the abacus prompt™ - abacusconsulting | your ... abacu… · chemicals financial services...

TRANSCRIPT

The Abacus Prompt™ Monthly Business Review – Pakistan

November 2012

Nov 2012

Issue 23, Vol. 2

Page 1

Your Transformation Partner

Consulting | Technology | Outsourcing

KSE-100 Index Performance

Nov 1 15,910 4.17%

Nov 30 16,574

KSE

Market Cap - (PKR Billion) Nov 1 3,965

4.72% Nov 30 4,152

KSE 100

Best Performing Stocks

Company Opening Price Closing Price Change

GRAYS 29.5 54.8 85.7% PICT

PCAL

150.0 206.0 37.4%

EFOODS

70.2 87.6 24.7%

IDYM 492.4 607.0 23.4%

SHFA 38.0 45.7 20.4%

KSE 100

Worst Performing Stocks Company Opening Price Closing Price Change

MUREB 177.4 160 -9.8% FFBL

39.23 36.05 -8.1%

MDTL 5.35 4.99 -6.7%

PCAL 53 49.74 -6.2%

EFUG 92.92 87.29 -6.1%

Top Picks (Stocks Offering Maximum Upside Potential)

Company Closing Price Target Price Potential

AH

L PTC 18.09 32.5 79.7%

FCCL 6.95 12.2 75.5%

KOHC 63.04 107.0 69.7%

KA

SB

PSO 225.8 266.9 18.2%

PTC 18.1 21.0 16.1%

PPL 174.8 203.0 16.1%

AK

D ENGRO 96.11 207.6 114.9%

PTC 18.09 37.7 108.4%

PSMC 86.26 124.8 44.7%

AFS*

NRL 210.01 342.96 63.3%

PPL 174.84 253.37 44.9%

SSGC 20.99 28.45 35.5%

Source: Abacus Research, KSE *Top picks reported as on 31st Oct’12

Stock Market

The KSE-100 index witnessed a bullish trend during Nov with the market closing 4.17% higher MoM. Average daily volumes were noted to be 216mn shares, up by 74% MoM, and value traded was also up by 19% MoM. Expectations for potential discount rate cuts in Dec added to the enthusiasm of investors despite the weakening of the PKR, while the recomposed free-float based KSE-100 index provided comfort that volatility would be kept in check. LHC’s decision on Kalabagh dam favored cement sector investments, while uncertainty over urea pricing and gas outages weakened fertilizer stocks. Reduction in age of imported cars (from 5 to 3 years) added to investor’s activity in autos sector. Unilever announced its decision to delist Unilever Pakistan and buy back shares at the price of PKR 9700, implying a potential investment inflow of USD 335mn. FPI, however, was down by 10% MoM at USD34.6mn, largely attributable to worsening law and order perception in Karachi and other cities with the advent of Muharram though it could not dampen the market’s positive thrust.

Pakistan’s equity market performed well as compared to the regional peers as 2

nd top performer on MoM basis and top performer on YTD basis.

Source: Bloomberg

‘Construction and Materials’ was the highest traded sector for Nov, accounting for almost 30% of the total turnover.

The highest traded individual stock was FCCL with a total of 604 million shares traded followed by MLCF for the month of Nov.

Source: KSE

-4.0% -4.0%

1.0%2.0% 2.0%

4.0% 5.0%

-5.0%

0.0%

5.0%

10.0% Regional Comparison

Malaysia China Singapore Thailand HongKong Pakistan India

8.09% 9.75% 11.79% 13.95%

30.01%

Highest Traded Sector (% of Total Turnover)

Chemicals Financial Services Commercial Banks Textile Construction and Materials

182 190265 286

604

Highest Traded Stocks on KSE (Million Shares)

DGKC ANL JSCL MLCF FCCL

Nov 2012

Issue 23, Vol. 2

Page 2

The Abacus Prompt™

Monthly Business Review - Pakistan

The Abacus Prompt™ The Abacus Prompt™ The Abacus Prompt™

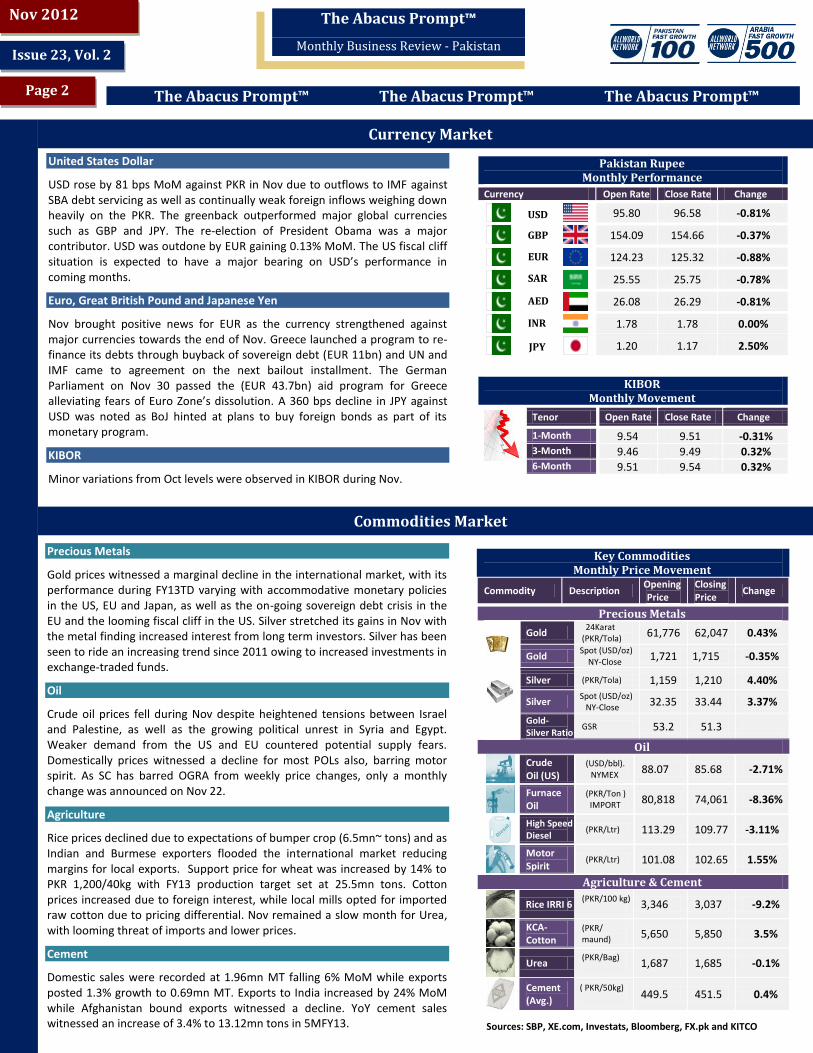

Pakistan Rupee Monthly Performance

Currency Open Rate Close Rate Change

95.80 96.58 -0.81%

154.09 154.66 -0.37%

124.23 125.32 -0.88%

25.55 25.75 -0.78%

26.08 26.29 -0.81%

1.78 1.78 0.00%

1.20 1.17 2.50%

KIBOR Monthly Movement

Tenor Open Rate Close Rate Change

1-Month 9.54 9.51 -0.31% 3-Month 9.46 9.49 0.32% 6-Month 9.51 9.54 0.32%

Key Commodities Monthly Price Movement

Commodity Description Opening Price

Closing Price

Change

Precious Metals

Gold

24Karat (PKR/Tola)

61,776 62,047 0.43%

Gold Spot (USD/oz) NY-Close 1,721 1,715 -0.35%

Silver (PKR/Tola) 1,159 1,210 4.40%

Silver Spot (USD/oz)

NY-Close 32.35 33.44 3.37%

Gold- Silver Ratio

GSR 53.2 51.3

Oil

Crude Oil (US)

(USD/bbl). NYMEX 88.07 85.68 -2.71%

Furnace Oil

(PKR/Ton ) IMPORT 80,818 74,061 -8.36%

High Speed Diesel

(PKR/Ltr) 113.29 109.77 -3.11%

Motor Spirit

(PKR/Ltr) 101.08 102.65 1.55%

Agriculture & Cement

Rice IRRI 6

(PKR/100 kg)

3,346 3,037 -9.2%

KCA- Cotton

(PKR/ maund) 5,650 5,850 3.5%

Urea

(PKR/Bag)

1,687 1,685 -0.1%

Cement (Avg.)

( PKR/50kg)

449.5 451.5 0.4%

Currency Market

United States Dollar

USD rose by 81 bps MoM against PKR in Nov due to outflows to IMF against SBA debt servicing as well as continually weak foreign inflows weighing down heavily on the PKR. The greenback outperformed major global currencies such as GBP and JPY. The re-election of President Obama was a major contributor. USD was outdone by EUR gaining 0.13% MoM. The US fiscal cliff situation is expected to have a major bearing on USD’s performance in coming months.

Euro, Great British Pound and Japanese Yen

Nov brought positive news for EUR as the currency strengthened against major currencies towards the end of Nov. Greece launched a program to re-finance its debts through buyback of sovereign debt (EUR 11bn) and UN and IMF came to agreement on the next bailout installment. The German Parliament on Nov 30 passed the (EUR 43.7bn) aid program for Greece alleviating fears of Euro Zone’s dissolution. A 360 bps decline in JPY against USD was noted as BoJ hinted at plans to buy foreign bonds as part of its monetary program.

KIBOR

Minor variations from Oct levels were observed in KIBOR during Nov.

Commodities Market

Precious Metals

Gold prices witnessed a marginal decline in the international market, with its performance during FY13TD varying with accommodative monetary policies in the US, EU and Japan, as well as the on-going sovereign debt crisis in the EU and the looming fiscal cliff in the US. Silver stretched its gains in Nov with the metal finding increased interest from long term investors. Silver has been seen to ride an increasing trend since 2011 owing to increased investments in exchange-traded funds.

Oil

Crude oil prices fell during Nov despite heightened tensions between Israel and Palestine, as well as the growing political unrest in Syria and Egypt. Weaker demand from the US and EU countered potential supply fears. Domestically prices witnessed a decline for most POLs also, barring motor spirit. As SC has barred OGRA from weekly price changes, only a monthly change was announced on Nov 22.

Agriculture

Rice prices declined due to expectations of bumper crop (6.5mn~ tons) and as Indian and Burmese exporters flooded the international market reducing margins for local exports. Support price for wheat was increased by 14% to PKR 1,200/40kg with FY13 production target set at 25.5mn tons. Cotton prices increased due to foreign interest, while local mills opted for imported raw cotton due to pricing differential. Nov remained a slow month for Urea, with looming threat of imports and lower prices.

Cement

Domestic sales were recorded at 1.96mn MT falling 6% MoM while exports posted 1.3% growth to 0.69mn MT. Exports to India increased by 24% MoM while Afghanistan bound exports witnessed a decline. YoY cement sales witnessed an increase of 3.4% to 13.12mn tons in 5MFY13.

USD

JPY

EUR

SAR

AED

INR

GBP

Sources: SBP, XE.com, Investats, Bloomberg, FX.pk and KITCO

Nov 2012

Issue 23, Vol. 2

Page 3

The Abacus Prompt™

Monthly Business Review - Pakistan

The Abacus Prompt™ The Abacus Prompt™ The Abacus Prompt™

Economy of Pakistan

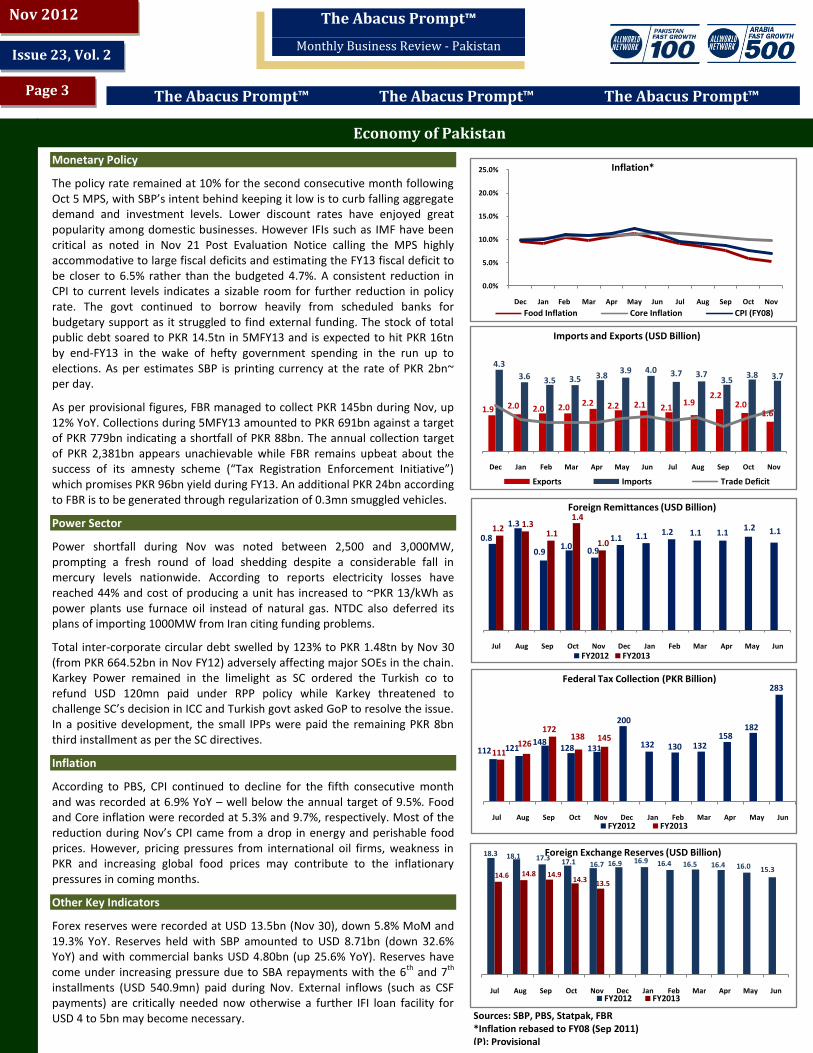

Sources: SBP, PBS, Statpak, FBR *Inflation rebased to FY08 (Sep 2011) (P): Provisional

Monetary Policy

The policy rate remained at 10% for the second consecutive month following Oct 5 MPS, with SBP’s intent behind keeping it low is to curb falling aggregate demand and investment levels. Lower discount rates have enjoyed great popularity among domestic businesses. However IFIs such as IMF have been critical as noted in Nov 21 Post Evaluation Notice calling the MPS highly accommodative to large fiscal deficits and estimating the FY13 fiscal deficit to be closer to 6.5% rather than the budgeted 4.7%. A consistent reduction in CPI to current levels indicates a sizable room for further reduction in policy rate. The govt continued to borrow heavily from scheduled banks for budgetary support as it struggled to find external funding. The stock of total public debt soared to PKR 14.5tn in 5MFY13 and is expected to hit PKR 16tn by end-FY13 in the wake of hefty government spending in the run up to elections. As per estimates SBP is printing currency at the rate of PKR 2bn~ per day.

As per provisional figures, FBR managed to collect PKR 145bn during Nov, up 12% YoY. Collections during 5MFY13 amounted to PKR 691bn against a target of PKR 779bn indicating a shortfall of PKR 88bn. The annual collection target of PKR 2,381bn appears unachievable while FBR remains upbeat about the success of its amnesty scheme (“Tax Registration Enforcement Initiative”) which promises PKR 96bn yield during FY13. An additional PKR 24bn according to FBR is to be generated through regularization of 0.3mn smuggled vehicles.

Power Sector

Power shortfall during Nov was noted between 2,500 and 3,000MW, prompting a fresh round of load shedding despite a considerable fall in mercury levels nationwide. According to reports electricity losses have reached 44% and cost of producing a unit has increased to ~PKR 13/kWh as power plants use furnace oil instead of natural gas. NTDC also deferred its plans of importing 1000MW from Iran citing funding problems.

Total inter-corporate circular debt swelled by 123% to PKR 1.48tn by Nov 30 (from PKR 664.52bn in Nov FY12) adversely affecting major SOEs in the chain. Karkey Power remained in the limelight as SC ordered the Turkish co to refund USD 120mn paid under RPP policy while Karkey threatened to challenge SC’s decision in ICC and Turkish govt asked GoP to resolve the issue. In a positive development, the small IPPs were paid the remaining PKR 8bn third installment as per the SC directives.

Inflation

According to PBS, CPI continued to decline for the fifth consecutive month and was recorded at 6.9% YoY – well below the annual target of 9.5%. Food and Core inflation were recorded at 5.3% and 9.7%, respectively. Most of the reduction during Nov’s CPI came from a drop in energy and perishable food prices. However, pricing pressures from international oil firms, weakness in PKR and increasing global food prices may contribute to the inflationary pressures in coming months.

Other Key Indicators

Forex reserves were recorded at USD 13.5bn (Nov 30), down 5.8% MoM and 19.3% YoY. Reserves held with SBP amounted to USD 8.71bn (down 32.6% YoY) and with commercial banks USD 4.80bn (up 25.6% YoY). Reserves have come under increasing pressure due to SBA repayments with the 6th and 7th installments (USD 540.9mn) paid during Nov. External inflows (such as CSF payments) are critically needed now otherwise a further IFI loan facility for USD 4 to 5bn may become necessary.

1.9 2.0 2.0 2.0 2.2 2.2 2.1 2.11.9

2.22.0

1.6

4.3

3.6 3.5 3.5 3.83.9 4.0 3.7 3.7

3.53.8 3.7

Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov

Imports and Exports (USD Billion)

Exports Imports Trade Deficit

0.8

1.3

0.9 1.0 0.9

1.1 1.1 1.2 1.1 1.1 1.2 1.1 1.2 1.3

1.1

1.4

1.0

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun

Foreign Remittances (USD Billion)

FY2012 FY2013

112 121 148

128 131

200

132 130 132 158

182

283

111 126

172 138 145

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun

Federal Tax Collection (PKR Billion)

FY2012 FY2013

18.3 18.1 17.3 17.1 16.7 16.9 16.9 16.4 16.5 16.4 16.0 15.3 14.6 14.8 14.9

14.3 13.5

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun

Foreign Exchange Reserves (USD Billion)

FY2012 FY2013

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov

Inflation*

Food Inflation Core Inflation CPI (FY08)

Nov 2012

Issue 23, Vol. 2

Page 4

The Abacus Prompt™

Monthly Business Review - Pakistan

The Abacus Prompt™ The Abacus Prompt™ The Abacus Prompt™

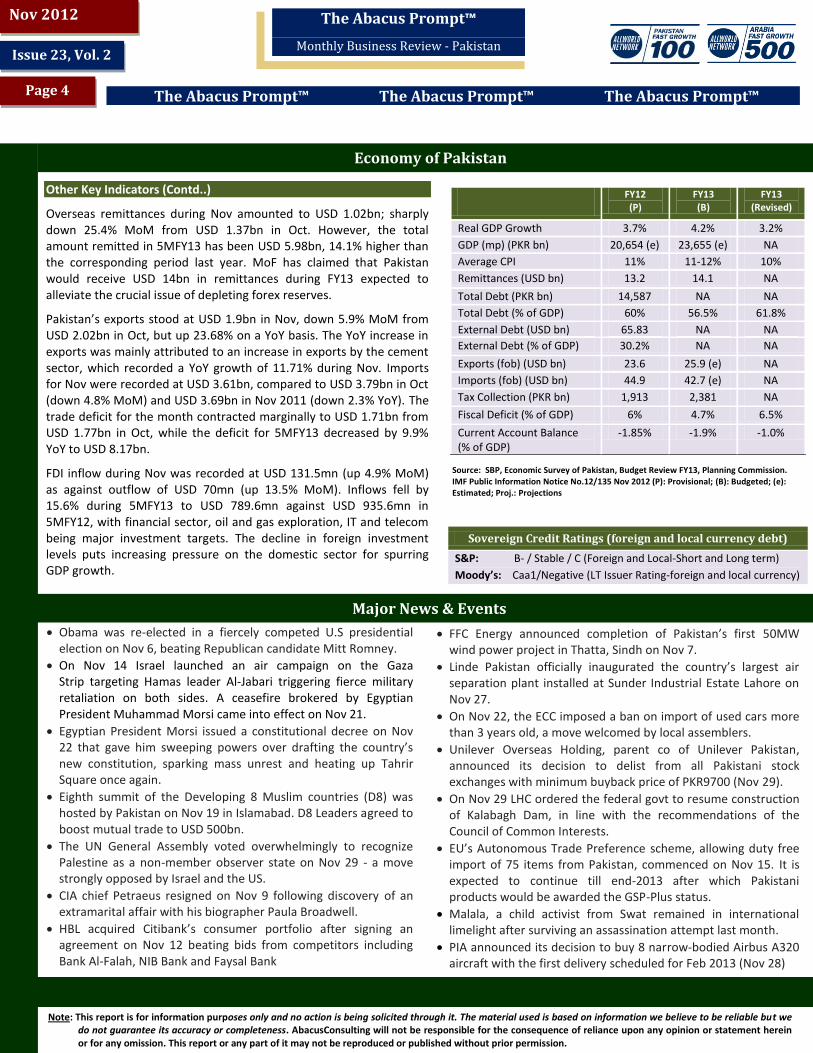

FY12

(P) FY13 (B)

FY13 (Revised)

Real GDP Growth 3.7% 4.2% 3.2%

GDP (mp) (PKR bn) 20,654 (e) 23,655 (e) NA

Average CPI 11% 11-12% 10%

Remittances (USD bn) 13.2 14.1 NA

Total Debt (PKR bn) 14,587 NA NA

Total Debt (% of GDP) 60% 56.5% 61.8%

External Debt (USD bn) 65.83 NA NA

External Debt (% of GDP) 30.2% NA NA

Exports (fob) (USD bn) 23.6 25.9 (e) NA

Imports (fob) (USD bn) 44.9 42.7 (e) NA

Tax Collection (PKR bn) 1,913 2,381 NA

Fiscal Deficit (% of GDP) 6% 4.7% 6.5%

Current Account Balance (% of GDP)

-1.85% -1.9% -1.0%

Sovereign Credit Ratings (foreign and local currency debt)

S&P: B- / Stable / C (Foreign and Local-Short and Long term)

Moody’s: Caa1/Negative (LT Issuer Rating-foreign and local currency)

Economy of Pakistan

Major News & Events

Source: SBP, Economic Survey of Pakistan, Budget Review FY13, Planning Commission. IMF Public Information Notice No.12/135 Nov 2012 (P): Provisional; (B): Budgeted; (e): Estimated; Proj.: Projections

Sovereign Credit Ratings (foreign and local currency debt):

Standard & Poor’s: B-/ Stable/ C Moody’s: B3 – Stable (foreign and local currency debt)

(P=Provisional, B=Budgeted)

Other Key Indicators (Contd..)

Overseas remittances during Nov amounted to USD 1.02bn; sharply down 25.4% MoM from USD 1.37bn in Oct. However, the total amount remitted in 5MFY13 has been USD 5.98bn, 14.1% higher than the corresponding period last year. MoF has claimed that Pakistan would receive USD 14bn in remittances during FY13 expected to alleviate the crucial issue of depleting forex reserves.

Pakistan’s exports stood at USD 1.9bn in Nov, down 5.9% MoM from USD 2.02bn in Oct, but up 23.68% on a YoY basis. The YoY increase in exports was mainly attributed to an increase in exports by the cement sector, which recorded a YoY growth of 11.71% during Nov. Imports for Nov were recorded at USD 3.61bn, compared to USD 3.79bn in Oct (down 4.8% MoM) and USD 3.69bn in Nov 2011 (down 2.3% YoY). The trade deficit for the month contracted marginally to USD 1.71bn from USD 1.77bn in Oct, while the deficit for 5MFY13 decreased by 9.9% YoY to USD 8.17bn.

FDI inflow during Nov was recorded at USD 131.5mn (up 4.9% MoM) as against outflow of USD 70mn (up 13.5% MoM). Inflows fell by 15.6% during 5MFY13 to USD 789.6mn against USD 935.6mn in 5MFY12, with financial sector, oil and gas exploration, IT and telecom being major investment targets. The decline in foreign investment levels puts increasing pressure on the domestic sector for spurring GDP growth.

Note: This report is for information purposes only and no action is being solicited through it. The material used is based on information we believe to be reliable but we do not guarantee its accuracy or completeness. AbacusConsulting will not be responsible for the consequence of reliance upon any opinion or statement herein or for any omission. This report or any part of it may not be reproduced or published without prior permission.

FFC Energy announced completion of Pakistan’s first 50MW wind power project in Thatta, Sindh on Nov 7.

Linde Pakistan officially inaugurated the country’s largest air separation plant installed at Sunder Industrial Estate Lahore on Nov 27.

On Nov 22, the ECC imposed a ban on import of used cars more than 3 years old, a move welcomed by local assemblers.

Unilever Overseas Holding, parent co of Unilever Pakistan, announced its decision to delist from all Pakistani stock exchanges with minimum buyback price of PKR9700 (Nov 29).

On Nov 29 LHC ordered the federal govt to resume construction of Kalabagh Dam, in line with the recommendations of the Council of Common Interests.

EU’s Autonomous Trade Preference scheme, allowing duty free import of 75 items from Pakistan, commenced on Nov 15. It is expected to continue till end-2013 after which Pakistani products would be awarded the GSP-Plus status.

Malala, a child activist from Swat remained in international limelight after surviving an assassination attempt last month.

PIA announced its decision to buy 8 narrow-bodied Airbus A320 aircraft with the first delivery scheduled for Feb 2013 (Nov 28)

Obama was re-elected in a fiercely competed U.S presidential election on Nov 6, beating Republican candidate Mitt Romney.

On Nov 14 Israel launched an air campaign on the Gaza Strip targeting Hamas leader Al-Jabari triggering fierce military retaliation on both sides. A ceasefire brokered by Egyptian President Muhammad Morsi came into effect on Nov 21.

Egyptian President Morsi issued a constitutional decree on Nov 22 that gave him sweeping powers over drafting the country’s new constitution, sparking mass unrest and heating up Tahrir Square once again.

Eighth summit of the Developing 8 Muslim countries (D8) was hosted by Pakistan on Nov 19 in Islamabad. D8 Leaders agreed to boost mutual trade to USD 500bn.

The UN General Assembly voted overwhelmingly to recognize Palestine as a non-member observer state on Nov 29 - a move strongly opposed by Israel and the US.

CIA chief Petraeus resigned on Nov 9 following discovery of an extramarital affair with his biographer Paula Broadwell.

HBL acquired Citibank’s consumer portfolio after signing an agreement on Nov 12 beating bids from competitors including Bank Al-Falah, NIB Bank and Faysal Bank