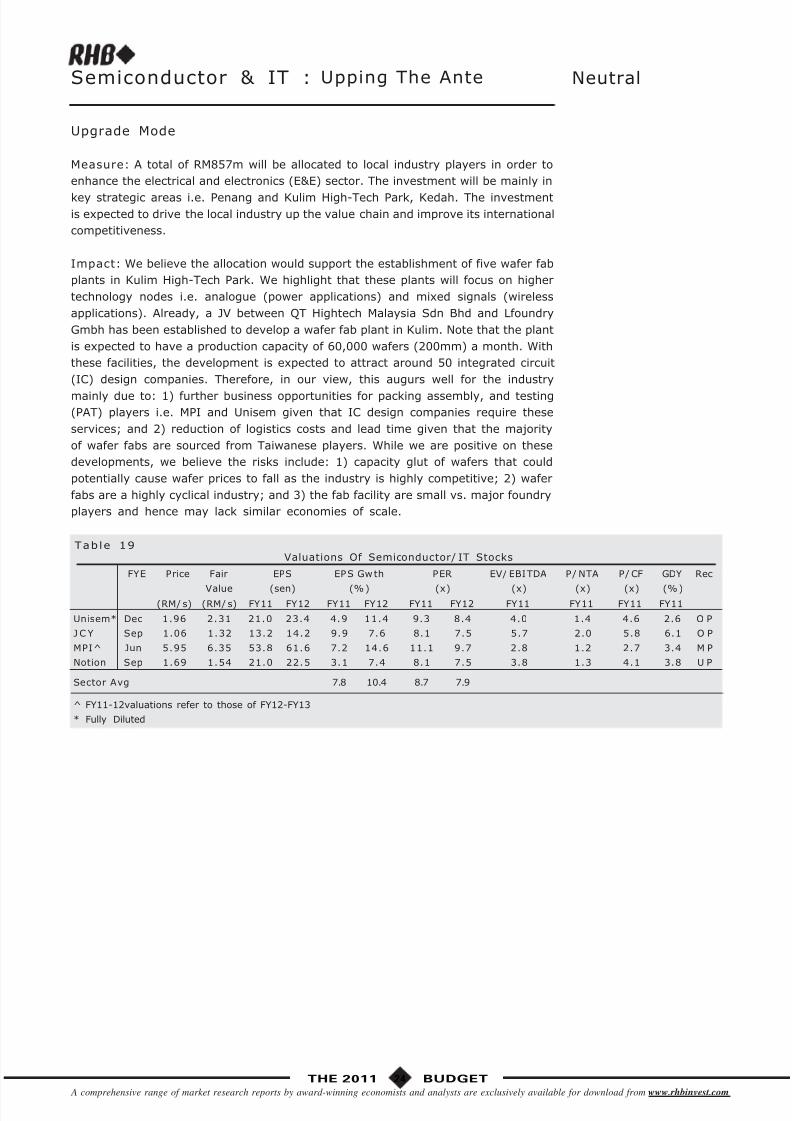

the 2011 budget : setting the pace towards transformation-15/10/2010

TRANSCRIPT

8/8/2019 The 2011 Budget : Setting The Pace Towards Transformation-15/10/2010

http://slidepdf.com/reader/full/the-2011-budget-setting-the-pace-towards-transformation-15102010 1/26

The 2011 Budget

Setting The Pace Towards Transformation

Executive Summary

Please read important disclosures at the end of this report.

◆ The 2011 Budget sets the pace of economic transformation with the right emphasis on reinvigorating private

investment and intensifying human capital development. These are the major positives in the Budget which,

in our view, are critical to chart the direction of the country in moving towards a high income economy.

There are, however, no substantial new information that will likely excite equity investors in the immediate

term, in our view.

◆ Whilst the Budget aims to strike a balance between fiscal consolidation and the need to sustain spending

to cushion the economy against the risk of a sharper-than-expected slowdown in the global economy, the

lack of broader measures to increase revenue, and reduce subsidies and other operating expenditure

suggests that there is limited room for manoeuvre. As a result, despite a less expansionary Budget, the

fiscal deficit is only projected to ease marginally to 5.4% of GDP in 2011, from 5.6% estimated for 2010.

◆ Consequently, our views on the market outlook, earnings and sector calls remain relatively unchanged. In

fact, the Budget speech focused attention primarily on private sector projects that are already in the news.

While there are still lack of details, we believe the news flow will likely come after the Budget speech, now

that the timelines for the major projects have been set and are mostly expected to begin in 2011. This

suggests that the groundwork will accelerate from here on and we believe this will maintain the positive

flow of news to the construction sector and, to a lesser extent, the property sector. Therefore, we believe

any knee jerk to sell would only be temporary as the post-Budget news flow continues to sustain the

liquidity-driven rally.

◆ Whilst market valuations are no longer cheap, the influx of G3 liquidity to Emerging Asia's equity, bond and

currency markets in search for higher returns could still send the market higher in the near term, in our

view. These short-term capital, however, are transient in nature and could reverse out relatively quicklywith changes in outlook. Already, the destabilising capital flows and sharp appreciation of currencies in

Emerging Asia have created concerns and induced policy intervention in the form of short-term capital

control and currency intervention in some countries. As a result, we believe the market may move into

a phase of greater volatility in the months ahead.

◆ Longer term, we believe there is still room for the market to trend higher in 2011. This is primarily

predicated on the view the global economy is more sustainable than feared, which in turn implies sustained

corporate earnings growth (+12.8% projected for 2011) that will continue to create new shareholders' value

for investors. Consequently, our end-2011 FBM KLCI target remains unchanged at 1,640, based on 15x

mid-cycle 2012 earnings. This, however, will not be without volatility as the global economy enters into

a period of slowing growth in an uneven phase of recovery.

◆ Under such circumstances, investors should remain vigilant and do some top slicing on stocks where

valuations have become rich in the run-up of the market. This would then provide more room for investorsto accumulate fundamentally-robust stocks on weakness.

15 October 2010

M a l a y s i a

•

P P 7

7 6 7 / 0 9 / 2 0 1 1 ( 0 2 8 7 3 0 )

M A R K E T D A

T E L I N E

8/8/2019 The 2011 Budget : Setting The Pace Towards Transformation-15/10/2010

http://slidepdf.com/reader/full/the-2011-budget-setting-the-pace-towards-transformation-15102010 2/26

THE 2011 BUDGET2

A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

Key Tax And Expenditure Measures

◆ Fiscal consolidation is not as sharp as earlier expected given that the projected budget deficit comes

in higher than the guidance provided under the Tenth Malaysia Plan. This suggests that the Government

intends to front load its expenditure to facilitate the implementation of the various initiatives proposed for the

NKRAs and NKEAs under the New Economic Model. This is prudent given rising risk of a sharper-than-

expected slowdown in the global economy.

◆ The deficit of the Federal Government is projected to drop slightly to 5.4% of GDP in 2011 , from

a deficit of 5.6% of GDP estimated for 2010. Taken together, the impact on the Malaysian economy

is likely to be less expansionary in 2011, but still contributing to growth, albeit by a smaller

magnitude compared with 2010, in our view.

◆ The consolidated public sector is projected to record a smaller deficit in 2011 due mainly to a reduction

in development expenditure by both the general government and the non-financial public enterprises (NFPEs).

As a result, the consolidated public sector is also expected to exert a less expansionary impact on

the economy during the year.

Reinvigorating Private Investment

Measures

◆ Given the budget constraints, the Government appears to be even more dependent on Public-Private Partnership

(PPP) initiatives to drive investments.

◆ Although some of the investments were already announced previously, the market has been waiting for

confirmation and more details on:

o RM46bn Kuala Lumpur International Financial District, to be developed by 1Malaysia Development Berhad

(1MDB) and Abu Dhabi’s Mubadala Development Company, commencing next year.

o Mass Rapid Transit (MRT) project within the Greater KL NKEA, which will be implemented between 2011 and

2020 with an estimated private investment of RM40bn.

o Development of the 2,680-acre Malaysian Rubber Board land in Sungai Buloh by EPF, which is estimated

to be worth RM10bn and expected to be completed by 2025.

o PNB’s RM5bn 100-storey Warisan Merdeka to be built on the site of the Stadium Merdeka and Stadium

Negara, and targeted for completion by 2015.

◆ The Government repeated earlier statements for the Government-Linked Investment Companies (GLICs) to

divest their shareholdings in major listed companies. However, the GLICs will now also be allowed to increase

their overseas investments, e.g. EPF’s overseas investments will be allowed to rise to 20%, from 7% currently.

◆ Three new stockbroking licences will be issued to local or foreign players to increase the retail market

participation, while new fixed income and equity products such as Exchange Traded Funds will be facilitated

by the Securities Commission and launched by Bursa Malaysia to meet investors’ demand.

◆ The Government will establish a RM1bn syariah-compliant Bumiputera Property Trust Scheme under the

Bumiputera Property Trust Foundation (BPTF) to enable more bumiputera ownership of prime commercial

properties in the Klang Valley, through a group ownership scheme.

◆ In the oil & gas industry, as previously mentioned in the Economic Transformation Programme (ETP), the

Government will allocate RM146m to help establish an Oil Field Services and Equipment Centre in Johoralthough the project will be mainly driven by RM6bn private investments over 10 years.

◆ For green technology, the Government extended the pioneer status and investment tax allowance for renewable

energy and energy efficiency activities until 31 Dec 2015. Import duty and sales tax exemption on related

equipment has been extended until 31 Dec 2012. Full import duty exemption for hybrid cars will be extended

to 31 Dec 2011, while excise duty exemption was raised to 100%, from 50% previously.

◆ The B5 programme to blend biofuels with petroleum diesel will be mandatory from June 2011 in Putrajaya,

Kuala Lumpur, Selangor, Negeri Sembilan and Melaka. The Government also intends to follow up with the Feed

in Tariff (FiT) mechanism under the Renewable Energy (RE) Act, but no timeline was given.

◆ The Government plans to boost the tourism industry via a number of measures including improving infrastructure

and facilities. The Government also mentioned but did not elaborate on the RM3bn integrated eco-nature resort

in Karambunai, Sabah, which will commence in 2011. More importantly, import duties on 300 consumer goods

(including apparel, handbags and shoes) ranging between 5% and 30% were abolished.◆ For palm oil, plans are to encourage replanting activity by replacing aged trees with high quality new clones,

through a RM297m fund, while RM150m will be allocated to support downstream oleo derivatives and vitamin

production.

8/8/2019 The 2011 Budget : Setting The Pace Towards Transformation-15/10/2010

http://slidepdf.com/reader/full/the-2011-budget-setting-the-pace-towards-transformation-15102010 3/26

3THE 2011 BUDGET A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

◆ RM199m will be allocated to multimedia content, while the import duty and sales tax exemption on broadband

equipment will be extended until 2012. The investment tax allowance period for the last mile broadband service

providers has also been extended. All mobile phones will also now be exempted from sales tax.

◆ Allocations have been given to the economic corridors of Iskandar Malaysia (RM339m), Northern (RM133m),

East Coast (RM178m), Sarawak (RM93m) and Sabah (RM110m) for development of infrastructure and industrial

projects.

◆ The service tax will be raised from 5% to 6%. The service tax will also be imposed on pay-TV services.

Intensifying Human Capital Development

Measures

◆ The Government will establish a Talent Corporation in early 2011.

◆ RM6.4bn is to be allocated for building and upgrading of schools, hostels, facilities and equipment, plus

RM250m to be allocated for development expenditure to religious schools, vernacular schools, missionary

schools, and Government-assisted schools nationwide.

◆ RM576m will be allocated for scholarships, while RM213m will be allocated to enhance proficiency in the

national and English languages.

◆ RM474m is provided to enhance productivity and skills of non-graduates to meet the demand for skilled

workforce in technical fields.

◆ The 1Malaysia Training Programme will commence in Jan 2011 with an allocation of RM500m.

◆ Basic minimum wages will be enforced for security guards with effect from Jan 2011. This follows the increase

in salaries of postmen on 1 Jul 2010.

Enhancing Quality Of Life Of The Rakyat

Measures

◆ RM1.2bn is allocated to the Ministry of Women, Family and Community Development to carry out various

welfare and community programmes.

◆ The rebate for electricity bills of less than RM20 will continue to ease the burden of the low-income group.

◆ RM568m is provided to build houses for the poor and low-income group, while a scheme is open to all

Malaysian permanent estate workers to obtain housing loans at 4% interest rate and a repayment period of

up to 40 years extending to the second generation.

◆ Cagamas will introduce the Skim Rumah Pertamaku, which will provide a guarantee on down payment of 10%

for houses below RM220,000, and only for first-time house buyers with household income less than RM3,000

per month.

◆ First time buyers will also be given stamp duty exemption of 50% on instruments of transfer and loan

agreement instruments on a house price not exceeding RM350,000.

◆ For the rural population, RM6.9bn will be allocated to implement basic infrastructure such as water and

electricity supply and rural roads.

◆ RM974m will be allocated to increase food production, plus RM170m incentives for fishermen as well as boat

owners and workers to increase fish landing.

◆ The Government is allocating RM200m to standardise the prices of rice, cooking oil, sugar, flour, gas, petrol

and diesel in rural areas.

◆ The Government will increase the monthly allowance for various community leaders, religious leaders and

village heads.

◆ Toll rates for four highways owned by PLUS Expressway will not be raised for the next five years, effective

immediately.

◆ RM15.2bn will be allocated to construct new hospitals, increase the number of doctors and nurses as well as

to obtain supplies of medicines and equipment.

◆ RM350m will be allocated to various programmes to combat crime.

◆ RM1.9bn will allocated to finance environmental preservation projects, including implementing the River of Life

Programme (under the ETP) and greening of Kuala Lumpur.

Strengthening Public Service Delivery

Measures

◆ The Government will introduce a point system to facilitate applications for permanent residence status.◆ Civil servants will be given financial assistance, and easier access to housing loans with effect 1 Jan 2011.

The maximum loan eligibility will be raised to RM450,000, from RM360,000 currently.

8/8/2019 The 2011 Budget : Setting The Pace Towards Transformation-15/10/2010

http://slidepdf.com/reader/full/the-2011-budget-setting-the-pace-towards-transformation-15102010 4/26

THE 2011 BUDGET4

A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

Impact On The Economy : Less Expansionary But Still

Contributing To Growth

THE REVENUE AND EXPENDITURE PROPOSALS

Federal Government : Less Expansionary

Although the Government will continue to reduce its budget deficit in 2011, it is

not as sharp as earl ier expected given that the projected budget deficit

comes in higher than the guidance provided under the Tenth Malaysia Plan (10MP).

As a result, the Federal Government’s budget deficit is projected to only narrow

slightly to 5.4% of GDP in 2011, from 5.6% of GDP estimated for 2010 and

compared with the guidance of 4.2% provided under the 10MP. We view it as a

prudent move given rising risk of a sharper-than-expected slowdown in the global

economy, which will in turn hurt the country’s exports. Furthermore, the

Government intends to spend more in the initial period of introducing the New

Economic Model (NEM), particularly to facilitate the implementation of various

initiatives under the model. This, together with measures announced in the 2011

Budget, is also aimed at convincing the general public and, investors in particular,

that the Government is serious in transforming the economy by taking the

lead and putting the money where its mouth is, in order to instill confidence.

We believe the Government’s initiatives announced in the 2011 Budget to

reinvigorating private investment w il l help to sustain the sector’s growth ,

albeit at a more moderate pace. These measures include an allocation to encourage

electrical & electronics industry to invest in high value-added activities, an extension

of tax incentives for another 5 years to 2015 to encourage companies to undertake

food production activities, a cut in import duties to boost tourism and incentives

to develop green technology. Infrastructure and property developments are

expected to drive private investment in 2011 as well, in our view. As it stands,

the Government has allocated RM1.0bn for the Facilitation Fund to drive the

Public-Private Partnership projects, targeting construction of highways, power plant

and healthcare related projects. It also indicated that the Mass Rapid Transit

(MRT) which cost about RM40bn will be implemented in 2011. The Government-

linked investment corporations such as the 1Malaysia Development Bhd, the

Employees Provident Fund and Permodalan National Bhd, have also been earmarked

to undertake some huge development projects. Similarly, the Government will

offer three new stock broking licences to increase retail market participation. As

a whole, we expect private investment to moderate to 7.8% in 2011, from +8.6%

estimated for 2010.

Although consumer spending will be affected somewhat by the reinstatement of

employees’ contribution to the Employee Provident Fund back to 11% in 2011, we

believe the 1.0% increase in services tax to 6.0%, is unlikely to impact consumer

spending significantly. The 1% increase is estimated to bring in additional tax

revenue of RM0.7bn for the Government. In addition, the abolishment of 5-30%

import duties of approximately 300 goods preferred by tourists and locals and the

RM500 Special Financial Assistance money provided for civil servants will help to

sustain consumer spending. As a result, we expect consumer spending to

remain resilient, underpinned by rising consumerism and high savings in the

country.

As a whole, given that the Federal Government will spend more than what it

collects in terms of revenue, this will exert a less expansionary impact on the

economy, but sti l l contributing to growth in 2011 , albeit by a smallermagnitude compared with 2010 (see Table 1). Meanwhile, we believe the

Government is committed to reduce its budget deficit, albeit gradually, to ensure

that fiscal policy remains supportive of economic growth.

The reduc t i on i n t he

Gove rnment ’ s budge t

deficit is not as sharp as

earlier expected in 2011

The Government is serious

i n t rans fo rm ing t he

economy by tak ing the

lead

Init iat ives announced in

the 2011 Budget will help

to sus ta in p r i vate

investment growth

Consumer spending wi l l

l i k e l y rema in res i l i en t ,unde rp i nned by r i s i ng

consumer i sm and h i gh

savings in the country

Fiscal policy will exert a

less expansionary impact

on the economy, but stil lcontributing to growth in

2011

8/8/2019 The 2011 Budget : Setting The Pace Towards Transformation-15/10/2010

http://slidepdf.com/reader/full/the-2011-budget-setting-the-pace-towards-transformation-15102010 5/26

5THE 2011 BUDGET A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

Consolidated Public Sector : Also Less Expansionary

The consolidated public sector’s fiscal spending, which includes the state

governments, statutory authorities, local governments and non-financial public

enterprises (NFPEs), will also be less expansionary in 2011. This is reflected in

a smaller deficit projected for the consolidated public sector, which is envisaged to

narrow slightly to 7.6% of GDP or RM63.5bn in 2011, from a deficit of 7.8% of GDP

or RM60.1bn estimated for 2010 (see Table 2). This is on account of a smaller deficit

of 5.1% projected at the general government level for 2011, compared with a deficit

of 5.2% of GDP estimated for 2010, on the back of a reduction in development

expenditure. Similarly, the NFPEs development expenditure is projected to slow

down and its deficit is projected to record a smaller deficit of 2.4% in 2011, compared

with a deficit of 2.5% estimated for 2010.

The consol idated publ ic

sector’s fiscal spending will

also be less expansionary

in 2011

Table 1

Federal Government Financial Posit ion

2009 2010(e) 20111(f) 2010(e) 2011(f)

(RM bil) (%, change)

Revenue 158.6 162.1 165.8 2.2 2.3

Operating Expenditure 157.1 152.2 162.8 -3.1 7.0

Current balance 1.6 10.0 3.0

Gross development expenditure 49.5 54.0 49.2 9.1 -9.0

Less : Loan recoveries 0.5 0.7 0.7 41.0 -6.8

Net development expenditure 49.0 53.3 48.5 8.8 -9.0

Overall balance -47.4 -43.3 -45.5

% to GDP -7.0 -5.6 -5.4

1 Budget estimate, excluding 2011 tax measures

e : Estimates f : Forecasts

Source : MOF's Economic Report 2010/2011

Table 2Consol idated P ublic Sector Financial Posit ion

2009 2010(e) 20111(f) 2009 2010(e) 2011(f)

(RM bil) (%, change)

Revenue 134.0 132.8 138.6 4.4 -0.9 4.4

Operating expenditure 170.3 168.0 176.8 3.2 -1.3 5.2

NFPEs current surplus 101.2 94.2 93.2 -15.2 -6.9 -1.1

Public sector current balance 64.9 59.0 55.0

% of GDP +9.6 +7.6 +6.6

Development expenditure 111.3 119.1 118.5 -10.5 7.0 -0.5

General government 54.5 57.1 54.8 7.9 4.8 -4.1

NFPEs 56.8 62.0 63.7 -23.1 9.2 2.8

Overall balance -46.4 -60.1 -63.5

% of GDP -6.8 -7.8 -7.6

1 Budget estimate, excluding 2011 tax measures

Source : Ministry Of Finance Economic Report 2010/2011

8/8/2019 The 2011 Budget : Setting The Pace Towards Transformation-15/10/2010

http://slidepdf.com/reader/full/the-2011-budget-setting-the-pace-towards-transformation-15102010 6/26

THE 2011 BUDGET6

A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

Impact On The Equity Market : Neutral

Given the 2011 Budget’s spending constraints, it is perhaps not surprising that there

was a lack of major incentives and significant measures from the Government. While

there were the usual allocations for healthcare, education, rural development, and

incentives for civil servants, there were no significant catalysts for other key

economic sectors.

In fact, the Budget speech focused attention primarily on private sector projects that

are already in the news. These included the RM40bn MRT, the RM26bn Kuala Lumpur

International Financial District, and EPF’s RM10bn development of the Malaysian

Rubber Board land in Sungai Buloh, plus the revival of PNB’s proposed 100-storey

RM5bn Warisan Merdeka building on the site of the old national stadium.

While the lack of details on these projects could be a major disappointment for

investors, we believe the news flow will in fact come after the Budget speech, now

that the timelines for each of these projects have been set. In fact, the projects are

mostly expected to begin in 2011, which suggest that the groundwork will accelerate

from here on. We believe this will maintain the positive flow of news to the

construction sector, and sustain the bullish sentiment for Gamuda (TB, FV =

RM4.51) and MRCB (TB, FV = RM2.49).

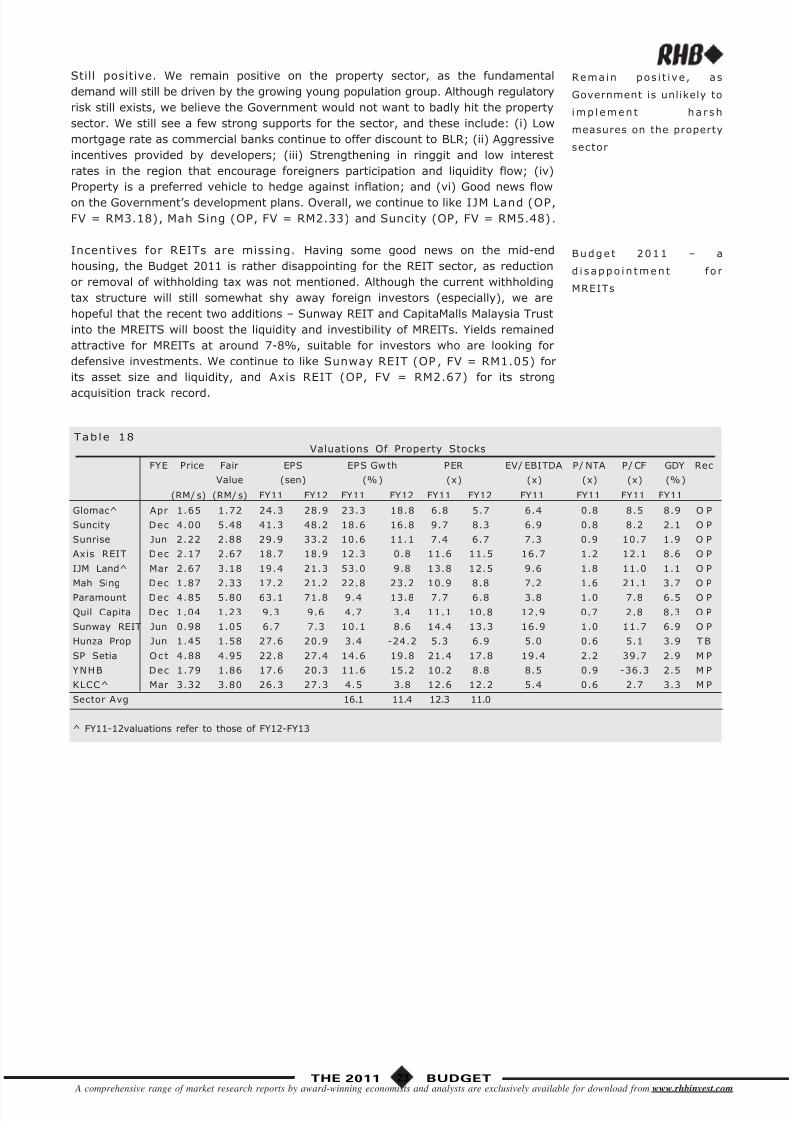

As for the property sector, we note the Government’s focus on the low- to mid-end

range housing with incentives for first-time buyers, which was in line with the theme

to assist the lower-income groups. However, we believe this does not preclude

subsequent post-Budget measures to curb speculation on mid- to high-end

properties, and this uncertainty could have a negative impact on the property sector.

Our preference would thus still be on the mass housing developers like Mah Sing

(OP, FV = RM2.33).

The PM’s call again to the Government-Linked Investment Companies (GLICs) to

divest their shareholdings in listed companies will once again focus attention on the

key GLCs, like Axiata (MP , FV = RM5.75), TM (MP , FV = RM3.55), TNB (OP, FV

= RM10.30) and MAHB (OP, FV = RM5.96). We note that EPF and UEM Group’s

proposal on 15 Oct to jointly acquire PLUS’s assets and liabilities for RM23bn cash

could be seen as a contradictory move, but the upshot is that investors will receive

a capital repayment that can be redeployed in other stocks, thereby indirectly

improving the market’s liquidity.

We believe the 2011 Budget has not provided major catalysts for the equity market,

but this has been the case even with past budget speeches. Therefore, we believe

that a knee jerk reaction to sell would only be temporary as the post-Budget news

flow (relating to the ETP blueprint to be published on 25 Oct, the MMHE and Petronas

Chemicals listings, and the potential Sarawak state election) continues to sustain the

liquidity-driven rally.

No significant catalysts for

key economic sectors

Focus on pr ivate sector

projects

News flow likely to come

after the Budget speech

Incent ive fo r f i rs t - t ime

house buyers

GLICs called upon to divest

GLC shares

Post-Budget news flow to

sus ta in l i qu id i ty-dr i ven

rally

8/8/2019 The 2011 Budget : Setting The Pace Towards Transformation-15/10/2010

http://slidepdf.com/reader/full/the-2011-budget-setting-the-pace-towards-transformation-15102010 7/26

7THE 2011 BUDGET A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

Market Outlook : Short-term Liquidity And NewsFlow Driven

The 2011 Budget sets the pace of economic transformation with the right emphasis

on reinvigorating private investment and intensifying human capital development.

These are the major positives in the Budget which, in our view, are critical to chart

the direction of the country in moving towards a high income economy. There are,

however, no substantial new information that will likely excite equity investors in the

immediate term, in our view.

Whilst the Budget aims to strike a balance between fiscal consolidation and the need

to sustain spending to cushion the economy against the risk of a sharper-than-

expected slowdown in the global economy, the lack of broader measures to increase

revenue, and reduce subsidies and other operating expenditure suggests that there

is limited room for manoeuvre. As a result, despite a less expansionary Budget, the

fiscal deficit is only projected to ease marginally to 5.4% of GDP in 2011, from 5.6%

estimated for 2010.

Consequently, our views on the market outlook, earnings and sector calls remain

relatively unchanged (see Tables 3 & 4). Whilst market valuations are no longer

cheap, the influx of G3 liquidity to Emerging Asia's equity, bond and currency mar-

kets in search for higher returns could still send the market higher in the near term,

in our view. These short-term capital, however, are transient in nature and could

reverse out relatively quickly with changes in outlook. Already, the destabilising

capital flows and sharp appreciation of currencies in Emerging Asia have created

concerns and induced policy intervention in the form of short-term capital control and

currency intervention in some countries. As a result, we believe the market may

move into a phase of greater volatility in the months ahead.

FBM KLCI RHBRI ’s Basket

COMPOSITE INDEX @1,489.86 2009a 2010f 2011f 2012f 2009a 2010f 2011f 2012f

15/10/2010

EBITDA Growth (%) -6.6 26.2 11.3 7.3 -2.0 23.5 11.2 7.3

Pre-Tax Earnings Growth (%) -10.0 38.5 17.8 9.0 -2.4 32.0 15.9 9.9

Normalised Earnings Growth (% )* -10.2 30.0 13.1 9.1 -6.3 28.8 13.9 9.8

Normalised EPS Growth (% )* -14.9 23.7 12.8 9.1 -9.7 19.7 13.8 9.8

Prospective PER (x)* 20.7 16.7 14.8 13.6 19.8 16.1 14.1 12.8

Price/EBITDA (x) 10.9 8.7 7.8 7.3 8.6 8.3 7.4 6.9

Price/Bk (x) 2.6 2.4 2.3 2.1 2.0 2.2 2.0 1.9

Price/NTA (x) 3.4 2.8 2.6 2.4 2.3 2.5 1.3 1.3

Net Interest Cover (x) 7.6 8.2 9.5 10.8 7.1 8.0 9.3 10.4

Net Gearing (%) 48.8 46.3 40.7 37.5 47.6 37.4 37.4 33.1

EV/EBITDA (x) 8.4 6.7 6.0 5.6 8.3 6.9 6.1 5.5

ROE (%) 12.3 14.7 15.2 15.4 11.7 13.6 14.2 14.8

* Exclude Mas earnings in 09-11

Table 3

Earnings Outlook And Valuations

Setting the pace towards

transformat ion wi th the

right emphasis

No subs t an t i a l new

in fo rmat i on f rom the

Budget , but in f lux o f

short-term liquidity could

s t i l l s end t he marke t

higher in the near term

Ba l anc i ng f i s ca l

consolidation with growth

but with limited room for

manoeuvre

8/8/2019 The 2011 Budget : Setting The Pace Towards Transformation-15/10/2010

http://slidepdf.com/reader/full/the-2011-budget-setting-the-pace-towards-transformation-15102010 8/26

THE 2011 BUDGET8

A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

Table 4Sector Weight ings & Valuat ions

Covered Stocks Mkt Cap Weight EPS Gwth (% ) PER (x) Recommendation

RMbn % FY10 FY11 FY12 FY10 FY11 FY12

Banks & Finance 213.3 25.6 24.0 13.4 10.5 15.4 13.5 12.2 Overweight

Power 63.9 7.7 16.8 12.3 12.3 13.7 12.2 10.9 Overweight

Construction 22.9 2.8 28.4 12.7 6.8 19.6 17.3 16.2 OverweightMotor 21.4 2.6 58.9 10.2 17.2 10.8 9.8 8.4 Overweight

Property 21.3 2.6 -13.5 16.1 11.4 14.4 12.3 11.0 Overweight

Media 15.0 1.8 40.5 8.9 7.5 14.0 12.9 12.0 Overweight

Timber 3.6 0.4 68.4 41.8 14.6 12.3 8.7 7.5 Overweight

Insurance 3.8 0.5 6.6 8.7 21.5 9.4 8.6 7.1 Neutral

Plantation 119.4 14.3 5.9 19.9 3.0 20.7 17.0 16.5 Neutral

Telecommunications 109.6 13.2 23.2 11.5 8.9 17.1 15.3 14.0 Neutral

Gaming 64.2 7.7 51.7 0.9 9.4 14.0 13.8 12.6 Neutral

Transportation* 59.7 7.2 44.9 12.5 17.3 21.1 18.7 13.7 Neutral

Oil & Gas 33.9 4.1 9.7 16.4 9.8 17.3 14.9 13.5 Neutral

Consumer 32.6 3.9 -6.2 11.1 10.7 16.9 15.9 14.3 Neutral

Infrastructure 23.5 2.8 2.0 49.0 9.0 17.3 11.6 10.7 Neutral

Building Materials 12.9 1.6 14.1 21.3 4.1 12.9 10.9 10.5 Neutral

Manufacturing 7.2 0.9 25.7 14.4 10.3 11.4 10.0 9.0 Neutral

Semiconductors & IT 5.0 0.6 32.7 7.8 10.4 8.8 8.7 7.9 Neutral

833.1 100.0

* Exclude MAS earnings in 10-11

Note : RHBRI’s basket

Longer term, we believe there is still room for the market to trend higher in 2011.

This is primarily predicated on the view the global economy is more sustainable than

feared, which in turn implies sustained corporate earnings growth (+12.8% projected

for 2011) that will continue to create new shareholders' value for investors. Con-sequently, our end-2011 FBM KLCI target remains unchanged at 1,640, based on 15x

mid-cycle 2012 earnings. This, however, will not be without volatility as the global

economy enters into a period of slowing growth in an uneven phase of recovery.

Longe r - t e rm ou t l ook ,

however, remains positive

and our end-2011 FBM

KLCI t a rge t rema ins

unchanged at 1,640

8/8/2019 The 2011 Budget : Setting The Pace Towards Transformation-15/10/2010

http://slidepdf.com/reader/full/the-2011-budget-setting-the-pace-towards-transformation-15102010 9/26

9THE 2011 BUDGET A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

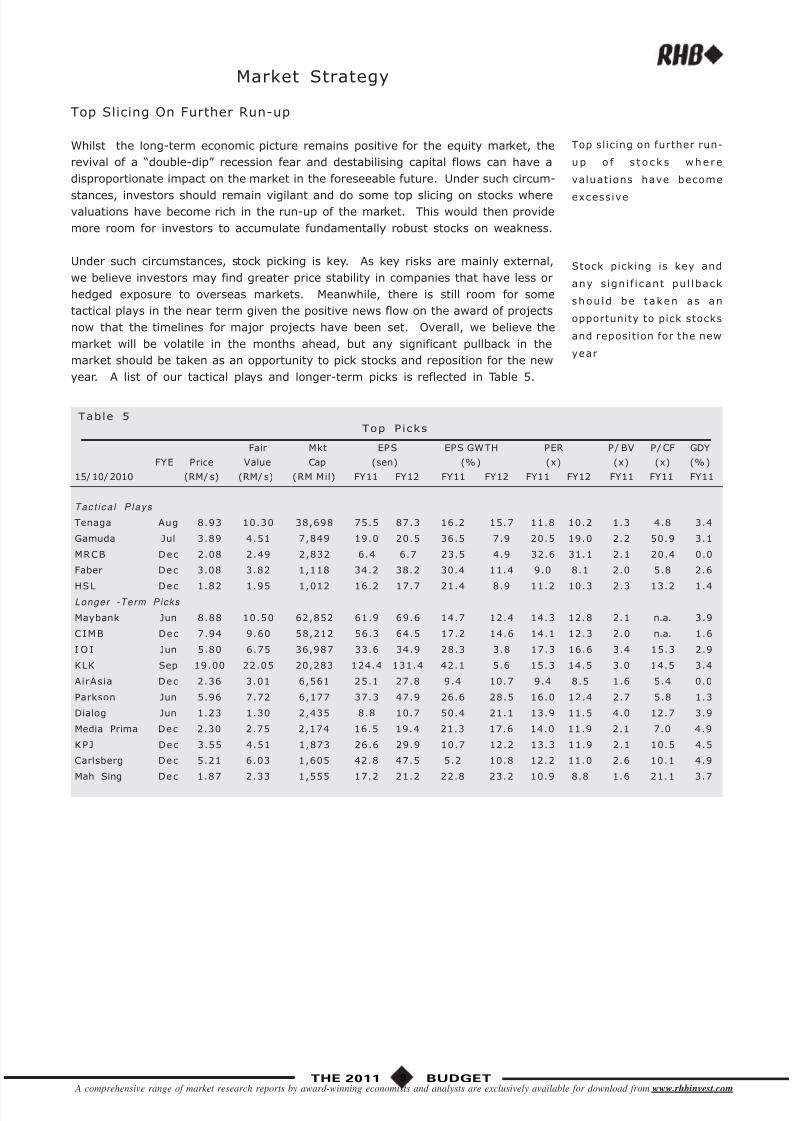

Market Strategy

Top Slicing On Further Run-up

Whilst the long-term economic picture remains positive for the equity market, the

revival of a “double-dip” recession fear and destabilising capital flows can have a

disproportionate impact on the market in the foreseeable future. Under such circum-

stances, investors should remain vigilant and do some top slicing on stocks wherevaluations have become rich in the run-up of the market. This would then provide

more room for investors to accumulate fundamentally robust stocks on weakness.

Under such circumstances, stock picking is key. As key risks are mainly external,

we believe investors may find greater price stability in companies that have less or

hedged exposure to overseas markets. Meanwhile, there is still room for some

tactical plays in the near term given the positive news flow on the award of projects

now that the timelines for major projects have been set. Overall, we believe the

market will be volatile in the months ahead, but any significant pullback in the

market should be taken as an opportunity to pick stocks and reposition for the new

year. A list of our tactical plays and longer-term picks is reflected in Table 5.

Table 5Top Picks

Fair Mkt EPS EPS GWTH PER P/ BV P/ CF GDY

FYE Price Value Cap (sen) (%) (x) (x) (x) (%)

15/10/2010 (RM/ s) (RM/ s) (RM Mil) FY11 FY12 FY11 FY12 FY11 FY12 FY11 FY11 FY11

Tac t i ca l P lays

Tenaga Aug 8.93 10.30 38,698 75.5 87.3 16.2 15.7 11.8 10.2 1.3 4.8 3.4

Gamuda Jul 3.89 4.51 7,849 19.0 20.5 36.5 7.9 20.5 19.0 2.2 50.9 3.1

MRCB Dec 2.08 2.49 2,832 6.4 6.7 23.5 4.9 32.6 31.1 2.1 20.4 0.0

Faber Dec 3.08 3.82 1,118 34.2 38.2 30.4 11.4 9.0 8.1 2.0 5.8 2.6

HSL Dec 1.82 1.95 1,012 16.2 17.7 21.4 8.9 11.2 10.3 2.3 13.2 1.4Longer -Term Picks

Maybank Jun 8.88 10.50 62,852 61.9 69.6 14.7 12.4 14.3 12.8 2.1 n.a. 3.9

CIMB Dec 7.94 9.60 58,212 56.3 64.5 17.2 14.6 14.1 12.3 2.0 n.a. 1.6

I O I Jun 5.80 6.75 36,987 33.6 34.9 28.3 3.8 17.3 16.6 3.4 15.3 2.9

KLK Sep 19.00 22.05 20,283 124.4 131.4 42.1 5.6 15.3 14.5 3.0 14.5 3.4

AirAsia Dec 2.36 3.01 6,561 25.1 27.8 9.4 10.7 9.4 8.5 1.6 5.4 0.0

Parkson Jun 5.96 7.72 6,177 37.3 47.9 26.6 28.5 16.0 12.4 2.7 5.8 1.3

Dialog Jun 1.23 1.30 2,435 8.8 10.7 50.4 21.1 13.9 11.5 4.0 12.7 3.9

Media Prima Dec 2.30 2.75 2,174 16.5 19.4 21.3 17.6 14.0 11.9 2.1 7.0 4.9

KPJ Dec 3.55 4.51 1,873 26.6 29.9 10.7 12.2 13.3 11.9 2.1 10.5 4.5

Carlsberg Dec 5.21 6.03 1,605 42.8 47.5 5.2 10.8 12.2 11.0 2.6 10.1 4.9

Mah Sing Dec 1.87 2.33 1,555 17.2 21.2 22.8 23.2 10.9 8.8 1.6 21.1 3.7

Top slicing on further run-

up o f s t o cks where

valuations have become

excessive

Stock picking is key and

any s igni f i cant pul lback

shou ld be taken as an

opportunity to pick stocks

and reposition for the new

year

8/8/2019 The 2011 Budget : Setting The Pace Towards Transformation-15/10/2010

http://slidepdf.com/reader/full/the-2011-budget-setting-the-pace-towards-transformation-15102010 10/26

THE 2011 BUDGET10

A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

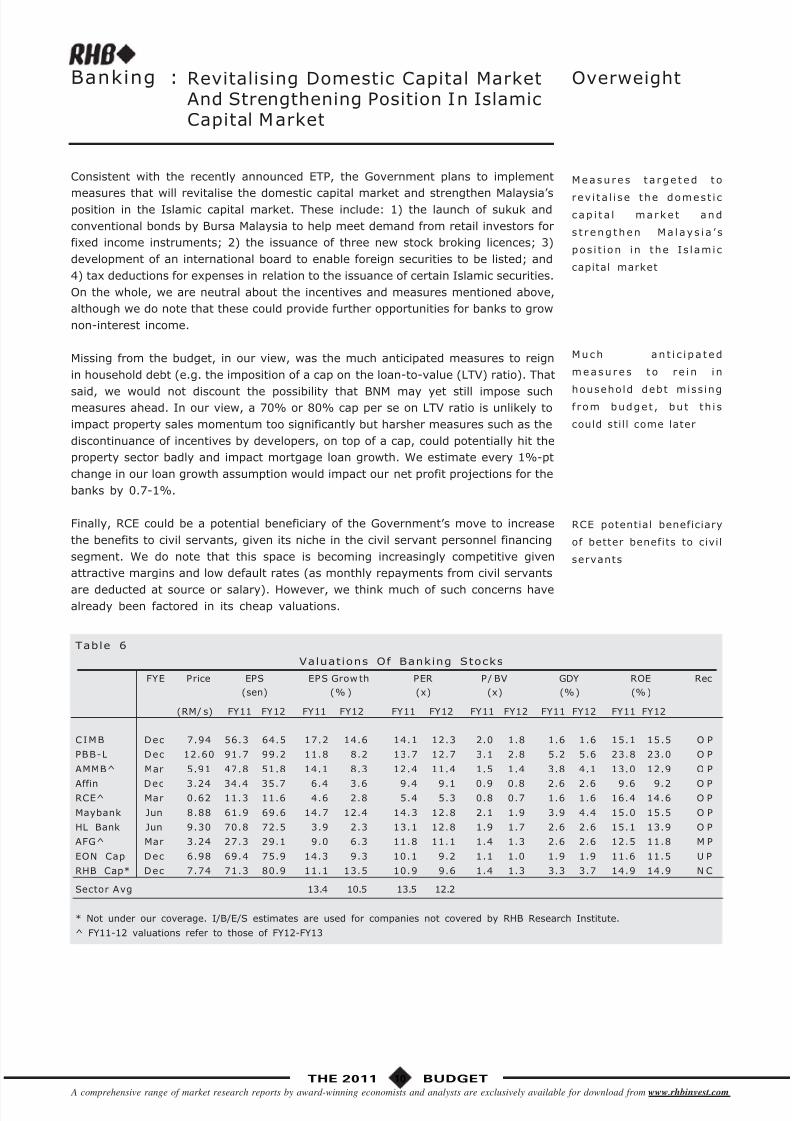

Banking : OverweightRevitalising Domestic Capital MarketAnd Strengthening Position In IslamicCapital Market

Consistent with the recently announced ETP, the Government plans to implement

measures that will revitalise the domestic capital market and strengthen Malaysia’sposition in the Islamic capital market. These include: 1) the launch of sukuk and

conventional bonds by Bursa Malaysia to help meet demand from retail investors for

fixed income instruments; 2) the issuance of three new stock broking licences; 3)

development of an international board to enable foreign securities to be listed; and

4) tax deductions for expenses in relation to the issuance of certain Islamic securities.

On the whole, we are neutral about the incentives and measures mentioned above,

although we do note that these could provide further opportunities for banks to grow

non-interest income.

Missing from the budget, in our view, was the much anticipated measures to reign

in household debt (e.g. the imposition of a cap on the loan-to-value (LTV) ratio). That

said, we would not discount the possibility that BNM may yet still impose suchmeasures ahead. In our view, a 70% or 80% cap per se on LTV ratio is unlikely to

impact property sales momentum too significantly but harsher measures such as the

discontinuance of incentives by developers, on top of a cap, could potentially hit the

property sector badly and impact mortgage loan growth. We estimate every 1%-pt

change in our loan growth assumption would impact our net profit projections for the

banks by 0.7-1%.

Finally, RCE could be a potential beneficiary of the Government’s move to increase

the benefits to civil servants, given its niche in the civil servant personnel financing

segment. We do note that this space is becoming increasingly competitive given

attractive margins and low default rates (as monthly repayments from civil servants

are deducted at source or salary). However, we think much of such concerns havealready been factored in its cheap valuations.

Measures t a rge t ed t o

rev i ta l i se the domest i c

cap i t a l marke t and

s t reng then Ma l ays i a ’ s

pos i t i on in the Is lamic

capital market

Much an t i c i pa t ed

measures t o re i n i n

household debt miss ingf rom budget , but th i s

could stil l come later

RCE potential beneficiary

of better benefits to civil

servants

Table 6

Valuations Of Banking Stocks

FYE Price EPS EPS Grow th PER P/ BV GDY ROE Rec

(sen) (% ) (x) (x) (%) (%)

(RM/ s) FY11 FY12 FY11 FY12 FY11 FY12 FY11 FY12 FY11 FY12 FY11 FY12

CIMB Dec 7.94 56.3 64.5 17.2 14.6 14.1 12.3 2.0 1.8 1.6 1.6 15.1 15.5 O P

PBB-L Dec 12.60 91.7 99.2 11.8 8.2 13.7 12.7 3.1 2.8 5.2 5.6 23.8 23.0 O P

AMMB^ Mar 5.91 47.8 51.8 14.1 8.3 12.4 11.4 1.5 1.4 3.8 4.1 13.0 12.9 O P

Affin Dec 3.24 34.4 35.7 6.4 3.6 9.4 9.1 0.9 0.8 2.6 2.6 9.6 9.2 O PRCE^ Mar 0.62 11.3 11.6 4.6 2.8 5.4 5.3 0.8 0.7 1.6 1.6 16.4 14.6 O P

Maybank Jun 8.88 61.9 69.6 14.7 12.4 14.3 12.8 2.1 1.9 3.9 4.4 15.0 15.5 O P

HL Bank Jun 9.30 70.8 72.5 3.9 2.3 13.1 12.8 1.9 1.7 2.6 2.6 15.1 13.9 O P

AFG^ Mar 3.24 27.3 29.1 9.0 6.3 11.8 11.1 1.4 1.3 2.6 2.6 12.5 11.8 M P

EON Cap Dec 6.98 69.4 75.9 14.3 9.3 10.1 9.2 1.1 1.0 1.9 1.9 11.6 11.5 U P

RHB Cap* Dec 7.74 71.3 80.9 11.1 13.5 10.9 9.6 1.4 1.3 3.3 3.7 14.9 14.9 N C

Sector Avg 13.4 10.5 13.5 12.2

* Not under our coverage. I/B/E/S estimates are used for companies not covered by RHB Research Institute.

^ FY11-12 valuations refer to those of FY12-FY13

8/8/2019 The 2011 Budget : Setting The Pace Towards Transformation-15/10/2010

http://slidepdf.com/reader/full/the-2011-budget-setting-the-pace-towards-transformation-15102010 11/26

11THE 2011 BUDGET A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

Building Materials : NeutralPositive But Priced In ForCement, Neutral For Steel

Domestic cement producers are expected to benefit from the anticipated pick-up in

domestic cement consumption, underpinned by the rollout of large-scale infrastructure

projects and pick-up in property development activities. An increase in domesticdemand will also enable cement producers to sell more domestically (which command

a better margin) rather than exporting their excess production. We believe net selling

prices will also be higher as rebates given by the cement producers will be lower.

Fuel and electricity cost constitute about 50% of cement production cost. We believe

high thermal coal price and potential hike in electricity tariff in the future will partly

offset the benefits of higher net selling price.

We are maintaining the forecasts for cement producers under over coverage (Lafarge

and YTL Cement) as the pick-up in domestic cement consumption has been widely

expected. However, with the recent run-up in its share prices, Lafarge’s (UP, FV

= RM6.88) valuation has become very rich at 16.1x to our estimated FY11 earnings(as opposed to our PER target of 14x FY11 earnings). For YTLCement (OP, FV =

RM4.69), its share price is currently close to our fair value of RM4.69 (based on 11x

CY2011 fully diluted EPS of 42.7 sen). We think YTLCement is due for a re-rating

given that it has been a laggard despite being the second largest cement producer

in Malaysia after Lafarge. For now, we maintain our recommendation on YTLCement

pending a meeting with management. Overall, our stance on the cement sub-sector

is maintained at Neutral. Both Lafarge and YTLCement offer decent dividend yield at

5-6% given their strong free cash flow and healthy balance sheet at net cash

position.

Although domestic long steel demand is expected to recover with the pick-up in

construction activities and infrastructure developments, we believe the impact islikely to be minimal, as fortunes of long steel players’ are tied more to the demand-

supply balance in the global market. Overcapacity (particularly in China) remains a

key issue over the medium to long term despite the recent plants closure, as the

excess capacity in China’s steel sector is still high. Maintain our Neutral stance on

the steel sub-sector.

… but will be partly offset

by higher energy prices

Valuation has become rich

Neutral stance maintained

for steel sub-sector

Cement sub-sector poised

to benefit

Table 7Valuations Of Building Materials Stocks

FYE Price Fair EPS EPS Gwth PER EV/ EBITDA P/ NTA P/ CF GDY Rec

Value (sen) (%) (x) (x) (x) (x) (%)

(RM/ s) (RM/ s) FY11 FY12 FY11 FY12 FY11 FY12 FY11 FY11 FY11 FY11

Hiap Teck Jul 1.26 1.63 16.0 16.7 25.3 4.1 7.9 7.5 8.8 0.6 n.m 2.0 O PYTL Cement Jun 4.59 4.69 58.9 57.5 17.5 -2.4 7.8 8.0 4.1 1.2 15.0 4.4 O P

CSC Steel Dec 1.83 2.33 23.3 24.7 6.4 5.9 7.8 7.4 0.9 0.8 6.4 8.2 O P

Perwaja Hldgs Dec 1.11 1.37 13.5 16.9 16.9 24.8 5.1 4.6 7.3 0.6 13.4 0.0 O P

Ann Joo Dec 2.98 3.14 38.9 41.1 18.6 5.6 7.7 7.3 5.8 1.1 30.0 5.0 M P

Lafarge Dec 7.94 6.88 49.2 50.6 15.8 2.8 16.1 15.7 10.6 2.0 12.2 3.8 U P

Sino Hua Dec 0.36 0.36 3.6 3.9 +>100 8.2 9.9 9.1 6.9 0.6 10.9 0.0 U P

Kinsteel Dec 0.91 0.86 8.6 9.2 77.0 6.4 10.5 9.9 4.9 0.9 7.5 1.1 U P

Sector Avg 21.3 4.1 10.9 10.5

8/8/2019 The 2011 Budget : Setting The Pace Towards Transformation-15/10/2010

http://slidepdf.com/reader/full/the-2011-budget-setting-the-pace-towards-transformation-15102010 12/26

THE 2011 BUDGET12

A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

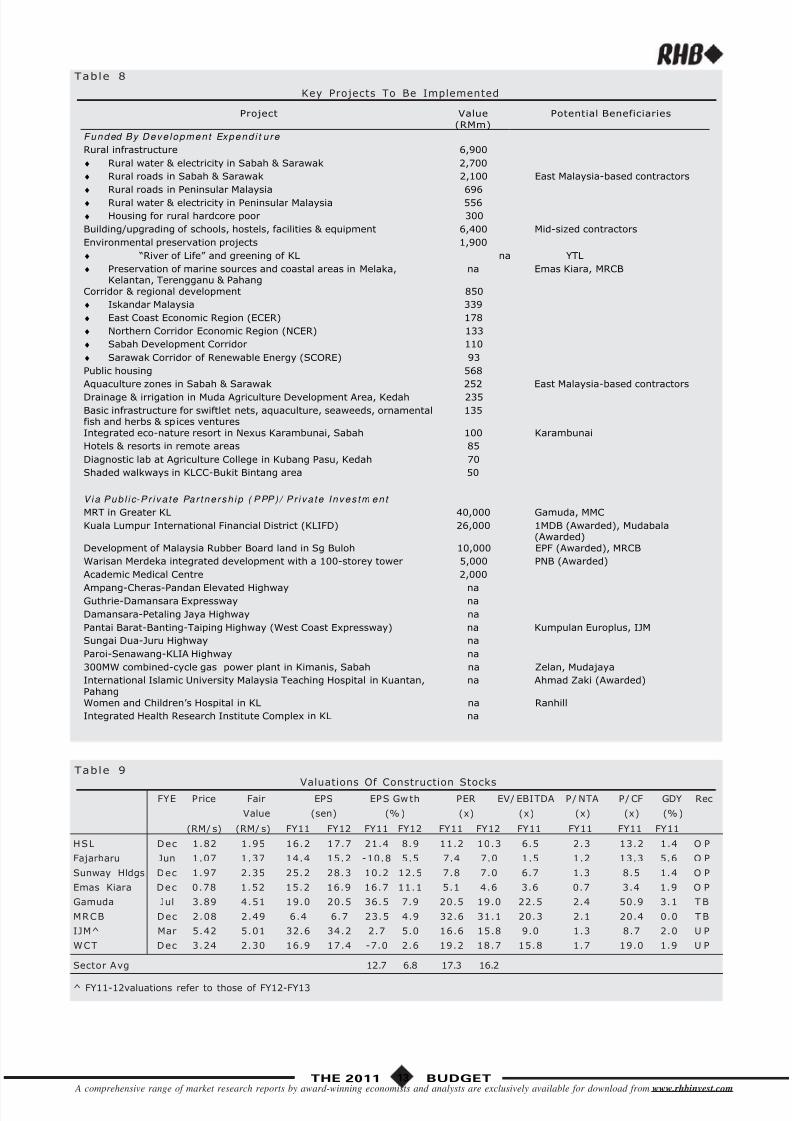

OverweightConstruction : Key Projects Reaffirmed, To Kick-Start In 2011

Gross development expenditure in 2011 is projected at RM49.2bn, down -9% from

RM54bn estimated for 2010. As a result, construction GDP growth is projected to

ease to +4.4% in 2011 from +4.9% estimated for 2010. Key areas of spending (that

will generate construction jobs) are rural infrastructure (RM6.9bn), building/upgradingof schools (RM6.4bn) and environmental preservation (RM1.9bn). Of total rural

infrastructure spending (comprising largely water, electricity and roads), 70% or

RM4.8bn goes to Sabah and Sarawak. The impact of a lower gross development

expenditure will be cushioned by projects to be carried out on a Public-Private

Partnership (PPP) or privatised basis, projected to rack up RM12.5bn private investment,

anchored by RM1bn facilitation fund (see Table 8).

We view positively that key high-profile projects identified during the announcement

of the 10th Malaysia Plan (10MP) (2011-2015) in June this year have been reaffirmed,

with commencement explicitly spelt out to be during the first year of the 10MP, i.e.

in 2011. These include the RM40bn MRT project, the RM26bn KL International

Financial District (KLIFD), the RM10bn redevelopment of the Rubber Research Board

land in Sungai Buloh and six toll roads including the West Coast Expressway.

One interesting observation is that the MRT project is regarded as a PPP/privatised

project “with an estimated private investment of RM40bn”. This is not consistent with

the Gamuda-MMC JV’s proposal to the Government, i.e. to fund the project with

RM10bn allocation each from the 10MP and the 11th Malaysia Plan (11MP), and the

balance to be financed via an off-balance sheet deferred payment scheme (to keep

the budget deficit under control). The Gamuda-MMC JV’s position has been not to

carry out the project on a PPP/privatised basis as it is fully aware that large public

transport projects are generally not commercially viable.

Three new inclusions that we believe worth highlighting are: (1) The “revived” RM5bn

Warisan Merdeka integrated development comprising a 100-storey tower led by

Permodalan Nasional Bhd; (2) The “River of Life”, i.e. the clean-up/beautification of

the Klang Valley that can unlock the real estate potential of land parcels along the

river, funded by part of the RM1.9bn allocation under environmental preservation;

and (3) The Academic Medical Centre, a JV between Academic Medical Centre, Johns

Hopkins Medicine International and Royal College of Surgeons, Ireland, that will

bring in RM2bn private investment.

The Government has reaffirmed its commitment towards key large-scale projects, as

well as the speediness of their implementation in Budget 2011. We view this

positively. We remain upbeat on construction stocks as we believe they will continue

to generally outperform the market from 4Q2010, buoyed by news flow from: (1)

The infrastructure development for the Greater KL National Key Economic Area

(NKEA) under the Economic Transformation Programme (ETP), particularly, the RM40bnMRT project; (2) The RM7bn Ampang and Kelana Jaya LRT line extension project;

and (3) Federal land deals. Our top “tactical” pick for the sector is Gamuda

(Trading Buy, FV = RM4.51) as we believe its share price will be buoyed by the

sustained news flow from the RM40bn MRT project. Our top “value” pick for the

sector is Sunway (Outperform, FV = RM 2.35) due to its undemanding valuations,

coupled with its strong earnings visibility stemming from its firm construction margins

and growing non-construction profits.

Gross deve l opment

expenditure down 9%

Key high-profile projects

reaff irmed, to kick-start

in 2011

MRT to at t rac t RM40bn

private investment?

Several new inclusions

Maintain Overweight

8/8/2019 The 2011 Budget : Setting The Pace Towards Transformation-15/10/2010

http://slidepdf.com/reader/full/the-2011-budget-setting-the-pace-towards-transformation-15102010 13/26

13THE 2011 BUDGET A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

Table 8

Key Projects To Be Implemented

Table 9

Valuations Of Construction StocksFYE Price Fair EPS EPS Gwth PER EV/ EBITDA P/ NTA P/ CF GDY Rec

Value (sen) (%) (x) (x) (x) (x) (%)

(RM/ s) (RM/ s) FY11 FY12 FY11 FY12 FY11 FY12 FY11 FY11 FY11 FY11

HSL Dec 1.82 1.95 16.2 17.7 21.4 8.9 11.2 10.3 6.5 2.3 13.2 1.4 O P

Fajarbaru Jun 1.07 1.37 14.4 15.2 -10.8 5.5 7.4 7.0 1.5 1.2 13.3 5.6 O P

Sunway Hldgs Dec 1.97 2.35 25.2 28.3 10.2 12.5 7.8 7.0 6.7 1.3 8.5 1.4 O P

Emas Kiara Dec 0.78 1.52 15.2 16.9 16.7 11.1 5.1 4.6 3.6 0.7 3.4 1.9 O P

Gamuda Jul 3.89 4.51 19.0 20.5 36.5 7.9 20.5 19.0 22.5 2.4 50.9 3.1 T B

MRCB Dec 2.08 2.49 6.4 6.7 23.5 4.9 32.6 31.1 20.3 2.1 20.4 0.0 T B

IJM^ Mar 5.42 5.01 32.6 34.2 2.7 5.0 16.6 15.8 9.0 1.3 8.7 2.0 U P

WCT Dec 3.24 2.30 16.9 17.4 -7.0 2.6 19.2 18.7 15.8 1.7 19.0 1.9 U P

Sector Avg 12.7 6.8 17.3 16.2

^ FY11-12valuations refer to those of FY12-FY13

Project Value

(RMm)

Potential Beneficiaries

Funded By Deve lopmen t Expend i t u re

Rural infrastructure 6,900

♦ Rural water & electricity in Sabah & Sarawak 2,700

♦ Rural roads in Sabah & Sarawak 2,100 East Malaysia-based contractors

♦ Rural roads in Peninsular Malaysia 696

♦ Rural water & electricity in Peninsular Malaysia 556

♦ Housing for rural hardcore poor 300

Building/upgrading of schools, hostels, facilities & equipment 6,400 Mid-sized contractors

Environmental preservation projects 1,900

♦ “River of Life” and greening of KL na YTL

♦ Preservation of marine sources and coastal areas in Melaka,Kelantan, Terengganu & Pahang

na Emas Kiara, MRCB

Corridor & regional development 850

♦ Iskandar Malaysia 339

♦ East Coast Economic Region (ECER) 178

♦ Northern Corridor Economic Region (NCER) 133

♦ Sabah Development Corridor 110

♦ Sarawak Corridor of Renewable Energy (SCORE) 93

Public housing 568

Aquaculture zones in Sabah & Sarawak 252 East Malaysia-based contractors

Drainage & irrigation in Muda Agriculture Development Area, Kedah 235

Basic infrastructure for swiftlet nets, aquaculture, seaweeds, ornamentalfish and herbs & spices ventures

135

Integrated eco-nature resort in Nexus Karambunai, Sabah 100 Karambunai

Hotels & resorts in remote areas 85

Diagnostic lab at Agriculture College in Kubang Pasu, Kedah 70

Shaded walkways in KLCC-Bukit Bintang area 50

Via Pub l i c-P r i va te Pa r tne rsh ip ( PPP) / P r iva te Inves tm en t

MRT in Greater KL 40,000 Gamuda, MMC

Kuala Lumpur International Financial District (KLIFD) 26,000 1MDB (Awarded), Mudabala(Awarded)

Development of Malaysia Rubber Board land in Sg Buloh 10,000 EPF (Awarded), MRCB

Warisan Merdeka integrated development with a 100-storey tower 5,000 PNB (Awarded)

Academic Medical Centre 2,000

Ampang-Cheras-Pandan Elevated Highway naGuthrie-Damansara Expressway na

Damansara-Petaling Jaya Highway na

Pantai Barat-Banting-Taiping Highway (West Coast Expressway) na Kumpulan Europlus, IJM

Sungai Dua-Juru Highway na

Paroi-Senawang-KLIA Highway na

300MW combined-cycle gas power plant in Kimanis, Sabah na Zelan, Mudajaya

International Islamic University Malaysia Teaching Hospital in Kuantan,

Pahang

na Ahmad Zaki (Awarded)

Women and Children’s Hospital in KL na Ranhill

Integrated Health Research Institute Complex in KL na

8/8/2019 The 2011 Budget : Setting The Pace Towards Transformation-15/10/2010

http://slidepdf.com/reader/full/the-2011-budget-setting-the-pace-towards-transformation-15102010 14/26

THE 2011 BUDGET14

A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

Consumer : NeutralNot As Exciting As Previous Budget

This time around, consumers did not get any new tax goodies from the

Government, although we believe there are some measures introduced which

would boost overall consumer spending in terms of promoting Malaysia as a

tourist destination and also to ease the burden of the rakyat:-

1. Import duty on approximately 300 goods preferred by tourists and locals, of

5% to 30% be abolished.

2. A continuation of a rebate on electricity bill payment for monthly consumption

of below RM20.

3. An extension to the current tax relief for parents to include other expenses

such as day care centre, cost incurred to employ caretaker for parents and

other daily needs such as diapers, from just medical treatments previously.

The tax relief amount is maintained at a maximum of RM5k.

4. Increasing the monthly allowance for various community leaders such as

Ketua Kampung, Imam etc. by 60-78%.

5. No increase in toll rates for the four highways owned by PLUS for the next

five years.

Aside from the above, the civil servants force, which comprises approximately

1.2m people, will benefit from:

1. A RM500 assistance for all civil servants grade 54 and below to cope with

schooling expenses.

2. Increasing the rate of Funeral Arrangement Assistance to RM3k from RM1k

previously. This is also extended to retired civil servants.

Although the measures introduced during the 2011 Budget is not as exciting as

the various income tax goodies introduced in the previous budget tabling, we

believe that all the measures above will, to a certain extent be a driver for

growth in consumer spending, as consumer disposable income is expected to

improve together with consumer sentiment. RHBRI projects a consumer spending

growth of 5.4% for 2011 (2010: 5.6%).

Retai l

These measures augur well for the retail and MLM players such as Parkson

(OP, FV=RM7.72), AEON (MP , FV=RM5.72), Amw ay (MP, FV=RM8.45), and

Hai-O (UP, FV=RM2.84) , as their revenues are generally driven by growth in

consumer spending. In particular, the abolishment of import duty on 300 various

products will be one of the key drivers for the retail players’ revenues (like

Parkson and AEON).

The Government also announced two non-quantitative policies which include: 1)

the establishment of a “1Malaysia Smart Consumer” portal to provide information

on price movements of goods in about 7k business premises nationwide; and 2)

introduction of the Retail Shop Transformation Programme (TUKAR), which will

be for the modernisation of small retailers (mom and pop stores). We believe

that the 1Malaysia Smart Consumer portal will increase consumer price sensitivity,

while the TUKAR programme would increase competition for department stores

cum supermarkets such as AEON’s Jusco as it gives the smaller players more

edge to compete with the bigger players.

F& B

The new policy which will affect F&B players is 1%-point increase to the current

5% service tax to 6%. This will increase KFCH’s (OP, FV=RM3.61) product

selling prices. However, we believe this will not have a significant impact on

demand, given that a 6% service tax will only increase the average sellingprices of KFCH’s products by 1%.

Basic food manufacturer QL Resources (OP, FV=RM5.41) will continue to

benefit from the extension of the food production tax incentive to 2015 and the

RM170m incentives allocated for fishermen. The incentives for fishermen will

Consumers did not get any

new tax goodies

Consumer spending growth

of 5.4% for 2011

Retail and MLM players to

benefit

Increase in Service Tax to

6%

QL Resources t o en j oy

various incentives for its

palm oil division

8/8/2019 The 2011 Budget : Setting The Pace Towards Transformation-15/10/2010

http://slidepdf.com/reader/full/the-2011-budget-setting-the-pace-towards-transformation-15102010 15/26

15THE 2011 BUDGET A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

ensure the sustainability of fish supply for its Marine Product Manufacturing

(MPM) division given that QL sources 95% of its fishes from local fishermen.

Besides the above incentives, QL’s palm oil division will benefit from the extension

of the application period for tax incentives for: 1) the generation of energy from

renewable sources; 2) energy conservation; and 3) reduction of greenhouse gas

emission to 2015. The palm oil division will benefit from these incentives given

its venture into renewable energy (RE) such as its palm pelletisers and biomass

boilers. Furthermore, the division will benefit from implementation of the FeedIn Tariff (FiT) mechanism under the RE Act, which allows QL to sell its RE

generated from its biomass plant to be sold to electricity utility companies. We

recently highlighted QL’s ultimate aim to manufacture a zero-waste palm oil

milling system to palm oil millers using its pelletising and biomass boiler

technology, which will be able to generate energy through palm oil wastes. QL’s

palm pelletisation is targeted to be commercialised by Dec 2010. The FiT will

further increase the attractiveness and marketability of this system, although we

are unable to gauge the impact of this yet, given the lack of details on the

incentives.

Brewery and Tobacco

The brewers enjoy another year of no increase in excise duty, which is positive

for Carlsberg (OP, FV=RM6.03). Note that the Government has not increased

excise duties on beer since the year 2005. Due to this, we expect that overall

Malt Liquor Market (MLM) TIV would not be affected in 2011, which is positive

for Carlsberg. We maintain our projected flat TIV growth of 0% for FY11. The

Government also did not introduce a subsequent hike in excise duty for cigarettes

after the increase of 16% earlier this month, nor did it mention anything regarding

the cess issue, which in the context of the 2011 Budget outcome, is positive for

BAT (UP , FV= RM42.90).

Heal thcare

As for the healthcare sector, the Government has committed to allocate RM15.2bn

in 2011 (vs. RM14.8bn in 2010) to construct new hospitals, increase the number

of doctors and nurses as well as to obtain supplies of medicines and equipment.Under the 10MP, out of the eight hospitals that will be built, four have been

identified, where two will be in Perak while the other two will be in Sabah. As

Faber (OP, RM=RM3.82) currently holds the concession agreement to provide

hospital support services in Perak and Sabah, it would likely benefit. However,

it would be dependent on whether Faber’s application for the concession is

renewed by the Government. Nevertheless, we maintain our view that the renewal

will likely be granted on the back of: 1) continuous effort by management to

improve its services; 2) Faber’s 14-year track record and technical expertise;

and 3) service benchmarks are consistently met without any unit price increase.

In addition, with more new government hospitals being built across Malaysia,

this could have an impact on private hospital operator KPJ (OP, FV=RM4.51).

Nevertheless, we expect this to be minimal due to Malaysia’s rising affluencetowards seeking better quality of care, greater uptake in medical insurance and

general dissatisfaction with the service of public hospitals.

Table 10Valuations Of Consumer Stocks

FYE Price Fair EPS EPS Gwth PER EV/ EBITDA P/ NTA P/ CF GDY Rec

Value (sen) (%) (x) (x) (x) (x) (%)

(RM/ s) (RM/ s) FY11 FY12 FY11 FY12 FY11 FY12 FY11 FY11 FY11 FY11

KFC Dec 3.26 3.61 22.5 26.1 16.7 15.7 14.5 12.5 7.3 1.6 10.7 2.1 O P

Carlsberg Dec 5.21 6.03 42.8 47.5 5.2 10.8 12.2 11.0 7.6 2.6 10.1 4.9 O P

KPJ Health Dec 3.55 4.51 26.6 29.9 10.7 12.2 13.3 11.9 7.8 1.6 10.5 4.5 O P

Parkson Jun 5.96 7.72 37.3 47.9 26.6 28.5 16.0 12.4 3.8 2.7 5.8 1.3 O P

Faber Dec 3.08 3.82 34.2 38.2 30.4 11.4 9.0 8.1 3.5 2.1 5.8 2.6 O P

QL Resources Mar 5.08 5.41 34.7 41.1 13.0 18.4 14.6 12.4 6.0 2.9 14.0 2.3 O P

Daibochi Dec 3.00 4.12 31.9 35.3 9.3 10.9 9.4 8.5 5.5 2.9 7.8 6.7 O PA E O N Dec 5.85 5.72 44.0 47.5 7.2 7.8 13.3 12.3 2.5 1.7 5.5 2.1 M P

Amway Dec 8.09 8.45 56.5 58.4 3.5 3.5 14.3 13.8 9.2 5.3 8.9 6.4 M P

Hai-O^ Apr 3.21 2.84 28.6 32.2 2.5 12.6 11.2 10.0 6.7 1.0 4.4 5.9 U P

B A T Dec 47.72 42.90 233.3 230.0 -7.8 -1.4 20.5 20.7 14.2 n.m 17.7 4.4 U P

Sector Avg 11.1 10.7 15.9 14.3

^ FY11-12valuations refer to those of FY12-FY13

Another year of cheer for

the brewers

8/8/2019 The 2011 Budget : Setting The Pace Towards Transformation-15/10/2010

http://slidepdf.com/reader/full/the-2011-budget-setting-the-pace-towards-transformation-15102010 16/26

THE 2011 BUDGET16

A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

Insurance : NeutralBudget Impact Not Significant

The 2011 Budget will not significantly impact the insurance sector given that there

were no new incentives introduced. However, indirectly, we believe that the insurance

sector will benefit from the various budget measures for other sectors to boost

economic activity. Heightened economic activities will provide opportunities for the

general insurers such as Allianz (OP, FV=RM5.32), LPI (UP, FV=11.40) and

Kurnia (MP, FV=RM0.44), to grow their other business segments such as workmen

compensation and marine, aviation and transit insurance. The sector will also benefit

from the government policy to make it mandatory for employers to procure health

insurance for their foreign workers as it would provide another avenue of premium

growth. For motor insurance, there was no update on the reform of the existing Third

Party Bodily Injury and Death (TPBID) policy.

For life insurance, no new measures were introduced that would boost the segment,

although we believe the new Private Pension Fund (PPF) that was introduced for the

private sector and self-employed workers could provide competition for life insurance

existing products. The PPF is an equivalent of the EPF and the RM6k tax incentive

for EPF contribution is also extended for the PPF.

Given that the measures introduced have limited impact for the sector, we are

maintaining our current forecasts and assumptions for all four insurance companies

under our coverage, i.e. Allianz, LPI, Kurnia, and MNRB (MP , FV=RM2.98).

No signif icant impact to

the sector

The new Private Pension

Fund (PPF ) cou l d pose

compet i t ion for the l i fe

insurance segment

Maintain Neutral

NeutralInfrastructure : Government Introduces Populist

Measures

Measure: To reduce transportation costs in the country, the Government announced

that the toll rates in the four highways owned by PLUS Expressways Berhad will not

be raised for the next five years, effective immediately.

Impact: We note that the toll hike freeze applies only to PLUS, while the other tollconcessionaires remain unaffected. However, no details on the form of compensation

to PLUS were forthcoming. While the announcement at first appears negative to

PLUS, we note that on the very same day itself, UEM and EPF together made a joint

offer to buy all the assets and liabilities of PLUS at an aggregate purchase consideration

of RM23bn or RM4.60 per share. We think the takeover offer is fair though not very

compelling given our fair value of RM4.76 (10% premium to NPV of RM4.60). Besides

that, the proposed takeover will essentially put aside any concern about the potential

adverse earnings impact of the toll hike freeze, which will be borne by UEM and EPF.

Toll hike freeze for next

five years

Table 12Valuations Of Insurance Stocks

FYE Price Fair EPS EPS Gwth PER EV/ EBITDA P/ NTA P/ CF GDY Rec

Value (sen) (%) (x) (x) (x) (x) (%)

(RM/ s) (RM/ s) FY11 FY12 FY11 FY12 FY11 FY12 FY11 FY11 FY11 FY11

Allianz Dec 4.11 5.32 86.2 99.7 19.9 15.8 4.8 4.1 -5.1 0.9 5.5 0.5 O P

MNRB^ Mar 2.74 2.98 19.5 29.5 -35.9 51.0 14.0 9.3 -36.0 0.6 12.0 3.6 M PKurnia Asia Dec 0.43 0.44 4.9 6.0 27.8 22.8 8.8 7.2 6.2 1.5 8.8 2.3 M P

LPI Capital Dec 11.70 11.40 70.2 82.9 12.4 18.0 16.7 14.1 10.8 1.5 2.8 5.9 U P

Sector Avg 8.7 21.5 8.6 7.1

^ FY11-12valuations refer to those of FY12-FY13

Table 11Valuations Of Infrastructure Stocks

FYE Price Fair EPS EPS Gwth PER EV/ EBITDA P/ NTA P/ CF GDY Rec

Value (sen) (%) (x) (x) (x) (x) (%)(RM/ s) (RM/ s) FY11 FY12 FY11 FY12 FY11 FY12 FY11 FY11 FY11 FY11

Puncak Dec 2.88 3.01 36.3 72.5 14.1 99.7 7.9 4.0 3.2 0.8 2.7 2.1 M P

PLUS Dec 4.46 4.60 37.4 38.0 52.7 1.8 11.9 11.7 8.7 3.2 9.7 4.5 U P

Sector Avg 49.0 9.0 11.6 10.7

8/8/2019 The 2011 Budget : Setting The Pace Towards Transformation-15/10/2010

http://slidepdf.com/reader/full/the-2011-budget-setting-the-pace-towards-transformation-15102010 17/26

17THE 2011 BUDGET A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

Motor : OverweightEnticing Hybrid Car Buyers

There was no mention of any incentives for the conventional passenger and commercial

car segments but the Government proposed to make do with the excise duty that

is currently being imposed for the hybrid cars. At present, we understand there are

only two hybrid car models in Malaysia – the Toyota Prius and the Honda Civic.

Previously, franchised holders of hybrid cars are given 100% exemption of import

duty and 50% exemption of excise duty on new completely-built-up (CBU) hybrid

cars until December 2010. The incentive was limited to new CBU hybrid passenger

cars with engine capacity below 2,000cc. This meant that hybrid car users previously

paid no import duty and around 40% of excise duty.

Table 13Duties And Taxes On Motor Vehicles

CBU & CKDEngine Capacity (cc)

Excise Duties (%) Sales Tax (%)

<1,800 75 10

1,800-1,999 80 10

2,000 -2,499 90 10

Above 2,500 105 10

Source: MAA

In the current Budget, the Government proposed that full exemption of import and

excise duties be given on new CBU hybrid cars, electric cars as well as hybrid and

electric motorcycles which applied with the Ministry of Finance from 1 January until

31 December 2011.

We gather that current on-the-road prices for the Toyota Prius and Honda Civic stand

at RM175k and RM130k respectively. With this incentive, prices could drop to RM141k

and RM111k respectively based on the Labuan prices (RM128k and RM101k

respectively) inclusive of the sales tax of 10%.

Overall, while the incentive is a big plus for interested hybrid car buyers, it will have

minimal impact on the total TIV of the industry, given its immaterial numbers thus

far. YTD TIV units for the Prius and Honda Civic Hybrid stand at 169 and 107

respectively. We reiterate our Overweight stance for the sector and maintain APM

Automotive as our top pick.

Full exemption of import

and excise duties ti l l 31

December 2011

Hybrid car pr ices could

potent ia l l y be pr i ced

14-19% lower

However, hybrid car unit

movements do l i t t l e to

change total TIV

Maintain Overweight call

on the sector

Table 14Valuations Of Motor Stocks

FYE Price Fair EPS EPS Gwth PER EV/ EBITDA P/ NTA P/ CF GDY Rec

Value (sen) (%) (x) (x) (x) (x) (%)

(RM/ s) (RM/ s) FY11 FY12 FY11 FY12 FY11 FY12 FY11 FY11 FY11 FY11

A P M Dec 4.85 5.53 50.3 57.2 7.0 13.8 9.7 8.5 3.0 1.2 5.2 2.7 O P

Proton^ Mar 4.87 5.50 75.2 80.3 11.6 6.8 6.5 6.1 7.2 0.5 n.m 0.0 O P

MBM Dec 3.17 5.30 48.2 50.7 5.3 5.0 6.6 6.3 14.3 0.7 14.8 3.8 O P

UMW Dec 6.75 7.27 59.2 66.3 7.2 11.9 11.4 10.2 5.3 1.7 7.9 3.6 M P

Tan Chong Dec 5.68 6.16 45.3 67.3 16.2 48.6 12.5 8.4 9.3 2.0 10.8 2.1 M P

Sector Avg 10.2 17.2 9.8 8.4

Sector Avg(ex-Proton) 9.69 20.8 11.01 9.1

^ FY11-12valuations refer to those of FY12-FY13

8/8/2019 The 2011 Budget : Setting The Pace Towards Transformation-15/10/2010

http://slidepdf.com/reader/full/the-2011-budget-setting-the-pace-towards-transformation-15102010 18/26

THE 2011 BUDGET18

A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

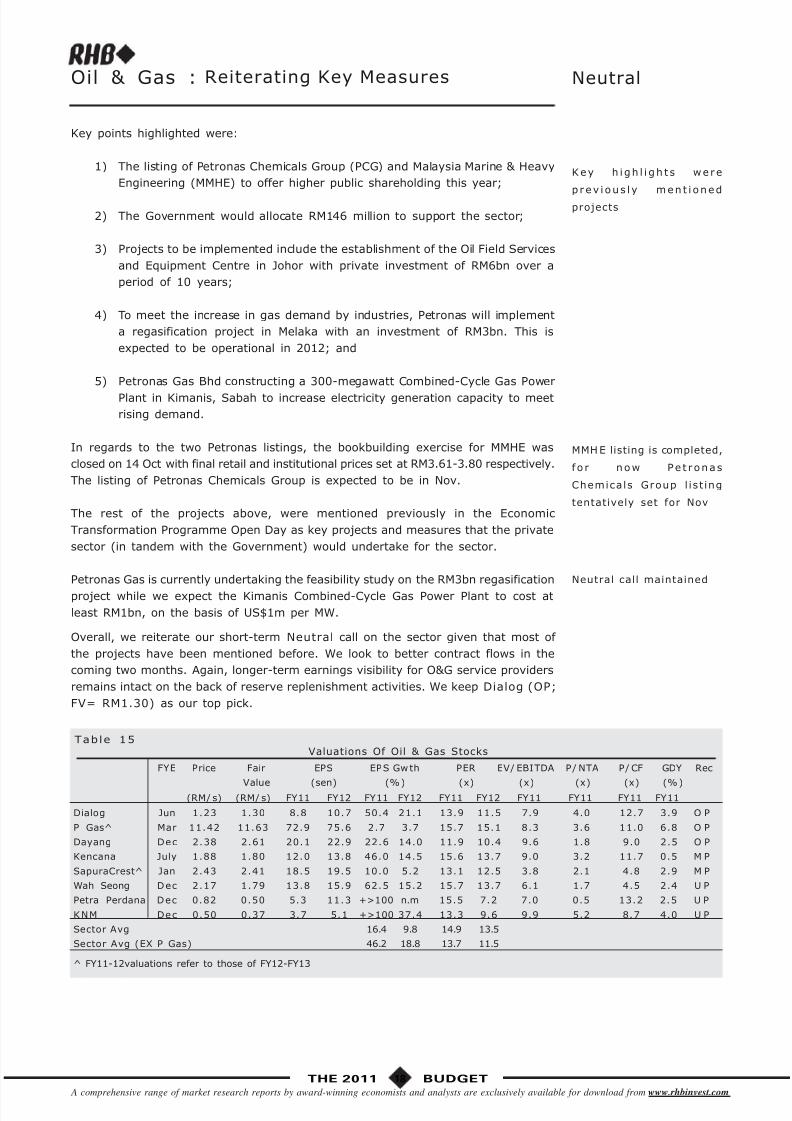

Oil & Gas : NeutralReiterating Key Measures

Key points highlighted were:

1) The listing of Petronas Chemicals Group (PCG) and Malaysia Marine & Heavy

Engineering (MMHE) to offer higher public shareholding this year;

2) The Government would allocate RM146 million to support the sector;

3) Projects to be implemented include the establishment of the Oil Field Services

and Equipment Centre in Johor with private investment of RM6bn over a

period of 10 years;

4) To meet the increase in gas demand by industries, Petronas will implement

a regasification project in Melaka with an investment of RM3bn. This is

expected to be operational in 2012; and

5) Petronas Gas Bhd constructing a 300-megawatt Combined-Cycle Gas Power

Plant in Kimanis, Sabah to increase electricity generation capacity to meet

rising demand.

In regards to the two Petronas listings, the bookbuilding exercise for MMHE was

closed on 14 Oct with final retail and institutional prices set at RM3.61-3.80 respectively.

The listing of Petronas Chemicals Group is expected to be in Nov.

The rest of the projects above, were mentioned previously in the Economic

Transformation Programme Open Day as key projects and measures that the private

sector (in tandem with the Government) would undertake for the sector.

Petronas Gas is currently undertaking the feasibility study on the RM3bn regasification

project while we expect the Kimanis Combined-Cycle Gas Power Plant to cost at

least RM1bn, on the basis of US$1m per MW.

Overall, we reiterate our short-term Neutral call on the sector given that most of

the projects have been mentioned before. We look to better contract flows in the

coming two months. Again, longer-term earnings visibility for O&G service providers

remains intact on the back of reserve replenishment activities. We keep Dialog (OP;

FV= RM1.30) as our top pick.

Key h i gh l i gh t s were

p rev i ous l y ment i oned

projects

MMHE listing is completed,

f o r now Pe t ronas

Chemicals Group l i s t ing

tentatively set for Nov

Neutral call maintained

Table 15Valuations Of Oil & Gas Stocks

FYE Price Fair EPS EPS Gwth PER EV/ EBITDA P/ NTA P/ CF GDY Rec

Value (sen) (%) (x) (x) (x) (x) (%)(RM/ s) (RM/ s) FY11 FY12 FY11 FY12 FY11 FY12 FY11 FY11 FY11 FY11

Dialog Jun 1.23 1.30 8.8 10.7 50.4 21.1 13.9 11.5 7.9 4.0 12.7 3.9 O P

P Gas^ Mar 11.42 11.63 72.9 75.6 2.7 3.7 15.7 15.1 8.3 3.6 11.0 6.8 O P

Dayang Dec 2.38 2.61 20.1 22.9 22.6 14.0 11.9 10.4 9.6 1.8 9.0 2.5 O P

Kencana July 1.88 1.80 12.0 13.8 46.0 14.5 15.6 13.7 9.0 3.2 11.7 0.5 M P

SapuraCrest^ Jan 2.43 2.41 18.5 19.5 10.0 5.2 13.1 12.5 3.8 2.1 4.8 2.9 M P

Wah Seong Dec 2.17 1.79 13.8 15.9 62.5 15.2 15.7 13.7 6.1 1.7 4.5 2.4 U P

Petra Perdana Dec 0.82 0.50 5.3 11.3 +>100 n.m 15.5 7.2 7.0 0.5 13.2 2.5 U P

KNM Dec 0.50 0.37 3.7 5.1 +>100 37.4 13.3 9.6 9.9 5.2 8.7 4.0 U P

Sector Avg 16.4 9.8 14.9 13.5

Sector Avg (EX P Gas) 46.2 18.8 13.7 11.5

^ FY11-12valuations refer to those of FY12-FY13

8/8/2019 The 2011 Budget : Setting The Pace Towards Transformation-15/10/2010

http://slidepdf.com/reader/full/the-2011-budget-setting-the-pace-towards-transformation-15102010 19/26

19THE 2011 BUDGET A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

Plantation : NeutralNo Exciting News

◆ There are not many new measures affecting the palm oil plantation sector in the

2011 Budget. Only two new proposals were made, including:

- (1) The encouragement of replanting activity to replace aged trees with

high quality new clones, through a fund of RM297m; and

- (2) A sum of RM127m to be allocated to support domestic oleo derivatives

companies as well as a sum of RM23.3m to expand downstream palm oil

industries including production of vitamins.

- As there were no details as to how the funds allocated will be distributed,

it is hard to gauge the impact of these measures. Firstly, we note that under

incentive (1), the fund of RM297m to encourage replanting activity is different

from the previous replanting incentive, where a sum of money is given to

planters for each hectare of land which is replanted. This time, the fund is

targeted to encourage replanting with high quality new clones, which could

mean that planters may get a subsidy for buying new clone seedlings from

government-backed research centres like MPOB. This, we believe, would

mainly benefit smaller companies and smallholders, who do not have their

own R&D division. Most of the companies under our coverage have their

own research centres and already develop their own high quality clones

which would be used for their new planting and replanting activities.

- Under incentive (2), again there is no clarity on how the sum of RM127m

is to be distributed to oleo derivatives companies. Assuming it is in the form

of a tax incentive, it would benefit companies like IOIC (OP, FV = RM6.75),

KLK (OP, FV = RM 22.05) and Sime Darby (MP , FV = RM9.40), as they

all have oleochemical manufacturing operations, although we would not be

able to quantify the impact given the lack of details. As for the RM23.3m

incentive to produce vitamins, this would likely benefit Carotech (Not Rated)

and KLK, as they produce nutraceuticals, which could be classified as a

form of vitamin.

◆ One measure which is not new, which was mentioned in the Budget, is the

mandatory implementation of the B5 biodiesel programme in Putrajaya, Kuala

Lumpur, Selangor, Negeri Sembilan and Melaka, starting from June 2011.

- This is not a new policy, as the Government first set out its Biofuel Policy

2006, with initial plans to commence nationwide implementation in 2010,

while the implementation deadline was pushed back to June 2011 back in

March 2010. Although the Government has since come up with a plan which

includes the RM43m instigation of depots with inline blending facilities to be

placed in Port Klang, the Klang Valley Distribution Terminal (KVDT) inSelangor, Port Dickson, Negri Sembilan and in Tangga Batu, Malacca, and

the rule that the costs of installing the blending terminals are to be borne

by the petroleum companies, it still has not come out with any details on

the B5 pricing issue. The only mention of pricing made by the Agriculture

Minister earlier in the year was to say that the price of biofuel under the

plan will not be fixed as it will oscillate depending on the price of palm oil

and diesel. If this is the case and pricing is based on market prices of CPO,

demand may not be too strong for the B5 blend, given the high price of

CPO currently at RM2,890/tonne.

◆ Other non-plantation related measures introduced in the Budget which

would affect some of the plantation companies include:

- Pioneer status and Investment Tax Allowance for the generation of energy

from renewable sources and energy efficiency activities for own consumption

and for sale be extended to 31 Dec 2015 (from 31 Dec 2010).

Tw o new m eas u re s

a f f e c t i ng p l an t a t i on

sector

Encouragement o f

rep lant ing ac t i v i t y to

replace aged trees with

high quality new clones…

… and R M127m to b e

a l l o ca t ed t o suppo r t

domestic oleo derivatives

companies

B5 biodiesel programme

mentioned again…

… but issue of pricing stil l

outstanding

Non-p l an t a t i on re l a t ed

measures like…

… t ax i ncen t i ves f o r

renewab l e ene rgy and

sa l e o f c a rbon c red i t s

extended…

8/8/2019 The 2011 Budget : Setting The Pace Towards Transformation-15/10/2010

http://slidepdf.com/reader/full/the-2011-budget-setting-the-pace-towards-transformation-15102010 20/26

THE 2011 BUDGET20

A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from www.rhbinvest.com

- Extension of tax incentive for reduction of greenhouse gas emission via the

sale of Certified Emission Reductions (CERs) to year of assessment 2012

(from YA 2010).

- We believe this is positive for CBIP (OP, FV = RM4.60) , who is in the

midst of developing and testing its zero discharge “green palm oil mill”,

which comes together with a biogas plant. Currently, four of these CPO

mills are being tested, two for Felda and two on its own premises. Although

the mill has not been commercialised yet, we believe once it is able to doso, it will be able to enjoy the tax incentives given not only for generating

renewable energy, but also for the sale of CERs.

◆ Overall, we believe the 2011 Budget is a slight positive for the plantation sector,

although the impact is not expected to be significant. We maintain our Neutral

stance on the sector, although we highlight selective stock picks which we have

Outperform recommendations on, including IOIC (FV = RM6.75), KLK

(FV=RM22.05), First Resources (FV = S$1.40) and CBIP (FV = RM4.60).

We maintain our Market Perform recommendations on Sime Darby (FV =

RM9.40) and IJMP ( FV = RM2.56) and our Underperform recommendation on

Genting Plantations (FV = RM7.40).

… which could be positive

for CBIP in the long term

Overa l l , s l i ght pos i t i ve

impact on sector, but not

significant

Table 16Valuations Of Plantation Stocks

FYE Price Fair EPS EPS Gwth PER EV/ EBITDA P/ NTA P/ CF GDY Rec

Value (sen) (%) (x) (x) (x) (x) (%)

(RM/ s) (RM/ s) FY11 FY12 FY11 FY12 FY11 FY12 FY11 FY11 FY11 FY11

KLK Sep 19.00 22.05 124.4 131.4 42.1 5.6 15.3 14.5 9.8 3.1 14.5 3.4 O P

IOI Corp Jun 5.80 6.75 33.6 34.9 28.3 3.8 17.3 16.6 12.0 3.3 15.3 2.9 O P