the external environment for developing countries january 2009 the world bank development economics...

TRANSCRIPT

The External Environment for Developing Countries

January 2009The World Bank

Development EconomicsProspects Group

Global industrial production plummets into 4th quarter of 2008...

manufacturing production, ch% (saar)

-20

-15

-10

-5

0

5

10

15

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08

Source: DEC Prospects Group.

OECD

Developing

World

50

60

70

80

90

100

110

Sep-08 Oct-08 Nov-08 Dec-08 Jan-09

Source: Thomson/Datastream, Morgan Stanley (*USD index).

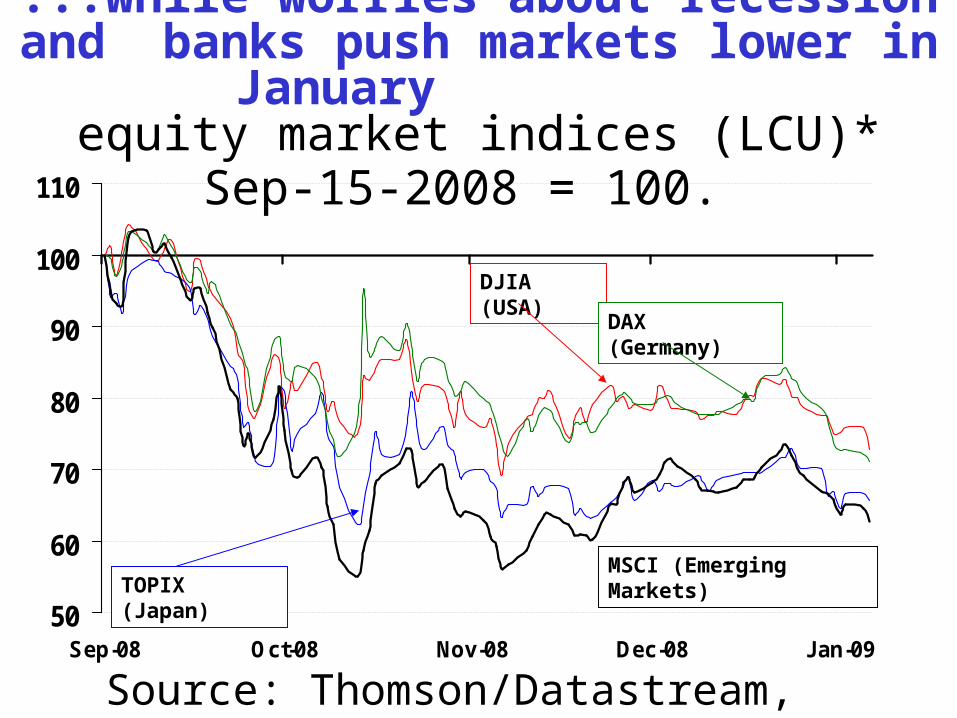

...while worries about recession and banks push markets lower in January

equity market indices (LCU)* Sep-15-

2008 = 100.

MSCI (Emerging Markets)TOPIX (Japan)

DJIA (USA)

DAX (Germany)

Industrial countries

U.S. employment losses in 2008 sum to 2.6 million...worst since 1945 change in non-farm employment,

‘000

-600

-500

-400

-300

-200

-100

0

100

200

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08

Source: U.S. Department of Labor.

monthly change

3mma change

Falling exports, orders and production pressure U.S. GDP

export volumes, durable goods orders and IPmfg, ch% saar

-20

-15

-10

-5

0

5

10

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08

-40

-30

-20

-10

0

10

20

30

40

Source: Department of Commerce, Federal Reserve.

Export volumes [R]

Durable goods orders [R]

Production [L]

0

1

2

3

4

5

6

Aug-07 Nov-07 Feb-08 May-08 Aug-08 Nov-08

Source: Thomson/Datastream.

Interbank market rates- and yield on ten-year note easing

Fed Funds target- and effective rates; Libor and T-note 10 yr

Fed Funds Target

LIBOR 6 months

T-note 10-year

Fed Funds Effective

Japan’s exports and production point to severe 4th quarter downturn

export volumes and manufacturing output, ch% saar

-25

-20

-15

-10

-5

0

5

10

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08

-30

-20

-10

0

10

20

30

Source: Bank of Japan and Japan Cabinet Office.

Industrial production [L]

Export volumes [R]

Household spending turns to the doldrums in the last months of 2008

household expend, retail sales [L]; Tokyo consumer confidence [R]

-2

-1

0

1

2

3

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08

25

30

35

40

45

50

Source: Japan Cabinet Office.

HH spending [L]

Consumer confidence [R]

Retail sales [L]

0.5

0.8

1.0

1.3

1.5

1.8

2.0

Jun-08 Jul-08 Aug-08 Sep-08 Oct-08 Nov-08 Dec-08 Jan-09

85

90

95

100

105

110

115

Source: Thomson/Datastream.

Yen strength on unwinding “carry trades” supports BOJ ease Yen/USD rate (inverse) [right]; TIBOR

and JGB 10-year [left]

Yen/dollar (inverse) [R]

TIBOR 6 months [L]

JGB- ten year [L]

European confidence plummets while ECB asesses economic damage

Euro Area consumer confidence [L]; IFO overall [R]

-30

-25

-20

-15

-10

-5

0

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-0885

90

95

100

105

110

115

Source: Eurostat-- Thomson/Datastream.

IFO overall [R]

EC Consumer confidence [L]

Production now in sharp decline across the Euro Area

manufacturing production, ch% (saar)

-20

-15

-10

-5

0

5

10

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08

Source: Eurostat.

Germany

France

Italy

Euro Area

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

Aug-07 Nov-07 Feb-08 May-08 Aug-08 Nov-081.22

1.30

1.38

1.46

1.54

1.62

Source: Thomson/Datastream.

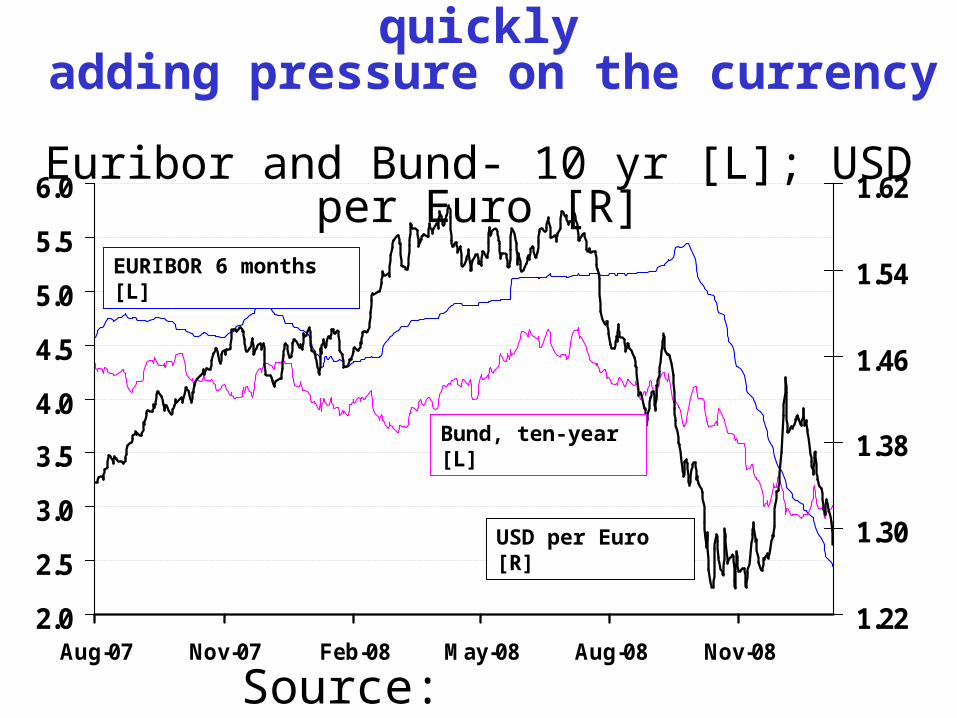

Euro interbank rates fall quickly adding pressure on the currency Euribor and Bund- 10 yr [L]; USD per

Euro [R]

USD per Euro [R]

EURIBOR 6 months [L]

Bund, ten-year [L]

Industrial production

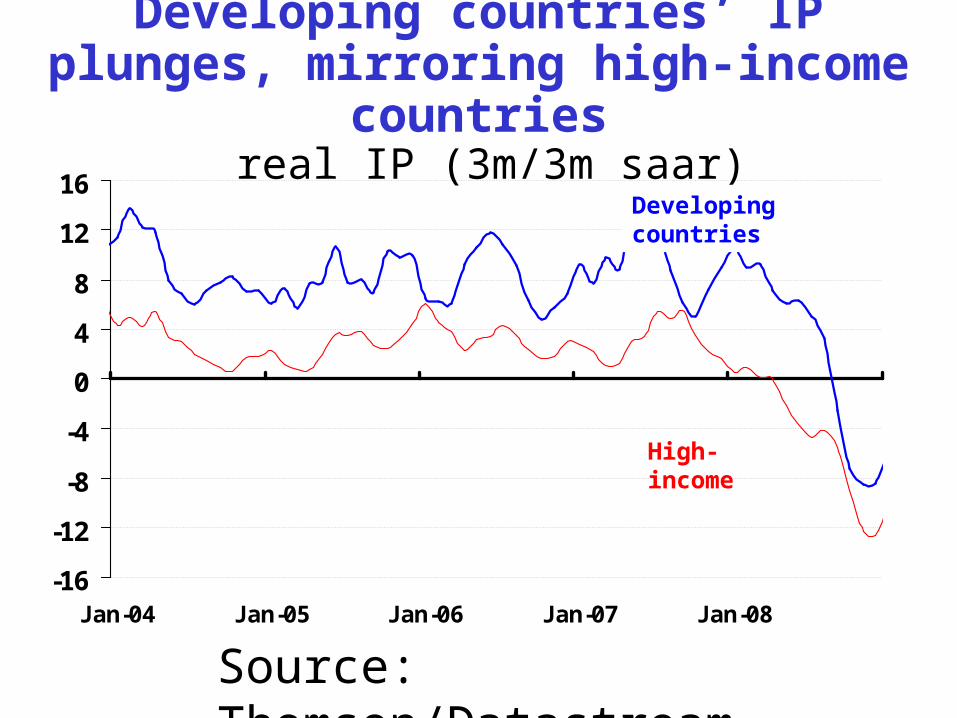

Developing countries’ IP plunges, mirroring high-income countries

real IP (3m/3m saar)

-16

-12

-8

-4

0

4

8

12

16

Jan-04 Jan-05 Jan-06 Jan-07 Jan-08

Source: Thomson/Datastream, DECPG.

High-income

Developing countries

East Asia and Central and Eastern Europe hit hardest

real IP (3m/3m saar)

-30

-20

-10

0

10

20

30

Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

ECA

East Asia, excl China

Source: Thomson/Datastream, DECPG.

Dramatic IP contraction in export intensive economies

real IP (6m/6m saar)

-50

-40

-30

-20

-10

0

10

20

30

Jan-99 May-00 Sep-01 Jan-03 May-04 Sep-05 Jan-07 May-08

HungaryTurkey

Czech Republic

Korea

Taiwan

Source: Thomson/Datastream, DECPG.

International trade

Major OECD imports contract in step with domestic demand

import volumes: U.S, Japan, Germany and U.K. ch% 3mma y/y

-7.5

-5.0

-2.5

0.0

2.5

5.0

7.5

10.0

12.5

15.0

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08

Source: National Agencies through Thomson/Datastream.

United States

Japan

Germany

U.K.

Developing exports in decline export volumes: China, India, Mexico and

Jordan ch% 3mma y/y

-15

-5

5

15

25

35

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08

Source: National Agencies through Thomson/Datastream.

China

India

Jordan

Mexico

-80

-60

-40

-20

0

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08

Source: Department of Commerce.

U.S. trade balance improves sharply in November on plummeting oil price

Goods balance

Oil balance

Non-oil balance

goods balance, and oil- and non-oil balances ($bn)

Oil prices

Oil prices appear to stabilize amid OPEC production cuts

25

35

45

55

65

75

85

95

105

115

125

135

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

25

26

27

28

29

30

31

$/bbl mb/d

Oil price [L scale]

OPEC-11 Production (x Angola) [R]

Source: IEA and DECPG Commodities Group.

Growth in U.S. Oil Demand (yr/yr)

-2000

-1500

-1000

-500

0

500

1000

Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

Other

Resid

Distillate

Gasoline

kb/d

Source: IEA and DECPG Commodities Group.

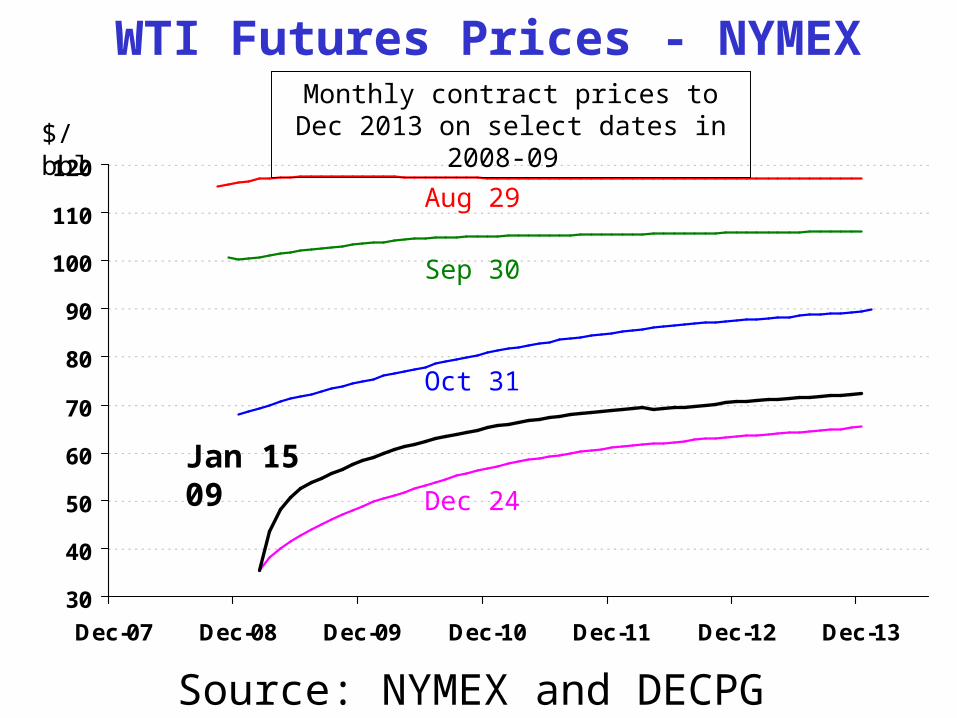

WTI Futures Prices - NYMEX

30

40

50

60

70

80

90

100

110

120

Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13

Jan 15 09

$/bbl

Monthly contract prices to Dec 2013 on select dates in 2008-09

Oct 31

Sep 30

Aug 29

Dec 24

Source: NYMEX and DECPG Commodities Group.

Non-oil commodity prices

100

150

200

250

300

350

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

Grains

Fats & Oils

Other Food

Agriculture price declines begin to moderate

2000=100

Source: Datastream and DECPG Commodities Group.

Metal prices rebound slightly on index rebalancing

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Jan-05Jan-06

Jan-07Jan-08

Jan-09

0

50

100

150

200

250

300

350

400

450

$/ton ‘000 tons

Copper price

LME stocks

Source: LME and DECPG Commodities Group.

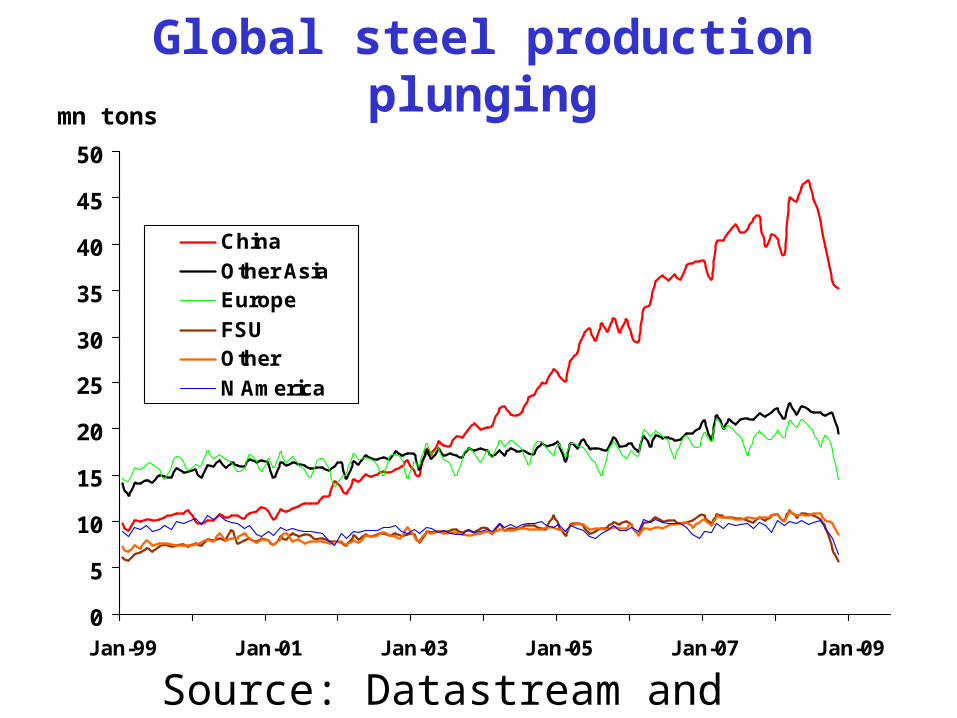

Global steel production plunging

0

5

10

15

20

25

30

35

40

45

50

Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09

China

Other AsiaEurope

FSUOther

N America

mn tons

Source: Datastream and DECPG Commodities Group.

International Finance

A difficult year for emerging market capital flows

Source: DECPG Finance Team.

Gross capital flows to emerging markets

$ billion

H1 Q3 Q4 Total H1 Q3 Q4 Dec Total

Total 349 163 139 652 253 73 44 16 371

Bonds 107 20 19 146 58 9 2 2 69

Banks 156 101 55 312 150 62 42 14 254

Equity 86 42 66 194 45 2 0 0 47

Lat. America 69 54 32 156 56 13 10 5 79

Bonds 31 6 8 45 17 1 2 2 20

E. Europe 156 45 46 247 101 35 21 4 158

Bonds 50 5 9 64 32 8 0.1 0.1 40

Asia 93 47 47 188 69 15 8 4 91

Bonds 18 5 1 23 7 0.4 0 0 7

Others 31 16 14 61 27 10 5 3 43

2007 2008

Equities post modest gains in December

percentage change (in local currency)

-55

-45

-35

-25

-15

-5

5

15

MSCIEmergingMarkets

MSCIMature

Markets

MSCI BRIC S&P 500 FTSE-100 Nikkei

Source: Bloomberg and DECPG Finance Team.

2008

Oct

Nov Dec

-20

-10

0

10

20

30

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

0

100

200

300

400

500

600

700

800

900

1000

Source: JPMorgan-Chase and DECPG Finance Team.

Sharp widening in EM bond spreads at year-end 2008

Yen/USD rate (inverse) [right]; TIBOR and JGB 10-year [left]

EMBIG annual retruns [Left]

EMBIG spread [Right]

Currencies

1.230

1.270

1.310

1.350

1.390

1.430

1.470

1.510

1.550

1.590

1.630

Jan-08 Mar-08 May-08 Jul-08 Sep-08 Nov-08 Jan-09

86

90

94

98

102

106

110

Source: Thomson/Datastream.

yen/USD

USD/Euro (inverse)

Dollar falls on Fed rate cutuntil ECB reduction seen as sure

USD per Euro (inverse) [Left] and Yen per USD [right]

1

2

3

4

5

6

Jan-08 Mar-08 May-08 Jul-08 Sep-08 Nov-08 Jan-09

Interest differentials well in favorof stronger euro since November USD Libor and EURIBOR (6 months),

percent EURIBOR 6 months

USD LIBOR 6 months

Source: Thomson/Datastream.

95

100

105

110

115

120

125

130

135

Sep-08 Oct-08 Nov-08 Dec-08 Jan-09

Source: Thomson/Datastream.

Dollar mixed against EM currencies LCU per USD indexes, Sept-15 2008=100

[*increase = weaker LCU] Turkish lira

Brazilian real

Korean won

Russian rouble

The External Environment for Developing Countries

January 2009The World Bank

Development EconomicsProspects Group