the automotive industry: global developments of production and registrations

DESCRIPTION

Presentation of the main issues relating to the automotive industry in the World: - Global Market - Current situation, Changes factors and Impact on global market. - Global Production - Current situation, Changing landscape of the automotive industry and Impact on global production. - Conclusion - Key points and view of 2020.TRANSCRIPT

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

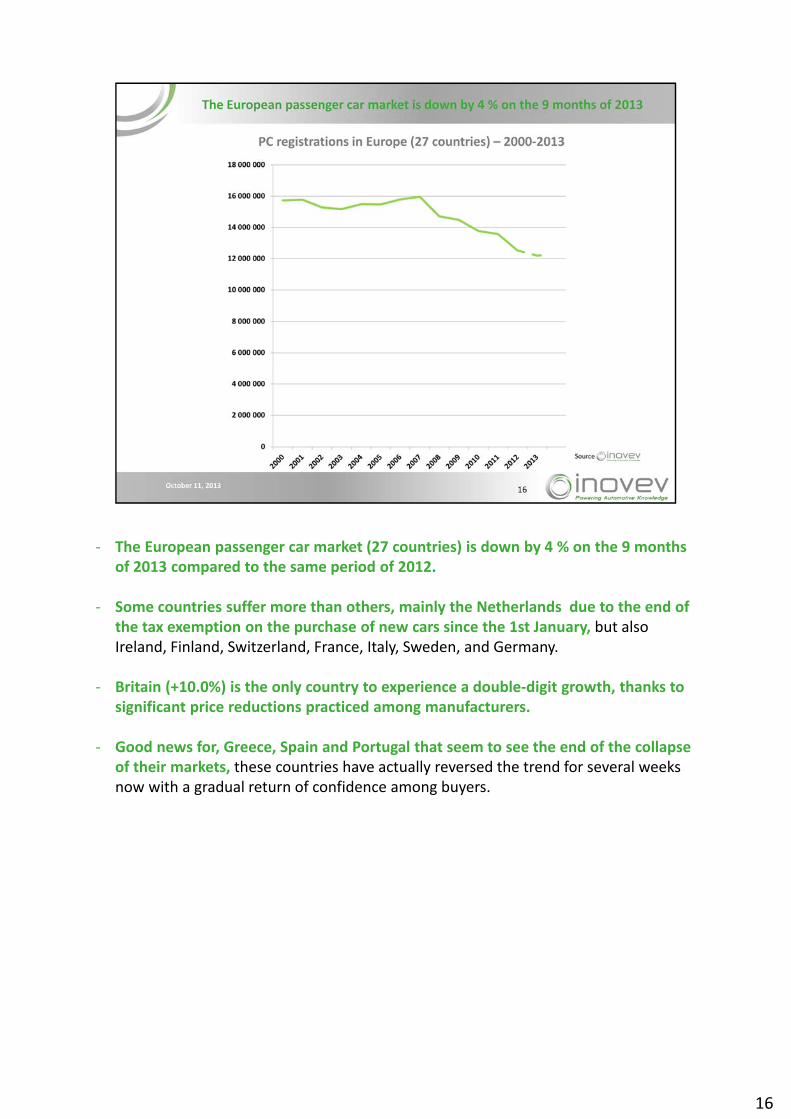

‐ The European passenger car market (27 countries) is down by 4 % on the 9 months of 2013 compared to the same period of 2012.

‐ Some countries suffer more than others, mainly the Netherlands due to the end of the tax exemption on the purchase of new cars since the 1st January, but also Ireland, Finland, Switzerland, France, Italy, Sweden, and Germany.

‐ Britain (+10.0%) is the only country to experience a double‐digit growth, thanks to significant price reductions practiced among manufacturers.

‐ Good news for, Greece, Spain and Portugal that seem to see the end of the collapse of their markets, these countries have actually reversed the trend for several weeks now with a gradual return of confidence among buyers.

16

17

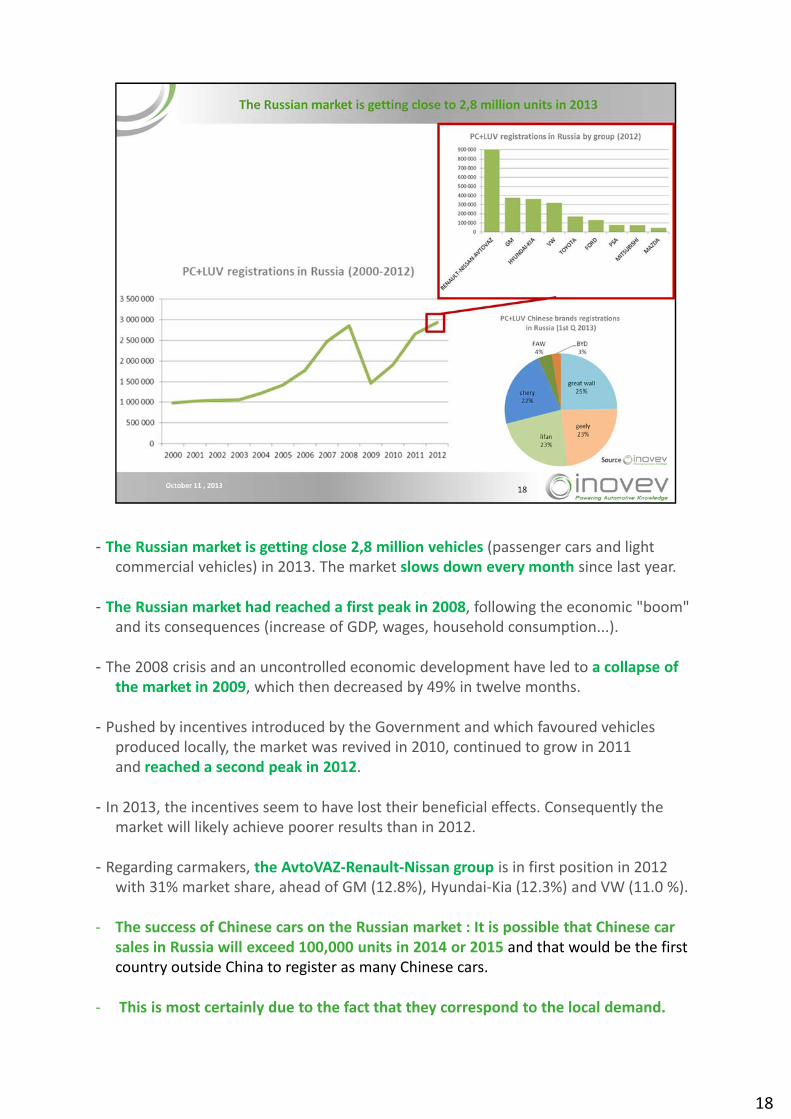

- The Russian market is getting close 2,8 million vehicles (passenger cars and light commercial vehicles) in 2013. The market slows down every month since last year.

- The Russian market had reached a first peak in 2008, following the economic "boom" and its consequences (increase of GDP, wages, household consumption...).

- The 2008 crisis and an uncontrolled economic development have led to a collapse of the market in 2009, which then decreased by 49% in twelve months.

- Pushed by incentives introduced by the Government and which favoured vehicles produced locally, the market was revived in 2010, continued to grow in 2011 and reached a second peak in 2012.

- In 2013, the incentives seem to have lost their beneficial effects. Consequently the market will likely achieve poorer results than in 2012.

- Regarding carmakers, the AvtoVAZ‐Renault‐Nissan group is in first position in 2012 with 31% market share, ahead of GM (12.8%), Hyundai‐Kia (12.3%) and VW (11.0 %).

‐ The success of Chinese cars on the Russian market : It is possible that Chinese car sales in Russia will exceed 100,000 units in 2014 or 2015 and that would be the first country outside China to register as many Chinese cars.

‐ This is most certainly due to the fact that they correspond to the local demand.

18

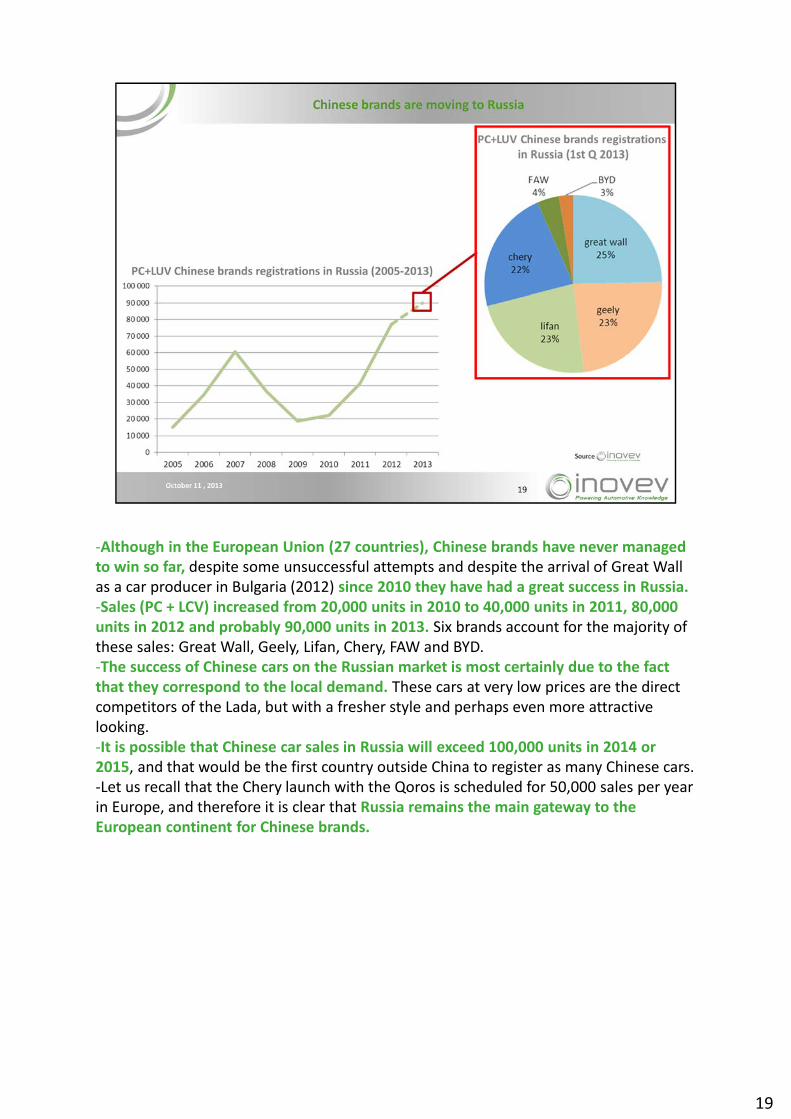

These cars at very low prices are the direct competitors of the Lada, but with a fresher style and perhaps even more attractive looking.

‐ Let us recall that the Chery launch with the Qoros is scheduled for 50,000 sales per year in Europe, and therefore it is clear that Russia remains the main gateway to the European continent for Chinese brands.

18

‐Although in the European Union (27 countries), Chinese brands have never managed to win so far, despite some unsuccessful attempts and despite the arrival of Great Wall as a car producer in Bulgaria (2012) since 2010 they have had a great success in Russia.‐Sales (PC + LCV) increased from 20,000 units in 2010 to 40,000 units in 2011, 80,000 units in 2012 and probably 90,000 units in 2013. Six brands account for the majority of these sales: Great Wall, Geely, Lifan, Chery, FAW and BYD.‐The success of Chinese cars on the Russian market is most certainly due to the fact that they correspond to the local demand. These cars at very low prices are the direct competitors of the Lada, but with a fresher style and perhaps even more attractive looking.‐It is possible that Chinese car sales in Russia will exceed 100,000 units in 2014 or 2015, and that would be the first country outside China to register as many Chinese cars.‐Let us recall that the Chery launch with the Qoros is scheduled for 50,000 sales per year in Europe, and therefore it is clear that Russia remains the main gateway to the European continent for Chinese brands.

19

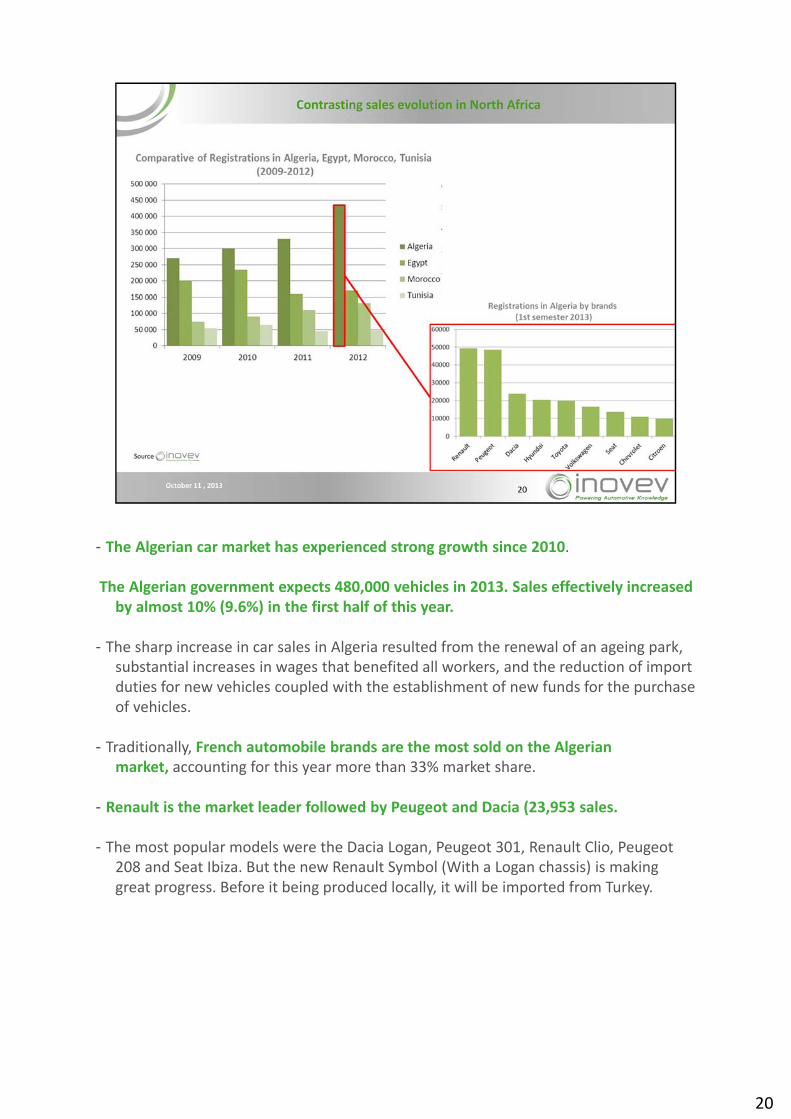

- The Algerian car market has experienced strong growth since 2010.

The Algerian government expects 480,000 vehicles in 2013. Sales effectively increased by almost 10% (9.6%) in the first half of this year.

- The sharp increase in car sales in Algeria resulted from the renewal of an ageing park, substantial increases in wages that benefited all workers, and the reduction of import duties for new vehicles coupled with the establishment of new funds for the purchase of vehicles.

- Traditionally, French automobile brands are the most sold on the Algerian market, accounting for this year more than 33% market share.

- Renault is the market leader followed by Peugeot and Dacia (23,953 sales.

- The most popular models were the Dacia Logan, Peugeot 301, Renault Clio, Peugeot 208 and Seat Ibiza. But the new Renault Symbol (With a Logan chassis) is making great progress. Before it being produced locally, it will be imported from Turkey.

20

21

22

23

24

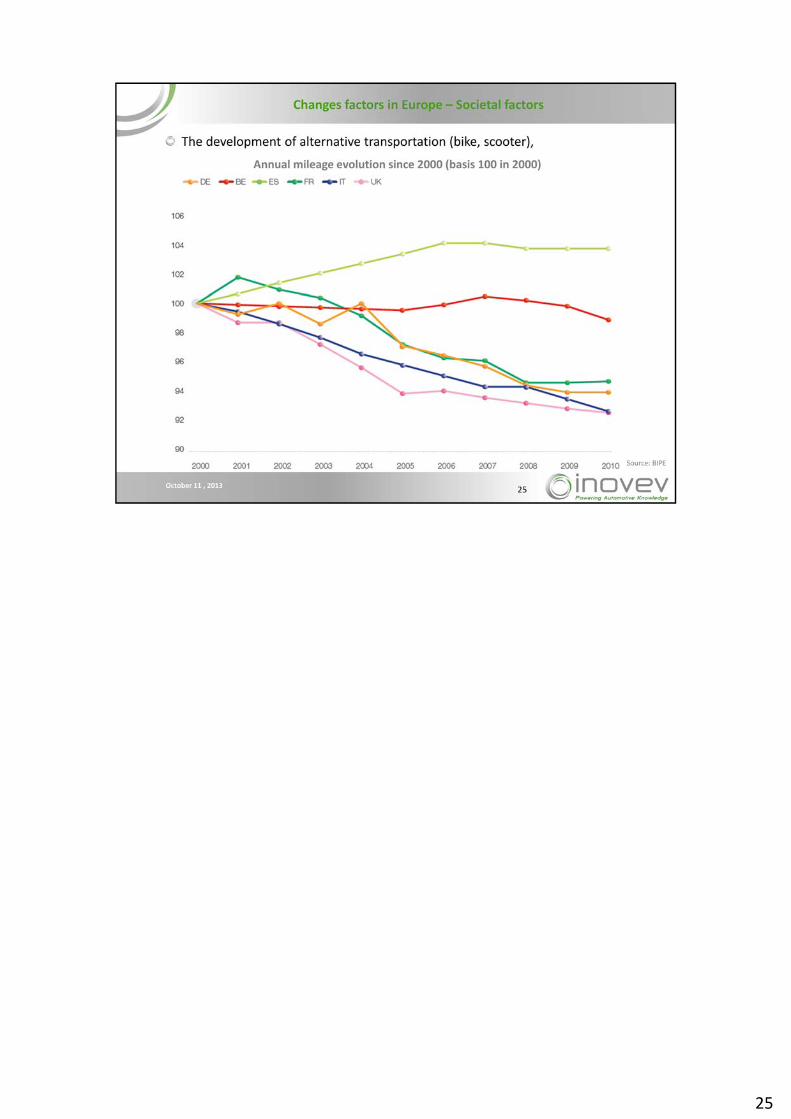

25

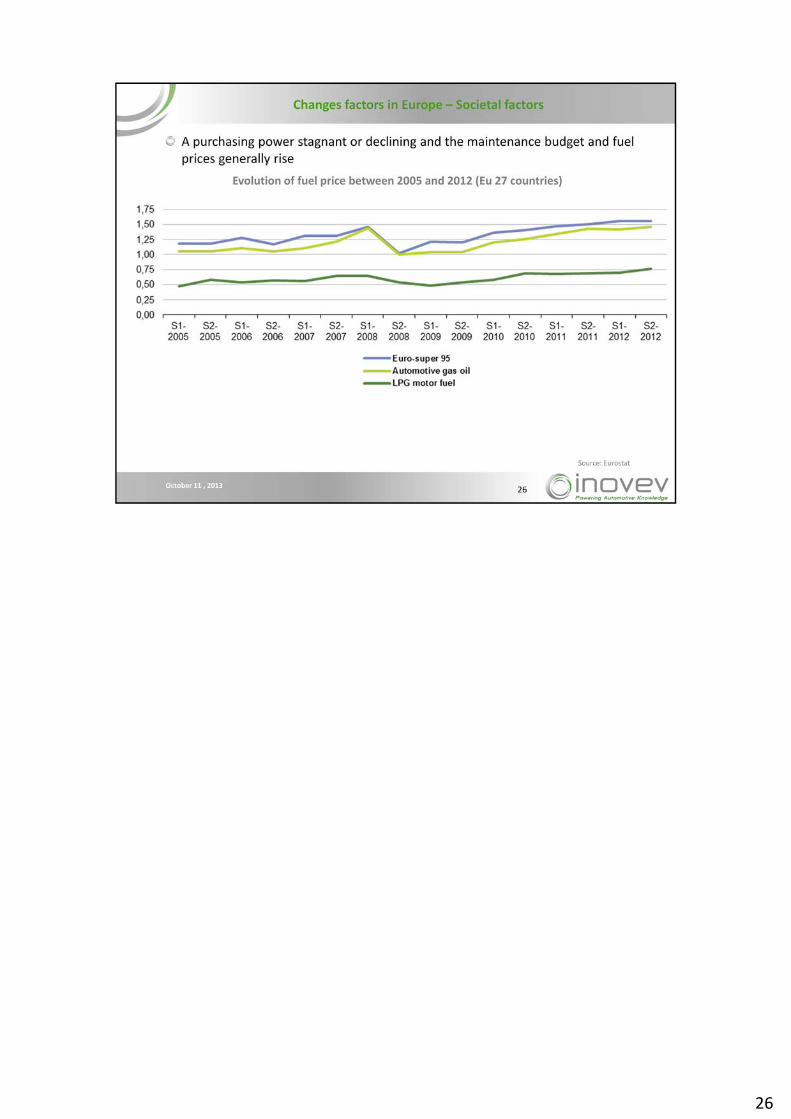

26

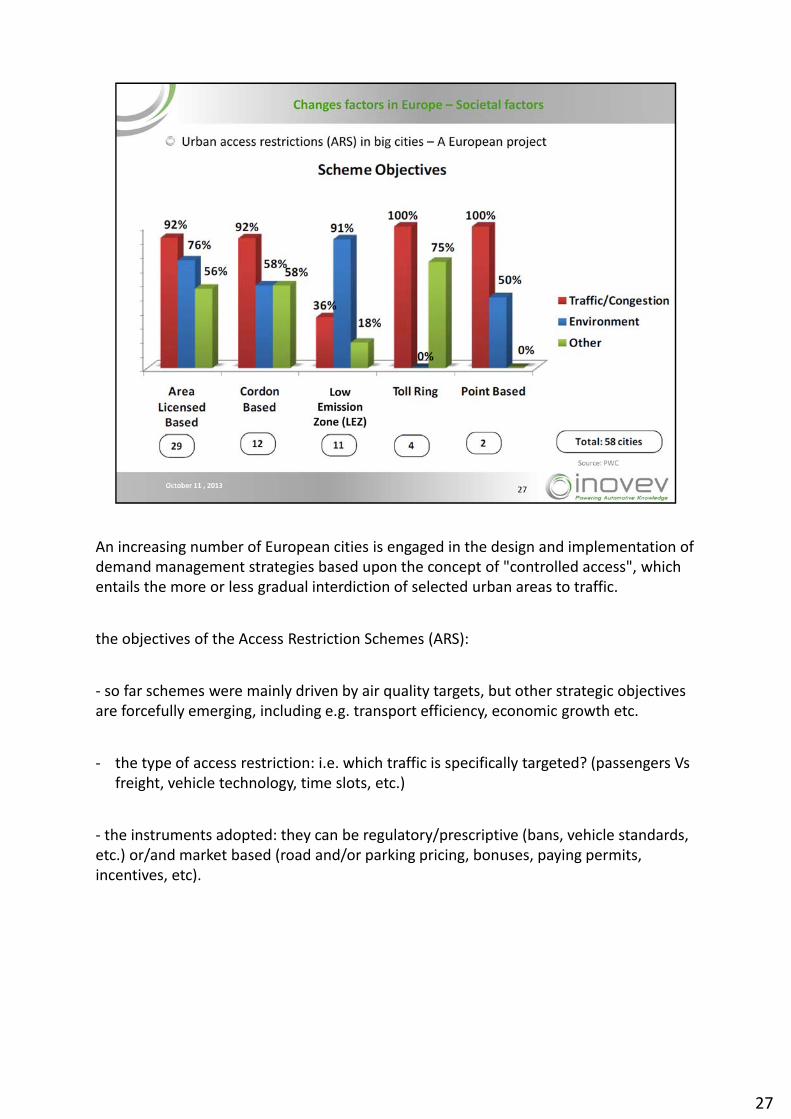

An increasing number of European cities is engaged in the design and implementation of demand management strategies based upon the concept of "controlled access", which entails the more or less gradual interdiction of selected urban areas to traffic.

the objectives of the Access Restriction Schemes (ARS):

‐ so far schemes were mainly driven by air quality targets, but other strategic objectives are forcefully emerging, including e.g. transport efficiency, economic growth etc.

‐ the type of access restriction: i.e. which traffic is specifically targeted? (passengers Vsfreight, vehicle technology, time slots, etc.)

‐ the instruments adopted: they can be regulatory/prescriptive (bans, vehicle standards, etc.) or/and market based (road and/or parking pricing, bonuses, paying permits, incentives, etc).

27

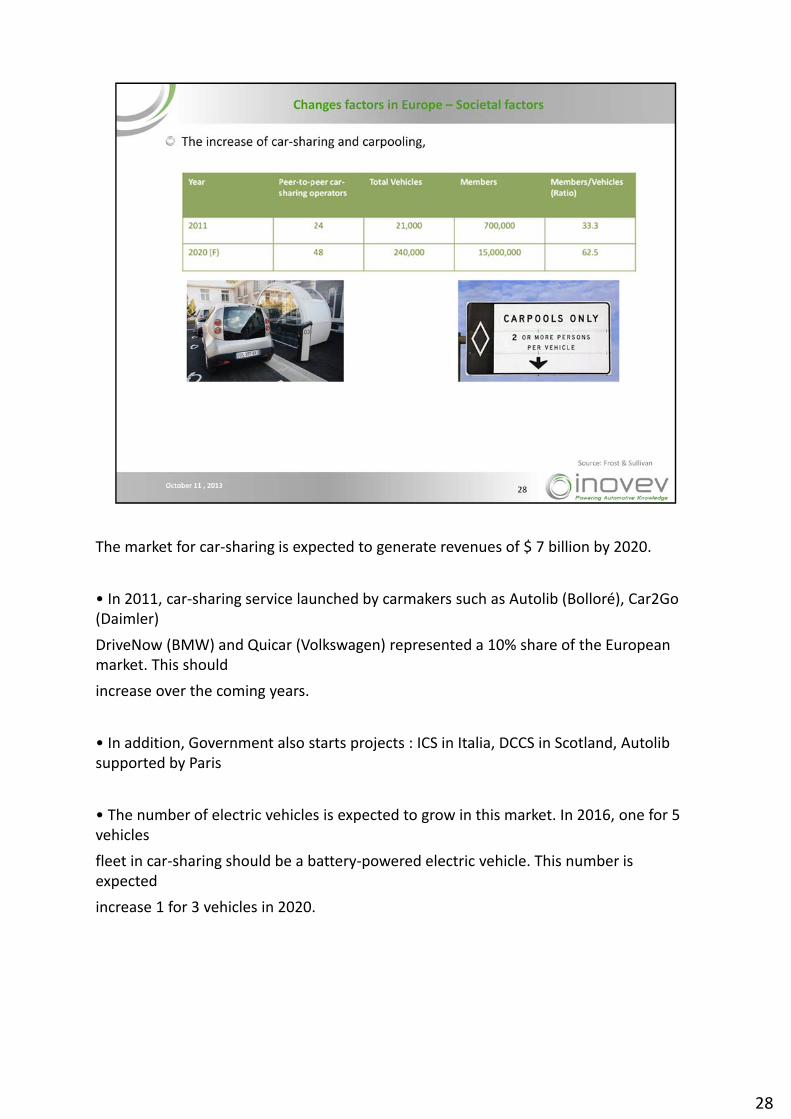

The market for car‐sharing is expected to generate revenues of $ 7 billion by 2020.

• In 2011, car‐sharing service launched by carmakers such as Autolib (Bolloré), Car2Go (Daimler)

DriveNow (BMW) and Quicar (Volkswagen) represented a 10% share of the European market. This should

increase over the coming years.

• In addition, Government also starts projects : ICS in Italia, DCCS in Scotland, Autolib supported by Paris

• The number of electric vehicles is expected to grow in this market. In 2016, one for 5 vehicles

fleet in car‐sharing should be a battery‐powered electric vehicle. This number is expected

increase 1 for 3 vehicles in 2020.

28

29

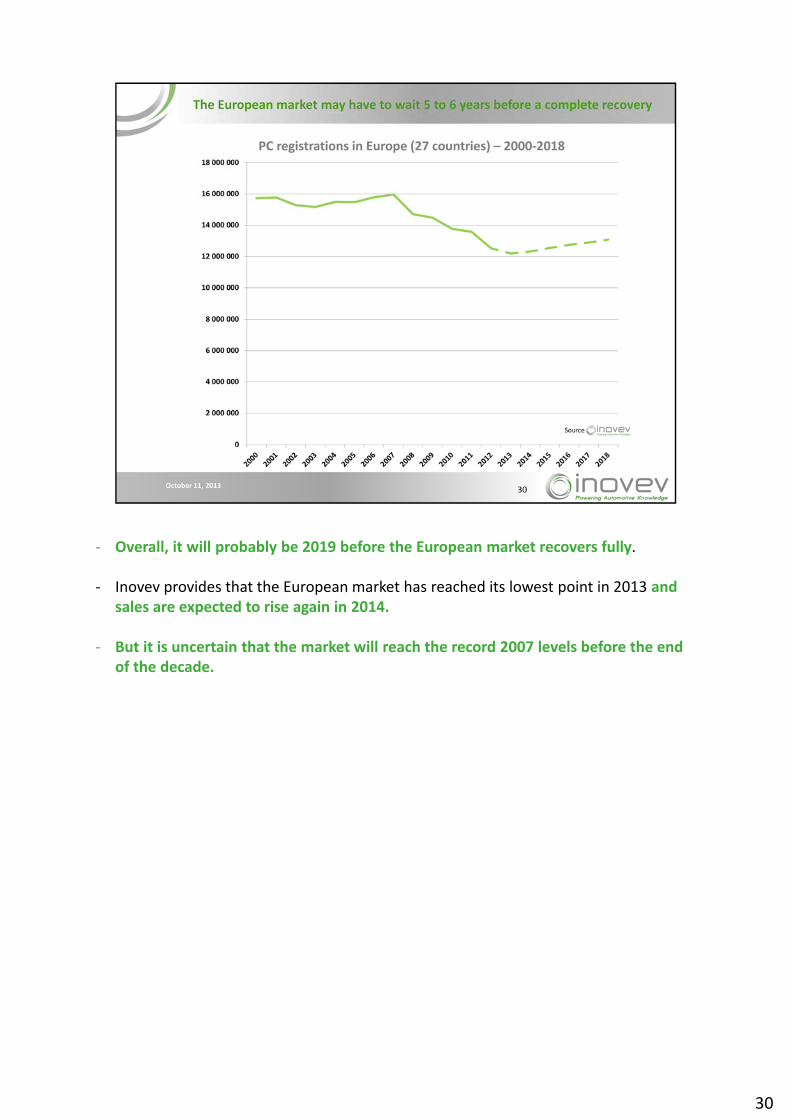

‐ Overall, it will probably be 2019 before the European market recovers fully.

‐ Inovev provides that the European market has reached its lowest point in 2013 and sales are expected to rise again in 2014.

‐ But it is uncertain that the market will reach the record 2007 levels before the end of the decade.

30

31

32

33

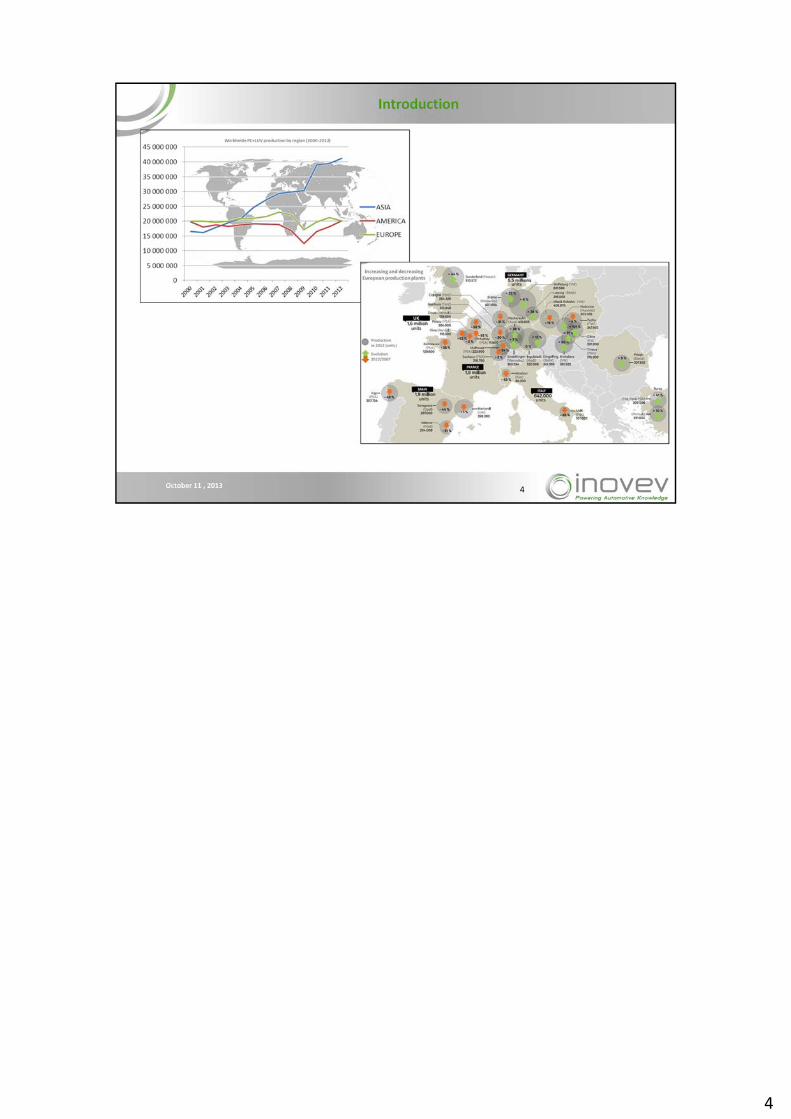

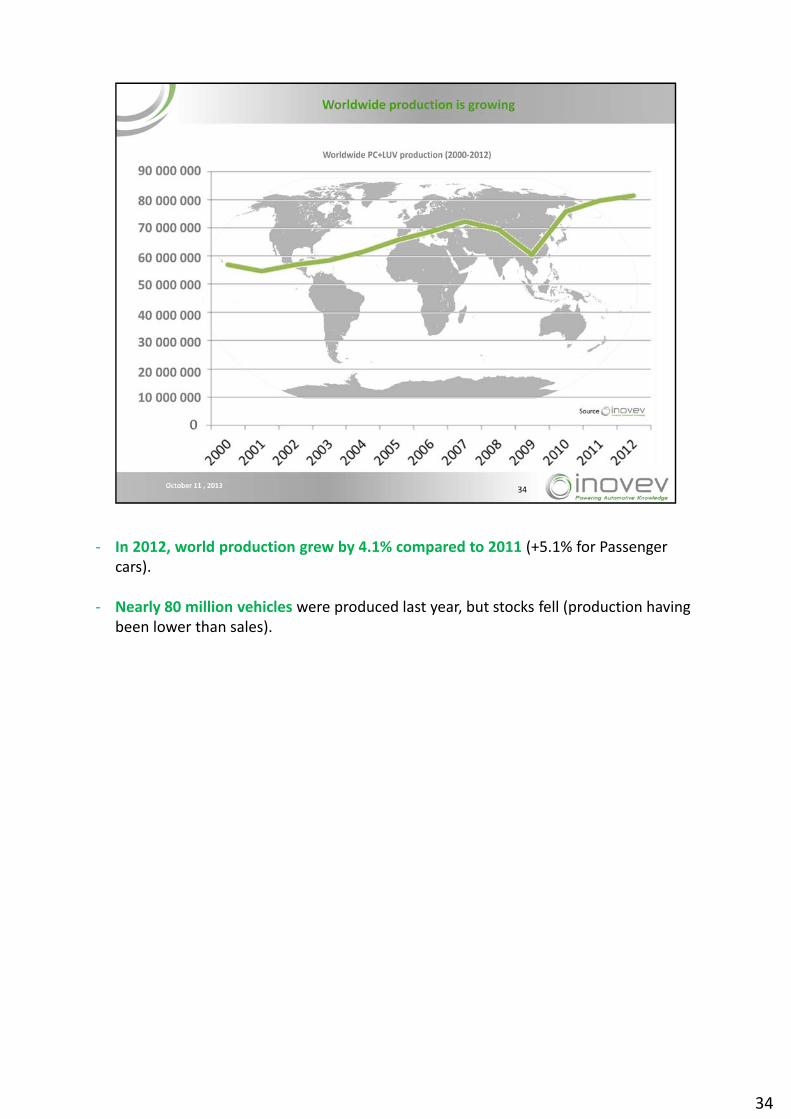

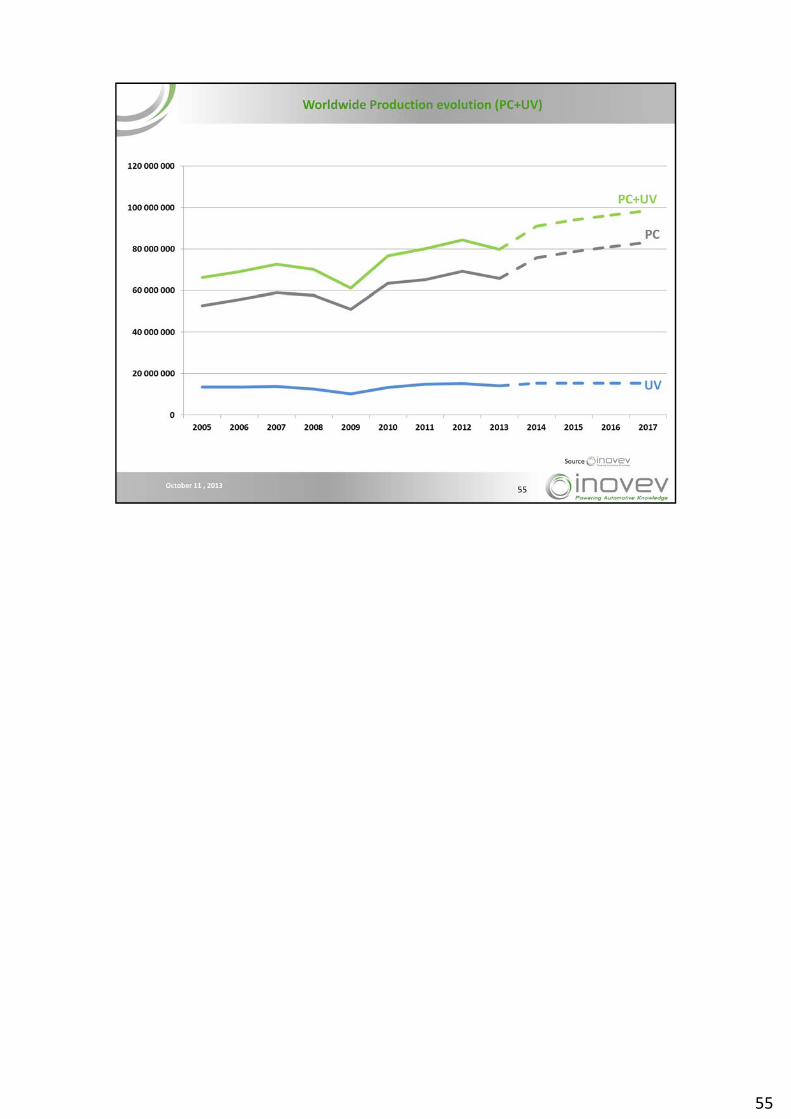

‐ In 2012, world production grew by 4.1% compared to 2011 (+5.1% for Passenger cars).

‐ Nearly 80 million vehicles were produced last year, but stocks fell (production having been lower than sales).

34

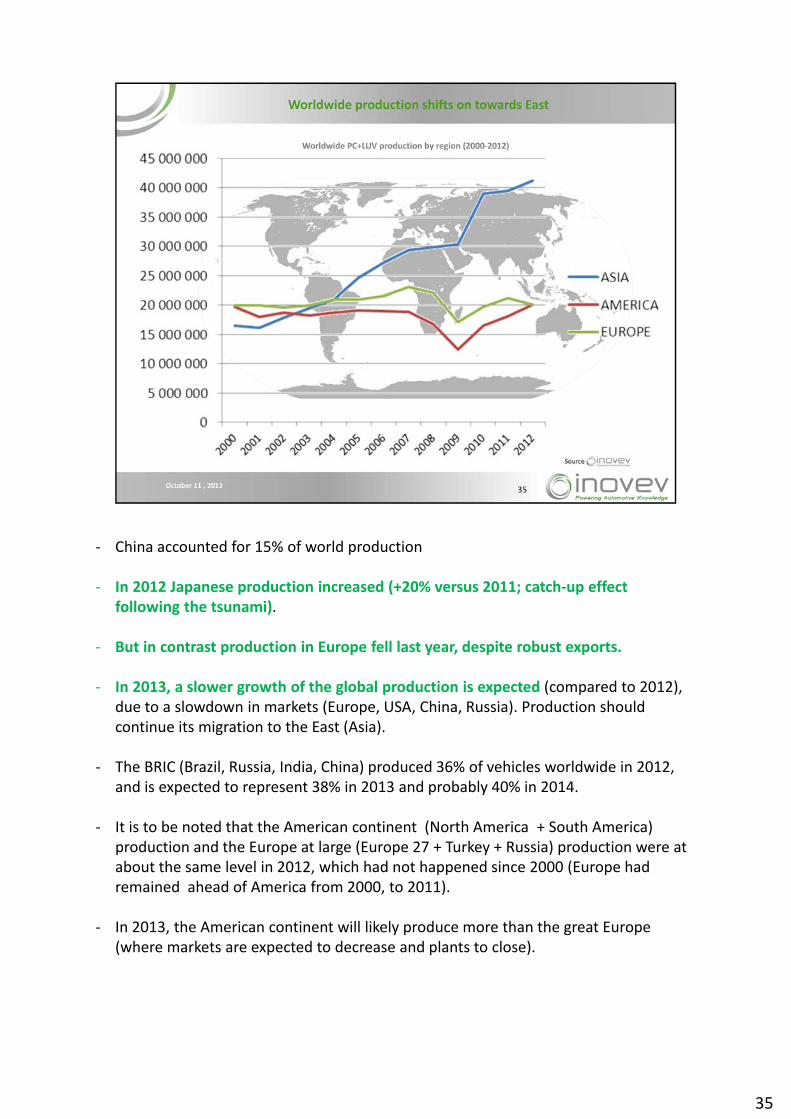

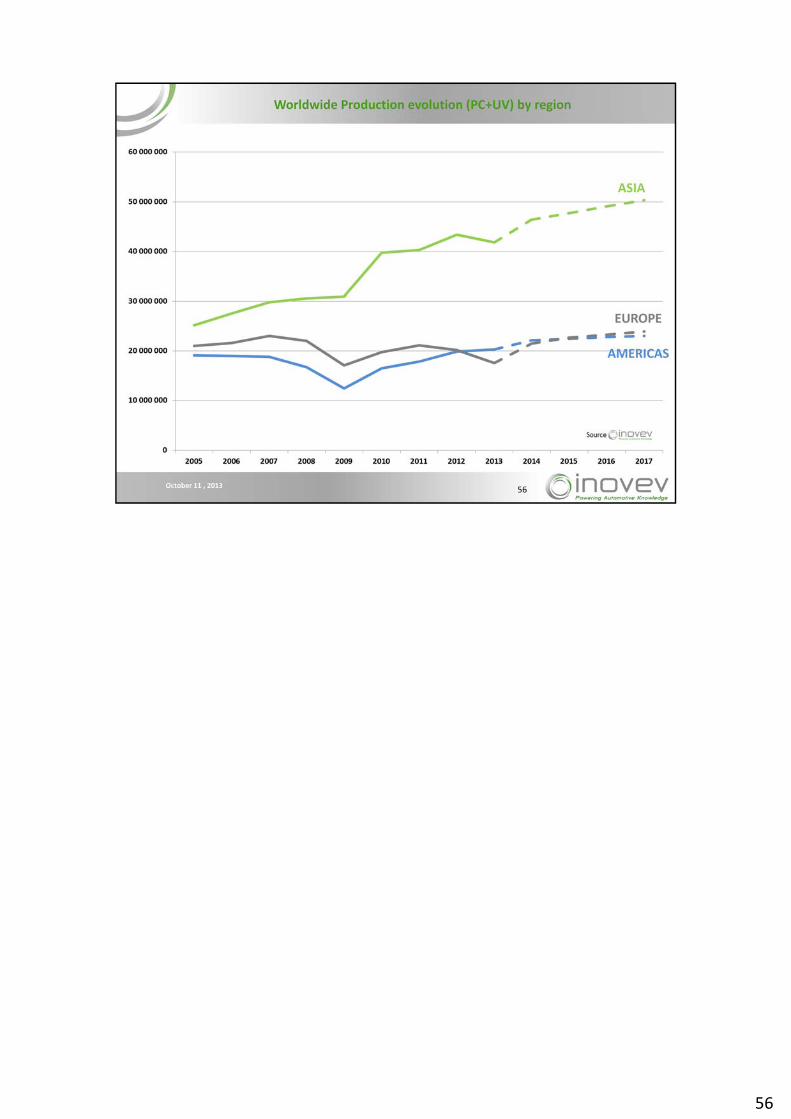

‐ China accounted for 15% of world production

‐ In 2012 Japanese production increased (+20% versus 2011; catch‐up effect following the tsunami).

‐ But in contrast production in Europe fell last year, despite robust exports.

‐ In 2013, a slower growth of the global production is expected (compared to 2012), due to a slowdown in markets (Europe, USA, China, Russia). Production should continue its migration to the East (Asia).

‐ The BRIC (Brazil, Russia, India, China) produced 36% of vehicles worldwide in 2012, and is expected to represent 38% in 2013 and probably 40% in 2014.

‐ It is to be noted that the American continent (North America + South America) production and the Europe at large (Europe 27 + Turkey + Russia) production were at about the same level in 2012, which had not happened since 2000 (Europe had remained ahead of America from 2000, to 2011).

‐ In 2013, the American continent will likely produce more than the great Europe (where markets are expected to decrease and plants to close).

35

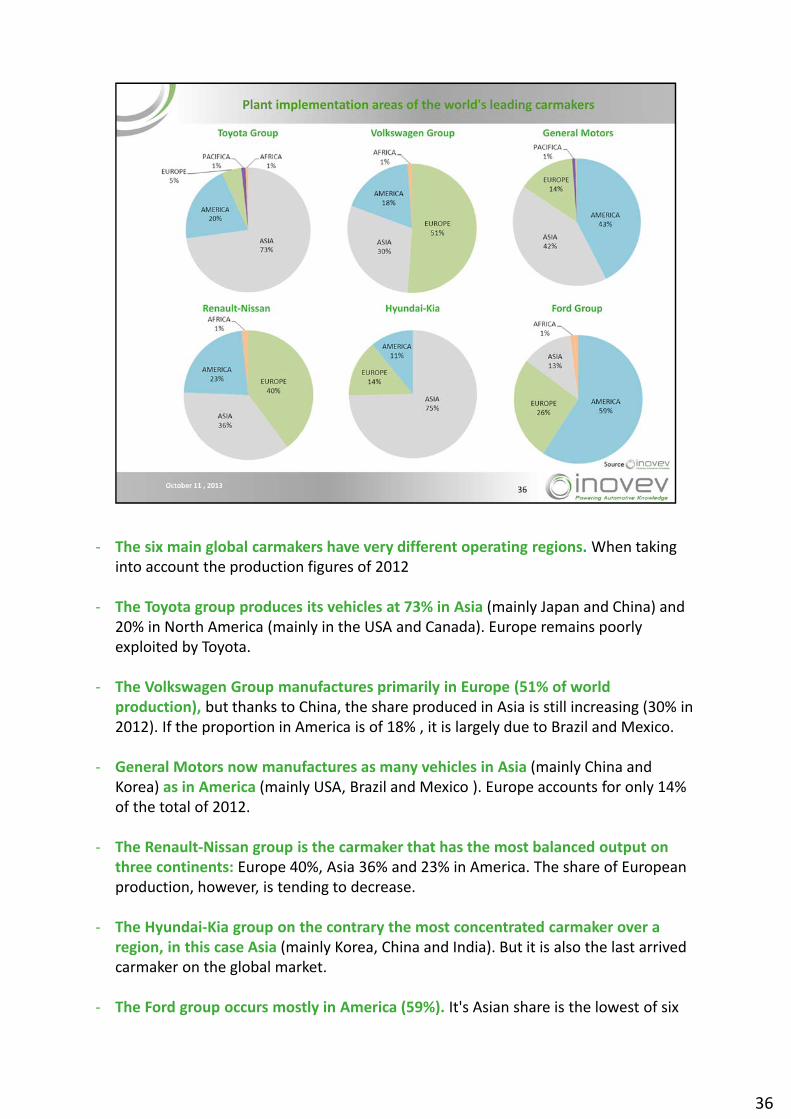

‐ The six main global carmakers have very different operating regions. When taking into account the production figures of 2012

‐ The Toyota group produces its vehicles at 73% in Asia (mainly Japan and China) and 20% in North America (mainly in the USA and Canada). Europe remains poorly exploited by Toyota.

‐ The Volkswagen Group manufactures primarily in Europe (51% of world production), but thanks to China, the share produced in Asia is still increasing (30% in 2012). If the proportion in America is of 18% , it is largely due to Brazil and Mexico.

‐ General Motors now manufactures as many vehicles in Asia (mainly China and Korea) as in America (mainly USA, Brazil and Mexico ). Europe accounts for only 14% of the total of 2012.

‐ The Renault‐Nissan group is the carmaker that has the most balanced output on three continents: Europe 40%, Asia 36% and 23% in America. The share of European production, however, is tending to decrease.

‐ The Hyundai‐Kia group on the contrary the most concentrated carmaker over a region, in this case Asia (mainly Korea, China and India). But it is also the last arrived carmaker on the global market.

‐ The Ford group occurs mostly in America (59%). It's Asian share is the lowest of six

36

leading global companies.

36

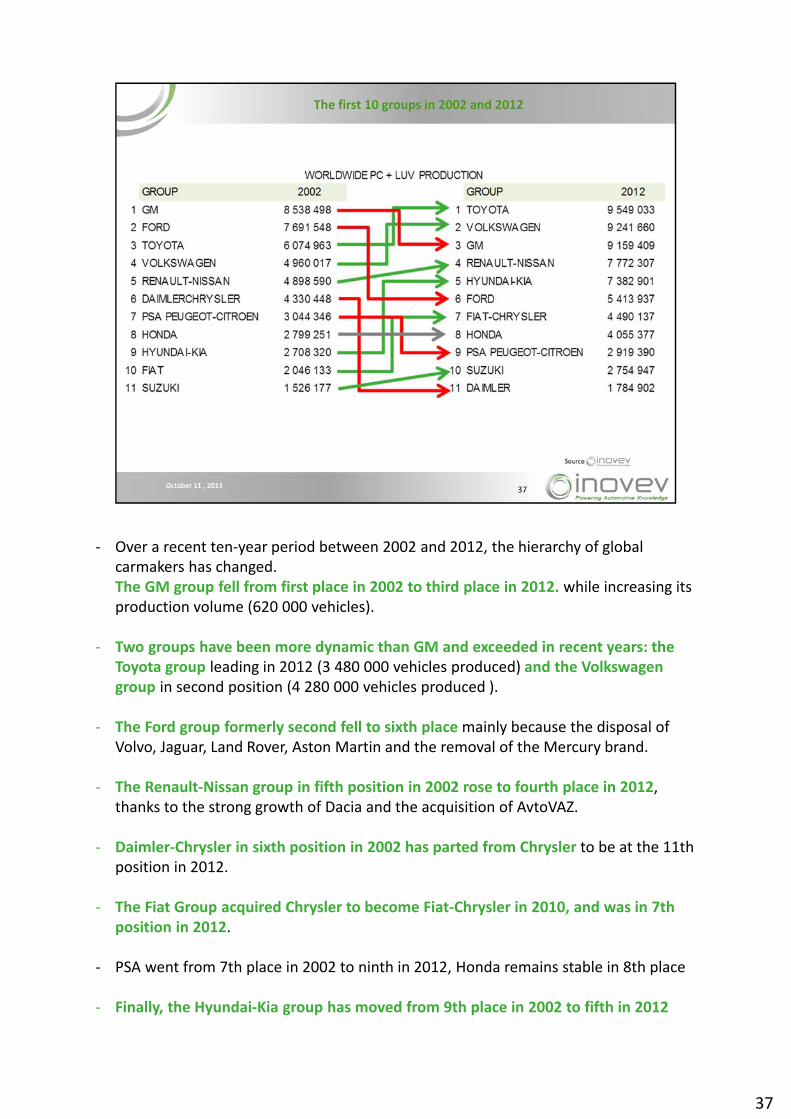

‐ Over a recent ten‐year period between 2002 and 2012, the hierarchy of global carmakers has changed.The GM group fell from first place in 2002 to third place in 2012. while increasing its production volume (620 000 vehicles).

‐ Two groups have been more dynamic than GM and exceeded in recent years: the Toyota group leading in 2012 (3 480 000 vehicles produced) and the Volkswagen group in second position (4 280 000 vehicles produced ).

‐ The Ford group formerly second fell to sixth place mainly because the disposal of Volvo, Jaguar, Land Rover, Aston Martin and the removal of the Mercury brand.

‐ The Renault‐Nissan group in fifth position in 2002 rose to fourth place in 2012, thanks to the strong growth of Dacia and the acquisition of AvtoVAZ.

‐ Daimler‐Chrysler in sixth position in 2002 has parted from Chrysler to be at the 11th position in 2012.

‐ The Fiat Group acquired Chrysler to become Fiat‐Chrysler in 2010, and was in 7th position in 2012.

‐ PSA went from 7th place in 2002 to ninth in 2012, Honda remains stable in 8th place

‐ Finally, the Hyundai‐Kia group has moved from 9th place in 2002 to fifth in 2012

37

thanks to the opening of factories in Europe, in the USA and in China (one million vehicles produced).

‐ Position are moving. Change is the only constant

37

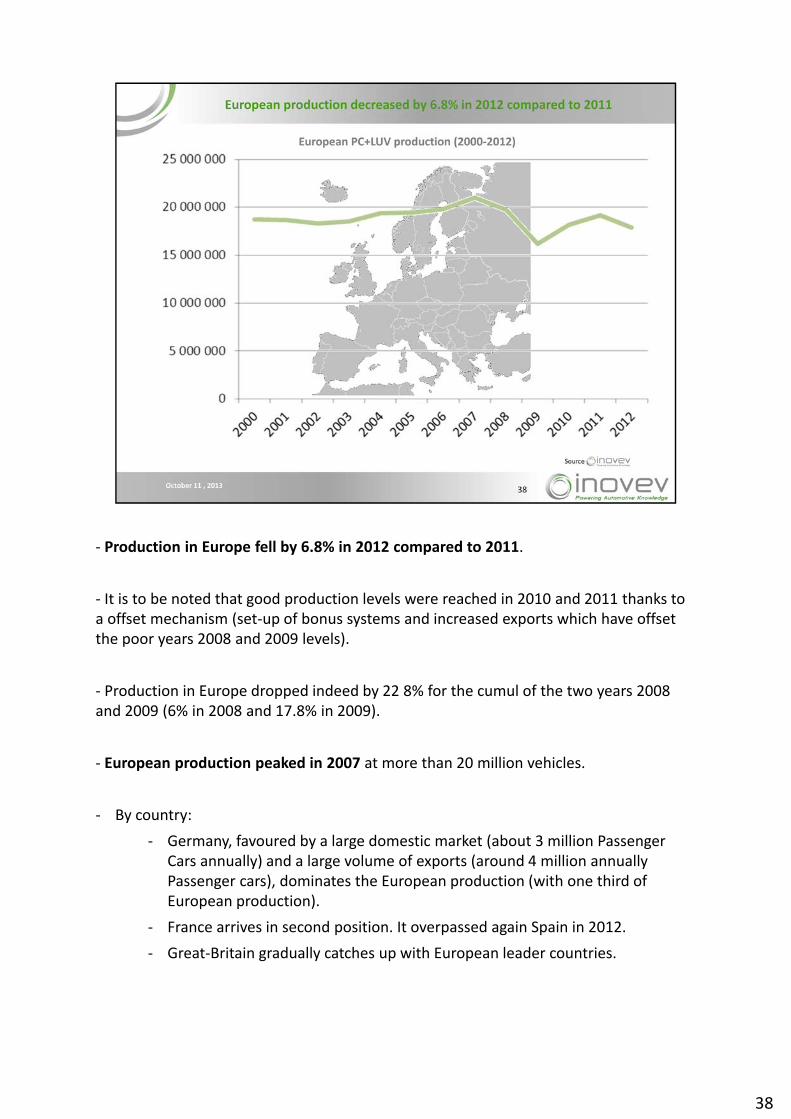

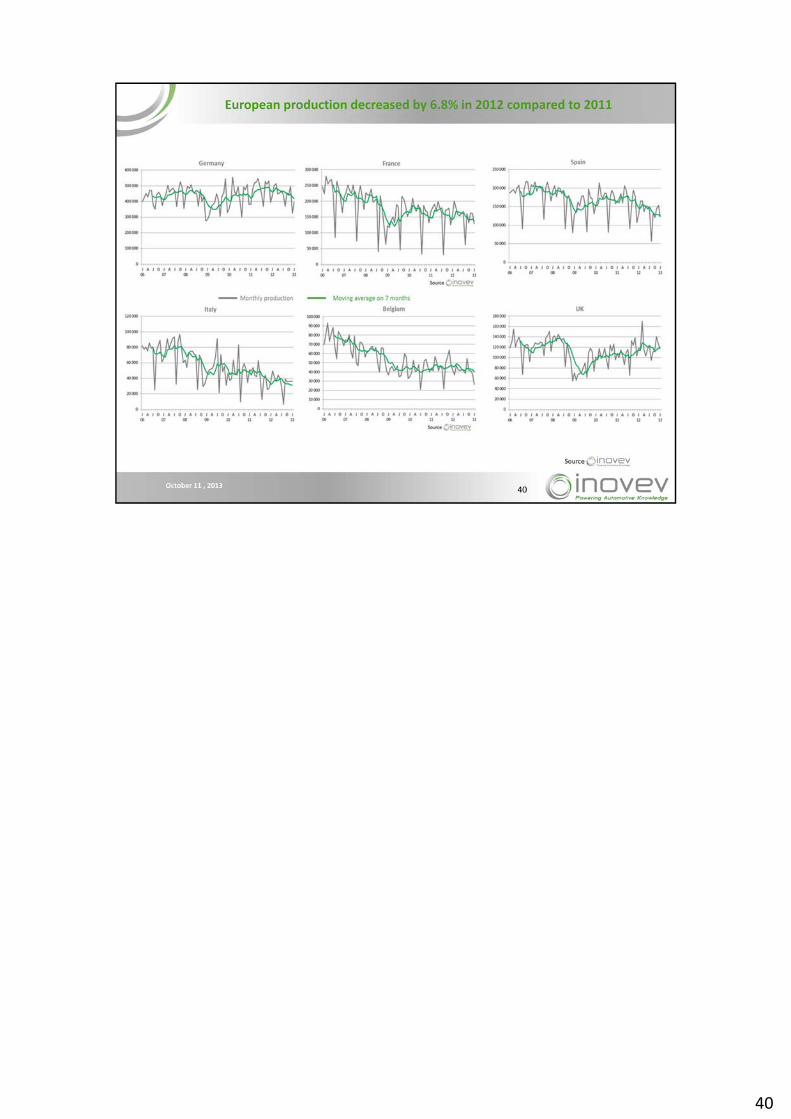

‐ Production in Europe fell by 6.8% in 2012 compared to 2011.

‐ It is to be noted that good production levels were reached in 2010 and 2011 thanks to a offset mechanism (set‐up of bonus systems and increased exports which have offset the poor years 2008 and 2009 levels).

‐ Production in Europe dropped indeed by 22 8% for the cumul of the two years 2008 and 2009 (6% in 2008 and 17.8% in 2009).

‐ European production peaked in 2007 at more than 20 million vehicles.

‐ By country:

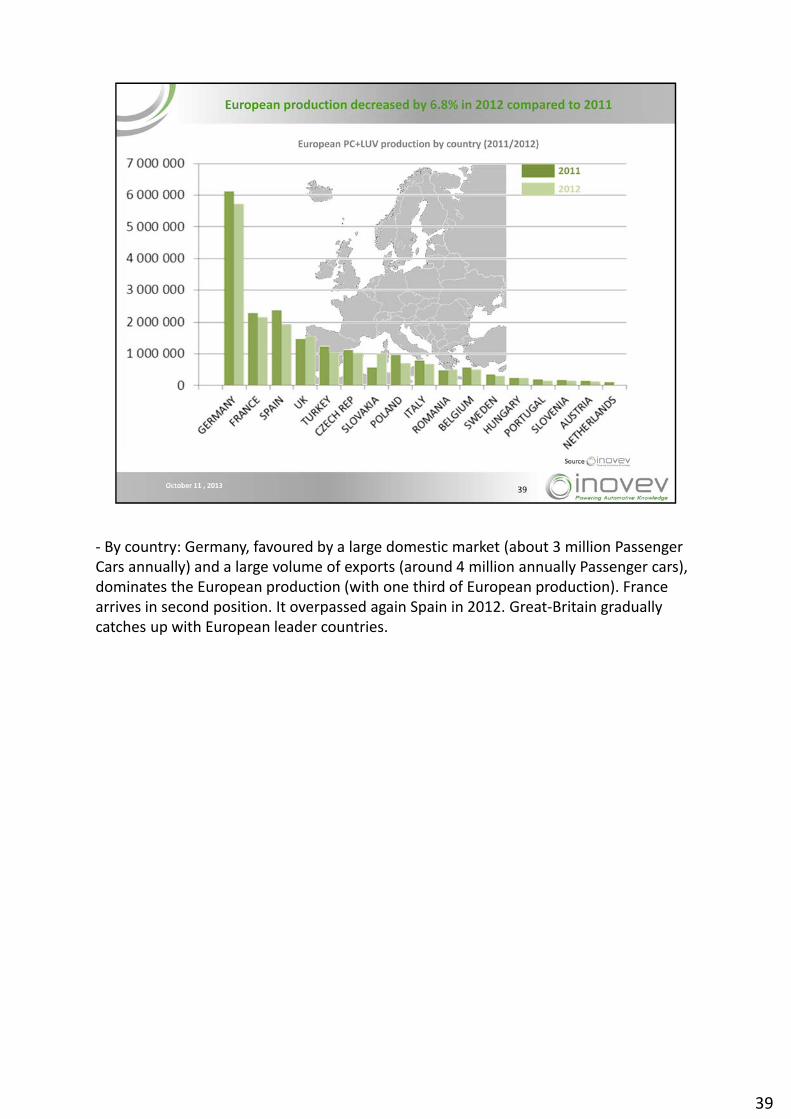

‐ Germany, favoured by a large domestic market (about 3 million Passenger Cars annually) and a large volume of exports (around 4 million annually Passenger cars), dominates the European production (with one third of European production).

‐ France arrives in second position. It overpassed again Spain in 2012.

‐ Great‐Britain gradually catches up with European leader countries.

38

‐ By country: Germany, favoured by a large domestic market (about 3 million Passenger Cars annually) and a large volume of exports (around 4 million annually Passenger cars), dominates the European production (with one third of European production). France arrives in second position. It overpassed again Spain in 2012. Great‐Britain gradually catches up with European leader countries.

39

40

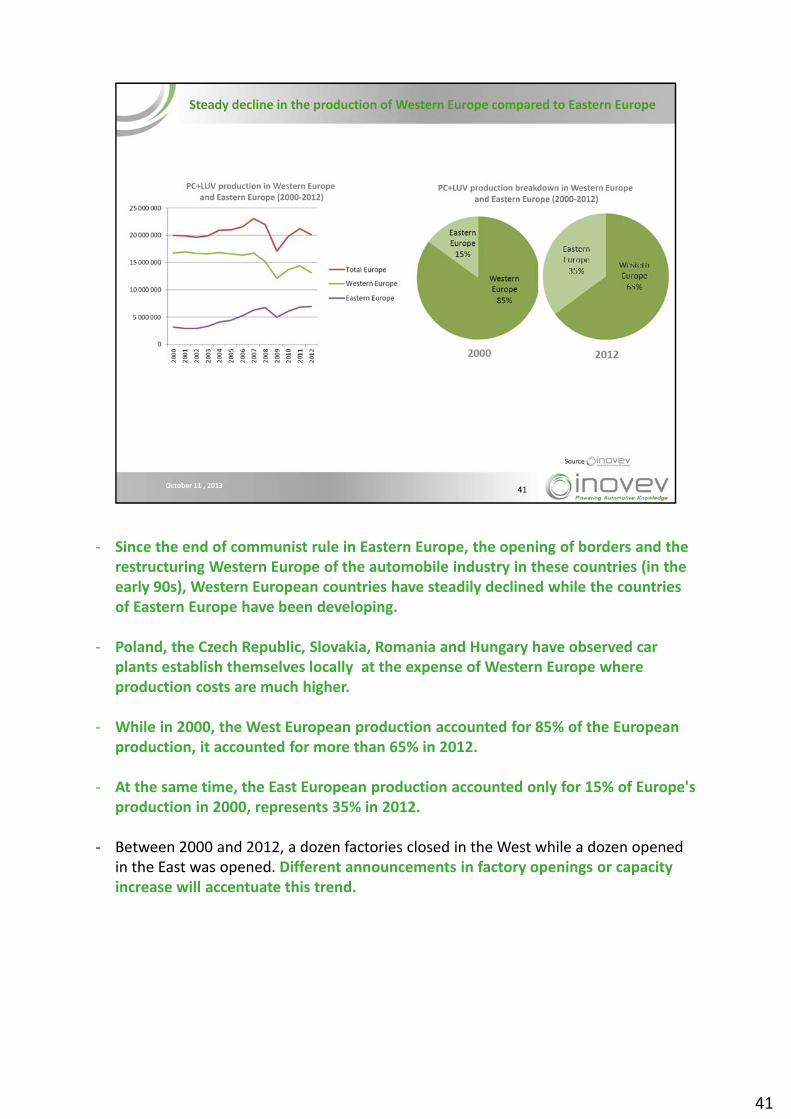

‐ Since the end of communist rule in Eastern Europe, the opening of borders and the restructuring Western Europe of the automobile industry in these countries (in the early 90s), Western European countries have steadily declined while the countries of Eastern Europe have been developing.

‐ Poland, the Czech Republic, Slovakia, Romania and Hungary have observed car plants establish themselves locally at the expense of Western Europe where production costs are much higher.

‐ While in 2000, the West European production accounted for 85% of the European production, it accounted for more than 65% in 2012.

‐ At the same time, the East European production accounted only for 15% of Europe's production in 2000, represents 35% in 2012.

‐ Between 2000 and 2012, a dozen factories closed in the West while a dozen opened in the East was opened. Different announcements in factory openings or capacity increase will accentuate this trend.

41

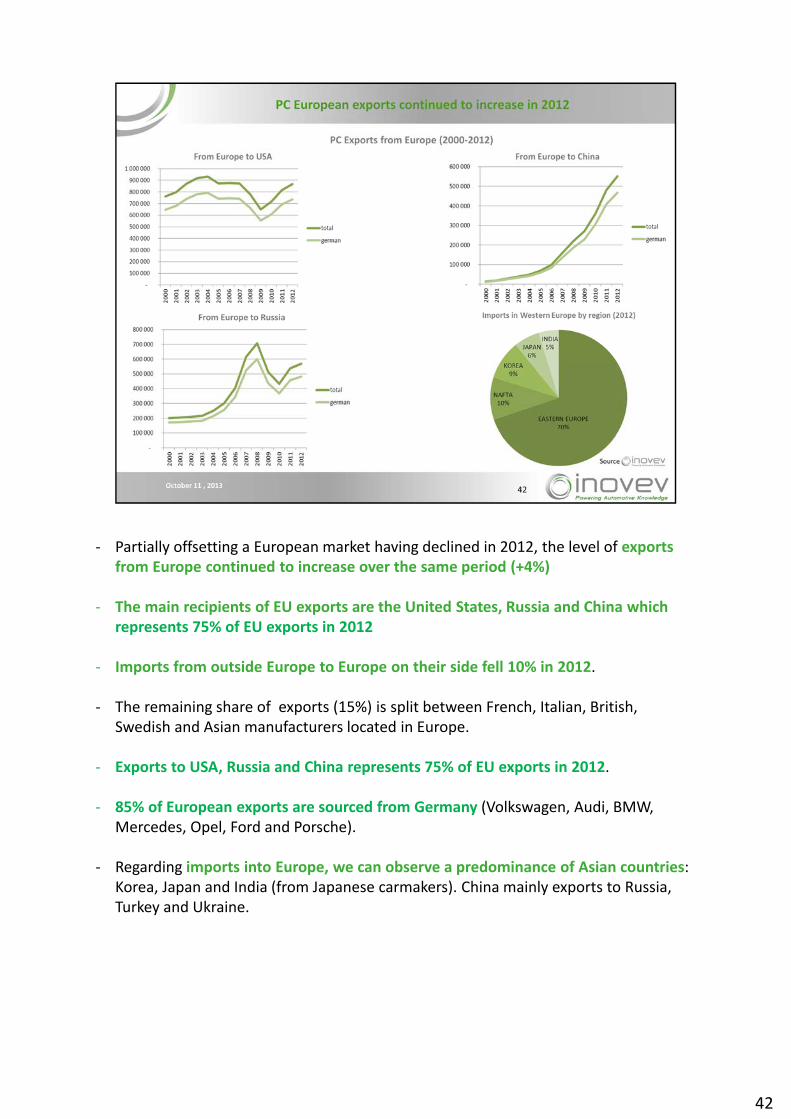

‐ Partially offsetting a European market having declined in 2012, the level of exports from Europe continued to increase over the same period (+4%)

‐ The main recipients of EU exports are the United States, Russia and China which represents 75% of EU exports in 2012

‐ Imports from outside Europe to Europe on their side fell 10% in 2012.

‐ The remaining share of exports (15%) is split between French, Italian, British, Swedish and Asian manufacturers located in Europe.

‐ Exports to USA, Russia and China represents 75% of EU exports in 2012.

‐ 85% of European exports are sourced from Germany (Volkswagen, Audi, BMW, Mercedes, Opel, Ford and Porsche).

‐ Regarding imports into Europe, we can observe a predominance of Asian countries: Korea, Japan and India (from Japanese carmakers). China mainly exports to Russia, Turkey and Ukraine.

42

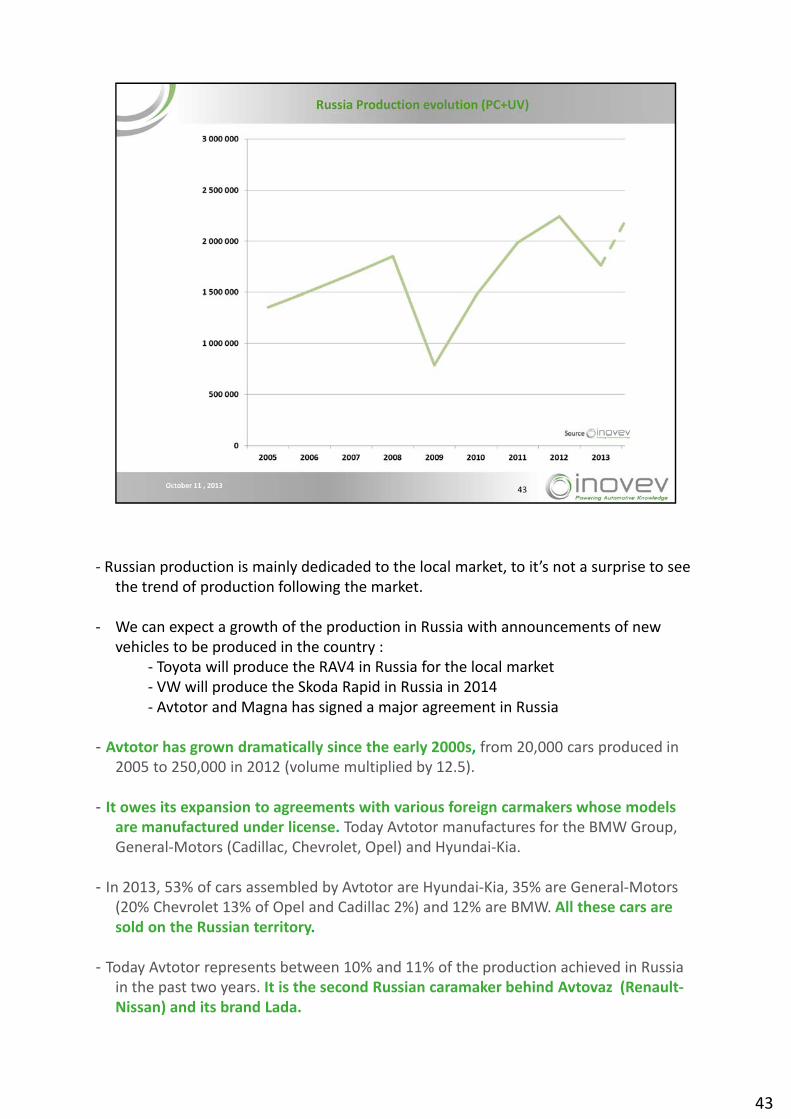

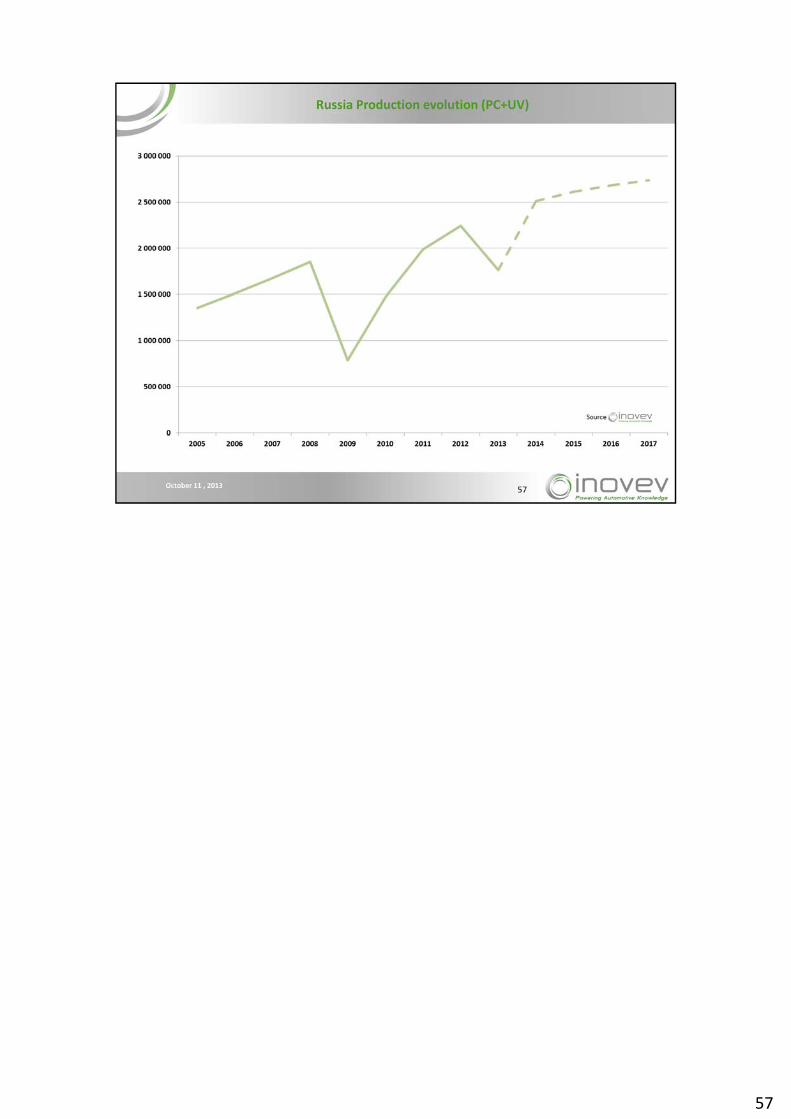

‐ Russian production is mainly dedicaded to the local market, to it’s not a surprise to see the trend of production following the market.

‐ We can expect a growth of the production in Russia with announcements of new vehicles to be produced in the country :

‐ Toyota will produce the RAV4 in Russia for the local market‐ VW will produce the Skoda Rapid in Russia in 2014‐ Avtotor and Magna has signed a major agreement in Russia

- Avtotor has grown dramatically since the early 2000s, from 20,000 cars produced in 2005 to 250,000 in 2012 (volume multiplied by 12.5).

- It owes its expansion to agreements with various foreign carmakers whose models are manufactured under license. Today Avtotor manufactures for the BMW Group, General‐Motors (Cadillac, Chevrolet, Opel) and Hyundai‐Kia.

- In 2013, 53% of cars assembled by Avtotor are Hyundai‐Kia, 35% are General‐Motors (20% Chevrolet 13% of Opel and Cadillac 2%) and 12% are BMW. All these cars are sold on the Russian territory.

- Today Avtotor represents between 10% and 11% of the production achieved in Russia in the past two years. It is the second Russian caramaker behind Avtovaz (Renault‐Nissan) and its brand Lada.

43

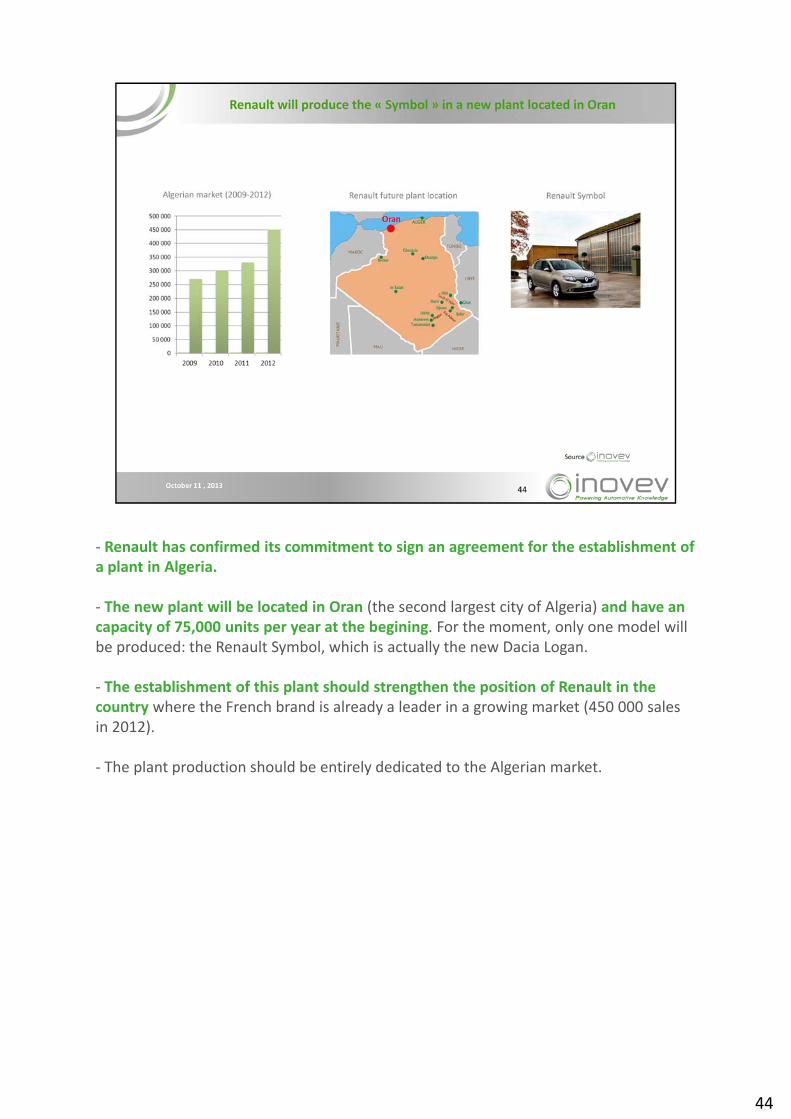

‐ Renault has confirmed its commitment to sign an agreement for the establishment of a plant in Algeria.

‐ The new plant will be located in Oran (the second largest city of Algeria) and have an capacity of 75,000 units per year at the begining. For the moment, only one model will be produced: the Renault Symbol, which is actually the new Dacia Logan.

‐ The establishment of this plant should strengthen the position of Renault in the country where the French brand is already a leader in a growing market (450 000 sales in 2012).

‐ The plant production should be entirely dedicated to the Algerian market.

44

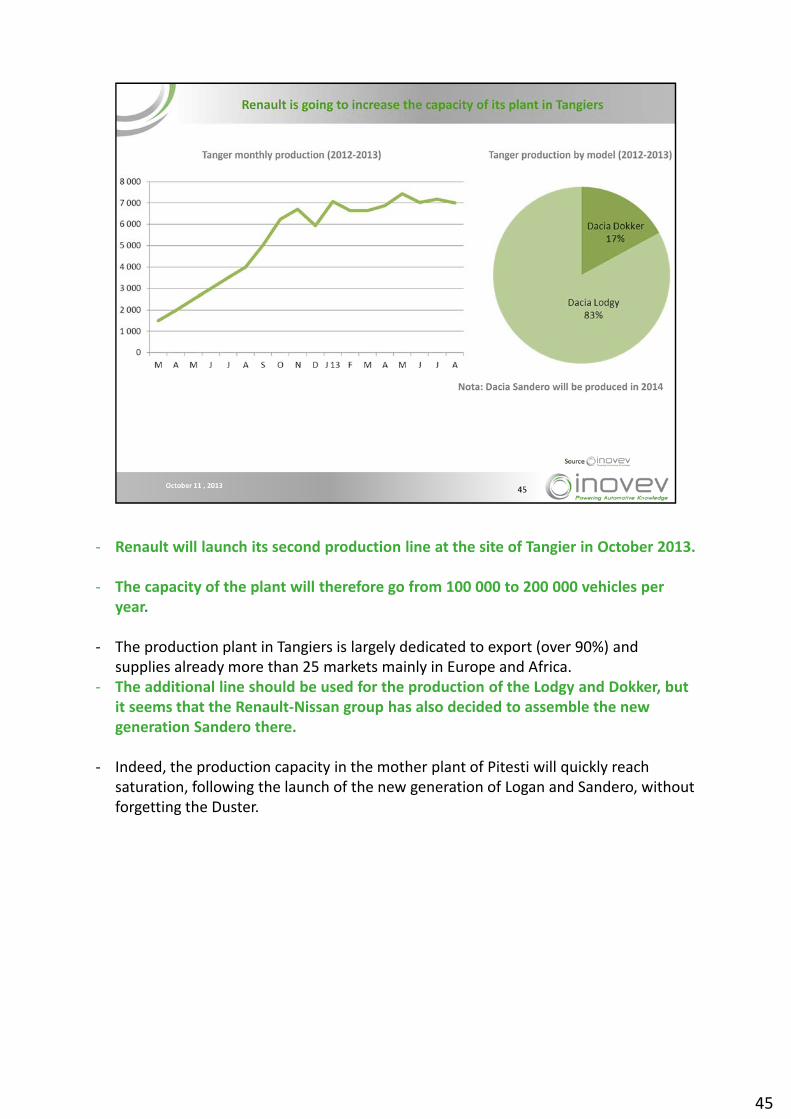

‐ Renault will launch its second production line at the site of Tangier in October 2013.

‐ The capacity of the plant will therefore go from 100 000 to 200 000 vehicles per year.

‐ The production plant in Tangiers is largely dedicated to export (over 90%) and supplies already more than 25 markets mainly in Europe and Africa.

‐ The additional line should be used for the production of the Lodgy and Dokker, but it seems that the Renault‐Nissan group has also decided to assemble the new generation Sandero there.

‐ Indeed, the production capacity in the mother plant of Pitesti will quickly reach saturation, following the launch of the new generation of Logan and Sandero, without forgetting the Duster.

45

46

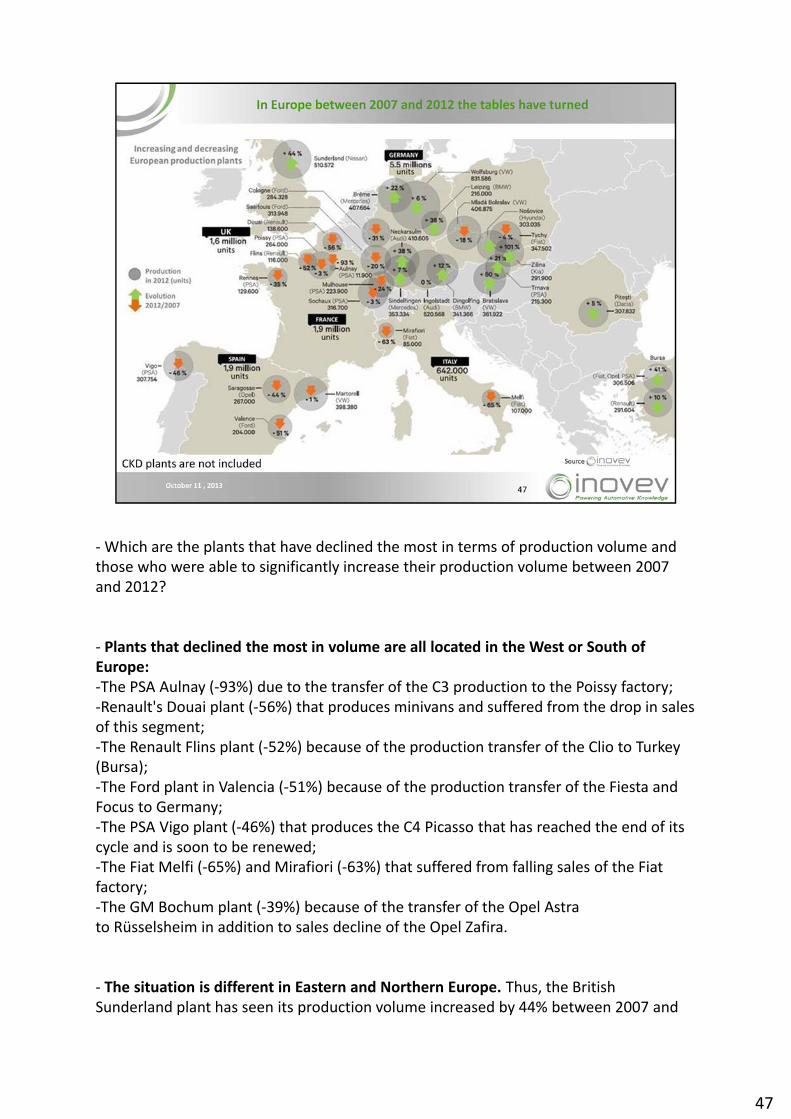

‐Which are the plants that have declined the most in terms of production volume and those who were able to significantly increase their production volume between 2007 and 2012?

‐ Plants that declined the most in volume are all located in the West or South of Europe:‐The PSA Aulnay (‐93%) due to the transfer of the C3 production to the Poissy factory;‐Renault's Douai plant (‐56%) that produces minivans and suffered from the drop in sales of this segment;‐The Renault Flins plant (‐52%) because of the production transfer of the Clio to Turkey (Bursa);‐The Ford plant in Valencia (‐51%) because of the production transfer of the Fiesta and Focus to Germany;‐The PSA Vigo plant (‐46%) that produces the C4 Picasso that has reached the end of its cycle and is soon to be renewed;‐The Fiat Melfi (‐65%) and Mirafiori (‐63%) that suffered from falling sales of the Fiat factory;‐The GM Bochum plant (‐39%) because of the transfer of the Opel Astra to Rüsselsheim in addition to sales decline of the Opel Zafira.

‐ The situation is different in Eastern and Northern Europe. Thus, the British Sunderland plant has seen its production volume increased by 44% between 2007 and

47

2012, thanks to the success of the Qashqai and Juke SUVs. Further east, Bratislava plant (50%), Zilina (101%) of Nosovice (which did not exist in 2007), Bursa (41%), Trnava(21% )and Leipzig (38%) plants took advantage of the arrival of new models on on their assembly lines.

47

‐ When analyzing the number of European plants (excluding Russia) that have opened since 2000, and those that have closed since that date, we observe that as many have opened as closed.

‐ On the other hand , while 11 factories opened in Eastern Europe, 12 were closed in Western Europe. Part of the production in Europe has thus gradually moved from west to east.

‐ Another enlightening element while generalist brands closed eight factories and opened nine since 2000, premium brands closed 4 and opened 3. But among generalists mainly Toyota, Hyundai and Kia have opened new plants, while mainly Ford, Vauxhall (Opel) and Rover have closed plants.

‐ Same phenomenon for premium: those who have opened new plants are BMW, Porsche and Mercedes, while those who have closed plants are Lancia, Jaguar and Saab. Production has been moved from some less dynamic or weak brands to other more vibrant and stronger brands.

‐ This means that competition in Europe has led to the emergence of certain brands and weakened others. In 2014, three other factories will be closed in Europe, and once again generalist brands: Vauxhall/Opel (Bochum), Ford (Genk) and Citroën (Aulnay).

48

49

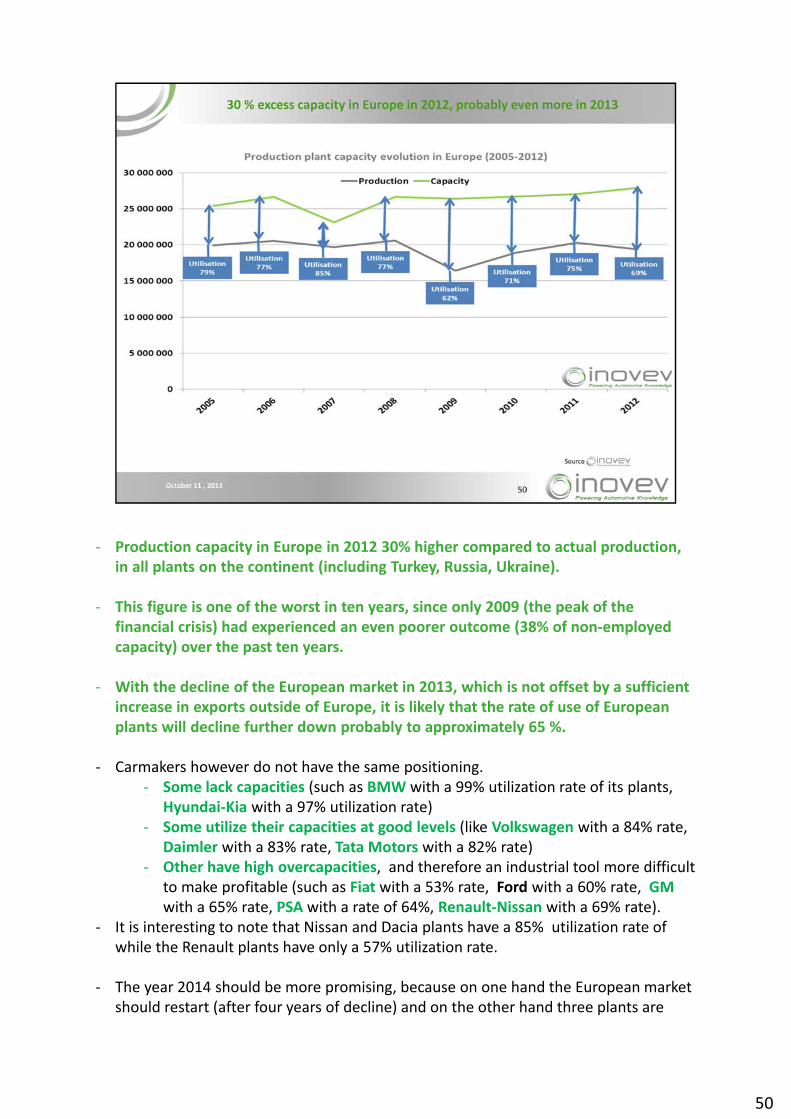

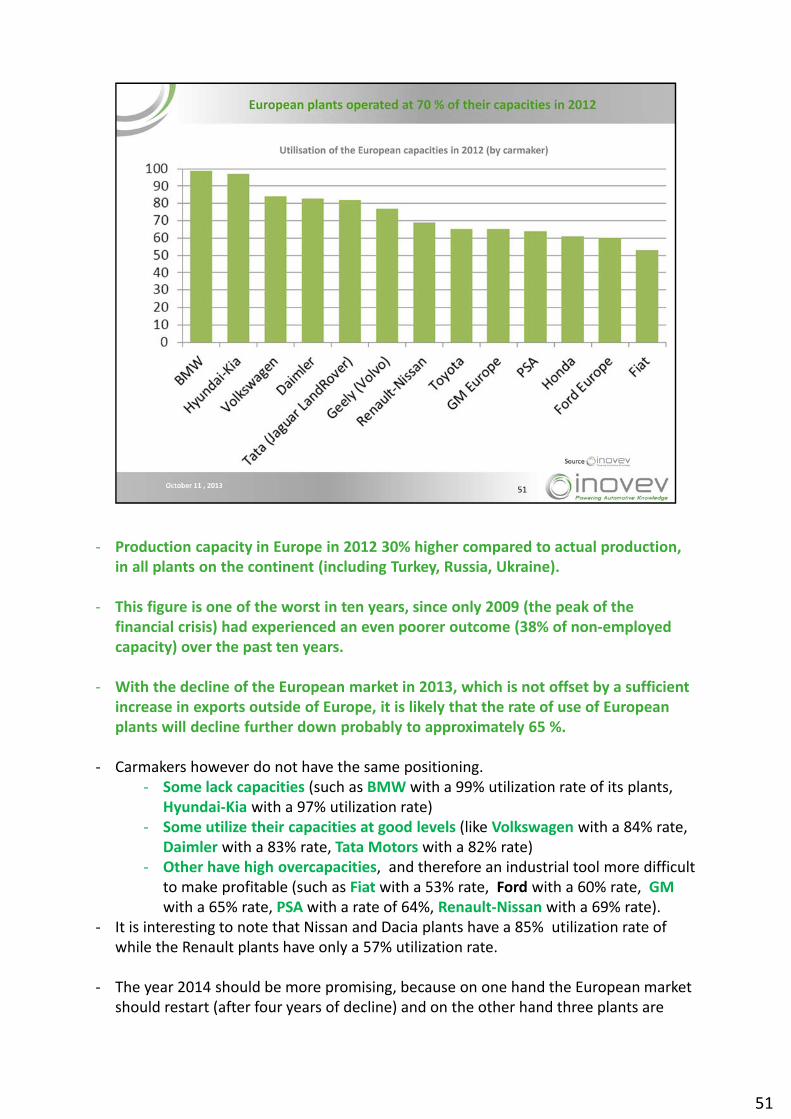

‐ Production capacity in Europe in 2012 30% higher compared to actual production, in all plants on the continent (including Turkey, Russia, Ukraine).

‐ This figure is one of the worst in ten years, since only 2009 (the peak of the financial crisis) had experienced an even poorer outcome (38% of non‐employed capacity) over the past ten years.

‐ With the decline of the European market in 2013, which is not offset by a sufficient increase in exports outside of Europe, it is likely that the rate of use of European plants will decline further down probably to approximately 65 %.

‐ Carmakers however do not have the same positioning. ‐ Some lack capacities (such as BMW with a 99% utilization rate of its plants,

Hyundai‐Kia with a 97% utilization rate)‐ Some utilize their capacities at good levels (like Volkswagen with a 84% rate,

Daimler with a 83% rate, Tata Motors with a 82% rate)‐ Other have high overcapacities, and therefore an industrial tool more difficult

to make profitable (such as Fiat with a 53% rate, Ford with a 60% rate, GMwith a 65% rate, PSA with a rate of 64%, Renault‐Nissan with a 69% rate).

‐ It is interesting to note that Nissan and Dacia plants have a 85% utilization rate of while the Renault plants have only a 57% utilization rate.

‐ The year 2014 should be more promising, because on one hand the European market should restart (after four years of decline) and on the other hand three plants are

50

going to close in Europe (Bochum, Aulnay, Genk), which will naturally generate a reduction in installed capacity.

50

‐ Production capacity in Europe in 2012 30% higher compared to actual production, in all plants on the continent (including Turkey, Russia, Ukraine).

‐ This figure is one of the worst in ten years, since only 2009 (the peak of the financial crisis) had experienced an even poorer outcome (38% of non‐employed capacity) over the past ten years.

‐ With the decline of the European market in 2013, which is not offset by a sufficient increase in exports outside of Europe, it is likely that the rate of use of European plants will decline further down probably to approximately 65 %.

‐ Carmakers however do not have the same positioning. ‐ Some lack capacities (such as BMW with a 99% utilization rate of its plants,

Hyundai‐Kia with a 97% utilization rate)‐ Some utilize their capacities at good levels (like Volkswagen with a 84% rate,

Daimler with a 83% rate, Tata Motors with a 82% rate)‐ Other have high overcapacities, and therefore an industrial tool more difficult

to make profitable (such as Fiat with a 53% rate, Ford with a 60% rate, GMwith a 65% rate, PSA with a rate of 64%, Renault‐Nissan with a 69% rate).

‐ It is interesting to note that Nissan and Dacia plants have a 85% utilization rate of while the Renault plants have only a 57% utilization rate.

‐ The year 2014 should be more promising, because on one hand the European market should restart (after four years of decline) and on the other hand three plants are

51

going to close in Europe (Bochum, Aulnay, Genk), which will naturally generate a reduction in installed capacity.

51

‐ Fiat is going to build a new factory in China with GAC in 2014‐ BAIC Group is going to build a second plant in Zhuzhou in 2015‐ Jiangling and Ford have inaugurated a new plant in Nanchang‐ Guangzhou Honda started building its third plant in China‐ Dongfeng Kia will open a third plant in China‐ SAIC‐GM‐Wuling will build a third plant in Chongqing and be operational in 2015‐ VW plans to build its 8th plant in China‐ Renault plans to sign an agreement with Dongfeng on the 25th of July in order to

set up its first factory in China. The plant that both partners will build in Wuhan

52

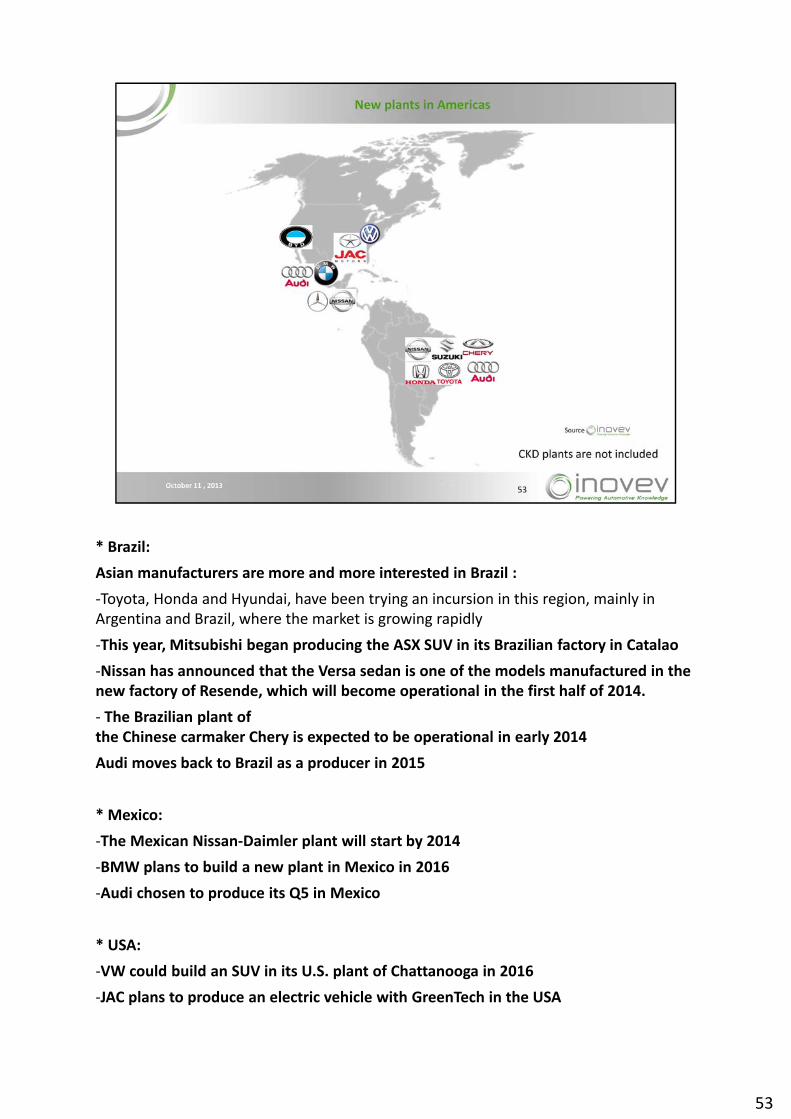

* Brazil:

Asian manufacturers are more and more interested in Brazil :

‐Toyota, Honda and Hyundai, have been trying an incursion in this region, mainly in Argentina and Brazil, where the market is growing rapidly

‐This year, Mitsubishi began producing the ASX SUV in its Brazilian factory in Catalao

‐Nissan has announced that the Versa sedan is one of the models manufactured in the new factory of Resende, which will become operational in the first half of 2014.

‐ The Brazilian plant of the Chinese carmaker Chery is expected to be operational in early 2014

Audi moves back to Brazil as a producer in 2015

* Mexico:

‐The Mexican Nissan‐Daimler plant will start by 2014

‐BMW plans to build a new plant in Mexico in 2016

‐Audi chosen to produce its Q5 in Mexico

* USA:

‐VW could build an SUV in its U.S. plant of Chattanooga in 2016

‐JAC plans to produce an electric vehicle with GreenTech in the USA

53

‐Lexus will produce vehicles in the U.S. at the end of 2014

‐BYD set up a production plant in the US in 2013 to produce electric buses

53

54

55

56

57

58

59

60

61

62

63