the antecedents and consequences of … logistic regression with state fixed-effects, ... chapter 1...

TRANSCRIPT

THE ANTECEDENTS AND CONSEQUENCES

OF PUBLIC HOSPITAL PRIVATIZATION

by

ZO-HARIVOLOLONA RAMAMONJIARIVELO

ROBERT WEECH-MALDONADO, COMMITTEE CHAIR

LARRY HEARLD

NIR MENACHEMI

MICHAEL MORRISEY

STEPHEN O’CONNOR

A DISSERTATION

Submitted to the graduate faculty of The University of Alabama at Birmingham,

in partial fulfillment of the requirements of the degree of

Doctor of Philosophy

BIRMINGHAM, ALABAMA

2012

Copyright by

Zo-Harivololona Ramamonjiarivelo

2012

iii

THE ANTECEDENTS AND CONSEQUENCES

OF PUBLIC HOSPITAL PRIVATIZATION

ZO-HARIVOLOLONA RAMAMONJIARIVELO

PH.D. PROGRAM IN ADMINISTRATION-HEALTH SERVICES

ABSTRACT

The purpose of this study was to explore the antecedents and consequences of

public hospital privatization with special attention to financial distress and financial

performance. A national sample of public hospitals using secondary longitudinal data

from 1997 to 2009 was used in this study. Data set from the American Hospital

Association, the Area Resource File, the Medicare Cost Report and the Local Area

Unemployment Statistics were merged to test the hypotheses pertaining to each research

question.

Based on the resource dependence theory, both environmental variables and

organizational variables were included in the analyses. This study adopted the Altman Z-

score method to assess public hospital financial distress. Fixed-effects logistic regression,

random-effects logistic regression with state fixed-effects, and fixed-effects linear

regression were used in this study.

Key findings indicated that environmental variable HMO penetration was

positively associated with the odds of public hospital financial distress. Organizational

variables hospital size, participation in a health network, and outpatient mix were

significantly and negatively associated with the odds of experiencing financial distress.

Membership of a multihospital system was significantly and positively associated with

the odds of experiencing financial distress. Additional findings suggested financial

iv

distress increased the odds of privatization and privatization improved financial

performance in terms of operating margin and total margin. In addition, findings

suggested privatization to public for-profit status resulted in better financial performance

compared to privatization to public-not-for-profit status.

Keywords: public hospital, privatization, financial distress, financial performance,

resource

v

DEDICATION

This dissertation is dedicated to God Almighty, Father, Son, and Holy Spirit, who

has been the source of all the strength, knowledge, ability, and resources that I needed to

pursue my education and complete this study. This dissertation is also dedicated to my

beloved and wonderful parents, my mother Honorine Ramahefarivelo and my late father

Paul Rakotomamonjy, who both sacrificed to raise and educate their children.

vi

ACKNOWLEDGMENTS

I could not have completed this dissertation alone. It has taken the support and

contribution of many scholars, namely my dissertation chair, Dr. Robert Weech-

Maldonado, and the members of my dissertation committee, Dr. Larry Hearld, Dr. Nir

Menachemi, Dr. Michael Morrisey, and Dr. Stephen O‘Connor. I could never thank Dr.

Weech-Maldonado enough for his contributions to this study. Dr. Weech-Maldonado

freely gave his time, expertise, support, and never-ending patience. Dr. Weech-

Maldonado is a wonderful role model with respect to scholarship, mentorship, kindness,

and humility.

I also would like to express my most sincere appreciation to the members of my

dissertation committee whose areas of expertise I came to depend on. I convey my

heartfelt thanks to Dr. Larry Hearld for spending invaluable time and effort reading and

editing my dissertation and showing me how to clearly and logically express my ideas. In

addition, Dr. Hearld provided advice and guidance with respect to the choice of

appropriate methods that matched the structure of the data used in this study. I also

extend my sincere gratitude to Dr. Nir Menachemi who has been an exceptional mentor

and role model. He not only helped me to find a dissertation topic, but also has been

gracious enough to assist me whenever I need help. I also appreciate Dr. Menachemi‘s

relentless encouragement to complete this dissertation.

vii

I would like to express my deep appreciation to Dr. Michael Morrisey whose

expertise in economics and experience with the American Hospital Association were vital

assets for this study. Dr. Morrisey‘s enthusiasm with respect to the dissertation topic was

contagious and his contribution to the careful choice of the variables needed for this study

was monumental. I also would like to state my profound gratitude to Dr. Stephen

O‘Connor for all his contributions. Dr. O‘Connor spent time reading and editing my

dissertation and his knowledge and expertise on health care organizations were priceless.

The contributions of other scholars deserve my deepest gratitude. I am deeply

indebted to Dr. Rohit Pradhan for his expertise on Medicare Cost Report and Area

Resource File. Dr. Pradhan guided me through the data collection, data cleaning, and data

analysis processes. I am also thankful to Mr. Josué Patien Epané for his help in data

collection and data cleaning processes, and for teaching me Statistical Analysis System

(SAS).

The help and support of my colleagues, friends and family merit my sincere

appreciation. I express my heartfelt thanks to Dr. DeLawnia Comer-Hagans, Dr.

Anantachai Panjamapirom, Dr. Gouri Gupte, Dr. Shamly Austin, Mr. Bob and Becka

Montgomery, Mr. Bill and Martha Allen, Mr. Corky and Greta Clark, Ms. Susan Elmore,

and Ms. Carolyn King for being my faithful and unconditional cheer leaders. In addition,

I acknowledge Dr. Comer-Hagan‘s help in editing this dissertation. Last but not least, I

express my sincere gratitude to my mother, brothers and sister for their love and support.

viii

TABLE OF CONTENTS

Page

ABSTRACT………………………………………………………………………...……iii

DEDICTATION………………………………………..……………………………...….v

ACKNOWLEDGMENTS………………………………………………………...…...…vi

TABLE OF CONTENTS……………………………………………………………… viii

LIST OF TABLES……………………………...……………………………………..…xii

LIST OF FIGURE……………………………………….………………………...……xiv

CHAPTER

1 INTRODUCTION……………………………………………………………….….......1

The Ownership Structure of U.S. Hospitals………………………………………….……3

Historical Perspective on Public Hospitals……………………………………….……….6

Public Hospitals Before and During the 19th

Century .............................................6

Public Hospitals During the 20th

Century and Beyond ............................................8

Rationale for the Study…………………….…………………………………………….14

2 REVIEW OF LITERATURE ........................................................................................19

Literature Review……...…………………………………………………………………19

Privatization of public hospitals and other healthcare organizations ....................20

The antecedents of healthcare organizations conversion

from public to for-profit status ..................................................................23

The antecedents of healthcare organizations conversion

from public to not-for-profit status ............................................................25

The consequences of ownership conversion

from public to for-profit status on financial performance. ........................26

The consequences of ownership conversion

from public to not-for-profit status on financial performance. ..................27

Conceptual Framework and Hypotheses……………………………………………...…28

ix

Theoretical Background ........................................................................................ 28

Resource dependence theory. ....................................................................29

The Environment ...................................................................................................35

Environmental munificence .......................................................................36

Environmental dynamism ..........................................................................36

Environmental complexity. ........................................................................37

Financial Performance .......................................................................................... 39

The association between environmental munificence

and financial performance........................................................................ 40

The association between environmental dynamism

and financial performance. ....................................................................…42

The association between environmental complexity

and financial performance. ........................................................................43

The association between organizational size

and financial performance. ........................................................................45

The association between teaching status

and financial performance. ........................................................................46

The association between financial performance

and privatization. .......................................................................................48

The impact of privatization on hospital

financial performance. ...............................................................................49

3 RESEARCH METHODOLOGY…….……………...…………………………………….53

Research Design ....................................................................................................54

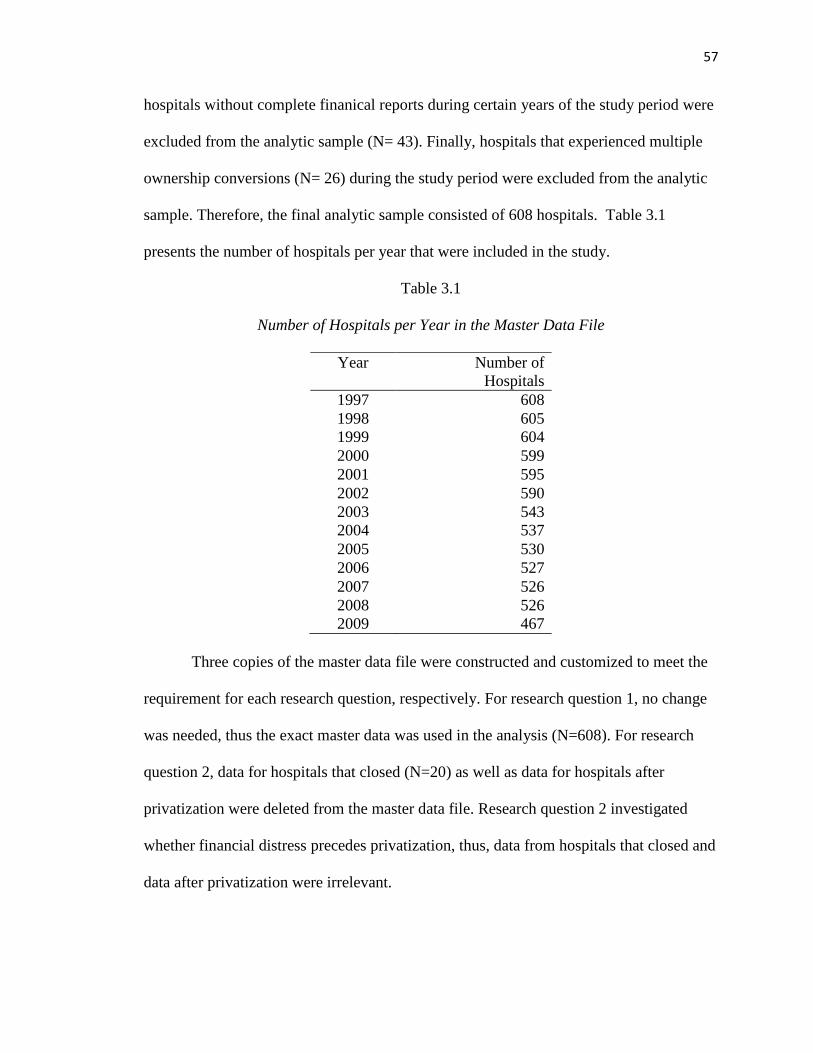

Data Sources................................................................................................................................55

Population and Sample ..........................................................................................56

Variables and their Operationalization ..................................................................58

Question 1: What are the organizational and environmental

factors associated with financial distress of public hospitals? ...................58

Question 2. Is financial distress associated with public

hospitals privatization? ............................................................................. 69

Question 3. Does privatization lead to a better financial

performance? ............................................................................................74

Analysis .................................................................................................................77

x

Potentially endogenous variables. .............................................................80

Models ...................................................................................................................80

Models for operating margin. ....................................................................81

Models for total margin. ............................................................................81

4 RESULTS……………...………………………………………………………………86

Results from Research Question 1 .........................................................................86

Results of fixed-effects logistic regressions. .............................................96

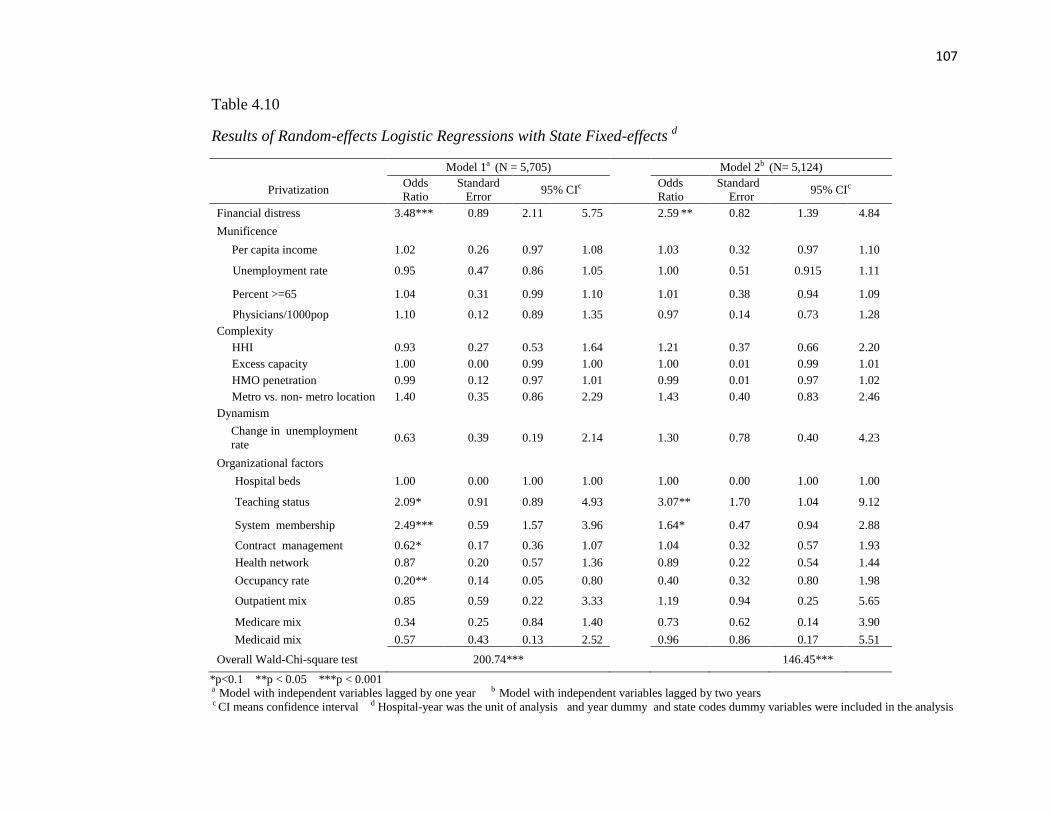

Results from Research Question 2 .........................................................................98

Results from Research Question 3 .......................................................................108

Results of hypothesis 7. ...........................................................................118

Results of Hypothesis 8 ...........................................................................123

Conclusion ...............................................................................................130

5 DISCUSSION……………………….………….……………………………………...……………134

Discussion of Findings from Research Question 1 ..............................................134

Findings from Hypothesis 1 .....................................................................135

Findings from Hypothesis 2 .....................................................................136

Findings from Hypothesis 3 .....................................................................136

Findings from Hypothesis 4 .....................................................................137

Findings from Hypothesis 5 .....................................................................137

Discussion of Findings from Research Question 2 ............................................. 140

Discussion of Findings from Research Question 3 ............................................. 142

Managerial and Policy Implications ....................................................................144

Limitations of the Study ......................................................................................147

Directions for Future Research ......................................................................…..148

xi

Conclusion .......................................................................................................... 159

LIST OF REFERENCES .................................................................................................150

APPENDIX A……………………………………………………………………………………….…164

IRB APPROVAL…………………………………………………………………………………...…172

xii

LIST OF TABLES

Table Page

1.1 Trends in Number of Hospitals and Hospital Beds by Ownership Type…………….12

3.1 Number of Hospitals per Year in the Master Data File………………………...........57

3.2 Normalization of Operating Margin………………………….……………………...79

3.3 Normalization of Total Margin………………………………………………………79

3.4 Summary of Variables Conceptual Definitions,

Operational Definitions, References and Data Sources …........................................82

4.1 Descriptive Analysis of all Variables………………………………………………..87

4.2 Independent Samples t-test on Dependent Variable

―Financial Distress‖…………...……………………………………………….……..90

4.3 Cross-tabulation and Pearson Chi-Square Test on

Dependent variable ―Financial Distress‖………………………...…………………..92

4.4 Pearson Correlation Matrix of Independent Variables………………………………93

4.5 Results of Fixed-effects Logistic Regression………………………………………..97

4.6 Descriptive Analysis of all Variables……..……………..……………………….….99

4.7 Independent Samples t-Tests on Dependent Variable Privatization…………….….102

4.8 Chi-square Test on Dependent Variable ―Privatization‖…………………………...103

4.9 Pearson Correlation Matrix Research Question 2…………………………………..104

4.10 Results of Random-effects Logistic Regression with State Fixed-Effects………..107

4.11 Descriptive Statistics on the Operating Margin Data Set…………………………109

4.12 Independent Samples t-Tests on Operating Margin……………………………….111

xiii

4.13 Correlation Matrix of Data Set for Operating Margin…………………………….112

4.14 Descriptive Statistics of total Margin Data………………………………………..114

4.15 Independent Samples t-Tests on Total Margin……………………………………116

4.16 Correlation Matrix Variables for Total Margin Data Set…………………….……117

4.17 Results of Fixed-effects Linear Regression on Operating Margin First

Hypothesis…………………………………………………………………………119

4.18 Results of Fixed-effects Linear Regression on

Total Margin First Hypothesis ………………….……………….…………………120

4.19 Operating Margin by Ownership Type………………...……...…….…………….124

4.20 Total Margin by Ownership Type…………...…………...……………...………..125

4.21 Results of Fixed-Effects Linear Regressions on Operating Margin-

Second Hypothesis…………………………………………………...….………...126

4.22 Results of Fixed-Effects Linear Regression on Total Margin -

Second Hypothesis…………………………………………………………………127

4.23 Summary of Findings from Hypothesis Testing…...……………………………...132

4.24 Summary of Findings for Each Research Question………...……………………..133

xiv

LIST OF FIGURE

Figure Page

1.1 Conceptual Framework………………………………………………………………34

1

CHAPTER 1

INTRODUCTION

In the past few decades there have been significant numbers of hospital ownership

status conversions. Ownership status conversion refers to any transactions that result in

the change of an organization‘s ownership status (Anderson, Allred, & Sloan, 2003;

Goodstein & Boecker, 1991; Hall & Conover, 2006; Needleman, 1999). Such

transactions can be performed either at the interorganizational or organizational level.

Interorganizational transactions resulting in ownership status change include merger,

sale, lease, or joint venture, among others; such transactions involve the transfer of

ownership from one organization to another (Anderson, et al., 2003; Goodstein &

Boecker, 1991; Legnini et al., 1999; Needleman, 1999).

Change in ownership status can also involve a single organization; the

management team or the board of directors purchases the organization‘s assets through a

leveraged buyout (Gray, Smelser, & Baltes, 2001) or the organization directly applies for

ownership conversion with legal authorities, but such transaction is not very common in

healthcare settings (Cutler & Horwitz, 1997; Needleman, 1999). An ownership

conversion is called privatization when it involves the conversion of an organization from

public to either private for-profit or private not-for-profit status (Wessel, 1995).

While hospital ownership conversion has occurred in various ways, from private

not-for-profit (NFP) to private for-profit (FP) or government (Gov), from FP to NFP or

Gov, and from Gov to FP or NFP, conversions from NFP to FP have been the focus of

2

most prior research (Burns, Shah, Frank, & Powell, 2009). Additionally, previous studies

have found that financial distress is the major factor leading to conversion but these

studies did not explore the reasons for financial distress (Amirkhanyan, 2007; Bovbjerg,

Held, & Pauly, 1987; Bovbjerg, Marsteller, & Ullman, 2000; Burns et al., 2009; Legnini

et al., 1999; Sloan, Ostermann, & Conover, 2003; Sloan, Taylor Jr, & Conover, 2000). A

more comprehensive study that investigates both the determinants and outcomes of

public hospitals ownership conversion will help stakeholders to pay close attention to

these factors so as to prevent financial distress and give empirical evidence whether

ownership conversion is the best way to turn the financial situation around. The purpose

of this study is to investigate the antecedents and consequences of the privatization of

non-federal general public hospitals. This study will attempt to answer the following

research questions:

1. What are the organizational and environmental factors associated with

financial distress of public hospitals?

2. Does financial distress precede public hospital privatization?

3. Does privatization lead to better financial performance?

The following three sections will discuss: (1) the ownership structure of U.S. hospitals,

(2) the historical perspective on U.S. public hospitals, (3) the rationale for the study.

3

The Ownership Structure of U.S. Hospitals

Hospitals are categorized by ownership status: government hospitals (Gov),

private not-for-profit hospitals (NFP), and private for-profit or investor-owned hospitals

(FP). Government hospitals are classified into two categories: federal hospitals that are

totally under the control and administration of the federal government such as the

Veterans‘ Affairs; and public hospitals that are under the administration of a city, county,

tax district, or state (Gapenski, 2004). The hospital‘s ownership status determines its

primary mission and sources of funding.

The principal mission of public hospitals is to provide healthcare for the indigent,

the needy and the uninsured and serve the community; they act as the ―provider of last

resort‖ or ―safety net‖ for the community. In addition, public hospitals are expected to

provide expensive and specialized healthcare services that private hospitals would not

deliver. Such services include neonatal intensive care, psychiatric treatments, burn care,

and trauma care. In addition, public hospitals play a major role in providing medical

education and clinical research (Andrulis, 1997; Bovbjerg et al., 1987; Brown, 1983;

Fishman, 1997).

Public hospitals obtain their capital in the form of governmental grants given by

the city, the county, or the state and excess revenue over costs from previous years. These

grants are business, property and personal income taxes collected from residents and

local businesses. While public hospitals are not allowed to raise capital through the sale

of stocks, they are allowed to sell tax-exempt bonds. In addition, public hospitals do not

pay property or corporate income tax and they are not allowed to share excess revenue

over costs among individuals (Gapenski, 2004).

4

Private not-for-profit hospitals are charitable entities under 501 (c) (3)

classification of the Internal Revenue Code. The main purpose of private not-for-profit

hospitals is to serve the community through the provision of quality healthcare, medical

education and research (Gray, 1986). Not-for-profit hospitals raise their capital from tax-

deductible contributions from philanthropists, tax-exempt bonds, and excess revenue over

costs, and governmental grants. As charities, not-for-profit hospitals do not pay property,

sales and corporate income taxes. In return, they are expected to provide charity care,

uncompensated care, and other community benefits such as the provision of preventive

care and healthcare education to the community. Even if not-for-profit hospitals do not

seek profit, they need to maintain good financial status to fulfill their mission (Gapenski,

2004).

Like public hospitals, not-for-profit hospitals are not authorized to raise capital

from the sale of stock and they are not allowed to share excess revenue over costs among

contributors. Excess revenue over costs should be reinvested in the hospital.

Furthermore, the proceeds from the sale of the hospital should not be distributed among

donors; they should be invested in a foundation that will serve the community. Not-for-

profit hospitals are allowed to pursue growth strategies (Clark, 1980; Gray, 1997; Gray,

1986; Gray, 1986; Marsteller, Bovbjerg, & Nichols, 1998).

For-profit hospitals are owned by shareholders. Their primary purpose is to

maximize shareholders wealth. For-profit hospitals raise capital by selling stocks to

investors, issuing bonds, and reinvesting retained earnings in the hospital‘s account. In

return, they pay property, sales, and income tax. For-profit hospitals are allowed to share

dividends among shareholders and shareholders have the right to divide the proceeds

5

from the sale of the hospitals (Gray, 1997; Gray, 1986; Marsteller, et al., 1998; Gapenski,

2004).

Regardless of ownership type, financial capital is one of the key resources of

every hospital. Hospitals require financial capital to support their operations, growth, and

survival. In addition to capital, hospitals also require other resources such as human

resources, medical equipments and technology, knowledge and reliable information to

adequately deliver quality healthcare. Lack of financial and other resources might induce

hospitals to engage in some strategic moves such as merger, sale, joint venture,

diversification, or ownership conversion. Such strategic change might help hospitals find

an alternative supply of resources and better access to knowledge and technology.

Comparing the three types of ownership, public hospitals carry the heaviest

burden in serving the community (Walker, 2005) and yet they have the least flexibility

regarding the ability to raise capital; they totally rely on the availability of funds from

government entities. However, the availability of funds depends on many factors such as

the capability of the residents and businesses to pay property and income taxes which is

contingent on the economic situation. During economic prosperity, government entities

might have more funds to give to public hospitals, but during an economic crisis, such

funds may deplete very quickly. Besides, the decision of the government to distribute tax

income among other public entities such as schools, public transportation, the post office,

and the armed forces might reduce the amount of capital granted to public hospitals

(Andrulis, 1997; Bovbjerg et al., 1987; Brown, 1983; Sataline, 2010).

Furthermore, unlike private hospitals, public hospital managers do not have the

freedom and the flexibility to decide and implement strategic change that would improve

6

the hospital‘s operation and enhance their financial situation. Public hospitals generally

operate under heavy bureaucracy and burdensome political pressure; politicians have the

power to decide on the strategic direction public hospitals should pursue (Siegel, 1996).

Regardless, all three types of hospitals have contributed to health care delivery in the

U.S; they all have their weaknesses and strengths. The next section presents a historical

perspective on public hospitals.

Historical Perspective on Public Hospitals

This section is divided into two sections: (1) public hospitals before and during

the 19th

century and (2) public hospitals during the 20th

century and beyond.

Public Hospitals Before and During the 19th

Century

The majority of public hospitals emerged from almshouses, but some were built

from scratch (Dowling, 1982). Almshouses were shelters for those in need of social

support such as the homeless, the drunkard, the mentally impaired, the outlaws, as well as

those with chronic illnesses. The provision of social, mental and physical support for the

needy was a practice from Great Britain that the immigrants wanted to carry on in the US

(Friedman, 1987). Almshouses were charitable organizations that were financially

supported by the local government; they were not-for-profit (Shi & Singh, 2004).

Since almshouses opened their doors to everyone in need without distinction, they

were not effective in providing the specific needs of their residents. Therefore,

specialized institutions such as orphanages, mental asylums and jails were established to

take care of people with specific social needs. Those with medical conditions remained in

7

the almshouse. Due to the stigma associated with the almshouse as the shelter for the

lowest class of the population, only the poor-sick stayed in the almshouses (Friedman,

1987). Those who could afford to pay for physicians preferred to be treated at home

(Starr, 1982). Thus, almshouses implicitly became the hospitals for the destitute.

Philadelphia General Hospital, founded in 1732, was the first public hospital that

emerged from almshouse status. It expanded, became successful, and acquired a

worldwide reputation in treating the sick as well as providing medical education and

research (Rosenberg, 1982). In 1736, New York City Almshouse morphed into Bellevue

Hospital and Charity Hospital in New Orleans was founded the same year (Rosenberg,

1982; NAPH, 2011). Due to the rapid growth of cities, most of the first public hospitals

were built in cities.

The growth of the population, the improvement in the quality of care, the progress

in medical education, and the professionalization of nursing served as catalysts to the

growth of public hospitals. Hospital use intensified due to the discovery of anesthesia by

William Thomas Green Morton in 1846, the discovery of antisepsis by Sir Joseph Lister

in 1867, and the discovery of x-rays by Wilhelm Rontgen in 1896 (McEachern, 1936;

Starr, 1982). The number of beds of all public hospitals increased from 12,000 in 1873 to

25,000 in 1889 (Dowling, 1982). Public hospitals became the largest hospitals relative to

the private ones and they totally relied on public funding. While public hospitals were

involved in training physicians and nurses they kept their primary mission which was

treating the very poor-sick (Starr, 1982). That mission stained the image of public

hospitals as they became undesirable for those who could afford better and more

expensive care (Dowling, 1982).

8

Public Hospitals During the 20th

Century and Beyond

The 20th

century experienced the fastest growth in hospital industry. This was

primarily due to population growth, increased confidence in hospital services, the

expansion of nursing and medical education and the professionalization of health

administration.

Despite this rapid expansion, the government felt the need to build more hospitals

firstly to care for the wounded soldiers of World War II and to provide additional care for

the communities. The Hospital Survey and Construction Act called the ―Hill-Burton Act‖

was signed in 1946 to authorize the issue of Federal grants, loans and loan guarantees for

hospital construction and health centers at states and community levels. Only public and

not-for-profit hospitals qualified for the Hill-Burton funds and the recipients of the funds

were expected to provide a certain amount of uncompensated care for 20 years

(Department of Health and Human Services, 1992). Since the Hill- Burton Act required

the provision of a certain amount of uncompensated care, for-profit hospitals did not

qualify for the program because the provision of uncompensated care was not the primary

purpose of for-profit hospitals.

Thus, the funding from the Hill-Burton Act enhanced the growth of public

hospitals even more. The recipients of the Hill-Burton funds were more competitive

relative to for-profit hospitals; they attracted more patients because they could offer

services at lower prices or free of charge for those who could not pay (Starr, 1982). The

number of public hospitals grew from 785 in 1946 to 1453 in 1965 (Friedman, 1987).

9

During the 20th century, the federal government did not only build more hospitals

and invest in healthcare education and research, but also provided access to healthcare to

the elderly and those who could not afford to pay. To provide better access to healthcare

for the retired and low income individuals, the government adopted Medicare and

Medicaid programs in 1965. The funding of these two programs, based on fee-for-

service, increased health care utilization and triggered escalating healthcare expenditures

(Starr, 1982). Under a fee-for-service plan, health care providers were reimbursed based

on the amount of services provided. Thus the plan encouraged providers to give as much

clinical care possible as to enhance revenue. In addition to the concern over raising

healthcare expenditures, there were growing concerns over the quality of care,

inefficiency, lack of access to care in rural areas, overcapacity, oversupply of physicians

and overspecialization (Starr, 1982). Consequently, in 1970, the government drew the

country‘s attention to the ―crisis in healthcare‖.

Among all hospitals, public hospitals were the most entrenched in crisis relative

to private hospitals as they were burdened with politics, depleted revenues and shrinking

government funding. They could not afford to renovate their buildings and were not able

to purchase updated medical equipment (Dowling, 1982).

Both the federal and state governments adopted some measures to reverse the

situation. Such measures included the Certificate of Needs (CON) laws and the

implementation of Medicare Prospective Payment System (PPS) in 1983. CON laws

provide legislation that individual states can adopt to restrict the building of new

constructions and curb overcapacity. States that adopted CON laws required health care

10

organizations to apply for an authorization to build or expand a facility. New York State

adopted the first CON law in 1964 (Stevens, 1989).

Medicare PPS was enacted by the Tax Equity and Fiscal Responsibility Act

(TEFRA) of 1982. With this law, the federal government took the initiative to impose

rates on services rendered to Medicare enrollees based on the Diagnosis-Related Groups

(DRGs) system. This system of payment combined all the services needed to treat a

certain disease; Medicare set the amount it paid for that particular bundle of services.

Medicare enrollees that belong to the same diagnosis group are charged the same rate.

Thus, a hospital benefits if its costs are below the PPS rate; it operates at a loss if its costs

are above the PPS rate (Shi & Singh, 2004).

In addition, the healthcare crisis has opened the opportunity to the emergence of

managed care organizations such as health maintenance organizations (HMO) as major

players in the healthcare industry. In order to control cost and utilization, HMOs provide

health insurance and contract with hospitals for the health care delivery of their enrollees.

Through tight control of consumption of specialized services by the systematic use of

primary care providers, health care utilization review, and strong negotiation on health

services costs, HMOs were successful in controlling healthcare expenditures during the

1980s.

Public hospitals have faced fierce competition with private hospitals. Private

hospitals are more attractive to the higher income population; as a result, the majority of

patients that public hospitals serve are low income people, the uninsured and the

underinsured. While private hospitals are more desirable than public hospitals, they

11

cannot provide all the services that public hospitals offer such as specialized tertiary

services including trauma care, HIV/AIDS treatments, and substance abuse rehabilitation

(Dowling, 1982). Furthermore, private hospitals prefer ―dumping‖ their uninsured

patients on public hospitals rather than treating them (Friedman, 1987). Thus, public

hospitals have coined themselves as ―safety net hospitals‖ as they serve the most

vulnerable population and provide critical services for critical needs (NAHP, 2011).

Since public hospitals have operated in an environment with fiscal pressure and

fierce competition coupled with an increasing number of uninsured and underinsured,

most of them have been in financial distress. Some of them could not survive and were

closed and some converted into private status. For example, the first public hospital,

Philadelphia General Hospital closed in 1976. A decreasing trend in the number of public

hospitals was noticed in the mid-1980s. The number of public hospitals decreased by

14 % between 1985 and 1995 (Legnini et al., 1999). Between 1980 and 2007 a total of

686 public hospitals converted into private status (Burns et al., 2009; Needleman,

Chollet, & Lamphere, 1997; Thorpe, Florence, & Sieber, 2000). Table 1.1 illustrates the

trends in the numbers of hospitals and hospital beds by ownership status from 1975 to

2008 (Department of Health and Human Services, 2011).

12

Table 1.1

Trends in Number of Hospitals and Hospital Beds by Ownership Type

Number of hospitals

and number of beds

by ownership type

1975 1980 1990 1995 2000 2006 2007 2008

Number of Hospitals

All hospitals 7,156 6,965 6,649 6,291 5,810 5,747 5,708 5,815

Nonfederal 1 6,774 6,606 6,312 5,992 5,565 5,526 5,495 5,602

Federal 382 359 337 299 245 221 213 213

Community2 5,875 5,830 5,384 5,194 4,915 4,927 4,897 5,010

Not-for-profit 3,339 3,322 3,191 3,092 3,003 2,919 2,913 2,923

For profit 775 730 749 752 749 889 873 982

State-Local

government 1,761 1,778 1,444 1,350 1,163 1,119 1,111 1,105

Number of Beds

All hospitals 1,465,828 1,364,516 1,213,327 1,080,061 983,628 947,412 945,199 9,5045

Nonfederal1 1,333,882 1,247,188 1,115,072 1,003,522 930,561 900,721 899,455 905053

Federal2 131,946 117,328 98,255 77,079 53,067 46,691 45,744 45,992

Community 941,844 988,387 927,360 872,736 823,560 802,658 800,892 808,069

Not-for-profit 658,195 692,459 656,755 609,729 582,988 559,216 553,748 556,651

For-Profit 73,495 87,033 101,377 105,737 109,883 115,337 115,742 120,887

State-Local

government 210,154 208,895 169,228 157,270 130,689 128,105 131,402 130,531

Source: Health, United States, 2010, page 372 (DHHS, 2011) 1 The category of nonfederal hospitals comprises psychiatric, tuberculosis and other respiratory diseases hospitals, and

long-term and short-term general and other special hospitals 2 Community hospitals are nonfederal short-term general and special hospitals whose facilities and services are

available to the public.

The information in Table 1.1 does not explicitly show how many hospitals

merged, got acquired, changed ownership or closed, but the numbers suggest one of these

strategies (Weil, 2011). For example, the decrease in the number of all hospitals from

7,156 in 1975 to 5,815 in 2008 suggests either hospital closures or mergers. The number

of all federal, nonfederal and community hospitals decreased between 1975 and 2008

except for the number of for-profit hospitals which increased from 775 (13% of all

community hospitals) to 982 (20%) between 1975 and 2008. This increase suggests the

growth of for-profit hospitals either through ownership change or entry of start-up

13

hospitals. The number of state-local government hospitals declined from 1,761 (30% of

all community hospitals) to 1,105 (22%) between the same period of time (DHHS, 2011).

Additionally, the capacity of hospitals measured as the number of beds also

demonstrates a decreasing trend for all federal, nonfederal and community hospitals

except for for-profit hospitals, which increased from 73,495 beds (8% of all community

hospital beds) to 120,887 beds (15%) between 1975 and 2008. The number of beds

owned by state-local government community hospitals decreased from 210,145 (22% of

all community hospital beds) to 130,531 (16%).

The history of public hospitals, has demonstrated that environmental factors such

as technology, war, population growth, government regulations and funding, economy,

advance in science, and competition have played a major role in the evolution of public

hospitals.

Government regulations can impose rules on but also allow flexibility for

healthcare organizations. Freedom of ownership status conversion is one of the

flexibilities granted to health care organizations. This freedom has permitted

organizations to solve organizational problems, pursue new opportunities, access

resources, or survive in a dynamic and competitive healthcare environment. The next

section discusses the rationale for the study.

14

Rationale for the Study

The purpose of this study is to investigate the impact of organizational and

environmental factors on public hospitals‘ financial distress, the impact of distress on

public hospitals‘ privatization, and the effect of public hospitals‘ privatization on

financial performance based on the resource dependence theory. This study focuses on

community public hospitals and does not include federal public hospitals like Veterans

Affairs. Since federal public hospitals operate in a different environment with special

rules and regulations and serve special populations such as the military, including them in

the study might bias the results.

The findings from the review of hospital ownership conversion literature revealed

that despite the different types of ownership conversion, the majority of the literature

studied hospital conversion from not-for-profit to for profit status or vice-versa. More

precisely, the number of hospital conversions from public ownership to private-not-for-

profit status slightly exceeded the number of hospital conversions from not-for-profit to

for-profit status between 1991 and 1997 and yet empirical studies on privatization of

public hospitals have been scarce (Burns et al., 2009). Nevertheless, the privatization of

public hospitals deserves greater attention given their major role in the life of the

community and the whole society.

Studying public hospitals is timely given their major role as safety net providers

to the community. The responsibility of public hospitals in providing care to the needy is

mostly needed during economic downturn when many people lose their jobs and

consequently their health insurance coverage and yet, public hospital funding decreases

the most during economic crisis. As of 2009, there were 51 million uninsured individuals

15

in U.S., representing a 10% increase from 2008 (U.S. Census Bureau, 2009). The

uninsured have imposed an additional strain in the operating environment of public

hospitals. Public hospitals members of the National Association of Public Hospitals and

Health Systems (NAPH), which represent 2% of all acute care hospitals, reported that

31% of their outpatient visits and 18% of their inpatient services were delivered to the

uninsured (NPHHI, 2009). More precisely, NAPH members provided 27% and 19% of

their total inpatient and outpatient services ($115 billion) to Medicaid patients and the

uninsured, respectively (NPHHI, 2009). Furthermore, 16% of their operating costs were

uncompensated relative to 6% of costs for all hospitals in the U.S.; in 2009, NAPH

members delivered 20% of all uncompensated care nationwide (NPHHI, 2009).

Given their public status, public hospitals are also expected to deliver expensive

and unprofitable tertiary services that private hospitals do not provide (Anderson,

Boumbulian & Pickens, 2004). The NAPH reported that specialty care provided by its

members represented 56% of all visits (NPHHI, 2009). Besides, public hospitals offer

substantial medical education and clinical research (Andrulis, 1997; Bovbjerg et al.,

1987; Brown, 1983; Fishman, 1997). While NAPH members represent only 2% of all

acute care hospitals, they provide medical training to more than 19,000 full-time

equivalent (FTE) medical and dental residents, representing 23% of all residents in acute

facilities (NPHHI, 2009).They also offer emergency relief in case of man-made or natural

disasters .

Despite the fact that public hospitals hold an important role in healthcare delivery,

they have faced the most challenging environment. Public hospitals have been struggling

to stay competitive while trying to overcome financial difficulties due to reduced

16

government funding and fiscal constraints, an increasing number of uninsured patients,

escalating healthcare costs, and pressure for efficiency. Moreover, public hospitals have

had a hard time competing for Medicare managed care contracts (Brown, 1983; Sataline,

2010; Siegel, 1996).

In summary, public hospitals have taken on the responsibilities that private

hospitals deem too costly and unprofitable to undertake (Andrulis, 1997). Therefore, lack

of access to adequate capital and expertise, intensifying competition, decreasing

operating income, and increasing expenditures and social burden have deeply affected the

financial situation of many public hospitals and as a result that they have experienced

financial distress (Bazzoli & Andes, 1995; Falik, 1983). Conceptually, a hospital is in

financial distress when it experiences a severe financial crisis that leads to radical

changes such as a merger, a reduction in the number of services, a diversification into

services unrelated to previous ones, an ownership conversion, a bankruptcy declaration

(Langabeer, 2006; Trussel & Patrick, 2010). Public hospitals have adopted these kinds of

survival strategies or exited the market (Bazzoli & Andes, 1995; Brown, 1983; Sataline,

2010).

Statistics have shown the declining trend in the number of public hospitals due to

either closure or privatization as demonstrated in Table 1. Privatization has been

considered the alternative solution to closure. Keeping the hospital open, under private

ownership, might preserve some access to healthcare for the community, ensure some

continuation of medical education and research, safeguard the access to emergency care

in case of national disaster and preserve some jobs. Privatization might turn the hospital

around and boost its financial health. Closure of a public hospital might result in a loss of

17

community benefits. Given the importance of public hospitals in healthcare delivery and

education, it is worth providing empirical evidence on why public hospitals privatize and

whether privatization has improved hospitals‘ outcomes (Sebelius, Frieden, & Sondik,

2010).

While previous studies on public hospitals privatization suggested poor financial

performance as the major factor leading to privatization, they did not investigate the

factors leading to poor financial performance. This study will investigate the

determinants of financial distress, then explore whether financial distress precedes

privatization and finally, examine whether privatization results in enhanced financial

condition.

This study fills the gap in the hospital ownership conversion literature by

empirically investigating both the antecedents and outcomes of public hospitals‘

privatization. Moreover, this study contributes to research based on the following points.

First, this study is more comprehensive compared to previous ones as it is based on a

national sample and covers thirteen years of data from 1997 to 2009. Second, it

contributes to knowledge by providing empirical evidence on three associations: the

impact of organizational and environmental factors on public hospitals financial distress,

the consequences of financial distress on public ownership status and the effects of

privatization on financial performance. A longitudinal study that follows the same

hospital over a certain number of years permits causal inference with respect to the

research questions that this study attempts to answer.

18

Third, studying public hospitals as a separate entity helps find more reliable and

helpful results for policy making. Prior studies on ownership conversion combined both

public hospitals and not-for profit hospitals into one category (Picone, Chou & Sloan,

2002; Shen, 2002, 2003; Sloan, 2002); the results from such studies might be biased since

public hospitals have a different operating environment than private not-for-profit

hospitals such as lack of access to private funding, heavy political constraints and

bureaucracy, lack of managerial flexibility and a heavier social burden.

Fourth, providing evidence on the outcomes of privatization and knowing whether

conversion from public to private for-profit status or from public to private not-for-profit

status results in a better outcome can help stakeholders make sound decisions based on

scientific evidence. Sixth, this is the first empirical study on public hospitals‘

privatization that applies a theoretical framework. Applying the resource dependence

theory will add value to extant literature as the majority of prior studies on ownership

conversion did not use theories; they did not examine the logical associations between the

main variables of interest. Theoretical frameworks are important because they serve as a

guide. They help researchers include other concepts and variables that might have been

overlooked. Moreover, theories are valuable tools for scientific research; they assist

researchers in logically and systematically explaining and predicting a phenomenon.

Furthermore, a study that includes a theoretical framework contributes to science as the

study tests the predicting strength of the theory (Hunt, 2002).

19

CHAPTER 2

REVIEW OF LITERATURE

This chapter contains two major sections: Section 1 includes the literature review

and section 2 includes the conceptual framework and hypotheses.

Literature Review

This section presents a review of the empirical studies on the antecedents and

consequences of ownership conversion of public hospitals. The search of the extant

literature was conducted by entering the phrases: ―ownership conversion‖, ―determinants

of ownership conversion‖, ―privatization of public hospitals‖, ―conversion of public

hospitals into private hospitals‖, ―consequences of privatization‖, and ―privatization‖ in

the following data bases: ABI Inform, JSTOR, Pubmed, Science Direct, Springer Link,

Web of Knowledge, Wiley Interscience, Business Source Premier, and Google Scholar,

respectively. Additionally, the reference list at the back of each article was checked

whether previously published relevant articles were cited.

In most cases, an organization changes ownership status through a transaction

with another organization of different ownership type. Such transactions include merger,

sale, lease, or joint venture (Anderson, Allred, & Sloan, 2003; Goodstein & Boecker,

1991; Hall & Conover, 2006; Needleman, 1999). An organization can directly change its

20

ownership status by filling out legal documents; a conversion that involves a single

organization rarely occurs in the healthcare setting (Cutler & Horwitz, 1997; Needleman,

1999). Public hospitals conversion into private not-for-profit or private for-profit status is

also called privatization of public hospitals (Legnini et al., 1999).

Ownership conversion is a dynamic phenomenon; a hospital might change

ownership status more than once in its lifetime (Burns et al., 2009; Cutler & Horwitz,

2000). Some healthcare organizations other than public hospitals such as public nursing

homes, have converted into private for-profit or private not-for-profit status

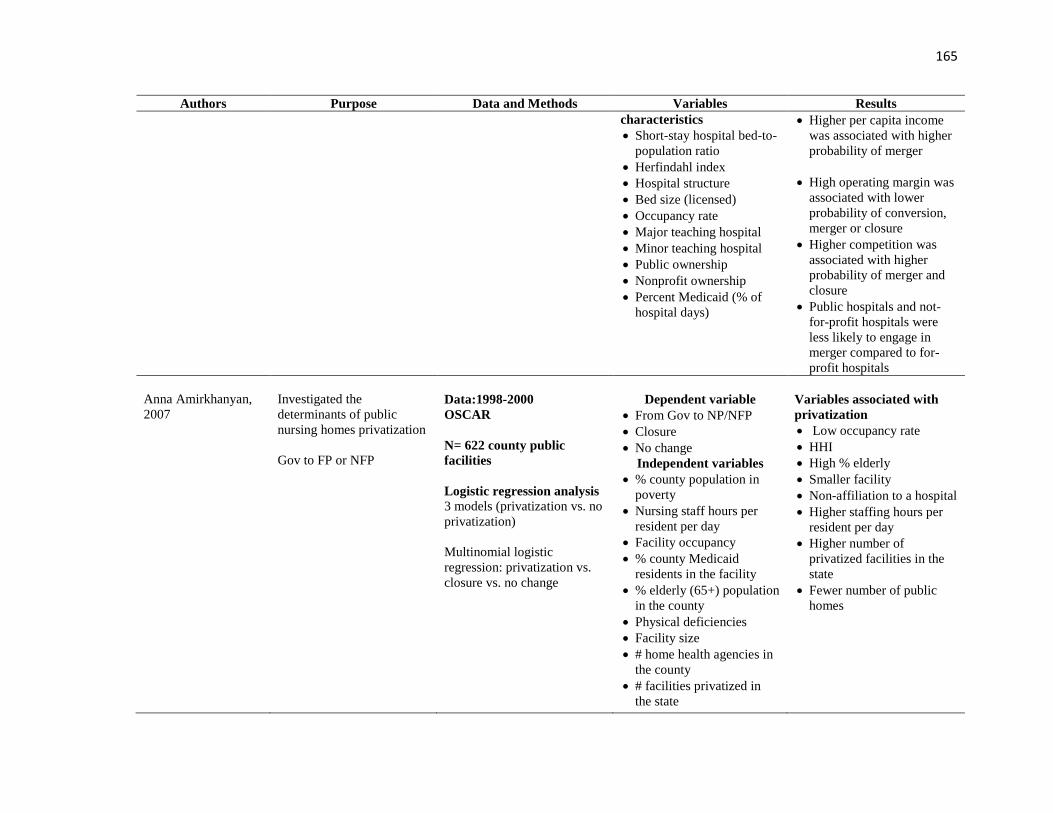

(Amirkhanyan, 2008; Amirkhanyan, 2007).

This literature review has four major sections: (1) the antecedents of public

healthcare organizations conversion into private for-profit status, (2) the antecedents of

public healthcare organizations conversion into private not-for-profit status, (3) the

consequences of public healthcare organizations conversions into private for-profit status

on financial performance, (4) the consequences of public healthcare organization

conversions into private not-for-profit status on financial performance.

Privatization of public hospitals and other healthcare organizations

As discussed in the previous chapter, public hospitals have been coined as the

―providers of last resort‖ or ―safety net hospitals‖ (Andrulis, 1997; Bovbjerg et al., 1987).

Public hospitals are mandated to provide healthcare services to everyone regardless of

health insurance status or ability to pay (Anderson, Boumbulian & Pickens, 2004) and yet

the expectations on public hospitals have been higher than that of private hospitals.

21

Public hospitals have been required to provide more charity care than private hospitals

and yet the funding from local or state government has diminished; they have lost

Medicaid patients to private hospitals and have had an increasing number of uninsured

and underinsured patients (Legnini et al., 1999). Public hospitals have been the providers

of expensive and tertiary services that private hospitals would not deliver. In addition,

public hospitals have played a major role in the provision of medical education. Medical

education enables hospitals to provide highly specialized care. While private hospitals

have also provided medical education, public teaching hospitals have been the major

providers of such highly specialized care freely to those unable to pay (Andrulis, 1997;

Bovbjerg, et al., 1987; Brown, 1983, Legnini et al., 1999). Moreover, public hospitals

have not been able to successfully compete for managed care contracts and they have no

freedom to raise capital, make major employee recruitment decision, and initiate

important strategic decisions to turn the financial performance of the hospital around.

All these factors have contributed to the financial crisis that most public hospitals

have been facing (Brown, 1983; Sataline, 2010). Consequently, public hospitals have

been motivated to change ownership status for financial stability and access to capital,

better patient mix, higher efficiency, and freedom from politics and public constraints.

Additionally, a hospital with budget deficit may change ownership status because the

local or state government cannot afford to financially support it anymore; therefore, it

becomes a financial burden to the community. Becoming private will set a public hospital

free from relying on tax income, which dramatically depletes during an economic crisis.

Becoming private also removes the public expectation of serving a large percentage of

low income population and providing costly tertiary services. Accordingly, handing the

22

operation of the hospital over to private entities through sale or joint ventures would

financially and fiscally relieve the community from social and fiscal burden (Burns et al.,

2009; Legnini et al., 1999; Sloan, Taylor Jr, & Conover, 2000; Needleman et al., 1997).

Furthermore, privatization has reflected the trend of public entities handing the

task of serving the public over to private entities (Sloan, et al., 2000). On the other hand,

privatization has been one of the long-term strategies for survival of public hospitals.

Likewise, privatization has also occurred in the nursing home industry (Amirkhanyan,

2007; Amirkhanyan, 2008).

The proponents of privatization of public hospitals argued that non-federal public

hospitals are the least efficient compared to private hospitals (Burgess & Wilson, 1996;

Coyne, Richards, Short, Shultz & Singh, 2009). Therefore, privatization helps hospitals

to be more efficient (Desai, Lukas, & Young, 2000) and save money (Bovbjerg et al.,

2000). Besides, privatization relieves the government from fiscal pressure and it enhances

tax revenue, specifically for privatization into for-profit status since for-profit hospitals

pay property and corporate income taxes (Gapenski, 2004). Moreover, privatization

releases public hospitals from the grip of politics and bureaucracy; and it offers hospitals

more freedom and flexibility in decision making (Bovbjerg, et al., 2000; Siegel, 1996).

Additionally, privatization offers hospitals better access to capital which may

result in the acquisition of updated technology, recruitment of capable managers and

clinical staff and restoration of infrastructure (Burgess & Wilson, 1996; Desai et al.,

2000; Siegel, 1996; Wessel, 1995), and improved healthcare quality (Bovbjerg, et al.,

2000). Some people argued that, in addition to public hospitals, private not-for-profit

hospitals have also acted as safety net providers for the community. Therefore,

23

privatizing public hospitals into not-for-profit hospitals will not alter the provision of

uncompensated care (Bovbjerg et al., 2000).

The opponents of privatization are concerned about the possible loss of access to

care for the indigent as the converted hospitals might not be committed to serving the

poor anymore; research has demonstrated that privatization decreased the level of

uncompensated care delivered to the needy (Thorpe et al., 2000; Desai et al., 2000).They

argued that only public hospitals are committed to the genuine ―open door‖ policy that

unconditionally ensures access to good care for everyone (Bovbjerg, et al., 2000; Desai,

et al., 2000). Conversion of public hospitals into for-profit status has raised concern that

the converted hospital will shut down expensive services and might eventually close the

hospital if it does not exhibit sound financial performance (Sataline, 2010).

The antecedents of healthcare organizations conversion from public to for-

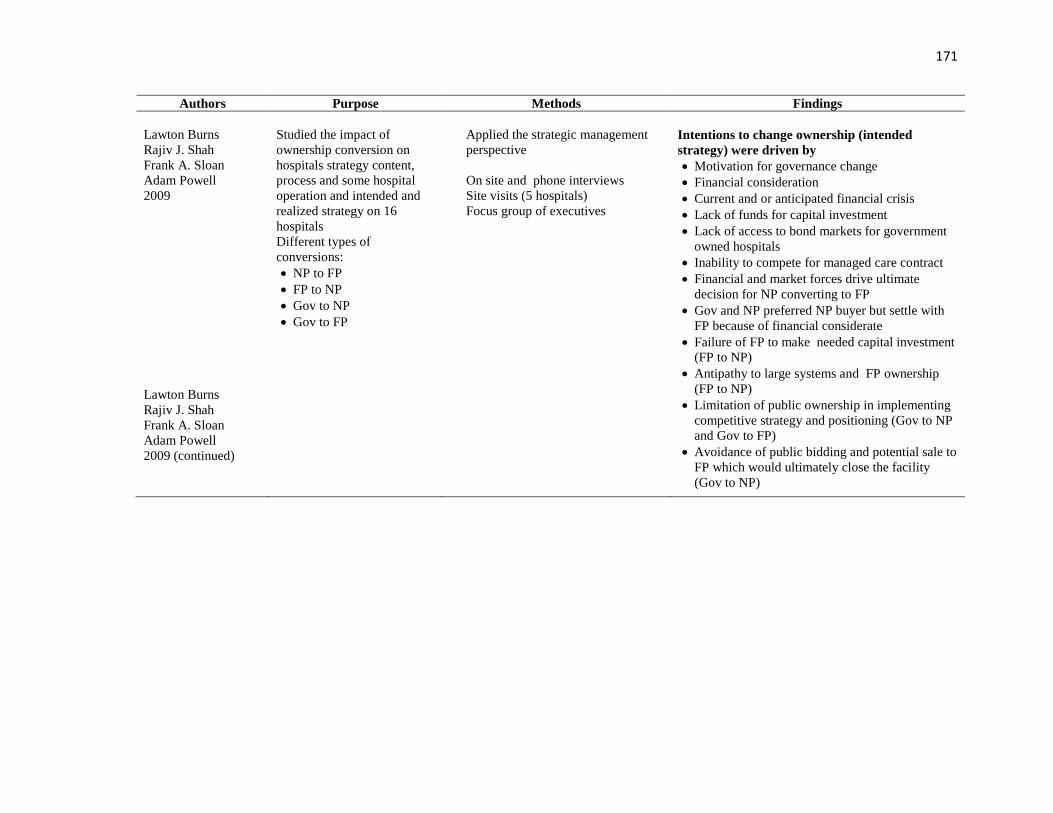

profit status. To my knowledge, one quantitative study (Sloan et. al, 2003) and four case

studies investigated the antecedents of hospital ownership conversion from public to for-

profits status ( Bovbjerg et al., 2000; Burns et al., 2009; Legnini et al., 1999; Sloan, et al.,

2000) and another quantitative study examined the antecedents of nursing homes

privatization (Amirkhanyan, 2007). Sloan et al. (2003) combined public hospitals and

not-for-profit hospitals in one category and explored the antecedents of conversions as

well as mergers and closures; Amirkhanyan (2007) did not distinguish between

conversion from public to for-profit status and conversion from public to not-for-profit

status. Both the studies on hospitals and nursing homes demonstrated that some

environmental factors and organizational factors influenced this type of conversion.

24

The environmental factors that were associated with hospital conversion from not-

for-profit or public status into for-profit status included: low percentage of elderly people

in the population, high competition among hospitals, lower unemployment rate, high

percentage of HMO enrollment, and low per capita income (Sloan, et al., 2003). Higher

unemployment rate was associated with higher probability of closure (Sloan, et al., 2003).

The environmental factors that significantly affected public nursing homes conversion

into for-profit status included: low percentage of elderly people in the population, high

competition among nursing homes, high number of privatized nursing home facilities in

the county and fewer number of nursing homes owned by counties within the state

(Amirkhanyan, 2007).

The organizational factors that significantly affected ownership status were

financial condition, capacity and utilization. Low operating margin and high debt-to-

asset ratio increased the probability of not-for-profit and public hospital conversion into

for-profit status (Sloan, et al., 2003). Furthermore, the case studies on conversion of

public hospitals into for-profit status suggested current financial distress or anticipated

financial crisis, operating inefficiency, changing healthcare environment that has resulted

in higher competition for managed care contracts, decrease in Medicare and Medicaid

reimbursement, lack of access to capital needed for infrastructure renovation,

unwillingness of political leaders to increase tax rates for higher tax revenue that would

financially support public hospitals, inadequate reimbursement system, cumbersome

purchasing and recruitment processes, lack of flexibility in adopting competitive

strategies, and prevention of hospital closure, as the major reasons for hospital

privatization (Bovbjerg et al., 2000; Burns et al., 2009; Legnini et al., 1999; Sloan et al.,

25

2000). Besides, the study on nursing homes found that nursing homes with lower

occupancy rate, fewer beds, higher number of nursing staff hours per resident days, and

older infrastructure, were more likely to privatize and facilities affiliated with hospitals

were less likely to privatize (Amirkhanyan, 2007).

While Sloan et al. (2003) included financial variables such as operating margin

and debt-to-capitalization ratio as factors leading to ownership conversion; they did not

use the Altman z-score method to measure hospitals‘ financial conditions. A hospital

might have high operating margin and high debt-to-capitalization ratio at the same time;

it is difficult to determine whether the hospital is in good or bad financial condition. The

Altman Z-score that combines four financial ratios into one discriminant equation is a

better measure of financial condition than operating margin and debt-to-asset ratio as it

has a cut-off score that determines whether the organization is in financial distress or not.

The antecedents of healthcare organizations conversion from public to not-

for-profit status. The choice of not-for-profit instead of for-profit status reflects the

willingness of the public hospital to pursue its current mission which is to provide quality

care and serve the community without a profit motive. This choice might also suggest

that public hospitals avoid the takeover of a for-profit hospital. A for-profit buyer might

be tempted to close the facility to reduce competition among its own hospitals located in

the public hospital‘s area (Burns et al., 2009). Quantitative empirical studies of the

antecedents of ownership conversion from public to not-for-profit status have been

scarce.

26

Most of the reasons for converting from public to not-for-profit status, found in

case studies, were quite similar to the reasons for converting from public to for-profit

status including financial hardships and operating losses, increased competition and

inability to compete for managed care and other third-party payers contracts,

apprehension of funding reduction from Medicaid reimbursement and disproportionate

share hospital funding, delayed reimbursement, need for access to capital, freedom for

public governance constraints , and strong pressure for tax relief ( Bovbjerg, et al., 2000;

Burns et al., 2009; Legnini et al., 1999; Sloan et al., 2003; Sloan et al., 2000).

The consequences of ownership conversion from public to for-profit status on

financial performance. Four studies investigated the consequences of conversion from

public to for-profit status on hospitals financial performance (Thorpe et al., 2000; Shen

2003; Picone et al., 2002; Sloan, Taylor & Conover, 2000). The first three studies used

panel data of national samples of acute care hospitals and investigated more than one type

of ownership conversions (Thorpe et al., 2000; Shen 2003; Picone et al., 2002) and the

last study of Sloan, Taylor and Conover (2000) was a case study of 10 hospitals located

in Tennessee, North Carolina and South Carolina. Thorpe, Florence and Sieber (2000)

isolated public hospitals as a single entity; (Shen 2003 & Picone et al., 2002) combined

public hospitals and private not-for-profit hospitals into one category. The effects of

conversion from public to for-profit status on total margin and profit margin were mixed;

there was no significant change in total margin after conversion (Thorpe et al., 2000), but

Shen (2003) and Picone et al., (2002) found that total margin and operating margin

increased after conversion, respectively.

27

The findings regarding the effect of conversion on operating costs were

consistent; cost per admission decreased (Thorpe et al., 2000) and operating costs per

discharge decreased (Shen, 2003). Sloan, Taylor and Conover (2000) explored the

impact of conversion on internal rate of return relative and cost of capital and found

mixed results. One hospital‘s internal rate of return exceeded the cost of capital by 3.14

percentage points over 30 years and another hospital‘s rate of return was lower than the

costs of capital after conversion.

The consequences of ownership conversion from public to not-for-profit

status on financial performance. Three studies investigated the impact of conversion

from public to not-for-profit status on financial performance in terms of operating cost,

efficiency and internal rate of return (Shen, 2003; Sloan, Taylor Jr, & Conover, 2000;

Anonymous). Similar to the conversion from public to for-profit hospitals, operating

costs declined after conversion from public to not-for-profit status (Shen, 2003). The

study on the impact of conversion on operating efficiency found that efficiency was

enhanced after conversion (Anonymous). The case study that examined the impact of

conversion on internal rate of return found that one public hospital that converted into

not-for-profit status posted 253% internal rate of return relative to 4.71% cost of capital

after conversion(Sloan, Taylor Jr, & Conover, 2000).

The paucity of empirical studies on privatization of healthcare organizations and

mixed results has left a gap in the literature. This gap is evidenced by the lack of

empirical studies on the antecedents of public hospitals conversion into not-for-profit

28

status. Additionally, only one empirical study investigated the antecedents of public

hospitals‘ conversion into for-profit status and one single study explored the antecedents

of privatization of nursing homes. Overall, poor financial performance and increased

competition were found to be the major factors leading to privatization and privatization

resulted in improved financial performance and enhanced efficiency.

As stated earlier, these studies have some limitations as they did not apply some

theoretical frameworks; as a result, they omitted key environmental variables such as

excess capacity, number of active physicians in the county, and variables that measure

the level of environmental dynamism; these variables can affects organizational financial

performance. This study addresses these limitations. Table 2 in Appendix A presents the

summary of the methods and variables of the studies reviewed in this chapter.

Conceptual Framework and Hypotheses

Theoretical Background

As previously mentioned, the healthcare environment has shaped the healthcare

system in the U.S. Since the purpose of this study is to investigate the impact of

organizational and environmental factors on public hospitals‘ financial distress, the

impact of financial distress on public hospitals‘ privatization, and the effect of

privatization on financial performance, applying an organizational theory that takes the

environment into consideration is deemed appropriate for this study. The resource

dependence theory is one of the organizational theories that consider the environment as

a major determinant of an organization‘s strategic behavior. The following section

29

discusses the resource dependence theory and how it has been applied in previous

empirical studies.

Resource dependence theory. Every organization needs resources to fulfill its

vision, complete its mission and reach its goals. An organization has great challenges to

stay competitive if it does not possess adequate and sufficient resources. The resource

dependence theory (RDT) posits that ―the key to organizational survival is the ability to

acquire and maintain resources‖ (Pfeffer & Salancik, 1978, p.2). Therefore, resources are

crucial for the organization‘s life and yet they are scarce and not equally distributed

across organizations. Resource scarcity imposes constraints to the organizations (Aldrich

& Pfeffer, 1976). Constraints prevent organizations from reaching their objectives.

Consequently, organizations compete to acquire these resources.

Resources are viewed as the inputs that organizations need to produce outputs

and the environment refers to the ―organization‘s source of inputs and sink of outputs‖

(Pennings & Tripathi, 1978, p.172). In other words, the focal organization‘s environment

includes other entities from which it acquires resources and to which it sells products and

services. This definition implies that organizations are neither self-sufficient nor self-

reliant; they cannot acquire all the resources they need from within and they cannot

consume their own products and services (Stearns, Hoffman, & Heide, 1987). However,

the continuous availability of resources is uncertain. Uncertainty is one of the

characteristics of the environment and it refers to the fluctuation of resource availability

and the magnitude of challenges the organization has to face to acquire key resources

30

(Ulrich & Barney, 1984). Thus, scarcity of resources, combined with their uncertain

supply, makes resource acquisition a critical element to organizational survival.

An organization depends on other organizations to ensure continuous exchange of

resources. However, dependence on other organizations for resources implies lack of

independence and lack of power; those who possess resources have power over those

who do not have them (Galaskiewicz, 1985; Pfeffer, 2005; Pfeffer & Salancik, 1978).

The level of dependence on resources depends on how widely available and how

important the resource is to the organization (Jacobs, 1974). Accordingly, dependence is

defined as ―the product of the importance of a given input or output of the organization

and the extent to which it is controlled by a relatively few organizations‖ (Pfeffer &

Salancik, 1978, p.51). More specifically, an organization‘s dependence on a resource is

not critical to its survival unless it is a key resource and only a few suppliers possess it.

For example, even if physicians are important to a hospital, the hospital‘s dependence on

physicians is not that crucial if the hospital can hire physicians from many medical

schools and other hospitals. And if only one organization supplies magnetic resonance

imaging devices (MRI) but the hospital prefers to use computer tomography scans (CT

scan), then the hospital‘s dependence on MRI equipment is not imperative to the

hospital‘s survival.

Since an organization‘s possession and control of resources implies power,

organizations have to adopt various strategic moves to acquire and control resources

(Ulrich & Barney, 1984). Mergers and acquisitions, vertical or horizontal integration,

establishment of interorganizational coalitions, differentiations, and recruitment of board

members who can facilitate access to resources, are among the various strategic moves

31

that organizations adopt to reduce dependence on and increase control over resources

(Aldrich & Pfeffer, 1976; Pfeffer, 2005; Pfeffer & Salancik, 1978; Sofaer & Myrtle,

1991). Thus, resource dependence theory seeks to explain and predict the impact of the

environment and resource availability on an organization‘s behavior; consequently this

behavior can change the structure of the environment. For example, mergers,

acquisitions, and vertical and horizontal integrations may result in higher market

concentration.

The major assumptions of the RDT can be summarized as follows: (a)

organizations seek to maximize their power and independence from other organizations

by acquiring critical resources, (b) the environment imposes constraints on the

organizations as it does not possess all the required resources to sustain all organizations

and the supply of these scarce resources is uncertain, (c) organizations can survive in

their environment as long as they obtain continuous access to resources, (d) organizations

are capable of changing the environment; the various strategic moves that organizations

undertake to ensure resource acquisition will change environmental condition (Aldrich &

Pfeffer, 1976; Pfeffer, 2005; Ulrich & Barney, 1984).

RDT is a suitable theory that can explain why hospitals change ownership status

because ownership status is based on fiscal and legal requirements. Since previous

studies revealed that the major cause of ownership conversion is poor financial

performance, RDT might help explain why some public hospitals have poor financial

performance and consequently convert into private status. Public hospitals might seek

conversion because the government does not have enough financial resources to support a

hospital operating at a deficit.

32

Previous studies suggested that the unwillingness of the community and

politicians to financially support a public hospital operating at a loss, which has become a

heavy fiscal burden to the community, is one of the reasons for a public hospital‘s

conversion (Bovbjerg et al., 2000). Some other studies suggested the inability of public

hospitals to hire human resources with adequate capabilities and competencies as one of

the reasons for conversion (Burns et al., 2009). In other words, public hospitals change

ownership because the alternative type of ownership has more resources or offers easier

access to resources. As a result of the improved access to resources through conversion,

converting hospitals might be able to regain their financial health and stay competitive.

Moreover, converting hospitals might get resources other than financial capital if they

change ownership. For example, a public hospital will have more autonomy to acquire

advanced technology and hire capable managers and medical staff if it privatizes.

RDT has been applied in several empirical studies of various industries of

healthcare organizations. Given the importance of the environment in RDT, these studies

included both environmental and organizational factors as determinants of various

strategic moves such as adoption of innovation in clinical practices (Zinn, Weech, &

Brannon, 1998), delivery of specialized care (Banaszak-Holl, Zinn, & Mor, 1996;

Campbell & Alexander, 2005; Goldberg & Mick, 2010; Weech-Maldonado, Qaseem, &

Mkanta, 2009; Zinn, et al., 1998), improvement of clinical practice (Alexander & Wells,

2008; Starkey, Weech-Maldonado & Mor, 2005; Zinn, Weimer, Spector, & Mukanel.,

2010), increased participation in health care delivery (Zakus, 1998), engaging in strategic

partnership ( Alexander & Morrisey, 1989; McKinney, Morrissey & Kaluzny, 1993;

Zinn, Mor, Castle, Intrator, & Brannon, 1999), community orientation (Proenca, Rosko,

33

& Zinn, 2000), and diversification into new services unrelated to previous ones

(Alexander, D'Aunno, & Succi, 1996a, 1996b). In addition, RDT has been applied to

explain the composition and function of hospital board members (Pfeffer, 1973); the

board of directors functions as boundary spanner that helps organizations to acquire

resources.

The studies mentioned above demonstrated that RDT has strong capabilities in

explaining an organization‘s strategic behavior. The reviews of the literature on resource

dependence theory confirmed this finding (Davis & Cobb, 2009; Nienhuser, 2008).

Interestingly, since the major reason for public hospital privatization is to obtain easier

access to resources such as financial resources, human resources as well as updated

technology and since better access to resources is expected to enhance financial

performance, the resource dependence theory has never been applied to the study of the

antecedents of public hospitals financial performance, their privatizations and the

consequences of privatization on financial performance. Based on the resource

dependence theory, this study is conducted using the conceptual framework illustrated in

Figure 1.1.

34

Figure 1.1 Conceptual Framework

The conceptual framework in Figure 1.1 illustrates the associations between

environmental factors and public hospital financial distress, the associations between

organizational factors and public hospital financial distress, the effect financial distress

has on public hospital privatization, and the impact of privatization on subsequent

financial performance. For the scope of this study, the major environmental factors of

interest include environmental munificence, environmental dynamism and environmental

complexity. The main organizational factors of interest include hospital size and hospital

teaching status.

The bold arrows in Figure 1.1 represent the associations between the independent

variables of interest and the dependent variable as stated in the hypotheses presented in

the following section. The dotted arrows represent the associations between the control