the dutch disease : causes, consequences, cures and calmatives

TRANSCRIPT

The Dutch Disease:

Causes, Consequences, Cures and Caimatives

By

Klaus Enders and Horst Herberg

C o n t e n t s : 1. I n t roduc t i on . - - II . The Model. - - l I I . Consequences of a Resource Boom. - - IV. Cures of t h e D u t c h Disease. - - V. Some E x t e n s i o n s . - - A p p e n d i x .

I. Introduction

I n r e c e n t y e a r s s e v e r a l i n d u s t r i a l i z e d c o u n t r i e s f o u n d to t h e i r s u r p r i s e

t h a t a s h a r p i nc r ea se of t h e i r r e v e n u e s f r o m r a w - m a t e r i a l p r o d u c t i o n

does n o t o n l y h a v e benef ic ia l e f fec t s b u t a l so p o s e s a t h r e a t t o t h e

s u r v i v a l of t h e i r t r a d i t i o n a l e x p o r t a n d i m p o r t - c o m p e t i n g i n d u s t r i e s a n d

m a y e v e n l ead to d e - i n d u s t r i a l i z a t i o n . T h i s p h e n o m e n o n w a s ca l l ed t h e

" D u t c h d i s e a s e " a f t e r i t w a s o b s e r v e d in t h e N e t h e r l a n d s in t h e s e v e n t i e s

w h e n t h e f low of N o r t h - S e a gas p e a k e d 1. T h e r e a r e t w o b a s i c m e c h a n i s m s

t h a t b r i n g a b o u t s u c h n e g a t i v e e f fec t s 2: U n d e r f ixed e x c h a n g e r a t e s h i g h e r

p r o d u c t i o n or p r i c e s of r a w m a t e r i a l s r a i s e d o m e s t i c s p e n d i n g on g o o d s

Remark: An earlier version of this paper was presented in seminars at the Norwegian School of Economics and Business Administration, Bergen, and at the University of Oslo; its main conclusions were outlined in discussions with representatives of several institutions like the Central Bureau of Statistics, the Christian Michelsen Institute, the Vestlandsbanken, Statoil and the Norwegian Petroleum Department during our visit to Oslo, Bergen and Stavanger in September]October i982. We are very grateful to all Norwegian economists we met, especially to J. Aarrestad, O. Bjerkholt, M. Hoel, E. Hope, L. Johansen, L. Lo- rentsen and A. Sandmo for valuable and helpful comments, suggestions and information. For similar services we also thank M. Schmid, H.-W. Sinn, H. Siebert and other participants of a seminar at the University of Mannheim. Moreover, we are grateful to the Deutsche Forschungsgemeinschaft for the research grant under which K. Enders worked and for providing some travel funds. As usual, we accept sole responsibility for any remaining de- ficiency or error.

1 See, e.g., Kaldor [1981 ]. Looking back into history one should easily find earlier eases of such a disease.

z To our knowledge these two mechanisms were first described and their implications studied by Eide [i973] and Gregory [I976], respectively. See also the early Norwegian White Paper, Finansdepartementet [i 973/74]. Since Eide's paper has so far remained widely unknown, Gregory has been credited for having initiated the analysis of the negative side-effects of a resource boom. Gregory's analysis has been improved and extended by Shape [I977], Corden and Neary [1982], Enders [i982], Ngo Van Long [i982], Neary and Purvis [1982], Wijn- bergen [1982], among others.

474 K l a u s E n d e r s a n d t l , , r s t l t e r b e r g

and services. As short-run output reactions can be expected to be minor, the prices of non-tradeables increase. Hence the sheltered sector 1 can afford to pay, and will pay, higher nominal wages. Intersectoral competi- tion for labour or central bargaining will raise wages in the exposed sector as well. With the prices of tradeables determined in the world marke t and hence (largely) fixed, the international competitiveness of the exposed sector deteriorates, its production of export and import- competing commodities shrinks, and its share in national product declines. Under flexible exchange rates the resource boom tends to improve the country 's current account b y lowering the value of imports of raw mate- rials or by raising the value of their exports. The consequent revaluation of the home currency again impairs the international competitiveness of the country 's exposed sector and lowers its share in national product 2.

However, when discussing such adverse side-effects and calling them a "disease", it should not be forgotten tha t on balance a country ex- periencing a resource boom faces an improved economic situation in the short as well as in the longer run. After all, its real income will rise, most ly due to higher raw-material revenues, and neo-classical t rade theory predicts additional welfare gains due to movements of factors of production into the now more profitable sectors, resource extract ion and non-trade- ables. Moreover, if raw-material production needs little labour and/or capital and hence if revenue originating there contains a large element of economic rent, as, e.g., in the case of oil and natura l gas, so much the better: the country gains additional income without having to work for it.

Some authors have argued tha t the necessary restructuring process should not be allowed to take place, as it would under laissez-faire, since there is special value in having a large manufactur ing sector and in deriving income, not as a rent, but from work. One observat ion is tha t a "rent ier" misses out "on the cultural, technical and intellectual development which only a strong, heal thy manufactur ing industry, and the associated urbanization, can provide" [Kaldor, I98I , p. 8]. Another view maintains that , since rental income may not last forever, de-industrialization " m a y eventually condemn tha t country to the typical fate of the ex- rentier - - inability to earn his/her own living when the source of the unearned income ceases" [Ellman, i98I , p. I65].

x The te rms "she l te red sec tor" and "exposed sec tor" are b o r r o w e d from the S c a n d i n a v i a n model [cf., e.g., Aukrus t , I977; E d g r e n et al., x973].

I t is no t easy to de te rmine the q u a n t i t a t i v e size of these s t ruc tu r a l changes s ince in modern indus t r i a l i zed economies there is an under ly ing t r end to a r e l a t ive decl ine of the secondary sector and a re la t ive increase of the t e r t i a r y sector. Moreover, g o v e r n m e n t pol ic ies m a y to some ex t en t and for some t ime d a m p e n the effects of the Du tch disease.

The Dutch Disease 475

I t is beyond the scope of this paper to discuss and assess such argu- ments. As to the first one, we only ask whether the "cultural, technical and intellectual development" could perhaps not also be s t imulated b y a "strong, heal thy" non-tradeables sector, especially b y services. And to deal with the second issue requires a long-term perspective and, inter alia, involves questions of inter temporal cost-minimization and uti l i ty maximization [see, e.g., Calvo, Findlay, 1978; I-Ioel, I 9 8 I b ].

We are interested here in a different kind of question, namely the macroeconomic effects of a resource boom on a small open economy, i.e., we are interested in the changes in prices, real income, employment and sectoral s tructure in the short and the longer run. Special at tention will be paid to the causes and consequences of the Dutch disease, i.e., the contraction of the traditional t rading sector. Clearly, once the symptoms of this illness become noticeable the domestic government will be urged to take steps to cure it. Therefore, we also look into the problem to what extent various policies which are likely to be advocated or enacted 1 will prove to be successful. I t will be shown tha t most of them are ra ther calmatives than cures.

Our analysis is based on a ra ther simple model with (i) a sectoral s tructure as in the well-known Scandinavian model, (ii) fixed exchange rates, (iii) resource extraction needing no variable factor inputs and being controlled b y the domestic government, (iv) short-run immobil i ty of labour between the sheltered and the tradit ional exposed sector, (v) a wage-bargaining process with wage leadership (as in the Scandinavian model and in Hoel [I98Ia]) and (vi) an absorption function as in the monetary approach to the balance of payments [as, e.g., in Dornbusch, Mussa, 1975].

In Section I I we outline our ra ther simple (and restrictive) model and derive some of its basic properties, and in Section I I I we s tudy the consequences of a sudden sharp and persistent rise in revenues from raw material exports. Section IV is devoted to an analysis of the effects of a number of policies, most of them often advocated b y groups adversely affected b y the resource boom. In the final section we summarize our main results and discuss to what extent our initial assumptions can be weakened without invalidating our conclusions. All calculations are relegated to a short appendix.

1 For a discussion of policies adop ted or op ted for in Norway , see B je rkho l t et al. [ I98I ] .

476 K l a u s E n d e r s a n d H o r s t H e r b e r a

II. T h e M o d e l

The world consists of a small domestic and a large foreign country. There are three domestic sectors, the traditional exposed sector, the sheltered sector, and the resource sector, producing manufactures, services, and raw materials, respectively 1. The foreign currency prices P~t and P~ of manufactures and raw materials are determined on the world market. Assuming the absence of all t rade impediments their home currency prices are

(I) P~ = eP~, P• = eP~

where e denotes the exchange rate, i.e., the domestic currency price of a foreign currency unit. We take the exchange rate to be kept fixed by the domestic central bank.

Raw-material production requires no variable factor inputs and its level is determined by the domestic government. The two other sectors, however, need labour and some specific fixed factor(s). Assuming declining labour productivity and either marginal-cost or mark-up pricing we obtain the supply functions for manufactures and services z

(2) QM = QM(PM/W), Qs = Qs(es/W) + -t-

a n d the sectoral labour demand functions

(3) L~t = L~(W/P=), I.ds = Lsa(W/Ps)

where W is the nominal wage rate and Ps is the price of services.

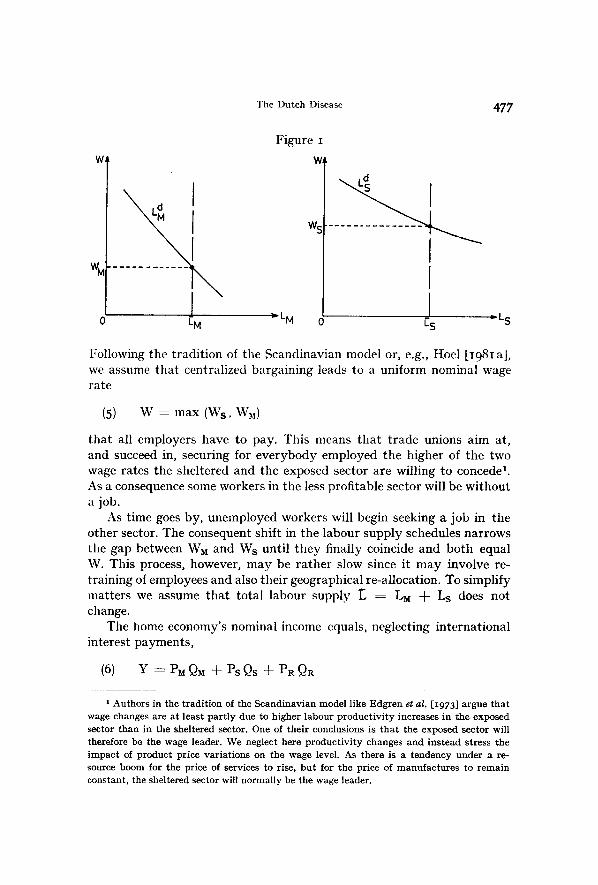

Let sectoral labour supplies F.M and r,s be fixed in tile short and the medimn run. Then, for these time periods there exist two, usually different, market-clearing wage rates WM and W s (see Figure I). Obviously, an increase in Pi leads to an upward shift of the labour demand curve of sector i ( = M, S) and therefore raises Wi but leaves Wj, i # j, unaffected. Moreover, a higher E i is associated with a lower Wi but the same Wj. Thus,

(4) W i = fi(Pi, i-.i) , i = M, S + - -

t I t shou ld be k e p t in m i u d t h a t the t e r m " s e r v i c e s " is s i m p l y a s h o r t - h a n d for p r o d u c t s of the she l t e red sec tor . I n r e a l i t y q u i t e a n u m b e r of serv ices c a n be i n t e r n a t i o n a l l y t r a d e d , a l t h o u g h some of t h e m h a v e on ly w e a k fo re ign s u b s t i t u t e s a n d t h e i r p r i ces a r e l a r g e l y do- ines t ica l ly d e t e r m i n e d . H o t e l a n d r e s t a u r a n t serv ices a r e obv ious e x a m p l e s . P a r t l y d u e to cos t -push effects of a resource b o o m such serv ices c a n become, as we e x p e r i e n c e d i n N o r w a y , r a t h e r expens ive . The consequence is a c r o w d i n g - o u t of fo re ign v i s i to r s w i t h o u t a c r o w d i n g - in b y d o m e s t i c c l ien ts ; a n o t h e r case of " t h e g r i n w i t h o u t the c a t " .

A s ign b e n e a t h a n a r g u m e n t i nd ica t e s the s ign of the c o r r e s p o n d i n g (pa r t i a l ) d e r i v a t i v e .

The Dutch Disease 477

W

wM

0 "- LS L M

Figure I

j'<.... ! I . . . . . . . . . . . . . .

I LM 0 ['S

Following the tradition of tile Scandinavian model or, e.g., Hoel [I981a], we assume that centralized bargaining leads to a uniform nominal wage rate

(5) W = max (Ws, WM)

tha t all employers have to pay. This means tha t t rade unions aim at, and succeed in, securing for everybody employed the higher of the two wage rates the sheltered and the exposed sector are willing to concede 1. As a consequence some workers in the less profitable sector will be without a job.

As time goes by, unemployed workers will begin seeking a job in the other sector. The consequent shift in the labour supply schedules narrows the gap between WM and Ws until they finally coincide and both equal W. This process, however, may be ra ther slow since it m a y involve re- training of employees and also their geographical re-allocation. To simplify matters we assume tha t total labour supply r, = LM + Ls does not change.

The home economy's nominal income equals, neglecting international interest payments ,

(6) Y--I'MQ~ +PsQs +PRQR

* Authors in the t radi t ion of the Scandinavian model like Edgren et al. [1973] argue tha t wage changes are at least par t ly due to higher labour product ivi ty increases in the exposed sector than in the sheltered sector. One of their conclusions is tha t the exposed sector will therefore be the wage leader. We neglect here product ivi ty changes and instead stress the impact of product price variat ions on the wage level. As there is a tendency under a re- source boom for the price of services to rise, but for the price of manufactures to remain constant, the sheltered sector will normally be the wage leader.

478 K ] a u s E n d e r s a n d H o r s t H e r b e r g

Suppose tha t the domestic government t ransfers its raw mater ial revenues to private households or tha t public and pr ivate spending follow the same pattern. Then it is reasonable to assume tha t total nominal absorp- tion A depends positively on nominal income Y and nominal financial wealth V,

(7) A = Y + ~ ( V - kY) ---= ( 1 - cr + ccV

where ~ and k are constant and positive parameters satisfying the restric- tion tha t the marginal rate of absorpt ion z-~k is larger than zero and less than unity. In other words, nominal hoarding Y-A serves to close the gap over t ime between actual wealth V and desired wealth V d = kY.

Financial wealth either consists of domestic money only, or of domestic money and some interest-bearing asset(s). In the la t ter case mone ta ry authorities at home and/or abroad keep interest rates fixed. Thus we need not s tudy interest ra te effects on portfolio composition and on absorption. As long as the domestic government ' s budget is balanced,

wealth accumulation ~r equals hoarding Y - A and hence the t rade balance.

For simplicity we assume tha t the total output of raw materials is ex- ported 1 and tha t fixed shares of absorption are spent on the other two commodities, manufactures and services

(8) P i D i = lx iA, lzi ---- const > 0; i = M, S; t~M + ~s = 1

where D i denotes the quant i ty demanded of the i-th commodity. The world marke t for manufactures is taken to be always in equilibrium

at a constant level of P~t tha t does not depend, since the home economy is small, on the demand and supply situation there. Equil ibrium in the marke t for the internationally non-tradeable services, however, requires

(9) Ds = Qs

A resource boom has three effects, an income/spending effect, a wealth/ spending effect and a labour-movement effect 2. The increase in income and spending initially induced by the boom brings about changes in the price of services, Ps, the wage rate, W, the output of manufactures, QM, and desired wealth, V d. The improved current account then leads to a gradual rise in actual wealth, V, towards V a and this is accompanied b y a fur ther increase in spending. Finally, sectoral employment levels, Ls and LM,

1 The case t h a t p a r t of d o m e s t i c r a w m a t e r i a l p r o d u c t i o n is used as a n i n p u t in t he o t h e r sec to r s of the h o m e c o u n t r y h a s been s t u d i e d in E n d e r s [1982].

2 In a s im i l a r c o n t e x t Corden a n d N e a r y [ i982] , a n d N e a r y a n d P u r v i s [1982 ] r e fe r to a s p e n d i n g effect w h i c h is ou r i n c o m e / s p e n d i n g effect a n d to a r e s o u r c e - m o v e m e n t effect w h i c h inc ludes i n t e r s ec to r a l shi f ts of c a p i t a l a n d l a b o u r .

The Dutch Disease 479

adjust to the new situation as workers move from the exposed to the sheltered sector until unemployment is eliminated. Although these effects to some extent work simultaneously we t rea t them as operating conse- cutively. In this way we t ry to capture the feature tha t it will take some time before actual wealth comes close to, or reaches, its desired level and tha t it may take even longer for workers to react appreciably to changed employment conditions.

Hence we also distinguish between three general equilibrial: A short- run equilibrium prevails if the last condition is satisfied together with the relationships (2) and (4)--(8) which describe commodi ty supply, wage formation, income, absorption and commodi ty demand. Insert ing (2), (4) and (6)--(8) into (9), and (4) into (5), we find tha t a short-run equilibrium is described by the two equations

( IO) W = max [fM(PM, ]-~M), fS (PS , r ' S ) ] + - - + - -

(II) Ps(Ds - Qs) = :Fs(W, Ps; PM, PRQR, V) ---- 0 ? - - + + +

The home economy is in a medium-run equilibrium if, in addition, wealth

accumulation V has ceased, i.e.,

(12) V -- Y - A = PM(QM - DM) + PRQR = : F v ( W , Ps; PM, PRQR, W) = 0 ? - - + + - -

Finally, a long-run equilibrium is reached once the wage gap WM-Ws has been closed by labour movements, sectoral employment is Ls and LM, and full employment prevails (Ls + LM = •):

(13) WM - Ws = fM(PM, LM) - fs(Ps, I--LM) ~-- 0 + - - + - -

Together with (5) the last relationship implies th at in a long-run equilibrium

(14) W ---- G(PM, Ps, L) + + - -

Our distinction between the three consecutive equilibria implies tha t we assume that , following any disturbance, initially only the price of services Ps, the wage rate W, the output levels Qs and QM as well as income Y change, tha t after some t ime wealth V at tains the level V d, and tha t

i In economics the t e rms " s h o r t r u n " , " m e d i u m r u n " an d " long r u n " are widely used

bu t h a v e no general ly accepted meaning . To avo id confusion i t should be kep t in m i n d tha t in the present pape r they are implic i t ly defined b y equa t ions ( i o ) - - ( i 2 ) an d (14). Fo r

example , we do not discuss capi ta l f o rma t ion and hence need no t be concerned wi th the question of whe ther or not net i nves tmen t is nil in the long run.

480 Klaus Endersarid Horst Herberg

finally sectoral employments Ls and LM adjust and unemployment ceases to exist.

Formally, the basic endogenous variables in a short-run equilibrium are Ps and W, in a medium-run equilibrium Ps, W and V, and in a long- run equilibrium Ps, W, V and LM. Obviously, the number of endogenous variables in each case equals the number of equations determining them. Finally, we assume tha t the home economy is initially in a long-run equilibrium, and after a disturbance reaches new stable equilibria.

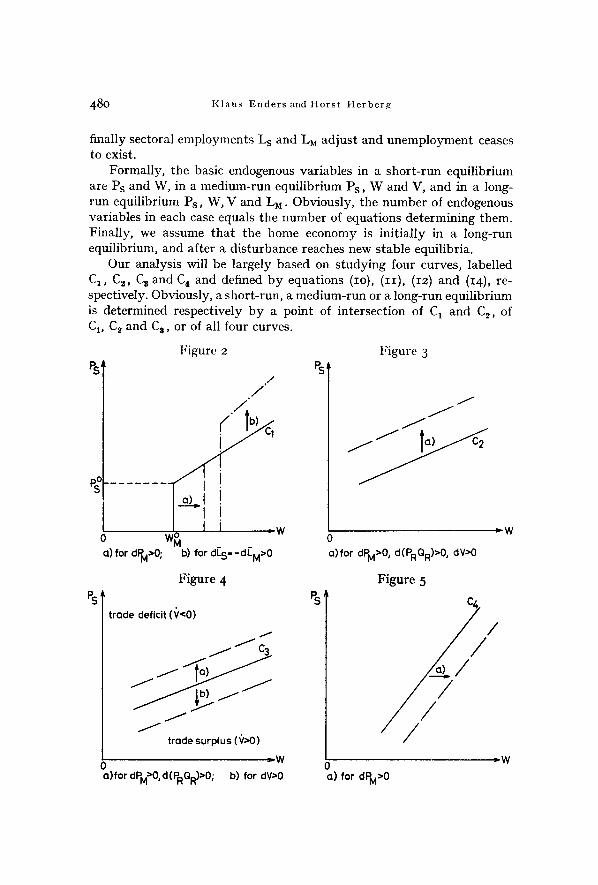

Our analysis will be largely based on s tudying four curves, labelled C1, C9., C 3 and C a and defined b y equations (IO), (II), (I2) and (14), re- spectively. Obviously, a short-run, a medium-run or a long-run equilibrium is determined respectively by a point of intersection of C 1 and C2, of C 1, C= and C s , or of all four curves.

Figure 2

. ~ '

o w~ cl) for d~=,O; b) for d~--dFM>O

Figure 4

trode deficit ( V <0)

j J c 3

trade surplu s (V>O)

0 J,W a)for dPM>O,d(PRQR)>O; b) for dV>O

Ps, Figure 3

J J

J

=W

Ps'

a)for dPM>O , d(PRQR)>O, dV>O

Figure 5

C4

//

0 , W o) for dPM>0

The D u t c h Disease 481

These curves are shown in Figures 2--5. Their properties are formally derived in the Appendix but most of them follow from simple economic rea- soning as well: Denote all values referring to the initial long-run equi- librium by tile superscript "o". Consider curve C 1 first. At the prices P~ and P~t for services and manufactures and at the wage ra te W ~ = W~ = W~t, full employment prevails in both the sheltered and the exposed sector. Suppose Ps falls below P~. Then the supply of services and hence the sheltered sector 's labour demand and its full employment wage ra te Ws decline. Ceteris paribus, the exposed sector becomes the wage leader (W = W~t > Ws) and some workers in the sheltered sector lose their job (Ls < E~). Such situations correspond to the vertical pa r t C~ of C 1 . Suppose, alternatively, Ps rises beyond P~. Now tile sheltered sector becomes the wage leader, i.e., it can pay higher wages and still retain full employment. (In fact, Ws increases b y the same percentage as Ps.) Since W = Ws > WE = W~, there will be some lay-offs in the exposed sector. These situations are represented b y points on the upper pa r t C~ of C1.

The "kink" in C 1 is thus the point of overall full employment , and ti~e locus of all corner points for the given P~t and ~o, but vary ing LM and Ls, is curve C 4 . I t is obviously positively sloped (see Figure 5) and closer inspection shows tha t it is steeper than C 1 .

C 2 represents, for given values of PM, PRQR and V, the locus of equilibria in the services market , i.e., the pairs (Ps,W) for which excess demand Ps(Ds-Qs) is nil. This curve may be rising, falling or horizontal, or m a y even have a par t ly positive and par t ly negative slope since the impact of a rise in the wage level upon excess demand is ambiguous: By reducing production in the sheltered and the exposed sector it lowers income, absorption and demand Ds, and at the same t ime reduces supply Qs. The reaction of excess demand to changes of the other variables, however, is definite: A higher Ps raises PsDs b y less than PsQs and thus reduces Ps(Ds-Qs) . Moreover, an increase in PM or PRQR boosts income and spending without affecting Qs, and an increase in wealth also st imuIates demand but leaves supply unchanged.

Finally, C 3 is the locus of pairs (Ps,W) associated with a zero t rade balance. I ts slope is also indeterminate since the effect of a wage change on the current account or, more precisely, on excess demand for manu- factures is ambiguous, and for similar reasons as above. All other changes have clear consequences. For example, a higher PR QR leads to an im- provement in the trade balance since export revenues increase b y more than expenditures on imported manufactures.

In addition, at least at points of intersection, the following impor tan t inequalities hold:

Weitwirtschaftliches Archly Bd. CXlX. ~2

482 K l a u s E n d e r s a n d H o r s t H e r b e r g

8Ps > 8Ps 8Ps 8Ps 8Ps

(I5) 8-.~;f c r ~ ! c . > 8W c: > ~ ! c ~ > ~Wc 3

Hence the points of intersection that by assumption exist between Cx, Ca, C a and C 4 are always unique.

III. Consequences of a Resource Boom

We shall now study the consequences of an increase in the value PRQR of raw-material production and exports. In our model it does not matter whether this disturbance is caused by a rising world market price of resources, P~, or a higher level of domestic production, QR, or by both changes 1.

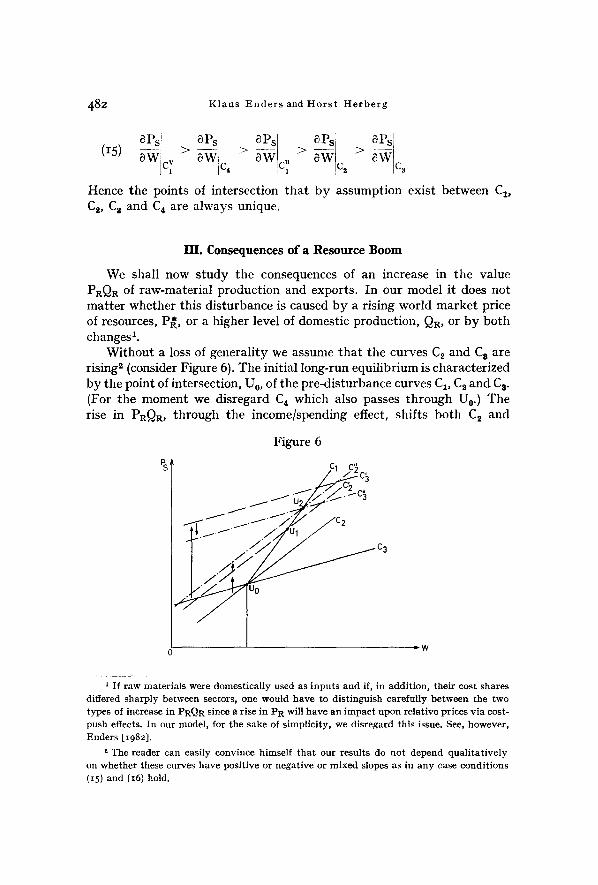

Without a loss of generality we assume that the curves C2 and C 8 are rising a (consider Figure 6). The initial long-run equilibrium is characterized by the point of intersection, U0, of the pre-disturbance curves C1, C a and C a. (For the moment we disregard C 4 which also passes through U0. ) The rise in P R Q R , through the income/spending effect, shifts both C 2 and

Figure 6

Ps' C! C~

~W

i I f r aw ma te r i a l s were domes t i ca l ly used as i n p u t s and if, in add i t ion , the i r cost shares differed sha rp ly be tween sectors, one would have to d i s t ingu i sh ca re fu l ly be tween the two types of increase in PRQR since a r i se in PR will h a v e an i m p a c t upon re l a t ive pr ices v i a cost- push effects. In our model , for the sake of s impl ic i ty , we d i s regard th i s issue. See, however , Enders [ i982 ].

* The reader can eas i ly convince himself t h a t our resul ts do no t depend q u a l i t a t i v e l y on whe the r these curves have pos i t ive or nega t ive or mixed slopes as in a n y case cond i t i ons (I5) and (i6) hold.

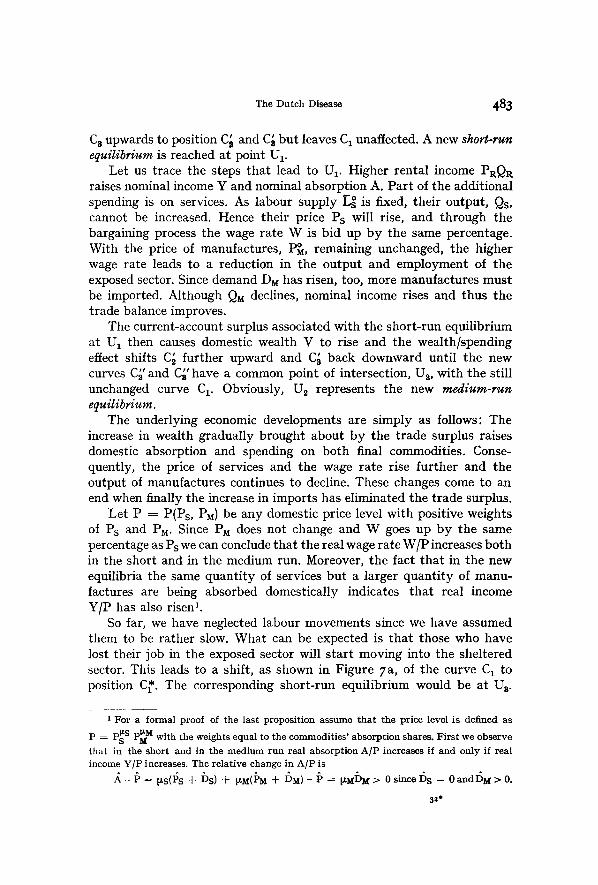

The Dutch Disease 483

C 8 upwards to position C: and C~ but leaves C x unaffected. A new short-run equilibrium is reached at point U 1.

Let us trace the steps tha t lead to UI. Higher rental income PRQR raises nominal income Y and nominal absorption A. Pa r t of the additional spending is on services. As labour supply TL~ is fixed, their output , Qs, cannot be increased. Hence their price Ps will rise, and through the bargaining process the wage ra te W is bid up b y the same percentage. With the price of manufactures, P~t, remaining unchanged, the higher wage rate leads to a reduction in the output and employment of the exposed sector. Since demand DM has risen, too, more manufactures mus t be imported. Although QM declines, nominal income rises and thus the trade balance improves.

The current-account surplus associated with the short-run equilibrium at U1 then causes domestic wealth V to rise and the wealth/spending effect shifts C6 fur ther upward and C~ back downward until the new curves C6' and C~' have a common point of intersection, Us, with the still unchanged curve C v Obviously, U~ represents the new medium-run equilibrium.

The underlying economic developments are s imply as follows: The increase in wealth gradually brought about b y the t rade surplus raises domestic absorption and spending on both final commodities. Conse- quently, the price of services and the wage rate rise fur ther and the output of manufactures continues to decline. These changes come to an end when finally the increase in imports has eliminated the t rade surplus.

Le t P = P(Ps, PM) be any domestic price level with positive weights of Ps and PM. Since PM does not change and W goes up b y the same percentage as Ps we can conclude tha t the real wage rate W/P increases both in the short and in the medium run. Moreover, the fact tha t in the new equilibria the same quant i ty of services but a larger quant i ty of manu- factures are being absorbed domestically indicates tha t real income Y/P has also risen 1.

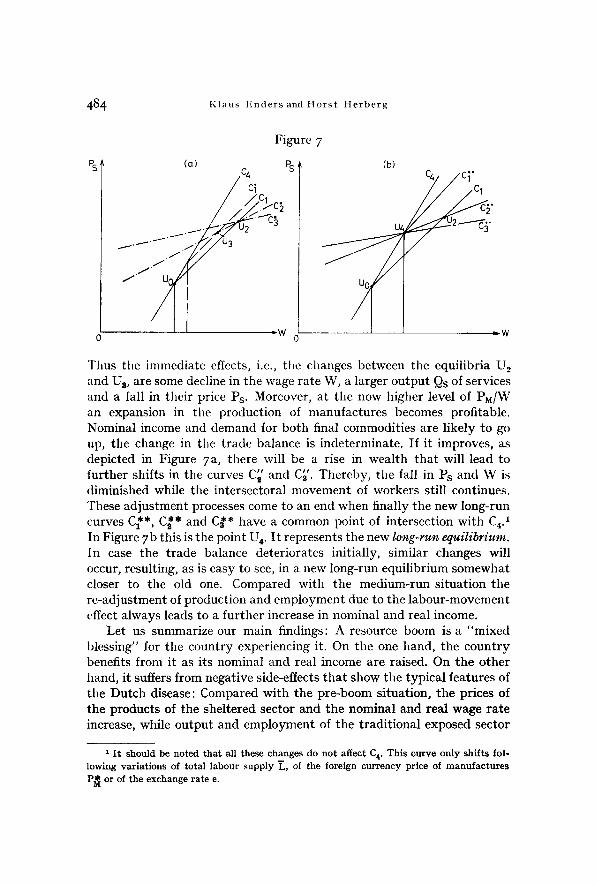

So far, we have neglected labour movements since we have assumed them to be rather slow. What can be expected is tha t those who have lost their job in the exposed sector will s t a r t moving into the sheltered sector. This leads to a shift, as shown in Figure 7 a, of the curve C1 to position C*. The corresponding short- run equilibrium would be at U 3.

x For a formal proof of the last proposition assume that the price level is defined as p = psgS p~M with the weights equal to the commodities' absorption shares. First we observe that in the short and in the medium run real absorption AlP increases if and only if real income Y/P increases. The relative change in A/P is

~ - ~ = ~S#S + bS) + ~MIf~ + 5M)-f~ = ~ b ~ > 0 since 5S = 0andS~ > 0.

32*

484 K l a u s E n d e r s a n d H o r s t H e r b e r g

Figure 7

(a)

3

1 1 . I / / - / / 0 3 / . / '

Ps, (b) % / c i "

q"

U,

Thus tile immediate effects, i.e., tile changes between the equilibria U~ and U s, are some decline in the wage rate W, a larger output Qs of services and a fall in their price Ps. Moreover, at the now higher level of PM/W an expansion in the production of manufactures becomes profitable. Nominal income and demand for both final commodities are likely to go up, the change in the t rade balance is indeternfinate. If it improves, as depicted in Figure 7 a, there will be a rise in wealth tha t will lead to further shifts in the curves C~' and C~'. Thereby, the fall in Ps and W is diminished while the intersectoral movement of workers still continues. These adjustment processes come to an end when finally the new long-run curves C~'*, C~'* and Cff'* have a common point of intersection with C4,1 In Figure 7 b this is the point U 4. I t represents the new long-run equilibrium. In case the trade balance deteriorates initially, similar changes will occur, resulting, as is easy to see, in a new long-run equilibrium somewhat closer to the old one. Compared with the medium-run situation the re-adjustment of production and employment due to the labour-movement effect always leads to a fur ther increase in nominal and real income.

Let us summarize our main findings: A resource boom is a "mixed blessing" for the country experiencing it. On the one hand, the country benefits from it as its nominal and real income are raised. On the other hand, it suffers from negative side-effects t ha t show the typical features of the Dutch disease: Compared with the pre-boom situation, the prices of the products of the sheltered sector and the nominal and real wage ra te increase, while output and employment of the tradit ional exposed sector

1 It should be noted tha t all these changes do not affect C a. This curve only shif ts fol- lowing variations of total labour supply L, of the foreign currency price of manufac tures P~ or of the exchange rate e.

The Dutch Disease 4 8 5

fall. These adverse effects are the more pronounced the lower the degree of intersectoral labour mobili ty is. Hence they tend to get smaller as t ime goes b y and as workers laid off b y the exposed sector seek and find employment in the sheltered sector. As par t of a Marshallian adjustment process the country thus faces an annoying overshooting phenomenon: The initial decline in the exposed sector 's activities is especially severe and only par t ly reversed later. In the end, the country has returned to full employment with the sheltered sector providing more and the exposed sector fewer jobs 1.

IV. Cures of the Dutch Disease

in tile present section we shall discuss tile effects of some policy responses tha t the Dutch disease is likely to provoke. Since the main symptoms comprise inter alia (i) a contraction in the exposed sector, both in the short and in the longer run, and (ii) some unemployment , at least as long as labour is not sufficiently mobile, it can be expected tha t one policy response could be an additional, deficit-financed public demand for manufactures. Moreover, as the exposed sector is likely to perceive "ex- cessive" nominal wages as the cause of its decline, it will lobby for a "wage freeze". Two other policies, geared at restoring profitabili ty in the exposed sector, could be a devaluation of the home currency or granting subsidies. A fifth policy would be to impose or raise an import tariff on manufactures. This has been advocated as par t of tile cure, e.g., b y Kaldor [1981 ] . Two more alternatives that , however, seem to have met with less attention would be to improve labour mobility or to invest part of the higher resource revenues in foreign interest-bearing assets ~. We shall deal

For a number of different models ana logous f indings h a v e been repor ted , a m o n g others , by the au thors ment ioned in footnote 2 on page 473. However , s ince they do no t m a k e a s imi l a r d is t inc t ion be tween the short , med ium and long run as in the p resen t paper , the ove r shoo t ing phenomenon is no t ment ioned and on ly imp l i c i t l y der ived. - - S t a t i s t i c a l m a t e r i a l on the de- indus t r ia l iza t ion process in the Uni ted K i n g d o m is p resen ted b y T h i r l w a l l [ i982 ]. The au thor also discusses the under ly ing causes and po in t s ou t t h a t in his v i ew " t h e m o s t con- v incing exp lana t ion of progressive de - indus t r i a l i za t ion in the U K is weaken ing of the foreign t rade sector" [p. 33]. I t is, however , su rp r i s ing t h a t he does no t men t i on the effects of the Br i t i sh oil boom as pa r t of the exp lana t ion .

2 In Norway, for example , there has been a wage freeze in I978179 and a d e v a l u a t i o n of the kroner in F e b r u a r y 1978. Moreover, subs id iz ing endangered b ranches of the t rad i - t ional exposed sector, especia l ly "o ld" indus t r ies and agr icul ture , ha s been, and s t i l l is, a pe rmanen t feature . One of the m a i n reasons for th i s pol icy is t h a t Norway , due to i t s topo- graphy, has m a n y small , i so la ted communi t ies , a m o n g them more t h a n 12o one-f i rm com- muni t ies , and t h a t there is a s t rong general s en t imen t aga in s t t a k i n g s teps to re- locate people. Del ibera te ac t iv i t i es to foster i n t e r sec to ra l l abour m o b i l i t y a re of a more recen t nature . F ina l ly , so far there has not been an " i n v e s t m e n t po l i cy" b u t t h i s m a y change to some extent . Several Norwegian ins t i tu t ions , inc lud ing gove rnmen t depa r tmen t s , are t r y i n g

486 K l a u s E n d e r s a n d H o r s t H e r b e r g

with these seven policies in turn, s tudy their effects oll the home economy and discuss their major advantages and disadvantages 1.

x. D e m a n d P o l i c y

Suppose the domestic government spends the amount GM on manu- factures and finances these purchases by issuing new money or new bonds. This policy is, however, totally ineffective. Domestic nominal absorption increases by GM, hoarding, i.e. the t rade balance, declines to Y - A - GM but wealth accumulation

(17) V ---- PM(QM - DM) - GM -J- PRQI~ -}- GM

t rade balance budget deficit

remains unaffected. Only its sources have par t ly changed: the accumula- tion of foreign reserves is reduced since exports of manufactures decrease or their imports increase but this is exactly matched by the additional supply of domestic money and bonds.

The curve C 8 merely has to be re-defined as the locus of pairs (Ps,W)

associated with zero wealth accumulation (V = 0). None of the curves C 1 to C, shifts, and there is no change in either of the equilibria. The basic reason why this policy fails to work is, of course, tha t the difficulties of the exposed sector are not due to "deficient" demand but ra ther to "excessive" costs of production. In fact, in the longer run it is outr ight disadvantageous since higher government demand is met by higher imports and these purchases are essentially financed by running down foreign reserves or foreign credit. (This appears to be par t of the current Mexican malaise2.)

to forecas t which fu ture oil and gas revenues can " s a f e l y " be expec ted and there seems to be a g rowing wi l l ingness no t to spend b u t r a t h e r to i n v e s t a n y "wind fa l l prof i ts" . - - Le t us also ment ion , a l though we canno t a p p r o p r i a t e l y s t u d y the consequences w i t h i n our model , t h a t for some t ime the Norwegian gove rnmen t has encouraged foreign f irms in t e re s t ed in exp lo i t ing Norweg ian oil and gas resources to p rov ide f inancia l and technica l a s s i s t ance to Norwegian f irms in the non-oil sector. The g o v e r n m e n t le t i t be known t h a t i t wou ld favoura - b ly appra i se such ac t iv i t i e s when g r a n t i n g new exp lo ra t ion or p roduc t ion licenses. Th i s pol icy which presen t ly is being re -examined , c l e a r l y a m o u n t s to an ind i rec t subs id i za t ion of Norwegian firms.

x Our ana lys i s wil l aga in be based on the a s s u m p t i o n t h a t the curves C2 and C s a re u p w a r d sloping, b u t i t is ea sy to confirm t h a t our resul ts c a r r y over to the r e m a i n i n g cases as well.

s I t should be kep t in m i n d t h a t i n the m e d i u m an d the long run wea l th a c c u m u l a t i o n ha s ceased and the t r ade deficit equals g o v e r n m e n t spend ing GM. Obvious ly , such a s i t u a t i o n canno t be sus ta ined indefini tely. - - The ou t look would be less b l eak if the wor ld supp ly o f manufac tu res was less t h a n perfect ly e las t ic so t h a t an increase in d e m a n d would to s o m e

The Dutch Disease 487

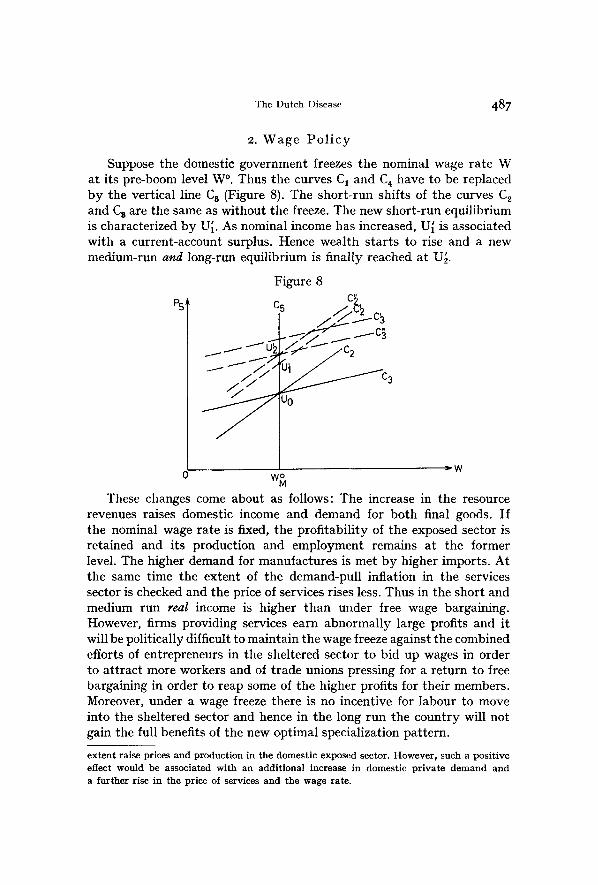

2. W a g e P o l i c y

Suppose the domestic government freezes the nominal wage ra te W at its pre-boom level W ~ Thus the curves C 1 and C 4 have to be replaced by the vertical line C 6 (Figure 8). The shor t - run shifts of the curves C2 and C 8 are the same as without the freeze. The new short-run equilibrium is characterized b y U~. As nominal income has increased, U[ is associated with a current-account surplus. Hence wealth s tar ts to rise and a new medium-run and long-run equilibrium is finally reached at U~.

Figure 8

0 w~

These changes come about as follows: The increase in the resource revenues raises domestic income and demand for both final goods. I f the nominal wage ra te is fixed, the profi tabil i ty of the exposed sector is retained and its production and employment remains at the former level. The higher demand for manufactures is met b y higher imports. At the same t ime the extent of the demand-pull inflation in the services sector is checked and the price of services rises less. Thus in the short and medium run real income is higher than under free wage bargaining. However, firms providing services earn abnormal ly large profits and it will be politically difficult to maintain the wage freeze against the combined efforts of entrepreneurs in the sheltered sector to bid up wages in order to a t t rac t more workers and of t rade unions pressing for a re turn to free bargaining in order to reap some of the higher profits for their members. Moreover, under a wage freeze there is no incentive for labour to move into the sheltered sector and hence in the tong run the country will not gain the full benefits of the new optimal specialization pat tern.

extent raise prices and production in the domestic exposed sector. However, such a posit ive effect would be associated with an addit ional increase in domestic pr ivate demand and a further rise in the price of services and the wage rate.

488 K l a u s E n d e r s a n d H o r s t t t e r b e r g

3. D e v a l u a t i o n

Since in the short and medium run a resource boom lowers the pro- fitability of the exposed sector, it can be expected that this sector's lobby will strongly advocate a devaluation of the home currency to reduce imports of manufactures and raise their domestic production. At first sight, such a policy does not appear to have negative effects for any identifiable group at home. Therefore, it will be tempting to resort to it, and the central bank will perhaps be the only institution to have reser- vations because of the expected inflationary consequences.

Applied in the post-boom situation a devaluation basically has two impact effects: I t raises the home currency prices of manufactures and raw materials and thus leads to a higher nominal income and spending, and it raises the full-employment wage rate in the exposed sector. We need to be more specific: Suppose the exchange rate has gone up by, say, IO percent. Obviously PM, PR and WM also rise by IO percent. Assume for the moment that production in each of the domestic sectors is still at the pre-devaluation level. The price changes then induce an increase in nominal income and nominal domestic demand for manufactures and services, however, by less than IO percent. Hence the price of services rises as well, and this reinforces, and is reinforced by, a further increase in income and demand. As long as wealth has not reached its desired level, nominal demand changes relatively less than nominal income. There- fore, Ps, Ws and W = max(Ws,WM) go up by less than IO percent, quantitative demand for manufactures, D~, falls and, most important, the price-wage ratio PM/W rises. The last change implies tha t in the short run a devaluation at least par t ly restores the profitability of the exposed sector. Hence, contrary to our assumption, it expands output and employment. I t even cannot be ruled out that the exposed sector becomes the wage leader and reaches its full-employment production level while the sheltered sector has to reduce its activities and lay off some workers 1. These changes have further effects on nominal income, spending etc., but the last conclusions obviously remain valid.

In addition, the devaluation affects the subsequent post-boom develop- ment of the home economy since higher income implies larger current account surplusses and augmented wealth accumulation. Instead of trying to trace the differences in the entire adjustment processes with and without an exchange rate change we simply compare the two medium- run equilibria these processes approach. Suppose again that the exchange rate and hence PM, PR and WM have gone up by IO percent and that

1 Such a n o u t c o m e , however , a p p e a r s to be r a t h e r un l ike ly s ince a d e v a l u a t i o n e n h a n c e s the resource b o o m b y f u r t h e r r a i s i n g r a w - m a t e r i a l p r ices a n d revenues .

The D u t c h Disease 489

production is still unchanged. Since in the medium run hoarding is zero, nominal income and nominal spending on both services and manufactures increase by the same percentage. This implies tha t similar effects as described above lead to a rise in Y, Ps, Ws and thus W by IO percent also. As the devaluation leaves the medium-run price-wage ratios PM/W and Ps/W unchanged, it has no effect on sectoral output and employment.

Thus a discomforting though not surprising result emerges: The real effects of a devaluation are merely transient; the exposed sector cannot sustain the initial expansion in output and employment but gradually has to reduce its activity to the pre-devaluation level The only lasting changes are purely nominal ones like price and wage increases, and they are certainly not desirable 1. The situation would get even worse if the domestic government, dissatisfied with the short-run rise in employment, or failing to understand the true reasons for its subsequent decline, would conclude the first devaluation was not large enough and would raise the exchange rate again. Unfortunately, such a wrong decision may well be made and hence the home economy may enter into a vicious circle of devaluations and price increases combined with continuing unemploy- ment.

4. P r o d u c t i o n S u b s i d y

Another request of the exposed sector, when experiencing the dismal short-run effects of a boom, could be for a subsidy to lower its costs. Assume that indeed the domestic government has agreed to pay a certain subsidy per unit of output and to finance it out of lump-sum taxes. As this improves its profitability, the exposed sector expands production and employment. Consequently, nominal income and spending rise. Due to the demand-pull effect there is some increase in the price of services which reinforces, and is reinforced by, the income increase. If the sheltered sector remains the wage leader, W goes up by the same percentage as Ps. Although the exposed sector then faces somewhat higher production costs, its output will remain above the pre-subsidy level. For a large enough subsidy, however, the exposed sector becomes tile wage leader and reaches full employment while tile sheltered sector's production declines to some extent. Under these circumstances the price of services is subject also to a cost-push effect as W has risen by more than Ws. Again the exposed sector has benefitted.

1 One of the bas i c r e a sons for th i s r e su l t is t h a t in the m e d i u m r u n the r ea l w a g e r a t e s W / P M a n d W / P s r e t u r n to t he i r in i t i a l (p re -deva lua t ion ) levels. The refore, i t is n o t s u r p r i s i n g t h a t H e r b e r g a n d M c C a n n [1982 ] a r r i v e a t a s im i l a r conc lus ion for a smal l e c o n o m y w i t h per fec t wage i ndexa t i on , i.e., w i th c o n s t a n t rea l wages .

49 ~ K l a u s E n d e r s a n d H o r s t l t e r b e r g

Clearly, these conclusions apply to tile short run as well as to the medium run. But it should be observed tha t a certain initial improvement in the exposed sector 's situation cannot always be sustained (although it never disappears completely). This is due to the fact tha t the income increase leads to a higher current account surplus and additional wealth accumulation. I-Ience there is some fur ther rise in the demand for, and the price of, services. I f the exposed sector has become and remains the wage leader, it can continue to produce at the full employment level. Otherwise, it has to cut back its activities. Moreover, in the first case the sheltered sector will, and in the second it may, gradual ly expand output and employment.

Thus we can state the exposed sector will gain from a subsidy policy, normally in the short run b y more than in the long run, and tha t the sheltered sector m a y lose. However difficult it m a y be, the beneficial effects should be weighed against the harmful consequences, especially against the inflationary pressures and against the long-run losses as- sociated with the imperfect adjus tment to the new optimal international division of labour. I t should be kept in mind tha t subsidies are seldom reduced and hardly ever abolished. In the present case it is ra ther more likely tha t the exposed sector will lobby for more support if the initial payments have not removed its employment problems or if they reappear over t ime a.

5. I m p o r t T a r i f f s

First we observe tha t in the medium and long run, the current account then being balanced, the home economy imports manufactures. We assume tha t this is, and remains, the case in the short run as well. By im- posing or increasing a tariff on imports the domestic price PM of manu- factures is raised while its world-market price is unaffected. Firms in the exposed sector will therefore expand their production. The higher value of P~QM causes a rise in nominal income, spending and hoarding and leads to an improvement of the t rade balance. Thus, forces similar to those in the previous case are at work and similar conclusions apply.

6. I m p r o v i n g L a b o u r M o b i l i t y

As we have seen, a resource boom is bound to lead to some de-indus- trialization through a contraction of the tradit ional exposed sector and

* If the resources can be expected to be only short-lived, the case for subsidies is obviously strengthened. This is par t icular ly true if there are learning-by-doing effects in the exposed sector due to which its future performance and its present size are posi t ively correlated. This interesting point has been made by Wijnbergen [I982],

The Dutch Disease 4 9 I

to inflationary pressures through rising prices for the products of the sheltered sector. Some of these changes are permanent , and there are good economic reasons for tolerating them (and little hope to aver t them). Others, however, are transitory, and as they create unnecessary strains their magnitude and duration should be reduced. These lat ter changes are due to an insufficient intersectoral mobil i ty of labour (and of other factors of production). Following the old and well-known rule tha t the best cure usually is to a t tack the disease as directly as possible it can be expected tha t any policy tha t effectively improves labour mobil i ty will really help. This conjecture can easily be confirmed b y comparing the short-run and medium-run equilibria with the long-run equilibrium (cf. Figures 6 and 7 and our discussion at the end of Section I I I ) . We only have to remember tha t it is the "migrat ion" of workers from the exposed to the sheltered sector tha t restores full employment in the long run.

A policy as envisaged here obviously can take various forms which we do not want to enumerate and discuss. We only observe tha t in a country like Norway (cf. note 2, p.485) it would have to include measures tha t offer new employment opportunities in the sheltered sector at locations where the exposed sector is forced to lay off workers. The costs of suitable policy measures may be substantial but they should be transient while their returns can be expected to be large and permanent .

7. I n v e s t m e n t A b r o a d

This policy is obviously followed by some of the Middle-East OPEC- countries like Saudi Arabia and Kuwait . These countries use a major par t of their revenues from oil exports to build up a portfolio of foreign securities and thus substitute oil-in-situ b y interest-bearing assets. Clearly, by lowering the rise or diminishing the fluctuation in current absorption, such a policy reduces the present adverse and possibly even disruptive effects of a resource boom and buys time for a slower and less erratic adjustment process. Moreover, it allows the economy to reap some of the benefits of the resource boom after it has come to an end.

I~owever, it should not be overlooked tha t in the case of a prolonged resource boom, as is predicted for Norway, such a policy will give rise to a secondary "boom" due to growing interest income from the foreign assets. Present difficulties would be reduced, thereby creating future ones. Under such circumstances it would be sensible to follow an investment policy tha t takes care of unexpected fluctuations in resource revenues and allows for a steady, or smoothly changing, spending pat tern.

492 K l a u s E n d e r s a n d H o r s t H e r b e r t .

8. C o n c l u s i o n

Thus we arrive at the following general conclusion: On balance, a country will always gain from a resource boom. However, some groups will lose and will press for policies to improve their fate. Of the seven policies to cure the Dutch disease tha t we studied, namely, demand policy, wage freeze, devaluation, subsidies, impor t tariffs, improving labour mobility, and investing abroad, only the last two can be relied upon as being definitely successful. The other five policies will at best provide a partial relief in the short as well as in the longer run. They are calmatives tha t relieve the pain ra ther than healing the malady 1.

V. Some Extensions

Our findings have been derived from a simple and restrictive model. Hence the question arises whether or not they are more generally valid. Tha t the answer is positive can be deduced, of course, from the results reported in other papers on the Dutch disease like those referred to in note 2 on page 473. But let us take a more direct approach to s tudy this question.

Basically, our foriner arguments imply that , following a resource boom, the economy will be plagued by the Dutch disease, in particular, tha t it will experience a decline in the production and employment of its tradit ional exposed sector, whenever (i) the boom raises domestic absorp- tion and (ii) the spending effect, by increasing the price of services, leads to higher wages in both the sheltered and the exposed sector. Therefore, the following conclusions are quite obvious: I. For our results to hold, the wage rates paid by the sheltered and the exposed sector need not change uniformly or proport ionally but only must move into the same direction. Hence, the intersectoral wage link could be much weaker than assumed above 2. 2. Moreover, this link could even be entirely different. We cannot, and need not, rule out tha t in a boom tile resource sector, although it employs little or no (additional) labour, sets the pace for wage increases 3. Under

1 As is well k n o w n , p a t i e n t s s o m e t i m e s need seda t ives . H o w e v e r , these shou ld be a p p l i e d c a u t i o u s l y wi th due r e g a r d to t he i r s ide-effects a n d as p a r t of a m o r e t h o r o u g h t h e r a p y .

t A l t h o u g h th i s impl ies t h a t a d e v a l u a t i o n m i g h t i m p r o v e the e x p o s e d s e c t o r ' s s i t u a t i o n p e r m a n e n t l y , such a n o u t c o m e seems to be r a t h e r un l ike ly s ince ove r a l onge r t i m e p e r i o d wages t end to c h a n g e b y more or less the s a m e pe rcen t age .

I n N o r w a y wages of off-shore w o r k e r s severa l t imes seem to h a v e h a d s o m e effect o n the gene ra l wage level. Af t e r the r e c e n t f o r m a t i o n of s e p a r a t e t r a d e u n i o n s fo r t he oil in- d u s t r y th i s is l ikely to h a p p e n aga in . To d i s c o u r a g e oil f i rms f r o m g r a n t i n g " e x c e s s i v e "

The Dutch Disease 493

such circumstances the exposed sector is even more severely affected and, moreover, the sheltered sector m a y also have to reduce its activities. 3. Tile assumption of constant expenditure shares can be relaxed as well. Suppose instead tha t services and manufactures are superior goods and substitutes of each other. Then the spending effects of a boom will again raise the price of services and the wage rate(s). Hence in the short and in the longer run the exposed sector will show the symptoms of the Dutch disease. However, they tend to be the less marked the larger the elasticity of commodity substitution is. 4. The relationships determining total nominal spending and desired wealth need not be as simple as we modelled them. For example, the marginal rate of absorption out of resource revenues m a y differ from and possibly even exceed, the marginal rate of absorption out of other income 1. As long as the first of these rates is positive, a resource boom will be associated with an income/spending effect and its consequences. Furthermore, it can well be argued tha t such a boom, if it is due to newly discovered deposits or iligher prices of the raw material , is reflected in a sudden and perhaps large increase in actual wealth. But this would imply a stronger wealth/spending effect than otherwise. 5. Finally, we can relax the assumption tha t labour is the only variable factor of production. Suppose instead tha t capital is also used in the sheltered and the exposed sector and tha t it is mobile in the long run. Then again a boom can be expected to cause a contraction of the exposed sector that initially is more severe than permanently. But there is an exceptional and ra ther unrealistic case, namely, tha t the production of services is much more capital-intensive than the production of manufactures. Under these conditions the then expansionary factor-movement effect will finally prove to be stronger than the contract ionary effects. Therefore, in the long run, the exposed sector will produce more and the sheltered sector less than before the boom. Initially, however, all changes are the same as described aboveL

Thus our findings turn out to be much more generally valid than our model seemed to indicate. They even largely survive if, in the longer run, there are noticeable differences in labour product ivi ty increases in the exposed and the sheltered sector, provided these differences do not

wage increases the gove rnmen t is, however , cons ider ing to fix taxes and roya l t i es on the bas is of " n o r m a l " labour costs only.

The gove rnmen t ' s r a t e of absorp t ion is l ikely to be u n i t y or a t l eas t to exceed the general publ ic ' s ra te .

i These conclusions are confirmed b y the resul ts of Corden and N e a r y [1982], and N e a r y

and Purv i s [I982].

494 Klaus Ender sand Florst Herbe rg

become too large. Moreover, we note that our approach can easily be adapted to deal with a resource bust, i.e., an unexpected and permanent drop in raw-material revenues.

I t would also be intriguing to analyse the case of flexible exchange rates and/or domestic capital formation. But as this would require a major reconstruction of our model, we presently refrain from studying these important problemsL

A p p e n d i x

Denote, for i = M, S, the supply elasticity of the i-th sector, i.e., the elasticity of Qi with respect to Pi/W by *i. Denote further the partial derivative of a function g with respect to its j-th argument by gj; for example, fsl = ~fs/~Ps.

From equations (3), (4) and (IO), for i, j : M, S and i # j:

8W/SPi ---- fil : W / P i > 0, 8 W / 8 ~ i : fi~ < 0 if Wi > Wj (I6)

ew/ePi = eW/e[i = 0 if w~ < w~

From equations (2), (6)--(8) and (II):

Fs(...) ---- ~s(i - ~k) (P~tQM -4- PsQs + PRQR) + at*sV - PsQs

Obviously, the partial derivatives of F s with respect to PM, PRQR and V are all positive. Moreover,

(17) %Fs/%Ps : - [i - ~s(l - =k)] Qs (i + cs) < o

(18) 8Fs/SW = [1 - ~s(1 - ak)] (PsQs/W) *s

- ~s(1 - r162 (PMQ~/W) *M > 0

From equations (2), (6)--(8) and (I2):

F v ( . . . ) : P~QM + PRQR - at~MV - ~M(i -- =k) (P~QM + PsQs + PRQR)

The partial derivatives of Fv with respect to PM and PRQR are positive and that with respect to V is negative. Furthermore,

(19) aFvlaPs ---aM(i-cr Qs(i + cs) <0

(20) ~Fv/~W = a~(1 - =k) (PsQs/W) Cs

- [1 - aM(1 -- =k)] (PMQm/W) *M ~ 0

1 The flexible-exchange-rates case has been covered by Neary and Purvis [I982], and implicitly also by Corden and Neary [i98~].

The Dutch Disease 495

F r o m e q u a t i o n s (4), (5) a n d (13):

W : fM(PM, LM), f~t(PM, LM) = fs(Ps, [~ - L~t)

T o t a l d i f f e r en t i a t i on of t h e l a s t t w o e q u a t i o n s y i e l d s :

(21) ~Ps/%W = (fM, + fs,)IfM2fs, > 0

(22) ~Ps/OPM = - fMlfS2/fMsfSx < 0

E q u a t i o n s (16)--(22) i m p l y t h a t t h e u p p e r p a r t C~ of C 1 a n d t h e e n t i r e

c u r v e C 4 a r e p o s i t i v e l y s loped w h i l e C 2 a n d C a m a y be r i s ing , f a l l i ng o r h o r i z o n t a l , o r e v e n c h a n g e t h e i r s lope. M o r e o v e r , t a k i n g t h e s a m e re-

l a t i o n s h i p s in to a c c o u n t i t is e a s y to p r o v e i n e q u a l i t y (15) in t h e m a i n t e x t .

References

Aukrust, Odd, "Inflation in the Open Economy: A Norwegian Model". In: Lawrence B. Krause, Walter S. Salant (Eds.), Worldwide Inflation - - Theory and Recent Experience. Washington, D.C., 1977, PP. lO7--153.

Bjerkholt, Olav, Lorents Lorentsen, and Steinar Strum, "Using the Oil and Gas Revenues: The Norwegian Case". In: Terry Barker and Vladimir Brailovsky (Eds.), Oil or Industry ? London x98I, pp. 171--184.

Calve, Guillermo, and Ronald Findlay, "On the Optimal Acquisition of Foreign Capital Through Investment of Oil Export Revenues". Journal el International Economics, Vol. 8, 1978, pp. 513--524 .

Corden, W. M., and J. Peter Neary, "Booming Sector and De-Industrialization in a Small Open Economy". The Economic Journal, Vol. 92, 1982, pp. 825--845.

Dornbusch, Rudiger, and Michael Mussa, "Consumption, Real Balances and the Hoarding Function". International Economic Review, Vol. 16, 1975, PP. 415--42 I.

Edgren, GOsta, Karl-Olof Fax~n, and Clas-Erik Odhner, Wage Formation and the Economy. Translated from the Swedish by Margareta Ekl6f. London 1973.

Eide, Erring, "Virkninger av Statens Oljeinntekter pa Norsk Okonomi". Sosial- ckonomen, Vol. 27, No. io, 1973, pp. 12--21.

Ellman, Michael, "Natural Gas, Restructuring and Re-industrialisation: The Dutch Experience of Industrial Policy". In: Terry Barker and Vladimir Brailovsky (Eds.), Oil or Industry? London 1981, pp. 149--166.

Enders, Klaus, Die "Holliindische Krankheit'" oder Problemc eines sektoralen Booms. Universitlit Kiel, 1982, mimeo.

Finansdepartementet, Petroleumsvirksomshetens plass i det norske sam/unn. St. meld. nr. 25, Oslo 1973/74.

Gregory, Robert G., "Some Implications of the Growth of the Mineral Sector". The Australian Journal of Agricultural Economics,Vol. 2o, 1976, pp. 71--91.

Herberg, Horst, and Ewen McCann, "Imported Intermediate Goods, Foreign Price Increases, and Domestic Monetary Policy: The IS-LM Analysis Revived" . Zeit- schrift/i~r Wirtschalts- und Sozialwissenscha/ten, Vol. lO2, 1982, pp. 237--258.

496 K l a u s E n d e r s a n d H o r s t H e r b e r g

Hoel, Michael [ 1981 a], " E m p l o y m e n t Effec ts of an I n c r e a s e d Oil Pr ice in a n E c o n o m y wi th S h o r t - R u n L a b o r I m m o b i l i t y " . The Scandinavian Journal of Economics, Vol. 83, 1981, pp. 269- -276 .

- - [198ib] , " R e s o u r c e E x t r a c t i o n by a Monopol i s t w i t h In f luence ove r t he R a t e of R e t u r n on N o n - R e s o u r c e Asse t s " . International Economic Review, Vol. 22, 1981, pp. 147--157.

Kaldor , Nicholas, " T h e E n e r g y I s sue s " . In : T e r r y Ba rke r a n d V l a d i m i r B r a i l o v s k y (Eds.), Oil or Industry ? L o n d o n 1981, pp. 3---9.

Neary, J . Peter, a n d Douglas D. Purvis , "Sec to ra l Shocks in a D e p e n d e n t E c o n o m y : L o n g - R u n A d j u s t m e n t a n d S h o r t - R u n A c c o m o d a t i o n " . The Scandinavian Journal of Economics, Vol. 84, 1982 , pp. 229- -253 .

Ngo Van Long, " T h e Effects of a B o o m i n g E x p o r t s I n d u s t r y on t h e R e s t of t he E c o n o m y " . The Economic Record, Vol., 58, 1982, pp . 57 - -6o .

Organisa t ion for Economic Co-operat ion and Deve lopmen t (OECD), OECD Economic Surveys: Norway. Paris , va r i ous issues.

Snape, Richard H., "Ef fec t s of Minera l D e v e l o p m e n t on t h e E c o n o m y " . The Australian Journal of Agricultural Economics, Vol. 21, 1977, Pp. I 4 7 - - t 5 6 .

Thir lwall , A. P., " D e - i n d u s t r i a l i s a t i o n in t he U n i t e d K i n g d o m " . Lloyds Bank Review, 1982, No. 144, pp. 22- -37 .

Wi jnbe rgen , Sweder van , The "Dutch Disease": A Disease After All? W o r l d B a n k , W a s h i n g t o n , D.C., 1982, mimeo .

Z u s a m m e n f a s s u n g : Die , ,holl~.ndische K r a n k h e i t " : Ur sachen , Folgen , Hei l - uud B e r u h i g u n g s m i t t e l . - - In dieser Arbe i t wird u n t e r s u c h t , w a r u m in e i n e m indu - s t r ia l i s ie r ten L a n d , das e inen wich t igcn Rohs to f f expor t i e r t , e iu z. B. d u r c h h6hc re W e l t m a r k t p r e i s e oder die E n t d e c k u n g ncue r Lagers t i~ t ten ausge l6s t e r R e s s o u r c e n - boom neben vor t e i lha f t en a u c h nachte i l ige Folgen h a b e n k a n n . I n s b e s o n d e r e g e h t es u m die Frage , w a r u m ein solches L a n d u n t e r de r , ,ho l l i ind ischen K r a n k h e i t " leiden, d. h. sein t r ad i t ione l le r H a n d e l s s e k t o r s c h r u m p f e n wird. Aul3erdem werden die Folgen ve rsch iedener Po l i t iken wie e ines L o h n s t o p p s , e iner A b w e r t u n g oder von S u b v e n t i o n e n be t r ach t e t , d ie v e r m u t l i c h als G e g e n m a l 3 n a h m e n ge fo rde r t ode r ein- gese tz t werden. Das E rgebn i s ist, d ab die m e i s t e n d ieser Po l i t iken k a u m wirk l ich e r fo lgversp rechend s ind u n d sogar nu tz los oder a u s g e s p r o c h e n schAdlich sein k6nnen .

R6 s u m 6 : L a , m a l a d i e ho l l anda i se , : ra isons , cons6quences , cures e t c a l m a n t s . - - D a n s l ' a r t ic le nous d i s cu t ons p o u r q u o i u n p a y s indus t r i a l i s6 e x p o r t a n t q u e l q u e nlati~.re p remiere i m p o r t a n t e es t affect6 n 6 g a t i v e m e n t p a r une h a u s s e en ma t i~ re premiere caus6e, pa r exemple , pa r u n e a u g m e n t a t i o n des p r i x au m a r c h 6 m o n d i a l ou pa r la d6couver te des n o u v e a u x g i semen t s . E n pa r t i cu l i e r nous nous o c c u p o n s de la ques t i on p o u r q u o i ii sera affect6 pa r la ~lnaladie hol landaise~, c ' e s t - s p a r une con t r ac t i on de son sec teur t r a d i t i o n n e l l e m e n t commerQant . De plus , n o u s 6 tud ions les cons6quences de que l ques pol i t iques , c o m m e pa r e x e m p l e d ' u n b locage des

The Dutch Disease 497

salaires, d ' u n e d d v a l u a t i o n ou d ' u n accord des s u b v e n t i o n s qu i p r o b a b l e m e n t s o n t optdes pour ou adop tdes comme cures, e t nous d d m o n t r o n s que p o u r la p l u p a r t de ces po l i t i ques on ne p e u t gu~re a t t e n d r e un succbs rdel e t q u ' e l l e s p e u v e n t ~tre m~me inu t i l e s ou d i r e c t e m e n t mal fa i san tes .

R e s u m e n : L a e n f e r m e d a d h o l a n d e s a : causas , consecuencias , cu ras y c a l m a n - tes. - - E n el a r t i cu lo se d i scu te como un pa l s i n d u s t r i a l i z a d o que e x p o r t e a l g u n a m a t e r i a p r i m a i m p o r t a n t e , puede ser a f e c t a d o a d v e r s a m e n t e p o t un ~boom,> en el mercado de m a t e r i a s p r i m a s deb ido po t e j emplo a l d e s c u b r i m i e n t o de n u e v o s yac imien tos , o a precios mas a l tos en los mercados m u n d i a l e s . Se a n a l i z a espec ia l - men te el caso de como el pa ls se verA a fec t ado po t l a e n f e r m e d a d ho landesa , es decir , por una con t racc idn de su sector comerc ia l t r ad i c iona l . A d i c i o n a l m e n t e , se e s t u d i a n las consccuencias de las m e d i d a s mas p r o b a b l e s de ser a d o p t a d a s p a r a r e m e d i a r l a s i tuac idn , t a les como una congelac idn de sa lar ios , u n a deva l uac i dn , o u n a conces idn de subsidios . Se m u e s t r a como la m a y o r p a r t e de ds tas no p u e d e n t e n e r dx i to e incluso pueden l l egar a ser perniciosas .

Weltwirtschaftliches Archly Bd. CXIX. ~kq