the budgeting process managerial accounting prepared by diane tanner university of north florida...

TRANSCRIPT

Copyright ©2015. University of North Florida. All rights reserved.

The Budgeting Process

Managerial Accounting

Prepared by Diane TannerUniversity of North Florida

Chapter 37

2 Budgets • What is a budget?

– A projection of future operations (costs, revenues, and cash) and the resulting financial position of a company

• Three basic types– Capital budgets

• Proposed expenditures for long-term capital expenditures

– Operating budgets• Costs, revenues, and cash flows relating to

operations– Financial budgets

• Proforma financial statements

2

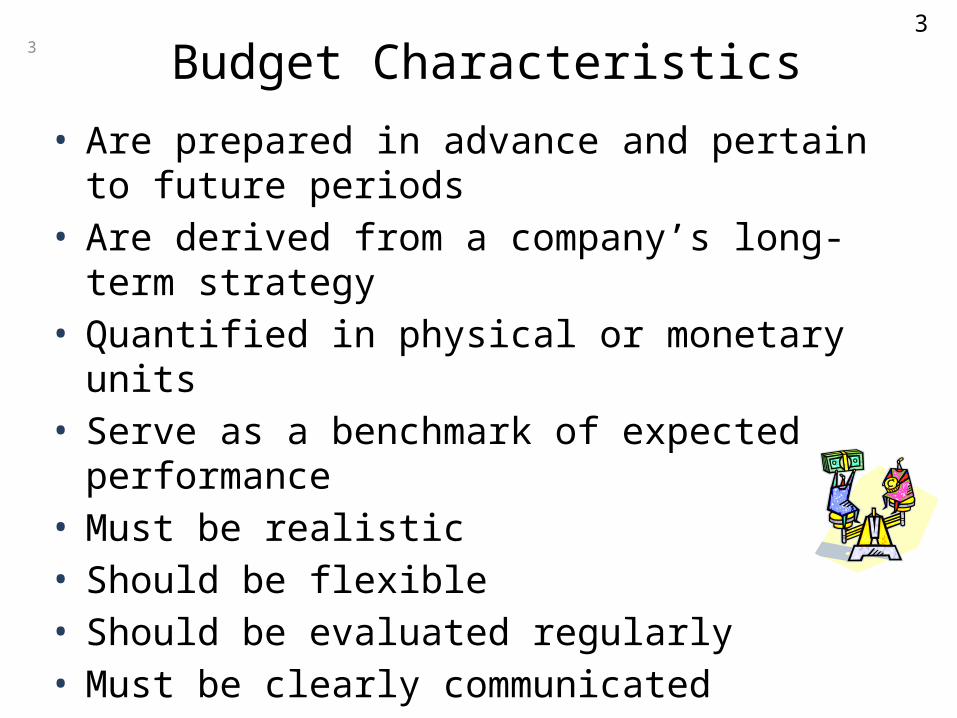

3 Budget Characteristics

• Are prepared in advance and pertain to future periods

• Are derived from a company’s long-term strategy • Quantified in physical or monetary units• Serve as a benchmark of expected performance• Must be realistic• Should be flexible• Should be evaluated regularly • Must be clearly communicated

3

Budgeting helps managers Communicate plans to other levels of

management and employees Quantify targets Determine directions in order to

allocate resources Promote forward thinking Turn strategic objectives into reality Specify a means of achieving goals

Planning Aspects of Budgeting4

Controlling Aspects of Budgeting

Budgeting helps managers…. Aid in measuring performance Provide direction and co-ordination Assign responsibilities Motivate managers to achieve goals Improve efficiency Establish targets and standards

5

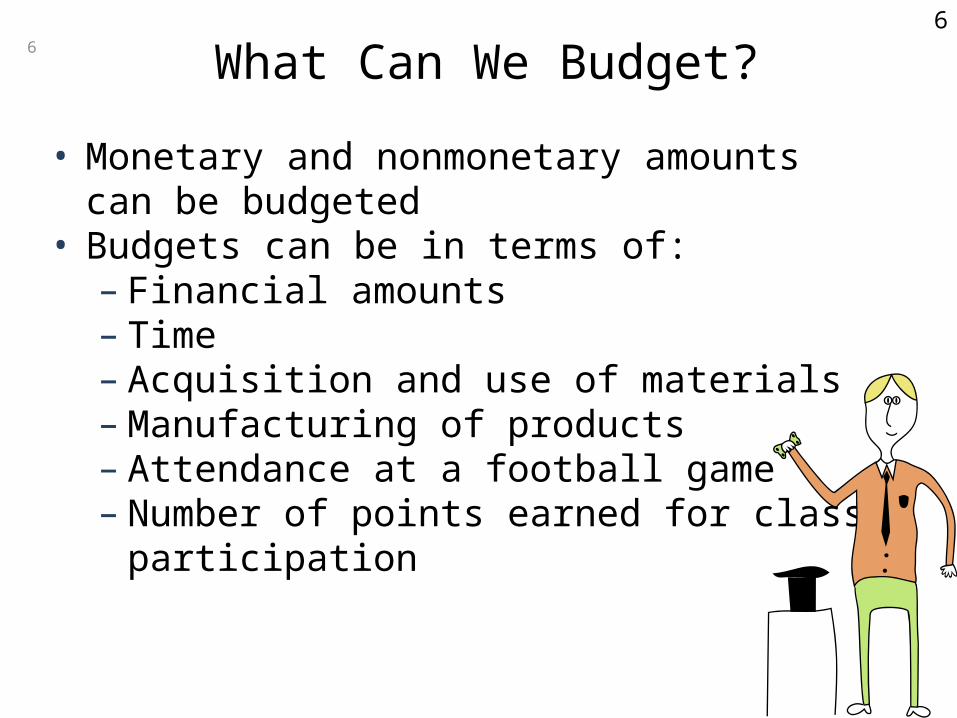

6 What Can We Budget?

• Monetary and nonmonetary amounts can be budgeted

• Budgets can be in terms of:– Financial amounts– Time– Acquisition and use of materials– Manufacturing of products– Attendance at a football game– Number of points earned for class

participation

6

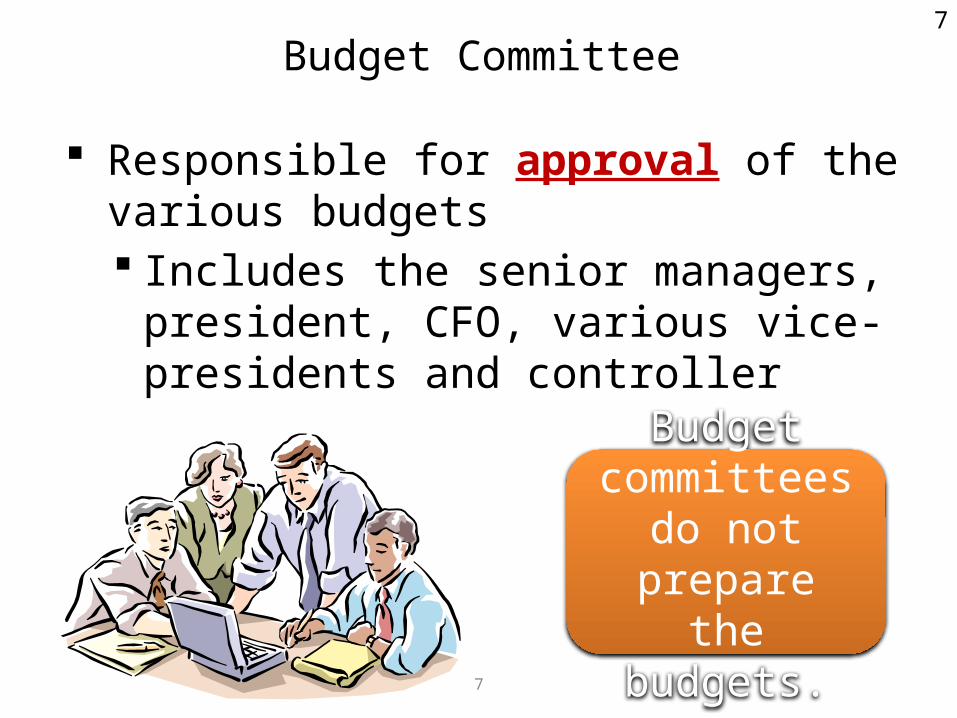

Budget Committee

Responsible for approval of the various budgets Includes the senior managers, president,

CFO, various vice-presidents and controller

7

Budget committees do not prepare the

budgets.

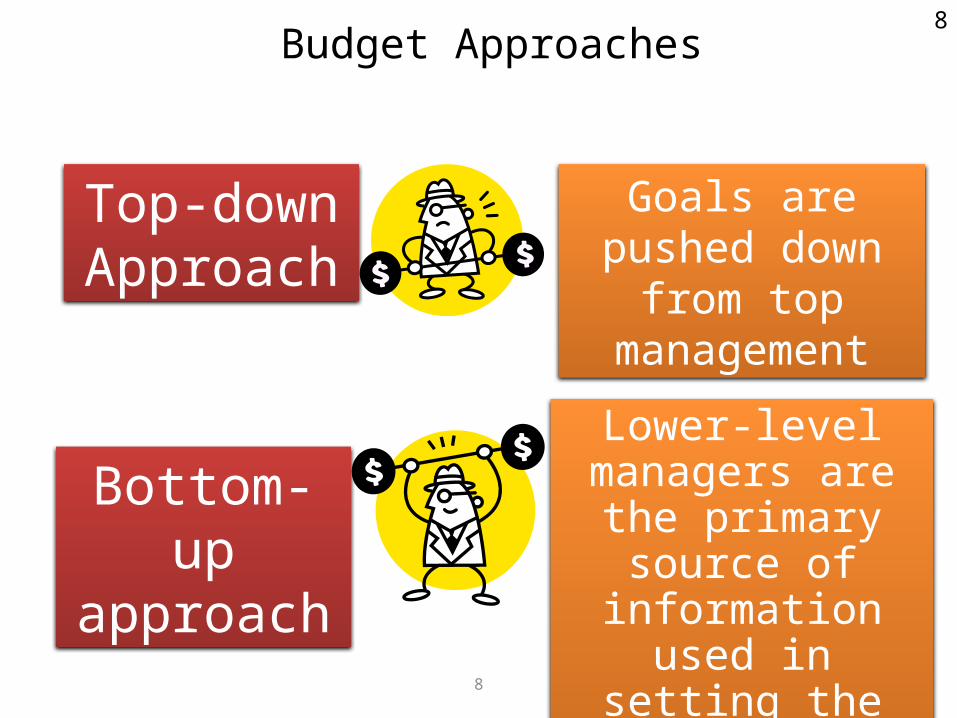

Budget Approaches

Top-down Approach

Goals are pushed down from top management

Bottom-up approach

Lower-level managers are the primary source of

information used in setting the budget

8

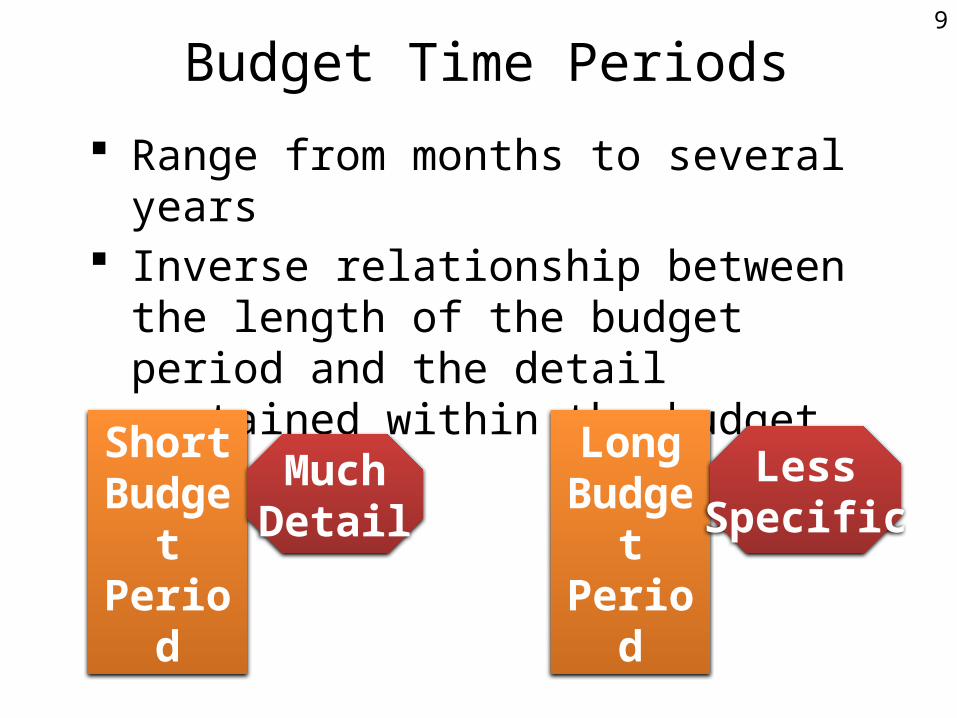

Budget Time Periods

Range from months to several years Inverse relationship between the length

of the budget period and the detail contained within the budget

ShortBudget Period

LongBudget Period

MuchDetail

LessSpecific

9

Specialized Budgeting Zero-based budgeting

A method of budget preparation which starts from zero each budget period

Managers must justify budgets every period Used primarily in government

Kaizen budgeting A Japanese model of budgeting Incorporates continuous improvement into each

subsequent budget period Assumes costs can be reduced somewhat as

time goes by because the company becomes more efficient

10

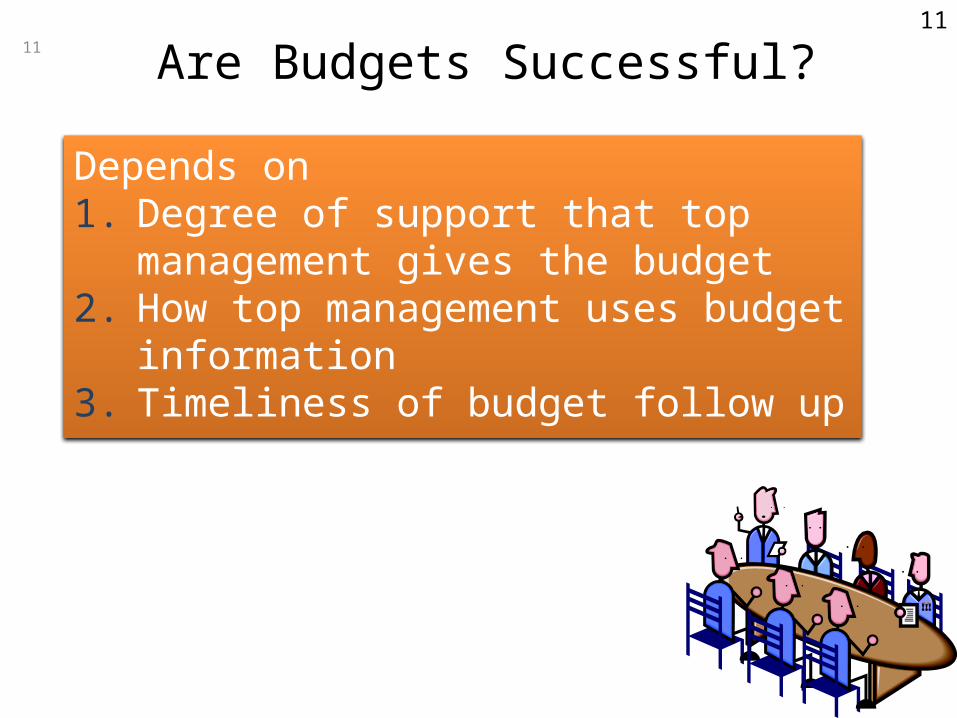

11 Are Budgets Successful?

Depends on1. Degree of support that top management

gives the budget 2. How top management uses budget

information3. Timeliness of budget follow up

11

12

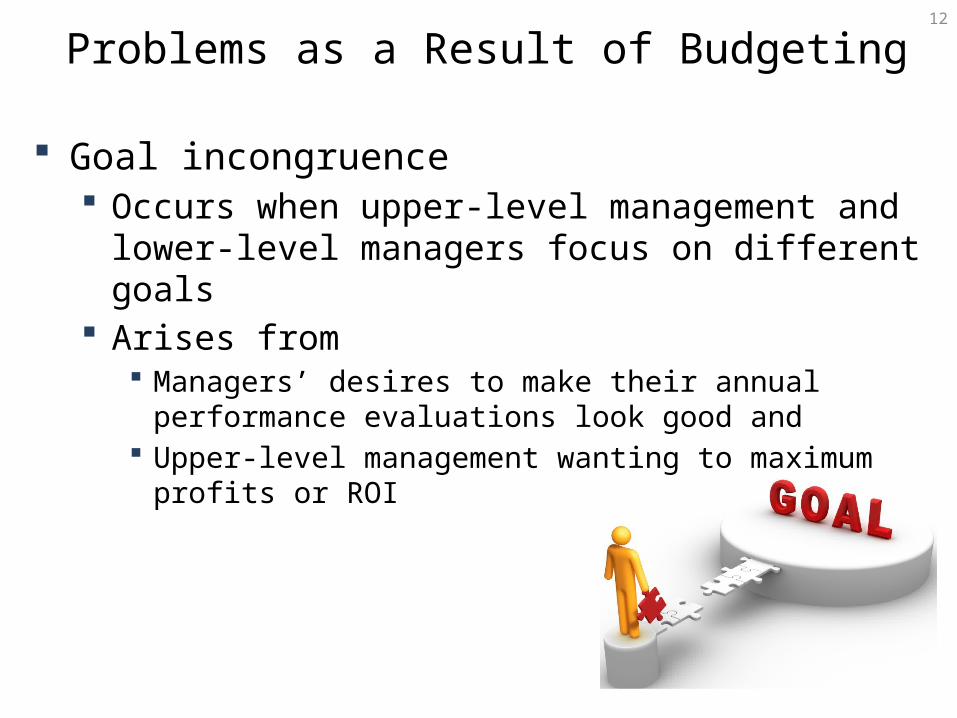

Problems as a Result of Budgeting

Goal incongruence Occurs when upper-level management and lower-

level managers focus on different goals Arises from

Managers’ desires to make their annual performance evaluations look good and

Upper-level management wanting to maximum profits or ROI

13

Problems as a Result of Budgeting

Budget slack Also known as padding the budget Only occurs when bottom-up budgeting is employed

Bottom-up budgeting allows lower-level managers to provide input into budgeted amounts

To avoid the possibility of not meeting the budget target, managers tend to Overstate budget expenses Understate revenue

14

Problems as a Result of Budgeting

Income shifting Occurs when a manager’s bonus is tied to

meeting or beating budget targets Causes managers to shift income between

periods to increase their performance evaluations

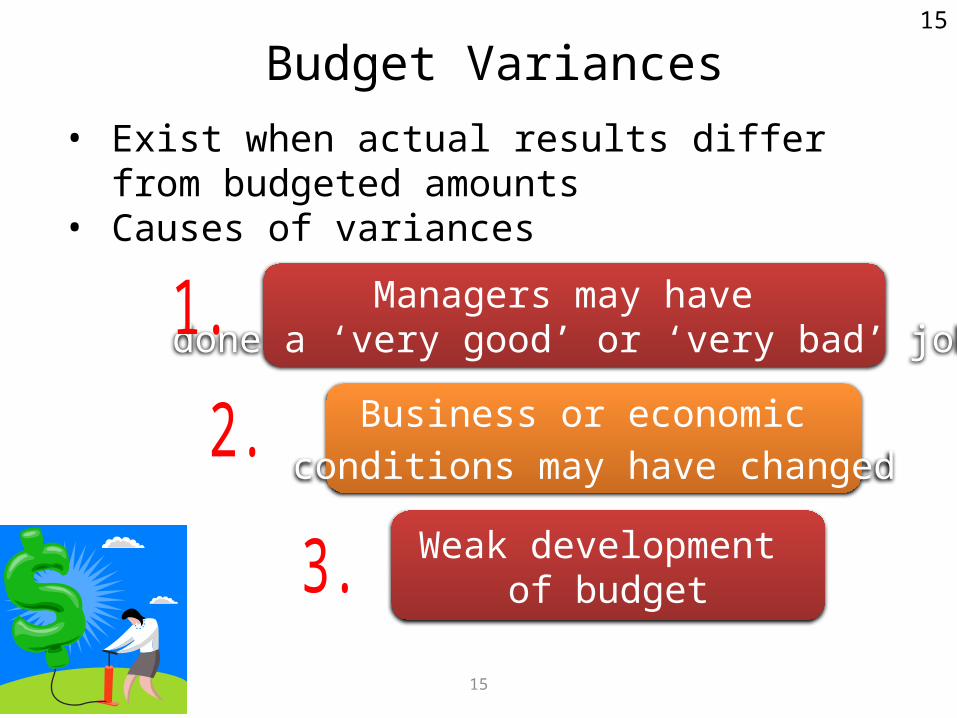

Budget Variances

Managers may have done a ‘very good’ or ‘very bad’ job

Business or economic conditions may have changed

Weak development of budget

15

• Exist when actual results differ from budgeted amounts

• Causes of variances

16

The End