telus investor booklet merrill lynch communications forum dallas, texas march 2005

TRANSCRIPT

TELUS investor booklet

Merrill LynchCommunications Forum

Dallas, TexasMarch 2005

2

This booklet and answers to questions contain forward-looking statements about expected future events including competition, labour relations developments and financial and operating results that are subject to risks and uncertainties. TELUS’ actual results, performance, or achievement could differ materially from those expressed or implied by such statements. For additional information on potential risk factors, see TELUS’ 2004 Annual Information Form, and other filings with securities commissions in Canada and the United States.

TELUS disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

forward-looking statements

all dollars in C$ unless otherwise specified

3

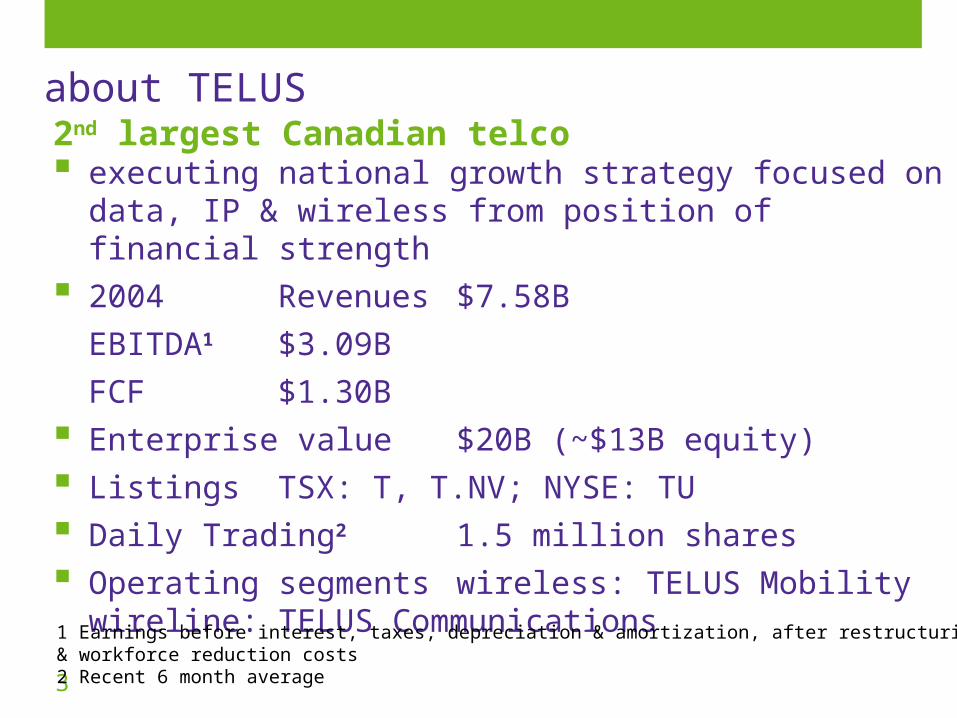

2nd largest Canadian telco executing national growth strategy focused on data, IP &

wireless from position of financial strength

2004 Revenues $7.58B

EBITDA1 $3.09B

FCF $1.30B

Enterprise value $20B (~$13B equity)

Listings TSX: T, T.NV; NYSE: TU

Daily Trading2 1.5 million shares

Operating segments wireless: TELUS Mobilitywireline: TELUS Communications

1 Earnings before interest, taxes, depreciation & amortization, after restructuring & workforce reduction costs2 Recent 6 month average

about TELUS

4

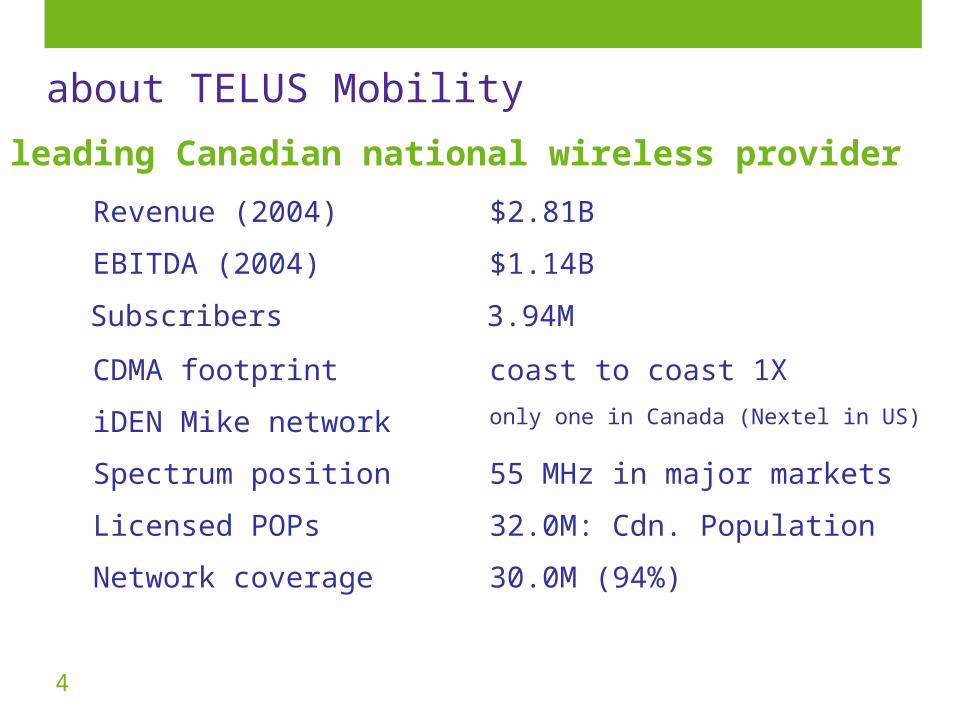

about TELUS Mobility

32.0M: Cdn. PopulationLicensed POPs

30.0M (94%)Network coverage

55 MHz in major marketsSpectrum position

only one in Canada (Nextel in US)iDEN Mike network

coast to coast 1XCDMA footprint

$1.14B EBITDA (2004)

$2.81BRevenue (2004)

3.94MSubscribers

leading Canadian national wireless provider

5

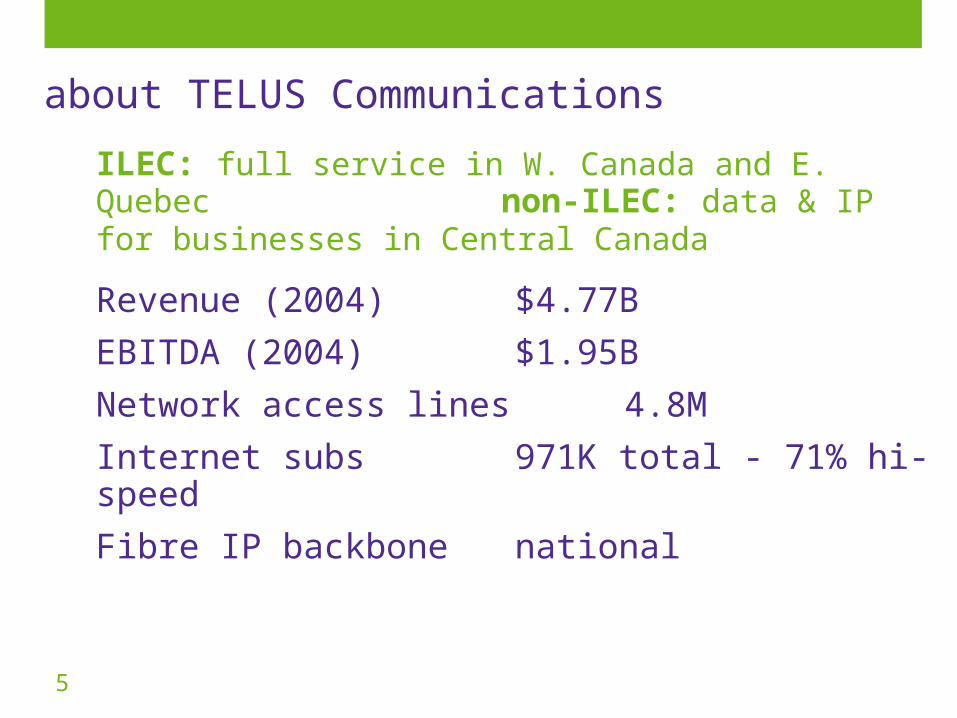

ILEC: full service in W. Canada and E. Quebec non-ILEC: data & IP for businesses in Central Canada

Revenue (2004) $4.77B

EBITDA (2004) $1.95B

Network access lines 4.8M

Internet subs 971K total - 71% hi-speed

Fibre IP backbone national

about TELUS Communications

6

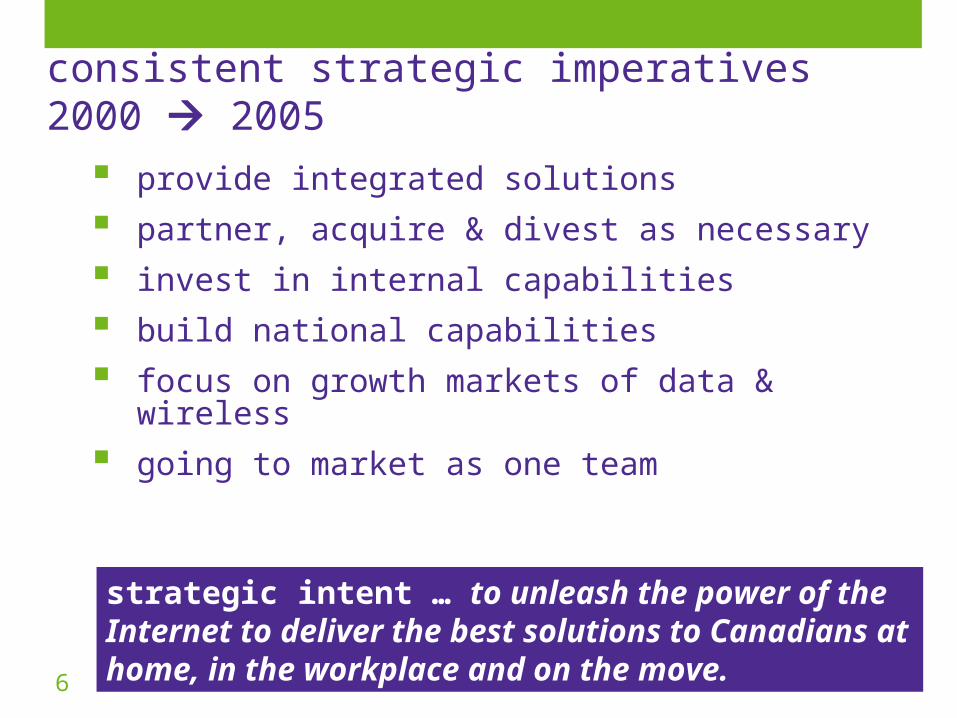

consistent strategic imperatives 2000 2005

provide integrated solutions

partner, acquire & divest as necessary

invest in internal capabilities

build national capabilities

focus on growth markets of data & wireless

going to market as one team

strategic intent … to unleash the power of the Internet to deliver the best solutions to Canadians at home, in the workplace and on the move.

7

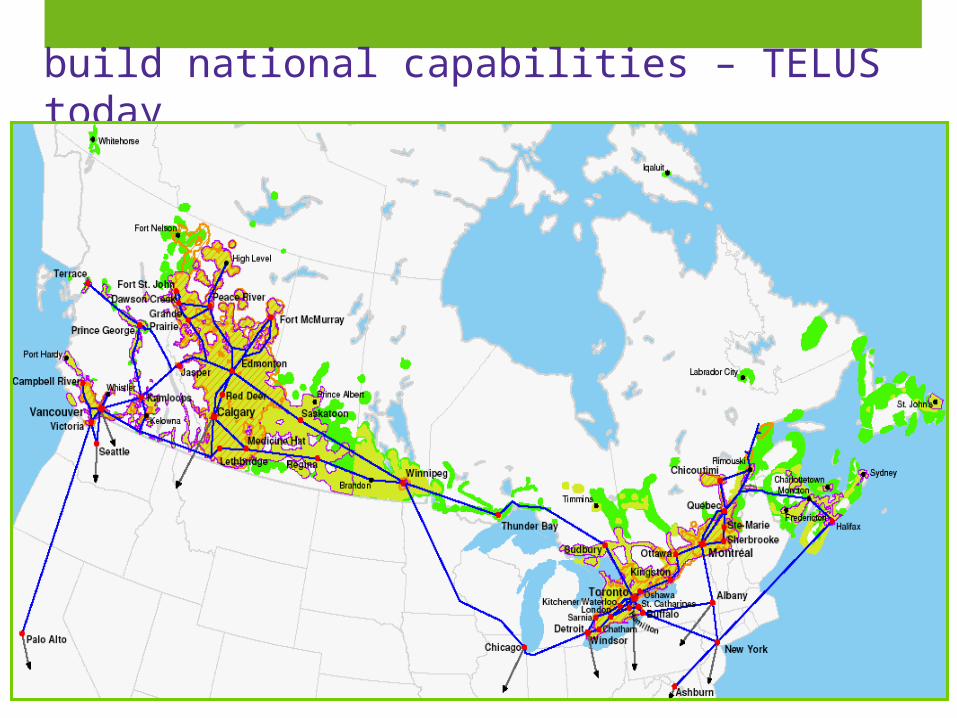

build national capabilities – TELUS today

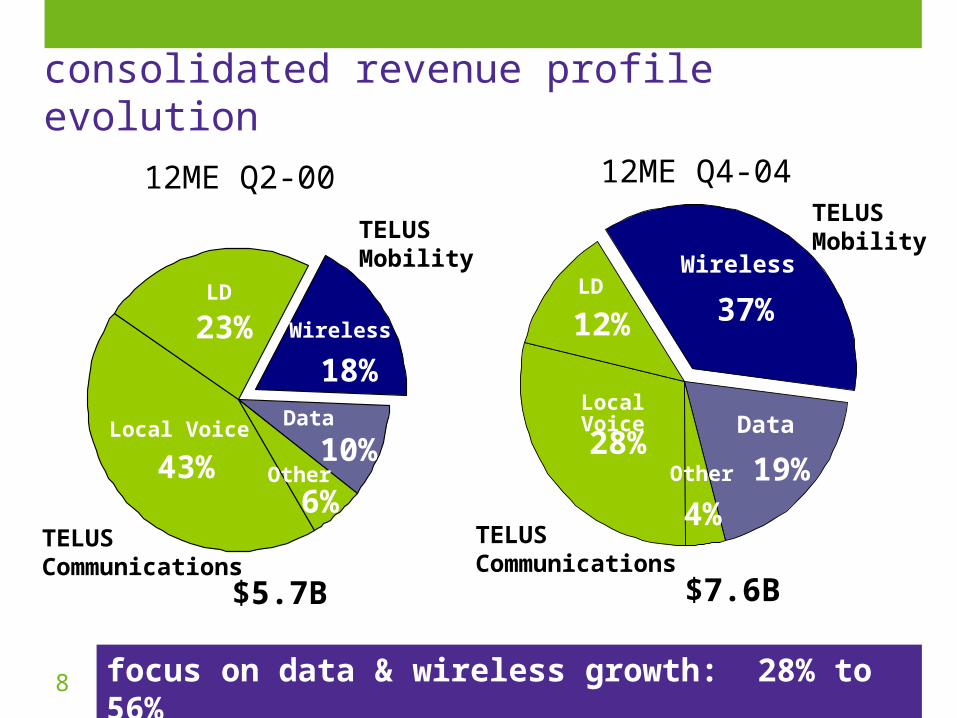

8 focus on data & wireless growth: 28% to 56%

$5.7B

43%

18%

10%

6%Other

12ME Q4-04

$7.6B

Local Voice

Wireless

Data28%

37%

19%

4%Other

LD

Wireless

12ME Q2-00

Local Voice

23%

Data

12%LD

TELUSCommunications

TELUSCommunications

TELUSMobility

TELUSMobility

consolidated revenue profile evolution

9

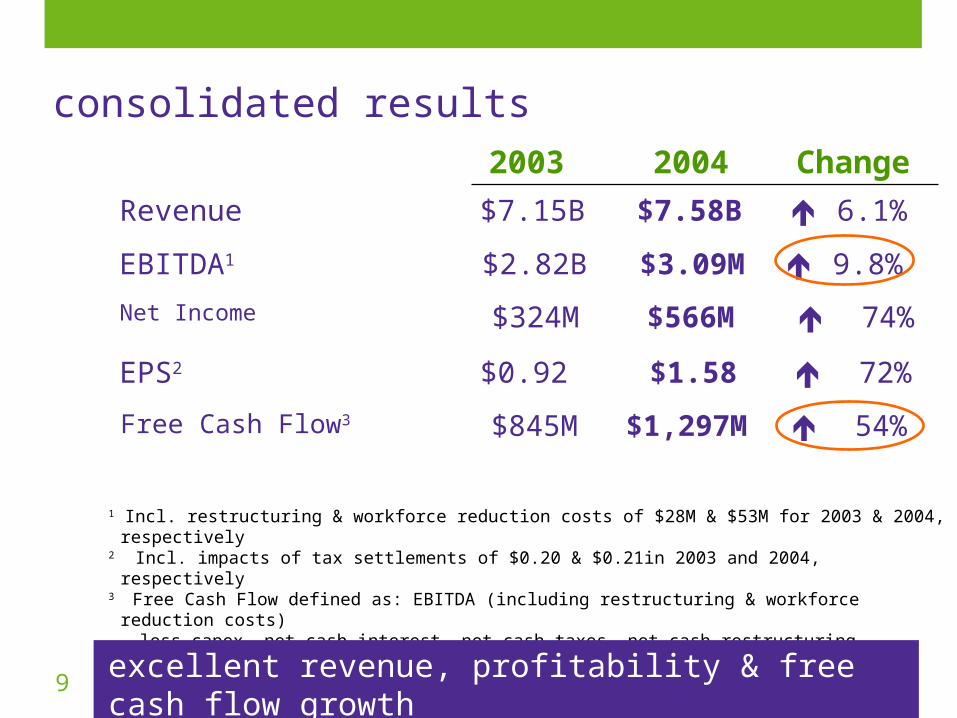

consolidated results

Change

1 Incl. restructuring & workforce reduction costs of $28M & $53M for 2003 & 2004, respectively2 Incl. impacts of tax settlements of $0.20 & $0.21in 2003 and 2004, respectively3 Free Cash Flow defined as: EBITDA (including restructuring & workforce reduction costs) less capex, net cash interest, net cash taxes, net cash restructuring payments, and excess share

compensation expense over share compensation payments

74%$566M$324MNet Income

72%

$1.58$0.92EPS2

6.1%$7.58B$7.15BRevenue

9.8%$3.09M$2.82BEBITDA1

20042003

excellent revenue, profitability & free cash flow growth

54%$1,297M$845MFree Cash Flow3

TELUS Mobility

11

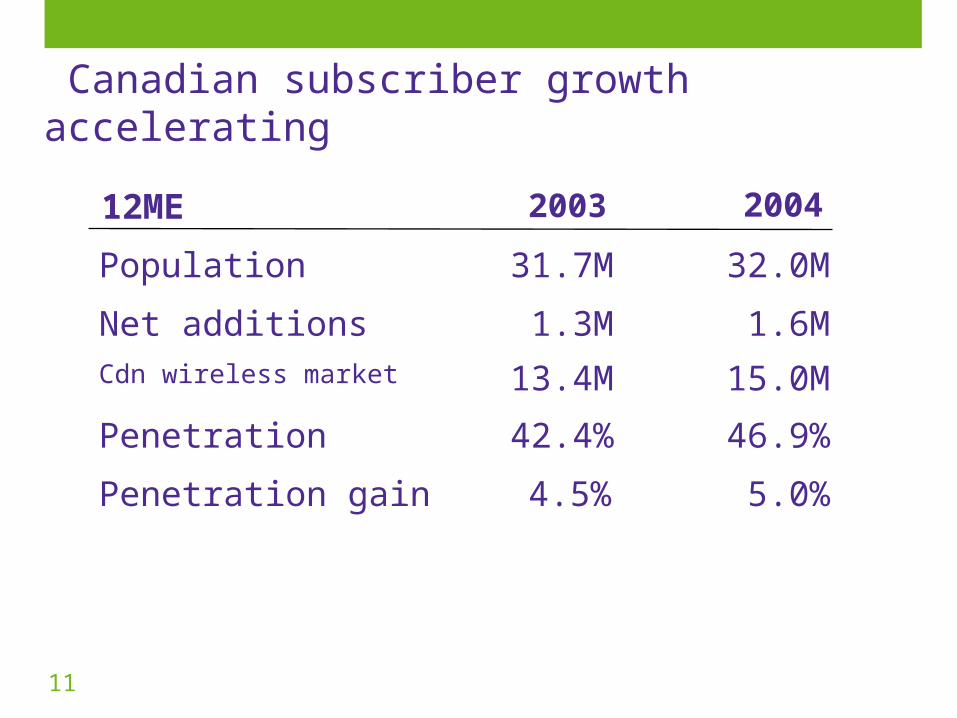

Canadian subscriber growth accelerating

5.0%4.5%Penetration gain

1.6M1.3MNet additions

32.0MPopulation 31.7M

15.0MCdn wireless market 13.4M

20042003

46.9%42.4%Penetration

12ME

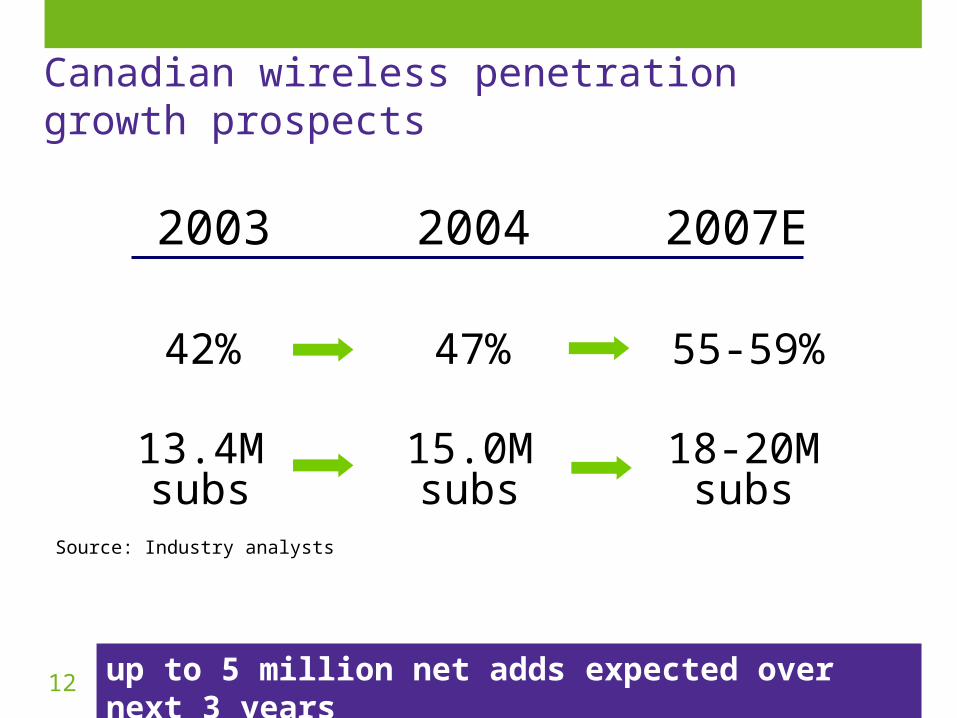

12 up to 5 million net adds expected over next 3 years

Source: Industry analysts

2003

42%

2007E

55-59%

2004

47%

13.4Msubs

18-20Msubs

15.0Msubs

Canadian wireless penetration growth prospects

13

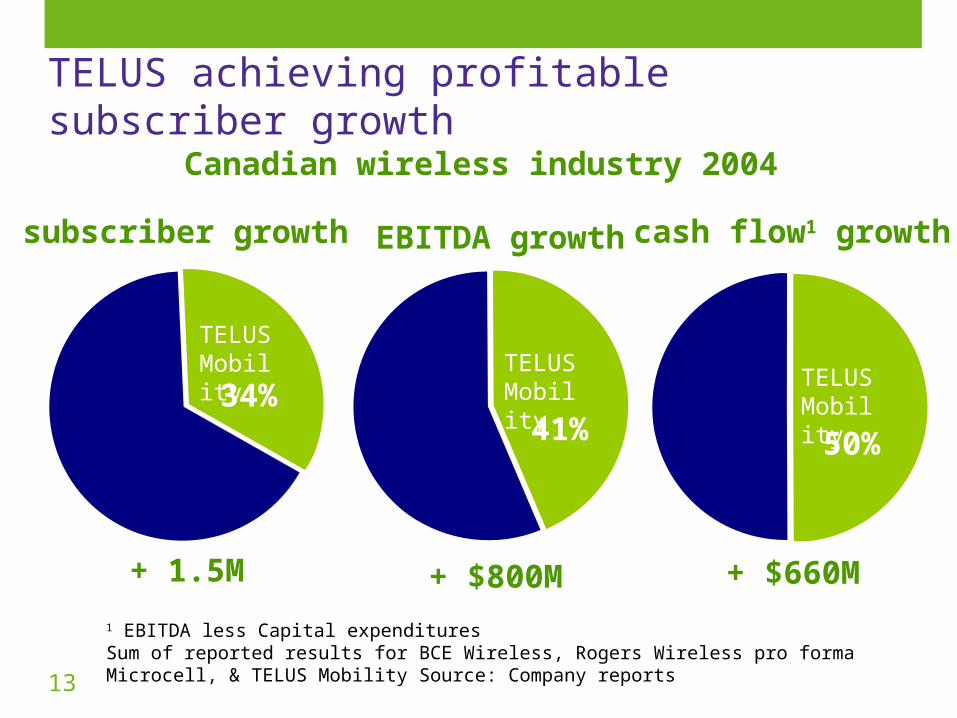

TELUS achieving profitable subscriber growth

1 EBITDA less Capital expendituresSum of reported results for BCE Wireless, Rogers Wireless pro forma Microcell, & TELUS Mobility Source: Company reports

EBITDA growth

subscriber growth

+ $800M+ 1.5M

TELUSMobility

41%34%

TELUSMobility

+ $660M

cash flow1 growth

50%

TELUSMobility

Canadian wireless industry 2004

14

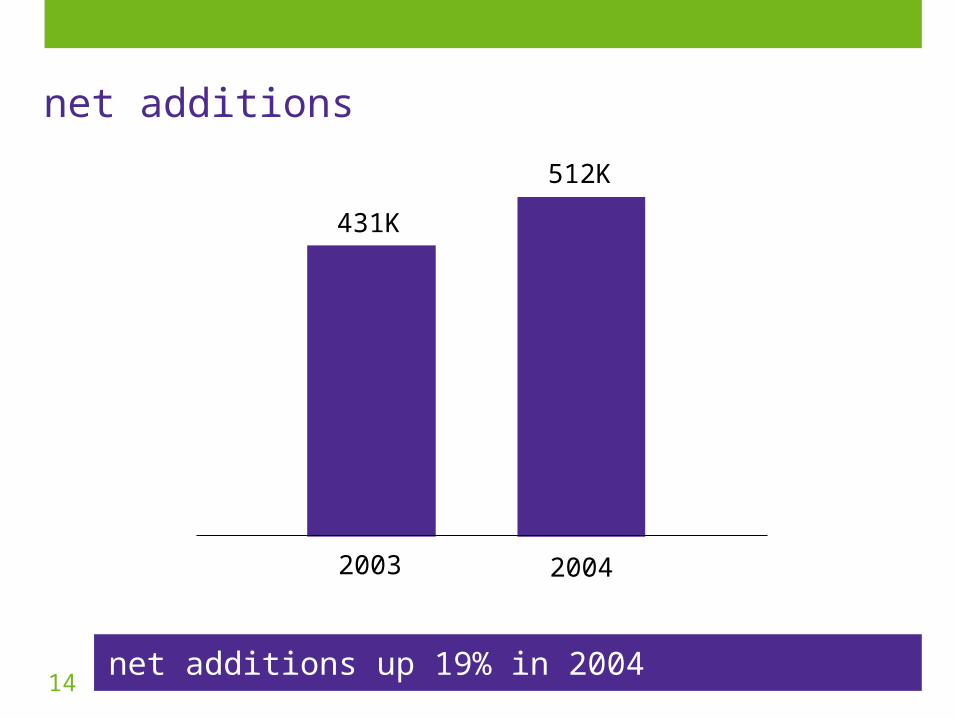

net additions

net additions up 19% in 2004

2003

431K

2004

512K

15

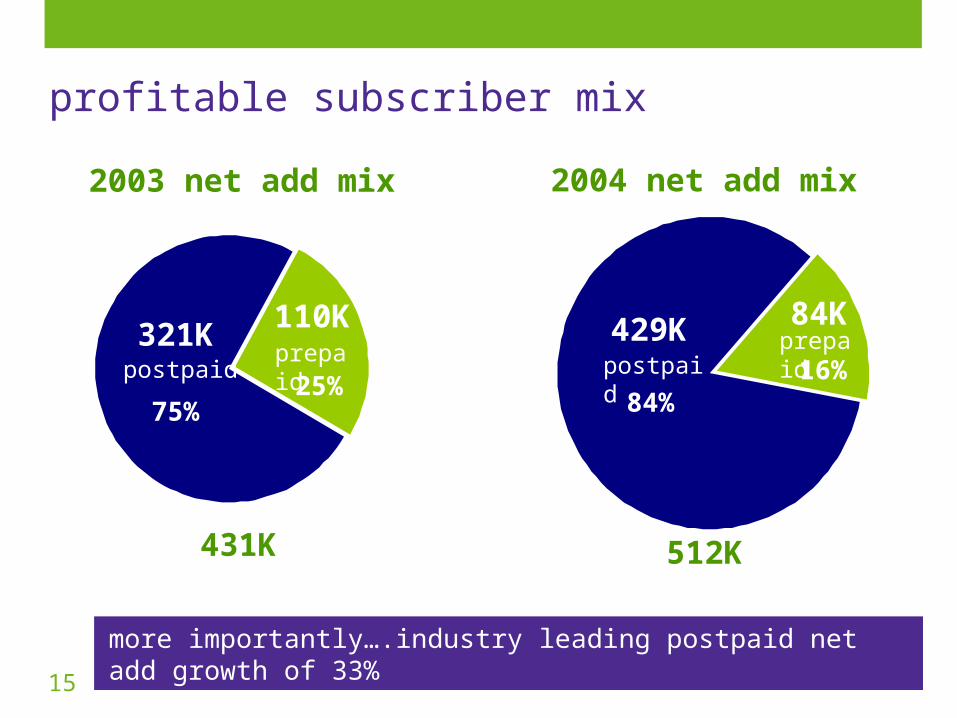

profitable subscriber mix

more importantly….industry leading postpaid net add growth of 33%

512K

2004 net add mix

84K

postpaidprepaid

84%

431K

2003 net add mix

prepaid

25%postpaid

75%

321K 429K110K

16%

16

Source: Company reports

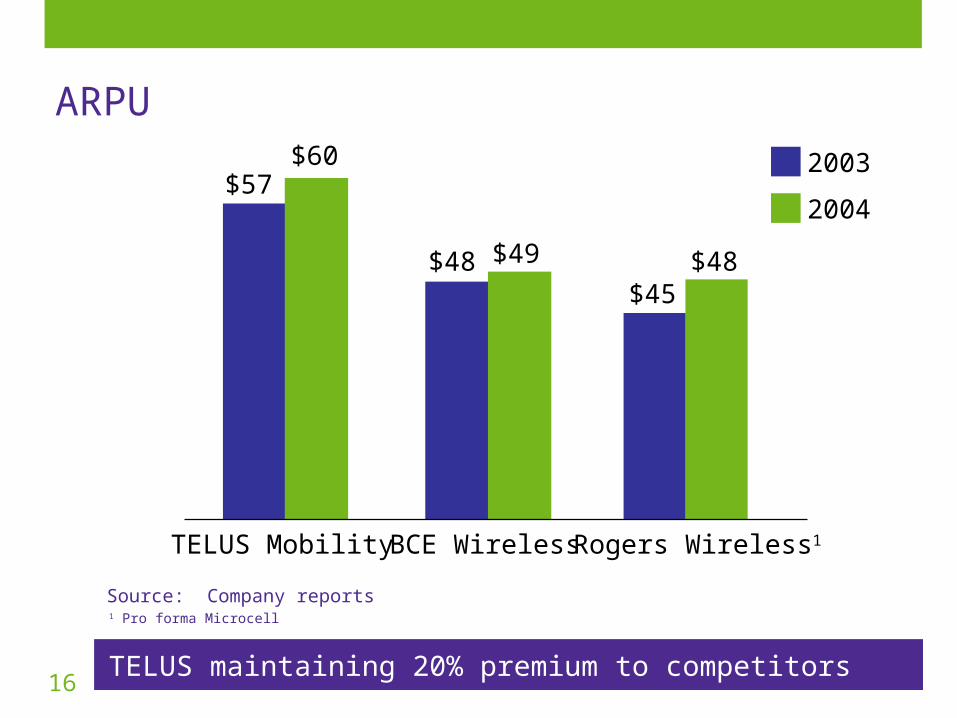

ARPU

TELUS maintaining 20% premium to competitors

TELUS Mobility Rogers Wireless1BCE Wireless

$57

$45$48

$60

$48$49

2003

2004

1 Pro forma Microcell

17

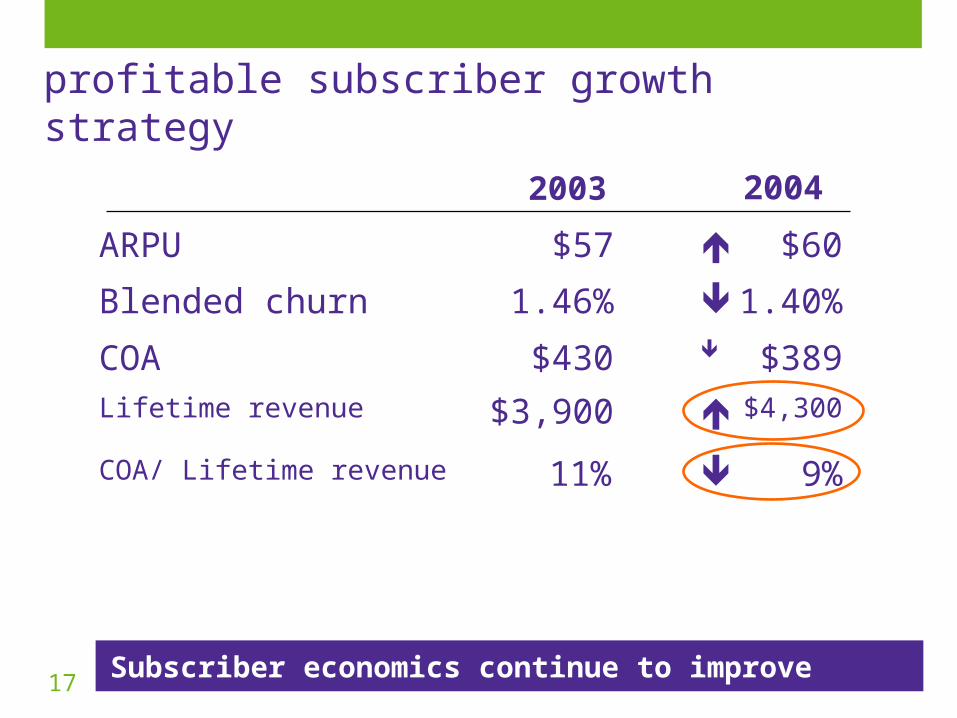

9%11%COA/ Lifetime revenue

1.40%1.46%Blended churn

$60ARPU $57

$389COA $430

20042003

$4,300

$3,900Lifetime revenue

Subscriber economics continue to improve

profitable subscriber growth strategy

18

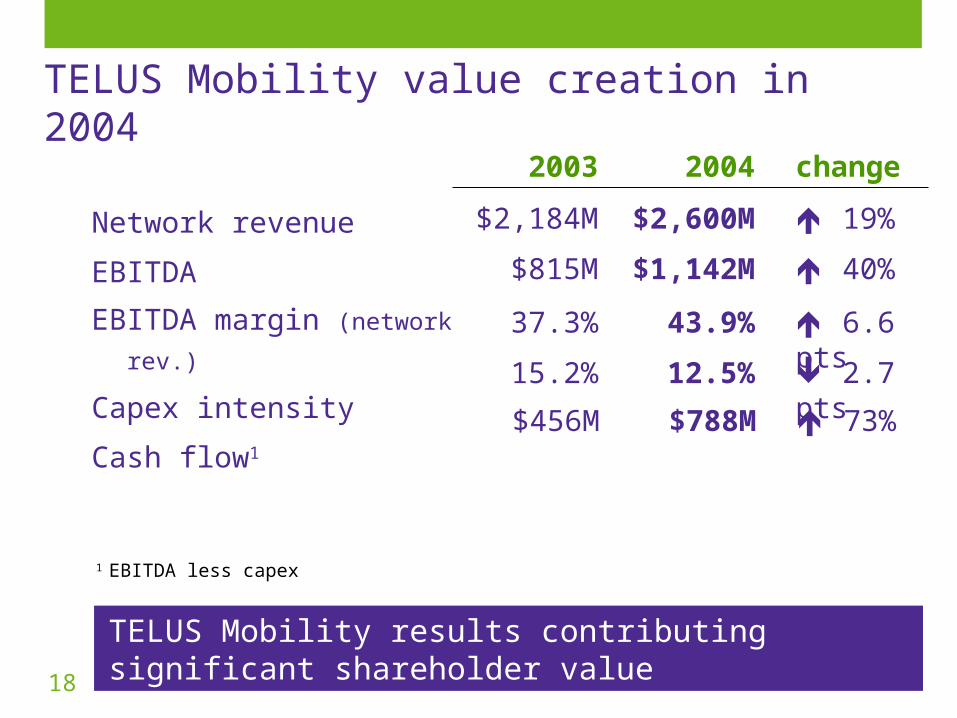

Network revenue

EBITDA

EBITDA margin (network rev.)

Capex intensity

Cash flow1

1 EBITDA less capex

2003 2004 change

$2,184M $2,600M 19%

$815M $1,142M 40%

37.3% 43.9% 6.6 pts

15.2% 12.5% 2.7 pts

$456M $788M 73%

TELUS Mobility value creation in 2004

TELUS Mobility results contributing significant shareholder value

19

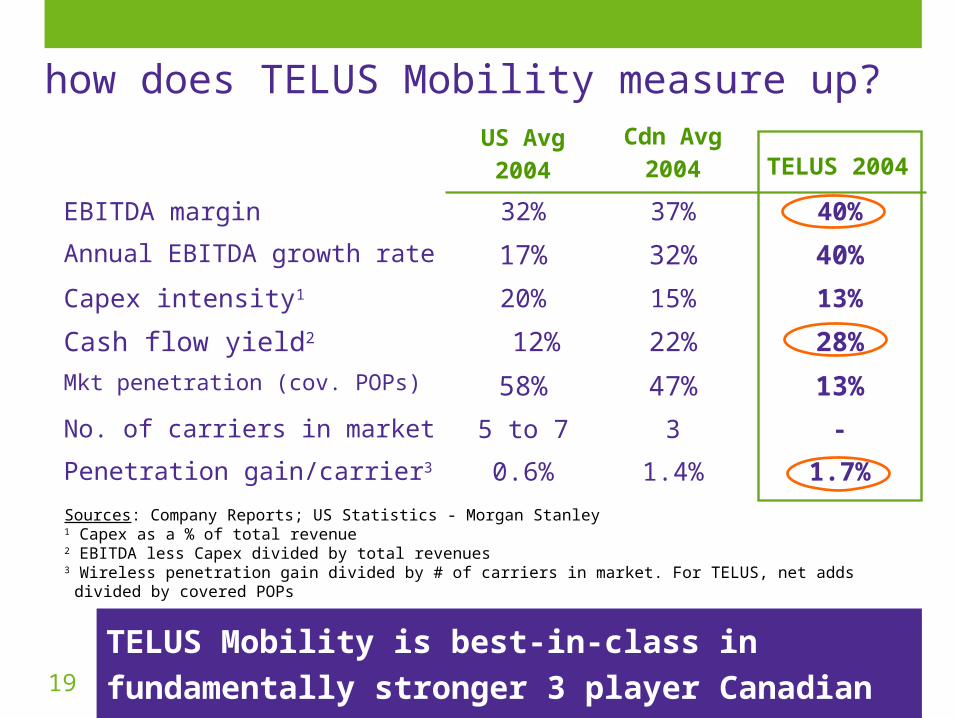

how does TELUS Mobility measure up?

Sources: Company Reports; US Statistics - Morgan Stanley1 Capex as a % of total revenue2 EBITDA less Capex divided by total revenues

3 Wireless penetration gain divided by # of carriers in market. For TELUS, net adds divided by covered POPs

Penetration gain/carrier3

No. of carriers in market

Mkt penetration (cov. POPs)

Cash flow yield2

Capex intensity1

Annual EBITDA growth rate

EBITDA margin

0.6%

5 to 7

58%

12%

20%

17%

32%

US Avg 2004

1.4%

3

47%

22%

15%

32%

37%

Cdn Avg

2004

1.7%

-

13%

28%

13%

40%

40%

TELUS 2004

TELUS Mobility is best-in-class in fundamentally

stronger 3 player Canadian wireless industry

20

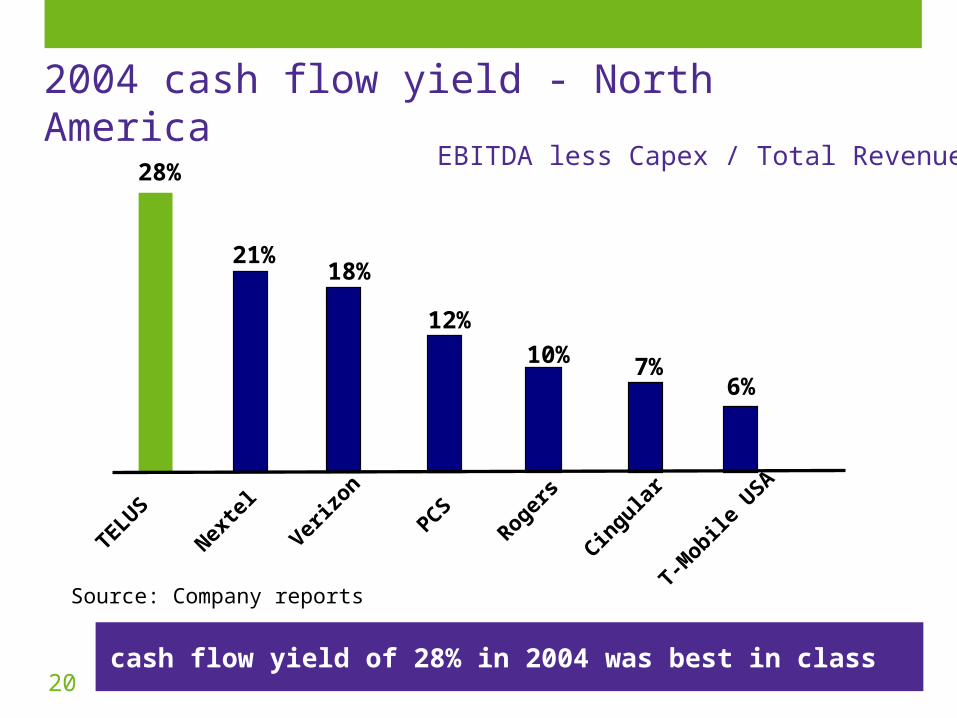

28%

21%18%

12%

10% 7%6%

TELUS

Verizo

n

Nexte

lPCS

Rogers

Cingula

r

T-Mobile

USA

2004 cash flow yield - North America

Source: Company reports

EBITDA less Capex / Total Revenue

cash flow yield of 28% in 2004 was best in class

21

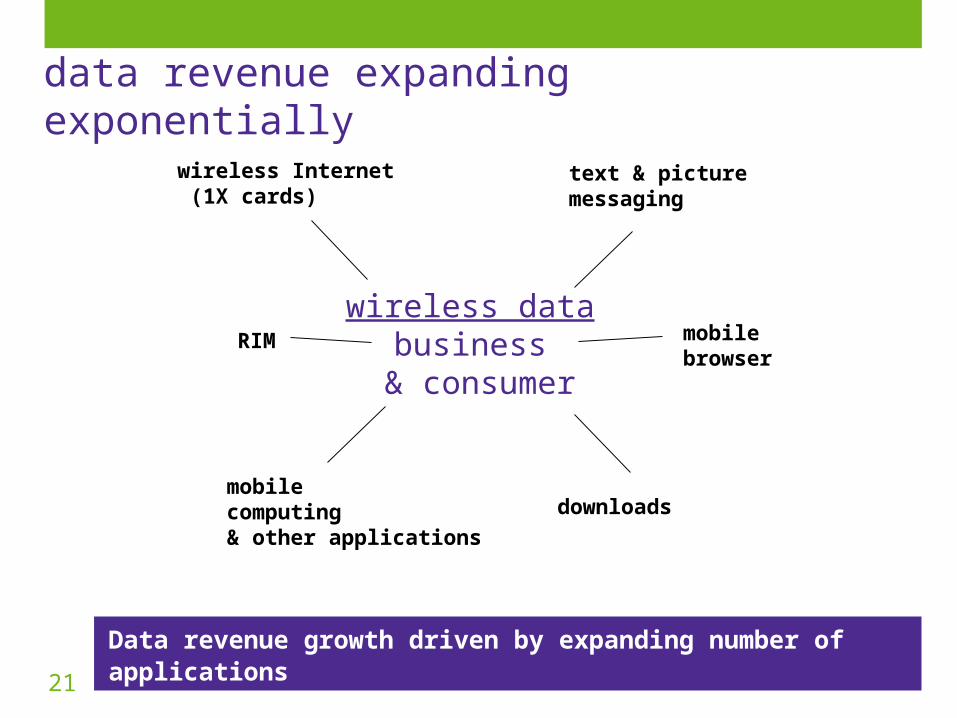

data revenue expanding exponentially

Data revenue growth driven by expanding number of applications

text & picturemessaging

mobilebrowser

downloadsmobilecomputing& other applications

RIM

wireless Internet (1X cards)

wireless databusiness

& consumer

22

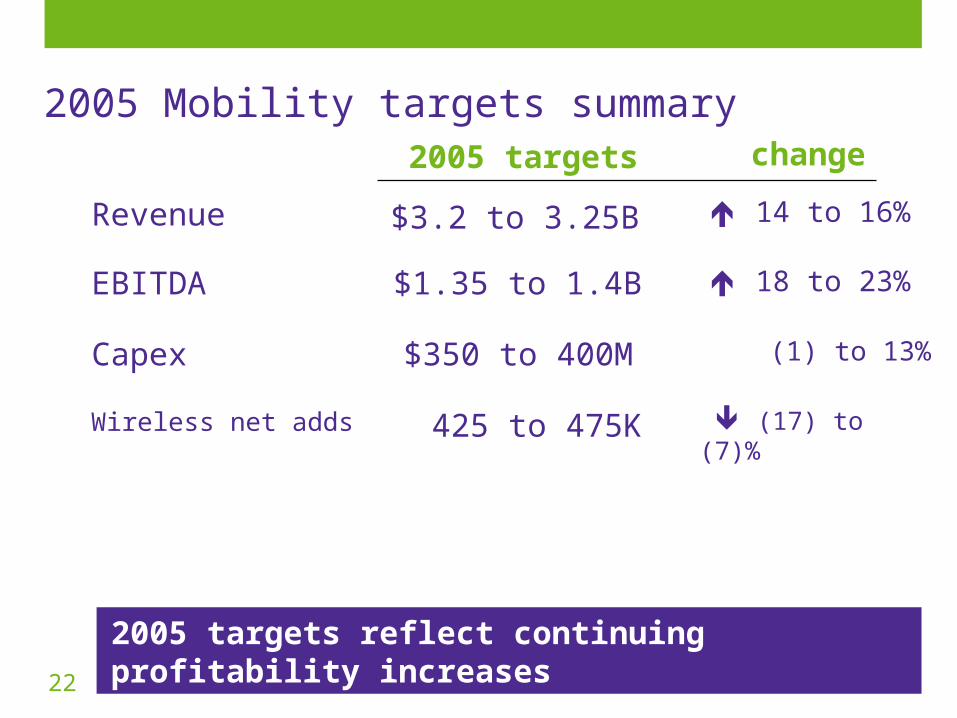

(1) to 13%$350 to 400MCapex

18 to 23%

change

EBITDA

Revenue

2005 targets

$1.35 to 1.4B

$3.2 to 3.25B 14 to 16%

2005 targets reflect continuing profitability increases

2005 Mobility targets summary

(17) to (7)% 425 to 475KWireless net adds

23

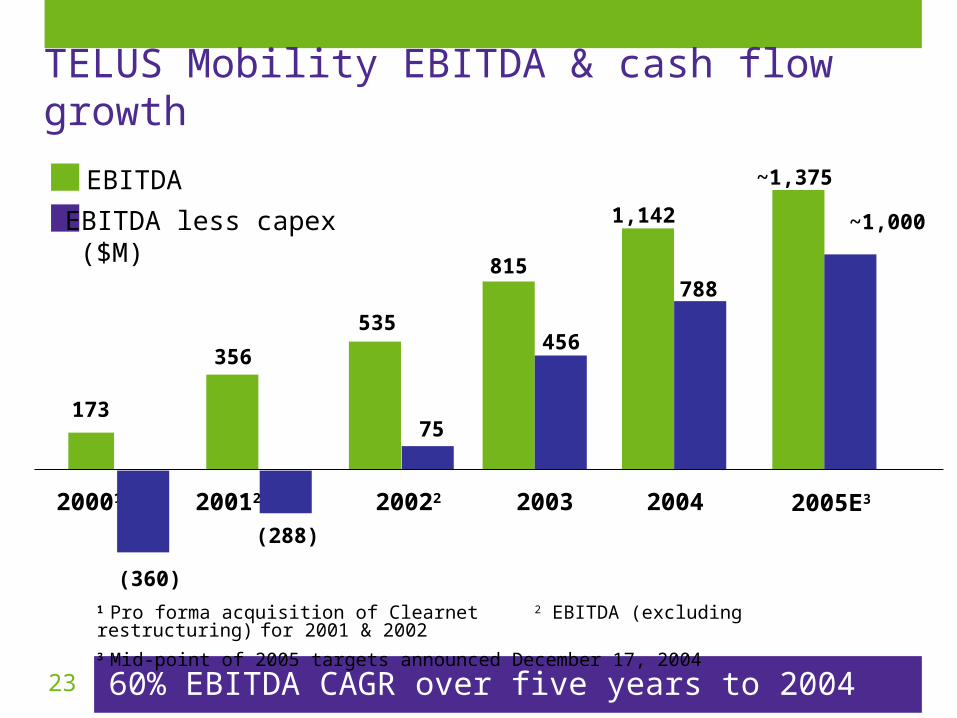

TELUS Mobility EBITDA & cash flow growth

60% EBITDA CAGR over five years to 2004

1 Pro forma acquisition of Clearnet 2 EBITDA (excluding restructuring) for 2001 & 2002

3 Mid-point of 2005 targets announced December 17, 2004

(360)

173

815

200320001

356

20012

535

20022

1,142

2004

456

(288)

75

EBITDA

EBITDA less capex($M)

788

2005E3

~1,375

~1,000

TELUS in 2005

25

Enhance our leadership position in wireless

Leverage our investments in high speed Internet through Future Friendly home services

Accelerate our wireline performance in Ontario & Quebec

Grow brand value through superior customer experience (via leading IP solutions and improved customer care)

Drive continual improvements in productivity

Reach a new collective agreement

corporate priorities for 2005

2005 priorities entirely consistent with 2004

26

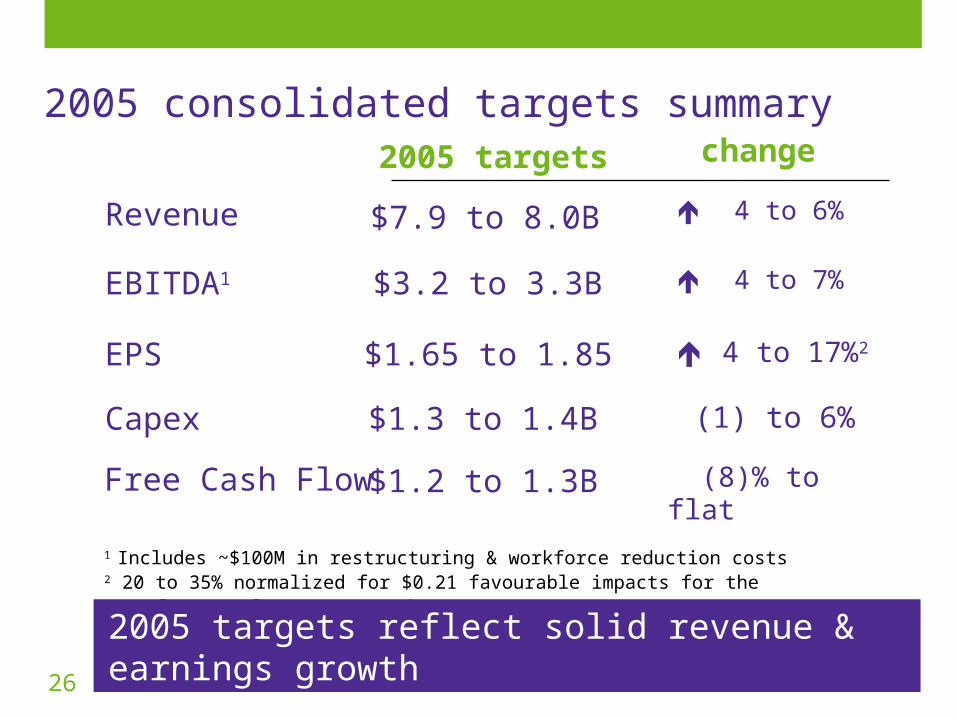

(1) to 6%$1.3 to 1.4BCapex

4 to 17%2$1.65 to 1.85EPS

4 to 7%

change

EBITDA1

Revenue

2005 targets

$3.2 to 3.3B

$7.9 to 8.0B

1 Includes ~$100M in restructuring & workforce reduction costs2 20 to 35% normalized for $0.21 favourable impacts for the settlement of tax matters in 2004

Free Cash Flow $1.2 to 1.3B

4 to 6%

2005 targets reflect solid revenue & earnings growth

2005 consolidated targets summary

(8)% to flat

27

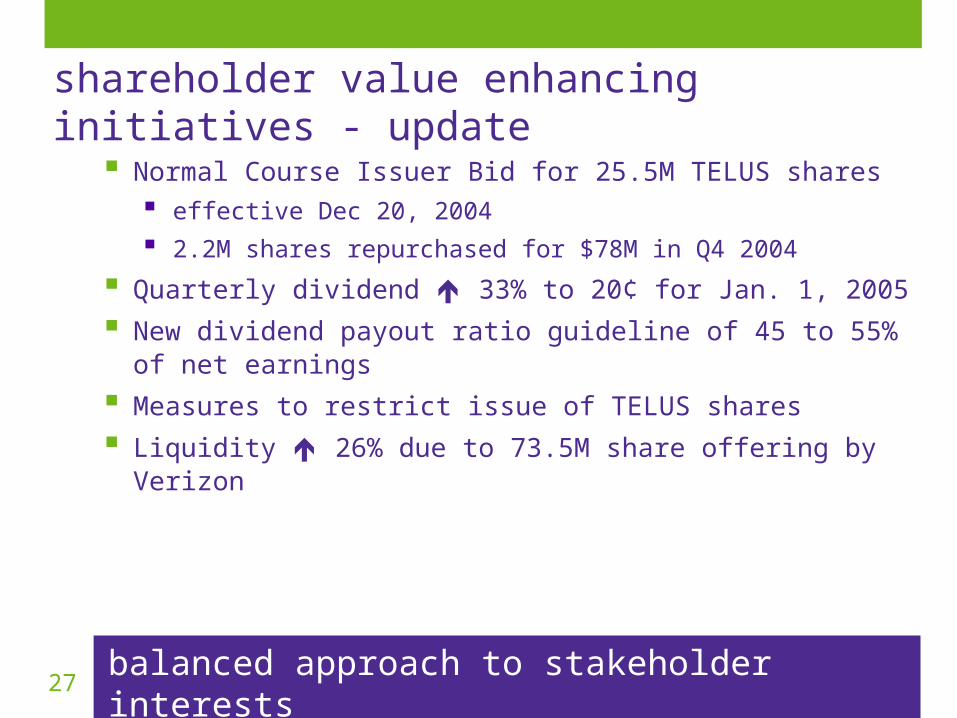

Normal Course Issuer Bid for 25.5M TELUS shares effective Dec 20, 2004

2.2M shares repurchased for $78M in Q4 2004

Quarterly dividend 33% to 20¢ for Jan. 1, 2005

New dividend payout ratio guideline of 45 to 55% of net earnings

Measures to restrict issue of TELUS shares

Liquidity 26% due to 73.5M share offering by Verizon

shareholder value enhancing initiatives - update

balanced approach to stakeholder interests

28

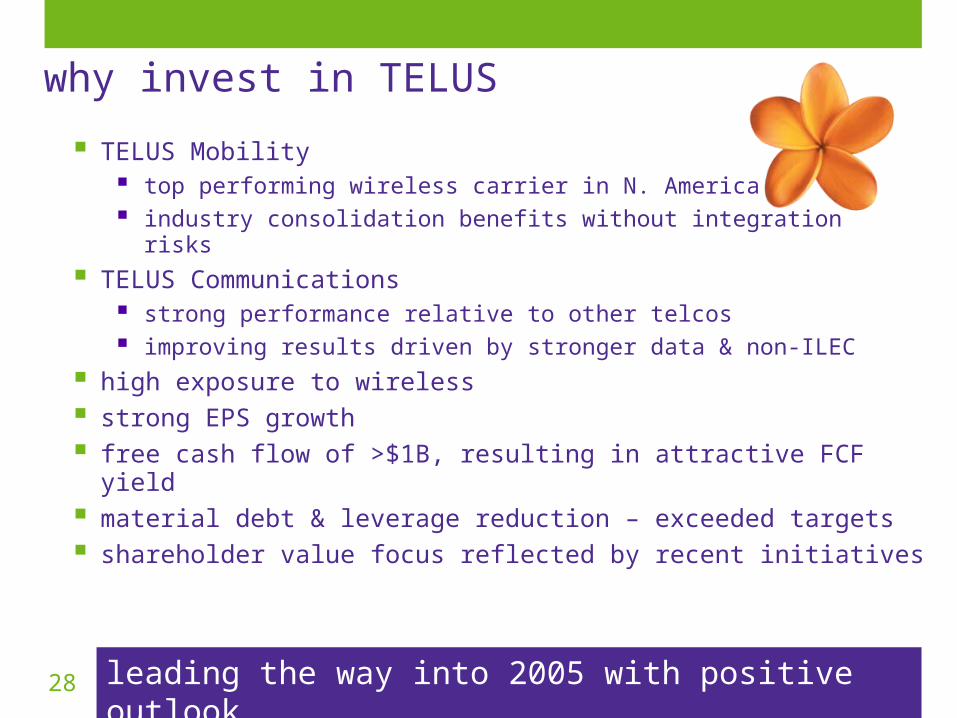

TELUS Mobility top performing wireless carrier in N. America industry consolidation benefits without integration risks

TELUS Communications strong performance relative to other telcos improving results driven by stronger data & non-ILEC

high exposure to wireless

strong EPS growth

free cash flow of >$1B, resulting in attractive FCF yield

material debt & leverage reduction – exceeded targets

shareholder value focus reflected by recent initiatives

leading the way into 2005 with positive outlook

why invest in TELUS

Appendix

31

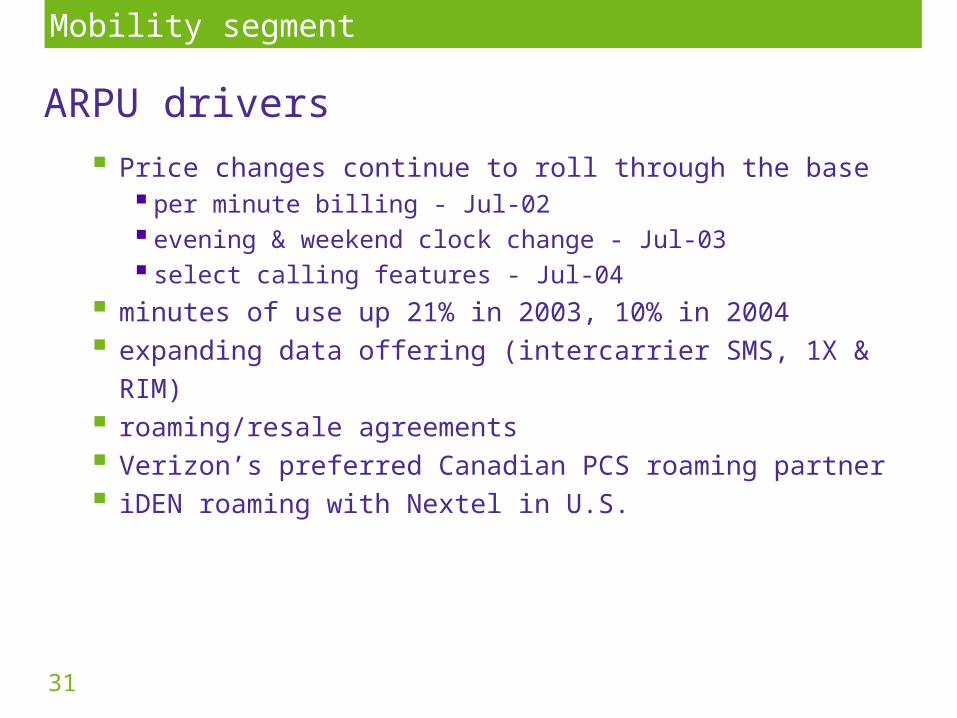

Price changes continue to roll through the base per minute billing - Jul-02 evening & weekend clock change - Jul-03 select calling features - Jul-04

minutes of use up 21% in 2003, 10% in 2004 expanding data offering (intercarrier SMS, 1X & RIM) roaming/resale agreements Verizon’s preferred Canadian PCS roaming partner iDEN roaming with Nextel in U.S.

ARPU drivers

Mobility segment

32

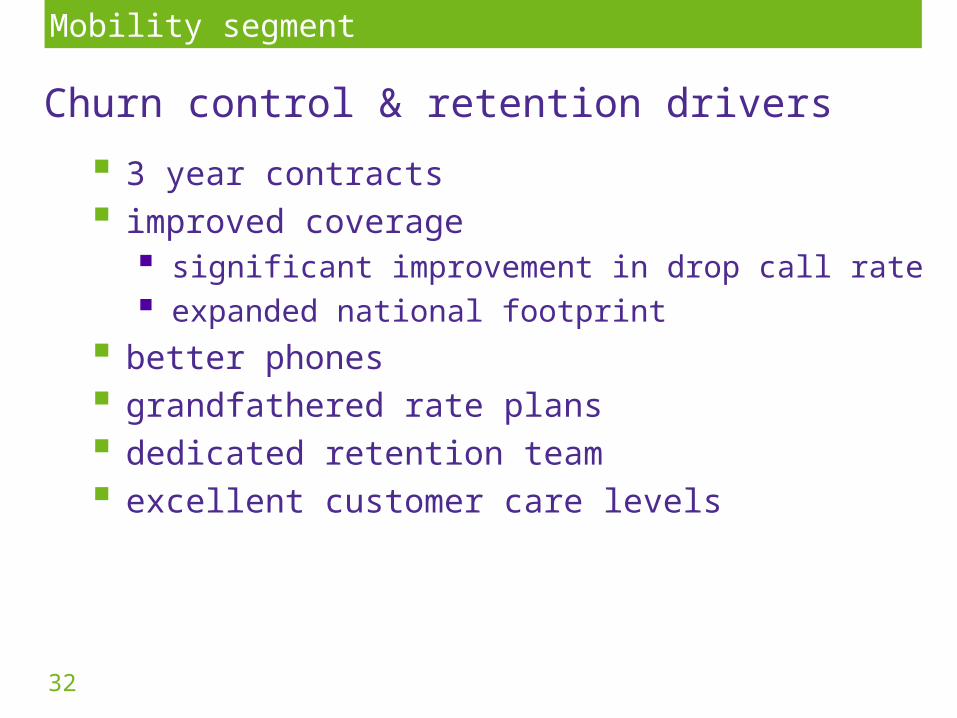

3 year contracts improved coverage

significant improvement in drop call rate expanded national footprint

better phones grandfathered rate plans dedicated retention team excellent customer care levels

Churn control & retention drivers

Mobility segment

33

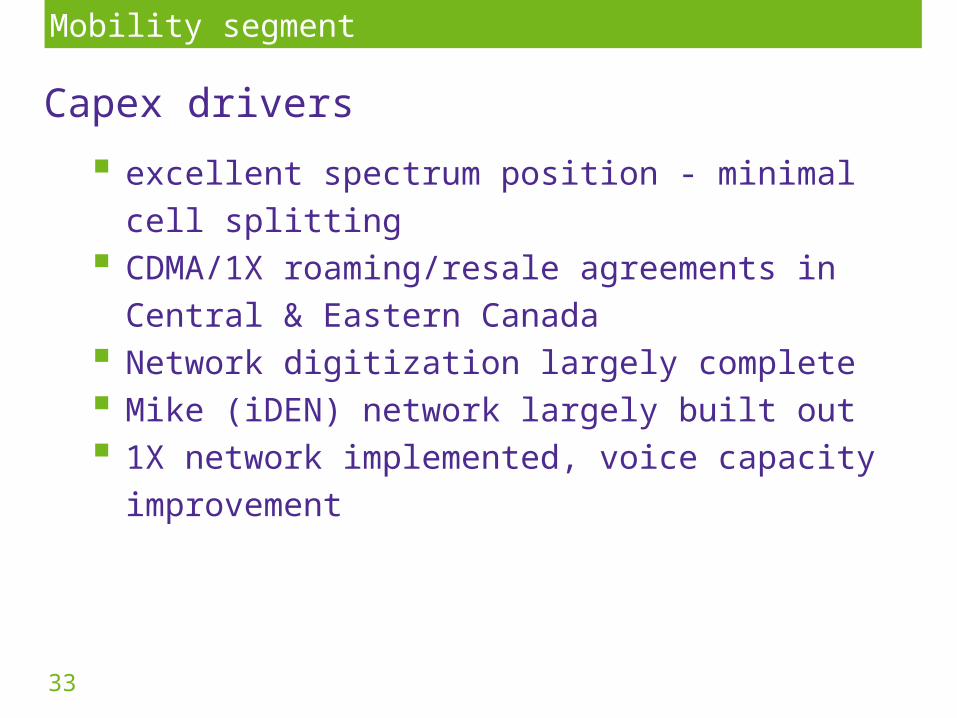

excellent spectrum position - minimal cell splitting CDMA/1X roaming/resale agreements in Central &

Eastern Canada Network digitization largely complete Mike (iDEN) network largely built out 1X network implemented, voice capacity

improvement

Capex drivers

Mobility segment

34

e.ComReport Watch

excellence in investor communications ranked 9th globally by Corporate Essentials, “Annual Report of

Annual Reports”

1st in Canada; 2nd in North America ranked #1 in world for “strategy, objectives & outlook”

10 years of disclosure excellence in corporate reporting awards by Canadian Institute of Chartered Accountants

2003 annual report rated best in Canada

IR website ranked 3rd among global telcos by IR Web Report

member of DJSI, only N. American telco

35

excellence in … recognized as Canada’s Best Environmental Corporate

Citizen

only Canadian company to receive BEST award (ranked 6th globally) for employee learning and development

Illuminati Award for Best Leadership Development Program

long time “Imagine” company

focused on support of education, health & sports and arts