the china-u.s. trade war and future economic relations

TRANSCRIPT

The China-U.S. Trade War

and Future Economic RelationsLawrence J. Lau

Ralph and Claire Landau Professor of Economics, The Chinese Univ. of Hong Kongand

Kwoh-Ting Li Professor in Economic Development, Emeritus, Stanford University

Tsinghua Entrepreneur and Executive ClubKerry Hotel

Hong Kong, 18 May 2019

Tel: +852 3943 1611; Fax: +852 2603 5230

Email: [email protected]; WebPages: www.igef.cuhk.edu.hk/ljl

*All opinions expressed herein are the author’s own and do not necessarily reflect the views of

any of the organisations with which the author is affiliated.

Introduction The National Bureau of Statistics of China has recently reported the

2019Q1 result for the Chinese economy. Real GDP grew at an annualized rate of 6.4%. The target range of the rate of growth of 2019 is 6%-6.5%. The economy is on course.

For 2018 as a whole, the rate of growth of real GDP was 6.6%, exceeding the target of 6.5%. The result also reflects the impacts of the expectation of a trade war since January 2018 and the uncertainty it has created, as well as half a year of U.S. tariffs on Chinese exports to the U.S., in addition to the rise of rates of interest globally.

In the following chart, the quarterly rates of growth of Chinese real GDP, year-on-year, are presented in colour-coded columns (light green for first quarter, red for second quarter, yellow for third quarter and blue for fourth quarter). The five quarterly year-on-year rates of growth were, from 2018Q1 through 2019Q1, respectively: 6.8%, 6.7%, 6.5%, 6.4% and 6.4%. It is clear from the chart that the rate of growth of Chinese real GDP has stabilized--an L-shaped soft landing.

2

Quarterly Rates of Growth of Chinese Real

GDP, Year-on-Year, 1983 to the Present

-5%

0%

5%

10%

15%

20%

25%

1983q

11983q

31984q

11984q

31985q

11985q

31986q

11986q

31987q

11987q

31988q

11988q

31989q

11989q

31990q

11990q

31991q

11991q

31992q

11992q

31993q

11993q

31994q

11994q

31995q

11995q

31996q

11996q

31997q

11997q

31998q

11998q

31999q

11999q

32000q

12000q

32001q

12001q

32002q

12002q

32003q

12003q

32004q

12004q

32005q

12005q

32006q

12006q

32007q

12007q

32008q

12008q

32009q

12009q

32010q

12010q

32011q

12011q

32012q

12012q

32013q

12013q

32014q

12014q

32015q

12015q

32016q

12016q

32017q

12017q

32018q

12018q

32019q

1

Per

cen

t p

er a

nn

um

Quarterly Rates of Growth of Chinese Real GDP, Y-o-Y

GDPQ1 GDPQ2

GDPQ3 GDPQ4

3

Introduction Thus far, the trade war does not seem to have done too much

noticeable damage to the Chinese economy. The rate of growth

of Chinese real GDP declined by only 0.4 percentage point from

2017Q4 to 2018Q4 and from 2018Q1 to 2019Q1. However, the

6.4% rate of growth in 2018Q4 and 2019Q1 was the lowest rate

of growth of the Chinese real GDP since the first quarter of 2009,

in the aftermath of the outbreak of the global financial crisis,

when it grew 6.2 percent.

Moreover, it might have also reflected the (positive) effects of

accelerated shipments of Chinese exports of goods to the U.S. in

an attempt to beat the tariffs.

4

Introduction This magnitude of the decline in the rate of growth is well within the

expected range of the potential negative impact caused by the U.S. tariffs on Chinese exports of goods to the U.S. I had predicted that the maximum negative impact to the Chinese economy, assuming that half of Chinese exports to the U.S. are halted, would be 0.43% in the first instance, and eventually cumulatively 1.12% if all the indirect effects are included.

Up to 10 May 2019, the 25% tariff rate applied to only US$50 billion of Chinese exports of goods to the U.S. A 10% tariff rate applied to another US$200 billion of Chinese exports. But on 10 May 2019, the 10% tariff rate has been raised to 25%. The negative impact of the trade war on the real GDP of 2019 is likely to be higher than 0.4%. However, the marginal effect of this increase in the tariff rate from 10% to 25% is not likely to be large as the 10% tariff rate is already high enough to be almost prohibitive for most Chinese exports to the U.S. There simply is not that kind of profit margin for such exports to be absorbed by the manufacturers.

5

Introduction While the impacts on the Chinese economy of the U.S. tariffs have certainly

been significant and negative, they are still relatively small in real terms and quite manageable for China. There is no need to panic. The sky is not falling!

The Chinese economy is sufficiently flexible and resilient that it will be able to adopt appropriate measures. survive the negative impacts, and maintain significant positive economic growth. For example, it can increase domestic aggregate demand by mandating the enhanced provision of public goods such as environmental preservation, protection and restoration, education, health care and elderly care.

But even if the trade war, or at least the mutual tariffs, ends, hopefully soon, economic and technological competition between China and the U.S. is likely to continue for a long time. It will become the “new normal”. Moreover, the trade war itself may do damage to the longer-term relations between the two countries.

It is also a reflection of the rise of populism, isolationism, nationalism and protectionism almost everywhere in the world, including in the U.S.

6

Immediate Impacts The Chinese stock markets have already taken a hit. This is an area where

the psychological factor dominates. As of the end of 2018, the shares on the Shenzhen Stock Exchange had on average lost 30%, Shanghai 20%, and Hong Kong 10%. In contrast, the Standard and Poor 500 Index of U.S. stocks did not suffer any loss on a whole-year (2018) basis.

It should also be borne in mind that the increase in the rates of interest in the U.S. and elsewhere in 2018 would also have affected asset prices around the world negatively, so it was not solely the effect of the China-U.S. trade war.

At the beginning of 2019, the Chinese stock market continued to fall, until the latter part of January, then it began to rise, buoyed by hopes of a successful conclusion of a China-U.S. trade agreement. More recently, however, it has become quite volatile, reflecting the progress or lack thereof of the trade negotiations.

The Standard and Poor 500 Index also fell at the beginning of 2019, but has also recovered but experienced volatility similar to the Chinese stock market price indices more recently. 7

The Chinese, Hong Kong and U.S. Stock

Market Indexes, 2018M1 to Date

50

60

70

80

90

100

110

120

50

60

70

80

90

100

110

120Stock Price Indices of Various Stock Exchanges, 1 January 2018 = 100

Hong Kong (Overall) Hong Kong (China Enterprise)

Shanghai Shenzhen

MSCI China S&P 500 Index

8

Immediate Impacts However, the Chinese stock markets are not a good barometer of the

state of the Chinese real economy. There is essentially no correlation between the rate of growth of Chinese real GDP and the rate of growth of the Chinese stock market price index (see the following scatter diagram between the quarterly rates of growth of Chinese real GDP and the Shanghai Stock Exchange Composite Index).

The majority (over 80%) of Mainland Chinese investors are individual retail investors. They are typically short-term traders who tend to leave the market at the first sign of potential trouble. The average holding period of individual Chinese investors is less than 20 trading days. The Chinese institutional investors have a slightly longer average holding period of between 30 and 40 trading days.

The short holding period is due in part to the fact that Chinese publicly listed enterprises pay little or no cash dividends. Investors can make money only through frequent trading and have little incentive to hold a particular stock long term. 9

The Rate of Growth of Real GDP versus the

Rate of Growth of the Stock Price Index

6

7

8

9

10

11

12

13

14

15

16

-50 0 50 100 150 200 250

Qu

arte

rly

Rea

l R

ates

of

Gro

wth

of

GD

P, p

erce

nt

Quarterly Rates of Changes of Stock Exchange Composite Index, percent

Quarterly Rates of Growth of Chinese Real GDP vs.

Quarterly Rates of Changes of the Shanghai Stock Exchange Composite Index

GDP vs. Index of Shanghai SE

10

Immediate Impacts The Renminbi exchange rate has also been affected by the trade war. In

2018, relative to the US$, the Renminbi has devalued by approximately 8% from the end of January 2018 (at one time almost 10%).

However, the deviation of the Renminbi central parity rate from the CFETS (China Foreign Exchange Trade System) Index, the exchange rate of a Chinese trade-weighted basket of currencies, has remained within the 3% range. Our focus should be on the central parity rate (onshore rate) rather than the offshore rate and on its relation to the CFETS Index.

The Renminbi does not follow the US$ any more because the U.S. accounts for only slightly more than 20% of Chinese international trade. For the Renminbi to follow the US$ when the US$ rises with respect to other currencies implies that China will raise its price of exports to all her other customers that account for almost 80% of Chinese exports, which makes very little sense. Similarly, when the US$ falls with respect to other currencies, if the Renminbi follows the US$, it will imply that China lowers its price of exports to all her other customers, which also makes little sense. 11

The Renminbi Central Parity Exchange Rate

and the CFETS Index (31/12/2014 = 100)

95

97

99

101

103

105

107

109

111

113

115

Dec

-201

4Ja

n-2

015

Feb

-201

5M

ar-2

015

Ap

r-20

15M

ay-2

015

Jun

-201

5Ju

l-20

15A

ug-

2015

Sep

-201

5O

ct-2

015

Nov

-201

5D

ec-2

015

Jan

-201

6F

eb-2

016

Mar

-201

6A

pr-

2016

May

-201

6Ju

n-2

016

Jul-

2016

Au

g-20

16S

ep-2

016

Oct

-201

6N

ov-2

016

Dec

-201

6Ja

n-2

017

Feb

-201

7M

ar-2

017

Ap

r-20

17M

ay-2

017

Jun

-201

7Ju

l-20

17A

ug-

2017

Sep

-201

7O

ct-2

017

Nov

-201

7D

ec-2

017

Jan

-201

8F

eb-2

018

Mar

-201

8A

pr-

2018

May

-201

8Ju

n-2

018

Jul-

2018

Au

g-20

18S

ep-2

018

Oct

-201

8N

ov-2

018

Dec

-201

8Ja

n-2

019

Feb

-201

9M

ar-2

019

Ap

r-20

19M

ay-2

019

Comparison of the Central Parity Rate and CFETS Indexes

12/31/2014 = 100

Index CFETS Currency Basket (Yuan/Currency Basket)

Index of Central Parity Rate (Yuan/US$)

12

The RMB Central Parity Exchange Rate and

the CFETS Index, 29/12/2017 to the Present

95

96

97

98

99

100

101

102

103

104

105

106

107

108

29-D

ec-1

7

12-J

an-1

8

26-J

an-1

8

09-F

eb-1

8

23-F

eb-1

8

09-M

ar-1

8

23-M

ar-1

8

06-A

pr-

18

20-A

pr-

18

04-M

ay-1

8

18-M

ay-1

8

01-J

un

-18

15-J

un

-18

29-J

un

-18

13-J

ul-

18

27-J

ul-

18

10-A

ug-

18

24-A

ug-

18

07-S

ep-1

8

21-S

ep-1

8

05-O

ct-1

8

19-O

ct-1

8

02-N

ov-1

8

16-N

ov-1

8

30-N

ov-1

8

14-D

ec-1

8

28-D

ec-1

8

11-J

an-1

9

25-J

an-1

9

08-F

eb-1

9

22-F

eb-1

9

08-M

ar-1

9

22-M

ar-1

9

05-A

pr-

19

19-A

pr-

19

03-M

ay-1

9

The Central Parity Rate and the CFETS Index, 29 Dec. 2017 = 100

Index of CFETS Currency Basket (Yuan/Currency Basket)

Index of Central Parity Rate (Yuan/US$)

13

Immediate Impacts Maintaining the relative stability of the Renminbi exchange rate

with respect to the CFETS (China Foreign Exchange Trade System) Index, the exchange rate of a Chinese trade-weighted basket of currencies, implies that the Renminbi exchange rate vis-a-vis the currency of an average trading-partner country of China will be relatively stable and that the international purchasing power of the Renminbi will also be relatively stable.

By not following the US$, the Renminbi exchange rate will be less volatile than the US$ exchange rate when viewed from a third country.

It is in China’s interests to maintain a relatively stable Renminbi exchange rate. It is the only way for the internationalisation of the Renminbi to become a reality.

14

Real Impacts Today, China, as a large continental economy with a huge

domestic market, has a relatively low degree of export

dependence, and has always been relatively immune to external

disturbances, just like the U.S.

During the past decades, while the rates of growth of Chinese

exports and imports of goods fluctuate like those of all other

economies, the rate of growth of Chinese real GDP has remained

relatively stable, and in fact has always stayed positive. (See the

following charts which display the quarterly rates of growth of

exports, imports and real GDP of selected Asian economies from

1997 to the present, with China represented by the red line).

15

16

Quarterly Rates of Growth of Exports of

Goods: Selected Asian Economies since 1997

-50

-40

-30

-20

-10

0

10

20

30

40

50

60

70

Q1

1997

Q2

1997

Q3

1997

Q4

1997

Q1

1998

Q2

1998

Q3

1998

Q4

1998

Q1

1999

Q2

1999

Q3

1999

Q4

1999

Q1

2000

Q2

2000

Q3

2000

Q4

2000

Q1

2001

Q2

2001

Q3

2001

Q4

2001

Q1

2002

Q2

2002

Q3

2002

Q4

2002

Q1

2003

Q2

2003

Q3

2003

Q4

2003

Q1

2004

Q2

2004

Q3

2004

Q4

2004

Q1

2005

Q2

2005

Q3

2005

Q4

2005

Q1

2006

Q2

2006

Q3

2006

Q4

2006

Q1

2007

Q2

2007

Q3

2007

Q4

2007

Q1

2008

Q2

2008

Q3

2008

Q4

2008

Q1

2009

Q2

2009

Q3

2009

Q4

2009

Q1

2010

Q2

2010

Q3

2010

Q4

2010

Q1

2011

Q2

2011

Q3

2011

Q4

2011

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

Q1

2016

Q2

2016

Q3

2016

Q4

2016

Q1

2017

Q2

2017

Q3

2017

Q4

2017

Q1

2018

Q2

2018

Q3

2018

An

nu

aliz

ed P

erce

nt

per

an

nu

m

Quarterly Rates of Growth of Exports of Goods: Selected East Asian Economies

China,P.R.:Hong Kong India

Indonesia Korea

Malaysia Philippines

Singapore Thailand

China,P.R.: Mainland Japan

Taiwan Prov.of China

16

17

Quarterly Rates of Growth of Imports of

Goods: Selected Asian Economies since 1997

-60

-50

-40

-30

-20

-10

0

10

20

30

40

50

60

70

80

Q1

199

7Q

2 1

997

Q3

199

7Q

4 1

997

Q1

199

8Q

2 1

998

Q3

199

8Q

4 1

998

Q1

199

9Q

2 1

999

Q3

199

9Q

4 1

999

Q1

200

0Q

2 2

000

Q3

200

0Q

4 2

000

Q1

200

1Q

2 2

001

Q3

200

1Q

4 2

001

Q1

200

2Q

2 2

002

Q3

200

2Q

4 2

002

Q1

200

3Q

2 2

003

Q3

200

3Q

4 2

003

Q1

200

4Q

2 2

004

Q3

200

4Q

4 2

004

Q1

200

5Q

2 2

005

Q3

200

5Q

4 2

005

Q1

200

6Q

2 2

006

Q3

200

6Q

4 2

006

Q1

200

7Q

2 2

007

Q3

200

7Q

4 2

007

Q1

200

8Q

2 2

008

Q3

200

8Q

4 2

008

Q1

200

9Q

2 2

009

Q3

200

9Q

4 2

009

Q1

201

0Q

2 2

010

Q3

201

0Q

4 2

010

Q1

201

1Q

2 2

011

Q3

201

1Q

4 2

011

Q1

201

2Q

2 2

012

Q3

201

2Q

4 2

012

Q1

201

3Q

2 2

013

Q3

201

3Q

4 2

013

Q1

2014

Q2

201

4Q

3 2

014

Q4

201

4Q

1 2

015

Q2

201

5Q

3 2

015

Q4

201

5Q

1 2

016

Q2

201

6Q

3 2

016

Q4

201

6Q

1 2

017

Q2

201

7Q

3 2

017

Q4

201

7Q

1 2

018

Q2

201

8Q

3 2

018

An

nu

aliz

ed P

erce

nt

per

an

nu

m

Quarterly Rates of Growth of Imports of Goods : Selected East Asian Economies

China,P.R.:Hong Kong IndiaIndonesia KoreaMalaysia PhilippinesSingapore ThailandChina,P.R.: Mainland Japan

17

18

Quarterly Rates of Growth of Real GDP, Y-o-

Y: Selected Asian Economies since 1997

-18

-15

-12

-9

-6

-3

0

3

6

9

12

15

18

21

Q1

1994

Q2

1994

Q3

1994

Q4

1994

Q1

1995

Q2

1995

Q3

1995

Q4

1995

Q1

1996

Q2

1996

Q3

1996

Q4

1996

Q1

1997

Q2

1997

Q3

1997

Q4

1997

Q1

1998

Q2

1998

Q3

1998

Q4

1998

Q1

1999

Q2

1999

Q3

1999

Q4

1999

Q1

2000

Q2

2000

Q3

2000

Q4

2000

Q1

2001

Q2

2001

Q3

2001

Q4

2001

Q1

2002

Q2

2002

Q3

2002

Q4

2002

Q1

2003

Q2

2003

Q3

2003

Q4

2003

Q1

2004

Q2

2004

Q3

2004

Q4

2004

Q1

2005

Q2

2005

Q3

2005

Q4

2005

Q1

2006

Q2

2006

Q3

2006

Q4

2006

Q1

2007

Q2

2007

Q3

2007

Q4

2007

Q1

2008

Q2

2008

Q3

2008

Q4

2008

Q1

2009

Q2

2009

Q3

2009

Q4

2009

Q1

2010

Q2

2010

Q3

2010

Q4

2010

Q1

2011

Q2

2011

Q3

2011

Q4

2011

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

Q1

2016

Q2

2016

Q3

2016

Q4

2016

Q1

2017

Q2

2017

Q3

2017

Q4

2017

Q1

2018

Q2

2018

Q3

2018

An

nu

aliz

ed R

ates

in

Per

cen

t

Quarterly Rates of Growth of Real GDP, Year-over-Year: Selected East Asian Economies

China,P.R.:Hong Kong India

Indonesia Korea

Malaysia Philippines

Singapore Thailand

China,P.R.: Mainland Japan

Taiwan Prov.of China

18

Real Impacts Moreover, over the past ten years, Chinese dependence on exports has been

declining. The share of exports of goods in Chinese GDP has fallen from a peak of 35.3% in 2006 to 19.5% in 2018. The share of exports of goods to the U.S. in Chinese GDP has also fallen by half, from a peak of 7.2% in 2006 to 3.6% in 2018. (See the following charts.)

The 3.6% represented an increase from the 3.4% in 2017. However, the increase reflected the acceleration of exports of goods to the U.S. from China in anticipation of the increases in tariffs. The trend of Chinese exports of goods to the U.S. as a percent of Chinese GDP is downwards.

During this same period, the growth of Chinese exports to the world and to the U.S. has also slowed significantly. Chinese exports to the world grew at an average annual rate of 23.5% in the decade 1998-2007, but slowed to only 5.9% in the following decade, 2008-2018. Similarly, exports to the U.S. grew at 23.7% per annum in the decade 1998-2008, but slowed to less than 6.6% per annum in the most recent decade. Exports is no longer the engine of Chinese economic growth. 19

Chinese Exports of Goods and Services and

Goods Only as a Percent of Chinese GDP

0

5

10

15

20

25

30

35

40

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Per

cent

Exports of Goods and Services as a Percentage of GDP

Exports of Goods Only to the World as a Percentage of GDP

20

Chinese Exports of Goods and Services and

Goods to the U.S. as Percent of Chinese GDP

3

3.5

4

4.5

5

5.5

6

6.5

7

7.5

8

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Per

cent

Exports of Goods

Exports of Goods and Services

21

The Annual Rates of Growth of Chinese

Exports of Goods to the World and to the U.S.

22

-20

0

20

40

60

80

100

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Per

cent

The Rate of Growth of Chinese Exports of Goods Only to the World

The Rate of Growth of Chinese Exports of Goods Only to the U.S.

Real Impacts U.S. tariffs have been imposed on US$250 billion of U.S. imports of

goods from China (arrival value, approximately equal to US$227 (250 x 10/11) billion of Chinese exports of goods to the U.S., f.o.b. or departure value), or slightly less than half of Chinese exports of goods to the U.S. in 2018. (Chinese exports of goods to the U.S. in 2018 amounted to US$540 billion according to U.S. data based on arrival value, which is approximately equivalent to US$500 billion at f.o.b. or departure value.)

The U.S. tariff rate has recently been raised to 25% on the value of the imports from China. These rates will be prohibitive for most of the Chinese exports of goods to the U.S., as neither the Chinese exporters nor the U.S. importers have the kind of profit margins that can afford these tariffs. There is no evidence that the Chinese producers or exporters will pay for the U.S. tariffs. The cost of the tariffs will be mostly borne by U.S. consumers and users of Chinese imports.

Thus, Chinese exports of goods amounting to slightly less than 1.8% (3.6%/2) of Chinese GDP will be affected.

23

Real Impacts on the Chinese Economy But the direct domestic value-added content of Chinese exports to the

U.S. is less than 25%. Thus, the maximum loss in Chinese GDP, assuming that half of the exports to the U.S. is completely halted, in the first instance, may be estimated at 0.45% (3.6%/2 x 0.25), a tolerable level, especially for an economy growing at an average annual real rate of 6.6 percent and with a per capita GDP of US$9,410 in 2018.

However, the reduction of exports leads to a reduction in the demand for domestic inputs used in their production, which in turn leads to a second-round reduction in the demand for domestic inputs used in the production of the domestic inputs.

With the indirect, that is, second-, third-, fourth- and higher-round effects of the reduction of Chinese exports kicking in, the total domestic value-added affected will eventually increase to 66 percent cumulatively. This implies ultimately a maximum total loss in Chinese GDP of 1.19% ((3.6%/2 x 0.66). In absolute terms, this amounts to US$156 billion in 2018 prices.

24

Real Impacts on the Chinese Economy A reduction of 1.2% from an expected annual real rate of growth of

6.5% leaves 5.3%, still a very respectable rate compared to the average of 3.7% for the world in 2018 projected by the International Monetary Fund (IMF). The IMF has recently lowered its projected rates of growth of world GDP for 2019 and 2020 to 3.5% and 3.6% respectively, compared to the 2.9% and 2.8% projected by the World Bank.

It is instructive to examine what transpired during the Global Financial Crisis of 2008-2009. Chinese exports of goods to the world and to the U.S. declined by 16.0% and 12.5% respectively in 2009, with a total decrease of Chinese exports of US$230 billion, approximately the same magnitude if half of Chinese exports of goods to the U.S. is completely halted in 2019. Yet the Chinese real GDP still managed to grow 9.7% and 9.4% in 2008 and 2009 respectively. What this shows is that a decline in Chinese exports of goods of this magnitude is still quite manageable. 25

Real Impacts on the Chinese Economy Bear in mind, however, that our calculation of the loss in real GDP

and other similar calculations do not take into account the effects of any possible economic stimulus measures that may be undertaken by the Chinese government. They also do not take into account the possibility of substitution of Chinese exports of goods from factories located elsewhere. For example, instead of shipping from a factory in China, the factory owner can ship goods to the U.S. from another factory it owns in Vietnam and instead ship goods to Japan from its factory in China. This would result in no decrease in its total Chinese export of goods despite the U.S. tariffs. More generally, exports of goods originally destined for the U.S. can be sold elsewhere in the world.

The same can apply to Chinese imports of goods. For example, instead of importing soybeans from the U.S., the Chinese importers can import from Brazil, and the U.S. exporters can sell to the original customers for the Brazilian soybeans. 26

Real Impacts on the Chinese Economy There is also the threat of a 25% tariff on the remaining half of

Chinese exports of goods to the U.S. (estimated to be US$290 billion according to U.S. data). Since a 25% tariff is basically prohibitive, if implemented, it will mean the total cessation of Chinese exports of goods to the U.S. The maximum damage that can be done is 2.38% (3.6% x 0.66) of GDP, which is significant but not intolerable.

However, it appears unlikely that the tariffs on this last batch of Chinese exports to the U.S. will be implemented in full because they consist of products such as the Apple iPhones (around US$50 billion), personal computers, garments and shoes and packaged re-exports of semi-conductors. The incidence of the tariffs will be mostly borne by U.S. consumers and producers including Apple Inc. (One incidental and unintended beneficiary will be Samsung of South Korea whose Galaxy cellphones compete with the Apple iPhones and they are not subject to the new tariffs on U.S. imports from China.)

27

Real Impacts on the Chinese Economy What is the impact on the Chinese trade surplus in goods and services with the

world? With a reduction of half of the total Chinese exports of goods to the U.S.,

amounting to 1.8% of Chinese GDP as a result of the trade war, a corresponding reduction in Chinese imports of goods from the U.S. is to be expected. Chinese imports of goods from the U.S. amounted to US$155 billion, or 1.18% of Chinese GDP in 2018. Assuming that half of such imports are halted because of the prohibitive Chinese tariff (for example on liquefied natural gas and soybeans), it would be 0.59% (=1.18%/2) of Chinese GDP. The net effect on the Chinese trade surplus with the world would be a negative 1.21% (1.8%-0.59%) of GDP.

This analysis does not take into account the possible diversion of Chinese exports of goods to other countries or the substitution of U.S. exports of goods to China by third country exports. It also does not take into account the possible reduction of the U.S. net trade surplus with China in services.

The Chinese trade in goods and services with the world had a surplus of 0.8% of GDP in 2018. It is likely to have a net deficit equal to 0.41% (0.8%-1.21%) of its GDP, or approximately US$54 billion. This is a relatively small amount that can be easily absorbed by the Chinese official foreign exchange reserves of US$3 trillion. Thus, there should be little pressure for the Renminbi to devalue. 28

Chinese Trade Surplus in Goods and Services

with the World and the U.S. as % of GDP

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

9

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Per

cent

Chinese Trade Surplus with the World

Chinese Trade Surplus with the U.S.29

Real Impacts on the Chinese Economy In fact, it is probably in the best interests of the Chinese economy

to maintain a relatively stable Renminbi exchange rate. By

following the CFETS Index, an index of a trade-weighted basket

of currencies, the Renminbi exchange rate will have a lower

volatility than the U.S. Dollar exchange rate because it will

move, in general, in the same direction as the U.S. Dollar but by

a smaller amount. This means when the U.S. Dollar appreciates

with respect to other currencies, the Renminbi will devalue

relative to the U.S. Dollar, and when the U.S. Dollar devalues

with respect to other currencies, the Renminbi will appreciate

relative to the U.S. Dollar. The Renminbi exchange rate will be

less volatile than the U.S. Dollar exchange rate. 30

Real Impacts on the Chinese Economy In the longer run, if tariffs continue on both sides, the U.S. importers

will begin to replace Chinese imports by imports from other Asian countries such as Vietnam, Cambodia and Bangladesh, and eventually perhaps even North Korea if an agreement can be struck between it and the U.S.

But the shift in the sourcing of imports away from China has already been occurring since 2010, because of the rise in labour costs in China and because of the appreciation of the Renminbi. This is similar to the earlier shift of the sources of U.S. imports of apparel from Hong Kong, South Korea and Taiwan to Mainland China (see the following chart). The new U.S. tariffs will accelerate this process.

The ASEAN and South Asian countries may benefit, but it is really hard to predict by how much because the supply chains today are so internationalised. However, it is unlikely, in most cases, that the tariffs will stimulate new domestic production in the U.S.

31

The Distribution of U.S. Apparel Imports by

Countries of Origin

32

Real Impacts on the Chinese Economy:

Specific Regional Impacts Even though the real impacts on the Chinese economy in the

aggregate are relatively small, they can be more significant for

individual specific municipalities and provinces, especially those

oriented towards exports.

Guangdong, including Shenzhen, is the largest exporting region

in China, followed by Shanghai and Zhejiang in second and third

places. Even then, Guangdong exports as a percent of its GDP,

which at one time had exceeded 90%, was just below 45.5% in

2018, and exports to the U.S. had fallen to only 7.9%. What this

means is that the economic growth of Guangdong is increasingly

dependent on internal demand rather than exports.

33

Real Impacts on the Chinese Economy:

Specific Regional Impacts The rate of growth of the Shenzhen real GDP in 2018 was 7.6%, a

decline of 1.2% from 2017. Exports as a percent of GDP in Shenzhen was 67.2% in 2018, and exports to the U.S. was 9.8%.

Assuming the direct domestic value-added content of Shenzhen exports to the U.S. is the same as that of China as a whole, that is, 25%, the maximum loss in Shenzhen GDP, assuming that half of the exports to the U.S. is completely halted, in the first instance may be estimated at 1.2% (9.8%/2 x 0.25). This turned out to be exactly the decline in the rate of growth of the Shenzhen real GDP in 2018.

Taking into account the indirect, that is, second-, third-, fourth- and higher-round effects of the reduction of exports, the total domestic value-added content affected increases to 66 percent. This implies ultimately a total loss in Shenzhen GDP of 3.2% (9.8%/2 x 0.66), implying a further decline of 2%. This still leaves Shenzhen with a rate of growth of 5.6% in 2019, significantly higher than the projected rate of growth of the world economy of 3.5% and that of neighbouring Hong Kong.

34

Exports to the World and the U.S. as Percent of

GDP: Shenzhen

0

50

100

150

200

250

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Per

cent

Exports to the World and Exports to the U.S. as Percentages of GDP: Shenzhen

Exports the the World as a Percent of GDP

Exports to the U.S.

35

Real Impacts on the Hong Kong Economy Hong Kong domestic exports of goods to the U.S. are not subject to

any of the new U.S. tariffs against China, whereas the Hong Kong re-exports of Chinese goods to the U.S. will be subject to the new U.S. tariffs and will be affected. Hong Kong re-exports to the U.S. grew rapidly from 1.1 percent of Hong Kong GDP to a peak of 23.3 percent in 2000, but has since fallen to 12.4 percent of Hong Kong GDP in 2018. However, the domestic Hong Kong value-added on Hong Kong re-exports of Chinese goods to the U.S. is very low, so that the real impacts on the GDP of Hong Kong will be basically negligible.

Hong Kong domestic exports to the U.S. was a highly significant 23.4 percent of the Hong Kong GDP back in 1984, but has since fallen to an insignificant 0.1 percent in 2018. Hong Kong exports of services to the U.S. amounted to 4.2 percent of Hong Kong GDP in 2018. In any case, neither Hong Kong domestic exports nor exports of services to the U.S. are subject to the new U.S. tariffs.

36

Exports to the World as Percent of GDP: Hong

Kong

0

30

60

90

120

150

180

210

1961

1963

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

Per

cen

t

Total Exports of Goods and Services

Total Exports of Goods Only

Domestic Exports of Goods Only

Re-Exports of Goods Only

37

Exports to the U.S. as Percent of GDP:

Hong Kong

0

5

10

15

20

25

30

35

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

Per

cen

t

Total Exports of Goods and Services

Total Exports of Goods Only

Domestic Exports of Goods Only

Re-Exports of Goods Only

38

Real Impacts on the Hong Kong Economy The principal real impacts of the China-U.S. trade war on the Hong

Kong economy are indirect. Actually, the Hong Kong economy has also been affected by the rise in the rates of interest globally, especially in its stock and residential housing markets, and not just by the trade war.

The sector that will be first affected is domestic consumption. The slowdown in the Mainland economy also affects the willingness of the Mainland investors to invest in Hong Kong, and also the number of Mainland tourists visiting Hong Kong as well as their level of spending. Mainland tourists to Hong Kong constitute almost 80% of the total number of tourists of 65 million per year. Of these Mainland visitors, approximately two-thirds are from the Province of Guangdong.

The reduction of tourists to Hong Kong would also affect the tour and travel, retail, lodging and food and beverage sectors in Hong Kong.

39

Real Impacts on the U. S. Economy The degree of dependence of the U.S., a large continental economy,

on exports is even lower than that of China’s. U.S. exports of goods and services combined as a share of GDP was 12.2% in 2018. The exports of goods alone as a share of GDP was only 8.2%.

Between 2017 and 2018, the shares of U.S. exports of goods and services and goods alone to China in U.S. GDP declined from 0.97% to 0.88% and 0.67% to 0.58% respectively, reflecting the effects of the trade war (all of which were borne by the exports of goods). In absolute value, they were respectively US$180 billion and US$121 billion in 2018, much lower than those of Chinese exports to the U.S. However, the shares of U.S. exports of both goods and services and goods only to China have been rising over time until more recently.

At the present time, Chinese tariffs have been imposed on US$110 billion of U.S. exports of goods, with rates up to 25%.

40

U.S. Exports of Goods and Services and Goods

Only as Percent of U.S. GDP

0

2

4

6

8

10

12

14

16

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Per

cent

Exports of Goods and Services as a Percent of GDP

Exports of Goods Only to the World as a Percent of GDP

41

U.S. Exports of Goods and Services and Goods

Only to China as Percent of U.S. GDP

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Per

cent

Exports of Goods and Services

Exports of Goods

42

Real Impacts on the U. S. Economy The direct domestic value-added content of U.S. exports of goods to

China may be estimated to be 50.8%. Thus, the maximum loss in the U.S., assuming that all of the exports to China is completely halted by the tariffs, may be estimated in the first instance at 0.29% (0.58% x 0.508), less than the initial impact on Chinese GDP of 0.43%, based on the assumption that half of Chinese exports of goods to the U.S. will be halted.

Moreover, it is unlikely that all of the U.S. exports of goods will be halted; for example, computer chips will continue to be imported by China in large quantities in the medium term. (The price elasticity is low.) Suppose only half of U.S. exports of goods to China is halted, it would amount to a loss of U.S. GDP of 0.145% (0.29%/2). This is not significant for the U.S. economy, which grew 2.9% in 2018 (2.6% in 2018Q4), as a whole. U.S. GDP per capita is approximately US$62,609. The U.S. economy can easily weather a reduction of 0.145% in its rate of growth. 43

Real Impacts on the U. S. Economy With the indirect, that is, second-, third-, fourth- and higher-round

effects of the reduction of U.S. exports of goods kicking in, the total domestic value-added affected increases to 88.7% cumulatively. This implies ultimately a total loss in U.S. GDP of 0.26% (0.58%/2 x 0.887), assuming that half of U.S. exports to China will be halted.

In absolute terms, this amounts to US$53.3 billion (0.26 x 20.5 trillion) in 2018 prices, much less than the estimated Chinese loss in terms of GDP of US$156 billion.

Thus, in both absolute and relative terms, the Chinese losses in real GDP will be much higher than those of the U.S.

However, the U.S. has a significant trade surplus in services with China, estimated to be US$40 billion by the U.S. Government but US$54 billion by the Chinese Government for 2017. This surplus may be in jeopardy if China-U.S. relations deteriorate further.

44

The Annual Rates of Growth of U.S. Exports

of Goods to the World and to China

-20

-10

0

10

20

30

40

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Per

cent

The Rate of Growth of U.S. Exports of Goods Only to the World

The Rate of Growth of U.S. Exports of Goods Only to China

45

Longer-Term Developments President Donald Trump’s primary objective is to run for and win re-

election in 2020. He will use China as a villain in the presidential election, as he did in the mid-term election. It is easy enough to bash China and he did promise that he would be tough on China during his presidential campaign in 2016. Bashing China will appeal to his base constituency of rural, non-college-educated, white males.

Moreover, Representative Nancy Pelosi, a Democrat who has been elected the Speaker of the U.S. House of Representatives, is also a persistent critic of China. So, one cannot expect a let-up of the anti-China rhetoric in the U.S. any time soon. In fact, there may be a China-bashing competition between the two parties.

By appearing to be touch on China, President Trump will be able to shield himself from attacks from the Democratic presidential candidates for being “soft on China”.

46

Longer-Term Developments One of the principal causes of the current trade war between China and the

United States is actually not trade itself, but the potential competition between China and the U.S. for economic and technological dominance in the world.

This competition, whether explicit or implicit, and whether intentional or not, will not go away soon. It did not begin with President Donald Trump. Both the “pivot to Asia” and the “Trans-Pacific Partnership” were initiated by President Barack Obama as initiatives aimed in part at containing China. It will not go away even after President Trump leaves office.

However, competition can potentially lead to constructive and positive as well as destructive and negative outcomes. For example, the competition on creating the fastest super-computer has already resulted in both countries producing better and faster super-computers. The champion in 2018 is the IBM Summit, a U.S. super-computer, which beat the Sunway TaihuLight, the champion in 2016 and 2017, a Chinese super-computer that was built entirely with indigenously designed chips. 47

Longer-Term Developments In terms of aggregate GDP, China went from only one-fifth of the

U.S. GDP in 2000 to two-thirds in 2017, taking only 17 years (64.1% in 2018 because of exchange rate changes). It is only a matter of time that the Chinese GDP will catch up with the U.S. GDP, probably in the early 2030s. However, in terms of GDP per capita, China is still way behind, with US$9,410 compared to almost US$62,609 for the U.S. in 2018. My own projections suggest that it will probably take until the end of the 21st Century before Chinese GDP per capita approaches the U.S. level.

In terms of the number of nuclear-armed warheads, according to the New York Times, the U.S. is estimated to have more than 6,000 such warheads, compared to less than 300 for China. The difference is even more striking in per capita terms. This is not a competition that China should wish to join. However, a race to find an effective cure for cancer or Alzheimer’s disease would be worthwhile for both countries and in fact for the entire mankind. 48

Longer-Term Developments U.S. grievances against China include insufficient intellectual property

rights protection, forced transfer of technology and cyber-theft. (Note that none of these grievances have much to do with trade per se.)

Intellectual property right protection in China has actually been vastly improved since special intellectual property courts were set up in Beijing, Shanghai and Guangzhou in 2014. Economically meaningful fines have begun to be levied on violators of intellectual property rights in China.

Both Japan and Taiwan in their early stages of economic development did not do much to protect intellectual property rights either. But as they changed from being a user and imitator to a creator of intellectual property, they began to enforce intellectual property rights vigorously.

Intellectual property right protection in China should get even better over time. Today, China grants the largest number of patents in the world, over 300,000 a year. And Chinese inventors and discoverers, just like their foreign counterparts, will want their intellectual property rights protected.

The way forward is to step up enforcement action in and by Chinese courts, through lawsuits filed by the victims against the perpetrators.

49

Longer-Term Developments Forced technology transfer has to do with the Chinese requirements

for foreign direct investors in certain industries to take Chinese

enterprises as equal (50-50) joint-venture partners.

However, the sharing of technology in a joint venture is a voluntary

one. The foreign direct investor will have to weigh the benefits of

having a local joint-venture partner versus the costs, including the

sharing of the technology. In any case, the technology used in the

current manufacturing process is probably already on the way to

becoming obsolete. What is more valuable is the next-generation

technology that has yet to be implemented. This is what the foreign

direct investor can still maintain as its own in its home factories and

laboratories. 50

Longer-Term Developments Forced transfer of technology is fast becoming a moot issue because

of recent Chinese liberalisation measures, including the abolition of

the joint-venture requirement. For example, in the automobile

manufacturing industry, Tesla of the U.S. has been able to establish a

wholly-owned subsidiary in Shanghai to manufacture electric cars;

Germany’s BMW has been able to increase its ownership stake in its

China automobile-manufacturing joint-venture to 75 percent; and even

though it is now possible for the U.S.’s General Motors to buy out its

Chinese joint-venture partner, it has indicated that it does not intend to

do so. Allianz of Germany and Chubb of the U.S. (based in

Switzerland) have been allowed to wholly-own insurance companies

in China. 51

Longer-Term Developments These latest policies and measures adopted by the Chinese

government and the new, much shortened negative list on foreign

direct investment should go a long way towards eliminating the issue

of forced technology transfer and market access.

If a foreign direct investor is no longer required to take an equal

domestic joint-venture partner, there is no transfer of technology, and

certainly no forced transfer of technology.

The newly passed foreign-investment law is a step in the right

direction. The expectation is that China will continue to open its

economy to international trade in goods and services and to both

inbound and outbound cross-border direct investment on a reciprocal

basis, regardless of the outcome of the China-U.S. trade war. 52

Longer-Term Developments The best solution is for China to grant national treatment to all

foreign direct investors on a reciprocal basis (with national

security consideration being the only possible exception).

Commercial cyber-thefts should be vigourously prosecuted, with

the collaboration and cooperation of both governments.

If Huawei is perceived as a national security risk by the U.S., will

the Apple iPhone be considered a national security risk by China

eventually?

53

Longer-Term Developments Another issue is that of “state-owned enterprises (SOEs)”. I believe

Chinese SOEs are here to stay. One should be specific as to why one objects to SOEs. It can be either behaviour, for example, anti-competitive behavior such as predatory pricing, or attempting to monopolise the market, etc.; or it can be government subsidies; or it can be something else. It is much more effective and productive to focus on the behaviour of the enterprises and discriminatory treatment by the government rather than the ownership. Otherwise, if all firms, domestic (state-owned or private), joint-venture and foreign firms are granted national treatment, it will be a level playing field for all. (National security considerations will be the only acceptable exception.)

Basic research will be financed and supported by the government and non-profit organization as is done in all countries including the U.S.

54

Projections of the Future: Long-Term Forecasts

of the Chinese and the U.S. Economies It is assumed that the Chinese economy will continue to grow above 6% per annum

for a few more years, declining gradually to between 5% and 6%, and that the U.S.

economy will grow at an average rate of 3% per annum between now and 2050.

In 2018, the Chinese economy grew 6.6%. The 2019 target growth rate for the

Chinese economy is between 6% and 6.5%. In 2019Q1, the Chinese economy

grew 6.4%. In 2018, the U.S. economy grew at 2.9%. But both the U.S. Federal

Reserve Board and the U.S. Congressional Budget Office expect 2.3% growth for

2019.

It may be thought that the Chinese economy will be unable to sustain an average

annual rate of growth of between 5% and 6% for such a long time. Experience

shows that the rate of growth of an economy declines as its real GDP per capita

rises. But given the still relatively low level of real GDP per capita in China, and

the low level of its capital per unit labor, such a rate of growth should still be

possible for at least several decades (see the following chart in which the

experiences of China, Japan and the U.S. are compared.)55

Growth Rate vs. Level of Real GDP per Capita

(2017 tril. US$): China, Japan and the U.S.

-30

-20

-10

0

10

20

30

0 10 20 30 40 50 60Per

cent

Real GDP per Capita, thousand USD, in 2017 prices

Rate of Growth of Real GDP vs. Real GDP per Capita (in 2017 US Dollars)

China USA Japan

56

Projections of the Future: Long-Term Forecasts

of the Chinese and the U.S. EconomiesThe Chinese national savings rate is very high, which

enables a very high investment rate. The capital-labour ratio of the Chinese economy is still very low compared to the U.S. and Japan. There is a great deal of room to grow.

In addition, there is still significant surplus labour in the Chinese economy. The share of employment in the primary sector is around 30% whereas the share of GDP originating from the primary sector is below 10%.

The projections of Chinses and U.S. real GDP and real GDP per capita between now and 2050 are presented in the following charts. 57

Projections of the Chinese and the U.S.

Economies In his work report to the Nineteenth National Congress of the

Communist Party of China, President XI Jinping identified several milestones in his speech at the Nineteenth Party Congress at 2020, 2035 and 2050.

The first milestone is to become a moderately well-off society by 2020. Our projections show that by 2020, Chinese real GDP per capita (in 2018 prices) will exceed US$10,582 (compared to US$65,541 for the U.S.).

Our projections also show that by 2033, Chinese real GDP will surpass U.S. real GDP (US$32.7 trillion versus US$31.9 trillion), making China the largest economy in the world. However, in terms of real GDP per capita, China will still lag behind significantly, with US$22,088 compared to US$89,363 for the U.S.

58

Projections of the Chinese and the U.S.

Economies By 2050, Chinese real GDP will reach US$83 trillion

compared to US$53 trillion for the U.S. In terms of real

GDP per capita, China will reach US$53,408, still below the

current (2018) level of U.S real GDP per capita of

US$62,609, compared to US$138,693 for the U.S.

It will not be until the end of the 21st Century for the

Chinese real GDP per capita to catch up with the U.S. real

GDP per capita.

59

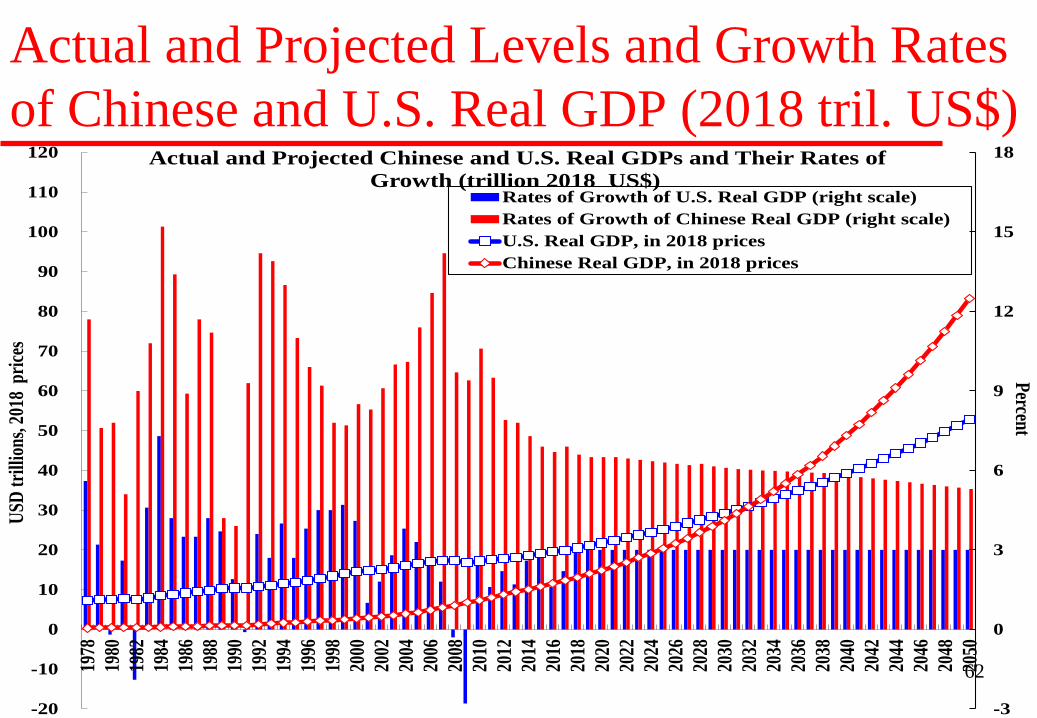

Actual and Projected Levels and Growth Rates

of Chinese and U.S. Real GDP (2018 tril. US$)

-3

0

3

6

9

12

15

18

21

24

-5

0

5

10

15

20

25

30

35

40

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

Percent

USD

tri

llion

s, 2

018

pri

ces

Actual and Projected Chinese and U.S. Real GDPs and Their Rates of

Growth (trillion 2018 US$)

Rates of Growth of U.S. Real GDP (right scale)

Rates of Growth of Chinese Real GDP (right scale)

U.S. Real GDP, in 2018 prices

Chinese Real GDP, in 2018 prices

60

Actual and Projected Chinese and U.S. Real GDP/Capita

and Their Annual Rates of Growth (1,000 2018 US$ & %)

-4

-2

0

2

4

6

8

10

12

14

16

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

85

90

95

100

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

percentU

SD th

ousa

nd, 2

018

pric

es

Actual and Projected Chinese and U.S. Real GDP per Capita and Their Rates of

Growth (thousand, 2018 US$)

Rates of Growth of U.S. Real GDP per capita (right scale)

Rates of Growth of Chinese Real GDP per Capita (right scale)

U.S. Real GDP per Capita, in 2018 prices

Chinese Real GDP per capita, in 2018 prices

61

Actual and Projected Levels and Growth Rates

of Chinese and U.S. Real GDP (2018 tril. US$)

-3

0

3

6

9

12

15

18

-20

-10

0

10

20

30

40

50

60

70

80

90

100

110

120

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

2032

2034

2036

2038

2040

2042

2044

2046

2048

2050

Percent

USD

tri

llion

s, 2

018

pri

ces

Actual and Projected Chinese and U.S. Real GDPs and Their Rates of

Growth (trillion 2018 US$) Rates of Growth of U.S. Real GDP (right scale)

Rates of Growth of Chinese Real GDP (right scale)

U.S. Real GDP, in 2018 prices

Chinese Real GDP, in 2018 prices

62

Actual and Projected Chinese and U.S. Real GDP/

Capita and Their Rates of Growth (1,000 2018 US$)

-4

-2

0

2

4

6

8

10

12

14

16

-40

-20

0

20

40

60

80

100

120

140

160

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

2032

2034

2036

2038

2040

2042

2044

2046

2048

2050

percentU

SD th

ousa

nd, 2

018

pric

es

Actual and Projected Chinese and U.S. Real GDP per Capita and Their Rates of

Growth (thousand, 2018 US$)

Rates of Growth of U.S. Real GDP per capita (right scale)

Rates of Growth of Chinese Real GDP per Capita (right scale)

U.S. Real GDP per Capita, in 2018 prices

Chinese Real GDP per capita, in 2018 prices

63

Technological Competition Technological competition is motivated by national security

considerations as well as commercial considerations. No individual or firm will want to give away or sell its core

competence. In old China, masters typically do not teach their apprentices everything, unless they are male lineal descendants.

It should therefore not be surprising that nations will protect their core competences,

In the case of the atomic bomb—the former Soviet Union developed it independently; China developed it independently, without any foreign assistance; the U.K., France, India, Pakistan and even North Korea developed their nuclear bombs independently.

China will have to continue to develop its own advanced semiconductor, artificial intelligence, and aircraft industries as it may not be able to import the best available from other countries.

64

Investment in Intangible Capital (Human and

R&D Capital) Investment in intangible capital (human capital and Research and

Development (R&D) capital) is indispensable for innovation. The annual expenditure on R&D as percentages of GDP are

presented for selected economies in the following chart. The chart shows that the U.S. has consistently invested a

relatively high percentage of its GDP in R&D, averaging 2.5% since 1963. The East Asian economies, including Mainland China, has been catching up fast, with the exception of Hong Kong.

China is expected to reach its target of 2.5% of GDP in 2020, approximately the same as the average U.S. share over the past more than fifty years. However, it will still be below the expected or targeted levels of the European countries (France, Germany and the U.K.), Japan and South Korea.

65

R&D Expenditures as a Share of GDP and Their Target Levels

at 2020: G-7 Countries, 4 East Asian NIEs, China & Israel

Japan

Germany, U.K.,

France

China

Italy

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2020

Taregt P

ercentP

erce

nt

R&D Expenditures as a Ratio of GDP: G-7 Countries, 4 East Asian NIEs, China & Israel

U.S. Japan W. Germany

Germany U.K. France

Canada Italy South Korea

Singapore Taiwan, China Mainland, China

HK, China Israel

66

Investment in Intangible Capital (R&D

Capital) One indicator of the potential for technical progress is the number of

patents created each year. In the following chart, the number of patents granted in the United States each year to the nationals of different countries, including the U.S. itself, over time is presented.

The U.S. is the undisputed champion over the past forty years, with 140,969 patents granted in 2015, followed by Japan, with 52,409. (Since these are patents granted in the U.S., the U.S. may have a home advantage; however, for all the other countries and regions, the comparison across them should be fair.)

The number of patents granted to Mainland Chinese applicants each year has increased from the single-digit levels prior to the mid-1980s to 8,166 in 2015.

The economies of South Korea and Taiwan, granted 17,924 and 11,690 U.S. patents respectively in 2015, were far ahead of Mainland China. In contrast, the number of U.S. patents granted to Hong Kong nationals was only 601 in 2015. 67

Patents Granted in the United States: G-7

Countries, 4 East Asian NIEs, China & Israel

68

Investment in Intangible Capital (R&D

Capital) The R&D capital stock, defined as the cumulative past real

expenditure on R&D less depreciation of 10% per year, is an useful indicator of innovative capacity. R&D expenditure should quite properly be treated as investment since R&D efforts generally take years to yield any results.

The R&D capital stock can be shown to have a direct causal relationship to the number of patents granted (see the following chart, in which the annual number of U.S. patents granted is plotted against the R&D capital stock of that year for each economy).

The chart shows clearly that the higher the stock of R&D capital of an economy, the higher is the number of patents granted to it by the U.S.

69

U.S. Patents Granted and R&D Capital Stocks:

G-7 Countries, 4 EANIEs, China & Israel

0

1

10

100

1,000

10,000

100,000

1,000,000

0 1 10 100 1,000 10,000

Nu

mb

er o

f U

.S. P

aten

ts G

ran

ted

R&D Capital Stocks, in 2016 US$ billions

Canada France

Germany Italy

Japan United Kingdom

United States China

Hong Kong, China South Korea

Singapore Taiwan, China

Israel Linear Regression

𝒚 = 2.160 + 1.145 𝐱 (0.126) (0.025)

70

Investment in Intangible Capital (R&D

Capital) In order for break-through discovery or invention to be made,

there must be significant investment in basic research. Basic research is by definition patient and long-term research.

The rate of return, at any reasonable discount rate, will be low. It must therefore be financed by the government or non-profit institutions and not by for-profit firms.

The atomic and hydrogen bombs, the nuclear reactors, the internet, the packets transmission technology and the browser are all outcomes of basic research done many years ago.

However, Chinese investment in basic research has remained low relative to the other major countries (see the following chart). China devoted only 5 percent of its R&D expenditures to basic research, compared to the more than 15 percent of the U.S.

71

Basic Research Expenditure as a Share of Total

R&D Expenditure: Selected Countries

72

Promoting Mutual Economic Interdependence The problem with a trade war is that there are no real winners—both

countries lose because the feasible choices open to each of them are

reduced.

Exporters in both countries will be hurt because of the reduction in

their exports, and importers in both countries will see their businesses

decline. And the consumers and producers who rely on imported

goods and inputs in both countries will have to pay higher prices.

A better way to narrow the U.S. trade deficit with China is for the U.S.

to increase its exports of goods and services to China, especially

newly created goods and services, for example, by exporting newly

developed liquefied natural gas from Alaska and shale oil and shale

gas from the continental U.S. and producing and exporting meat (beef,

pork and poultry) instead of feed grains (corn and soybeans) to China. 73

Concluding Remarks: What is the outlook for

the Chinese economy in the near term? Even though the direct real impacts of the China-U.S. trade war are

relatively small and manageable for the Chinese economy, the uncertainty that it has created, and the negative influence it has on public confidence and expectations, have also affected the real economy.

Regardless of whether China and the U.S. can reach an agreement, once it is settled one way or the other, it will at least eliminate the uncertainty. And firms and households can make their investment and consumption decisions accordingly.

The Chinese Government is expected to implement cuts in its tax rates, including the value-added tax, corporate and individual income tax, social insurance contribution rates, and continue investing in basic infrastructure projects such as high-speed railroads and urban mass-transit systems. Additional investments in public goods provisions such as environmental preservation, protection and restoration are also possible, especially if an agreement fails to materialise as expected.

The Chinese economy should be able to achieve a real rate of growth of at least 6% in 2019 even though the level of its exports may decline.

74

Concluding Remarks The competition between China and the U.S., whether friendly or

unfriendly, can be assumed to be an ongoing and long-term one. It is the “new normal”. The trade dispute is only a symptom of the potential possible conflicts between the two countries.

Graham Allison, a professor at the Kennedy School of Harvard University, has written about the inevitability of a China-U.S. war. As a rising power challenges the dominance of an established power, the established power is likely to respond with force. He refers to this “inevitability” as the “Thucydides Trap”, drawing on the book by Thucydides, History of the Peloponnesian War.

However, the rise of the former Soviet Union between the end of the Second World War and 1990 provides a counter-example that an established power and a rising power must go to war. The truth is that a thermonuclear war today is so devastating that there are effectively no real winners.

75

Concluding Remarks To reduce the probability of an armed conflict between China and the

U.S. down the road, China-U.S. relations must be carefully managed going forward. Both countries should promote greater mutual economic interdependence, to make their relations win-win, so that a war between them would be unthinkable, just as another war between France and Germany, which fought three wars between them, in 1870, 1914 and 1939, is not possible today.

It is likely that the China-U.S. trade negotiations will be stretched out, perhaps with an interim “understanding”, and that the U.S. tariffs on the remaining approximately half of Chinese exports of goods to the U.S. (US$290 billion in 2018 according to U.S. data) will be put on hold. I believe a complete rupture of the China-U.S. relation is unlikely as the U.S. still needs Chinese cooperation on such issues as North Korean denuclearization and large U.S. corporations still have significant interests in the large and growing Chinese market. China also needs the U.S. to supply critical semi-conductors and semi-conductor manufacturing equipment.

76

Concluding Remarks President Donald Trump is focused solely on his re-election in 2020.

Signing an agreement with China will most certainly expose him to attacks by his Democratic opponent(s). Dragging things out is not such a bad strategy because it shows that he is tough on China and that he will not hesitate to walk away from a “bad deal”. No one will attack him openly for no agreement.

President XI Jinping is also not likely to accept any terms that appear to infringe on Chinese sovereignty because it may arouse domestic discontent and possible opposition. Accepting U.S. terms under duress also creates moral hazard and encourages similar behaviour in the future.

Moreover, the Chinese side is also concerned about the possibility of imposition of last-minute additional conditions by the U.S. as in the Trump-Kim summit in Hanoi. In addition, if even Kim Jong-Un can refuse to accept last-minute U.S. conditions, it is most unlikely that President XI Jinping will be willing or able to accept them. 77

Concluding Remarks China and the rest of the world, except possibly the U.S., will

continue to uphold the current multilateral trading system under the World Trade Organisation (WTO). After all, they have all benefitted and will continue to benefit from it.

China should avoid turning inward or becoming isolated. It should continue to open its economy to international trade and both inbound and outbound direct investment, by lowering tariffs, reducing non-tariff barriers and offering national treatment to foreign direct investors on a reciprocal basis.

Maintaining good economic relations with the rest of the world, and opening its economy further to international trade and investment, in particular, to the European Union, ASEAN, Japan and Russia on a reciprocal basis, is a must for China going forward.

78

Concluding Remarks In the long run, if China and the U.S. cooperate and work

together, many global problems such as prevention of climate change, denuclearisation, and the economic development of Africa, can be solved.

China and the U.S. can both collaborate and compete in finding cures for diseases such as cancer and Alzheimer’s disease, and every country in the world will benefit from it.

The U.S. can invite China to participate in the exploration of Mars and share in the cost, which has been estimated to be hundreds of billions of U.S. dollars.

If the two countries compete in a friendly way, much innovation is possible, as in the competition to build the fastest super-computer. The two countries should aim to become competitive partners!

79