the effects of oil revenue on the nigerian macro-economy

TRANSCRIPT

ID: 05209555

1

The Effects of Oil Revenue on the

Nigerian Macro-economy:

The Nigerian Curse!

By Chris Ibekwe

ID: 05209555

Adviser: Dr. W. David McCausland

JEL Classification – E00, E24, E41, E52, E62, F31, F41 "This dissertation is submitted in part requirement for the Degree of M.A. with

Honours in Economics at the University of Aberdeen, Scotland, and is solely the

work of the above named candidate".

Submitted: 11 February 2009

Word Count: 9,917

ID: 05209555

2

Table of Contents

Abstract 3

Acknowledgement 4

Introduction 5

Economic Background and Oil History 7

Third Structural Adjustment Programme 12

Macroeconomic Oil Contributions 14

Circular Flow 17

Mundel-Fleming Model 18

LM Curve

Money Demand 18

Money Supply 20

Money Market Equilibrium 21

Open IS Curve

Consumption 22

Investment 23

Government Spending 24

Exports and Imports 24

FE Curve 26

Fiscal Policy – Nigerian Case 29

Monetary Policy - Nigerian Case 33

Marshall Lerner Condition 37

J Curve 39

Unemployment and the Phillips Curve 41

Waste and Dutch Disease 44

Conclusion 46

Bibliography 48

ID: 05209555

3

Abstract

The single biggest challenge for an oil-producing country is the management and

use of its oil wealth and the organisation of its policies, to strategically promote and sustain

macro and socio-economic development. Macroeconomic policy formulation involves the

collection, analysis, arrangement and interpretation of various economic data and factors.

After nearly 50 years since oil was first discovered in Nigeria, the government is still

confronted with significant uncertainties with the management of its oil revenues and its

monetary and fiscal policies. The unpredictable nature of oil revenues stemming from

issues such as future oil prices, cartels and size of oil reserves has long been a major

problem for Nigerian policy makers. This paper seeks to analyze and suggest solutions for

an active management of various macroeconomic policies through the use of the Mundell-

Fleming model. It also seeks to understand why various macroeconomic policies and

theories applied by the Nigerian government fail so miserably. In doing this, the paper finds

that the Nigerian economy is riddled with bad management, lack of foresight and

corruption, all of which severely restrict the growth and development of the Nigerian

economy.

An argument often raised by many researchers with regards to the Nigerian economy has

been the issue of rent-seeking, waste and Dutch disease, all of which will be examined in

other to understand whether such an argument carries any weight in Nigerian context.

Key words – Nigeria, macroeconomic policies, governments, oil, Africa, oil producing

ID: 05209555

4

Acknowledgements

Firstly, I would like to thank God for the giving me the opportunity to undertake

and write this dissertation. Special thanks must also go to my dearest mother, sisters and

brothers for their unconditional support and encouragement to pursue my chosen degree. A

very special thanks and appreciation also goes to my very special girlfriend Abeola

Gilfillian, for listening to my constant complaints, frustration and for believing in me whole

heartedly and to her parents for proof reading my work and making suggestions.

Finally and importantly, I wish to express my sincere gratitude and thanks to my

supervisor Dr. W David McCausland for his attention, time, guidance and the critical and

challenging advice given to me in writing this dissertation.

ID: 05209555

5

Introduction

From a primary-producer country depending for her foreign exchange earnings on a

few primary commodities, to an oil producing country depending almost exclusively on

revenues generated from oil exports. Since the world energy crisis of the 1970s many of the

oil developing countries have set up and managed a relatively stable economy while raising

the standard of living in the country to well above the poverty line of $1 a day. The huge oil

price fluctuations of 1973 – 74 and 1979 resulted in a large transfer of wealth to Nigeria,

which caused a huge increase in the level of gross public expenditure and increased the

country‟s access to foreign markets. Yet, although the oil revenues of the 1970s provided

the Nigerian government with adequate funds to provide basic infrastructure needs and

investment for her people while paving the way for an industrial take off and development

of other sectors, Nigeria still finds herself coupled in severe poverty and restricted by huge

national debts.

Ordinarily, the objective of a macroeconomic policy is to improve the welfare of the

people, either in the short-run or the long-run. Macroeconomic policies are normally

formulated to solve identified and analyzed problems that prevent the economy from

reaching its goal; however several factors like Dutch disease (relationship between

exploitation of natural resources and decline in manufacturing sector) corruption and

mismanagement constrict the effectiveness of such policies. Following the collapse of oil

prices in 1982 and the rise in real interest rate and inflation, coupled with gross economic

mismanagement, lack of foresight, neglect and corruption on the side of government, the

global economic downturn became a Nigerian national economic crisis in 1983 as GDP

fell, interest rates rose to 12.5% and inflation rose also to 16% .

The socioeconomic dimensions of the oil price collapse and the general inability of the

government to control the economy in the 1980s, brought poverty alleviation to the fore

front of Nigeria‟s policies. The rate of unemployment was very high, purchasing power was

low, economic growth was negative; poverty became entrenched in the average Nigerian‟s

standard of living. In essence there were severe macroeconomic imbalances both

domestically and internationally and it became apparent that the economy required major

adjustment.

ID: 05209555

6

Further failures from the government to recognize the reality of a crisis

meant that nothing was done to control the falling economy until 1986 when the SAP –

Structural Adjustment Programme was introduced by the then President Ibrahim

Babangida. The aim of the programme was to release the country‟s overvalued currency so

that it could find its natural place in the international market, hence eliminating smuggling,

black marketing and trafficking whilst encouraging the inflow of foreign investments and

increased export earnings from the non-oil sector.

Despite several fiscal measures introduced since 1986 such as the increase in government

expenditure and the active management of other macroeconomic policies, economic growth

did not accelerate as expected and poverty still remained widespread particularly in the

rural areas where the living standards are below the poverty line of $1 a day. The

implications of such boom-bust fiscal policies include the transmission of oil-volatility to

the rest of the economy as well as disruptions to the stable provision of basic government

services. Since fiscal and monetary policy is widely recognized as a major macroeconomic

tools available to governments as means of redistributing income and reducing poverty, one

must then ask and wonder what role has such policies played in the Nigerian case? And

could fiscal and monetary policy actually alleviate poverty in Nigerian while achieving

economic stability and growth?

ID: 05209555

7

Economic Background and Oil History

Nigeria is the largest geographical unit in West Africa, with a land area of 923,768

square kilometres and an estimated population of 147million1 of which 47% are below 15

years of age and another 3% aged 65 years and above2. Before gaining political

independence in October 1960, Agriculture was the dominant productive sector of the

economy and contributed to about 70% of the economy‟s Gross Domestic Product (GDP)

while accounting for about 90% of foreign earnings through the export of cocoa, palm oil

and nuts. Petroleum exploration in Nigeria first began in 1908 by the German Nigerian

Bitumen Corporation and the British Colonial Petroleum Company who drilled in heavy oil

seeps which occurs in the cretaceous Abeokuta formation just outside the old capital city

Lagos. This venture was abandoned briefly for the First and Second World Wars until in

1956 when the Shell-BP Development Company of Nigeria restarted exploration for oil in

the Niger Delta with successful results.

The discovery of oil in commercial quantities massively changed the Nigerian

economy from an agricultural dependant one, to one dependent severely on oil. It is now

thought that Nigeria has proven oil reserves of about 32 million barrels of predominantly

low-sulphur light crude which at the rate of exploitation could last another 38 years. The

massive increase in oil revenue in the after-math of the Middle-East war of 1973 created

unprecedented, unexpected and unplanned wealth for Nigeria, which then signalled the

dramatic shift from policies aimed at developing the agricultural sector to policies

benchmarked on unrealistic expectations for revenues from the new oil state. At present,

Nigeria has four refineries with a combined installed refining capacity of 445,000 barrels

per day; however, these are operating at far below their maximum capacity levels as they

have more or less been abandoned during the military era. This means that the issue of

routine and mandatory maintenance were easily skipped therefore making production less

likely and oil importation inevitable.

1 World Development Indicators database, World Bank Database- Accessed 20

th November 2008

2 World Bank database - Accessed 20

th November 2008

ID: 05209555

8

The foreign exchange management system adopted by the Nigerian government

from 1960 to 1985 went from extremes of fixed exchange rates to flexible rates with a view

of preserving the value of the domestic currency, the naira, maintaining favourable reserve

and ensuring price stability. However, more importantly, the post independence era

witnessed a regime of a fixed exchange rate used side by side with the British pound until

the British pound was devalued in 1967. From 1967 to 1974, the Naira was fixed to the US.

Dollar using an import weighted basket of currencies of Nigeria‟s seven main trading

countries i.e. United States dollar, British pound, German mark, French franc, Japanese

yen, Dutch guilder and Swiss franc.

Subsequently all the various attempt at exchange rate management policies could

not lead to the stated aim of preserving the value of the Nigerian naira while ensuring stable

price levels. Consequently a flexible exchange rate policy was adopted in 1986 following

the introduction of the Structural Adjustment Programme (SAP) by the then President,

General Ibrahim Babangida.

ID: 05209555

9

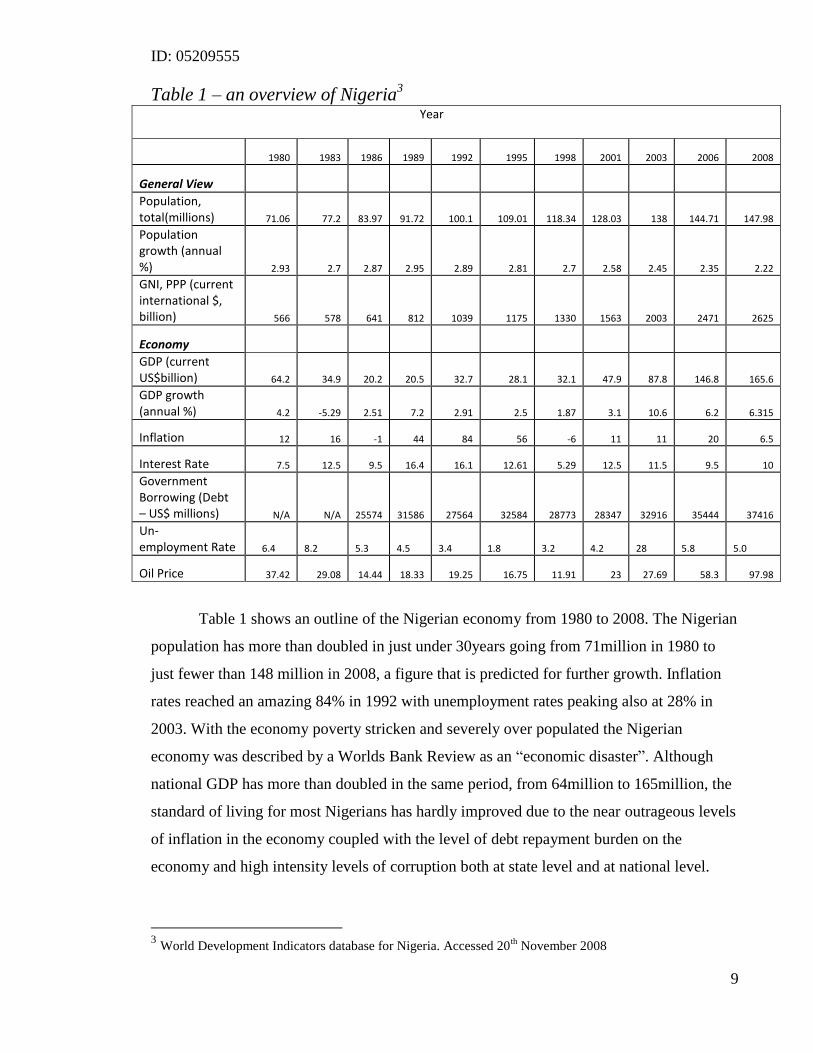

Table 1 – an overview of Nigeria3

Year

1980 1983 1986 1989 1992 1995 1998 2001 2003 2006 2008

General View

Population, total(millions) 71.06 77.2 83.97 91.72 100.1 109.01 118.34 128.03 138 144.71 147.98

Population growth (annual %) 2.93 2.7 2.87 2.95 2.89 2.81 2.7 2.58 2.45 2.35 2.22

GNI, PPP (current international $, billion) 566 578 641 812 1039 1175 1330 1563 2003 2471 2625

Economy

GDP (current US$billion) 64.2 34.9 20.2 20.5 32.7 28.1 32.1 47.9 87.8 146.8 165.6

GDP growth (annual %) 4.2 -5.29 2.51 7.2 2.91 2.5 1.87 3.1 10.6 6.2 6.315

Inflation 12 16 -1 44 84 56 -6 11 11 20 6.5

Interest Rate 7.5 12.5 9.5 16.4 16.1 12.61 5.29 12.5 11.5 9.5 10

Government Borrowing (Debt – US$ millions) N/A N/A 25574 31586 27564 32584 28773 28347 32916 35444 37416

Un- employment Rate 6.4 8.2 5.3 4.5 3.4 1.8 3.2 4.2 28 5.8 5.0

Oil Price 37.42 29.08 14.44 18.33 19.25 16.75 11.91 23 27.69 58.3 97.98

Table 1 shows an outline of the Nigerian economy from 1980 to 2008. The Nigerian

population has more than doubled in just under 30years going from 71million in 1980 to

just fewer than 148 million in 2008, a figure that is predicted for further growth. Inflation

rates reached an amazing 84% in 1992 with unemployment rates peaking also at 28% in

2003. With the economy poverty stricken and severely over populated the Nigerian

economy was described by a Worlds Bank Review as an “economic disaster”. Although

national GDP has more than doubled in the same period, from 64million to 165million, the

standard of living for most Nigerians has hardly improved due to the near outrageous levels

of inflation in the economy coupled with the level of debt repayment burden on the

economy and high intensity levels of corruption both at state level and at national level.

3 World Development Indicators database for Nigeria. Accessed 20

th November 2008

ID: 05209555

10

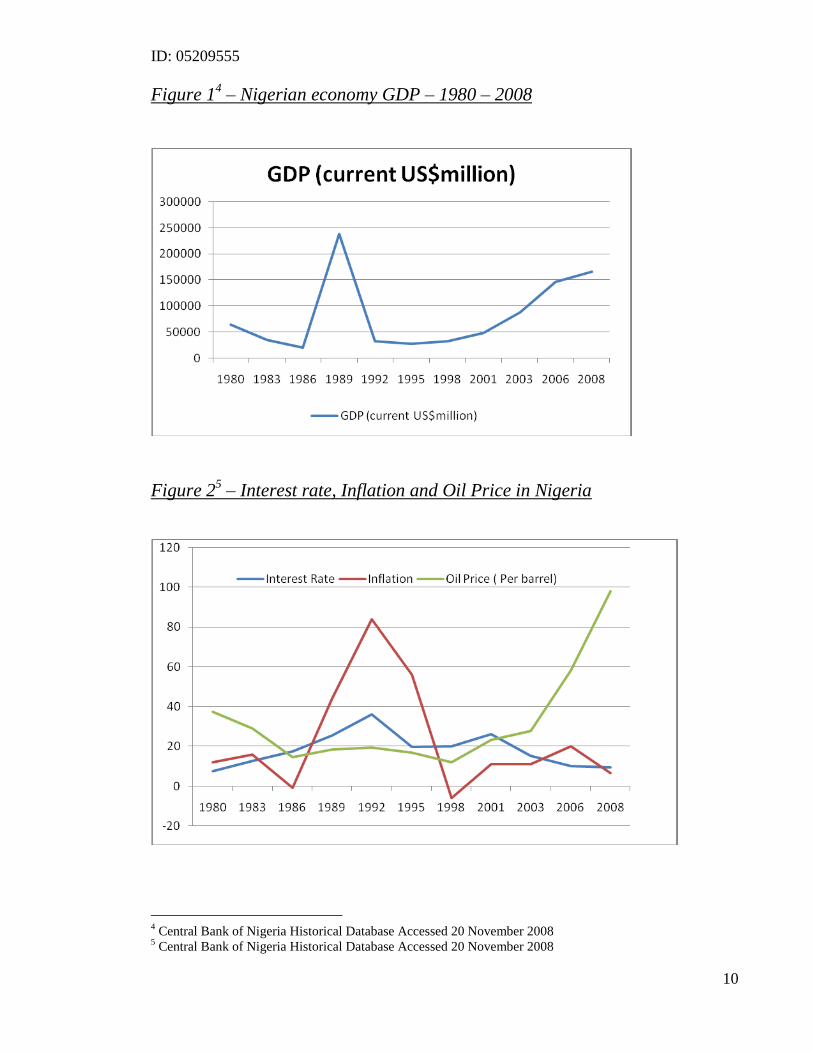

Figure 14 – Nigerian economy GDP – 1980 – 2008

Figure 25 – Interest rate, Inflation and Oil Price in Nigeria

4 Central Bank of Nigeria Historical Database Accessed 20 November 2008

5 Central Bank of Nigeria Historical Database Accessed 20 November 2008

ID: 05209555

11

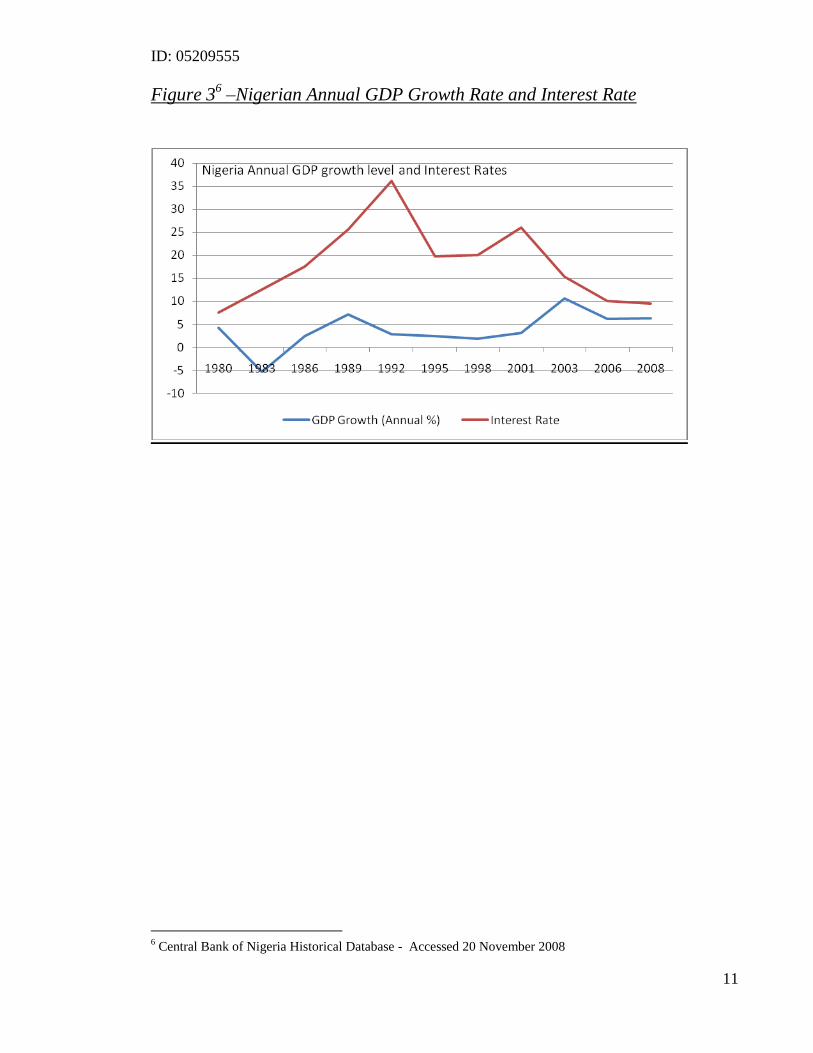

Figure 36 –Nigerian Annual GDP Growth Rate and Interest Rate

6 Central Bank of Nigeria Historical Database - Accessed 20 November 2008

ID: 05209555

12

Third Structural Adjustment Programme

Having unsuccessfully attempted to restructure the economy through the first and

second structural adjustment programmes, the Nigerian government embarked on a third

development plan. This is by far their most ambitious and it envisages a capital expenditure

of ₦30 billion with a growth rate in real terms of over 9%.7 The aim was that by the end of

the plan period, every Nigerian should experience a definite improvement in their overall

welfare. Emphasis was placed on restructuring those sectors which directly affect the

welfare of ordinary citizen such as housing, health and water.

According to the Third Plan statement, the primary objective was to achieve a rapid

increase in the standard of living of the average Nigerian, improve the overall distribution

of income so as to further improve the welfare of the citizens. The programme also had a

significant plan to diversify the economy away from its great dependence on petroleum

revenue and thus foster a growing development of other primary sectors. The Third Plan

attempted to achieve this through the use of fiscal, monetary and income policies in other to

ensure the development, stability, growth and social equity in Nigeria. Another aim of the

plan worth noting was its determination to relax import and export duties and controls in

other to aid the growth of agricultural sector which was previously Nigeria‟s main source of

revenue before the discovery of oil. It aimed to stimulate production and incomes of rural

farmers through the provision of subsidies for essential agricultural inputs such as fertilizer

and manure. Furthermore, the plan aims to increase agricultural production, through the

improvement of farmers‟ incomes and general standard of living in the rural areas through

the erection of over 100,000 housing units.

7 Oil and Development Planning – Arphad et al

ID: 05209555

13

From the above analysis of Nigeria‟s fiscal policy position, it is clear to see why the

Third National Development plan was already in difficulty before it had even been

implemented. Although the government attempted to stabilize the economy through the

Third Plan, it was still obvious that vast amounts of funds needed to carry out the plan still

relied heavily on revenues generated from oil. One of the main aims of the plan was to

control inflationary pressures in the economy, which in part is traceable to the monetization

of oil receipts and increased government spending and distribution of the oil wealth. It is

therefore clear that the optimistic picture portrayed of the Nigerian economy through the

release of the Development Plan was firmly based on the continued productivity of the oil

sector and revenue generation.

ID: 05209555

14

Macroeconomic Oil Contributions

Since oil discovery nearly over thirty years, the Nigerian oil industry has made a

variety of contributions to the aggregate economy. These have come in the form of the

creation of employment opportunities, multiplier effects gained from local expenditure on

goods and services, huge additions to government revenues, foreign exchange reserves,

gross domestic product and energy supply to industry and commerce.

Employment Opportunities

One important contribution by the oil sector in Nigeria was the creation of

employment. Previously, the economy was heavily dependent on agricultural based

employment but as the oil sector grew, it created a variety of employment such as road and

bridge building, material and equipments transportation, staff house building, clearing of

drilling sites and catering opportunities. Although direct oil industry employment was not

likely due to the very high capital intensive nature of the industry it still created the chance

for improving the living and earning standards of a working Nigerian.

Gross Domestic Product

An industry‟s contribution to the gross domestic product in any accounting period is

measured by its gross output less the cost of inputs-materials, equipments, services

purchased from other industries (where deduction of any taxes net of subsidies paid, gives

the GDP at market prices.) In the oil industry this consists of the proceeds from oil exports

and local sales but because of the very high level of involvement from foreign oil operators,

not all of the industry‟s value added is retained in the country. This is simply because a

substantial proportion of the revenue generated in Nigeria from oil is sent back in the form

of benefits, dividends, wages and salaries to the operator‟s home country.

ID: 05209555

15

Foreign Exchange Reserves

This is an important aspect of the oil industry's contribution to the Nigerian

economy, which came at a great moment as the country was embarking upon a massive

programme of industrialization and economic development. Such programmes require huge

imports of capital goods and specialized services involving massive expenditure of foreign

exchange earnings. In many developing countries, especially those such as Nigeria that

depend heavily on a narrow range of primary commodities, shortages in foreign exchange,

often worsened by massive declines in world commodity prices, constitute a major obstacle

to effective economic development8.

Local Expenditure on Goods and Services

The oil industry's periodic injection of purchasing power through its local

expenditure on goods and services is another important contribution to the Nigerian

economy. This takes the form of wage payments, salaries, licenses, charges, awards,

external social charges and local rents. Also apart from the direct stimulation given to the

producers of these goods and services in the form of subsidies and tax reliefs, the economy

also further benefits from secondary influences through the multiplier effect on the nations

aggregate economy9. This is however dependent on the magnitude, size and overall effect

of the initial injection and the extent of leakages out of the local economy.

Government Revenue

Revenues from oil account for a huge proportion of the Nigerian government

profits. The significant increase in government receipts in recent years has been a true

reflection of various factors attributed to the changing conditions of the oil industry such as

an increased production of crude oil in Nigeria, increase in world crude oil prices and a

more favourable fiscal arrangements obtained by the industry as a result of its improved

bargaining position over the years. Before the Nigerian oil boom, the government were in a

favourable bargaining position with the oil companies but however the above changes have

resulted in most significant increases in the government oil revenue receipts.

8 Crude oil and the Nigerian economy performance (2008)- Olusegun Odularu

9 Crude oil and the Nigerian economy Performance (2008)- Olusegun Odularu

ID: 05209555

16

Macro Energy Supply

Another contribution of the oil industry to the Nigerian economy was the provision

of a cheap and readily available source of energy for industry and commerce, through the

operations of the local refinery and the utilization of locally discovered natural gas. The

objective is to eliminate the appalling shortage of petroleum products in a country that is

currently swimming in oil. The availability of huge reserves of natural gas provides a good

opportunity for the supply of cheap energy to industry and commerce10

.

The above brief review shows that the oil industry has made a variety of

macroeconomic contributions to Nigeria, especially in the provision of government

revenues and foreign exchange. But, however, when a longer lasting view of the

macroeconomic impact of oil revenues on the Nigerian economy is taken, it becomes

apparent that, notwithstanding the massive increase in oil wealth, the industry has yet to

make a significant impact on economic development in Nigeria. As a recent World Bank

Economic Report (2007) on Nigeria commented, “At present, petroleum remains a typical

enclave industry whose contribution to the Nigerian economy is limited largely to its

contribution to government revenue and foreign exchange earnings”.

10

Crude oil and the Nigerian economy Performance (2008)- Olusegun Odularu

ID: 05209555

17

Circular Flow

The circular flow of income indicates the way income and money flows around an

economy. It has the relevance and ability to highlight the implications of fiscal and

monetary operations within a nation‟s macro economy. It also conveys how such policies

function for the purpose of stabilising and encouraging growth in the economy and as well

as depicting how the government actions affects the private sector of the domestic

economy and even the external sector. All spending in an economy must add up to the

same amount as incomes, with significant factors taken into account. These factors come in

the form of leakages and incorporate peoples saving, taxes by government and people

purchasing foreign goods, however, the economy receives injections to cover for leakages

through government expenditure in the form of fiscal policy, investments and exports.

Hence, macroeconomic policies are governed by the below equation;

Y = C + I + G + (X-M) (1)

Where Y = National Output, C= Aggregate Consumption, I = Investment, G= Government

Spending, X = Exports, M= Imports.

ID: 05209555

18

Mundell-Fleming Model__________________________________________

The Mundell-Fleming model is an economic model first discovered by Robert

Mundell and Marcus Fleming. It is a valuable tool for analyzing macroeconomic issues. It

comprises of the goods market (IS), the money market (LM) and the foreign exchange

market (FE). The model‟s simplicity has made it a very powerful tool for understanding the

roles of aggregate demand in an economy‟s business cycle. The model has often been used

to argue that an economy cannot maintain a fixed exchange rate, free capital movement and

independent monetary policies simultaneously. Applying the above model to the Nigerian

case would uncover the inaccuracies and mismanagement in the Nigerian aggregate

economy.

LM CURVE

Money Demand

In order to fully further understand the effectiveness of various macroeconomic

policies employed by the Nigerian government in running the economy, one must examine

and analyze the demand and supply of money which is measured by the LM Curve.

The LM curve identifies combinations of income and the interest rate for which the demand

for money equals money supply. The Nigerian government has tried to control the money

supply in the economy for some time in a bid to curb inflation and reduce currency

smuggling and black marketeering. This is especially important because the demand for

money is basically a demand for the services of money.

The money demand function combines the opportunity cost of holding lots of money in the

form of interest foregone and the benefits of carrying money i.e. avoiding withdrawal cost

and time losses.

L = kY – hi (2) Money Demand Function

Where, L - Denotes the demand for money of the liquidity

k – Measures the sensitivity of money to income (Income sensitivity of Money demand)

Y – Income

i – Nominal interest rate

-hi – speculative demand

ID: 05209555

19

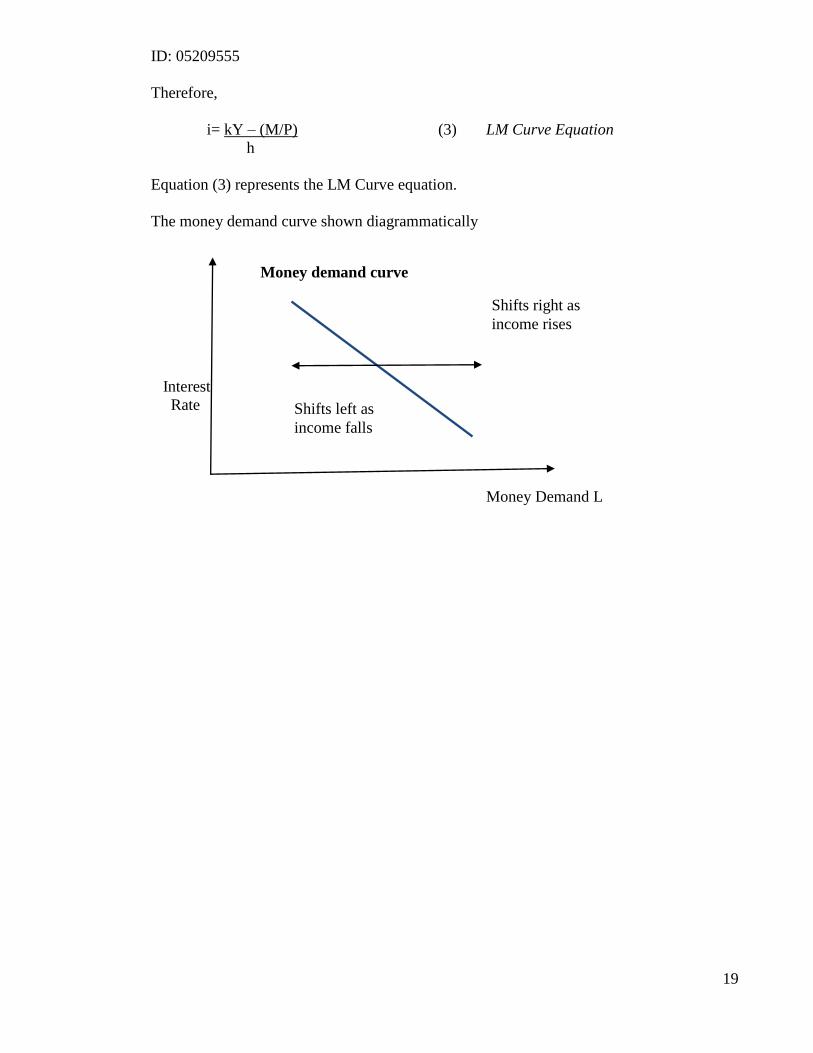

Therefore,

i= kY – (M/P) (3) LM Curve Equation

h

Equation (3) represents the LM Curve equation.

The money demand curve shown diagrammatically

Interest

Rate

Money Demand L

Shifts left as

income falls

Shifts right as

income rises

Money demand curve

ID: 05209555

20

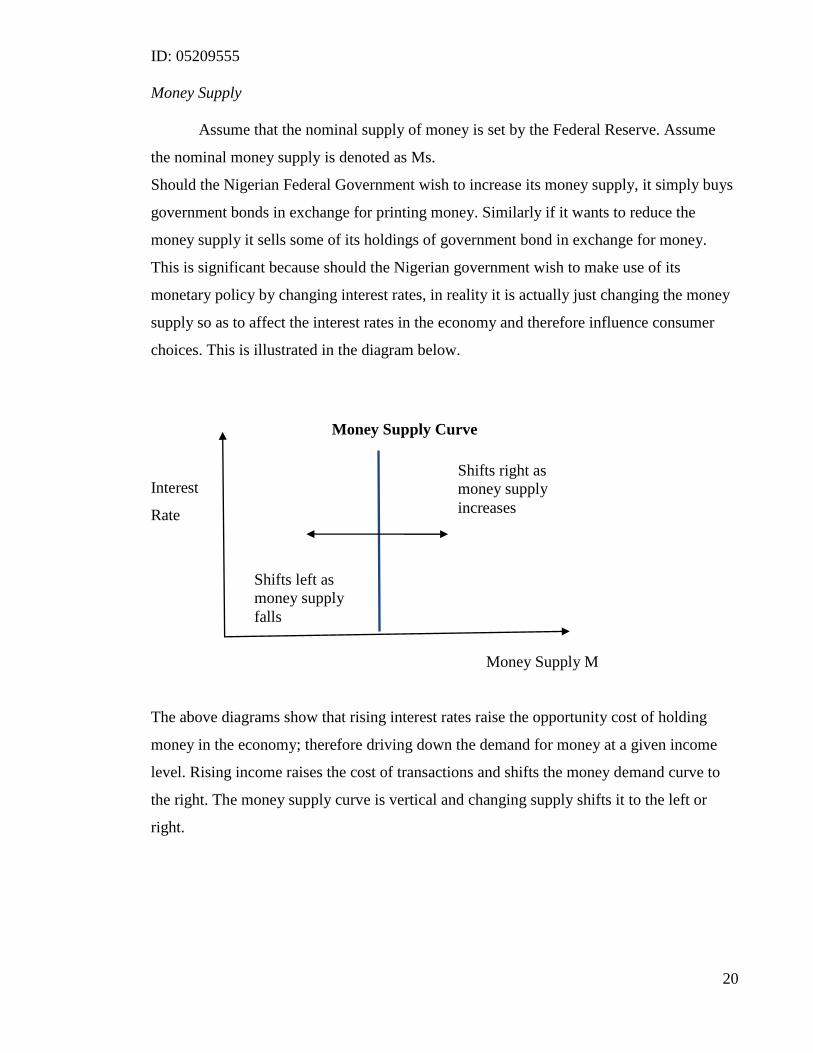

Money Supply

Assume that the nominal supply of money is set by the Federal Reserve. Assume

the nominal money supply is denoted as Ms.

Should the Nigerian Federal Government wish to increase its money supply, it simply buys

government bonds in exchange for printing money. Similarly if it wants to reduce the

money supply it sells some of its holdings of government bond in exchange for money.

This is significant because should the Nigerian government wish to make use of its

monetary policy by changing interest rates, in reality it is actually just changing the money

supply so as to affect the interest rates in the economy and therefore influence consumer

choices. This is illustrated in the diagram below.

Interest

Rate

Money Supply M

The above diagrams show that rising interest rates raise the opportunity cost of holding

money in the economy; therefore driving down the demand for money at a given income

level. Rising income raises the cost of transactions and shifts the money demand curve to

the right. The money supply curve is vertical and changing supply shifts it to the left or

right.

Money Supply Curve

Shifts left as

money supply

falls

Shifts right as

money supply

increases

ID: 05209555

21

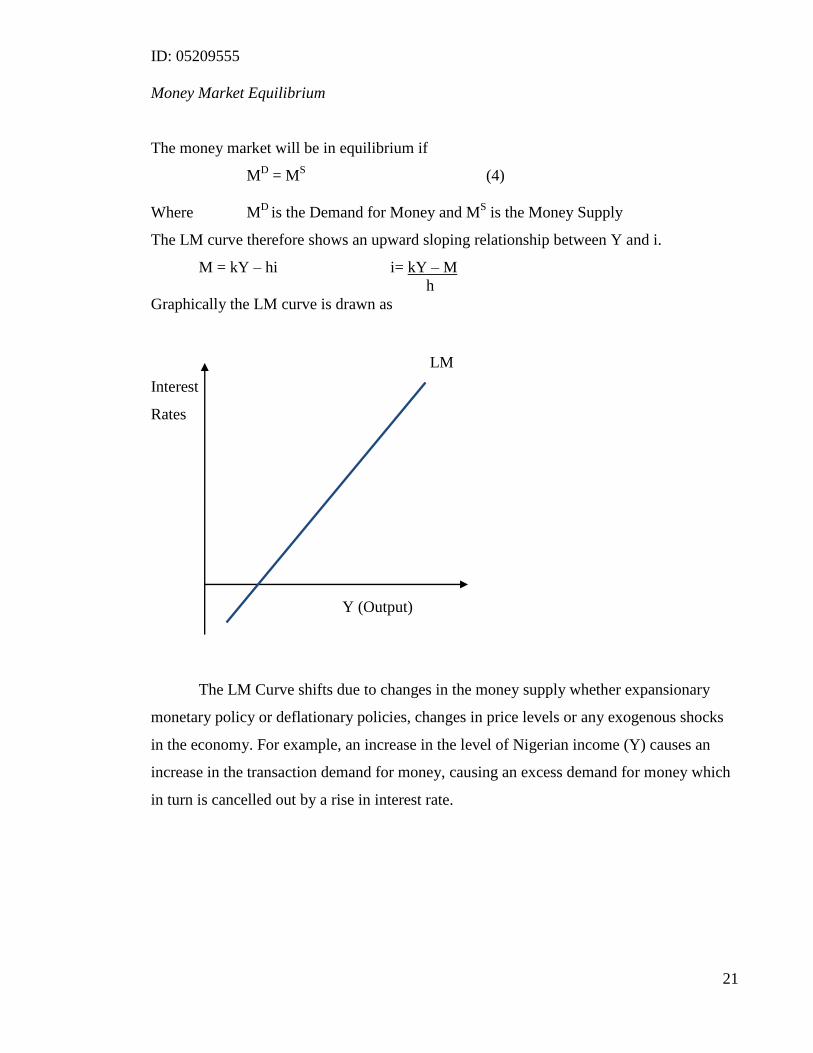

Money Market Equilibrium

The money market will be in equilibrium if

MD = M

S (4)

Where MD

is the Demand for Money and MS is the Money Supply

The LM curve therefore shows an upward sloping relationship between Y and i.

M = kY – hi i= kY – M

h

Graphically the LM curve is drawn as

Interest

Rates

Y (Output)

The LM Curve shifts due to changes in the money supply whether expansionary

monetary policy or deflationary policies, changes in price levels or any exogenous shocks

in the economy. For example, an increase in the level of Nigerian income (Y) causes an

increase in the transaction demand for money, causing an excess demand for money which

in turn is cancelled out by a rise in interest rate.

LM

ID: 05209555

22

Open Economy IS Curve

The IS curve describes the combination of Nigerian interest rates and output that

create equilibrium in the goods and services market in the short run. This is said to clear

when spending by consumers, firms, the government (and foreigners if an open economy)

on goods and services equals the production of goods and services. The basic equation for

the IS curve in an open economy is closely related to the national income accounting

identity;

Y= Aggregate Expenditure (5)

Y = C+I+G + NX (6)

Where Y is GDP, C Consumption, I Investment, G government spending and NX net

exports

Consumption

Consumption is assumed to dependent on three factors in an economy i.e.

consumer confidence, National GDP (Y) and taxes (T). Consumer spending in an economy

increases when confidence is high, this is because consumers are more certain about the

future and are not afraid of drastic events in the economy, which is not the case in the

Nigerian economy. Consumer spending in Nigeria is also affected by increases in the tax

rates, meaning that there is a fall in disposable income in the economy. This is important in

understanding what exactly has restricted the Nigerian economy and kept confidence at a

low.

A simple consumption function is derived as

C = cY (7)

Where c is the proportion of each extra unit of Naira of income that is consumed (marginal

propensity to consume)

ID: 05209555

23

Investment

Another component of the IS curve is investment. The level of investment in the

economy is positively related to the level of investor confidence. This is purely because

individuals or firms are unwilling to sink money into infrastructure building if they believe

that the government will be overthrown in a civil war at any moment. This is exactly the

case with Nigeria as it has undergone seven military and civil presidential coups since

gaining independence from Britain.

Investment has to be financed either through borrowing or savings which are both reliant on

the level of interest rates in the economy. An increase in the interest rate reduces

investment by making it more expensive for firms to borrow money and by increasing the

opportunity cost for those who use their own funds.

A simple investment function is derived as

I = Ī – bi (8)

Where Ī, is autonomous investment i.e. (Investment that would take place irrespective of

interest rates)

bi= interest sensitive investment

ID: 05209555

24

Government

In an economy, fiscal policy comprises all policy measures related to government

spending and budgets. At the aggregate level this is done by increasing or decreasing

government spending, borrowings and taxes. If the Nigerian government increases

spending in the economy, G, firms experience an excess increase in demand for their

products which they cannot meet. To counter this, firms raise production which in-turn

raises income. Therefore an increase in the government spending squeezes some investment

out of the economy by instigating the crowding out theory. This is when an increase in one

category of aggregate demand goes at the expense of a reduction in some other component

of aggregate demand. Hence, G rises at the expense of I investment.

Net Exports and Imports

In an open economy, the real exchange rate R is the ratio between the prices of a

bundle of goods abroad and at home. If the real exchange rate of the Naira falls below

purchasing power parity it is cheaper to buy imported goods.

Therefore the import function is

IM = m1Y – m2R (9)

The export function is a mirror image of the import function, since Nigerian exports are

simply the imports of the rest of the world from them. Thus the two determinants of

Nigerian exports would be world income and the real exchange rate.

Export function is therefore;

EX = x1Yw

+ x2R (10)

The exchange rate is said to affect exports with a positive coefficient hence, if the Naira

depreciates against other currencies, other currencies appreciates against the Naira. This

makes Nigerian exports cheaper for foreigners and they will want to buy more Nigerian

goods.

ID: 05209555

25

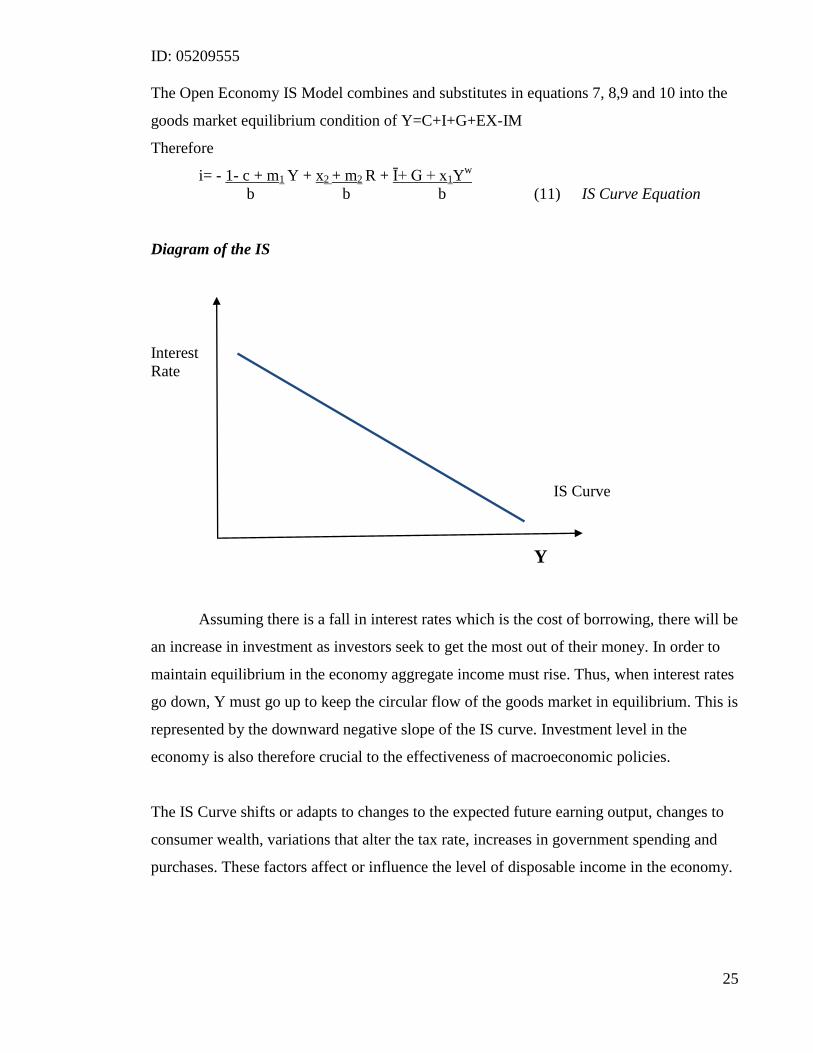

The Open Economy IS Model combines and substitutes in equations 7, 8,9 and 10 into the

goods market equilibrium condition of Y=C+I+G+EX-IM

Therefore

i= - 1- c + m1 Y + x2 + m2 R + Ī+ G + x1Yw

b b b (11) IS Curve Equation

Diagram of the IS

Interest

Rate

Y

Assuming there is a fall in interest rates which is the cost of borrowing, there will be

an increase in investment as investors seek to get the most out of their money. In order to

maintain equilibrium in the economy aggregate income must rise. Thus, when interest rates

go down, Y must go up to keep the circular flow of the goods market in equilibrium. This is

represented by the downward negative slope of the IS curve. Investment level in the

economy is also therefore crucial to the effectiveness of macroeconomic policies.

The IS Curve shifts or adapts to changes to the expected future earning output, changes to

consumer wealth, variations that alter the tax rate, increases in government spending and

purchases. These factors affect or influence the level of disposable income in the economy.

IS Curve

ID: 05209555

26

Nigerian Foreign Exchange Market and the FE Curve

The final side of a nation‟s aggregate economy is the foreign exchange market and

the balance of payments. A country‟s openness has many dimensions; the most frequently

used measure of an economy‟s openness, is the ratio of exports or imports to income. The

vital determinant of Nigeria‟s exports and imports is the Nigerian exchange rate as this

affects the relative price of goods both at home and abroad. Any transaction that requires

the purchase of a domestic currency is a credit item in that Nigeria‟s balance of payments

and any transaction that requires the sale of domestic currency is a debit item in the balance

of payments.11

Therefore, since a currency can only be purchased if someone is willing to

sell, the sum of all credit must equal the sum of all debits. Hence the demand for Nigerian

currency will always equals the supply which means that the conditions that equalize the

balance of payments also equalize the foreign exchange market.

Balance of Payments = Current Account + Capital Account + Official Reserves

Current Account = NX = EX – IM

=x1Yw

+ x2R - m1Y – m2R (12)

Capital Accounts and Uncovered Interest Parity

Suppose ₦1 this year invested at home => ₦1 (1+i)

₦1 this year invested abroad => ₦1 (1+ iw) (1+ E)

Where, iw is assumed to be the interest rate of Nigeria‟s main trading partner USA.

Therefore,

(1+i) = (1+ iw) (1+ E) (13)

If investors are risk-neutral, they are only indifferent between holding domestic and foreign

assets if the projected returns are equal – assuming no arbitrage.

If E=0, then the interest rate disparity between the two countries should lead to some

capital flows which in turn is dependent on the ease of capital mobility in Nigeria.

11

Macroeconomics. 3rd

Edition. (2003) Manfred Gartner Page 93

ID: 05209555

27

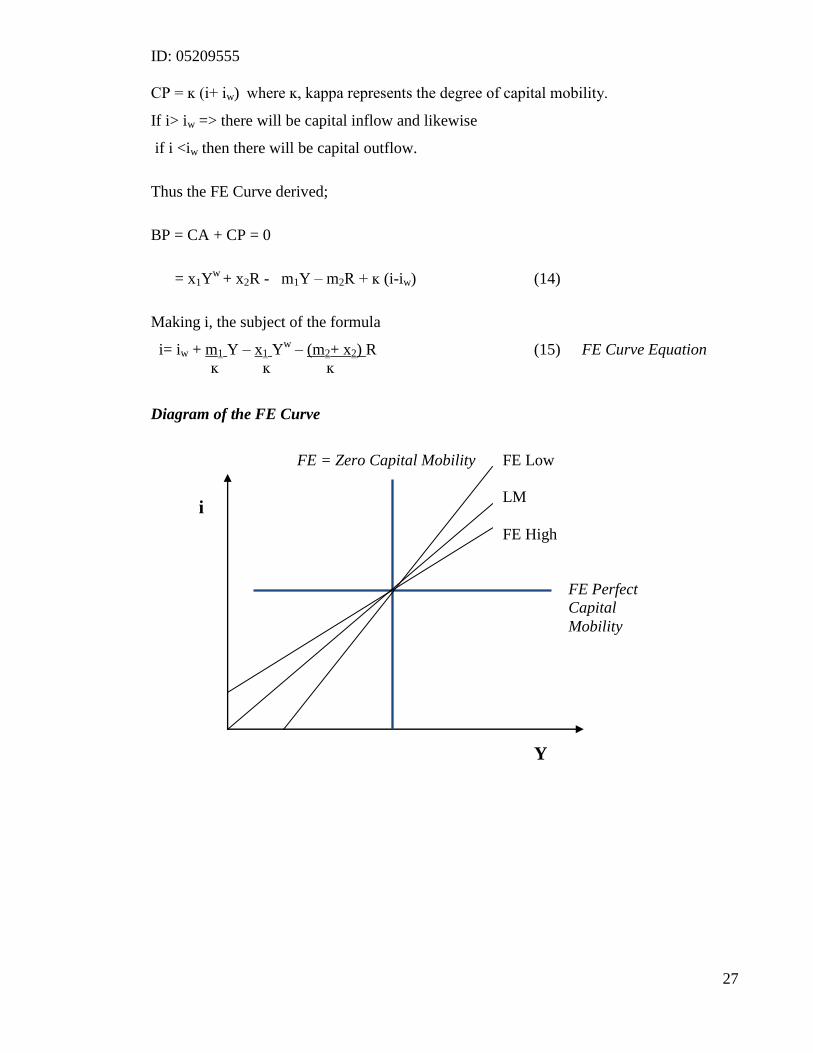

CP = ĸ (i+ iw) where ĸ, kappa represents the degree of capital mobility.

If i> iw => there will be capital inflow and likewise

if i <iw then there will be capital outflow.

Thus the FE Curve derived;

BP = CA + CP = 0

= x1Yw

+ x2R - m1Y – m2R + ĸ (i-iw) (14)

Making i, the subject of the formula

i= iw + m1 Y – x1 Yw – (m2+ x2) R (15) FE Curve Equation

ĸ ĸ ĸ

Diagram of the FE Curve

i

Y

FE Low

LM

FE High

FE Perfect

Capital

Mobility

FE = Zero Capital Mobility

ID: 05209555

28

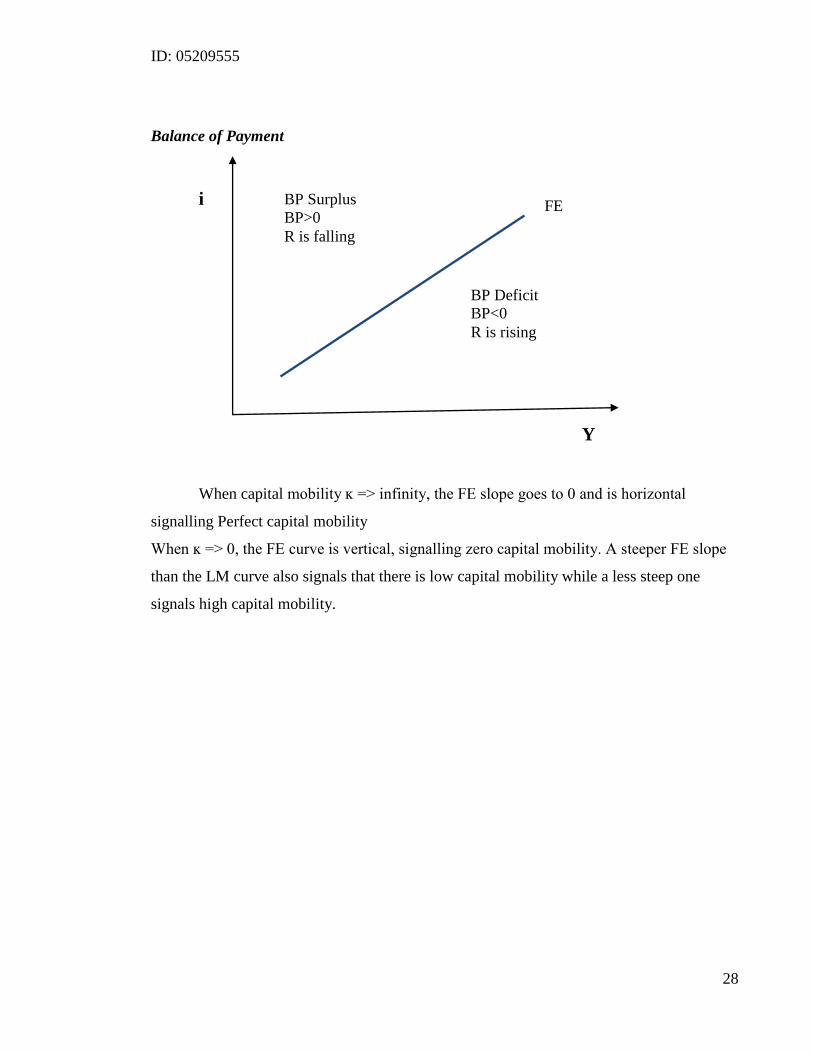

Balance of Payment

i

Y

When capital mobility ĸ => infinity, the FE slope goes to 0 and is horizontal

signalling Perfect capital mobility

When ĸ => 0, the FE curve is vertical, signalling zero capital mobility. A steeper FE slope

than the LM curve also signals that there is low capital mobility while a less steep one

signals high capital mobility.

BP Surplus

BP>0

R is falling

BP Deficit

BP<0

R is rising

FE

ID: 05209555

29

Fiscal Policy – Nigerian Case

The formulation and proper implementation of macroeconomic policies targeted for

economic growth, along with increased access to basic social services and infrastructure are

essential in any Nigerian strategy in distributing oil revenues. Fiscal policy serves as an

automatic economic stabilizer; it comprises all policy measures related to the government

budget including government spending, borrowing and raising revenue through taxes.

Nigeria faces two challenges when dealing with revenues from oil; in the long run it needs

to ensure that her fiscal stance is sustainable without the reliance on natural assets such as

oil. She also needs to ensure that in the short to medium term, her budget and planning is

not affected by volatilities in oil prices. Nigeria having learnt from past experience has

attempted to use oil revenue and fiscal policies to de link government expenditure from

volatile oil revenues. However, the current revenue sharing scheme whereby oil revenue is

divided between the state and federal governments has facilitated an expansion of

expenditure programs at the sub national level. This has further constrained the national

governments effort to control and stabilize government expenditure.

When compared to Indonesia, another developing country that has benefited from

the increasing global demand for oil products a 12

World Bank Economic Review paper on

Nigeria found that a significant bulk of government spending from oil revenues went to

transport, primary education and the construction of the steel production sector13

whereas

Indonesia pursued an expansive expenditure strategy that was relatively balanced between

physical infrastructure, education, maintaining the agricultural sector and its capital

intensive industry. This again provides telling evidence of mismanagement on the part of

the Nigerian government in handling oil revenues. At the microeconomic level, the

Nigerian agricultural sector which was previously the country‟s main sector has been

criticized for its deficiencies in several areas. These includes its failure to encourage private

price setting and marketing, failure to create a satisfactory credit system to finance and

support farming through government subsidy and its general failure to create infrastructure

and an economically viable environment to support the agricultural sector in machinery

12

The World Bank Economic Review, Vol.1, No.3: 419 – 445 – Nigeria During and After The Oil Boom: A

Policy Comparison with Indonesia – Brian Pinto 13

The World Bank Economic Review, Vol.1, No.3: 419 – 445 – Nigeria During and After The Oil Boom: A

Policy Comparison with Indonesia – Brian Pinto

ID: 05209555

30

maintenance, repairs and training. The most serious criticism of the government‟s policies

towards the development of the agricultural sector however is its decision to impose heavy

taxes on the sector and the retention of producer payments, while setting producers prices

that bear no relation with international prices.

In theory an effectively implemented fiscal rule could play a crucial role in overcoming

constraints on fiscal policy formulation by providing a working framework for a more

stable and controlled government budget which would go far to alleviate poverty and the

ever growing economic crisis. A fiscal rule was introduced however by President Obasanjo

with the intention of controlling and stabilizing the economy, but nevertheless this will not

change the impact of government activities on the economy unless serious measures are

taken to combat entrenched corruption and increase transparency and accountability of

fiscal operations both at state and national level.

With a proven oil reserve of about 32 million barrels and since oil is a national

asset, the Nigerian government can facilitate trade and allow the economy to run current

account deficits now and repay them through surpluses in the future. However in

developing countries such as Nigeria and Indonesia, the government has become in effect

the biggest borrower and investor. Therefore, since fiscal deficits feed into current account

deficit, which are in turn financed by either running down reserves or by government

borrowing, a clear link has now developed between Nigeria‟s fiscal policy and her

borrowing strategies. In the oil boom years the government accumulated surpluses and in

the recession it ran deficits. This strategy although reasonable was very dangerous purely

because in the event of a prolonged period of sustained economic sluggishness there would

be severe account imbalances as is the case with Nigeria.

ID: 05209555

31

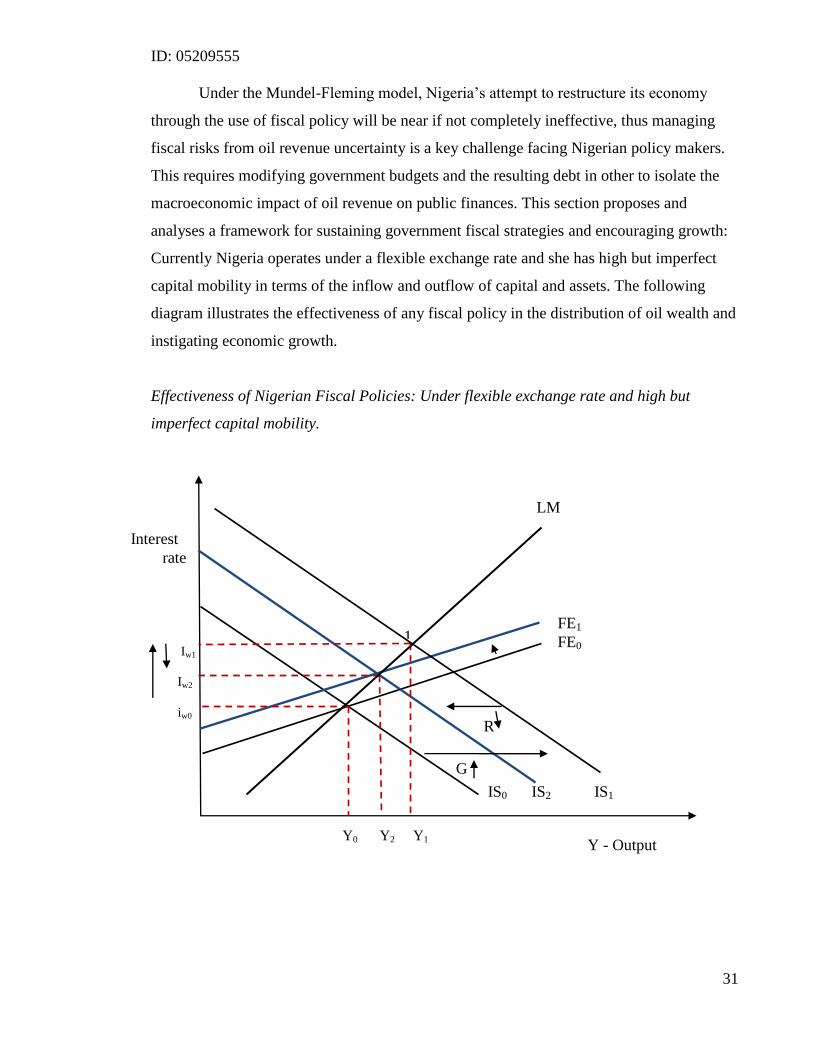

Under the Mundel-Fleming model, Nigeria‟s attempt to restructure its economy

through the use of fiscal policy will be near if not completely ineffective, thus managing

fiscal risks from oil revenue uncertainty is a key challenge facing Nigerian policy makers.

This requires modifying government budgets and the resulting debt in other to isolate the

macroeconomic impact of oil revenue on public finances. This section proposes and

analyses a framework for sustaining government fiscal strategies and encouraging growth:

Currently Nigeria operates under a flexible exchange rate and she has high but imperfect

capital mobility in terms of the inflow and outflow of capital and assets. The following

diagram illustrates the effectiveness of any fiscal policy in the distribution of oil wealth and

instigating economic growth.

Effectiveness of Nigerian Fiscal Policies: Under flexible exchange rate and high but

imperfect capital mobility.

Iw1

Iw2

iw0

Y0 Y2 Y1

FE1

FE0

LM

IS0 IS2 IS1

G

R

1

Y - Output

Interest

rate

ID: 05209555

32

A rise in the level of government spending shifts the IS goods curve to the right. At

point 1, i> iw, therefore there will be an inflow of capital into Nigeria as investors seek to

maximize the benefits from the higher interest rates. However as the capital account

increases, there is a balance of payment surplus, leading to a fall in R which is the exchange

rate level. In order to restore the balance of payment equilibrium, there will be a fall in R

which shifts the IS curve downward and the FE curve upwards resulting in a new

equilibrium at Y2I2.

The result is that fiscal policy has some effect on promoting economic growth and

redistributing income but still much of the effect has been offset by the Naira appreciating.

ID: 05209555

33

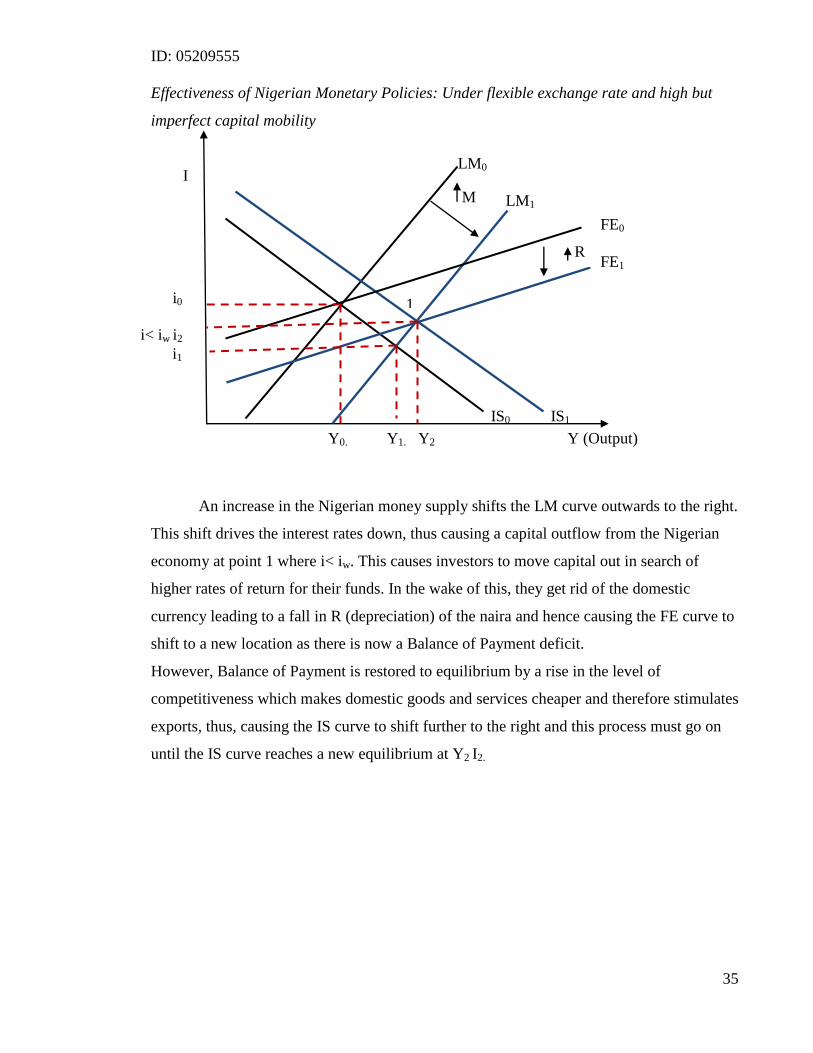

Monetary Policy – Nigerian Case

In their 1986 paper Arpad von Lazar et al stated that the Nigerian monetary policy

was directed at controlling inflationary pressures in the economy and stabilizing the

economy. The Nigerian banking system is also increasingly faced with the problem of

excess liquidity due to the increased level of government borrowing while at the same time

certain sectors of the economy have been faced with tighter credit conditions. 14

Monetary

Policy comprises central bank action geared towards steering the money supply. This can

happen directly through the government purchasing and selling of bonds and foreign

currency or indirectly through the setting of interest rates and inducing the market to hold

liquidity in the desired amount. There has been two major phases in Nigeria in the pursuit

of an effective monetary policy, namely, before and after 1986. The first emphasised on

direct controls and the latter on indirect reliance on market mechanisms.

The economic environment in Nigeria that guided monetary policy formulation

before 1986 was mainly characterized by the dominance of the oil sector, over dependence

on the external sector and the expanding role of the public sector and fiscal policies. The

Nigerian government then understood that in order to maintain price stability, a healthy

balance of payments position and the distribution of oil revenues around the country, it

needed an active management of the monetary system. However this was still heavily

dependent on the use of alternative monetary instruments such as credit ceilings, selective

credit controls, administered interest and exchange rates. This reliance was mainly because

the use of market-based instruments was not feasible at this point due to the severe

underdeveloped nature of the country‟s financial markets and deliberate restraint on the use

of interest rates by corrupt government.

14

Macro-economics. 3rd

Edition. (2003) Manfred Gartner (p115)

ID: 05209555

34

Biodun Adedipe in his article on the Impact of Oil on Nigeria‟s Economic Policy

Formulation (2004) believed that “The fixing of interest rates at relatively low levels pre

1986 was done primarily to promote investment and growth in the economy while

stemming inflationary pressures”15

. He also believed that because generally, monetary

aggregates, government fiscal deficit, GDP growth rate and inflation did not move in

desirable directions, it became harder for the Nigerian government to implement their

policies. Compliance by banks on interest rate issues was also less than satisfactory further

making macroeconomic policy implementation harder.

The low interest rate employed by the Nigerian government pre 1986 did not sufficiently

attract private sector savers and investors into the economy hence the government was left

to rely even further on oil revenue in other to promote or sustain growth and injections into

the economy. Also since government expenditures were not rationalised, the government

resorted further to borrowing from the Nigerian Central Bank to finance its huge deficits.

Post 1986 the Structural Adjustment Programme (SAP) was adopted following the

crash in the international oil market and the resulting deteriorating economic conditions in

the country. The policies were designed to achieve a fiscal balance and balance of

payments viability by altering and restructuring the Nigerian production and consumption.

These would be achieved by eliminating price distortions, reducing heavy dependence on

crude oil revenue and consumer goods imports, enhancing the non-oil export base and

achieving sustainable growth. Its other aims were to rationalize the role of the public sector

and accelerate the growth potentials of the private sector. In order to improve

macroeconomic stability and control the effects of oil revenue, efforts were directed to the

active management of excess liquidity. The rising level of fiscal deficit was identified as a

major source of instability and consequently the Nigerian government agreed not only to

reduce her deficit but also to synchronize fiscal and monetary policies.

15

The Impact of Oil on Nigeria‟s Economic Policy Formulation – Biodun Adedipe (2004)

ID: 05209555

35

Effectiveness of Nigerian Monetary Policies: Under flexible exchange rate and high but

imperfect capital mobility

I

An increase in the Nigerian money supply shifts the LM curve outwards to the right.

This shift drives the interest rates down, thus causing a capital outflow from the Nigerian

economy at point 1 where i< iw. This causes investors to move capital out in search of

higher rates of return for their funds. In the wake of this, they get rid of the domestic

currency leading to a fall in R (depreciation) of the naira and hence causing the FE curve to

shift to a new location as there is now a Balance of Payment deficit.

However, Balance of Payment is restored to equilibrium by a rise in the level of

competitiveness which makes domestic goods and services cheaper and therefore stimulates

exports, thus, causing the IS curve to shift further to the right and this process must go on

until the IS curve reaches a new equilibrium at Y2 I2.

FE0

FE1

IS0 IS1

LM0

LM1

Y0. Y1. Y2 Y (Output)

i0

i< iw i2

i1

R

M

1

ID: 05209555

36

Essentially, interest rate levels are affected by movements in the price levels, fiscal

policy stance, intermediation costs (cost of funds), level of risks and uncertainty. If inflation

is expected to increase, the nominal interest rates need to adjust to induce positive real

interest rates which will not render savers worse-off. Although some monetary policy

effects have been eroded by the imperfect mobility nature of capital, it is however by far

the most useful government Nigerian macroeconomic tool for stabilizing, stimulating,

encouraging and controlling growth in the economy.

Therefore, under flexible exchange rates, monetary policy sets the pace.

ID: 05209555

37

Marshall Lerner Condition

The real exchange rate is defined as the product of the nominal exchange rate and

the ratio of the price indices for two countries.

Suppose that Nigeria is the home country and US the foreign country

S denotes the nominal exchange rate for the US dollar – hence the amount of Naira that is

needed to purchase one dollar.

PN – Price level in Nigeria

PUS- Price level in USA

The real exchange rate is hence defined as

R = S PUS (16)

PN

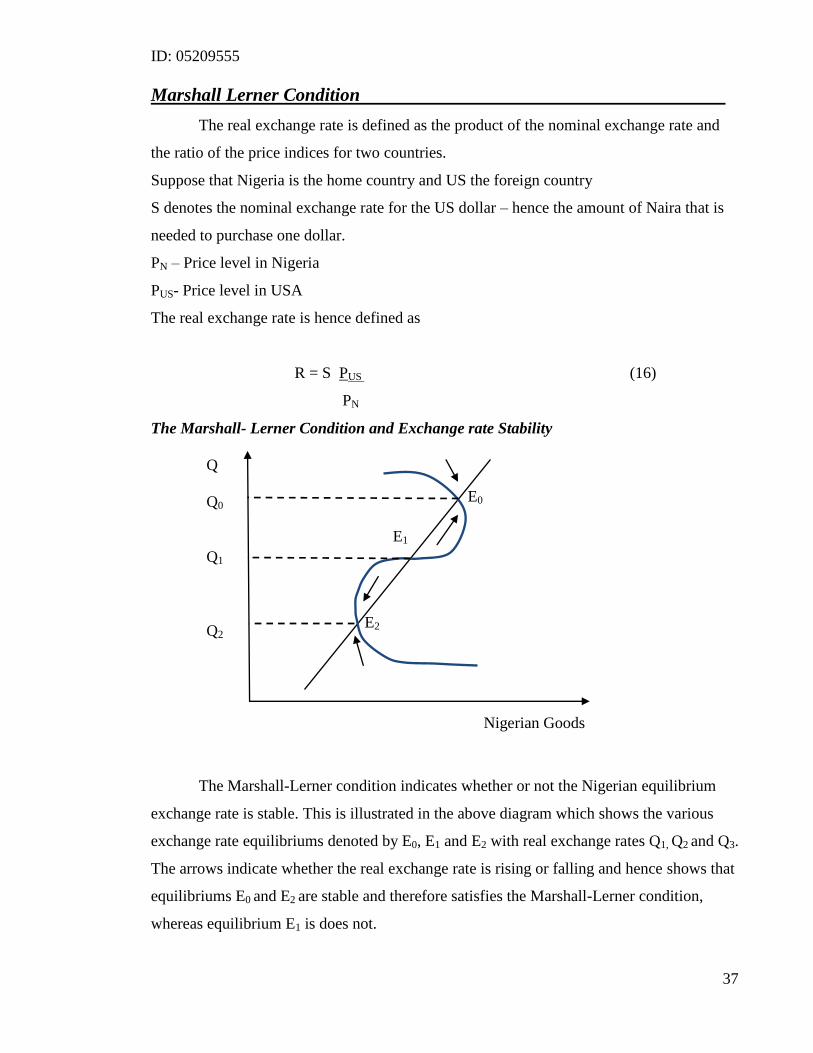

The Marshall- Lerner Condition and Exchange rate Stability

The Marshall-Lerner condition indicates whether or not the Nigerian equilibrium

exchange rate is stable. This is illustrated in the above diagram which shows the various

exchange rate equilibriums denoted by E0, E1 and E2 with real exchange rates Q1, Q2 and Q3.

The arrows indicate whether the real exchange rate is rising or falling and hence shows that

equilibriums E0 and E2 are stable and therefore satisfies the Marshall-Lerner condition,

whereas equilibrium E1 is does not.

Q

Q0

Q1

Q2 E2

E1

E0

Nigerian Goods

ID: 05209555

38

An increase in the real exchange rate between the Naira and the Dollar will cause a

substitution of consumption away from American goods towards Nigerian goods in both

countries. This elasticity approach focuses on the relationship between real exchange rate

and the flow of goods and services as measured by the current account balance16

. A rise in

net exports is referred to as an improvement of the current account balance and a fall in net

exports a deterioration.

The Marshall Lerner Condition hence shows the conditions under which a change in

the exchange rate of the Naira leads to an improvement or worsening of Nigeria‟s balance

of payments. Under a flexible exchange rate regime as used in Nigeria, a balance of

payment disequilibrium should automatically be restored to equilibrium without the need

for governmental policies. This is based on certain key assumptions which economists still

argue, do not apply to less economically developed countries like Nigeria. These

assumptions concern the degree to which changes in import and export prices affect the

immediate demand quantity of exports and imports.

16

International Economics – Charles van Marrewijk. Page 488

ID: 05209555

39

J-Curve

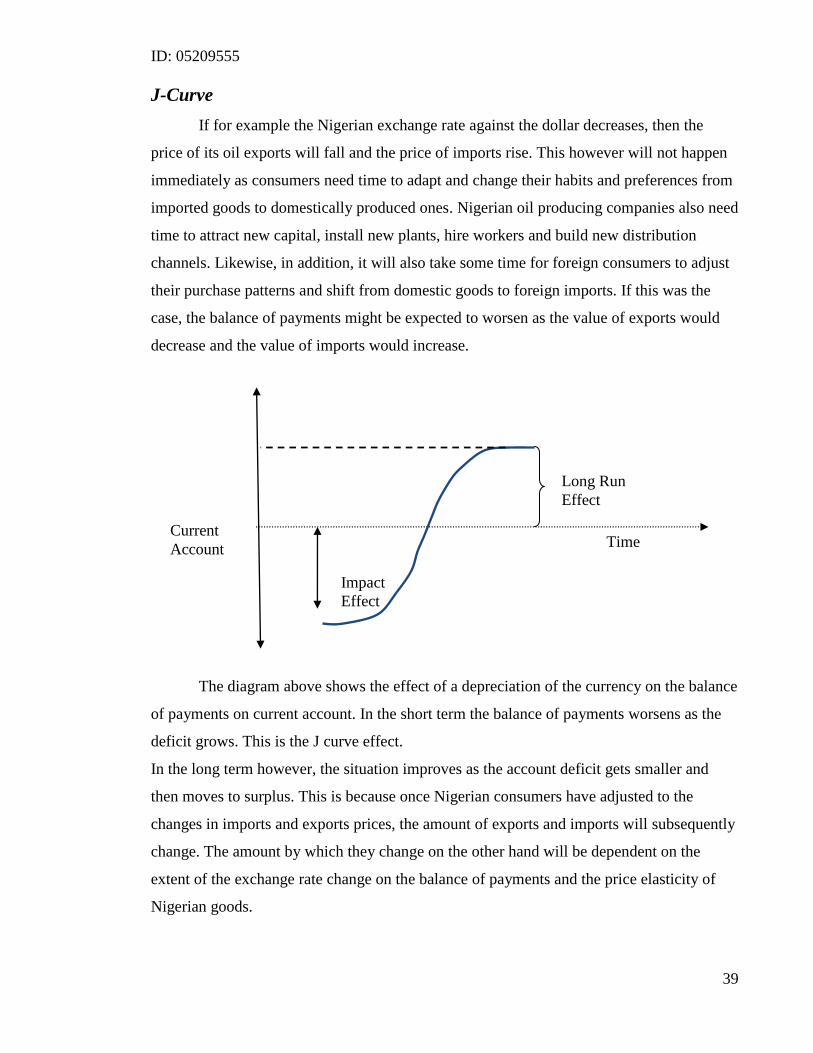

If for example the Nigerian exchange rate against the dollar decreases, then the

price of its oil exports will fall and the price of imports rise. This however will not happen

immediately as consumers need time to adapt and change their habits and preferences from

imported goods to domestically produced ones. Nigerian oil producing companies also need

time to attract new capital, install new plants, hire workers and build new distribution

channels. Likewise, in addition, it will also take some time for foreign consumers to adjust

their purchase patterns and shift from domestic goods to foreign imports. If this was the

case, the balance of payments might be expected to worsen as the value of exports would

decrease and the value of imports would increase.

The diagram above shows the effect of a depreciation of the currency on the balance

of payments on current account. In the short term the balance of payments worsens as the

deficit grows. This is the J curve effect.

In the long term however, the situation improves as the account deficit gets smaller and

then moves to surplus. This is because once Nigerian consumers have adjusted to the

changes in imports and exports prices, the amount of exports and imports will subsequently

change. The amount by which they change on the other hand will be dependent on the

extent of the exchange rate change on the balance of payments and the price elasticity of

Nigerian goods.

Impact

Effect

Time

Long Run

Effect

Current

Account

ID: 05209555

40

Since the demand for oil from Nigeria is relatively price inelastic, a fall in the price

of exports caused by a fall in the exchange rate will lead to a proportionately greater

increase in the quantity of exports demanded. This should then improve the Nigerian

balance of payments.

If a balance of payments disequilibrium is to be restored then it is important that the Price

Elasticity of Demand coefficient for exports is greater than 1 and that the Price Elasticity of

Demand coefficient for imports is greater than 1. This is embodied in the Marshall Lerner

condition which demonstrates that provided the sum of the price elasticities of demand for

Nigerian exports and imports is greater than one then a fall in the exchange rate will reduce

a deficit and likewise a rise will induce a surplus.

If the Marshall Lerner Condition is not met and the sum of the price elasticity of

demand for exports and imports is less than one, then a fall in the Nigerian exchange rate

will bring about a worsening of the nations balance of payments accounts. The fall in the

price of exports will lead to a proportionately smaller increase in the number of exports

demanded and a rise in the price of imports will lead to a proportionately smaller reduction

in the amount demanded. Both of these factors will contribute to a deterioration of the

balance of payments. Therefore in assessing the likely impact of a policy that will lead to a

fall in the value of the Naira, the Nigerian government must give consideration to the price

elasticity of demand for both exported and imported goods.

ID: 05209555

41

Unemployment and the Phillips Curve

The level of unemployment in Nigeria is a serious issue for the government and

policy makers. In 2003 the level of unemployment was as high as 28%. Although Nigeria is

endowed with diverse and infinite resources, years of negligence and adverse policies as

illustrated previously has led to the under-utilization of the country‟s natural resources

leading to severe under employment in the economy. Unemployment is a major problem

both economically and socially and has resulted in a higher percentage of the population

having no purchasing power. As a result, consumption levels have fallen leading to lower

production of goods and services and hence generally hampering economic growth.

A successful policy to reduce the level of unemployment in the long run needs to

encourage an improvement in the employability of the labour supply through education and

training. Policies should focus on improving the occupational mobility of labour and an

improvement in the incentives for people to search and accept work. This however may

require some reforms of the Nigerian tax and benefits system. Aggregate demand also

needs to remain sufficiently high for businesses to look at expanding their workforce. For

this to happen, there needs to be a sustained period of economic growth in order to boost

expectation levels in the economy. The government must also use macroeconomic policies

to increase the level of aggregate demand in the economy. These policies might involve

lowering interest rates or lowering direct taxes, it may also wish to encourage foreign

investments into the economy from multinational companies by employing favourable

taxes and subsidies.

The relationship between unemployment and inflation discovered in 1958 by A.W

Phillips, shows clear evidence of a negative relationship between inflation and

unemployment. It found that when inflation was high, unemployment was low and vice-

versa. The role of expectations in this relationship transmission is very important and this

approach is based on price and wage rigidities, arising for example, by the need to fix

prices and wages for some period.

ID: 05209555

42

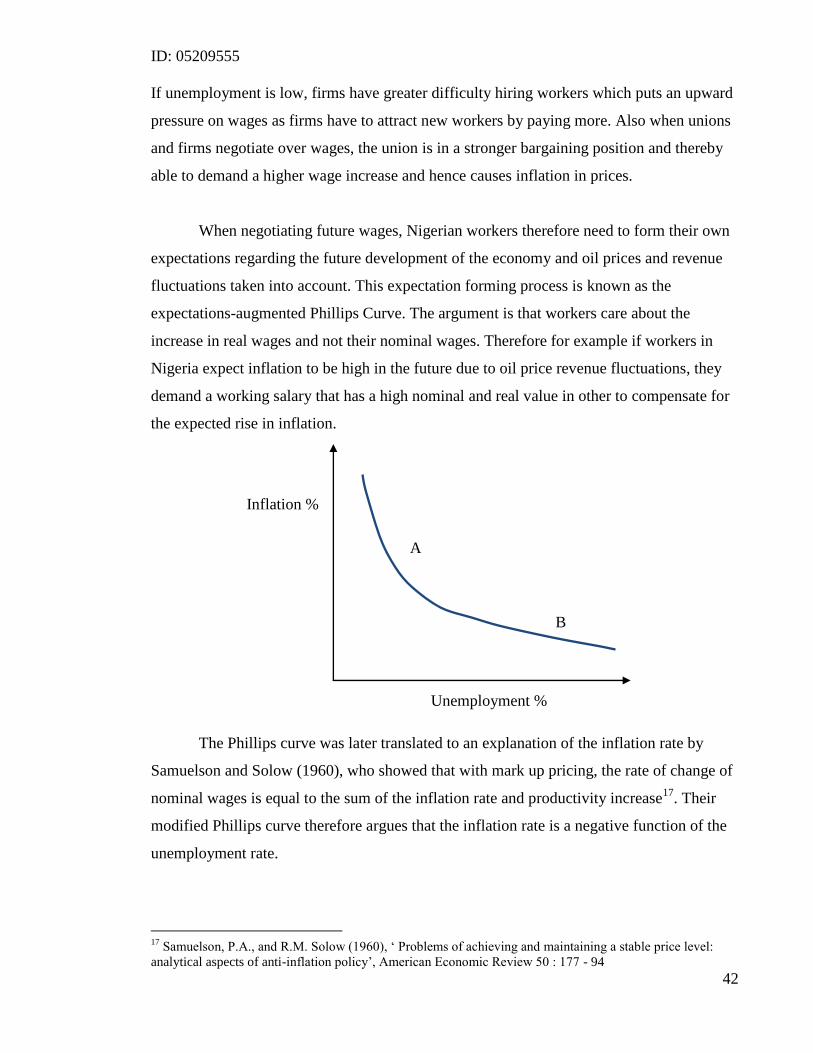

If unemployment is low, firms have greater difficulty hiring workers which puts an upward

pressure on wages as firms have to attract new workers by paying more. Also when unions

and firms negotiate over wages, the union is in a stronger bargaining position and thereby

able to demand a higher wage increase and hence causes inflation in prices.

When negotiating future wages, Nigerian workers therefore need to form their own

expectations regarding the future development of the economy and oil prices and revenue

fluctuations taken into account. This expectation forming process is known as the

expectations-augmented Phillips Curve. The argument is that workers care about the

increase in real wages and not their nominal wages. Therefore for example if workers in

Nigeria expect inflation to be high in the future due to oil price revenue fluctuations, they

demand a working salary that has a high nominal and real value in other to compensate for

the expected rise in inflation.

Inflation %

The Phillips curve was later translated to an explanation of the inflation rate by

Samuelson and Solow (1960), who showed that with mark up pricing, the rate of change of

nominal wages is equal to the sum of the inflation rate and productivity increase17

. Their

modified Phillips curve therefore argues that the inflation rate is a negative function of the

unemployment rate.

17

Samuelson, P.A., and R.M. Solow (1960), „ Problems of achieving and maintaining a stable price level:

analytical aspects of anti-inflation policy‟, American Economic Review 50 : 177 - 94

Unemployment %

A

B

ID: 05209555

43

The new downward sloping Phillips Curve suggests a policy trade-off between

inflation and unemployment, provided that the underlying Phillips curve is stable.

Therefore, the short-run trade-off between inflation and unemployment depends on the

expected inflation rate and the friction in the labour market which is measured by changes

away from the natural rate of unemployment. If the Nigerian government was keen on

keeping unemployment low, it could achieve its objective at the cost of a high inflation rate

by choosing point A on the diagram. Similarly, if Nigeria was seeking to maintain a

reasonable level of inflation, it could achieve this at the cost of high unemployment by

choosing point B on the Phillips Curve.

Since the discovery of oil in commercial quantities, Nigeria has seen a trend and

movement of labour from the rural areas to urban cities in search of job opportunities. A

major reason for this trend has been blamed on the aftermath of the first oil price shock,

which for Nigeria resulted in a reduction in the size of the rural labour workforce, leading

to a sharp decline in agricultural production and hence a sharp rise in food prices.

ID: 05209555

44

Waste and Dutch Disease

Economists argue that the main broad themes that preceed any macroeconomic

account of Nigeria‟s development disease can be traced back to the problem of waste and

Dutch disease. Dutch disease is the relationship between the exploitation of a nation‟s

natural resources and the decline in the manufacturing sector, combined with moral fallout.

The argument is that an increase in government revenue from natural resources will de-

industrialise a nation‟s economy by raising exchange rates which makes the manufacturing

sector less competitive and the public service sectors entangled with business interest.

Nigeria, like other oil and mineral producing countries suffers from poor

institutional quality, stemming from the use of its natural resources. In most accounts of

Nigerian economic history, the impact of huge oil revenues on the economy through its

effect in raising the relative prices of non-tradable to tradable assets occupies a central and

significant role in explaining its drastic poor macroeconomic performance. The overall

picture that emerges is that Nigeria has over invested in physical capital and has

consequently suffered from poor productivity. Quality has suffered at the expense of

quantity. This is captured accurately by Bevan et al (1998) paper “This conjunction of a

powerful political impetus to public investment and lack of civil service skill is what makes

Nigeria‟s economic history in this period so spectacular; almost the entire windfall was

invested and yet... there was nothing to show for it” (p67)18

Historically, the politics of Nigeria has been shaped and moulded around getting

access to the huge revenues from oil. The Biafra civil war even was caused by the Igbo

community in the south attempting to gain control of the oil reserves. Successive military

dictatorships have also plundered oil wealth, more notably the Late President General Sani

Abacha. It is also important to understand that although oil wealth has been squandered

badly, it has also provided the government with the revenue to increase its expenditure and

thus provide better public services for the citizens. It is plausible that not only has Nigeria

squandered its oil wealth on ineffective policies as demonstrated earlier, but oil wealth has

also fundamentally altered politics and governance in Nigeria.

18

Bevan, D., P. Collier, J.W. Gunning, 1999, The Political Economy of Poverty, Equity, and

Growth: Nigeria and Indonesia, Oxford University Press

ID: 05209555

45

Oil is a natural resource endowment, an unalterable geographical feature of the economic

and natural landscape. If indeed the revenues and wealth it generates are in actual fact the

cause of a decline in the institutional well being of Nigeria as has been suggested, then

countries that have any sort of natural resources are destined to institutional decline and

poor growth.

ID: 05209555

46

Conclusion

Natural resources such as oil may or may not be a curse, on the balance that they

provide necessary revenues for the successful running of an economy whilst providing

opportunities for rent seeking and corruption. The best chance of lifting the “curse of oil”

lies in the successful implementation of various macroeconomic policies and the adoption

of a transparent economy and accountability, at both state and national levels. Although

Nigeria is now formally a democracy, it is clear that the balance of power between citizens

and public officials is skewed greatly in favour of the latter by virtue of easier access to oil

revenues. To solve this, the Nigerian government should demand that oil companies declare

all payments rather than just providing an aggregate figure for all transactions. This is an

essential tool in breaking the link between conflict and crime and natural resources because

it makes politicians, businesses and individuals accountable for their actions. It helps curb

corruption and reduces the incentives for indulging in rent seeking and other criminal

activities.

Another simple solution to the Nigerian curse lies in preventing the government

from approaching the oil revenues directly. Revenues should be distributed ultimately to

the citizens who are their true and legitimate owners, thereby replicating an economy that

resembles a country with no natural resources to rely on. The main task for the Nigerian

government is to ensure there is adequate transparency, accountability and sound oil

revenue management, all of which can be achieved by enlisting the help of large scale

organisations such as the World Bank and the IMF to provide support, advice, regulation

and administration of the country‟s oil revenues. The responsibility of the active

management and monitoring of oil revenues relies on the Nigerian government and its

ability to distinguish between temporary and permanent fluctuations in the level of oil

revenues generated and responding to them accordingly.

ID: 05209555

47

Having reviewed Nigeria‟s economic state over the last 30 years, it is clear that the

Nigerian economy would benefit greatly from efficiently managed macroeconomic

policies. Monetary policy in particular, is significant in instigating and promoting economic

growth whist alleviating poverty. The lack of investment into the country, due to volatile

interest and exchange rate levels is somewhat responsible for restricting economic growth,

especially when large investments are essential for rebuilding spare capacity, creating jobs

and controlling the level of oil revenue expenditure.

Although it is clear that the Nigerian macro-economy has suffered from the so

called “curse of oil”, she however can still succeed and grow by analysing all the historical

effects of oil revenue and ensuring an active regulation of government revenue,

accountability and transparency implementation. Therefore, with careful planning and

cooperation on several levels, the curse can be sidestepped or lifted.

ID: 05209555

48

Bibliography

A. Adeikinju. N.Falobi Macroeconomic and distributional consequences of energy

supply shocks in Nigeria. AERC Research Paper 162, Published for the African

Economic Research Consortium in Dec 2006.

Arpad von lazar and Althea L. Duersten (1976).Oil and Development Planning:

Implications for Nigeria.

Ayodele Olalekan Teriba(2006). Demand for M1 in Nigeria.

B. O. Obi (2007). Fiscal Policy and Poverty Alleviation: Some Policy options for

Nigeria. AERC Research Paper 164, African Economic Research Consortium.

Biodun Adedipe (2004) The Impact of Oil on Nigeria‟s Economic Policy

Formulation.

Brian Pinto (1987). Nigeria During and After the Oil Boom: A Policy Comparison

with Indonesia. The World Bank Economic Review, Vol.1, No. 3: 419 – 445.

International Bank for Reconstruction and Development

D. Bevan, P. Collier, J.W. Gunning, (1999). The Political Economy of Poverty,

Equity and Growth: Nigeria and Indonesia. Oxford University Press

D. Ghosh and U. Kazi. A Macroeconomic Model for Nigeria, 1958 – 1974.

Empirical Economics, Vol. 3, Issue 3, page 135 – 154.

Dr. Bright E. Okogu, D. Phil (2006). The Role of Fiscal Rules in Oil Revenue

Management – Nigerian Experience.

Dr. J.O. Sanusi. Central Bank and the Macroeconomic Environment in Nigeria.

Published on Aug 2002 for the Institute for Policy and Strategic Studies.

Emeka Duruigbo (2004). Managing Oil revenues for socio – economic development

in Nigeria: The case for Community based trust funds.

Ezekiel Ayodele Walker (2000) Structural change, the oil boom and the cocoa

economy of southwestern Nigeria, 1973 -1980s.. The Journal of Modern African

Studies, Vol. 38, Issue 1. Pp 71 – 87. Published by the Cambridge University Press

Frederic H. Murphy, Michael A. Toman, Howard J. A Dynamic Nash Game Model

of Oil Market Disruption and Strategic Stockpiling Operations Research, Vol. 37,

No. 6 (Nov. - Dec., 1989), pp. 958-971 Published by: Informs

G.B Olusegun Odularu (2008). Crude Oil and the Nigerian Economic Performance.

ID: 05209555

49

Godwin C Nwaobi (2003). Oil Policy in Nigeria: A Critical Assessment (1958-

1992). A Central Bank of Nigeria Publication. Published by Kas Arts Service

Limited

Godwin C Nwaobi. Corruption and Bribery in the Nigeria Economy. Quantitative

Economic Research Bureau.

I. H. McNicoll (1980). The Impact of Oil on the Shetland Economy. Managerial

and Decision Economics, Vol. 1, No. 2, Oil and Energy, pp. 91- 98. Published by

John Wiley & Sons

J. Raymond, R. Rich (1997). Oil and the Macro-Economy; A Markov State

switching Approach. Journal of Money, Credit and Banking; Vol. 29, Issue 2.

Pg.193. Published by ABI/Inform Global

James E. Smith and Kevin F. McCardle (1999). Options in the Real World: Lessons

Learned in Evaluating Oil and Gas Investments. Operations Research, Vol. 47, No.

1 (Jan. - Feb., 1999), pp. 1-15 Published by: Informs

Joseph E. Stiglitz and Carl E. Walsh (2002). Principles of Macroeconomics. Third

Edition. W.W. Norton & Company Inc.

Manfred Gartner (2006). Macroeconomics. Second Edition. Pearson Education

Limited.

Matthew Nga Uwakonye, Gbolahan Solomon Osho, Hyacinth Anucha(2006). The

Impact of Oil and Gas Production on the Nigerian Economy: A Rural Sector

Econometric Model. International Business & Economics Research Journal.

Volume 5, Number 2

Misan Rewane (2007). Overrated? The Impact of Oil Revenue on Nigeria‟s

Creditworthiness Debt Profile & Sustainability, 1973 – 2004.

O. Felix Ayadi (2005). Oil Price Fluctuations and the Nigerian Economy.

Organisation of the Petroleum Exporting Countries.

O. Felix Ayadi, Esther O. Adegbite. Funso, S. Ayadi (2008). Structural Adjustment,

Financial Sector Development and Economic Prosperity in Nigeria. International

Research Journal of Finance and Economics Issue 15. EuroJournals Publishing, Inc

Oliver J. Blanchard (1997). Macroeconomics. Prentice-Hall, Inc

ID: 05209555

50

P, Olomola. A, Adejumo (2006). Oil Price Shock and Macroeconomic Activities in

Nigeria. International Research Journal of Finance and Economic. Issue. Published

by EuroJournals Publishing, Inc

P.A.Samuelson, R.M. Solow (1960). Problems of achieving and maintaining a

stable price level: analytical of anti-inflation policy, American Economic Review

50: Pg 177 – 180.

Petroleum Economist. Volume 73/ Issue 11. Published Nov 2006

Petroleum Economist. Volume 75/ Issue 5. Published May 2008

R. M. Auty (1992) Sowing the Oil in Eight Developing Countries. Transactions of

the Institute of British Geographers, New Series, Vol. 17, No. 3 (1992), pp. 376-

377. Published by Blackwell Publishing on behalf of The Royal Geographical

Society (with the Institute of British Geographers)

Robert B Barsky, Lutz Killian (2004). Oil and the Macro-Economy since the 1970s.

The Journal of Economic Perspectives; Vol.18. Issue 4. pg 115. Published by

ABI/Inform Global

Robert J. Gordon. (1998) Macroeconomics. Seventh Edition. Addison Wesley

Longman, Inc.

S. Tomori, O. Akano, A. Adebiyi, W. Isola, O. Lawanson and O. Quadri(2005).

Protecting the Poor from Macroeconomic Shocks in Nigeria: An Empirical

Investigation and Policy Options.

Steven E. Landsburg and Lauren J. Feinstone (1997). Macroeconomics.

International Edition. McGraw-Hill Companies.

T Mogues, M Morris, L Freinkman, A Adubi, S Ehui with C Nwoko, O Taiwo, C

Nege, P Okonji, L Chete. Agricultural Public Spending in Nigeria. International

Food Product Research Institute Discussion Paper 00789. Published Sept 2008 for

the Development Strategy and Governance Division.

Timothy Ch. U. Kalu. Determining the Impact of Nigeria's Economic Crisis on the

Multinational Oil Companies: A Goal Programming Approach. The Journal of the

Operational Research Society, Vol. 45, No. 2 (Feb., 1994). Published by Palgrave

Macmillian Journals on behalf of the Operational Research Society

U.Ukwu, A.W. Obi, S. Ukeje (2004). Policy Options for Managing Macroeconomic

Volatility in Nigeria. Published for the African Institute for Applied Economics.

ID: 05209555

51

Xavier – Sala- i- Martin and Arvind Subramanian (2003). Addressing the Natural

Resource Curse: An Illustration from Nigeria.

Yinne Yu (2003). The Impact of Private International Cartels on Developing

Countries. Department of Economics Stanford University.

Internet Sources

World Bank Database –

http://www.worldbank.org/data/countrydata/countrydata.html accessed 20 Jan 2009

11:11

Nigerian Central Bank http://www.cenbank.org/ Accessed 20th

November 2008

17:00