the commonwealth fund the commonwealth fund realizing health reform’s potential: small businesses...

TRANSCRIPT

THE COMMONWEALTH

FUND

THE COMMONWEALTH

FUND

Realizing Health Reform’s Potential: Small Businesses and the Affordable Care Act of

2010

Sara R. Collins, Ph.D.Vice President, Affordable Health Insurance

The Commonwealth Fund

Media TeleconferenceSeptember 1, 2010

THE COMMONWEALTH

FUND

Exhibit 1. Workers in Small Firms Are More Likely to be Uninsured

Percent of wage and salary workers ages 18-64 who are uninsured

Source: P. Fronstin, Sources of Health Insurance and Characteristics of the Uninsured: Analysis of the March 2009 Current Population Survey, EBRI, No. 334, September 2009.

35.7

29.9

20.7

15.513.3 13.5

0

10

20

30

40

50

Less than10 workers

10-24workers

25-99workers

100-499workers

500-999workers

1,000 ormore

workers

THE COMMONWEALTH

FUND

Percent

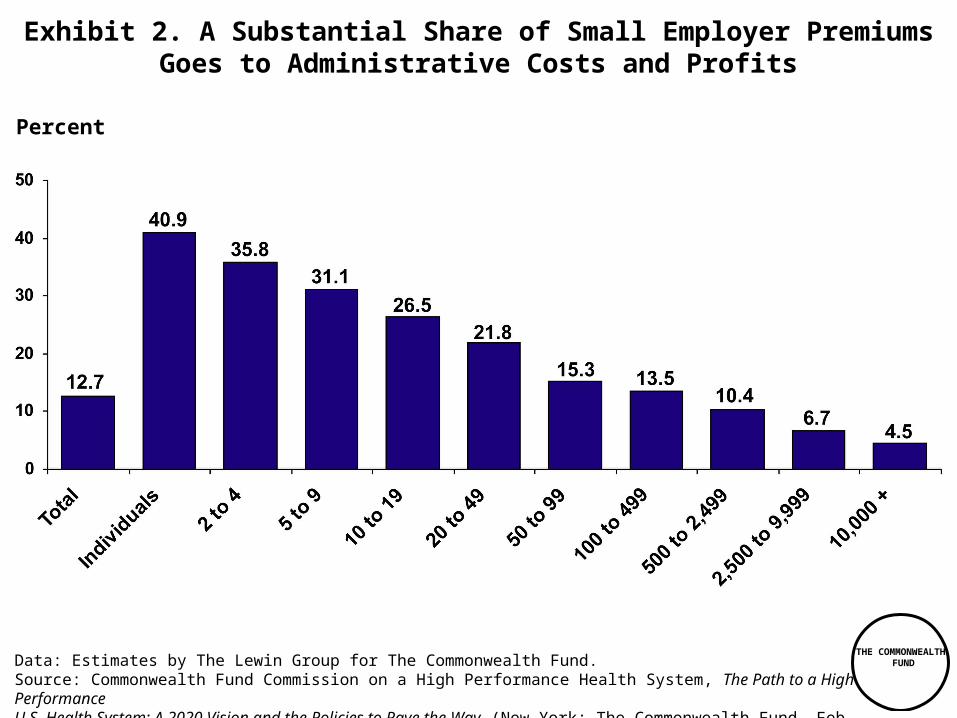

Data: Estimates by The Lewin Group for The Commonwealth Fund.Source: Commonwealth Fund Commission on a High Performance Health System, The Path to a High Performance U.S. Health System: A 2020 Vision and the Policies to Pave the Way (New York: The Commonwealth Fund, Feb. 2009).

Exhibit 2. A Substantial Share of Small Employer Premiums Goes to Administrative Costs and Profits

THE COMMONWEALTH

FUND

Exhibit 3. More Than Half of Working Adults in Small Firms Were Uninsured or Underinsured During the Year, 2007

Small Firms (fewer than 50 employees)39.0 million

Uninsured anytime36%

Underinsured16%

Adequately insured48%

Uninsured anytime15%

Underinsured13%

Adequately insured73%

Large Firms (50 or more employees)76.9 million

Notes: Includes both part-time and full-time workers. Underinsured is defined as having continuous health insurance coverage and spending 10 percent or more of income on out-of-pocket health care costs (or 5 percent or more if low income), or having deductibles of 5 percent or more of income.Source: The Commonwealth Fund Biennial Health Insurance Survey (2007).

THE COMMONWEALTH

FUND

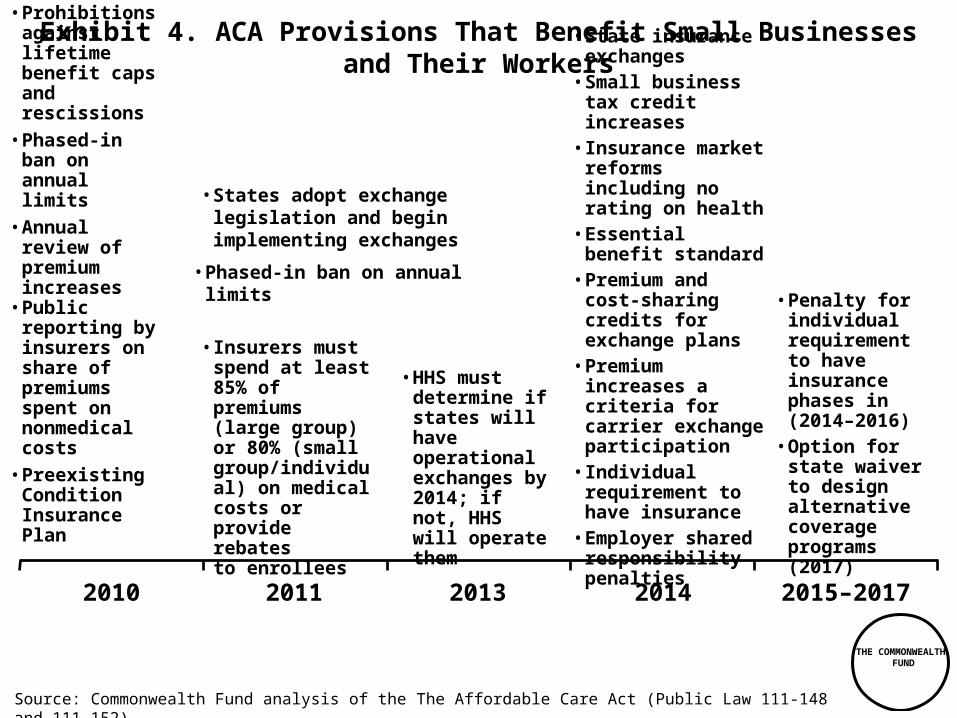

Exhibit 4. ACA Provisions That Benefit Small Businesses and Their Workers

• Small-business tax credit

• Prohibitions against lifetime benefit caps and rescissions

• Phased-in ban on annual limits

• Annual review of premium increases

• Public reporting by insurers on share of premiums spent on nonmedical costs

• Preexisting Condition Insurance Plan

Source: Commonwealth Fund analysis of the The Affordable Care Act (Public Law 111-148 and 111-152).

• Insurers must spend at least 85% of premiums (large group) or 80% (small group/individual) on medical costs or provide rebates to enrollees

• HHS must determine if states will have operational exchanges by 2014; if not, HHS will operate them

• State insurance exchanges

• Small business tax credit increases

• Insurance market reforms including no rating on health

• Essential benefit standard

• Premium and cost-sharing credits for exchange plans

• Premium increases a criteria for carrier exchange participation

• Individual requirement to have insurance

• Employer shared responsibility penalties

• Penalty for individual requirement to have insurance phases in (2014–2016)

• Option for state waiver to design alternative coverage programs (2017)

• States adopt exchange legislation and begin implementing exchanges

• Phased-in ban on annual limits

2010 2011 2013 2014 2015–2017

THE COMMONWEALTH

FUND

Exhibit 5. Small Employer Tax Credit, 2010

• Starting with taxable year 2010, small employers will be eligible for new tax credits to offset their premium costs, they may claim the credits on their 2010 tax returns for premium costs incurred in 2010.

• Eligible companies are those with fewer than 25 employees and with average wages under $50,000.

• The full credit will be available to companies with 10 or fewer employees and average wages of $25,000 or less, phasing out for larger firms.

• Eligible businesses will have to contribute at least 50 percent of their employees' premiums.

• For tax years 2010–13, the full credit will cover 35 percent of a company's premium contribution, 25 percent for tax-exempt organizations, which receive refundable credits

• An estimated 16.6 million workers are in firms that will be eligible for the tax credit by 2013, 3.4 million are estimated to be in firms that take-up the credit.

• Beginning in 2014, the full credit will cover 50 percent of the contribution, 35 percent for tax-exempt organizations, for plans purchased through insurance exchanges, for a two-year period.

• This means that the credits are available for eligible firms for up to six years.

• For-profit businesses with no taxable income in one year may carry the credit forward, or back (but not in 2010)

THE COMMONWEALTH

FUND

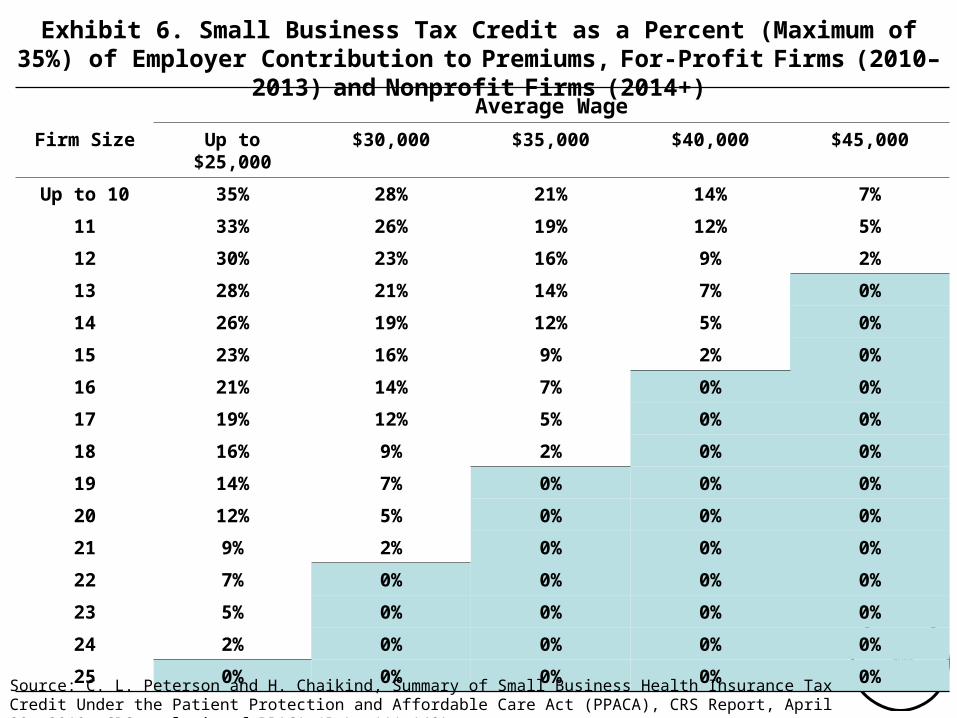

Exhibit 6. Small Business Tax Credit as a Percent (Maximum of 35%) of Employer Contribution to Premiums, For-Profit Firms (2010–2013) and Nonprofit Firms (2014+)

Average Wage

Firm Size Up to $25,000 $30,000 $35,000 $40,000 $45,000

Up to 10 35% 28% 21% 14% 7%

11 33% 26% 19% 12% 5%

12 30% 23% 16% 9% 2%

13 28% 21% 14% 7% 0%

14 26% 19% 12% 5% 0%

15 23% 16% 9% 2% 0%

16 21% 14% 7% 0% 0%

17 19% 12% 5% 0% 0%

18 16% 9% 2% 0% 0%

19 14% 7% 0% 0% 0%

20 12% 5% 0% 0% 0%

21 9% 2% 0% 0% 0%

22 7% 0% 0% 0% 0%

23 5% 0% 0% 0% 0%

24 2% 0% 0% 0% 0%

25 0% 0% 0% 0% 0%

Source: C. L. Peterson and H. Chaikind, Summary of Small Business Health Insurance Tax Credit Under the Patient Protection and Affordable Care Act (PPACA), CRS Report, April 20, 2010, CRS analysis of PPACA (P.L. 111-148).

THE COMMONWEALTH

FUND

Exhibit 7. Small Business Tax Credits Under Affordable Care Act for Family Premiums

* To be eligible for tax credits, firms must contribute 50% of premiums. Firms receive 35% and later 50% of their contribution in tax credits.Note: Projected premium for a family of four in a medium-cost area in 2009 (age 40). Premium estimates are based on actuarial value = 0.70. Actuarial value is the average percent of medical costs covered by a health plan.Small businesses are eligible for new tax credits to offset their premium costs in 2010. Tax credits will be available for up to a two-year period, starting in 2010 for small businesses with fewer than 25 employees and with average wages under $50,000. The full credit will be available to companies with 10 or fewer employees and average wages of $25,000, phasing out for larger firms. Eligible businesses will have to contribute 50 percent of their employees' premiums. Between 2010–13, the full credit will cover 35 percent of a company's premium contribution. Beginning in 2014, the full credit will cover 50 percent of that contribution. Tax-exempt organizations will be eligible to receive the tax credits, though the credits are somewhat lower: 25 percent of the employer's contribution to premiums in 2010–13 and 35 percent beginning in 2014. Source: Commonwealth Fund analysis of Affordable Care Act (Public Law 111-148 and 111-152). Premium estimates are from Kaiser Family Foundation Health Reform Subsidy Calculator, http://healthreform.kff.org/Subsidycalculator.aspx.

$9,435—projected family premium

50% employer contribution

$4,718*

Credit per employee

THE COMMONWEALTH

FUND

Exhibit 8. State Insurance Exchanges, 2014

• Each state must establish insurance exchanges by 2014 for individuals and small employers; federal grants available March 2011-Jan 2015 to states; HHS will operate exchanges in states that opt not to do so.

• Individual and small-group markets are not replaced by exchanges, but same market rules apply inside and outside the exchanges.

• States can provide single exchange for individuals and small employers.

• In 2014, small businesses with up to 100 employees will be able to offer plans to employees through the exchanges; states have option until 2016 to limit enrollment to those with 50 employees.

• After 2017 states may open the exchanges to employers with more than 100 employees.

• Small employer tax credits (2014) and individual premium and cost sharing subsidies, can be used only for plans purchased through the exchanges.

THE COMMONWEALTH

FUND

Exhibit 9. Essential Benefit Package Under Affordable Care Act

Four levels of cost-sharing

1st tier (Bronze) actuarial value: 60%2nd tier (Silver) actuarial value: 70%3rd tier (Gold) actuarial value: 80%4th tier (Platinum) actuarial value: 90%

Employers offering through exchange may provide premium support for a level of coverage and employees may choose a plan within the designated level

Out-of-pocket maximum capped at HSA level of

$5,950 for individuals and $11,900 for families

Deductibles for small group policies cannot exceed $2,000 for individuals, $4,000 for families

Catastrophic policy with essential benefit package for those < age 30 or who cannot find premium <8% of income

Note: Actuarial values is the average percent of medical costs covered by a health plan.Source: Commonwealth Fund analysis of Affordable Care Act (Public Law 111-148 and 111-152).

THE COMMONWEALTH

FUND

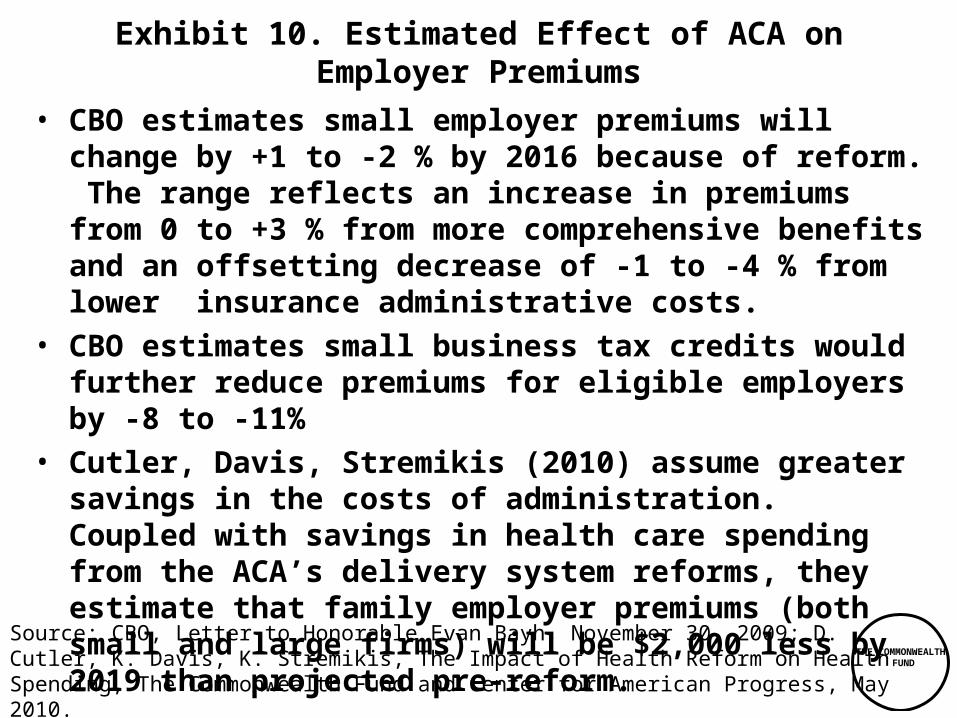

Exhibit 10. Estimated Effect of ACA on Employer Premiums

• CBO estimates small employer premiums will change by +1 to -2 % by 2016 because of reform. The range reflects an increase in premiums from 0 to +3 % from more comprehensive benefits and an offsetting decrease of -1 to -4 % from lower insurance administrative costs.

• CBO estimates small business tax credits would further reduce premiums for eligible employers by -8 to -11%

• Cutler, Davis, Stremikis (2010) assume greater savings in the costs of administration. Coupled with savings in health care spending from the ACA’s delivery system reforms, they estimate that family employer premiums (both small and large firms) will be $2,000 less by 2019 than projected pre-reform.

Source: CBO, Letter to Honorable Evan Bayh, November 30, 2009; D. Cutler, K. Davis, K. Stremikis, The Impact of Health Reform on Health Spending, The Commonwealth Fund and Center for American Progress, May 2010.

THE COMMONWEALTH

FUND

Exhibit 11. Individual Premium CreditsUnder Affordable Care Act

Premium contributions for silver plan coverage through insurance exchanges are limited as a share

of income to:

Up to 133% FPL: 2.0%

133%–150% FPL: 3.0–4.0%;

150%–200% FPL: 4.0–6.3%;

200%–250% FPL: 6.3%–8.05%;

250%–300% FPL: 8.05%–9.5%;

300%–400% FPL: 9.5%

Note: FPL refers to Federal Poverty Level.Source: Commonwealth Fund analysis of Affordable Care Act (Public Law 111-148 and 111-152).

THE COMMONWEALTH

FUND

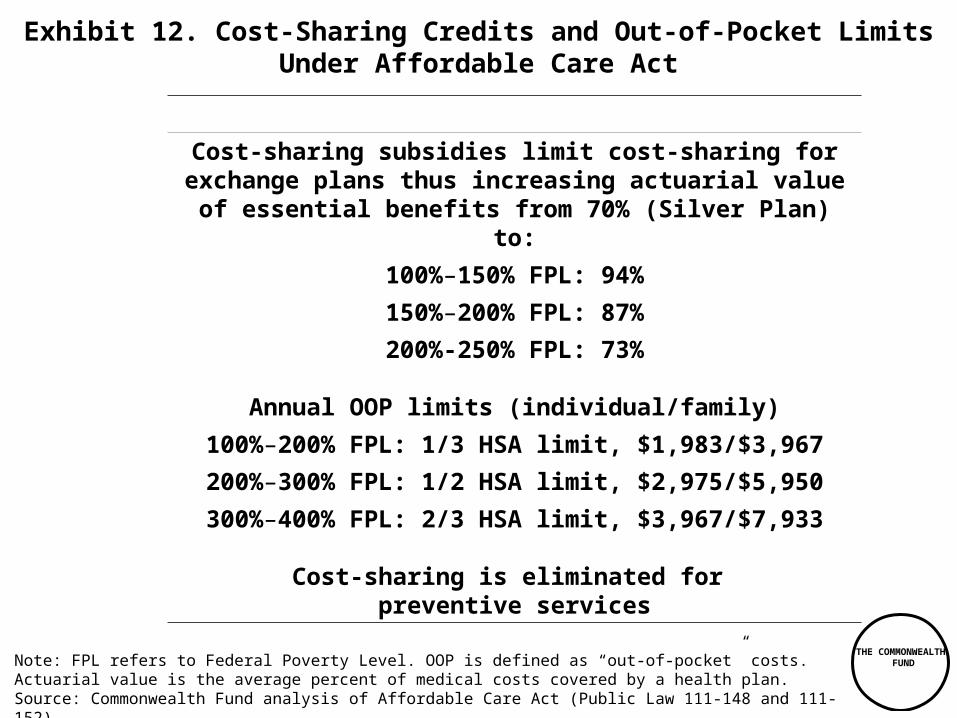

Exhibit 12. Cost-Sharing Credits and Out-of-Pocket LimitsUnder Affordable Care Act

Cost-sharing subsidies limit cost-sharing for exchange plans thus increasing actuarial value of essential benefits

from 70% (Silver Plan) to:

100%–150% FPL: 94%

150%–200% FPL: 87%

200%-250% FPL: 73%

Annual OOP limits (individual/family)

100%–200% FPL: 1/3 HSA limit, $1,983/$3,967

200%–300% FPL: 1/2 HSA limit, $2,975/$5,950

300%–400% FPL: 2/3 HSA limit, $3,967/$7,933

Cost-sharing is eliminated for preventive services

Note: FPL refers to Federal Poverty Level. OOP is defined as “out-of-pocket” costs. Actuarial value is the average percent of medical costs covered by a health plan.Source: Commonwealth Fund analysis of Affordable Care Act (Public Law 111-148 and 111-152).

THE COMMONWEALTH

FUND

Exhibit 13. Conclusion: Leveling the Playing Field

• The combination of provisions in the ACA enabling small firms to offer high value benefits to their employees will: – allow companies to protect their employees from

catastrophic health care costs– reduce the considerable disadvantage that small

businesses have had in the labor market, allowing them to recruit and retain high quality workers

• The ACA will also reduce the high uninsured and underinsured rates among small firm workers, equalizing access to comprehensive health insurance for all American workers regardless of health, economic circumstances, or employment status