the future development of structured commodity finance in emerging markets – examples and trends...

TRANSCRIPT

The future development of structured commodity finance in emerging markets –

examples and trends

Lamon RuttenChief, Risk management, finance and information

United Nations Conference on Trade and Development

Global Commodities Finance ConferenceLondon, 21-22 September 2004

“For unrated borrowers or borrowers with a B rating or lower (or borrowers that operate in a country with a B rating or lower), structuring techniques will make the

difference between reasonably-priced costs of funds and financing costs that would render their operations

uncompetitive.”

(Nicholas Budd, DentonWildeSapte)

There are many factors that are influencing international trade finance. For example, the new Basel Capital Accord:

And another factor: banks have new competitors.

The walls are coming down….

“as soon as you hear the sound of the trumpet, then all the people shall shout with a great shout; and the wall of the city will fall down flat” (The Bible, Joshua 6:1-5 RSV)

Investors Banks

TradersInsurers

Banks are competing with traders…

while traders are trying to dis-intermediate banks.

Investors are setting up specialized trade finance funds.

Insurers are developing new products for trade finance.

“Gone appear to be the days when banks made loans and investors invested equity.

Nowadays, lenders that used to tiptoe quietly into mezzanine territory (calling it quasi-debt or quasi-equity depending on their credit committees) are

boldly crossing over into fully fledged equity investment”

This is called “principal finance”.

Banks are taking a hard look at what business they are really in…

Normal finance Interest rate streams

Mezzanine finance

Equity-linked streams

Equity-linked streams

Interest rate streams

Principal finance

“Structuring fees”

OR

But in this presentation, I will concentrate on two issues:

1. the growing importance of South-South trade

2. the impact of technological developments on commodity trade finance opportunities

1. South-South trade

South-South trade is growing much faster than South-North trade.

Some numbers:

- over the past decade, South-South trade has grown at 10% a year, twice as fast as world total trade. China and India saw 14% growth.

- it now accounts for 43% of developing country exports and 11% of world trade

- for 32 countries, its share is over 50%

- but still, 70% of exports and 60% of imports are by ten countries

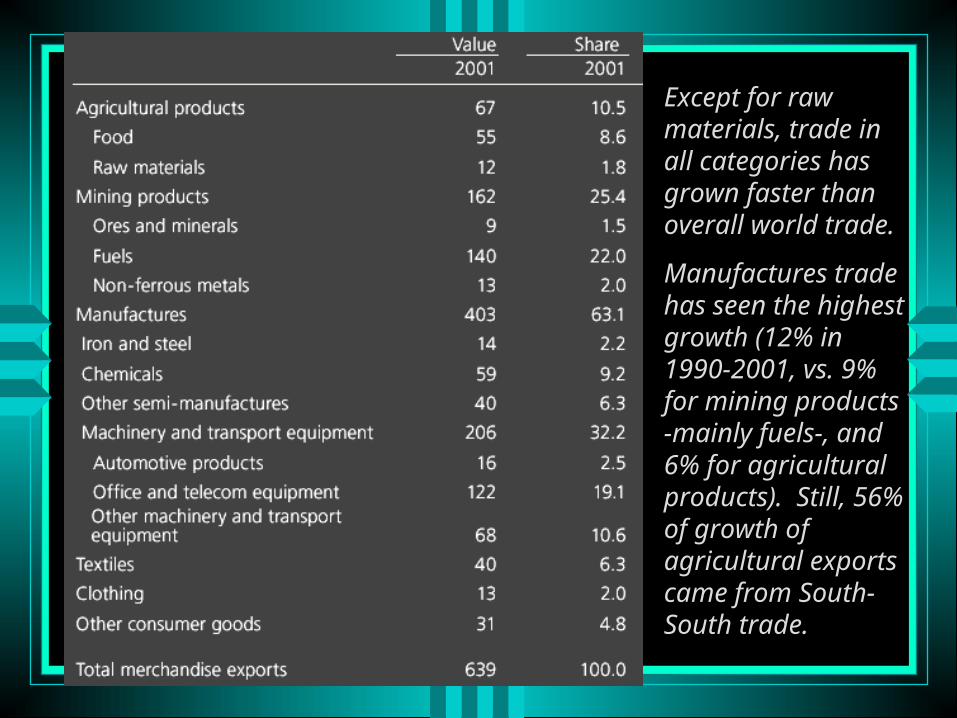

Except for raw materials, trade in all categories has grown faster than overall world trade.

Manufactures trade has seen the highest growth (12% in 1990-2001, vs. 9% for mining products -mainly fuels-, and 6% for agricultural products). Still, 56% of growth of agricultural exports came from South-South trade.

Intra-Asian trade is the major component of South-South trade, accounting for 54% of the total (345 billion US$ in 2001). For Africa, South-South exports were 36 billion US$.

%

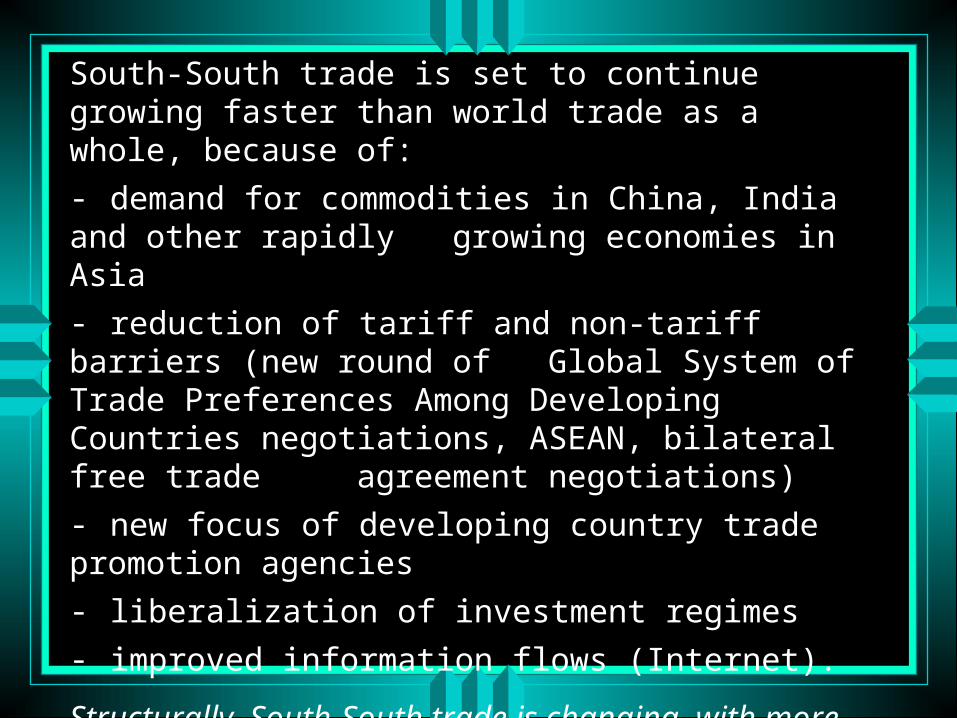

South-South trade is set to continue growing faster than world trade as a whole, because of:

- demand for commodities in China, India and other rapidly growing economies in Asia

- reduction of tariff and non-tariff barriers (new round of Global System of Trade Preferences Among Developing Countries negotiations, ASEAN, bilateral free trade agreement negotiations)

- new focus of developing country trade promotion agencies

- liberalization of investment regimes

- improved information flows (Internet).

Structurally, South-South trade is changing, with more stress on quality and timeliness: trade links are being formalized.

The needs for commodity finance will continue increasing, with trade in processed foods growing particularly fast.

Difficulties in trade finance are one of the key obstacles to South-South trade…

But for a banker, this provides opportunities.

In intra-OECD or North-South trade, it may make sense for the exporter to carry the burden of credit, as interest rates are low. But there are very few developing countries with low interest rates, and international trade finance should normally be attractive.

Source: World Bank

Finance is a major bottleneck in developing countries…

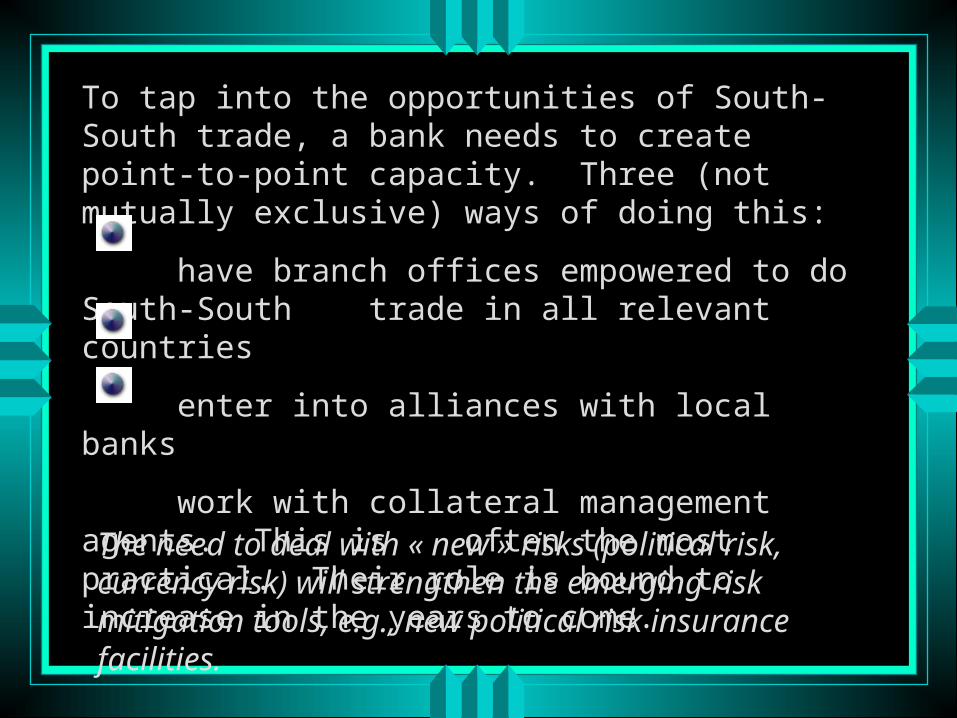

To tap into the opportunities of South-South trade, a bank needs to create point-to-point capacity. Three (not mutually exclusive) ways of doing this:

have branch offices empowered to do South-South trade in all relevant countries

enter into alliances with local banks

work with collateral management agents. This is often the most practical. Their role is bound to increase in the years to come.

The need to deal with « new » risks (political risk, currency risk) will strengthen the emerging risk mitigation tools, e.g., new political risk insurance facilities.

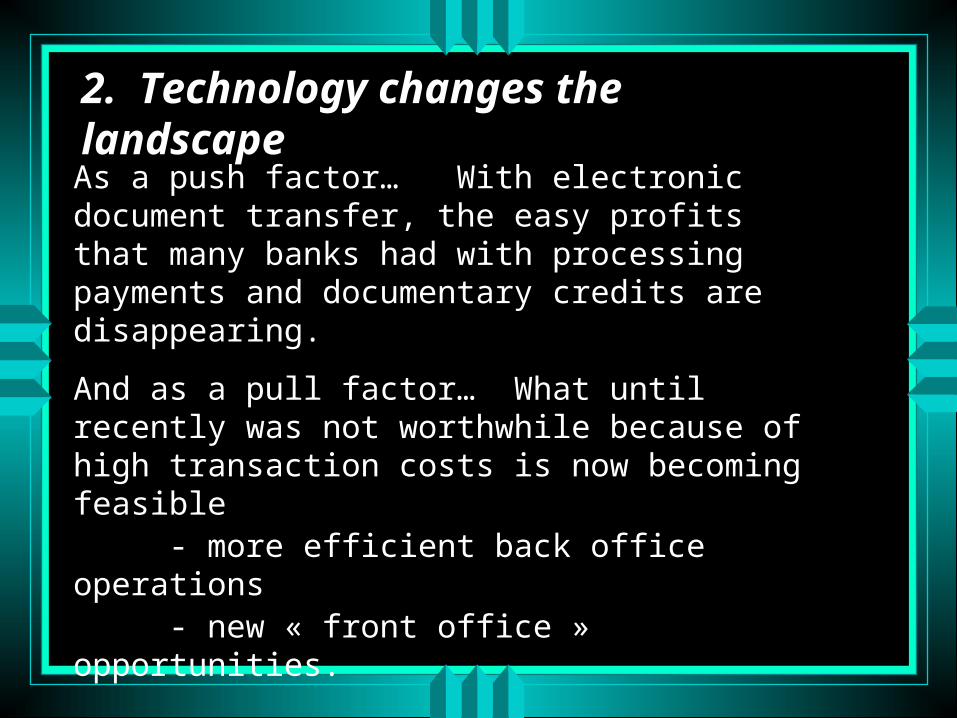

2. Technology changes the landscape

As a push factor… With electronic document transfer, the easy profits that many banks had with processing payments and documentary credits are disappearing.

And as a pull factor… What until recently was not worthwhile because of high transaction costs is now becoming feasible

- more efficient back office operations- new « front office » opportunities.

Consider the spectrum of opportunities…

How much are banks really gaining on the Cocobod, Sonangol and similar financings

….

and contrast this with

….

farmers in many countries willing to pay more than 10% a month for a loan.

Reaching small farmers is difficult; most microfinance institutions, which charges rates of some 40% a year, have hardly had any success.

But changes in underlying marketing practices (tying farmers into the organized economy) and technological developments are creating new opportunities.

Just consider where the capital market is now. Among the major categories of securitizations:- credit card receivables- automobile loans- student loans- migrant remittances

A large number of small payments is aggregated, using credit risk models

Back office opportunities come from the reduction of costs made possible by:

• Much more efficient processing of credit applications through credit scoring

• Improved internal communications

• Electronic payments technologies

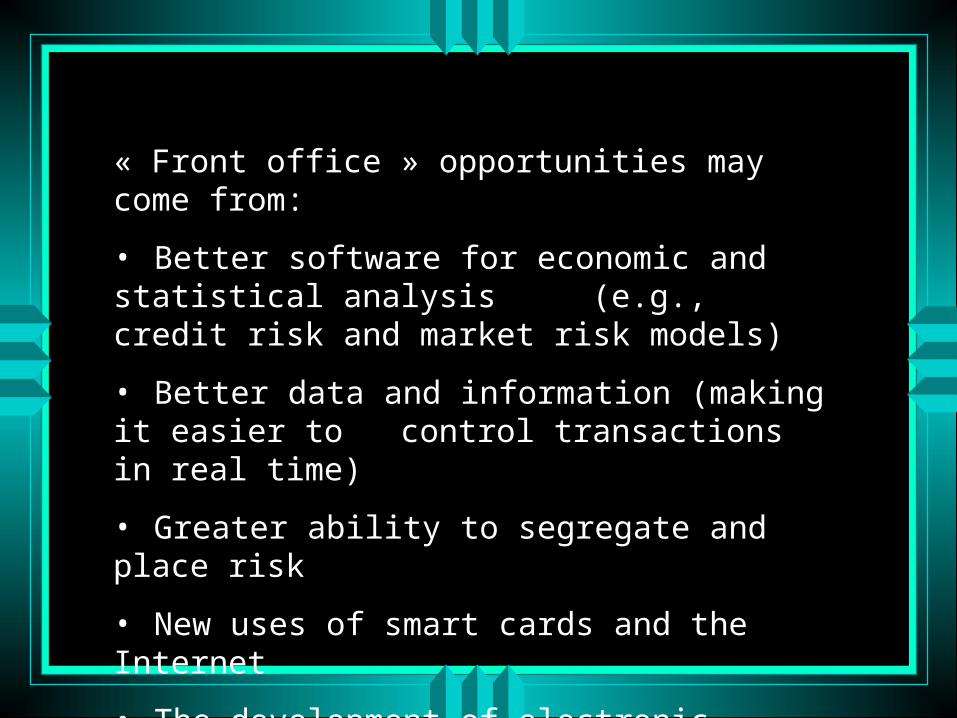

« Front office » opportunities may come from:

• Better software for economic and statistical analysis (e.g., credit risk and market risk models)

• Better data and information (making it easier to control transactions in real time)

• Greater ability to segregate and place risk

• New uses of smart cards and the Internet

• The development of electronic market places

Better data and information create new opportunities

For example, the Grading on Site (Go-S) system offered by SGS in grain trade:

- identifies, grades and segregates grains; thereafter,

- allocates such grains into pre- determined bins; and

- tracks their movement up to exit of the storage.

Some collateral managers have already created electronic access for their clients to their warehouse receipts and other parts of the trade flows that they are managing.

Source: SGS. The stars indicate possible SGS intervention points.

Go-S allows bankers to track, on a real-time basis, grains as they enter into warehouses, are charged into rail wagons, etc.

Better systems for gathering data and providing information to financiers will create a much better range of options for bankers.

They no longer have to go for full collateral control (which can be expensive), but rather, combine real-time information on physical commodity flows with stronger control over the commodities in critical parts of the chain.

« One point » financing (goods in a warehouse) may well become obsolete (except where storage is in itself the objective, e.g. food or fuels security stocks).

Greater ability to segregate and place risk

Various developments (new insurance tools, better understanding of risks, more savvy institutional investors) have made it possible to « syndicate » deals not horizontally (with each participant taking a tranche of the deal), but vertically (with each participant taking a part of the risk, with concommitant returns).

This can make it possible for deals to pass a bank’s internal hurdles, in terms of risk-adjusted rates of return.

Highest risk tranche

Mezzanine tranche

Low-risk tranche

Kept by bank/trader

High risk investors

Institutional investors4/5 at 10%

rate of return

1/10 at 20%

40%

14%

Use of new risk management tools enables risk segregation.

Smart cards and the InternetAn example from rural India: the InfoThela

It is basically a pedal driven vehicle just like a common cycle rickshaw and there will be a personal computer on board which will be connected to internet using wireless technology. It is designed keeping in mind the village conditions in the country where electric power is not available all the time. So a pedal generator is designed in such a way that while pedaling, the battery will keep on charging for running the on board computers and equipments.

The InfoThela can provide an Internet Wi-Fi Network in a radius of some 20 km around the nearest Internet access point, without access charges.

5 - 8 Km

MetroInternet

Village

802.11b range extensionusing directional, home grown,custom made antennas

802.11b range extensionusing directional, home grown,custom made antennas

Internet access for InfoThela within 0.5 Km radius of the village center

Internet access for InfoThela within 0.5 Km radius of the village center

Further range extensionusing multi-hopping

Further range extensionusing multi-hopping

Alternate path routingfor high reliability

Alternate path routingfor high reliability

On this platform, an electronic trading and financing system can be built. Salient features:

Biometric identification-based

dematerializing of warehouse

receipts: easier to use, cheaper, and more secure Human-ATM: workers from Micro Finance Corporations

go on InfoThela to villages and do the identification, disburse loan etc.: saves on the costs of ATM

The integration of futures trading automatically solves key issues of price smoothening and giving some predictability to farmers’ sales prices.

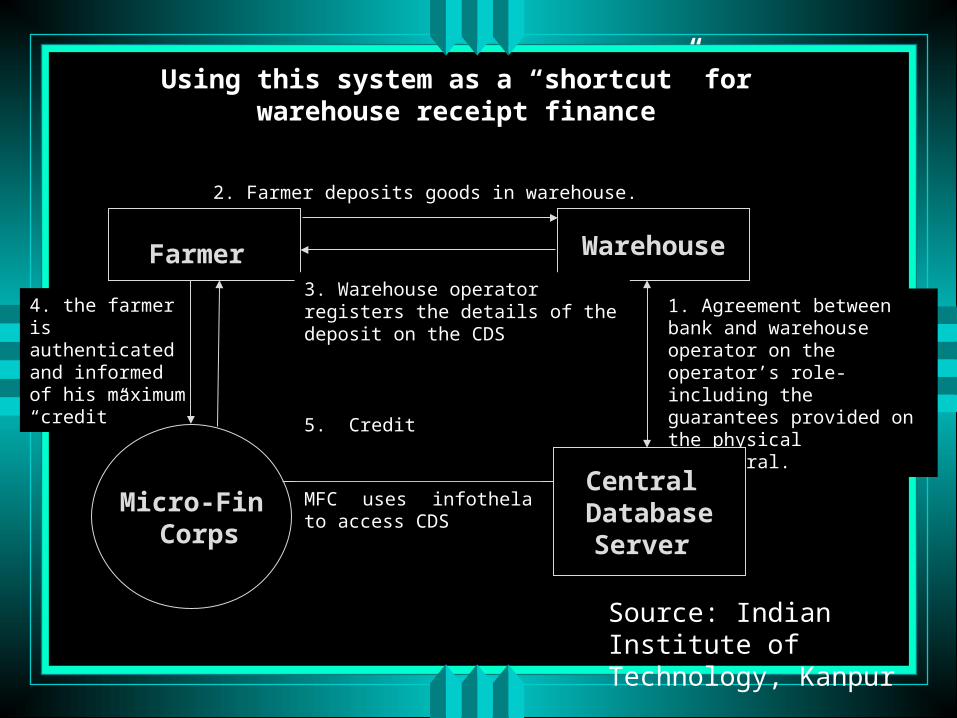

Using this system as a “shortcut” for warehouse receipt finance

2. Farmer deposits goods in warehouse.

1. Agreement between bank and warehouse operator on the operator’s role-including the guarantees provided on the physical collateral.

4. the farmer is authenticated and informed of his maximum “credit”

WarehouseFarmer

Central DatabaseServer

Micro-Fin Corps

3. Warehouse operator registers the details of the deposit on the CDS

5. Credit

MFC uses infothela to access CDS

Source: Indian Institute of Technology, Kanpur

An example

Harvilas Singh wants to sell 10 tons of soybeans in January He deposits the soybeans in the warehouse at Hapur where he is registered He is authenticated by his id and fingerprint His produce is graded by inspectors Details entered, through the infothela into Central Database Server (CDS) ,

in his account are

• Type of commodity

• Quality, quantity

• Date of deposit, Date of expiry

• Commodity code identifying warehouse and location inside the warehouse

Source: Indian Institute of Technology, Kanpur

Harvilas Singh wants money urgently He approaches the Micro-Finance Corporation (MFC) He is authenticated using infothela and details of his assets

are available to the MFC MFC checks up the CDS for current average market price

and calculates maximum credit limit for Harvilas Singh Based on credit limit loan is given Details of loan are entered into the system The transaction is re-authenticated in a non-repudiable

manner (e.g., finger print scanner)

Smart card and internet-based systems of this nature can act as aggregators of financing needs.

The whole can then be (re-)financed by banks or on the capital market.

The scope for these applications is increasing fast, in particular as farmers are being tied into formal networks, e.g., for the sale of equipment, the provision of inputs, or the marketing of their products through contract farming arrangements.

(and similar developments can be seen in livestock/poultry and fisheries markets).

You see things and say “Why?” But I dream things that never were, and I say “Why not?”(George Bernard

Shaw)

Electronic trading platforms (e.g., commodity exchanges) have to set up mechanisms to secure the transactions arranged through the platform.

The goods concerned may be in the “transaction pipeline” for a reasonable period.

Banks should consider evaluating the mechanisms, and if OK, provide “automatic” financing for “goods in the pipeline”.

The organization of electronic market places

BuyerB2B-exchange-

approvedwarehouse

Buyer makes successful bid

This system has been implemented in an Asian exchange. A seller puts his products into a warehouse approved by the B2B exchange. The offer is put on the web, and a buyer successfully bids. He pays 20% of the value, and if he wishes, a bank that cooperates with the B2B exchange automatically finances the remaining 80% (so that the seller can be immediately paid). As long as the goods are in the warehouse, the finance remains in place.

The bank relies on the creditworthiness of the B2B exchange and its clearinghouse - there is less work and less credit risk than when lending through individual loans to traders.

Goods come “packaged” with automatic financing possibility

On the other hand, electronic market places can dis-intermediate banks, by directly linking holders of commodity « stocks » with the capital market.

E.g., in Colombia and Venezuela, large and small investors bid, on the countries commodity exchanges, for the right to finance commodities, e.g.

- commodities in storage (cotton, grains, sugar)

- livestock and poultry being prepared for the market.

The exchange builds in safeguards, similar to what one would do for a securitization. And the cheapest financier gets the deal…

In times of change, learners inherit the Earth, while the learned find themselves beautifully equipped to deal with a world that no longer exists.

Eric Hoffer

THANK YOU