the explosive growth opportunity in china's automotive aftermarket

TRANSCRIPT

TheExplosiveGrowthOpportunityinChina’sAutomotiveAftermarket

BillRussoRobertZhangEmilyWang

August2016

©2016GaoFengAdvisoryCompany

Introduction

China’s automotive market is transitioning from a period of rapid growth in new car sales to a slower pattern of expansion going forward. While this slower pattern of growth is a concern for automakers and suppliers, the market remains at historically high levels of sales, and the car population continues to expand at double digit rates annually. In addition, the average age of the vehicle population is rising.

Add to this a recent push by the Chinese government to allow sales of original equipment service (OES) parts by independent service providers, coupled with the emergence of digital platforms for accessing services, the conditions are ripe for discontinuous expansion of the independent aftermarket (IAM).

All of these factors are contributing to an explosive expansion of the automotive aftermarket services business in China. In this environment, automakers and suppliers are seeking ways to offer a clear and differentiated value proposition in order to succeed in the aftermarket, and they must act quickly to compete with new entrants who are seeking to disrupt the traditional service model.

© 2016 Gao Feng Advisory Company

© 2016 Gao Feng Advisory Company

TheExplosiveGrowthOpportunityinChina’sAutomotiveAftermarket3

After a decade of unprecedented growth and expansion, China’s auto market has decelerated. After achieving 24 percent compound annual sales growth in the period from 2008 through 2011, new car sales growth has been in the single digits for 4 out of the past 5 years, prompting market watchers to label this slower growth pattern as the “new normal”.

Slower new car sales growth is a function of several inter-related drivers, including: the government’s desire for slower (and more sustainable) overall macroeconomic growth, restricted access to license plates in certain densely populated cities, the availability of good quality used cars, and changing attitudes towards ownership. In the latter case, On-Demand-Mobility (ODM) has emerged as a very popular alternative to vehicle ownership1.

On top of this, inventories of unsold vehicles have been steadily rising, which is indicative of excess capacity which places pressure on pricing. Dealer groups have openly expressed concerns over their ability to achieve sales targets, and have demanded adjustments and higher incentives in order to sell-down the excess inventory of unsold units.

China’s Automotive Industry in Transition

While there is certainly cause for near-term concern, we believe that the China automotive market is transitioning to a more mature stage - one that still offers the most profitable growth opportunities in the world for both local and global carmakers and their value chain partners. While the age of exponential growth has surely passed, a more moderate single-digit growth pattern has now arrived, and is likely more sustainable going forward.

In a market that is accustomed to rapid growth in new vehicle sales, automakers and their partners must now seek opportunities to unlock a more diversified mix of profit streams to drive growth. However, a more sophisticated and nuanced understanding of the market is needed in order to unlock such opportunities.

1 Reimagining Mobility in the China Context, Gao Feng Viewpoint, by Bill Russo, Edward Tse, Alan Chan and Alexander Loke, February 2016

© 2016 Gao Feng Advisory Company

TheExplosiveGrowthOpportunityinChina’sAutomotiveAftermarket4

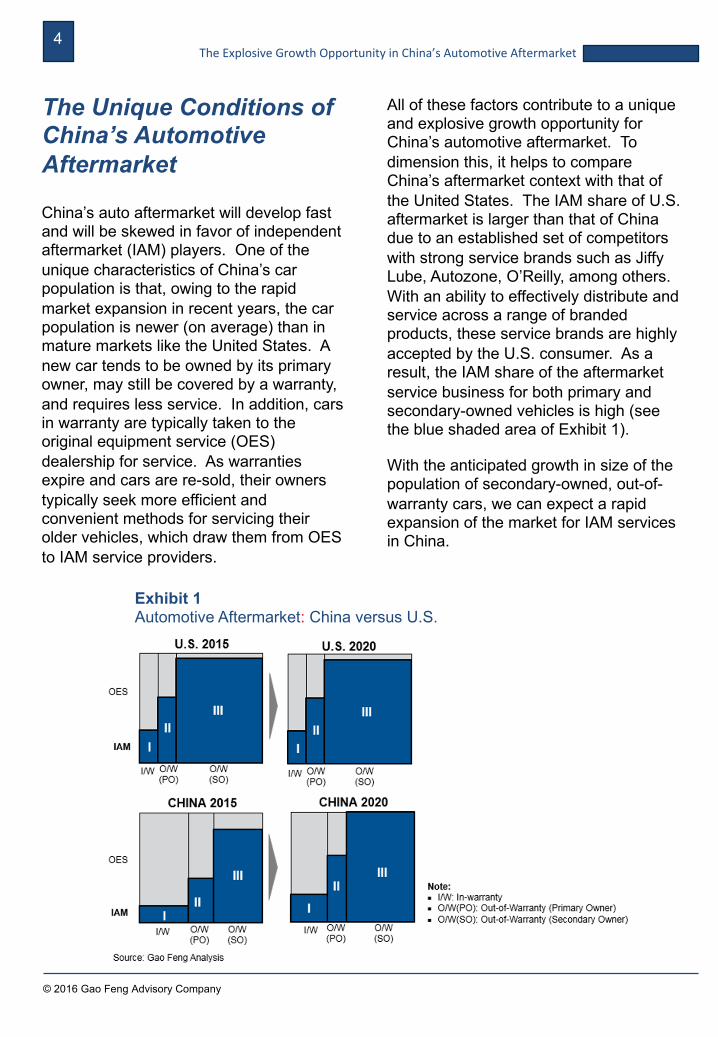

China’s auto aftermarket will develop fast and will be skewed in favor of independent aftermarket (IAM) players. One of the unique characteristics of China’s car population is that, owing to the rapid market expansion in recent years, the car population is newer (on average) than in mature markets like the United States. A new car tends to be owned by its primary owner, may still be covered by a warranty, and requires less service. In addition, cars in warranty are typically taken to the original equipment service (OES) dealership for service. As warranties expire and cars are re-sold, their owners typically seek more efficient and convenient methods for servicing their older vehicles, which draw them from OES to IAM service providers.

The Unique Conditions of China’s Automotive Aftermarket

All of these factors contribute to a unique and explosive growth opportunity for China’s automotive aftermarket. To dimension this, it helps to compare China’s aftermarket context with that of the United States. The IAM share of U.S. aftermarket is larger than that of China due to an established set of competitors with strong service brands such as Jiffy Lube, Autozone, O’Reilly, among others. With an ability to effectively distribute and service across a range of branded products, these service brands are highly accepted by the U.S. consumer. As a result, the IAM share of the aftermarket service business for both primary and secondary-owned vehicles is high (see the blue shaded area of Exhibit 1).

With the anticipated growth in size of the population of secondary-owned, out-of-warranty cars, we can expect a rapid expansion of the market for IAM services in China.

Exhibit 1 Automotive Aftermarket: China versus U.S.

© 2016 Gao Feng Advisory Company

5

Several concurrent forces will drive the rapid growth of the IAM share of the total aftermarket business, all of which are unique for China:

1. The aging car population with an increasing share of used cars

With the rise in new car sales in recent years (21.1 million units of passenger vehicles were sold in 2015), the majority of cars in China’s 131 million-unit passenger car population were actually sold since 2009. This is a significantly younger car population than exists in other developed markets. As these cars age, demand for repair and maintenance increases.

As cars exit their warranty period and are re-sold as used cars, consumers often seek value when they shop for aftermarket services (see Exhibit 2).

In addition, the used car sales channel has developed independently from the new car sales channel in China. Primary owners in China typically sell their cars 5-6 years after purchasing the car. The “wave” of cars sold since 2009 are now coming back on the market as used cars. Recently, the China government has published regulations to encourage sales of used cars, including the requirement for provincial governments to lift restrictions on intra-city used car transactions. This regulation will shorten ownership cycles by facilitating the movement of cars from upper tier to lower tier cities. Importantly, virtually all of this expanding group of secondary owners will service their cars through the IAM channel.

Drivers for Explosive Development of the Independent Aftermarket

Exhibit 2China’s Aging Car Population and Demand for Maintenance

TheExplosiveGrowthOpportunityinChina’sAutomotiveAftermarket

© 2016 Gao Feng Advisory Company

6

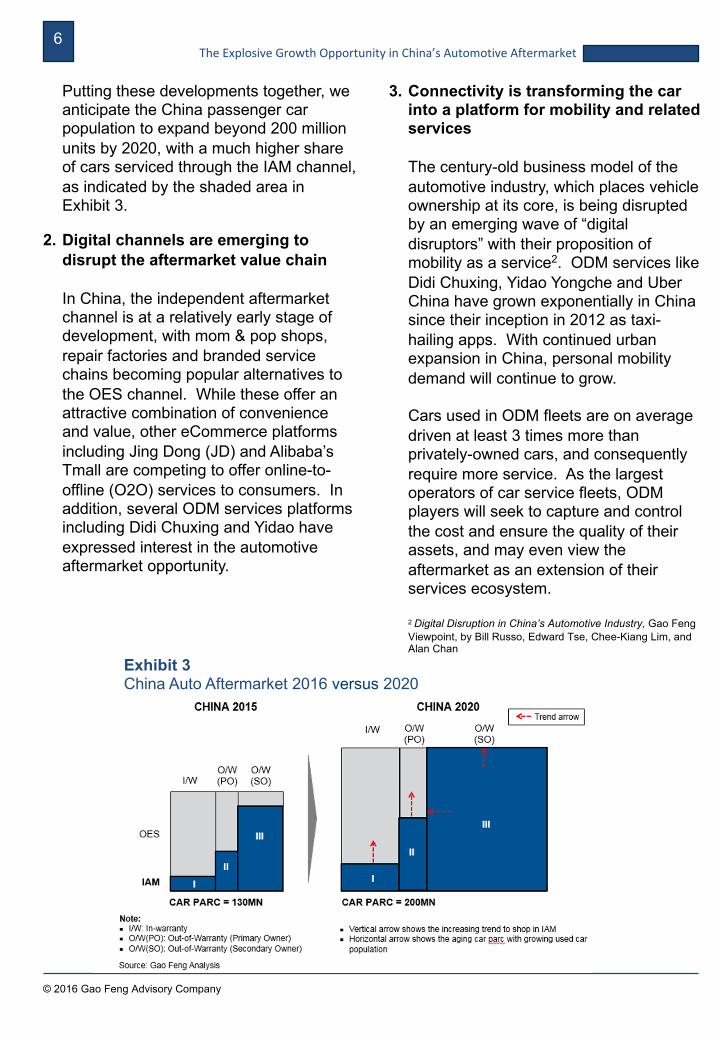

Putting these developments together, we anticipate the China passenger car population to expand beyond 200 million units by 2020, with a much higher share of cars serviced through the IAM channel, as indicated by the shaded area in Exhibit 3.

2. Digital channels are emerging to disrupt the aftermarket value chain

In China, the independent aftermarket channel is at a relatively early stage of development, with mom & pop shops, repair factories and branded service chains becoming popular alternatives to the OES channel. While these offer an attractive combination of convenience and value, other eCommerce platforms including Jing Dong (JD) and Alibaba’s Tmall are competing to offer online-to-offline (O2O) services to consumers. In addition, several ODM services platforms including Didi Chuxing and Yidao have expressed interest in the automotive aftermarket opportunity.

3. Connectivity is transforming the car into a platform for mobility and related services

The century-old business model of the automotive industry, which places vehicle ownership at its core, is being disrupted by an emerging wave of “digital disruptors” with their proposition of mobility as a service2. ODM services like Didi Chuxing, Yidao Yongche and UberChina have grown exponentially in China since their inception in 2012 as taxi-hailing apps. With continued urban expansion in China, personal mobility demand will continue to grow.

Cars used in ODM fleets are on average driven at least 3 times more than privately-owned cars, and consequently require more service. As the largest operators of car service fleets, ODM players will seek to capture and control the cost and ensure the quality of their assets, and may even view the aftermarket as an extension of their services ecosystem.

2 Digital Disruption in China’s Automotive Industry, Gao Feng Viewpoint, by Bill Russo, Edward Tse, Chee-Kiang Lim, and Alan Chan

Exhibit 3China Auto Aftermarket 2016 versus 2020

TheExplosiveGrowthOpportunityinChina’sAutomotiveAftermarket

© 2016 Gao Feng Advisory Company

7

4. The China government is actively campaigning to improve the efficiency of the automotive retail channel

Through a series of interventions, China’s National Development and Reform Commission (NDRC) has been actively promoting initiatives which spur competition and improve price transparency for products, replacement parts, and services. The recent anti-monopoly campaign and change of deregulation on “Auto Dealer License Certification” is designed to create more competition, shifting pricing power away from OEMs.

TheExplosiveGrowthOpportunityinChina’sAutomotiveAftermarket

© 2016 Gao Feng Advisory Company

8

customers often need to wait more than 24 hours for their parts to arrive at the repair shops.

Efficient parts matching and logistics & warehousing are barriers to the development of the IAM branded services channel.

Based on research conducted by Gao Feng Advisory Company across the full range of players in the IAM channel, we have identified five Key Success Factors for competing in the aftermarket services business, which are listed here:

1. Stickiness to the Point of Sale (POS)2. In-Store Service

3. Product Availability4. Price Competitiveness5. Product Brand

Driven by the explosive expansion of the addressable market for IAM services, we expect that the Branded Service channel and Digital Platforms (including O2O/eCommerce and ODM) will expand rapidly in the next 5 years, as they are effectively addressing the Key Success Factors and closing capability gaps.

TheExplosiveGrowthOpportunityinChina’sAutomotiveAftermarket

IAM in China is at an early stage of development, with a landscape of service providers which operate in a relatively inefficient manner. 90 percent of the sales of easy-wearing parts (including filters, spark plugs, brake pads and windshield wipers) are sold to physical IAM shops, of which roughly half are sold through more than 100,000 individually-owned repair factories and mom-pop shops across China.

IAM service quality in China is below the commonly accepted service standards of developed markets due to the fragmentation of service providers and the lack of efficiency in parts distribution. There are thousands of auto parts distributors in China, each covering a limited geographical area (typically 1-2 provinces), many of which only deal with specific parts and car models.

This presents several challenges. On one hand, replacement parts suppliers must manage a large number of distributors. On the other hand, each service outlet must also work with multiple distributors, who they rely on for warehousing and parts matching. Further complicating the situation, there is no publicly available source or platform that provides car model and parts matching information. As a result, parts distribution cost is high, and

Building China’s Automotive Aftermarket Ecosystem

Key Success Factors for Competing in China’s Automotive Aftermarket

© 2016 Gao Feng Advisory Company

9

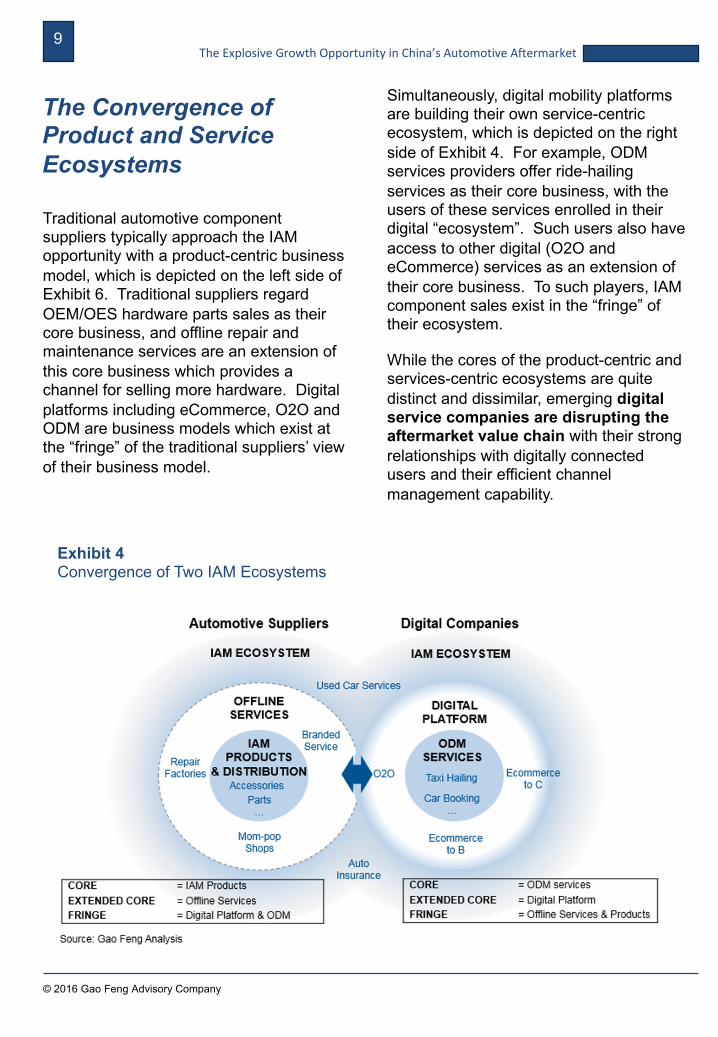

Traditional automotive component suppliers typically approach the IAM opportunity with a product-centric business model, which is depicted on the left side of Exhibit 6. Traditional suppliers regard OEM/OES hardware parts sales as their core business, and offline repair and maintenance services are an extension of this core business which provides a channel for selling more hardware. Digital platforms including eCommerce, O2O and ODM are business models which exist at the “fringe” of the traditional suppliers’ view of their business model.

Simultaneously, digital mobility platforms are building their own service-centric ecosystem, which is depicted on the right side of Exhibit 4. For example, ODM services providers offer ride-hailing services as their core business, with the users of these services enrolled in their digital “ecosystem”. Such users also have access to other digital (O2O and eCommerce) services as an extension of their core business. To such players, IAM component sales exist in the “fringe” of their ecosystem.

While the cores of the product-centric and services-centric ecosystems are quite distinct and dissimilar, emerging digitalservice companies are disrupting the aftermarket value chain with their strong relationships with digitally connected users and their efficient channel management capability.

The Convergence of Product and Service Ecosystems

Exhibit 4Convergence of Two IAM Ecosystems

TheExplosiveGrowthOpportunityinChina’sAutomotiveAftermarket

10

Both product-centric and service-centric companies seek to expand their revenue streams by accessing the explosive growth potential of China’s automotive aftermarket. We describe several case examples here.

Traditional Automotive Supplier Case Example: Robert Bosch

Traditional automotive suppliers understand the explosive growth potential of China’s aftermarket, but lack the full set of capabilities to access this opportunity. Such suppliers are typically product centric, and sell their products through OES (dealership) channels and through distributors. As previously described, successfully competing in China’s aftermarket requires a capability system that can deliver against the consumer’s product and service needs.

© 2016 Gao Feng Advisory Company

Disruptions in China’s Automotive Aftermarket: Case Examples

Therefore, suppliers must build an ecosystem which can deliver against a “hybrid” set of product and service capabilities.

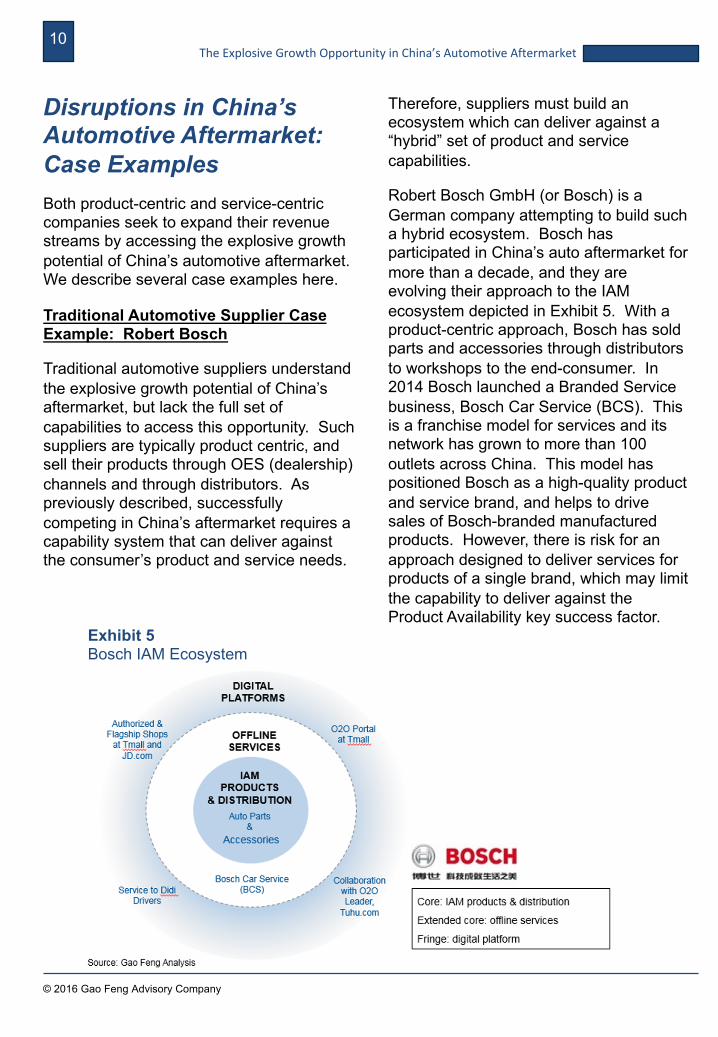

Robert Bosch GmbH (or Bosch) is a German company attempting to build such a hybrid ecosystem. Bosch has participated in China’s auto aftermarket for more than a decade, and they are evolving their approach to the IAM ecosystem depicted in Exhibit 5. With a product-centric approach, Bosch has sold parts and accessories through distributors to workshops to the end-consumer. In 2014 Bosch launched a Branded Service business, Bosch Car Service (BCS). This is a franchise model for services and its network has grown to more than 100 outlets across China. This model has positioned Bosch as a high-quality product and service brand, and helps to drive sales of Bosch-branded manufactured products. However, there is risk for an approach designed to deliver services for products of a single brand, which may limit the capability to deliver against the Product Availability key success factor.

Exhibit 5Bosch IAM Ecosystem

TheExplosiveGrowthOpportunityinChina’sAutomotiveAftermarket

11

On the digital channel, Bosch is selling product through its flagship service shops and authorized e-retail partners via Tmall and JD. Its Tmall flagship shop also markets offline services of BCS. Meanwhile, Bosch also collaborates with O2O player Tuhu as well as ODM player Didi Chuxing to expand its reach to more online consumers.

Digital Platform Case Examples: ODM and O2O/eCommerce

Digital companies typically focus on building communities of users around a core product or service. They then expand from this core by adding a range of services. These services may at times appear to be dissimilar, but they often share a digital platform used to access these services. The decision to expand into a new category of product or service is typically driven by their ability to enhance user loyalty or “stickiness” to the platform.

© 2016 Gao Feng Advisory Company

China-based ODM companies like Didi Chuxing (invested by Apple, Alibaba and Tencent etc.), Yidao (invested by LeEco) and UCAR (a Shenzhou ride hailing platform) view the IAM business as an important area for expanding their digital ecosystem.

This “core to fringe” ecosystem expansion is illustrated for Didi Chuxing in Exhibit 6. For example, Didi Chuxing (the market leader in ride hailing) has created Didi driver’s club (see Exhibit 7) that connects its online ODM car drivers to offline service sites which provide registration, car leasing, repair & maintenance, and car insurance services. The goal is to offer drivers access to convenient, high-quality and good value-for-money services, in order to increase the stickiness of drivers/users to the platform. Several offline service outlets have been built in major tier 1 and tier 2 cities since 2015.

Exhibit 6Didi Chuxing’s IAM Ecosystem

TheExplosiveGrowthOpportunityinChina’sAutomotiveAftermarket

12

eCommerce and O2O companies, such as Tuhu, JD and Carzone are leveraging their big data and logistics capability to disintermediate traditional distributors and thereby add value to customers. China’s leading O2O platform Tuhu has set up 17 warehouses (in cities such as Beijing, Shanghai, Shenyang, Xi’an, Guangzhou, Chengdu, and Kunming) which allow 8-hour delivery in major cities (see Exhibit 8). Tuhu’s distribution network covers more than 10,000 authorized service outlets in 330 cities around China. Consumers can place their order online, and go directly to those outlets for service as parts arrive.

© 2016 Gao Feng Advisory Company

Exhibit 7Didi Driver’s Club

Exhibit 8Tuhu Offline Services Footprint in China

TheExplosiveGrowthOpportunityinChina’sAutomotiveAftermarket

13

Case Example: Hella and JD

Hella and JD (a major Chinese eCommerce player, NASDAQ: JD) recently formed a strategic partnership in 2015 to develop their O2O vehicle quick service network. Hella will participate by developing the offline, “Hella-JD” branded service chain through franchising. JD will bring their online users to offline aftermarket service outlets, and provide logistics and distribution services to the Hella-JD branded service franchisees.

Case Example: Federal-Mogul and China Automotive Import and Export Co. (CAIEC)

Federal-Mogul and CAIEC formed a joint venture in 2015, targeting the automotive aftermarket vehicle repair business within China. This JV will develop a network of “Motorcare” branded service stores, backed by CAIEC’s network development and operations capabilities. Federal-Mogul will be the preferred supplier to the JV, providing its broad portfolio of premium-branded automotive parts.

© 2016 Gao Feng Advisory Company

TheExplosiveGrowthOpportunityinChina’sAutomotiveAftermarket

Building a hybrid product and service ecosystem is challenging since the capabilities for traditional product and emergent services players are very different. It is critical that each understand the key success factors and the capability system required to compete for the IAM service business (see Exhibit 5), and determine how to access capabilities which are missing in each respective organization. Key questions to consider include:

§ What are the required capabilities?

§ What businesses are in the “fringe” and how to bring them to the “core”?

§ What are the capability gaps?

§ Can the capability gaps be closed organic (internally) or inorganic (acquisition, JV, partnership) means?

§ How do we expand our business from “core” to “fringe”?

A Collaboration Model for Building the Aftermarket Ecosystem

Filling Capability Gaps Through Collaborations Among Existing and Emergent Players

14

© 2016 Gao Feng Advisory Company

The automotive aftermarket is an opportunity too big to ignore for automotive enterprises in China. Driven by demand, supply and regulatory factors highlighted in this paper, China’s auto aftermarket offers explosive growth opportunities for organizations that are prepared to adapt their approach to the China context. As the China market enters a more mature stage with slower new car sales growth, OEMs and suppliers must act now to find opportunities to profitably grow their business. New profit growth opportunities abound in the world’s largest automotive market, especially in the aftermarket. However, unlocking this potential requires a new set of capabilities, developed in collaboration with new value chain partners.

In the automotive aftermarket, the ecosystems of product-centric companies and service-centric companies are converging. Emerging service companies are disrupting the traditional value chain with strong customer relationship and channel management capabilities. Auto suppliers must expand from their core and adapt new capabilities from the fringe and bring them into their expanded core. Experimenting in the fringe is an essential way to bring innovative new solutions to the market. Suppliers must offer a clear and differentiated value proposition in order to succeed in the aftermarket, and they must act quickly to compete and potentially collaborate with disruptive companies that are experimenting in the fringe.

Looking Forward

TheExplosiveGrowthOpportunityinChina’sAutomotiveAftermarket

Maximizing participation in China’s Automotive Aftermarket requires a Customer-to-Business (C2B) ecosystem that blends product and services capabilities. This poses a huge challenge for automotive suppliers because their basic DNA is centered around sales of their products. Suppliers must expand their business scope to build a hybrid product and services ecosystem with a “customer first” emphasis (hence the term C2B). Automotive suppliers must fundamentally rethink their role in this emerging new business model and be prepared to redefine their company value proposition to the aftermarket customer.

A set of questions need to be considered for this purpose:

§ What is the mission and vision of your organization?

§ What is your value proposition?

§ Are you a B2B or C2B company?

§ What is your role and function in the C2B product and services ecosystem?

§ What is the organization’s DNA and what should it become in order to serve the aftermarket?

§ How could this impact on your China strategy and global strategy?

The answers to these questions will have far-reaching implications to the organization and its future growth trajectory.

Building an Automotive Aftermarket Organization

15

© 2016 Gao Feng Advisory Company

Robert Zhang is a Senior Associate at Gao Feng Advisory Company based in Beijing. He previously worked at Siemens Limited China as a senior manager. He led a major channel management project for transforming the client’s distribution network, covering multiple product business units and regional sales organizations. In his management consulting career, he has helped a range of leading global Automotive, Industrial Products and Energy companies to deploy their market entry strategy, optimize their local production and distribution networks, and create their product strategy and investment models.

Emily Wang is a Senior Consultant at Gao Feng Advisory Company based in Shanghai. She has worked with clients from various industries including Automotive, Industrial Goods, Real Estate, Home Appliances, Consumer Goods and Agriculture. She is experienced with solving client’s most strategic problems, ranging from operating model design, organizational transformation, go-to-market strategy, and market opportunity assessment. Ms. Wang has worked with multinational organizations and start-up companies across China and the United States.

Bill Russo is Managing Director and the Automotive Practice leader at Gao Feng Advisory Company based in Shanghai. With 15 years as an Automotive executive, including over 11 years of experience in China and Asia, Mr. Russo has worked with numerous multi-national and local Chinese firms in the formulation and implementation of their global market and product strategies. He was previously Vice President of Chrysler North East Asia, where he managed the business operations for the Greater China and South Korea markets. Prior to this, Mr. Russo was Head of Product & Business Strategy for Chrysler. He also has nearly 12 years of experience in the electronics and IT industry, having worked at IBM Corporation as a manufacturing and systems engineer, and formerly served as Vice President of Corporate Development at Harman International.

About the authors

TheExplosiveGrowthOpportunityinChina’sAutomotiveAftermarket

GaoFengAdvisoryCompany(www.gaofengadv.com)isapre-eminentstrategyandmanagementconsultingfirmwithrootsinChinacoupledwithglobalvision,capabilities,andabroadresourcesnetwork.Wehelpourclientsaddressandsolvetheirtoughestbusinessandmanagementissues-- issuesthatariseinthecurrentfast-changing,complicatedandambiguousoperatingenvironment.Wecommittoputtingourclients’interestfirstandforemost.Weareobjectiveandweviewourclientengagementsaslong-termrelationshipsratherthanone-offprojects.Wenotonlyhelpourclients“formulate”thesolutionsbutalsoassistinimplementation,oftenhand-in-hand.Webelieveinteamingandworkingtogethertoaddvalueandcontributetoproblemsolvingforourclients,fromthemostjuniortothemostsenior.

Ourseniorteamismadeupofseasonedconsultantspreviouslyatleadingmanagementconsultingfirmsand/orex-topexecutivesatlargecorporations.Webelievethiscombinationofmanagementtheoryandoperationalexperiencewoulddeliverthemostbenefittoourclients.

OurnameGaoFengistakenfromtheSongDynastyChineseproverbGaoFengLiangJie.GaoFengdenotesnoblecharacterwhileLiangJiereferstoasharpsenseofintegrity.Webelievethatthisprincipleliesatthecoreofmanagementconsulting– atrulytrustworthypartnerwhowillhelpclientstackletheirtoughestissues.

© 2016 Gao Feng Advisory Company

For More Information:

Bill RussoManaging DirectorGao Feng Advisory [email protected]

Robert ZhangSenior AssociateGao Feng Advisory [email protected]

Emily WangSenior ConsultantGao Feng Advisory [email protected]