the central goods and service tax act, 2017

TRANSCRIPT

[email protected] www.arsconsultants.net 1 23-Feb-19

©

The Central Goods and Service Tax Act, 2017

Concept of Supply

Arun Kumar Agarwal

[email protected] www.arsconsultants.net 2 23-Feb-19

©

Concept of Dual GST

Intra-State Supply

CGST (9%) SGST (9%)

Inter-State Supply

IGST (18%)

CE Duty, Service Tax, etc.

VAT, Entry Tax, Entertainment Tax, etc

CE Duty (Hidden)+ CST / Service Tax

CENTER STATES SHARED b/w

CG & SG

[email protected] www.arsconsultants.net 4 23-Feb-19

©

Levy CGST on intra-state supplies, except on alcoholic liquor, of value determined under Sec 15, at a rate not exceeding 20%, payable by taxable person

Specify categories of G/S - tax payable on Reverse Charge basis

central tax on petroleum crude, high speed diesel, petrol, natural gas and aviation turbine fuel shall be levied from such date as may be notified

Supply of G/S by an unregistered person to a registered person - tax to be paid by recipient on Reverse charge basis

Central Govt shall

If E-Commerce operator have no physical presence in the taxable territory, - any person representing it or

- as to be appointed by it,

shall be liable to pay tax.

1

2

3

4

5

CGST Act

Section 9

[email protected] www.arsconsultants.net 5 23-Feb-19

©

Levy IGST on inter-state supplies, except alcoholic liquor at a rate not exceeding 40%

Specify G/S – tax payable on Reverse Charge basis

Specify services - tax payable by E-Commerce operator,

Central Govt. Shall

If E-Commerce operator have no physical presence in taxable territory, then any person representing it or has to appoint if no representative, to pay tax.

1

3

1. IGST on goods imported to be levied /Collected in acc with Sec 3 of Custom Tariff Act, 1975

2. At point when custom is levied under Sec 12 Customs Act,1962 3. On value determined in CTA

Custom Tariff Act, 1975

IGST on petroleum crude, high speed diesel, petrol, natural gas and aviation fuel- be levied from notified date

2

Unregistered Dealer - tax payable on Reverse Charge basis 5

4

IGST Act

Section 5

[email protected] www.arsconsultants.net 6 23-Feb-19

©

Section 7 (CGST Act, 2017) Section 5 (IGST Act, 2017)

Levy CGST on intra-state

supplies, except on

alcoholic liquor, of value

determined under Sec 15, at a

rate not exceeding 20%,

payable by taxable person

Levy IGST on inter-state

supplies, except alcoholic

liquor at a rate not

exceeding 40

Charging Sections

[email protected] www.arsconsultants.net 8 23-Feb-19

©

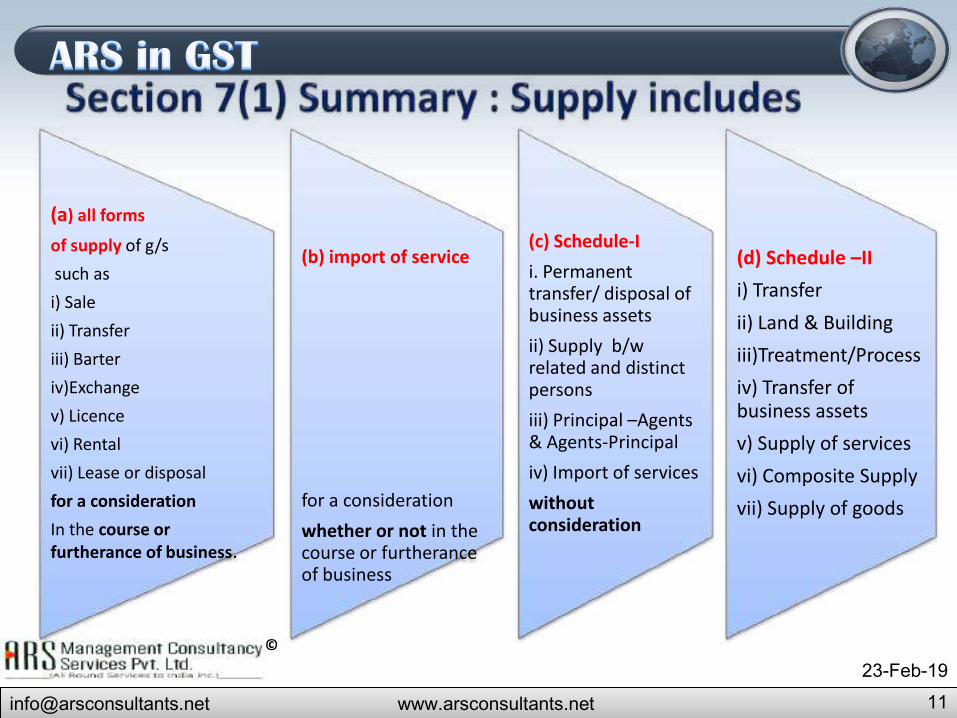

Section 7 - Scope of supply (1) Supply includes

(a) all forms of supply of goods and/or services such as sale, transfer,

barter, exchange, license, rental, lease or disposal made or agreed to be

made for a consideration by a person in the course or furtherance of

business,

(b) importation of services, for a consideration whether or not in the

course or furtherance of business, and

(c) The activities specified in Schedule I, made or agreed to be made

without a consideration.

(d) The activities to be treated as supply of goods or supply of services as referred to in Schedule II.

[Omitted by CGST (Amendment) Act, 2018]

[email protected] www.arsconsultants.net 9 23-Feb-19

©

. (2) Notwithstanding anything contained in sub-section (1), (a) activities or transactions specified in schedule III; or (b) such activities or transactions undertaken by the Central Government,

a State Government or any local authority in which they are engaged as public authorities, as may be notified by the Govt on the recommendations of the Council,

shall be treated neither as a supply of goods nor a supply of services.

Section 7 – Contd.... Inserted by CGST (Amendment) Act, 2018 (1A) where certain activities or transactions constitute a supply in accordance with the provisions of sub-section (1), they shall be treated either as supply of goods or supply of services as referred to in Schedule II

[email protected] www.arsconsultants.net 10 23-Feb-19

©

Section – 7 Contd.... (3) Subject to sub-section (1) and sub-section (2), the

Government may, on the recommendations of the Council, specify, by notification, the transactions that are to be treated as—

(i) a supply of goods and not as a supply of services; or (ii) a supply of services and not as a supply of goods.

[email protected] www.arsconsultants.net 11 23-Feb-19

©

(a) all forms

of supply of g/s such as i) Sale ii) Transfer iii) Barter iv)Exchange v) Licence vi) Rental vii) Lease or disposal for a consideration In the course or furtherance of business.

(b) import of service for a consideration whether or not in the course or furtherance of business

(c) Schedule-I i. Permanent transfer/ disposal of business assets ii) Supply b/w related and distinct persons iii) Principal –Agents & Agents-Principal iv) Import of services without consideration

(d) Schedule –II i) Transfer ii) Land & Building iii)Treatment/Process iv) Transfer of business assets v) Supply of services vi) Composite Supply vii) Supply of goods

[email protected] www.arsconsultants.net 13 23-Feb-19

©

Sale of Goods A wider connotation Supreme Court: Gannon Dunkerley (1958)-

Same as that in “Sale of Goods Act, 1930” Transaction (s.t. levy of sales tax)- - Parties competent to contract; - Mutual assent; and - Transfer of property

[email protected] www.arsconsultants.net 14 23-Feb-19

©

Tax Avoidance • Consignment Transfers • Indivisible works contracts • Hire Purchase; • Unincorporated Club/ Association to members • Controlled commodities • Lease of films • Supply of food by restautants

[email protected] www.arsconsultants.net 15 23-Feb-19

©

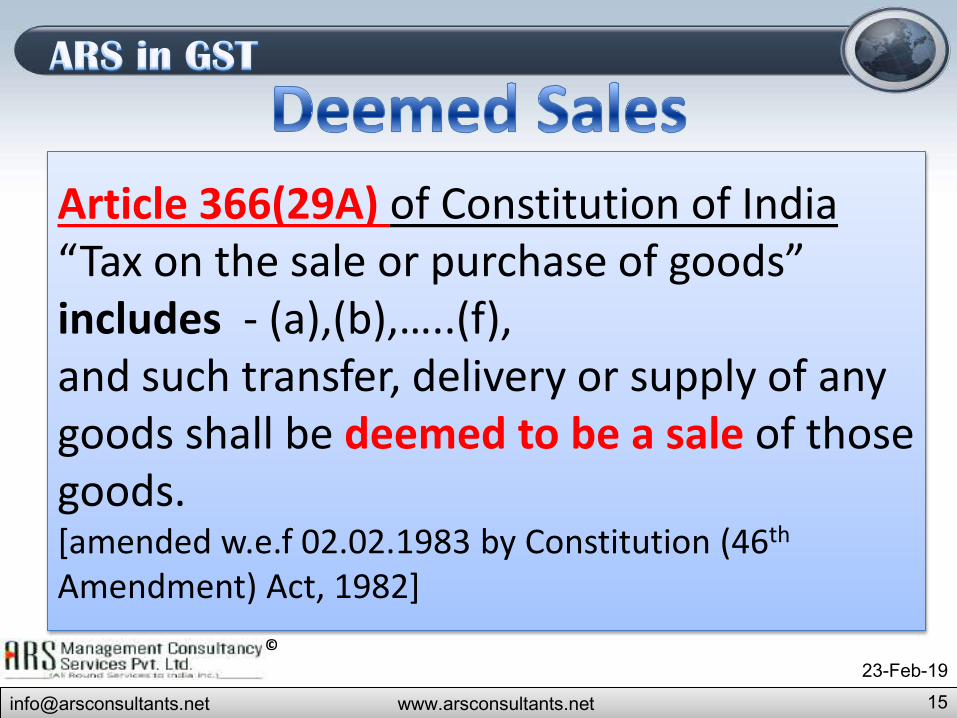

Article 366(29A) of Constitution of India “Tax on the sale or purchase of goods” includes - (a),(b),…..(f), and such transfer, delivery or supply of any goods shall be deemed to be a sale of those goods. [amended w.e.f 02.02.1983 by Constitution (46th Amendment) Act, 1982]

[email protected] www.arsconsultants.net 16 23-Feb-19

©

(a) Transfer, otherwise than in pursuance of a Contract, of property in any goods (Compulsory Transfer)

(b) Transfer of property in goods involved in Works Contract

(c) Delivery of goods on Hire-Purchase

(d) Transfer of the Right to use any goods

(e) Supply of goods by un-incorporated body of persons to a member

(f) Supply of food, articles for human consumptions and drinks

[email protected] www.arsconsultants.net 17 23-Feb-19

©

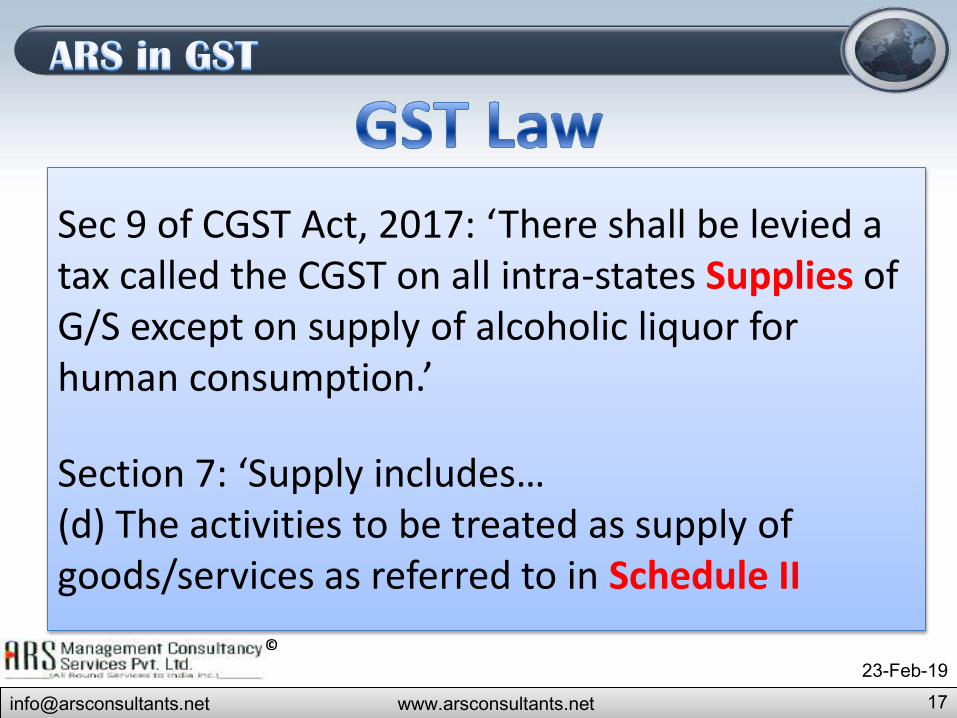

Sec 9 of CGST Act, 2017: ‘There shall be levied a tax called the CGST on all intra-states Supplies of G/S except on supply of alcoholic liquor for human consumption.’ Section 7: ‘Supply includes… (d) The activities to be treated as supply of goods/services as referred to in Schedule II

[email protected] www.arsconsultants.net 19 23-Feb-19

©

Clause 29A- Existing GST Law

(a): Transfer, otherwise than in pursuance of a contract, of property in any goods Shall be treated as sale of goods

Supply includes all forms of supply, such as sale, transfer, …. Or disposal made or agreed to be made for a consideration

[email protected] www.arsconsultants.net 20 23-Feb-19

©

Supreme Court- New India Sugar Mills: Volition by seller/ mutual assent absent Over-ruled in case of Vishnu Agencies (Pvt) Ltd. Versus CTO [(1977 (12) TMI 118 - (16.12.1977) For the purpose of levy of sales tax, the condition of valid consent of both parties is not essential. CST is payable even if goods are controlled commodity.

SC- ONGC: The Indian Steel & Wire Products Ltd. Vs. The State of Madras [1967 (9) TMI 115 - Supreme Court of India (11.09.1967)] Compulsory sale is also sale

[email protected] www.arsconsultants.net 22 23-Feb-19

©

As per Constitution As given in Schedule II

366(29A)(b): Transfer of property in goods, whether as goods or in any other form involved in execution of a works contract. Goods portion shall be treated as sale of goods and service portion as rendering of services

6(a): works contract as defined in Sec 2(119) Shall be treated as supply of services

[email protected] www.arsconsultants.net 23 23-Feb-19

©

As per Sec. 2 of CGST Act, 2017, (119) “works contract” means a contract for building(1), assembling, manufacturing, processing, construction(2), fabrication(3), completion(4), erection(5), installation(6), fitting out(7), improvement(8), modification(9), repair(10), maintenance(11), renovation(12), alteration(13) or commissioning(14) of any movable or immovable property wherein transfer of property in goods (whether as goods or in some other form) is involved in the execution of such contract;

[email protected] www.arsconsultants.net 24 23-Feb-19

©

In Gannon Dunkerley and Co. v. State of Rajasthan [1992 (11) TMI 254 - Supreme Court of India

(17.11.1992)] It was held that the taxable event is transfer of

property in goods involved in execution of a works contract. Transfer of property can take place by any one

of the following –

Accession – movable goods are

attached to movable property

(Spare parts attached in car)

Blending – movable goods mixed with

goods of contractee (printing/dyeing)

Accretion – movable goods are

imbedded in immovable

property (Const. contracts)

[email protected] www.arsconsultants.net 25 23-Feb-19

©

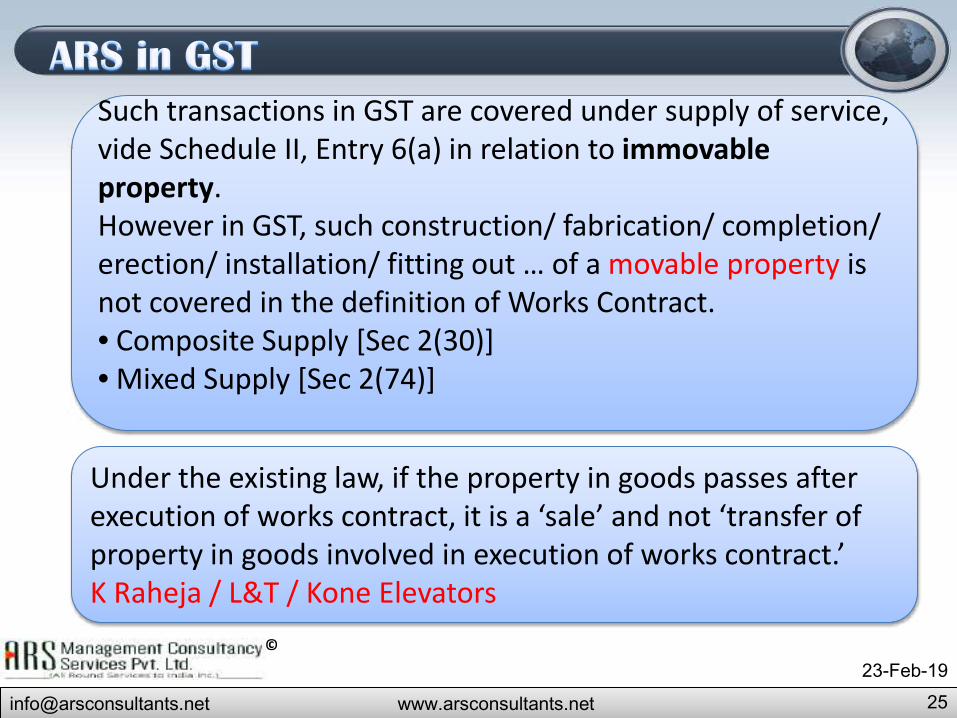

Such transactions in GST are covered under supply of service, vide Schedule II, Entry 6(a) in relation to immovable property. However in GST, such construction/ fabrication/ completion/ erection/ installation/ fitting out … of a movable property is not covered in the definition of Works Contract. • Composite Supply [Sec 2(30)] • Mixed Supply [Sec 2(74)]

Under the existing law, if the property in goods passes after execution of works contract, it is a ‘sale’ and not ‘transfer of property in goods involved in execution of works contract.’ K Raheja / L&T / Kone Elevators

[email protected] www.arsconsultants.net 27 23-Feb-19

©

As per Constitution As given in Schedule II

366(29A)(c): Delivery of goods on hire purchase or any system of payment by installment Shall be treated as sale of goods

1(c): any transfer of title in goods under an agreement which stipulates that property in goods shall pass at a future date upon payment of full consideration as agreed, Shall be is treated as supply of goods.

However, the words ‘hire purchase’ has not been used in the CGST Act, 2017.

[email protected] www.arsconsultants.net 28 23-Feb-19

©

Association of Leasing & Financial Service Companies Versus Union of India and others [2010 (10) TMI 4 -Supreme Court Of India (26.10.2010)] “According to Chitty on Contract, a hire purchase agreement is a vehicle of installment credit. It is an agreement under which an owner lets chattels out on hire and further agrees that the hirer may either return the goods and terminate the hiring or elect to purchase the goods when the payments for hire have reached a sum equal to the amount of the purchase price stated in the agreement or upon payment of a stated sum. The essence of the transaction is bailment of goods by the owner to the hirer and the agreement by which the hirer has the option to return the goods at some time or the other.”

[email protected] www.arsconsultants.net 30 23-Feb-19

©

As per Constitution As given in Schedule II

366(29A)(d): Transfer of right to use on any goods for any purpose (whether or not for a specific period) Shall be treated as sale of goods.

5(f): Transfer of the right to use any goods for any purpose (whether or not for a specific period) -same wordings Shall be treated as supply of services.

[email protected] www.arsconsultants.net 31 23-Feb-19

©

The transaction is taxable only when exclusive possession of goods and right to enjoy them freely for contracted period is given. If owner retains effective control with him, there is no ‘transfer of right to use goods.’

[email protected] www.arsconsultants.net 32 23-Feb-19

©

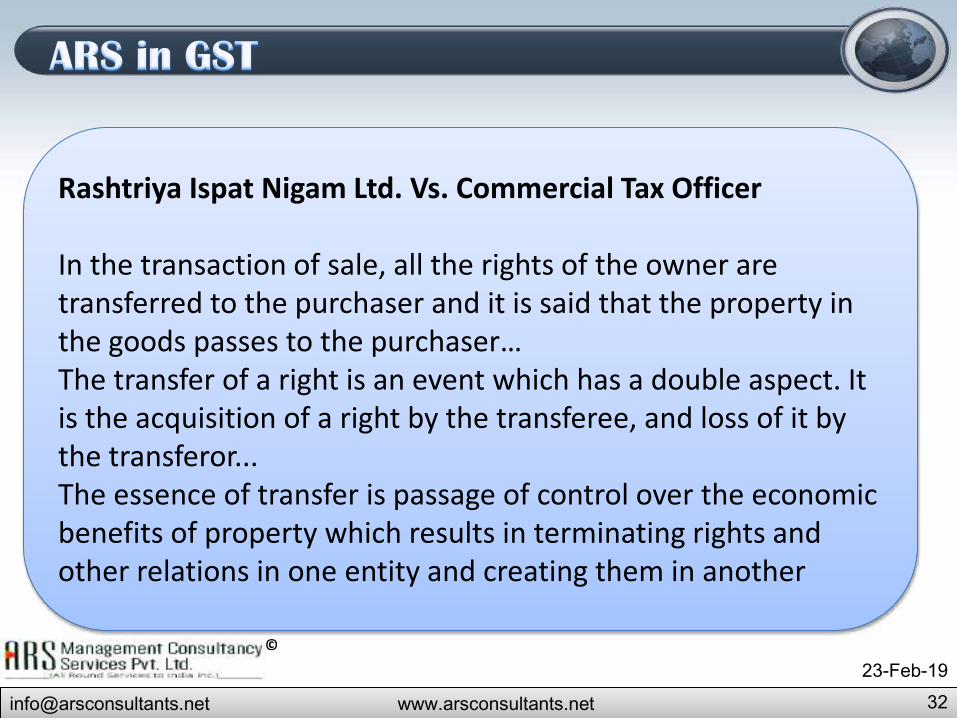

Rashtriya Ispat Nigam Ltd. Vs. Commercial Tax Officer In the transaction of sale, all the rights of the owner are transferred to the purchaser and it is said that the property in the goods passes to the purchaser… The transfer of a right is an event which has a double aspect. It is the acquisition of a right by the transferee, and loss of it by the transferor... The essence of transfer is passage of control over the economic benefits of property which results in terminating rights and other relations in one entity and creating them in another

[email protected] www.arsconsultants.net 34 23-Feb-19

©

As per Constitution As given in Schedule II

366(29A)(e): supply of goods by any un-incorporated association or body of persons to a member Shall be treated as sale of goods.

7: Supply of goods by any unincorporated association or body of persons to a member -same wordings Shall be treated as supply of goods.

Various judicial pronouncements are delivered on- whether goods/services provided by a club/hotel/hostel/society to its members are covered under ‘sale’ or not.

[email protected] www.arsconsultants.net 35 23-Feb-19

©

Mahomed Bagh Club Ltd. Vs Commissioner of Trade Tax, UP. [2009 (12) TMI 861 - Allahabad High Court (20.12.2009)] Club supplying food, snacks, etc. and selling of magazines, papers etc. to members is liable to sales tax.

Vasim Tanning Company Vs The State of Tamil Nadu [2008 (9) TMI 877 - Madras High Court (30.09.2008)] Sale by society to its members is taxable, even if society is an unincorporated body Service Tax - Concept of mutuality

[email protected] www.arsconsultants.net 37 23-Feb-19

©

As per Constitution As given in Schedule II

366(29A)(f): Tax on supply of food or any other article for human consumption or any drink (whether or not intoxicating) Shall be treated as sale of goods.

5(f): Tax on supply of food or any other article for human consumption or any drink (other than alcoholic liquor for human consumption). -same wordings except alcoholic liquor for human consumption is excluded. Shall be treated as supply of goods.

[email protected] www.arsconsultants.net 38 23-Feb-19

©

East India Hotels Ltd. and Vs Union of India [2000 (11) TMI 1065 - Supreme Court of India(15.11.2000)] Sales tax can be levied on food or drink served for consumption in hotel/restaurant. K Damodar Swamy Naidu (SC): Sales Tax Conflict between Kerala High Court and P&H High Court

[email protected] www.arsconsultants.net 40 23-Feb-19

©

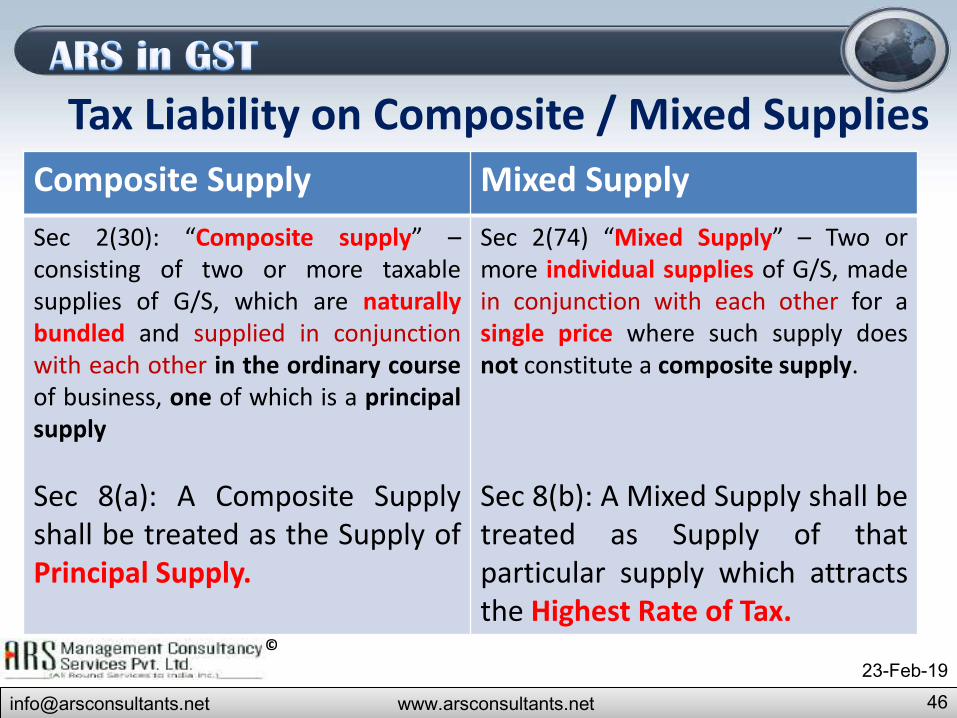

Sec 2(30) “Composite supply” – consisting of two or more taxable supplies of G/S, which are naturally bundled and supplied in conjunction with each other in the ordinary course of business, one of which is a principal supply. Illustration: Goods packed (with packing materials), transported with insurance.

Composite Supply

[email protected] www.arsconsultants.net 41 23-Feb-19

©

Sec 2(74) “Mixed Supply” – Two or more individual supplies of G/S, made in conjunction with each other for a single price where such supply does not constitute a composite supply. Illustration: A package consisting of canned foods, sweets, chocolates, cakes, dry fruits, aerated drinks and fruit juices when supplied for a single price. Each of these items can be supplied separately and is not dependent on any other. It shall not be a mixed supply if these items are supplied separately.

Mixed Supply

[email protected] www.arsconsultants.net 42 23-Feb-19

©

Sec. 2(90) of The CGST Rules, 2017- “principal supply” means the supply of G/S which constitutes the predominant element of a composite supply and to which any other supply forming part of that composite supply is ancillary

[email protected] www.arsconsultants.net 43 23-Feb-19

©

Party • Carl Still G.m.b.h v. State of Bihar [Supreme Court] [19th April, 1961]

Issue

• Contract for assembling and installing machinery, plant and accessories for a coke-oven battery and by-products plan. Whether a contract for sale or Works Contract?

Decision

• Price was agreed for the execution of the works and there was no agreement for sale of materials as such by the appellant therein to the owner and, therefore, the agreement in question was an indivisible one for the construction of specified works for a lump sum and not a contract for sale of materials as such.

Principle followed

• Intention of the contract was installation of machine. Accordingly, not a sale contract.

Case Laws relating to Predominant Element – Dominant Nature Test

[email protected] www.arsconsultants.net 44 23-Feb-19

©

Party • Patnaik & Co. v. State of Orissa [Supreme Court] [19th January, 1965]

Issue • Construction of bus bodies on the Chassis and the appellant had taken responsibility

to bear the loss, till the delivery of chassis with bus body

Decision

• The present contract is one for work and not a contract for sale, because the contract is not that the parties agreed that the "bus body" constructed by the appellants shall be sold to the State of Orissa. The contract is one in which the appellants agreed to construct "bus bodies" on the chasis supplied to them as bailees and such a contract being one for work, the consideration paid is not taxable under the Orissa Sales Tax Act.

Principal followed

• Intention of the contract was to construct bus bodies for their customer. No sale involved.

[email protected] www.arsconsultants.net 45 23-Feb-19

©

Party • State of Madras v. Richardson & Cruddas Ltd. [1968]

Issue • Contract for fabrication, supply and erection at site of all steelwork. Whether a

contract for sale or works contract?

Decision

• There was no provision under the contract for dissecting the value of the goods supplied and the value of the remuneration for the work and labour bestowed in the execution of the work and the predominant idea underlying the contract was bestowing of special skill and labour by the experienced engineers and mechanics

Principal followed

• Intention of the contract was getting all steel work done at site.

[email protected] www.arsconsultants.net 46 23-Feb-19

©

Tax Liability on Composite / Mixed Supplies Composite Supply Mixed Supply Sec 2(30): “Composite supply” – consisting of two or more taxable supplies of G/S, which are naturally bundled and supplied in conjunction with each other in the ordinary course of business, one of which is a principal supply Sec 8(a): A Composite Supply shall be treated as the Supply of Principal Supply.

Sec 2(74) “Mixed Supply” – Two or more individual supplies of G/S, made in conjunction with each other for a single price where such supply does not constitute a composite supply. Sec 8(b): A Mixed Supply shall be treated as Supply of that particular supply which attracts the Highest Rate of Tax.

[email protected] www.arsconsultants.net 48 23-Feb-19

©

Definitions 2(52)- “Goods” means every kind of movable property other than money and securities but includes actionable claim, growing crops, grass and things attached to or forming part of the land which are agreed to be severed before supply or under a contract of supply. 2(102)- “Services” means anything other than goods, money and securities but includes activites relating to the use of money … 2(32)- “continuous supply of goods” means a supply of goods which is provided or agreed to be provided continuously or on recurrent basis under a contract whether or not by means of a wire, cable, pipeline or other conduit and for which the supplier invoices the recipient on a regular or periodic basis and includes supply of such goods as the Govt may … 2(33)- “continuous supply of services” means a supply of services which is provided or agreed to be provided continuously or on recurrent basis under a contract for a period exceeding three months with periodic payment obligations and includes supply of such services as the Govt may …

[email protected] www.arsconsultants.net 49 23-Feb-19

©

Definitions- contd. 2(108)- “taxable supply” means a supply of goods or services or both which is leviable to tax under this Act. 2(78)- “non taxable supply” means a supply of goods or services or both which is not leviable to tax under this Act or under the IGST. 2(71)- “location of supplier of services” means,-

(a) where a supply is made from a place of business for which the registration has been obtained, the location of such POB;

(b) Where a supply is made from a place other than the POB for .. (a fixed establishment elsewhere), the location of such fixed establishment;

(c) Where a supply is made from more than one establishment, whether the POB or FE, the location of the establishment most directly concerned with the provisions of the supply; and

(d) In absence of such places, the location of the usual place of residence of the supplier.

[email protected] www.arsconsultants.net 50 23-Feb-19

©

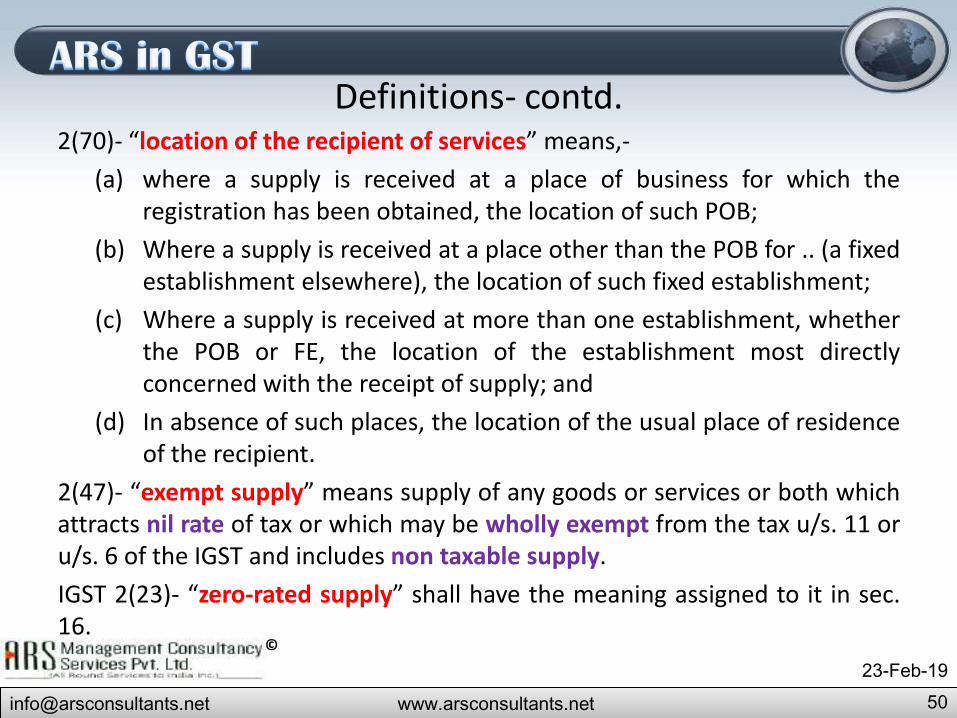

Definitions- contd. 2(70)- “location of the recipient of services” means,-

(a) where a supply is received at a place of business for which the registration has been obtained, the location of such POB;

(b) Where a supply is received at a place other than the POB for .. (a fixed establishment elsewhere), the location of such fixed establishment;

(c) Where a supply is received at more than one establishment, whether the POB or FE, the location of the establishment most directly concerned with the receipt of supply; and

(d) In absence of such places, the location of the usual place of residence of the recipient.

2(47)- “exempt supply” means supply of any goods or services or both which attracts nil rate of tax or which may be wholly exempt from the tax u/s. 11 or u/s. 6 of the IGST and includes non taxable supply. IGST 2(23)- “zero-rated supply” shall have the meaning assigned to it in sec. 16.

[email protected] www.arsconsultants.net 51 23-Feb-19

©

Definitions- contd. IGST Act / Section 16(1) “zero rated supply” means any of the following supplies of goods or services or both, namely:-

(a) Export of goods or services or both; or (b) Supply of goods or services or both to a SEZ developer or a SEZ unit.

2(20)- “casual taxable person” means a person who occasionally undertakes transactions involving supply of goods or services or both in the course or furtherance of business, whether as principal, agent or in any other capacity, in a State of a UT where he has no fixed place of business. 2(77)- “non-resident taxable person” means any person who occasionally undertakes transactions involving supply of goods or services or both, whether as principal or agent or in any other capacity, but who has no fixed place of business or residence in India.

[email protected] www.arsconsultants.net 52 23-Feb-19

©

Definitions- contd. 2(39)- “deemed exports” means such supplies of goods as may be notified u/s. 147. Section 147- The government may, on the recommendation of the Council, notify certain supplies of goods as deemed exports, where goods supplied do not leave India, and payment for such supplies is received either in Indian rupees or in convertible foreign exchange, if such foods are manufactured in India.

[email protected] www.arsconsultants.net 54 23-Feb-19

©

Sec 7 – Inter-State Supply [Coastal goods??]

Goods/ services

(a) Location of supplier & place of supply in different states/UT or a state & a UT

(b) Import

(c) Supplier is in India &

POS is outside

India

(d) SEZ (1) & (3)

(2) & (4) (5)(a)

(5)(b)

[email protected] www.arsconsultants.net 55 23-Feb-19

©

Sec 8 – Intra - State Supply

Goods / services

Location of supplier &

place of supply in

same state/UT

(1) & (2)

Intra State supply shall not include - • Supply goods/services to or by SEZ developer or SEZ unit • Supply of goods brought into India in the course of import • Supplies made to tourist

[email protected] www.arsconsultants.net 57 23-Feb-19

©

Sec – 10 Composition Levy

- permit a regd. person - aggr. turnover in preceding FY < 75/100 lacs - pay tax at rates

1. For manufacturers – 1/0.5% 2. For supply of foods, article for human

consumption – 2.5% 3. For Others – 0.5 %

- on turnover in each state

Central Govt. may

permission to be granted , if such person is not :- a. Supplying service [above 5 lacs or 10%], other than supply of

food, article of human consumption except alcoholic liquor b. Supplier of non-taxable goods c. Making inter-state outward supplies of goods d. Supplying goods through an E- Commerce operator e. Manufacturing such goods as may be notified

All assessee regd. with same PAN to opt simultaneously for composition levy

Withdraw permission -aggregate turnover during a FY > 75/100 lakhs

PR

OVI

DED

FU

RTH

ER

1 3

2

[email protected] www.arsconsultants.net 58 23-Feb-19

©

Sec – 10 Composition Levy ( Contd…..)

Taxable Person

-shall not collect any tax -nor be entitled to any credit of Input tax

If Taxable person not eligible for composition Levy , he shall be liable to:- 1. Tax (if any) 2. Penalty , along with provisions of Sec

73 or 74.

4 5

[email protected] www.arsconsultants.net 60 23-Feb-19

©

Dictionary meaning of SUPPLY

Shorter Oxford English dictionary gives a large number of

definition for the word supply and they have a common feature,

viz., that in the word supply is inherent the furnishing or

providing of something which is wanted. R. Vs Delgado, (1984) 1

All ER 449, 452. [Misuse of drugs Act, 1971, S. 5(3)]

Back