the brazilian economy - bcb.gov.br · banco central do brasil 8 * seasonal range: seasonal pattern...

TRANSCRIPT

The Brazilian Economy

Governor of the Central Bank of Brazil

Ilan Goldfajn

April, 2018

BANCO CENTRAL

DO BRASIL

1

BANCO CENTRAL

DO BRASIL

THREE POSITIVE PHENOMENA IN THE BRAZILIAN ECONOMY

- Lower inflation

- Lower interest rates

- Economic recovery

2

Lower inflation and interest rates, with economic recovery

BANCO CENTRAL

DO BRASIL

Dec 15

10.67Aug 16

8.97

Aug 17

2.46

Mar 18

2.68

Dec 18

3.80

Dec 19

4.10

0

2

4

6

8

10

12Se

p 1

5

Dec

15

Mar

16

Jun

16

Sep

16

Dec

16

Mar

17

Jun

17

Sep

17

Dec

17

Mar

18

Jun

18

Sep

18

Dec

18

Mar

19

Jun

19

Sep

19

Dec

19

%

3

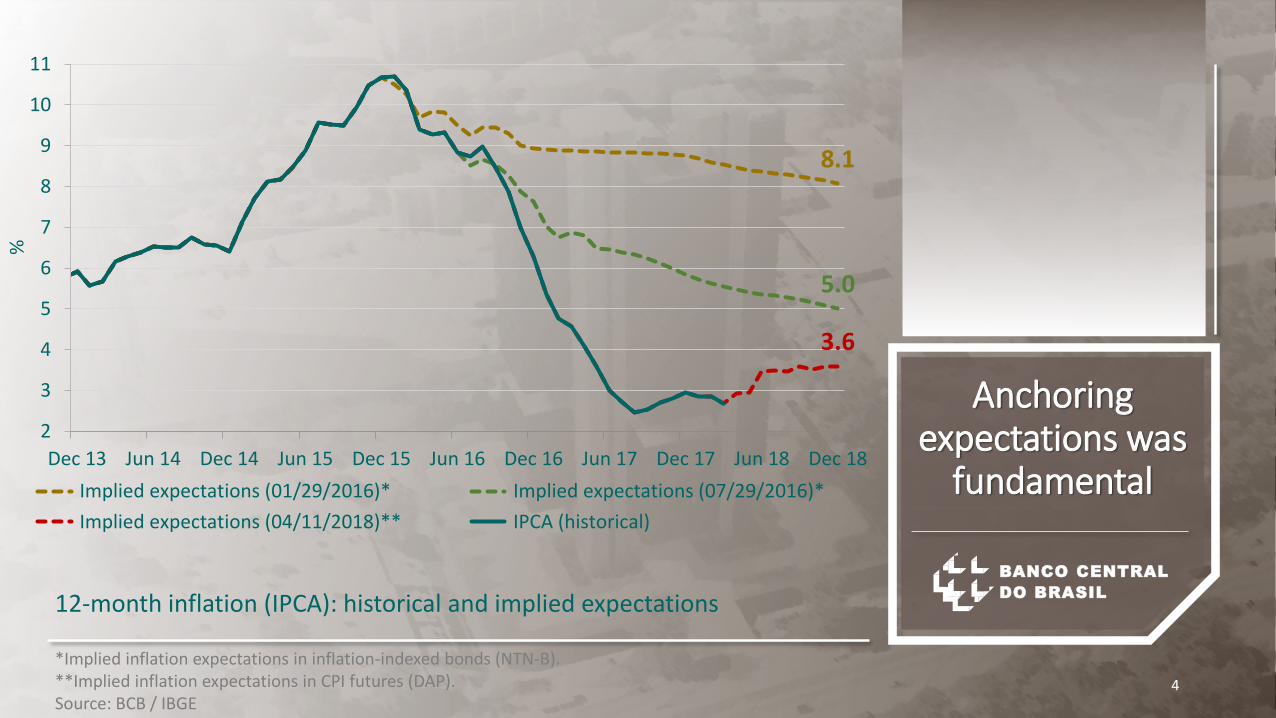

12-month inflation (IPCA)

Conditional forecasts*

*Considering interest and exchange rates from the Focus survey (Inflation Report, 2018/March).Source: BCB / IBGE

IPCA is converging

to the targets

BANCO CENTRAL

DO BRASIL

8.1

5.0

3.6

2

3

4

5

6

7

8

9

10

11

Dec 13 Jun 14 Dec 14 Jun 15 Dec 15 Jun 16 Dec 16 Jun 17 Dec 17 Jun 18 Dec 18

%

Implied expectations (01/29/2016)* Implied expectations (07/29/2016)*

Implied expectations (04/11/2018)** IPCA (historical)

4

*Implied inflation expectations in inflation-indexed bonds (NTN-B).**Implied inflation expectations in CPI futures (DAP).Source: BCB / IBGE

12-month inflation (IPCA): historical and implied expectations

Anchoring expectations was

fundamental

BANCO CENTRAL

DO BRASIL

5

Selic rate

SELIC rate at historical lows

14.25

6.505

6

7

8

9

10

11

12

13

14

15

Mar 16 Jun 16 Sep 16 Dec 16 Mar 17 Jun 17 Sep 17 Dec 17 Mar 18

% p

.a.

BANCO CENTRAL

DO BRASIL

160

165

170

175Se

p 1

4

Dec

14

Mar

15

Jun

15

Sep

15

Dec

15

Mar

16

Jun

16

Sep

16

Dec

16

Mar

17

Jun

17

Sep

17

Dec

17

Mar

18

Jun

18

Sep

18

Dec

18

Mar

19

Jun

19

seas

on

ally

ad

just

ed in

dex

(1

99

5 =

10

0)

2018

+2.8%

2019

+3.0%

6

Accumulated decrease*

-7.8%

Real GDP

In yellow, market expectations (Focus survey, 04/06/2018).*Growth between the fourth quarter of 2014 and the fourth quarter of 2016.Source: BCB / IBGE

GradualGDP recovery

BANCO CENTRAL

DO BRASIL

Economic Outlook

1. The global outlook has been favorable, as economies grow

and interest rates are low worldwide

This has so far contributed to support risk appetite towards

emerging economies

2. The set of indicators of economic activity shows consistent

recovery of the Brazilian economy

3. Low inflation in Brazil, converging to the targets

7

Low inflation with economic

recovery

BANCO CENTRAL

DO BRASIL

8

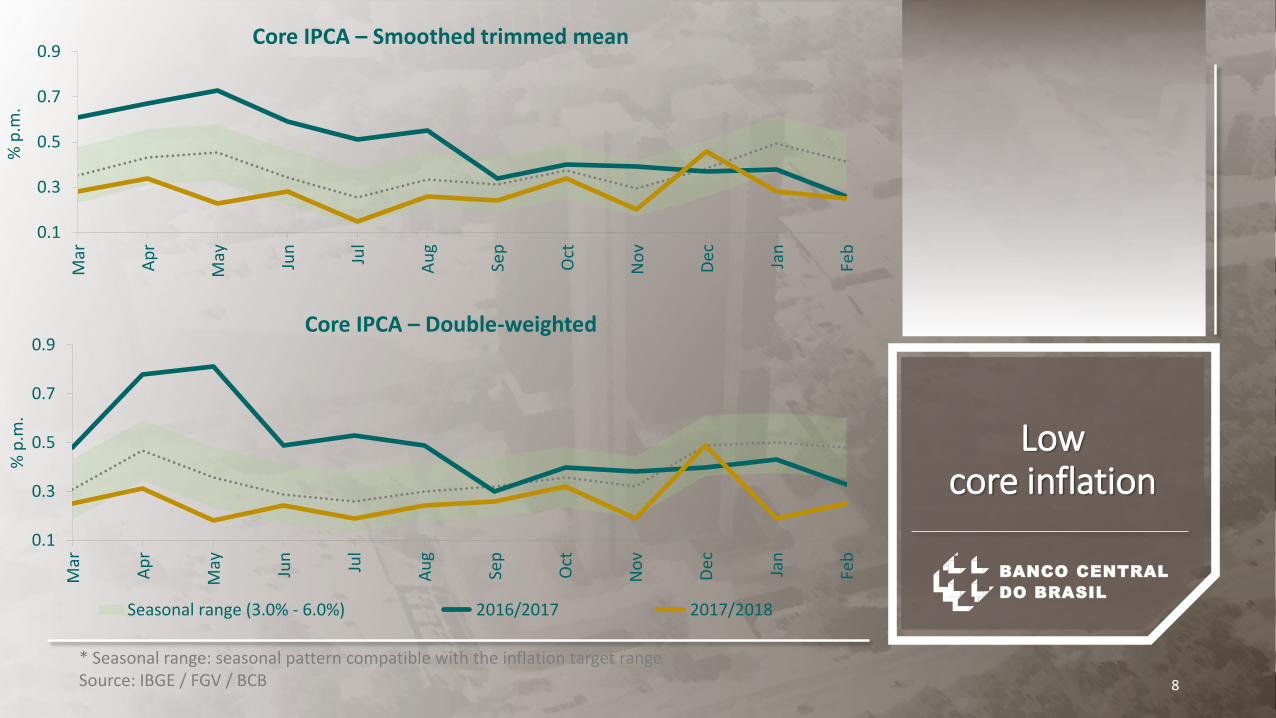

* Seasonal range: seasonal pattern compatible with the inflation target rangeSource: IBGE / FGV / BCB

0.1

0.3

0.5

0.7

0.9

Mar

Ap

r

May Jun

Jul

Au

g

Sep

Oct

No

v

Dec Jan

Feb

% p

.m.

Core IPCA – Smoothed trimmed mean

0.1

0.3

0.5

0.7

0.9

Mar

Ap

r

May Jun

Jul

Au

g

Sep

Oct

No

v

Dec Jan

Feb

% p

.m.

Core IPCA – Double-weighted

Seasonal range (3.0% - 6.0%) 2016/2017 2017/2018

Low core inflation

BANCO CENTRAL

DO BRASIL

9

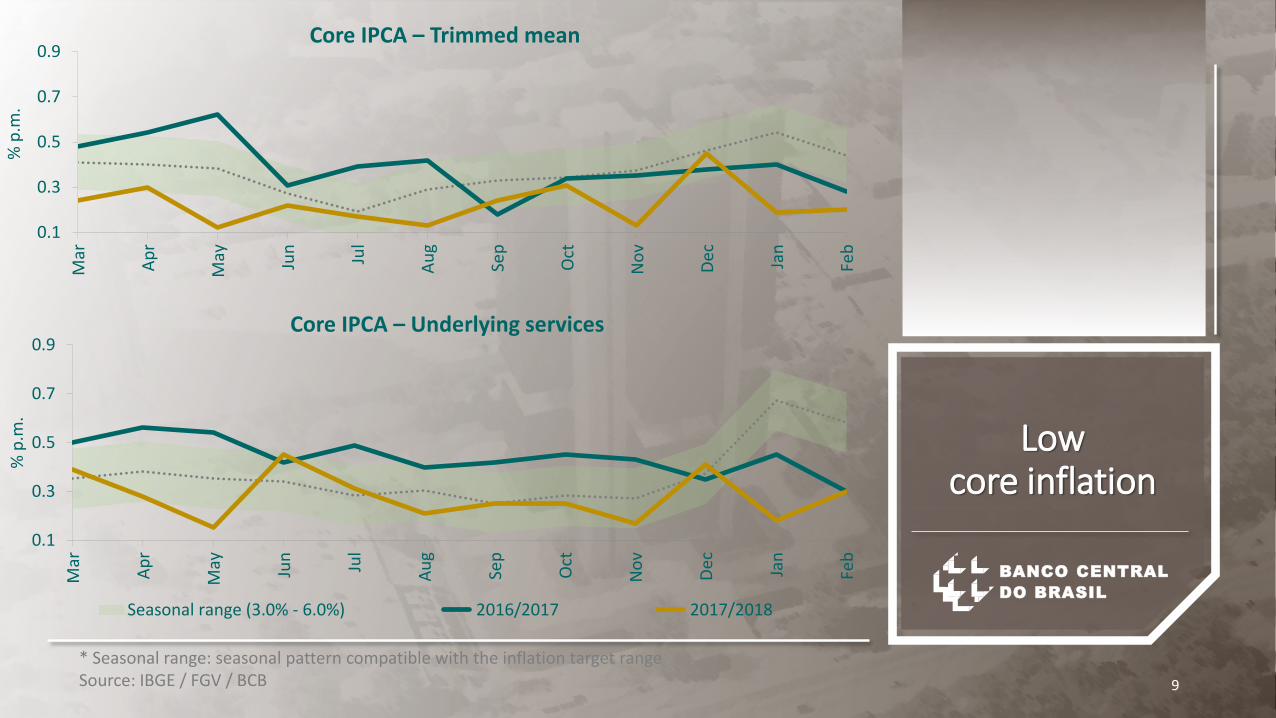

* Seasonal range: seasonal pattern compatible with the inflation target rangeSource: IBGE / FGV / BCB

0.1

0.3

0.5

0.7

0.9

Mar

Ap

r

May Jun

Jul

Au

g

Sep

Oct

No

v

Dec Jan

Feb

% p

.m.

Core IPCA – Trimmed mean

0.1

0.3

0.5

0.7

0.9

Mar

Ap

r

May Jun

Jul

Au

g

Sep

Oct

No

v

Dec Jan

Feb

% p

.m.

Core IPCA – Underlying services

Seasonal range (3.0% - 6.0%) 2016/2017 2017/2018

Low core inflation

BANCO CENTRAL

DO BRASIL

Monetary Policy

1. Risks around the baseline scenario remain in both directions:

Downside risk for inflation: (i) possible propagation through

inertial mechanisms of low inflation levels

Upside risk for inflation: (ii) frustration of expectations regarding

the continuation of reforms and adjustments; and (iii) a reversal

of the current benign global outlook for emerging economies

2. Monetary policy has the flexibility to react to risks in both

directions

10

Flexibility to react to risks in both

directions

BANCO CENTRAL

DO BRASIL

Monetary Policy

3. Copom – current assessment (baseline scenario):

Next meeting: the Copom views an additional moderatemonetary easing as appropriate and judges that this additionalstimulus mitigates the risk of delayed convergence of inflation

Beyond the next meeting: the Copom deems appropriate tointerrupt the monetary easing process, with the aim ofevaluating next steps

4. The Copom emphasizes that the next steps in the conduct ofmonetary policy will continue to depend on:

Evolution of economic activity

Balance of risks

Possible reassessments of the extension of the cycle

Inflation projections and expectations

11

Copom baseline scenario

BANCO CENTRAL

DO BRASIL

12

Monetary Policy

5. The Copom understands that monetary policy has to

balance two dimensions

Inflation convergence to the targets at a proper pace

Endurance of a low inflation environment, even in the

event of adverse shocks

Monetary policy has to balance

two dimensions

BANCO CENTRAL

DO BRASIL

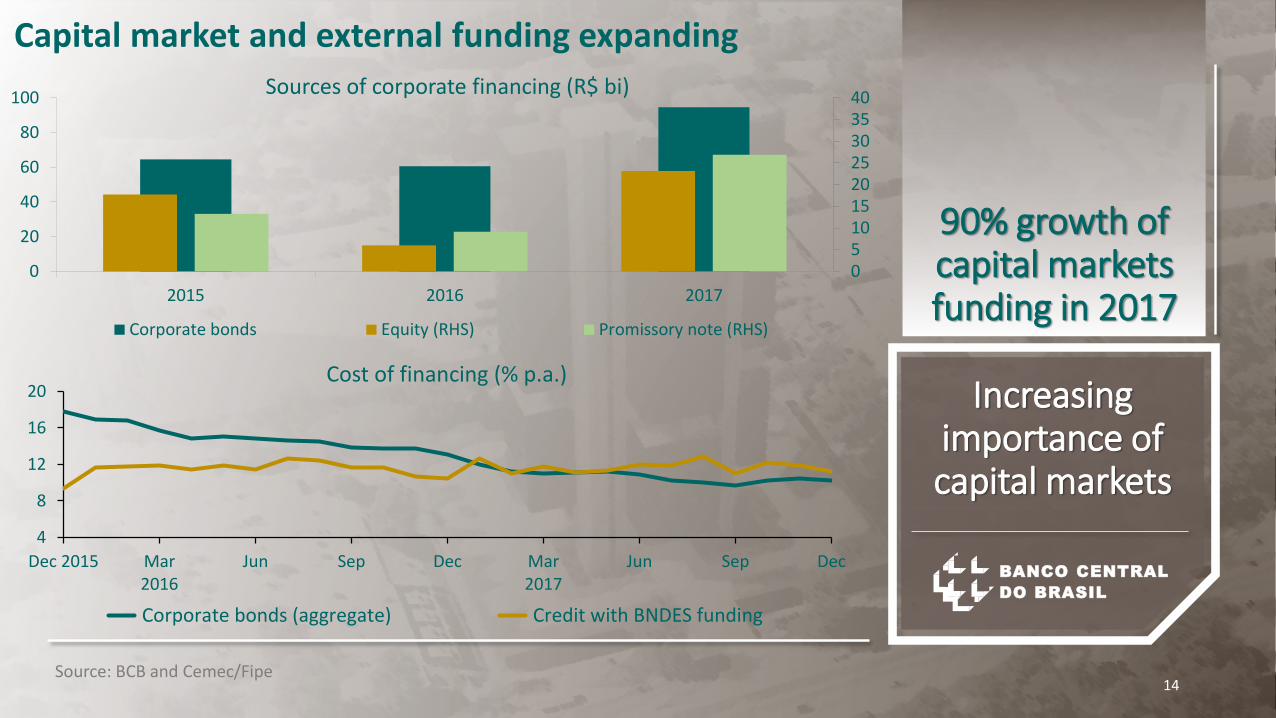

13*Non-earmarked market

Expansionary Monetary Policy Cyclesvariations from the start of the cycle (t0)

-12

-10

-8

-6

-4

-2

0

t-16 t-12 t-8 t-4 t0 t+4 t+8 t+12 t+16

Selic rate – pp

-25

-20

-15

-10

-5

0

5

t-16 t-8 t0 t+8 t+16

Credit interest rate* – pp

-15

-5

5

15

25

35

t-16 t-8 t0 t+8 t+16

New credit concessions* - %

R$ bi

178

218

254

323

246

% p.a.

26.3

19.8

13.7

12.4

14.2

% p.a.

57.8

47.4

43.3

38.1

53.3

1st cycle (may/03) 2

nd cycle (aug/05) 3

rd cycle (dec/08) 4

th cycle (aug/11) 5

th cycle (sep/16)

Current monetary easing cycle has a standard impact

BANCO CENTRAL

DO BRASIL

4

8

12

16

20

Dec 2015 Mar2016

Jun Sep Dec Mar2017

Jun Sep Dec

Cost of financing (% p.a.)

Corporate bonds (aggregate) Credit with BNDES funding

14Source: BCB and Cemec/Fipe

Capital market and external funding expanding

0510152025303540

0

20

40

60

80

100

2015 2016 2017

Sources of corporate financing (R$ bi)

Corporate bonds Equity (RHS) Promissory note (RHS)

Increasing importance of capital markets

90% growth of capital markets funding in 2017

BANCO CENTRAL

DO BRASIL

Final Remarks

• Economic Outlook:• Consistent economic activity recovery with the IPCA converging to

the inflation targets, but there are risks

• The global outlook is benign, but this scenario will not last forever

• Significant progress in adjustments and reforms, with severalstructural measures already approved and multiple initiativesin progress

• Brazil must continue along that path in order to sustain a lowinflation, a low structural interest rate and the economicrecovery

15

Brazil must continue on the path of reforms

The Brazilian Economy

Governor of the Central Bank of Brazil

Ilan Goldfajn

April, 2018

BANCO CENTRAL

DO BRASIL

16

THANK YOU