the cfo act and federal financial management: the end of ... · foreword this year marks the...

TRANSCRIPT

IBM Business Consulting Services

May 2005

The CFO Act and Federal Financial Management: The End of the Beginning

© Copyright IBM Corporation 2005. All Rights Reserved IBM and the IBM logo are registered trademarks of International Business Machines Corporation in the United States, other countries, or both.

Foreword

This year marks the fifteenth anniversary of the Chief Financial Officer’s Act, which permanently transformed financial management in the federal government. Since passage of the Act, federal departments and agencies have made sweeping changes in how they manage public resources with varying degrees of success. During this time, they have also been confronted with demands for greater fiscal accountability and transparency. At this critical stage in the evolution of the CFO Act, it is important to learn from the past and to take further steps to improve in the future.

This paper highlights the many accomplishments and lessons learned from the past fifteen years and offers a series of strategies to further improve how federal departments and agencies do business. On behalf of IBM Business Consulting Services, we are pleased to present this paper as a knowledge resource for federal CFOs and other financial managers as they look to improve financial performance at their agencies and contribute to the government-wide effort to manage public resources effectively and efficiently.

George Cruser, CPA Steve Watson, CPA, CGFM Vice President and Partner Partner Public Sector Financial Management Public Sector Financial Management IBM Business Consulting Services IBM Business Consulting Services [email protected] [email protected]

Federal Financial Management: The End of the Beginning Page i

Table of Contents

The CFO Act and Federal Financial Management: The End of the Beginning ...............1

The CFO Act, Landmark Legislation ...............................................................................3

Role of the Federal CFO.................................................................................................9

Strategies for Becoming a Successful Federal CFO.....................................................10

Strategy 1: Integrate Planning Budgeting and Performance .....................................11

Strategy 2: Secure Confidence and Trust among Stakeholders ...............................14

Strategy 3: Have Fresh, Accurate Financial Information on Demand .......................23

Strategy 4: Operate a Lean, Efficient Financial Organization....................................30

Looking Ahead ..............................................................................................................44

List of Tables and Figures

Levels of Financial Management Maturity .................................................................................... 2

History of Financial Management Legislation ............................................................................... 4

Summary of Agency Fiscal Year 2004 Financial Status............................................................... 8

Four Key Strategies for a Successful Federal CFO.................................................................... 10

Cumulative PART Results by Ratings Category (2004-2006) .................................................... 13

Fiscal Year 2004 Material Weaknesses Summary Chart ........................................................... 15

Comparison of Private and Federal Sector Internal Control Requirements................................ 20

Cost Information Usefulness vs. Discretionary Decision Making................................................ 25

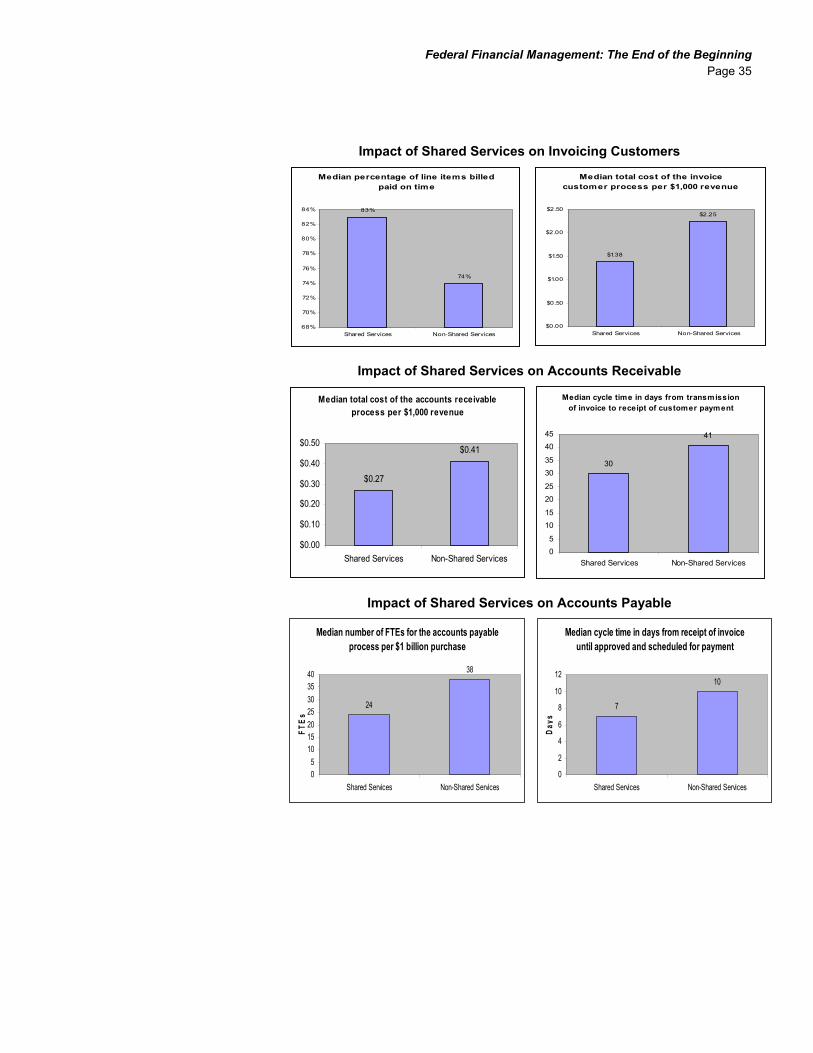

Impact of Shared Services on Invoicing Customers ................................................................... 35

Impact of Shared Services on Accounts Receivable .................................................................. 35

Impact of Shared Services on Accounts Payable....................................................................... 35

Impact of Shared Services on General Accounting .................................................................... 36

Outsourcing vs. Retaining Accounting Functions ....................................................................... 36

The Evolution of the Finance Function ....................................................................................... 38

Twelve Steps to a More Efficient Finance Function.................................................................... 41

Federal Financial Management: The End of the Beginning Page ii

This page intentionally left blank.

Federal Financial Management: The End of the Beginning Page 1

The CFO Act and Federal Financial Management: The End of the Beginning

Winston Churchill was not referring to the status of financial management when he uttered this phrase in 1942. His words, however, provide a fitting characterization of the status of financial management in the federal government today. There has been clear progress, and the current fifteen year anniversary of the Chief Financial Officers (CFO) Act is a good time to recognize the many accomplishments within federal financial management.

Efforts will continue to be expended to realize the full potential of federal financial management. Challenges and issues continually sprout. Greater transparency, enhanced accuracy, more complete accountability, and more timely delivery of data and reports---these are just some of the demands facing the federal CFO (as well as his or her private sector counterpart). The federal financial management community—the user, customer, and stakeholder— recognizes the struggles and gains of the past, acknowledges the progress in addressing the issues of today, is mindful of, and prepares for, the challenges and opportunities of the future, and, most importantly, looks to the federal CFO to continue to lead, to direct, to resolve, and to grow.

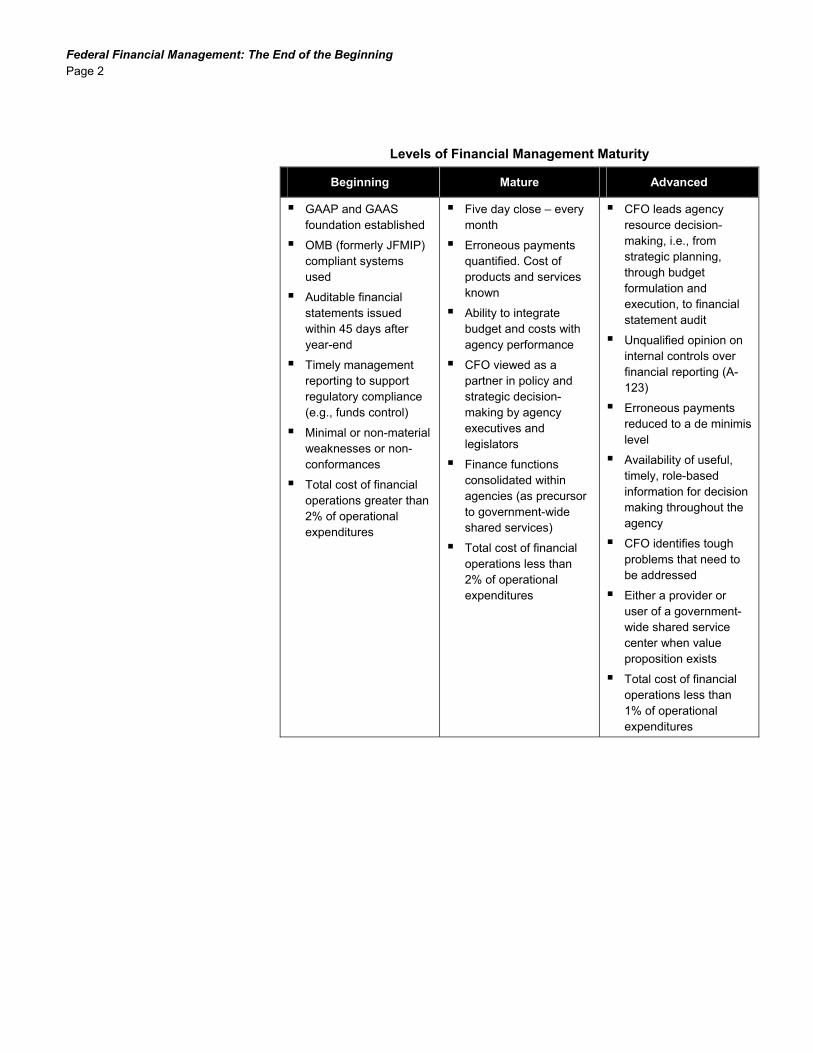

This whitepaper provides an overview of the CFO Act and highlights the many accomplishments that have been achieved since its passage. It then offers a series of actions that newly appointed and seasoned CFOs can take to improve financial management in their agencies. The following chart groups financial management capabilities into three levels of maturity – beginning, mature and advanced. Most agencies have completed the beginning phase, and while some have implemented aspects of a mature or even advanced system in some areas, most have not. Our recommended actions will help financial managers advance financial management and become true partners in helping our legislators and agency executives better manage our public resources.

“Now this is not the end. It’s not even the beginning of the end. But what it is, perhaps, is the end of the beginning.”

Winston Churchill

Federal Financial Management: The End of the Beginning Page 2

Levels of Financial Management Maturity

Beginning Mature Advanced

GAAP and GAAS foundation established

OMB (formerly JFMIP) compliant systems used

Auditable financial statements issued within 45 days after year-end

Timely management reporting to support regulatory compliance (e.g., funds control)

Minimal or non-material weaknesses or non-conformances

Total cost of financial operations greater than 2% of operational expenditures

Five day close – every month

Erroneous payments quantified. Cost of products and services known

Ability to integrate budget and costs with agency performance

CFO viewed as a partner in policy and strategic decision-making by agency executives and legislators

Finance functions consolidated within agencies (as precursor to government-wide shared services)

Total cost of financial operations less than 2% of operational expenditures

CFO leads agency resource decision-making, i.e., from strategic planning, through budget formulation and execution, to financial statement audit

Unqualified opinion on internal controls over financial reporting (A-123)

Erroneous payments reduced to a de minimis level

Availability of useful, timely, role-based information for decision making throughout the agency

CFO identifies tough problems that need to be addressed

Either a provider or user of a government-wide shared service center when value proposition exists

Total cost of financial operations less than 1% of operational expenditures

Federal Financial Management: The End of the Beginning Page 3

The CFO Act, Landmark Legislation

The CFO Act represents a historical milestone in shaping financial management in the federal government. Prior to the CFO Act, two governing provisions dominated the financial landscape – the Constitution itself which established the appropriations process and the Anti-Deficiency Act.

To ensure a balance of power in the newly formed government, the Constitution in 1789 provided Congress with the power of the purse, specifically stating:

…no money shall be drawn from the Treasury but in the consequence of an appropriation made by law.

The 1789 Constitution was the primary governing provision in financial management until passage of the Budget and Accounting Act of 1921, except for a few exceptions around the turn of the twentieth century. In 1870, the legislative appropriations bill was the vehicle for a number of reforms relating to appropriations practices, including the section later known as the Anti-Deficiency Act. Specifically, the Anti-Deficiency Act (1906) stated that no agency shall:

…make or authorize an expenditure or obligation exceeding an amount available in an appropriation or fund for the expenditure or obligation.

Building upon the early Anti-Deficiency Acts, the Budget and Accounting Act of 1921 was enacted in response to the consensus that developed shortly after the turn of the century that a more centralized approach to financial policy and processes was needed, in both the executive and legislative branches. The 1921 Act codified the submission of the President's budget and created the Bureau of the Budget (the predecessor to the Office of Management and Budget (OMB)) to oversee the executive budget process. This Act also established the General Accounting Office (the predecessor to the Government Accountability Office (GAO)) as the government's auditor, responsible only to Congress. The mission of GAO was to provide Congress with an independent audit of executive accounts and to report on violations of the fiscal statutes.

The following table summarizes the changes to federal financial management operations from the Constitution to passage of the CFO Act.

Federal Financial Management: The End of the Beginning Page 4

History of Financial Management Legislation Year Legislation Impact

1789 The Constitution Gives Congress the power to levy taxes and requires appropriations by Congress before funds are disbursed

1802-67 Committee Structure

House Ways and Means Committee established as standing committee in 1802. House Appropriations Committee established in 1865. Senate Finance Committee established in 1816. Senate Appropriations Committee in 1867

1837, 1850 House and Senate Rules

House and Senate bar unauthorized appropriations

1870, 1905-1906 Anti-Deficiency Act Requires apportionment of funds to prevent over expenditure

1921 Budget and Accounting Act

Requires the President to send a comprehensive executive budget; established the Bureau of the Budget and the GAO.

1939 Reorganization Plan #1

Transfers the Bureau of the Budget to the new Executive Office of the President and expands the Bureau’s role.

1967 President’s Commission on Budget Concepts

Adoption of the unified budget, including trust funds

1974 Congressional Budget and Impoundment Control Act

Establishes the Congressional budget process, House and Senate Budget Committees, and the Congressional Budget Office (CBO). Establishes procedures for legislative review of impoundment of funds.

1980 Reconciliation Process

Reconciliation used for the first time at the start of the Congressional budget process.

1982 Federal Managers' Financial Integrity Act

Requires on-going evaluations and reports on each agency's system of internal controls so as to provide assurance that obligations and costs are in compliance with law

1985, 1987 Gramm-Rudman-Hollings Act

Set deficit reduction targets and sequestration procedures.

1990 Budget Enforcement Act

Shifts from fixed to adjustable deficit targets, caps discretionary spending, establishes “pay-as-you-go” rules for revenues and direct spending, and establishes new budgeting rules for direct and guaranteed loans.

1990 Chief Financial Officers Act

Provides for a CFO in all major agencies to oversee financial management and integrate accounting and budgeting.

Source: The Federal Budget, Politics, Policy, and Process by Allen Schick, Table 3-3; Thomas.loc.gov; OMB.gov

Federal Financial Management: The End of the Beginning Page 5

The focus of financial management before the CFO Act was fairly simple. Systems were established to track appropriations and apportionments, obligations made, and funds remaining to ensure that agency obligations remained within the authorized funding. This process is referred to as funds control.

Limited focus on funds control resulted in limited visibility into federal assets and liabilities. Federal assets and liabilities (liabilities, commitments, and obligations, for example, amounted to $43 trillion at the end of fiscal year 20041) were not accounted for on the government’s books. The government also generally did not know the cost of goods and services it provided each year or what value it received for its expenditures. Further, except for audits of small portions of government activities, audits of financial information were not performed. Generally, financial information was not accurate or useful, and, as a result, was perceived to be of little value. Accounting was a back-office function only receiving attention when instances of fraud, waste, abuse or mismanagement came to public attention.

Passage of the 1990 CFO Act dramatically changed the landscape of federal financial management by knitting the budget and accounting functions together and centralizing all financial management functions at the department or agency level. It created CFO positions in the major agencies. For most of the major agencies, the CFO is to be a presidential appointee and is to be assisted by a Deputy CFO. Both are required to have extensive financial management experience.

With the CFO reporting directly to the agency head, the role of government financial managers was elevated to a level comparable to their counterparts in the private sector. The CFO Act also established that the Deputy Director for Management within OMB would assume CFO responsibilities for the entire executive branch and that a controller position be established within OMB to assist the Deputy Director in carrying out assigned financial management duties.

Within an agency, the CFO Act assigns responsibility to the CFO for all financial management activities relating to the programs and operations of the agency including;

Developing and maintaining an integrated agency accounting and financial management system which is responsive to the financial information needs of agency management;

Developing and reporting cost information; Systematic measurement of performance; Reviewing fees, royalties, rents, and other agency charges for goods and

services on a routine basis to ensure that such charges are reasonable based on incurred costs;

Developing agency financial management budgets; Recruiting, selecting, and training financial personnel, including

recommendations to the agency head regarding selection of the Deputy CFO;

1 GAO Report 05-248T, “Fiscal Year 2004 US Government Financial Statements, Sustained Improvement in

Federal Management Is Critical to Addressing Out Nation’s Future Fiscal Challenges,” p.4.

Federal Financial Management: The End of the Beginning Page 6

Monitoring the financial execution of the budget of the agency in relation to actual expenditures; and

Maintaining a five-year plan to achieve the Act’s requirements and comply with requirements prescribed by OMB.

The CFO Act also established a CFO Council, chaired by the OMB Deputy Director for Management. The Council was designed to coordinate financial activities of the agencies on matters requiring cross-government attention such as consolidation and modernization of financial systems, improved quality of financial information, financial data and information standards, internal controls, and legislation affecting financial operations and organizations.

The CFO Act mandated the performance of annual financial statement audits of pilot agencies, expanded to all large agencies by the Government Management Reform Act (GMRA) of 1994 and to smaller agencies by the Accountability of Tax Dollars Act of 2002. Each agency’s Office of the Inspector General (OIG) is responsible for the audit, unless the agency is audited by the GAO. In many cases, the OIGs contract the financial statement audits to public accounting firms.

The CFO Act also led to the development of the Federal Accounting Standards Advisory Board (FASAB) in October 1990 to define Generally Accepted Accounting Principles (GAAP) for federal reporting, a cornerstone for achieving the Act’s objectives. Lastly, the CFO Act spawned other helpful legislation designed to improve federal financial management, including the:

Government Management Reform Act (GMRA) of 1994, which set further guidelines for financial management, including the preparation of annual financial statements, streamlining management control, human resource management, and pay adjustments.

Federal Financial Management Improvement Act (FFMIA) of 1996, which built on the foundation laid by the CFO Act by emphasizing the need for agencies to have systems that can generate reliable, useful, and timely information with which to make better informed decisions and to ensure accountability on an ongoing basis. FFMIA requires Inspectors General to report on whether the financial management systems of their agencies are compliant with federal requirements pertaining to accounting and the standard general ledger.

Clinger-Cohen Act of 1996, which established a comprehensive approach for agencies to improve the acquisition and management of their information resources by focusing information resource planning to support their strategic missions; implementing a capital planning and investment control process that links to budget formulation and execution; and rethinking and restructuring the way they do their work before investing in information systems. This Act also established agency Chief Information Officers (CIOs) and entrusted them with financial systems responsibilities.

Federal Financial Management: The End of the Beginning Page 7

By and large, starting with the CFO Act, recent financial management legislation has focused more on government reform particularly government finances; measuring the effects of federal deficits on the economy; applying private sector financial standards and processes to the federal sector; aligning spending and performance; reducing the size of government; and competing federal functions that are commercial in nature. Consequently, federal financial management was elevated to a more sophisticated platform.

CFOs had to replace outmoded and inefficient financial management systems; implement internal controls and standard processes and procedures; enhance the capabilities of their financial management staff; produce clean financial statements; and mature their role from mere invoice processing to value-added financial analysis. In some agencies (but not all), CFOs are responsible for the entire financial processes of the agency, i.e., from planning, budgeting, and performance measure setting to the daily accounting for resources, and finally, to the production and audit of annual financial statements. It was, and is, a significant change, a radical leap into a future that was largely modeled after the private sector.

The agencies stepped up to meet the challenge, albeit at varying paces and levels of sophistication. As shown in the following table, by the end of fiscal year 2004, 17 of the 24 large federal agencies have improved financial operations sufficiently to receive an unqualified opinion on their financial statements. Six agencies have received a green score in the areas of financial management and seven agencies have received a green score on budget and performance integration, the highest ratings issued by OMB under the President’s Management Agenda (See left side bar). An additional three agencies have received yellow scores in financial management and 14 agencies have received yellow scores for budget and performance integration, an indicator of improvement.

President’s Management Agenda (PMA)The PMA is an ongoing effort in the executive branch for “improving management and performance in the federal government.” One of the government-wide initiatives of the PMA is improved financial performance, which seeks to enhance the quality and timeliness of financial information available to the agencies and Congress. Other facets of the PMA involve improving assets management, reducing improper payments, and strengthening controls over federal charge cards.The PMA scorecard uses a traffic light motif of green for success, yellow for mixed results, and red for unsatisfactory. For each initiative, there are multiple “standards for success,” or core criteria which an agency must meet in order to get a green rating. The four core criteria for “getting to green” on the improving financial performance initiative are:1. Financial management

systems meet federal financial management system requirements and applicable federal accounting and transaction standards as reported by the agency head;

2. Accurate and timely financial information;

3. Integrated financial and performance management systems supporting day-to-day operations; and

4. Unqualified and timely audit opinions on the annual financial statements and no material internal control weaknesses.

Federal Financial Management: The End of the Beginning Page 8

Summary of Agency Fiscal Year 2004 Financial Status

President’s

Management Agenda2

Agency FY 2004

Audit Opinion

FY 2004 No. of

Material Weaknesses

Financial Performance

Budget/ Performance Integration

Agriculture Unqualified 2 Red Yellow

Commerce Unqualified 0 Yellow Yellow

Defense Disclaimer 11 Red Yellow

Education Unqualified 0 Green Yellow

Energy Unqualified 0 Green Green

EPA Unqualified 0 Green Yellow

HHS Unqualified 2 Red Yellow

DHS3 Disclaimer 10 Red Yellow

HUD Disclaimer 3 Red Red

Interior Unqualified 4 Red Red

Justice Disclaimer 2 Red Yellow

Labor Unqualified 0 Green Green

State Unqualified 0 Yellow Green

DOT Unqualified 4 Red Green

Treasury Unqualified 1 Red Yellow

VA Unqualified 2 Red Yellow

USAID Unqualified 1 Red Yellow

GSA Unqualified 0 Red Yellow

NASA Disclaimer 4 Red Green

NRC Unqualified 1 Not reported Not reported

NSF Unqualified 0 Green Yellow

OPM Unqualified 1 Yellow Yellow

SBA Qualified 2 Red Green

SSA Unqualified 0 Green Green

2 Scorecard ratings for the President’s Management Agenda are as of September 30, 2004.

3 DHS was not a CFO Act Agency in fiscal year 2004; however DHS prepared and submitted audited financial

statements. For fiscal year 2005, DHS is a CFO Act Agency.

Federal Financial Management: The End of the Beginning Page 9

Role of the Federal CFO

A federal CFO, like his or her private sector counterpart, should:

Be the financial counsel to the agency head; Maintain responsibility and be held accountable for all financial

management activities and programs of the agency, including planning and budgeting;

Provide input into all financial decisions; Provide insightful analysis into on-going and prospective programs; and Have the capability and access to bring issues of a financial nature to the

attention of the agency head.

For some agencies, this is the goal and not necessarily the reality. Many federal agencies continue to struggle with implementing FFMIA-compliant financial systems, securing clean financial statement audits, and earning a “green” score for financial management on OMB’s scorecard for the PMA. The magnitude of difficulty in succeeding in these endeavors is immense. Accounts must be reconciled, years of errors corrected, systemic deficiencies resolved, erroneous payments reduced, and internal controls strengthened, particularly surrounding bankcards and procurements of goods and services. Moreover, staff capabilities must be enhanced and accounting clerks may need to be replaced by accountants.

In the beginning stages of financial management, the CFO will find himself or herself totally immersed in these basic but extremely critical issues. Until the agency has a financial management system, processes, and procedures that work and that produce clean financial information, the CFO is unlikely to have the time or ability to focus on analysis, forecasting, alternative methods of doing business, and being the omnibus financial counselor to the agency head.

Lack of Clarity for CFO Roles and Responsibilities CFO oversight responsibilities vary from agency to agency. CFOs are responsible for financial management activities of the agency, yet not all CFOs are responsible for budgeting and planning. Similarly, implementation of financial management systems may be shared with the agency CIO. Moreover, in some agencies, the CFOs are also responsible for many other agency activities including human resources, asset management, procurement, facilities, bankcards, and general administration in addition to financial management. In some agencies, the CIO also reports to the CFO. In other words, there are no clear standards for federal CFO responsibilities.

Federal Financial Management: The End of the Beginning Page 10

Strategies for Becoming a Successful Federal CFO

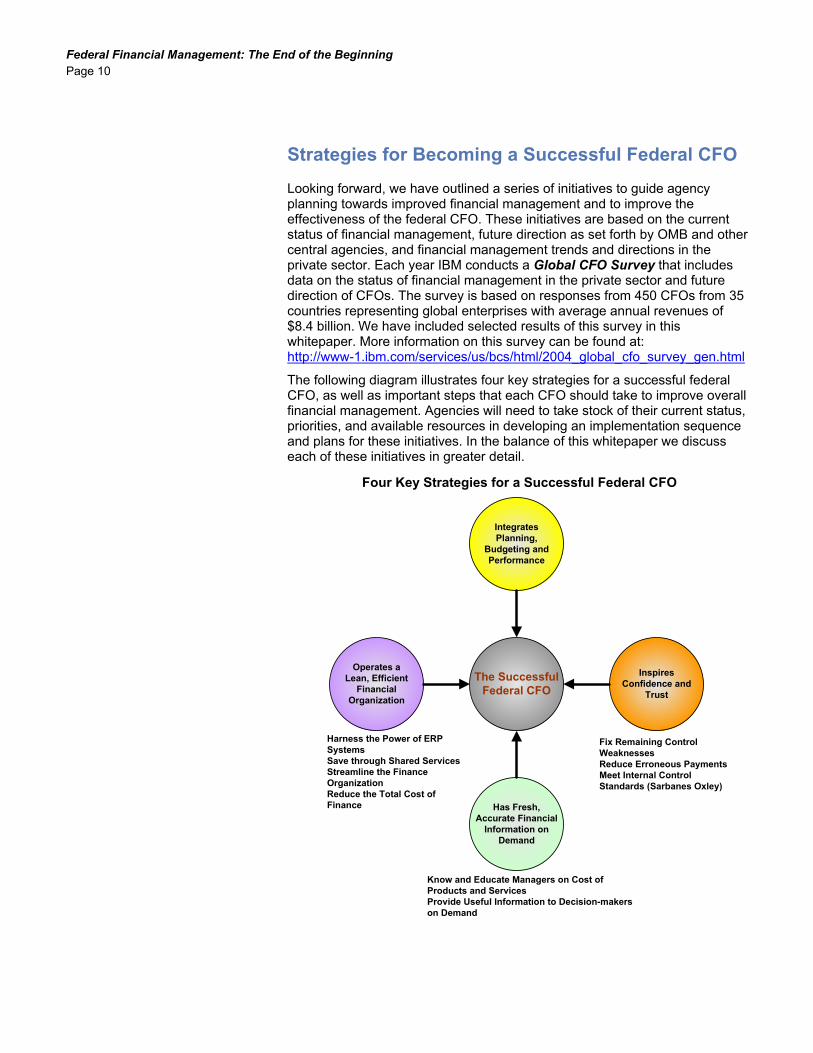

Looking forward, we have outlined a series of initiatives to guide agency planning towards improved financial management and to improve the effectiveness of the federal CFO. These initiatives are based on the current status of financial management, future direction as set forth by OMB and other central agencies, and financial management trends and directions in the private sector. Each year IBM conducts a Global CFO Survey that includes data on the status of financial management in the private sector and future direction of CFOs. The survey is based on responses from 450 CFOs from 35 countries representing global enterprises with average annual revenues of $8.4 billion. We have included selected results of this survey in this whitepaper. More information on this survey can be found at: http://www-1.ibm.com/services/us/bcs/html/2004_global_cfo_survey_gen.html

The following diagram illustrates four key strategies for a successful federal CFO, as well as important steps that each CFO should take to improve overall financial management. Agencies will need to take stock of their current status, priorities, and available resources in developing an implementation sequence and plans for these initiatives. In the balance of this whitepaper we discuss each of these initiatives in greater detail.

Four Key Strategies for a Successful Federal CFO

IntegratesPlanning,

Budgeting andPerformance

InspiresConfidence and

Trust

Operates aLean, Efficient

FinancialOrganization

Has Fresh,Accurate Financial

Information onDemand

The SuccessfulFederal CFO

Fix Remaining ControlWeaknessesReduce Erroneous PaymentsMeet Internal ControlStandards (Sarbanes Oxley)

Know and Educate Managers on Cost ofProducts and ServicesProvide Useful Information to Decision-makerson Demand

Harness the Power of ERPSystemsSave through Shared ServicesStreamline the FinanceOrganizationReduce the Total Cost ofFinance

Federal Financial Management: The End of the Beginning Page 11

Strategy 1: Integrate Planning, Budgeting and Performance The 18 month federal budget process, preceded by strategic and long-range planning, and integrated with agency performance measures, is where policy and strategic decisions are made in the federal government. Actions, events and issues associated with financial accounting follow the budget process and are literally an “accounting” of how plans, budgets, and performance measures are or were realized. The federal budget process is forward looking and includes visioning, planning, strategizing, proposing solutions, and building futures. The fully positioned federal CFO must be a leader of or, at the very least, a major player in, the agency’s planning, budgeting, and performance programs and activities

Planning before Budgets Strategic and long-range planning are critical components of the effective federal budget process. Federal budgets were often formulated without the benefit of formal planning processes. The new budget request was frequently an incremental adjustment to the prior year request, i.e., increased for inflation, responsive to new legislation when applicable, and, perhaps, addressing new issues. The federal budget was the statement of the agency on how programs would be conducted, legislation would be implemented, issues would be addressed, and how much all of these programs would cost the citizen in terms of dollars and numbers of employees.

In the private sector, stockholders held management and the board of directors responsible for the “bottom line,” i.e., profits. Within the federal government, agency “stockholders,” i.e., the President, the Congress, and the taxpaying citizen, demanded to know the value, the worth, and the results from the investments of their hard-earned tax dollars. Congress passed legislation and the executive branch issued directives demanding results from taxpayer investments. Thus, the pressure was on for federal agencies to plan their future, and not just simply reinvent their “tried and true” budgets each year.

Agencies embarked on long-range, strategic planning that set program visions, missions, goals, and objectives. Agencies struggled to define missions, goals and objectives that were not only meaningful, but were also measurable. Imagine the difficulty in setting a handful of goals that meaningfully captured the essence of the mission and myriad of programs of large federal agencies such as Health and Human Services. Agencies struggled then, and still struggle today, in defining and refining their mission, goals, and objectives. But today, budgets more fully reflect prior planning efforts.

The CFO’s Role in the Federal Budget Process Throughout the internal agency budget formulation process, the CFO is a lead player. The CFO provides overall direction, leads the planning process, receives the program manager requests and undertakes preliminary analyses, defines and leads the decision-making process, and assumes responsibility for the production of the agency budget request. The CFO advises on which budget proposals best fulfill agency goals and objectives, proposes refinements to resource needs and associated measures, advises on which budgetary initiatives are most likely to secure the agreement of the President and the Congress, and projects current and future year costs of each program.

Federal Financial Management: The End of the Beginning Page 12

As the agency budget proceeds through the levels of review, i.e., the department, OMB, and the Congress, the CFO should be out-front—selling the budget, justifying changes, responding to questions, and adjusting the budget as necessary. The CFO supports the agency head in all formal meetings and hearings, and represents the agency in other arenas.

Upon enactment of the appropriations bill and/or receipt of revenues, the CFO executes the budget. Apportionments are requested, spending plans are entered into the financial system, warrants are received, and spending occurs. As the year progresses, the CFO may respond to requests for reprogramming of funds, supplemental appropriations, and rescission of funds. The CFO monitors commitments, obligations, and disbursements of funds to insure that funds are expended for the purposes intended, that expenditures fulfill performance measures and that performance goals are met, and that the agency fulfills all of its fiduciary responsibilities.

Aligning Budget and Performance Federal programs are increasingly pressed to ensure that programs deliver results. Because of the deepening federal deficit, there is great pressure to squeeze savings out of the budget by cutting poorly-performing programs. To address a rapidly approaching budget crisis, Comptroller General David M. Walker of the GAO states that the federal government must: Adopt new approaches to accounting and reporting and new budget

control mechanisms to consider the long-term implications of spending and tax policies.

Develop ways to measure the effectiveness of federal programs over the long run.

Re-examine the base of current federal activity, and question the need for, or adequacy of, existing programs and policies.

Since the passage of the Government Performance and Results Act of 1993, federal managers and CFOs have refined techniques for measuring whether programs work as intended and thus provide administration officials and members of Congress with the information needed to efficiently allocate scarce resources. President Bush has made the integration of an agency’s budget and performance one of five4 key measures of the President’s Management Agenda (PMA). In the most recent PMA scorecard of December 31, 2004, only eight of the 26 agencies regularly evaluated earned a “green” score for integration of budget and performance.

To better promote the administration’s management initiative aimed at connecting budget decisions to program performance, OMB developed and implemented the Program Assessment Rating Tool (PART). The PART questionnaire evaluates agency programs and assigns programs one of five ratings: effective, moderately effective, adequate, results not demonstrated, or ineffective. Through the fiscal year 2006 budget cycle, OMB has evaluated 60 percent of all agency programs. Of the 607 programs assessed through the fiscal year 2006 cycle, 71 percent have defined and are tracking clear outcome goals to measure their results and 59 percent have efficiency measures in

4 The other four critical elements of the PMA are Human Capital, Competitive Sourcing, Financial Performance,

and E-Government.

Federal Financial Management: The End of the Beginning Page 13

place to manage costs. PART evaluation results are summarized in the following table.

Cumulative PART Results by Ratings Category (2004-2006)

Ratings/Year FY 2004 FY 2005 FY 2006

Number of Programs 234 407 607

Effective 6% 11% 15%

Moderately Effective 24% 26% 26%

Adequate 15% 20% 26%

Ineffective 5% 5% 4%

Results Not Demonstrated 50% 38% 29%

While federal agencies focus on program reviews and assessments, the Congress is struggling to balance the program evaluations with traditional budget oversight. Administration officials are working closely with Congress to provide better understanding of PART and its utility in the budget process. Rep. Todd Platts, chairman of the House Government Management, Finance and Accountability Subcommittee, convened hearings on budget and performance integration and introduced legislation in the last session of Congress that would require future administrations to continue performing PART-like program analyses. The bill was subsequently voted out of committee to the House in March 2005.

So, what does all this imply for the federal CFO? Like their private sector counterparts, CFOs must be prepared to deliver results for the investments of their agency’s stakeholders. While profit is not a requirement, effectiveness, efficiency, and customer satisfaction are requirements. The successful CFO will ensure that the programs of his or her agency can deliver results.

Federal Financial Management: The End of the Beginning Page 14

Strategy 2: Secure Confidence and Trust among Stakeholders One of the responsibilities of the federal CFO is to maintain the confidence and trust from U.S. taxpayers by ensuring that the agency’s financial systems and procedures adhere to federal accounting standards and properly account for the expenditure of agency funds. Federal agencies have made significant progress since the passage of the CFO Act in securing and maintaining clean (unqualified) financial statement audit opinions. Yet in 2005, there are agencies that have yet to secure an unqualified opinion and others that have lost that designation. Material weaknesses and reportable conditions exist and must be resolved. Erroneous payments—whether over-payments or under-payments—remain a major issue in many federal agencies, particularly those that provide large federal subsidies, grants and loans. Goals are now set by each agency to reduce the numbers and associated dollar amounts of erroneous payments. Internal controls, long a focus among federal CFOs, are receiving added attention as OMB revised its Circular A-123 to incorporate relevant sections of the Sarbanes-Oxley Act (SOX). Just as the private sector CFO attests to the accuracy and completeness of the organization’s financial statements, so, too, is the federal CFO under scrutiny to ensure that strong internal controls are maintained throughout the agency.

In the following sections, we describe three actions that CFOs can take to help inspire the confidence and trust from U.S. taxpayers:

Fix remaining control weaknesses Reduce erroneous payments Meet internal control standards (i.e. Sarbanes-Oxley)

Fix Remaining Control Weaknesses To effectively move beyond basic financial management, agencies need to eliminate remaining material weaknesses, other reportable conditions and material non-conformances with financial management laws and regulations identified through CFO Act audits. Agencies have made good strides in correcting weaknesses identified during the initial audits; however, almost two thirds of the 24 large agencies still had material weaknesses as of the end of fiscal year 2004, and while nine agencies did not have any material weaknesses, most of these agencies had one or more reportable conditions or non-conformances.

The material weaknesses reported by the auditors are not new. As summarized in the following table, many involve fundamental problems that have existed in government for years.

Federal Financial Management: The End of the Beginning Page 15

Fiscal Year 2004 Material Weaknesses Summary Chart

Material Weaknesses Number of Agencies

Inadequate controls and processes supporting financial reporting

15

Inadequate security over financial systems and data 11

Inability to properly account for property, plant, and equipment

8

Inability to identify intergovernmental transactions 4

Fund Balance not reconciled with Treasury 3

Other accounting and control issues 9

Total material weaknesses reported by auditors 50

Often, weaknesses identified by auditors are symptoms of larger systemic problems, such as old, un-integrated financial systems. Agencies, however, do not have to wait until new systems are implemented to eliminate the weaknesses. Strong fiscal discipline is most often what is required to eliminate, or at least mitigate, weaknesses. Agencies can implement “work-arounds” to eliminate or mitigate the effect of weakness, typically utilizing manual and spreadsheet based processes to supplement deficiencies in older systems. While not the end-state solution, these temporary actions are worth taking. They help improve historical data and help an agency understand the causes of problems so they are not repeated when new systems are implemented. These actions also help instill fiscal discipline in the financial environment, a benefit that will carry forward. Lastly, these temporary fixes provide the agency with more reliable data in advance of fully modernized systems, so that the agency can continue forward with other useful financial management initiatives such as cost management and budget-performance integration.

As a first priority, agencies must dedicate resources to address weaknesses. Agencies usually find that the highest level of resources are required in the initial year due to time spent analyzing the problem, developing corrective actions, cleaning up historical data that has accumulated over many years, and changing the environment that tolerated the situation. Once these initial steps are taken, maintaining the solution in subsequent years usually requires considerably fewer resources until eventually automated solutions are in place. In the past, attempts have been made to correct weaknesses without a clear realization of the work or schedule that would be required. This led to false attempts where results were not achieved, causing frustration and a belief that the problems were not fixable. To avoid these problems, realistic plans, schedules and milestones to fix the weaknesses must be developed. We recognize that often the early solutions are temporary fixes, but in most cases, the temporary fixes still represent good investments until structural and systemic improvements can be made.

The accelerated financial statement reporting cycle that was mandated beginning with fiscal year 2004 also should enable agencies to correct material weaknesses. In fiscal year 2004, agencies were required to issue their Performance and Accountability Reports (PAR) by November 15th - 45 days

Federal Financial Management: The End of the Beginning Page 16

after the end of the fiscal year. In previous years, agencies were required to issue their audited financial statements by March 31. Under the previous reporting schedule, agencies had only a few months after completing one year’s financials before initiating the close process for the succeeding year. Agencies now have significantly more time to correct weaknesses from the prior year and more timely, prior-year financial information for use in the current year.

Need to Balance Accelerated Reporting with Accuracy

While accelerated reporting has freed up more time for agencies to correct weaknesses, an unexpected surge in financial statement restatements has emerged in the past year, and agencies are being reminded to balance accelerated reporting with accuracy. During fiscal year 2004, a growing number of CFO Act agencies restated certain facets of their fiscal year 2003 financial statements to correct errors. Alarmingly, 11 out of 24 agencies fell into this category, compared with only five agencies that had restatements covering their fiscal year 2002 financial statements that were reported in fiscal year 2003. Management needs to set as a high priority correction of the control weaknesses that have permitted this level of reporting inaccuracy to occur.

Reduce Erroneous Payments While it is impossible to know the exact amount of improper payments made by the federal government, OMB estimates the figure to be $35 billion annually. Given the extraordinary cost to the government and the U.S. taxpayer, reducing improper and erroneous payments is essential to effective financial management, fiscal responsibility, and accountability. To address this challenge, Congress passed the Improper Payments Information Act of 2002 (IPIA) which requires agency heads to review all programs and activities annually; identify those that may be susceptible to significant improper payments; estimate annual improper payments in the susceptible programs and activities; and report the results of their improper payment remediation activities.

Improper payments are government payments that should not have been made or were made for incorrect amounts, including:

Inadvertent erroneous payments, such as duplicate payments, and incorrectly calculated payments (which include underpayments);

Unsupported or inadequately supported payment claims; Payments for services not rendered or services rendered to ineligible

beneficiaries; and Payments resulting from fraud and abuse by program participants and/or

federal employees.

Challenges of Erroneous Payments

Depending on the size, type, and complexity of programs, each agency has its own unique challenges to reducing improper payments. However, some of the more common problems which increase the risk of improper payments include:

Weak internal controls, including deficient systems, procedures, and management oversight that are critical in detecting and preventing improper payments;

Federal Financial Management: The End of the Beginning Page 17

Lack of information sharing among agencies necessary to prevent fraud, maintain consistent eligibility requirements, measure improper payments across government, and share best practices; and

Regulatory and policy restrictions inherent in individual programs which limit the possibility for oversight and create risk for improper payments.

Since enactment of the IPIA, a number of strategies and best practices to reduce improper payments have emerged from GAO and OMB studies and government-wide collaborations from the CFO Council (CFOC) and the President’s Council on Integrity and Efficiency (PCIE). While it is not cost-effective or even feasible to eliminate all improper payments, agencies can take action to reduce this problem to an acceptable level of risk.

Create an Effective Control Environment

In order to reduce improper payments effectively, senior leadership must give adequate attention to problems inherent in the dissemination of government funds to external entities, including benefit recipients, grantees, contractors, suppliers, and employees. It is the responsibility of managers to establish and implement systems and procedures to detect, prevent, and/or eliminate fraud. This technique is also called “data mining.” The following are two common approaches:

Review payment files to detect possible duplicate or erroneous payments, a practice known as “recovery auditing.” Recovery auditing can be performed in-house or by an outside contractor. While this technique typically is used to detect improper payments that have already been made, it also can be used to prevent future improper payments by identifying and correcting past problems or errors.

Institute post-award and post-contract monitoring and audit procedures to provide assurance that payments are made according to federal requirements. These procedures can include regular reviews of contract or award documentation, transaction histories, invoices, and banking records in order to detect possible errors.

Improve Communication and Knowledge Sharing

To adequately address the problem of improper payments, managers need timely and accurate information in order to make informed decisions. The outcomes and lessons learned from risk assessments, development of internal controls, studies and evaluations, and audits must be readily available and leveraged by decision makers to create plans, policies and procedures to continue to reduce the rate of improper payments from year to year.

Effective communication and collaboration between program and financial managers is necessary to provide assurance that correct payments are going to the right recipients, based on program requirements, and that payments are made in compliance with federal financial requirements. Further, agencies must receive timely information from recipients, such as annual reports, program reports, and audit information, in order to monitor the use of payments as appropriate.

Communication and knowledge sharing across agencies also is an effective way to reduce improper payments through applicant eligibility verification, fraud detection, and dissemination of best practices. Moving forward, greater collaboration and communication among agencies, combined with regulatory

Federal Financial Management: The End of the Beginning Page 18

changes, could also lead to more standardization of payment processes and risk mitigation measures. More standardization and risk mitigation could further improve the government’s ability to reduce improper payments and thus provide greater accountability and fiscal discipline to the U.S. taxpayer.

Importance of Addressing the Erroneous Payments Issue

Reducing erroneous payments is an unquestionable area for real savings. It is also an area that can save an agency embarrassment from public reporting of fraud, waste, abuse and mismanagement. Agencies with high risk programs have worked to quantify the extent of misspending for years. However, most agencies have not addressed this issue fully. It is worth an agency’s time to assess the situation even when the risk is not apparent. For example, the IRS conducts random audits of annual tax returns to deter cheating and to quantify the scope and areas of cheating. The Department of Education is working with the Internal Revenue Service to validate statements of annual income reported by students and parents on the Free Application for Federal Student Aid with income reported in annual tax returns. The same level of scrutiny should be applied to check other federal payment programs as well.

Role of the Single Audit Act (SAA) in Detecting Erroneous Payments

Recipients of federal grants and loans are responsible for the proper use of those funds, according to federal requirements and guidelines. As such, federal agencies rely on information provided by recipients for assurance that taxpayer money is being used and disbursed properly.

The SAA requires recipients of federal grants and loans to undergo a single annual audit of their finances, even if they receive federal funding from multiple sources. A single audit focuses on the recipient’s internal controls and its compliance with federal award laws and regulations. Federal awards include grants, loans, loan guarantees, property, cooperative agreements, interest subsidies, insurance, food commodities, direct appropriations, and federal cost reimbursement contracts. OMB provides agencies direction in implementing the SAA in Circular A-133, Audit of States, Local Governments, and Non-Profit Institutions. The Federal Audit Clearinghouse received about 34,000 single audit reports during calendar year 2000, of which about 5,500 contained audit findings. Federal awards for fiscal year 2001 totaled about $325 billion of that year’s $1.8 trillion federal budget.

The federal CFO must rely on audits conducted on behalf of the recipient organization and respond to the requirements of the SAA and OMB Circular A-133. In testimony before the House on June 26, 2002, GAO reported on effectiveness issues pertaining to the SAA5. GAO recommended the following actions:

Agencies must establish and follow guidance to address the requirements of SAA and OMB Circular A-133; and,

Agencies must implement policies and procedures for reporting information to senior-level agency management on findings identified in single audit reports and on status of corrective actions.

5 GAO, Single Audit Effectiveness Issues, June 26, 2002, Statement before the Subcommittee on Government

Efficiency, Financial Management and Intergovernmental Relations, Committee on Government Reform, House of Representatives

Federal Financial Management: The End of the Beginning Page 19

The quality and coverage of the single audit, when the scope of review covers multiple programs, is subject to debate. GAO questioned whether:

All required audits are being conducted; Recipients perform the required monitoring of sub-recipient’s uses of

federal awards, e.g., state funds transferred to local governments, and follow-up on corrective actions; and

All single audits comply with government auditing standards.

Even though the thoroughness and effectiveness of single audits can be debated, the CFO must respond to single audit findings and seek corrective actions.

Meet Internal Control Standards (i.e. Applying OMB Circular A-123) The Sarbanes-Oxley Act of 2002 (SOX) was passed in order to prevent more hardships for investors of public companies due to improper financial disclosures. The Act sets forth a systematic approach to internal controls with which companies are to comply in order to restore confidence in the financial reporting of publicly-traded companies. Business credibility was enhanced by reducing conflicts of interest, increasing third party independence, strengthening the audit committee role in the financial reporting process, and reinforcing management responsibility for financial statements.

Who is impacted by Sarbanes-Oxley?

The Sarbanes-Oxley Act has implications for the federal government and for the federal CFO. In December 2004, OMB released new requirements and guidelines that administratively mirror Section 404 of the Act for federal government implementation. Circular A-123 was revised and issued with a new title of Management’s Responsibility for Internal Control. A-123 governs implementation of the Federal Managers’ Financial Integrity Act (FMFIA), which requires agency officials to annually report on the effectiveness of their internal accounting and administrative controls. The revised circular is effective for fiscal year 2006. The need for stronger guidance on financial reporting emerged after a joint committee of OMB, the CFO Council and members of the President's Council on Integrity and Efficiency evaluated corporate reporting requirements created by the Sarbanes-Oxley Act. The committee voted to adopt, rule and form, amendments to administratively implement many requirements of Section 404 of the Sarbanes-Oxley Act, which deals specifically with internal controls over financial reporting and audit requirements.

In the following chart we summarize private and public sector requirements for internal controls over financial reporting and highlight the differences between the two, the most significant of which relates to auditor reporting on internal controls.

Federal Financial Management: The End of the Beginning Page 20

Comparison of Private and Federal Sector Internal Control Requirements

Private Federal

SOX requires managers to issue a report stating their responsibility for establishing and maintaining an adequate internal control structure and procedures for financial reporting

A-123 is augmented to emphasize management’s responsibility for controls over financial reporting and requires an annual statement acknowledging this responsibility

SOX requires management to identify the framework used to evaluate the effectiveness of internal controls

A-123 is augmented to provide a framework for evaluating internal controls and requires reference to this framework in management’s report

SOX requires audit attestation on the assessment made by management

A-123 does not require a separate audit attestation of controls over financial reporting. Agencies may secure a separate audit opinion. OMB may also require a separate audit if management is not achieving progress in correcting control weaknesses in accordance with its approved plan

SOX requires management to assess the effectiveness of internal control as of the end of the company's fiscal year

A-123 requires management’s assessment as of June 30, unless an audit is done, at which time the report may be dated the same as the auditors report. Management is also required to update the report for any new issues coming to their attention between June 30 and September 30, the government’s fiscal year end

SOX and implementing guidance requires management to disclose any material weakness. Management will be unable to conclude that the company's internal controls over financial reporting are effective if there are one or more material weaknesses in such controls.

A-123 precludes management from concluding that the agency’s internal controls over financial reporting are effective if there are one or more material weaknesses. Management is required to disclose all material weaknesses that exist as of June 30.

Federal vs. Corporate Financial Management Reporting: Similarities and Differences

The integrity of financial reporting in both the federal sector and for publicly traded companies is critical to the operations of both entities. The Journal of Government Financial Management6 recently discussed the similarities and differences between the two entities and the challenges in applying SOX to the federal sector. 6 Journal of Government Financial Management, ”Putting SOX on Federal Agencies” Dennis J. Duquette,

Spring 2005

Federal Financial Management: The End of the Beginning Page 21

The similarities in financial management include common internal control standards, comparably qualified and experienced individuals, and similar accounting processes and technologies. However, there are major differences:

Different Risks: Federal financial transactions are prescribed by law; private sector transactions are proscribed by law. Private sector entities are highly motivated to report favorable earnings; federal entities lack that “bottom-line” metric. It would thus appear less likely that a federal financial manager would alter financial reporting for personal gain. Federal entities are governed by law and regulation to ensure accountability. And the actions of federal entities, in the main, are open to public scrutiny.

Different Culture: The bottom line --the profit-- is paramount in the private sector. In government, budget rules. With no profit factor, a major measure of success is the level of funding appropriated for the federal entity.

Different Financial Reporting Model: The Federal Accounting Standards Advisory Board (FASAB) standards are different from commercial generally accepted accounting principles (GAAP). In government, the focus of reporting is on assets and expenditures; in the commercial sector, the focus of reporting is on generating revenues and net income.

Different Financial Management Maturity: As stated earlier in this paper, the federal government is still relatively new to financial reporting.

So what do these similarities and differences mean with regard to the administrative application of SOX Section 404 to the federal financial management environment? The federal interpretation of SOX will be applied to the federal sector per OMB Circular A-123, notwithstanding the considerable challenges inherent in such an application. There is some good news, however. The elements that can provide the basis for federal entities to meet SOX requirements—existing laws requiring significant testing and evaluation of internal controls, managerial self-assessments, accelerated financial reporting, and prior audit requirements on internal controls—are already present. Transparency and accountability will be enhanced in both the federal and commercial sectors as a result of SOX. Getting there will be the effort.

A-123 Requirements for the Federal Sector

The transmittal of the revisions to OMB Circular A-123 includes a summary of changes based on an interpretation of Sarbanes-Oxley for use by the federal CFO.

Applicability: The revised Circular applies to all 24 CFO Act agencies and is effective in fiscal year 2006.

Scope: Assessment and documentation of internal controls over financial reporting includes the annual financial statements and other significant internal or external financial reports as well as compliance with laws and regulations that pertain to those financial reports.

Planning Materiality: Materiality is defined within the Circular for the purposes of assessing and documenting internal controls over financial reporting.

Assessment Team: The Circular recommends that each CFO Act Agency establish a senior assessment team that, at a minimum, oversees the assessment process.

Federal Financial Management: The End of the Beginning Page 22

Assessing Financial Reporting Internal Control: The Circular defines financial reporting assessment processes for internal controls at the entity level as well as at the process, transaction, or application level.

Documentation: Documentation is required of controls over financial reporting and of the assessment process of the controls.

Assessment of Internal Control by Management: Management is required to assert to the effectiveness of internal controls via an assurance statement “as of June 30.” The assurance statement and corrective actions, if required, are to be submitted in the annual Program Assessment Review (PAR) no later than 45 days after the end of the fiscal year.

Internal Control Audit Opinions: Agencies may secure a separate audit opinion on internal controls over financial reporting. In those situations, the “as of” reporting date of June 30 may be adjusted to align better with the “as of” date of the audit opinion. (A-123 does not require a separate audit.)

Correcting Internal Control Material Weaknesses: If the agreed-on deadlines for corrective actions are not continuously met by a CFO agency, the Circular contains a non-compliance clause that permits OMB to require an agency to obtain an audit opinion over the internal controls over financial reporting.

Implementing A-123 may require increased expenditures for federal agencies, especially if OMB determines that an agency is not making progress in correcting weaknesses and an independent audit is ordered. But this potential for added costs should be viewed in light of the large number of restatements that occurred with the 2004 audits, which decrease confidence in federal financial statements, and the estimated $35.7 billion worth of improper payments reported by agencies that stronger internal controls should help mitigate.

Federal Financial Management: The End of the Beginning Page 23

Strategy 3: Have Fresh, Accurate Financial Information on Demand We live in an information saturated world. Federal executives want and need financial information at their fingertips to grasp the financial condition of the agency, to undertake “what if” scenarios, and to support decision-making. The federal CFO is expected to provide this executive and managerial level financial information on demand, to keep the information continuously updated, and assure that the information is totally accurate.

Financial management systems, processes, procedures and, most importantly, routine and ad hoc reports must be attuned to the needs of the customers. Standard accounting data provides information on the amounts of funds spent, for which major programs the funds are spent, the time period for the spent funds and how the spent funds are characterized.

Cost management data provides the federal executive and manager with more detailed information on spent funds, i.e., aligning the funds with major functions and activities, identifying spending drivers, and associating spent funds with specific performance measures. Financial information is prevalent; the challenge is to hone that information to meet the needs of the CFO’s customers.

In the following sections, we describe two actions that CFOs can take to produce accurate and useful financial information on-demand:

Know and educate managers on cost of products and services Provide useful information for decision-makers on demand

Know and Educate Managers on Cost of Products and Services Budget and performance integration is a major thrust of the President’s Management Agenda (PMA) and the Government Performance and Results Act (GPRA). The Administration and Congress are demanding that agencies demonstrate the results of investments in federal programs. Useful cost information is an important element in achieving this objective. Agencies need cost information to 1) evaluate how well programs are efficiently achieving results; 2) produce performance-based budgets; and 3) fairly price goods and services sold to the public or other agencies. Detailed cost information, aligned with performance measures and outcomes, provides agency senior leadership with valuable information to make informed decisions such as setting priorities among programs during periods of tight funding; evaluating programs; controlling costs, particularly indirect or ancillary overhead costs; and evaluating management performance.

While cost management relies on accounting data, it is important to stress that it is a management tool, not an accounting tool. Standard accounting data provides information such as how funds were spent (for example, compensation, travel, and contracts); when funds were spent and at what rate; and how well the agency fulfilled its fiduciary responsibilities based on the annual financial statement audit. In contrast, cost information provides agency leadership with the costs of program activities; the costs of outputs or outcomes; and, when aligned with a rigorous performance management system, information on how well the agency spends its resources to fulfill its mission, goals, and objectives.

Federal Financial Management: The End of the Beginning Page 24

Activity Based Costing (ABC)

Activity Based Costing (ABC) is a cost management technique widely used within the private sector and rapidly being adopted within the federal sector as well. ABC is simple in its premise:

Define programs into a series of activities; Identify the number of outputs or outcomes of the activities, for a set

period of time, e.g., on an annual basis; Determine the cost drivers for each activity; and Calculate the unit cost of each output or outcome.

A number of agencies have begun implementing cost systems, and to date, the results have been mixed. In agencies where cost systems have been in use for several years, managers use the information to streamline operations and reduce costs; to make difficult decisions on how best to use limited resources; to set fees for costs of goods and services; and to set goals for, and to evaluate results of, reducing unit costs. This enables the CFOs to equip program managers so that they better understand their resource needs. It also encourages the CFO to refine data collection and cost systems to support these needs.

There are also many instances where cost information provided by CFOs is not used by the program managers. These instances arise due to inaccuracy of cost data (real or perceived), because managers are not accustomed to using cost information, because managers have not fully participated in the cost gathering processes and/or have not been fully educated in cost management, or because they do not see the value of such information for their programs. These issues can be addressed as the cost management processes, systems and data are refined, become better honed and become ingrained within the financial and program management culture of the agency.

In those situations where the program managers do not feel they need the data to support decision making, they are often times dealing with programs where actions are legislated or the percent of program controllable expenditures (usually the salary and expense component) is so small they do not feel there is sufficient value in focusing on cost. This often applies to subsidy and entitlement programs or programs that are carried out largely by third parties (typically state and local governments). For example, managers may feel that their attention and limited resources might be better focused on correcting erroneous payments.

CFOs should be persistent in introducing a culture of cost management. A critical element in successfully changing an agency’s cost management culture is senior leadership support. Without the demonstrable and personal support of agency senior leadership, CFOs will not be successful in changing an agency’s cost management culture. Assuming leadership support, CFOs may begin by focusing on those key program areas where cost information for decision making provides the greatest return (i.e., when decisions supported by cost need to be made).

Federal Financial Management: The End of the Beginning Page 25

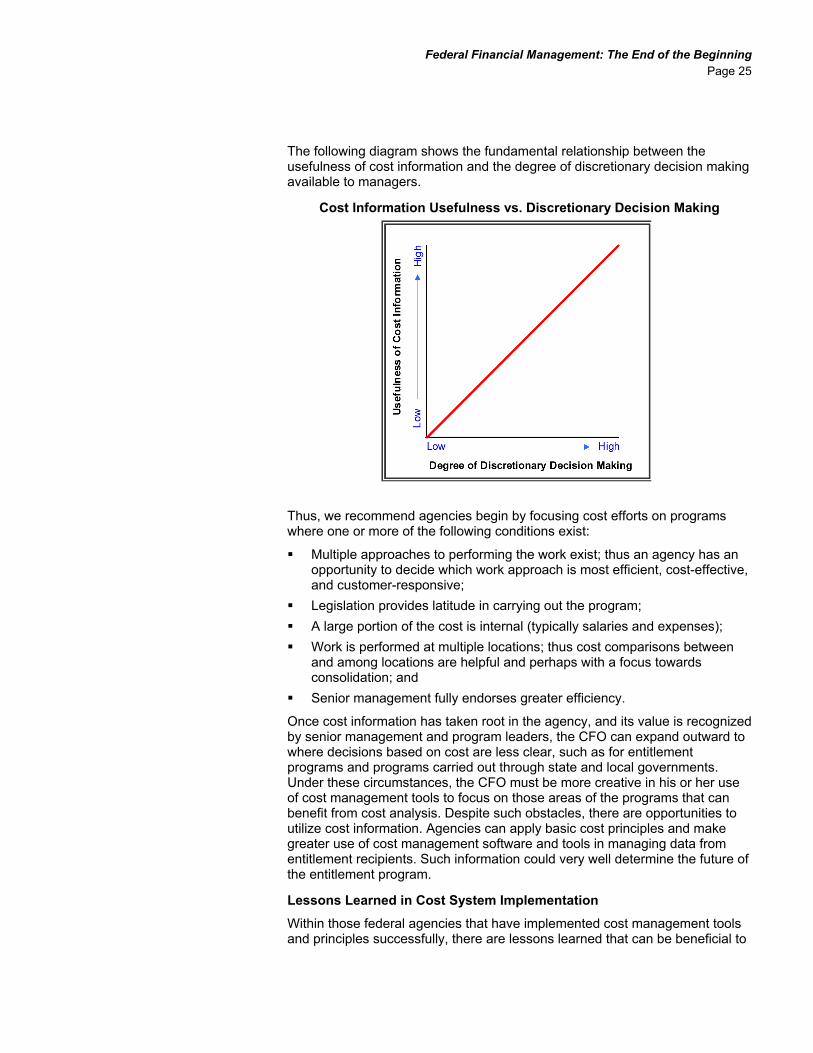

The following diagram shows the fundamental relationship between the usefulness of cost information and the degree of discretionary decision making available to managers.

Cost Information Usefulness vs. Discretionary Decision Making

Thus, we recommend agencies begin by focusing cost efforts on programs where one or more of the following conditions exist:

Multiple approaches to performing the work exist; thus an agency has an opportunity to decide which work approach is most efficient, cost-effective, and customer-responsive;

Legislation provides latitude in carrying out the program; A large portion of the cost is internal (typically salaries and expenses); Work is performed at multiple locations; thus cost comparisons between

and among locations are helpful and perhaps with a focus towards consolidation; and

Senior management fully endorses greater efficiency.

Once cost information has taken root in the agency, and its value is recognized by senior management and program leaders, the CFO can expand outward to where decisions based on cost are less clear, such as for entitlement programs and programs carried out through state and local governments. Under these circumstances, the CFO must be more creative in his or her use of cost management tools to focus on those areas of the programs that can benefit from cost analysis. Despite such obstacles, there are opportunities to utilize cost information. Agencies can apply basic cost principles and make greater use of cost management software and tools in managing data from entitlement recipients. Such information could very well determine the future of the entitlement program.

Lessons Learned in Cost System Implementation

Within those federal agencies that have implemented cost management tools and principles successfully, there are lessons learned that can be beneficial to

Federal Financial Management: The End of the Beginning Page 26

the CFO who intends to implement or is now implementing cost management systems.

Cost management systems can only be successful if the agency leadership endorses and meaningfully supports implementation.

Cost management will be taken seriously by managers if, starting at the agency head level, they are held accountable in their annual performance plans for reducing unit costs and for improving performance and overall program efficiency and effectiveness.

Cost management training is critical. Using benchmarks and best practices from other agencies or the private sector are helpful means to train managers and convince them of the utility of cost information.

The cost management implementation team must work closely with, and respect the opinions and knowledge of, program managers. To achieve this goal, the cost management team must produce and distribute reports that are simple, direct, user-friendly, electronic, and with a “drill-down” capability to more detailed levels of information; and thereby strike a chord with managers who have identified the value of the information to his or her program.

Cost management data is only as good as the information fed into it. Thus, if the underlying accounting system produces poor or erroneous data, the cost management system will simply report the same poor data and erroneous information, only in a different manner.

Implementation of a cost management system requires significant dedication and time. Most federal employees, particularly those of the “rank and file,” have never been asked to quantify what they do, the time it takes them to complete a task or deliver a product, or the results of their delivered product or service. The prospect of having to use cost management for the first time is intimidating to many employees. As such, patience is necessary when introducing cost management. Facilitation and “hand-holding” are critical.

Be prepared to deal with employee concerns. The best way to secure accurate data on the amount of time spent performing activities is to institute a recurring mechanism for recording time by project. The CFO may have to negotiate such a requirement with the union(s) or even develop an alternative approach to collecting labor hour data, such as annual employee surveys.

Research and apply best practices from the private and government sectors. There is no need to create from scratch what others already have implemented.

The ability to measure unit costs will vary depending on the situation. The clearer and more definite the product or service, the easier it is to define unit cost. Even with entitlement programs, the cost to review applications, make decisions, and disburse funds via grants or loans can be measured. How the funds are used (for example, the number of individuals served by a particular program) will be dependent upon data delivered by the recipient, but this information could be required as a condition of receipt of federal funding. There is a wealth of information on the utilization of cost management tools and processes, so be creative.

Federal Financial Management: The End of the Beginning Page 27

Provide Useful Information on Demand One of the ultimate goals of improved federal financial management under the CFO Act is for agencies to have systems and processes in place to provide useful information to senior leadership, managers, and other agency decision-makers to manage their programs more effectively and efficiently. The importance of useful management information is discussed throughout this whitepaper as a means to make informed decisions in areas ranging from erroneous payments to cost management to systems implementation. Managers need to have accurate and timely financial and performance information to assign costs to a product or service, develop realistic and strategic budgets, allocate resources appropriately, and manage programs efficiently and effectively.

Integrating and Disseminating Performance, Budget and Cost Information

The federal government has emphasized the integration of performance, budget and cost information as a means to provide greater transparency into public finances and improved accountability for the use of public funds. The PMA stresses performance and budget integration as one of the dimensions on which major agencies are evaluated. Also, recent performance management legislation and policy, including the GPRA and OMB’s PART, have mandated that agencies develop and track annual performance goals and report performance outcomes to OMB, and the Congress annually, alongside their financial results.

Activity-based costing (ABC) is one of a number of effective management tools. ABC, when fully implemented, can provide managers with useful cost information that, in turn, assists the manager in making decisions to improve programmatic and operating efficiency and effectiveness. To maximize the utility of the cost information tool, ABC must be integrated with performance information in order to provide managers with a complete picture of how well they are managing their resources to achieve programmatic objectives. Looking ahead, managers can then use integrated information to plan for the future and create budgets that reflect prior year results, both from a programmatic and cost perspective. We offer the following recommendations to provide useful, integrated information to managers:

Set realistic, quantifiable performance goals and benchmarks for programs. Hold managers and staff accountable for achieving the goals and for providing senior leadership with up-to- date performance, cost, and budget information on their progress. Establish employee performance plans to link individual performance with achievement of agency goals and objectives, and hold management and staff responsible for achieving individual performance plan measures. Effective performance measurement is a key objective of GPRA, PART and the PMA.

Develop systems to provide accurate and timely performance information to managers and to track spending and resource levels needed to achieve performance goals. Data warehouses can provide historical and current information in real time; historical trends; performance progress against goals and benchmarks; and scaleable management reports.

Establish cross-agency committees and working groups to foster knowledge sharing, best practice dissemination, strategic planning, and

Federal Financial Management: The End of the Beginning Page 28

issue resolution. There is often a lack of communication among individual programs and offices within an agency, leading to problems such as inconsistent implementation of agency-wide and federal requirements, repetitive work, delays in receiving information, and lack of understanding of programs. Forming collaborative committees and working groups is a useful way to bridge these gaps.

Align annual GPRA and PART performance goals with cost information. Many agencies have developed a crosswalk in the Statement of Net Costs between their performance goals and the costs expended to achieve these performance goals. The complexity of aligning budget, costs and performance is significant. Yet when this alignment is fully achieved, assigning cost estimates to individual goals is a useful way to begin improving transparency, integrating cost with performance, and providing managers with a picture of the cost efficiency of their programs.

Incorporate performance results and cost information into the development of annual budgets. Developing a schedule for receiving both performance and cost information in time to prepare budgets is a useful way to allocate limited resources, based on programmatic and cost effectiveness.

Users of Management Information