the american dream: owning a car and a home finances part 4

TRANSCRIPT

THE AMERICAN DREAM: OWNING A CAR AND A HOME

Finances Part 4

Mortgages

A home mortgage is an installment loan designed specifically to finance a home.

A down payment is the amount of money you must pay up front in order to be given a mortgage or other loan.

Closing costs are fees you must pay in order to be given the loan. They may include a variety of direct costs, or fees charged as points, where each point is 1% of the loan amount. In most cases, lenders are required to give you a clear assessment of closing costs before you sign for the loan.

Choosing or Refinancing a Loan

The primary factors in determining loan payments are interest rate and loan term.

Other factors include: Understand the loan. Is a down payment required? What fees and closing costs are required? Watch out for fine print.

Other Factors Continued

Be very careful of offers to refinance loans. Always consider these two factors:

1. How long will it take before your monthly savings cover the fees and closing costs you must pay for the new loan?

2. Remember that refinancing “resets the clock” on a loan.

Fixed Rate Mortgages

The simplest type of home loan is a fixed rate mortgage, in which you are guaranteed that the interest rate will not change over the life of the loan.

Most fixed rate loans have a term of 15 or 30 years.

We use the loan payment formula (from student loan discussion) to calculate payments on home mortgages.

Side note: The word mortgage comes from Latin and old French and means “dead pledge.”

Comparing Loan Options

You need a $200,000 loan. Compare monthly payments and total loan burden. Option 1: a 30-year loan at an APR of 8%. Option 2: a 15-year loan at an APR of 7%.

You need a $60,000 loan. Compare monthly payments and total loan burden. Option 1: a 30-year loan at an APR of 7.15%. Option 2: a 15-year loan to an APR of 6.8%.

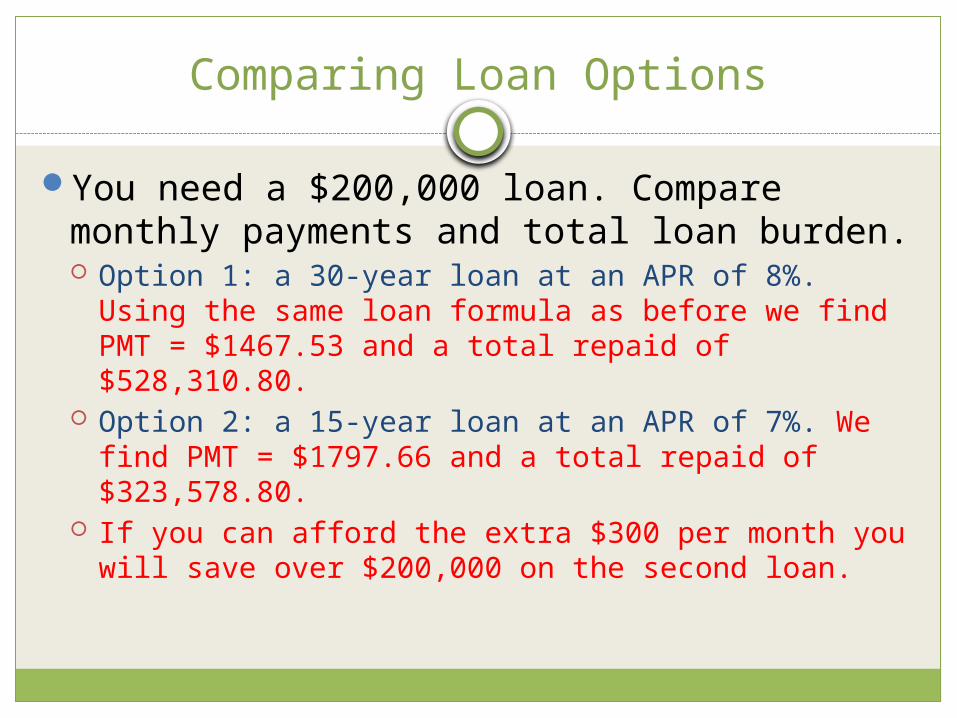

Comparing Loan Options

You need a $200,000 loan. Compare monthly payments and total loan burden. Option 1: a 30-year loan at an APR of 8%. Using the

same loan formula as before we find PMT = $1467.53 and a total repaid of $528,310.80.

Option 2: a 15-year loan at an APR of 7%. We find PMT = $1797.66 and a total repaid of $323,578.80.

If you can afford the extra $300 per month you will save over $200,000 on the second loan.

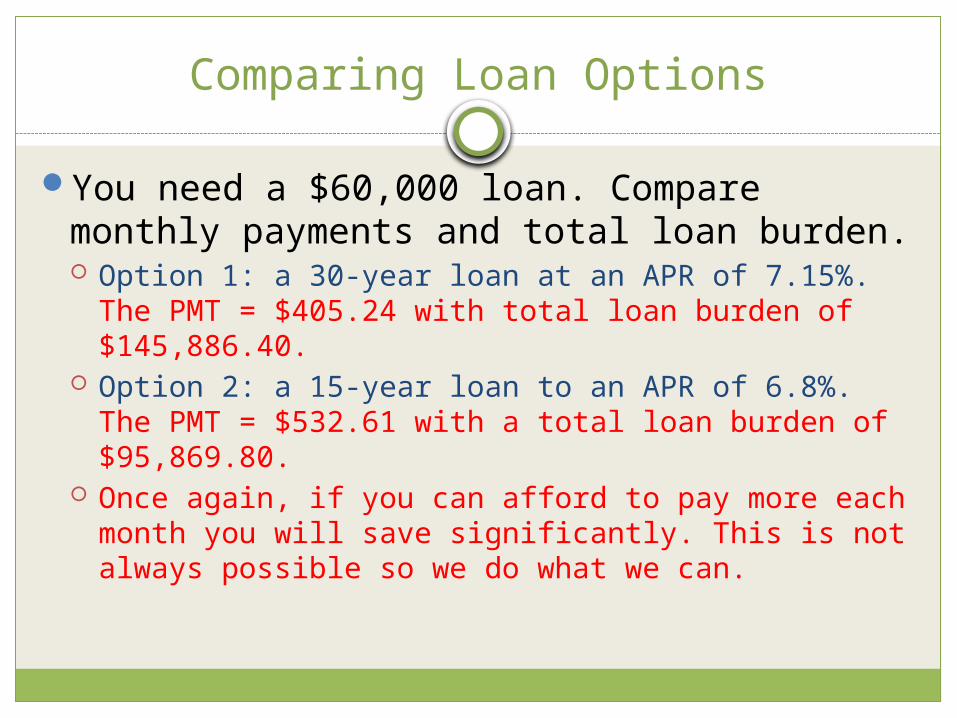

Comparing Loan Options

You need a $60,000 loan. Compare monthly payments and total loan burden. Option 1: a 30-year loan at an APR of 7.15%. The PMT

= $405.24 with total loan burden of $145,886.40. Option 2: a 15-year loan to an APR of 6.8%. The PMT

= $532.61 with a total loan burden of $95,869.80. Once again, if you can afford to pay more each month

you will save significantly. This is not always possible so we do what we can.

Closing Costs

You need a $120,000 mortgage. Calculate the monthly payment and total closing costs for each option. Which would you choose?

1. Choice 1: 30-year fixed rate of 8% with closing costs of $1200 and no points. Choice 2: 30-year fixed rate of 7.5% with closing costs of $1200 and 2 points.

2. Choice 1: 30-year fixed rate of 8.5% with no closing costs and no points. Choice 2: 30-year fixed rate of 7.5% with closing costs of $1200 and 4 points.

Closing Costs Solutions

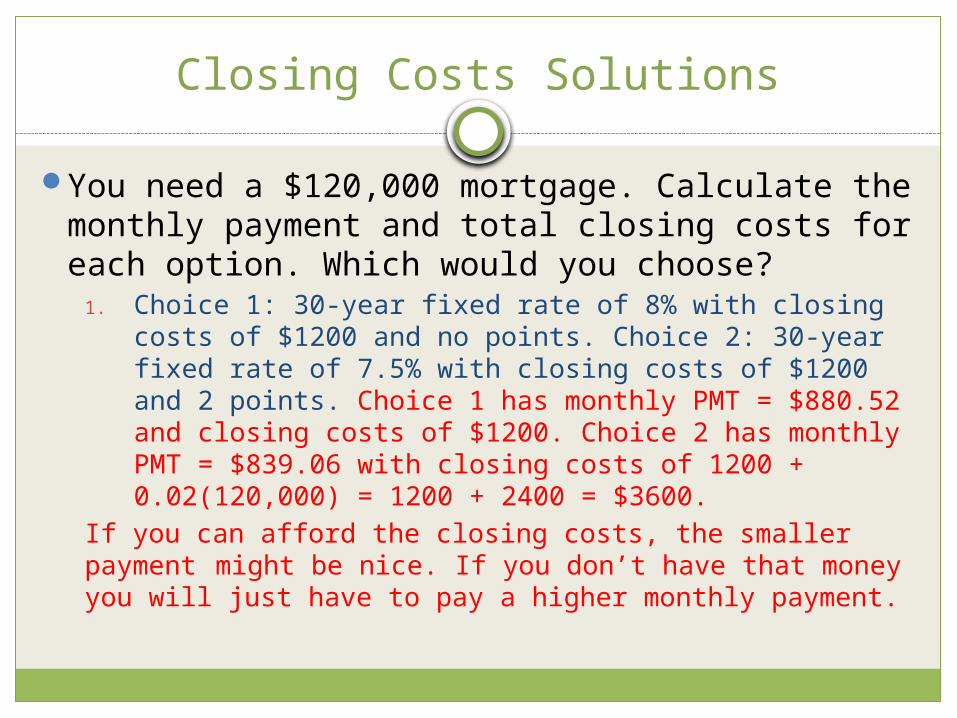

You need a $120,000 mortgage. Calculate the monthly payment and total closing costs for each option. Which would you choose?

1. Choice 1: 30-year fixed rate of 8% with closing costs of $1200 and no points. Choice 2: 30-year fixed rate of 7.5% with closing costs of $1200 and 2 points. Choice 1 has monthly PMT = $880.52 and closing costs of $1200. Choice 2 has monthly PMT = $839.06 with closing costs of 1200 + 0.02(120,000) = 1200 + 2400 = $3600.

If you can afford the closing costs, the smaller payment might be nice. If you don’t have that money you

will just have to pay a higher monthly payment.

Closing Costs Solutions

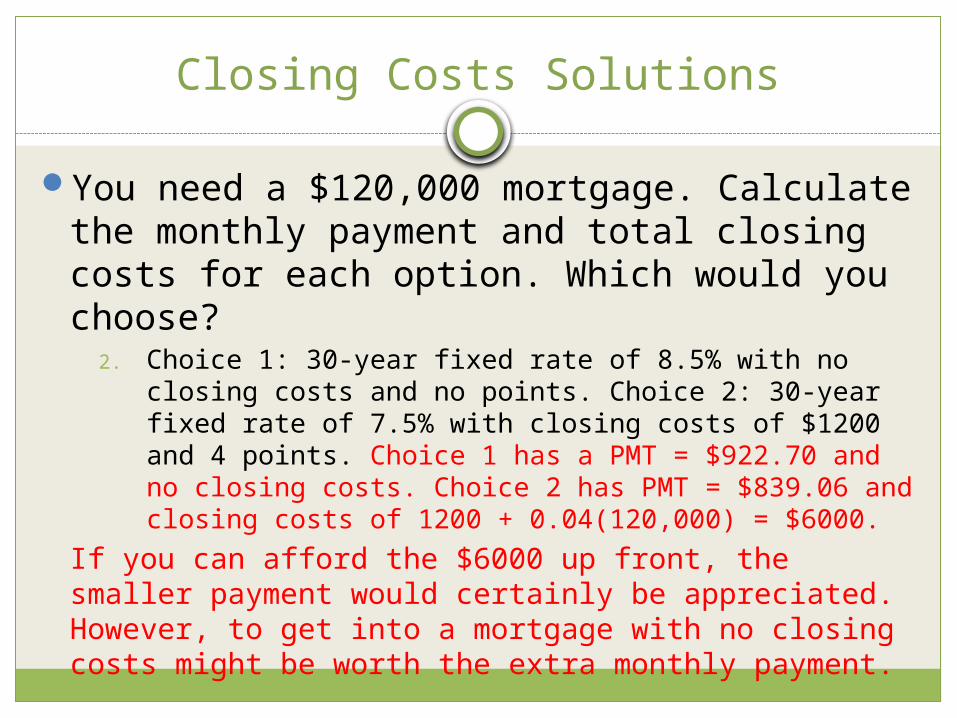

You need a $120,000 mortgage. Calculate the monthly payment and total closing costs for each option. Which would you choose?

2. Choice 1: 30-year fixed rate of 8.5% with no closing costs and no points. Choice 2: 30-year fixed rate of 7.5% with closing costs of $1200 and 4 points. Choice 1 has a PMT = $922.70 and no closing costs. Choice 2 has PMT = $839.06 and closing costs of 1200 + 0.04(120,000) = $6000.

If you can afford the $6000 up front, the smaller payment would certainly be appreciated. However, to get into a mortgage with no closing costs might be worth the extra monthly payment.

Prepayment Strategies

As the terms of a home mortgage are so long, the initial payments are almost entirely interest and very little principal.

Every extra dollar you can pay over your payment will be applied to the principal. That is one less dollar that accrues interest in the long life of the loan.

Accelerated Payments

Suppose you have a loan of $117,500 at an APR of 4%.

1. What would be your monthly payments for a 30 year loan?

2. What would be your monthly payments for a 15 year loan?

3. If your loan is set up for 30 years and you wanted to pay it off in 15, how much extra should you pay each month?

4. Compare the total amounts paid in each loan.

Accelerated Payment Solutions

Suppose you have a loan of $117,500 at an APR of 4%.1. What would be your monthly payments for a 30 year loan?

PMT = $560.96.2. What would be your monthly payments for a 15 year loan?

PMT =$869.13.3. If your loan is set up for 30 years and you wanted to pay it

off in 15, how much extra should you pay each month? You should pay an extra 869.13 – 560.96 = $308.17 each month.

4. Compare the total amounts paid in each loan. For the first loan you pay a total of $201,945.60 but for the 15-year loan you only pay $156,443.40. If you can make the accelerated payments you will save over $50,000 on the cost of your house.

Adjustable Rate Mortgage(aka a horrible decision)

A fixed rate mortgage guarantees that your monthly payments never change. This is bad for lenders if the interest rates rise.

Lenders can lessen the risk of losing out by charging a higher APR for a longer term loan. That is why 30 year loans generally have a higher APR than 15 year loans.

An even better idea (for the lenders) is to offer an adjustable rate mortgage.

ARM

Your interest rate will change based on the economy.

You could have a sweet home loan paying $550 per month for several years but then the market tanks and your interest rate changes and the bank expects you to pay $1800 per month for the same loan.

Most ARMs include a rate cap, that is, a rate that the APR can never go higher than.

Rate Approximation for ARMs

You have a choice between a 30-year fixed rate loan at 8.5% and an ARM with a first-year rate of 5.5%. Neglecting compounding and changes in principal, estimate your monthly savings with the ARM during the first year on a $125,000 loan.

Suppose that the ARM rate rises to 10 % at the start of the second year. Approximately how much extra will you then be paying over what you would have paid if you had taken the fixed rate loan?

Rate Approximation for ARMs

You have a choice between a 30-year fixed rate loan at 8.5% and an ARM with a first-year rate of 5.5%. Neglecting compounding and changes in principal, estimate your monthly savings with the ARM during the first year on a $125,000 loan.

The 30-yr fixed rate loan has PMT = $961.14. The payment for the first year of the ARM would be PMT = $709.74. This is a major savings over the fixed rate loan, it is very tempting to take it. However …

Rate Approximation for ARMs

Suppose that the ARM rate rises to 10 % at the start of the second year. Approximately how much extra will you then be paying over what you would have paid if you had taken the fixed rate loan?

After the first year, you will still owe close to the total you borrowed of $125,000. If we do the payment calculation with APR of 10% for 29 years, we find PMT = $1103.10. Now we are stuck paying $141.96 more than the original fixed rate loan.

Cars

All that house buying seems too complicated; is it just as bad for cars?

Car buying is much like student loan shopping only easier.

Most car terms are now 6 years. This allows for less accumulation of interest. (But there is still some, to make the loan worthwhile to the lender.)

Let’s buy a vehicle

A 2013 Dodge Challenger retails for $27,295. If you trade in your car and receive a $2500 credit as down payment and are offered a 6 year loan with an APR of 5.7%, how much would you pay each month?

The only Harley-Davidson motorcycle I have ever considered owning is a Sportster Iron 883 which retails for $7,999. I want to keep my current bike so I don’t really have a down payment. If I have a 4.5 year loan at 5.1%, how much would I have to pay each month?

Let’s buy a vehicle

A 2013 Dodge Challenger retails for $27,295. If you trade in your car and receive a $2500 credit as down payment and are offered a 6 year loan with an APR of 5.7%, how much would you pay each month? We need a loan for 27,295 – 2500 = $24,795. This would make our monthly PMT = $407.42.

The only Harley-Davidson motorcycle I have ever considered owning is a Sportster Iron 883 which retails for $7,999. I want to keep my current bike so I don’t really have a down payment. If I have a 4.5 year loan at 5.1%, how much would I have to pay each month? Although I’ve changed my mind on this bike, I would have to make a monthly payment of PMT = $166.09. (And you thought Harley’s were expensive!)

Income Tax Basics

Gross incomeAdjusted gross incomeExemptions and DeductionsTax tablesWithholdings

Income on Tax Forms Example

Karen earned wages of $34,200, received $750 in interest from a savings account, and contributed $1200 to a tax-deferred retirement plan. She was entitled to a personal exemption of $3650 and to deductions totaling $5900. Find her gross income, adjusted gross income, and taxable income.

Solution 1

Karen’s gross income is the sum of all her income: Gross income = $34,200 + $750 = $34,950.

Her contribution to tax-deferred retirement plan is an adjustment so AGI = $34,950 - $1200 = $33,750 is her adjusted gross income.

To find her taxable income, we subtract exemptions and deductions: Taxable Income = AGI – Exemptions – Deductions = $33,750 - $3650 - $5900 = $24,200.

That is, she only needs to pay taxes on the amount of $24,200.

Filing Status

SingleMarried filing jointlyMarried filing separatelyHead of household

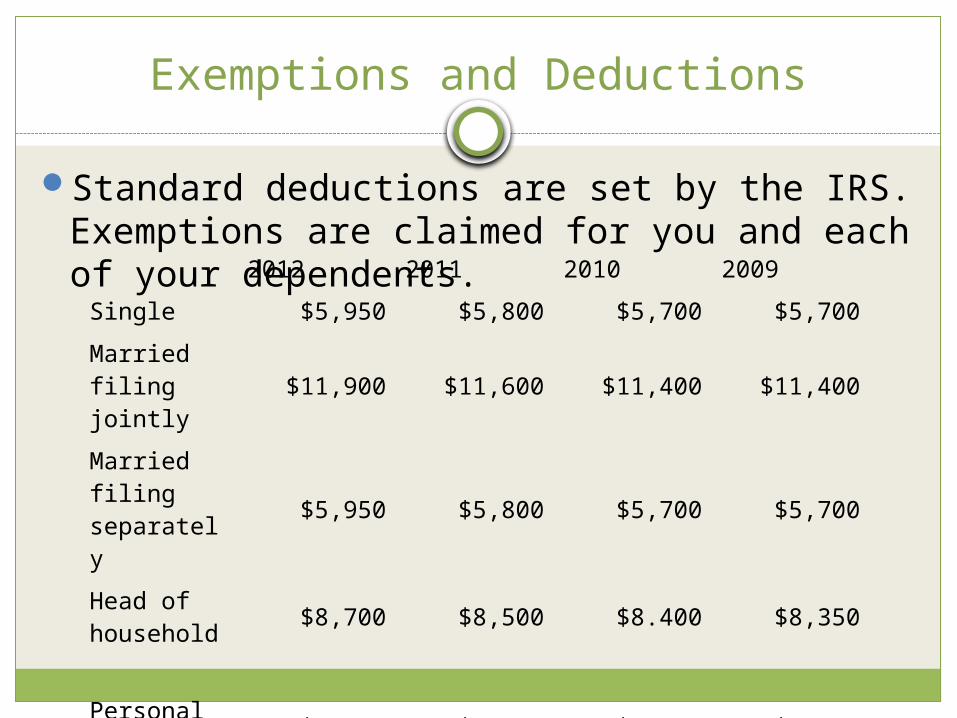

Exemptions and Deductions

Standard deductions are set by the IRS. Exemptions are claimed for you and each of your dependents.2012 2011 2010 2009

Single $5,950 $5,800 $5,700 $5,700

Married filing jointly

$11,900 $11,600 $11,400 $11,400

Married filing separately

$5,950 $5,800 $5,700 $5,700

Head of household $8,700 $8,500 $8.400 $8,350

Personal exemption $3,800 $3,750 $3,650 $3,650

Deductions

Deductions vary from one person to the next.You have two basic options when it comes to

deductions: Standard deduction, an amount that depends on your

filing status. Itemized deduction, which takes a lot of time and

record keeping.

Should you itemize?

1. Your deductible expenditures are $8600 for interest on a home mortgage, $2700 for contributions to charity, and $645 for state income taxes. Your filing status entitles you to a standard deduction of $11,400.

2. Your deductible expenditures are $3700 for contributions to charity and $760 for state income taxes. Your filing status entitles you to a standard deduction of $5700.

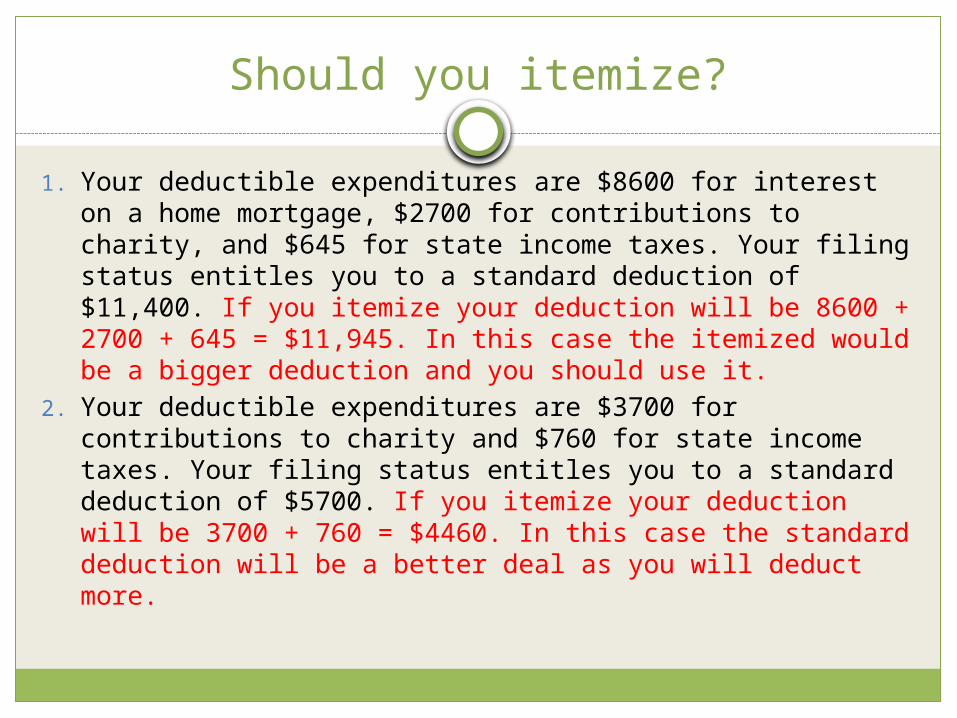

Should you itemize?

1. Your deductible expenditures are $8600 for interest on a home mortgage, $2700 for contributions to charity, and $645 for state income taxes. Your filing status entitles you to a standard deduction of $11,400. If you itemize your deduction will be 8600 + 2700 + 645 = $11,945. In this case the itemized would be a bigger deduction and you should use it.

2. Your deductible expenditures are $3700 for contributions to charity and $760 for state income taxes. Your filing status entitles you to a standard deduction of $5700. If you itemize your deduction will be 3700 + 760 = $4460. In this case the standard deduction will be a better deal as you will deduct more.

Tax Rates

The U.S. has a progressive income tax. This means that people with higher taxable incomes pay at a higher tax rate.

The system assigns different marginal tax rates to different income ranges (or margins).

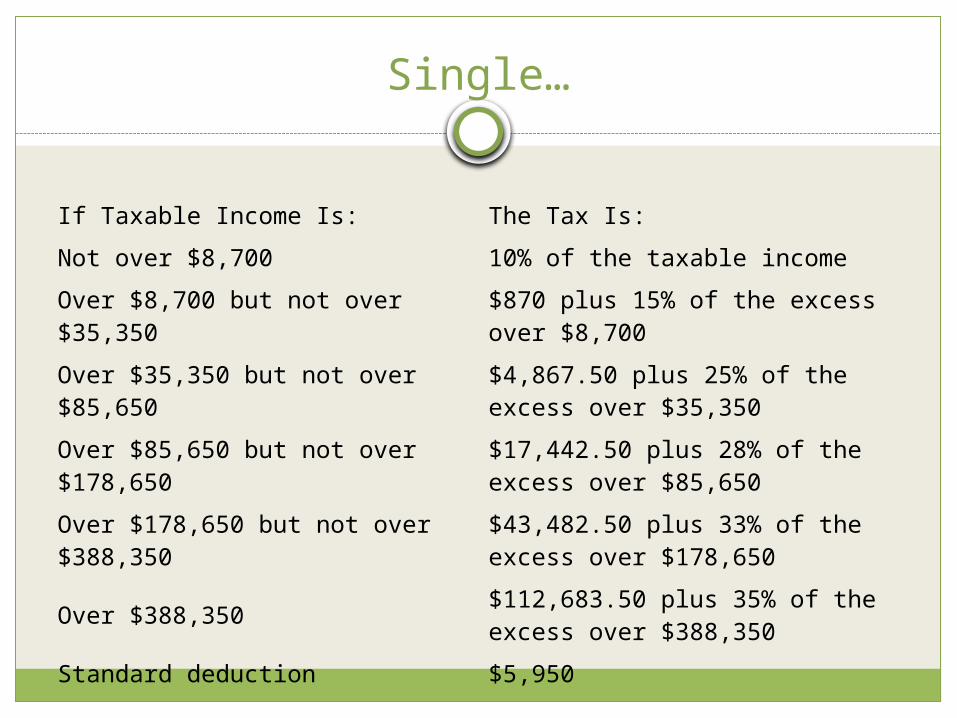

Single…

If Taxable Income Is: The Tax Is:

Not over $8,700 10% of the taxable income

Over $8,700 but not over $35,350

$870 plus 15% of the excess over $8,700

Over $35,350 but not over $85,650

$4,867.50 plus 25% of the excess over $35,350

Over $85,650 but not over $178,650

$17,442.50 plus 28% of the excess over $85,650

Over $178,650 but not over $388,350

$43,482.50 plus 33% of the excess over $178,650

Over $388,350 $112,683.50 plus 35% of the excess over $388,350

Standard deduction $5,950

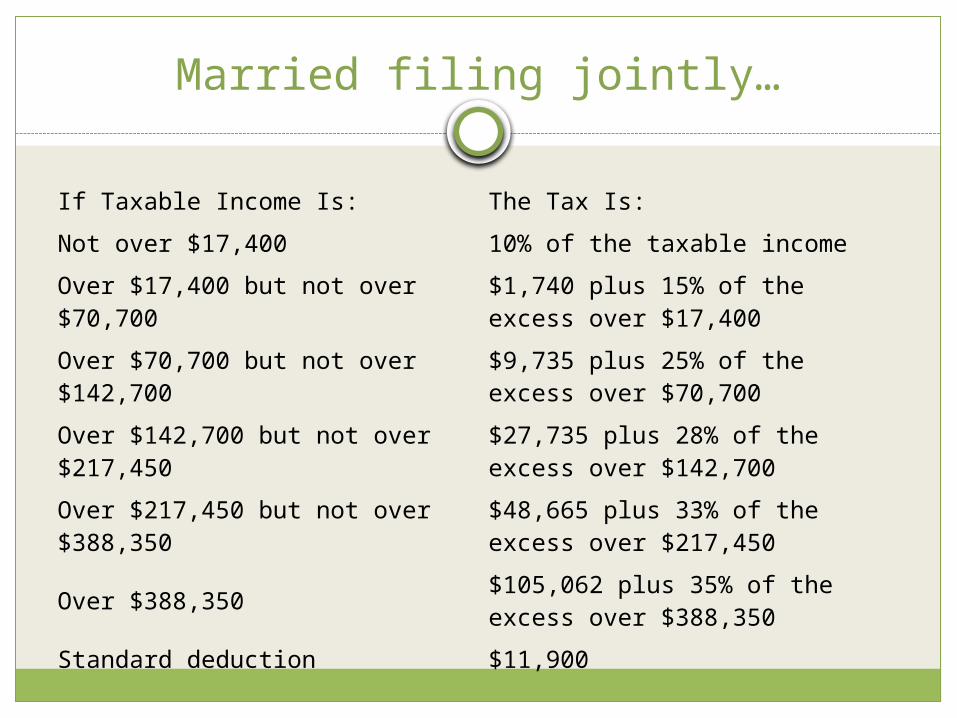

Married filing jointly…

If Taxable Income Is: The Tax Is:

Not over $17,400 10% of the taxable income

Over $17,400 but not over $70,700

$1,740 plus 15% of the excess over $17,400

Over $70,700 but not over $142,700

$9,735 plus 25% of the excess over $70,700

Over $142,700 but not over $217,450

$27,735 plus 28% of the excess over $142,700

Over $217,450 but not over $388,350

$48,665 plus 33% of the excess over $217,450

Over $388,350 $105,062 plus 35% of the excess over $388,350

Standard deduction $11,900

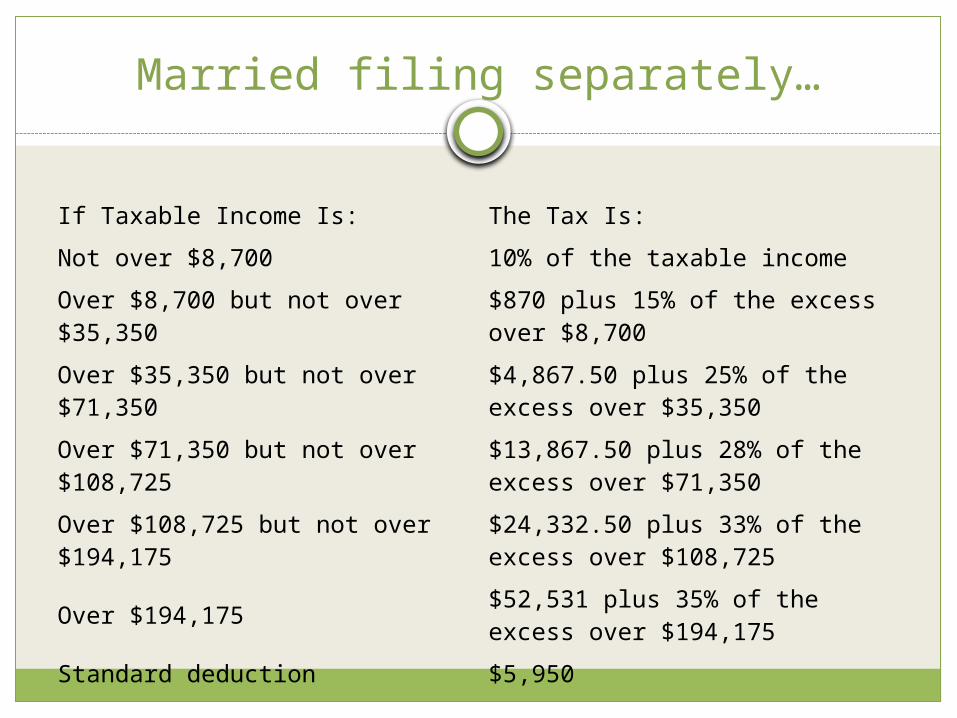

Married filing separately…

If Taxable Income Is: The Tax Is:

Not over $8,700 10% of the taxable income

Over $8,700 but not over $35,350

$870 plus 15% of the excess over $8,700

Over $35,350 but not over $71,350

$4,867.50 plus 25% of the excess over $35,350

Over $71,350 but not over $108,725

$13,867.50 plus 28% of the excess over $71,350

Over $108,725 but not over $194,175

$24,332.50 plus 33% of the excess over $108,725

Over $194,175 $52,531 plus 35% of the excess over $194,175

Standard deduction $5,950

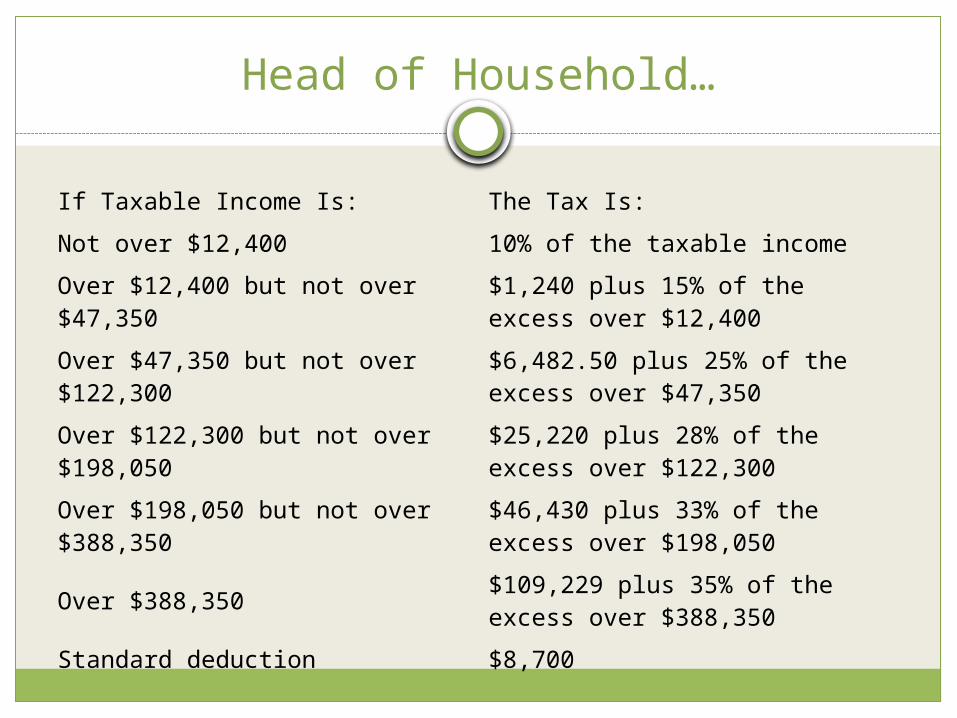

Head of Household…

If Taxable Income Is: The Tax Is:

Not over $12,400 10% of the taxable income

Over $12,400 but not over $47,350

$1,240 plus 15% of the excess over $12,400

Over $47,350 but not over $122,300

$6,482.50 plus 25% of the excess over $47,350

Over $122,300 but not over $198,050

$25,220 plus 28% of the excess over $122,300

Over $198,050 but not over $388,350

$46,430 plus 33% of the excess over $198,050

Over $388,350 $109,229 plus 35% of the excess over $388,350

Standard deduction $8,700

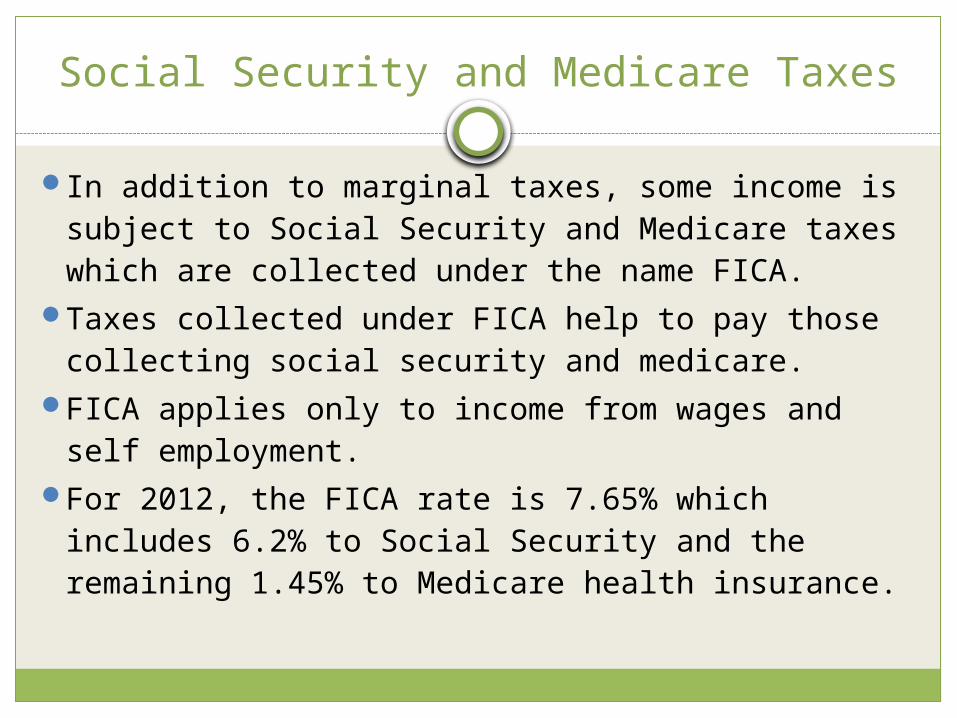

Social Security and Medicare Taxes

In addition to marginal taxes, some income is subject to Social Security and Medicare taxes which are collected under the name FICA.

Taxes collected under FICA help to pay those collecting social security and medicare.

FICA applies only to income from wages and self employment.

For 2012, the FICA rate is 7.65% which includes 6.2% to Social Security and the remaining 1.45% to Medicare health insurance.

Dividends and Capital Gains

These incomes get special treatment in the eyes of the tax collector.

Capital gains have two main subcategories: Short-term capital gains – items sold within 12 months

of their purchase. Long-term capital gains – items held more than 12

months before being sold.In general, capital gains taxes are at a lower

rate than standard income.A dividend is money earned on stocks and

other investments.

Tax-Deferred Income

IRA – individual retirement accounts, allow you to invest money into a personalized savings plan without having to pay taxes when the money is invested.

However, you do have to pay taxes eventually so when the money is removed from the account you will be responsible for paying taxes on this “income.”

Collecting Retirement

In collecting retirement we use the loan formula.

Why? We have the money in the account still collecting interest as we withdraw money until the account is down to zero.

Retirement examples

If I would have invested $75 a month in a retirement account paying 3.6% beginning at age 22 and ending when I retire at age 55, how much would I expect to have in the account when I want to access it?

Now I’m 55 and I want to make withdrawals (payments to me) that last the next 20 years. If the account rate of 3.6% holds during that period of time, how much will I earn from my retirement account each month?

Retirement Solution 1

If I would have invested $75 a month in a retirement account paying 3.6% beginning at age 22 and ending when I retire at age 55, how much would I expect to have in the account when I want to access it?

We can once again use the savings plan formula to determine the amount accumulated is $56,867.11.

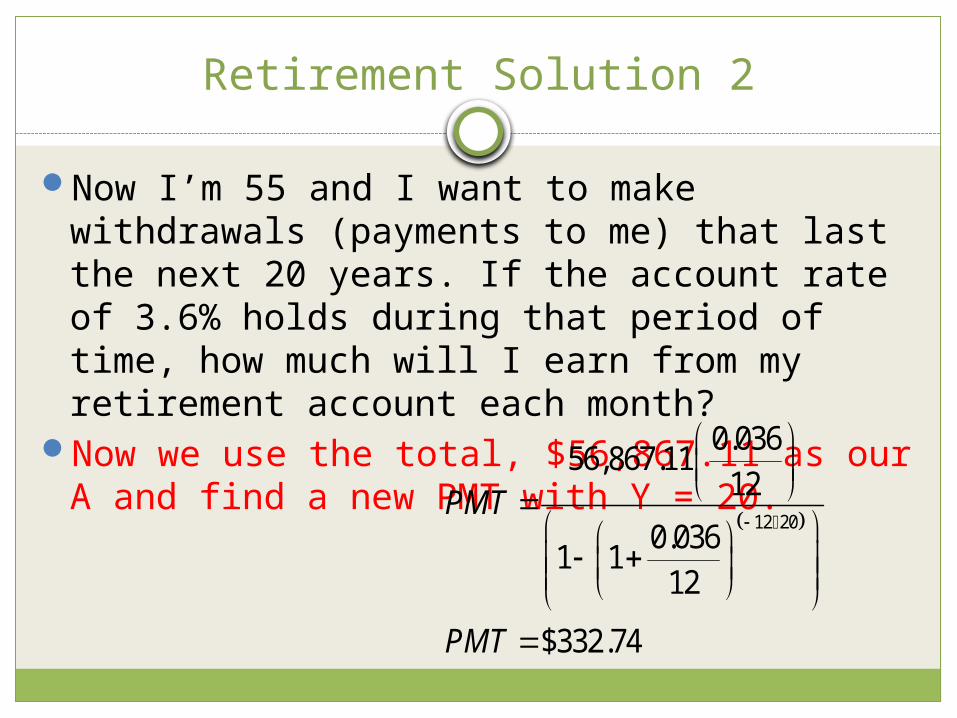

Retirement Solution 2

Now I’m 55 and I want to make withdrawals (payments to me) that last the next 20 years. If the account rate of 3.6% holds during that period of time, how much will I earn from my retirement account each month?

Now we use the total, $56,867.11 as our A and find a new PMT with Y = 20.

12 20

0.03656,867.11

12

0.0361 1

12

$332.74

PMT

PMT

Homework

You can now complete problems 1.18 – 1.26 in Jack Appreciates Math chapter one.