technology venture capital financing in canada (h1 2016) - extreme venture partners

TRANSCRIPT

Technology Venture Capital Financing in Canada

H1 2016

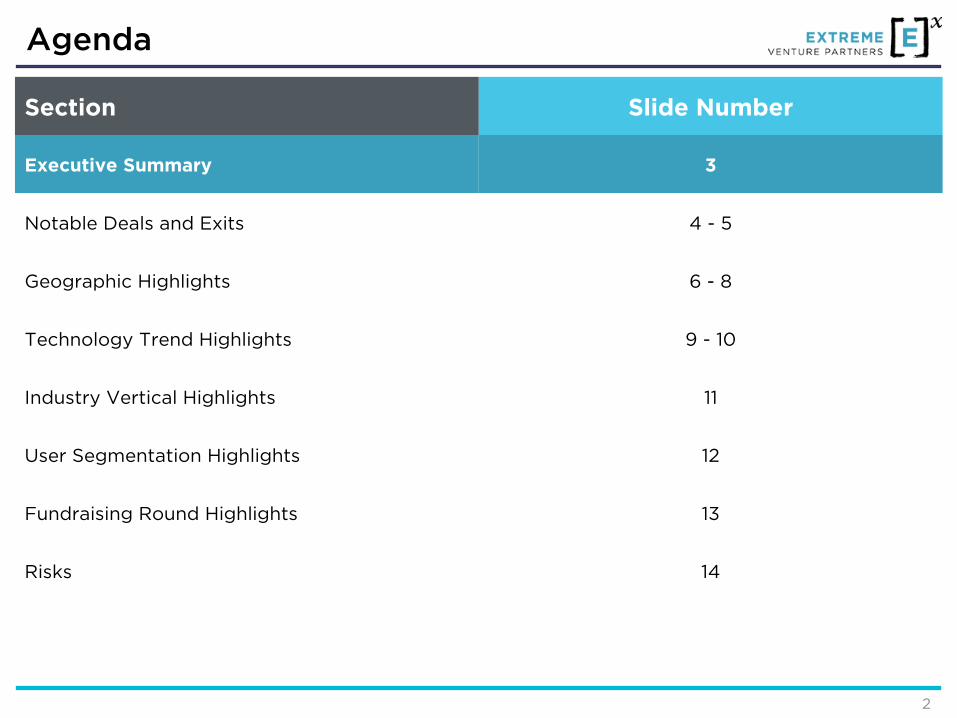

Agenda

Section Slide Number

Executive Summary 3

Notable Deals and Exits 4 - 5

Geographic Highlights 6 - 8

Technology Trend Highlights 9 - 10

Industry Vertical Highlights 11

User Segmentation Highlights 12

Fundraising Round Highlights 13

Risks 14

2

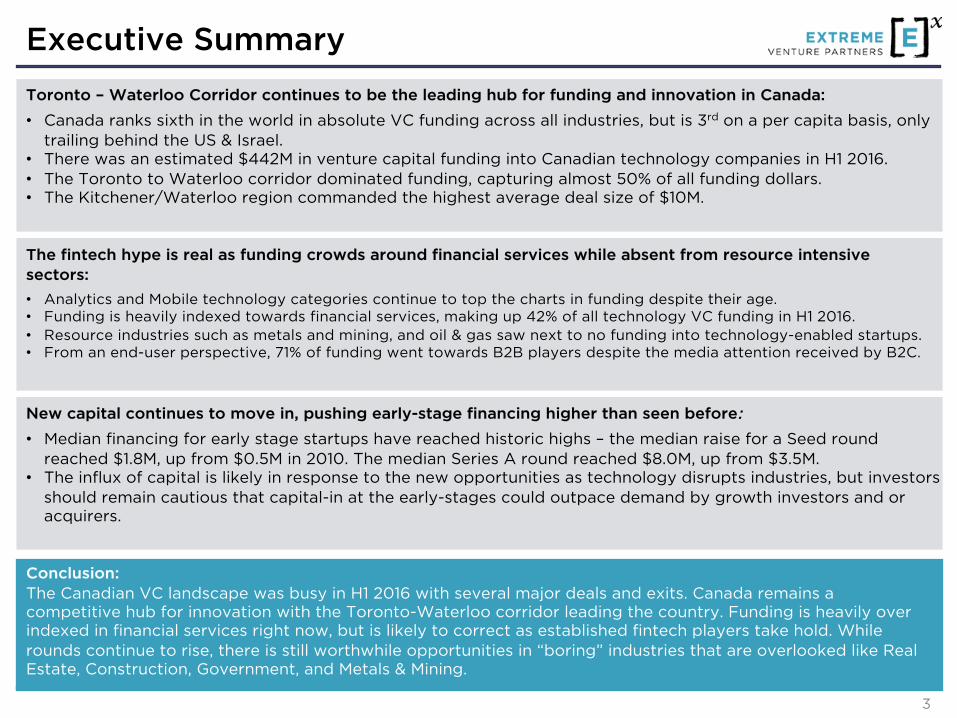

Executive Summary

Conclusion:The Canadian VC landscape was busy in H1 2016 with several major deals and exits. Canada remains a competitive hub for innovation with the Toronto-Waterloo corridor leading the country. Funding is heavily over indexed in financial services right now, but is likely to correct as established fintech players take hold. While rounds continue to rise, there is still worthwhile opportunities in “boring” industries that are overlooked like Real Estate, Construction, Government, and Metals & Mining.

Toronto – Waterloo Corridor continues to be the leading hub for funding and innovation in Canada:

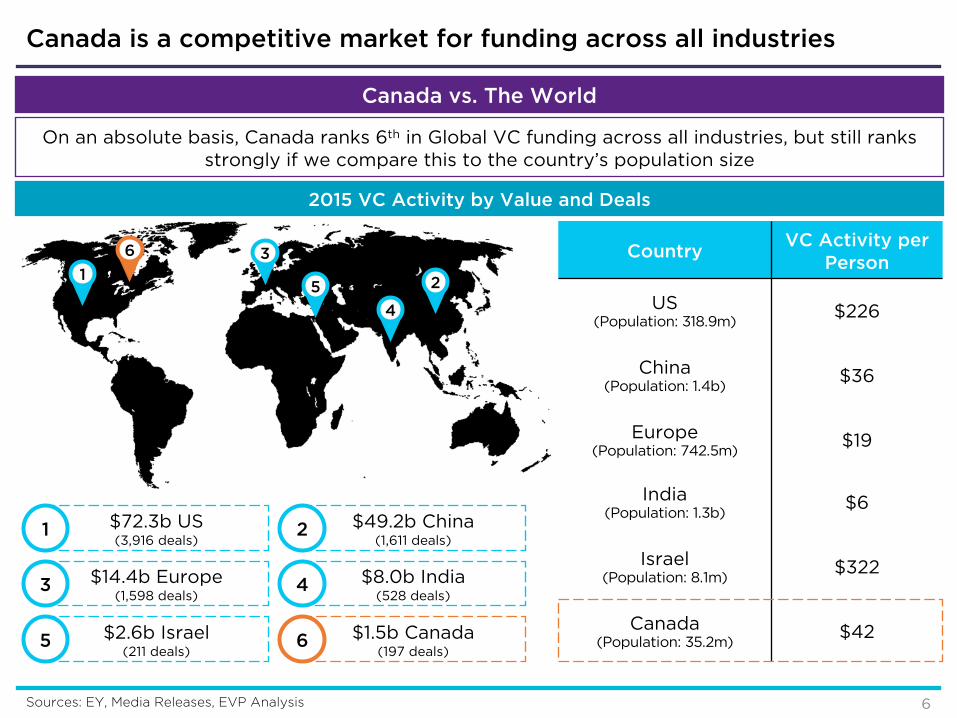

• Canada ranks sixth in the world in absolute VC funding across all industries, but is 3rd on a per capita basis, only trailing behind the US & Israel.

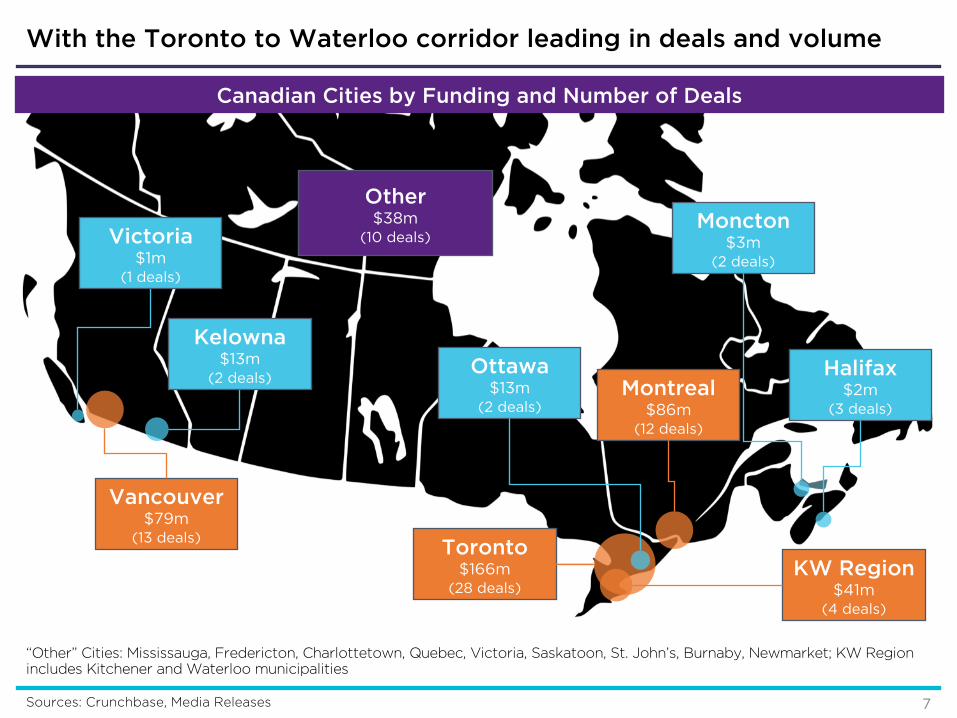

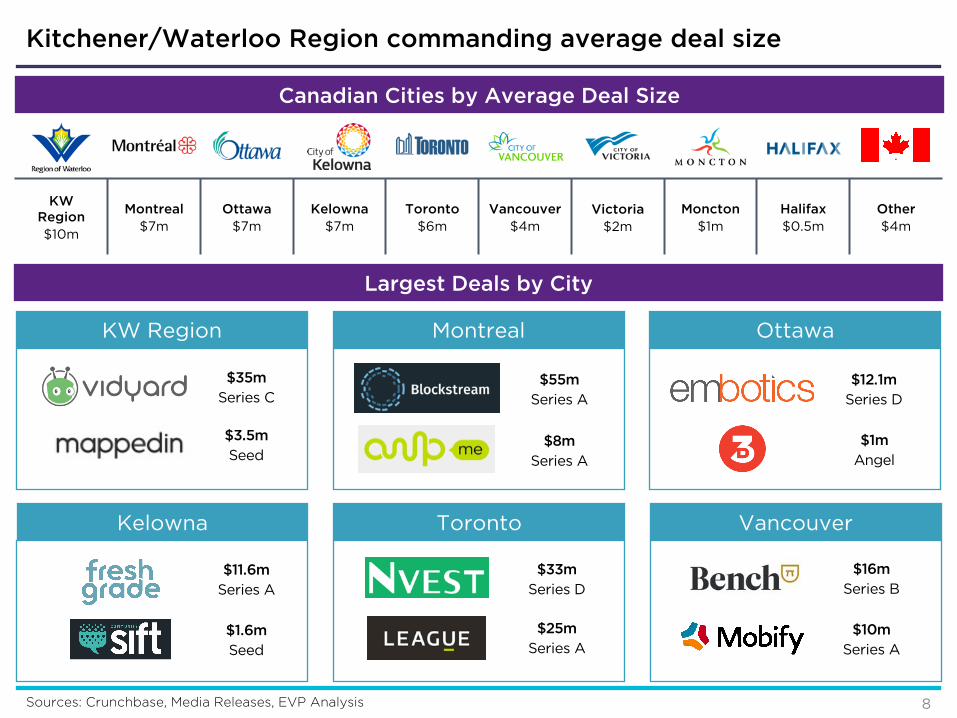

• There was an estimated $442M in venture capital funding into Canadian technology companies in H1 2016.• The Toronto to Waterloo corridor dominated funding, capturing almost 50% of all funding dollars.• The Kitchener/Waterloo region commanded the highest average deal size of $10M.

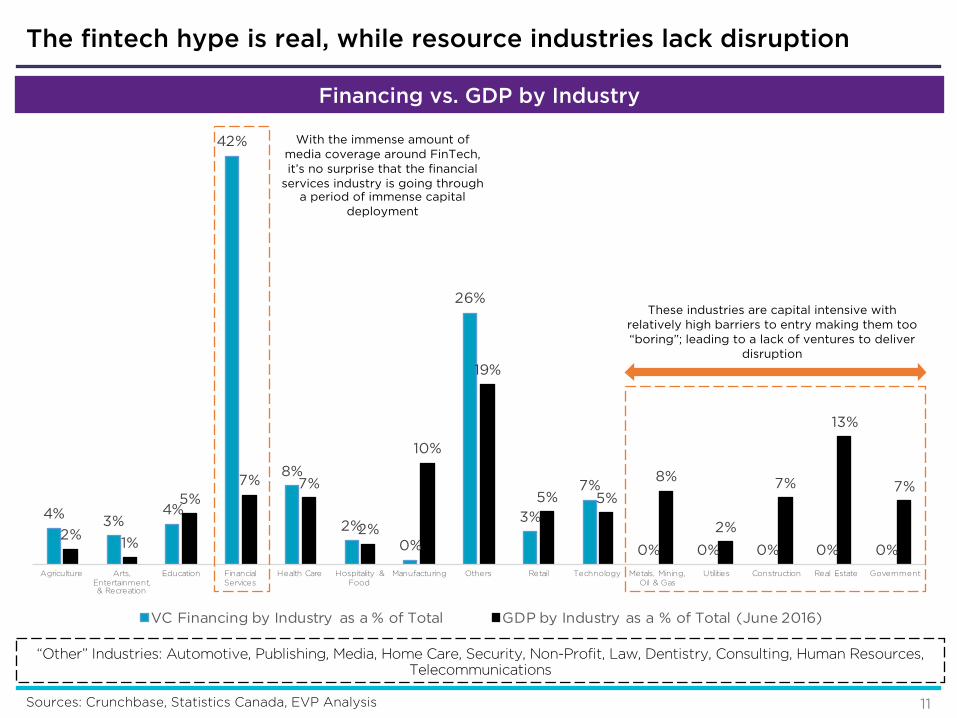

The fintech hype is real as funding crowds around financial services while absent from resource intensive sectors:

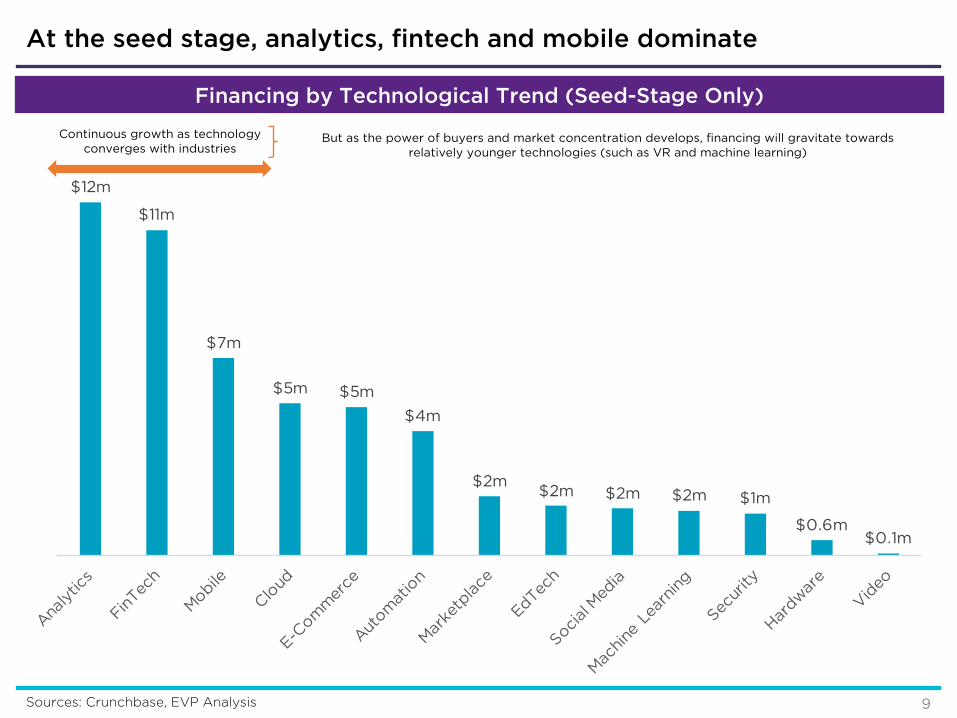

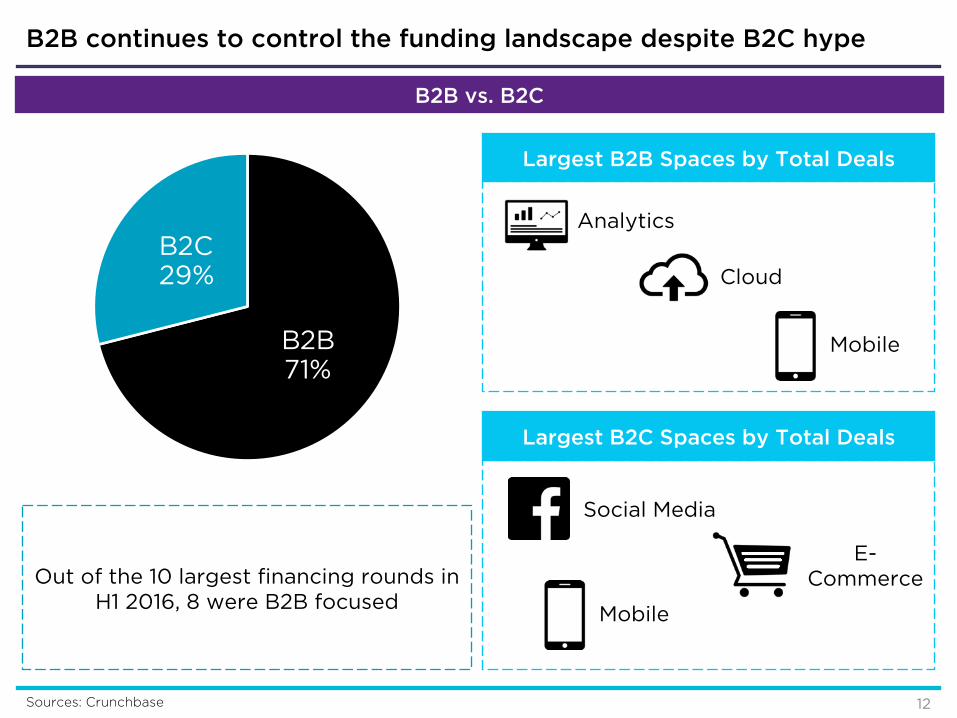

• Analytics and Mobile technology categories continue to top the charts in funding despite their age.• Funding is heavily indexed towards financial services, making up 42% of all technology VC funding in H1 2016.• Resource industries such as metals and mining, and oil & gas saw next to no funding into technology-enabled startups.• From an end-user perspective, 71% of funding went towards B2B players despite the media attention received by B2C.

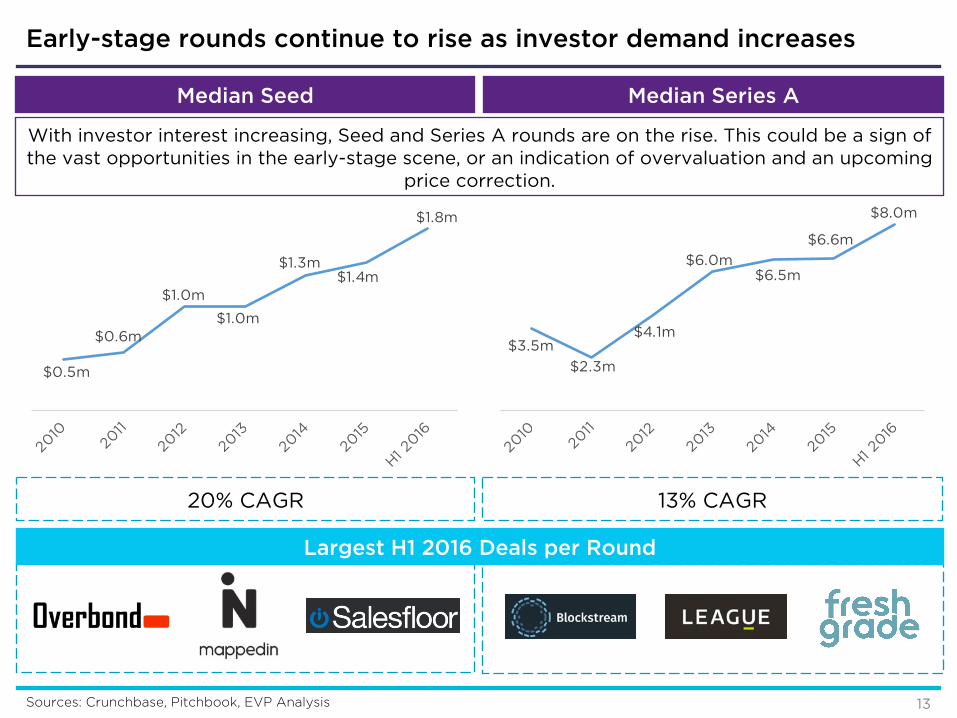

New capital continues to move in, pushing early-stage financing higher than seen before:

• Median financing for early stage startups have reached historic highs – the median raise for a Seed round reached $1.8M, up from $0.5M in 2010. The median Series A round reached $8.0M, up from $3.5M.

• The influx of capital is likely in response to the new opportunities as technology disrupts industries, but investors should remain cautious that capital-in at the early-stages could outpace demand by growth investors and or acquirers.

3

Sources: Crunchbase, CVCA

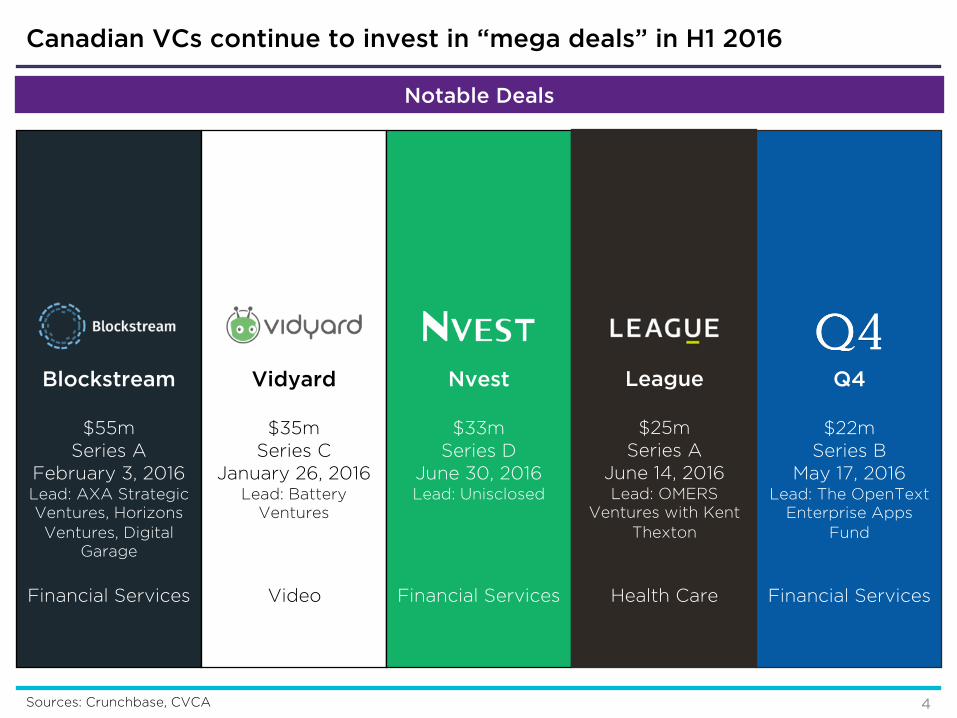

Notable Deals

Blockstream

$55mSeries A

February 3, 2016Lead: AXA Strategic Ventures, Horizons Ventures, Digital

Garage

Vidyard

$35mSeries C

January 26, 2016Lead: Battery

Ventures

Nvest

$33mSeries D

June 30, 2016Lead: Unisclosed

Canadian VCs continue to invest in “mega deals” in H1 2016

Financial Services Video Financial Services

League

$25mSeries A

June 14, 2016Lead: OMERS

Ventures with Kent Thexton

Health Care

4

Q4

$22mSeries B

May 17, 2016Lead: The OpenText

Enterprise Apps Fund

Financial Services

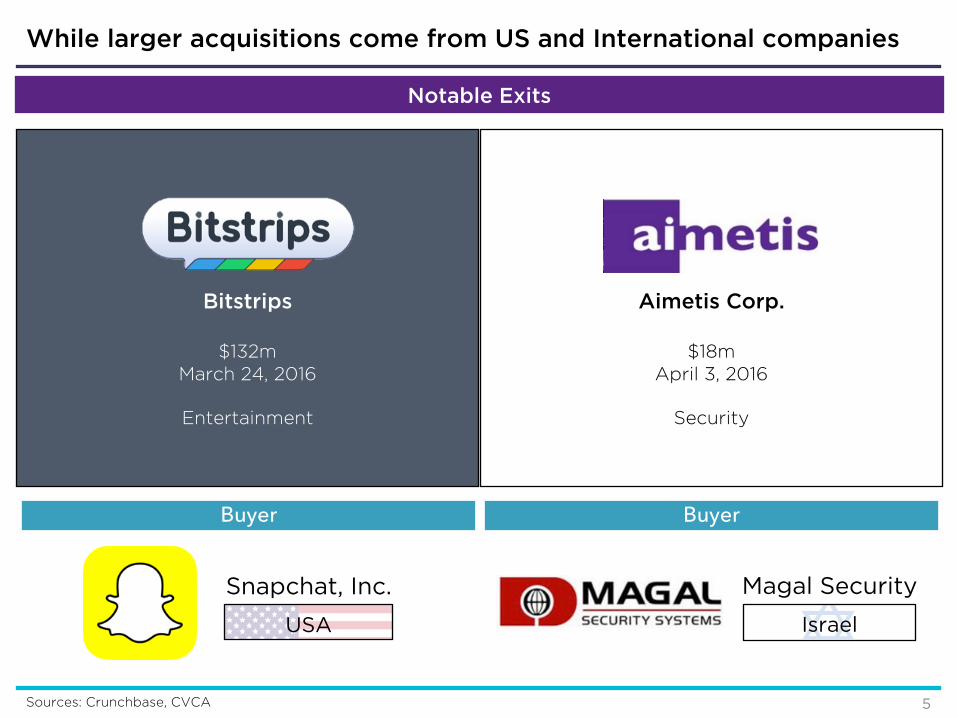

Notable Exits

Bitstrips

$132mMarch 24, 2016

Entertainment

Buyer

Aimetis Corp.

$18mApril 3, 2016

Security

Buyer

Sources: Crunchbase, CVCA

While larger acquisitions come from US and International companies

Snapchat, Inc.

USA

Magal Security

Israel

5

On an absolute basis, Canada ranks 6th in Global VC funding across all industries, but still ranks strongly if we compare this to the country’s population size

2015 VC Activity by Value and Deals

1 2

3

4

5

6

$72.3b US(3,916 deals)

1 $49.2b China(1,611 deals)

2

$14.4b Europe(1,598 deals)

3 $8.0b India(528 deals)

4

$2.6b Israel(211 deals)

5 $1.5b Canada(197 deals)

6

CountryVC Activity per

Person

US(Population: 318.9m)

$226

China(Population: 1.4b)

$36

Europe(Population: 742.5m)

$19

India(Population: 1.3b)

$6

Israel(Population: 8.1m)

$322

Canada(Population: 35.2m)

$42

Sources: EY, Media Releases, EVP Analysis

Canada vs. The World

Canada is a competitive market for funding across all industries

6

“Other” Cities: Mississauga, Fredericton, Charlottetown, Quebec, Victoria, Saskatoon, St. John’s, Burnaby, Newmarket; KW Region includes Kitchener and Waterloo municipalities

Sources: Crunchbase, Media Releases

Canadian Cities by Funding and Number of Deals

Toronto$166m

(28 deals)

Montreal$86m

(12 deals)

Vancouver$79m

(13 deals)

KW Region$41m

(4 deals)

Ottawa$13m

(2 deals)

Moncton$3m

(2 deals)

Kelowna$13m

(2 deals) Halifax$2m

(3 deals)

Victoria$1m

(1 deals)

Other$38m

(10 deals)

With the Toronto to Waterloo corridor leading in deals and volume

7

Sources: Crunchbase, Media Releases, EVP Analysis

Canadian Cities by Average Deal Size

KW Region$10m

Montreal$7m

Ottawa$7m

Kelowna$7m

Toronto$6m

Vancouver$4m

Victoria$2m

Moncton$1m

Halifax$0.5m

Other$4m

KW Region

$35mSeries C

$3.5mSeed

Montreal

$55mSeries A

$8mSeries A

Ottawa

$12.1mSeries D

$1mAngel

Kelowna

$11.6mSeries A

$1.6mSeed

Toronto

$33mSeries D

$25mSeries A

Vancouver

$16mSeries B

Largest Deals by City

Kitchener/Waterloo Region commanding average deal size

8

$10mSeries A

$12m

$11m

$7m

$5m $5m

$4m

$2m$2m $2m $2m $1m

$0.6m$0.1m

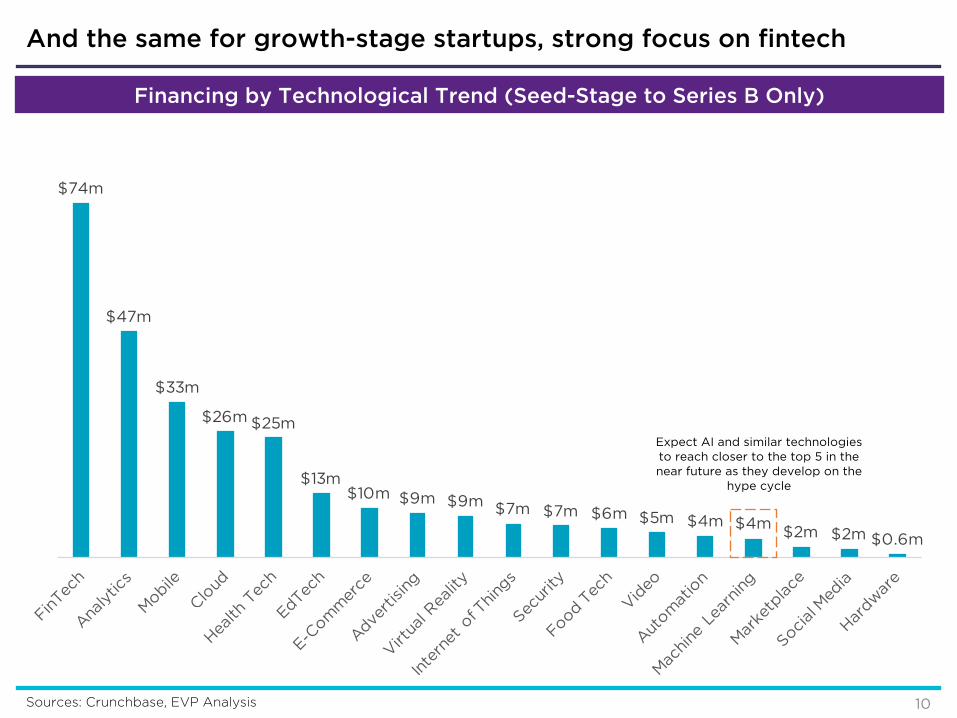

Sources: Crunchbase, EVP Analysis

Financing by Technological Trend (Seed-Stage Only)

Continuous growth as technology converges with industries

But as the power of buyers and market concentration develops, financing will gravitate towards relatively younger technologies (such as VR and machine learning)

At the seed stage, analytics, fintech and mobile dominate

9

$74m

$47m

$33m

$26m $25m

$13m$10m $9m $9m $7m $7m $6m $5m $4m $4m

$2m $2m $0.6m

Sources: Crunchbase, EVP Analysis

Financing by Technological Trend (Seed-Stage to Series B Only)

Expect AI and similar technologies to reach closer to the top 5 in the near future as they develop on the

hype cycle

And the same for growth-stage startups, strong focus on fintech

10

4% 3%4%

42%

8%

2%0%

26%

3%

7%

0% 0% 0% 0% 0%2%

1%

5%7% 7%

2%

10%

19%

5% 5%

8%

2%

7%

13%

7%

Agriculture Arts, Entertainment, & Recreation

Education Financial Services

Health Care Hospitality & Food

Manufacturing Others Retail Technology Metals, Mining, Oil & Gas

Utilities Construction Real Estate Government

VC Financing by Industry as a % of Total GDP by Industry as a % of Total (June 2016)

Sources: Crunchbase, Statistics Canada, EVP Analysis

“Other” Industries: Automotive, Publishing, Media, Home Care, Security, Non-Profit, Law, Dentistry, Consulting, Human Resources,Telecommunications

Financing vs. GDP by Industry

These industries are capital intensive with relatively high barriers to entry making them too “boring”; leading to a lack of ventures to deliver

disruption

With the immense amount of media coverage around FinTech, it’s no surprise that the financial

services industry is going through a period of immense capital

deployment

The fintech hype is real, while resource industries lack disruption

11

Out of the 10 largest financing rounds in H1 2016, 8 were B2B focused

Largest B2C Spaces by Total Deals

Largest B2B Spaces by Total Deals

Analytics

Cloud

Mobile

Mobile

Social Media

E-Commerce

Sources: Crunchbase

B2B vs. B2C

B2B continues to control the funding landscape despite B2C hype

12

B2B71%

B2C29%

$0.5m

$0.6m

$1.0m

$1.0m

$1.3m$1.4m

$1.8m

$3.5m

$2.3m

$4.1m

$6.0m$6.5m

$6.6m

$8.0m

With investor interest increasing, Seed and Series A rounds are on the rise. This could be a sign of the vast opportunities in the early-stage scene, or an indication of overvaluation and an upcoming

price correction.

Largest H1 2016 Deals per Round

Sources: Crunchbase, Pitchbook, EVP Analysis

Median Seed

20% CAGR 13% CAGR

Median Series A

Early-stage rounds continue to rise as investor demand increases

13

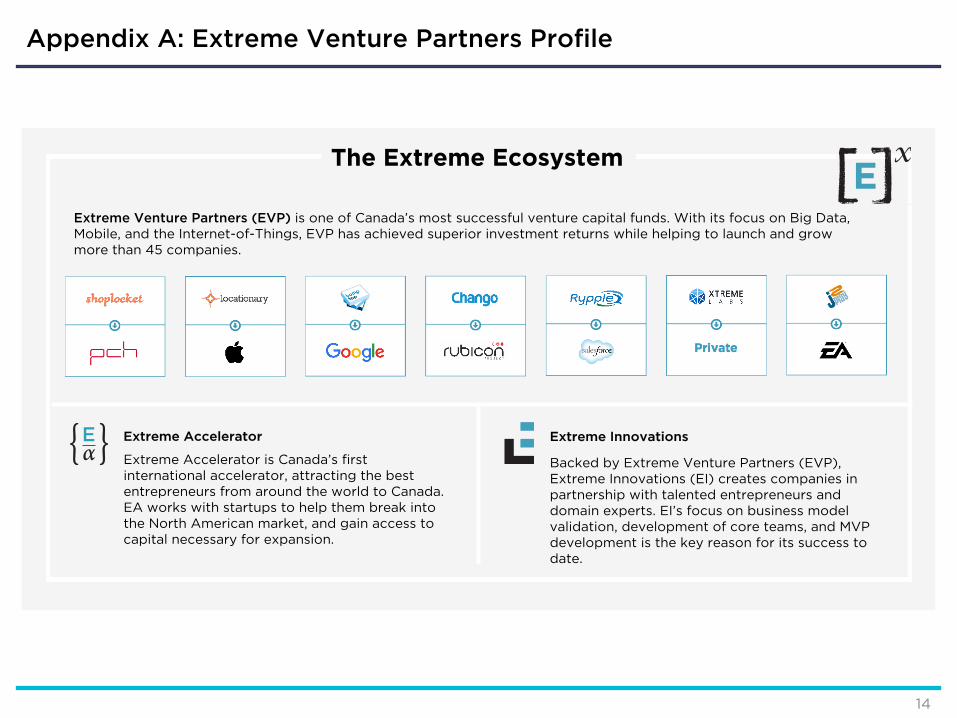

The Extreme Ecosystem

Extreme Venture Partners (EVP) is one of Canada’s most successful venture capital funds. With its focus on Big Data, Mobile, and the Internet-of-Things, EVP has achieved superior investment returns while helping to launch and grow more than 45 companies.

Extreme Accelerator

Extreme Accelerator is Canada’s first international accelerator, attracting the best entrepreneurs from around the world to Canada. EA works with startups to help them break into the North American market, and gain access to capital necessary for expansion.

Extreme Innovations

Backed by Extreme Venture Partners (EVP), Extreme Innovations (EI) creates companies in partnership with talented entrepreneurs and domain experts. EI’s focus on business model validation, development of core teams, and MVP development is the key reason for its success to date.

Appendix A: Extreme Venture Partners Profile

14

• Information was collected from public sources such as Crunchbase, BetaKit, and other media sources. That being said, not all information from every venture capital deal was collected (as a result of disclosure agreements) - making this a not perfect picture of the Canadian venture capital landscape.

• H2 2015 considers funding rounds from January 1st, 2016 to June 30th 2016

• A technology category was assigned to each company based on where most value was extracted. For instance, a company may operate as an analytics firm that uses cloud based software. If the major value proposition for said company is analytics, then analytics is the assigned technology category. This methodology was also applied when considering what vertical each company belongs to.

• The calculation for determining median funding by rounds (slide 13) was determined by taking a sample set of the most active venture capital funds in Canada. Only the disclosed deals from these funds were used to calculate the median funding per round.

Appendix B: Disclosures

15