the epa manual for waste minimization audits - draftinfohouse.p2ric.org/ref/32/31702.pdf · n the...

TRANSCRIPT

United States Office of Research and Development EPA ###-XX-##-### Environmental Protection Hazardous Waste Engineering August 1987

CincinnafiXJFl45268 ~

~~ ~ ~~

- 1 Agency Research Laboratory

The EPA Manual for Waste Minimization Audits

I 1

n

n

The EPA Manual for Waste Minimization Audits

Gregory A. Lorton, Carl H. Fromm, Michael P. Meltzer, Michael S. Callahan, and Srinivas Budaraju

Jacobs Engineering Group Hazardous and Toxic Materials Division

251 S. Lake Avenue Pasadena, CA 91 101

Submitted to

Harry M. Freeman Research Program Manager

Hazardous Waste Engineering Research Laboratory Office of Research and Development

U. S. Environmental Protection Agency Cincinnati, OH 45268

August 14, 1987

1

1 1. 1 2. I 3. 1 4.

5. 11

6. 3 3 7.

Introduction

Waste Minimization Audit Overviews

WM Audit Program Planning and Organization

WM Audit Preparation and Information Gathering

Waste Minimization Auditing

Feasibility Analysis

Implementing Waste M ini mizati on Options

n Appendices

A. WM Audit Program Worksheets 6. Waste Minimizatiw Techniques C, State TechnicallFinancial Assistance Programs 0. Economic Evaluation Example

3 1

- * ~ ~ ~ . * ~ ~ ~

paqe

1

3

11

22

30

41

51

A- 1

B- 1 c- 1 D- 1

Waste minimization (WM) is a policy specifically mandated by the U.S. Congress in i t s

Hazardous and Solid Waste Amendments of 1984 t o the Resource Conservation and

Recovery A c t (RCRA) of 1976. These Amendments state that:

"The Congress hereby declares it t o be the national policy of the

Uni ted States that, wherever feasible, the generation of hazardous waste is

t o be reduced or eliminated as expeditiously as possible. Waste that i s

nevertheless generated should be treated, stored or disposed of so as t o

minimize the present and fu ture threat t o human health and the environ-

ment" (RCRA 1003(b), PL 98 -616).

This mandate, coupled w i th other RCRA provisions that have led t o unprecedented

increases in costs o f waste management, have heightened general interest in waste

minimization. A strong contributing factor has been a desire, on the par t of

generators, t o reduce their environmental impairment l iabi l i t ies under the provisions

o f the Comprehensive Environmental Response, Compensation and Liabi l i t ies A c t

(CERCLA or "Superfund").

In i t s e f fo r t to assist waste generators t o meet current demands t o reduce waste, the

EPA has sponsored the preparation of th is guide. The guide is intended t o provide

basic information t o individuals interested in developing a waste minimization audit

program in their firm. This includes activi t ies such as conducting waste reduction

audits, implementing W M measures, and assessing their progress.

The guide is t o be used as a source of concepts and ideas. It begins wi th a br ie f

definit ion of waste minimization and related terms. Next, incentives for WM are

described and a br ie f discussion of economic considerations is provided. Five phases of

a W M audit program are outl ined in this manual: planning and organization;

information gathering; waste minimization audits; feasibil i ty analysis; and program

implement a t i on.

Throughout the manual the terms "company1', "firm", and "corporationrr are used. It

should be recognized tha t this mater ia l is applicable in large part t o other

1

organizations, such as government agencies and non-profit organizations. Similarly, although most of t h e material is aimed a t manufacturing facilities, much of t h e

material is applicable t o other segments o f industry, government, or business.

~ - _ - _ - ~ _ _ _ - - ~ - ~ - - ~

1 The manual has been prepared for t h e people responsible for planning, managing, and

implementing waste minimization activities at t h e plant and corporate levels. The manual concentrates mainly on waste minimization audit procedures that mot iva te people t o search, sc reen and put into practice measures involving administrative, material , or technology changes tha t result in decreased waste generation. A partial ca ta log and brief discussion of these measures is provided in t h e appendices f o r

common waste-intensive operations. There, t h e prime emphasis is given to source reduction, in accordance with the EP A-recognized hierarchy.

n n 3 13

IJ 1 3 I) 2

. I

EFINITION OF WASTE MINIMIZATION

The working definit ion of Waste Minimization used by EPA in i t s recent Report t o

Congress i s presented in Figure 2-1. WM is viewed as consisting of three components:

(source reduction, recycling, and treatment), o f which source reduction clearly i s the

most preferable approach in terms of environmental considerations. The components

o f source reduction are shown in Figure 2-2.

The EPA does not consider the reduction of waste tox ic i ty by di lut ion or of quantity by

dewatering (or more generally, by the removal of iner t components) as valid W M

activi t ies in and o f themselves. However, i f a dilution or dewaterinq step i s necessary

t o render the resulting waste recyclable or treatable, then such a step i s considered as

an integral par t of t h e recycling or treatment operation, both of which are viable WM

m e as ur es.

It should also be noted that the present focus of WM activit ies are hazardous wastes

tha t f a l l under RCRA jurisdiction. There are, however, strong reasons for using a

mult imedia approach when structuring and executing a WM audit program. Such an

approach calls fo r consideration of releases of environmental pollutants in to a l l media,

Le. air, water and land, t o prevent shift ing of pollutants f rom one media t o another.

Examples of such shift ing include land disposal of treatment sludges resulting f rom

wastewater cleanup or of condensates resulting f r o m steam regeneration of carbon

beds used t o control volati le organic emissions. An emissions inventory ideally should

account fo r all pollutants leaving the plant in a l l media including air, water, and land.

INCENTIVES FOR WASTE MIMMlZATlON

There are several powerful and compelling reasons fo r minimizing waste generation.

summarized in Table 2-1.

3

. . #

WASTE MINIMIZATION

SOURCE REDUCTION RECYCLING TREATMENT

RELATIVE ENVIRONMENTAL DESIRABILITY HIGH LOW

ORDER OF EXPLOWTON FIRST LAST

WASTE MINIMIZATION Tho reduction. to the extent fwbk, of hazardous waste that k generated or subsequently treated, stored or di8po8.d d. A includoa any aoum reduction or recycling activw undertrken by 8 generator that results in either (1) the redudion of total wlume or quantity of hazardous wasto or (2) the redudion of toxicity of the hptardou8 waste, or both, so bng a8 such reduction is consistent with the goal of minimizing present and future throat8 to human h d t h and the environment (€PA8 Report to Congreu, 1986, EPA630-SW-86-033).

SOURCE REDUCTION

Any activity that reducw or eliminatw the generation of hazardous waste a! the aoura, usually within a pmceu (op. Cit.).

RECYCLING A material is "yded' if it k used, reused, or rdaimed (40 CFA 261 .l (c) (7)). A materkl k ' u d or reused' if 1 k either (1) employed 01 an ingredient (including b use a8 an intermediate) to mako 8 product: however a material will not satisfy this condition W distinct components of the matorial are recovered a8 separate end product8 (aa whon metab are mxrvered from m.W aontoining seandary materials) or (2) empbyed in a particular fundion u UI effective suktitute for a commercial product (40 CFR 261.1 (c) (5)). A material k 'reclaimed' if W k pmcaood b reawor a usoful product or if it ir regenerated. Example$ of recovery of kad valuoa from apnt bdtoriea ud regeneration of spent solvents (40 CFR 261 .l (c) (4)).

TREATMENT

Any mothod, tochniqw, or m, including neutralization, duigned to change tho phy8iUl. chemical, or biobgicrl chmu or compooitbn of any huardow waste 10 a8 to neutnlite such wort0 or w 88 to render such waste m-hazardous, safer for transport, amenabk for recovery, amensMe for stongo or reduwd in volume. Such term mludes my activity or pmceuing designed to chango the phyriUr form or chemical comporition of hazardous w a r so sr to render it non-huordour (RCRA, Subtitk A, S.ctkn 1004(34). PL- 98-61 6).

Figure 2-1. Components of waste minimization, their hierarchy and definitions.

4 1

I SOURCE REDUCTION -1

TECHNOLOGY CHANGES

PRODUCT CHANGES 1

I

Product Substitution Product Conservation Change in Product

Composition

I INPUT MATERIAL r CHANGES

I MaterialPuffiiion Material Substitution

Processchanges Equipment, Piping, or

Layout changes Additional Automation Changes in Operational

settings Energy Conservation Water Conservation

TECHNOLOGY CHANGES

Processchanges Equipment, Piping, or

Layout changes Additional Automation Changes in Operational

settings Energy Conservation Water Conservation

PROCEDURAL OR INSTITUTIONAL CHANGES

~~

Procedural Measures Loss Prevention Personnel Practices Waste Stream Segregation Material Handling

Improvements

Figure 2-2. Elements of Source Reduction

1 I

Economics o Landfill disposal cost increases. o Costly alternative t rea tment technologies. o Savings in raw material costs.

Regulations o o Biennial WM program reporting. o

Certif ication of a WM program on t h e Hazardous Waste Manifest.

Phase-in of land disposal restrictions.

Liability o Reduction in generator liability fo r environmental

problems a t offsite TSD facilities.

Economic performance of WM projects has been enhanced by the rising costs of land disposal and other forms of waste management. Regulation-driven upgrading of RCRA-approved landfills has increased the costs of land disposal from as l i t t le as $10-$15/ton in t h e early 1970's t o $200-300/ton today. The costs for land disposal increased by a f ac to r of 2 t o 6 over the last 3 years depending on t h e type of waste and locality. These costs have not yet shown any signs of stabilizing.

Future increases in was te management costs are likely because of t h e difficulties associated with siting and permitt ing new t rea tment , storage and disposal facilities (TSDF) and with t h e increasing scope of land disposal bans. Current and fu ture land disposal restrictions will force the generators t o turn t o expensive t r ea tmen t or incineration ($500 -51200 per met r ic ton) and/or seek more cost e f fec t ive source reduction or recycling alternatives. In addition t o accounting fo r t hese rising costs, t h e economic performance of WM projects improves if raw materials savings are included along with the savings related t o avoided processing costs. The details of economic feasibility analysis are discussed in Section 8.

The cur ren t regulations for hazardous waste generations (40 CFR 262) provide several direct and indirect incentives for waste minimization. Di rec t incentives include:

6

1 1 A t h e m a n d a t a r y VfM certification requirement tha t must be signed by t h e

generators on every Uniform Hazardous Waste Manifest (Figure 2-3).

o the mandatory biennial reporting detailing progress of WM programs.

Indirect incentives consist of:

Land disposal restrictions, enac ted in stages, beginning with solvents on November 8, 1986, continuing with t h e ''California List" (liquid hazardous wastes containing f r e e cyanides, PCBs, corrosives, or cer ta in heavy metals; and hazardous wastes containing halogenated organic compounds) on July 1987 and with successive tiers by "thirds" coming on August 8, 1988, June 1989 and May 8, 1990).

Low regulatory permitting burden for projects involving on-site source reduction and recycling. Many source reduction measures do not require any permitting whatsoever. Installation of equipment for onsite recycling, such as stills for solvent recovery, does not require RCRA permits, although air permits may be required. \&&$*

@i"k- F,;lkm LU.&uy L/Pc&bL.%&4j I t l L t 4 S J L h d ( G ' J b anAp4 / h L e L A k * ? L + 4 ' L c v h ,

An often used argument for minimizinq waste is t h e reduction of risk associated with environmental impairment liability of the generator. Waste management using offsite t rea tment , storage and disposal facilities (TSDF) poses the risk of release of such was te to the environment due t o poor handling by transporters or TSDF operators or due t o flaws in the design or construction of such facilities. The risks can be reduced by careful inspection of TSOFs and their management, but never totally eliminated. If there is migration of t h e wastes off t h e TSOF site, the waste generators can be held liable for clean-up costs merely because their wastes were taken t o tha t facility. Under provisions of CERCLA, Section 106 and 107, the generator can be held financially liable for t h e en t i re cos t of cleaning or restoring t h e TSDF site.

PHASES IN A WASTE MIMMIZATION PROGRAM

Although the main objective of a waste minimization audit program is t o reduce or eliminate waste, t h e program can also bring about an improvement in a company's production efficiency. In th i s sense, t h e W M audit program is similar in concept t o

7

1

other proqrams and -€unctinns that are aimed at improving concentrating on a specific aspect of a company's operation.

1 1

overall performance by

Four examples of these

types of programs and functions a r e energy conservation programs, environmental audits, value engineering, and managerial accounting. Descriptions of these programs and functions are shown in Table 2-2.

The conception and a waste minimization audit program will typically

involve several

o program planning and organization o information gathering o was te minimization audit o feasibility analysis o implementation of W M options

Each of these phases is briefly described in Table 2-3. The following chapters discuss t h e details of each of t h e W M audit program phases outlined here.

8

~~~!J~.QJ"-"-~~~~~~~~~~~~

Table 2-2. PROGRAMS AND FUNCTIONS SIMILAR TO WASTE MINIMIZATION AUDIT

Program/Function

PROGRAMS

Energy Conservation program

Environmental Audits

Value Engineering W

Managerial Accounting

Description

This program centers around energy audits of a facility, with the goal of reducing energy losses and energy consumption.

These a u d i provide a systematic examination of a firm's activ51ies to determine its compliance status with environmental regulations.

This discipline is a systematic approach toward reducing a project's (or a product's) cost, while maintaining its functionality.

This function is the use of accounting data to control (and reduce) a firm's costs, and improve eff icincy and effectiveness.

~~

Relevance to Waste Minimization

I Energy conservation is analogous to WM, with the emphasis on energy losses, rather than waste reduction. Energy audit procedures are generally applicable to W audiis, and the programs can benefit each other. Energy audits have been widely used in industry since the 1970%.

Environmental audts deal with the same waste streams as the WM audl. However. in environmental audits, the emphasis is more on effluent treating processes than on production processes or maintenance activities, and the focus is on regulatory compliance, rather than improving efficiency. Environmental audits and WM audits can be carried out together.

Value engineering concentrates on reducing costs. The principles and procedures are well-established and are directly applicable to WMaudits.

Managerial accounting (or cost accounting) deals with all aspects of a firm's operations. Managerial accounting data is useful in analyzing waste management operations. Also, managerial accounting procedures can be used or modiiied to bring about waste reduction. (For example, waste treatment and disposal fees can be included into the internal costs of input materials charged to the waste generating departments.)

- - - I- ~-Luuuud d L J - . A 2 “ 1

Table 2-3. PHASES OF THE WASTE MINIMIZATION AUDIT PROGRAM

Program Phase

WM Program Planning andOrganizatbn

WM AudiP Preparation and Infomation Gathering

w Waste Minimization Auditii 0

Feasibility Analysis

Implementation of WMopt i i

Stem or Tasks

Get top management commilment Set goals for the program Organize the program task force and audi teams

I

Identify and track waste streams Collect and compile process and facility data Select the waste streams or faci l i areas to audit

Inspect the site Generate options Screen and rank the options Select the promising options for further study

Perform technical evaluation Perform economic evaluation Select the attractive options and issue final report

. Obtain funding Install the option Evaluate the option’s performance . Continre looking for potential new options

Remarks

An effective planning and organization phase necessary to overcome potential barriers and eff eaively irrQement the WM program

11

- is to

Effective preparation is criiical to understanding the mechanisms by which wastes are produced, and how waste generation can be reduced.

The audit is a systematic procedure by which options are proposed that will minimize waste. The procedure also provides a means for screening potential options for further study.

The feasibility analysis is aimed at determining whether a promising option will wok, and do SO economically. in a specific application.

Attractive options generally require funding, followed by installation. Performance, measured by waste reduction, determines whether an option is truly effective. The WM audii program should be an ongoing one.

SECTION 3 ___ -- - -.

WM AUDIT PROGRAM PLANNING AND ORGANIZATION

A comprehensive waste minimization audit program affects many functional groups within a company. A good program will bring these different groups together t o solve or reduce the company's waste problem. The formality of the program depends upon the s ize and complexity of t h e organization and i t s waste problem. The program s t ruc ture must be flexible enough to accommodate unforeseen changes and unexpected occurrences. The developmental activit ies of a waste minimization audit program include:

o initiating the program o set t ing goals and objectives o staffing the program o gett ing commitment and dealing with conflict

INITIATING A WM PROGRAM

The successful WM audit program begins with a formal policy s ta tement or directive f rom top management. The person in charge of t he company's environmental affairs is responsible t o advise top management of the need for this formal commitment. An example of a formal policy s t a t emen t is t h e following:

~

[A mapr chemical compmny] ..." is committed to continue excellence, kadership, and stewardship in protecting the environmont. Environmental protection is a primary management r ~ n r b i l i t y , as well as the responsibility of evory empbyw.

In keeping with thb policy, our objodivo aa a company k to reduce waste and achiove minimal adverse imp.d on tho air, water, and land through excellence in environmental control.

The Environmental Guidelinoe induck the folbwing points:

Environmontal protection h a lino rmponaibility and an importrnt moaoun d unpkyw petfmaolr. In addition, ovory emp@oe ia reaponsiblo for environmental protection in the m o manrul ho or rho is for safety.

Minimizing or eliminating tho generation d waute has beon and continues to be a prime considuatbn in rosmafch, ploceu design, and plant opwstions; and is v h o d by management~like safhy, yie#, and h a prevention.

Rwuw and roqding d moderiak has been and will continuo to bo given first conrider8tbn prior to daasifiiion and disposal of waste:

11

1 1 7 1 :I

GOALS

To faci l i tate the WM audit program, establish goals to define the program's objectives.

Waste reduction goals can be qualitative. For example, the goal might be "a

significant reduction o f toxic substance emissions into the workplace environment.''

However, it i s better to establish measurable, quantifiable goals, since qualitative

goals can be interpreted ambiguously. Quantifiable goals establish a clear guide as to

the degree of success expected of the program. A major chemical company has

adopted a corporate-wide goal of 5% waste reduction per year. In addition, each

fac i l i ty within the company i s setting i t s own waste reduction goal. Many o f the

plants have alceady reported signifiFant reductions in waste. ' j A 4 & *AiL?' /

As part of i t s general policy on hazardous waste, a large defense contractor has

established an ambitious corporate-wide goal of zero discharge o f hazardous wastes

f rom their faci l i t ies by the end of 1988. Each division within the corporation is given

the responsibility and freedom to develop i t s own program (with intermediate goals) t o

meet this overall goal. This has resulted in an extensive investigation of procedures

and technologies to accomplish source reduction, resource recovery, and onsi te

treatment.

?( "%&k p.& * f h L L c 1 . L b d t h G & f -ru\.c_Y T U b m fq y; .h 'M * W k G d i b d 4 t )ah- ye-13 _. 3

Table 3-1 l ists the qualities that the goals should possess. It i s important that the

company's overall waste minimization goals be incorporated into the appropriate

individual departmental goals.

Table 3-1. ATTRIBUTES OF EFFECTIVE GOALS

o o o MEASURABLE over time. o MOTIVATIONAL. o o UNDERSTANDABLE. o ACHIEVABLE.

ACCEPTABLE to those who w i l l work t o achieve them. FLEXIBLE and adaptable t o changing requirements.

SUITABLE t o the overall corporate goals and mission.

Source: Pearce and Robinson, Strateqic Management (1985)*

12

1

-1 :1 7

:-I ... 'I

3 1

I .1

The waste minimization audit program w i l l affect a number of groups wi th in a large

company. For th is reason, a program team or task force should be assembled. This

team should include members of any group or department in the company that has a

significant interest in the outcome of the program. Table 3-2 l ists departments or groups of a typical manufacturing company that should be involved in the program.

Table 3-2 IMPORTANT PARTICIPANTS H A WASTE MINIMIZATION PRO(#AM

For a manufacturing company, include representatives f rom

the following departments/functions:

o Production

o

o Process Engineering

o Quality Contro l

o Environmental Staf f

Faci l i t ies E ngi neeri ng/ Mai nt enance

Depending on the nature o f the W M audit program and the facil i ty,

also include representatives f rom the following

departments/functions, as appropriate:

o Safety

o Purchasing

o Mater ia l Control

o Information Systems

o Legal

o Finance / Accounti ng

o Product Inventory and Distr ibution

'7 d

The formal i ty or in formal i ty of the WM audit program w i l l depend on the nature of the

company. The program in a large, highly structured company w i l l probably develop t o

be quite formal in contrast t o a small company or a company in a dynamic industry,

where the organization's structure changes frequently.

13

J

Since the ~- program - w i l l consist of one or more projects, the program should be run as a

project task force. Table 3-3 l i s t the typical responsibilities of a W M audit program

task force. As such, i t w i l l draw on expertise wi th in the company as required. The

scope of the program w i l l determine whether ful l- t ime part icipation i s required by any

of the team members. Figure 3-1 illustrates a sample organization chart showing how

a W M audit program can fit into the structure of a large multi-division corporation.

Table 3-3. RESPoNSBUTlES OF TFE WM A m I T PROC4AM TASK FORE

0

0

0

0

0

0

0

0

0

0

0

~ ~~~~

Get commitment and policy statement f rom top management

Establish W M audit program goals

Establish a waste tracking system

Select the waste streamb) or fac i l i t y area(s) f o r audit

Select waste minimization audit team(s)

Conduct (or supervise) audits

Conduct (or supervise) technical/economic feasibi l i ty studies of favorable options

Select feasible opt ions for implement at ion

Obtain funding and establish schedule fo r implementation

Monitor (and/or direct) implementation progress

Monitor performance of the option once it i s operating

In a small company, several people a t most, w i l l be al l that are required t o implement

a WM audit program. Include the people w i th responsibility f o r production, facilities,

maintenance, quality control, and waste disposal on the team. It may be that a single

person, such as the plant manager, may have a l l of these responsibilities at a small

fac i l i ty .

Some larger companies have developed a system in which audit teams periodically

visi t the company’s dif ferent divisions. This allows the company t o benefit by sharing

the ideas and experiences of other divisions. Similar results can be achieved w i th

periodic in-house seminars workshops, or meetings. A large chemical manufacturer

held a corporate-wide symposium in 1986 dealing specifically w i th waste

minimization. The company has also developed other

wide awareness of waste minimization, including an

and an instruct ional videotape.

14

programs t o increase company-

internally-published newsletter

I I I I I I I I I I I

GROUP VICE PRESIDENT

GRbUP I VICE PflESIDENT

I I

Corporate Envlronmental

Staff

Dlvlslon Vice Presklent

Dlvlslon Vlce PresMent

I I

Waste

Program

. Facllltles Englneerlng Department

Production

Malntenance Department

Department

Production Operations

Departments

ProCeSS Englneerlng Department

I I I I I I I I I I

Director of Procurement and Materhl

Control

Raw Materlals

Supplies

ProdUd Inventory

Dlstrlbutlon

Research and Development

Dkector of tdminlstratlon

Legal Flnance

Account Ing Personnel

lnformatlon

Contract ldmlnlstratlon

Safety

............................................... Figure 3-1. Waste Management Audit Program within a Large Corporation

FormWMA 1.6 MC-7/87

J

1

SELECTING ~ ~ TI€ ALJDIT TEAM

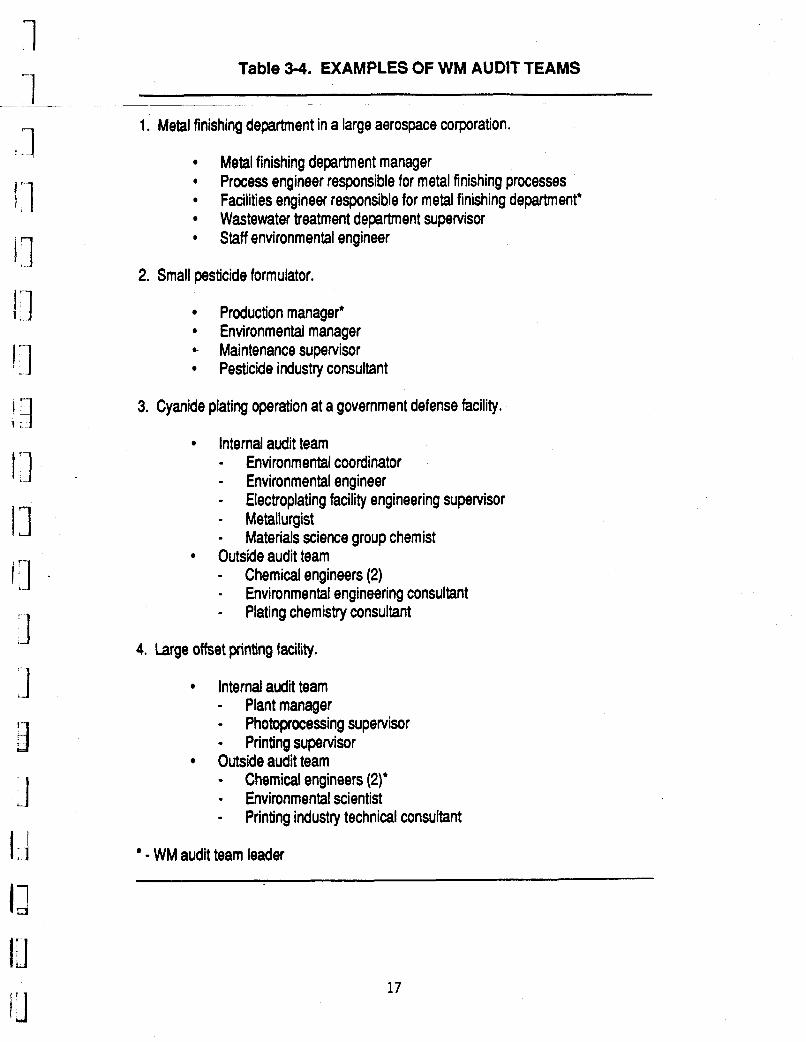

W M audits are a principal activity of a WM audit program. The selection of audit teams, therefore, is a n important function of t h e WM audit program manager. As with the W M audit program task force, the W M audit t e a m should be represented by members of the various a f fec ted groups. While t h e WM audit program t a sk force considers t h e whole facility, the focus of t h e audit t eam is more specific, concentrating on a particular waste s t ream or a particular a rea of t h e facility. As

such, t h e audit t eam should include people with direct responsibility and knowledge of the particular waste s t ream or a rea of t h e facility. Table 3-4 presents four examples of audit t e a m s for facilities of various sizes in different industries.

In addition t o t h e internal s taff , consider using outside people, especially in t h e audit and implementation phases. They may be independent consultants or experts from a different facility of t h e same company. In large multi-division companies, a centralized s ta f f of experts at the corporate headquarters may be available. One or more "outsiders" can bring in new ideas and provide a n objective viewpoint. 4 n outsider also is more likely t o counteract bias brought about by inbreeding and t h e

"sacred cow" syndrome.

Outside consultants can bring a wide variety of experience and expertise t o a waste minimization audit program. Consultants may be especially useful t o smaller companies who may not have in-house expertise in t h e appropriate waste minimization techniques and technologies.

Production operators and line employees are of ten an excellent source of WM

suggestions. These people are useful in identifying important waste streams. They a l so have an intuitive feel how changes a f fec t the production process. This can be especially useful in suggesting operational or procedural changes. Companies t h a t have quality circles can use these as a means of eliciting suggestions for waste minimization. Several large manufacturing companies reported successful suggestions for waste minimization originating f rom quality circles.

16

1 " I

'1 I . 1

I:]

_-

Table 3-4. EXAMPLES OF WM AUDIT TEAMS

1. Metal finishing department in a large aerospace corporation.

Metal finishing department manager *

Wastewater treatment department supervisor * Staff environmental engineer

Process engineer responsible for metal finishing processes Facilities engineer responsible for metal finishing department'

2. Small pesticide formulator.

Production manager' Environmental manager

.- Maintenance supervisor Pesticide industry consultant

3. Cyanide plating operation at a govemment defense facility.

Internal audit team - Environmental coordinator - Environmental engineer - Electroplating facility engineering supervisor - Metallurgist - Materials science group chemist Outside audit team - Chemical engineers (2) - Environmental engineering consultant - Plating chemistry consultant

+. Large offset prillting facility.

Internal audit team - Plant manager - Photoprocessing supervisor - Printing supervisor Outside audit team - Chemical engineers (2)' - Environmental scientist - Printing industry technical consultant

- WM audit team leader

la

17

OVERCOMING ~ BARFUERS

Although waste minimization pr cts can reduce operating costs and improve

environmental compliance, they can also lead to conflicts between dif ferent groups.

For example, a change aimed at reducing waste in a plat ing operation may be

detr imental t o the production ra te or product quality. In the defense industry, the

abi l i ty t o continue meeting mi l i ta ry specifications (Mil Specs) i s an important

consideration fo r WM projects. Therefore, production and quality control personnel

must be included in the waste minimization evaluation process. Table 3-5 l i s t s

examples of confl icts tha t can arise during the implementation of a waste

minimit a t ion project.

In addition t o jurisdictional confl icts related t o these objective barriers, there are

attitude-related barriers that can disrupt a W M audit program. A commonly held

at t i tude i s "If it ain't broke, don't f i x it!" This att i tude stems f rom the desire t o

maintain the status quo and avoid the unknown. It is also based on the fear tha t a new

W M option may not work as advertised. Without the commitment t o carefully

conceive and implement the option, this att i tude can become a self-fulf i l l ing

prophecy.

Another attitude-related barrier i s the feeling that "it won't work.'' This response i s

o f ten given when a person does not fu l ly understand the nature of a proposed waste

minimization option and i t s impact on operations. The danger here i s that promising

options may be dropped before they can be evaluated. The brainstorming process for

generating WM options (described in Section 7) i s organized t o l imi t interference by

these attitudes. The W M audit procedure is designed so tha t a large number of options

are proposed, and then each option i s evaluated upon i t s merits afterword.

A n often-encountered barrier i s the fear tha t the W M option w i l l deteriorate the

product quality. This is part icularly prevalent in situations where unprocessed feed

materials are recovered from the waste and then recycled back t o the process. The

deterioration o f product quality can be a valid concern if unacceptable concentrations

o f waste materials build up in the recycle loop. The best way t o quell this belief is t o

set up a small-scale demonstration in the facil i ty, or t o observe the particular option

in operation at another faci l i ty.

Table 3-5. EXAMPLES OF BARRIERS TO WASTE MINIMIZATION

Potential Con flict or Barrier

Production

s

Facilit ies/Mai ntenance .. I; s- - . .. - - _-r- .

~ -. d

Quality Control

Inventory

Finance

Purchasing

Environmental

A new operating procedure will reduce waste but may also be a bottleneck that decreases the overall production rate.

Production will be stopped while the new process equipment is installed.

similar service. It may not work here.

Adequate space is not availabl equipment.

Adequate utilities are not available for the new equipment.

&,a .&*-. -2uy, ' )k Nj-oe, Tb yh*f*uh& A\ P&kLiW-Li M LL

o i x w

d' 4.r. $ l h c n . J T-""C A new piece of equipment 3 as not been demonstrated in a d'

r r y c-c LLJL.

/- --.

Engineering or construction manpower will not be available in time to meet the project schedule.

Extensive maintenance may be required.

More intensive QC may be needed. !

i, More rework may not be required.

A program to reduce inventory (to avoid product deterioration and reprocessing) may lead to stockouts during high customer demand.

There is not enough money to fund the project.

I replacement of a hazardous raw material with a non-hazardous substitute. I

I I 1

i, Existing stocks (or binding contracts) will delay the , \

Installation of solvent recovery equipment will be delayed in order to get air pollution control permits.

c s e of a new non-hazardous raw material will adversely 1 impact the wastewater treatment facility. Waste Treatment

i

__ ~~ ___ __- Commitment throughout an organization i s necessary in order t o resolve confl icts and

t o remove barriers t o the WM audit program. Commitment and direction f rom top

management are essential t o the success of the program, along w i th employee

n '-1

cooperation and participation. Bonuses, awards, plaques, and other forms o f

recognition are of ten used t o provide motivation. In some companies, meeting waste

reduction goals are used as one measure of employee performance.

Any WM audit program needs one or more people t o champion the cause. These "cause

champions" overcome the iner t ia present when changes t o an existing operation are

proposed. They also lead the WM audit program, either formally or informally.

Although an. environmental engineer, production manager, or plant process engineer

are good candidates, the interplay of personalities between the program members w i l l

usually determine who takes on th is role.

7 I 1 :-I 3

Table 3-6. DESIRABLE AllRlBUTES OF A W M AUDIT P R a A M CHAMPION "I

0 Fami l iar i ty w i th the companyls production departments including: - Faci l i t ies - Processes - People Fami l iar i ty w i t h the companyls waste management operations. Fami l iar i ty w i th new production and waste treatment technologies. Fami l iar i ty w i th WM principles and techniques. Aggressive managerial style. Understanding o f environmental regulations. Understanding o f product quality control requirements. Ab i l i t y t o communicate and interact wel l w i th people. Good rapport w i th top management.

I f the champion i s lacking in the t ra i ts shown in Table 3-6, then he or she must re ly

more heavily on other members of the WM audit program team.

Table 3-7 summarizes the important steps in planning and organizing the WM audit

program.

20

Table 3-7. WASTE MINIMIZATION AUDIT PROGRAM PLANNING AND ORGANIZATION ACTIVITIES SUMMARY

SETTING UP THE PROGRAM Get Top Management Commitment to:

- Establish WM as a corporate goal - Establish a WM Audit Program to meet this goal - Give authority to the WM Audit Program Task Force to implement this program

Set Goals These goals should be: - ACCEPTABLE to those who will work to achieve them I FLEXIBLE to adapt to changing requirement8 I MEASURABLE over time

- SUITABLE to the overall corporate goals I MOTIVATIONAL

- UNDERSTANDABLE I ACHIEVABLE

STAFFING

. Get Get

THE PROGRAM TASK FORCE

people who know the facllity, processes, and procedures people from affected departments or groups I

I

I

I - . I

I

I

I

Production Facilities/Maintenance Process Engineering Quality Control Environmental Staff Safety Staff Purchasing Material Control/lnventory Legal Staff Finance information Systems

Find a "cause champion", with the following attributes: - Familiar with the facility, its production processes, and its waste management operations - Familiar with the people - Familiar with quality control requirements - Good rapport with management - Familiar with new production and waste management technology - Familiar with WM principles and techniques - Familiar with environmental regulations

I Aggressive managerial style

GET COMPANY-WIDE COMMITMENT

Incorporate the company's WM goals into departmental goals Solicit employee cooperation and participation Develop incentives and/or awards for managers and employees

21

SECTION 4 W M AUOIT PREPARATION A N 3 INFORMATION GATHERING

The objective of this phase i s t o gain background information regarding the fac i l i t y t o

be studied, and t o decide on the focus for the review t o follow. Preparation for the

audit should include an examination of information sources related t o the processes,

operations, and waste management practices at the facil i ty. While audit preparation

can take many forms depending on the situation at hand, it typical ly involves the steps

shown in Table 4-1. +hll #!s L’I4cu.A-k a O-A nw-cRu 7 IX pd (0- l c 1 8 L 1

These steps are described in the following sections.

Table 4-1. W M AUOIT PREPARATION STEPS

o Ide t i f y and t rack waste streams

- Collect waste stream da a

- Develop mater ia l balances

- € s w ‘ - A 4””””

o Collect and compile data

- Design information (processes and equipment)

- Environmental information

- Raw mater ia l and production information

- Other information

o Select waste streams or process areas t o audit

WASTE STREAM IDENTIFICATION AND TRACKING

One of the first tasks o f a waste minimization audit program is t o identi fy and

characterize the facility’s waste streams. Indeed, this step is an important one for the

purpose of establishing goals for the programs. Information about waste streams can

come f rom a variety of sources.

22

Some information on waste quantities i s readily available f rom the completed

hazardous waste manifests, which include the description and quantity of hazardous

waste shipped t o a TSDF. The to ta l amount of hazardous waste shipped during a one

year period, fo r example, is a convenient means of measuring waste generation and

waste reduction efforts. Much of a company's disposal costs are based d i rect ly on this

measure. However, manifests of ten lack such information as waste analysis, source of

the waste, and the t ime period during which the waste was generated. Also, the

manifests do not cover wastewater effluents, air emissions, or non-hazardous solid

wastes.

Material Balances

Mater ia l balances should be developed t o bet ter understand the facil i ty's waste

situation. In i t s simplest form, the mater ia l balance is represented by the mass

conser vat i on principle: Lk.LL,,MG LR/y\

u[ Fu&J

01 '

SLWL irjh LhCC-. a +-'-n

,-

Mater ia l in = Material out + Material accumulated L W . C . ~ ~ ~ ph"'

The quantities are best expressed on a mass basis. The material balances should be

made individually for a l l of the components that enter and leave the process When

chemical reactions take place in a system, there is often an advantage t o doing

"elemental balances" for specific chemical elements in a system. Figure 4-1 i s a

sample mater ia l balance fo r a process that recovers copper meta l f rom copper sulfate

solution by concentration w i t h aluminum shavings.

To characterize waste streams by material balance can require considerable effort.

However, b y doing so, a more complete picture of the waste situation results. This

helps t o establish the focus of the W M activi t ies and provides a baseline fo r measuring

performance. Also, an accurate material balance can also be used t o determine

fugit ive emissions, such as evaporation of solvent f rom a parts cleaning tank.

23

I

M0l.W. kmoUh kglh kmolh kg/h

Solutlon Flows

cuso, 159.6 0.13 20.7

H,SO, 98.1 0.1 4 13.7

AI,( SO,), 342.3 0 0

H,O 18.0 65.3 1,175

Solld Flows cu 63.5

AI 27.0 0.15 4.1

TOTAL 65.57 1,209.4 0.15 4.1

I

kmoUh k g h kmolh kgh

0.01 1.6

0.14 13.7

0.04 13.7

65.3 1,175

0.12 7.6

0.07 1.9

65.49 1204.0 0.19 9.5

Figure 4-1. Material Balance Copper Cementation Tank

(to metal reclaimer)

i J 1 Copper

13 Sulfate

S a " of Material Balance Informatian

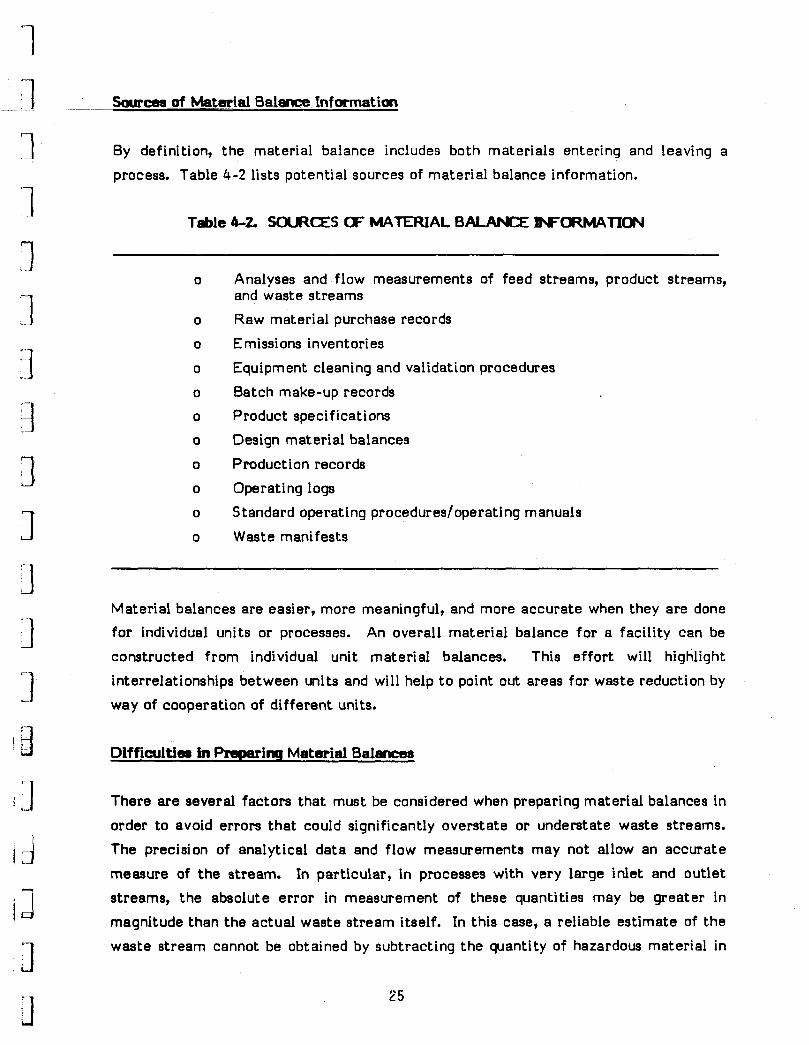

By definition, t h e material balance includes both mater ia l s entering and leaving a

process. Table 4-2 lists potential sources of material balance information.

Table 4-2. S o U i C E S OF MATERIAL BALANCE aFORMAlIoN

0

0

0

0

0

0

0

0

0

0

0

Analyses and flow measurements of feed streams, product streams, and waste s t reams Raw material purchase records E missions inventories Equipment cleaning and validation procedures Batch make-up records Product spe ci f icat i ons Design material balances Production records Operating logs Standard operating pr ocedur es/operat i ng manuals Waste manifests

Material balances are easier, more meaningful, and more accu ra t e when t h e y are done for individual units or processes. An overall material balance fo r a facility can be constructed f rom individual unit material interrelationships between units and will help way of cooperation of different units.

balances. This e f for t will highlight t o point out areas for waste reduction by

Difficultim in f%par inq Material Balrrnces

There are several fac tors tha t must be considered when preparing mater ia l balances in order t o avoid errors t h a t could significantly overs ta te or understate waste streams. The precision of analytical d a t a and flow measurements may not allow an accurate measure of t h e stream. In particular, in processes with very large inlet and out le t streams, t h e absolute e r ror in measurement of these quantities may be grea te r in magnitude than t h e actual was te s t r eam itself. In this case, a reliable es t imate of t he

was te s t ream cannot be obtained by subtracting t h e quantity of hazardous material in

25

I - 1 _ _

n I 1 7

-tbepmduct f rom that in the feed. Generally, subtraction of two large numbers t o

obtain a small number yields erroneous results.

In calculating material balances, it is necessary t o know how much material enters the

process. Raw mater ia l purchasing records can be used t o provide this data, if more

direct measures are not available. However, using purchasing data fo r feed streams

entails some of the same problems tha t using manifest data f o r waste streams. The

main problem is that purchasing quantities and ordering frequencies do not necessarily

correspond t o production rates. This can lead t o large errors in the calculation of

waste stream flows and compositions. For example, raw materials may be ordered

quarterly in large volumes or perhaps when prices are low.

It i s crucial to consider the t ime span when constructing a material balance. Mater ia l

balances constructed over a shorter t ime span require more accurate and more

frequent stream monitoring in order t o obtain a good balance. Mater ia l balances done

over the duration of a production campaign are typical ly the easiest t o perform and

are reasonably accurate.

Developing material balances around complex processes can be a complicated

undertaking especially if recycle streams are present. Such tasks are usually

performed by chemical engineers, o f ten w i th the assistance of computerized process

sim u l at om.

Measuring waste mass flows and compositions i s something that should not be done

only once. Indeed, waste reduction cannot be meaningfully measured unless the

information is collected both before and a f te r a waste minimization audit program is

implemented. Fortunately, i t i s easier t o do mater ia l balances the second time, and

gets even easier as more are done because of the "learning curve" effect. In some

companies, computerized database systems have been used t o track wastes. Section 7 discusses the importance o f periodic measurement of waste generation and reduction

as par t of the implementation of a WM audit program.

26

I

Table 4-3. FACILITY INFORMATION FOR WASTE MINIMIZATION AUDITS 1

I 1 ~ - -~

DESIGN INFORMATION Process flow diagrams Material and heat balances (both design balances and actual balances) for 1

1 CI

production processes pollution control processes

Operating manuals and process descriptions Equipment lists Equipment specifications and data sheets Piping and instrument diagrams Plot and elevation plans General arrangement diagrams and work flow diagrams

i ENVIRONMENTAL INFORMATION Hazardous waste manifests Emission inventories Biennial hazardous waste reports Waste assays Environmeatal audit reports

L 7 * Permits and/or permit applications

‘I 1

RAW MATERIALPRODUCTION INFORMATION ’

Product composition and batch sheets Material application diagrams Material safety data sheets Product and raw material inventory records Operator data logs Production schedules

3: 3 3

OTHER INFORMATION Company environmental policy statements 3 Organization charts

IJ

27

-1 I

~ ~ f33ttECTTBtK: A N 3 COWLING DATA

' 1 This step involves a compilation and review of information regarding the process or area t o be audited. Table 4-3 l ists information that can be useful in preparing for the

audit. A review o f this information w i l l provide important background fo r

understanding the facility's waste situation and should result in a well-defined

information needs l i s t or inspection agenda designed t o f i l l in the gaps. Comments of

1 J

operators found in the i r logs can be among the most useful data fo r identi fying

problems and possible solutions. 1 WASTE STREAM SELECTION 1 Because th is step establishes the focus of the entire audit activity, selecting a waste

stream fo r the audit requires a great deal of care. Table 4-4 l ists important cr i ter ia

t o consider when selecting which waste stream(s) t o audit. ' 1

Table 44. TYPICAL CONSIDERAT'IONS FOR SELEClNG WASTE STREAMS TO AUDIT

o Disposal cost of the waste

1 I I

J : I i

I-; 1 .I I-)

o Quantity o f the waste

o

o

o Hazardous nature o f the waste (toxicity, f lammability, reactivity,

o

o

o

Potential for (or ease of) minimization and/or recycling

Compliance w i th current and fu ture environmental regulations

corrosivity)

Potential for removing production or waste treatment bottlenecks

Other undesirable characteristics of waste (e.g., strong odors, potential degradation t o toxic compounds, etc.)

Available budget fo r waste minimization program and projects c v&q*** h & d

1

One or more of the above considerations can be the driving force behind the selection

o f a particular waste stream t o audit. A wr i t ten summary i s prepared a f te r the

selection of waste streams, and should include the following items:

28

0 - ~-

0

0

0

Facility description

Description of the process operations of concern, including diagrams necessary t o pinpoint pertinent waste generation aspects of the process.

Description of t h e was te s t r eams concentrating on waste sources, current methods of management, generation rates, composition, disposal costs, and raw material costs.

Rationale for was te s t r eam selection.

The result of a proper review preparation should be a well-defined needs list and inspection agenda t o be used during t h e ac tua l review. The needs l ist can be presented in t h e form of a checklist detailing objectives, questions and issues to be resolved, and fur ther information required. The needs list should be given to the appropriate people before t h e ac tua l site visit t o allow them t o assemble materials and information for t h e review t eam in advance. Of course, it may be t h a t t he members of the review t e a m are in the best position t o collect and compile much of this data. Af te r this is accomplished, t h e review can begin.

29

:1 SECTION 5

WASTE MINIMIZATION AUOrr 1 The objectives of the waste minimization audit include:

o generation of a comprehensive set of WM options for a specific waste stream or waste source of concern;

o prel iminary evaluation and screening of identi f ied options t o select those that

deserve additional, more detailed analysis.

The audit itself, as defined here, must be targeted on a specific waste stream or waste

source. Selection of a waste-stream for the audit was described in the previous

section. For example, consider the case of minimizing sludge produced in a ref inery

API separator unit. The API separator i s used t o separate water f rom an oi ly sludge

composed o f oi ly solids and emulsions. These can originate through cleaning o f heat

exchanger bundles, area washdowns, tank cleaning, and slop o i l emptying f rom knock-

out drums and other sources. The audit team w i l l identi fy these sources and examine

WM options related t o each source selected for analysis.

J R

Sometimes it i s beneficial t o look a t an entire operation rather than a waste stream.

For instance, consider a task involving minimizing solvent wastes produced by

numerous cold cleaning tanks located in a large a i rcraf t repair and maintenance

facility. There are three di f ferent types of wastes: spent d i r ty solvent, tank

evaporation losses and losses due t o solvent dragout. It is not ef fect ive t o focus just

on one of those wastes when analyzing a simple unit such as cleaning tanks; therefore,

a l l three types of wastes are considered. Also, basic source reduction techniques

related t o a simple cold cleaning operation do not vary f rom one tank t o another. As

a result, it is not necessary t o address each tank or cleaning stat ion individually fo r

the purpose of generating WM options. Instead, a general checklist containing WM

options i s prepared and then applied t o each station. (Appendix A contains a set of

worksheets that have been designed t o fac i l i ta te a WM audit.) Whether the focus is a

specific waste stream or a waste source, such focus must be f i rm ly in place before the

commencement of the audit .

30

--.

1-1 1-1

SlTE AN) PROCESS INSPECTION

The previous activi t ies have provided a general understanding of the faci l i ty 's

processes and wastes characteristics. Also, the focus of the audit was established in

the fo rm of a target waste stream or waste source. The audit inspection can now be

conducted. I t s governing objective is t o develop a full understandinq o f a l l causes of

waste generation, and t o examine i tems missed in previous activities.

The fac i l i t y inspection i s the u l t imate step in the information gathering process,

Typically, the inspection focuses on select aspects of the operation ident i f ied in the

preceding phase. The inspection guidelines for the audit team are presented in Table

5-1. Table 5-2 i s a sample agenda of a site inspection.

The audit team should "walk the line" f rom the suspected source of waste generation

t o the point of exit, be it a treatment unit, storage facil i ty, or haulage t o off-si te

disposal facilities. This inspection often results in forming suspicions about the causes

o f waste generation. Full resolution of these suspicions may require additional data

collection, analysis and site visits.

GEIERATION OF W M OPTIONS

Once an understanding of waste generation origins or causes has been achieved, the

audit process enters creative phase. The objective of this step is to generate a

comprehensive set of WM options fo r further consideration by the audit team. During

the review of fac i l i t y data and following the site inspection, some potential W M

options w i l l become apparent. However, t o develop a comprehensive l i s t of potential

options, it is helpful t o have a background knowledge of WM techniques tha t have been

used elsewhere. Table 5-3 l i s ts various sources of background information.

Options generation should fol low a hierarchy in which source reduction i s explored

e f fo r t stems f rom the environmental desirabil ity of source reduction over other

methods. Treatment should be considered only as a last resort. In the option

generation process, the proponents provide a l ist ing of ideas which includes br ie f

descriptions of the rationales fo r their selection, backed by l i terature references or wv discussions w i th equipment or mater ia l vendors, or consultants. Appendix B l ists W M

techniques fo r several commonly encountered waste-intensive operations.

first, followed by recycling, and then by t reatment approaches. Such a hierarchy o f

w 31

Table 5-1. GUIDELUES FOR SITE AN3 PROCESS INSPECTION

0

0

0

0

0

0

0

0

Prepare an agenda i n advance that covers a l l points that s t i l l require clarification. Provide staff contacts at the fac i l i t y w i th the agenda several days before the inspection. A sample agenda i s depicted in Table 5-2.

Schedule the inspection to coincide w i th the particular operation that is of interest, (e.g., make-up chemical addition, bath sampling, bath replacement, e tc.).

Monitor the operation at dif ferent times during the shift, and, i f needed, during a l l 3 shifts, especially when waste generation is highly dependent on human involvement (for example, in painting or parts cleaning operations).

Interview operators, sh i f t supervisors, and foremen directly. Do not hesitate t o question more than one person if an answer is no t forthcoming. Assess the operators' and their supervisors' awareness of waste generation aspects of the operation. Note the i r famil iar i ty (or the lack thereof) wi th the impacts their operation may have on other operations.

Photograph the facil i ty. Photographs are especially valuable in the absence of plan layout drawings. Many details can be captured i n photographs that otherwise could be forgotten or inaccurately recalled at a la ter date.

Observe the "housekeeping" aspect of the operation. Check fo r signs of spills or leaks. Ask t o visit the maintenance shop and inquire about their problems in maintaining the equipment leak-free. Assess the overall cleanliness and order of the site.

Assess the organizational structure and level of coordination o f environ- mental act ivi t ies between various departments.

Assess administrative controls, such as cost accounting procedures, mater ia l purchasing procedures, and waste collection procedures.

Methock for Generating Op ti0m

Option generation should occur in an environment that encourages creat iv i ty and

formulation of independent ideas by dif ferent members of the auditing team. Two

methods that are particularly e f fect ive in accomplishing th is are the "nominal group

technique" and Table 5-4 describes the methods, along w i th

advantages and disadvantages.

32

Table 52. AGENDA FOR A WASTE MlNlMlZATlON AUDIT IN A WEB OFFSET PRINTING FACILITY

A. Introduction.

8. Description of the waste minimization audit.

C. Discussion of general information. Facility size. Staffingem ployees. Products.

D. Discussion of printing operations. Photoprocessing .

Printing. Sheeting, folding, trimming, packaging.

Film processing. Plate processing.

E. Discussion of input materials and wastes. Input materials.

Photoprocessing chemicals and materials. Aluminum plates. Paper. Inks. Fountain solutions. Clean-up chemicals.

Waste materials. Waste developing solutions. Waste inks. Waste paper. Waste oils. Vapor emissions. Wastewater. Trash.

F. Discussion of maintenance operations.

G. Walk through the facility.

H. Discussion of possible causes of high waste flows.

1. Concluding remarks and additional information needs.

33

Table 5-3. SOURCES OF BACKGROUND INFORMATION ON WM OPTIONS

Published literature

State environmental agencies

Equipment vendors

Consultants

Plant engineers and operators

Technical magazines, particularly industry trade journals, have articles describing specific WM techniques. These articles tend to be quite practical in nature.

The following states have, or are developing, programs that include technical assistance, information on industry-specific waste minimization techniques, and co m pi led bibliographies.

California Connecticut Georgia Illinois Ke n t uc k y Maryland Massachusetts Minnesota New Jersey New York North Carolina Pennsylvania Ten n essee

Appendix C provides a list of addresses for state and federal programs for WM assistance.

Meetings with equipment vendors, as well as vendor literature, is particularly useful in identifying potential equipment-oriented options. Vendors are eager to assist companies in implementing projects. Remember, though, that the vendor's job is to sell his company's equipment.

Consultants can provide information about waste minimization techniques. Section 3 discusses the use of consultants in WM programs.

The employees that are intimately familiar with a facility's operations can often make significant practical suggestions.

34

Table 5-4. GROUP CREATIVITY TECHNIQUES BRAINSTORMING VERSUS NOMINAL GROUP TECHNIQUE ~ -1

1 '

Coordinator 1 par t i c i pan t 6

I - POCEDURE

1 '--I

i

ADVANTAGES

DISADVANTAGES

BRAINSTORMING

Face-to-face interaction between participants.

Before the meeting, the participants review the background information and the requirements of the project. One participant serves as the leader. Another serves as the recorder. The meeting starts with a description of the project as a problem in need of a solution. The participants propose solutions to the problem. The participants are not allowed to critique the proposed solutions, but are encouraged to build and expand on earlier responses. All responses are recorded for later review and evaluation.

The free association process stimulates creative thinking. One person's ideas stimulate others. A large number of ideas are generated.

Little thought goes into many of the ideas that are developed during the meeting. Many of the ideas generated are not practical. (This is not true, necessarily, of ideas generated by participants while reviewing information prior to the meeting.)

NOMINAL GROUP TECHNIQUE

Face-to-face interaction organized by a coordinator.

The participants are brought together for the meeting, without reviewing the problem beforehand.

The coordinator describes the problem and asks each participant to review it.

The participants individually write down as many possible solutions as they can they can think of. The participants then, one by one, read one of their responses, going around the table as often as necessary to read all of the responses. After all of the ideas have been read, the ideas are discussed individually. Duplicate responses are eliminated.

Finally, the participants individually prioritize the ideas. The results are totalled (based on "one participant, one vote") to arrive at the group consensus.

More thought goes into the responses. The responses tend to be more practical. The meeting also results in a prelimin- ary screening.

This procedure is less likely to "stumble onto" a truly innovative new idea.

35

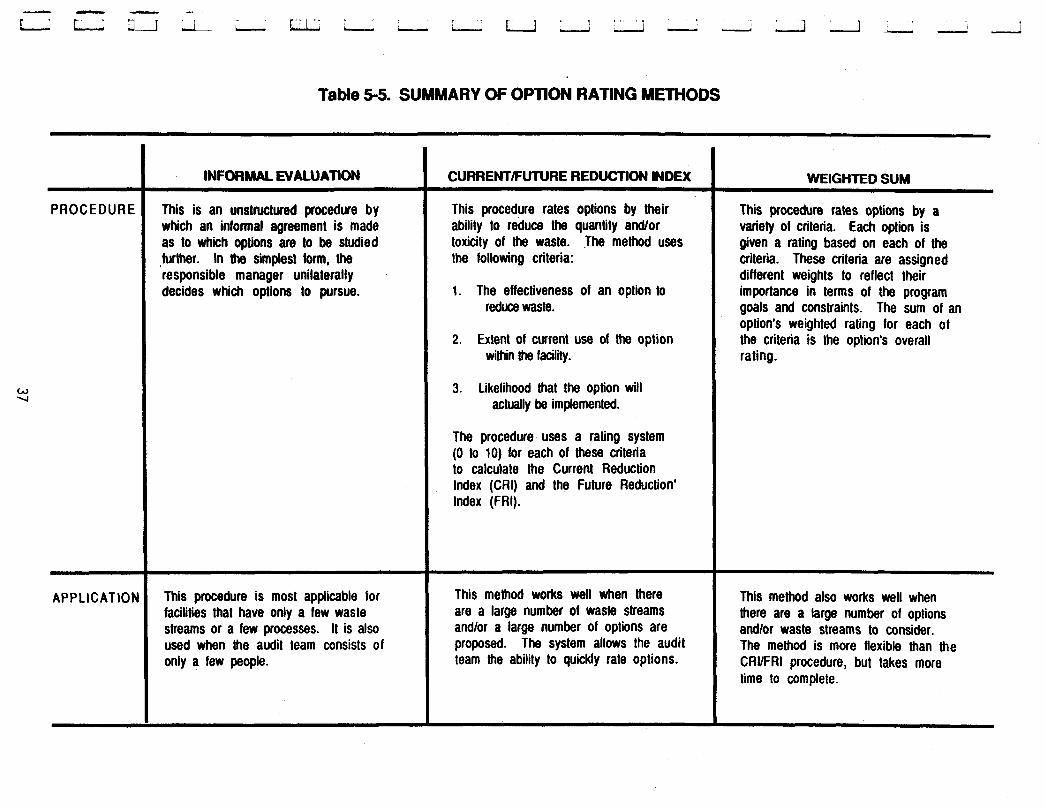

Since detailed evaluation of economic and technical feasibil i ty i s usually costly, W M

options that were generated in the previous step may need t o be screened t o identify

those that deserve further evaluation. A variety o f methodologies exist f o r evaluating

the options. Three methods (informal evaluation, CRI/FRI method and weighted sum

method) are compared in Table 5-5. Tables 5-6, 5-7, and 5-8 describe each o f the

methods in more detail.

SELECTION OF MOST PROMISING OPTIONS FOR MORE OETAlLED EVALUATION

The above rat ing systems are, in essence, ac t i v i t y management tools fo r evaluation.

Their main advantages are that they 1) compel the audit members t o consider a wide

range of cr i ter ia before making decisions; and 2) provide a framework for resolving

differences concerning specific options. These systems should not be confused w i th

the more detailed feasibil i ty analyses, which are described in the next section.

The results of the options evaluation ac t iv i t y are used as the basis fo r choosing

options fo r more detailed analysis (i.e., technical and feasibil i ty analyses). The higher

the ranking that an option has received, the more at t ract ive it is as a candidate for

additional consideration. Options should be chosen in a joint meeting of external

auditors and in-house participants. The number of options chosen for feasibil i ty

analysis depends on the time, budget and resources available fo r such a study.

It is important t o note that some options may be considered worthy of immediate

implementation without further study. Typically, such options involve application of

good operating practices (e.g., closer supervision, keeping covers on degreasers, or training of paint spray booth operators) which require l i t t l e or no capital expenditure.

36

Table 5.5. SUMMARY OF OPTION RATING METHODS

PROCEDURE

w v

APP LIC AT IO!'

INFORMAL EVALUATION

This is an unstructured procedure by which an informal agreement is made as to which options are to be studied ,further. In the simples1 form, the responsible manager unilaterally decides which options to pursue.

~~~

This procedure is most applicable for facilities that have only a few waste streams or a few processes. It is also used when the audit team consists of only a few people.

CURRENTFUTURE REDUCTION INDEX ~ --

This procedure rates options by their ability to reduce the quantity andlor toxicity of the waste. The method uses the following criteria:

1. The effectiveness of an option to reduce waste.

2. Extent of current use of the option within the facility.

3. Likelihood that the option will actually be implemented.

The procedure uses a rating system (0 to 10) for each of these criteria to calculate the Current Reduction Index (CRI) and the Future Reduction' Index (FRI).

This method works well when there are a large number of waste streams and/or a large number of options are proposed. The system allows the audit team the ability to quickly rate options.

WEIGHTED SUM

This procedure rates options by a variety of criteria. Each option is given a rating based on each of the criteria. These criteria are assigned different weights to reflect their importance in terms of the program goals and constraints. The sum of an option's weighted rating for each of the criteria is the option's overall rating.

~

This method also works well when there are a large number of options andlor waste streams to consider. The method is more flexible than the CRUFRI procedure, but takes more time to complete.

1 :1

n .1 :1 1 L ..

3 3

Table 5-6. OPTION RATING INFORMAL EVALUATION

......................................................... This method is useful in small facilities, with small management groups, or in situations in which only a few options have been generated. The method consists of informal discussion and examination of each option. At the extreme, the WM audit program leader decides unilaterally which projects to pursue. Useful questions to consider for include the following:

Does the necessary technology exist to develop the option?

How much does it cost? Is it cost effective?

Can the option be implemented within a reasonable amount of time?

Does the option have a good "track record"? If not, is there convincing evidence that the option will work as required?

What other benefits will occur?

1.1

38

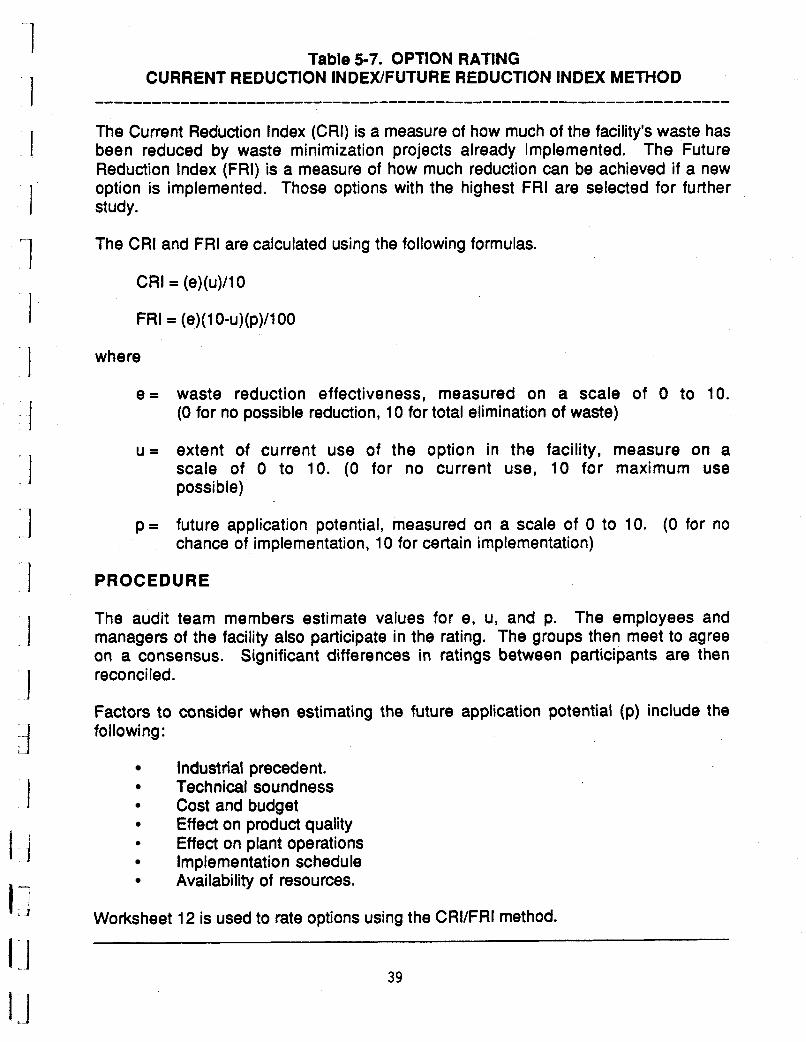

Table 5-7. OPTION RATING CURRENT REDUCTION INDUVFUTURE REDUCTION INDEX METHOD

The Current Reduction Index (CRI) is a measure of how much of the facility's waste has been reduced by waste minimization projects already implemented. The Future Reduction Index (FRI) is a measure of how much reduction can be achieved if a new option is implemented. Those options with the highest FRI are selected for further study.

The CRI and FRI are calculated using the following formulas.

CRI = (e)(~)/lO

FRI = (e)( 1 O-U)(p)/lOO

where

e = waste reduction effectiveness, measured on a scale of 0 to 10. (0 for no possible reduction, 10 for total elimination of waste)

u = extent of current use of the option in the facility, measure on a scale of 0 to 10. (0 for no current use, 10 for maximum use possible)

p = future application potential, measured on a scale of 0 to 10. (0 for no chance of implementation, 10 for certain implementation)

PROCEDURE

The audit team members estimate values for e, u, and p. The employees and managers of the facility also participate in the rating. The groups then meet to agree on a consensus. Significant differences in ratings between participants are then reconciled.

Factors to consider when estimating the future application potential (p) include the following:

Industrial precedent. Technical soundness Cost and budget Effect on product quality

4 Effect on plant operations Implementation schedule Availability of resources.

Worksheet 12 is used to rate options using the CRVFRI method.

39

n '1 1 1 -- I 1 :I 1 3 3 1 1 1

II 4 a I 1

Table 5-8. OPTION RATING WEIGHTED SUM METHOD

The Weighted Sum method evaluates each option in a more flexible manner than the CRVFRI method. This method involves three steps.

1.

2.

3.

Determine what the important criteria are in terms of the WM audit program goals and constraints, and the overall corporate goals and constraints. Examples of criteria are the following:

0

0

0

0

0

0

0

0

0

0

0

0

Reduction in waste quantity Reduction in waste hazard (e.g., toxicity, flammability,

reactivity, corrosivity, concentration, etc.) Reduction in waste treatmenVdisposa1 costs Reduction in raw material costs Reduction in liability and insurance costs Previous successful use within the company Previous successful use in industry Not detrimental to product quality Low capital cost Low operating and maintenance costs Short implementation period (and minimal disruption of

plant operations Ease of implementation

The weights (on a scale of 0 to 10, for example) are assigned to the criteria in relation to their importance. For example, if reduction in waste treatment and disposal costs are very important, while previous successful use within the company is of minor importance, then the reduction in waste costs is given a weight of 10 and the previous use within the company is given a weight of 1 or 2. Criteria that are not important are not included (or given a weight of 0).

Each option is then rated on each of the criteria. Again, a scale of 0 to 10 can be used (0 for low and 10 for high).

Finally, the rating of each option from particular criteria is multiplied by the weight of the criteria. An option's overall rating is then sum of the products of rating times the weight of the criteria, for all of the criteria.

The options with the best overall ratings are then selected for the technical and economic feasibility analyses. Worksheet 13 is used to rate options using the Weighted Sum method.

......................................................... 40

SECTION 6

FEAsH3ILlTY ANALYSIS

The f inal product of a waste minimization audit i s a l i s t o f promising WM options for a

facil i ty. The audit w i l l have screened out infeasible or unattractive options. The next

step i s to determine if the remaining options are feasible. The options are evaluated

on both a technical and an economic basis.

TECHNICAL EVALUATION

The technical evaluation determines whether a particular W M option w i l l work in a

specific application. For equipment-related options or process changes, visits t o see

existing installations are very desirable. Information on existing installations can be

obtained through equipment vendors and industry contacts. The ooerator's comments

are especially important and should be compared w i t h the vendor's claims. Bench

scale or pilot-scale demonstration i s often necessary. Of ten it is possible t o obtain

scale-up data using a rental test unit fo r bench-scale or pilot-scale experiments. Some

vendors w i l l instal l equipment on a t r i a l basis, wi th acceptance and payment after a

prescribed time, if the user is satisfied.

The technical evaluation o f an option also must consider fac i l i ty constraints and

product requirements, such as those described in Table 6-1.

Table 6-1 TYPICAL TECHNICAL EVALUATION CRITERIA

0

0

I s space available?

Are ut i l i t ies available? Or must these be installed, thereby raising capital costs?

Is the new equipment or technique compatible w i th production operating procedures, work flow, and production rates?

W i l l product qual i ty be maintained?

How long w i l l production be stopped in order t o install the system?

Is special expertise required t o operate or maintain the new system? Does the vendor provide acceptable service?

Does the system create other environmental problems?

I s the system safe?

41

Although an inabi l i ty t o meet these constraints may not present insurmountable

problems, correcting them w i l l likely add t o the capital and/or operating costs.

All affected groups in the fac i l i ty should contribute t o and review the results of the

technical evaluation. Pr ior consultation and review wi th the affected qroups (e.g.,

production, maintenance, purchasing), i s needed t o ensure the viabil ity and acceptance

of an option. I f the option calls fo r a change in production methods, the project’s

effects on the quality o f the f ina l product must be determined. If a f ter the technical

evaluation, the project appears infeasible or impractical, it should be dropped.

ECONOMlC EVALUATION

The economic evaluation i s carried out using standard measures of prof i tabi l i ty, such

as payback period, re turn on investment, and net present value. Each company has i t s

own economic cr i ter ia fo r selecting projects for implementation. In performing the

economic evaluation, various costs and savings must be considered. As in any project,

the cost elements of a WM project can be broken down in to capital costs and operating

costs.

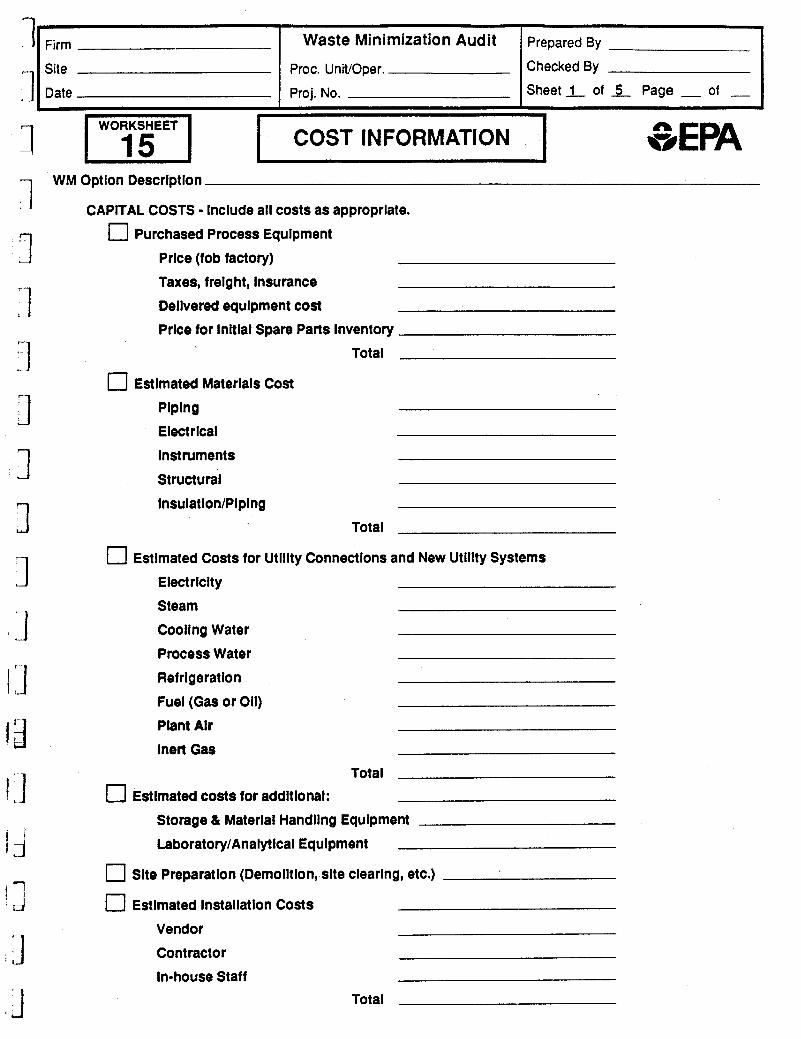

Capital Costs

Table 6-2 l ists capital cost i tems typically associated w i t h the largest waste

minimization projects. These costs include not only the f ixed capital costs for designing, purchasing, and install ing equipment, but also costs fo r working capital,

permitting, training, start-up, and financing charges. Table 6-2 includes a number of

cost i tems that normally would not be required for many W M projects. For example,

new u t i l i t y systems are usually not required fo r WM projects, although connections t o

existing u t i l i t y systems may be required. Some WM options, especially those involving

operational or housekeeping changes, w i l l have no significant capital costs.

Wi th the increasing level of environmental regulations, in i t ia l permi t t ing costs are

becoming a significant port ion of capital costs fo r many recycling options (as wel l as

treatment, storage, and disposal options). Most source reduction techniques have the

advantage o f not requiring environmental permitt ing in order to be implemented.

42

-1 ' 1 .-I

1 :1 7

' I ' J 11 *

3 I J -1 . I 3 1

1 - 1 11 I IJ 1.1

Table 6-2. CAPITAL INVESTMENT FOR A TYPICAL LARGE WM PROJECT

Direct Capital Costs Site Development

Demolition and alteration work Site clearing and grading Walkways Fencing

Process Equipment All equipment listed on flow sheets Spare parts Taxes, freight, insurance, and duties

Piping and ducting (including valves, fittings, and hangers) Insulation and painting Electrical (including wiring, conduits, panels, switches, motors) Instrumentation and controls Buildings and structures (including foundations, structures, supports, cranes,

ladders, and platforms) Note - This includes concrete and structural steel.

Process water, cooling water, and wastewater connections Heating, ventilation, air conditioning, and dust collection Electric power Steam Refrigeration Fuels Plant air and inert gas Lighting Fire control

Materials

Connections to Existing Building Utilities and Services

New Utility and Service Facilities Storage and Handling Equipment Laboratory Equipment Other Non-Process Equipment Construct ion/lnstallation

Construction/lnstallation labor salaries and burden Safety, medical, and fringe benefits Supervision, accounting, timekeeping, purchasing, and expediting Temporary facilities Construction tools and equipment Taxes and insurance Buiiding permits, field tests, licenses

Indirect Capital Costs In-house Engineering, Procurement, and other Home Office Costs Outside Engineering, Design, and Consulting Services Permitting Costs Contractors' Fees Training Costa Start-up Costs Initial Charge of Catalysts and Chemicals Contingency Interest Accrued during Construction

TOTAL FIXED CAPITAL COSTS

Working Capital Raw Materials Inventory . Finished Product Inventory Materials and Supplies

Total Working Capital TOTAL CAPITAL INVESTMENT

Source: Adapted from Perry, $hem ical Fna ineer's H W (1 985); and Peters and Timmerhaus, Des ian and EEonomics for c hemical Fna ineers (1 980).

43

Operating Costs and Savinqs

I-II

.1

The basic economic goal of waste minimization projects i s to reduce (or eliminate)

waste disposal costs and to reduce input material costs. However, a variety of other

operating costs (and savings) should also be considered. In making the economic

evaluation, it i s convenient to use incremental operating costs in comparing the

existing system wi th the new system incorporating the waste minimization option.

('"Incremental operating costs" represent the difference between the estimated

operating costs associated w i th the WM option and the actual operating costs of the

existing system, without the option.) Table 6-3 describes incremental operating costs

and savings and incremental revenues typically associated w i t h waste minimization

projects.

Operating costs associated w i th hazardous waste treatment, storage, and disposal are

major elements of WM project economic evaluation. Companies have tended t o ignore

these costs in the past,@&kii Recent regulatory requirements imposed on generators

and waste management faci l i t ies have caused waste management costs t o increase t o

the point where waste management i s becoming a significant factor in a company's

overall operating cost structure. Table 6-4 presents typ ica l costs fo r waste treatment

and disposal.

A

For the purpose o f evaluating a project to reduce waste quantities, some types of costs

are larger and more easily quantified. These include disposal fees, transportation

costs, predisposal treatment costs, raw materials costs, and operation and