the future of fintech: crystal balls and tasseography

TRANSCRIPT

The Future of FintechCrystal balls and tasseography

What is Fintech?

• Fintech is the innovative application of technology and ideas to banking, trading, and financial services• Many people think Fintech is just payments

• But what about capital markets and the Fintech around it?

• Three overall components include:

1) Payments, payment tech, retail tech (ATMs) are all one segment of the consumer bank

• Very large component because it is physical

2) Traditional banking, such as consumer lending has moved to heavy iron (cloud computing and corporate intranet)

• What they do internally is increasingly important relative to outside customer base

• Insurance / reinsurance - services that relate to consumer funds (for risk management)

3) Capital markets, investment markets, trading (all of which is a legion of tech)

Fintech Structure – Innovation ComponentsConsumer Bank Commercial Bank Investment Banking Wealth and Investment Mgt General

Payments Credit Analytics (ZestFinance)

Algorithms Robo advisors (Wealthfront, Nutmeg, Betterment)

Security (IDGate)

P2P Lending Education lending (CommonBond)

Visualization, analytics Thematic investing (Motif) Mass storage

Crowdfunding Working Capital solutions (Marketinvoice)

New Exchanges (Second market)

CRM tools HTML 5 and Web 2.0

Mobile Banking Market surveillance tools –monitor client flow (Nasdaq)

Quantum Computing (QxBranch)

Robo-investing Prediction - AI Secure ID’s , remote devicesecurity

Alt Currency Conversion to e-Platforms (Electronifie, Bondcube,TruMid)

Data driven marketing

Investment banking changes

• In terms of where things currently are: • Regulatory overhang globally on trading businesses

• Most institutions have spent a lot of money on compliance (Basel, MiFID, Dodd-Frank, EMIR)

• Thus a lot of non-revenue generating investment has gone to “Fintech” • Into systems to update for reporting, business conduct

• This has been an opportunity cost: has displaced a lot of investment in other revenue generating technologies

• Number of 3rd parties, such as ClearPar, one of many entities that sits in the middle because the space has inefficiencies

Investment banking changes cont’d

• Front office: • Investment in “speed” (speed of light) no longer driver of investment – marginal cost

of investment far too expensive for upside• There have been two phases of algorithms for sophisticated price management and

execution• First was price makers and their ability to serve high frequency clients to help gain volume• Second was algo’s for trade excecution to lower cost of trade• The last couple of years algos have really incorporated intelligence venue selection per trade,

asset allocation, geographic market advantage, and predictive capabilities. • Next wave could capitalize on that along with ability to attract retail flow.• Aggregation, real big struggle between banks and end user execution now that customer has

multiple choices (FX space: Tradeweb, 360T, Citi; who's customer is it?)• All of that has occurred over the past several years; banks are now playing the game of Orbitz

(“it is just channels”)

Raja’s Tea Leaves: Several other drivers at banks• Regulatory impact has put a hold on some of these trends and as a result innovation has moved into these banks

(e.g., algos for market makers)

Peering into the future:

• These venues will have to be commercial bank friendly, align with credit issuance, take on and issue debt (interest rates areglobally low, constant churning of bond syndication because it is cheap)

• Many originators of debt are going to push that, banks will get more of it

• FX has had consolidation with increasingly more activity around the exchanges

• Consolidation around multiparties around bonds (fixed income), commodities, options platforms are independent and the “last bastion” (haven't changed the flow because of regulations)

• Analytic platforms and heavy move towards Web 2.0, HTML 5

• Ongoing need for algorithmic as speed is less of an issue due to costs; tech that will enable multiplatform trading management

• Banks that trade on venues that have "last look" -- have last look before they price, creates a greater equality if this goes away (this will favor market makers like Virtu as they don’t have cost overhead associated with banks – lower spreads)

• Banks will have to create better adapters because as spreads widen a bit, costs will be absorbed by customers (could lead to cost efficiency, rebating)

• This also cover the front office (portfolio management, big databases, regulatory implementation)

• Next 2-3 years “last mile of regulatory implementation,” systems are fairly compliant, now is just more of an increment

• The next 5-7 years: improving their web infrastructure, cost containment (potentially where some type of blockchain(s) could be used to reduce costs?)

Consumer banking

• Where all the buzz and buzzwords are around:• Crowdlending, microtransactions, cross border payments, peer to peer tech

• Open question as to whether P2P lending sustainable due to lack of robust credit ratings (e.g., subprime borrowers incentivized to take out loans they cannot repay in China and UK)

• Big banks will buy the innovation (acquisition of startups) and whatever “network effect” these startups had

• Consumer base is willing and ready to work with this (ApplePay, Square Cash)• Banks will want to build inroads on traditional processors for consumers• Will be based on growth markets such as Eastern Europe, India, Latin America• “Intelligent bots” (like Wealthfront) will work with price sensitive investors who do not want to pay

heavy management fees• Get bots that pick the stocks based on risk profiles• E.g., if you're geared towards stocks that grow at 4-6%, multiple venues to track this based on risk profile

• This type of institutional logic coming down to retail level; firms like Schwab, eTrade and Fidelity are already fairly sophisticated (and increasingly automated)

• (Note: it may ultimately be deemed unorthodox and unrealistic to include investment firms under “consumer banking” and not under “investment management.”)

So you are an entrepreneur or run an in-house incubator?

“Assume a can opener”

• Who are the first adopters: banks, funds, insurance?

• What do they specifically want to do, what is the use-case? (e.g., instant clearing and settlement of OTC derivatives and FX trading)

• How is it currently done?

• What is the problem with how it is currently done? (Very important)

• What are the available solutions such as technologies?

• How to pilot and build proof of concept?

• How to implement?

• How to scale?

• Is there a revenue model, or do these just reduce costs?

Is disaggregation the new normal?

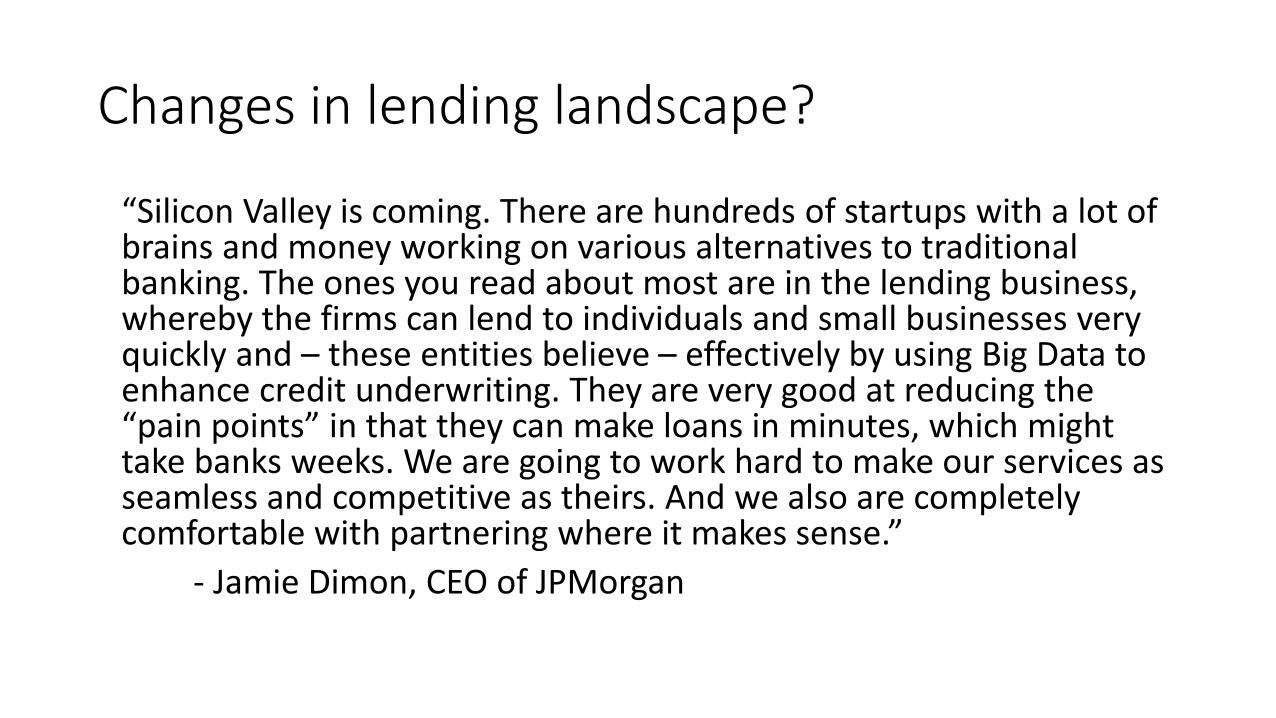

Changes in lending landscape?

“Silicon Valley is coming. There are hundreds of startups with a lot of brains and money working on various alternatives to traditional banking. The ones you read about most are in the lending business, whereby the firms can lend to individuals and small businesses very quickly and – these entities believe – effectively by using Big Data to enhance credit underwriting. They are very good at reducing the “pain points” in that they can make loans in minutes, which might take banks weeks. We are going to work hard to make our services as seamless and competitive as theirs. And we also are completely comfortable with partnering where it makes sense.”

- Jamie Dimon, CEO of JPMorgan

The Fintech landscape a year ago in March 2014

… as of December 2014 …

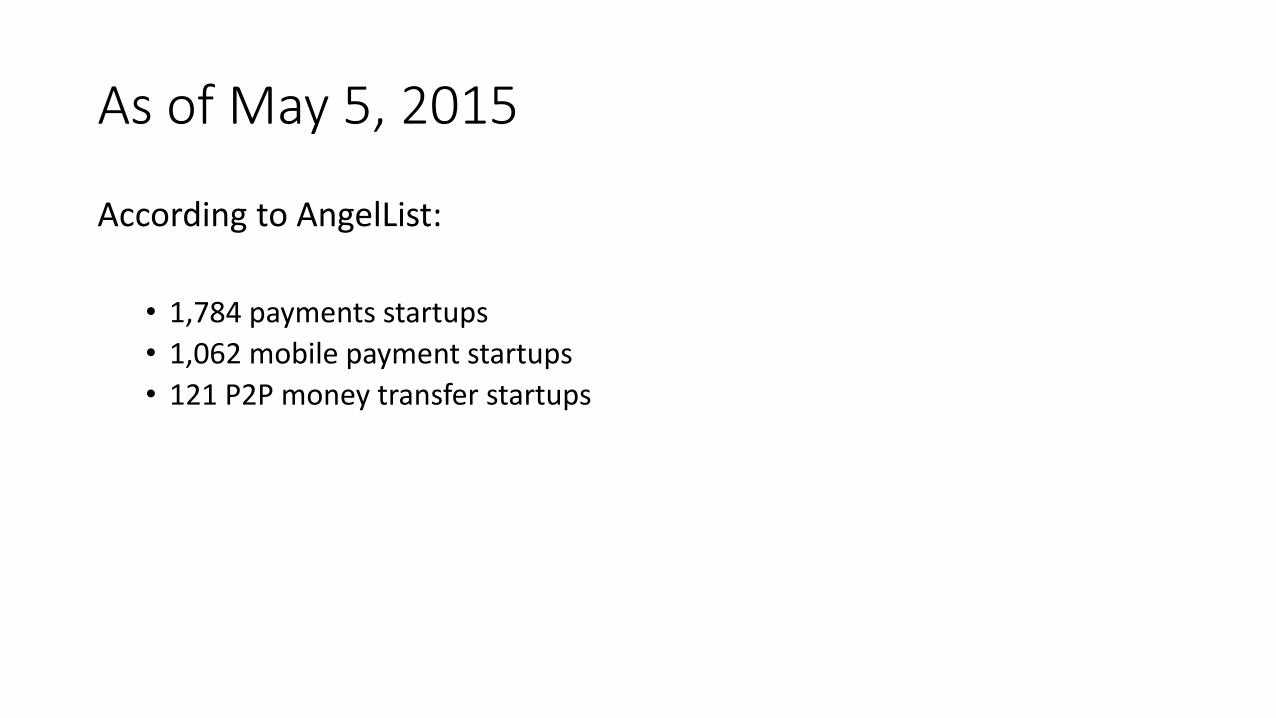

As of May 5, 2015

According to AngelList:

• 1,784 payments startups

• 1,062 mobile payment startups

• 121 P2P money transfer startups

But… but blockchains! Right?

Minimal to maximal future scenarios

• There’s the minimalistic consumer Bitcoin company. They do something minimal like provide a way to convert your airlines miles into bitcoin, or provide a toolbox to access bitcoin markets with some API. They use Ruby on Rails and node.js.

• There’s the less minimalistic but still single focused financial Bitcoin company. They have former bankers as founders. They give you an expensive way to buy bitcoin that makes institutional clients comfortable.

• There’s the maximalists that want to airlift capital and labor away from New York and London with 3D printed drones paid for and powered with bitcoin. Sandhill VC’s watch through their Oculus-powered goggles as Washington DC slips off into the Atlantic all while drinking Soylent in their robotically chauffeured Uber vehicles, all of which is paid for with bitcoin.

Min to max con’td

• There’s the Fintech company that wants to target the unbanked. They offer services based on bitcoin but they're thinking about using Stellar. The founders have trust funds and they love to talk on conference panels and attend Burning Man.

• There’s the Fintech company that wants to bring blockchain technology to the mainstream. They are forking a cornucopia of projects. God forbid they be mistaken as a currency, they are a software company. Or middle-ware. They use the words “stack“ and “disrupt” a lot.

• Cryptosingularity: protocol research and development continues by the Young Turks (Zerocash, Ethereum, Tezos, Hyperledger, Tendermint, Augur) until Metalic Boterin -- the mothership -- recalls its fully formed AGI progeny, Vitalik Buterin. Everyone speaks Esperanto.

Consequently some of the funded projects seem like they came from: Butwithbitcoins.com

What might really happen?

The fate of blockchains?• Bitcoin survives as a regulated asset class for a few years, but doesn’t quite take

off. No other cryptocurrency retains any substantial market share. No one buys a Wi-Fi mining “toaster.” Washington DC stays above sea level.

• No one on Wall Street bothers with the swap startup or graph/API. As soon as (and if) there is regulatory clarity, they replicate those services because they already know how to do this.

• One or two “Universal” buckets survive by replicating and offering every virtual currency service available but fiat-related services remain their dominant revenue source. They are like a cross between Venmo and Beenz.

• Developing world scenario: the unbanked somehow acquire smartphones and use a Stellar-like service operated by the local phone company that curates a variety of apps around it.

• Developed world scenario: after a few years of playing with the tech, a bank decides to use some kind of blockchain, but internally. They end up not really seeing the point, the project is scrapped. Silicon Valley is auctioned off by monocle-wearing New York and London yacht owners navigated by humans eating caviar and smoking cigars.

What is actually happening on-chain?

Are many cryptocurrency-focused companies simply just window and tire companies?“I would say that your general characterization of some in the space is correct. But if you had a really good idea about how to build a better tire for an automobile, you would probably be really interested in talking to the auto companies because they are the people that ultimately are going to make use of your technology. You could think that maybe, because of the power of your tire, there might emerge a whole new brand of auto companies that supplant the General Motors of the world because the incumbents never really got the whole concept of what a good tire should be all about. But I’m not sure that would be a good move.”

• Blythe Masters (formerly JPMorgan now at DAH)

Mixing dry code with wet code

According to Deutsche Bank: measured as a percentage of revenues, financial services firms spend more on IT than any other industry. Banks’ IT costs equal 7.3% of their revenues, compared to an average of 3.7% across all other industries surveyed.

[Note: to understand and use this tech you do not necessarily need to set up an office in SOMA/Mission District, additional innovation can and will continue exist outside hipster corridors]

Are shared, replicated ledgers part of the future? Can they help reduce costs?

What are some replicated ledger projects in the Fintech space?

Is it only a binary choice between permissionedand permissionless ledgers? How much co-existence and cooperation will occur between the two ecosystems?

Or is the future something else entirely?