the credit suisse commodity index framework · pdf filelondon, monday, 29 october 2012 v1.00,...

TRANSCRIPT

London, Monday, 29 October 2012

v1.00, H1-2013

Commodity Group

Credit Suisse Commodity Index Framework

The Credit Suisse Backwardation UCITS Index (CSCU4BK)

Page 1

The Credit Suisse Commodity Index Framework Summary Operating Manual

The Credit Suisse Backwardation UCITS Index (CSCU4BK)

B1. Index Parameters

B. Index Parameters

Oct-13

Disclaimers and Legal Considerations

Executive Summary - General Index Characteristics

CSCU4BK Index Advisory Committee

Index publication

1. Key Index Terms and Definitions

2. The CSCU4BK Allocation Model

3. CSCU4BK Index Parameters

Appendixes

This Section B1. Index Parameters should be read in

conjunction with Section A. Core Index Methodology and is an

abridged version of the full Section B. Index Parameters.

Capitalised terms used but not defined herein shall have the

meaning ascribed to them in Section A.

Section A. and Section B. together constitute the Index

Operating Manual in respect of the Credit Suisse

Backwardation UCITS Index (CSCU4BK).

London, Monday, 29 October 2012

v1.00, H1-2013

Commodity Group

Credit Suisse Commodity Index Framework

The Credit Suisse Backwardation UCITS Index (CSCU4BK)

Page 2

Summary

Contents Disclaimers and Legal Considerations ............................................................................................ 3

Executive Summary - General Index Characteristics ....................................................................... 7

Index publication ............................................................................................................................ 8

1. Key Index Terms and Definitions ................................................................................................. 0

2. The CSCU4BK Allocation Model ............................................................................................... 2

3. CSCU4BK Index Parameters ..................................................................................................... 6

Appendix ..................................................................................................................................... 11

London, Monday, 29 October 2012

v1.00, H1-2013

Commodity Group

Credit Suisse Commodity Index Framework

The Credit Suisse Backwardation UCITS Index (CSCU4BK)

Page 3

Disclaimers and Legal Considerations

This disclaimer extends to CSi, its affiliates or it’s designate in any of its capacities as Index Sponsor,

Index Calculation Agent and its constitution of the Index Advisory Committee, and Framework Steering

Committee, and any reference to CSi shall also mean a reference to its affiliates or designates in any

such capacity.

This document is published by CSi. CSi is authorised by the Prudential Regulation Authority (“PRA”)

and regulated by the Financial Conduct Authority (“FCA”) and the PRA. Notwithstanding that CSi is so

authorised and regulated, the rules of neither the PRA nor the FCA are incorporated into this

document.

The Index Sponsor and the Index Calculation Agent are the same entity and the members of the

Framework Steering Committee and Index Advisory Committee may be employed by Credit Suisse AG

and CSi or its affiliate may be the issuer of the Investment Products. CSi and its affiliates may,

therefore, in each of its capacities face a conflict in its obligations carrying out such role with investors

in the Investment Products and may resolve such conflict in its own interests.

CSi is described as Index Sponsor under the Core Index Methodology and the Index. CSi may transfer

or delegate to another entity, at its discretion, the authority associated with the role of Index Sponsor

under the Index Operating Manual.

The Signals assigned through the CSi proprietary models are rule based, and in the absence of any

special event provided for in the Index Operating Manual, are not at the discretion of CSi.

This document is published for information purposes only and CSi expressly disclaims (to the fullest

extent permitted by applicable law) all warranties (express, statutory or implied) regarding this

document the Core Index Methodology or the Index, including but not limited to all warranties of

merchantability, fitness for a particular purpose of use and all warranties arising from course of

performance, course of dealing or usage of trade and their equivalents under applicable laws of any

jurisdiction.

CSi or its affiliates may offer securities or other financial products including the Investment Products

the return on which is linked to the performance of the Index. This document is not to be used or

considered as an offer or solicitation to buy or subscribe for such financial products nor is it to be

considered to be or to contain any advice or a recommendation with respect to such financial products.

Before making an investment decision in relation to such financial products one should refer to the

prospectus or other disclosure document relating to such financial products.

Trading and other transactions by CSi and/or its affiliates in the futures contracts comprising the Index

and the underlying commodities may affect the value of the Index, and there may be conflicts of

interest between investors in the Index and CSi and/or its affiliates. The Index is based on

commodities futures contracts as described in the Core Index Methodology. CSi and/or its affiliates

actively trade futures contracts and options on futures contracts on these commodities. CSi and/or its

affiliates also actively enter into or trade and market securities, swaps, options, derivatives, and related

instruments which are linked to the performance of these commodities or are linked to the

performance of the Index. CSi and/or its affiliates may underwrite or issue other securities or financial

instruments indexed to the Index, and CSi or its affiliates may license the Index for publication or for

use by unaffiliated third parties. These activities could present conflicts of interest and could affect the

value of the Index. For instance, a market maker in a financial instrument linked to the performance of

the Index may expect to hedge some or all of its position in that financial instrument. Purchase (or

selling) activity in the futures contracts included in the Index in order to hedge the market maker’s

position in the financial instrument may affect the market price of such futures contracts included in

the Index, which in turn may affect the value of the Index. With respect to any of the activities

described above, neither CSi nor its affiliates has any obligation to take the needs of any investors in

the Index into consideration at any time.

London, Monday, 29 October 2012

v1.00, H1-2013

Commodity Group

Credit Suisse Commodity Index Framework

The Credit Suisse Backwardation UCITS Index (CSCU4BK)

Page 4

CSi (including its officers, employees and delegates) shall not be under any liability to any party on

account of any loss suffered by such party (however such loss may have been incurred) in connection

with anything done, determined, interpreted, amended or selected (or omitted to be done, determined

or selected) by it in connection with the Core Index Methodology or the Index. Without prejudice to the

generality of the foregoing, CSi shall not be liable for any loss suffered by any party as a result of any

determination, calculation, interpretation, amendment or selection it makes (or fails to make) in relation

to the construction or the valuation of the Index and, once made, CSi shall not be under any obligation

to revise any calculation, determination, amendment, interpretation and selection made by it for any

reason.

The Allocation Model is a proprietary model of CSi. Neither CSi nor any of its affiliates shall be under

any liability to any party on account of any loss suffered by such party (however such loss may have

been incurred) in connection with any change in any such model, or determination or removal in

respect of such model (or omitted to be changed, determined or removed).

Neither CSi nor any of its affiliates makes any warranty or representation whatsoever, express or

implied, as to the results to be obtained from the use of the Index, or as to the performance and/or

the value thereof at any time (past, present or future).

CSi as Index Sponsor (including its officers, employees and delegates) has no obligation and will not

take into account the interests of any investors in transactions or securities linked in whole or in part to

the Index when determining, composing or calculating such Index.

CSi as Index Sponsor or as Index Calculation Agent may delegate to an affiliate or a third party some

or all of its functions and calculations in respect of the Index.

The Core Index Methodology is proprietary to CSi. Neither CSi nor any of its affiliates shall be under

any liability to any party on account of any loss suffered by such party (however such loss may have

been incurred) in connection with any change in any such model, or determination or removal in

respect of such model (or any omissions to make any such change, determination or removal).

The performance of the Index will depend, inter alia, on the performance of the underlyings in the

Index Components and the performance of the Allocation Model and CSi, therefore, makes no

guarantee or representation of any kind in relation to the performance of the Index, the level of which

may go down as well as up. Past performance of the Index is no guarantee of future performance.

CSi does not purport to be a source of information on market risks with respect to the underlyings in

any Index Component.

CSi as Index Sponsor or Index Calculation Agent does not warrant or guarantee the accuracy or

timeliness of calculations of the Index value and does not warrant or guarantee the availability of an

Index value on any particular date or at any particular time.

CSi is under no obligation to monitor whether or not a Commodity Disruption Event or an Index

Disruption Event has occurred and shall not be liable for any losses resulting from (i) any determination

that a Commodity Disruption Event or Index Disruption Event has occurred or has not occurred in

relation to an Index Component in the Index, (ii) the timing relating to the determination that a

Commodity Disruption Event has occurred in relation to an Index Component in the Index or (iii) any

actions taken or not taken by CSi as a result of such determination that an Commodity Disruption

Event or Index Disruption Event has occurred.

Unless otherwise specified, CSi shall make all calculations, determinations, amendments,

interpretations and selections in respect of the Index. CSi (including its officers, employees and

delegates) shall have no responsibility for good faith errors or omissions in its calculations,

determinations, amendments, interpretations and selections as provided in the Core Index

Methodology. The calculations, determinations, amendments, interpretations and selections of CSi

London, Monday, 29 October 2012

v1.00, H1-2013

Commodity Group

Credit Suisse Commodity Index Framework

The Credit Suisse Backwardation UCITS Index (CSCU4BK)

Page 5

shall be made by it in accordance with the Core Index Methodology and the Index Parameters, acting

in its sole, absolute and unfettered discretion, but in good faith (having regard in each case to the

criteria stipulated herein and (where relevant) on the basis of information provided to or obtained by

employees or officers of CSi responsible for making the relevant calculations, determinations,

amendments, interpretations and selections). For the avoidance of doubt, any calculations or

determinations made by CSi under the Core Index Methodology on an estimated basis shall not be

revised following the making of such calculation or determination.

CSi is the final authority on the Index and the interpretation and application of the rules in the

Operating Manual (the Core Index Methodology and the Index Parameters).

CSi may supplement, amend (in whole or in part), revise or withdraw the Index Operating Manual at

any time if the Index is no longer calculable under the Index Operating Manual. Such a supplement,

amendment, revision or withdrawal may lead to a change in the way the Index is calculated or

constructed. CSi may determine that a change to the Index Operating Manual is required to address

an error, ambiguity or omission. Such changes, for example, may include changes to eligibility

requirements or construction as well as changes to the Core Index Methodology

All amendments to the Index Operating Manual are proposed by the Index Advisory Committee via its

members. The proposed changes are approved or rejected by the Framework Steering Committee and

are documented in the Index Operating Manual.

CSi will apply the Credit Suisse Commodity Index Framework Operating Manual in a reasonable

manner and in doing so may rely upon various sources of market information.

No person may reproduce or disseminate the information contained in this document without the prior

written consent of CSi as Index Sponsor. This document is not intended for distribution to, or use by

any person in a jurisdiction where such distribution or use is prohibited by law or regulation.

The Index Operating Manual shall be governed by and construed in accordance with English law.

Investment Products

CSi or its affiliates may offer securities or other financial products (“Investment Products”) the return

on which is linked to the performance of the Index. These Investment Products may include options,

swaps, other over-the-counter derivatives, certificates and notes. The Index was developed with the

formation of such Investment Products and related hedging strategies as key commercial elements to

its development. Accordingly, CSi’s approach to the Index has been, and any change to the Index will

be, influenced by CSi’s objective of creating and maintaining a commodity index that is suitable as an

underlying for Investment Products.

Notice

These Index Rules, the Excess Return Index Level or Total Return Index Level and any other

information contained in the Index Rules may not be reproduced or disseminated in any form without

the prior written permission of Credit Suisse International. No one is permitted to use any of the

information in these Index Rules, any information contained herein or the Excess Return Index Level or

Total Return Index Level in connection with the writing, trading, marketing, or promotion of any

financial instruments or products or to create any indices.

London, Monday, 29 October 2012

v1.00, H1-2013

Commodity Group

Credit Suisse Commodity Index Framework

The Credit Suisse Backwardation UCITS Index (CSCU4BK)

Page 6

Copyright © 2009 – 2014 CREDIT SUISSE GROUP AG and/or its affiliates.

All rights reserved. "Credit Suisse", “Credit Suisse AG”, the Credit Suisse logo, "Credit Suisse

Commodity Index" are trademarks or service marks or registered trademarks or service marks of Credit

Suisse Group AG or one of its affiliates.

London, Monday, 29 October 2012

v1.00, H1-2013

Commodity Group

Credit Suisse Commodity Index Framework

The Credit Suisse Backwardation UCITS Index (CSCU4BK)

Page 7

Executive Summary - General Index Characteristics

Main Characteristics

The Credit Suisse Backwardation UCITS Index (“CSCU4BK”, or the “Index”) is a Long-Only Index

of Indexes, dynamically allocating to the components with the highest degree of backwardation

within the Investment Universe,

History: CSCU4BK was designed and launched in 2012, with Index levels back-tested to 1998,

CSCU4BK Components: The CSCU4BK Index Components are selected from the universe of

CSCB 4x6F and prompt single commodity indices. Only commodities with a CSCB Prompt target

investment weight that is greater than 1% are included into the Universe,

Weighting & Rebalancing: CSCU4BK features a monthly reweighting and rebalancing

mechanism,

Reweighting/Roll Period. In respect of a monthly Calculation Period, the Reweighting Period of

CSCU4BK takes place monthly and begins on the 5th Index Business Day of each month and ends

on the 9th Index Business Day of each month at the rate of 20% per day.

CSCU4BK Index Advisory Committee

Any amendments to the Core Index Methodology and/or Index Parameters documents are

proposed by the Index Advisory Committee via its members. The proposed changes are approved

or rejected by the Framework Steering Committee and are documented in this Index Operating

Manual.

Index documentation: structure of the Index Operating Manual

Each Index described under the Framework is documented by two separate master sections: a

section A. called Core Index Methodology which is common to all indices, and a Section B. called

Index Parameters which is specific to a given version of the Index calculation,

The Core Index Methodology provides an overall description of the Framework, describes the

meaning of Key Index Terms and provides definitions for terms and notions used throughout the

documentation. The section proposes an in-depth technical description of the calculations

performed for all indices under the Framework, regardless of the specific static data associated

with each version of the Index,

The Index Parameters section provides specific details regarding parameters used for a particular

version of the Index, such as :

The Calculation Engine,

The composition of the Index (selected from the Index Component Universe),

The weighting and/or allocation methodology and the definition of Target Investment Weights

(futures/forwards based indices) or Index Target Investment Weight (Index of Indices or

Generic Basket of Assets indices),

The Rebalancing periods,

The Roll Period,

The determination of Designated Commodity Derivatives Instruments (DCDI) and Index Pricing

Instruments (IPIs) (futures/forwards based indices),

London, Monday, 29 October 2012

v1.00, H1-2013

Commodity Group

Credit Suisse Commodity Index Framework

The Credit Suisse Backwardation UCITS Index (CSCU4BK)

Page 8

Index publication

Information relating to the Index is accessible via a wide range of sources, including Bloomberg and

Reuters, and as defined in Table II below.

TABLE II. INFORMATION ON THE INDEX

Index Name Bloomberg Ticker (Excess Return) Ticker (Total Return)

CS Backwardation UCITS CSCU4BK <index> CSCU4BKE <index> CSCU4BKT <index>

Source: Credit Suisse, Index Calculation Agent

Rounding of published Index figures

All CSCU4BK Indices are calculated with 8 decimals precision following the procedure set forth in

Section B.3.6.

Published figures are provided to 2 decimals (for avoidance of doubt, an Index level of

1234.567898765… is published as 1234.57).

London, Wednesday, 16 October 2013

v1.00, H1-2013

Commodity Group

Credit Suisse Commodity Index Framework

The Credit Suisse Backwardation UCITS Index (CSCU4BK)

Page 0

1. Key Index Terms and Definitions

1.1. Definitions

Term

Definition

Index Advisory

Committees

In respect of an Index, a committee with membership comprised of personnel

within CSi and other appropriate representatives outside the organization

relevant to such Index. The Index Advisory Committees are assigned with the

task of advising on operational and technical aspects relating to a specific

Index or Indices. The responsibilities of the Index Advisory Committees are

outlined in detail in Section A.2.

If not otherwise specified in the individual Section B of a given index, the

members of the Index Advisory Committee are as specified in Section A.2.3.

Index The “Credit Suisse Backwardation UCITS Index” or the “CSCU4BK”

Index Business Day A day on which the Index is scheduled to be published as determined by the

NYSE Euronext Holiday Schedule.

Any deviation from this schedule is ratified by the Framework Steering

Committee and is announced in advance

Index Sponsor CSi, or any successor to CSi which continues to calculate and publish the

Index. The Index Sponsor is responsible for approving certain actions under

this Index Operating Manual, giving consideration if possible to any advice

provided by the relevant Index Advisory Committee. In addition, the Index

Sponsor calculates and publishes the level of the Index in accordance with

this Index Operating Manual

London, Wednesday, 16 October 2013

v1.00, H1-2013

Commodity Group

Credit Suisse Commodity Index Framework

The Credit Suisse Backwardation UCITS Index (CSCU4BK)

Page 1

1.2. Key Index Terms

Term

Definition

Allocation Model

A Credit Suisse proprietary systematic weighting and rebalancing model to

calculate the TIW used by the Index for the relevant Reference Period

(Please see Section B.2. The CSCU4BK Allocation Model)

Allocation Calculation

Date (ACD)

The day on which the Allocation Model is run. This is defined as the 4th Index

Business Day of each month.

Applicable Universe

The universe of Index Components as selected by the Allocation Model

described in the Section B.2. The CSCU4BK Allocation Model

Static Data Calculation

Date (SDCD)

The day on which associated static data is calculated as appropriate, and

defined as the 4th Index Business Day of each calendar month (also noted

as [0(m)].

Index Component

Level

(ICL)

With respect to an Index Component c, the official closing level of such Index

Component, as published by Index Publication Agent

Index Component c

An Index Component in the Applicable Universe

Disrupted Valuation

Day

A Disrupted Valuation Day as described in Section A.5. Disruption events

and Emergency

Roll Period

The period from and including the Index Business Day following the Static

Data Calculation Date to and including the 5th Index Business Day following

the Static Data Calculation Date (also noted [+1(m);+5(m)] for the first and

fifth Index Business Days in the Reference Period m)

Reference Period

(m)

For a given Calculation Date t, the period from and including the previous

Static Data Calculation Date to and excluding the next Static Data

Calculation Date.

Investment Universe

The universe of potential Index Components for the CSCU4BK Index (Please

see B.2.0. Definition of the CSCU4BK Investment Universe).

TIW

(also TIWmc)

The absolute US dollar notional investment weight associated to the Index

Component c for a given Reference Period m as a result of the Allocation

Model (also refer to the calculation, Section B.2. The CSCU4BK Index

Allocation Model)

Index Category

In respect to an index, this is defined as the Master Categories (as defined in

Section A - Core Index Methodology ) where at least 2 components

contained in a Master Category are Index Components in the Index

Index Category

Monitor List

The Index Categories where the sum of the Target Investment Weights

relating to the Index Components may breach the Category Cap

Category Cap

The maximum percentage of Target Investment Weights for a category in the

Index Category Monitor List

London, Wednesday, 16 October 2013

v1.00, H1-2013

Commodity Group

Credit Suisse Commodity Index Framework

The Credit Suisse Backwardation UCITS Index (CSCU4BK)

Page 2

2. The CSCU4BK Allocation Model

The Credit Suisse Backwardation UCITS Index (CSCU4BK) is an Index of Indexes. It dynamically

allocates to the components with the highest degree of backwardation within the Investment Universe subject to the Sector constraints, and any applicable Sub-sector constraints, specified below.

The Index Sponsor shall review the Sector and Sub-sector constraints on an annual basis and, in

accordance with Section A.2.5, upon the occurrence or prospective occurrence of any Extraordinary

Event, and may amend, add or remove such constraints in order to ensure that the Index complies with

any applicable law or regulation.

2.0. Definition of the CSCU4BK Investment Universe and Sector / Sub Sector Maximum

Allocation

TABLE 2.0.2. CSCU4BK INVESTMENT UNIVERSE AND SECTOR / SUB SECTOR MAXIMUM ALLOCATION

Index Component

Underlying

Exchange

Bloomberg

Index

Ticker

Sector

Max

Sector

Allocation

Sub-

sector

Max Sub

Sector

Allocation

4 3

CSCB 59 4x6F WTI Crude

Oil

NYMEX CS59CLE2 Energy Oil

CSCB 59 4x6F Brent Crude

Oil

ICE CS59BRE2 Energy Oil

CSCB 59 4x6F NY Harbor

ULSD

NYMEX CS59HOE2 Energy Oil

CSCB 59 4x6F Gasoil ICE CS59GOE2 Energy

CSCB 59 4x6F RBOB

Gasoline

NYMEX CS59RBE2 Energy Oil

CSCB 59 4x6F Natural Gas NYMEX CS59NGE2 Energy

4

CSCB 59 4x6F Copper

grade A. LME

CS59CUE2 Industrial Metals

CSCB 59 4x6F Zinc high

grade LME

CS59ZNE2 Industrial Metals

CSCB 59 4x6F Aluminium

primary LME

CS59ALE2 Industrial Metals

CSCB 59 4x6F Nickel

primary LME

CS59NIE2 Industrial Metals

CSCB 59 4x6F Lead

Standard LME

CS59PBE2 Industrial Metals

4

CSCB 59 4x6F Gold COMEX CS59GCE2 Precious Metals

CSCB 59 4x6F Silver COMEX CS59SIE2 Precious Metals

CSCB 59 prompt Platinum NYMEX CS59PLER Precious Metals

CSCB 59 prompt Palladium NYMEX CS59PAER Precious Metals

4 1

CSCB 59 4x6F SRW Wheat CBOT CS59WHE2 Agriculture Wheat

CSCB 59 4x6F HRW Wheat KCBOT CS59KWE2 Agriculture Wheat

CSCB 59 4x6F Corn CBOT CS59CNE2 Agriculture

CSCB 59 4x6F Soybeans CBOT CS59SYE2 Agriculture

CSCB 59 4x6F Sugar #11 ICE CS59SBE2 Agriculture

CSCB 59 4x6F Coffee “C”

Arabica ICE

CS59KCE2 Agriculture

CSCB 59 4x6F Cotton ICE CS59CTE2 Agriculture

1

London, Wednesday, 16 October 2013

v1.00, H1-2013

Commodity Group

Credit Suisse Commodity Index Framework

The Credit Suisse Backwardation UCITS Index (CSCU4BK)

Page 3

CSCB 59 4x6F Live Cattle CME CS59LCE2 Livestock

CSCB 59 4x6F Lean Hogs CME CS59LHE2 Livestock

Source: Credit Suisse, Index Advisory Committee.

Index Component Index Categories

Index Category

Monitor List

CSCB 59 4x6F WTI Crude Oil Oil Oil

CSCB 59 4x6F Brent Crude Oil Oil Oil

CSCB 59 4x6F NY Harbor ULSD Oil Oil

CSCB 59 4x6F Gasoil Oil Oil

CSCB 59 4x6F RBOB Gasoline Oil Oil

CSCB 59 4x6F Natural Gas

CSCB 59 4x6F Copper grade A.

CSCB 59 4x6F Zinc high grade

CSCB 59 4x6F Aluminium primary

CSCB 59 4x6F Nickel primary

CSCB 59 4x6F Lead Standard

CSCB 59 4x6F Gold

CSCB 59 4x6F Silver

CSCB 59 prompt Platinum

CSCB 59 prompt Palladium

CSCB 59 4x6F SRW Wheat Wheat

CSCB 59 4x6F HRW Wheat Wheat

CSCB 59 4x6F Corn

CSCB 59 4x6F Soybeans

CSCB 59 4x6F Sugar #11

CSCB 59 4x6F Coffee “C” Arabica

CSCB 59 4x6F Cotton

CSCB 59 4x6F Live Cattle

CSCB 59 4x6F Lean Hogs

Source: Credit Suisse, Index Advisory Committee.

The Category Cap is defined as 20% for Wheat and 35% for Oil

London, Wednesday, 16 October 2013

v1.00, H1-2013

Commodity Group

Credit Suisse Commodity Index Framework

The Credit Suisse Backwardation UCITS Index (CSCU4BK)

Page 4

2.1. Determination of CSCU4BK Target Investment Weights (TIW)

2.1.1. The Allocation Model

On the Allocation Calculation Date, the Index Calculation Agent determines the components to be

included using the Allocation Model as follows:

STEP 1 Rank the components (i.e. the CSCB 59 single commodity indices) by backwardation in

descending order

STEP 2 Apply any applicable sub sector constraints by removing the lowest ranked component in the

relevant sub sector.

STEP 3 Apply the sector constraints by removing the lowest ranked component in the relevant sector.

STEP 4 Select the top 9 components and assign TIWs of 1/9 to each of the 9 selected components.

The rest of the components receive TIWs of 0%.

London, Wednesday, 16 October 2013

v1.00, H1-2013

Commodity Group

Credit Suisse Commodity Index Framework

The Credit Suisse Backwardation UCITS Index (CSCU4BK)

Page 5

2.1.2. Reweighting/Roll Periods

The CSCU4BK index utilizes one Reweighting/Roll Period per Reference Period:

The Reweighting/Roll: taking place monthly, it starts on the 5th Index Business Day and ends on the

9th Index Business Day of each month.

The procedure is illustrated in Exhibit I below.

EXHIBIT I. THE CALCULATION PERIOD, THE REFERENCE PERIOD AND THE STATIC DATA CALCULATION DATE

ROLL/REWEIGHTING PERIOD, EXAMPLE NOV2010- JAN2011

Source: Credit Suisse, Index Advisory Committee

2.2. Calculation of CSCU4BK Static Data Parameters

The Calculation Engine detailed in Section A.6.3. Generic Basket of Assets Calculation Methodology

is applied to the Target Investment Weights defined above for the Reference Period m.

For the purpose of each Roll/Reweighting Periods, the following Static Data is calculated:

The Units Weights.

London, Wednesday, 16 October 2013

v1.00, H1-2013

Commodity Group

Credit Suisse Commodity Index Framework

The Credit Suisse Backwardation UCITS Index (CSCU4BK)

Page 6

3. CSCU4BK Index Parameters

3.0. Calculation Engine

The CSCU4BK references the calculation methodology formulated in Section A.6.3. Generic Basket

of Assets calculation methodology.

3.1. CSCU4BK Investment Universe

The CSCU4BK Index Components are selected from the universe of CSCB 4x6F and prompt single

commodity indices. Only commodities with CSCB prompt target investment weight that is greater than 1%

are included into the Universe. The universe of CSCB single commodity indices and their respective

target weights in the CSCB Index are reviewed annually. Any additional commodities, recommended

by the Index Advisory Committee, are reviewed by the Framework Steering Committee at their AGM

for inclusion in the following calendar year.

The CSCU4BK Index Components, selected from the broad universe of commodities, invest in a variation

of the CSCB 4x6F single commodity indices referred to as the CSCB 59 4x6F single commodity indices

(see Appendix for further details). If a CSCB 59 4x6F single commodity index is not available, the relevant

CSCB 59 prompt single commodity index is used as the index component.

The Calculation Agent for all CSCU4BK Index Components is CSi.

For further details on the CSCU4BK Investment Universe, please refer to table 2.0.2

London, Wednesday, 16 October 2013

v1.00, H1-2013

Commodity Group

Credit Suisse Commodity Index Framework

The Credit Suisse Backwardation UCITS Index (CSCU4BK)

Page 7

3.2. Inclusion factors per Index Component

Inclusion factors are equal to ‘1’ in respect of each Index Component with a prompt TIW in the CSCB

index that is greater than 1%, and ‘0’ in respect of all other Index Components.

3.3. Roll Period, Reweighting and Static Data Calculation Date (SDCD)

Please refer to Section B. 2. The CSCU4BK Allocation Model, for a complete description of the

Reweighting and Roll mechanism.

TABLE 3.3.1. CSCU4BK REWEIGHTING & ROLL PERIOD Reference

Period Jan Feb Mar Apr May Jun Jul Apr Sep Oct Nov Dec

Roll & Reweight

Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes

Source: Credit Suisse, Index Advisory Committee. Yes (No): Reweighting occurs (doesn’t occur) during that month

The notation for the CSCU4BK Primary Roll Period is [+1(m)/+5(m)]. The Static Data Calculation

Date (SDCD) precedes the First Roll Day, noted [0(m)].

TABLE 3.3.2. CSCU4BK PRIMARY ROLL PERIOD

Month Jan Feb Mar Apr May Jun Jul Apr Sep Oct Nov Dec

Type Custom Custom Custom Custom Custom Custom Custom Custom Custom Custom Custom Custom

SDCD 0(m) 0(m) 0(m) 0(m) 0(m) 0(m) 0(m) 0(m) 0(m) 0(m) 0(m) 0(m)

FRD +1(m) +1(m) +1(m) +1(m) +1(m) +1(m) +1(m) +1(m) +1(m) +1(m) +1(m) +1(m)

LRD +5(m) +5(m) +5(m) +5(m) +5(m) +5(m) +5(m) +5(m) +5(m) +5(m) +5(m) +5(m)

Source: Credit Suisse, Index Advisory Committee.

3.4. FX rate source

Foreign exchange rates references required for any FX hedged versions of the CSCU4BK are as per

Table 3.4. below.

TABLE 3.4. FOREIGN EXCHANGE RATE DEFINITIONS AND SOURCES

Ccy

Definition

Data Source Time

EUR

The mid EUR-USD exchange rate, expressed as the amount of USD

per one EUR, as determined by WM Company, the calculation agent

and published on the relevant observation date

Bloomberg: WMCO <GO> & Menu

Ticker: EUR WMIS Curncy

7PM London

Source: Credit Suisse, Index Advisory Committee

London, Wednesday, 16 October 2013

v1.00, H1-2013

Commodity Group

Credit Suisse Commodity Index Framework

The Credit Suisse Backwardation UCITS Index (CSCU4BK)

Page 8

3.5. Interest Rate Definitions

Collateral Reference Rates (CRR), CreditAdjustCCY and standard Total Return Index calculation

parameters for CSCU4BK are defined in Table 3.5. below.

TABLE 3.5. INTEREST RATE DEFINITIONS

Ccy

Definition or CRR

Data Source Rate

TypeCCY

Credit-

AdjustCCY

BasisCCY

Short-

BasisCCY

USD

3 months U.S. Treasury Bill

(91 days) “High Rate”

auction rate published by the

Bureau of public Debt as the

“treasury security auction

Results”

Reuters: USAUCTION9

Bloomberg USB3MTA Index <GO>

Internet:

http://www.treasurydirect.gov/RI/OFGateway

T-Bill

0.0%

360

91

EUR

The EUR-EONIA-OIS-

COMPOUND rate as defined

in the 2006 ISDA Definitions

applicable on the relevant

value date as published daily

by the European Central

Bank

Reuters: EONIA

Bloomberg EONIA Index <GO>

Money

Market

0.0%

360

1

Source: Credit Suisse, Index Advisory Committee

London, Wednesday, 16 October 2013

v1.00, H1-2013

Commodity Group

Credit Suisse Commodity Index Framework

The Credit Suisse Backwardation UCITS Index (CSCU4BK)

Page 9

3.6. Rounding

Table 3.6. below features the rounding characteristics used for the calculation of the CSCU4BK Index.

TABLE 3.6. ROUNDING CHARACTERISTICS

Parameter

Rounding methodology used

Weight Data

TIW Eight (8) decimal places1

Static Data

UW No rounding

Index Levels

Price Return Index (PR) Eight (8) decimal places1

Excess Return Index (ER) Eight (8) decimal places

Total Return Index (TR) Eight (8) decimal places

Source: Credit Suisse, Index Advisory Committee

(1): A quantity with value 0.12345678998756 (resp. 12.345678998756%) shall be rounded to 0.12345679 (resp. 12.345679%)

3.7. Disrupted Valuation Day methodology

The following table indicates the methodology adopted for each Reweighting Period. Please refer to

Section A.6.3. for a detailed description of methodologies supported by the Generic Baskets of Assets

calculation methodology.

TABLE 3.7. CSCU4BK - COMMODITY DISRUPTION EVENT METHODOOGY

Month Jan Feb Mar Apr May Jun Jul Apr Sep Oct Nov Dec

Roll &

Reweight S S S S S S S S S S S S

Source: Credit Suisse, Index Advisory Committee.

S : Methodology for that month is the Standard Roll methodology

E : Methodology for that month is the Extended Roll methodology

3.8. Total Return index Calculation methodology

For the purpose of the calculation of the CSCU4BK Total Return Index, the Index uses the Daily

Equivalent Rate method (see Section A. 6.3.4.3. Calculation of the Total Return Index).

London, Wednesday, 16 October 2013

v1.00, H1-2013

Commodity Group

Credit Suisse Commodity Index Framework

The Credit Suisse Backwardation UCITS Index (CSCU4BK)

Page 10

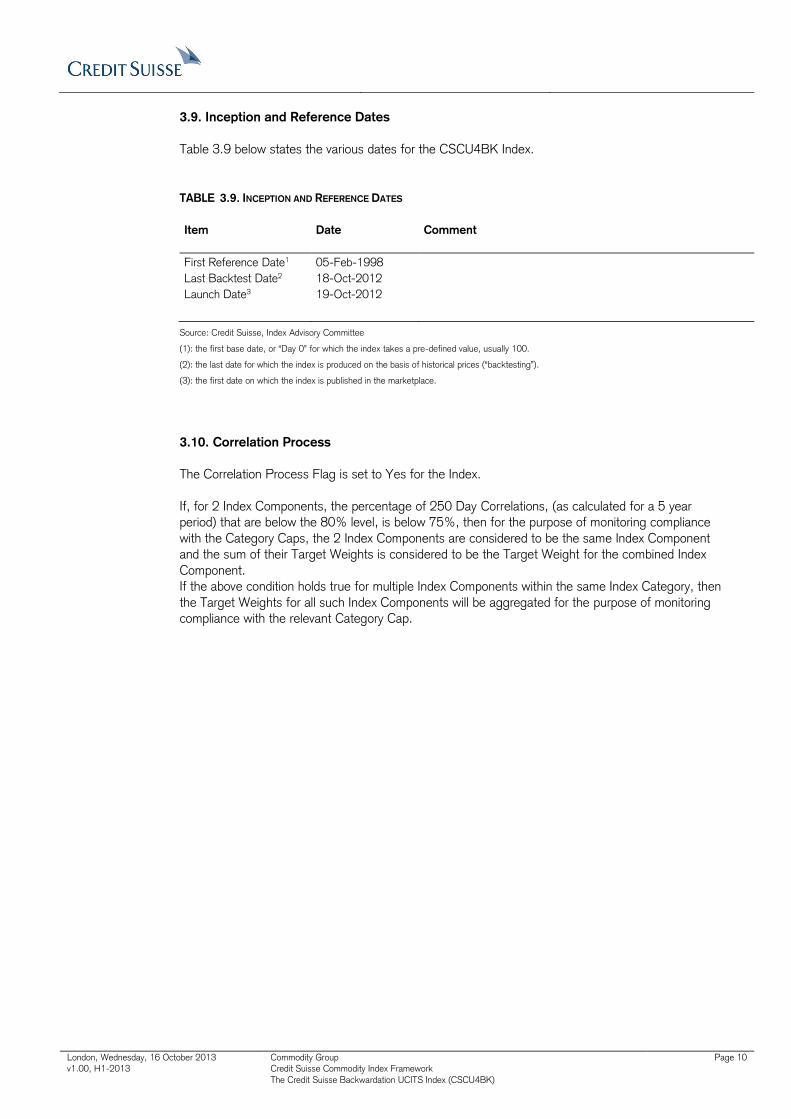

3.9. Inception and Reference Dates

Table 3.9 below states the various dates for the CSCU4BK Index.

TABLE 3.9. INCEPTION AND REFERENCE DATES

Item

Date Comment

First Reference Date1 05-Feb-1998

Last Backtest Date2 18-Oct-2012

Launch Date3 19-Oct-2012

Source: Credit Suisse, Index Advisory Committee

(1): the first base date, or “Day 0” for which the index takes a pre-defined value, usually 100.

(2): the last date for which the index is produced on the basis of historical prices (“backtesting”).

(3): the first date on which the index is published in the marketplace.

3.10. Correlation Process

The Correlation Process Flag is set to Yes for the Index.

If, for 2 Index Components, the percentage of 250 Day Correlations, (as calculated for a 5 year

period) that are below the 80% level, is below 75%, then for the purpose of monitoring compliance

with the Category Caps, the 2 Index Components are considered to be the same Index Component

and the sum of their Target Weights is considered to be the Target Weight for the combined Index

Component.

If the above condition holds true for multiple Index Components within the same Index Category, then

the Target Weights for all such Index Components will be aggregated for the purpose of monitoring

compliance with the relevant Category Cap.

London, Wednesday, 16 October 2013

v1.00, H1-2013

Commodity Group

Credit Suisse Commodity Index Framework

The Credit Suisse Backwardation UCITS Index (CSCU4BK)

Page 11

Appendix

CSCB 59 4x6F single commodity indices and CSCB 59 Prompt single commodity indices

The CSCB 59 4x6Fsingle commodity indices and CSCB 59 Prompt single commodity indices are the same

as the relevant CSCB 4x6F single commodity indices and CSCB Prompt single commodity indices defined

in Index Operating Manual in respect of the Credit Suisse Commodity Benchmark (CSCB) except for the

following feature:

In the CSCB 59 4x6F single commodity indices and CSCB 59 Prompt single commodity indices, the

monthly roll period begins on the 5th Index Business Day and ends on the 9th Index Business Day of each

month, rolling at a rate of 1/5 each Index Business Day.

In the CSCB 4x6F single commodity indices and CSCB Prompt single commodity indices, the monthly roll

period begins on the 5th Index Business Day prior to the last Index Business Day of the previous month and

ends on the 9th Index Business Day of the month, rolling at a Rate of 1/15 each Index Business Day.