term- damir filipovi c outlines term-structure models · term-structure models damir filipovi c...

TRANSCRIPT

Term-StructureModels

DamirFilipovic

Outlines

Part 1: InterestRates andRelatedContracts

Part 2:Estimating theTerm-Structure

Part 3:Arbitrage Theory

Part 4: ShortRate Models

Part 5: Heath–Jarrow–Morton(HJM)Methodology

Part 6: ForwardMeasures

Part 7: Forwardsand Futures

Part 8:ConsistentTerm-StructureParametrizations

Part 9: AffineProcesses

Part 10: MarketModels

Term-Structure ModelsA Graduate Course

Damir Filipovic

Version 5 November 2009

Term-StructureModels

DamirFilipovic

Outlines

Part 1: InterestRates andRelatedContracts

Part 2:Estimating theTerm-Structure

Part 3:Arbitrage Theory

Part 4: ShortRate Models

Part 5: Heath–Jarrow–Morton(HJM)Methodology

Part 6: ForwardMeasures

Part 7: Forwardsand Futures

Part 8:ConsistentTerm-StructureParametrizations

Part 9: AffineProcesses

Part 10: MarketModels

Course Book

Term-StructureModels

DamirFilipovic

Outlines

Part 1: InterestRates andRelatedContracts

Part 2:Estimating theTerm-Structure

Part 3:Arbitrage Theory

Part 4: ShortRate Models

Part 5: Heath–Jarrow–Morton(HJM)Methodology

Part 6: ForwardMeasures

Part 7: Forwardsand Futures

Part 8:ConsistentTerm-StructureParametrizations

Part 9: AffineProcesses

Part 10: MarketModels

Outline

Part 1: Interest Rates and Related ContractsPart 2: Estimating the Term-StructurePart 3: Arbitrage TheoryPart 4: Short Rate ModelsPart 5: Heath–Jarrow–Morton (HJM) MethodologyPart 6: Forward MeasuresPart 7: Forwards and FuturesPart 8: Consistent Term-Structure ParametrizationsPart 9: Affine ProcessesPart 10: Market Models

Term-StructureModels

DamirFilipovic

Outlines

Part 1: InterestRates andRelatedContracts

Part 2:Estimating theTerm-Structure

Part 3:Arbitrage Theory

Part 4: ShortRate Models

Part 5: Heath–Jarrow–Morton(HJM)Methodology

Part 6: ForwardMeasures

Part 7: Forwardsand Futures

Part 8:ConsistentTerm-StructureParametrizations

Part 9: AffineProcesses

Part 10: MarketModels

Outline of Part 1

1 Zero-Coupon Bonds

2 Interest Rates

3 Money-Market Account and Short Rates

4 Coupon Bonds, Swaps and YieldsFixed Coupon BondsFloating Rate NotesInterest Rate SwapsYield and Duration

5 Market Conventions

6 Caps and FloorsBlack’s Formula

7 SwaptionsBlack’s Formula

Term-StructureModels

DamirFilipovic

Outlines

Part 1: InterestRates andRelatedContracts

Part 2:Estimating theTerm-Structure

Part 3:Arbitrage Theory

Part 4: ShortRate Models

Part 5: Heath–Jarrow–Morton(HJM)Methodology

Part 6: ForwardMeasures

Part 7: Forwardsand Futures

Part 8:ConsistentTerm-StructureParametrizations

Part 9: AffineProcesses

Part 10: MarketModels

Outline

Part 1: Interest Rates and Related ContractsPart 2: Estimating the Term-StructurePart 3: Arbitrage TheoryPart 4: Short Rate ModelsPart 5: Heath–Jarrow–Morton (HJM) MethodologyPart 6: Forward MeasuresPart 7: Forwards and FuturesPart 8: Consistent Term-Structure ParametrizationsPart 9: Affine ProcessesPart 10: Market Models

Term-StructureModels

DamirFilipovic

Outlines

Part 1: InterestRates andRelatedContracts

Part 2:Estimating theTerm-Structure

Part 3:Arbitrage Theory

Part 4: ShortRate Models

Part 5: Heath–Jarrow–Morton(HJM)Methodology

Part 6: ForwardMeasures

Part 7: Forwardsand Futures

Part 8:ConsistentTerm-StructureParametrizations

Part 9: AffineProcesses

Part 10: MarketModels

Outline of Part 2

8 A Bootstrapping Example

9 Non-parametric Estimation MethodsBond MarketsMoney MarketsProblems

10 Parametric Estimation MethodsEstimating the Discount Function with Cubic B-splinesSmoothing SplinesExponential–Polynomial Families

11 Principal Component AnalysisPrincipal Components of a Random VectorSample Principle ComponentsPCA of the Forward CurveCorrelation

Term-StructureModels

DamirFilipovic

Outlines

Part 1: InterestRates andRelatedContracts

Part 2:Estimating theTerm-Structure

Part 3:Arbitrage Theory

Part 4: ShortRate Models

Part 5: Heath–Jarrow–Morton(HJM)Methodology

Part 6: ForwardMeasures

Part 7: Forwardsand Futures

Part 8:ConsistentTerm-StructureParametrizations

Part 9: AffineProcesses

Part 10: MarketModels

Outline

Part 1: Interest Rates and Related ContractsPart 2: Estimating the Term-StructurePart 3: Arbitrage TheoryPart 4: Short Rate ModelsPart 5: Heath–Jarrow–Morton (HJM) MethodologyPart 6: Forward MeasuresPart 7: Forwards and FuturesPart 8: Consistent Term-Structure ParametrizationsPart 9: Affine ProcessesPart 10: Market Models

Term-StructureModels

DamirFilipovic

Outlines

Part 1: InterestRates andRelatedContracts

Part 2:Estimating theTerm-Structure

Part 3:Arbitrage Theory

Part 4: ShortRate Models

Part 5: Heath–Jarrow–Morton(HJM)Methodology

Part 6: ForwardMeasures

Part 7: Forwardsand Futures

Part 8:ConsistentTerm-StructureParametrizations

Part 9: AffineProcesses

Part 10: MarketModels

Outline of Part 3

12 Stochastic CalculusStochastic Differential Equations

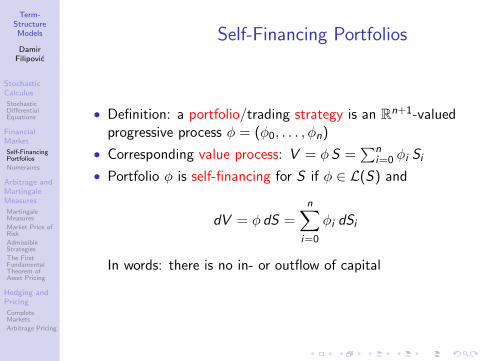

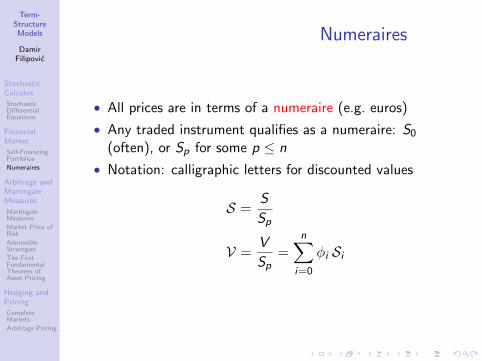

13 Financial MarketSelf-Financing PortfoliosNumeraires

14 Arbitrage and Martingale MeasuresMartingale MeasuresMarket Price of RiskAdmissible StrategiesThe First Fundamental Theorem of Asset Pricing

15 Hedging and PricingComplete MarketsArbitrage Pricing

Term-StructureModels

DamirFilipovic

Outlines

Part 1: InterestRates andRelatedContracts

Part 2:Estimating theTerm-Structure

Part 3:Arbitrage Theory

Part 4: ShortRate Models

Part 5: Heath–Jarrow–Morton(HJM)Methodology

Part 6: ForwardMeasures

Part 7: Forwardsand Futures

Part 8:ConsistentTerm-StructureParametrizations

Part 9: AffineProcesses

Part 10: MarketModels

Outline

Part 1: Interest Rates and Related ContractsPart 2: Estimating the Term-StructurePart 3: Arbitrage TheoryPart 4: Short Rate ModelsPart 5: Heath–Jarrow–Morton (HJM) MethodologyPart 6: Forward MeasuresPart 7: Forwards and FuturesPart 8: Consistent Term-Structure ParametrizationsPart 9: Affine ProcessesPart 10: Market Models

Term-StructureModels

DamirFilipovic

Outlines

Part 1: InterestRates andRelatedContracts

Part 2:Estimating theTerm-Structure

Part 3:Arbitrage Theory

Part 4: ShortRate Models

Part 5: Heath–Jarrow–Morton(HJM)Methodology

Part 6: ForwardMeasures

Part 7: Forwardsand Futures

Part 8:ConsistentTerm-StructureParametrizations

Part 9: AffineProcesses

Part 10: MarketModels

Outline of Part 4

16 Generalities

17 Diffusion Short-Rate ModelsExamplesInverting the Forward Curve

18 Affine Term-Structures

19 Some Standard ModelsVasicek ModelCIR ModelDothan ModelHo–Lee ModelHull–White Model

Term-StructureModels

DamirFilipovic

Outlines

Part 1: InterestRates andRelatedContracts

Part 2:Estimating theTerm-Structure

Part 3:Arbitrage Theory

Part 4: ShortRate Models

Part 5: Heath–Jarrow–Morton(HJM)Methodology

Part 6: ForwardMeasures

Part 7: Forwardsand Futures

Part 8:ConsistentTerm-StructureParametrizations

Part 9: AffineProcesses

Part 10: MarketModels

Outline

Part 1: Interest Rates and Related ContractsPart 2: Estimating the Term-StructurePart 3: Arbitrage TheoryPart 4: Short Rate ModelsPart 5: Heath–Jarrow–Morton (HJM) MethodologyPart 6: Forward MeasuresPart 7: Forwards and FuturesPart 8: Consistent Term-Structure ParametrizationsPart 9: Affine ProcessesPart 10: Market Models

Term-StructureModels

DamirFilipovic

Outlines

Part 1: InterestRates andRelatedContracts

Part 2:Estimating theTerm-Structure

Part 3:Arbitrage Theory

Part 4: ShortRate Models

Part 5: Heath–Jarrow–Morton(HJM)Methodology

Part 6: ForwardMeasures

Part 7: Forwardsand Futures

Part 8:ConsistentTerm-StructureParametrizations

Part 9: AffineProcesses

Part 10: MarketModels

Outline of Part 5

20 Forward Curve Movements

21 Absence of Arbitrage

22 Implied Short-Rate Dynamics

23 HJM ModelsProportional Volatility

24 Fubini’s Theorem

Term-StructureModels

DamirFilipovic

Outlines

Part 1: InterestRates andRelatedContracts

Part 2:Estimating theTerm-Structure

Part 3:Arbitrage Theory

Part 4: ShortRate Models

Part 5: Heath–Jarrow–Morton(HJM)Methodology

Part 6: ForwardMeasures

Part 7: Forwardsand Futures

Part 8:ConsistentTerm-StructureParametrizations

Part 9: AffineProcesses

Part 10: MarketModels

Outline

Part 1: Interest Rates and Related ContractsPart 2: Estimating the Term-StructurePart 3: Arbitrage TheoryPart 4: Short Rate ModelsPart 5: Heath–Jarrow–Morton (HJM) MethodologyPart 6: Forward MeasuresPart 7: Forwards and FuturesPart 8: Consistent Term-Structure ParametrizationsPart 9: Affine ProcessesPart 10: Market Models

Term-StructureModels

DamirFilipovic

Outlines

Part 1: InterestRates andRelatedContracts

Part 2:Estimating theTerm-Structure

Part 3:Arbitrage Theory

Part 4: ShortRate Models

Part 5: Heath–Jarrow–Morton(HJM)Methodology

Part 6: ForwardMeasures

Part 7: Forwardsand Futures

Part 8:ConsistentTerm-StructureParametrizations

Part 9: AffineProcesses

Part 10: MarketModels

Outline of Part 6

25 T -Bond as Numeraire

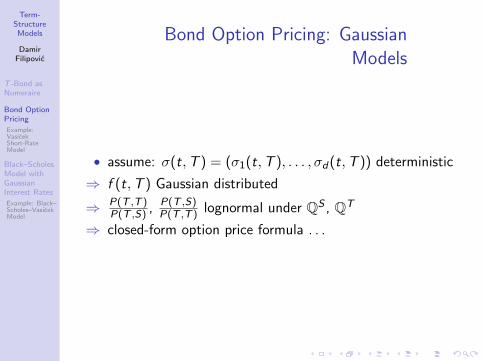

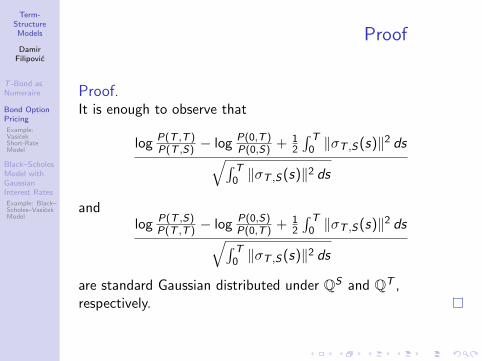

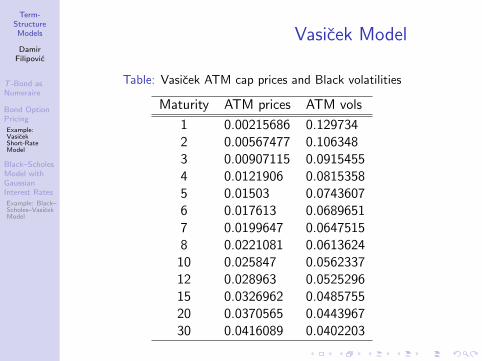

26 Bond Option PricingExample: Vasicek Short-Rate Model

27 Black–Scholes Model with Gaussian Interest RatesExample: Black–Scholes–Vasicek Model

Term-StructureModels

DamirFilipovic

Outlines

Part 1: InterestRates andRelatedContracts

Part 2:Estimating theTerm-Structure

Part 3:Arbitrage Theory

Part 4: ShortRate Models

Part 5: Heath–Jarrow–Morton(HJM)Methodology

Part 6: ForwardMeasures

Part 7: Forwardsand Futures

Part 8:ConsistentTerm-StructureParametrizations

Part 9: AffineProcesses

Part 10: MarketModels

Outline

Part 1: Interest Rates and Related ContractsPart 2: Estimating the Term-StructurePart 3: Arbitrage TheoryPart 4: Short Rate ModelsPart 5: Heath–Jarrow–Morton (HJM) MethodologyPart 6: Forward MeasuresPart 7: Forwards and FuturesPart 8: Consistent Term-Structure ParametrizationsPart 9: Affine ProcessesPart 10: Market Models

Term-StructureModels

DamirFilipovic

Outlines

Part 1: InterestRates andRelatedContracts

Part 2:Estimating theTerm-Structure

Part 3:Arbitrage Theory

Part 4: ShortRate Models

Part 5: Heath–Jarrow–Morton(HJM)Methodology

Part 6: ForwardMeasures

Part 7: Forwardsand Futures

Part 8:ConsistentTerm-StructureParametrizations

Part 9: AffineProcesses

Part 10: MarketModels

Outline of Part 7

28 Forward Contracts

29 Futures ContractsInterest Rate Futures

30 Forward vs. Futures in a Gaussian Setup

Term-StructureModels

DamirFilipovic

Outlines

Part 1: InterestRates andRelatedContracts

Part 2:Estimating theTerm-Structure

Part 3:Arbitrage Theory

Part 4: ShortRate Models

Part 5: Heath–Jarrow–Morton(HJM)Methodology

Part 6: ForwardMeasures

Part 7: Forwardsand Futures

Part 8:ConsistentTerm-StructureParametrizations

Part 9: AffineProcesses

Part 10: MarketModels

Outline

Part 1: Interest Rates and Related ContractsPart 2: Estimating the Term-StructurePart 3: Arbitrage TheoryPart 4: Short Rate ModelsPart 5: Heath–Jarrow–Morton (HJM) MethodologyPart 6: Forward MeasuresPart 7: Forwards and FuturesPart 8: Consistent Term-Structure ParametrizationsPart 9: Affine ProcessesPart 10: Market Models

Term-StructureModels

DamirFilipovic

Outlines

Part 1: InterestRates andRelatedContracts

Part 2:Estimating theTerm-Structure

Part 3:Arbitrage Theory

Part 4: ShortRate Models

Part 5: Heath–Jarrow–Morton(HJM)Methodology

Part 6: ForwardMeasures

Part 7: Forwardsand Futures

Part 8:ConsistentTerm-StructureParametrizations

Part 9: AffineProcesses

Part 10: MarketModels

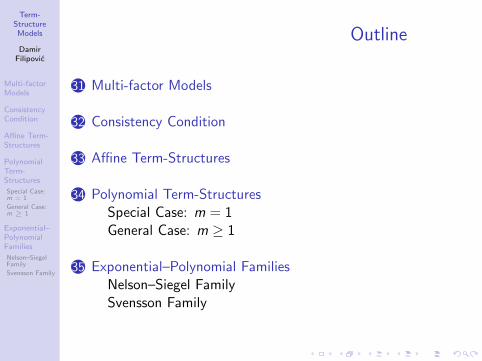

Outline of Part 8

31 Multi-factor Models

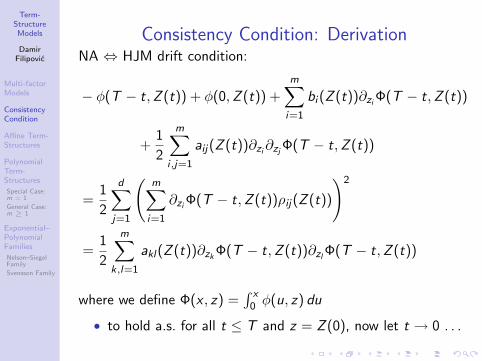

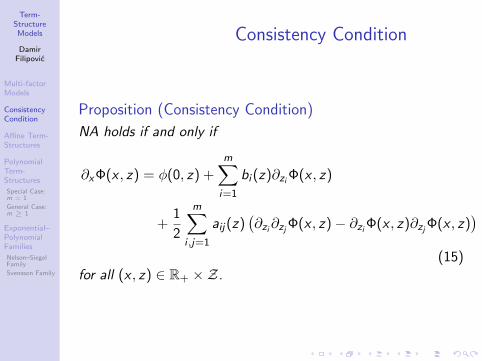

32 Consistency Condition

33 Affine Term-Structures

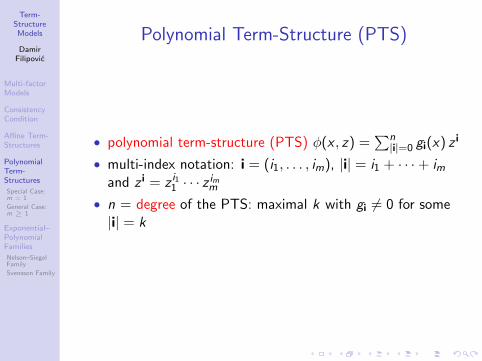

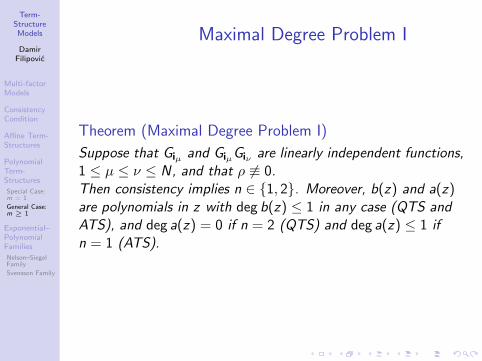

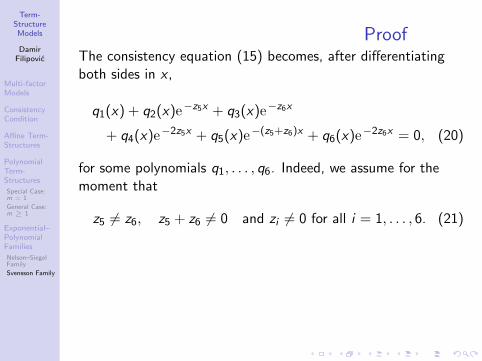

34 Polynomial Term-StructuresSpecial Case: m = 1General Case: m ≥ 1

35 Exponential–Polynomial FamiliesNelson–Siegel FamilySvensson Family

Term-StructureModels

DamirFilipovic

Outlines

Part 1: InterestRates andRelatedContracts

Part 2:Estimating theTerm-Structure

Part 3:Arbitrage Theory

Part 4: ShortRate Models

Part 5: Heath–Jarrow–Morton(HJM)Methodology

Part 6: ForwardMeasures

Part 7: Forwardsand Futures

Part 8:ConsistentTerm-StructureParametrizations

Part 9: AffineProcesses

Part 10: MarketModels

Outline

Part 1: Interest Rates and Related ContractsPart 2: Estimating the Term-StructurePart 3: Arbitrage TheoryPart 4: Short Rate ModelsPart 5: Heath–Jarrow–Morton (HJM) MethodologyPart 6: Forward MeasuresPart 7: Forwards and FuturesPart 8: Consistent Term-Structure ParametrizationsPart 9: Affine ProcessesPart 10: Market Models

Term-StructureModels

DamirFilipovic

Outlines

Part 1: InterestRates andRelatedContracts

Part 2:Estimating theTerm-Structure

Part 3:Arbitrage Theory

Part 4: ShortRate Models

Part 5: Heath–Jarrow–Morton(HJM)Methodology

Part 6: ForwardMeasures

Part 7: Forwardsand Futures

Part 8:ConsistentTerm-StructureParametrizations

Part 9: AffineProcesses

Part 10: MarketModels

Outline of Part 9

36 Definition and Characterization of Affine Processes

37 Canonical State Space

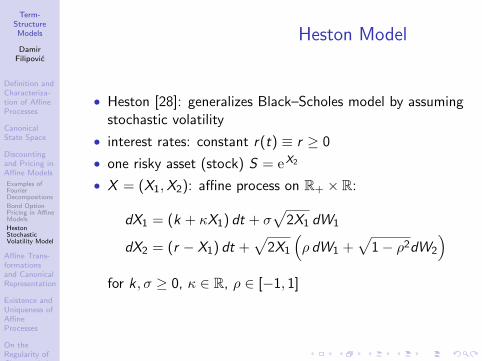

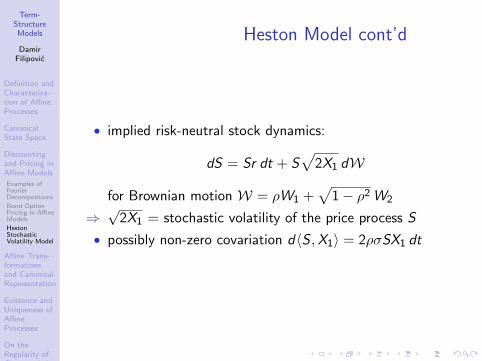

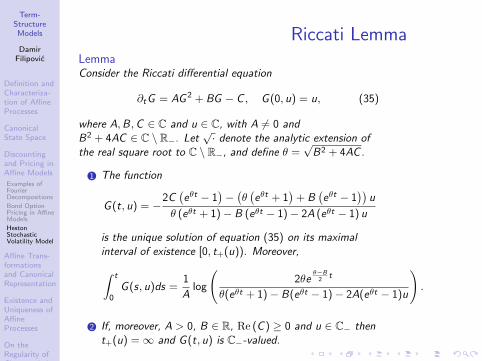

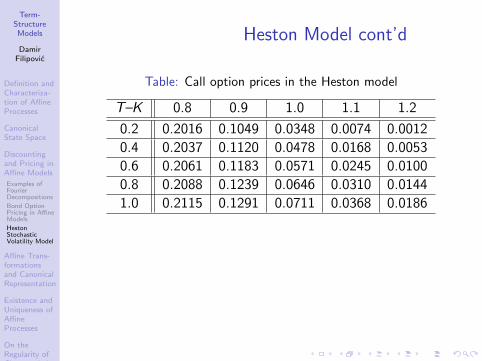

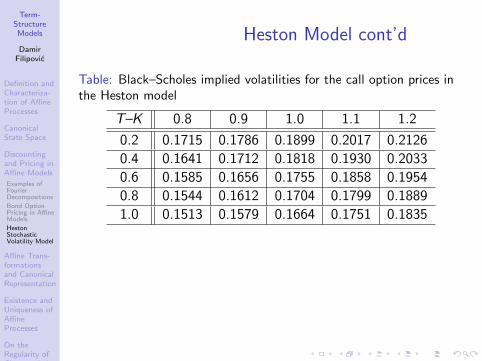

38 Discounting and Pricing in Affine ModelsExamples of Fourier DecompositionsBond Option Pricing in Affine ModelsHeston Stochastic Volatility Model

39 Affine Transformations and Canonical Representation

40 Existence and Uniqueness of Affine Processes

41 On the Regularity of Characteristic Functions

42 Auxiliary Results for Differential Equations

Term-StructureModels

DamirFilipovic

Outlines

Part 1: InterestRates andRelatedContracts

Part 2:Estimating theTerm-Structure

Part 3:Arbitrage Theory

Part 4: ShortRate Models

Part 5: Heath–Jarrow–Morton(HJM)Methodology

Part 6: ForwardMeasures

Part 7: Forwardsand Futures

Part 8:ConsistentTerm-StructureParametrizations

Part 9: AffineProcesses

Part 10: MarketModels

Outline

Part 1: Interest Rates and Related ContractsPart 2: Estimating the Term-StructurePart 3: Arbitrage TheoryPart 4: Short Rate ModelsPart 5: Heath–Jarrow–Morton (HJM) MethodologyPart 6: Forward MeasuresPart 7: Forwards and FuturesPart 8: Consistent Term-Structure ParametrizationsPart 9: Affine ProcessesPart 10: Market Models

Term-StructureModels

DamirFilipovic

Outlines

Part 1: InterestRates andRelatedContracts

Part 2:Estimating theTerm-Structure

Part 3:Arbitrage Theory

Part 4: ShortRate Models

Part 5: Heath–Jarrow–Morton(HJM)Methodology

Part 6: ForwardMeasures

Part 7: Forwardsand Futures

Part 8:ConsistentTerm-StructureParametrizations

Part 9: AffineProcesses

Part 10: MarketModels

Outline of Part 10

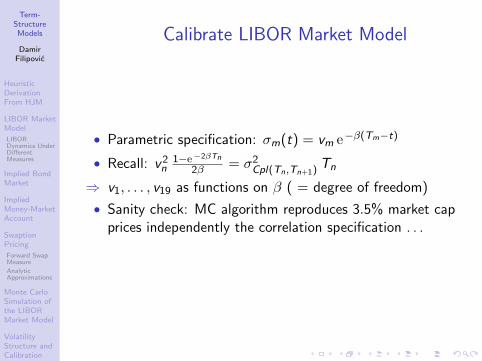

43 Heuristic Derivation From HJM

44 LIBOR Market ModelLIBOR Dynamics Under Different Measures

45 Implied Bond Market

46 Implied Money-Market Account

47 Swaption PricingForward Swap MeasureAnalytic Approximations

48 Monte Carlo Simulation of the LIBOR Market Model

49 Volatility Structure and CalibrationPrincipal Component AnalysisCalibration to Market Quotes

50 Continuous-Tenor Case

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Part I

Interest Rates and Related Contracts

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Overview

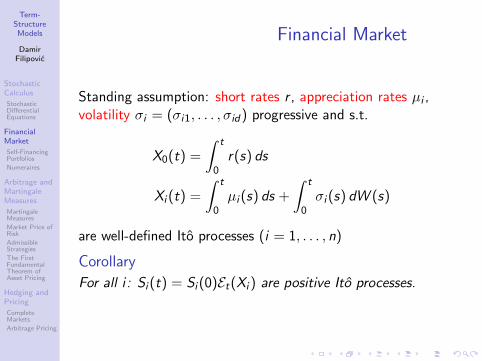

• Bond = securitized form of a loan

• Bonds: primary financial instruments in the market wherethe time value of money is traded

• This chapter: basis concepts of interest rates and bondmarkets:

• zero-coupon bonds• related interest rates• market conventions• market practice for pricing caps, floors and swaptions

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Outline

1 Zero-Coupon Bonds

2 Interest Rates

3 Money-Market Account and Short Rates

4 Coupon Bonds, Swaps and YieldsFixed Coupon BondsFloating Rate NotesInterest Rate SwapsYield and Duration

5 Market Conventions

6 Caps and FloorsBlack’s Formula

7 SwaptionsBlack’s Formula

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Outline

1 Zero-Coupon Bonds

2 Interest Rates

3 Money-Market Account and Short Rates

4 Coupon Bonds, Swaps and YieldsFixed Coupon BondsFloating Rate NotesInterest Rate SwapsYield and Duration

5 Market Conventions

6 Caps and FloorsBlack’s Formula

7 SwaptionsBlack’s Formula

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Zero-Coupon Bonds

• 1 euro today is worth more than 1 euro tomorrow

• zero-coupon bond pays 1 euro at maturity T

• time t value denoted by P(t,T )

Figure: Cash flow of a T -bond.

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Standing Assumptions

In theory we will assume that:

• there exists a frictionless market for all T -bonds

• P(T ,T ) = 1 for all T

• P(t,T ) is differentiable in T

In reality these assumptions are not always satisfied!Q: why not assuming P(t,T ) ≤ 1?

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Term-Structure

The term-structure of zero-coupon bond prices (or discountcurve) T 7→ P(t,T ) is smooth:

Figure: Term-structure T 7→ P(t,T ).

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Trajectories

Note: t 7→ P(t,T ) is stochastic process:

Figure: T -bond price process t 7→ P(t,T ).

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Outline

1 Zero-Coupon Bonds

2 Interest Rates

3 Money-Market Account and Short Rates

4 Coupon Bonds, Swaps and YieldsFixed Coupon BondsFloating Rate NotesInterest Rate SwapsYield and Duration

5 Market Conventions

6 Caps and FloorsBlack’s Formula

7 SwaptionsBlack’s Formula

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Forward Rate Agreement (FRA)FRA: current date t, expiry date T > t, maturity S > T :

• At t: sell one T -bond and buy P(t,T )P(t,S) S-bonds: zero net

investment.

• At T : pay one euro.

• At S : receive P(t,T )P(t,S) euros.

Figure: Net cash flow

Net effect: forward investment of one euro at time T yieldingP(t,T )P(t,S) euros at S with certainty.

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Simply Compounded Interest Rates

• simple forward rate for [T , S ] prevailing at t:

F (t; T ,S) =1

S − T

(P(t,T )

P(t, S)− 1

),

which is equivalent to

1 + (S − T )F (t; T , S) =P(t,T )

P(t, S).

• simple spot rate for [t,T ]:

F (t,T ) = F (t; t,T ) =1

T − t

(1

P(t,T )− 1

).

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

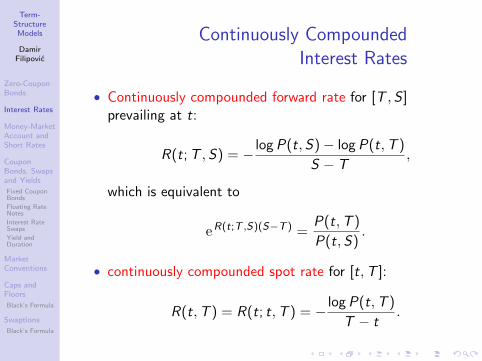

Continuously CompoundedInterest Rates

• Continuously compounded forward rate for [T ,S ]prevailing at t:

R(t; T ,S) = − log P(t,S)− log P(t,T )

S − T,

which is equivalent to

eR(t;T ,S)(S−T ) =P(t,T )

P(t,S).

• continuously compounded spot rate for [t,T ]:

R(t,T ) = R(t; t,T ) = − log P(t,T )

T − t.

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Instantaneous Interest Rates

• let S ↓ T :

• forward rate with maturity T prevailing at time t:

f (t,T ) = limS↓T

R(t; T , S) = −∂ log P(t,T )

∂T

which is equivalent to

P(t,T ) = e−∫ Tt f (t,u) du.

T 7→ f (t,T ) is called forward curve at time t.

• short rate at time t:

r(t) = f (t, t) = limT↓t

R(t,T ).

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Market Example: LIBOR

• LIBOR (London Interbank Offered Rate): rate at whichhigh-credit financial institutions can borrow in interbankmarket.

• maturities: from overnight to 12 months

• quoted on a simple compounding basis. E.g.:three-months forward LIBOR for period [T ,T + 1/4] attime t is

L(t,T ) = F (t; T ,T + 1/4).

• under normal conditions considered as risk-free, but . . .

• . . . LIBOR may reflect liquidity and credit risk (August2007!)

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

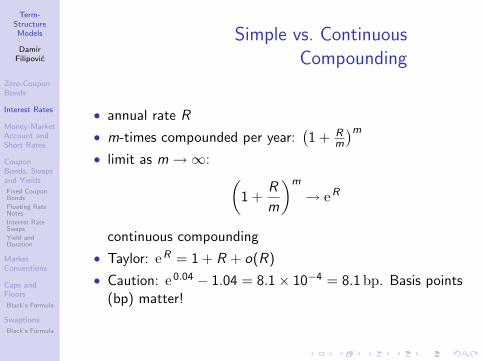

Simple vs. ContinuousCompounding

• annual rate R

• m-times compounded per year:(1 + R

m

)m• limit as m→∞: (

1 +R

m

)m

→ eR

continuous compounding

• Taylor: eR = 1 + R + o(R)

• Caution: e0.04 − 1.04 = 8.1× 10−4 = 8.1 bp. Basis points(bp) matter!

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Forward vs. Future Rates

• Can forward rates predict future spot rates?

• Thought experiment: deterministic world: all future ratesare known today (t)

• Consequence: P(t, S) = P(t,T )P(T , S) for all t ≤ T ≤ S

• This is equivalent to shifting forward curve:

f (t, S) = f (T ,S) = r(S), t ≤ T ≤ S

• In reality (non-deterministic): forecast of future short rateby forward rate have little predictive power

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Outline

1 Zero-Coupon Bonds

2 Interest Rates

3 Money-Market Account and Short Rates

4 Coupon Bonds, Swaps and YieldsFixed Coupon BondsFloating Rate NotesInterest Rate SwapsYield and Duration

5 Market Conventions

6 Caps and FloorsBlack’s Formula

7 SwaptionsBlack’s Formula

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Money-Market Account

• money-market account: instantaneous return r(t):

dB(t) = r(t)B(t)dt

• with B(0) = 1 this is equivalent to: B(t) = e∫ t

0 r(s) ds

• B is risk-free asset, r is risk-free rate of return

• B as numeraire: relate amounts of euro at different times

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Proxies for the Short Rate

• r(t) cannot be directly observed

• overnight interest rate not considered a good proxy(liquidity and microstructure effects)

• practiced solution: use longer rates as proxies, e.g. one- orthree months LIBOR (liquid)

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Outline

1 Zero-Coupon Bonds

2 Interest Rates

3 Money-Market Account and Short Rates

4 Coupon Bonds, Swaps and YieldsFixed Coupon BondsFloating Rate NotesInterest Rate SwapsYield and Duration

5 Market Conventions

6 Caps and FloorsBlack’s Formula

7 SwaptionsBlack’s Formula

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Outline

1 Zero-Coupon Bonds

2 Interest Rates

3 Money-Market Account and Short Rates

4 Coupon Bonds, Swaps and YieldsFixed Coupon BondsFloating Rate NotesInterest Rate SwapsYield and Duration

5 Market Conventions

6 Caps and FloorsBlack’s Formula

7 SwaptionsBlack’s Formula

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Fixed Coupon BondsA (fixed) coupon bond is specified by

• coupon dates T1 < · · · < Tn (Tn=maturity)

• fixed coupons c1, . . . , cn

• a nominal value N

Figure: cash flow

The price at t ≤ T1 is

p(t) =n∑

i=1

P(t,Ti )ci + P(t,Tn)N.

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Outline

1 Zero-Coupon Bonds

2 Interest Rates

3 Money-Market Account and Short Rates

4 Coupon Bonds, Swaps and YieldsFixed Coupon BondsFloating Rate NotesInterest Rate SwapsYield and Duration

5 Market Conventions

6 Caps and FloorsBlack’s Formula

7 SwaptionsBlack’s Formula

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Floating Rate NotesA floating rate note is specified by

• reset/settlement dates T0 < · · · < Tn (T0=first resetdate, Tn=maturity)

• a nominal value N• floating coupon payments at T1, . . . ,Tn

ci = (Ti − Ti−1)F (Ti−1,Ti )N

Figure: cash flow

Price at t ≤ T0 (replicate cash flow by buying N T0-bonds):

p(t) = NP(t,T0)

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Outline

1 Zero-Coupon Bonds

2 Interest Rates

3 Money-Market Account and Short Rates

4 Coupon Bonds, Swaps and YieldsFixed Coupon BondsFloating Rate NotesInterest Rate SwapsYield and Duration

5 Market Conventions

6 Caps and FloorsBlack’s Formula

7 SwaptionsBlack’s Formula

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

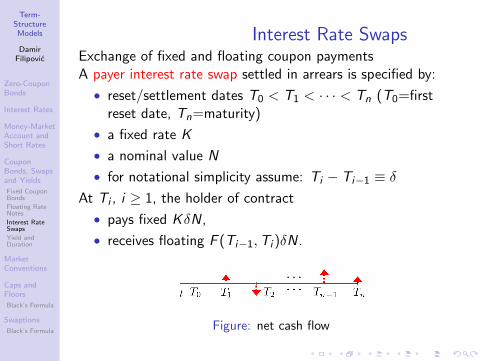

Interest Rate SwapsExchange of fixed and floating coupon paymentsA payer interest rate swap settled in arrears is specified by:

• reset/settlement dates T0 < T1 < · · · < Tn (T0=firstreset date, Tn=maturity)

• a fixed rate K

• a nominal value N

• for notational simplicity assume: Ti − Ti−1 ≡ δAt Ti , i ≥ 1, the holder of contract

• pays fixed KδN,

• receives floating F (Ti−1,Ti )δN.

Figure: net cash flow

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Swap Value

• value of payer interest rate swap at t ≤ T0:

Πp(t) = N

(P(t,T0)− P(t,Tn)− Kδ

n∑i=1

P(t,Ti )

)

= Nδn∑

i=1

P(t,Ti ) (F (t; Ti−1,Ti )− K )

• value of receiver interest rate swap at t ≤ T0:Πr (t) = −Πp(t)

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Swap Rate

• forward (or par) swap rate makes Πr (t) = −Πp(t) = 0:

Rswap(t) =P(t,T0)− P(t,Tn)

δ∑n

i=1 P(t,Ti )

=n∑

i=1

wi (t)F (t; Ti−1,Ti )

with weights wi (t) = P(t,Ti )∑nj=1 P(t,Tj )

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Market Quotes for Par Swap Rates

source: WestLBURL: www.westlbmarkets.de/cms/sitecontent/ib/investmentbankinginternet/de/services/new swapindikationen.standard.gid

Figure: forward swap rates from 25 Sep 09 (for illustration)

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Swap Example

Swaps were developed because different companies couldborrow at fixed or at floating rates in different markets.Example:

• company A is borrowing fixed at 5 12 %, but could borrow

floating at LIBOR plus 12 %;

• company B is borrowing floating at LIBOR plus 1%, butcould borrow fixed at 6 1

2 %.

By agreeing to swap streams of cash flows both companiescould be better off, and a mediating institution would alsomake money:

• company A pays LIBOR to the intermediary in exchangefor fixed at 5 3

16 % (receiver swap);

• company B pays the intermediary fixed at 5 516 % in

exchange for LIBOR (payer swap).

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

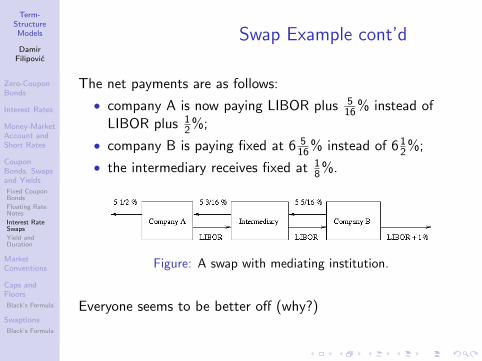

Swap Example cont’d

The net payments are as follows:

• company A is now paying LIBOR plus 516 % instead of

LIBOR plus 12 %;

• company B is paying fixed at 6 516 % instead of 6 1

2 %;

• the intermediary receives fixed at 18 %.

Figure: A swap with mediating institution.

Everyone seems to be better off (why?)

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Interest Rate Swap Markets

• interest rate swap markets are over the counter

• but swap contracts exist in standardized form, e.g. by theISDA (International Swaps and Derivatives Association,Inc.).

• swap markets are extremely liquid

• maturities from 1 to 30 years are standard, swap ratequotes available up to 60 years

• gives market participants, such as life insurers, opportunityto create synthetically long-dated investments

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Outline

1 Zero-Coupon Bonds

2 Interest Rates

3 Money-Market Account and Short Rates

4 Coupon Bonds, Swaps and YieldsFixed Coupon BondsFloating Rate NotesInterest Rate SwapsYield and Duration

5 Market Conventions

6 Caps and FloorsBlack’s Formula

7 SwaptionsBlack’s Formula

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Zero-Coupon Yield

• zero-coupon yield is the continuously compounded spotrate R(t,T ):

P(t,T ) = e−R(t,T )(T−t).

• T 7→ R(t,T ) is called (zero-coupon) yield curve

Figure: Yield curve T 7→ R(t,T ).

• note: term “yield curve” is ambiguous

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Yield-to-Maturity

• consider fixed coupon bond (short hand: cn contains N)

p =n∑

i=1

P(0,Ti )ci

• bond’s “internal rate of interest”: (continuouslycompounded) yield-to-maturity y : unique solution to

p =n∑

i=1

cie−yTi .

• Schaefer [47]: yield-to-maturity is inadequate statistic forbond market:

• coupon payments occurring at the same point in time arediscounted by different discount factors, but

• coupon payments at different points in time from the samebond are discounted by the same rate.

In reality, one would wish to do exactly the opposite !

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Macaulay duration

• bond price change as function of y : Macaulay duration:

DMac =

∑ni=1 Ticie−yTi

p

= weighted average of the coupon dates T1, . . . ,Tn (“meantime to coupon payment”)

= first-order sensitivity of bond price w.r.t. changes in theyield-to-maturity:

dp

dy=

d

dy

(n∑

i=1

cie−yTi

)= −DMacp

(interest rate risk management!)

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Duration

• write yi = R(0,Ti )

• duration of the bond

D =

∑ni=1 Ticie−yiTi

p=

n∑i=1

ciP(0,Ti )

pTi

= first-order sensitivity of bond price w.r.t. parallel shifts ofyield curve:

d

ds

(n∑

i=1

cie−(yi +s)Ti

)|s=0 = −Dp.

→ duration is essentially for bonds (w.r.t. parallel shift of theyield curve) what delta is for stock options

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Convexity

• bond equivalent of gamma is convexity:

C =d2

ds2

(n∑

i=1

cie−(yi +s)Ti

)|s=0 =

n∑i=1

cie−yiTi (Ti )2

→ second-order approximation for bond price change ∆pw.r.t. parallel shift ∆y of yield curve:

∆p ≈ −Dp∆y +1

2C (∆y)2

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Outline

1 Zero-Coupon Bonds

2 Interest Rates

3 Money-Market Account and Short Rates

4 Coupon Bonds, Swaps and YieldsFixed Coupon BondsFloating Rate NotesInterest Rate SwapsYield and Duration

5 Market Conventions

6 Caps and FloorsBlack’s Formula

7 SwaptionsBlack’s Formula

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Day-Count Conventions

• convention: measure time in units of years

• market evaluates year fraction between t < T in differentways

• examples of day-count conventions δ(t,T ):• actual/365: year has 365 days

δ(t,T ) =actual number of days between t and T

365.

• actual/360: as above but year counts 360 days• 30/360: months count 30 and years 360 days. Let

t = d1/m1/y1 and T = d2/m2/y2

δ(t,T ) =min(d2, 30) + (30− d1)+

360+

(m2 −m1 − 1)+

12+y2−y1.

Example: t = 4 January 2000 and T = 4 July 2002:

δ(t,T ) =4 + (30− 4)

360+

7− 1− 1

12+ 2002− 2000 = 2.5.

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

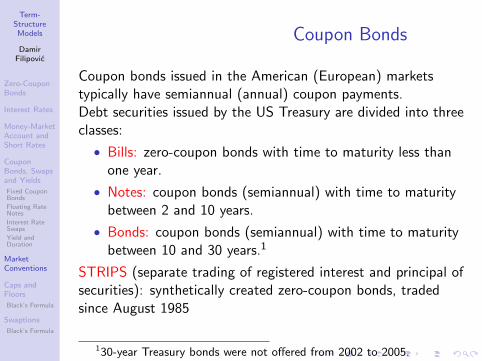

Coupon Bonds

Coupon bonds issued in the American (European) marketstypically have semiannual (annual) coupon payments.Debt securities issued by the US Treasury are divided into threeclasses:

• Bills: zero-coupon bonds with time to maturity less thanone year.

• Notes: coupon bonds (semiannual) with time to maturitybetween 2 and 10 years.

• Bonds: coupon bonds (semiannual) with time to maturitybetween 10 and 30 years.1

STRIPS (separate trading of registered interest and principal ofsecurities): synthetically created zero-coupon bonds, tradedsince August 1985

130-year Treasury bonds were not offered from 2002 to 2005.

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Accrued Interest, Clean Price andDirty Price

• recall coupon bond price formula

p(t) =∑Ti≥t

ciP(t,Ti )

→ systematic discontinuities of price trajectory at t = Ti

• accrued interest at t ∈ (Ti−1,Ti ] is defined by

AI (i ; t) = cit − Ti−1

Ti − Ti−1

• clean price (quoted) of coupon bond at t ∈ (Ti−1,Ti ] is

pclean(t) = p(t)− AI (i ; t)

→ dirty price (to pay) is

p(t) = pclean(t) + AI (i ; t)

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Yield-to-Maturity

see course book Section 2.5.4

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Outline

1 Zero-Coupon Bonds

2 Interest Rates

3 Money-Market Account and Short Rates

4 Coupon Bonds, Swaps and YieldsFixed Coupon BondsFloating Rate NotesInterest Rate SwapsYield and Duration

5 Market Conventions

6 Caps and FloorsBlack’s Formula

7 SwaptionsBlack’s Formula

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Caplets

• caplet with reset date T and settlement date T + δ: paysthe holder difference between simple market rateF (T ,T + δ) (e.g. LIBOR) and strike rate κ

• cash flow at time T + δ:

δ(F (T ,T + δ)− κ)+

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Caps

• cap: strip of caplets, specified by• reset/settlement dates T0 < T1 < · · · < Tn (T0=first reset

date, Tn=maturity)• a cap rate κ• for notational simplicity assume: Ti − Ti−1 ≡ δ

• cap price at t ≤ T0 is

Cp(t) =n∑

i=1

Cpl(t; Ti−1,Ti )

where Cpl(t; Ti−1,Ti ) is price of ith caplet

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

CapsAt Ti , the holder of the cap receives

δ(F (Ti−1,Ti )− κ)+,

which is equivalent (. . . ) to cash flow

(1 + δκ)

(1

1 + δκ− P(Ti−1,Ti )

)+

at Ti−1 (= (1 + δκ) times put option on Ti -bond with strikeprice 1/(1 + δκ) and maturity Ti−1)

→ protects against rising interest rates

Figure: cash flow of cap

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Floors

• floor: converse to a cap, protects against low rates

• strip of floorlets with cash flow at time Ti :

δ(κ− F (Ti−1,Ti ))+

• ith floorlet price: Fll(t; Ti−1,Ti )

• floor price at t ≤ T0 is

Fl(t) =n∑

i=1

Fll(t; Ti−1,Ti )

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

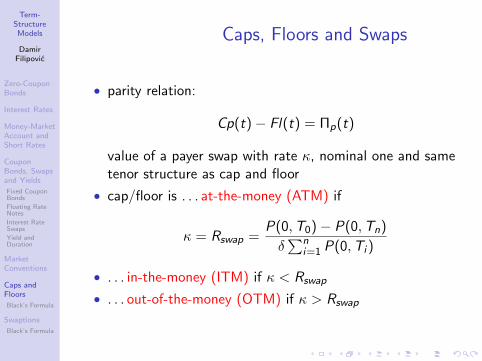

Caps, Floors and Swaps

• parity relation:

Cp(t)− Fl(t) = Πp(t)

value of a payer swap with rate κ, nominal one and sametenor structure as cap and floor

• cap/floor is . . . at-the-money (ATM) if

κ = Rswap =P(0,T0)− P(0,Tn)

δ∑n

i=1 P(0,Ti )

• . . . in-the-money (ITM) if κ < Rswap

• . . . out-of-the-money (OTM) if κ > Rswap

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Outline

1 Zero-Coupon Bonds

2 Interest Rates

3 Money-Market Account and Short Rates

4 Coupon Bonds, Swaps and YieldsFixed Coupon BondsFloating Rate NotesInterest Rate SwapsYield and Duration

5 Market Conventions

6 Caps and FloorsBlack’s Formula

7 SwaptionsBlack’s Formula

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Black’s Formula

Black’s formula for ith caplet value is

Cpl(t; Ti−1,Ti ) = δP(t,Ti )

× (F (t; Ti−1,Ti )Φ(d1)− κΦ(d2))

where

d1,2 =log(

F (t;Ti−1,Ti )κ

)± 1

2σ(t)2(Ti−1 − t)

σ(t)√

Ti−1 − t,

• Φ: standard Gaussian cumulative distribution function

• σ(t): cap (implied) volatility (same for all capletsbelonging to a cap)

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Black’s Formula cont’d

Black’s formula assumes F (Ti−1,Ti ) = X (Ti−1) where

dX = σX dW , X (t) = F (t; Ti−1,Ti )

and

Cpl(t; Ti−1,Ti ) = δP(t,Ti )E[(X (Ti−1)− κ)+ | Ft

](to be justified later: in Market Models)

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Black’s Formula cont’d

Black’s formula for ith floorlet is

Fll(t; Ti−1,Ti ) = δP(t,Ti ) (κΦ(−d2)− F (t; Ti−1,Ti )Φ(−d1))

• cap/floor prices are quoted in the market in terms of theirimplied volatilities

• typically: t = 0, T0 = δ = Ti − Ti−1 = three months (USmarket) or half a year (euro market)

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Example of Cap Quotes

Table: US dollar ATM cap volatilities, 23 July 1999

Maturity (in years) ATM vols (in %)

1 14.12 17.43 18.54 18.85 18.96 18.77 18.48 18.2

10 17.712 17.015 16.520 14.730 12.4

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Example of Cap Quotes

Figure: US dollar ATM cap volatilities, 23 July 1999.

It is a challenge for any market realistic interest rate model tomatch the given volatility curve.

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Outline

1 Zero-Coupon Bonds

2 Interest Rates

3 Money-Market Account and Short Rates

4 Coupon Bonds, Swaps and YieldsFixed Coupon BondsFloating Rate NotesInterest Rate SwapsYield and Duration

5 Market Conventions

6 Caps and FloorsBlack’s Formula

7 SwaptionsBlack’s Formula

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Swaptions

• payer (receiver) swaption with strike rate K : right to entera payer (receiver) swap with fixed rate K at swaptionmaturity

• usually, swaption maturity = first reset date T0 ofunderlying swap

• tenor of the swaption: underlying swap length Tn − T0

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Swaption Payoff

• swaption payoff at maturity

N

(n∑

i=1

P(T0,Ti )δ(F (T0; Ti−1,Ti )− K )

)+

= Nδ(Rswap(T0)− K )+n∑

i=1

P(T0,Ti )

cannot be decomposed into more elementary payoffs!

→ dependence between different forward rates will entervaluation procedure

• payer (receiver) swaption is ATM, ITM, OTM if

K = Rswap(t), K < (>)Rswap(t), K > (<)Rswap(t)

• x × y -swaption: maturity in x years, underlying swap yyears long

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

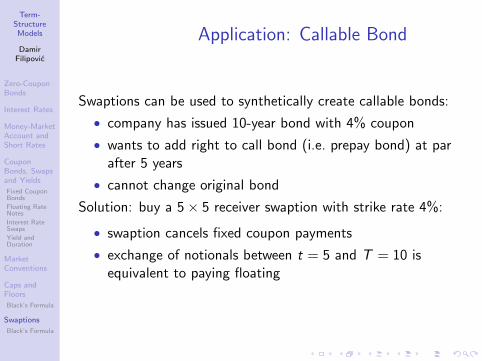

Application: Callable Bond

Swaptions can be used to synthetically create callable bonds:

• company has issued 10-year bond with 4% coupon

• wants to add right to call bond (i.e. prepay bond) at parafter 5 years

• cannot change original bond

Solution: buy a 5× 5 receiver swaption with strike rate 4%:

• swaption cancels fixed coupon payments

• exchange of notionals between t = 5 and T = 10 isequivalent to paying floating

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Outline

1 Zero-Coupon Bonds

2 Interest Rates

3 Money-Market Account and Short Rates

4 Coupon Bonds, Swaps and YieldsFixed Coupon BondsFloating Rate NotesInterest Rate SwapsYield and Duration

5 Market Conventions

6 Caps and FloorsBlack’s Formula

7 SwaptionsBlack’s Formula

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Black’s Formula

Black’s price formula for payer and receiver swaption is

Swptp(t) = Nδ (Rswap(t)Φ(d1)− K Φ(d2))n∑

i=1

P(t,Ti ),

Swptr (t) = Nδ (K Φ(−d2)− Rswap(t)Φ(−d1))n∑

i=1

P(t,Ti ),

with

d1,2 =log(

Rswap(t)K

)± 1

2σ(t)2(T0 − t)

σ(t)√

T0 − t,

• Φ: standard Gaussian cumulative distribution function

• σ(t): swaption implied volatility

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Swaption Quotes

• swaption prices are quoted in terms of implied volatilitiesin matrix form

• note: accrual period δ = Ti − Ti−1 for underlying swapcan differ from prevailing δ for caps within the samemarket region!

• e.g. euro zone: caps are written on semiannual LIBOR(δ = 1/2), while swaps pay annual coupons (δ = 1)

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Example of Swaption Quotes

Table: Black’s implied volatilities (in %) of ATM swaptions on May16, 2000. Maturities are 1,2,3,4,5,7,10 years, swaps lengths from 1 to10 years

1y 2y 3y 4y 5y 6y 7y 8y 9y 10y1y 16.4 15.8 14.6 13.8 13.3 12.9 12.6 12.3 12.0 11.72y 17.7 15.6 14.1 13.1 12.7 12.4 12.2 11.9 11.7 11.43y 17.6 15.5 13.9 12.7 12.3 12.1 11.9 11.7 11.5 11.34y 16.9 14.6 12.9 11.9 11.6 11.4 11.3 11.1 11.0 10.85y 15.8 13.9 12.4 11.5 11.1 10.9 10.8 10.7 10.5 10.47y 14.5 12.9 11.6 10.8 10.4 10.3 10.1 9.9 9.8 9.6

10y 13.5 11.5 10.4 9.8 9.4 9.3 9.1 8.8 8.6 8.4

Term-StructureModels

DamirFilipovic

Zero-CouponBonds

Interest Rates

Money-MarketAccount andShort Rates

CouponBonds, Swapsand Yields

Fixed CouponBonds

Floating RateNotes

Interest RateSwaps

Yield andDuration

MarketConventions

Caps andFloors

Black’s Formula

Swaptions

Black’s Formula

Example of Swaption Quotes

Figure: Black’s implied volatilities (in %) of ATM swaptions on May16, 2000.

An interest rate model for swaptions valuation must fit today’svolatility surface.

Term-StructureModels

DamirFilipovic

ABootstrappingExample

Non-parametricEstimationMethods

Bond Markets

Money Markets

Problems

ParametricEstimationMethods

Estimating theDiscountFunction withCubic B-splines

SmoothingSplines

Exponential–PolynomialFamilies

PrincipalComponentAnalysis

PrincipalComponents of aRandom Vector

Sample PrincipleComponents

PCA of theForward Curve

Correlation

Part II

Estimating the Term-Structure

Term-StructureModels

DamirFilipovic

ABootstrappingExample

Non-parametricEstimationMethods

Bond Markets

Money Markets

Problems

ParametricEstimationMethods

Estimating theDiscountFunction withCubic B-splines

SmoothingSplines

Exponential–PolynomialFamilies

PrincipalComponentAnalysis

PrincipalComponents of aRandom Vector

Sample PrincipleComponents

PCA of theForward Curve

Correlation

Overview

• in theory: assume given initial term-structure for all T

• reality: finitely many (possibly noisy) market quoteobservations

• pricing exotic derivatives: cash flow dates possibly do notmatch the predetermined finite time grid

→ interpolate the term-structure

• simples method: build up term structure from shortermaturities to longer maturities (“bootstrapping”)

Term-StructureModels

DamirFilipovic

ABootstrappingExample

Non-parametricEstimationMethods

Bond Markets

Money Markets

Problems

ParametricEstimationMethods

Estimating theDiscountFunction withCubic B-splines

SmoothingSplines

Exponential–PolynomialFamilies

PrincipalComponentAnalysis

PrincipalComponents of aRandom Vector

Sample PrincipleComponents

PCA of theForward Curve

Correlation

Outline

8 A Bootstrapping Example

9 Non-parametric Estimation MethodsBond MarketsMoney MarketsProblems

10 Parametric Estimation MethodsEstimating the Discount Function with Cubic B-splinesSmoothing SplinesExponential–Polynomial Families

11 Principal Component AnalysisPrincipal Components of a Random VectorSample Principle ComponentsPCA of the Forward CurveCorrelation

Term-StructureModels

DamirFilipovic

ABootstrappingExample

Non-parametricEstimationMethods

Bond Markets

Money Markets

Problems

ParametricEstimationMethods

Estimating theDiscountFunction withCubic B-splines

SmoothingSplines

Exponential–PolynomialFamilies

PrincipalComponentAnalysis

PrincipalComponents of aRandom Vector

Sample PrincipleComponents

PCA of theForward Curve

Correlation

Outline

8 A Bootstrapping Example

9 Non-parametric Estimation MethodsBond MarketsMoney MarketsProblems

10 Parametric Estimation MethodsEstimating the Discount Function with Cubic B-splinesSmoothing SplinesExponential–Polynomial Families

11 Principal Component AnalysisPrincipal Components of a Random VectorSample Principle ComponentsPCA of the Forward CurveCorrelation

Term-StructureModels

DamirFilipovic

ABootstrappingExample

Non-parametricEstimationMethods

Bond Markets

Money Markets

Problems

ParametricEstimationMethods

Estimating theDiscountFunction withCubic B-splines

SmoothingSplines

Exponential–PolynomialFamilies

PrincipalComponentAnalysis

PrincipalComponents of aRandom Vector

Sample PrincipleComponents

PCA of theForward Curve

Correlation

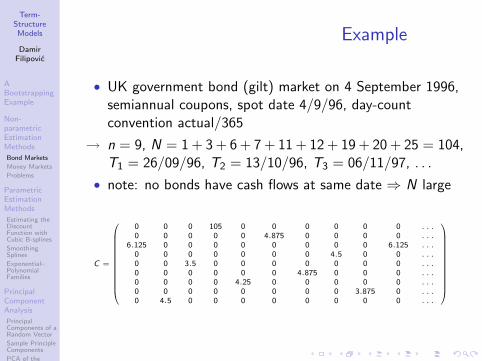

Bootstrapping Example

Table: Yen data, 9 January 1996

LIBOR (%) Futures Swaps (%)

o/n 0.49 20 Mar 96 99.34 2y 1.141w 0.50 19 Jun 96 99.25 3y 1.601m 0.53 18 Sep 96 99.10 4y 2.042m 0.55 18 Dec 96 98.90 5y 2.433m 0.56 7y 3.01

10y 3.36

• spot date t0: 11 January, 1996

• day-count convention: actual/360 (note: 1996 was leapyear):

δ(T ,S) =actual number of days between T and S

360

Term-StructureModels

DamirFilipovic

ABootstrappingExample

Non-parametricEstimationMethods

Bond Markets

Money Markets

Problems

ParametricEstimationMethods

Estimating theDiscountFunction withCubic B-splines

SmoothingSplines

Exponential–PolynomialFamilies

PrincipalComponentAnalysis

PrincipalComponents of aRandom Vector

Sample PrincipleComponents

PCA of theForward Curve

Correlation

Maturity Overlap

0 2 4 6 8 10 12

Time to maturity

Figure: Overlapping maturity segments (from bottom up) of LIBOR,futures and swap markets.

Term-StructureModels

DamirFilipovic

ABootstrappingExample

Non-parametricEstimationMethods

Bond Markets

Money Markets

Problems

ParametricEstimationMethods

Estimating theDiscountFunction withCubic B-splines

SmoothingSplines

Exponential–PolynomialFamilies

PrincipalComponentAnalysis

PrincipalComponents of aRandom Vector

Sample PrincipleComponents

PCA of theForward Curve

Correlation

First Column: LIBOR

• maturities S1, . . . ,S5 = 12/1/96, 18/1/96, 13/2/96,11/3/96, 11/4/96

• zero-coupon bonds are

P(t0, Si ) =1

1 + δ(t0,Si )F (t0,Si ).

Term-StructureModels

DamirFilipovic

ABootstrappingExample

Non-parametricEstimationMethods

Bond Markets

Money Markets

Problems

ParametricEstimationMethods

Estimating theDiscountFunction withCubic B-splines

SmoothingSplines

Exponential–PolynomialFamilies

PrincipalComponentAnalysis

PrincipalComponents of aRandom Vector

Sample PrincipleComponents

PCA of theForward Curve

Correlation

Second Column: Futures

• quoted as: futures price for settlement day Ti =100(1− FF (t0; Ti ,Ti+1))

• FF (t0; Ti ,Ti+1): futures rate for period [Ti ,Ti+1]prevailing at t0

• reset/settlement dates

T1, . . . ,T5 = 20/3/96, . . . 19/3/97

hence δ(Ti ,Ti+1) ≡ 91/360

• proxy: F (t0; Ti ,Ti+1) = FF (t0; Ti ,Ti+1) (see later)

Term-StructureModels

DamirFilipovic

ABootstrappingExample

Non-parametricEstimationMethods

Bond Markets

Money Markets

Problems

ParametricEstimationMethods

Estimating theDiscountFunction withCubic B-splines

SmoothingSplines

Exponential–PolynomialFamilies

PrincipalComponentAnalysis

PrincipalComponents of aRandom Vector

Sample PrincipleComponents

PCA of theForward Curve

Correlation

Second Column: Futures

• for P(t0,T1): use geometric interpolation (S4 < T1 < S5)

P(t0,T1) = P(t0, S4)q P(t0, S5)1−q

which is equivalent to linear interpolation of yields

R(t0,T1) = q R(t0,S4) + (1− q) R(t0, S5)

where

q =δ(T1, S5)

δ(S4,S5)=

22

31= 0.709677

• to derive P(t0,T2), . . . ,P(t0,T5) use:

P(t0,Ti+1) =P(t0,Ti )

1 + δ(Ti ,Ti+1) F (t0; Ti ,Ti+1)

Term-StructureModels

DamirFilipovic

ABootstrappingExample

Non-parametricEstimationMethods

Bond Markets

Money Markets

Problems

ParametricEstimationMethods

Estimating theDiscountFunction withCubic B-splines

SmoothingSplines

Exponential–PolynomialFamilies

PrincipalComponentAnalysis

PrincipalComponents of aRandom Vector

Sample PrincipleComponents

PCA of theForward Curve

Correlation

Third Column: Swaps

• semiannual cash flows at dates

U1, . . . ,U20 =

11/7/96, 13/1/97,11/7/97, 12/1/98,13/7/98, 11/1/99,12/7/99, 11/1/00,11/7/00, 11/1/01,11/7/01, 11/1/02,11/7/02, 13/1/03,11/7/03, 12/1/04,12/7/04, 11/1, 05,11/7/05, 11/1/06

• from data: Rswap(t0,Ui ) for i = 4, 6, 8, 10, 14, 20

Term-StructureModels

DamirFilipovic

ABootstrappingExample

Non-parametricEstimationMethods

Bond Markets

Money Markets

Problems

ParametricEstimationMethods

Estimating theDiscountFunction withCubic B-splines

SmoothingSplines

Exponential–PolynomialFamilies

PrincipalComponentAnalysis

PrincipalComponents of aRandom Vector

Sample PrincipleComponents

PCA of theForward Curve

Correlation

Third Column: Swaps

• recall

Rswap(t0,Un) =1− P(t0,Un)∑n

i=1 δ(Ui−1,Ui ) P(t0,Ui )(set U0 = t0)

• overlap: T2 < U1 < T3 and T4 < U2 < T5

• linear interpolation of yields → R(t0,U1), R(t0,U2)

→ P(t0,U1), P(t0,U2) and hence Rswap(t0,U1), Rswap(t0,U2)

• remaining swap rates by linear interpolation, e.g.

Rswap(t0,U3) =1

2(Rswap(t0,U2) + Rswap(t0,U4))

• inversion of above formula:

P(t0,Un) =1− Rswap(t0,Un)

∑n−1i=1 δ(Ui−1,Ui ) P(t0,Ui )

1 + Rswap(t0,Un)δ(Un−1,Un)

gives P(t0,Un) for n = 3, . . . , 20

Term-StructureModels

DamirFilipovic

ABootstrappingExample

Non-parametricEstimationMethods

Bond Markets

Money Markets

Problems

ParametricEstimationMethods

Estimating theDiscountFunction withCubic B-splines

SmoothingSplines

Exponential–PolynomialFamilies

PrincipalComponentAnalysis

PrincipalComponents of aRandom Vector

Sample PrincipleComponents

PCA of theForward Curve

Correlation

Obtain Term Structure

• set P(t0, t0) = 1

→ have constructed term structure P(t0, ti ) for 30 points:

ti = t0, S1, . . . ,S4,T1, S5,T2,U1,T3,T4,U2,T5,U3, . . . ,U20

0

0,2

0,4

0,6

0,8

1

1,2

0 2 4 6 8 10 12

Time to maturity

Figure: Zero-coupon bond curve.

Term-StructureModels

DamirFilipovic

ABootstrappingExample

Non-parametricEstimationMethods

Bond Markets

Money Markets

Problems

ParametricEstimationMethods

Estimating theDiscountFunction withCubic B-splines

SmoothingSplines

Exponential–PolynomialFamilies

PrincipalComponentAnalysis

PrincipalComponents of aRandom Vector

Sample PrincipleComponents

PCA of theForward Curve

Correlation

Yield and Forward Rate Curves

• continuously compounded yield and forward rates:R(t0, ti ) and R(t0, ti , ti+1)

• “sawtooth”: linear interpolation of swap ratesinappropriate for implied forward rates

0

0,01

0,02

0,03

0,04

0,05

0,06

0 2 4 6 8 10 12

Time to maturity

Figure: yields (lower curve), forward rates (upper curve)

Term-StructureModels

DamirFilipovic

ABootstrappingExample

Non-parametricEstimationMethods

Bond Markets

Money Markets

Problems

ParametricEstimationMethods

Estimating theDiscountFunction withCubic B-splines

SmoothingSplines

Exponential–PolynomialFamilies

PrincipalComponentAnalysis

PrincipalComponents of aRandom Vector

Sample PrincipleComponents

PCA of theForward Curve

Correlation

Larger Time Scale

0

0,001

0,002

0,003

0,004

0,005

0,006

0,007

0,008

0 0,1 0,2 0,3 0,4 0,5 0,6

Time to maturity

Figure: yields (lower curve), forward rates (upper curve)

• “sawtooth”: systematic inconsistency of our use of LIBORand futures rates data (we have treated futures rates asforward rates)

Term-StructureModels

DamirFilipovic

ABootstrappingExample

Non-parametricEstimationMethods

Bond Markets

Money Markets

Problems

ParametricEstimationMethods

Estimating theDiscountFunction withCubic B-splines

SmoothingSplines

Exponential–PolynomialFamilies

PrincipalComponentAnalysis

PrincipalComponents of aRandom Vector

Sample PrincipleComponents

PCA of theForward Curve

Correlation

Futures vs. Forward Rates

• “sawtooth”: systematic inconsistency of our use of LIBORand futures rates data (we have treated futures rates asforward rates)

• in reality: futures rates often greater than forward rates

• difference is called convexity adjustment (modeldependent)

• example: forward rate = futures rate −12σ

2τ2 where• τ = time to maturity of futures contract• σ = volatility parameter

(later: we will derive a more general formula)

Term-StructureModels

DamirFilipovic

ABootstrappingExample

Non-parametricEstimationMethods

Bond Markets

Money Markets

Problems

ParametricEstimationMethods

Estimating theDiscountFunction withCubic B-splines

SmoothingSplines

Exponential–PolynomialFamilies

PrincipalComponentAnalysis

PrincipalComponents of aRandom Vector

Sample PrincipleComponents

PCA of theForward Curve

Correlation

Summary

• we constructed entire term-structure from relatively fewinstruments

• method exactly reconstructs market prices (desirable forinterest rate option traders: marking to market), but . . .

• . . . forward curve (derivative −∂T log P(t0,T )!) irregular,sensitive to bond price variations/errors

• three curves resulting from LIBOR, futures and swaps: notcoincident to common underlying curve

• bootstrapping: example of non-parametric estimationmethod

Term-StructureModels

DamirFilipovic

ABootstrappingExample

Non-parametricEstimationMethods

Bond Markets

Money Markets

Problems

ParametricEstimationMethods

Estimating theDiscountFunction withCubic B-splines

SmoothingSplines

Exponential–PolynomialFamilies

PrincipalComponentAnalysis

PrincipalComponents of aRandom Vector

Sample PrincipleComponents

PCA of theForward Curve

Correlation

Outline

8 A Bootstrapping Example

9 Non-parametric Estimation MethodsBond MarketsMoney MarketsProblems

10 Parametric Estimation MethodsEstimating the Discount Function with Cubic B-splinesSmoothing SplinesExponential–Polynomial Families

11 Principal Component AnalysisPrincipal Components of a Random VectorSample Principle ComponentsPCA of the Forward CurveCorrelation

Term-StructureModels

DamirFilipovic

ABootstrappingExample

Non-parametricEstimationMethods

Bond Markets

Money Markets

Problems

ParametricEstimationMethods

Estimating theDiscountFunction withCubic B-splines

SmoothingSplines

Exponential–PolynomialFamilies

PrincipalComponentAnalysis

PrincipalComponents of aRandom Vector

Sample PrincipleComponents

PCA of theForward Curve

Correlation

Non-parametric EstimationMethods: General Problem

• finding today’s (t0) discount curve (term-structure)x 7→ D(x) = P(t0, t0 + x)

• can be formulated as p = C d + ε where• p = column vector of n market prices• C = related cash flow matrix• d = (D(x1), . . . ,D(xN))>

• cash flow dates t0 < T1 < · · · < TN , Ti − t0 = xi

• ε = vector of pricing errors, subject to being minimized

• including errors reasonable: prices never exactsimultaneously quoted, bid ask spreads, allows forsmoothing

• next: bring data from bond and money markets into aboveformat

Term-StructureModels

DamirFilipovic

ABootstrappingExample

Non-parametricEstimationMethods

Bond Markets

Money Markets

Problems

ParametricEstimationMethods

Estimating theDiscountFunction withCubic B-splines

SmoothingSplines

Exponential–PolynomialFamilies

PrincipalComponentAnalysis

PrincipalComponents of aRandom Vector

Sample PrincipleComponents

PCA of theForward Curve

Correlation

Outline

8 A Bootstrapping Example

9 Non-parametric Estimation MethodsBond MarketsMoney MarketsProblems

10 Parametric Estimation MethodsEstimating the Discount Function with Cubic B-splinesSmoothing SplinesExponential–Polynomial Families

11 Principal Component AnalysisPrincipal Components of a Random VectorSample Principle ComponentsPCA of the Forward CurveCorrelation

Term-StructureModels

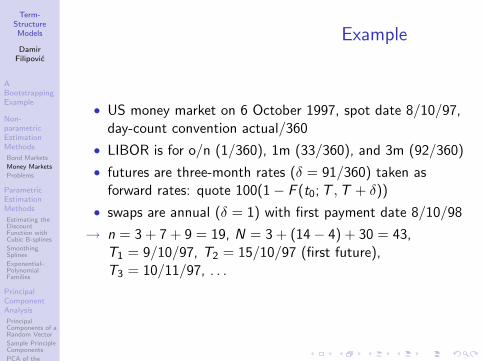

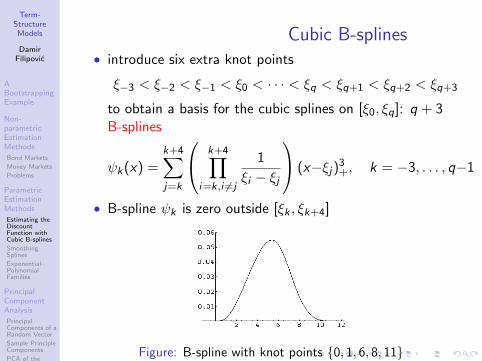

DamirFilipovic

ABootstrappingExample

Non-parametricEstimationMethods

Bond Markets

Money Markets

Problems