the economics of lng export contract flexibility · the economics of lng export contract...

TRANSCRIPT

www.eprg.group.cam.ac.uk

Yichi Zhang, Chi Kong Chyong, Pierre Noël

EPRG, University of Cambridge

EPRG Winter Research Seminar – 07 December 2012

The Economics of LNG Export Contract Flexibility:

a quantitative approach

1

www.eprg.group.cam.ac.uk

Introduction: Gas market and long term contracts (LTC)

Research questions

Methodology: Value of LNG contracts flexibility

Gas market equilibrium model

Results: Impact of LTC flexibility on prices

Impact of LTC flexibility on producer profits and market efficiency.

Sensitivity analysis

Conclusion

Contents

2

www.eprg.group.cam.ac.uk

IEA: Gas consumption could rise more than 50% over the next 25 years.

Golden Age for Natural Gas?

Massively expanding unconventional gas in North America.

Uncertainty about nuclear power after Fukushima

Surging gas demand, especially in emerging markets (e.g, China, India, Middle East)

Introduction: Gas market and long term contracts (LTC)

3

www.eprg.group.cam.ac.uk

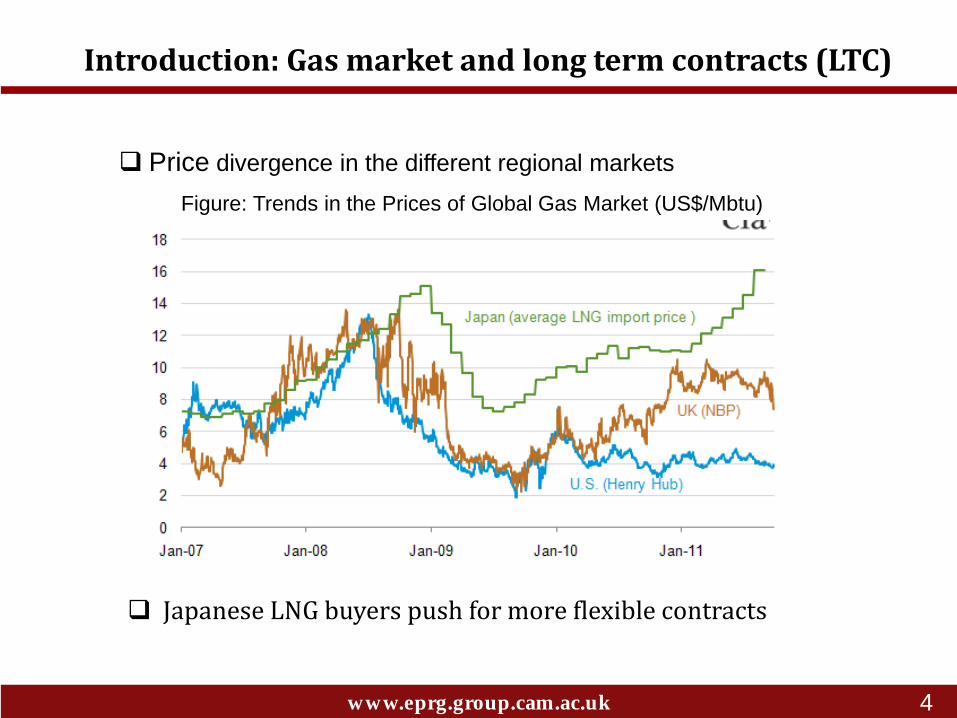

Figure: Trends in the Prices of Global Gas Market (US$/Mbtu)

Price divergence in the different regional markets

Introduction: Gas market and long term contracts (LTC)

Japanese LNG buyers push for more flexible contracts

4

www.eprg.group.cam.ac.uk

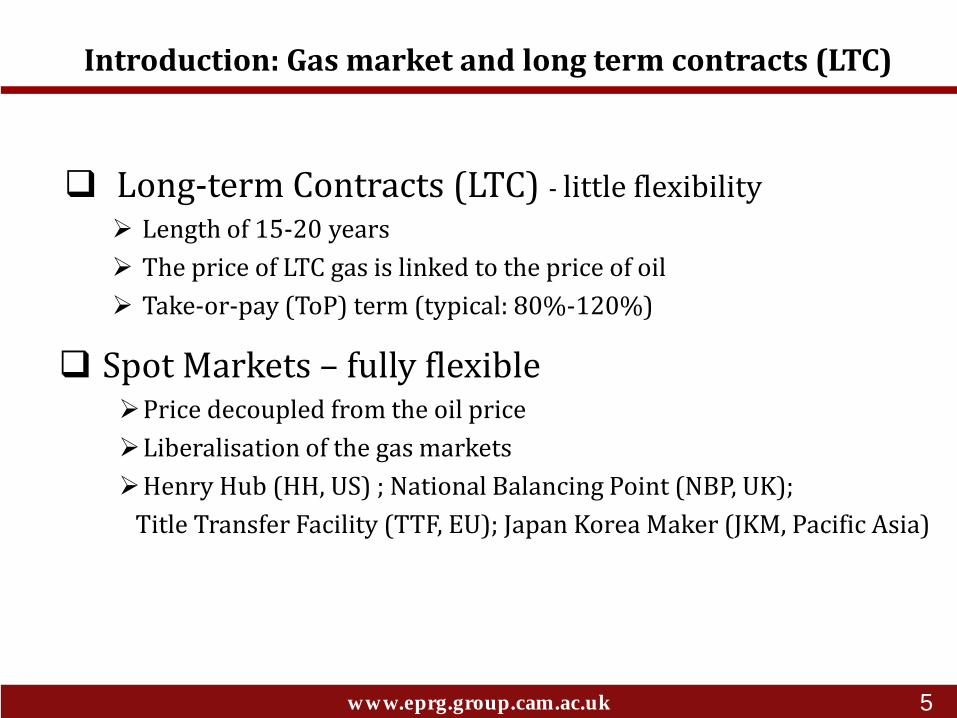

Long-term Contracts (LTC) - little flexibility

Length of 15-20 years

The price of LTC gas is linked to the price of oil

Take-or-pay (ToP) term (typical: 80%-120%)

Spot Markets – fully flexible Price decoupled from the oil price

Liberalisation of the gas markets

Henry Hub (HH, US) ; National Balancing Point (NBP, UK);

Title Transfer Facility (TTF, EU); Japan Korea Maker (JKM, Pacific Asia)

Introduction: Gas market and long term contracts (LTC)

5

www.eprg.group.cam.ac.uk

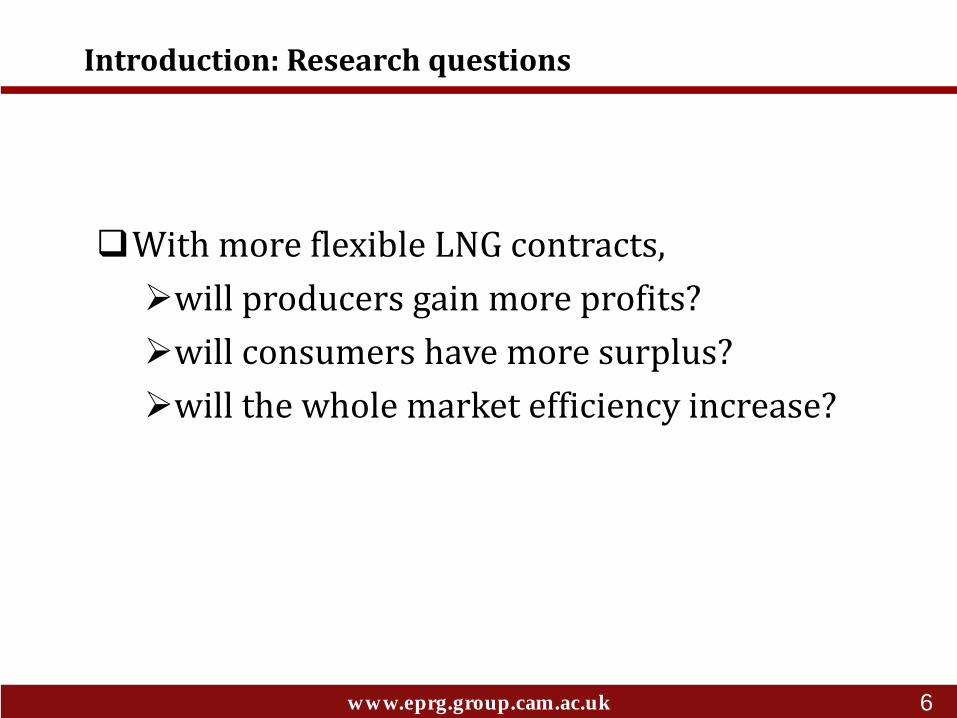

With more flexible LNG contracts,

will producers gain more profits?

will consumers have more surplus?

will the whole market efficiency increase?

Introduction: Research questions

6

www.eprg.group.cam.ac.uk

Introduction: Gas market and long term contracts (LTC)

Research questions

Methodology: Value of LNG contracts flexibility

Gas market equilibrium model

Results: Impact of LTC flexibility on prices

Impact of LTC flexibility on producer profits and market efficiency.

Sensitivity analysis

Conclusion

Contents

7

www.eprg.group.cam.ac.uk

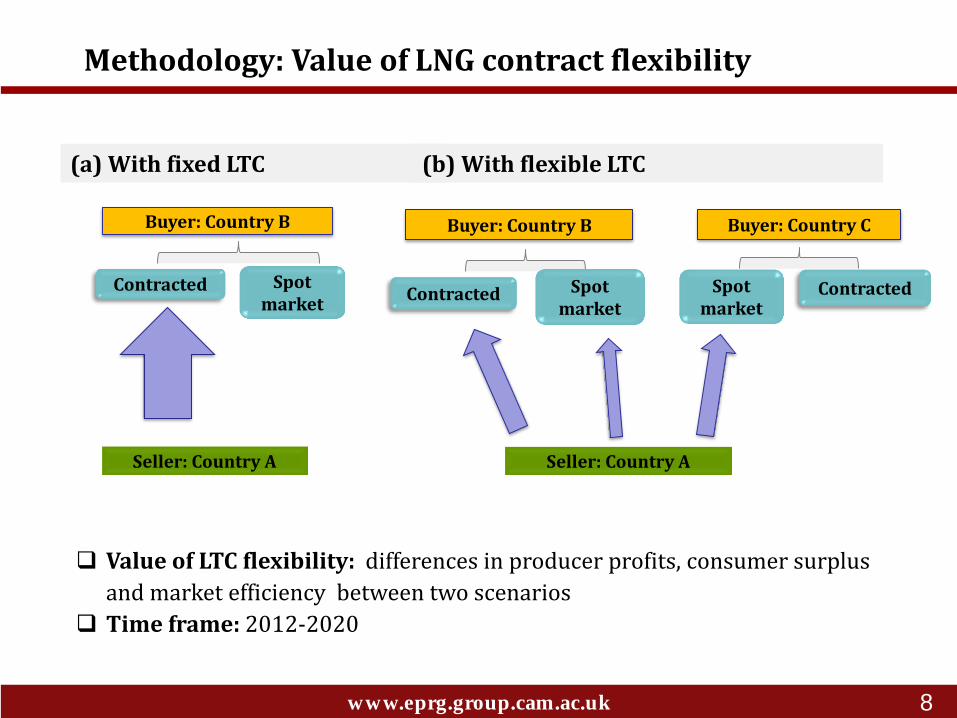

Seller: Country A

Buyer: Country B

Contracted Spot market

(a) With fixed LTC

Seller: Country A

Buyer: Country B

Spot market

Buyer: Country C

Spot market

Contracted

(b) With flexible LTC

Contracted

Methodology: Value of LNG contract flexibility

Value of LTC flexibility: differences in producer profits, consumer surplus

and market efficiency between two scenarios

Time frame: 2012-2020

8

www.eprg.group.cam.ac.uk

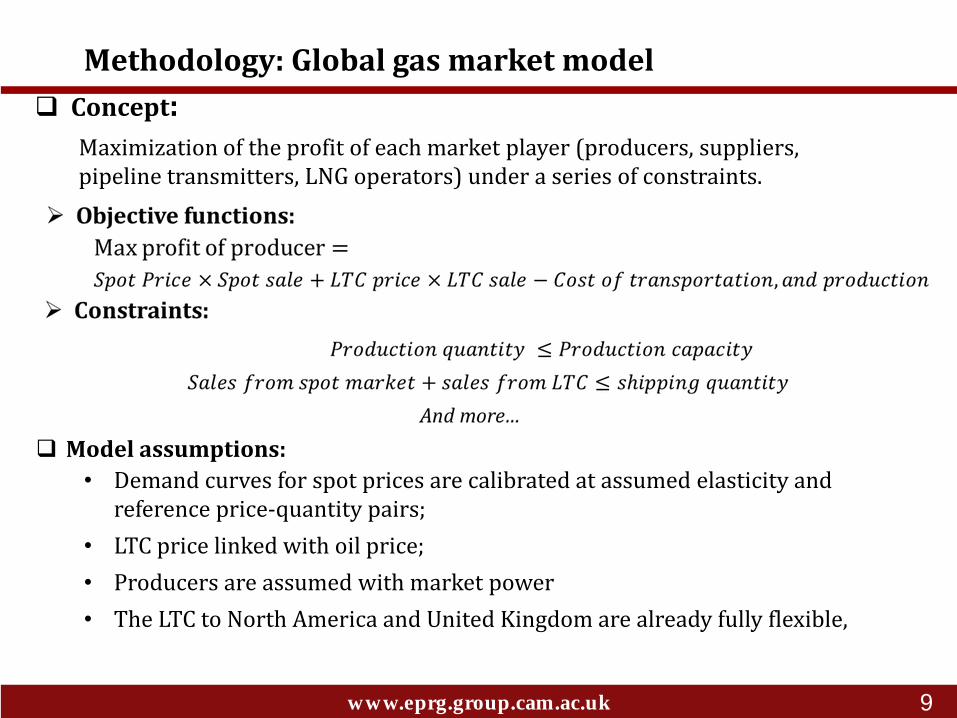

Maximization of the profit of each market player (producers, suppliers, pipeline transmitters, LNG operators) under a series of constraints.

Concept:

Methodology: Global gas market model

Model assumptions:

• Demand curves for spot prices are calibrated at assumed elasticity and reference price-quantity pairs;

• LTC price linked with oil price;

• Producers are assumed with market power

• The LTC to North America and United Kingdom are already fully flexible,

9

www.eprg.group.cam.ac.uk

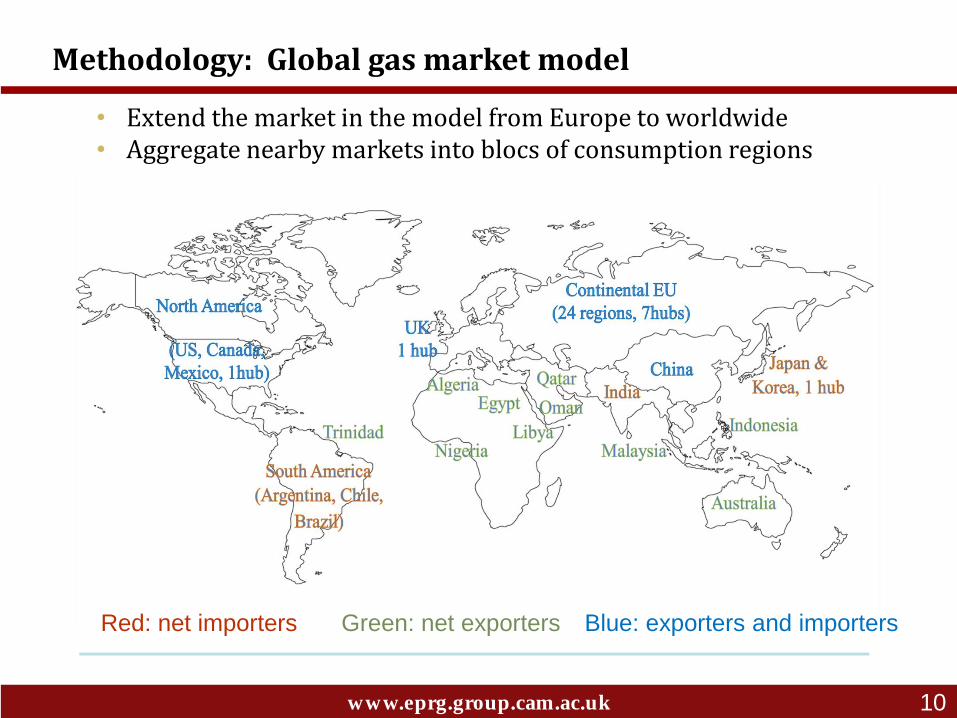

Methodology: Global gas market model

• Extend the market in the model from Europe to worldwide • Aggregate nearby markets into blocs of consumption regions

Red: net importers Green: net exporters Blue: exporters and importers

10

www.eprg.group.cam.ac.uk

…

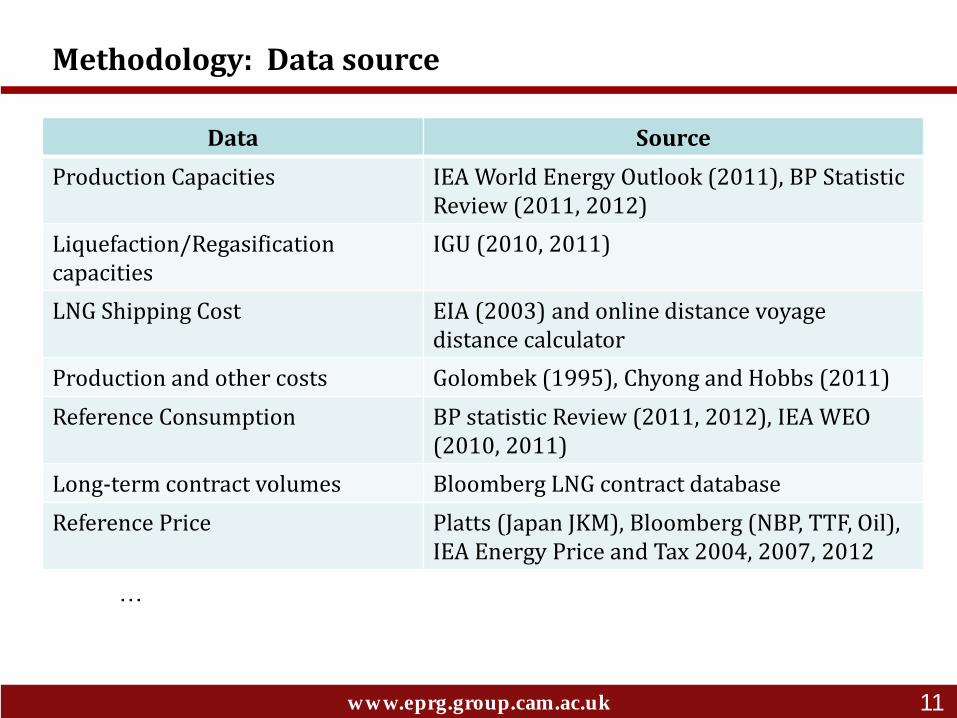

Data Source

Production Capacities IEA World Energy Outlook (2011), BP Statistic Review (2011, 2012)

Liquefaction/Regasification capacities

IGU (2010, 2011)

LNG Shipping Cost EIA (2003) and online distance voyage distance calculator

Production and other costs Golombek (1995), Chyong and Hobbs (2011)

Reference Consumption BP statistic Review (2011, 2012), IEA WEO (2010, 2011)

Long-term contract volumes Bloomberg LNG contract database

Reference Price Platts (Japan JKM), Bloomberg (NBP, TTF, Oil), IEA Energy Price and Tax 2004, 2007, 2012

Methodology: Data source

11

www.eprg.group.cam.ac.uk

Introduction: Gas market and long term contracts (LTC)

Research questions

Methodology: Value of LNG contracts flexibility

Gas market equilibrium model

Results: Impact of LTC flexibility on prices

Impact of LTC flexibility on producer profits and market efficiency.

Sensitivity analysis

Conclusion

Contents

12

www.eprg.group.cam.ac.uk

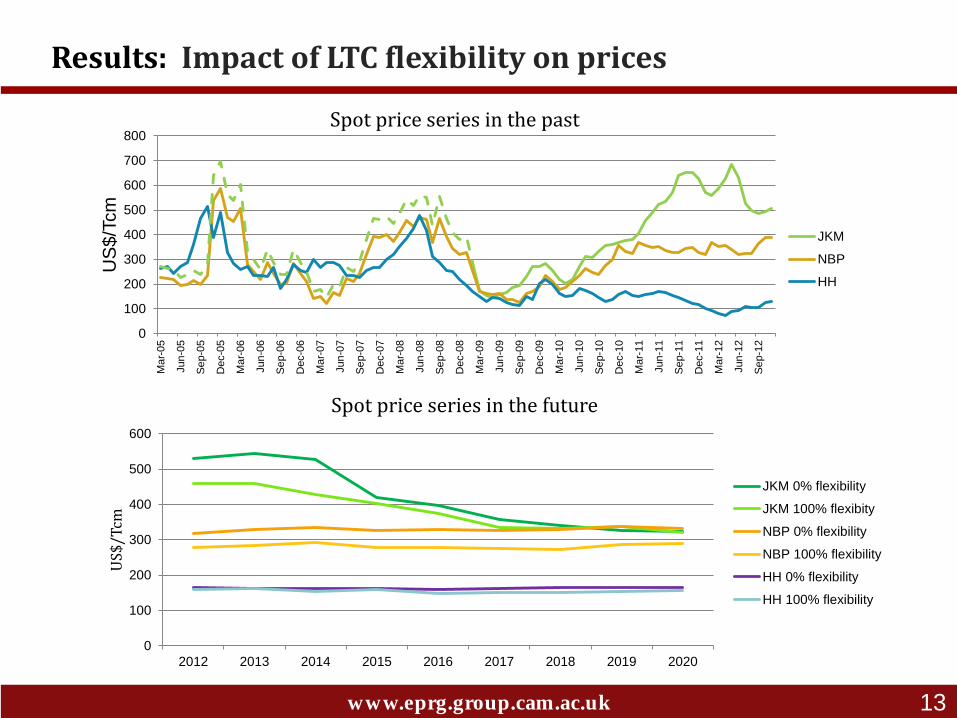

Results: Impact of LTC flexibility on prices

0

100

200

300

400

500

600

700

800

Ma

r-05

Jun

-05

Se

p-0

5

Dec-0

5

Ma

r-06

Jun

-06

Se

p-0

6

Dec-0

6

Ma

r-07

Jun

-07

Se

p-0

7

Dec-0

7

Ma

r-08

Jun

-08

Se

p-0

8

Dec-0

8

Ma

r-09

Jun

-09

Se

p-0

9

Dec-0

9

Ma

r-10

Jun

-10

Se

p-1

0

Dec-1

0

Ma

r-11

Jun

-11

Se

p-1

1

Dec-1

1

Ma

r-12

Jun

-12

Se

p-1

2

US

$/T

cm

JKM

NBP

HH

Spot price series in the past

Spot price series in the future

0

100

200

300

400

500

600

2012 2013 2014 2015 2016 2017 2018 2019 2020

US

$/T

cm

JKM 0% flexibility

JKM 100% flexibity

NBP 0% flexibility

NBP 100% flexibility

HH 0% flexibility

HH 100% flexibility

13

www.eprg.group.cam.ac.uk

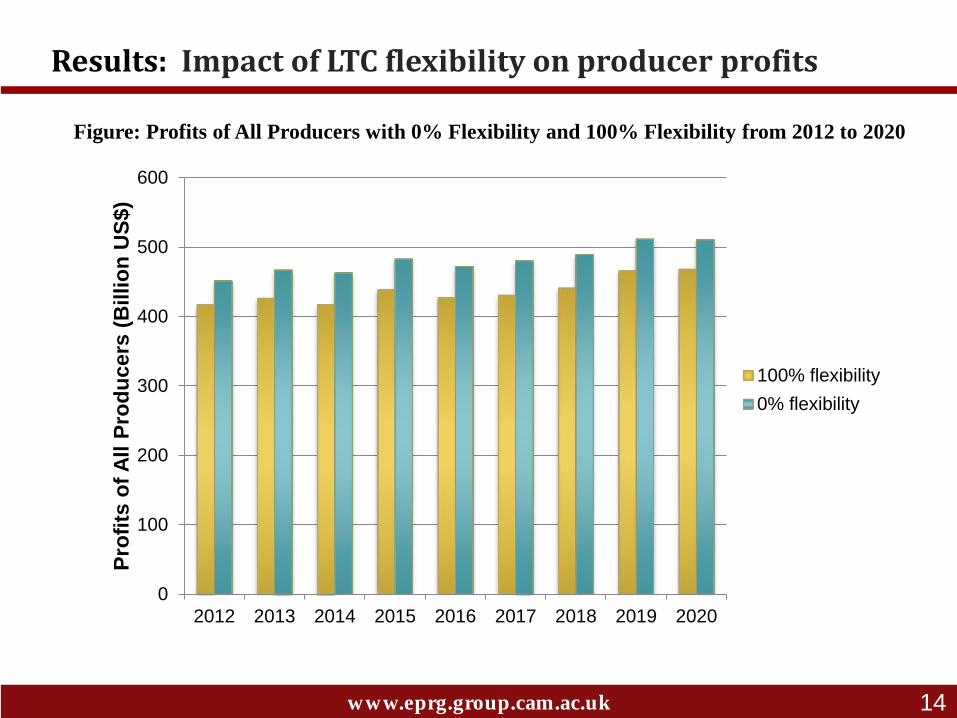

Figure: Profits of All Producers with 0% Flexibility and 100% Flexibility from 2012 to 2020

Results: Impact of LTC flexibility on producer profits

0

100

200

300

400

500

600

2012 2013 2014 2015 2016 2017 2018 2019 2020

Pro

fits

of

All P

rod

ucers

(B

illio

n U

S$)

100% flexibility

0% flexibility

14

www.eprg.group.cam.ac.uk

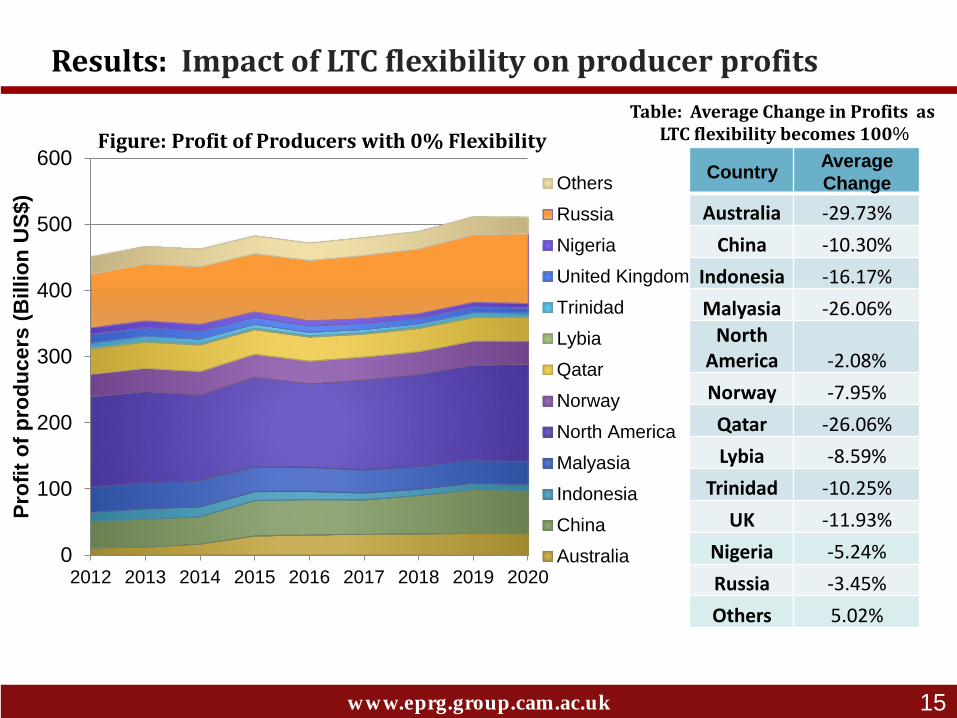

Country Average

Change

Australia -29.73%

China -10.30%

Indonesia -16.17%

Malyasia -26.06%

North America -2.08%

Norway -7.95%

Qatar -26.06%

Lybia -8.59%

Trinidad -10.25%

UK -11.93%

Nigeria -5.24%

Russia -3.45%

Others 5.02%

Figure: Profit of Producers with 0% Flexibility

Table: Average Change in Profits as LTC flexibility becomes 100%

Results: Impact of LTC flexibility on producer profits

0

100

200

300

400

500

600

2012 2013 2014 2015 2016 2017 2018 2019 2020

Pro

fit

of

pro

du

cers

(B

illio

n U

S$)

Others

Russia

Nigeria

United Kingdom

Trinidad

Lybia

Qatar

Norway

North America

Malyasia

Indonesia

China

Australia

15

www.eprg.group.cam.ac.uk

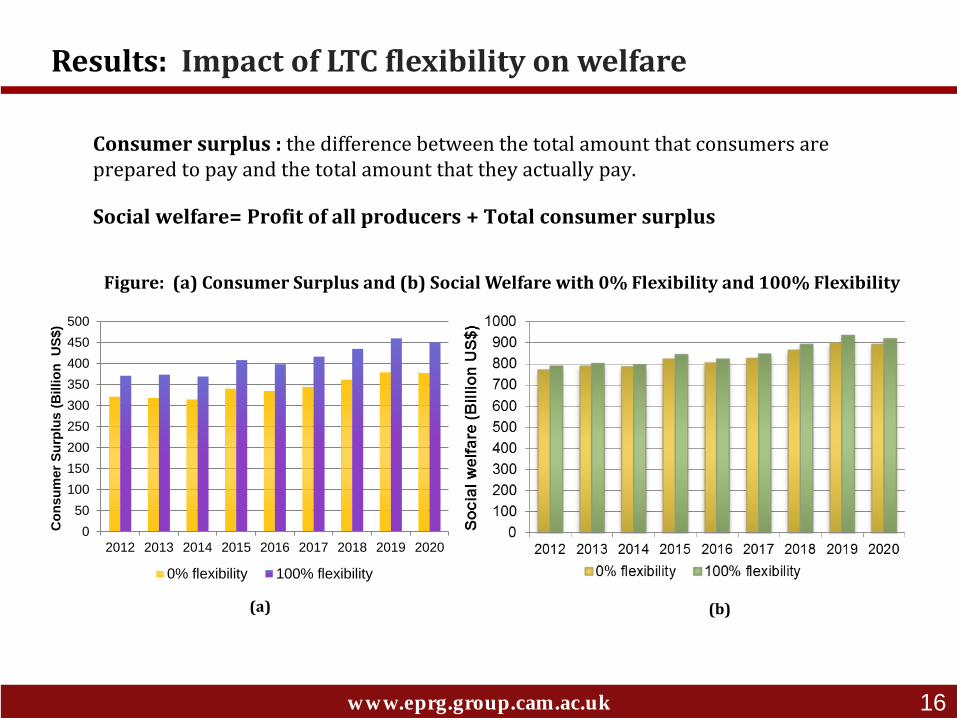

Consumer surplus : the difference between the total amount that consumers are prepared to pay and the total amount that they actually pay.

Figure: (a) Consumer Surplus and (b) Social Welfare with 0% Flexibility and 100% Flexibility

(a) (b)

Social welfare= Profit of all producers + Total consumer surplus

Results: Impact of LTC flexibility on welfare

16

0

50

100

150

200

250

300

350

400

450

500

2012 2013 2014 2015 2016 2017 2018 2019 2020

Co

nsu

mer

Su

rplu

s (

Billio

n U

S$)

0% flexibility 100% flexibility

www.eprg.group.cam.ac.uk

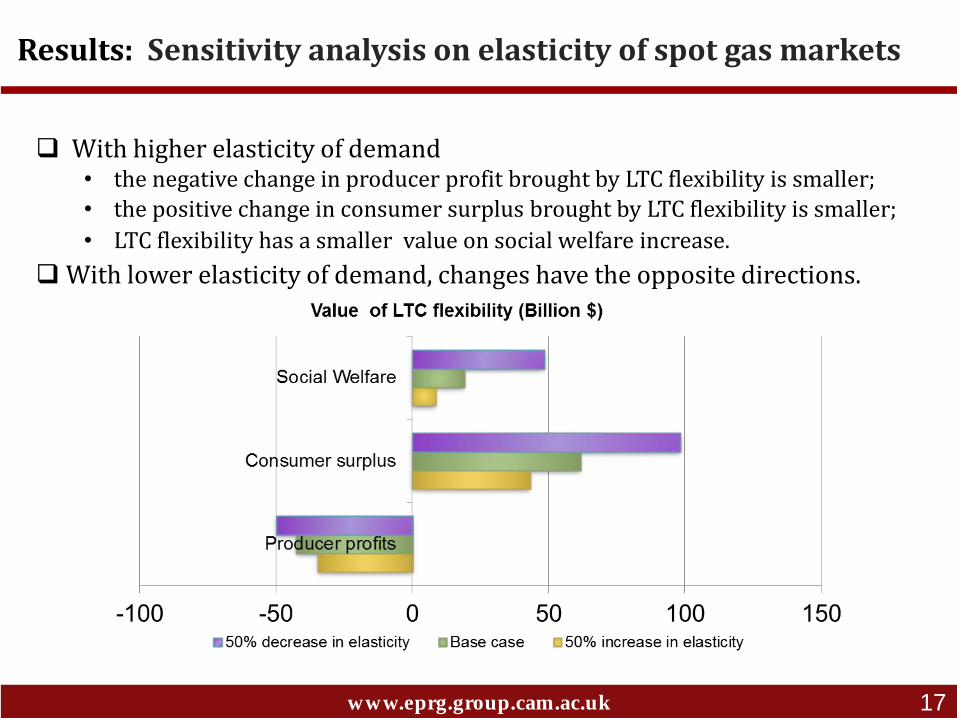

With higher elasticity of demand • the negative change in producer profit brought by LTC flexibility is smaller;

• the positive change in consumer surplus brought by LTC flexibility is smaller;

• LTC flexibility has a smaller value on social welfare increase.

With lower elasticity of demand, changes have the opposite directions.

Results: Sensitivity analysis on elasticity of spot gas markets

17

www.eprg.group.cam.ac.uk

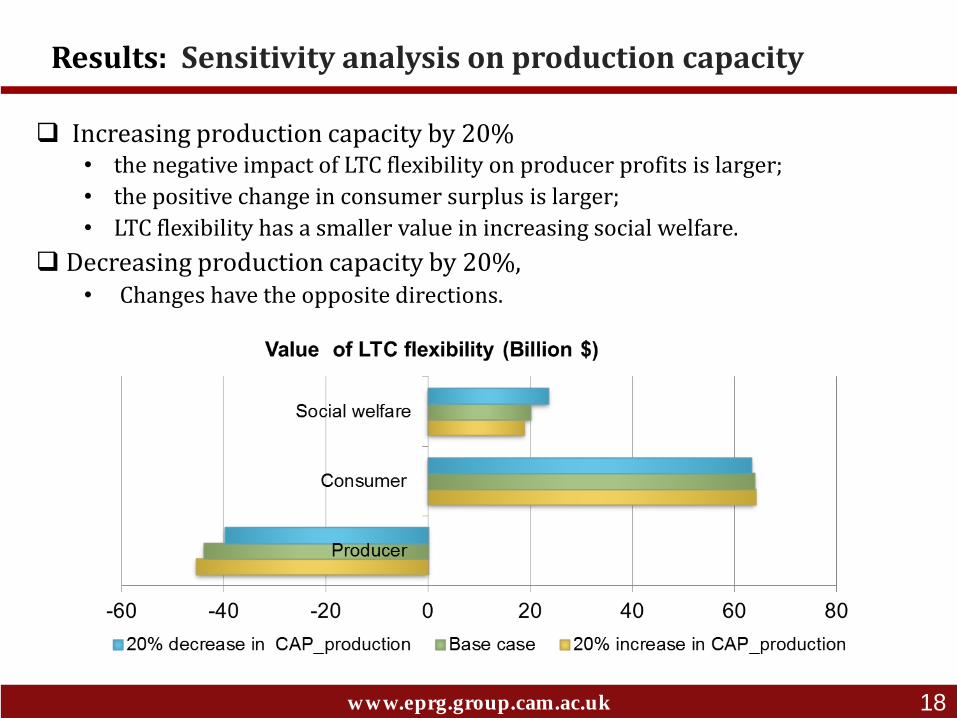

Increasing production capacity by 20% • the negative impact of LTC flexibility on producer profits is larger;

• the positive change in consumer surplus is larger;

• LTC flexibility has a smaller value in increasing social welfare.

Decreasing production capacity by 20%, • Changes have the opposite directions.

Results: Sensitivity analysis on production capacity

18

www.eprg.group.cam.ac.uk

With more flexible LNG contracts,

◦ will producers gain more profits? No

◦ will consumers surplus increase? Yes

◦ will the whole market efficiency increase? Yes

Open questions and future work:

◦ The liquefaction and regasification capacities are considered but not the LNG shipping capacities.

◦ More detailed modelling in the North America market.

Conclusion

19