the african development bank financial management

TRANSCRIPT

7170

African Development Bank Chapter 005

Annual Report 2007 7170

This chapter discusses the management of the financial resources of the Bank Group’s windows—the African Development Bank (ADB), the African Development Fund (ADF), and the Nigeria Trust Fund (NTF)—during the year. It also presents the Audited Financial Statements for 2007 for the three windows, as well as the ADB and ADF Administrative Budgets for the financial year 2008.

tHE AfRICAN dEVELOPMENt bANK

financial Management

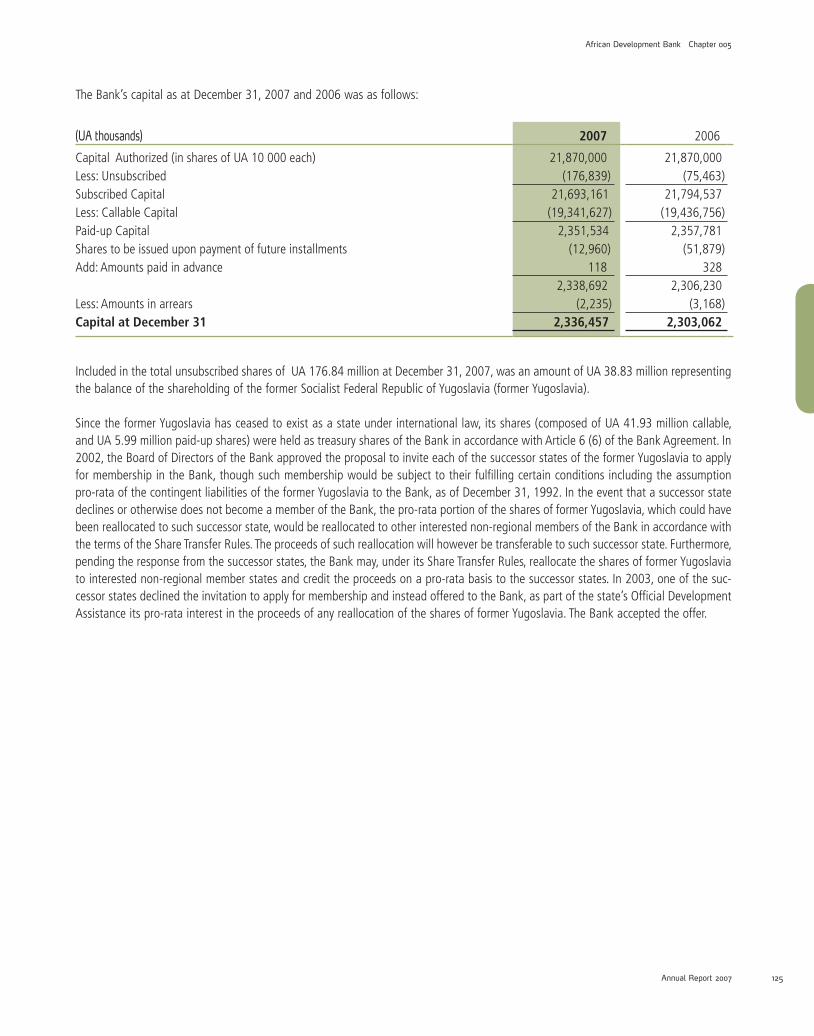

Capital SubscriptionThe authorized capital stock of the Bank stood at UA 21.87 billion as of December 31, 2007, and has been allocated to regional and non-regional members in such proportion so that, when fully subscribed, the regional group holds 60 percent of the total capital stock and the non-regional group 40 percent. At December 31, 2007, members’ subscrip-tions reached UA 21.69 billion, that is 99.18 percent of the capital stock.

The capital stock is composed of paid-up and callable capital. The paid-up capital is the amount of capital payable over a period determined by the Board of Governors’ resolution for the relevant General Capital Increase (10 years for the fourth General Capital Increase and 8 years for the fifth General Capital Increase). The paid-in capital, which represents the portion of paid-up capi-tal that has been actually paid, reached UA 2.34 billion. As of December 31, 2007, the Bank’s callable capital was UA 19.34 billion of which UA 6.66 billion was from countries rated double-A and higher. The callable capital is subject to payment as and when required by the Bank to meet its incurred obligations, (a) by making or participating in direct loans out of funds borrowed or otherwise acquired by the Bank for inclusion in its ordinary capital resources or in special resources; or (b) by guaranteeing in whole or in part, loans made by other entities. It is a protection of the Bank’s creditors and

holders of Bank’s guarantees in the event that it is not able to meet its financial obli-gations. There has never been a call on the callable capital of the Bank.

In accordance with the Shares Transfer Rules, shares for which payment have become due and remain outstanding are forfeited after a prescribed period and offered for subscription to member countries. A member country’s payment of the first GCI-V installment trig-gers the subscription to the entire callable capital portion of shares allocated to it, however, shares representing the paid-up portion of subscriptions are issued only as and when the Bank receives actual payments for such shares.

The position of capital subscriptions at December 31, 2007 is shown in the Statement of Subscriptions to the Capital Stock and Voting Power, which forms part of the Financial Statements in this Report.

Bank RatingThe rating agencies Standard & Poor’s, Moody’s, Fitch Ratings, and the Japan Credit Rating Agency reaffirmed their AAA and AA+ rating of the African Development Bank’s senior and subordinated debt respectively, with a stable outlook. Their rating reflects the Bank’s strong membership support, its preferred creditor status, sound capital adequacy and prudent financial management and policies.

Borrowings The Bank strives to raise funds from the capital markets at the lowest possible cost to support its lending activities. The top-

notch credit ratings enjoyed by the Bank enable it to issue securities at low interest rates. Its borrowing activities are guided by client and cashflow requirements, assets and liability management goals, and risk management policies.

As at December 31, 2007, the borrowing portfolio of the Bank stood at UA 6.20 billion. The Bank is well within its debt policy limits. The key debt ratios are as follows:

• Total debt/total callable capital (max 80 percent): 32.05 percent

• Senior debt/non-borrowing members’ callable capital (max 80 percent): 65.04 percent

In December 2006, the ADB Board of Directors approved for the year 2007, a bor-rowing program of up to UA 1,015 million including a UA 140 million component for the Enhanced Private Sector Assistance for Africa Initiative (EPSA). In 2007, the Bank raised UA 724 million from the capital mar-kets at a weighted average cost of 6-month US Dollar LIBOR minus 32 basis points. In addition, the Bank raised UA 55 million under the EPSA initiative.

The highlight of the year was the Bank’s first transaction in the domestic bond market of any African country with the raising of ZAR 1.2 billion for a five-year maturity in the domestic bond market of South Africa. The transaction is also the first by any supranational in that market and is listed on the Bond Exchange of South Africa. The listing enables the Bank to offer its bond issues to the domestic South African investors. This is based on the specific

Chapter 005 African Development Bank

05_Chapter5_UK.indd 71 11/04/08 13:39:32

Chapter 005 African Development Bank

Annual Report 2007 7372 7372

documentation framework that has now been created by the Bank which is in line with local financial regulations in South Africa.

During 2007, the Bank also raised funds through transactions in the public market, the private placement market, the Uridashi market and through African currency-linked bonds.

The Bank maintained its presence in the public market through a highly successful five-year maturity inaugural transaction for an amount of Canadian Dollar 400 million in the Canadian domestic bond market in July 2007.

The Bank continues to focus its efforts on the possibility of issuance in African currencies. Following the successes of the earlier years, the Bank concluded offshore transactions linked to Nigerian Naira, Kenyan Shilling, Tanzanian Shilling and Ghanaian Cedi in 2007 in addition to the domestic South African Rand transaction. InvestmentsThe Bank’s cash and treasury investments (net of repurchase agreements) as of December 31, 2007 totaled UA 5.40 billion, compared to UA 5.34 billion at the end of 2006. Investment income for 2007 amounted to UA 238.40 million, or a return of 4.59 percent on an average liquidity of UA 5.20 billion, compared to UA 213.82 million in 2006, or a return of 4.22 percent, on an average liquidity of UA 5.06 billion.

Effective January 1, 2001, the ADB’s liquid assets were tranched into 3 portfolios, namely operational portfolio, prudential portfolio, and equity-backed portfolio, each with a different benchmark that reflects the cashflow and risk profile of its assets and funding sources. These benchmarks are one-month LIBID for the operational portfolio, and 6-month marked-to-market LIBOR, resetting on February 1 and August 1 for the prudential portfolio. The equity-backed

portfolio is managed against a re-pricing profile benchmark with 10 percent of the Bank’s net assets re-pricing uniformly over a period of 10 years.

Loan PortfolioLoans signed, net of cancellations, as at December 31, 2007 amounted to UA 18.83 billion. Total outstanding loans, as at December 31, 2007, was UA 5.54 billion, UA 249 million higher than the UA 5.29 billion outstanding as at the end of 2006. This increase was in spite of prepayments during the year amounting to UA 199.06 million. Undisbursed balances at December 31, 2007 totaled UA 1.62 billion, a decrease of UA 408.93 million from December 31, 2006. The number of active signed loans stood at 276 for a total amount of UA 5.54 billion. Also, at December 31, 2007, 547 loans amounting to UA 8.27 billion had been fully repaid. A breakdown of the loan portfolio by product type is presented below.

DisbursementsDisbursements on Bank loans increased from UA 548.44 million in 2006 to UA 884.75 million, representing an increase of 61.3 percent. At December 31, 2007, cumulative disbursements (including non-sovereign

loans) amounted to UA 16.87 billion. Fully disbursed loans at December 31, 2007 were 747 for a total amount of UA 15.78 billion, representing 93.40 percent of cumulative disbursements.

Financial ProductsLoans. The Bank offers 3 loan products: variable, floating, and fixed interest rate loans with a selection of loan currencies, currently, US Dollars, Euro, Japanese Yen, and South Africa Rand. To suit the long-term financing needs of borrowers, loans have a maximum maturity of 20 years, including a grace period on the repayment of the principal amount, generally not exceeding 5 years. For the single currency variable interest rate loan, the base rate is determined twice a year, on January 1 and July 1, and is based on the Bank’s average cost of a designated pool of borrowings funding the loans in the specific currency. The base rate for the floating interest rate loan is derived from the 6-month market reference rate in the specific currency, for example, LIBOR, EURIBOR or JIBAR. The base rate is reset on February 1 and August 1 each year and applies to the 6-month period following the reset date. For the fixed interest rate loan, the lending rate in

Loans Outstanding, december 31, 2007(percentages)

Undisbursed balances, december 31, 2007(percentages)

Multi-CurrencyFixed Rate

5.94%Single CurrencyVariable Rate

9.34%Multi-CurrencyVariable Rate

6.66%

Single CurrencyFloating Rate

31.85%

Single CurrencyFixed Rate46.21%

Multi-CurrencyFixed Rate

0.11%Single CurrencyVariable Rate

0.75%Multi-CurrencyVariable Rate

0.00%

Single CurrencyFloating Rate

35.25%

Single CurrencyFixed Rate63.89%

05_Chapter5_UK.indd 72 11/04/08 13:39:32

7372

African Development Bank Chapter 005

Annual Report 2007 7372

each currency is the fixed amortizing swap rate derived from the 6-month market reference rates. Borrowers may select from a number of rate-fixing alternatives, includ-ing fixing at each disbursement or after all disbursements have been completed. Prior to rate fixing, the currency-specific floating interest rate applies. The pricing formula applicable to all 3 loan products is the same. The applicable rate of interest is the sum of the chosen base rate plus a lending spread. Loans to sovereign and sovereign-guaranteed borrowers enjoy a lending spread of 40 basis points above the 6-month market reference rate. For non-sovereign guaranteed borrowers in both the private and public sector, the lending spread is computed based on the Bank’s risk-based pricing framework.

Agency Lines. Loans to private sector enterprises can be extended directly or through a private financial institution (PFI). In an agency line (AL), the credit risk of the borrower is borne by the Bank. In addition, the PFI acts as an agent for the Bank, to carry out a variety of activities, including, but not limited to, identifying projects within certain parameters; appraising such projects on behalf of the Bank; when approved, undertaking all of the administrative steps related to disbursement (billing, collection of Bank’s funds, filing of security); supervis-ing projects, monitoring the performance of the borrower, submitting reports thereon; and transmitting amounts related to the repayment of the loan to the Bank.

Guarantees. Through the guarantee product, the Bank seeks to leverage its preferred creditor status to assist eligible borrowers to obtain financing from third party lenders, including capital markets. Guarantees will also enable borrowers to obtain financing in their own local currency where the Bank is not able to provide such financing directly from its own resources.

Risk Management Products are offered to enable borrowers to manage the market risks associated with their loans from the Bank, including interest rate, cur-rency, and commodity price risks. These products assist borrowers to manage their balance sheets and their changing needs more efficiently over time. Risk manage-ment products such as interest rate swaps, currency swaps, interest rate caps and col-lars are available to borrowers at any time during the life of the loan.

Equity Participation or Quasi Equity Products. The Bank’s ability to provide risk capital through equity invest-ments is a key element of its resource mobi-lization role. Even though the Bank cannot be a majority shareholder in a company, it can participate in a project by acquir-ing ordinary stocks, redeemable preferred stocks, or debentures.

Other Financial Services. In addition to the products described above, the Bank may offer loan syndication and under-writing services through its private sector window.

Risk Management Policies and Processes

As a development finance institution, the African Development Bank seeks to reduce its exposure to risks that are not essential to its core business of providing development finance and related assistance. To this end, the Bank has adapted its risk management policies, guidelines and processes to reduce exposure to interest rate, currency, liquidity, counterparty, legal and other operational risks, while maximizing its capacity to assume credit risks to public and private sector clients, within approved risk limits.

Note D of the Financial Statements provides the details regarding the Risk Management policies and processes applied by the Bank to manage these risks.

financial Results

Since 2006, the Bank has accounted for distributions to organizations, funds or institutions for purposes complementary with the Bank’s mission as grant expenses in the period such distributions are approved by the Board of Governors. Prior to 2006, such distributions were presented as direct reductions of equity. Due to current expense treatment of distributions approved by the Board of Governors, “Income before transfer of income approved by the Board of Governors” is separately disclosed on the income statement, to highlight income from normal or ordinary operations of the Bank.

The highlights of the Bank’s financial perform-ance in 2007 include the following:

• Income before transfers approved by the Board of Governors increased by 66.81 percent from UA 194.03 million in 2006 to UA 323.67 million in 2007. The increase is mainly attributable to the following factors: a) net write-back of provision for impairment on loans and related charges receivable of UA 69.96 million in 2007 compared to a net charge for provision of UA 51.69 million in 2006, b) an increase of UA 21.24 million in 2007 in the unrealized gains on derivatives and borrowings for which fair value option was elected, and c) a reduction of UA 27.52 million in the amount of impairment for equity investments and other receivables.

• Loan income increased by UA 12.92 million, or 3.93 percent, in 2007. The increase in loan income was mainly due to a higher average loan balance during 2007. Investment income also increased in 2007 by UA 24.57 million, or 11.49 percent, as a result of higher average investment balances and higher yields, but the increase was more than offset by a UA 50.18 million increase in borrowing-related charges. In 2007,

05_Chapter5_UK.indd 73 11/04/08 13:39:33

Chapter 005 African Development Bank

Annual Report 2007 PB74

the Bank earned income of UA 4.97 million on investments in debt instru-ments issued by entities in its regional member countries.

• As a result of the arrears clearance mechanism approved by the Board of Directors during 2007, the number of sovereign borrowers in arrears for six months or more decreased from 6 at December 31, 2006 to 4 at December 31, 2007. Consequently, there was a write-back of impairment for losses on loans and related charges receivable in 2007 compared to a charge for impair-ment in 2006. At December 31, 2007 total accumulated provision for losses on principal and charges was UA 364.72 million, which was 6.10 percent of gross principal and charges receivable at that date, compared to UA 436.77 million, or 7.60 percent of gross principal and charges receivable at December 31, 2006.

• Total Bank Group administrative expenses increased from UA 154.34 million in 2006 to UA 180.65 million in 2007. The Bank’s share of the Bank Group administrative expenses amounted to UA 42.22 million for 2007, compared to UA 36.86 million for 2006. Bank Group administrative expenses are allocated between the Bank, the ADF and the NTF based on a predetermined cost-sharing formula driven primarily by the relative levels of certain operational volume indicators.

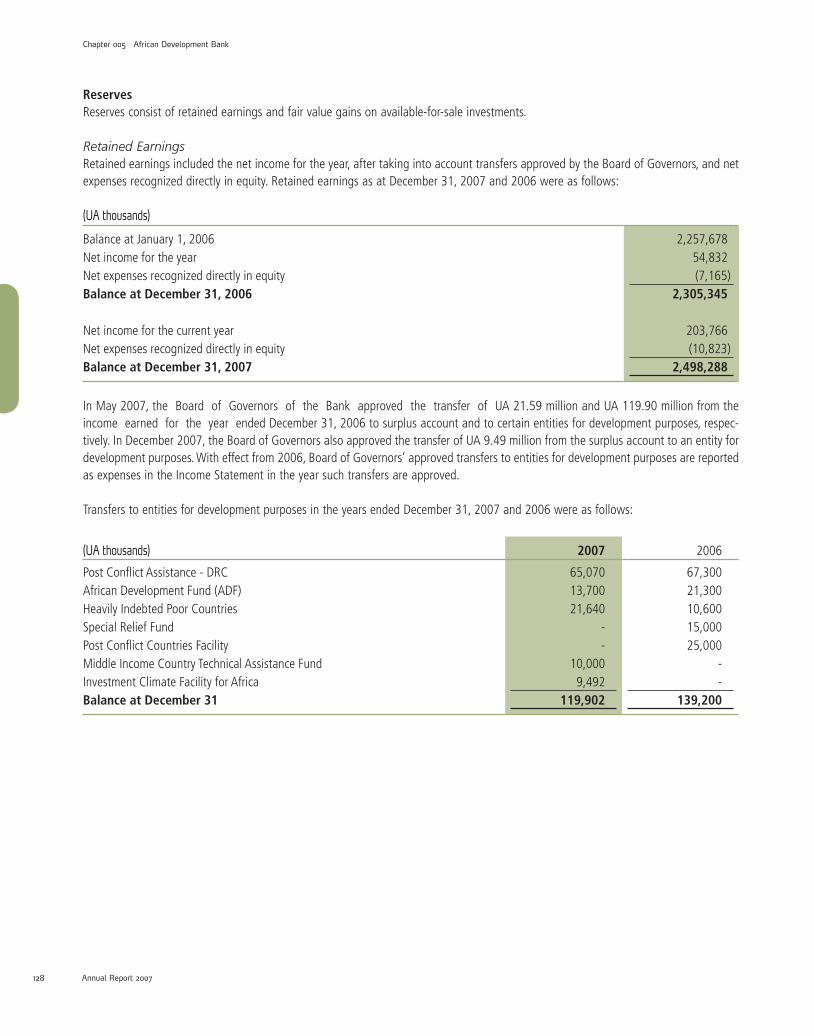

• For the past several years, the Bank has earned levels of net income sufficient to enable not only the further strengthening of the Bank’s reserves position, but also contributions on behalf of its sharehold-ers to other development initiatives for Africa. Total reserves plus accumulated loss provisions on outstanding loan principal and charges at December 31, 2007 were UA 2.90 billion, up from UA 2.74 billion at December 31, 2006. As a

percentage of gross loans, reserves plus loss provisions on loan principal increased from 47.7 percent at December 31, 2006 to 49.24 percent at December 31, 2007. Against the background of the strong risk-bearing capacity of the Bank, the Board of Governors in 2007 approved transfers of UA 119.90 million to various development initiatives in Africa. These transfers included UA 65.07 million to the special fund for post-conflict assistance to the Democratic Republic of Congo, UA 13.70 million to the ADF, UA 21.64 million to the Heavily Indebted Poor Countries (HIPC) initiative, UA 10 million to the Middle Income Countries Technical Assistance Fund, and UA 9.49 million to the Investment Climate Facility for Africa.

05_Chapter5_UK.indd 74 11/04/08 13:39:33

African Development Bank

Financial Statements and Report of the Independent Auditors

Years ended December 31, 2007 and 2006

Page

Balance Sheet 76

Income Statement 78

Statement of Recognized Income and Expense 79

Statement of Cash Flows 80

Notes to the Financial Statements 81

Report of the Independent Auditors 144

06_ADB_part a_UK.indd 75 11/04/08 13:40:41

Chapter 005 African Development Bank

Annual Report 200776

BALANCE SHEET AS AT DECEMBER 31, 2007 AND 2006(UA thousands - Note B)

ASSETS 2007 2006

CASH 95,528 129,329

DEMANDOBLIGATIONS 3,801 3,801

TREASURYINVESTMENTS(NoteF) 5,303,540 6,093,361

DERIVATIVEASSETS(NoteG) 425,338 273,310

NON-NEGOTIABLEINSTRUMENTS

ONACCOUNTOFCAPITAL(NoteH) 15,385 20,383

ACCOUNTSRECEIVABLE

Accruedincomeandchargesreceivableonloans(NoteI) 267,149 232,935

Otheraccountsreceivable 328,726 368,037

595,875 600,972

DEVELOPMENTFINANCINGACTIVITIES

Loans,net(NotesD&I) 5,344,073 5,076,771

Equityparticipations(NoteJ) 189,248 119,119

Otherdebtsecurities(NoteK) 94,622 -

5,627,943 5,195,890

OTHERASSETS

Property,equipmentandintangibleassets(NoteL) 14,362 14,241

Miscellaneous 667 713

15,029 14,954

TOTAL ASSETS 12,082,439 12,332,000

Theaccompanyingnotestothefinancialstatementsformpartofthisstatement.

06_ADB_part a_UK.indd 76 11/04/08 13:40:41

African Development Bank Chapter 005

Annual Report 2007 77

LIABILITIES & EQUITY 2007 2006

ACCOUNTSPAYABLE Accruedfinancialcharges 418,706 328,751 Otheraccountspayable 165,633 320,209

584,339 648,960

SECURITIESSOLDUNDERAGREEMENTSTOREPURCHASEANDPAYABLEFORCASHCOLLATERALRECEIVED(NoteF) - 877,833

DERIVATIVELIABILITIES(NoteG) 591,047 481,937

BORROWINGS(NoteM) Borrowingsatfairvalue 5,226,279 4,823,648 Borrowingsatamortizedcost 972,594 1,046,821

6,198,873 5,870,469EQUITY(NoteN) Capital Subscriptionspaid 2,336,457 2,303,062 CumulativeExchangeAdjustmentonSubscriptions(CEAS) (160,075) (155,742) Subscriptionspaid(netofCEAS) 2,176,382 2,147,320

Reserves Retainedearnings 2,498,288 2,305,345 Fairvaluegainsonavailable-for-saleinvestments 33,510 136 Totalreserves 2,531,798 2,305,481Totalequity 4,708,180 4,452,801

TOTAL LIABILITIES & EQUITY 12,082,439 12,332,000

06_ADB_part a_UK.indd 77 11/04/08 13:40:42

INCOME STATEMENT FOR THE YEARS ENDED DECEMBER 31, 2007 AND 2006(UA thousands - Note B)

2007 2006

OPERATIONALINCOME&EXPENSES Incomefrom: Loans(NoteO) 341,945 329,027 Investmentsandrelatedderivatives(NoteO) 238,397 213,824 Otherdebtsecurities 4,966 - Totalincomefromloansandinvestments 585,308 542,851

Borrowingexpenses(NoteP) Interestandamortizedissuancecosts (268,023) (245,413) Netinterestonborrowing-relatedderivatives (62,706) (35,137) Unrealizedgainonfair-valuedborrowingsandrelatedderivatives 21,239 10,672 Unrealizedgainonderivativesonnonfair-valuedborrowingsandothers 34,774 21,067

Provisionforimpairment(NoteI) Loanprincipal 17,453 (22,566) Loancharges 52,503 (29,120)Provisionforimpairmentonequityinvestmentsandotherreceivables (7,222) (34,745)Translation(losses)/gains (8,895) 4,101Otherincome 7,323 23,736Netoperationalincome 371,754 235,446

OTHEREXPENSES Administrativeexpenses(NoteQ) (42,218) (36,859) Depreciation-Property,equipmentandintangibleassets(NoteL) (5,375) (6,233) Sundry(expenses)/gains (493) 1,678Totalotherexpenses (48,086) (41,414)

IncomebeforetransfersapprovedbytheBoardofGovernors 323,668 194,032

TransfersofincomeapprovedbytheBoardofGovernors(NoteN) (119,902) (139,200)

NET INCOME 203,766 54,832

Theaccompanyingnotestothefinancialstatementsformpartofthisstatement.

Chapter 005 African Development Bank

Annual Report 200778

06_ADB_part a_UK.indd 78 11/04/08 13:40:42

STATEMENT OF RECOGNIZED INCOME AND EXPENSEFOR THE YEARS ENDED DECEMBER 31, 2007 AND 2006(UA thousands - Note B)

2007 2006

Gain/(loss)onavailable-for-saleinvestmentstakentoequity 33,374 (8,574)

Actuariallossesondefinedbenefitplans (10,823) (7,165)

Netincome/(loss)recognizeddirectlyinequity 22,551 (15,739)

Netincomefortheyear 203,766 54,832

TOTAL RECOGNIZED INCOME FOR THE YEAR 226,317 39,093

Theaccompanyingnotestothefinancialstatementsformpartofthisstatement.

African Development Bank Chapter 005

Annual Report 2007 79

06_ADB_part a_UK.indd 79 11/04/08 13:40:42

Chapter 005 African Development Bank

Annual Report 200780

STATEMENT OF CASH FLOWS FOR THE YEARS ENDED DECEMBER 31, 2007 AND 2006(UA thousands - Note B)

2007 2006

CASH FLOwS FROM:

OPERATING ACTIvITIES:Netincome 203,766 54,832Adjustmentstoreconcilenetincometonetcashprovidedbyoperatingactivities: Depreciation 5,375 6,233 Provisionforimpairmentonloanprincipalandcharges (69,956) 51,686 Unrealizedgainsoninvestmentsandrelatedderivatives (5,997) (2,638) Amortizationofdiscountorpremiumonheld-to-maturityinvestments (5,645) 2,814 Provisionforimpairmentonequityinvestmentsandreceivables 7,222 34,745 Amortizationofborrowingissuancecosts 3,333 2,936 Unrealizedgainonfairvalueborrowingsandderivatives (56,013) (48,799) Translationlosses/(gains) 8,895 (4,101) Shareofprofitsinassociate (479) (379)Netmovementsinderivatives (51,659) 130,972Changesinaccruedincomeonloans 15,640 (4,877)Changesinaccruedfinancialcharges 90,409 79,132Changesinotherreceivablesandpayables (123,330) 19,412Netcashprovidedbyoperatingactivities 21,561 321,968

INvESTING, LENDING AND DEvELOPMENT ACTIvITIES:Disbursementsonloans (884,747) (548,440)Repaymentsofloans 704,045 706,408Investmentsmaturingafter3monthsofacquisition: Held-to-maturityportfolio (79,764) (410,735) Tradingportfolio 359,145 (85,443)Otherdebtsecurities (92,801) -Changesinotherassets (5,451) (4,209)Equityparticipationsmovement (40,150) 2,919Netcashusedininvesting,lendinganddevelopmentactivities (39,723) (339,500)

FINANCING ACTIvITIES:Newissuesonborrowings 779,649 730,741Repaymentsonborrowings (402,541) (621,486)Netcashfromcapitalsubscriptions 33,363 40,302Netcashprovidedbyfinancingactivities 410,471 149,557Effectofexchangeratechangesoncashandcashequivalents (12,363) (18,150)Increaseincashandcashequivalents 379,946 113,875Cashandcashequivalentsatthebeginningoftheyear 705,890 592,015Cash and cash equivalents at the end of the year 1,085,836 705,890

COMPOSED OF:Investmentsmaturingwithin3monthsofacquisition: Held-to-maturityportfolio 24,114 80,075 Tradingportfolio 966,194 1,374,319Securitiessoldunderagreementstorepurchaseandpayableforcashcollateralreceived - (877,833)Cash 95,528 129,329Cash and cash equivalents at the end of the year 1,085,836 705,890

SUPPLEMENTARY DISCLOSURE:Movementresultingfromexchangeratefluctuations: Loans (70,008) 32,776 Borrowings (77,088) (251,558) Currencyswaps 89,729 163,523

Theaccompanyingnotestothefinancialstatementsformpartofthisstatement.

06_ADB_part a_UK.indd 80 11/04/08 13:40:43

African Development Bank Chapter 005

Annual Report 2007 81

NOTES TO THE FINANCIAL STATEMENTSYEARS ENDED DECEMBER 31, 2007 AND 2006

NOTE A – OPERATIONS AND AFFILIATED ORGANIZATIONS

TheAfricanDevelopmentBank(ADBortheBank)isamultilateraldevelopmentfinanceinstitutiondedicatedtotheeconomicandsocialprogressofitsregionalmemberstates.TheBankfinancesdevelopmentprojectsandprogramsinitsregionalmemberstates,typicallyincooperationwithothernationalor internationaldevelopment institutions. In furtheranceof thisobjective, theBankparticipates intheselection,studyandpreparationofprojectscontributingtosuchdevelopmentand,wherenecessary,providestechnicalassistance.TheBankalsopromotesinvestmentsofpublicandprivatecapitalinprojectsandprogramsdesignedtocontributetotheeconomicandsocialprogressoftheregionalmemberstates.TheactivitiesoftheBankarecomplementedbythoseoftheAfricanDevelopmentFund(ADFortheFund),whichwasestablishedbytheBankandcertaincountries;andtheNigeriaTrustFund(NTF),whichisaspecialfundadministeredbytheBank.Notably,theADB,ADF,andNTFeachhaveseparateanddistinctassetsandliabilities.ThereisnorecoursetotheADBforobligationsinrespectofanyoftheADForNTFliabilities.TheADFwasestablishedtoassisttheBankincontributingtotheeconomicandsocialdevelopmentoftheBank’sregionalmembers,topromotecooperationandincreasedinternationaltradeparticularlyamongtheBank’smembers,andtoprovidefinancingonconcessionaltermsforsuchpurposes.

NOTE B – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

TheBank’sfinancialstatementsarepreparedinaccordancewithInternationalFinancialReportingStandards(IFRS)promulgatedbytheInternationalAccountingStandardsBoard.Thefinancialstatementshavebeenpreparedunderthehistoricalcostconventionexceptforcertainfinancialassetsandfinancialliabilitiesthatarecarriedatfairvalue.

ThesignificantaccountingpoliciesemployedbytheBankaresummarizedbelow.

Revenue RecognitionInterestincomeisaccruedandrecognizedbasedontheeffectiveinterestrateforthetimesuchinstrumentisoutstandingandheldbytheBank.Theeffectiveinterestrateistheratethatdiscountstheestimatedfuturecashflowsthroughtheexpectedlifeofthefinancialassettotheasset’snetcarryingamount.

Incomefrominvestmentsincludesrealizedandunrealizedgainsandlossesontradingfinancialinstruments.

DividendsrelatingtoinvestmentsinequityarerecognizedwhentheBank’srighttoreceivepaymentisestablished.

Functional and Presentation CurrenciesTheBankconductsitsoperationsinthecurrenciesofitsmembercountries.AsaresultoftheapplicationofIAS21revised,“TheEffectsofChangesinForeignExchangeRates”,theBankprospectivelychangeditsfunctionalcurrencyfromthecurrenciesofallitsmembercoun-triestotheUnitofAccount(UA)effectiveJanuary1,2005.TheUAisalsothecurrencyinwhichthefinancialstatementsarepresented.ThevalueoftheUnitofAccountisdefinedinArticle5.1(b)oftheAgreementEstablishingtheBank(theAgreement)asequivalenttooneSpecialDrawingRight(SDR)oftheInternationalMonetaryFund(IMF)oranyunitadoptedforthesamepurposebytheIMF.

Currency TranslationIncomeandexpensesare translated toUAat the ratesprevailingon thedateof the transaction.Monetaryassetsand liabilitiesaretranslatedintoUAatratesprevailingatthebalancesheetdate.TheratesusedfortranslatingcurrenciesintoUAatDecember31,2007and2006arereportedinNoteV-1.Non-monetaryassetsandliabilitiesaretranslatedintoUAathistoricalrates.Translationdifferencesareincludedinthedeterminationofnetincome.CapitalsubscriptionsarerecordedinUAattheratesprevailingatthetimeofreceipt.ThetranslationdifferencerelatingtopaymentsofcapitalsubscriptionsisreportedinthefinancialstatementsastheCumulativeExchangeAdjustmentonSubscriptions (CEAS).This is composedof thedifferencebetween theUAamountat thepredetermined rateand theUAamountusingtherateatthetimeofreceipt.Whencurrenciesareconvertedintoothercurrencies,theresultinggainsorlossesareincludedinthedeterminationofnetincome.

06_ADB_part a_UK.indd 81 11/04/08 13:40:44

Chapter 005 African Development Bank

Annual Report 200782

Member Countries’ SubscriptionsAlthoughtheAgreementestablishingtheADBallowsforamembercountrytowithdrawfromtheBank,nomemberhaseverwithdrawnitsmembershipvoluntarily,norhasanyindicatedtotheBankthatitintendstodoso.ThestabilityinthemembershipreflectsthefactthatthemembersareindependentAfricanandnon-Africancountries,andthatthepurposeoftheBankistocontributetothesustain-ableeconomicdevelopmentandsocialprogressofitsregionalmembercountriesindividuallyandjointly.Accordingly,asofDecember31,2007,theBankdidnotexpecttodistributeanyportionofitsnetassetsduetomembercountrywithdrawals.

Intheunlikelyeventofawithdrawalbyamember,theBankshallarrangefortherepurchaseoftheformermember’sshares.Therepur-chasepriceofthesharesisthevalueshownbythebooksoftheBankonthedatethecountryceasestobeamember,hereafterreferredtoas“theterminationdate.”TheBankmaypartiallyorfullyoffsetamountsdueforsharespurchasedagainstthemember’sliabilitiesonloansandguaranteesduetotheBank.Theformermemberwouldremainliablefordirectobligationsandcontingent liabilitiestotheBankforsolongasanypartsoftheloansorguaranteescontractedbeforetheterminationdateareoutstanding.Ifatadatesub-sequenttotheterminationdate,itbecomesevidentthatlossesmaynothavebeensufficientlytakenintoaccountwhentherepurchasepricewasdetermined,theformermembermayberequiredtopay,ondemand,theamountbywhichtherepurchasepriceoftheshareswouldhavebeenreducedhadthelossesbeentakenintoaccountwhentherepurchasepricewasdetermined.Inaddition,theformermemberremainsliableonanycall,subsequenttotheterminationdate,forunpaidsubscriptions,totheextentthatitwouldhavebeenrequiredtorespondiftheimpairmentofcapitalhadoccurredandthecallhadbeenmadeatthetimetherepurchasepriceofitsshareswasdetermined.

Wereamembertowithdraw,theBankmaysetthedatesinrespectofpaymentsforsharesrepurchased.If,forexample,payingaformermemberwouldhaveadverseconsequencesfortheBank’sfinancialposition,theBankcoulddeferpaymentuntiltheriskhadpassed,andindefinitelyifappropriate.Furthermore,sharesthatbecomeunsubscribedforanyreasonmaybeofferedbytheBankforpurchasebyeligiblemembercountries,basedonthesharetransferrulesapprovedbytheBoardofGovernors.Inanyevent,nopaymentsshallbemadeuntilsixmonthsaftertheterminationdate.

IftheBankweretoterminateitsoperations,allliabilitiesoftheBankwouldfirstbesettledoutoftheassetsoftheBankandthen,ifnecessary,outofmembers’callablecapital,beforeanydistributioncouldbemadetoanymembercountry.SuchdistributionissubjecttothepriordecisionoftheBoardofGovernorsoftheBankandwouldbebasedonthepro-ratashareofeachmembercountry.

Employee Benefits

1) Pension ObligationsThe Bank operates a contributory defined benefit pension plan for its employees.The Staff Retirement Plan (SRP) provides benefitpaymentstoparticipantsuponretirement.Adefinedbenefitplanisapensionplanthatdefinesanamountofpensionbenefitthatanemployeewill receiveon retirement,usuallydependentononeormore factors suchasage, yearsof serviceandcompensation.AnactuarialvaluationofthecostofprovidingbenefitsfortheSRPisdeterminedusingtheProjectedUnitCreditMethod.Uponreachingretirementage,pensioniscalculatedbasedontheaverageremunerationforthefinalthreeyearsofpensionableserviceandthepensionissubjecttoannualinflationaryadjustments.Actuarialgainsandlossesarerecognizedimmediatelyinretainedearningsintheyeartheyoccur.Pastservicecostisrecognizedimmediatelytotheextentthatbenefitsarealreadyvested,otherwise,amortizedonastraight-linebasisovertheaverageperioduntilthebenefitsbecomevested.Thepensionliabilityisrecognizedaspartofotheraccountspayableinthebalancesheet.TheliabilityrepresentsthepresentvalueoftheBank’sdefinedbenefitobligations,netofthefairvalueofplanassetsandunrecognizedactuarialgainsandlosses.

2) Post-Employment Medical BenefitsTheBankoperatesacontributorydefinedMedicalBenefitPlan(MBP),whichprovidespost-employmenthealthcarebenefitstoeligibleformerstaff,includingretirees.MembershipoftheMBPincludesbothstaffandretireesoftheBank.Theentitlementtothepost-retire-ment healthcare benefit is usually conditional on the employee remaining in service up to retirement age and the completion of aminimumserviceperiod.Theexpectedcostsof thesebenefitsderive fromcontributions fromplanmembersaswellas theBankandareaccruedovertheperiodofemploymentandduringretirement.ContributionsbytheBanktotheMBParechargedtoexpensesandincludedinthestatementofincomeandexpenses.TheMBPBoard,anindependentbodycreatedbytheBank,determinestheadequacyofthecontributionsandisauthorizedtorecommendchangestothecontributionratesofboththeBankandplanmembers.

06_ADB_part a_UK.indd 82 11/04/08 13:40:44

African Development Bank Chapter 005

Annual Report 2007 83

Financial InstrumentsFinancialassetsandfinancialliabilitiesarerecognizedontheBank’sbalancesheetwhentheBankassumesrelatedcontractualrightsorobligations.

1) Financial AssetsTheBankclassifiesitsfinancialassetsinthefollowingcategories:financialassetsatfairvaluethroughprofitorloss;loansandreceiva-bles;held-to-maturityinvestments;andavailable-for-salefinancialassets.Managementdeterminestheclassificationofitsinvestmentsatinitialrecognition.

i) FinancialAssetsatFairValuethroughProfitorLossAlltradingassetsarecarriedatfairvaluethroughtheincomestatementandgainsandlossesarereportedintheincomestatementintheperiodinwhichtheyarise.Theinvestmentsinthetradingportfolioareacquiredprincipallyforthepurposeofsellingintheshortterm.Derivativesarealsocategorizedasheld-for-trading.

ii) LoansandReceivablesTheBankhasclassifieddemandobligations,accruedincomeandreceivablesfromloansandinvestmentsandothersundryamountsasreceivables.Loansandreceivablesarenon-derivativefinancialassetswithfixedordeterminablepaymentsthatarenotquotedinanactivemarket.TheyarisewhentheBankprovidesmoney,goodsorservicesdirectlytoadebtorwithnointentionoftradingthereceivable.Loansandreceivablesarecarriedatamortizedcostusingtheeffectiveinterestmethod.

iii) Held-to-MaturityInvestmentsTheBankhasclassifieditsinvestmentsincertaindebtsecuritiesasheld-to-maturity.Held-to-maturityinvestmentsarenon-derivativefinancialassetswithfixedordeterminablepaymentsandfixedmaturitiesthattheBank’smanagementhasthepositiveintentionandabilitytoholdtomaturity.Held-to-maturityinvestmentsaresubsequentlymeasuredatamortizedcost.Held-to-maturityinvestmentsarecarriedatamortizedcostusingtheeffectiveinterestmethod.

iv) Available-for-SaleFinancialAssetsTheBankhasclassifiedequityinvestmentsoverwhichitdoesnothavecontrolorsignificantinfluenceasavailable-for-sale.Available-for-saleinvestmentsarethoseintendedtobeheldforanindefiniteperiodoftime,andmayormaynotbesoldinthefuture.Gainsand losses arising from changes in the fair valueof available-for-sale financial assets are recognizeddirectly in equity, until thefinancialassetisderecognizedorimpairedatwhichtimethecumulativegainorlosspreviouslyrecognizedinequityisrecognizedinprofitorloss.

Purchasesandsalesoffinancialassetsatfairvaluethroughprofitorloss,held-to-maturityandavailable-for-saleinvestmentsarerec-ognizedonatrade-datebasis,whichisthedateonwhichtheBankcommitstopurchaseorselltheasset.Loansarerecognizedwhencashisadvancedtotheborrowers.Financialassetsnotcarriedatfairvaluethroughprofitorlossareinitiallyrecognizedatfairvalueplustransactioncosts.FinancialassetsarederecognizedwhentherightstoreceivecashflowsfromthefinancialassetshaveexpiredorwheretheBankhastransferredsubstantiallyallrisksandrewardsofownership.

Securitiespurchasedunderresaleagreementsandsecuritiessoldunderrepurchaseagreementsarereportedatmarketrates.TheBankreceivessecuritiespurchasedunderresaleagreements,monitorsthefairvalueofthesecuritiesandifnecessarymayrequireadditionalcollateral.

Cashandcashequivalentscomprisecashonhand,demanddepositsandothershort-term,highly liquid investments thatarereadilyconvertibletoaknownamountofcash,aresubjecttoinsignificantriskofchangesinvalueandhaveatimetomaturityuponacquisitionofthreemonthsorless.

06_ADB_part a_UK.indd 83 11/04/08 13:40:45

Chapter 005 African Development Bank

Annual Report 200784

2) Financial Liabilitiesi) Borrowings

Intheordinarycourseofitsbusiness,theBankborrowsfundsinthemajorcapitalmarketsforlendingandliquiditypurposes.TheBankissuesdebtinstrumentsdenominatedinvariouscurrencies,withdifferingmaturitiesatfixedorvariableinterestrates.TheBank’sborrowing strategy is drivenby threemajor factors, namely: timeliness inmeeting cash flow requirements, optimizingasset andliabilitymanagementwiththeobjectiveofmitigatingexposuretofinancialrisks,andprovidingcost-effectivefunding.Inadditiontolongandmedium-termborrowings,theBankalsoundertakesshort-termborrowingforcashandliquiditymanagementpurposesonly.Borrowingsnotdesignatedatfairvaluethroughprofitorlossarecarriedonthebalancesheetatamortizedcostwithinterestexpensedeterminedusingtheeffectiveinterestmethod.Borrowingexpensesarerecognizedinprofitorlossandincludetheamortizationofissuancecosts,discountsandpremiums,whichisdeterminedusingtheeffectiveinterestmethod.CertainoftheBank’sborrowingshavebeenobtainedfromthegovernmentsofsomemembercountriesoftheBankandareinterest/free.InaccordancewithIAS20–”AccountingforGovernmentGrantsandDisclosureofGovernmentAssistance”,thebenefitofborrowingatsubsidizedratesfrommembercountries’governmentshasnotbeenrecognizedthroughtheimputationofinterestexpenseinthefinancialstatements.

ii) FinancialLiabilitiesatFairValuethroughProfitorLossThiscategoryhastwosub-categories:financialliabilitiesheldfortrading,andthosedesignatedatfairvaluethroughprofitorlossatinception.Derivativesarecategorizedasheld-for-trading.TheBankprimarilyappliesfairvaluedesignationtoborrowingswhichhavebeenswappedintofloating-ratedebtusingderivativecontracts.Inthesecases,thedesignationoftheborrowingatfairvaluethroughprofitorlossismadeinordertosignificantlyreduceanaccountingmismatchwhichwouldotherwisehaveariseniftheborrowingswerecarriedonthebalancesheetatamortizedcostwhiletherelatedswapsarecarriedonthebalancesheetatfairvalue.

iii) OtherLiabilitiesAllfinancialliabilitiesthatarenotderivativesordesignatedatfairvaluethroughprofitorlossarerecordedatamortizedcost.Theamountsincludeaccruedfinancechargesonborrowingsandotheraccountspayable.

Financialliabilitiesarederecognizedwhentheyaredischargedorcancelledorwhentheyexpire.

DerivativesThe Bank uses derivative instruments in its portfolios for asset/liability management, cost reduction, risk management and hedgingpurposes.Theseinstrumentsincludecross-currencyswapsandinterestrateswaps.ThederivativesonborrowingsareusedtomodifytheinterestrateorcurrencycharacteristicsorbothofthedebttheBankissues.Thiseconomicrelationshipisestablishedonthedatethedebtisissued,andmaintainedthroughoutthetermsofthecontracts.Theinterestcomponentofthesederivativesisreportedaspartofborrowingexpenses.

AlthoughIAS39allowshedgeaccountingforcertainqualifyinghedgingrelationships,theBankhaselectednottoapplyhedgeaccount-ingtoanyqualifyinghedgingrelationship,butratherclassifiesallderivativesasheld-for-tradingatfairvalue,withallchangesinfairvaluerecognizedintheincomestatement.Whenthecriteriafortheapplicationofthefairvalueoptionaremet,thentherelateddebtisalsocarriedatfairvaluewithchangesinfairvaluerecognizedintheincomestatement.

Derivatives embedded in other financial instruments or other non-financial host contracts are treated as separate derivatives whentheirrisksandcharacteristicsarenotcloselyrelatedtothoseofthehostcontractandthehostcontractisnotcarriedatfairvaluewithunrealizedgainsorlossesreportedinprofitorloss.Suchderivativesarestrippedfromthehostcontractandmeasuredatfairvaluewithunrealizedgainsandlossesreportedinprofitorloss.

Impairment of Financial Assets

1) Assets Carried at Amortized CostTheBankfirstassesseswhetherobjectiveevidenceofimpairmentexistsindividuallyforfinancialassets.IftheBankdeterminesthatnoobjectiveevidenceofimpairmentexistsforanindividuallyassessedfinancialasset,thatassetisincludedinagroupoffinancialassetswithsimilarcreditcharacteristicsandcollectivelyassessedforimpairment.Assetsthatareindividuallyassessedforimpairmentandfor

06_ADB_part a_UK.indd 84 11/04/08 13:40:45

African Development Bank Chapter 005

Annual Report 2007 85

whichanimpairmentlossisorcontinuestoberecognizedarenotincludedinacollectiveassessmentofimpairment.Afinancialassetoragroupoffinancialassetsisimpairedandimpairmentlossesareincurredif,andonlyif,thereisobjectiveevidenceofimpairmentasaresultofoneormoreeventsthatoccurredaftertheinitialrecognitionoftheasset(a‘lossevent’)andthatlossevent(orevents)hasanimpactontheestimatedfuturecashflowsofthefinancialassetorgroupoffinancialassetsthatcanbereliablyestimated.

IftheBankdeterminesthatthereisobjectiveevidencethatanimpairmentlossonloansandreceivablesorheld-to-maturityinvestmentscarriedatamortizedcosthasbeenincurred,theamountofthelossismeasuredasthedifferencebetweentheasset’scarryingamountand thepresent valueof estimated future cash flows (excluding future credit losses thathavenotbeen incurred)discountedat thefinancialasset’soriginaleffectiveinterestrate.Forsovereign-guaranteedloans,theestimatedimpairmentarisesfromdelaysthatmaybeexperiencedinreceivingamountsdue.Fornon-sovereign-guaranteedloans,theimpairmentreflectsmanagement’sbestestimateofthenon-collectibility,inwholeorinpart,ofamountsdueaswellasdelaysinthereceiptofsuchamounts.

Thecarryingamountoftheassetisreducedthroughtheuseofanallowanceaccountandtheamountofthelossisrecognizedintheincomestatement.Ifaloanorheld-to-maturityinvestmenthasavariableinterestrate,thediscountrateformeasuringanyimpairmentlossisthecurrenteffectiveinterestratedeterminedunderthecontract.

Interestandchargesareaccruedonallloansincludingthoseinarrears.

2) Available-for-Sale AssetsTheBankassessesateachbalancesheetdatewhetherthereisobjectiveevidencethatafinancialassetoragroupoffinancialassetsisimpaired.Foravailable-for-saleequityinstrumentscarriedatfairvalue,asignificantorprolongeddeclineinthefairvalueofthesecuritybelowitscostisconsideredindeterminingwhethertheassetsareimpaired.Ifanysuchevidenceexistsforavailable-for-saleequityinstru-mentscarriedatfairvalue,thecumulativeloss,whichismeasuredasthedifferencebetweentheacquisitioncostandthecurrentfairvalue,netofanyimpairmentlosspreviouslyrecognizedinprofitorloss,isreclassifiedfromequitytotheincomestatement.Impairmentlossesrecognizedintheincomestatementonavailable-for-saleequityinstrumentscarriedatfairvaluearereversedthroughequity.

Ifthereisobjectiveevidencethatanimpairmentlosshasbeenincurredonanavailable-for-saleequityinstrumentthatiscarriedatcostbecauseitsfairvaluecannotbereliablymeasured,theamountofimpairmentlossismeasuredasthedifferencebetweenthecarryingamountoftheimpairedequityinstrumentandthepresentvalueoftheestimatedfuturecashflowsdiscountedatthecurrentmarketrateofreturnforasimilarequity instrument.Oncerecognized, impairmentlossesontheseequity instrumentscarriedatcostarenotreversed.

Offsetting Financial InstrumentsFinancialassetsandliabilitiesareoffsetandreportedonanetbasiswhenthereisalegallyenforceablerighttooffsettherecognizedamountsandthereisanintentiontosettleonanetbasis,orrealizetheassetandsettletheliabilitysimultaneously.

Fair value DisclosureThefairvaluesofquoted investments inactivemarketsarebasedoncurrentbidprices.For financialassetswith inactivemarketsorunlistedsecurities,theBankestablishesfairvaluebyusingvaluationtechniquesthatincorporatethemaximumuseofmarketdatainputs.Theseincludetheuseofrecentarm’slengthtransactions,discountedcashflowanalysis,optionpricingmodelsandothervaluationtech-niquescommonlyusedbymarketparticipants.Financial instrumentsforwhichmarketquotationsarenotreadilyavailablehavebeenvaluedusingmethodologiesandassumptionsthatnecessarilyrequiretheuseofsubjectivejudgments.Accordingly,theactualvalueatwhichsuchfinancialinstrumentscouldbeexchangedinacurrenttransactionorwhethertheyareactuallyexchangeableisnotreadilydeterminable.Managementbelievesthatthesemethodologiesandassumptionsarereasonable;however,thevaluesactuallyrealizedinasalemightbedifferentfromthefairvaluesdisclosed.

ThemethodsandassumptionsusedbytheBankinestimatingthefairvaluesoffinancialinstrumentsareasfollows:

06_ADB_part a_UK.indd 85 11/04/08 13:40:45

Chapter 005 African Development Bank

Annual Report 200786

Cash:Thecarryingamountisthefairvalue.Investments:Fairvaluesforinvestmentsecuritiesarebasedonquotedmarketprices,whereavailable.Ifquotedmarketpricesarenotavailable,fairvaluesarebasedonquotedmarketpricesofcomparableinstruments.

Borrowings:ThefairvaluesoftheBank’sborrowingsarebasedonmarketquotationswhenpossibleorvaluationtechniquesbasedondiscountedcashflowmodelsusingLIBORmarket-determineddiscountcurvesadjustedbytheBank’screditspread.CreditspreadsareobtainedfrommarketdataaswellasindicativequotationsreceivedfromcertaincounterpartiesfortheBank’snewpublicbondissues.TheBankalsousessystemsbasedonindustrystandardpricingmodelsandvaluationtechniquestovalueborrowingsandtheirassociatedderivatives.Themodelsusemarket-sourcedinputssuchasinterestrates,yieldcurves,exchangeratesandoptionvolatilities.Valuationmodelsaresubjecttointernalandperiodicexternalreviews.

EquityInvestments:TheunderlyingassetsofentitiesinwhichtheBankhasequityinvestmentscarriedatfairvalueareperiodicallyfair valuedbothby fundmanagersand independentvaluationexpertsusingmarketpractices.The fair valueof investments in listedenterprisesisbasedonthelatestavailablequotedbidprices.Thefairvalueofinvestmentsinunlistedentitiesisassessedusingappropri-atemethods,forexample,discountedcashflows.ThefairvalueoftheBank’sequityparticipationsisestimatedastheBank’spercentageownershipofthenetassetvalueofthefunds.

DerivativeFinancialInstruments:Thefairvaluesofderivativefinancialinstrumentsarebasedonmarketquotationswhenpossibleorvaluationtechniquesthatusemarketestimatesofcashflowsanddiscountrates.TheBankalsousesvaluationtoolsbasedonindustrystandardpricingmodelsandvaluationtechniquestovaluederivativefinancialinstruments.Themodelsusemarket-sourcedinputssuchasinterestrates,yieldcurves,exchangeratesandoptionvolatilities.AllfinancialmodelsusedforvaluingtheBank’sfinancialinstrumentsaresubjecttobothinternalandperiodicexternalreviews.

Loans:TheBankdoesnotsellitsloans,nordoesitbelievethereisacomparablemarketforitsloans.Thefairvalueofloansreportedinthesefinancialstatementsrepresentsmanagement’sbestestimatesofthepresentvalueoftheexpectedcashflowsoftheseloans.Formulti-currencyandsinglecurrencyfixedrateloans,fairvaluesareestimatedusingadiscountedcashflowmodelbasedontheyear-endvariable lendingrate in thatcurrency,adjustedfor impairment.Forall loansnot impaired, fairvalueadjustmentsaremadetoreflectexpectedloanlosses.TheestimatedfairvalueofloansisdisclosedinNoteI.

Day One Profit and LossThebestevidenceofthefairvalueofafinancialinstrumentatinitialrecognitionisthetransactionprice(i.e.thefairvalueoftheconsiderationgivenorreceived).Againorlossmayonlyberecognizedoninitialrecognitionofafinancialinstrumentifthefairvalueofthatinstrumentisevidencedbycomparisonwithotherobservablecurrentmarkettransactionsinthesameinstrument(i.e.withoutmodificationorrepackaging)orbasedonavaluationtechniquewhosevariablesincludeonlydatafromobservablemarkets.Oninitialrecognition,againorlossmaynotberecognizedwhenusingavaluationtechniquethatdoesnotincorporatedatasolelyfromobservablemarkets.TheBankonlyrecognizesgainsorlossesafterinitialrecognitiontotheextentthattheyarisefromachangeinafactor(includingtime)thatmarketparticipantswouldconsiderinsettingaprice.Thegainorlossisamortizedoverthelifeoftheapplicableborrowingonastraight-linebasis.

Investment in AssociateUnderIAS28,“InvestmentsinAssociates”,theADFisconsideredanassociateoftheBank.AnassociateisanentityoverwhichtheBankhassignificantinfluence,butnotcontrol,overtheentity’sfinancialandoperatingpolicydecisions.TherelationshipbetweentheBankandtheADFisdescribedinmoredetailinNoteJ.IAS28requiresthattheequitymethodbeusedtoaccountforinvestmentsinassociates.Undertheequitymethod,aninvestmentinanassociateisinitiallyrecognizedatcostandthecarryingamountisincreasedordecreasedtorecognizetheinvestor’sshareoftheprofitorlossoftheinvesteeafterthedateofacquisition.Theinvestor’sshareoftheprofitorlossoftheinvesteeisrecognizedintheinvestor’sincomestatement.ThesubscriptionsbytheBanktothecapitaloftheADFoccurredbetween1974and1990.AtDecember31,2007,suchsubscriptionscumulativelyrepresentedapproximately1%oftheeconomicinterestinthecapitaloftheADF.AlthoughADFisanot-for-profitentityandhasneverdistributedanydividendtoitssubscriberssinceitscreationin1972,therevisionstoIAS28requirethattheequitymethodbeusedtoaccountfortheBank’sinvestmentintheADF.Furthermore,inaccordancewithIAS36,thenetinvestmentintheADFisassessedforimpairment.Cumulativelossesasmeasuredundertheequitymethodarelimitedtotheinvestment’soriginalcostastheADBhasnotguaranteedanypotentiallossesoftheADF.

06_ADB_part a_UK.indd 86 11/04/08 13:40:46

African Development Bank Chapter 005

Annual Report 2007 87

Property and EquipmentPropertyandequipmentismeasuredathistoricalcostlessdepreciation.Historicalcostincludesexpendituredirectlyattributabletotheacquisitionoftheitems.Subsequentcostsareincludedintheasset’scarryingamountorarerecognizedasaseparateasset,asappropri-ate,onlywhenitisprobablethatfutureeconomicbenefitsassociatedwiththeitemwillflowtotheBankandthecostoftheitemcanbemeasuredreliably.Repairsandmaintenancearechargedtotheincomestatementwhentheyareincurred.

Landisnotdepreciated.Depreciationonotherassetsiscalculatedusingthestraight-linemethodtoamortizethedifferencebetweencostandestimatedresidualvaluesoverestimatedusefullives.Theestimatedusefullivesareasfollows:

-Buildings:15-20years-Fixturesandfittings:6-10years-Furnitureandequipment:3-7years-Motorvehicles:5years

Theresidualvaluesandusefullivesofassetsarereviewedperiodicallyandadjustedifappropriate.Assetsthataresubjecttoamortizationarereviewedannuallyforimpairment.Anasset’scarryingamountiswrittendownimmediatelytoitsrecoverableamountiftheasset’scarryingamountisgreaterthanitsestimatedrecoverableamount.Therecoverableamountisthehigheroftheasset’sfairvaluelesscoststosellanditsvalueinuse.Gainsandlossesondisposalaredeterminedasthedifferencebetweenproceedsandtheasset’scarryingamountandareincludedintheincomestatementintheperiodofdisposal.

Intangible AssetsIntangibleassetsincludecomputersystemssoftwareandarestatedathistoricalcostlessamortization.Amortizationonintangibleassetsiscalculatedusingthestraight-linemethodover3-5years.

LeasesTheBankhasentered intoseveraloperating leaseagreements, including those for itsoffices inTunisiaand incertainother regionalmembercountries.Undersuchagreements,alltherisksandbenefitsofownershipareeffectivelyretainedbythelessor.Paymentsmadeunderoperatingleasesarechargedtotheincomestatementonastraight-linebasisovertheperiodofthelease.Benefitsreceivedandreceivableasan incentivetoenter intoanoperating leasearealsorecognizedonastraight-linebasisoverthe leaseterm.Whenanoperatingleaseisterminatedbeforetheleaseperiodhasexpired,anypaymentrequiredtobemadetothelessorbywayofpenaltyisrecognizedasanexpenseintheperiodinwhichtheterminationtakesplace.

Transfers Approved by the Board of GovernorsInaccordancewiththeAgreementestablishingtheBank,theBoardofGovernorsisthesoleauthorityforapprovingallocationsfromincometosurplusaccountordistributionstootherentitiesfordevelopmentpurposes.SurplusconsistsofearningsfromprioryearswhichareretainedbytheBankuntilfurtherdecisionismadeontheirdispositionortheconditionsoftransferforspecifieduseshavebeenmet.Distributionsfordevelopmentpurposes,referredtoas“BoardofGovernors’ApprovedTransfers”,arereportedasexpensesontheIncomeStatementintheyearofapproval.Transfersfordevelopmentpurposesmaybefundedfromamountspreviouslytransferredtosurplusaccountorfromthecurrentyear’sincome.

Retained EarningsRetainedearningsoftheBankconsistofamountsallocatedtoreservesfromprioryear’sincome,balanceofamountsallocatedtosurplusafterdeductingtransfersapprovedbytheBoardofGovernors,unallocatedcurrentyearnetincome,andexpensesrecognizeddirectlyinequityasrequiredbyIFRS.

Critical Accounting Judgments and Key Sources of Estimation UncertaintyInthepreparationoffinancialstatementsinconformitywithIFRS,managementmakescertainestimates,assumptionsandjudgmentsthataffect the reportedamountsofassets, liabilities, revenueandexpensesaswellas thedisclosureof contingent liabilities.Actualresultscoulddifferfromsuchestimates.Estimatesandjudgmentsarecontinuallyevaluatedandarebasedonhistoricalexperienceand

06_ADB_part a_UK.indd 87 11/04/08 13:40:46

Chapter 005 African Development Bank

Annual Report 200788

otherfactors,includingexpectationsoffutureeventsthatarebelievedtobereasonableunderthecircumstances.Themostsignificantjudgmentsandestimatesaresummarizedbelow:

1) Significant JudgmentsTheBank’saccountingpoliciesrequirethatassetsandliabilitiesbedesignatedatinceptionintodifferentaccountingcategories.Suchdecisionsrequiresignificantjudgmentandrelatetothefollowingcircumstances:

Held-for-Trading-Inclassifyingfinancialassetsorliabilitiesas“trading”,theBankhasdeterminedthatsuchassetsorliabilitiesmeetitsdescriptionandsetcriteriaforclassificationassuch.

FairValuethroughProfitandLoss-Indesignatingfinancialassetsorliabilitiesatfairvaluethroughprofitorloss,theBankhasdeter-minedthatsuchassetsorliabilitiesmeetthecriteriaforthisclassification.

Held-to-Maturity -TheBank follows theguidanceof IAS39onclassifyingnon-derivative financialassetswith fixedordeterminablepaymentsand fixedmaturityasheld-to-maturity. Inmaking this judgment, theBankevaluates its intentionandability tohold suchinvestmentstomaturity.

2) Significant estimatesTheBankalsousesestimatesforitsfinancialstatementsinthefollowingcircumstances:

ImpairmentLossesonLoansandAdvances-Ateachfinancialreportingdate,theBankreviewsitsloanportfoliosforimpairment.TheBankfirstassesseswhetherobjectiveevidenceofimpairmentexistsforindividualloans.Ifsuchobjectiveevidenceexists,impairmentisdeterminedbydiscountingexpectedfuturecashflowsusingtheloan’soriginaleffectiveinterestrateandcomparingthisamounttotheloan’snetcarryingamount.Determiningtheamountandtimingoffuturecashflowsonimpairedloansrequiressignificantjudgment.IftheBankdeterminesthatnoobjectiveevidenceofimpairmentexistsforanindividuallyassessedloan,thatloanisincludedinagroupof loanswith similar credit characteristicsandcollectivelyassessed for impairment.Objectiveevidenceof impairment foragroupofloansmayincludeobservabledataindicatingthattherehasbeenanadversechangeinthepaymentstatusofborrowersinagroup,ornationalorlocaleconomicconditionsthatcorrelatewithdefaultsonassetsinthegroup.Managementusesestimatesbasedonhistori-callossexperienceforassetswithcreditriskcharacteristicsandobjectiveevidenceofimpairmentsimilartothoseintheportfoliowhenschedulingitsfuturecashflows.Themethodologyandassumptionsusedforestimatingboththeamountandtimingoffuturecashflowsarereviewedregularlytoreduceanydifferencesbetweenlossestimatesandactuallossexperience.

FairValueofFinancialInstruments-Thefairvalueoffinancialinstrumentsthatarenotquotedinactivemarketsisdeterminedbyusingvaluationtechniques.Wherevaluationtechniques(forexample,models)areusedtodeterminefairvalues,theyarevalidatedandperi-odicallyreviewedbyqualifiedpersonnelindependentoftheareathatcreatedthem.Allvaluationmodelsarecalibratedtoensurethatoutputsreflectactualdataandcomparativemarketprices.Totheextentpractical,valuationmodelsuseonlyobservabledata;however,areassuchascreditrisk(bothownandcounterparty),volatilitiesandcorrelationsrequiremanagementtomakeestimates.Changesinassumptionsaboutthesefactorscouldaffectthereportedfairvalueoffinancialinstruments.

ImpairmentofAvailable-for-SaleEquityInvestments-TheBankdeterminesthatavailable-for-saleequityinvestmentsareimpairedwhentherehasbeenasignificantorprolongeddeclineinfairvaluebelowthecarryingamount.Thedeterminationofwhatissignificantorprolongedrequiresjudgment.Inmakingthisjudgment,theBankevaluatesanyevidenceofdeteriorationinthefinancialhealthoftheinvestee,industryandsectorperformance,changesintechnology,andoperationalandfinancingcashflows.

06_ADB_part a_UK.indd 88 11/04/08 13:40:47

African Development Bank Chapter 005

Annual Report 2007 89

NOTE C – THE EFFECT OF NEW AND REVISED INTERNATIONAL FINANCIAL REPORTING STANDARDS

In2007,theBankadoptedInternationalFinancialReportingStandard(IFRS)7,FinancialInstruments:Disclosuresandrelatedamend-mentstoInternationalAccountingStandard(IAS)1,PresentationofFinancialStatements–CapitalDisclosures.IFRS7supersedesIAS30,DisclosuresintheFinancialStatementsofBanksandSimilarFinancialInstitutionandIAS32,FinancialInstruments:Presentation,andintroducesnewandenhancedqualitativeandquantitativedisclosuresaboutexposurestorisksarisingfromfinancialinstrumentsandhowtheBankmanagesthoserisks.TheamendmentstoIAS1requirenewdisclosuresontheBank’sobjectives,policiesandprocessesformanagingcapital.ThenewdisclosuresarepresentedinNoteD.

Atthedateofauthorizationofthesefinancialstatements,certainnewandamendedInternationalFinancialReportingStandardsandInterpretationshavebeenissuedandwillbecomeeffectiveforperiodsafterDecember31,2007. IFRS8,OperatingSegments,whichbecomeseffectiveforfinancialstatementsfortheperiodbeginningJanuary1,2009,replacesthesegmentalreportingrequirementsofIAS14,SegmentReporting,andrequiresalignmentofthesegmentsinthefinancialstatementswiththoseusedinternallybymanage-ment in theallocationof resourcesandassessingperformance.Theamendments to IAS1 require theBank to present in separatestatements, changes in equity related to its shareholders and those related to comprehensive income (i.e., non-shareholder-relatedcomponents),includingrelatedreclassificationadjustmentsofthosecomponents.ItalsorequiresthepresentationofabalancesheetasatthebeginningoftheearliestcomparativeperiodinacompletesetoffinancialstatementswhentheBankappliesanaccountingpolicyretrospectivelyormakesa retrospective restatement.Noneof thesenewstandardsoramendments isexpectedtohaveasignificantimpactontheBank’sfinancialstatements.

OnFebruary14,2008,theInternationalAccountingStandardsBoard(IASB)issuedamendmentstoIAS32andIAS1.Theamendmentsrequireanentitytoclassifyaspartofitsequitythosefinancialinstrumentsthatitissuesthatareeither(a)puttablefinancialinstruments,or(b)financialinstrumentsorcomponentsoffinancialinstrumentsthatimposeanobligationtodelivertoanotherpartyapro-ratashareofitsnetassetsonlyonliquidation,ifcertaincriteriaaremet.Priortotheseamendments,suchfinancialinstrumentsweretobeclassifiedasliabilities.TheamendmentsareeffectiveforannualperiodsbeginningonorafterJanuary1,2009,withearlyadoptionpermitted.

SubscriptionsbythemembercountriestotheBank’scapitaldescribedinNoteBareputtablefinancialinstrumentsthatmeettherequire-mentsforequityclassificationundertheamendedstandards.Whilethestandardspriortotheamendmentsrequiredliabilityclassificationbytheissuerofputtablefinancialinstruments,theBankhasalwaysreportedthesubscriptionsbythemembercountriestoitscapitalasequity.UndertheAgreementestablishingtheBank,suchinstrumentsprovideanequalandresidualrighttoitsmembercountriesthataresubordinatetotherightsofitscreditors.TheequityclassificationrequirementsundertheamendedstandardsarefullyconsistentwithandconfirmtheBank’spriorclassificationoftheseinstrumentsasequity.TheamendmentstoIAS32andIAS1relatingtoputtablefinancialinstrumentswereissuedafterthebalancesheetdatebutbeforetheapprovalofthefinancialstatements.TheBankhasoptedtoearlyadopttheamendments.TheapplicationoftheseamendedstandardshadnoeffectsontheBank’sfinancialstatements.

NOTE D - RISK MANAGEMENT POLICIES AND PROCEDURES

Incarryingoutitsdevelopmentmandate,theBankseekstomaximizeitscapacitytoassumecorebusinessrisksresultingfromitslendingandinvestingoperationswhileatthesametimeminimizingitsnon-corebusinessrisks(marketrisk,counterpartyrisk,andoperationalrisk)thatareincidentalbutneverthelesscriticaltotheexecutionofitsmandate.

ThedegreeofrisktheBankiswillingtoassumetoachieveitsdevelopmentmandateislimitedbyitsrisk-bearingcapacity.Thisinstitu-tionalriskappetiteisembodiedintheBank’scapitaladequacypolicyanditscommitmenttomaintainaprudentriskprofileconsistentwiththehighestcreditrating.

The policies, processes and procedures by which the Bank manages its risk profile continually evolve in response to market, credit,product,andotherdevelopments.ThehighestlevelofriskmanagementoversightisassuredbytheBank’sBoardofExecutiveDirectors,

06_ADB_part a_UK.indd 89 11/04/08 13:40:47

Chapter 005 African Development Bank

Annual Report 200790

whichischairedbythePresident.Inadditiontoapprovingallriskmanagementpolicies,theExecutiveDirectorsregularlyreviewtrendsintheBank’sriskprofilesandperformancetoensurecompliancewiththeunderlyingpolicies.

Theguidingprinciplesbywhich theBankmanages itscoreandnon-core risksaregovernedby theGeneralAuthorityontheBank’sFinancialProductsandServices(theFPSAuthority)andtheGeneralAuthorityonAssetLiabilityManagement(theALMAuthority).

TheFPSAuthorityprovidestheframeworkunderwhichtheBankdevelopsandimplementsfinancialproductsandservicesforitsborrow-ers’andseparateguidelineswhichprescribetherulesgoverningthemanagementofcreditandoperationalriskfortheBank’ssovereignandnon-sovereignloanandequityinvestmentportfolios.

TheALMAuthorityistheoverarchingframeworkthroughwhichManagementhasbeenvestedwiththeauthoritytomanagetheBank’sfinancialassetsand liabilitieswithindefinedparameters.TheALMAuthority setsout theguidingprinciples formanaging theBank’sinterestraterisk,currencyexchangeraterisk,liquidityrisk,counterpartycreditriskandoperationalrisk.TheALMAuthoritycoverstheBank’sentirearrayofALMactivitiessuchasdebt-fundingoperationsandinvestmentofliquidresources.ItalsoincludestheinterestrateandcurrencyriskmanagementaspectsoftheBank’slendingandequityinvestmentoperations.

UndertheumbrellaoftheFPSAuthorityandtheALMAuthority,thePresidentisauthorizedtoapproveandamendmoredetailedopera-tionalguidelinesasnecessary,upontherecommendationsoftheAssetandLiabilityManagementCommittee(ALCO).ALCOistheotheroversightandcontrolorganoftheBank’sriskmanagementactivities.ItistheBank’smostseniormanagementforumonriskmanage-mentissuesandischairedbytheVicePresidentforFinance.

ALCOmeetsonaregularbasistoperformitsoversightrole.AmongALCO’skeyfunctions, itreviewsregularandad-hocfinanceandriskmanagementreportsandprojections,approvesstrategiestoadjustthebalancesheet,andconfirmscountryandprojectcreditriskratingsandtheassociatedincurredlossestimates.ALCOissupportedbyseveralstandingworkinggroupsthatreportonspecificissuesincludingcountryrisk,non-sovereigncreditrisk,counterpartycreditrisk,interestraterisk,currencyrisk,operationalrisk,financialprojec-tions,andfinancialproductsandservices.

Day-to-dayoperationalresponsibilityforimplementingtheBank’sriskmanagementpoliciesandguidelinesisdelegatedtotheappro-priatebusinessunits,andtheFinancialManagementDepartmentisresponsibleformonitoringtheday-to-daycompliancewiththosepoliciesandguidelines.

ThefollowingsectionsdescribeindetailthemannerinwhichtheindividualsourcesofriskaremanagedbytheBank.

Credit RiskCreditriskisthepotentialfinanciallossduetodefaultofoneormoredebtors/obligors.CreditriskisthelargestsourceofriskfortheBankarisingessentiallyfromitslendingandtreasuryoperations.

TheBankmanagesthreeprincipalsourcesofcreditrisk:(i)sovereigncreditriskonitspublicsectorportfolio;(ii)non-sovereigncreditriskonitsportfolioofprivatesector,non-sovereignandenclaveprojects;and(iii)counterpartycreditriskonitsportfoliooftreasuryinvest-mentsandderivativetransactions.Theserisksaremanagedwithinanintegratedframeworkofcreditpolicies,guidelinesandprocesses,whicharedescribedinmoredetailinthefollowingsections.

1) Sovereign Credit RiskWhentheBanklendstopublicsectorborrowers,itgenerallyrequiresafullsovereignguaranteeortheequivalentfromtheborrowingmemberstate.Inextendingcredittosovereignentities,itisexposedtocountryriskwhichincludespotentiallossesarisingfromacoun-try’sinabilityorunwillingnesstoserviceitsobligationstotheBank.TheBankmanagescountrycreditriskthroughfinancialpoliciesandlendingstrategies,includingindividualcountryexposurelimitsandoverallcreditworthinessassessments.Theseincludetheassessmentofthecountry’smacroeconomicperformanceaswellasitssociopoliticalconditionsandfuturegrowthprospects.

06_ADB_part a_UK.indd 90 11/04/08 13:40:48

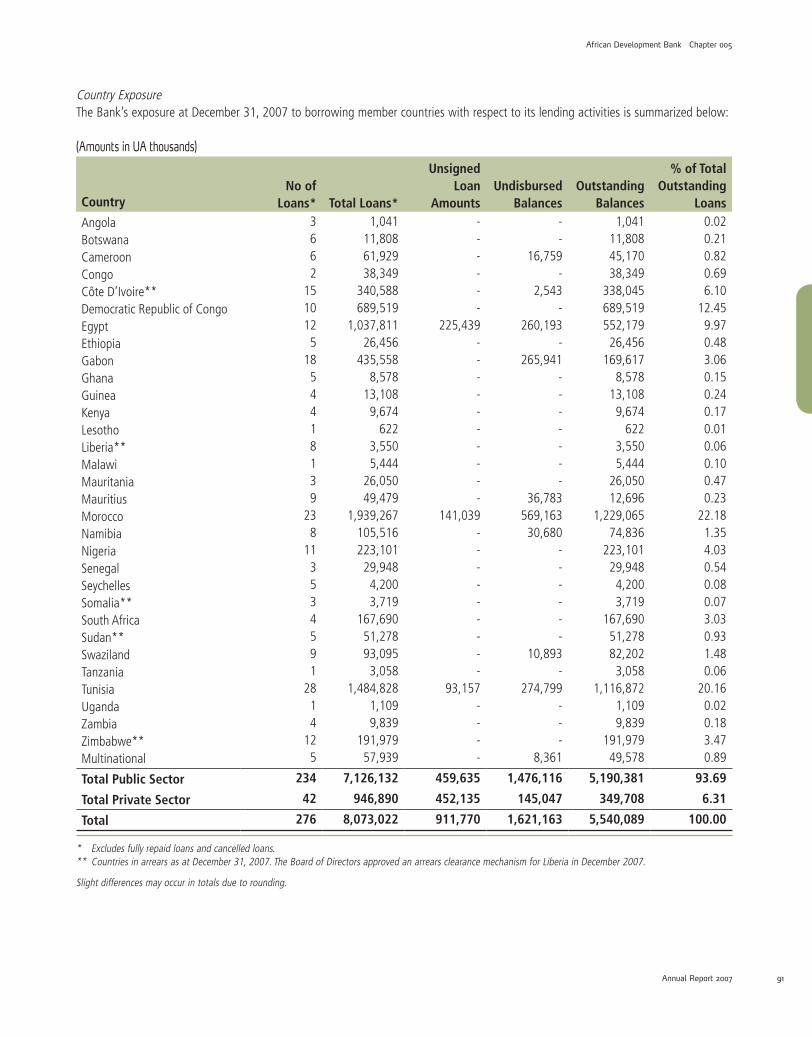

CountryExposureTheBank’sexposureatDecember31,2007toborrowingmembercountrieswithrespecttoitslendingactivitiesissummarizedbelow:

(Amounts in UA thousands)

CountryNo of

Loans* Total Loans*

Unsigned Loan

AmountsUndisbursed

BalancesOutstanding

Balances

% of Total Outstanding

LoansAngolaBotswanaCameroonCongoCôteD’Ivoire**DemocraticRepublicofCongoEgyptEthiopiaGabonGhanaGuineaKenyaLesothoLiberia**MalawiMauritaniaMauritiusMoroccoNamibiaNigeriaSenegalSeychellesSomalia**SouthAfricaSudan**SwazilandTanzaniaTunisiaUgandaZambiaZimbabwe**Multinational

3662

1510125

1854418139

238

113534591

2814

125

1,04111,80861,92938,349

340,588689,519

1,037,81126,456

435,5588,578

13,1089,674

6223,5505,444

26,05049,479

1,939,267105,516223,10129,9484,2003,719

167,69051,27893,0953,058

1,484,8281,1099,839

191,97957,939

------

225,439----------

141,039---------

93,157----

--

16,759-

2,543-

260,193-

265,941-------

36,783569,16330,680

------

10,893-

274,799---

8,361

1,04111,80845,17038,349

338,045689,519552,17926,456

169,6178,578

13,1089,674

6223,5505,444

26,05012,696

1,229,06574,836

223,10129,9484,2003,719

167,69051,27882,2023,058

1,116,8721,1099,839

191,97949,578

0.020.210.820.696.10

12.459.970.483.060.150.240.170.010.060.100.470.23

22.181.354.030.540.080.073.030.931.480.06

20.160.020.183.470.89

Total Public Sector 234 7,126,132 459,635 1,476,116 5,190,381 93.69

Total Private Sector 42 946,890 452,135 145,047 349,708 6.31

Total 276 8,073,022 911,770 1,621,163 5,540,089 100.00

* Excludesfullyrepaidloansandcancelledloans.** CountriesinarrearsasatDecember31,2007.TheBoardofDirectorsapprovedanarrearsclearancemechanismforLiberiainDecember2007.

Slightdifferencesmayoccurintotalsduetorounding.

African Development Bank Chapter 005

Annual Report 2007 91

06_ADB_part a_UK.indd 91 11/04/08 13:40:48

SystematicCreditRiskAssessmentThefoundationoftheBank’screditriskmanagementframeworkisasystematiccreditriskassessmentbasedonauniforminternalcreditriskratingscalethatiscalibratedtoreflecttheBank’sstatisticallossexpectationsasshowninthefollowingtable.

Risk Rating Description Risk Class International Equivalent1 Excellent VeryLowRisk A-BBB2 VeryGood LowRisk BB3 Good

ModerateRisk B4 Fair5 Acceptable

HighRisk CCC6 Marginal7 SpecialAttention

VeryHighRisk <CCC8 Substandard9 Doubtful10 KnownLoss

These sovereign risk credit ratingsarederived froma riskassessmenton five risk indices that includemacroeconomicperformance,debtsustainability,sociopoliticalfactors,businessenvironmentandportfolioperformance.Thesefiveriskindicesarecombinedtoderiveacompositesovereigncountryriskindexandacompositenon-sovereigncountryriskindexwhichinturnareconvertedintoseparatecountryriskratingforthesovereignandnon-sovereignportfolios.Thesecountryriskratingsarevalidatedagainsttheaveragecountryriskratingsfromaccreditedratingagenciesandotherspecializedinternationalbodies.TheALCOreviewsthecountryratingsonaquar-terlybasistoensurecompliancewithcountryexposurelimits,changesincountrycreditriskconditions,andtoapprovechangesinlossprovisioning,ifany.

PortfolioRiskMonitoringIn2007,theoverall riskprofileof theBank’ssovereignguaranteedportfolio improvedslightly,mainlyduetothecombinedeffectofimprovement in theweightedaveragecredit ratingofcertain regionalmembercountriesand theBank’s increasedexposure tohighgradedcountries.

Theportfolio’sweighted-averageriskratingshowedamarginalstrengtheningfrom2.93attheendof2006to2.67attheendof2007.ThedistributionofthesovereignportfolioacrosstheBank’sfivecreditriskclassesisshowninthetablebelow.

Risk Profile of the Outstanding Sovereign-Guaranteed Loan Portfoliovery Low Risk Low Risk Moderate Risk High Risk very High Risk

2007 37% 31% 8% 15% 9%2006 28% 35% 10% 17% 10%

2005 26% 26% 18% 17% 13%

2004 28% 28% 21% 11% 12%

2003 25% 32% 21% 16% 6%

It is theBank’spolicy that if thepaymentofprincipal, interestorotherchargeswith respect toanyBankGroupcreditbecomes30daysoverdue,nonewloanstothatmembercountry,ortoanypublicsectorborrowerinthatcountry,willbepresentedtotheBoardofDirectorsforapproval,norwillanypreviouslyapprovedloanbesigned,untilallarrearsarecleared.Furthermore,forsuchcountries,disbursementsonallloanstoorguaranteedbythatmembercountryaresuspendeduntilalloverdueamountshavebeenpaid.Thesecountriesalsobecomeineligibleinthesubsequentbillingperiodforawaiverof0.50%onthecommitmentfeeschargedonqualifyingundisbursedloans.

Chapter 005 African Development Bank

Annual Report 200792

06_ADB_part a_UK.indd 92 11/04/08 13:40:49

African Development Bank Chapter 005

Annual Report 2007 93

AlthoughtheBankbenefitsfromtheadvantagesofpreferredcreditorstatusandrigorouslymonitorstheexposureonnon-performingsovereignborrowers, somecountrieshaveexperienceddifficulties to service theirdebts to theBankona timelybasis.Aspreviouslydescribed,theBankmakesprovisionsforimpairmentinitssovereignloanportfoliocommensuratewiththeassessmentoftheincurredlossinsuchportfolio.

Tocoverpotentialunexpectedcredit-related lossesdue toextremeandunpredictableevents, theBankmaintainsaconservative riskcapitalcushionforsovereigncredit risks.TheBank’scapitaladequacypolicyarticulatesdifferentiatedriskcapital requirementsforallcredit-sensitiveassets (loansandequity investments)plus contingent liabilities (guaranteesandclient riskmanagementproducts) ineachriskclass1.Attheendof2007,theBank’spublicsectorloanportfoliousedup37%oftheBank’stotalriskcapitalbasedontheBank’scapitaladequacyframework.Thiscompareswith45%attheendof2006andreflectstheimprovementinthecompositionofthesovereignportfolio.TheBankdefinesriskcapitalasthesumofpaid-incapitalplusaccumulatedreservesnetoftranslationadjustments.Callablecapitalisnotincludedinthecomputationofriskcapital.

2) Non-Sovereign Credit RiskWhentheBanklendstoprivatesectorborrowersortoenclaveprojectsitdoesnotbenefitfromfullsovereignguarantees.TheBankmayalsoprovidefinancingtocreditworthycommerciallyorientedentitiesthatarepubliclyowned,withoutasovereignguarantee.

Toassessthecreditriskofnon-sovereignprojectsorfacilities,theBankusesasimilaruniforminternalcreditriskratingasforsovereignprojects.However,theseinternalcreditratingsarederivedonthebasisoffourmajorgroupsoffactors.

Thefirstfactorinvolvestheoverallevaluationandassessmentoftheprojectcompany’sfinancialstrength.Thisassessmentlooksat:1)capacityoftheprojecttogeneratesufficientcashflowtoserviceitsdebt;2)thecompany’soperatingperformanceandprofitability;3)theprojectcompany’scapitalstructure,financialflexibilityandliquiditypositions.

Secondly,thefollowing,fourmainnon-financialparametersareanalyzed:1)theoutlookoftheindustryinwhichtheprojectcompanyoperates;2)thecompetitivepositionoftheprojectcompanywithintheindustry;3)thestrengthoftheprojectcompany’smanagementwithparticularemphasisonitsabilitytodealwithadverseconditions;4)thequalityoftheinformationonwhichtheanalysisisbased.

Thirdly,theriskfactorsthatconsiderthestructureofthefacilityintermsofmaturity,theexistenceofthirdpartyguarantee,thevalueofanyassignedcollateral,andothercreditenchancementareextensivelyexamined.

Finally,theprojectcompany’sriskratingisadjustedtoreflecttheoverallhostcountryriskrating.

Allnewnon-sovereignprojects requireaminimum initialcredit ratingandundergo rigorousprojectapproval.TheALCOreviews thenon-sovereigncreditratingofeachprojectonaquarterlybasisandmayrecommendchangesifjustifiedbyevolvingcountryandprojectconditions.

In2007,theBankincreaseditsinvestmentsinthenon-sovereignloanandequityportfolios.Theweighted-averageriskratinghaddete-rioratedmarginallyfrom3.52attheendof2006to3.82atyear-end2007.Thedistributionofthenon-sovereignportfolioacrosstheBank’sfivecreditriskclassesisshowninthetablebelow.

1 Reflectingitshigherriskoperatingenvironmentandunavoidableportfolioconcentrations,theBankrequiresriskcapitalbackingthatisthreetotentimesmoreconservativethanBiScommercialbankingstandards.Verylowrisk=25%,lowrisk=28%,moderaterisk=35%,highrisk=50%,veryhighrisk=75%,andequityinvestments=100%.

06_ADB_part a_UK.indd 93 11/04/08 13:40:49

Chapter 005 African Development Bank

Annual Report 200794

Risk Profile of the Outstanding Non-Sovereign Loan and Equity Portfolio very Low Risk Low Risk Moderate Risk High Risk very High Risk

2007 8% 10% 46% 31% 5%

2006 16% 15% 52% 6% 11%2005 14% 20% 56% 7% 3%2004 15% 14% 55% 10% 6%2003 - 20% 62% 10% 8%

IncompliancewiththerevisedIFRS,theBanknolongermakesgeneralprovisionstocovertheexpectedlossesintheperformingnon-sovereignportfolio.Forthenon-performingportfolio,theBankmakesaspecificprovisionbasedonanassessmentofthecreditimpair-ment,orincurredloss,oneachloan.Attheendof2007,theimpairmentallowancetocovertheincurredlossonimpairedloansinthenon-sovereignportfoliodecreasedmarginallytoUA12.13millionasacomparisontoUA15.40millionin2006becauseofthereductioninthesizeoftheportfolioofimpairednon-sovereignloans.

Inadditiontoprivatesectorlending,theBankmakesequityinvestmentsinprivatesectorprojects,eitherdirectlyorthroughinvestmentfunds.Totheextentpossible,equityinvestmentsarecarriedatfairvalue.Intheeventthatthefairvalueofanequityinvestmentcannotbereliablydetermined,itiscarriedatamortizedcost,andperiodicallyassessedforimpairment.TheBankrecognizeslossprovisionbasedonacceptedimpairmenttestsmeasuredagainstthecarryingcostoftheequityinvestment.Attheendof2007,theprovisionforimpair-mentonequityinvestmentwasequivalentto6.58%oftheoutstandingequityportfolio.

Tocoverpotentialunexpectedcreditrelatedlossesduetoextremeandunpredictableevents,theBankmaintainsaconservativeriskcapi-talcushionfornon-sovereigncreditrisks.Attheendof2007,theBank’snon-sovereignportfoliorequiredasriskcapitalapproximately5.3%oftheBank’stotalon-balancesheetriskcapitalsources,slightlyabovethelevelattheendof2006.Thiswasstillwellbelowthelimitof20%determinedbytheBankfortotalnon-sovereignoperations.

CreditExposureLimitsTheBankoperatesasystemofexposurelimitstoensurethedevelopmentofanadequatelydiversifiedportfolio.TheBankmanagescreditriskatthegloballevel(combinedsovereignguaranteedandnon-sovereignguaranteedportfolios)byensuringthatintheaggregate,thetotalcountryexposurelimitdoesnotexceed15%ofthemaximumsustainableportfolio.Themaximumsustainableportfolioisdeter-minedasthelargestoutstandingportfolio(outstandingloanspluspotentialnewlending)thatcanbesupportedbythecurrentlevelofriskcapitalapplyingtheBank’scapitaladequacypolicy.Eachspecificcountrylimitisbasedontheeconomicpotentialofthecountryandperceivedrisklevel.Countryexposurelimitsarereviewedannuallyandareusedasarisk-basedbenchmarktoplantheBank’smedium-termcountryassistancestrategies.

Thecreditexposureonthenon-sovereignportfolioisfurthermanagedbylimitingexposurestocertainindustrysectors,equityinvest-mentsandsingleobligor.Inaddition,theBankgenerallyrequiresarangeofsecuritiesandguaranteesfromprojectsponsorstopartiallymitigatethecreditriskfordirectprivatesectorloans.

3) Counterparty Credit RiskInthenormalcourseofbusiness,theBankutilizesvariousfinancialinstrumentstomeettheneedsofitsborrowers,manageitsexposureto fluctuations inmarket interestandcurrencyrates,andtotemporarily invest its liquidresourcesprior todisbursement.Allof thesefinancialinstrumentsinvolve,tovaryingdegrees,theriskthatthecounterpartytothetransactionmaybeunabletomeetitsobligationtotheBank.

GiventhenatureoftheBank’sbusiness,itisnotpossibletocompletelyeliminatecounterpartycreditrisk,however,theBankminimizesthisriskbyexecutingtransactionswithinaprudentialframeworkofapprovedcounterparties,minimumcreditratingstandards,counter-partyexposurelimits,andcounterpartycreditriskmitigationmeasures.

06_ADB_part a_UK.indd 94 11/04/08 13:40:50

African Development Bank Chapter 005

Annual Report 2007 95

CounterpartiesmustmeettheBank’sminimumcreditratingrequirementsandareapprovedbytheBank’sVicePresidentforFinance.Forlocalcurrencyoperations,lessstringentminimumcreditratinglimitsarepermittedinordertoprovideadequateavailabilityofinvestmentopportunitiesandderivativecounterpartiesforimplementingappropriateriskmanagementstrategies.ALCOapprovescounterpartiesthatareratedbelowtheminimumratingrequirements.

Counterpartiesareclassifiedasinvestmentcounterparties,derivativecounterparties,andtradingcounterparties.Theirratingsarecloselymonitored.

TradingcounterpartiesaregenerallyratedA/A2.

Thefollowingtabledetailstheminimumcreditratingsforauthorizedinvestmentcounterparties:

Maturity6 months 1 year 5 years 10 years 15 years 30 years

Government A/A2 AA-/Aa3 AAA/AaaGovernmentAgenciesandSupranationals

A/A2 AA-/Aa3 AAA/Aaa

Banks A/A2 AA-/Aa3 AAA/AaaCorporationsincludingnonbankfinancialinstitutions

A/A2 AA-/Aa3 AAA/Aaa

MBS/ABS Nomaturitylimit,butrepaymentprojectionsmandatory

TheBankalsoinvestsinmortgage-backedandasset-backedsecuritieswithaminimumratingofAAA/Aaa;moneymarketmutualfundswithaminimumratingofAA-/Aa3;andentersintocollateralizedsecuritiesrepurchaseagreements.

Asarule,theBankexecutesanISDAmasteragreementandnettingagreementwithitsderivativecounterpartiespriortoundertakinganytransactions.DerivativecounterpartiesarerequiredtoberatedAA-/Aa3byatleasttwoapprovedratingagenciesorA-forcounterpartieswithwhomtheBankhasenteredintoacollateralexchangeagreement.Approvedtransactionswithderivativecounterparties includeswaps,forwards,optionsandotherover-the-counterderivatives.

Inadditiontotheseminimumratingrequirements,theBankoperateswithinaframeworkofexposurelimitsbasedonthecounterpartycreditratingandsize,subjecttoamaximumof8%oftheBank’stotalriskcapitalforanysinglecounterparty.Individualcounterpartycredit exposures are aggregated across all instruments using the Bank for International Settlements (BIS) potential future exposuremethodologyandmonitoredregularlyagainsttheBank’screditlimitsafterconsideringthebenefitsofanycollateral.

Asshowninthefollowingtable,theestimatedpotentialcounterpartycreditexposureoftheinvestmentandderivativeportfolioscontin-uestobepredominantlyAAorhigherrated.

Credit Risk Profile of the Investment and Derivative Portfolios

AAA AA A

2007 43% 54% 3%

2006 56% 39% 5%

2005 56% 36% 8%

2004 62% 36% 2%

2003 67% 27% 6%

06_ADB_part a_UK.indd 95 11/04/08 13:40:50