the berman value folio - forbes · 22/05/2012 · wmt 72.53 62.20 jnj 72.45 63.72 ... return to its...

TRANSCRIPT

Dull (but Effective) Stocks for Higher Interest Rates: Payroll Processors

An explosion of information, overwhelming at every turn...technology

reinventing itself with maddening speed, the relentless spread of self-

publishing and information exchange — and the disruptive effects of new

media...Palo Alto in 2012?

Would you believe: 16th century Switzerland. As

Vaughan Bell wrote recently in Slate, Swiss

botanist Conrad Gessner decried the eruption of

data in the wake of the printing press, calling it

“confusing and harmful” to the mind. — and

Gessner died in 1565. Where did I read this? On

my Kindle. Nothing ever changes.

Today, people worry about the Nook and iPad

replacing the old paperback. Back then, it was the

scribes who were rendered useless by a strange new device with moveable type. The Luddites,

those who revolted against automation and industrialization in the 19th century, were right to

be fearful. Breaking the machines that stole their livelihood appeared to be their only solution.

But history shows that resisting change is always a losing proposition. More new jobs are

eventually created than old ones are destroyed. Where there were once scribes, along come

typesetters. For every obsolete handloom weaver, two new mechanized loom manufacturers

are needed — as the new technology spurs growth. Best to learn and adapt, not fight the losing

battle against change. That’s easier said than done, especially for manual laborers set in their

ways — and for companies resting on their laurels. The disruptive effects of technology are so

intense that it’s hard to ever bet on any particular tech player. AOL was broken by Google, RIM

by Apple, HP by Adobe, and Kodak by everyone. Today there’s Facebook. The company that

will break them is still an unknown, working out of a garage, or a lab at Stanford. Or Mumbai.

THE BERMAN VALUE FOLIO A Trefis Interactive Portfolio Report

Volume 1 Number 6 May 2012

James Berman

James Berman, the president and founder of JBGlobal.com LLC, a registered investment advi-

sory firm (SEC registered), specializes in asset management for high-net-worth individuals and

trusts. Mr. Berman is a faculty member in the Finance Department of NYU SCPS. He has ap-

peared on CNBC and the Fox Business Channel and has been quoted and published in a vari-

ety of publications, including Barron's, Fortune, Bloomberg, The Huffington Post and CNN Mon-

ey. Mr. Berman holds a B.A., Magna Cum Laude, Phi Beta Kappa, in English & American Liter-

ature from Harvard and a J.D. from Harvard Law School.

CONTENTS Stocks for Higher Interest Rates: 1

The Wonders of Float 3

The Opportunity: ADP 4 Valuation Stress Test: ADP 5 Company Highlights 6 J.P. Morgan Chase (JPM) 6 Wal-Mart (WMT) 7 Alcoa (AA) 8 Facebook (FB) 9

Look for our

Facebook Special

Report — coming to

all subscribers soon!

2

Yet, some tech companies are able to resist

disruptive changes by a peculiar blend of barrier to

entry, consistent cash flows and what I call the

“great moat of boredom”— a business so dull, so

unglamorous, that it flies beneath the radar,

hidden from entrepreneurs hell-bent on

disruption. Take payroll processing, only rivaled

by waste management in its lack of sex appeal.

Many wouldn’t consider a company that processes

paychecks as “tech” but it is. A payroll processor

effectively sell licenses to their payroll software,

both PC and cloud-based. In fact, it’s the original

software-as-a-service (SAAS), a sector that fetches

the highest multiples and the greatest attention,

highlighted by stocks like Salesforce.com (CRM).

Payroll stocks trade at more modest multiples,

with many of the same advantages. With a drab

image and an underappreciated business model,

payroll stocks sell for the right price. In the Folio, I

own both Paychex (PAYX) and ADP (ADP), the

two large payroll players that form a virtual

duopoly. These two firms enjoy all the favorable

characteristics of software companies: high net

margins and superior returns on invested capital.

They enjoy recurring fee revenue and low capital

requirements. To further appreciate how good the

payroll business is, you also have to understand

the “stickiness” of the model. To change payroll

processors is to invite chaos: missing paychecks,

bungled withholding, and angry employees.

Businesses just don’t do it if they can avoid it. This

stickiness allows high returns, as prices can be

raised marginally faster than the rate of inflation.

But the real glory of the payroll machine comes in

the form of “float,” cash via payroll funds held

temporarily for clients — money that can be

invested for a short time, pending remittance to

the tax authorities. Unlike a bank’s deposits, (and

due to the short holding period) no interest need

be paid on the float. Float is the closest thing to

“free money.” And when interest rates rise, so do

the earnings on the float.

The Trefis Dow

Ticker

Trefis

Market Price Price

IBM 223.00 200.04

CVX 109.00 101.13

CAT 108.00 89.32

UTX 102.00 74.04

MCD 98.20 91.41

MMM 97.11 85.36

XOM 93.22 82.17

BA 90.91 71.25

WMT 72.53 62.20

JNJ 72.45 63.72

PG 72.88 64.13

KO 75.70 75.49

TRV 63.13 63.22

DD 58.98 49.69

DIS 52.15 44.89

AXP 51.25 56.84

HD 49.36 48.02

VZ 41.90 40.80

KFT 39.92 38.45

MRK 41.15 38.31

JPM 47.94 34.52

HPQ 38.80 21.96

MSFT 39.20 30.12

T 34.00 33.30

INTC 30.62 26.50

PFE 25.11 22.70

CSCO 23.40 16.63

GE 19.97 18.96

AA 12.04 8.60

BAC 9.86 7.70

Raw Sum 1893.78 1661.47

Dow Divisor 0.132129493 0.132129493

DOW

Trefis Market

Price Price

14,333 12,575

Undervaluation 14%

The Trefis Price for the Dow

is now 14,333, 14% above

the market price.

3

The Wonders of Float The wonders of float are known to any financial services company. The ability to use other people’s money for a limited period of time (pending payment of claims) is the bread and

butter of the insurance business. The ability to gain incremental use of cash across all manner of transaction is the lifeblood of bankers.

But insurance companies must manage the risk of claims, with a bad year destroying all profit on the float, and bankers must pay interest on deposits eventually.

Payroll processors have very little cost to their float. They don’t need to pay out claims in excess of the dollars held and they don’t need to pay interest on deposits. Their burden is a different one: the short-

dated nature of the liabilities. Payroll funds are only held for the blink of an eye, so the funds cannot be invested aggressively. They need to be held in short-term bonds and commercial paper. The fixed income investments can be laddered to extend average duration. This increases yield, but only to the very low single digits. A good payroll processor cannot take risks

on its funds held for clients.

The pitiful yield on short rates, (courtesy of an ultra-easy Fed) has punished the net income of the payroll companies, but when it rises, along comes a windfall. PAYX and ADP hold $22 billion and $5.5 billion in client funds respectively. An extra hundred basis points on ADP’s float means $220 million to the bottom line — and this drops straight to that proverbial bottom. The operating leverage is extreme.

If the Fed Funds Rate were to return to its historical norm of 5%, ADP’s interest on float would

increase by nearly $800 million — atop a free cash flow base of $1.6 billion. That’s real money. A rise in rates like that would not happen overnight, but if you recall 1994, you remember the velocity can be surprising.

If the double-digit rates of the 1980’s were to return, ADP’s free cash flow could double. Regardless of your interest rate forecast, there’s not much doubt that the interest rate on float is pretty much as low as it can go. That implies only one direction going forward.

4

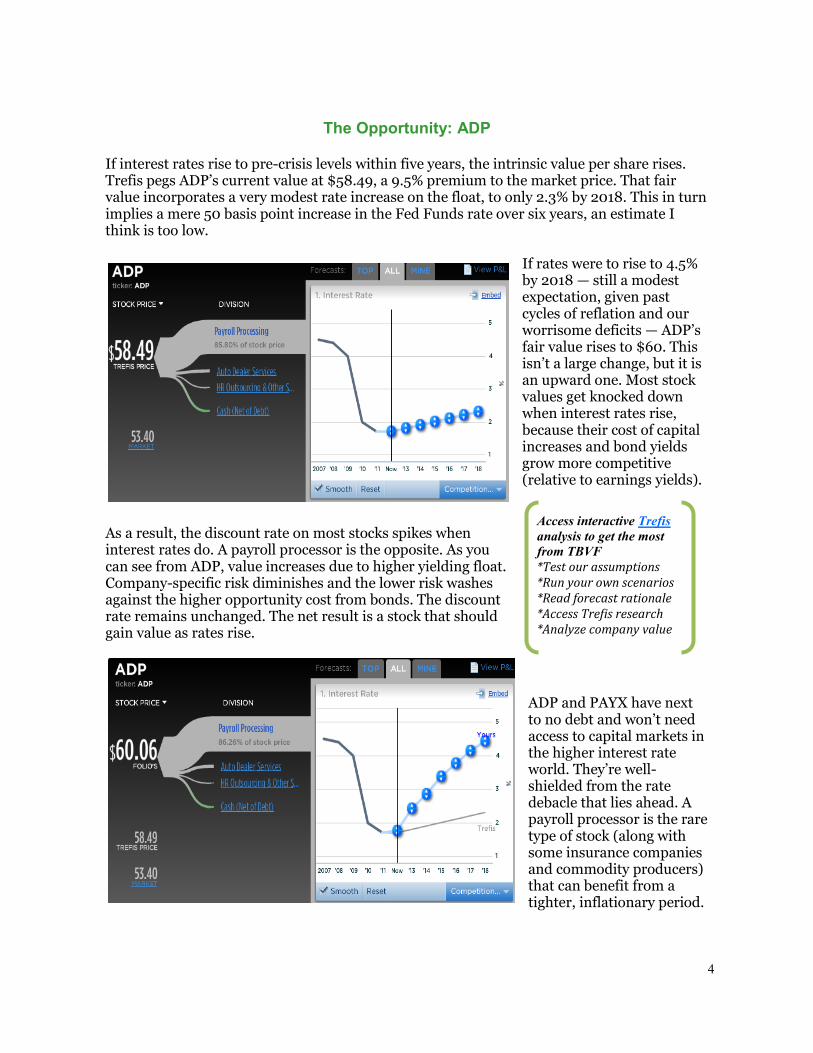

The Opportunity: ADP

If interest rates rise to pre-crisis levels within five years, the intrinsic value per share rises. Trefis pegs ADP’s current value at $58.49, a 9.5% premium to the market price. That fair value incorporates a very modest rate increase on the float, to only 2.3% by 2018. This in turn implies a mere 50 basis point increase in the Fed Funds rate over six years, an estimate I think is too low.

If rates were to rise to 4.5% by 2018 — still a modest expectation, given past cycles of reflation and our worrisome deficits — ADP’s fair value rises to $60. This isn’t a large change, but it is an upward one. Most stock values get knocked down when interest rates rise, because their cost of capital increases and bond yields grow more competitive (relative to earnings yields).

As a result, the discount rate on most stocks spikes when interest rates do. A payroll processor is the opposite. As you can see from ADP, value increases due to higher yielding float. Company-specific risk diminishes and the lower risk washes against the higher opportunity cost from bonds. The discount rate remains unchanged. The net result is a stock that should gain value as rates rise.

ADP and PAYX have next to no debt and won’t need access to capital markets in the higher interest rate world. They’re well-shielded from the rate debacle that lies ahead. A payroll processor is the rare type of stock (along with some insurance companies and commodity producers) that can benefit from a tighter, inflationary period.

Access interactive Trefis

analysis to get the most

from TBVF

*Test our assumptions *Run your own scenarios *Read forecast rationale *Access Trefis research *Analyze company value

5

Valuation Stress Test: ADP

ADP is currently suffering from the double whammy of low interest rates and high unemployment. The higher the unemployment rate, the fewer checks processed and the lower the size of the float. If the economy drifts back into recession, sending unemployment levels higher and capping rates, ADP will suffer accordingly. To assume another recessionary period, we can drop the number of ADP’s payroll accounts across the board. We can also keep interest rates low for the next three years, to model in an extended period of monetary easing. This brings the fair value of ADP down to $56.37, still a premium to market.

To model an even deeper recession, one that involves a possible Euro collapse and deflationary spiral, we can leave the interest rates flat and crush the number of checks processed, along with the size of the float.

This harsh scenario still yields a fair value of $52.79, roughly in line with the market price.

ADP’s cheap price can withstand even the most punishing stress-testing. I recommend buying ADP at any price up to $56. The payroll processors ADP & PAYX: deadly dull and extremely profitable.

6

Company Highlights

J.P. Morgan Chase (JPM) Berman’s Take:

J.P. Morgan Chase (JPM) stunned markets with a colossal hedging loss of $2 billion. The loss, blamed on the office tasked with managing risk, is expected to tally as much as $3 or $4 billion (once all the losing positions are unwound). A multi-billion dollar fiasco would sink many banks but not JPM, with its run rate of $20 billion in annual profit. The more worrisome question is how such a disastrous “hedge” went awry on Jamie Dimon’s watch. The uncomfortable answer is that “value-at-risk” models do nothing to truly capture all the moving parts of a bank’s real, underlying risk. This shows the caution necessary in owning any bank stock, but also highlights the need for a fortress-like balance sheet, which JPM did have—and still does. I would buy JPM on this short-term weakness.

(Access Interactive Model at Trefis)

Trefis Key Drivers:

J.P. Morgan’s sales and trading division accounts for nearly 20% of the Trefis price estimate. While the recent trading loss may not directly impact the Trefis valuation in a material way, the ramifications across the industry could be massive. The fact that one of the stronger U.S. banks, one which emerged from the financial crisis relatively unscathed, could have such glaring risk management issues plays into the hands of supporters of the Volcker Rule and those who want tighter bank regulations. Many banks had been lobbying for more leniency in the Volcker Rule, which restricts banks’ ability to engage in proprietary trading, but this appears to be a significant blow to those efforts. While Trefis still expects sales and trading to account for a significant portion of the bank’s value going forward, should more stringent regulation be implemented it could have a significant adverse impact on the bank’s revenues.

Market Capitalization

Annual Revenues Dividend/Yield

52 Week Range

$127.5 B $96.6 B $1.20/3.1% $27.85-46.49

7

Company Highlights

Wal-Mart (WMT) Berman’s Take: Wal-Mart (WMT) posted decent same-store growth of 2.6% for the quarter, a pleasing result but not enough to erase the tarnish from the bribery scandal dogging the company. WMT is alleged to have paid illegal kickbacks to advance its business interests in Mexico. Analysts estimate $3-5 billion in resulting losses, a staggering number even for a business with half a trillion in annual revenue. If the scandal remains isolated, it won’t have much more impact to the stock than it already has. I’m more concerned to see if the scandal impairs the juggernaut of international growth, given that Mexico was the best performing international region. I’ve raised the discount rate on the International Operations from 7% to 9% to account for the increased uncertainty (see below). This lowers the fair value to $60.58, just below market. I’m lowering WMT to Hold as a result.

(Access Interactive Model at Trefis)

Trefis Key Drivers:

Wal-Mart’s international stores account for about 41% of the Trefis price estimate given the expectation of further expansion in markets like China and Brazil. Trefis expects that Wal-Mart’s international store count will increase at a rate of more than 5% annually throughout its forecast period. Consumers in many of these markets are relatively cost-conscious which has led to a steady decline in the company’s international revenue per square foot. The scandal in Mexico could further exacerbate this trend, but Trefis forecasts that long-term revenue per square foot will only decline modestly as increasing discretionary income in emerging markets should offset any Mexico-related pressure.

Market Capitalization

Annual Revenues Dividend/Yield

52 Week Range

$212.5 B $123.2 B $1.59/2.4% $48.31.-62.63

8

Company Highlights

Alcoa (AA) Berman’s Take: Alcoa (AA) has sold off on growth concerns. With recessionary headwinds looking greater as Europe once again comes under stress, short-term demand for AA’s industrial products is unclear. Long-term, worldwide demand for Aluminum, however, should grow by at least 3-5%. AA specializes in value-added aluminum products to increase margins and differentiate itself. AA has done a good job of improving efficiency and returns. I think the future for AA is very bright. At a 42% discount to fair value, the price is more than right.

(Access Interactive Model on Trefis)

Trefis Key Drivers:

Engineered Products account for nearly 30% of the Trefis price estimate for Alcoa’s stock. Engineered Products include castings, forgings, fasteners, aluminum wheels and other products primarily used in the aerospace, automotive, construction, power generation and transportation industries. An increasing number of applications for aluminum products, particularly in the automotive segment as manufacturers look to reduce vehicle weights and improve fuel efficiency, should allow for significant growth in Alcoa’s Engineered Products shipments.

Alcoa is very sensitive to macroeconomic factors as aluminum demand is highly correlated to industrial activity and therefore global economic conditions. As economic conditions eventually improve, industrial demand should pick up and lead to higher realizations for Alcoa. However, should conditions in the Eurozone worsen and have an impact on global industrial activity it could have an adverse impact on Alcoa’s stock.

Market Capitalization

Annual Revenues Dividend/Yield

52 Week Range

$9.1B $24.7 B $0.12/1.4% $8.38—16.83

9

Company Highlights

Facebook (FB) Berman’s Take: I just couldn’t leave this issue without a quick note on Facebook (FB). I don’t own it, wouldn’t buy it and wouldn’t short it either. But the fascination with FB is truly an astounding phenomenon. As I write this, the IPO has just been priced at $38 and the underwriters hope it will skyrocket. It might seem absurd to even write about FB at all in a value investing letter: FB is debuting at 26 times sales, 100 times earnings and appears to be discounting not just the future, but the hereafter. This is hardly a value stock — by any definition. Trefis values the company at $33 per share, 13% lower than the IPO price.

Watch for our special report on Facebook, which will be sent to all subscribers shortly.

(Access Interactive Model on Trefis)

Trefis Key Drivers:

Socially powered text and display advertising is Facebook’s most valuable business. It accounted for

nearly 85% of Facebook’s overall revenue in 2011, and is likely to remain the company’s most lucrative

revenue driver going forward. Facebook offers a self-serve advertising platform for advertisers that

enables them to create advertisements targeting users based on their social demographic data. Trefis

expect Facebook’s active user base to more than double by the end of the Trefis forecast period which,

when coupled with the increase in average ad revenue generated per user, should lead to steady growth

in social text and display ad revenue.

Market Capitalization

Annual Revenues Dividend/Yield

52 Week Range

$104.8 B $3.7B $ - / - $38.01-42.03

10

Ticker Name

Buy Hold Sell

Reference Date

Reference Price ($)

Market Price ($)

Total Re-turn Since Reference Date($)1

Trefis Estimate

($)

Basic Materials

AA Alcoa Buy 12/21/2011 $8.87 $8.43 (4.7%) $12.04

DOW Dow Chemi-cal

Buy 12/21/2011 $26.98 $29.45 10.0% $38.64

Consumer

HNZ H.J. Heinz Buy 12/21/2011 $53.15 $54.10 3.6% $51.21

PG Procter & Gamble

Buy 12/21/2011 $65.84 $63.52 (1.9%) $70.10

WMT Wal-Mart Hold 12/21/2011 $59.49 $62.43 6.3% $72.53

Energy

BP BP Buy 12/21/2011 $41.33 $37.10 (9.3%) $57.72

Financial Services

BK BNY Mellon Buy 12/21/2011 $19.43 $20.24 5.4% $27.04

C Citigroup Buy 12/21/2011 $25.74 $26.01 1.1% $36.28

JPM JP Morgan Buy 12/21/2011 $32.12 $33.49 5.7% $47.94

Pharmaceuticals

JNJ Johnson & Johnson

Buy 03/21/2012 $65.21 $63.35 (2.9%) $72.45

PFE Pfizer Buy 01/21/2012 $21.90 $22.57 4.1% $25.11

Tech, Media, Telecom

ADP ADP Buy 12/21/2011 $53.21 $51.99 (0.9%) $58.49

EBAY eBay Hold 12/21/2011 $30.18 $38.36 27.1% $47.58

PAYX Paychex Buy 12/21/2011 $29.14 $29.41 3.0% $29.34

Industrials & Transportation

CSX CSX Corp Buy 12/21/2011 $20.80 $20.78 0.5% $27.65

UPS UPS Buy 12/21/2011 $72.40 $74.03 3.0% $83.60

UTX UTX Buy 04/21/2012 $80.40 $72.38 (10.0%) $102.00

Total 4.6%

1Since inception, including reinvested dividends on an equal dollar-weighted portfolio.

The Berman Value Folio

PORTFOLIO CHANGES

Wal-Mart (WMT) is downgraded to

Hold from Buy on valuation concerns

in wake of Mexican Bribery scandal.

11

The Berman Value Folio (TBVF) is published monthly and provides information and investment ideas on stocks. All material in TBVF is copyright 2012 by Trefis and may not be reproduced in whole or in part in any form without written consent. TBVF is intended for experienced investors, who understand the risks, costs, mechanics and consequences of investing. None of the content in this newsletter is intended to be, nor should be interpreted as, a solicitation to buy or sell securities. The selection of portfolio stocks is based on rigorous fundamental analysis. There is, however, no assurance that these securities will produce profits.

Performance results are based on model portfolios and do not reflect actual trading. Actual performance will vary based on a variety of factors, including market conditions and trading costs. TBVF results may not reflect the impact that material economic and market factors might have had on the adviser's decision-making if the adviser were actually managing clients' money in this portfolio. TBVF contains stocks that are managed with a view towards capital appreciation. James Berman and JBGlobal.com may manage other portfolios with different strategies and returns that materially differ from TBVF results. TBVF model results do not reflect the deduction of any advisory fees, brokerage or other commissions, bid-ask spreads and any other expenses that a client would have paid or actually paid in a real portfolio. All return figures assume the reinvestment of all dividends. Returns quoted are for an equal dollar-weighted portfolio, where each holding is purchased in equal dollar weights. Past performance does not guarantee future results. Any forward-looking statement is inherently uncertain and cannot be relied upon as a statement of actual performance. Investment in stocks can result in serious loss. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list.

Although all content is derived from data believed to be reliable, accuracy cannot be guaranteed. James Berman, JBGlobal.com LLC, Insight Guru Inc., Trefis, TBVF’s publisher and distributor(s) and their employees assume no liability whatsoever for any investment losses as a result of securities purchased on TBVF recommendations. TBVF is not intended to provide personalized investment advice. Readers and subscribers should consult their financial advisor before investment.

James Berman is an investor in Insight Guru Inc., the parent company of Trefis, both personally and through the venture fund he subadvises. Employees of TBVF, Insight Guru Inc., JBGlobal.com L.L.C. and Trefis may hold positions in some or all of the stocks mentioned here. James Berman and JBGlobal.com L.L.C. may hold positions in some or all of the stocks mentioned here, both personally and in the accounts and funds they manage for others. No compensation for recommending particular securities, services, or financial advisors is solicited or accepted. If you are unwilling or unable to abide by any conditions of this disclaimer, then you may obtain a refund for the unused portion of your subscription at any time.