the farmland market:the farmland market: buy, sell, hold · aapex february 2011 © 2011 1 the...

TRANSCRIPT

AAPEX February 2011

© 2011 1

The Farmland Market:The Farmland Market:The Farmland Market: The Farmland Market: Buy, Sell, HoldBuy, Sell, Hold

The MarketThe Market

Two Iowa Sales – Sioux County– Parcel 1 – 80 acres, 70+ GSR - $3,260– Parcel 2 – 80 acres, 70+ GSR - $13,950Chicago Fed Survey – October 2010– Indiana – 11%– Illinois – 8%– Michigan – 10%

AAPEX February 2011

© 2011 2

The MarketThe Market

Iowa Realtors Survey – November, 2010– State average – 16% increase– 11 North Central Counties – 20% increaseIndiana – 270% increase since 1985 –5.4% per year

Average Value Per Acre of Average Value Per Acre of Iowa FarmlandIowa Farmland

Source: Iowa Agriculture Experiment Station

AAPEX February 2011

© 2011 3

First line:

Estimates of average dollar value per Estimates of average dollar value per acres as Nov. 1, 2010, by Iowa crop acres as Nov. 1, 2010, by Iowa crop reporting districts.reporting districts.

First line: high‐, medium‐, and low‐grade farmland values.

Second line: district average.

Third line: Third line:average percentage change since Nov. 1, 2009.

4,500

5,000

Price per Acre for Average Quality Price per Acre for Average Quality Indiana Farmland, 1975Indiana Farmland, 1975--20102010

2 000

2,500

3,000

3,500

4,000

Price pe

r Acre ($'s)

500

1,000

1,500

2,000

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

P

AAPEX February 2011

© 2011 4

Land Value per Bushel of LongLand Value per Bushel of Long--Term Term Corn YieldCorn Yield

30 00

35.00

10 00

15.00

20.00

25.00

30.00

$ pe

r bus

hel

Top

Average

Poor

0.00

5.00

10.00

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Year

Department of Agricultural Economics Purdue University

Value/Cash Rent Multiple Value/Cash Rent Multiple Average Indiana Land, 1975 Average Indiana Land, 1975 –– 20102010

32

Current = 27.4

17

22

27

Valu

e/R

ent M

ultip

le

Mean = 18.0

7

12

1975 1979 1983 1987 1991 1995 1999 2003 2007Year

AAPEX February 2011

© 2011 5

Farmland Total ReturnFarmland Total Return

50%

60%

70%

0%

10%

20%

30%

40%

50%

Perc

ent R

etur

n

-30%

-20%

-10%

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

YearRent/Value Change in Value Total

Department of Agricultural Economics Purdue University

Land Demand and SupplyLand Demand and Supply

Supply Issues– Market offerings

• Normal turnover – 3-5% per year• Current turnover – 1.5% per year

– Dominance of gift/bequest transfersl i i / f i i• Rental opportunities/returns for recipients

• Return potential for proceeds

AAPEX February 2011

© 2011 6

Land Demand and SupplyLand Demand and Supply

Supply Issues– Competitive returns and portfolio

motivations of owners/investors– Forced sales/liquidators– Tax considerations – future expected

i d i l i iincreased capital gains tax rates increase supply today

Land Demand Land Demand and Supplyand Supply

Demand Issues– Development/non ag production potential– Competitive returns and portfolio

motivations of owners/investors– Inflation hedge potential of real assets

AAPEX February 2011

© 2011 7

Land Demand Land Demand and Supplyand Supply

Demand Issues– Tax considerations – lower capital gains

tax increase demand– Expected incomes – prices, costs,

productivityE d i /di– Expected interest/discount rates

– Expected growth in income

Valuation FundamentalsValuation Fundamentals

Fundamental drivers– Incomes/earnings– The discount rate– The growth rate for income/earnings– The residual/terminal value

AAPEX February 2011

© 2011 8

(for an infinite life asset)

The Capitalization ConceptThe Capitalization Concept

(for an infinite life asset)

Value = income or earnings_____discount rate – growth rate

Income/EarningsIncome/Earnings

Cash rentsResidual Returns to Land

AAPEX February 2011

© 2011 9

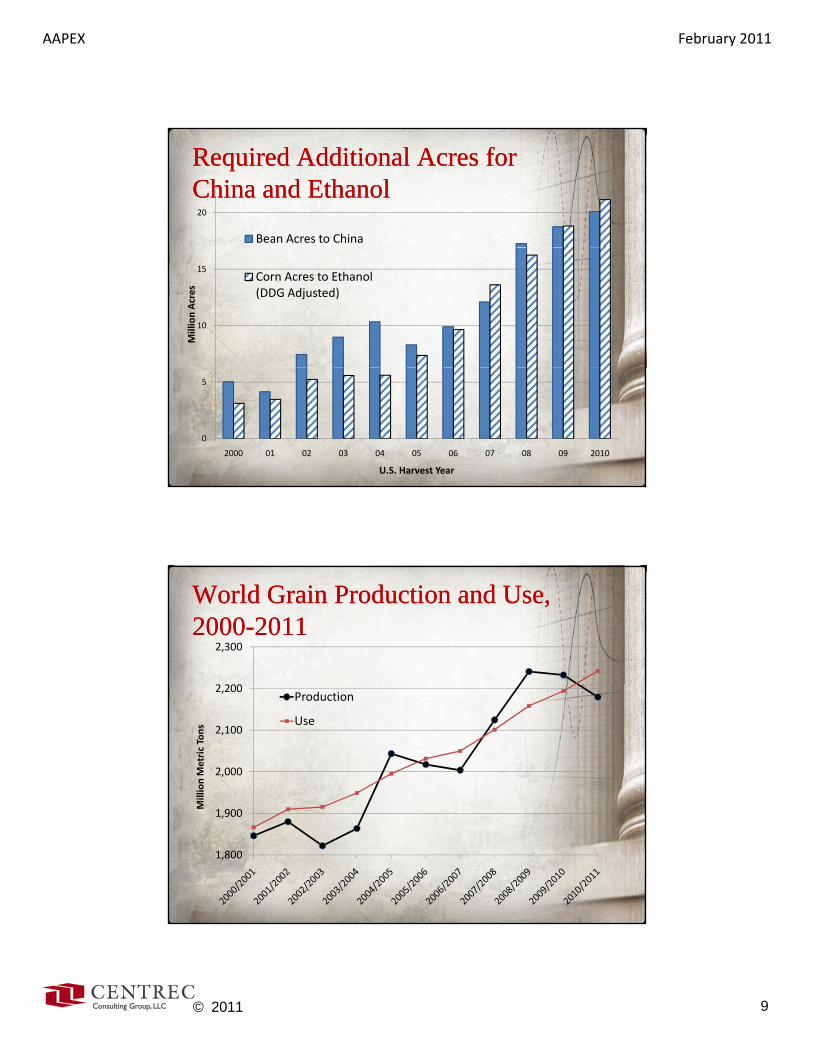

20

Bean Acres to China

Required Additional Acres forRequired Additional Acres forChina and EthanolChina and Ethanol

10

15

Million Acres

Corn Acres to Ethanol (DDG Adjusted)

0

5

2000 01 02 03 04 05 06 07 08 09 2010

U.S. Harvest Year

2 200

2,300

World Grain Production and Use, World Grain Production and Use, 20002000--20112011

2,000

2,100

2,200

Million Metric Tons

Production

Use

1,800

1,900

M

AAPEX February 2011

© 2011 10

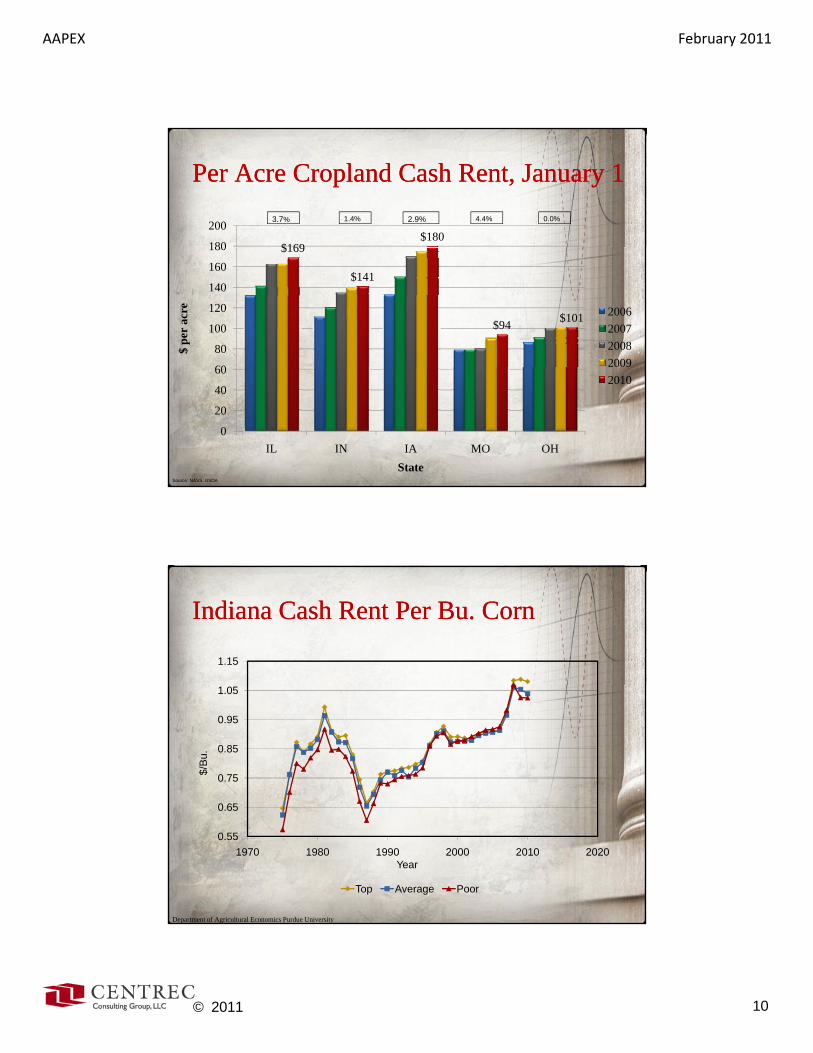

Per Acre Cropland Cash Rent, January 1Per Acre Cropland Cash Rent, January 1

$169$180

180

200 3.7% 1.4% 2.9% 4.4% 0.0%

$169

$141

$94 $101

60

80

100

120

140

160

180

$ pe

r ac

re 2006200720082009

0

20

40

60

IL IN IA MO OHState

2010

Source: NASS, USDA

Indiana Cash Rent Per Bu. CornIndiana Cash Rent Per Bu. Corn

1.15

0 65

0.75

0.85

0.95

1.05

$/B

u.

0.55

0.65

1970 1980 1990 2000 2010 2020Year

Top Average Poor

Department of Agricultural Economics Purdue University

AAPEX February 2011

© 2011 11

Residual Returns to Land Residual Returns to Land –– Indiana Indiana (high quality)(high quality)

1975 1990 $111/acre1975-1990 -- $111/acre1991-2000 -- $123/acre2001-2010 -- $188/acre2007-2010 -- $310/acre

The Discount RateThe Discount Rate

Pure time preference for money – 2-4%Inflation premium– Results in the riskless rate– Proxy is U.S. treasury interest ratesRisk premiumRisk premium

AAPEX February 2011

© 2011 12

14

16

18

Interest Rate on 10Interest Rate on 10--Year Treasury Year Treasury Bonds, 1970Bonds, 1970--20102010

6

8

10

12

14

Interest Rate (%

)

0

2

4

1970

‐01

1971

‐03

1972

‐05

1973

‐07

1974

‐09

1975

‐11

1977

‐01

1978

‐03

1979

‐05

1980

‐07

1981

‐09

1982

‐11

1984

‐01

1985

‐03

1986

‐05

1987

‐07

1988

‐09

1989

‐11

1991

‐01

1992

‐03

1993

‐05

1994

‐07

1995

‐09

1996

‐11

1998

‐01

1999

‐03

2000

‐05

2001

‐07

2002

‐09

2003

‐11

2005

‐01

2006

‐03

2007

‐05

2008

‐ 07

2009

‐09

PeriodAverage

Interest Rate (%)

Average Rate on 10Average Rate on 10--Year U.S. Treasury Year U.S. Treasury Bonds, 1970Bonds, 1970--20092009aa

Period Interest Rate (%)1970 to 1979 7.5

1980 to 1989 10.6

1990 to 1999 6.7

2000 to 2009 4.5Entire period 1970 to 2009 7.3

a Calculated as the average of the annual average rate on 10-Year Constant Maturity U.S. Treasury Bond, reported by the Board of Governors of the U.S. Federal Reserve System.

AAPEX February 2011

© 2011 13

Risk PremiumRisk Premium

Low for cash rents –a “real” bond – 1-2%Higher for farm operators – 2-4%

The Growth RateThe Growth Rate

Cash rents – 3% Residual returns – 2-3%

AAPEX February 2011

© 2011 14

Capitalization Rates 1970Capitalization Rates 1970--1980’s1980’s

Capitalization Rate

GrowthRate

RiskPremium

Risk Free Rates

82

0 103 7

83

0 113 8

Capitalization Rates 1990’sCapitalization Rates 1990’s

Capitalization Rate

GrowthRate

RiskPremium

Risk Free Rates

62

0 83 5

63

0 93 6

AAPEX February 2011

© 2011 15

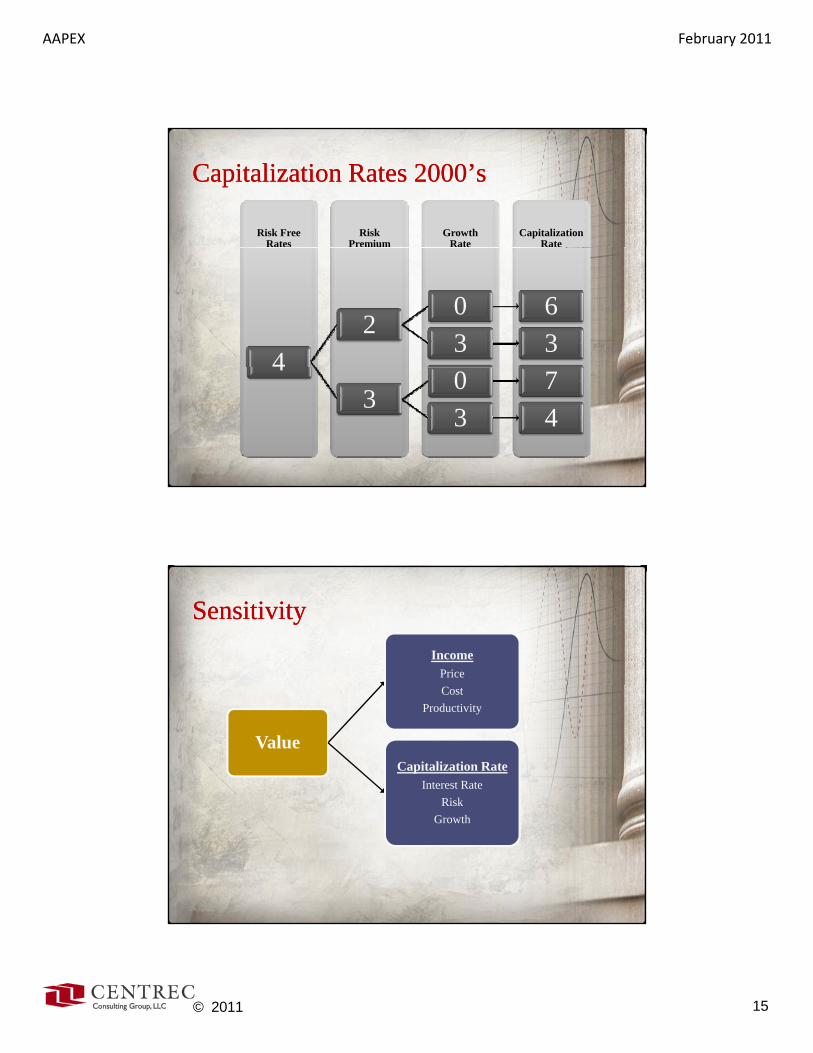

Capitalization Rates 2000’sCapitalization Rates 2000’s

Capitalization Rate

GrowthRate

RiskPremium

Risk Free Rates

42

0 63 3

43

0 73 4

SensitivitySensitivityIncome

Price

Value

CostProductivity

Capitalization RateInterest Rate

RiskRiskGrowth

AAPEX February 2011

© 2011 16

Scenario AnalysisScenario Analysis

Time Period ‘75-’90 ‘91-’00 ‘00-’10 ‘07-’10 2010Residual Returns $111 $123 $188 $310 $280

Capitalization Rate (%)

3 $3,667 $4,100 $6,267 $10,333 $9,333

4 $2,750 $3,075 $4,700 $7,750 $7,000

5 $2,200 $2,460 $3,760 $6,200 $5,600

6 $1,850 $2,050 $3,133 $5,167 $4,667

Last Year of Period $1,589 $2,715 $5,310 $5,310 $5,310

What If?What If?

Value Income Implied Cap Rate

$5 310 $280 5 27%2010

• Decline in come by 10% to $252• Value = $4,781 (-$528)

• Increase in cap rate by 1%• Value = $465 (-$844)

$5,310 $280 5.27%2010

$ ( $ )• Both

• Value = $4,019 (-$1291)

AAPEX February 2011

© 2011 17

Land As a Portfolio AssetLand As a Portfolio Asset

$9,000

Value of $1,000 Investment in 1990: Value of $1,000 Investment in 1990: (pre(pre--tax)tax)

$4,000

$5,000

$6,000

$7,000

$8,000S&P 500 Farm Land

$0

$1,000

$2,000

$3,000

90 91 92 93 94 95 96 97 98 99 0 1 2 3 4 5 6 7 8 9

AAPEX February 2011

© 2011 18

Risk and ReturnRisk and Return

Investment TotalFrom

IncomeFrom Capital

Gains----------------- (Percent) -----------------

Average annual returns 1960-88

( )

Farm:

Farmland 10.6 5.4 5.2

“Typical” farm 10.7 8.2 2.5

Nonfarm:

Stocks 10.4 3.9 6.5

Mutual funds 10.5 -- --

Gov’t bonds 6.1 7.3 -1.2

Municipal bonds 5.4 6.2 -0.8

Corporate bonds 6.6 8.2 -1.6

Treasury bills 6.5 6.5 --

Commercial paper 7.1 7.1 --

Certificate of deposit 6.8 6.8 --

Average Annual Returns, 1997 Average Annual Returns, 1997 -- 20102010

11%11%

10%

12%

IL Farmland

7%7%8%

%4%

6%

8%

10%

etur

n (A

nnua

l Per

cent

)

IL Farmland

Large Co. Stocks

Small Co Stocks

LT Corp BondsLT Govt Bonds

3%

0%

2%

0% 5% 10% 15% 20% 25% 30%

Re

Risk (Standard Deviation)

T-Bills

AAPEX February 2011

© 2011 19

Risk and ReturnRisk and Return

Correlation and Beta (1992Correlation and Beta (1992--2008)2008)

Farmland Correlations– S&P 500 - .153– Ag Products - .218– CRB Index – (.087)– Fertilizer and Ag chain - .318– Packaged Foods & Meats - .135

AAPEX February 2011

© 2011 20

Correlation and Beta (1992Correlation and Beta (1992--2008)2008)

Beta’s– Farmland – .098– Packaged Foods & Meats - .585– Fertilizer & Ag Chem - .909– Ag Products – .744– CRB Index - .151

Closing ThoughtsClosing Thoughts

Ag is a good to place to be – NOWi ili– Recession Resilient

– Strong Earnings Future– Real Assets/Good Inflation Mitigation Strategy

BUT…the risk has increased– Margin riskMargin risk– Interest rate risk– Don’t ignore the weather– Strategic risk

AAPEX February 2011

© 2011 21

Closing ThoughtsClosing Thoughts

Earnings Pressures will Increaseb ildi f l k– Rebuilding of Supply Stocks

– Cost Increases– Current Margins are not Sustainable– Capital Costs will Rise

And Safety is RelativeAnd Safety is Relative– Economic turbulence

So What Should You Do?So What Should You Do?

Don’t Drink the Kool-Aid – 9 billion people by 20502050– They need money– A lot can happen in 40 years

Managing/Assessing the Risk is the Key– The differentiator between Success and Survival

Uncertainty Provides Opportunity– Assess According to the Criteria– Be more Selective/Discriminating

AAPEX February 2011

© 2011 22

So What Should You Do?So What Should You Do?

Manage operating/financial Risk in your current b i t tbusiness so you can capture new venturesIncrease your hurdle rate for new ventures –risk is higher, you need a higher returnLock in interest rates and deleverage – maybe it’s time to take some money off the table

Thanks!!Thanks!!