the geopolitics64be6584f535e2968ea8-7b17ad3adbc87099ad3f7b89f2b60a7a.r38.cf2.rackcdn.com/...access...

TRANSCRIPT

Finding Petroleum – Russia and the FSU London 18 June 2013

The Geopolitics

Julian Lee

Senior Energy Analyst Centre for Global Energy Studies

The good bits

Stable government Stable currency Wide range of opportunities available Widespread infrastructure in core areas Well educated staff Low entry and holding costs 20

22

24

26

28

30

32

34

36

38

Jan-0

5

Jul-0

5

Jan-0

6

Jul-0

6

Jan-0

7

Jul-0

7

Jan-0

8

Jul-0

8

Jan-0

9

Jul-0

9

Jan-1

0

Jul-1

0

Jan-1

1

Jul-1

1

Jan-1

2

Jul-1

2

Jan-1

3

Rubles per US Dollar

Restrictions

Legal restrictions on foreign company access to ‘strategic’ deposits >= 70 mn tonnes (500 mn bbls) oil >= 50 bcm gas Offshore (shelf) deposits reserved for Rosneft and Gazprom Core oil areas are tightly controlled by Russian majors (Rosneft, Lukoil, Gazprom Neft, Surgutneftegas) Although under attack, Gazprom retains its monopoly on gas exports from Russia. This may be undermined, but only for LNG and only in a very controlled way.

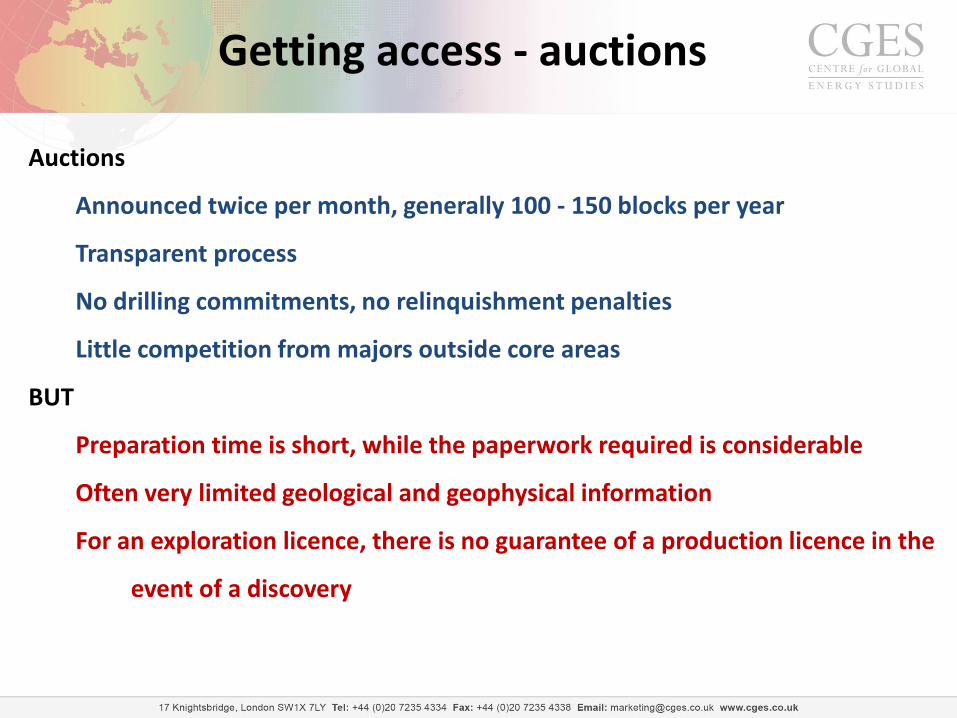

Getting access - auctions

Auctions

Announced twice per month, generally 100 - 150 blocks per year

Transparent process

No drilling commitments, no relinquishment penalties

Little competition from majors outside core areas

BUT

Preparation time is short, while the paperwork required is considerable

Often very limited geological and geophysical information

For an exploration licence, there is no guarantee of a production licence in the

event of a discovery

Getting access - acquisitions

Little transparent M&A activity

Few truly independent companies

Cultural resistance to foreign ownership

Lack of standard reporting practices, making valuation difficult

Strict controls of acquisition of more than 20% of enterprises involved in the development of ‘strategic’ deposits

There are a number of foreign listed independent companies operating in Russia and Kazakhstan

Getting access - jvs

There have been some successful jvs

Salym [Shell & Sibir (now Gazprom Neft)]

Samara-Nafta [Hess & Simon Kukes]

There have been some very unsuccessful ones

Naryanmarneftegas [ConocoPhillips & Lukoil]

Offshore:

Deep pockets required !

Access to overseas projects is also a bonus

-

10

20

30

40

50

60

Jan-02

Sep-02

May-03

Jan-04

Sep-04

May-05

Jan-06

Sep-06

May-07

Jan-08

Sep-08

May-09

Jan-10

Sep-10

May-11

Jan-12

Sep-12

'000 bpd

Source: Argus, EIG & CGES

-

20

40

60

80

100

120

140

160

180

200

Jan-02

Sep-02

May-03

Jan-04

Sep-04

May-05

Jan-06

Sep-06

May-07

Jan-08

Sep-08

May-09

Jan-10

Sep-10

May-11

Jan-12

Sep-12

'000 bpd

Source: Argus, EIG & CGES

-

20

40

60

80

100

120

140

160

180

Jan-02

Sep-02

May-03

Jan-04

Sep-04

May-05

Jan-06

Sep-06

May-07

Jan-08

Sep-08

May-09

Jan-10

Sep-10

May-11

Jan-12

Sep-12

'000 bpd

Source: Argus, EIG & CGES

Assessing opportunities

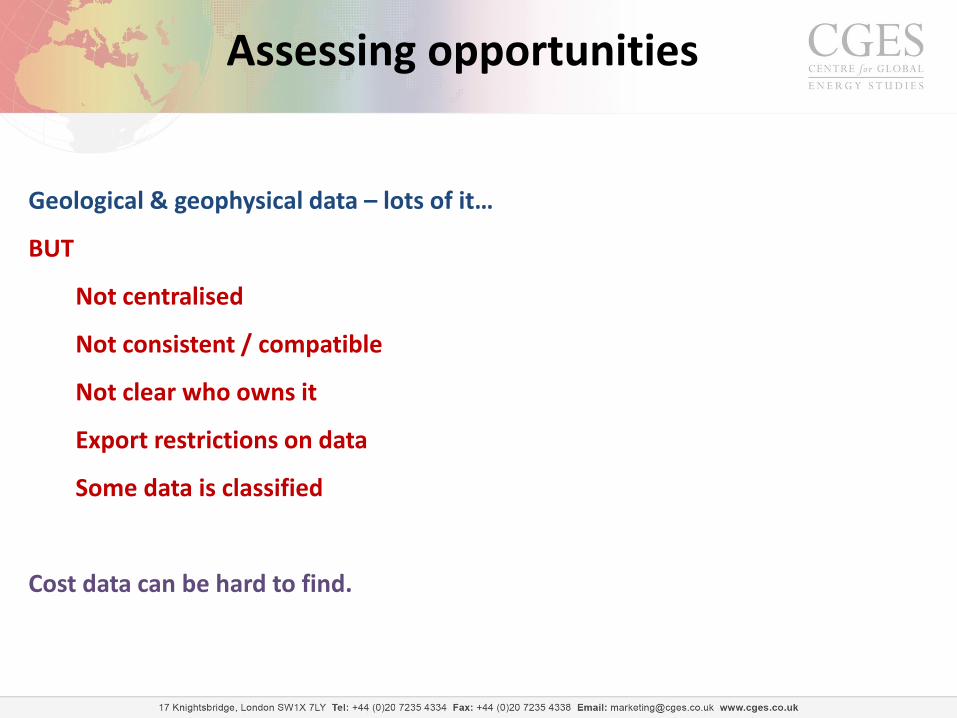

Geological & geophysical data – lots of it…

BUT

Not centralised

Not consistent / compatible

Not clear who owns it

Export restrictions on data

Some data is classified

Cost data can be hard to find.

Challenging terrain…

…but not everywhere

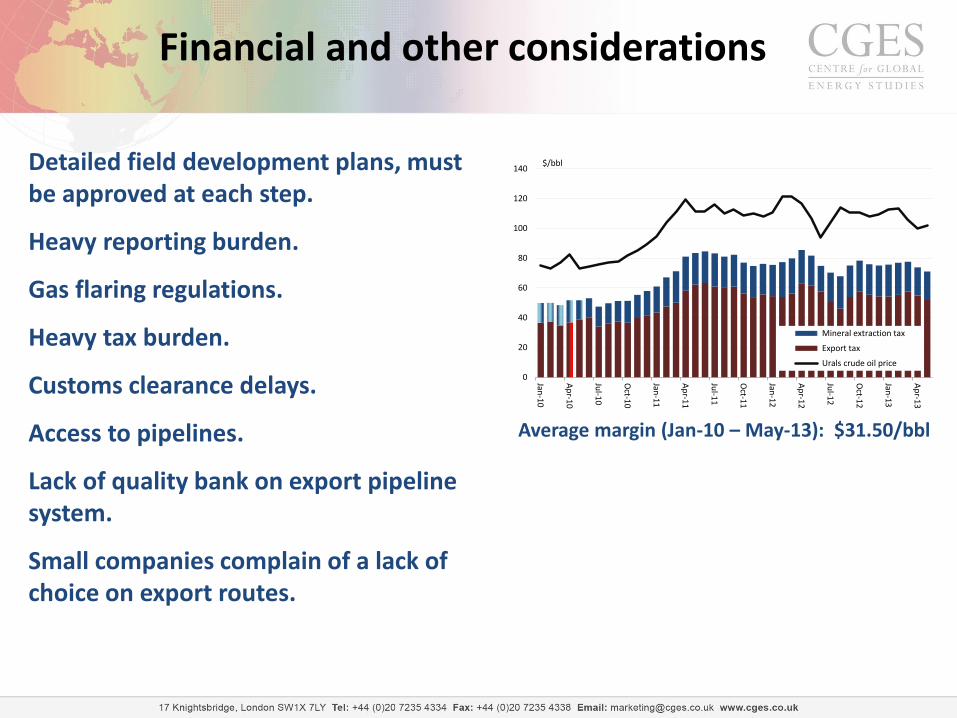

Financial and other considerations

0

20

40

60

80

100

120

140

Jan-10

Ap

r-10

Jul-1

0

Oct-1

0

Jan-11

Ap

r-11

Jul-1

1

Oct-1

1

Jan-12

Ap

r-12

Jul-1

2

Oct-1

2

Jan-13

Ap

r-13

Mineral extraction tax

Export tax

Urals crude oil price

$/bbl

Average margin (Jan-10 – May-13): $31.50/bbl

Detailed field development plans, must be approved at each step.

Heavy reporting burden.

Gas flaring regulations.

Heavy tax burden.

Customs clearance delays.

Access to pipelines.

Lack of quality bank on export pipeline system.

Small companies complain of a lack of choice on export routes.

The opportunities

Industry consolidation is releasing experienced executives.

Brownfield and greenfield acreage is available.

Opportunities for EOR and late-life field management.

Growing interest in hard-to-recover and unconventional liquids resources.

Technological partnerships with Russian companies.

The Caspian Sea region

Azerbaijan

Running out of opportunities?

Offshore – deep gas (reservoirs at ~ 6 km)

Onshore – largely depleted?

Kazakhstan

Offshore moratorium to be lifted?

Personal relationships are important

Competition from the Chinese

Turkmenistan

Offshore exploration – a slow process

Onshore – service contracts only

Caspian Sea region infrastructure

CGES provides a range of analysis on the oil and gas sectors of Russia and

the Caspian Sea region

FSU Oil & Gas Advisory • Comment and analysis of developments

in the oil and gas sectors of the FSU

• Subscription service

The outlook for Caspian oil exports • Study

FSU oil and gas maps • A set of 30 maps covering the oil and gas

sectors of the FSU

FSU digital mapping data • Digital data for accurate mapping of FSU

oil and gas fields and infrastructure

Russia and the Caspian

Julian Lee Senior Energy Analyst

Centre for Global Energy Studies 17 Knightsbridge London SW1X 7LY

UK

www.cges.co.uk