the future of corporate mobile banking

DESCRIPTION

The Future of Corporate Mobile Banking. January 25, 2012. Jacob Jegher Senior Analyst Celent Banking Event, Boston. Agenda. Why mobile, why now? Is corporate mobile banking safe? The convergence of online and mobile Corporate mobile solutions and capabilities X. Why mobile, why now?. - PowerPoint PPT PresentationTRANSCRIPT

© 2012 OLIVER WYMAN

FINANCIAL SERVICES

Jacob JegherSenior Analyst

Celent Banking Event, Boston

January 25, 2012

The Future of Corporate Mobile Banking

2© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC. April 19, 2023

1. Why mobile, why now?

2. Is corporate mobile banking safe?

3. The convergence of online and mobile

4. Corporate mobile solutions and capabilities

X

Agenda

3© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC. April 19, 2023

Why mobile, why now?

4© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC. April 19, 2023

Why mobile, why now?

• Mobile is a natural fit in the corporate and business banking space:– Users have the devices (smartphones and possibly tablets)– Users are paying for data plans

• Not all business users are destined to be mobile banking users– Persona/role based. e.g. Great for traveling executive, poor for office based junior

employees– Great for small business owners

• Financial institutions are increasingly emphasizing their business customers, particularly in an unprofitable retail banking climate

• Banks have learned a tremendous amount from their retail mobile banking initiatives and can apply learnings to the business space

5© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

Corporate mobile banking is immature but will become mainstream

April 19, 2023

2007 2008 2009 2010 2011

Bank Announcements – PNC, Union Bank,

Citizens, etc.

Wells Fargo launches CEO Mobile

Ph

as

e 1

Ph

as

e 2

Ph

as

e 3

Early Adopter Financial Crisis; Reprioritization;

Consumer Mobile Emphasis

Becoming Mainstream

Celent publishes Corporate Mobile Report

Source: Celent

6© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

Wells Fargo was the pioneer. A handful of other banks have only recently jumped into the market

• With mobile banking:

• Global commercial banks with mobile payments initiatives:

April 19, 2023

7© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

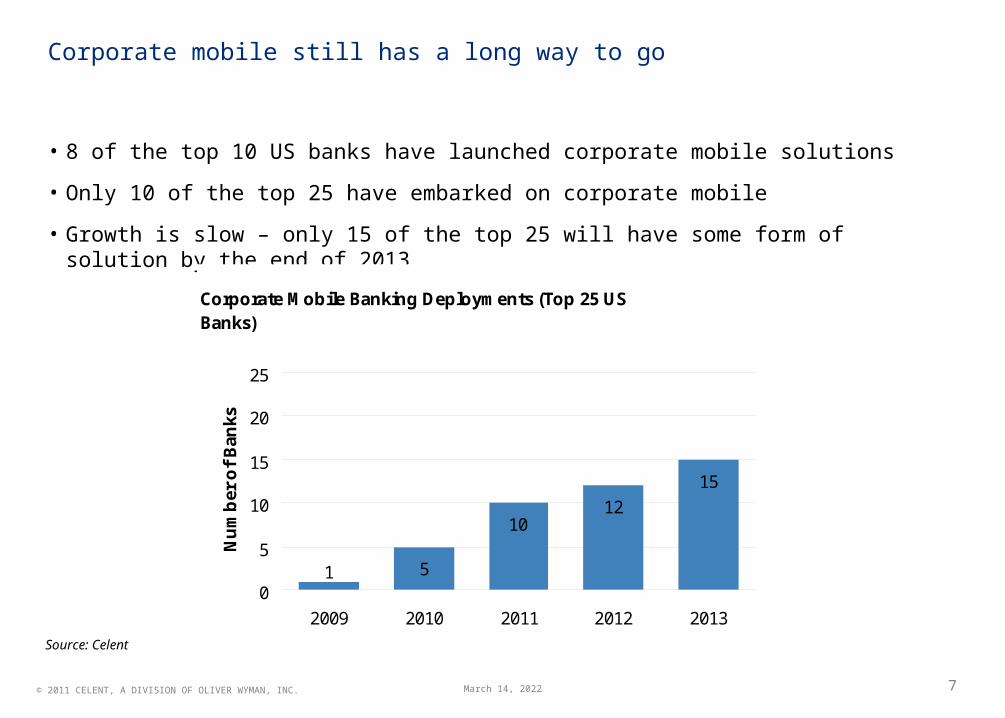

Corporate mobile still has a long way to go

• 8 of the top 10 US banks have launched corporate mobile solutions

• Only 10 of the top 25 have embarked on corporate mobile

• Growth is slow – only 15 of the top 25 will have some form of solution by the end of 2013

April 19, 2023

Corporate Mobile Banking Deployments (Top 25 US Banks)

5

10

1512

10

5

10

15

20

25

2009 2010 2011 2012 2013

Num

ber

of Ban

ks

Source: Celent

8© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

In consumer banking, the “triple play” has become an accepted standard. The browser still dominates for corporate mobile banking

• Triple play is standard fare in consumer banking:– Mobile browser– App– Text

• In corporate banking, the majority of banks have opted to focus on the mobile browser:– Simpler and less expensive to deploy– Friendly to a variety of devices and form factors

• Banks are already graduating to application deployment for:– iOS– Android– Blackberry

• Will HTML 5 web apps take over from native apps?

April 19, 2023

9© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

The browser dominates, apps are starting to emerge (top 25 US banks)

April 19, 2023

Modalities Deployed for Corporate Mobile Banking

0

0

2

3

5

0

0

0 1 2 3 4 5 6 7

Triple play

App and text

Browser and text

Text only

Browser and app

App only

Browser only

Number of Banks

Source: Celent

10© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

iPhone apps reign supreme (top 25 US banks)

April 19, 2023

Native Apps Deployed by Operating System

0

0

0

2

3

0

0

0 1 2 3 4 5

Blackberry only

Android only

Android and Blackberry

iOS and Blackberry

iOS and Android

iOS, Android, Blackberry

iOS only

Number of Banks

“The overwhelming majority of my corporate clients have Blackberries.”

– Senior Executive, Top 5 US bank

Source: Celent

11© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC. April 19, 2023

Is corporate mobile banking safe?

12© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

Is mobile banking safe?

• For now mobile banking appears to be safe. Banks and corporates can’t rely on this short sighted approach

• Celent believes that mobile banking fraud is going to explode – It’s not a question of if– It’s a question of who will be targeted, when, and how

• Banks must take a multilayer approach and have a safety net in place (e.g. behavior/transaction monitoring)

• Banks must enforce an entitlements structure and separation of duties. This must be carried over into mobile experiences

April 19, 2023

13© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

Will alternative authentication mechanisms kill the good old token?

• Celent believes that the trusty token has been reduced to a measly sentry

• Sophisticated attacks (e.g. zeus trojan) have demonstrated the ineffectiveness of multifactor authentication in general

• A physical token is too much of a bother, particularly for those saddled with token necklaces

• Out of band authentication (e.g. one time password via text message) and soft tokens (mobile app) will replace the hard token

April 19, 2023

14© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

Apple’s Siri has the potential to change mobile banking

• Voice recognition tools have been around for ages, they just haven’t worked very well

• Ford is heavily promoting voice control in it’s vehicles with SYNC (recognizes 10,0000 voice commands)

• Apple’s Siri has the potential to bring voice control to the masses

• It’s still in beta so too soon to tell if it will be a hit or not. Early reviews are mixed

April 19, 2023

15© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

Voice authentication for the mobile is on its way

April 19, 2023

AuthenticationApp

InteractivityTask control

Basic voice recognition

1 32 4

• “Call Karen”• Dictation of a

document or email

• Natural language Q&A

• Integration with other apps (e.g. banking)

• Book calendar appointment

• Read out an email or text message

• For mobile banking• For online banking• For telephone

banking• For out of band

confirmations (e.g. call back)

1 2 31 2 431 21 2 31 2 431 2

Source: Celent

16© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

Gesture based authentication is another solid option for mobile devices and tablets

April 19, 2023

iPhone Android

If it was built by humans it can be broken or bypassed by humans

17© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

“Bring your own device” is a misnomer

• Device “crippling” kills the convenience

• Users often desire their own separation of duties

• It’s a nightmare for firms to support and manage a wide range of devices

• Policies and user education have to be in place with regards to personal devices– It’s next to impossible to enforce

April 19, 2023

18© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC. April 19, 2023

The convergence of online and mobile

19© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

An ideal scenario would be for the bank to be able to house all of its electronic banking components in a single place

Full Solution

Bite Sized

Selective / Full

Module A

ModuleD

Electronic Banking Platform

ModuleB

ModuleC

Source: Celent

April 19, 2023

20© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC. April 19, 2023

Users expect to pick up any device and have the appropriate experience. The

burden is on the bank to provide it.

Corporate triple play = web, app, desktop

21© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

This convergence is becoming apparent in the consumer space as desktop apps gain steam

April 19, 2023

22© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

Tablets wars: online and mobile banking will never be the same – 1

• iPad mania has swept the globe. Android based Honeycomb tablets are starting to pop up like weeds. The Blackberry Playbook was launched recently to mixed reviews

• Is banking on a tablet considered online banking or mobile banking? The answer is both and neither

• Do tablets impact consumer banking, small business banking, or corporate banking? The answer is all of the above

April 19, 2023

23© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

Tablets wars: online and mobile banking will never be the same – 2

• Tablets are going to have a massive impact on corporate and business banking:– Senior executives are on the go– Senior executives like fancy toys– Online banking portal evolution is a natural fit with the tablet experience

• Several questions for banks to answer:– What brand of tablet is going to steal the heart of business users?– Should banks build native apps or rely on the browser?– What OS should banks be developing for?

April 19, 2023

24© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

The tablet will act as a catalyst to the redesign of online cash and treasury management

• Celent believes that banks and software vendors are on course to provide an online banking dashboard, and the tablet will be one of the catalysts.

• Tablets will:– Contribute to the design and user experience of online banking dashboards– Speed up financial institutions’ interest in an online banking dashboard– Help banks recognize that online banking, tablet banking, and mobile banking require a

common framework

• Whether banks choose to deploy native apps or showcase online banking in a browser, the tablet is acting as a catalyst to the redesign of online banking

April 19, 2023

25© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC. April 19, 2023

Corporate mobile solutions and capabilities

26© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

Corporate mobile isn’t meant for everyone

• Role based

• Consumer mobile = mass marketCorporate mobile = selected users

• Leverage entitlements infrastructure and hierarchy in place for the online channel

• Corporate administrators assign mobile capabilities to specific roles/groups/users

April 19, 2023

27© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

Banks should determine mobile requirements by surveying customers

• Challenge is determining what customers will want 2-3 years out

• Customers have strong opinions that banks should obviously take into consideration and prioritize

• Banks should be developing functionality and emphasize usability elements that they think customers will be asking for. Guidance should also come from:– Bank employees – Research analysts– General online and mobile trends (outside of financial services)– Software vendors

April 19, 2023

“Don’t go where the puck is, go where the puck is going to be.”

– Mark Tabrum, Director of USA Hockey’s Coaching Education Program

28© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

Banks must deploy the right mix of functionality while respecting online banking entitlements infrastructure

April 19, 2023

Fundamental Requirements Nice To Have• Informational

– Customizable alerts– Balances, account info– Transaction details, search, filter

• Managerial– Payment approvals– Positive pay decisioning

• Transactional– Transfers (all business accounts)

• Customer service– Call my banker, send email/open ticket– Branch locator

• Informational– Alerts (loan and card accounts)– View check images– Basic information reporting– Purchase card reporting

• Managerial– Stops

• Transactional– Payment initiation (existing template) – Remote deposit capture (RDC)– Investments

• Customer service– Video chat

ILLUSTRATIVESource: Celent

29© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

Celent recommends a phased approach to mobile corporate banking

• It’s impossible to conquer corporate client requirements in a one fell swoop– Select devices to support– Select modalities – Select features/capabilities for initial release and build out a product roadmap– Tie features to user roles– Tie features and user roles to device type (tablet or mobile)

• Alerts alone are not mobile banking. They are a building block to a range of other mobile services

April 19, 2023

30© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

The vendor landscape is expanding. Corporate mobile requires a lot more than viewing account balances

• Only a handful of vendors are ready to deploy mobile banking solutions:

• Other solutions are forthcoming from:– Internet banking vendors– Consumer mobile banking vendors– Systems integrators

April 19, 2023

31© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC.

The million dollar question – can banks charge for business or corporate mobile banking?

• Celent believes that banks should not charge their customers (directly) for corporate mobile banking– Mobile is simply an additional delivery channel, one that banks cannot ignore– Monthly account fees and per transaction pricing should be consistent regardless of

electronic delivery channel chosen by customer

• Banks want to enable their customers on as many self-service channels as possible

• Charging for mobile will hinder adoption. Counterintuitive to goals of driving transaction volume and activity, relationship building

• Banks will have a difficult time justifying project investment and ROI in the short term. Business cases should emphasize:– Customer retention– Customer satisfaction– Fraud prevention– Transaction volume– Relationship building (mobile marketing)– Packaged pricing

April 19, 2023

32© 2011 CELENT, A DIVISION OF OLIVER WYMAN, INC. April 19, 2023

Jacob JegherSenior Analyst

[email protected]: @jjegher

Thank You