th latin america eu symposium on ict regulation sources: nsn and cisco vni mobile forecast, 2013...

TRANSCRIPT

4th Latin America – EU Symposium on ICT Regulation

Marcelo Mejias November 19th, 2013

1

2

Agenda

Brazilian telecommunications: a case of success Big sport events, big data, big challenges

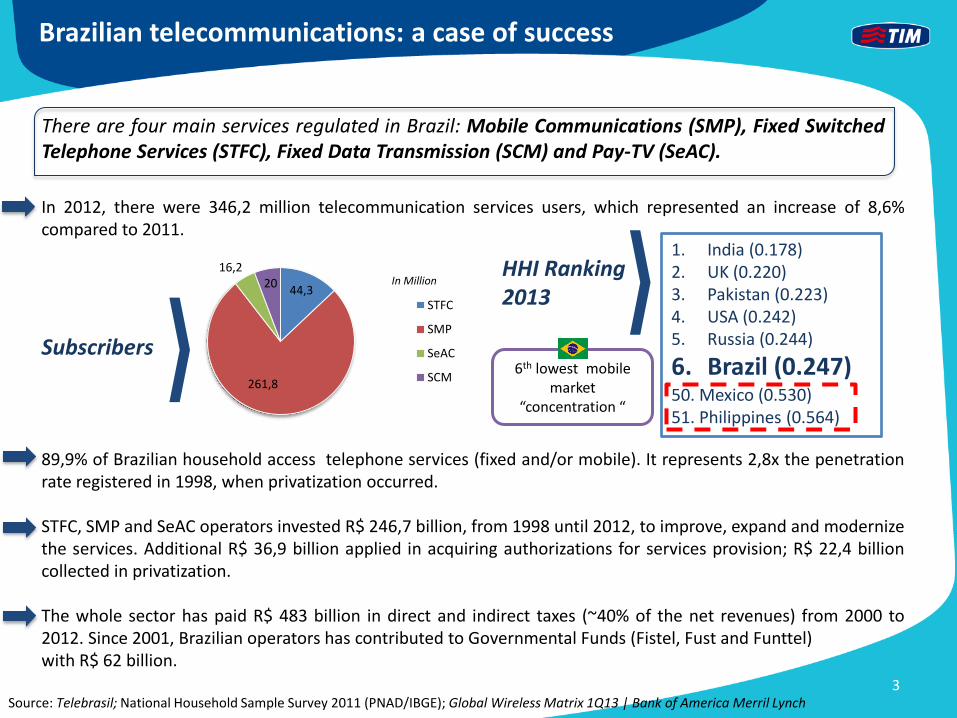

In 2012, there were 346,2 million telecommunication services users, which represented an increase of 8,6% compared to 2011.

89,9% of Brazilian household access telephone services (fixed and/or mobile). It represents 2,8x the penetration rate registered in 1998, when privatization occurred. STFC, SMP and SeAC operators invested R$ 246,7 billion, from 1998 until 2012, to improve, expand and modernize the services. Additional R$ 36,9 billion applied in acquiring authorizations for services provision; R$ 22,4 billion collected in privatization. The whole sector has paid R$ 483 billion in direct and indirect taxes (~40% of the net revenues) from 2000 to 2012. Since 2001, Brazilian operators has contributed to Governmental Funds (Fistel, Fust and Funttel) with R$ 62 billion.

There are four main services regulated in Brazil: Mobile Communications (SMP), Fixed Switched Telephone Services (STFC), Fixed Data Transmission (SCM) and Pay-TV (SeAC).

44,3

261,8

16,2 20

STFC

SMP

SeAC

SCM

In Million

Source: Telebrasil; National Household Sample Survey 2011 (PNAD/IBGE); Global Wireless Matrix 1Q13 | Bank of America Merril Lynch

Brazilian telecommunications: a case of success

3

1. India (0.178) 2. UK (0.220) 3. Pakistan (0.223) 4. USA (0.242) 5. Russia (0.244)

6. Brazil (0.247)

50. Mexico (0.530) 51. Philippines (0.564)

HHI Ranking 2013

Subscribers 6th lowest mobile

market “concentration “

... Waves of

Technologies

Evolution of the role of the State

State as Legislator State as Regulator State as Promoter

Creation Coexistence

Competition Expansion

Incentives Development

“Generations” of the relations between competitors RAN

Sharing

Interconnection RGQs

Spectrum Sharing

[?] EILD

Unbundling

Co-siting

Co-billing

Roaming

1997 2013

PGMC

Telebrás

Internet Bill of Law

[?]

Number Portability

Technologies, competitors’ relations and the role of the State

4

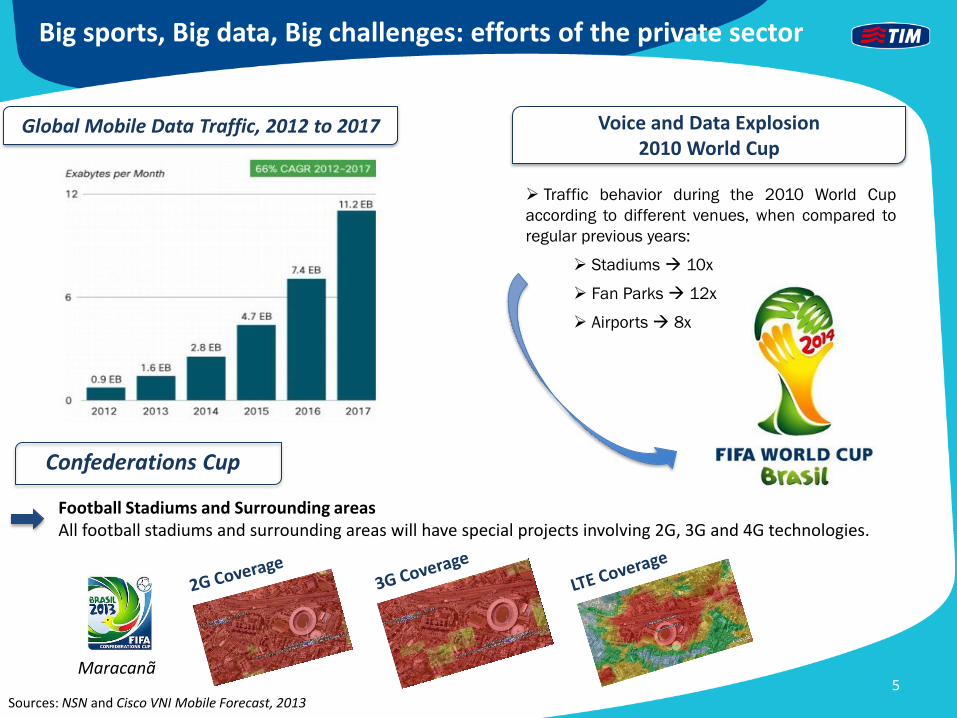

Global Mobile Data Traffic, 2012 to 2017

Sources: NSN and Cisco VNI Mobile Forecast, 2013

Voice and Data Explosion

2010 World Cup

Football Stadiums and Surrounding areas All football stadiums and surrounding areas will have special projects involving 2G, 3G and 4G technologies.

Confederations Cup

Maracanã

Traffic behavior during the 2010 World Cup

according to different venues, when compared to

regular previous years:

Stadiums 10x

Fan Parks 12x

Airports 8x

Big sports, Big data, Big challenges: efforts of the private sector

5

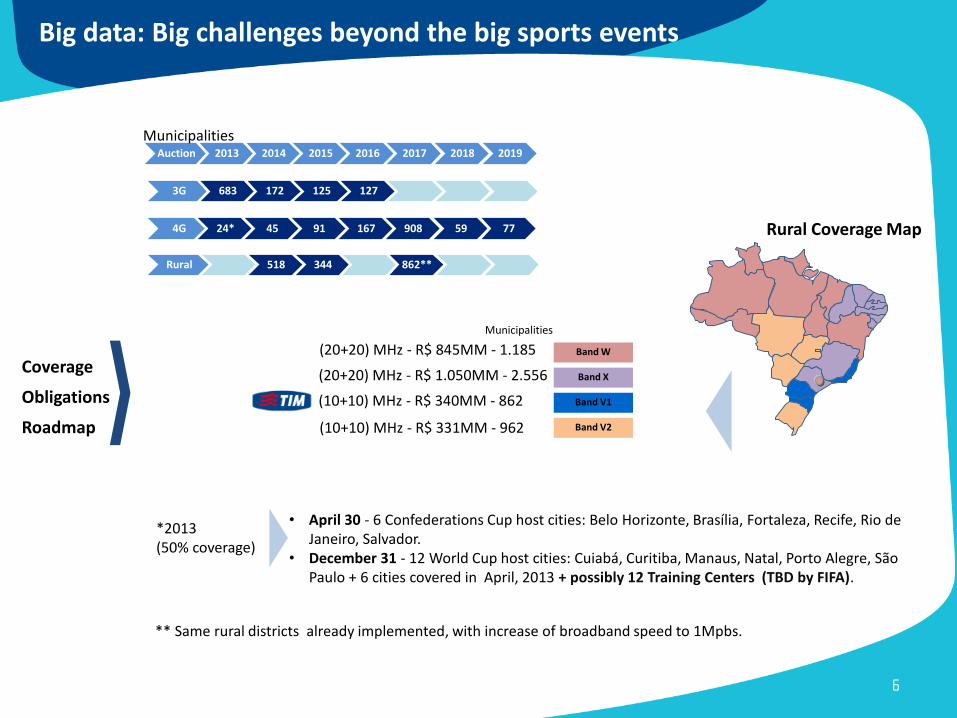

Coverage

Obligations

Roadmap

Auction 2013 2014 2015 2016 2017 2018 2019

3G 683 172 125 127

4G 24* 45 91 167 908 59 77

Rural 518 344 862**

• April 30 - 6 Confederations Cup host cities: Belo Horizonte, Brasília, Fortaleza, Recife, Rio de Janeiro, Salvador.

• December 31 - 12 World Cup host cities: Cuiabá, Curitiba, Manaus, Natal, Porto Alegre, São Paulo + 6 cities covered in April, 2013 + possibly 12 Training Centers (TBD by FIFA).

*2013 (50% coverage)

** Same rural districts already implemented, with increase of broadband speed to 1Mpbs.

Rural Coverage Map

Band W

Band X

Band V1

Band V2

(20+20) MHz - R$ 845MM - 1.185

(20+20) MHz - R$ 1.050MM - 2.556

(10+10) MHz - R$ 340MM - 862

(10+10) MHz - R$ 331MM - 962

Municipalities

Municipalities

Big data: Big challenges beyond the big sports events

6

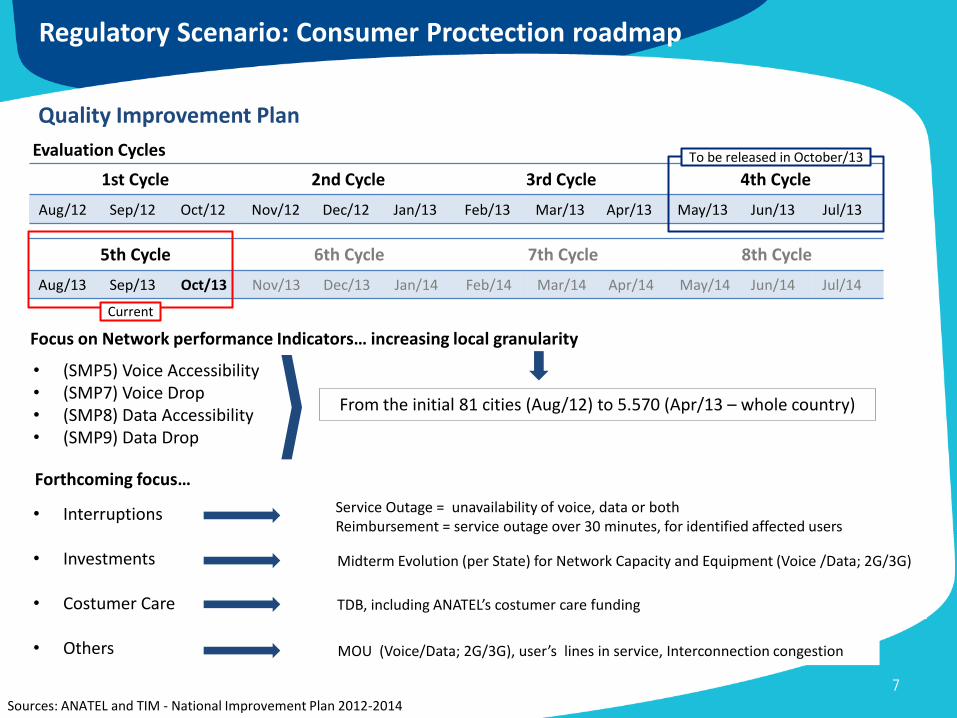

Sources: ANATEL and TIM - National Improvement Plan 2012-2014

Quality Improvement Plan

• (SMP5) Voice Accessibility • (SMP7) Voice Drop • (SMP8) Data Accessibility • (SMP9) Data Drop

• Interruptions

• Investments

• Costumer Care

• Others

Midterm Evolution (per State) for Network Capacity and Equipment (Voice /Data; 2G/3G)

Service Outage = unavailability of voice, data or both Reimbursement = service outage over 30 minutes, for identified affected users

MOU (Voice/Data; 2G/3G), user’s lines in service, Interconnection congestion

1st Cycle 2nd Cycle 3rd Cycle 4th Cycle

Aug/12 Sep/12 Oct/12 Nov/12 Dec/12 Jan/13 Feb/13 Mar/13 Apr/13 May/13 Jun/13 Jul/13

5th Cycle 6th Cycle 7th Cycle 8th Cycle

Aug/13 Sep/13 Oct/13 Nov/13 Dec/13 Jan/14 Feb/14 Mar/14 Apr/14 May/14 Jun/14 Jul/14

Evaluation Cycles

Focus on Network performance Indicators… increasing local granularity

Forthcoming focus…

From the initial 81 cities (Aug/12) to 5.570 (Apr/13 – whole country)

TDB, including ANATEL’s costumer care funding

Current

To be released in October/13

Regulatory Scenario: Consumer Proctection roadmap

7

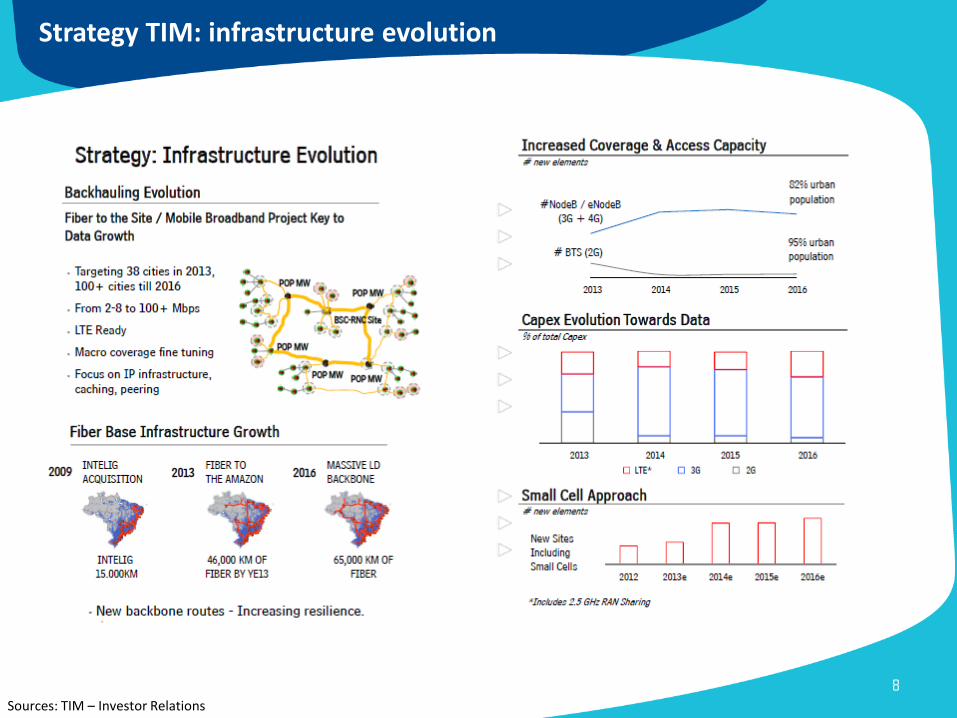

Sources: TIM – Investor Relations

Strategy TIM: infrastructure evolution

8

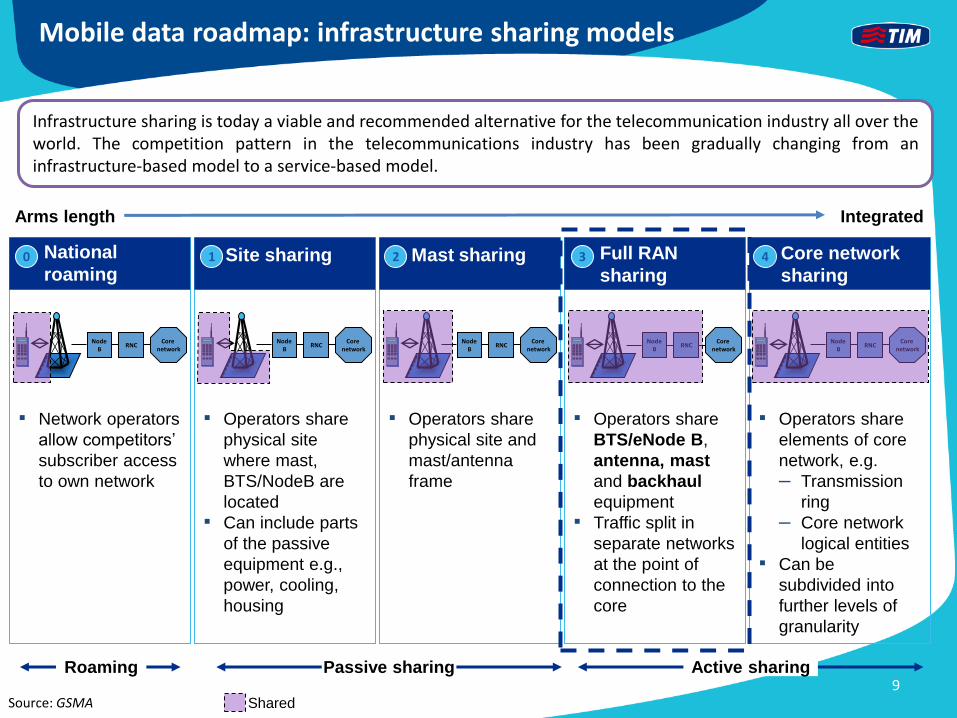

National

roaming 0 Site sharing 1 Mast sharing 2 Full RAN

sharing 3 Core network

sharing 4

▪ Network operators

allow competitors’

subscriber access

to own network

Node B

Core network

RNC

▪ Operators share

physical site

where mast,

BTS/NodeB are

located

▪ Can include parts

of the passive

equipment e.g.,

power, cooling,

housing

Node B

Core network

RNC

▪ Operators share

physical site and

mast/antenna

frame

▪ Operators share

BTS/eNode B,

antenna, mast

and backhaul

equipment

▪ Traffic split in

separate networks

at the point of

connection to the

core

Node B

Core network

RNC Node

B Core

network RNC

Node B

Core network

RNC

▪ Operators share

elements of core

network, e.g.

– Transmission

ring

– Core network

logical entities

▪ Can be

subdivided into

further levels of

granularity

Arms length Integrated

Passive sharing Active sharing Roaming

Source: GSMA Shared

Infrastructure sharing is today a viable and recommended alternative for the telecommunication industry all over the world. The competition pattern in the telecommunications industry has been gradually changing from an infrastructure-based model to a service-based model.

Mobile data roadmap: infrastructure sharing models

9

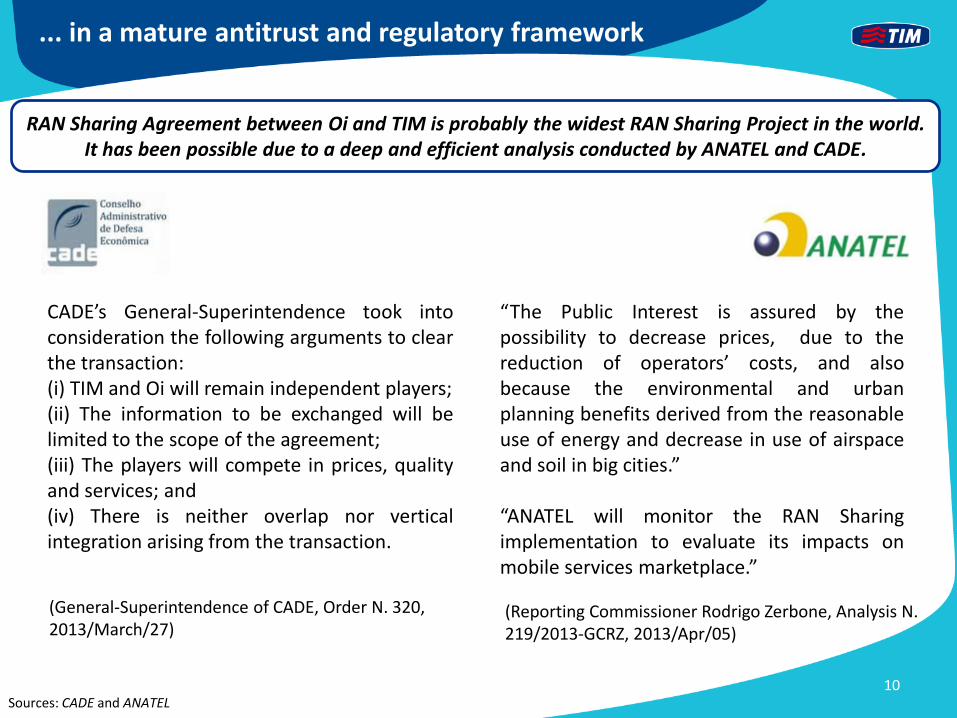

CADE’s General-Superintendence took into consideration the following arguments to clear the transaction: (i) TIM and Oi will remain independent players; (ii) The information to be exchanged will be limited to the scope of the agreement; (iii) The players will compete in prices, quality and services; and (iv) There is neither overlap nor vertical integration arising from the transaction.

“The Public Interest is assured by the possibility to decrease prices, due to the reduction of operators’ costs, and also because the environmental and urban planning benefits derived from the reasonable use of energy and decrease in use of airspace and soil in big cities.” “ANATEL will monitor the RAN Sharing implementation to evaluate its impacts on mobile services marketplace.”

RAN Sharing Agreement between Oi and TIM is probably the widest RAN Sharing Project in the world. It has been possible due to a deep and efficient analysis conducted by ANATEL and CADE.

... in a mature antitrust and regulatory framework

Sources: CADE and ANATEL 10

(General-Superintendence of CADE, Order N. 320, 2013/March/27)

(Reporting Commissioner Rodrigo Zerbone, Analysis N. 219/2013-GCRZ, 2013/Apr/05)

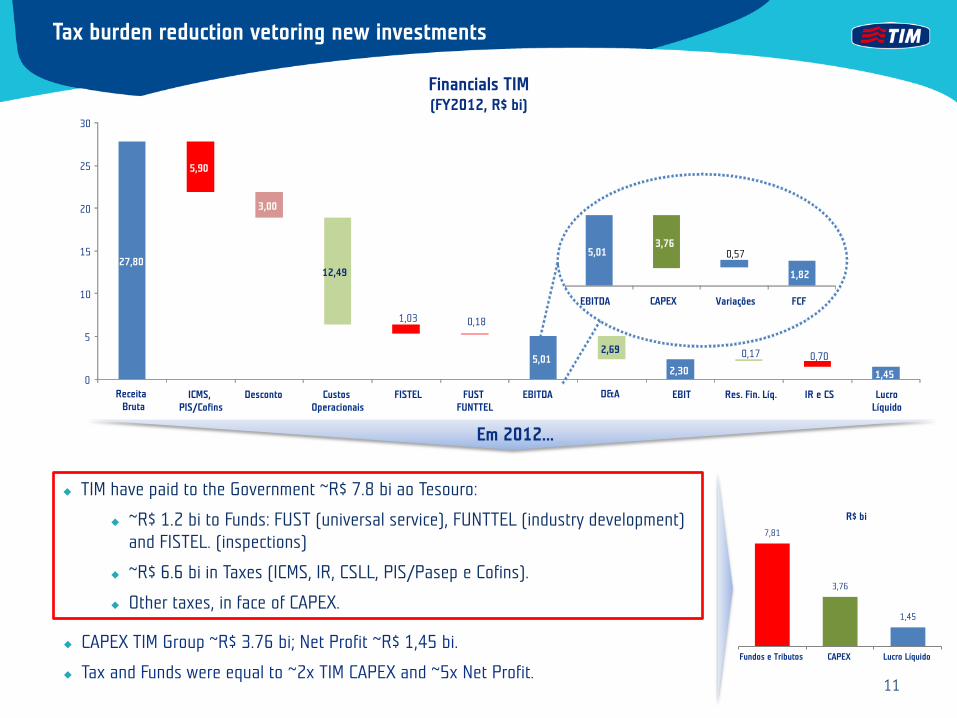

Tax burden reduction vetoring new investments

Financials TIM (FY2012, R$ bi)

TIM have paid to the Government ~R$ 7.8 bi ao Tesouro:

~R$ 1.2 bi to Funds: FUST (universal service), FUNTTEL (industry development) and FISTEL. (inspections)

~R$ 6.6 bi in Taxes (ICMS, IR, CSLL, PIS/Pasep e Cofins).

Other taxes, in face of CAPEX.

7,81

3,76

1,45

Fundos e Tributos CAPEX Lucro Líquido

R$ bi

CAPEX TIM Group ~R$ 3.76 bi; Net Profit ~R$ 1,45 bi.

Tax and Funds were equal to ~2x TIM CAPEX and ~5x Net Profit.

Em 2012...

5,90

3,00

12,49

1,03 0,18

2,69 0,17 0,70

0

5

10

15

20

25

30

Receita Bruta

ICMS, PIS/Cofins

Desconto Custos Operacionais

FISTEL FUST FUNTTEL

EBITDA D&A EBIT Res. Fin. Líq. IR e CS Lucro Líquido

3,76 0,57

EBITDA CAPEX Variações FCF

27,80

5,01 2,30 1,45

5,01

1,82

11

Thank you!

12