telecom quarterly review - pta · a) seminar on 3g in lahore b) seminar on 3g devices in islamabad...

TRANSCRIPT

PTAPTA

December 2010

www.pta.gov.pk

Telecom Quarterly

Review

Pakistan Telecommunication Authority

Contents

Regulatory Measures01

Telecom Economy12

Cellular Mobile Services17

Basic Services22

Telecoms in AJK & GB37

Consumer Protection& Complaint Handling

41

Broadband Services31

Annex-1 Telecom Revenue 44

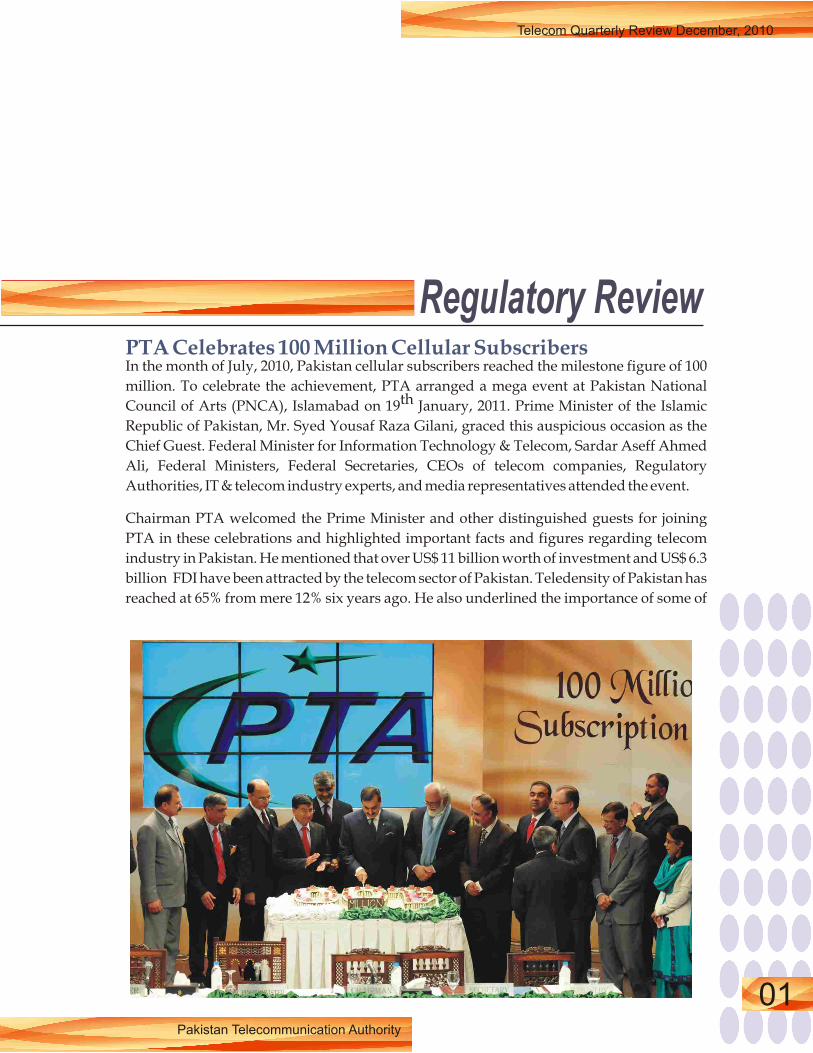

Regulatory ReviewPTA Celebrates 100 Million Cellular Subscribers In the month of July, 2010, Pakistan cellular subscribers reached the milestone figure of 100

million. To celebrate the achievement, PTA arranged a mega event at Pakistan National thCouncil of Arts (PNCA), Islamabad on 19 January, 2011. Prime Minister of the Islamic

Republic of Pakistan, Mr. Syed Yousaf Raza Gilani, graced this auspicious occasion as the

Chief Guest. Federal Minister for Information Technology & Telecom, Sardar Aseff Ahmed

Ali, Federal Ministers, Federal Secretaries, CEOs of telecom companies, Regulatory

Authorities, IT & telecom industry experts, and media representatives attended the event.

Chairman PTA welcomed the Prime Minister and other distinguished guests for joining

PTA in these celebrations and highlighted important facts and figures regarding telecom

industry in Pakistan. He mentioned that over US$ 11 billion worth of investment and US$ 6.3

billion FDI have been attracted by the telecom sector of Pakistan. Teledensity of Pakistan has

reached at 65% from mere 12% six years ago. He also underlined the importance of some of

Telecom Quarterly Review December, 2010

01Pakistan Telecommunication Authority

PTA's most successful projects such as Rabta Ghar PCOs to provide business and

communication opportunities to rural area people, SIM Verification system '668' and SIM

Activation System '789' to help combat terrorism, Quality of Service Surveys and raids to

crack down illegal networks and Consumer Protection Regulations. Chairman PTA also

requested to the Government of Pakistan that 3G licensing process be expedited as soon as

possible so that a new paradigm emerges in the cellular mobile services to focus upon. Federal Minister for IT & Telecom, Mr. Sardar Aseff Ahmed Ali appreciated PTA efforts to

achieve the 100 million subscribers milestone. He discussed the importance of telecom in the

Pakistan's national economy and the role of PTA in achieving this landmark. He assured the

Prime Minister and the notables that Ministry of IT & T will proactively work on the policies,

guidelines and telecom development plans for the country.

At the occasion, Mr. Rashid Khan, CEO Mobilink expressed cellular industry's views on this

magnificent landmark and lauded PTA for being the nucleus of this achievement. He vowed

on the behalf of cellular industry that cellular customers will continue to enjoy

uninterrupted, high quality, innovative cellular services at affordable rates.

To commemorate this historic moment, Pakistan Post representative presented a

commemorative stamp to the Prime Minister of Pakistan especially designed and issued in

lieu of this remarkable achievement.

A t t h e o c c a s i o n , T h e

Honourable Prime Minister

of Pakistan highly apprec-

iated the efforts of PTA and

cellular mobile industry for

providing efficient services

to the people of Pakistan. The

Prime Minister expressed his

satisfaction over the regula-

tory initiatives taken by PTA

and acknowledged the vital

contributions made by

telecom industry to the

national economy. He urged

PTA, Ministry of IT & T and

the cellular industry to

c o n t i n u e t h e t e l e c o m

developments and bring

more innovative telecom

solutions for the people of

Pakistan.

Pakistan Telecommunication Authority

02

Telecom Quarterly Review December, 2010

th100 Million SIM Presented to the Prime Minister of Pakistan

PTA - Most Progressive Telecom Regulator in South AsiaChairman PTA Best Telecom Regulatory Leader of the Year

Creating Awareness for 3G Prospects in Pakistan

On the occasion of achieving 100 million cellular subscribers, Chairman PTA presented the th100 million SIMs to the Honourable Prime Minister of Pakistan, Mr. Syed Yousaf Raza

Gillani as a commemoration of this thlandmark on 30 September,

2010. The Prime Minister congrat-

ulated the Pakistan Telecommuni-

cation Authority for achieving 100

million marks of subscribers. The

Chairman PTA presented SIMs of

all five cellular mobile operators of

Pakistan to commemorate the 100

millionth subscription to the

Prime Minister of Pakistan at PM

Chamber in the Parliament house. The Prime Minister expressed his

satisfaction over the extraordinary

growth of cellular mobile industry

in Pakistan.

3G licensing is one of the most important telecom prospects in Pakistan, a baseline which can

enable the cellular mobile operators to provide their customers with diverse and rich voice

and data service, thereby sparking social and economic growth and increasing revenues.

With the launch of 3G, in future, Pakistani cell phone subscribers will be able to transmit and

receive high speed data through their mobile phones. PTA held a number of seminars in

collaboration with the telecom industry in order to induce expert deliberations among the

renowned telecom professionals and create awareness among the general public about the

potential of 3G services and 3G devices in Pakistan and to attract the major investors into

Pakistan.

Pakistan Telecommunication Authority has been declared Most Progressive Telecom

Regulator in South Asia for the year, while Chairman PTA Dr. Mohammed Yaseen has been

recognized as Best Telecom Regulatory Leader of the Year by South Asian, Middle Eastern

and North African (SAMENA) Telecommunication Council. SAMENA conferred these

awards in an exclusive ceremony held at Casablanca on 26-28 October 2010. SAMENA is a

multi-continent telecom consortium and a unified, consensus-based platform in the region.

Telecom Quarterly Review December, 2010

03Pakistan Telecommunication Authority

a) Seminar on 3G in Lahore

b) Seminar on 3G Devices in Islamabad

Pakistan Telecommunication Authority (PTA) organized a seminar in collaboration with th(Zhongxing Telecom) ZTE Corporation at Lahore on 3G mobile services on 27 December,

2010 . The theme was “To be or not to be is not the question: 3G is coming”. Federal Minister

for Information Technology & Telecom, Sardar Aseff Ahmed Ali was the chief guest on this

occasion, while Chairman PTA, Dr. Mohammed Yaseen, presided over the ceremony. Chief

Executive Officer ZTE Pakistan Mr. Peng Aiguang, IT & telecom industry experts, CEOs of

telecom companies, academia and media representatives attended the seminar.

Federal Minister for Information Technology, Sardar Aseff Ahmed Ali said that “The

introduction of 3G networks, devices and services in countries around the world is

enhancing quality of life and providing expanded economic opportunities, both in the

public and private sectors. On the occasion, Chairman PTA, Dr. Mohammed Yaseen

highlighted the future prospects of 3G in Pakistan. Mr. Cao Long Wang Li Heng, Mr. Rahel

Kamal, representative of Qualcom also made presentations highlighting impact of 3G

services. On this occasion all five cellular mobile operators signed MoUs to boost localized

applications, content and services.

Pakistan Telecommunication Authority organized a seminar on 3G mobile services in th

collaboration with Qualcomm Incorporation, USA at Islamabad on 11 January, 2011. The

theme was “Manufacturing 3G Devices in Pakistan Opportunities for all”. Delegates from

Board of Investment, Pakistan Engineering Council, Ministry of IT, Representatives from

Qualcomm, IT & telecom Industry experts, CEOs of telecom companies, International

Original Equipment Manufacturers (OEMs), Local Investors, Mobile Distributors,

Academia and media representatives attended the seminar.

On the occasion, Chairman PTA apprised the audience that Pakistan offers an excellent

opportunity for investment in 3G handset manufacturing with availability of skilled

manpower and upward growth of mobile market. Mr. Raheel Kamal, Mr. Sanjeet Pandit and

Pakistan Telecommunication Authority

04

Telecom Quarterly Review December, 2010

Mr. Hani Yassin of Qualcom also made

presentations highlighting magnitude

and importance of 3G Manufacturing in

Pakistan.

In cont inuat ion o f the PTA's

commitment to promote telecom

research in academic circles, PTA

started collaboration with renowned

universities of Pakistan in 2010.

National University of Science and

Technology (NUST) and COMSATS

Institute of Information Technology

(CIIT) have already endorsed PTA's

effort by signing the MoUs. In lieu of the

same effort, PTA and University of

Engineering and Technology (UET) Taxila signed a Memorandum of Understanding

(MoU) to promote telecom related research among the university students. Chairman PTA

Dr. Mohammed Yaseen and Vice Chancellor UET Professor Dr. Muhammed Abbas

Choudhary were present while representatives of PTA and UET signed the MoU in a

ceremony held at UET Taxila.

Under the terms of this MoU, PTA would help UET in identification of research areas related

to telecom industry and innovative technologies while UET would cooperate with PTA on different issues of trade, business and economy related to telecom sector.

PTA and UET Taxila Sign MoU for Mutual Cooperation

Telecom Quarterly Review December, 2010

05Pakistan Telecommunication Authority

Refining the Regulatory Framework Pakistan Telecom Authority monitors the telecom sector of Pakistan under the strict legal

provisions of the Pakistan Telecommunication (Re-organization) Act, 1996 as well as PTA's

Rules and Regulations. With ever changing trends in the global as well as local telecom

market, there is a constant need to refine the regulatory tools of the Authority so that every

plausible circumstance is met with strong legal and regulatory support. For this purpose,

following regulations have been drafted, reviewed or amended by the Authority during the

period under review: -

a) The draft Telecommunication System Clock, Time & Date Synchronization

Regulations, 2010 were drafted with the purpose of synchronization of the clock, time

and date of the telecommunication systems of all the licensees to ensure error free data

recovery, accurate reconciliation of call data record & internet protocol record as

determined by the Authority. Upon completion of the consultation process with

stakeholders, the regulations were finalized and approved by the Authority. The

Telecommunication System Clock, Time & Date Synchronization Regulations, 2010

have been gazette notified.

b) The draft GPRS / EDGE Service Quality of Service Standards Regulations, 2010

were prepared and are applicable on all cellular mobile Licensee(s) with the objective

of laying down quality of service parameters for GPRS/EDGE service, to ensure

consumer satisfaction in line with the criterion determined by the Authority. Upon

completion of the consultation process with stakeholders, the regulations were

approved by the Authority. The GPRS / EDGE Service Quality of Service Standards

Regulations, 2010 are in the process of gazette notification.

c) The draft Broadband Quality of Service (QoS) Regulations, 2011 were formulated in

order to define the KPI(s) for Broadband services. These KPI(s) act as benchmarks for

determining quality of service standards for Broadband from the consumers'

perspective. The objective of laying down these indicators is to create transparent,

quantifiable QOS parameters. Upon completion of the consultation process the same

is being evaluated.

d) The draft Cellular Mobile Network Quality of Service (QoS) Regulations, 2011 were

drafted to put into place the quality of service testing benchmarks for all cellular

mobile communication service licensees. The regulations were drafted to identify the

minimum quality of service standards and associated measurement, reporting and

record keeping tasks except packet switched or GPRS/EDGE services. Upon

completion of the consultation process with stakeholders, the regulations will be

submitted to the Authority for approval.

e) The draft Subscribers Antecedents Verification Regulations, 2010 were formulated

pursuant to the policy directive issued by the MoIT vide No.4-1/2005-M(T) dated th24 January,2008 on the mobile subscriber documentation and antecedent

verification. The regulations are applicable on all mobile communications service

licensees to ensure the registration and maintenance of accurate data of their

subscribers antecedents through proper documentation and verification through the

NADRA database in accordance with the procedures specified the regulations. Upon

Pakistan Telecommunication Authority

06

Telecom Quarterly Review December, 2010

completion of the consultation process with stakeholders and the regulations were

finalized and approved by the Authority. The said regulations are in the process of

gazette notification.

f) For the purpose of verification of Cellular Mobile Network's billing for various voice

packages announced by the CMTOs from time to time, The Cellular Mobile Network

Billing Verification Regulations, 2010 have been drafted and the same are under

consideration by the Authority.

g) The Number Allocation and Administration Regulations,2005 were reviewed and the

same were suggested to be repealed considering the significant changes in the number

administration and allocation procedure. Upon completion of the consultation

process with stakeholders regulations were finalized. However, a policy directive of

the MoIT with regard to the allocation of UAN, UIN and toll free numbers is

currently being pursued with the MoIT by the Authority for clarification of the said

directive.

h) The Type Approval Regulations, 2004 have been reviewed with the objective to

streamline the procedure of approval of terminal equipment in line with section 29 of

the Pakistan Telecommunication (Re-organization) Act, 1996.

i) The Telecom Consumer Protection Regulations, 2009 are in process of amendment to

the extent of providing an express time line and procedure by the Authority for the

withdrawal of a service by all licenses. The same is currently under consideration by

the Services Division.

j) The Protection from Spam, Unsolicited, Fraudulent and Obnoxious Communication

Regulation, 2009 are currently under review to cater for the significant increase in

the number of complaints related to unsolicited communication and to provide strict

regulatory control on telemarketers.

In continuation of the joint

statement of interest signed

between PTA and Ericsson to

facil itate and promote ICT

proliferation in Pakistan, PTA and

Ericsson announced “Ericsson -

PTA Mobile Excellence Award” in

a ceremony held in Islamabad on

December 2, 2010. The ceremony

was attended by Mrs. Ewa

Björling, Minister of Trade of

PTA-Ericsson Mobile Excellence Awards 2010

Telecom Quarterly Review December, 2010

07Pakistan Telecommunication Authority

Sweden, Dr. Mohammed Yaseen, Chairman PTA, Mr. Mohsen Tavakol, President of

Ericsson Pakistan, and senior management of Ericsson and PTA. The award and cash prize

of Rs. 100,000/- was conferred to Mr. Muhammad Bilal Junaid and Mr. Talha Shabib

Ahmed, the developers of an SMS SPAM Interceptor application. The application they

developed is an Android based applic-ation for the Open EMR (Electronic Medical Records)

system. It is intended to empower doctors sitting in rural areas in maintaining patient record

through their mobiles. The winner of the Mobile Excellence Award will also be given an

opportunity to qualified practice through internship at Ericsson for a period of 6 months

from the time of graduation.

Pakistan Telecommunication Authority has launched National Rabta Information Portal

(www.pakistan.pk), a single source facilitation web portal to provide information and content

repository to information seekers from within and outside the country at one place. The web

portal has currently more than 1000 web links, 84 downloadable forms of various categories,

links to educational institutions, hospitals, print and electronic media, federal and

provincial institutions and private sector. State Minister for Information & Broadcasting Mr.

Syed Sumsam Ali Shah Bukhari inaugurated the 'National Rabta Information Portal

(www.pakistan.pk) at PTA Headquarters, Islamabad. Secretary Cabinet Division, Mr. Abdur

Rauf Chaudhry and Member Telecom, Ministry of IT Mr. Mushtaq Ahmad Bhatti were also

present during the ceremony. The Honourable Minister appreciated the unique effort by

PTA and declared that the Government of Pakistan has a strong believe in utilizing

Information Communication Technologies (ICTs) to move into the era of electronic service

delivery (e-Services) by simplifying procedures, and making credible and timely

information available to all the citizens at all levels.

PTA Launches National Rabta Information Portal

Chairman PTA Dr. Mohammed Yaseen highlighted that portal would act as an enabler

platform for fast access to one source of information and will increase effective-ness of public

and private sector. PTA has also planned to develop the Urdu and Mobile version of this

National Portal in order to provide more facilitation to the internet community of Pakistan.

Pakistan Telecommunication Authority

08

Telecom Quarterly Review December, 2010

Survey to Check Power Level of Mobile Towers

Billing Verification of Mobile Operators

PTA and Alcatel Present Laptops to SOS Children Village

Base Transceiver Stations (BTSs)/Towers installed by cellular mobile companies are the core

infrastructure of the cellular set up in Pakistan. However, there were some reservations in

general public about the hazardous effects of the radiations emitted by these towers. In order

to ensure that health of the citizens of Pakistan is not compromised, Chairman PTA directed

the relevant quarters at PTA to carry out a technical survey in this regard on priority basis as

the issue directly relates to the health of general public.

Therefore, PTA along with Frequency Allocation Board (FAB) conducted an extensive

survey in major cities of Pakistan and AJ&K with special equipment to check the emission of

power level from transmitters and receivers of Base Transceiver Stations (BTSs)/Towers

installed by cellular mobile companies. The survey was conducted at Karachi, Hyderabad,

Lahore, Faisalabad, Mirpur, Muzaffarabad, Peshawar, Quetta, Sibi, Rawalpindi and

Islamabad. Survey Results showed that the power level of BTSs is below the prescribed

danger limits and in line with the policy directives of Ministry of IT & Telecom, World

Health Organization (WHO) and International Commission on Non-Ionizing Radiation

Protection (ICNIRP) guidelines. The impression, therefore, regarding hazardous effects on

health of humans by radiation from the towers was negated as towers were found working

within the specified parameters defined by the regulator as well as the international bodies

monitoring the issue.

Consumer Protection is one of the top priorities at PTA and multiple initiatives have been

undertaken by PTA to ensure that high quality, fair and uninterrupted cellular mobile

services are provided to the general public. Among one of such initiatives, PTA decided to

carry out billing verification of all cellular mobile operators by using computer software

based solution to ensure that unfair tariff is not charged to the consumers. For this purpose,

30-second billing package was selected as majority of the subscribers have opted for this

package. One hundred (100) rupees scratch cards were loaded in the SIMs of all CMOs. In

order to verify billing system of CMOs, on-net and off-net calls of different durations were

made ranging from 28 seconds to 175 seconds. During billing verification exercise, it was

observed that billing systems of majority of CMOs were accurate and amounts were being

deducted correctly in accordance with their advertised tariffs. It was observed that in most of

the cases, operators were actually giving benefit to their subscribers by charging lesser tariffs

in comparison to their advertised tariffs.

Pakistan Telecommunication Authority joined hands with Alcatel Lucent (ALU) Pakistan to

donate laptops to the children of SOS Village as a Corporate Social Responsibility gesture.

Laptop donation ceremony was held at SOS Village, Bahria Town, Islamabad. Chairman

PTA Dr. Mohammad Yaseen and CEO ALU, Mr. Aadil Rauf attended the ceremony. SOS

Children's Villages is a private social welfare organization providing orphans and

abandoned children a home, good nurturing and a fair chance in life.

Chairman PTA Dr. Mohammed Yaseen urged the private sector to ensure that Corporate

Social Responsibility must at all times remain a priority, especially in Pakistan's perspective

Telecom Quarterly Review December, 2010

09Pakistan Telecommunication Authority

Telecom Quarterly Review December, 2010

11Pakistan Telecommunication Authority

Cancellation of M/s Pakcom (Instaphone) License

Inauguration of Online Complaint Management System

M/s Pakcom (Instaphone) was granted license by the Government of Pakistan in April 1990

for providing cellular mobile services in the country. The company deployed mobile

network based on analogue (AMPS) technology and remained successful service provider

till 2004. Due to lack of strong competition mobile phone charges remained very high and

out of the reach of the licensees. To proliferate the mobile services through competition, PTA

issued two new mobile phone licenses in 2004.

Unfortunately M/s Pakcom (Instaphone) could not upgrade the network technology and

therefore could not keep up with the pace of competition witnessed in Pakistan 2005

onwards. Resultantly, the company started loosing business and defaulted on payments to

PTA. A long legal course was adopted as per Pakistan Telecom Re-Organization Act 1996 in

which the operator was consulted in meetings, helped by giving extension, warned and

show caused. Failing all the efforts, the Authority cancelled the license of M/s Pakcom th(Instaphone) through a determination dated 4 March 2008.

M/s Pakcom (Instaphone) challenged the Authority's decision in Islamabad High Court

Islamabad which was dismissed by the honourable Court. The operator appealed against

the decision of the Islamabad High Court Islamabad in the Supreme Court of Pakistan. The thhonourable Supreme Court also disposed off the appeal on 27 May 2010 in favour of PTA.

thOn receipt of the detailed judgment, PTA issued final cancellation letter on 24 January

2011.

Pakistan Telecommunication Authority (PTA) launched an automated revamped “Online

Complaint Management System” to better facilitate the telecom users in terms of complaint

lodging, processing and resolution. Federal Minister for Information Technology & Telecom

Sardar Aseff Ahmad Ali inaugurated the new system developed by Pakistan

Telecommunication Authority (PTA) while Chairman PTA Dr. Mohammad Yaseen,

Member Finance, Syed Nasrul Karim Ghaznavi, and Member Technical, Dr. Khawar

Siddique Khokhar, were also present during the ceremony. The new system has been

d e s i g n e d t o

minimize the

c o m p l a i n t

resolution time

and for th i s

purpose, it has

been integrated

with operators

and the telecom

Authority.

Pakistan Telecommunication Authority

12

Telecom Quarterly Review December, 2010

Telecom EconomyPakistan's economy remained stressed in the first half of the financial year 2011 (July-Dec),

mainly due to unprecedented floods that damaged one-fourth of the country's agriculture

land and surge in oil prices. The damages to private public infrastructure, impact of supply

disruptions, energy shortages and inflation hit the economy. However, an unexpected good

performance by the services sector provided support to GDP growth and the government

successfully managed growing macroeconomic imbalances in the economy. State Bank of

Pakistan continued tight monetary policy to contain the inflationary impact and the only

positive activity as a consequence to the floods was the strength of external sector, where

large inflow of aid and remittances played positive role to economic recovery. Government

of Pakistan took visible steps to contain the fiscal deficit which remained under pressure due

to subsidies on energy and petroleum during the first half of the FY 2010-11.

In contrast to the Pakistan economic situation the growth of telecom sector remained healthy and positive.Telecom regulator continued to facilitate the sector in regulatory issues and maintaining competition in the sector.

Teledensity In contrast to the Pakistan economic

situation the growth of telecom

sector remained healthy and

positive. The total teledensity growth

kept oscillating between highs and

lows till the end of year. Total

teledensity including mobile, fixed

and WLL services stood at 65.2%.

The teledensity growth in the first

half of the year (Jan to June 10) was

0.9% whereas in the second half of

the year (July-Dec10) the growth was

1.7%, showing more stability and stresilience as compared to 1 half of the year. Total teledensity of the country grew by more

than 2.67% in the last one year.

58.659.6 59.1

60.4 60.161.7

2.2

2.22.1

2.11.93

1.9

1.6

1.71.6

1.61.6

1.6

54

56

58

60

62

64

66

Jul -Sep 09 Oct-Dec 09 Jan -Mar 10 Apr-Jun 10 Jul-Sep 10 Oct - Dec 10

WLL Density FLL Density Mobile Density

(63.5) (62.8)(64.1) (63.3)

(65.2)

(62.4)

eg

a tn

ecre

P

Total Teledensity

Telecom Quarterly Review December, 2010

13Pakistan Telecommunication Authority

Telecom Financials Although the telecom sector has been experiencing decreasing ARPU's, exorbitant

advertisement budgets,

p o w e r c r i s i s , a n d

negative net profits,

aggressive competition,

market saturation and

decreasing exchange

rates, the financial health

of the sector remained

stable. The telecom

revenues reported in 1st

half of the FY2011 were

over Rs. 180 billion

which were 167 billion in

the same period of FY

2009-10. The revenue

growth dur ing the

reported period kept

moving between highs and lows where in July-Sep 2010 it was -3% whereas in Oct-Dec 2010

it was 4%. Cellular Mobile sector is a driving force in terms of revenue in the telecom sector

where it counts 67% of the total telecom revenue whereas fixed line services share is 26% of

total revenue generation of telecom sector. The share of mobile operators in total revenue of

mobile services is according to subscriber share of each operator, where mobilink has

maximum share in total revenue followed by Telenor and Ufone.

The contribution of telecom sector to national exchequer through taxes, duties and

regulatory charges kept growing. The sector has been contributing over Rs. 100 billion each

year since last few years. At the end of FY2010 the total contribution was over Rs. 109 billion

of which almost 50% came from GST. In the first half of the FY2011 the total contribution to

national exchequer was Rs. 56.3 billion which was almost Rs. 49 billion in the first half of

FY2010 showing growth of 15% since last year. It is therefore expected that by end of FY2011

the total contribution to national exchequer would be higher than the last year's

contribution.

According to an estimate, telecom sector contributes more than 90% share in total taxes by ththe services sector of Pakistan which is being diverted to provinces under 18 Amendment.

Similarly share of GST in total contribution from telecom sector is also very impressive

where almost 50% of total contribution comes from GST collection. Only in the 1st half of FY

2010-11, total GST collection is Rs. 23 billion which was Rs. 21 billion in the same period of FY

2010. GST collection in telecom services mainly comes from mobile sector and its share in

total GST collection is 86% followed by basic services as 11%. The Activation Tax st contribution to national exchequer stands at Rs. 3 billion at the end of 1 half of FY2010-11

81,224

86,484 85,684 90,754

87,649

91,540

0.28

6.48

-0.97

5.96

-3.4

4.4

-4

-2

0

2

4

6

8

74,000

76,000

78,000

80,000

82,000

84,000

86,000

88,000

90,000

92,000

94,000

Jul - Sep 09 Oct-Dec 09 Jan -Mar -10 Apr - Jun 10 Jul - Sep 10 Oct- Dec-10

Telecom Revenues Growth

noi lli

M .sR

Pe

rcen

tag

e

Telecom Revenues

Last quarter data of union Estimated

Pakistan Telecommunication Authority

14

which was Rs. 4 billion in the same period last year. Main reason for drop in the activation tax

is due to market maturity, there is time for the Government to abolish this tax on operators to

further strengthen its growth whereas in order to increase GST the government needs to

reduce the existing 19.5% rate, so that usage could be enhanced, which would result in better

GST collection.

The overall inflow of Foreign Direct Investment in the country shows a negative trend in last

few years and same is the case in Pakistan Telecom sector where FDI has reduced up to some

extent in the last two years, however, no drastic reduction has been witnessed. FDI in

telecom sector of Pakistan shows about 17% decline in quarter ending December 2010 on

compared to previous quarter. In case of telecom the FDI is showing some major reduction

since early 2010. At the end of FY 2010 the total FDI in telecom sector was US$ 374 million

Foreign Direct Investment

Telecom Quarterly Review December, 2010

no il l i

B .s

R

36.2844.61 49.35 43.97

22.87

17.6

19.2 14.2

6.61

3.27

9.72

10.86 9.15

13.56

10.76

36.95

36.96 39.344.91

19.46

0

20

40

60

80

100

120

2006 -07 2007-08 2008 -09 2009-10 Jul - Dec - 2010 -11

Others PTA Deposits Activation Tax GST

(100.55)(111.6) (109.05)

(56.36)

(112.00)

Telecom Contribution to Exchequer

noilli

M $

SU

Per ce

nta

ge

Foreign Direct Investment

471.64

540.6 535.9

651.3

394.8433.7

39.02

142.7

82.3109.6

60.7 50.5

8.27

26.4

15.416.8

15.4

11.6

0

5

10

15

20

25

30

0

100

200

300

400

500

600

700

Jul - Sep 09 Oct-Dec 09 Jan - Mar 10 April -Jun 10 Jul - Sep 102 Oct - Dec 10

Total FDI (US$ Million) FDI in Telecom (US$ Million) Share in Total FDI

Source: Central Board of Revenue and Pakistan Telecommunication Authority. Note: PTA's contributions comprise of all its receipts including Initial and Annual License Fee, Annual Spectrum Administrative Fee, USF and R&D Fund Contributions, Numbering Charges, License Application Fee, etc.Others include custom duties, WH Tax and other taxes.

Telecom Quarterly Review December, 2010

15Pakistan Telecommunication Authority

which was US$ 815 million in 2009. Similarly the FDI in telecom was US$ 112 million in the st1 half of FY 2011, where as it was 181 million in the same period of FY2010. It is predicted

that the total FDI in telecom for FY2011 would be less than FY2010. However if we look at the

share of telecom in total FDI there does not seem to be any drastic change since the Jan-March

2010 to Oct-Dec 2010 which implies that total FDI of the country is reducing with same pace

as telecom sector.

To analyze the capital flight from Pakistan telecom sector, PTA made an effort to measure

the profit repatriation from telecom sector to abroad where it was found that repatriation of

profit is about US $ 19.7 million in last eight quarters which is not worrying when compared

with FDI inflows that is about US$ 73.5 Million per quarter in the last 6 quarters. However, a

detailed analysis is required of the repatriation trems of technical fee and other mesuare

allowed under Investment Policy of the Government of Pakistan.

Telecom sector now moving towards maturity and saturation is experienced in

metropolitan cities investment in the sector is decreasing. Although in FY 2010 the

investment situation was not alarming. However, investment figures for first two quarters

of FY 2010-11 are not very encouraging. A total of US$ 270 million have been invested during

Jul-Dec 2010 in telecom sector in Pakistan which is 36% less then the investment made first

six months of 2010 which stands at US$ 423 million. While comparing figures of first quarters

of FY 2011 with FY 2010 there is a drop of 65% in total investment made in telecom sector of

Pakistan.

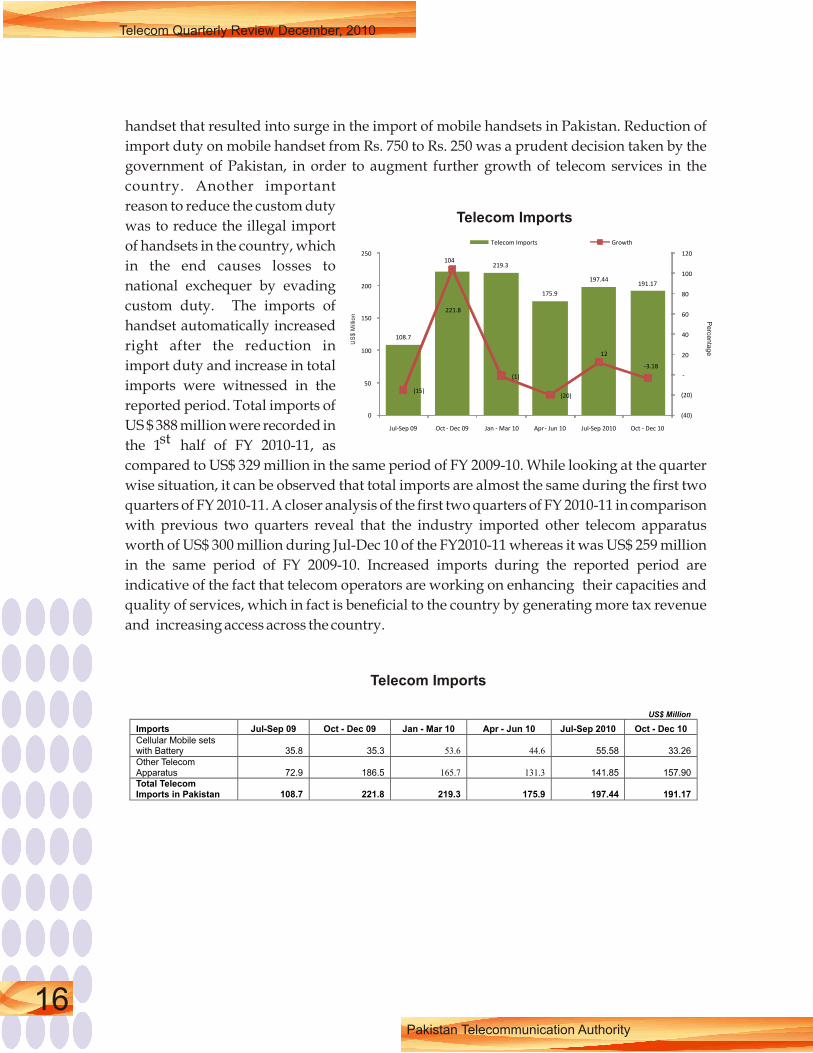

Total Telecom imports showed negative trend in Quarter ending December 2010 where total

imports declined about 3.2% in one

quarter. However, this decline was

observed due to decline in cellular

mobile handsets where as the other

equipments imports increased in the

same quarter by about 11.3% in the

same period. Last year, Government

of Pakistan imposed Custom Duty and

regulatory duty @ Rs. 750 per mobile

handset that curtailed the import of

m o b i l e h a n d s e t s h o w e v e r ,

Government of Pakistan abolished the

regula-tory duty @Rs. 250/ per

handset and reduced the custom duty

from Rs. 500 to Rs. 250/ per mobile

Investment in Telecom Sector

Total Telecom Imports

Telecom Investment

Jul - Sep 09 Jul -Dec 09 Jan -Mar-10 Apr - Jun 10 Jul - Sep 10 Oct- Dec-10

0

100

200

300

400

500

600

700

203.8

567.9

106.9

316.1

156.5113.3

no illi

M $

SU

Pakistan Telecommunication Authority

16

Telecom Quarterly Review December, 2010

handset that resulted into surge in the import of mobile handsets in Pakistan. Reduction of

import duty on mobile handset from Rs. 750 to Rs. 250 was a prudent decision taken by the

government of Pakistan, in order to augment further growth of telecom services in the

country. Another important

reason to reduce the custom duty

was to reduce the illegal import

of handsets in the country, which

in the end causes losses to

national exchequer by evading

custom duty. The imports of

handset automatically increased

right after the reduction in

import duty and increase in total

imports were witnessed in the

reported period. Total imports of

US $ 388 million were recorded in st the 1 half of FY 2010-11, as

compared to US$ 329 million in the same period of FY 2009-10. While looking at the quarter

wise situation, it can be observed that total imports are almost the same during the first two

quarters of FY 2010-11. A closer analysis of the first two quarters of FY 2010-11 in comparison

with previous two quarters reveal that the industry imported other telecom apparatus

worth of US$ 300 million during Jul-Dec 10 of the FY2010-11 whereas it was US$ 259 million

in the same period of FY 2009-10. Increased imports during the reported period are

indicative of the fact that telecom operators are working on enhancing their capacities and

quality of services, which in fact is beneficial to the country by generating more tax revenue

and increasing access across the country.

108.7

221.8

219.3

175.9

197.44191.17

(15)

104

(1)

(20)

12

-3.18

(40)

(20)

-

20

40

60

80

100

120

0

50

100

150

200

250

Jul-Sep 09 Oct - Dec 09 Jan - Mar 10 Apr - Jun 10 Jul-Sep 2010 Oct - Dec 10

Telecom Imports Growth

no illi

M $

SU

Per c

en

tag

e

Telecom Imports

US$ Million

Imports

Jul-Sep 09 Oct -

Dec 09

Jan -

Mar 10

Apr -

Jun 10

Jul-Sep 2010 Oct - Dec 10

Cellular Mobile sets with Battery

35.8

35.3

53.6

44.6

55.58 33.26 Other Telecom Apparatus

72.9

186.5

165.7

131.3

141.85 157.90 Total Telecom Imports in Pakistan

108.7 221.8

219.3 175.9 197.44 191.17

Telecom Imports

Telecom Quarterly Review December, 2010

17Pakistan Telecommunication Authority

Cellular MobileSector Overview

Cellular Penetration

Cellular industry of Pakistan has matured into a competitive and progressive market which

requires new ventures to be explored by cellular operators and ultimately delivered to end

users. From a mere 5 million cellular subscribers in 2004, cellular subscribers jumped to 100

million in 2010. Voice has been the focus of cellular operators since the inception of cellular

mobile services in Pakistan but now the focus is shifting towards utilizing the huge potential

lying in data and value added services (non-voice). PTA is well aware of this situation and

constantly pursuing the Government of Pakistan to announce 3G licensing policy which is

believed to be the right ingredient required to boost up the data services scenario in Pakistan.

Infrastructure/BTS sharing is also an area which the regulator has rigorously focused upon.

After detailed study, industry consultation and expert analysis, an SOP has been issued

regarding infrastructure sharing among the cellular operators so that quality cellular

services can be delivered to the end users efficiently.

The ultimate fruit of such efforts by the regulator resulted into low-cost mobile connection

charges, reduced tariffs, almost complete coverage area and quality mobile services for the

general public throughout the country. Today, cellular teledensity has reached 62.5% from

just 3.3% in 2004 while almost 92% of the land area and more than 10,000

cities/towns/villages are under the umbrella of by cellular services. From only 2000 cell

sites to 30,417 in just six years, cellular services have reached to every nook and corner of the

country. However, there still exist challenges for the regulator and industry alike such as

quality of service, heavy taxation, lack of local content on mobile phones and economic

slowdown.

Cellular penetration in the country

has reached 62.5% at the end of

January 2011 which means that every

6 out of 10 people in Pakistan owns

ce l lu lar connect ion . Cel lu lar

penetration had a topsy-turvy trend

in the recent past due to continuous

data cleaning process by the

operators.

Cellular Penetration

eg

a tn

ecre

P

59.57

59.08

60.41 60.14

61.73

62.47

57

58

59

60

61

62

63

Dec -09 Mar-10 Jun-10 Sep-10 Dec-10 Jan-11

Pakistan Telecommunication Authority

18

Telecom Quarterly Review December, 2010

Subscriber Mix

Market Share

According to latest available statistics, there are currently 104 million cellular subscribers in

Pakistan at the end of January, 2011 as compared to 99.2 million at the end of June,2010

showing a net increase of 4.8 million subscribers over the last seven months. Almost all of the

cellular mobile operators have contributed in this subscriber addition and managed to

maintain positive growth trend during the last two quarters. Mobilink has reached 32.1

million subscribers followed by Telenor with 25.1 million cellular subscribers. Ufone

performed well during the last four quarters and managed to increase its subscriber base to

20.4 million whereas Warid has 17.6 million subscribers and Zong holds 8.9 million figure till

January, 2011.

Cellular market is moving towards maturity, stability and intense competition as operators

are dedicating their best efforts to achieve a higher stake in the overall market share. Over the

last calendar year, cellular market share has not altered significantly. Mobilink still leads the

Cellular Subscribers

30.8 31.5 32.2 31.4 31.8 32.1

18.5 18.8 19.5 20.2 20.3 20.4

6.9 6.9 6.7 7.5 8.5 8.9

22.5 23.3 23.8 23.8 24.7 25.1

18.8 16.3 16.9 17.2 17.5 17.6

-

20.0

40.0

60.0

80.0

100.0

120.0

Dec - 09 Mar - 10 Jun - 10 Sep- 10 Dec - 10 Jan-11

Warid Telenor CMPak Ufone Mobilink

(97.6)(102.8)(100.1)(99.2)(96.8)

(104.0)

noill i

M

Cellular Subscribers Market Share

Dec 09 Dec 10 Mobilink

31%

Ufone20%CMPak

8%

Telenor24%

Warid17%

Warid17%

CMPak7%

Telenor24%

Mobilink32%

Ufone20%

58,189

59,222

63,369

61,770

64,730

54,000

56,000

58,000

60,000

62,000

64,000

66,000

Oct - Dec-09 Jan - Mar 10 Apr - Jun 10 Jul - Sep 10 Oct - Dec 10

noi lli

M .sR

Telecom Quarterly Review December, 2010

19Pakistan Telecommunication Authority

pack with 31% market share while Telenor stands at 24%. Ufone increased its market share to

20% and Warid has 17% stake in the overall subscriber base. Zong has improved its market

share and reached at 8% at the end of December, 2010.

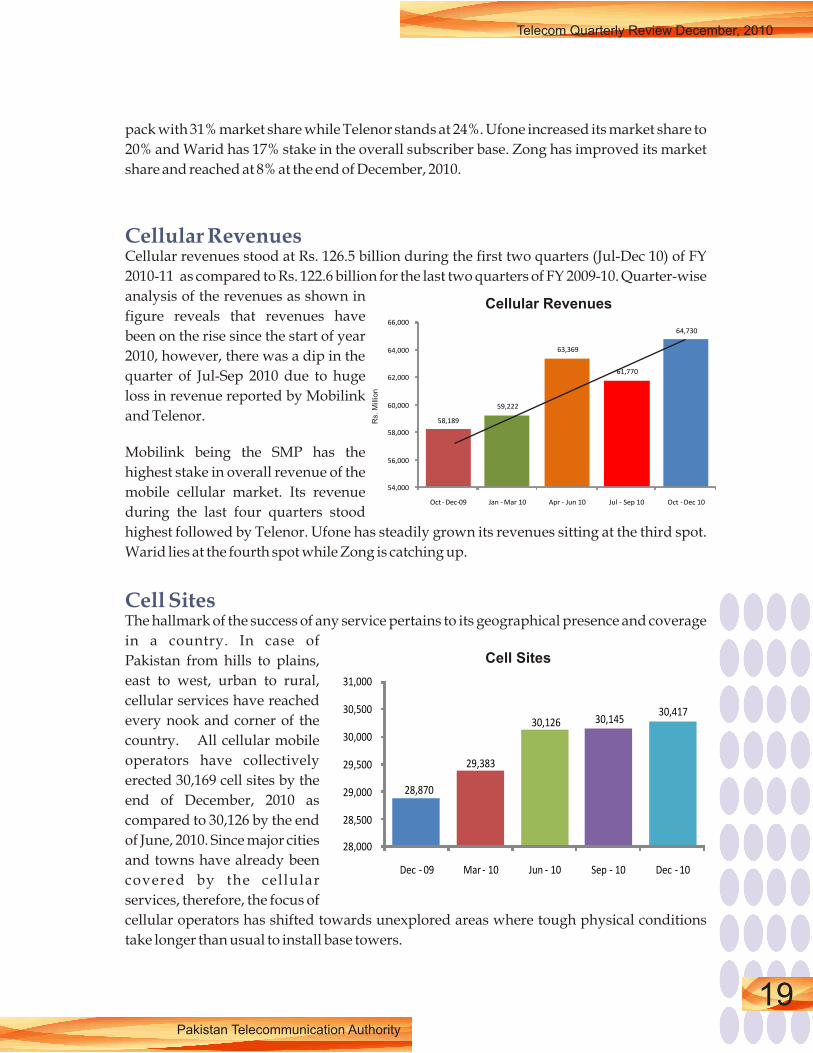

Cellular revenues stood at Rs. 126.5 billion during the first two quarters (Jul-Dec 10) of FY

2010-11 as compared to Rs. 122.6 billion for the last two quarters of FY 2009-10. Quarter-wise

analysis of the revenues as shown in

figure reveals that revenues have

been on the rise since the start of year

2010, however, there was a dip in the

quarter of Jul-Sep 2010 due to huge

loss in revenue reported by Mobilink

and Telenor.

Mobilink being the SMP has the

highest stake in overall revenue of the

mobile cellular market. Its revenue

during the last four quarters stood

highest followed by Telenor. Ufone has steadily grown its revenues sitting at the third spot.

Warid lies at the fourth spot while Zong is catching up.

The hallmark of the success of any service pertains to its geographical presence and coverage

in a country. In case of

Pakistan from hills to plains,

east to west, urban to rural,

cellular services have reached

every nook and corner of the

country. All cellular mobile

operators have collectively

erected 30,169 cell sites by the

end of December, 2010 as

compared to 30,126 by the end

of June, 2010. Since major cities

and towns have already been

covered by the cellular

services, therefore, the focus of

cellular operators has shifted towards unexplored areas where tough physical conditions

take longer than usual to install base towers.

Cellular Revenues

Cell Sites

Cellular Revenues

28,870

29,383

30,126 30,14530,417

28,000

28,500

29,000

29,500

30,000

30,500

31,000

Dec - 09 Mar - 10 Jun - 10 Sep - 10 Dec - 10

Cell Sites

2.58

2.28 2.30

2.60

2.39

2.46

2.48

2.50

2.53

2.10

2.20

2.30

2.40

2.50

2.60

2.70

Dec -08 Mar -09 Jun - 09 Sep -09 Dec -09 Mar -10 Jun - 10 Sep - 10 Dec - 10

Pakistan Telecommunication Authority

20

Telecom Quarterly Review December, 2010

Table shows an interesting comparison of the cellular operator market share and their

respective share in cell sites. Among the cellular operators, Mobilink has the highest number

of cell sites i.e. 7,952 and 26% share

in overall cell sites. However, if

compared with its market share of

31% and no net additions throug-

hout the year, it is probable that

focus of the company is more

towards increasing its subscriber

base rather than expand its existing

infrastructure. Similar is the case

with Telenor, Ufone and Warid who lag behind in infrastructure share as compared to their

respective market shares. Zong is the only cellular operator which has a significantly higher

infrastructure share rather than its market share. Despite being the smallest operator, Zong

has focused more towards raising the network realizing the potential for future growth in

the market.

Average Revenue Per User (ARPU) is one of the key indicators to the financial status of

telecom market in any country. Pakistan's cellular companies had to face a tough time by the

end of last year due to

amplified fixed investments

and global recession. Howe-

ver, the cellular industry with

the help of PTA has bounced

back from this temporary

shaky period and industry

ARPUs are on the rise ever

since. The industry reached a

collective ARPU of US$ 2.48 by

the end of FY 2009-10 and

currently, it stands at US $2.53

as of December, 2010. With the

upcoming 3G licensing and

other PTA initiatives in the pipeline, it is expected that rise in ARPU will sustain for a longer

period of time as cellular operators owe to find new revenue streams via data services and

Value added services.

Cellular international traffic of Pakistan reached a record high with 3.4 billion minutes

recorded in the first two quarters (Jul-Dec 10) of FY 2010-11. Compared with 2.8 billion

minutes during last two quarters (Jan-Jun 2010) of FY 2009-10 it shows that cellular traffic has

increased by 22% thereby establishing the fact that mobile usage is increasingly becoming

Average Revenue Per User (ARPU)

Traffic

Cell Sites Vs Market Share by Operator (%)

Operator Market Share Share in Total Sites Mobilink 31 26 Ufone

20

19

Zong

8

18

Telenor

24

22

Warid

17

15

(December 2010)

Cellular ARPU

h tn

oM /

$S

U

the preferred medium of

c o m m u n - i c a t i o n f o r

inbound and outbound

calls to Pakistan. Total

outgoing traffic trend as

depicted by figure reveals

the steadily growing trend

of making calls from

P a k i s t a n t o o t h e r

destinations around the

world as 0.96 billion

international outgoing

m i n u t e s h a v e b e e n

recorded during the first two quarters (Jul-Dec 10) of FY 2010-11 as compared to 0.93 billion

minutes in the last two quarters of FY 2009-10 (Jan-Jun10). Similarly, international incoming

traffic has also been growing continuously for the last two quarters and reached 2.5 billion

minutes as compared to 1.9 billion minutes during previous two quarters (Jan-Jun 10). The

increase in traffic is attributed to the low international tariffs and bundled international

packages being offered by cellular mobile companies.

Short Messaging Service (SMS) is one of the important features of cellular mobile services

and a vital source of revenue for cellular companies. Figure below shows a steadily growing

trend of SMS over the last five quarters. All cellular companies generated approximately 100

billion SMS during Jul-Dec 10 as compared to 86 billion during the preceding two quarters .

This shows a 16% increase in the SMS traffic in just two quarters. Ufone again leads the SMS

traffic parameters by a clear margin followed by Telenor and Mobilink. Warid and Zong

have significantly low SMS traffic as compared to their competitors. This huge rise in the

SMS traffic owes largely to the attractive and wide range of bundle packages being offered

by all the operators. Daily, weekly, fortnightly, monthly even unlimited packages are being

offered at very low rates by cellular companies to cap the true potential of this value added

service.

Telecom Quarterly Review December, 2010

21Pakistan Telecommunication Authority

International Traffic

455 464 469 486 474

1,012 805

1,128 1,233 1,273

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Oct-Dec 09 Jan-Mar 10 Apr-Jun 10 Jul-Sep 10 Oct - Dec 10

International Incoming Traffic Total International Outgoing

(1,467)

(1,269)

(1,597)(1,719) (1,747)

set

uni

M n

oi lliM

35,069

41,99744,417

48,84751,214

0

10,000

20,000

30,000

40,000

50,000

60,000

Dec -09 Mar -10 Jun - 10 Sep -10 Dec -10

no illi

M

SMS by Cellular Mobile Operators

Pakistan Telecommunication Authority

22

Telecom Quarterly Review December, 2010

Basic ServicesSector OverviewBasic services include fixed local loop (FLL), wireless local loop (WLL) and long distance

international (LDI) services of Pakistan. Since the de-regulation of sector in 2004, almost 200

licenses were issued to several companies in these sectors in a bid to introduce effective

competition and break the monopoly of incumbent. However, due to exponential rise in

cellular uptake and delayed roll out of networks, the desired results could not be fully

achieved. Situation is much better in case of LDI industry where incumbent's share in traffic

and revenues has fallen substantially; however, the FLL and WLL sector are still under the

firm grip of the incumbent. PTA is cognizant of the situation and striving hard to elevate the

penetration level of the local loop services.

FLL sector of Pakistan has performed well in the last quarter of the year 2010, bouncing back

from negative growth to positive net additions. Currently, there are 3.2 million FLL

subscribers in the country with 12,375 net additions during the QE Dec, 2010. PTCL

maintains its virtual monopoly in the FLL sector with over 95% share in revenues and

subscribers. FLL revenues by new FLL operators have been stable during the year 2010.

Teledensity of FLL services stands at 1.9%.

WLL Sector has been maintaining steady growth over the past years and current teledensity

of the sector stands at 1.72%. WLL subscribers have reached 2.8 million having 82,489 net

additions and 3% growth during the calendar year 2010. PTCL is the leader in WLL market

followed by World Call, Telecard and Wateen. A total of 3,654 cell sites have been erected by

WLL operators with PTCL being the leader in this category as well. A 27% increase in WLL

revenues has been witnessed during Jul-Dec 2010.

LDI industry of Pakistan has flourished in the recent past due to aggressive campaign

against illegal telecom operators by PTA and improvement in settlement rates. LDI revenues

for the second quarter (Oct-Dec 10) of FY 2011 have shown substantial positive growth. Link

Direct, Wateen, Multinet and World Call have highest share in revenues among new

operators in the LDI market. Total international traffic during the last two quarters of FY

2010 was almost the same as first two quarters of FY 2011 i.e. 4.6 billion minutes.

Telecom Quarterly Review December, 2010

23Pakistan Telecommunication Authority

Fixed Local Loop (FLL)

FLL Subscribers

Fixed local loop services have been extensively strained over the last decade due to rapid

advancements in the wireless arena especially cellular mobile services and online

communication facilities. According to ITU's World Telecommunication/ICT Indicators

Database 2010, global fixed line subscriptions have dropped from 1.259 billion to 1.197

billion whereas the fixed line subscriptions per 100 inhabitants have dropped from 19.3 to

17.3 during the last five years. Pakistan's fixed line market trend is synonymous with the

global scenario as subscriptions have been declining for the last five years despite numerous

efforts by PTA. Current penetration of FLL subscribers has reached 1.9%. Since the FLL

market of Pakistan is more or less a monopoly of the incumbent, any positive outcome of the

regulator's efforts is also dependent upon the incumbent's strategic and business plans as

well. A good sign for the sector is the positive growth of subscribers in the quarter of Oct-Dec

10 owing to the re-gain of customers by the incumbent.

Fixed Local Loop market of Pakistan consists of 3.2 million subscribers at the end of

December, 2010. Figure shows the quarterly performance of fixed local loop market in the

last few quarters. The declining trend in the FLL market is evident from the figure, however,

this trend seems to be reversing with a net increase of 12,375 subscribers in second quarter of

FY 2010-11.

As FLL segment of the telecom industry of Pakistan is 95% owned by PTCL in terms of

subscriber share, the rise and fall of overall subscriber figures can be directly attributed to the

performance of PTCL. Table shows the quarter-wise division of fixed line subscribers since

December 2009. PTCL has been losing subscribers on regular basis for the last five quarters

concentrating more on its broadband and corporate services, however, the company has re-

40.3

28.126.6

17.1

14.0

9.4

1.6

0

5

10

15

20

25

30

35

40

45

Europe Americas CIS** World Asia &

Pacific

Arab States Africa

Fixed Telephone Lines per 100 Inhabitants - 2010

**Commonwealth of Independent StatesSource: ITU World Telecommunication/ICT Indicators database

Pakistan Telecommunication Authority

24

Telecom Quarterly Review December, 2010

aligned its objectives in the year 2010. The

incumbent started offering attractive

packages such as PTCL Quad-Play

Unlimited, Zero Line Budget, Landline

WoW etc coupled with customer

facilitation initiatives such as Online

Complaint and Billing System. These

steps have started to bring positive

influence to the market as 11,221 new

subscribers have been added by the

company during the second quarter of FY

2011. NTC provides telecom services

mainly to the Government institutions

and holds the second spot with 106,640

subscribers, steadily rising over the last

few quarters. NayaTel launched South Asia's first fiber to the home (FTTH)/fiber to the user

(FTTU) network in Islamabad in September 2006, however, due to relatively higher tariff

and less coverage area, its subscriber base had been growing slowly over the years and

3,416,417

3,276,4633,225,402 3,214,807 3,227,182

2,100,000

2,300,000

2,500,000

2,700,000

2,900,000

3,100,000

3,300,000

3,500,000

Dec-09 Mar-10 Jun-10 Sep-10 Dec -10

FLL Subscribers

FLL Subscribers Share by Province(Dec -10)

Sindh

29%

KPK

11%

Balochistan

3%

Punjab

57%

Dec-09

Mar-10

Jun-10

Sep -10

Dec-10

PTCL

3,268,642

3,128,822

3,082,215

3,063,229

3,074,450

NTC

104,404

104,819

105,788

106,464

10,640 Nayatel

19,100

19,250

12,160

19,700

19,700*

WorldCall

11,358

9,763

9,772

9,947

9,488.0

Brain

9,213

10,109

11,267

11,267 12,404

Union 3,700* 3,700* 4,200* 4,200* 4,500*

Total 3,416,417 3,276,463 3,225,402 3,214,807 3,227,182

FLL Operators Subscriber Base

Note: June PTCL Subscribers revised* Estiamated

Telecom Quarterly Review December, 2010

25Pakistan Telecommunication Authority

stands at 19,700 at the end of December, 2010. WorldCall, Brain and Union have 9,488, 12,404

and 4,500 subscribers respectively till Dec 2010.

Province-wise situation of market share at the end of calendar year 2010 remains the same as

before. Punjab has a 57% share in the total fixed line market followed by Sindh at 29%. KPK

has 11% market share while Baluchistan still resides at 3%.

FLL revenues stood at Rs. 29 billion for the first two quarters of FY 2011 as compared to Rs. 31

billion for the last two quarters of FY 2010. Although the subscribers have dropped

significantly for the same period yet the revenues remained relatively stable showing that

companies are cognizant of the fact that subscribers are expected to drop in line with the

global trend, therefore, they are concentrating on revenue-centric business plans. Quarter-

wise analysis of the revenues as shown in figure reveals that apart from quarter ending June

2010, revenues have been on the decline since the start of year 2010. Similar to subscriber

situation, PTCL has 95% share in overall FLL revenues as well.

Wireless local loop services have been steadily growing in the recent past but like the overall

scenario of local loop services, this sector has also been marred with slow roll out by new

licensees and lack of investment. Cellular boom in the country has also been a factor in

creating tough business environment for the new WLL operators as they struggled to

compete with the incumbent and reach respectable penetration levels. In parallel with the

cellular industry, PTA has also issued SOP regarding data cleaning and issuance of new

connections whereby WLL operators are obligated to undergo extensive data cleaning

FLL Revenues

Wireless Local Loop (WLL)

15,74915,463

15,847

14,74514,550

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

16,000

17,000

Dec -09 Mar-10 Jun -10 Sep-10 Dec -10

no illi

M .sR

FLL Revenues

Pakistan Telecommunication Authority

26

Telecom Quarterly Review December, 2010

activity as well as adhere to the SOP on verification of subscriber antecedents for new

connections. The teledensity of the WLL services has reached 1.72 as of December, 2010 as

compared to 1.62 at the end of June, 2010. WLL Penetration has been rising continuously

through all four quarters of 2010 which is a good sign for the sector.

Wireless local loop subscribers have reached 2.8 million at the end of December, 2010. A net

addition of 159,983 subscribers has been achieved with a growth of 6% when compared with

2,658,825 subscribers at the end of last fiscal year. A slight dip in the quarter ending March

2010 had been the only decline during the last year as operators prepared to comply with the

SOP issued by PTA regarding data cleaning and issuance of new connections.

PTCL is still a dominant

operator in the WLL market of

Pakistan with 1,318,637 subscr-

ibers as of December, 2010.

Compared with 1,234,339 subs-

cribers as of June, 2010, the

company has added 84,298 new

subscribers with a growth of 7%

over the last six months

WorldCall lies at the second

spot with 588,079 subscribers at

the end of December, 2010 as

compared to 581,580 subscribers by end of FY 2009-10. With a net addition of 6,499

subscribers, growth of 1.1% has been achieved by the company during Jul-Dec 2010.

Telecard is another big operator in the WLL market lying closely behind WorldCall with

569,843 subscribers as of December, 2010. However, it is the only WLL company which has

WLL Subscribers

WLL Teledensity

1.4

1.6

1.6 1.6 1.6 1.6

1.6 1.6

1.7

1.0

1.2

1.4

1.6

1.8

Dec - 08 Mar -09 Jun 09 Sep 09 Dec - 09 Mar -10 Jun 10 Sep 10 Dec - 10

eg

a tn

ecre

P

2,660,234 2,646,3652,607,077

2,659,824 2,681,663

2,818,808

2,000,000

2,100,000

2,200,000

2,300,000

2,400,000

2,500,000

2,600,000

2,700,000

2,800,000

2,900,000

Sep-09 Dec-09 Mar-10 Jun-10 Sep -10 Dec -10

WLL Subscribers

Telecom Quarterly Review December, 2010

27Pakistan Telecommunication Authority

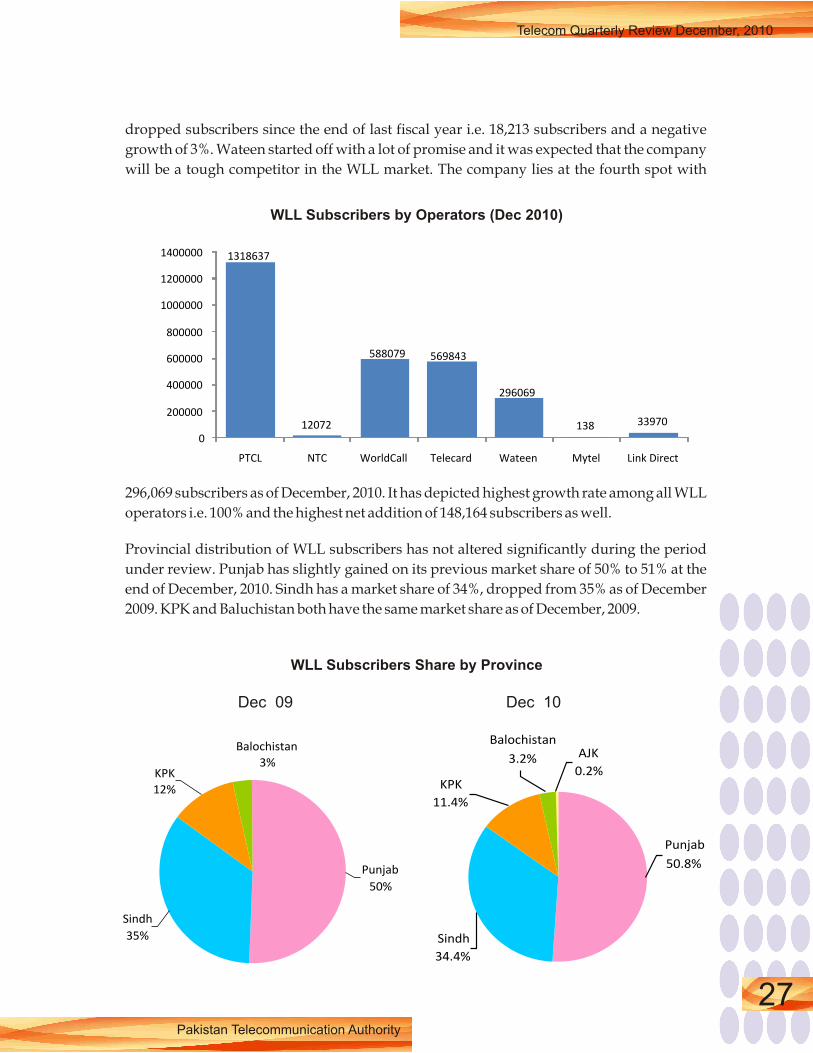

dropped subscribers since the end of last fiscal year i.e. 18,213 subscribers and a negative

growth of 3%. Wateen started off with a lot of promise and it was expected that the company

will be a tough competitor in the WLL market. The company lies at the fourth spot with

296,069 subscribers as of December, 2010. It has depicted highest growth rate among all WLL

operators i.e. 100% and the highest net addition of 148,164 subscribers as well.

Provincial distribution of WLL subscribers has not altered significantly during the period

under review. Punjab has slightly gained on its previous market share of 50% to 51% at the

end of December, 2010. Sindh has a market share of 34%, dropped from 35% as of December

2009. KPK and Baluchistan both have the same market share as of December, 2009.

WLL Subscribers by Operators (Dec 2010)

WLL Subscribers Share by Province

Sindh

35%

Balochistan

3%KPK

12%

Punjab

50%

AJK

0.2%

Balochistan

3.2%

KPK

11.4%

Sindh

34.4%

Punjab

50.8%

Dec 09 Dec 10

1318637

12072

588079 569843

296069

138 33970

0

200000

400000

600000

800000

1000000

1200000

1400000

PTCL NTC WorldCall Telecard Wateen Mytel Link Direct

Pakistan Telecommunication Authority

28

Telecom Quarterly Review December, 2010

WLL Cell Sites

WLL Revenues

Long Distance International (LDI)

Cell sites are an important factor in assessment of infrastructure, investment and coverage of

any wireless media. At the end of Dec, 2010, PTCL leads with 1,639 cell sites all across

Pakistan as given in table below. Wateen has almost same number of cell sites as end of last

fiscal year despite highest subscriber growth rate. WorldCall has got 436 cell sites across

Pakistan. Link Direct, Telecard and other operators have also made no significant addition

to their respective networks in terms of new cell sites during the last two quarters.

Better growth in subscribers has yielded better revenues for the WLL sector in the year 2010.

A total revenue of Rs. 2.3 billion have been generated by the WLL companies during the first

two quarters of FY 2010-11. Compared with Rs. 1.8 billion during the previous two quarters

(Jan-Jun10), it shows a 27% growth in revenues. Wateen leads the revenue statistics with

WorldCall, Wi-Tribe and Telecard playing catch up.

Long Distance International (LDI) services are gateway to international communication for

any country. Pakistan's LDI sector has developed into a competitive environment, slipping

away from the grip of incumbent. Huge investments and revenues are hall mark of LDI

services and performance of new LDI operators has ensured that fierce competition will

carry on in Pakistan in the near future. PTA is constantly working in close coordination with

Punjab Sindh KPK Baluchistan AJK GB Total PTCL 869 386 247 99 35 3 1,639 WorldCall 294 121 21 436 Telecard 137 116 13 8 274 Great Bear

38

3

3

1

45

Wateen

603

258

45

24

930

Mytel

2

2

Link Direct

111

213

3

1

328 Total

2,052

1,097

332

135

35

3

3,654

WLL Cell Sites (Dec - 10)

756854

984879

1,032

1,287

0

200

400

600

800

1000

1200

1400

Jul-Sep 09 Oct -Dec 09 Jan -Mar 10 Apr -Jun 10 Jul-Sep 10 Oct - Dec 10

WLL Revenues

noilli

M .sR

Telecom Quarterly Review December, 2010

29Pakistan Telecommunication Authority

the LDI industry to address their issues as well as launching an aggressive campaign against

the illegal telecom traffickers all across the country. Through the technical monitoring

facility installed at PTA and help of Federal Investigation Agency (FIA), a total of 12 raids

have been carried out by PTA in the cities of Lahore, Karachi and Islamabad during the last

two quarters. Five persons were apprehended during these raids in addition to illegal

telecom equipment worth millions of rupees being confiscated.

LDI revenues have been topsy-turvy in the recent past hovering around Rs. 7.4 billion to Rs.

8.1 billion. Figure shows the quarterly

performance of LDI companies in

terms of revenues for the last six

quarters. Revenues were at a low mark

at the start of the year 2010 i.e. Rs. 7.4

billion. However, the year ended on a

high of Rs. 8.1 billion turn over by the

LDI companies in the last quarter of

2010. Revenue comparison of the last

two quarters of FY 2009-10 with first

two quarters of FY 2010-11 reveals that

revenues have grown by 2.3%. Since

PTCL revenues are not included in

these figures, the actual revenues of LDI industry will be much higher.

PTCL is the biggest operator in Pakistan's basic services market having highest share in

revenue for local loop and LDI services. Figure shows the quarterly performance of PTCL in

terms of revenue for the last six quarters. There has been an oscillating growth trend in the

recent quarters with revenues falling down at the start of FY 2010-11. However, the negative

growth has been minimal during the second quarter of FY 2010-11 owing to positive net

additions in subscriber figures.

LDI Revenues

13,625

14,953

14,541 14,621

13,856 13,842

-4.2

9.7

-2.8

0.5

-5.2-0.1

-6

-4

-2

0

2

4

6

8

10

12

12,500

13,000

13,500

14,000

14,500

15,000

15,500

Jul -Sep 09 Oct-Dec 09 Jan-Mar 10 Apr-Jun 10 Jul -Sep 10 Oct -Dec 10

PTCL Growth

noilli

M .sR

Per ce

nta

ge

PTCL Revenues

REVENUES BY NEW LDI OPERATORS

Pakistan Telecommunication Authority

30

Telecom Quarterly Review December, 2010

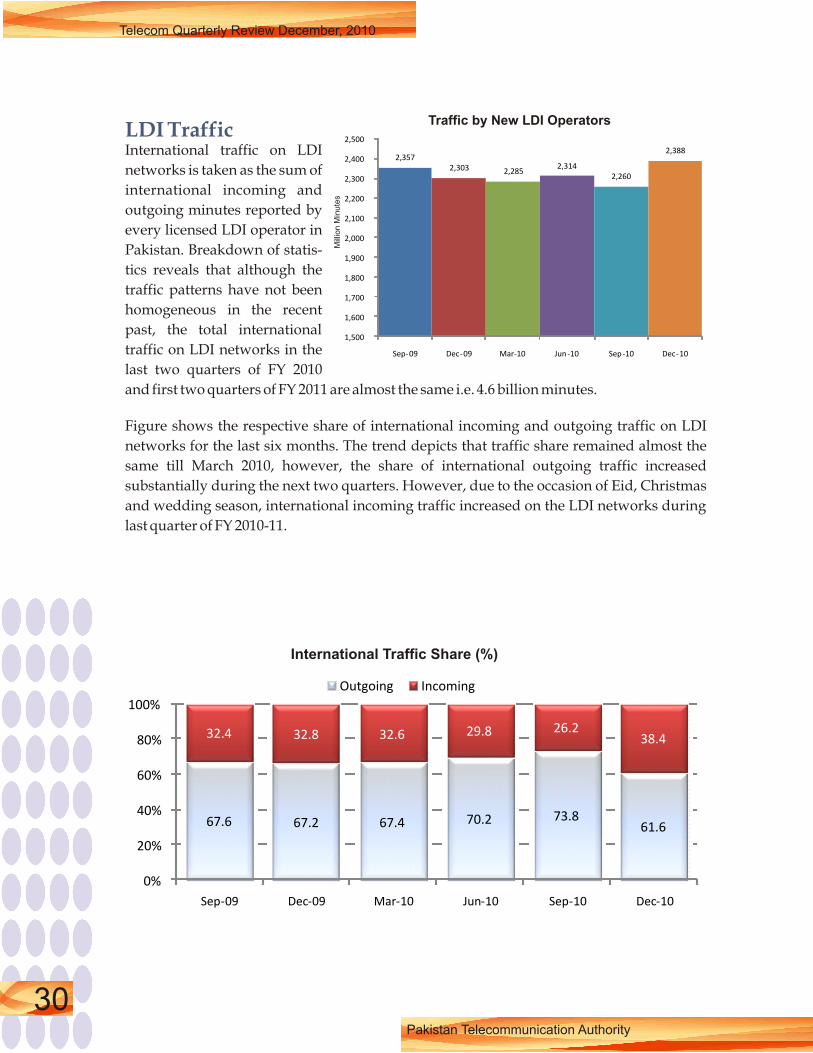

LDI TrafficInternational traffic on LDI

networks is taken as the sum of

international incoming and

outgoing minutes reported by

every licensed LDI operator in

Pakistan. Breakdown of statis-

tics reveals that although the

traffic patterns have not been

homogeneous in the recent

past, the total international

traffic on LDI networks in the

last two quarters of FY 2010

and first two quarters of FY 2011 are almost the same i.e. 4.6 billion minutes.

Figure shows the respective share of international incoming and outgoing traffic on LDI

networks for the last six months. The trend depicts that traffic share remained almost the

same till March 2010, however, the share of international outgoing traffic increased

substantially during the next two quarters. However, due to the occasion of Eid, Christmas

and wedding season, international incoming traffic increased on the LDI networks during

last quarter of FY 2010-11.

67.6 67.2 67.4 70.2 73.861.6

32.4 32.8 32.6 29.8 26.238.4

0%

20%

40%

60%

80%

100%

Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10

Outgoing Incoming

International Traffic Share (%)

Traffic by New LDI Operators

2,357 2,303 2,285

2,314 2,260

2,388

1,500

1,600

1,700

1,800

1,900

2,000

2,100

2,200

2,300

2,400

2,500

Sep-09 Dec-09 Mar-10 Jun -10 Sep -10 Dec-10

Mill

ion M

inute

s

Sector OverviewInformation accessibility, dissemination and knowledge sharing has become the hallmark of

today's “electronic age”. The pace of economic, social and technological developments of st21 century has been synonymous with the revolutionary propagation of ICT services.

Broadband internet and mobile cellular services have been instrumental in connecting

people, increasing social interactions, produce new income sources, provide platform for

freedom of speech and develop portals for entertainment of the human beings.

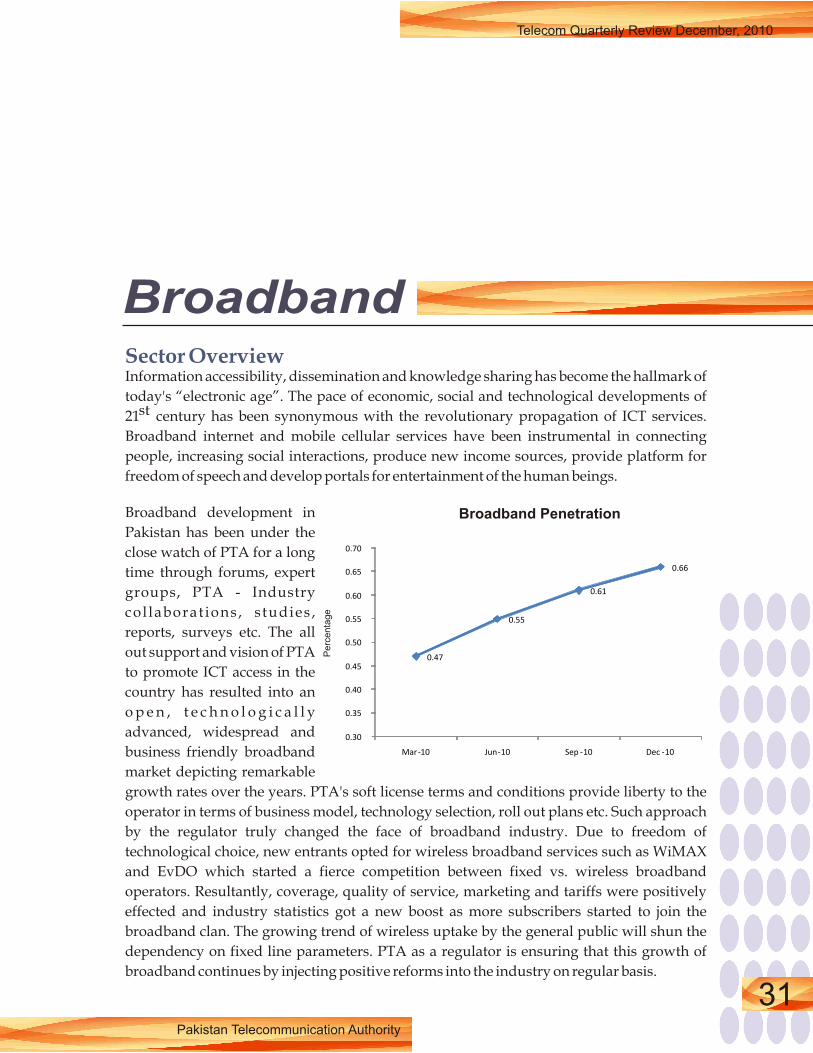

Broadband development in

Pakistan has been under the

close watch of PTA for a long

time through forums, expert

groups, PTA - Industry

col laborat ions, s tudies ,

reports, surveys etc. The all

out support and vision of PTA

to promote ICT access in the

country has resulted into an

o p e n , t e c h n o l o g i c a l l y

advanced, widespread and

business friendly broadband

market depicting remarkable

growth rates over the years. PTA's soft license terms and conditions provide liberty to the

operator in terms of business model, technology selection, roll out plans etc. Such approach

by the regulator truly changed the face of broadband industry. Due to freedom of

technological choice, new entrants opted for wireless broadband services such as WiMAX

and EvDO which started a fierce competition between fixed vs. wireless broadband

operators. Resultantly, coverage, quality of service, marketing and tariffs were positively

effected and industry statistics got a new boost as more subscribers started to join the

broadband clan. The growing trend of wireless uptake by the general public will shun the

dependency on fixed line parameters. PTA as a regulator is ensuring that this growth of

broadband continues by injecting positive reforms into the industry on regular basis.

Telecom Quarterly Review December, 2010

31Pakistan Telecommunication Authority

Broadband

Broadband Penetration

0.47

0.55

0.61

0.66

0.30

0.35

0.40

0.45

0.50

0.55

0.60

0.65

0.70

Mar-10 Jun-10 Sep -10 Dec -10

eg

atn

ecre

P

Pakistan Telecommunication Authority

32

Telecom Quarterly Review December, 2010

Subscriber Mix

Major Broadband Players

Broadband industry of Pakistan has been growing at an astounding pace over the last few

years. There are currently 1,140,781 broadband subscribers in Pakistan as compared to

643,892 at the end of December, 2009 showing a 77% growth over the last calendar year.

Although this growth rate may seem less than that of the same period last year, it must be

noted that the number of net additions this year (496,889) are more than that of last year

(376,712). This is an encouraging sign as the number of subscribers directly affect the

broadband penetration

leve l in the country .

Current ly , broadband

penetration of the country

stands at 0.66% at the end of

December, 2010 which was

0.39% in December 2009,

depict ing almost 69%

growth in just one year. It is

also a fact that Broadband is

s t i l l a n e m e r g i n g

phenomenon with inherent

constraints associated with

it like lack of connectivity to

rural areas, low literacy rate, lack of local content and applications etc, therefore, it will take

some time for the penetration level to reach the high mark.

PTCL, Wateen and WorldCall are the three biggest broadband operators of Pakistan having

a combined share of 86%. PTCL holds 55% market share having 626,748 subscribers with

both its DSL and EvDO services topping in their respective broadband technology charts.

PTCL has added the highest number of new broadband subscribers as well i.e. 294,481

showing 89% growth rate in the previous year. Wateen successfully rolled out World's first

commercial WiMAX based network in 2007, however, out of the 232,541 subscribers,

company statistics show

t h a t i t a d d e d 8 1 , 5 2 6

subscribers in the previous

year with a 54% growth rate

which is much lesser than its

direct competitor PTCL.

With 125% growth rate

during calendar year 2010

and 122,813 subscribers,

WorldCall has been the

s t a n d o u t b r o a d b a n d

operator in terms of growth

Broadband Subscribers

Per ce

nta

ge

643,892

772,437

900,648

994,911

1,140,781

29

20

17

10

15

0

5

10

15

20

25

30

35

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

Dec -09 Mar-10 Jun-10 Sep -10 Dec -10

Subscribers Growth

Broadband Subscribers by Operator

332,267

151,015

54,685 33,675 28,226

626,748

232,541

122,813

73,739 36,391

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

PTCL Wateen WorldCall Wi- Tribe Link Dot Net

Dec - 09 Dec -10

Telecom Quarterly Review December, 2010

33Pakistan Telecommunication Authority

rate whereas it added 68,128 new subscribers as well. Wi-Tribe follows World Call closely in

terms of growth rate as it added 40,064 new subscribers depicting 118% growth during the

last calendar year. Link Dot Net stays at the fifth spot with 36,391 subscribers up 28% from

December 2009.

Broadband market of Pakistan is a true amalgamation of latest fixed and wireless

technologies from around the world. Ranging from primitive fixed line technologies like

Cable TV, FTTH and DSL to latest wireless technologies like WiMAX and EvDO, the nation

has a variety of options when selecting a suitable broadband package.

Figure shows a historical view of Pakistan's broadband technology evolution over the years.

DSL ruled the broadband market of Pakistan since 2007 due to an established fixed line

infrastructure by the incumbent, PTCL. HFC and WiMAX broke the monopoly of DSL by

getting a combined chunk of almost 37% in the market in 2007-08. The scenario changed

again when WiMAX truly established itself as a viable wireless broadband solution and

EvDO made a promising start in the market however, HFC declined sharply due to

introduction of new technologies.

Currently, there exists a fierce competition between fixed and wireless technologies as

EvDO and WiMAX are collectively increasing their market share over DSL and other fixed

line services.

Fixed line broadband technologies provide a direct physical connection to the subscriber's

residence or business. Many broadband technologies such as cable modem, xDSL (digital

subscriber line) and broadband over power line have evolved to use an existing form of

subscriber connection as the medium for communication. In general, all fixed line

Broadband Technologies in Pakistan

Major Fixed Line Technologies

100 98.9

61.2 63.552.9 48.6

25.48.7

5.53.7

11.7

21.4

28.628.7

5.412.3

18.4

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%