the 4 truths of indexed ul - imdrt.orgthe 4 truths of . indexed ul . ten x talks at the top . ......

TRANSCRIPT

Stephan Mitchell

The 4 Truths of Indexed UL

TEN X Talks at the Top Thursday, October 19, 2017, 12:45 pm

Investment and Insurance Products: Not a Deposit – Not FDIC Insured –Not Insured by any Federal Government Agency – No Bank Guarantee – May Lose Value

Pacific Life Insurance Company Newport Beach, CA 92660

(800) 800-7681 www.PacificLife.com

This material is not intended to be used, nor can it be used by any taxpayer, for the purpose of avoiding U.S. federal, state or local tax penalties. This material is written to support the promotion or marketing of the transaction(s) or matter(s) addressed by this material. Pacific Life, its affiliates, their distributors and respective representatives do not provide tax, accounting or legal advice. Any taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor or attorney.

Pacific Life is a product provider. It is not a fiduciary and therefore does not give advice or make recommendations regarding insurance or investment products.

Pacific Life’s individual life insurance products are marketed exclusively through independent third-party life insurance producers, which may include bank affiliated entities.

Pacific Life refers to Pacific Life Insurance Company and its affiliates, including Pacific Life & Annuity Company. Insurance products are issued by Pacific Life Insurance Company in all states except New York and in New York by Pacific Life & Annuity Company. Product availability and features may vary by state. Each insurance company is solely responsible for the financial obligations accruing under the products it issues. Insurance products and their guarantees, including optional benefits and any crediting rates, are backed by the financial strength and claims-paying ability of the issuing insurance company. Look to the strength of the life insurance company with regard to such guarantees as these guarantees are not backed by the broker-dealer, insurance agency, or their affiliates from which products are purchased. Neither these entities nor their representatives make any representation or assurance regarding the claims-paying ability of the life insurance company.

The S&P 500 Index is a product of S&P Dow Jones Indices LLC (“SPDJI”), and has been licensed for use by Pacific Life. S&P® and S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”); and these trademarks have been licensed for use by SPDJI and sublicensed for certain purposes by Pacific Life. Pacific Life product(s) are not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, their respective affiliates, and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions, or interruptions of the S&P 500 Index.

Pacific Life reserves the right to change or modify any non-guaranteed or current elements. The right to modify these elements is not limited to a specific time or reason.

Indexed Universal Life Insurance generally requires additional premium payments after the initial premium. If either no premiums are paid, or subsequent premiums are insufficient to continue coverage, it is possible that coverage will expire.

The indexed universal life products discussed in this presentation do not directly participate in any stock or equity investments. Failure to maintain the policy to maturity may result in no participation in the equity index.

Pacific Life & Annuity Company Newport Beach, CA 92660

(888) 595-6996 www.PacificLife.com

2 of 16For Financial Professional Use Only. Not For Use With The Public.

Indexed Universal Life(IUL)

• Industry Growth• Differentiators

• The Noble Truths

For Financial Professional Use Only. Not For Use With The Public.3 of 16

The Four IUL Truths1. A company can potentially

support a high cap rate at the expense of profits or enforce policy owners.

For Financial Professional Use Only. Not For Use With The Public.4 of 16

Many life insurance products have some flexibility in how they are structured. For example, death benefit coverage under certain products may be provided through a combination of the base policy and any available term or other riders. Each policy selected, illustrated, and sold should be structured based upon your client’s particular insurance needs and financial objectives. It is your responsibility to know that the particular policy selected, illustrated, and sold will meet your client’s needs and objectives.

Competitor information presented based on illustrations received directly from the company. While we believe it is accurate, we cannot assure you that this is the most current information. Please contact the company for a current product information.

Additional competitor and product information can be found on slide 16 for slides 8-9 and 13-14.

5 of 16

Example of Inforce IUL versus Currently Sold IUL Current Indexed Account Growth Caps for 1-Year S&P 500 Point-to-Point

Accounts*

14.00%10.50% 12.00%

9.00%10.50%

8.75%

For Financial Professional Use Only. Not For Use With The Public.6 of 16

*SOURCE: Pacific Life Competition Unit Survey, January 2016 (inforce); Product information listed on Slide 16.

Company A Company CPacific Life

The Four IUL Truths

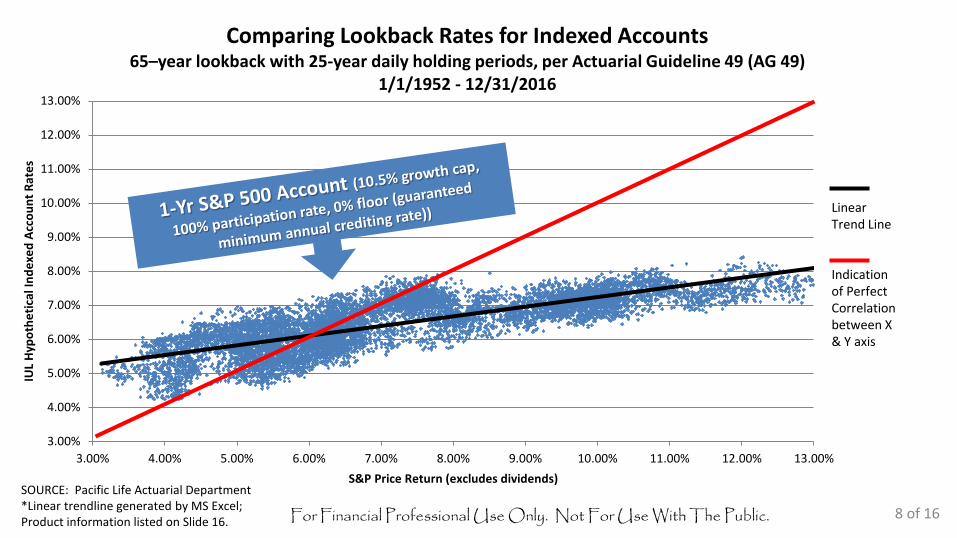

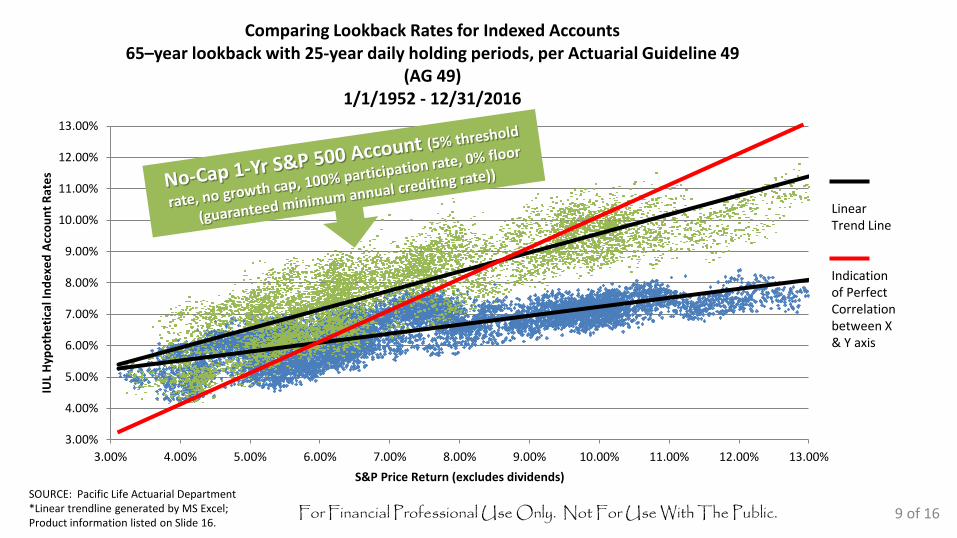

2. To potentially increase indexed crediting rates in an IUL, consider a multi-year account or a threshold account.

For Financial Professional Use Only. Not For Use With The Public.7 of 16

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

11.00%

12.00%

13.00%

3.00% 4.00% 5.00% 6.00% 7.00% 8.00% 9.00% 10.00% 11.00% 12.00% 13.00%

IUL

Hypo

thet

ical

Inde

xed

Acco

unt R

ates

S&P Price Return (excludes dividends)

Comparing Lookback Rates for Indexed Accounts65–year lookback with 25-year daily holding periods, per Actuarial Guideline 49 (AG 49)

1/1/1952 - 12/31/2016

8 of 16SOURCE: Pacific Life Actuarial Department*Linear trendline generated by MS Excel; Product information listed on Slide 16. For Financial Professional Use Only. Not For Use With The Public.

Linear Trend Line

Indication of Perfect Correlation between X & Y axis

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

11.00%

12.00%

13.00%

3.00% 4.00% 5.00% 6.00% 7.00% 8.00% 9.00% 10.00% 11.00% 12.00% 13.00%

IUL

Hypo

thet

ical

Inde

xed

Acco

unt R

ates

S&P Price Return (excludes dividends)

Comparing Lookback Rates for Indexed Accounts65–year lookback with 25-year daily holding periods, per Actuarial Guideline 49

(AG 49)1/1/1952 - 12/31/2016

9 of 16SOURCE: Pacific Life Actuarial Department*Linear trendline generated by MS Excel; Product information listed on Slide 16.

For Financial Professional Use Only. Not For Use With The Public.

Linear Trend Line

Indication of Perfect Correlation between X & Y axis

The Four IUL Truths

3. Service and performance are potentially more important than a high current cap rate.

For Financial Professional Use Only. Not For Use With The Public.10 of 16

IUL Policy Tracking Report (available in Planned Performance Tracking (PPT))

11 of 16For Financial Professional Use Only. Not For Use With The Public.

The Four IUL Truths

4. Ling Jou Shi Fou.*

For Financial Professional Use Only. Not For Use With The Public.12 of 16

*Literally, in Chinese, “Zero is beautiful”

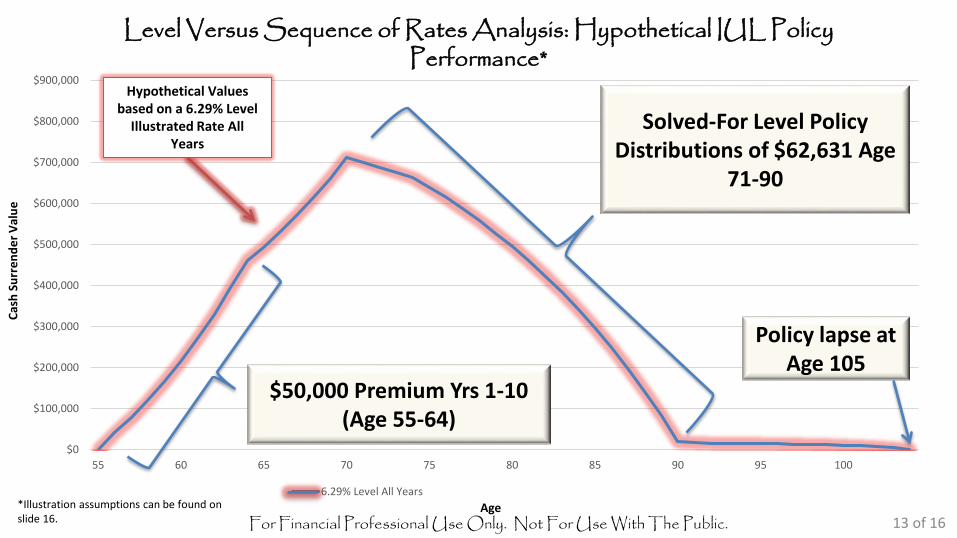

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000

55 60 65 70 75 80 85 90 95 100

6.29% Level All Years Sequence of Rates that Averages 6.29%*

Level Versus Sequence of Rates Analysis: Hypothetical IUL Policy Performance*

Age

Cash

Sur

rend

er V

alue

Solved-For Level Policy Distributions of $62,631 Age

71-90

For Financial Professional Use Only. Not For Use With The Public. 13 of 16

Hypothetical Values based on a 6.29% Level

Illustrated Rate All Years

$50,000 Premium Yrs 1-10(Age 55-64)

Policy lapse at Age 105

*Illustration assumptions can be found on slide 16.

$286,169

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000

55 60 65 70 75 80 85 90 95 100

6.29% Level All Years Sequence of Rates that Averages 6.29%*

Hypothetical values based on the rate sequence

that averaged out to

6.29%*

Age

Cash

Sur

rend

er V

alue

For Financial Professional Use Only. Not For Use With The Public. 14 of 16

Level Versus Sequence of Rates Analysis: Hypothetical IUL Policy Performance**

*25-year rate sequences are applied two times back-to-back to produce 50 years of rates for the illustration.**Illustration assumptions can be found on slide 16.

The Four IUL Truths

Cap RatesMulti-Year and Threshold Accounts

Service, Service, ServiceThe Floor

15 of 4215 of 16For Financial Professional Use Only. Not For Use With The Public.

Company InforceProduct

Policy Form No.*

Guaranteed Growth Cap Rate

Currently Sold Product

Policy Form No. Guaranteed Growth Cap Rate

Company A (F&G/Old Mutual) MasterChoice FGL EIUL-C (4-03) 1.00% Elite II ICC12-LPI1061(07-12) 1.00%Company C (Global Atlantic/AmerUs /Accordia)

Vision/Liberty/Advantage Builder 2WSCJ07 4.00% Lifetime Builder III IULA-E14-CRT 3.00%

Pacific Life Insurance Company

Pacific Indexed Accumulator P05PIA 3.00%

Pacific Indexed Performer LT2

P15IUL and S15PIAP or ICC15 P15IUL and ICC15 S15PIAP, based on state of policy issue. 3.00%

For Financial Professional Use Only. Not For Use With The Public.

Pacific Life Insurance Company Newport Beach, CA 92660

(800) 800-7681 www.PacificLife.com

Pacific Life & Annuity Company Newport Beach, CA 92660

(888) 595-6996 www.PacificLife.com

*Products no longer available for sale. The Threshold Rate (5% current, 20% guaranteed) is subtracted from the performance of a segment's underlying index to determine the crediting rate.Slides 7-8: Scatter graph data based on Actuarial Guideline 49 methodology (65-Yr lookback (1952-2016)) measuring 10,054 25-Yr holding period compound rates for hypothetical indexed accounts and how they correlate to the S&P price index. These hypothetical returns are only intended to demonstrate the mechanics of an indexed universal life insurance policy, and is not a prediction of how an indexed UL might have operated had it existed over the period depicted above. The actual historical growth cap and growth floor of an indexed life insurance product existing over the period depicted may have been higher or lower than assumed, and likely would have fluctuated subject to product guarantees. Historical returns are no guarantee of future performance. Pacific Life’s first Indexed Account was introduced in September 2005.Slide 13-14 Assumptions: Pacific Life Insurance Company’s Pacific Indexed Performer – LT2 (PIP-LT2, Policy Form #P15IUL and S15PIAP or ICC15 P15IUL and ICC15 S15PIAP, based on state of policy issue, Male, Age 55, Preferred Nonsmoker, $50,000 Premium Yrs 1-10, No Premiums or Distributions Ages 66-70, Minimum Level Death Benefit ($1,401,575), 100% allocation to 1-Yr Indexed Account with 10.5% cap, 0% floor, 100% participation rate. Solve for level policy distributions (withdrawal to basis then switch to standard loans) from Age 71-90. Varying rate assumptions: The following rate sequence was assumed and run two times consecutively: 0%, 0%, 10.50%, 10.50%, 0%, 0%, 10.50%, 10.50%, 0%, 9.54%, 10.50%, 10.50%, 0%, 10.50%, 10.50%, 0.21%, 10.50%, 10.50%, 0%, 10.50%, 10.50%, 0%, 10.50%, 3.36%, 10.50%. After age 104, an illustrated rate of 6.29% was assumed. Distributions of $62,631 from Age 71-90. Both the level and varying rate illustrations assume 100% Basic Coverage.

16 of 1616-124APT-44915-01 8/17