the centre for business mathematics and...

TRANSCRIPT

THE CENTRE FOR BUSINESS MATHEMATICS AND INFORMATICS® (Centre for BMI)

PROFILE MAY 2017

“I believe that this programme has bridged a significant gap between very theoretical research and business reality. The success of candidates in getting jobs with the institutions with whom they have done their research projects clearly indicates how institutions value the project output, but just as importantly that they know that they are employing individuals who can add value from day one.”

David HodnettDeputy CEO: Barclays Africa Group

“My experience of BMI graduates is that they compare favourably with the best graduates that we employ from universities in the UK.”

Ian WilsonHead of Wholesale Credit Risk Measurement: Group Risk, Barclays, London

1

SYNOPSIS 2

THE TEAM 2

BACKGROUND 3

TRAINING PROGRAMMES 4

INDUSTRY DIRECTED RESEARCH PROJECTS 4

DIRECTED RISK/REWARD RESEARCH PROGRAMME 5

COMMERCIALISATION OF RESEARCH 5

INTERNATIONAL NETWORKS 6

INDUSTRY COLLABORATION AND SUPPORT 8

INDUSTRY CLIENTS 10

PUBLICATIONS DIRECTLY RELEVANT TO THE BMI PROFILE 11

SELECTED RESEARCH PAPERS BY THE CENTRE FOR BMI AND COLLABORATORS 12

CONTACT DETAILS 14

CONTENT

2

SYNOPSIS The North-West University’s (NWU) Centre for Business Mathematics and Informatics® (Centre for BMI) is a leading tertiary risk training and research entity supplying resources to the financial services industry. It boasts:

• an extensive corporate client footprint in the financial services industry in Africa;

• collaborative relationships with clients, involving a spectrum of industry

• directed research projects;• a globally recognised quantitative risk

management programme (accredited with PRMIA);• a globally recognised actuarial and business

analytics programme;• international accolades for risk research;• the banking industry’s preferred talent source for

risk and business analytic talent; and• consistently high client satisfaction and

recommendation levels.

Front: Mr J Myburgh, Prof MF Kruger, Prof DCJ de Jongh, Prof PJ de Jongh, Prof JH Venter, Prof HP Mashele and Prof H Raubenheimer.Back: Ms L Hendriks, Prof T Verster, Mr T Cronje, Ms M Geldenhuys, Prof SE Terblanche, Ms J Larney, Ms C Klaassen, Mr RK Maxwell and Ms C Kruger.

THE TEAM

“The Centre for BMI hits the sweet spot between academic excellence and practical business skills. Due to this mix we find that BMI graduates are not only bright but hit the ground running with practical business skills. In short, industry enjoy excellent productivity from day one and BMI graduates an accelerated career path.”

Pravin Burra(FASSA) Director Capital Markets: Deloitte & Touche

3

BACKGROUNDThe Centre for Business Mathematics and Informatics® (Centre for BMI) was founded in 1998 as a joint initiative between the erstwhile Potchefstroom University (now North-West University) and ABSA Bank Limited (now Barclays Africa Group Limited). The primary aim was to establish a centre of excellence in financial risk/reward management training and research to support the South African financial services industry.

The BMI concept was designed following a similar concept that existed at the time between RABO bank and the Vrije

Universiteit (VU) Amsterdam. In 1997, three academics, namely Proff Neels Erasmus, Riaan de Jongh and

Andre de Waal, were appointed at the NWU to found the Centre for BMI. Their aim was to

build capacity and to develop the necessary know-how in the field of financial risk/

reward management training, in line with the goals already mentioned

above. Prof Neels Erasmus was appointed in June

1997 as the first director of the Centre for BMI, and was succeeded in November 2002 by Prof Riaan de Jongh.

Since its inception, the Centre for BMI has grown into a sustainable unit that has surpassed all initial expectations. The Centre for BMI currently comprises twelve full-time academic personnel and four support personnel. The Centre is highly regarded by local and international financial services companies due to the quality of its training and applied research programmes. The BMI training programme has grown from three MSc students in 1998 to about thirty five MSc students in more recent years. In 1998, a total of fifteen students enrolled for the BMI programme and this number has grown to 549 students in May 2017. This includes all students enrolled for BMI programmes (including PhD-programmes) at the Potchefstroom Campus and the Vaal Triangle Campus and 40% of these students are from a previously disadvantaged background.

The Centre for BMI has established long-term relationships with their industry partners, namely Barclays Africa and SAS. At first, the main focus was on the establishment of training programmes and research capacity building. However, since 2005, the Centre has been delivering a vibrant practical risk research service to the financial services industry and Barclays Africa in particular, including amongst others, assistance with model validation. SAS became involved in 2000 when the SAS Risk Laboratory was established at the Centre, with Prof Machiel Kruger appointed as the first head. During 2012, SAS further invested in the establishment of the SAS Advanced Analytics Laboratory and the Data Science training programme that was designed with a similar blueprint to the Advanced Analytics programme of the North Carolina State University. Prof Helgard Raubenmeimer is currently responsible for the professional MSc programme and the Analytics Laboratory, which includes the Risk Laboratory.

On the next page we report on the achievements of the Centre under the headings Training Programmes, Industry Directed Research Projects (conducted by Master’s students), Directed Risk/Reward Research Programme (conducted by staff), commercialisation of research, international networks, industry collaboration and clients, publications directly relevant to this profile, other research papers, and we conclude the profile with quotes from people in industry.

4

TRAINING PROGRAMMESThe Centre for BMI offers four training courses that focus on the financial services sector, namely: Quantitative Risk Management, Financial Mathematics, Business Analytics / Data Science and Actuarial Science. All these fields are built on the foundation laid by the mathematical sciences (e.g. Statistics, Mathematics and Operational Research) as well as the economic and computer sciences.

The Actuarial Science programme is accredited with the Institute / Faculty of Actuaries in the UK and the Actuarial Society of South Africa. Recently the Quantitative Risk Management programme received accreditation status from the Professional Risk Manager International Association (PRMIA) for Levels I and II of their Professional Risk Managers (PRM) qualification. NWU is the third university world-wide, and the first in Africa to receive accreditation status from this internationally-recognised professional body. The quality assurance processes of the NWU require that academic programmes are externally evaluated every five years. During 2014, the MSc BMI (with specialisations in Quantitative Risk Management, Financial Mathematics and Business Analytics / Data Science) was evaluated by an eminent international panel consisting of, amongst others, Paul Sweeting (an actuary from the University of Kent and Deutsche Bank), Sandjai Buhlai (a data scientist from the Free University in the Netherlands) and Paul Fatti (Chairman of the panel and emeritus professor from the University of the Witwatersrand). The panel of industry and academic representatives, comprising eight members, awarded the MSc programme the highest possible assessment: a Commendation. This is the second time that the BMI training and research programmes have received this rating from an evaluation panel, providing testimony of its excellent quality.

Graph 1 shows the growth in the BMI student numbers since its inception, broken down into year level.

Graph 1 Graph 2

INDUSTRY DIRECTED RESEARCH PROJECTSIn the second semester of their master’s degree, students are placed at a specific company for a period of five months and three to four days per week. They are then required to apply their knowledge and skills in solving a real-world problem for the company, under the joint supervision of both a BMI academic supervisor and an industry project officer. The dual requirement of this project is for the student to add value to the company, but also to demonstrate the ability to conduct academic research commensurate with a master degree’s level. This process is well-structured and managed according to a meticulously-articulated methodology that has proven to be very popular in the industry. This process has several benefits, amongst others, that students find employment easily, but also with the valuable inputs from industry, the project results in highly relevant research outcomes. BMI students are highly regarded by industry, as can be seen from the statements made by prominent business executives. Since its inception, the Centre for BMI has produced 387 MSc students (see graph below) who have all delivered an industry directed research report. Most of these reports were evaluated very positively by industry as adding direct business value (85% of these were rated higher than 3 out of 5 on a 5-point scale).

The programme delivers about 35 MSc students to industry each year. Another statistic - indicative of the popularity of the programme in industry - is that the number of project requests received from industry each year, outnumbers the available students at a ratio of almost 2:1.

Graph 2 shows the growth in BMI MSc students since inception.

5

DIRECTED RISK/REWARD RESEARCH PROGRAMMEWhen the Centre was first established, Prof Bert Kersten from

the Vrije Universiteit Amsterdam remarked that one could only expect their first peer reviewed publication in a

leading journal after about five to seven years (i.e. at the end of the capacity building phase). BMI’s first

peer reviewed paper was published after only four years (during 2002) in the Journal

of Risk, and the second paper in the same journal, two years later. These

papers had such impact on the industry, that they were selected by world experts

to appear in two books containing forefront research in the area of risk management and analysis. These books

are ‘Innovations in Risk Management: Seminal Papers from the Journal of Risk’

(ed. Philippe Jorion, University of California at Irvine) and ‘The Value-at-Risk Reference: Key Issues in the Implementation of Market

Risk’ (ed. Jon Danielsson, London Business School). Recently, Risk.net (Incisive Media)

selected the Centre’s latest paper, published in the Journal of Operational Risk in April 2016, as ‘Operational Risk Paper of the Year’. Another

paper published in the Journal of Operational Risk (March 2015), was incorporated into the Institute and Faculty of Actuaries’ 2016 ‘Good Practice Guide

to Setting Inputs for Operational Risk Models’.

Under the Memorandum of Agreement between the Centre and the Department of Science and Technology (DST), the DST has provided funding to the Centre

for BMI to stimulate and drive directed risk research on a national level. A national survey of risk research

conducted in 2014 highlighted a shortage of industry-relevant papers produced by universities. In order to stimulate relevant directed risk research, discussions have

been initiated with the Banking Association of South Africa in order to host a website, which enables industry to post risk research problem statements and academia to respond

with research proposals, followed by research projects. Funds are allocated to the participating universities in order to guide

the research efforts to be aligned to industry priorities. A very successfull directed risk research conference was hosted under the auspices of this agreement, where apart from BMI, the University of Pretoria, the University of Cape Town and the University of South Africa gave feedback on the utilisation of their allocated funds. The workshop was attended by more than 60 delegates from industry and academia.

COMMERCIALI SATION OF RESEARCHBMI research has led to the development of two systems that are in various stages of commercialisation. Both these systems were developed through grants from the Technology and Human Resources for Industry Programme (THRIP) and the National Research Foundation (NRF).

The UltimateAlpha systemThe Centre for BMI negotiated an agreement to form a consortium with the company S-Software Design. According to the agreement, the company will deliver services to industry using the UltimateAlpha system that was developed by Prof Dawie de Jongh, professor at the Centre. The UltimateAlpha system is the result of a research project funded amongst others by the Department of Trade and Industry’s THRIP initiative, and is aimed at assisting large fund managers in analysing the performance of their trading strategies and decisions. By using the system, fund managers can also evaluate the performance of brokers executing their trading instructions. Fund managers can send their trading data to S-Software Design who will analyse the data using the UltimateAlpha system as well as the Centre for BMI’s intra-day database (BMI IDDB). The BMI IDDB contains a ten-year history of the trade-by-trade data of all shares on the Johannesburg Stock Exchange. The results from this analysis are then transported to a secure server from which they may be viewed on the web. Clients include Stanlib, Old Mutual, Sanlam, Polaris Capital, Credit Suisse and Investec.

The AutoGann systemBMI researchers developed a system that constructs Generalized Additive Neural Networks (GANNs) automatically. The resulting system is called AutoGann and is fully integrated as a modelling node into SAS® Enterprise Miner™ data mining system. Model building is one of the most challenging and time consuming analytical tasks (some call it an art). Any system that can reduce the time and effort required to build accurate models could therefore result in huge financial benefits to the companies that have access to such systems. Not only does it free resources for other tasks, but it also shortens the model development time and facilitates quicker implementation of the newly developed models. The AutoGANN system has already been successfully applied to several large datasets from some of the leading banks in South Africa. Some of its uses include the computation of benchmark Gini coefficients for behavioural scorecards as well as model validation.

6

In 2005 the Academic Intelligence Award was presented to the Centre for BMI at the SAS Forum in Lisbon for bridging the industry-academia gap. The SAS Advanced Analytics Lab was officially opened in 2013 at the Centre by the SAS Vice President for Middle East and Africa. Subsequently the Data Science programme of the Centre for BMI was listed on the SAS website (the only programme outside the USA, see http://support.sas.com/learn/ap/prof/index.html#t4 and the video Shaping the Data Scientists of Tomorrow on the same web page). At the SAS Forum on Advanced Analytics held at SAS’ Headquarters (Cary, USA) in April 2015, experts from the Centre for BMI played leading roles as plenary speakers, panel participants and workshop facilitators.

In 2012 the Centre signed a Memorandum of Agreement with the Duisenberg School of Finance (DSF) in Amsterdam, the Netherlands, whereby two eligible BMI students are selected annually by the NWU for final evaluation by the DSF for their masters’ programme. Successful applicants receive a guaranteed 60% tuition fee waiver from the DSF, including a guaranteed study loan from ING Bank to cover the remainder of his/her tuition fees and other living expenses for the period of study at DSF. So far, six BMI students have been proposed by the NWU, and DSF has accepted all of them into their master’s programmes. At the end of 2015, three students (two of whom were actuarial students), completed their studies under this agreement. Their excellent performance subsequently motivated the decision by DSF to increase the annual intake of BMI students to four. The Amsterdam Business School of the University of Amsterdam has offered three potential BMI students waivers of €2900 per person for studies towards a Master’s in International Finance.

Memoranda of Agreement were signed with the Albstadt-Sigmaringen University in Germany, Strathmore University in Kenya and the National Economics University of Vietnam. These agreements involve the mutual exchange of graduate students between the postgraduate courses and the mutual acceptance of certain training and research modules. The Centre for BMI is currently negotiating a Memorandum of Agreement with the Kenya School of Monetary Studies (KSMS), whereby the MSc BMI with specialisation in Business Analytics will be presented via distance-learning in collaboration with KSMS in mid-Africa. The agreement also entails research collaboration and possible expansion to other BMI and NWU programmes. Discussions regarding the presentation of the Texas A&M distance learning programme (Statistics and Business Analytics) in Africa have also been initiated.

The NWU’s Centre for BMI plays a leading role in organising the triennial international conference on Mathematics in Finance in the Kruger National Park. The conference is organised by a consortium of four universities comprising

North-West University, the University of Pretoria, the University of Cape Town and the University of Johannesburg. This conference was held in 2014 for the 5th time and featured well-known actuaries and eminent world experts in financial risk research, such as Paul Embrechts (ETH), Alexander McNeil (Heriot Watt), Rudiger Frey (Vienna), DirkTasche (Imperial College) and Jonathan Crook (Edinburgh) (see picture on the right). More than half of the participants at this conference are from Europe and the USA.

INTERNATIONAL NETWORKS

7

Paul Embrechts, Alex McNeil, Rüdiger Frey, Dirk Tasche, Jonathan Crook

Mathematics in Finance Conference 2014:BMI Official Visitors

Mathematics in Finance Conference 2014:Representatives from Barclays Africa with Visiting Professors.

Frederik van der Walt, Morne Joubert, Wickes Robbertse, Paul Embrechts, Ina de Vry, Jonathan Crook, Dirk Tasche and Rüdiger Frey

8

INDUSTRY COLLABORATION AND SUPPORT

Industry partner Barclays AfricaBarclays Africa has been a seeding partner and has supported the Centre ever since its inception in 1998.

The first five years was a capacity building phase, but the Centre has since become sustainable and Barclays Africa expects the Centre to add value to its organisation in particular, but also the banking industry in general,

through its training and research programmes. To this end Barclays Africa has also established an Applied Risk Research Committee, which manages and monitors research progress on a regular basis. The BMI research team

has completed several projects for Barclays Africa and the local banking industry. The project reports are all classified and are not published in open sources. More than sixty reports have been delivered to the banking industry, and most

have received high ratings in terms of quality and relevance.

Absa Award Ceremony:BMI Risk Training and Research Programmes (2009).

Neels Erasmus, Maria Ramos, David Hodnett and Riaan de Jongh

Absa commits to strengthening and expanding their relationship with the NWU’s Centre for BMI (2009).

9

Industry partner SAS InstituteThe SAS Institute recognised the Centre for outstanding innovation in bridging the gap between industry and academia. SAS has more than 4 million users and more than 40,000 customer sites worldwide, with more than 2000 universities using SAS software. The SAS Academic Intelligence Award was presented to the Centre for BMI in Lisbon at the SAS Forum International 2005, a major conference attended by more than 2600 delegates from all around the world.

In 2012, SAS Institute donated $300,000 to establish a new Advanced Analytics Laboratory at the Centre. The funds were used to acquire state-of-the-art infrastructure and software to support risk and business analytics research and industry directed research projects. It should be noted that, although SAS support the Centre, there is no pressure to exclusively use their software, and students are also exposed to other programming languages like R, Java, Python, Hadoop, Oracle, C# and Visual Basic.

Opening of the SAS Labat the Centre for BMI (2013).

Riad Gydien, Machiel Kruger and Riaan de Jongh

BMI-SASA Workshop at Statistics in Finance (2010).

Murray de Villiers (SAS), Robert Engle (Nobel Laureate) and Theuns Eloff (NWU Vice-Chancellor)

10

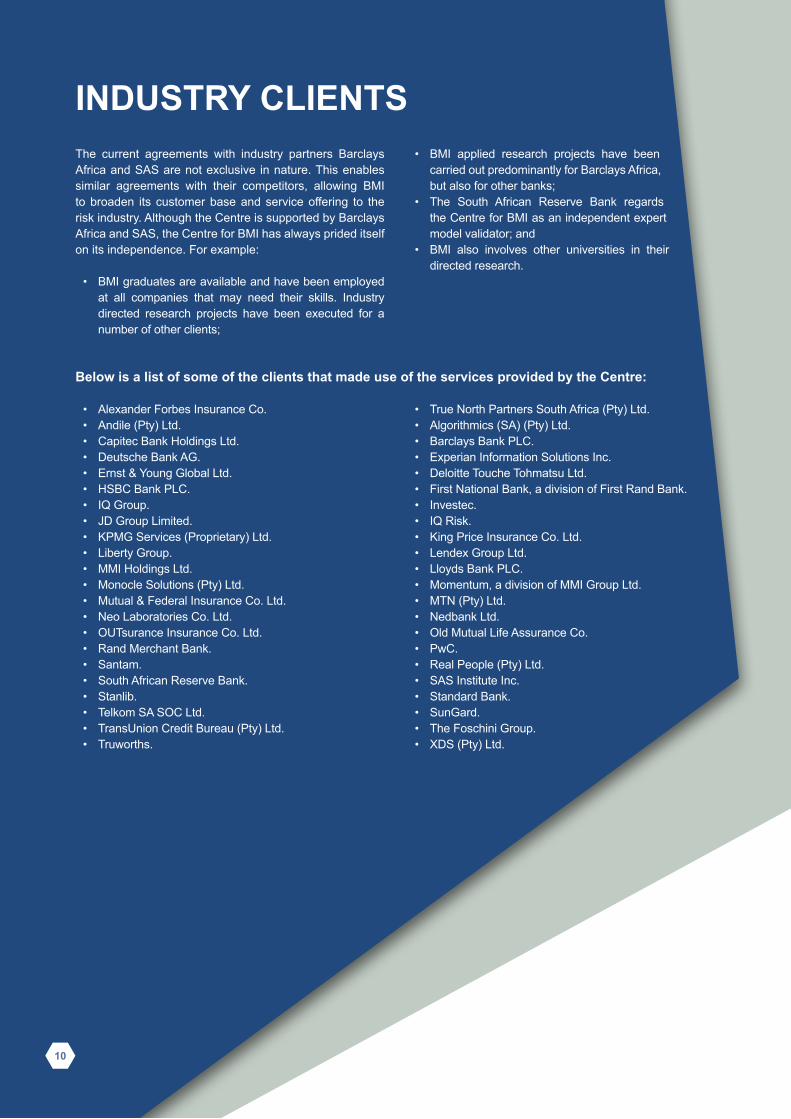

The current agreements with industry partners Barclays Africa and SAS are not exclusive in nature. This enables similar agreements with their competitors, allowing BMI to broaden its customer base and service offering to the risk industry. Although the Centre is supported by Barclays Africa and SAS, the Centre for BMI has always prided itself on its independence. For example:

• BMI graduates are available and have been employed at all companies that may need their skills. Industry directed research projects have been executed for a number of other clients;

• Alexander Forbes Insurance Co.• Andile (Pty) Ltd.• Capitec Bank Holdings Ltd.• Deutsche Bank AG.• Ernst & Young Global Ltd.• HSBC Bank PLC.• IQ Group.• JD Group Limited.• KPMG Services (Proprietary) Ltd.• Liberty Group.• MMI Holdings Ltd.• Monocle Solutions (Pty) Ltd.• Mutual & Federal Insurance Co. Ltd.• Neo Laboratories Co. Ltd.• OUTsurance Insurance Co. Ltd.• Rand Merchant Bank.• Santam.• South African Reserve Bank.• Stanlib.• Telkom SA SOC Ltd.• TransUnion Credit Bureau (Pty) Ltd.• Truworths.

• True North Partners South Africa (Pty) Ltd.• Algorithmics (SA) (Pty) Ltd.• Barclays Bank PLC.• Experian Information Solutions Inc.• Deloitte Touche Tohmatsu Ltd.• First National Bank, a division of First Rand Bank.• Investec.• IQ Risk.• King Price Insurance Co. Ltd.• Lendex Group Ltd.• Lloyds Bank PLC.• Momentum, a division of MMI Group Ltd.• MTN (Pty) Ltd.• Nedbank Ltd.• Old Mutual Life Assurance Co.• PwC.• Real People (Pty) Ltd.• SAS Institute Inc.• Standard Bank.• SunGard.• The Foschini Group.• XDS (Pty) Ltd.

• BMI applied research projects have been carried out predominantly for Barclays Africa, but also for other banks;

• The South African Reserve Bank regards the Centre for BMI as an independent expert model validator; and

• BMI also involves other universities in their directed research.

INDUSTRY CLIENTS

Below is a list of some of the clients that made use of the services provided by the Centre:

11

PUBLICATIONS DIRECTLY RELEVANT TO THE BMI PROFILE

For a detailed discussion of the BMI training and research philosophies, the interested reader is referred to Boersma et al. (2008) and de Jongh and Erasmus (2014).Below also find references to the first two peer-reviewed papers incorporated into the two Risk Books (see Venter and de Jongh, 2004 and 2007), the paper incorporated into the Institute and Faculty of Actuaries’ 2016 Good Practice Guide to Setting Inputs for Operational Risk Models (see de Jongh et al. 2015) and the Operational Risk: Paper of the Year (see de Jongh et al. 2016). The second paper recently won the RGA Prize from the Actuarial Society of South Africa and the Sichel medal from the South African Statistical Association for the best published research in 2015.

Boersma, F.K., Reinecke, C.J & Gibbons, M. 2008. Organising the university- industry relationship: A case study of research policy and curriculum restructuring at the North-West University in South Africa. Tertiary Education and Management, 14(3):209-226.

De Jongh, P.J. & Erasmus, C.M. 2014. Industry-directed training and research programmes: The BMI experience. South African Journal of Science, 10(11/12):17-24.

De Jongh, P.J., De Wet, T., Panman, K. & Raubenheimer, H. 2016. A simulation comparison of quantile approximation techniques for compound distributions in Operational Risk. Journal of Operational Risk, 11(1):23-48.

Venter, J.H. & De Jongh, P.J. 2004. Risk Estimation using the Normal Inverse Gaussian Distribution. (In Jorion, P., ed. Innovations in Risk Management: Seminal papers of the Journal of Risk. London: Riskwaters Publ.).

Venter, J.H. & De Jongh, P.J. 2007. Selecting an innovation distribution for Garch models to improve efficiency of risk and volatility estimation. (In Danielson, J., ed. The Value-at-Risk Reference: Key issues in the implementation of market risk. London: Incisive Media).

Operational Risk: Paper of the year 2016:Kevin Panman (BMI PhD) and Helgard Raubenheimer (Centre for BMI) received the award in London, United Kingdom.

12

SELECTED RESEARCH PAPERS BY THE CENTRE FOR BMI

Asset and liability managementRaubenheimer, H. & Kruger, M.F. 2010. Generating interest rate scenarios for fixed income portfolio optimisation. South African Actuarial Journal, 10:43-70.

Raubenheimer, H. & Kruger, M.F. 2010. A stochastic programming approach to integrated asset and liability management of insurance products with guarantees. South African Actuarial Journal, 10:1-42.

Raubenheimer, H. & Kruger, M.F. 2010. A stochastic programming approach to managing liquid asset portfolios. Kybernetika, 46(3): 536-547.

Investment riskDe Jongh, P.J., De Wet, T. & Cloete, G.S. 2002. Combining Vasicek and Robust Estimators for Forecasting Systematic Risk. Investment Analysts Journal, 31(55):37- 44.

Du Plessis, J.L. & Swanepoel, J.W.H. 2002. An analysis of financial ratios of listed South African industrial companies. Management Dynamics, 11(1):7.

Mashele, H.P., Terblanche, S.E. & Venter, J.H. 2013. Pairs trading on the Johannesburg Stock Exchange. Investment Analysts Journal, 42(78):17-30.

Sonono, M.E. & Mashele, H.P. 2013. Assessing the risks of trading strategies using acceptability Indices. Journal of Mathematical Finance, 3(4):465-475.

Terblanche, S.E. & Venter, J.H. 2015. Profitability of short term reversal strategies on the JSE. Studies in Economics and Econometrics, 39(3):1-25.

Venter, J.H. 2008. The profitability of CFD trading of the JSE. Investments Analysts Journal, 37(67):37-347.

Venter, J.H. 2009. Intra-day momentum and contrarian effects on the JSE.Investment Analysts Journal, 38(70):47-59.

Venter, J.H. & De Jongh, D.C.J. 2006. Extending the EKOP model to estimate the probability of informed trading. Studies in Economics and Econometrics, 30:25-39.

Venter, J.H. & De Jongh, D.C.J. 2006. Further extensions of the EKOP model.Studies in Economics and Econometrics, 30:25-39.

Van Vuuren, G, and Yacumakis, R. 2015. Hedge fund performance evaluation using the Kalman filter. J. Stud. Economentrics, 39(3), 1-23

13

Market riskDe Jongh, P.J. & Venter, J.H. 2015. A framework for normal mean variance mixture innovations with application to GARCH modeling. South African Statistical Journal, 49(2):139-152.

Elllis, S.M., Steyn, H.S. & Venter, J.H. 2003. Fitting a Pareto-Normal-Pareto distribution to the residuals of financial data. Computational Statistics, 18(3):477- 491.

Pagel, I.M., De Jongh, P.J. & Venter, J.H. 2007. An introduction to realized volatility. Investment Analysts Journal, 36(65):47-57.

Venter, J.H. & De Jongh, P.J. 2002. Risk Estimation using the Normal Inverse Gaussian Distribution. The Journal of Risk, 4(2):1-23.

Venter, J.H. & De Jongh, P.J. 2004. Selecting an innovation distribution for Garch models to improve efficiency of risk and volatility estimation. The Journal of Risk, 6(3):27-52.

Venter, J.H. De Jongh, P.J. & Griebenow, G. 2005. NIG-GARCH models based on open, close, high and low prices. South African Statistical Journal, 39(2):79-102.

Venter, J.H., De Jongh, P.J. & Griebenow, G. 2004. GARCH-type volatility models based on Brownian inverse Gaussian intraday return processes. The Journal of Risk, 8(4):97-116.

Venter, J.H. & De Jongh, P.J. 2014. Extended stochastic volatility models incorporating realised measures. Computational Statistics and Data Analysis, 76:687– 707.

Credit riskDe Jongh, E., De Jongh, P.J., Grant Gordon, H., Oberholzer, M., Pienaar, M. & Santana, L. 2015. The impact of pre-selected VIF thresholds on the stability and predictive power of logistic regression models in credit scoring. Orion, 31(1):17-36.

De Jongh, P.J., Joubert, M., Reynolds, E., Verster, T. & Raubenheimer, H. 2017. A critical review of the Basel margin of conservatism requirement in a retail credit context. Submitted for publication.

Terblanche, S.E. & De la Rey, T. 2014. Credit Price Optimisation within Retail Banking. Orion, 30(2):85-102.Venter, J.H. & De la Rey, T. 2007. Detecting outliers using weights in logistic regression. South African Statistical Journal, 41(2):127-161.

Van Dyk, J.; Lange, J. & van Vuuren, G. 2017. The Impact of systemic loss given default on economic capital.

International Business and Economics Research Journal, 15(6), 1-14.

Operational riskDe Jongh, E., De Jongh, P.J., De Jongh, D.C.J. & Van Vuuren, G. 2013. A review of operational risk in banks and its role in the financial crisis. South African Journal of Economic and Management Sciences, 16(4):364-382.

De Jongh, P.J., De Wet, T., Raubenheimer, H. & Venter, J.H. 2015. Combining scenario and historical data in the loss distribution approach: A new procedure that incorporates measures of agreement between scenarios and historical data. Journal of Operational Risk, 10(1):1- 31.

De Jongh, P.J., De Wet, T., Panman, K. & Raubenheimer, H. 2016. A simulation comparison of quantile approximation techniques for compound distributions in Operational Risk. Journal of Operational Risk, 11(1):23-48.

Panman, K., Haasbroek, L.J. & Pieters, W.D. 2016. A simulation comparison of aggregation periods for estimating correlations within operational loss data. Journal of Operational Risk, 11(2), 69-86.

Enterprise Risk ManagementBurra, P., De Jongh, P.J., Raubenheimer, H., Van Vuuren, G. & Wiid, H. 2015. Implementing the countercyclical capital buffer in South Africa: Practical considerations. South African Journal of Economic and Management Sciences, 18(1):1-13.

De Jongh, P.J., Larney, J., Maré, E., Van Vuuren, G. & Verster, T. 2017. A proposed best practice model validation framework for banks. Accepted for publication in South African Journal of Economic and Management Sciences.

Fourie, E., Styger, P., De la Rey, T. & Van Vuuren, G. 2013. Review of subnational credit rating methodologies and the applicability in the South African context. Politeia, 32(3):74-99.

Van Biljon. L. & Haasbroek, L.J. 2017. A practical maturity assessment method for model risk management in banks. Accepted for publication in the Journal of Risk Model Validation.

Van Vuuren, Gary & De Jongh, Riaan. 2016. A comparison of risk aggregation estimates using copulas and Fleishman distributions. Applied Economics, 49 (17), 1715-1731, DOI: 10.1080/00036846.2016.1223832.Venter, J.H. & Styger, P. 2009. Structural default models applied to South African banks. Journal for Studies in Economics and Econometrics, 32(1):1-21.

14

“SAS Institute believes that the world leading programmes at BMI deliver superior professionals to our customers. The core of this success is found in the quality of their students, teaching and leadership.”

Murray de VilliersGeneral Manager: Middle East & Africa Regional Academic Programme

Director Centre for BMIPJ de JonghTel: 018 299 2585Cell: 082 905 0880Email: [email protected]

SecretaryC KlaassenTel: 018 299 2575Email: [email protected]

Head: SAS Lab and BMI Professional Masters ProgrammesH RaubenheimerTel: 018 299 2565Email: [email protected]

Public Relations and Marketing ManagerM GeldenhuysTel: 018 299 2581Email: [email protected]

Visit the Centre for BMI’s website, www.nwu.ac.za/bmi, for more information, videos and other marketing material.

CONTACT DETAILS