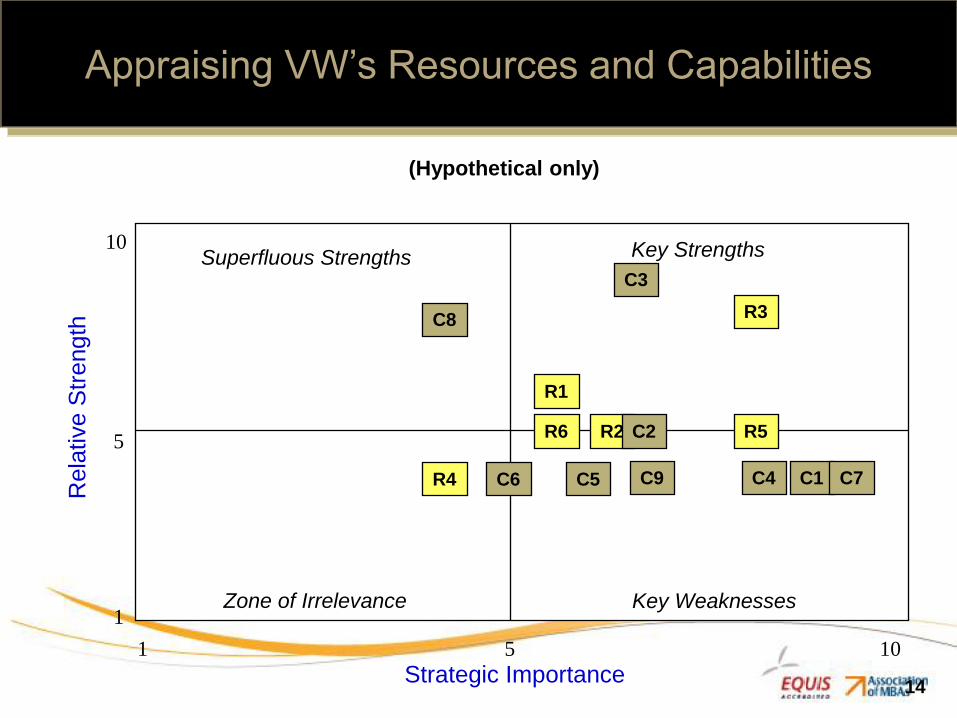

Compare importance resources and competences

along value chain of industry with Volkswagen’s

relative strengths along its own value chain

USE HISTORICAL TRACK RECORD OF COMPANY

TO DECIDE ON RELATIVE STRENGTH

Rela

tive S

trength

Strategic Importance

Superfluous Strengths Key Strengths

Zone of Irrelevance Key Weaknesses

1

1

5 10

5

10

R1

R2

R3

R4

R5

C1

C2

C3

C4 C5 C6 C7

C8

(Hypothetical only)

Appraising VW’s Resources and Capabilities

C9

R6

14

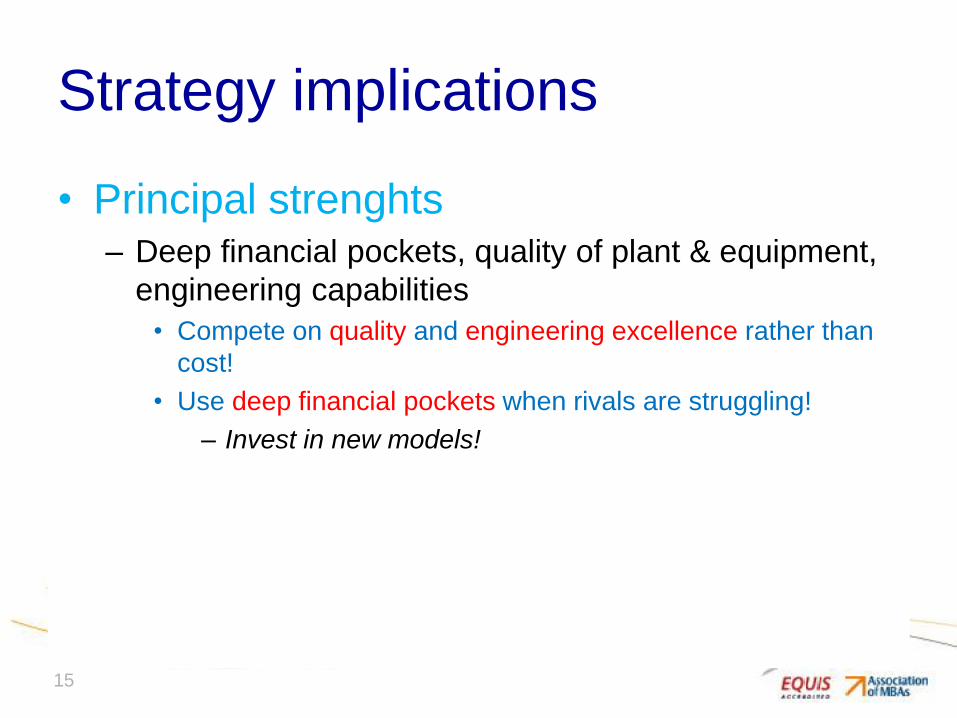

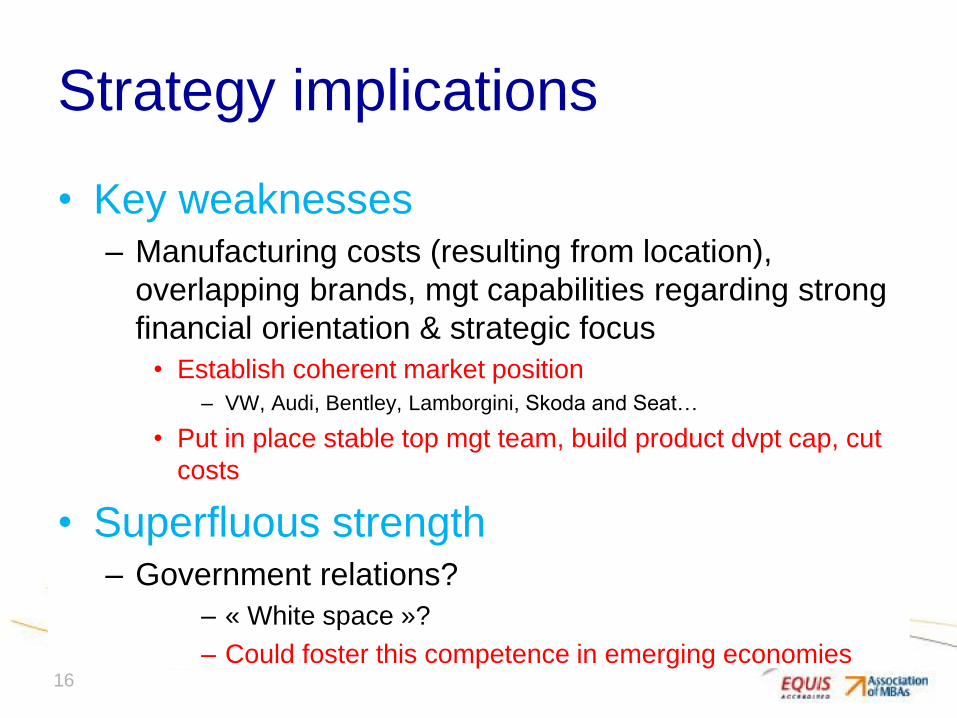

Strategy implications

• Principal strenghts – Deep financial pockets, quality of plant & equipment,

engineering capabilities

• Compete on quality and engineering excellence rather than

cost!

• Use deep financial pockets when rivals are struggling!

– Invest in new models!

15

Strategy implications

• Key weaknesses – Manufacturing costs (resulting from location),

overlapping brands, mgt capabilities regarding strong

financial orientation & strategic focus

• Establish coherent market position

– VW, Audi, Bentley, Lamborgini, Skoda and Seat…

• Put in place stable top mgt team, build product dvpt cap, cut

costs

• Superfluous strength – Government relations?

– « White space »?

– Could foster this competence in emerging economies

16

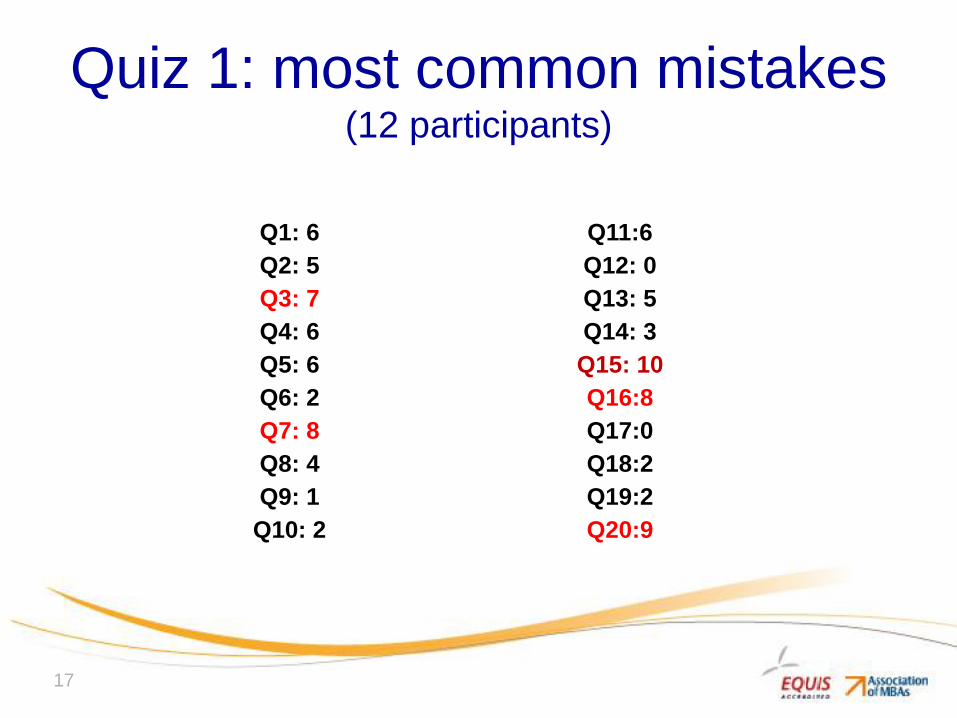

Quiz 1: most common mistakes (12 participants)

17

Q1: 6 Q11:6

Q2: 5 Q12: 0

Q3: 7 Q13: 5

Q4: 6 Q14: 3

Q5: 6 Q15: 10

Q6: 2 Q16:8

Q7: 8 Q17:0

Q8: 4 Q18:2

Q9: 1 Q19:2

Q10: 2 Q20:9

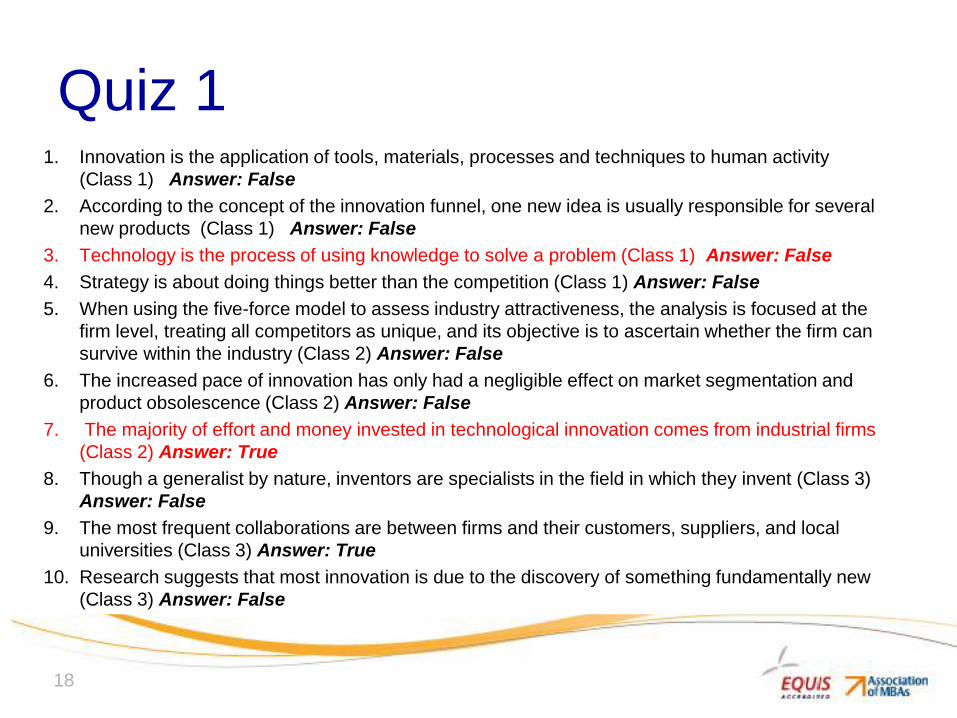

Quiz 1 1. Innovation is the application of tools, materials, processes and techniques to human activity

(Class 1) Answer: False

2. According to the concept of the innovation funnel, one new idea is usually responsible for several

new products (Class 1) Answer: False

3. Technology is the process of using knowledge to solve a problem (Class 1) Answer: False

4. Strategy is about doing things better than the competition (Class 1) Answer: False

5. When using the five-force model to assess industry attractiveness, the analysis is focused at the

firm level, treating all competitors as unique, and its objective is to ascertain whether the firm can

survive within the industry (Class 2) Answer: False

6. The increased pace of innovation has only had a negligible effect on market segmentation and

product obsolescence (Class 2) Answer: False

7. The majority of effort and money invested in technological innovation comes from industrial firms

(Class 2) Answer: True

8. Though a generalist by nature, inventors are specialists in the field in which they invent (Class 3)

Answer: False

9. The most frequent collaborations are between firms and their customers, suppliers, and local

universities (Class 3) Answer: True

10. Research suggests that most innovation is due to the discovery of something fundamentally new

(Class 3) Answer: False

18

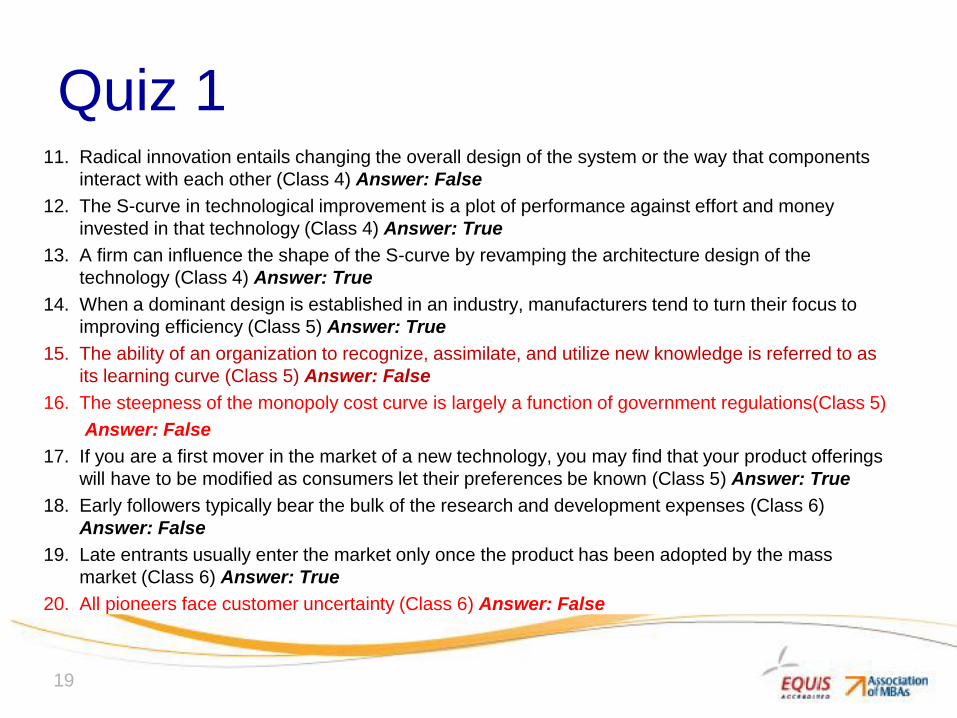

Quiz 1 11. Radical innovation entails changing the overall design of the system or the way that components

interact with each other (Class 4) Answer: False

12. The S-curve in technological improvement is a plot of performance against effort and money

invested in that technology (Class 4) Answer: True

13. A firm can influence the shape of the S-curve by revamping the architecture design of the

technology (Class 4) Answer: True

14. When a dominant design is established in an industry, manufacturers tend to turn their focus to

improving efficiency (Class 5) Answer: True

15. The ability of an organization to recognize, assimilate, and utilize new knowledge is referred to as

its learning curve (Class 5) Answer: False

16. The steepness of the monopoly cost curve is largely a function of government regulations(Class 5)

Answer: False

17. If you are a first mover in the market of a new technology, you may find that your product offerings

will have to be modified as consumers let their preferences be known (Class 5) Answer: True

18. Early followers typically bear the bulk of the research and development expenses (Class 6)

Answer: False

19. Late entrants usually enter the market only once the product has been adopted by the mass

market (Class 6) Answer: True

20. All pioneers face customer uncertainty (Class 6) Answer: False

19

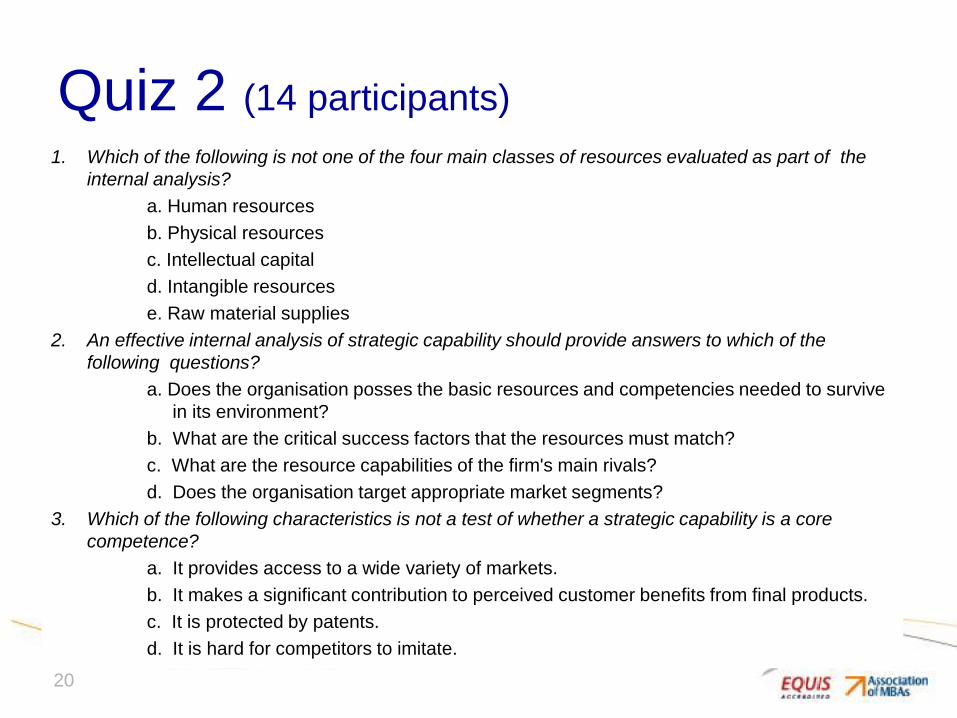

Quiz 2 (14 participants)

1. Which of the following is not one of the four main classes of resources evaluated as part of the

internal analysis?

a. Human resources

b. Physical resources

c. Intellectual capital

d. Intangible resources

e. Raw material supplies

2. An effective internal analysis of strategic capability should provide answers to which of the

following questions?

a. Does the organisation posses the basic resources and competencies needed to survive

in its environment?

b. What are the critical success factors that the resources must match?

c. What are the resource capabilities of the firm's main rivals?

d. Does the organisation target appropriate market segments?

3. Which of the following characteristics is not a test of whether a strategic capability is a core

competence?

a. It provides access to a wide variety of markets.

b. It makes a significant contribution to perceived customer benefits from final products.

c. It is protected by patents.

d. It is hard for competitors to imitate.

20

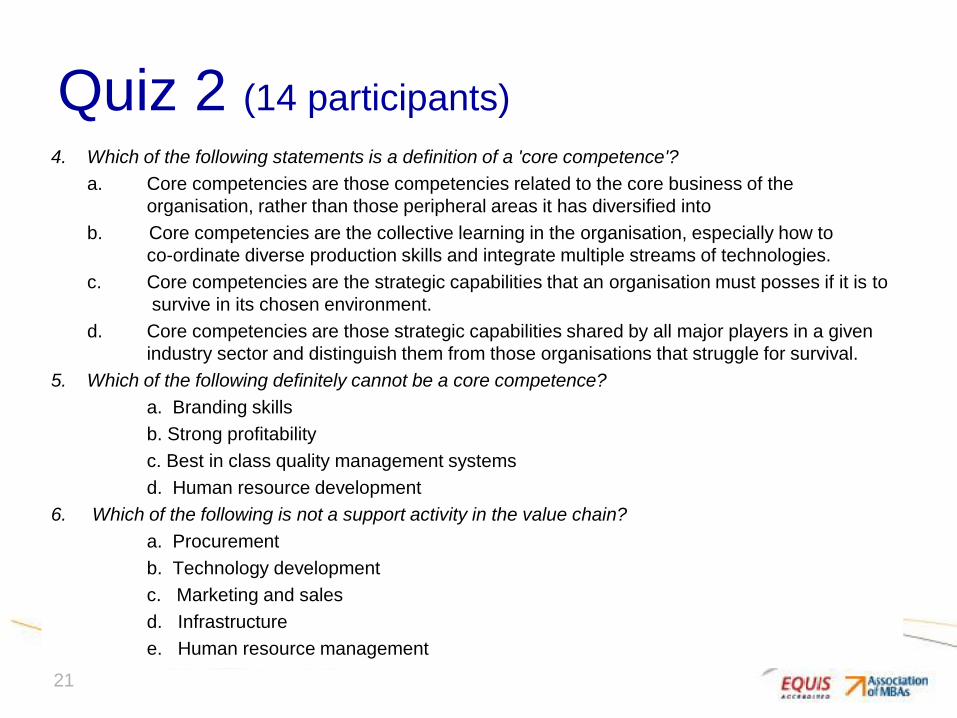

Quiz 2 (14 participants)

4. Which of the following statements is a definition of a 'core competence'?

a. Core competencies are those competencies related to the core business of the

organisation, rather than those peripheral areas it has diversified into

b. Core competencies are the collective learning in the organisation, especially how to

co-ordinate diverse production skills and integrate multiple streams of technologies.

c. Core competencies are the strategic capabilities that an organisation must posses if it is to

survive in its chosen environment.

d. Core competencies are those strategic capabilities shared by all major players in a given

industry sector and distinguish them from those organisations that struggle for survival.

5. Which of the following definitely cannot be a core competence?

a. Branding skills

b. Strong profitability

c. Best in class quality management systems

d. Human resource development

6. Which of the following is not a support activity in the value chain?

a. Procurement

b. Technology development

c. Marketing and sales

d. Infrastructure

e. Human resource management

21

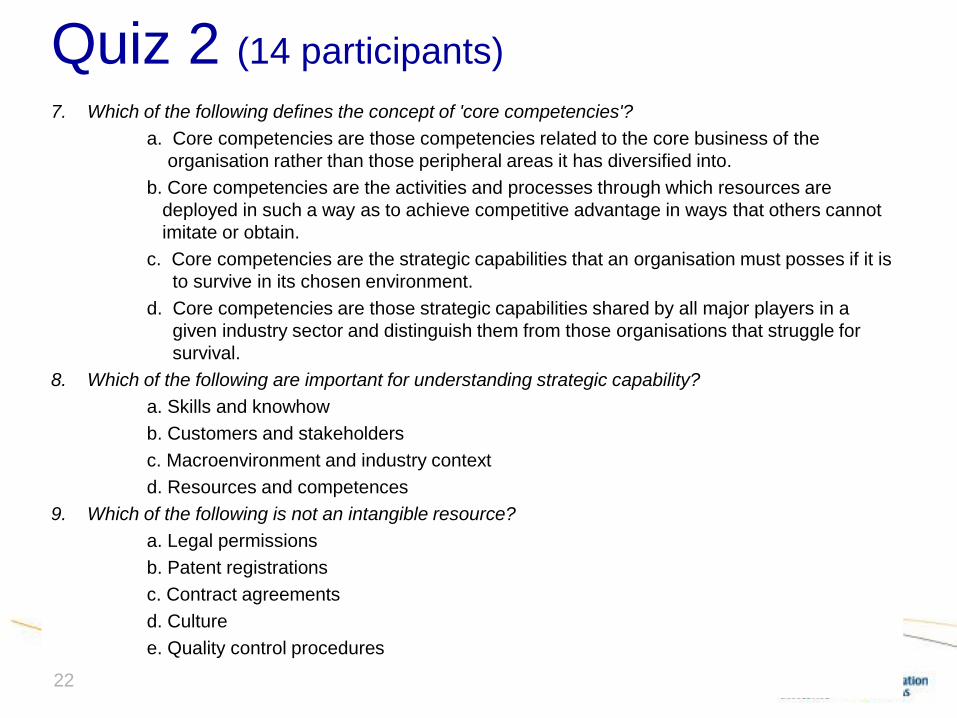

Quiz 2 (14 participants)

7. Which of the following defines the concept of 'core competencies'?

a. Core competencies are those competencies related to the core business of the

organisation rather than those peripheral areas it has diversified into.

b. Core competencies are the activities and processes through which resources are

deployed in such a way as to achieve competitive advantage in ways that others cannot

imitate or obtain.

c. Core competencies are the strategic capabilities that an organisation must posses if it is

to survive in its chosen environment.

d. Core competencies are those strategic capabilities shared by all major players in a

given industry sector and distinguish them from those organisations that struggle for

survival.

8. Which of the following are important for understanding strategic capability?

a. Skills and knowhow

b. Customers and stakeholders

c. Macroenvironment and industry context

d. Resources and competences

9. Which of the following is not an intangible resource?

a. Legal permissions

b. Patent registrations

c. Contract agreements

d. Culture

e. Quality control procedures

22

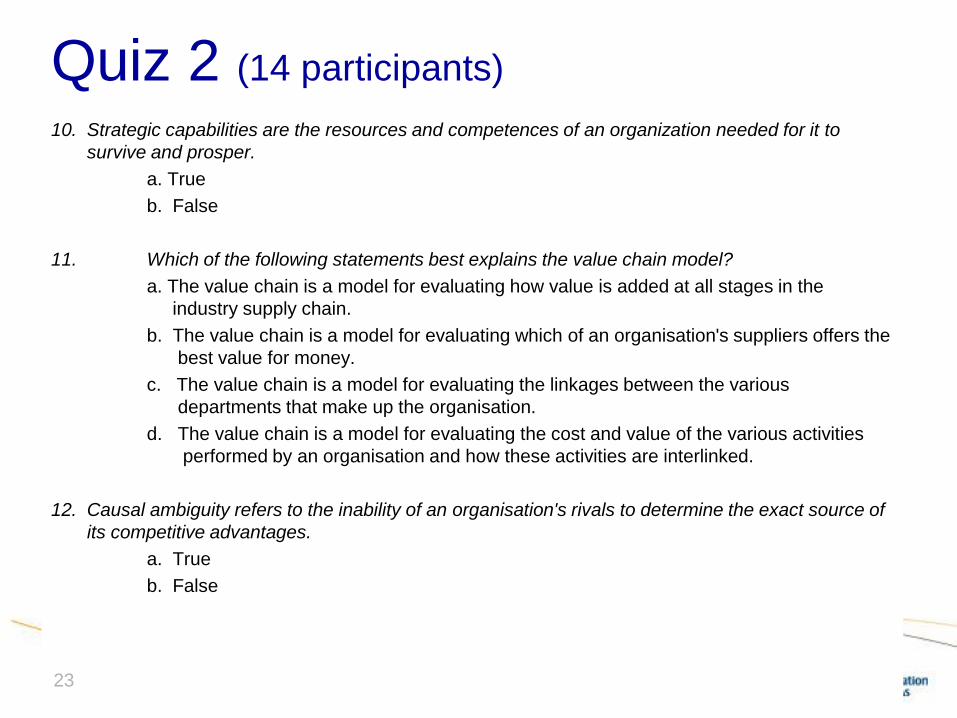

Quiz 2 (14 participants)

10. Strategic capabilities are the resources and competences of an organization needed for it to

survive and prosper.

a. True

b. False

11. Which of the following statements best explains the value chain model?

a. The value chain is a model for evaluating how value is added at all stages in the

industry supply chain.

b. The value chain is a model for evaluating which of an organisation's suppliers offers the

best value for money.

c. The value chain is a model for evaluating the linkages between the various

departments that make up the organisation.

d. The value chain is a model for evaluating the cost and value of the various activities

performed by an organisation and how these activities are interlinked.

12. Causal ambiguity refers to the inability of an organisation's rivals to determine the exact source of

its competitive advantages.

a. True

b. False

23

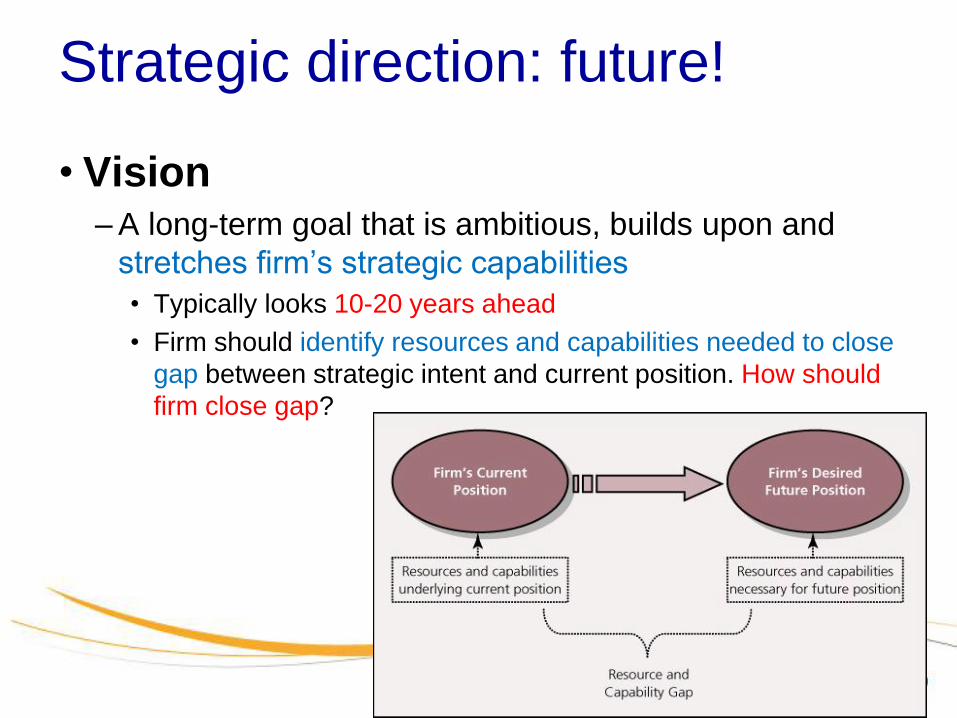

Strategic direction: future!

• Vision – A long-term goal that is ambitious, builds upon and

stretches firm’s strategic capabilities

• Typically looks 10-20 years ahead

• Firm should identify resources and capabilities needed to close

gap between strategic intent and current position. How should

firm close gap?

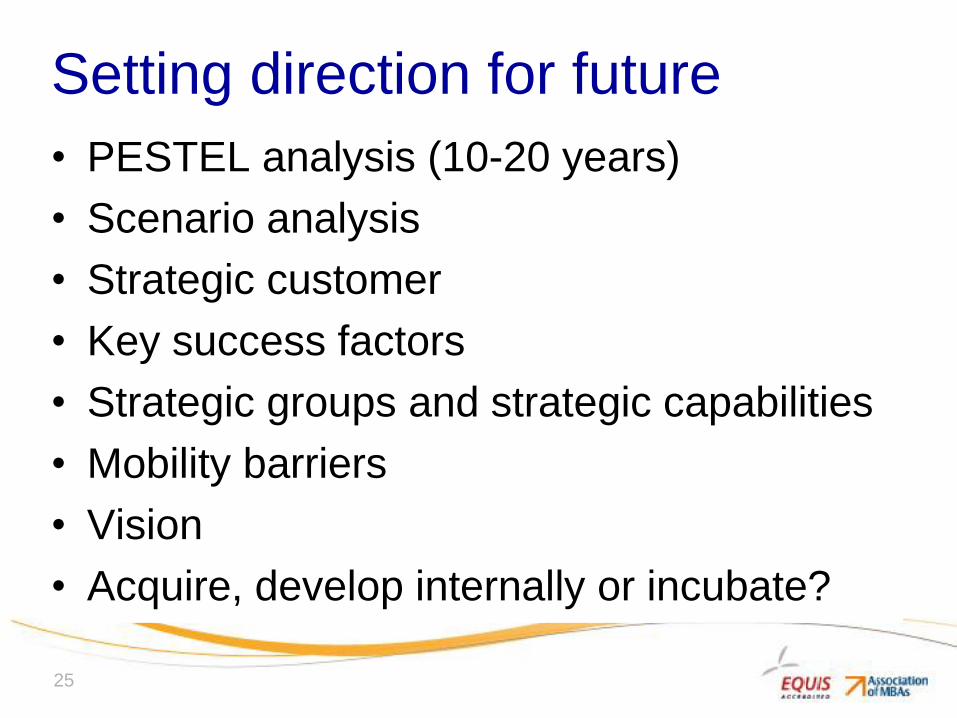

Setting direction for future

• PESTEL analysis (10-20 years)

• Scenario analysis

• Strategic customer

• Key success factors

• Strategic groups and strategic capabilities

• Mobility barriers

• Vision

• Acquire, develop internally or incubate?

25

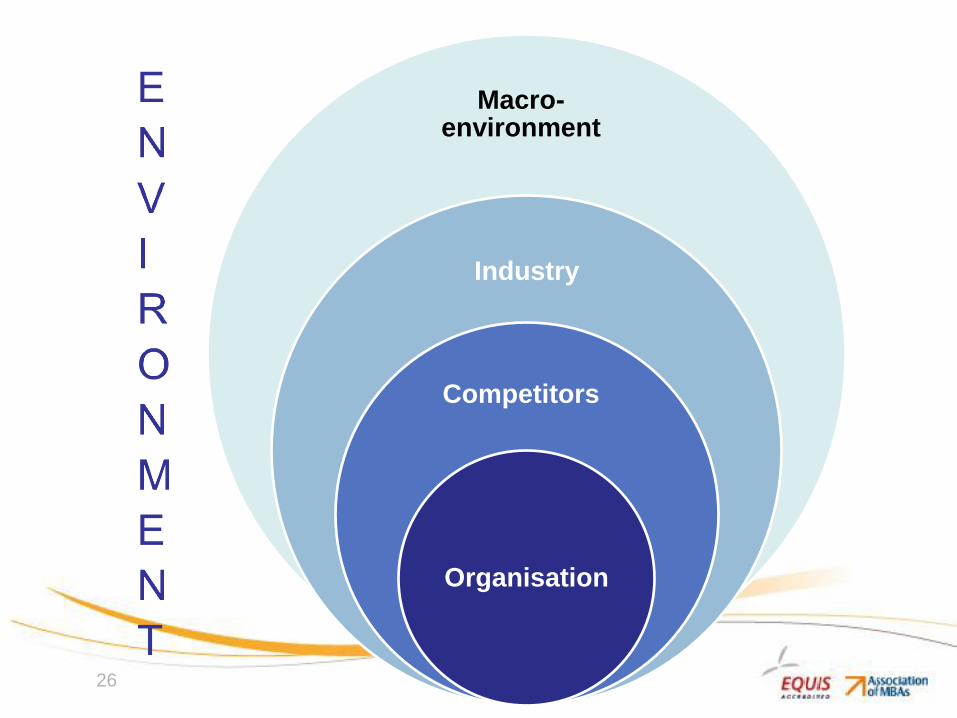

26

Macro-environment

Industry

Competitors

Organisation

27

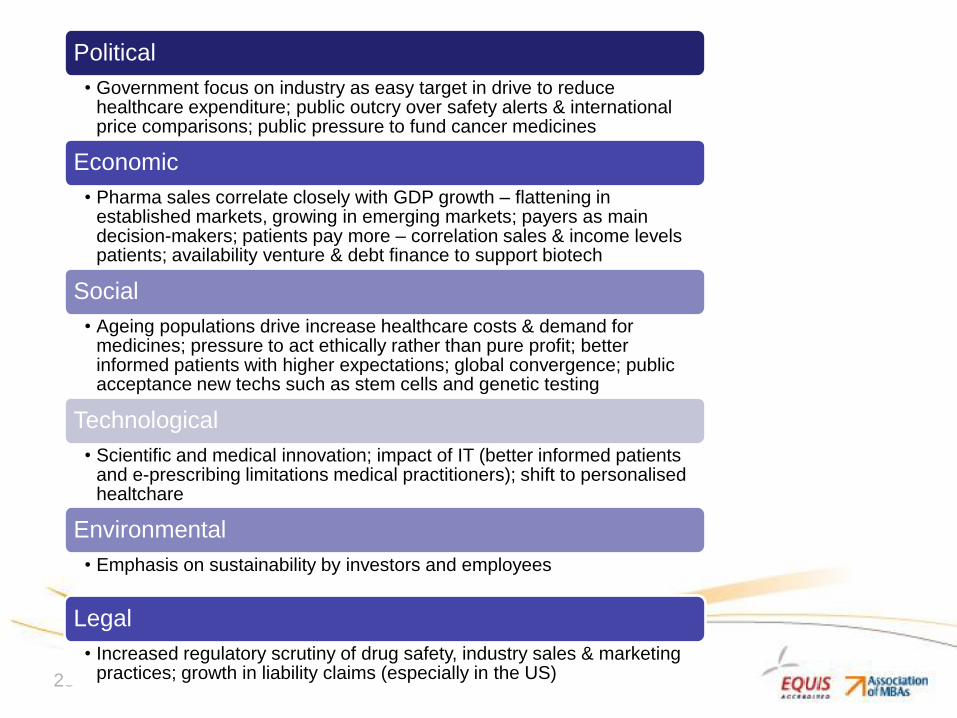

Political

• ?

Economic

• ?

Social

• ?

Technological

• ?

Environmental

• ?

Legal

• ?

28

Political

• Government focus on industry as easy target in drive to reduce healthcare expenditure; public outcry over safety alerts & international price comparisons; public pressure to fund cancer medicines

Economic

• Pharma sales correlate closely with GDP growth – flattening in established markets, growing in emerging markets; payers as main decision-makers; patients pay more – correlation sales & income levels patients; availability venture & debt finance to support biotech

Social

• Ageing populations drive increase healthcare costs & demand for medicines; pressure to act ethically rather than pure profit; better informed patients with higher expectations; global convergence; public acceptance new techs such as stem cells and genetic testing

Technological

• Scientific and medical innovation; impact of IT (better informed patients and e-prescribing limitations medical practitioners); shift to personalised healtchare

Environmental

• Emphasis on sustainability by investors and employees

Legal

• Increased regulatory scrutiny of drug safety, industry sales & marketing practices; growth in liability claims (especially in the US)

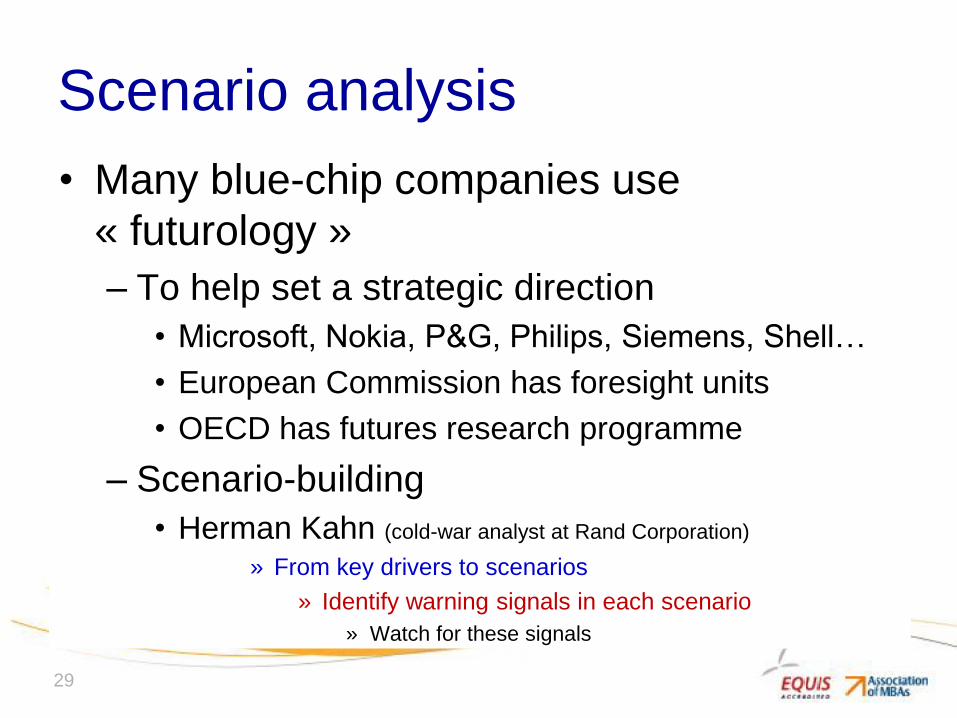

Scenario analysis

• Many blue-chip companies use

« futurology »

– To help set a strategic direction

• Microsoft, Nokia, P&G, Philips, Siemens, Shell…

• European Commission has foresight units

• OECD has futures research programme

– Scenario-building

• Herman Kahn (cold-war analyst at Rand Corporation)

» From key drivers to scenarios

» Identify warning signals in each scenario

» Watch for these signals

29

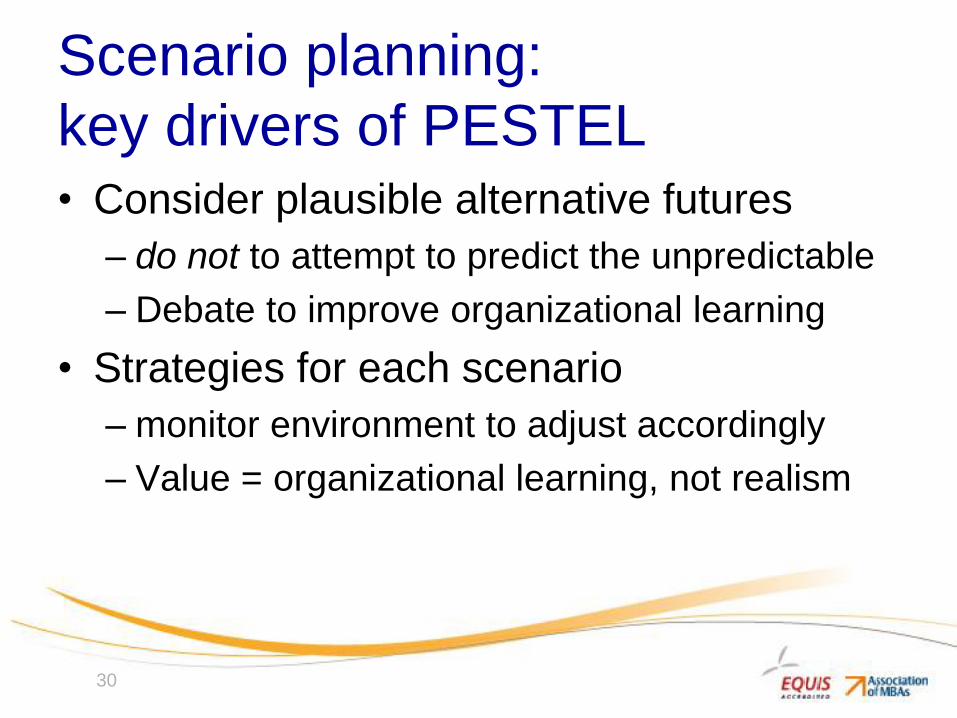

Scenario planning:

key drivers of PESTEL • Consider plausible alternative futures

– do not to attempt to predict the unpredictable

– Debate to improve organizational learning

• Strategies for each scenario

– monitor environment to adjust accordingly

– Value = organizational learning, not realism

30

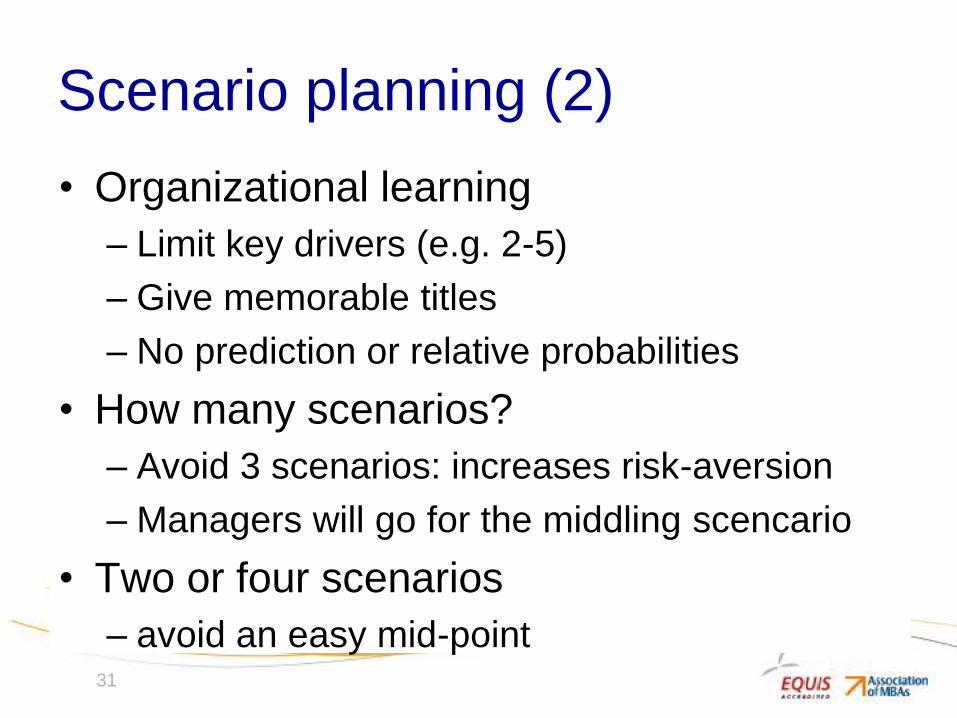

• Organizational learning

– Limit key drivers (e.g. 2-5)

– Give memorable titles

– No prediction or relative probabilities

• How many scenarios?

– Avoid 3 scenarios: increases risk-aversion

– Managers will go for the middling scencario

• Two or four scenarios

– avoid an easy mid-point

31

Scenario planning (2)

Selecting key drivers

• Focus on drivers (2 to 5) that are likely to?

– Have a high impact on the industry

– Bring most uncertainty to the industry

32

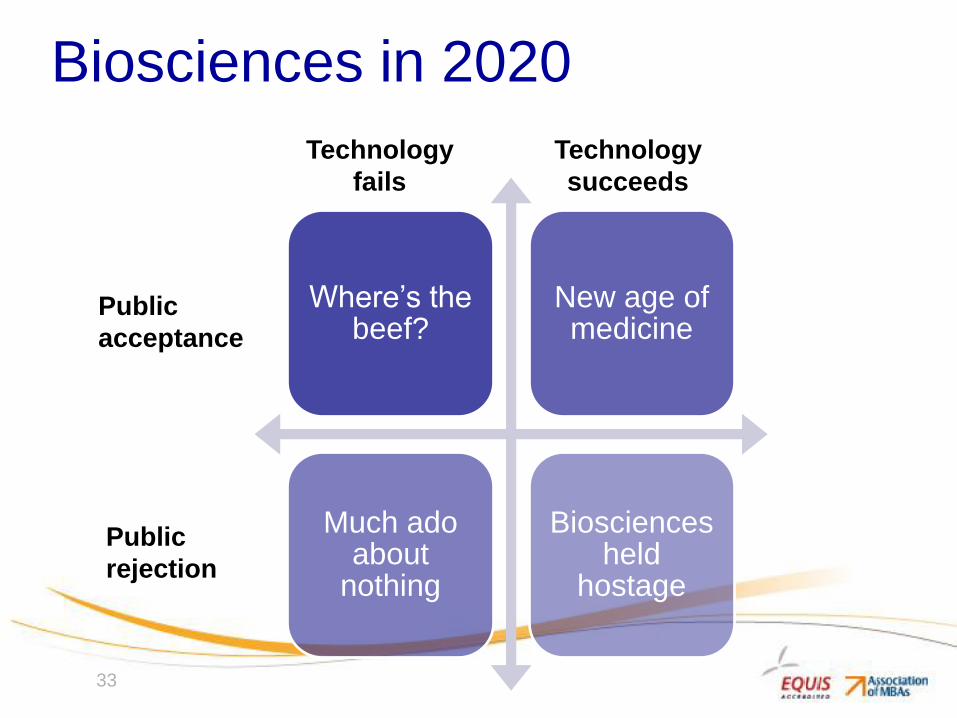

Biosciences in 2020

33

Where’s the beef?

New age of medicine

Much ado about

nothing

Biosciences held

hostage

Public

acceptance

Public

rejection

Technology

fails

Technology

succeeds

Case pharmaceutical industry

• Reading

– « The global pharmaceutical industry:

swallowing a bitter pill »

– Questions

• PESTEL analysis

• Key drivers of PESTEL?

• Scenarios?

• Strategic customer

34

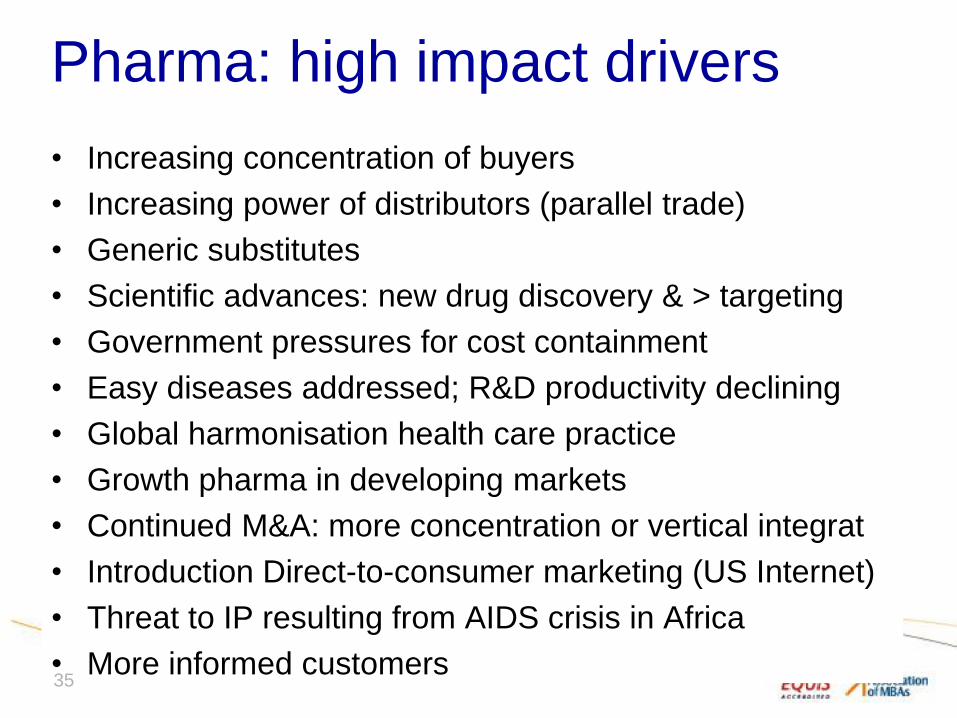

Pharma: high impact drivers

• Increasing concentration of buyers

• Increasing power of distributors (parallel trade)

• Generic substitutes

• Scientific advances: new drug discovery & > targeting

• Government pressures for cost containment

• Easy diseases addressed; R&D productivity declining

• Global harmonisation health care practice

• Growth pharma in developing markets

• Continued M&A: more concentration or vertical integrat

• Introduction Direct-to-consumer marketing (US Internet)

• Threat to IP resulting from AIDS crisis in Africa

• More informed customers 35

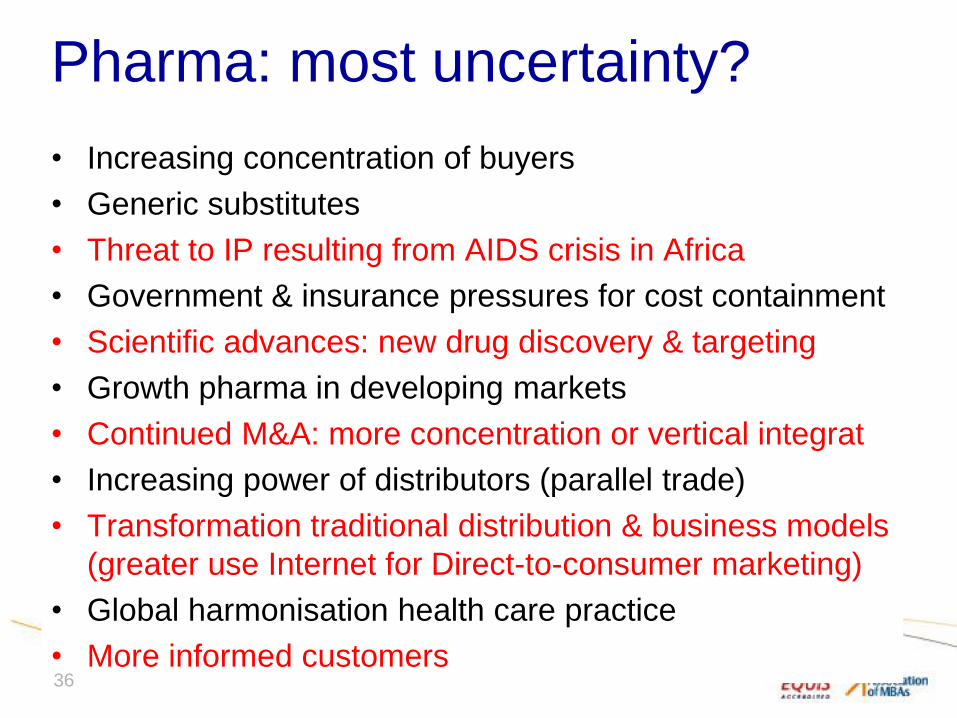

Pharma: most uncertainty?

• Increasing concentration of buyers

• Generic substitutes

• Threat to IP resulting from AIDS crisis in Africa

• Government & insurance pressures for cost containment

• Scientific advances: new drug discovery & targeting

• Growth pharma in developing markets

• Continued M&A: more concentration or vertical integrat

• Increasing power of distributors (parallel trade)

• Transformation traditional distribution & business models

(greater use Internet for Direct-to-consumer marketing)

• Global harmonisation health care practice

• More informed customers 36

37

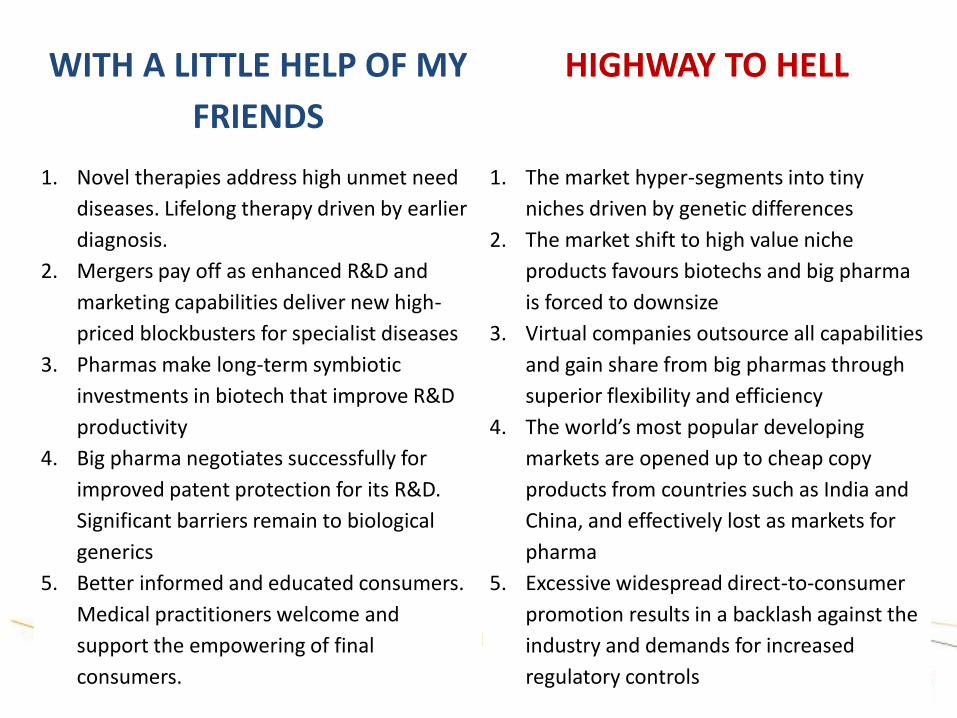

WITH A LITTLE HELP OF MY

FRIENDS

HIGHWAY TO HELL

1. Novel therapies address high unmet need

diseases. Lifelong therapy driven by earlier

diagnosis.

2. Mergers pay off as enhanced R&D and

marketing capabilities deliver new high-

priced blockbusters for specialist diseases

3. Pharmas make long-term symbiotic

investments in biotech that improve R&D

productivity

4. Big pharma negotiates successfully for

improved patent protection for its R&D.

Significant barriers remain to biological

generics

5. Better informed and educated consumers.

Medical practitioners welcome and

support the empowering of final

consumers.

1. The market hyper-segments into tiny

niches driven by genetic differences

2. The market shift to high value niche

products favours biotechs and big pharma

is forced to downsize

3. Virtual companies outsource all capabilities

and gain share from big pharmas through

superior flexibility and efficiency

4. The world’s most popular developing

markets are opened up to cheap copy

products from countries such as India and

China, and effectively lost as markets for

pharma

5. Excessive widespread direct-to-consumer

promotion results in a backlash against the

industry and demands for increased

regulatory controls

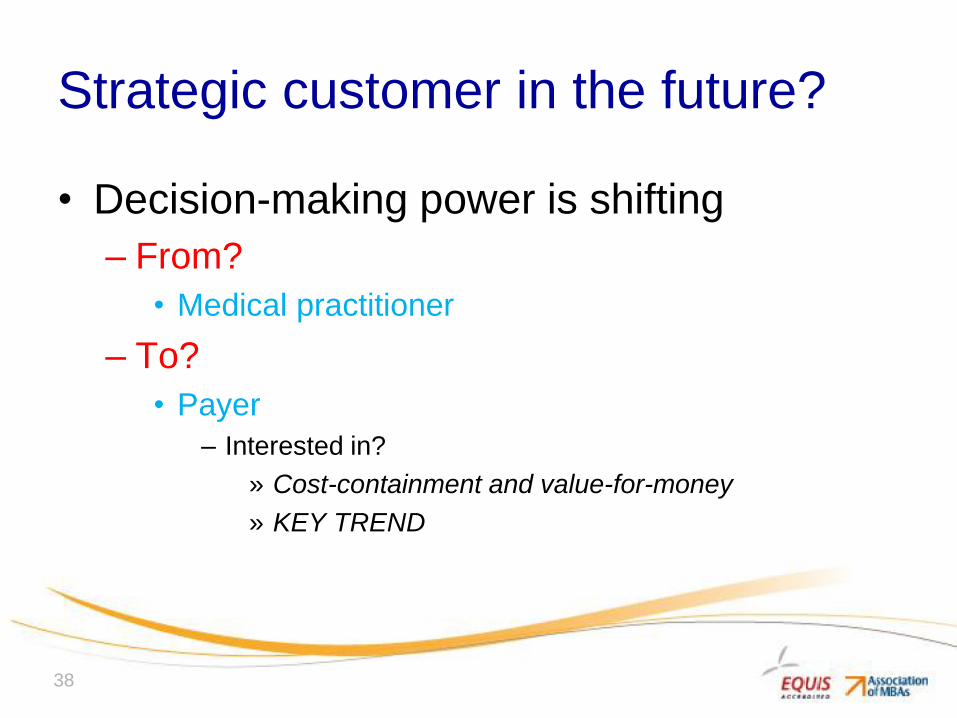

Strategic customer in the future?

• Decision-making power is shifting

– From?

• Medical practitioner

– To?

• Payer

– Interested in?

» Cost-containment and value-for-money

» KEY TREND

38

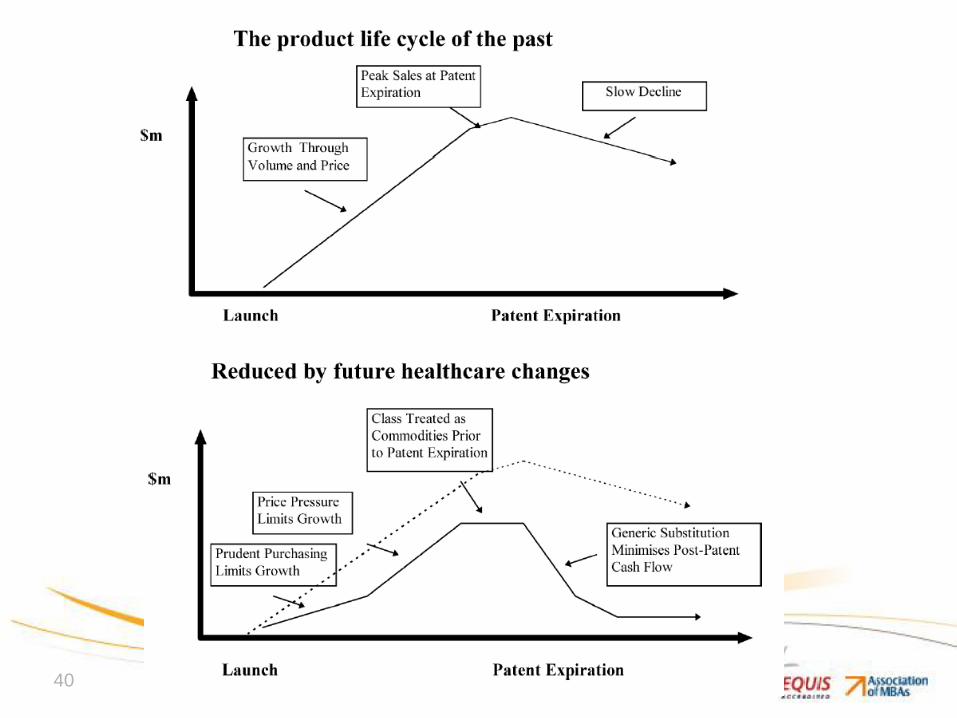

Key success factors in the future?

• Past ksf?

– Size R&D investments

• To introduce blockbuster brands

– Effective marketing and large sales forces

• To undertake customer « detailing »

• Past market leaders?

– Blockbuster model

• Brands that offered moderate improvements

– In tolerability & convenience

– Sustainably protected by patents 39

40

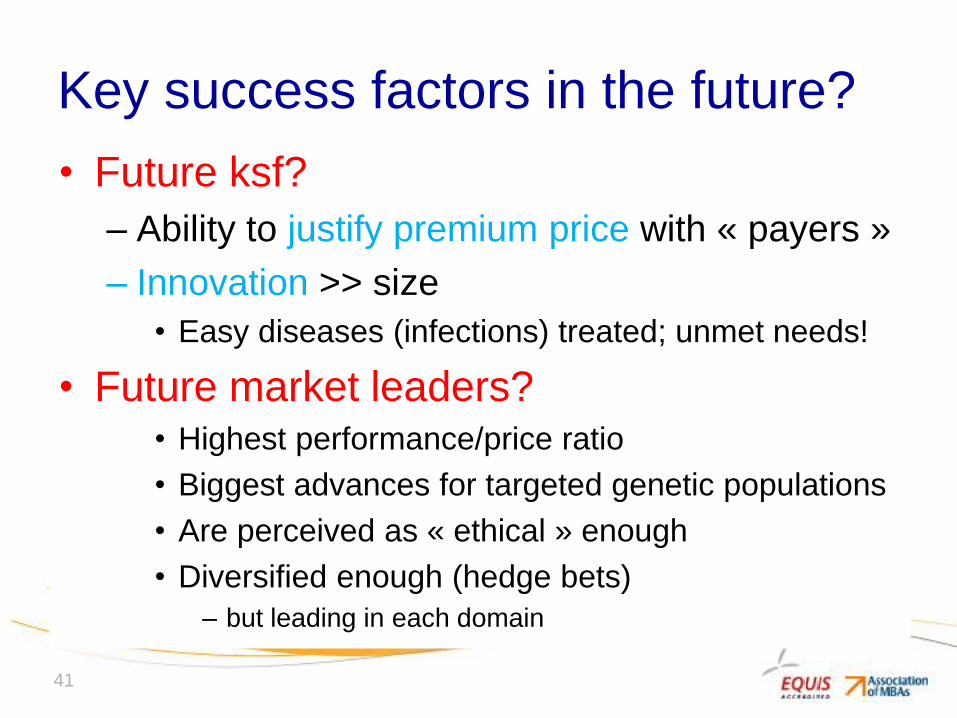

Key success factors in the future?

• Future ksf?

– Ability to justify premium price with « payers »

– Innovation >> size

• Easy diseases (infections) treated; unmet needs!

• Future market leaders? • Highest performance/price ratio

• Biggest advances for targeted genetic populations

• Are perceived as « ethical » enough

• Diversified enough (hedge bets)

– but leading in each domain

41

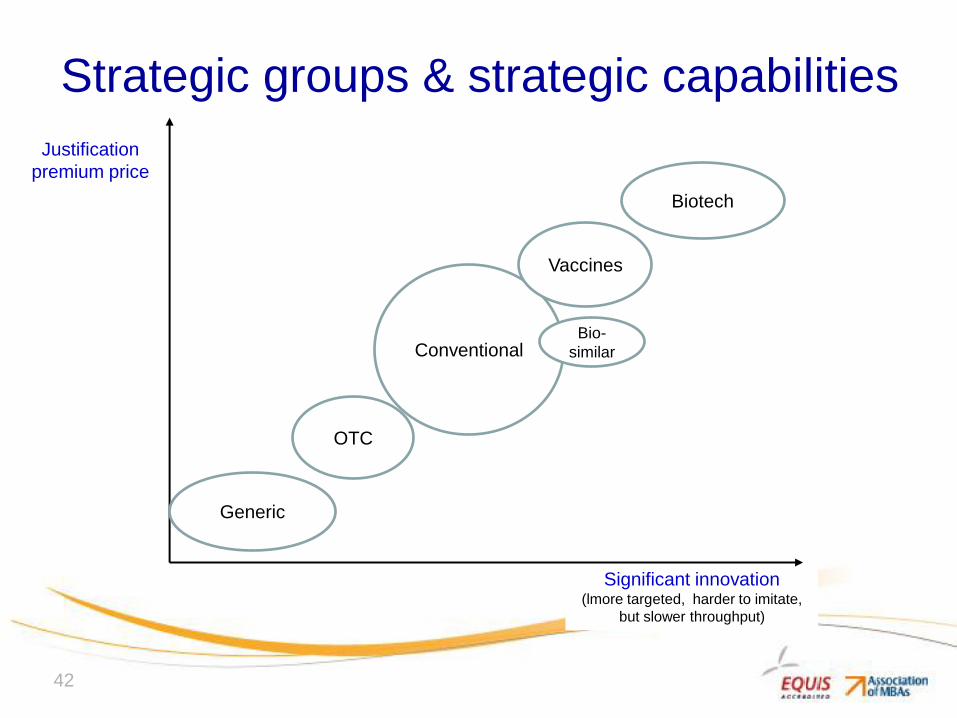

Significant innovation (lmore targeted, harder to imitate,

but slower throughput)

Strategic groups & strategic capabilities

42

Justification

premium price

Generic

Conventional

Vaccines

Biotech

OTC

Bio-

similar

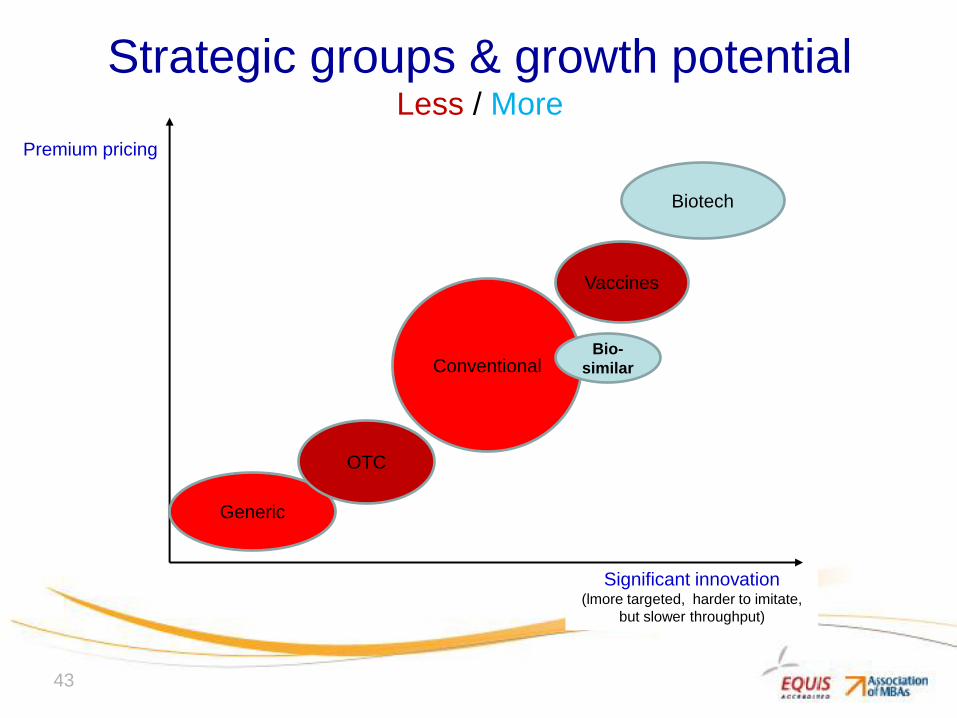

Significant innovation (lmore targeted, harder to imitate,

but slower throughput)

Strategic groups & growth potential Less / More

43

Premium pricing

Generic

Biotech

Conventional

Vaccines

OTC

Bio-

similar

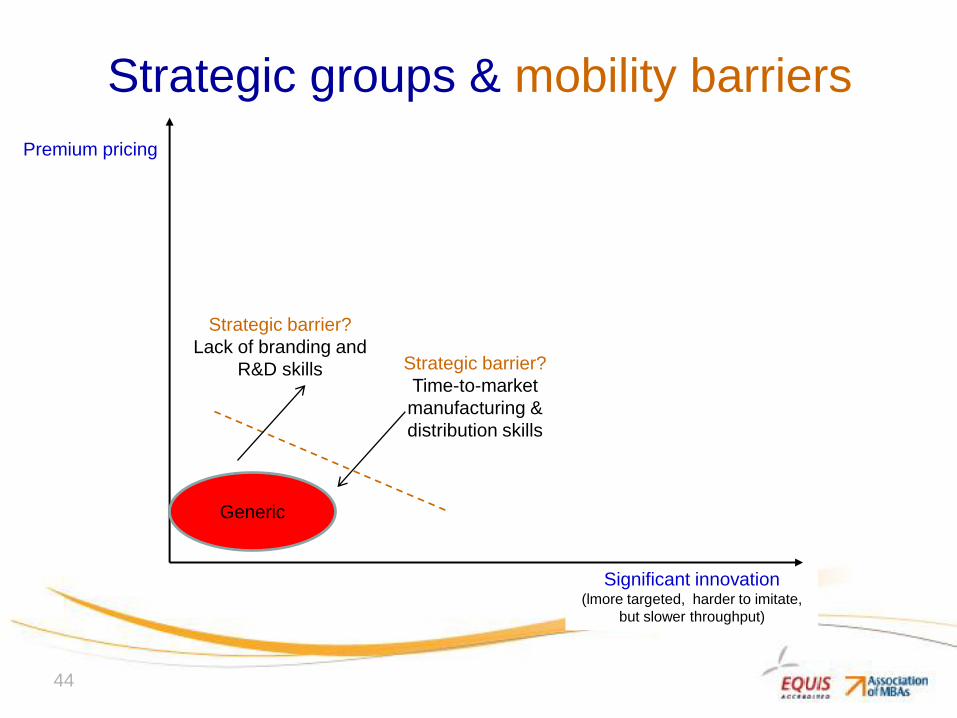

Significant innovation (lmore targeted, harder to imitate,

but slower throughput)

Strategic groups & mobility barriers

44

Premium pricing

Generic

Strategic barrier?

Lack of branding and

R&D skills Strategic barrier?

Time-to-market

manufacturing &

distribution skills

Significant innovation (lmore targeted, harder to imitate,

but slower throughput)

Strategic groups & mobility barriers

45

Premium pricing

Strategic barrier?

Highly consolidated,

specialised skills required

in manufacturing, clinical

trials…

Strategic barrier?

Huge amounts of

financial, marketing and

distribution capacity

needed

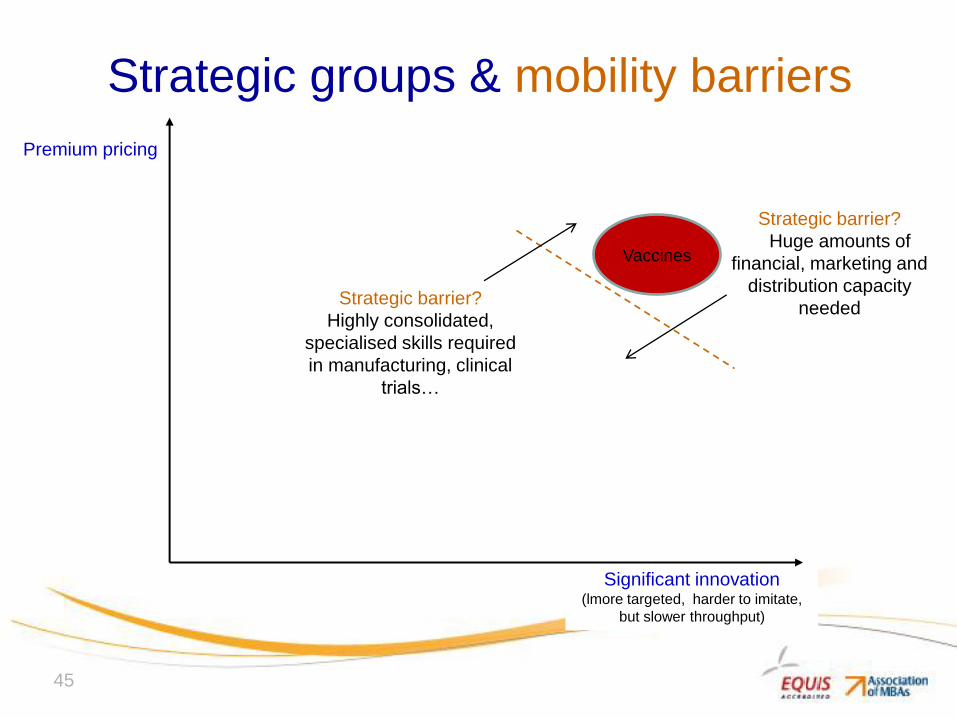

Vaccines

Significant innovation (lmore targeted, harder to imitate,

but slower throughput)

Strategic groups & mobility barriers

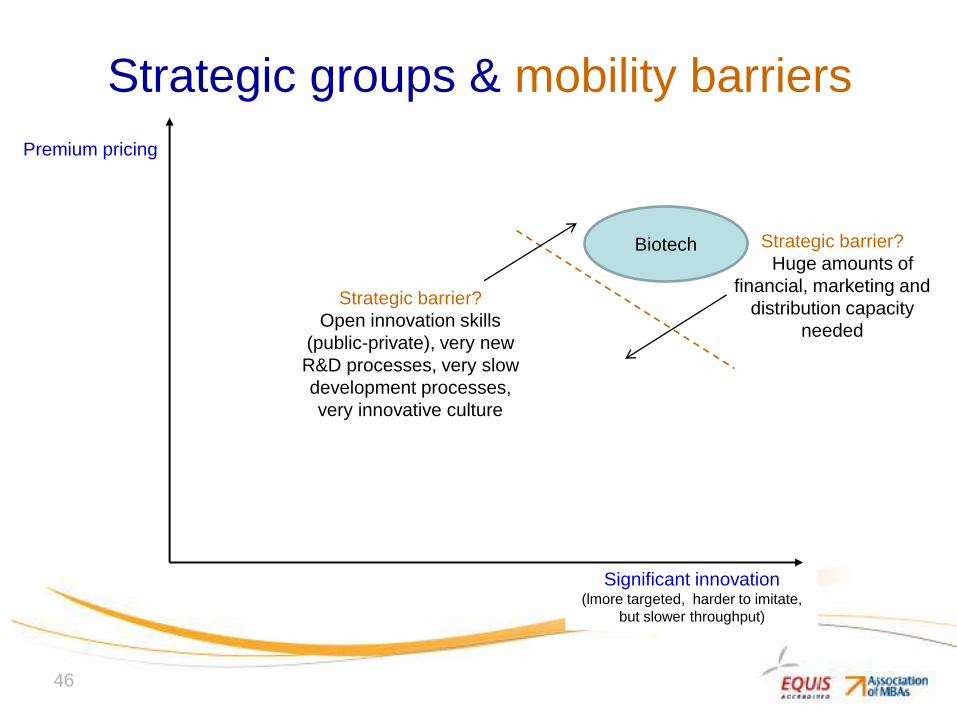

46

Premium pricing

Strategic barrier?

Open innovation skills

(public-private), very new

R&D processes, very slow

development processes,

very innovative culture

Strategic barrier?

Huge amounts of

financial, marketing and

distribution capacity

needed

Biotech

Significant innovation (lmore targeted, harder to imitate,

but slower throughput)

Strategic groups & mobility barriers

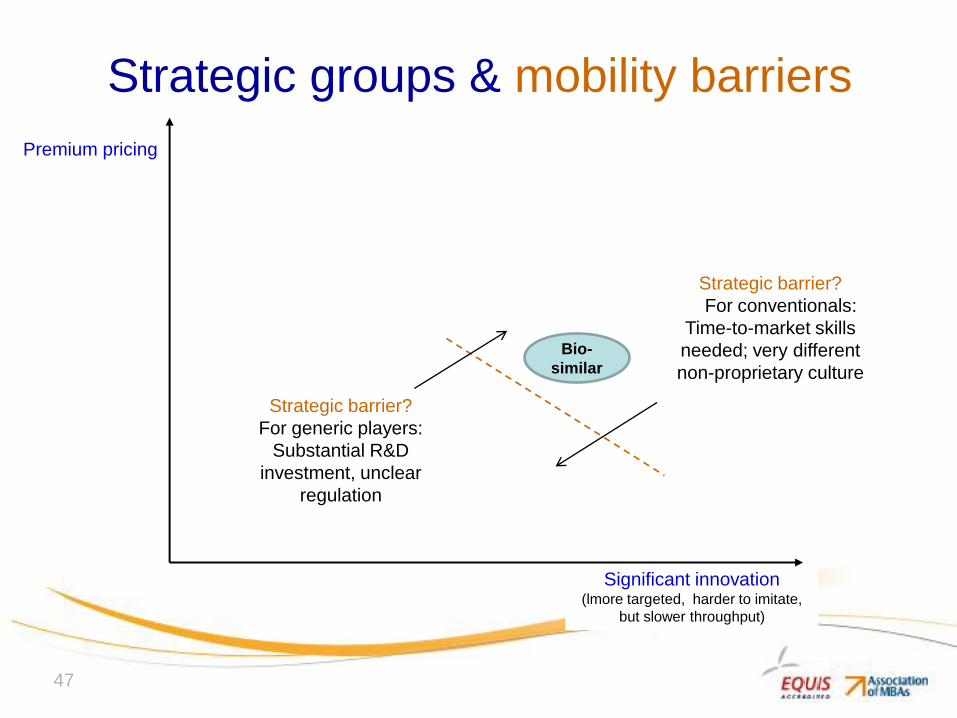

47

Premium pricing

Bio-

similar

Strategic barrier?

For generic players:

Substantial R&D

investment, unclear

regulation

Strategic barrier?

For conventionals:

Time-to-market skills

needed; very different

non-proprietary culture

Significant innovation (lmore targeted, harder to imitate,

but slower throughput)

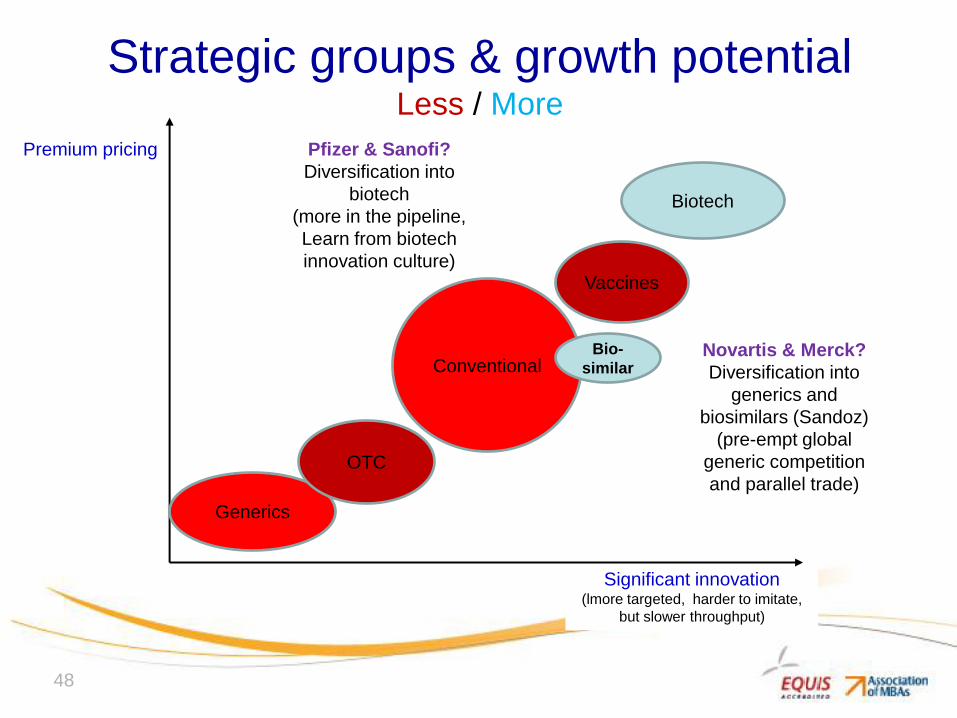

Strategic groups & growth potential Less / More

48

Premium pricing

Generics

Biotech

Conventional

Vaccines

OTC

Bio-

similar Novartis & Merck?

Diversification into

generics and

biosimilars (Sandoz)

(pre-empt global

generic competition

and parallel trade)

Pfizer & Sanofi?

Diversification into

biotech

(more in the pipeline,

Learn from biotech

innovation culture)