the gic weekly digest - amazon web services bloomberg, haver analytics, morgan stanley wealth...

TRANSCRIPT

The GIC Weekly Digest

February 5, 2018

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

Weekly Summary (as of 2/2/2018)

Discussion Points From The GIC Weekly • While economic momentum remains strong, shifting

dynamics in both the rates and currency markets augurs growing caution that P/E multiples could be at risk.

• Economic surprises and earnings revisions may be cresting at the same time that stress from Washington is increasing.

• In our view, a garden-variety correction of as much as 10% is not out of the question. Still, our full-year S&P 500 target remains 2,750.

• Watch the level of the VIX and the gap between realized and anticipated volatility. Consider equity long/short hedge funds to manage market volatility.

Market Snapshot

Equities Closing Price Weekly ChangeS&P 500 2762.13 -3.82%DJ Industrial Average 25520.96 -4.11%NASDAQ Composite 7240.95 -3.51%

CommoditiesWTI Crude $65.45 -1.04%Gold Spot $1,333.39 -1.17%

CurrenciesEUR/USD 1.25 0.29%US Dollar Index (DXY) 89.20 0.14%

Fixed Income (Corporate) OASBarclays US Aggregate 85 -2Barclays US High Yield 324 13

US Treasury Yields Yield2-Year 2.14% 0.035-Year 2.59% 0.1210-Year 2.84% 0.1830-Year 3.09% 0.18

Source: Bloomberg, FactSet, Morgan Stanley Wealth Management GIC. Option-Adjusted Spread (OAS) is a measurement of the spread of a fixed income security rate and the risk-free rate of return, which is adjusted to take into account an embedded option. Equity risk premium is the excess return that an individual stock or the overall stock market provides over a risk-free rate. The risk-free rate represents the interest an investor would expect from an absolutely risk-free investment over a specified period of time.

As of February 2, 2018

Weekly Focus

Market/Asset Class Performance

• US equities finished down 3.82%, with Telecom and Utilities leading, and Materials and Energy lagging. The S&P 500 closed Friday down over 2%—its worst day since September 2016.

• Gold fell 1.17% and WTI crude oil prices retreated 1.04% on the week, closing at $65.45 per barrel.

• Rates rose meaningfully last week with the 10-year Treasury rising 18bps to 2.84%. The 2-year yield increased slightly to 2.14%. The 10’s 2’s yield curve steepened back to 70 bps.

• European equities (STOXX 600) finished the week down 2.89% (in USD) while Japanese equities fell 2.33% (TOPIX in USD). Emerging markets (MSCI EM) traded lower as well, losing 3.32% (in USD).

• The dollar stayed mostly flat last week, rising 0.14% after hitting its lowest value since December 2014. This occurred as the yen depreciated 1.44% to 110.17. The euro and the pound remained steady at 1.24 and 1.41, respectively.

Macro Growth Indicators

• Change in Nonfarm Payrolls came in at 200k, above expectations of 180k, while unemployment was unchanged at 4.1%.

• Average hourly earnings rose 0.3% month over month and 2.9% year over year—the fastest pace since 2009.

• University of Michigan consumer sentiment also beat expectations at 95.7, slightly ahead of estimates of 95.

• Japanese retail sales were much stronger than survey results, rising 0.9% month over month versus a projected decline of 0.4%.

Policy

• The FOMC kept interest rates unchanged in the 1.25-1.50% range on Wednesday. The statement from the committee expressed that recent economic data has been “solid,” risks remain “roughly balanced,” and that further hikes are warranted if conditions remain.

• The Congressional Budget Office warned that the US will hit the debt ceiling a month sooner than previously expected as a result of lost revenue from the recent tax cut. Congress will need to act by early March in order to avoid a government default.

• Some members of the ECB are pushing for the group to be more forthcoming in its discussions on rate guidance. They fear that opaqueness will create volatility and hurt the accelerating Eurozone economy.

Company Fundamentals

• 251 S&P 500 companies have reported earnings so far, with 79% reporting positive earnings surprises.

• Forward earnings for the S&P 500 increased to $156 from $153 for 2018.

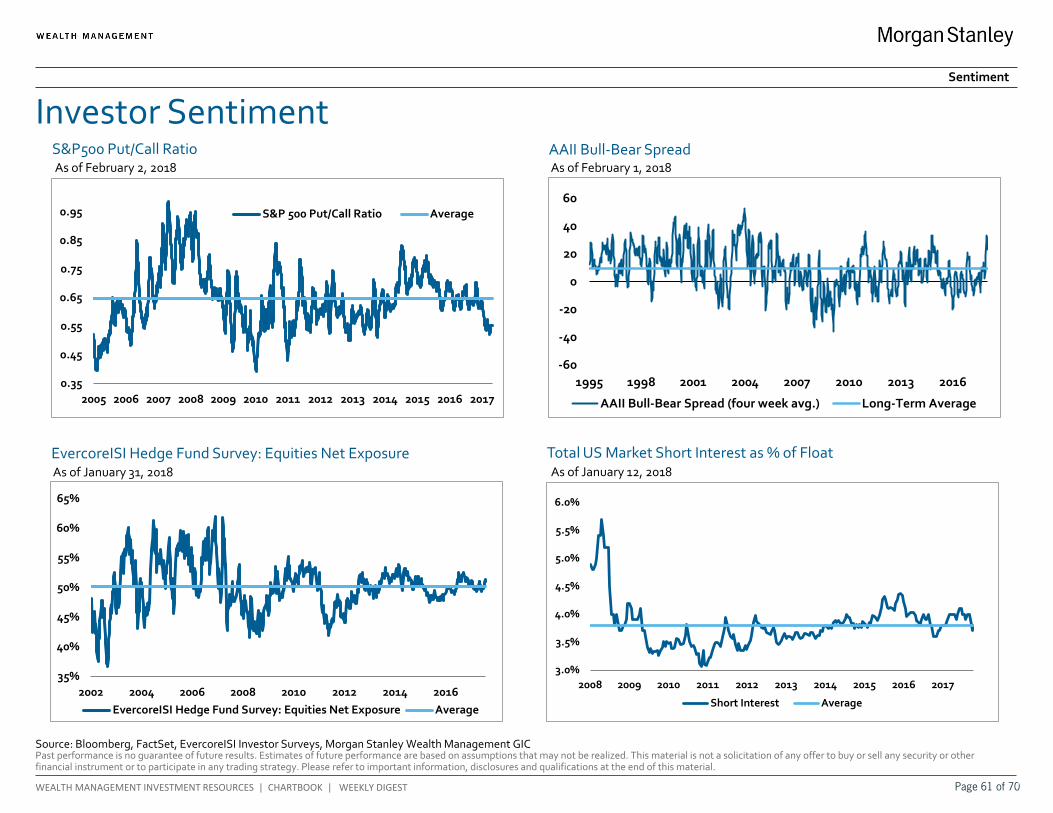

Sentiment & Technicals

• AAII Bulls fell to 45%, as neutrals increased to 26% and bears rose slightly to 29%.

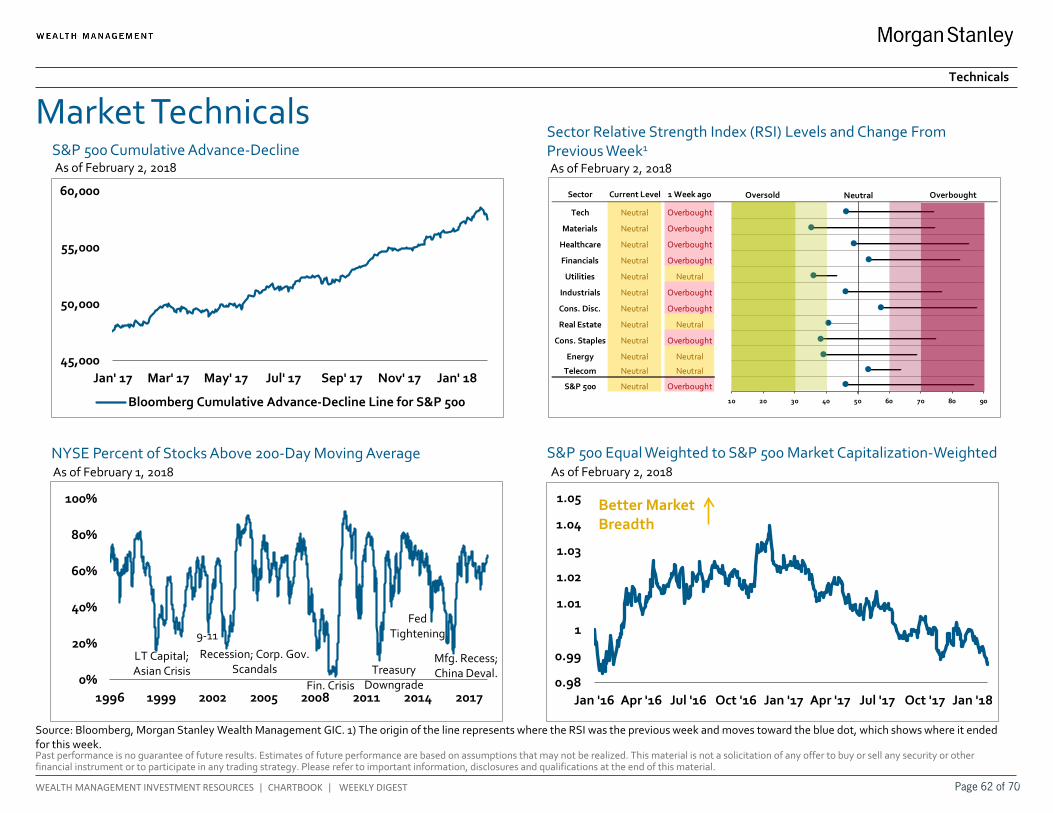

• The percent of NYSE stocks closing above their 200-day averages decreased slightly to 64% week over week.

Page 2 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

-40%

-30%

-20%

-10%

0%

10%

20%

30%

-30

-20

-10

0

10

20

30

40

Capex Plans Index (3 Month Moving Avg, Left axis)

Equipment Investment (Year Over Year, Right axis)

Chart of the Week: Capital Spending Intentions at All-Time High

Source: Bloomberg, Haver Analytics, Morgan Stanley Wealth Management GIC. Morgan Stanley Capex Plans Index tracks how much businesses are likely to spend in the coming months.

Weekly Focus

Capex Plans Vs. Equipment Investment Data as of January 31, 2018

Despite Friday’s correction, stocks are still trading near all-time highs. We believe the one element that will contribute to a normalization of volatility from historically low levels is mean reversion in key economic variables. A data series that has seen an impressive rebound during the past year is the MS & Co. Capex Plans Index, which tends to lead equipment investment (see chart). While a rebound in capital spending has been anticipated for much of the cycle, recent readings are at all-time highs, reflecting high levels of both business and consumer confidence. Capital equipment investment has shown a strong high correlation with industrial production growth which, in turn, is linked to S&P 500 earnings.

Page 3 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

2%

3%

4%

5%

6%

7%

8%

9%

1996

1997

1998

1999

2001

2002

2003

2004

2006

2007

2008

2009

2011

2012

2013

2014

2016

2017

Recession

Capex as a % of Sales

R&D as a % of Sales

Buybacks and Dividends as a % of Sales

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

Buybacks and Dividends as a % of Sales

Capex + R&D as a % of sales

Market Spotlight: Business Investment Is Growing at the Fastest Pace in 15 Years

Weekly Focus

Source: FactSet, Morgan Stanley Wealth Management GIC

Business Investment Growing, While Buybacks and Dividends Are Falling Monthly Data as of October 1995 to December 2017

R&D and Capex Both Accelerating Monthly Data as of October 1995 to December 2017

Page 4 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

Market Spotlight: Economic Cycle Is Approaching Record Length Weekly Focus

Source: OECD, Morgan Stanley& Co. Research, BEA, NBER, Morgan Stanley Wealth Management GIC. Note: The number labels represent the recovery period in quarters.

Current DM Recovery Already the Longest on Record Since the Mid-1970s Quarterly Data as of September 30, 2017

Current US Recovery Inching Towards the Record Expansion of the 1990s Quarterly Data as of December 31, 2017

57 19 28 29 24 34

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

US GDP YearOver Year

35 12 20 31

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

OECD GDP YearOver Year

4 40 24 34

Page 5 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

Tactical Theme: Long European Equities Weekly Focus

-40 %

-30 %

-20 %

-10 %

0 %

10 %

1975 1981 1987 1993 1999 2005 2011 2017

MSCI Europe vs MSCI USA (Avg % Prem/Disc On P/E, P/B & P/D) Median

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

MSCI Europe S&P 500

Real Estate

Utilities

Telecom

Information Technology

Energy

Materials

Consumer Discretionary

Health Care

Industrials

Consumer Staples

Financials

Overview – As we enter the new year, we should recognize the significance of 2017 to our European equities call. In 2017, MSCI Europe returned 26.3%, which was 4.5% more than the 21.8% of the S&P 500. However, much of this relative outperformance came in the first half of 2017, with Europe generally giving back most of this outperformance as idiosyncratic progress on tax reform lifted US equities in the latter half of the year. As we head into 2018, we believe Europe has a more attractive risk/reward skew than the US based on an improving economy, earnings growth that is finally turning a corner, a beneficial sector exposure, and attractive valuations.

Economic Data – As good as the US economic data has been recently, in many cases Europe has been ever more impressive. Eurozone manufacturing PMI hit 60.6 on its latest tick, well above the 55.1 seen in the US. Additionally, GDP has surprised to the upside, coming in at 2.6% year over year in 3Q17. On top of this, unemployment is back to levels last seen in 2005. With improving economic data, capital has flowed into the economy helping the euro appreciate to 1.23 vs the US dollar. This has aided US investor returns as we have recommended unhedged exposure to the region.

Earnings – While economic data is critical to the region’s continuing outperformance, even more important is the earnings story. Prior to 2017, Europe’s earnings declined for 6 straight years. However, 2017 posted very strong growth, with estimates pointing to up 27% for the year (even with an appreciating euro). For 2018, consensus estimates are calling for 13% earnings growth. While this is below the consensus growth estimate for the US at 14.4%, we would argue that in Europe the earnings growth is more organic and stable since a chunk of the US’s growth will come from a one-time lift due to tax reform.

Sector Exposures – Much of the reason why Europe underperformed over the last 5 years was due to a larger exposure in the region to commodities, financials, and EM (with tech notably absent). In fact, as shown in the chart to the right, Europe’s exposure to tech is only around 5% vs the US at around 24%. While this “value tilt” certainly hindered performance during the past cycle, with the global economic outlook finally improving, Europe’s tilt to these value sectors may actually provide potential considerable upside in 2018.

Valuations – Despite Europe’s rally in 2017, equities continue to have attractive valuations, trading at 15.2x consensus 12-month forward PE vs the S&P 500’s 18.5x 12-month forward PE (a ~17% discount). When looking at a combination of P/E, P/B, and price to dividend, European equities are trading at a 35% discount to the US, well below the long-term average. While a portion of the valuation discount is due to the sector differences mentioned above, there are likely other factors weighing down multiples such as skepticism that the economic and earnings recovery is real as well as whether the recent euro strength could derail it.

Risks – Global growth disappoints, tighter-than-expected monetary policy from ECB. Source: Bloomberg, Morgan Stanley Wealth Management Market Strategy as of 1/17/2018

MSCI Europe is at a 35% Discount to US on Forward P/E, P/B, & P/D

MSCI Europe Has a Value Tilt Compared to the S&P 500, Significantly Less Technology Exposure

Source: MSCI, IBES, Morgan Stanley & Co. Research as of 1/12/2018. Note: Average relative valuations use 12M forward data where available (forward P/E data starts in 1987) and trailing data where forward P/E not available – P/E = price / earnings; P/B = price / book; P/D = price / dividend

Page 6 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

1.1%2.5%

3.5% 3.6%4.9%

10.1%

-2.0% -1.6% -1.8%

0.8%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Model 3Benchmark

Model 3Tactical

MSCIUSA

MSCIEAFE

MSCIJapan

MSCIChina

BarclaysUS

Treasury

BarclaysUS

Municipal

BarclaysUS Agg

BarclaysGlobal HY

Year-to-Date 1-Year 3-Year (annualized)

Model 3 Strategic

Model 3 Tactical

Model 3 Benchmark

S&P 500

Citi 3M T Bill

Barclays US Agg

HFRX Global HF

MSCI ACWI

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

0% 1% 2% 3% 4% 5% 6% 7% 8%R

etur

nsVolatility

GIC Balanced Growth Model Hypothetical Performance Comparison

Source: FactSet, Bloomberg, Morgan Stanley Wealth Management GIC. Barclays indices are Bloomberg Barclays Indices. Within alternatives, HFRX Indices are used as an estimate until HFRI and Credit Suisse indices become available. HFRI data is as of 12/31/17, Credit Suisse data is as of 12/31/17. HFRX data is used for HFRI indices from 1/1/2018 to 2/2/2018 and Credit Suisse indices from 1/1/2018 to 2/2/2018. Model 3 = GIC Balanced Growth Model and is shown for illustrative purposes only, representing the GIC’s moderate asset allocation profile aimed at balancing risk and return. Model 3 Benchmark as shown represents the average of the blended benchmark indices as selected by the GIC: 50% MSCI ACWI, 45% Bloomberg Barclays US Aggregate Bond Index, and 5% Citi 3-Month T-Bill Index. S&P 500 and HFRX Global HF indices are shown for illustrative purposes only and are meant to be representative of the US large-cap equity market and the overall hedge fund universe, respectively, to complement the benchmark indices and serve as further comparison for the asset classes included in Model 3 . Model 3 Strategic return and volatility represent the GIC’s proposed 7-year investment horizon. Model 3 Tactical return and volatility represent the GIC’s proposed 20-year investment horizon. The Global Investment Committee Asset Allocation Models are not provided as part of an investment advisory service offered by Morgan Stanley Wealth Management, are not available to be directly implemented as part of an investment advisory service and should not be regarded as a recommendation of any Morgan Stanley Wealth Management investment advisory service. Returns expressed in US dollars. The hypothetical Model 3 performance does not reflect the investment or performance of actual portfolios. Hypothetical performance results do not reflect advisory fees or brokerage commissions. Had the results reflected these costs, the hypothetical performance would have been lower. For more information about the risks to hypothetical performance please refer to the Risk Considerations section at the end of this material. Please refer to the GIC’s Tactical Asset Allocation Changes report dated August 11, 2016 and the GIC Profiles for more information regarding current model positioning. Standard deviation (volatility) is a measure of the dispersion of a set of data from its mean. Volatility as shown is measured over the most recent rolling six months.

YTD Hypothetical Model 3 Performance and Volatility

For Illustrative Purposes Only

Asset Class Performance (USD) As of February 2, 2018 As of February 2, 2018

Weekly Focus

Page 7 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

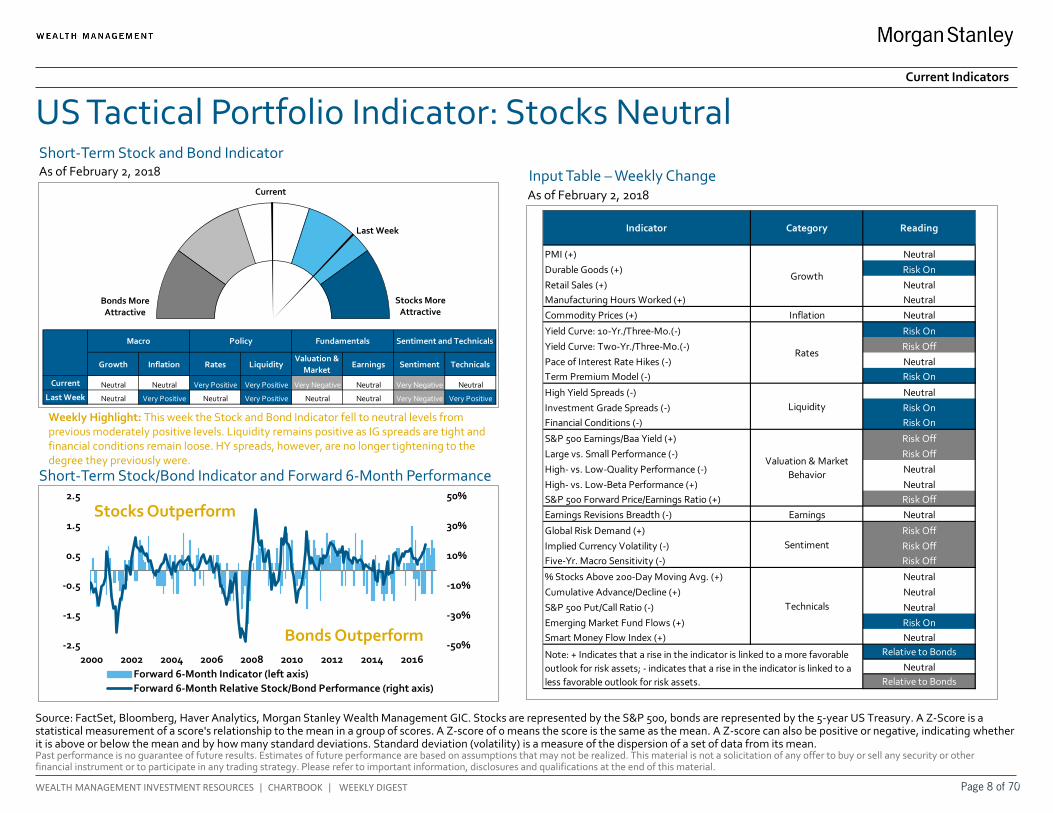

Indicator Category Reading

PMI (+) NeutralDurable Goods (+) Risk OnRetail Sales (+) NeutralManufacturing Hours Worked (+) NeutralCommodity Prices (+) Inflation Neutral

Yield Curve: 10-Yr./Three-Mo.(-) Risk OnYield Curve: Two-Yr./Three-Mo.(-) Risk OffPace of Interest Rate Hikes (-) NeutralTerm Premium Model (-) Risk On

High Yield Spreads (-) NeutralInvestment Grade Spreads (-) Risk OnFinancial Conditions (-) Risk On

S&P 500 Earnings/Baa Yield (+) Risk OffLarge vs. Small Performance (-) Risk OffHigh- vs. Low-Quality Performance (-) NeutralHigh- vs. Low-Beta Performance (+) NeutralS&P 500 Forward Price/Earnings Ratio (+) Risk OffEarnings Revisions Breadth (-) Earnings Neutral

Global Risk Demand (+) Risk OffImplied Currency Volatility (-) Risk OffFive-Yr. Macro Sensitivity (-) Risk Off

% Stocks Above 200-Day Moving Avg. (+) NeutralCumulative Advance/Decline (+) NeutralS&P 500 Put/Call Ratio (-) NeutralEmerging Market Fund Flows (+) Risk OnSmart Money Flow Index (+) Neutral

Relative to BondsNeutral

Relative to Bonds

Technicals

Note: + Indicates that a rise in the indicator is linked to a more favorable outlook for risk assets; - indicates that a rise in the indicator is linked to a less favorable outlook for risk assets.

Growth

Rates

Liquidity

Valuation & Market Behavior

Sentiment

Growth Inflation Rates LiquidityValuation &

MarketEarnings Sentiment Technicals

Current Neutral Neutral Very Positive Very Positive Very Negative Neutral Very Negative Neutral

Last Week Neutral Very Positive Neutral Very Positive Neutral Neutral Very Negative Very Positive

Macro Policy Fundamentals Sentiment and Technicals

-50%

-30%

-10%

10%

30%

50%

-2.5

-1.5

-0.5

0.5

1.5

2.5

2000 2002 2004 2006 2008 2010 2012 2014 2016Forward 6-Month Indicator (left axis)Forward 6-Month Relative Stock/Bond Performance (right axis)

Bonds More Attractive

Stocks More Attractive

Last Week

Current

Source: FactSet, Bloomberg, Haver Analytics, Morgan Stanley Wealth Management GIC. Stocks are represented by the S&P 500, bonds are represented by the 5-year US Treasury. A Z-Score is a statistical measurement of a score's relationship to the mean in a group of scores. A Z-score of 0 means the score is the same as the mean. A Z-score can also be positive or negative, indicating whether it is above or below the mean and by how many standard deviations. Standard deviation (volatility) is a measure of the dispersion of a set of data from its mean.

US Tactical Portfolio Indicator: Stocks Neutral As of February 2, 2018

Short-Term Stock/Bond Indicator and Forward 6-Month Performance

Current Indicators

Short-Term Stock and Bond Indicator

Input Table – Weekly Change

Stocks Outperform

Bonds Outperform

As of February 2, 2018

Weekly Highlight: This week the Stock and Bond Indicator fell to neutral levels from previous moderately positive levels. Liquidity remains positive as IG spreads are tight and financial conditions remain loose. HY spreads, however, are no longer tightening to the degree they previously were.

Page 8 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

Source: Bloomberg, FactSet, dailysentimentindex.com, Morgan Stanley & Co., Morgan Stanley Wealth Management GIC. This page features Morgan Stanley & Co.’s proprietary US Equity Risk Indicator, which is a gauge of US equity market sentiment/positioning. It also features a table of some of the key sentiment, positioning, breadth and volatility measures that we watch on a regular basis. Each factor is ranked against its three-year history to provide some historical context. Equity Risk Indicator is a standardized measure of investor sentiment and positioning and earnings revision factors, compiled using a statistical Z-score methodology. A Z-Score is a statistical measurement of a score's relationship to the mean in a group of scores. A Z-score of 0 means the score is the same as the mean. A Z-score can also be positive or negative, indicating whether it is above or below the mean and by how many standard deviations. Standard deviation (volatility) is a measure of the dispersion of a set of data from its mean. (1) % rank inverted. Global Risk Demand Index (GRDI): Proprietary gauge of global risk asset sentiment. Daily Sentiment Index: Poll that tracks trader sentiment of US stocks. AAII % Bulls: Individual investor sentiment poll of US equities. Mutual Fund Beta: Measure of mutual fund volatility vs. S&P 500 volatility. Relative Strength Index: Measures momentum; >70=overbought; <30=oversold.

US Equity Market Indicators: US Stock Risk Elevated Current Indicators

Morgan Stanley Equity Risk Indicator As of January 26, 2018

Buy

Sell

• The US Equity Risk Indicator came in at 1.9 last week

• Sentiment polls and market breadth inputs remain bullish

Page 9 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

0

20

40

60

80

100

120

140

160

Jan' 16 May' 16 Sep' 16 Jan' 17 May' 17 Sep' 17 Jan' 18

US 10Yr vs. 2Yr Spread

-100

-50

0

50

100

150

200

250

30010

20

40

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

VIX Index (log, 3M avg., lagged 30 months, LS)

US 10Yr vs. 2Yr Spread (inverted, RS)

Yield Curve Flattening

Source: Bloomberg, Morgan Stanley Wealth Management GIC

Current Indicators

VIX Index Vs. Yield Curve

As of February 2, 2018

US 10-Year vs 2-Year Spread

As of February 2, 2018

Page 10 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

-0.7%

-0.6%

-0.5%

-0.4%

-0.3%

-0.2%

-0.1%

0.0%

0.1%

0.2%

Feb-17 Apr-17 Jun-17 Aug-17 Oct-17 Dec-17 Feb-18

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

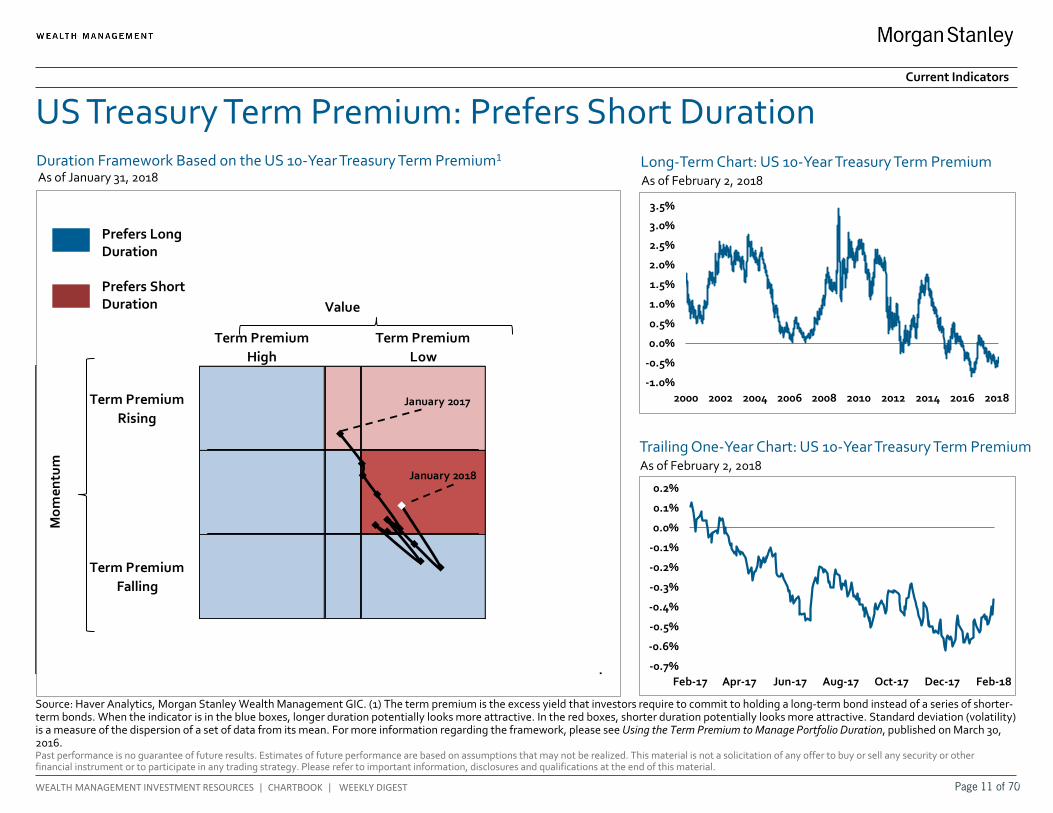

Duration Framework Based on the US 10-Year Treasury Term Premium1

US Treasury Term Premium: Prefers Short Duration

Source: Haver Analytics, Morgan Stanley Wealth Management GIC. (1) The term premium is the excess yield that investors require to commit to holding a long-term bond instead of a series of shorter-term bonds. When the indicator is in the blue boxes, longer duration potentially looks more attractive. In the red boxes, shorter duration potentially looks more attractive. Standard deviation (volatility) is a measure of the dispersion of a set of data from its mean. For more information regarding the framework, please see Using the Term Premium to Manage Portfolio Duration, published on March 30, 2016.

Term Premium High

Term Premium Low

Term Premium Rising

Short Duration

Term Premium Falling

Value

Mom

entu

m

January 2017

January 2018

Prefers Long Duration

Prefers Short Duration

Long-Term Chart: US 10-Year Treasury Term Premium As of February 2, 2018

Trailing One-Year Chart: US 10-Year Treasury Term Premium As of February 2, 2018

As of January 31, 2018

Current Indicators

Page 11 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

VIX Index (Equities)

MOVE Index (Fixed Income)

CVIX Index (Currency)

US Equity, Fixed Income and Currency Volatility

Source: Bloomberg, Morgan Stanley Wealth Management GIC. Standard deviation (volatility) is a measure of the dispersion of a set of data from its mean.

As of February 2, 2018

As of February 2, 2018

As of February 2, 2018

Current Indicators

Page 12 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

15%

20%

25%

30%

35%

40%

45%

50%

2003 2005 2007 2009 2011 2013 2015 2017

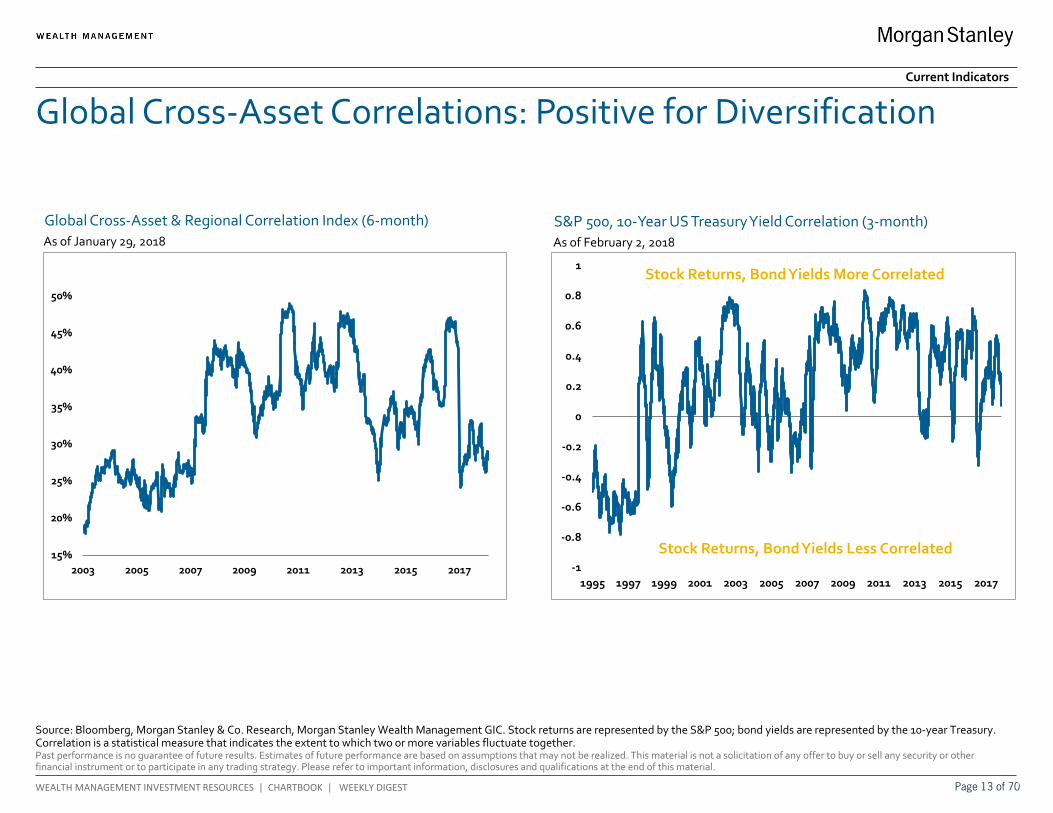

S&P 500, 10-Year US Treasury Yield Correlation (3-month)

Global Cross-Asset Correlations: Positive for Diversification

Source: Bloomberg, Morgan Stanley & Co. Research, Morgan Stanley Wealth Management GIC. Stock returns are represented by the S&P 500; bond yields are represented by the 10-year Treasury. Correlation is a statistical measure that indicates the extent to which two or more variables fluctuate together.

As of February 2, 2018

Current Indicators

Global Cross-Asset & Regional Correlation Index (6-month) As of January 29, 2018

Stock Returns, Bond Yields More Correlated

Stock Returns, Bond Yields Less Correlated

Page 13 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

Pai

rwis

e Co

rrel

atio

n (T

raili

ng 3

M)

US EM Global Developed International

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Jan '16 Apr '16 Jul '16 Oct '16 Jan '17 Apr '17 Jul '17 Oct '17 Jan '18S&P 500 MSCI ACWI 10-Year Treasury

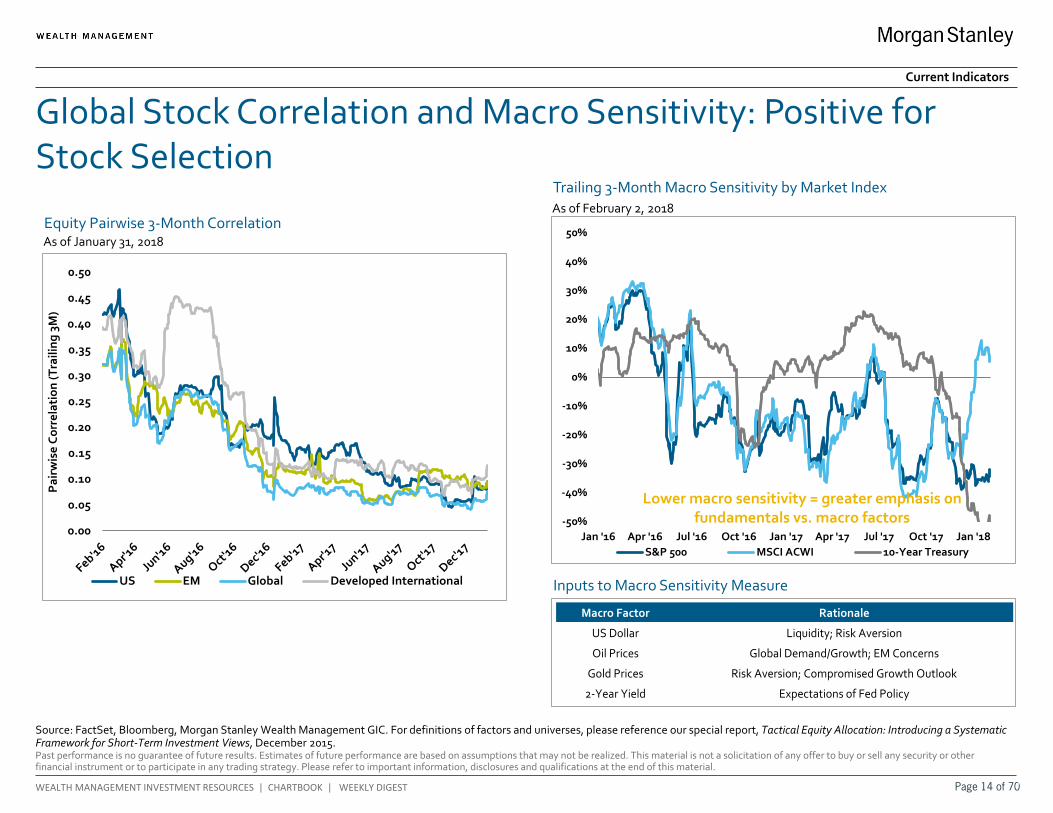

Equity Pairwise 3-Month Correlation

Global Stock Correlation and Macro Sensitivity: Positive for Stock Selection

Source: FactSet, Bloomberg, Morgan Stanley Wealth Management GIC. For definitions of factors and universes, please reference our special report, Tactical Equity Allocation: Introducing a Systematic Framework for Short-Term Investment Views, December 2015.

As of January 31, 2018

Trailing 3-Month Macro Sensitivity by Market Index As of February 2, 2018

Macro Factor Rationale

US Dollar Liquidity; Risk Aversion

Oil Prices Global Demand/Growth; EM Concerns

Gold Prices Risk Aversion; Compromised Growth Outlook

2-Year Yield Expectations of Fed Policy

Inputs to Macro Sensitivity Measure

Lower macro sensitivity = greater emphasis on fundamentals vs. macro factors

Current Indicators

Page 14 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

-3

-2

-1

0

1

2

3

4

5

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018Morgan Stanley Financial Conditions Index¹

QE1

QE1.5

QE2

Twist

LTRO

LTRO II

Draghi

QE3BOJQQE²

Fed Ends QE

BOJQQE+

ECBQE

China/OPEC FX Reserves Repatriated

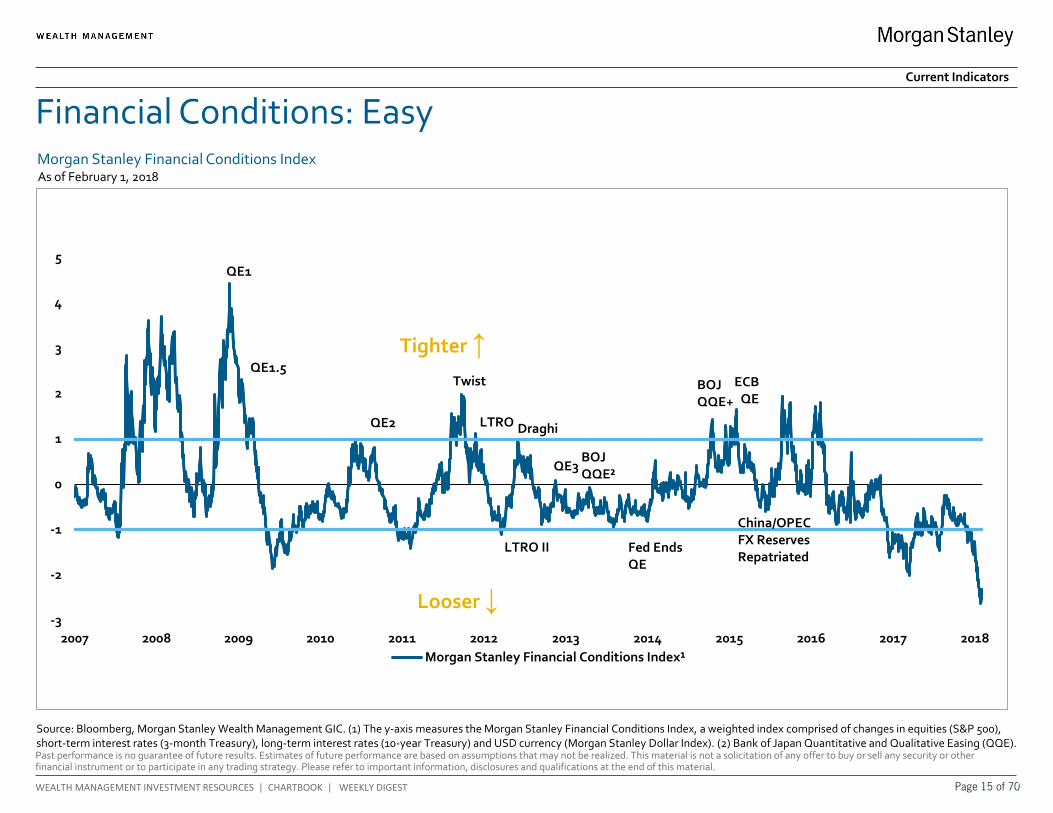

Morgan Stanley Financial Conditions Index

Source: Bloomberg, Morgan Stanley Wealth Management GIC. (1) The y-axis measures the Morgan Stanley Financial Conditions Index, a weighted index comprised of changes in equities (S&P 500), short-term interest rates (3-month Treasury), long-term interest rates (10-year Treasury) and USD currency (Morgan Stanley Dollar Index). (2) Bank of Japan Quantitative and Qualitative Easing (QQE).

Financial Conditions: Easy

Tighter ↑

Looser ↓

As of February 1, 2018

Current Indicators

Page 15 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

-4

-3

-2

-1

0

1

2

3

4

2011 2012 2013 2014 2015 2016 2017

Morgan Stanley Standardized GRDI

Morgan Stanley Global Risk Demand Index

Global Risk Indicator: Sentiment Neutral

Source: Bloomberg, Morgan Stanley & Co. Research. (1) There is one composite market timing indicator (CMTI) and four components: the valuation, risk, fundamentals and capitulation indicators. They help decide the tactical outlook for equity markets for the next three-to-six months.

Morgan Stanley Europe Combined Market Timing Indicator1

Sell

Buy -1.5

-1.0

-0.5

0.0

0.5

1.0

2010 2011 2012 2013 2014 2015 2016 2017 2018

Combined Market Timing Indicator (CMTI)

Sell

Buy

As of January 31, 2018 As of January 18, 2018

Current Indicators

Page 16 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

-2.5-2.0-1.5-1.0-0.50.00.51.01.52.02.5

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

-$80

-$60

-$40

-$20

$0

$20

$40

$60

$80

$100

Jan' 14 Jul' 14 Jan' 15 Jul' 15 Jan' 16 Jul' 16 Jan' 17 Jul' 17

US Bond Mutual Fund + ETF Net Flows (trailing 3M)

US Equity Mutual Fund + ETF Net Flows (trailing 3M)Bil. Crude Oil

Gold

Euro

Yen

Dollar

S&P 500

2 Yr Trsry

10 Yr Trsry

Legend

-14% 36%-61% -7%0.991

-29% 44%-51% 3%0.991

16% 30%-45% -2%0.991

-9% 87%-24% 37%0.991

-55% 69%-85% -17%0.991

40% 63%-75% -21%0.991

53% 78%3% 50%0.991

74% 74%2% 42%0.991

Min MaxCurrent Avg Since 2010

100%

47%

96%

31%

7%

92%

5%

32%

Percentile

35%

40%

45%

50%

55%

60%

65%

2002 2004 2006 2008 2010 2012 2014 2016EvercoreISI Hedge Fund Survey: Equities Net Exposure Average

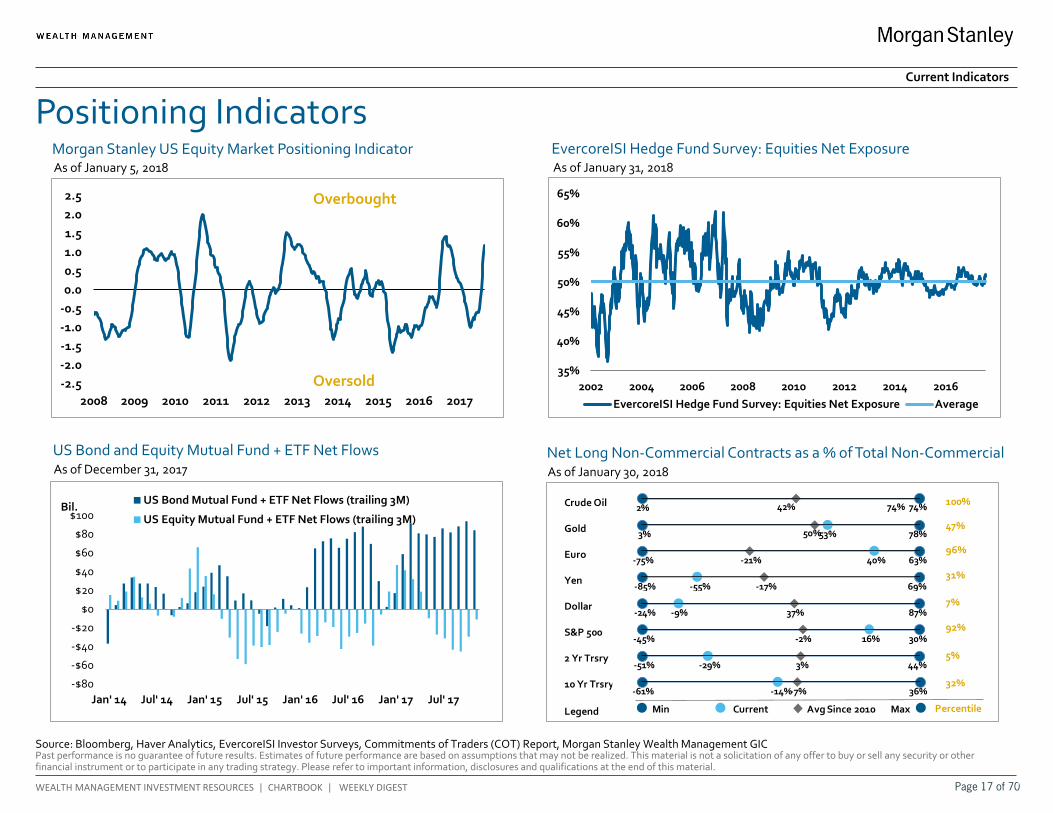

Positioning Indicators Current Indicators

Morgan Stanley US Equity Market Positioning Indicator

Source: Bloomberg, Haver Analytics, EvercoreISI Investor Surveys, Commitments of Traders (COT) Report, Morgan Stanley Wealth Management GIC

Net Long Non-Commercial Contracts as a % of Total Non-Commercial

EvercoreISI Hedge Fund Survey: Equities Net Exposure As of January 5, 2018 As of January 31, 2018

As of January 30, 2018

US Bond and Equity Mutual Fund + ETF Net Flows As of December 31, 2017

Overbought

Oversold

Page 17 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

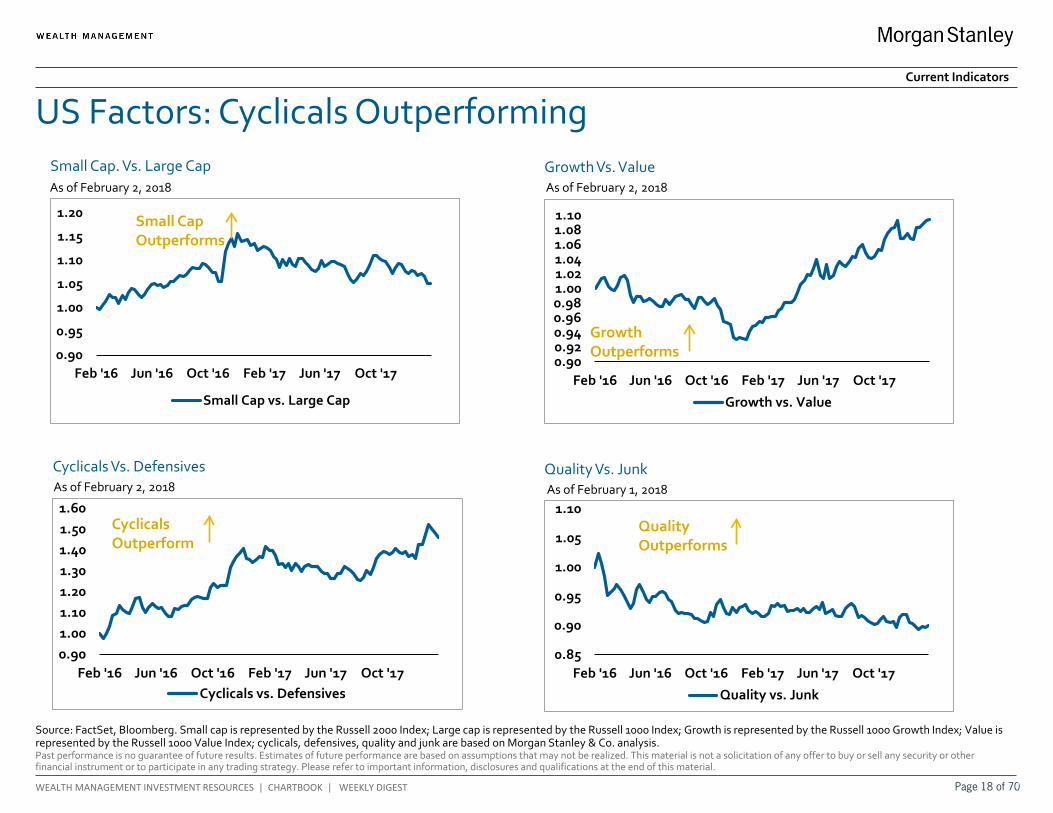

Small Cap. Vs. Large Cap

Growth Vs. Value

Cyclicals Vs. Defensives

US Factors: Cyclicals Outperforming

Quality Vs. Junk

Source: FactSet, Bloomberg. Small cap is represented by the Russell 2000 Index; Large cap is represented by the Russell 1000 Index; Growth is represented by the Russell 1000 Growth Index; Value is represented by the Russell 1000 Value Index; cyclicals, defensives, quality and junk are based on Morgan Stanley & Co. analysis.

0.90

0.95

1.00

1.05

1.10

1.15

1.20

Feb '16 Jun '16 Oct '16 Feb '17 Jun '17 Oct '17

Small Cap vs. Large Cap

0.900.920.940.960.981.001.021.041.061.081.10

Feb '16 Jun '16 Oct '16 Feb '17 Jun '17 Oct '17

Growth vs. Value

0.901.001.101.201.301.401.501.60

Feb '16 Jun '16 Oct '16 Feb '17 Jun '17 Oct '17Cyclicals vs. Defensives

0.85

0.90

0.95

1.00

1.05

1.10

Feb '16 Jun '16 Oct '16 Feb '17 Jun '17 Oct '17

Quality vs. Junk

Growth Outperforms

Small Cap Outperforms

Cyclicals Outperform

Quality Outperforms

As of February 2, 2018 As of February 2, 2018

As of February 2, 2018 As of February 1, 2018

Current Indicators

Page 18 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

~70% ~10% ~20%

Asset Class Sector Subsector Total SignalFundamental Momentum

Valuation Technicals

Equities US Large-Cap Growth 6 Strong Weak Weak

Equities US Large-Cap Value 6 Neutral Weak Neutral

Equities US Mid-Cap Growth 8 Neutral Weak Neutral

Equities US Mid-Cap Value 7 Neutral Weak Neutral

Equities US Small-Cap Growth 8 Neutral Weak Neutral

Equities US Small-Cap Value 9 Neutral Neutral Weak

Equities International Ex-US 9 Strong Neutral Neutral

Equities International Europe 9 Strong Weak Neutral

Equities International Japan 7 Neutral Weak Neutral

Equities Emerging Markets 8 Neutral Weak Strong

Fixed-Income US Core Treasuries 1 Weak Weak Weak

Fixed-Income US Core Credit 2 Weak Strong Weak

Fixed-Income US Core MBS 1 Weak Strong Weak

Fixed-Income Other International 1 Weak Strong Weak

Fixed-Income Other Emerging Markets 1 Weak Neutral Weak

Fixed-Income Other High-Yield 8 Neutral Weak Weak

Fixed-Income Other TIPS 4 Weak Strong Weak

Alternatives Real Assets Commodities 9 Neutral Weak Neutral

Alternatives Real Assets MLPs 9 Strong Weak Weak

Alternatives Real Assets REITs 5 Strong Weak Weak

Currencies EUR/USD 8 Neutral Weak Strong

Currencies USD/JPY 8 Strong Strong Weak

Weighting

Dynamic Allocation Framework Signals

Source: Bloomberg, FactSet, Morgan Stanley Wealth Management GIC. Note: A total signal of 10 represents the highest score and a total signal of 1 represents the lowest score. For more details on the Dynamic Allocation Framework, please see US Equity Factor Dynamic Allocation Factsheet dated October 2017.

Current Indicators

Asset Class and Sector Factor Scores Based on Fundamentals, Valuation and Technicals Data as of February 3, 2018

Page 19 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

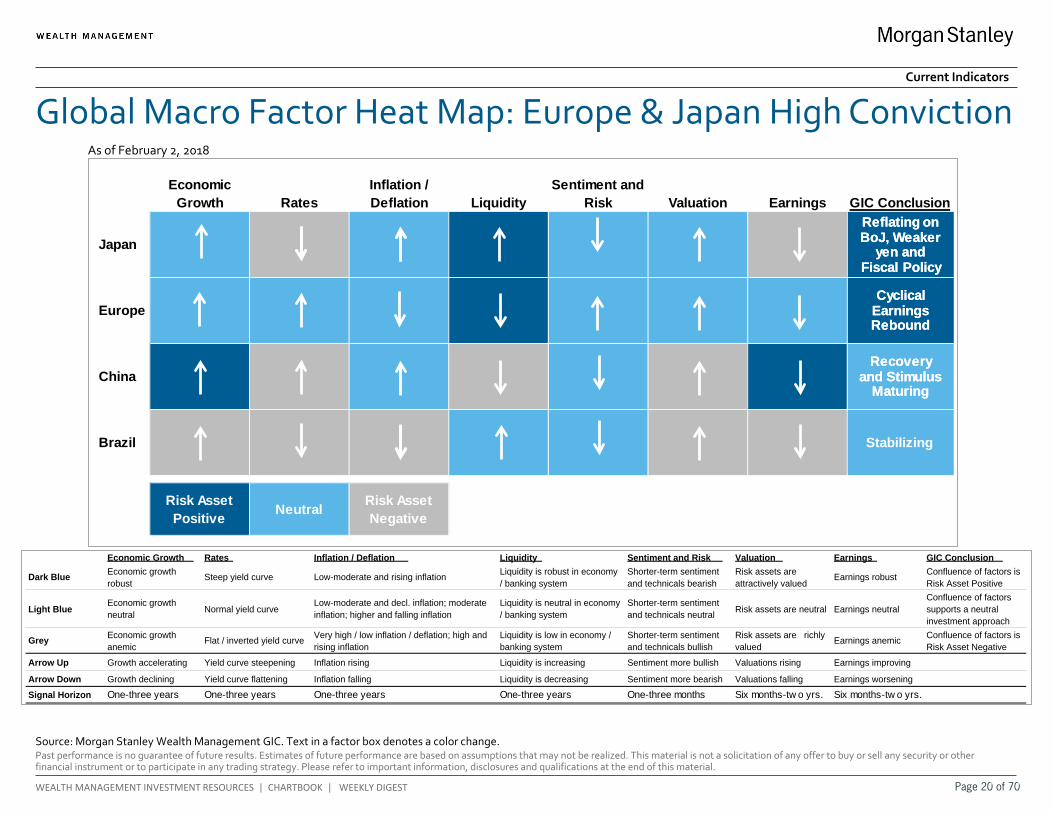

Economic Growth Rates

Inflation / Deflation Liquidity

Sentiment and Risk Valuation Earnings GIC Conclusion

Japan 0 -1 0 1 0 0 -1 1

Europe 0 0 0 1 0 0 0 1

China 1 -1 0 -1 0 -1 1 0

Brazil -1 -1 -1 0 0 -1 -1 0

Risk Asset Positive Neutral Risk Asset

Negative

Reflating on BoJ, Weaker

yen andFiscal Policy

Cyclical Earnings Rebound

Recovery and Stimulus

Maturing

Stabilizing

Reflating on BoJ, Weaker

yen andFiscal Policy

Cyclical Earnings Rebound

Recovery and Stimulus

Maturing

Stabilizing

Global Macro Factor Heat Map: Europe & Japan High Conviction As of February 2, 2018

Economic Growth Rates Inflation / Deflation Liquidity Sentiment and Risk Valuation Earnings GIC Conclusion

Dark Blue Economic growth robust

Steep yield curve Low-moderate and rising inflation Liquidity is robust in economy / banking system

Shorter-term sentiment and technicals bearish

Risk assets are attractively valued

Earnings robust Confluence of factors is Risk Asset Positive

Light Blue Economic growth neutral Normal yield curve

Low-moderate and decl. inflation; moderate inflation; higher and falling inflation

Liquidity is neutral in economy / banking system

Shorter-term sentiment and technicals neutral Risk assets are neutral Earnings neutral

Confluence of factors supports a neutral investment approach

Grey Economic growth anemic

Flat / inverted yield curve Very high / low inflation / deflation; high and rising inflation

Liquidity is low in economy / banking system

Shorter-term sentiment and technicals bullish

Risk assets are richly valued

Earnings anemic Confluence of factors is Risk Asset Negative

Arrow Up Growth accelerating Yield curve steepening Inflation rising Liquidity is increasing Sentiment more bullish Valuations rising Earnings improving

Arrow Down Growth declining Yield curve flattening Inflation falling Liquidity is decreasing Sentiment more bearish Valuations falling Earnings worseningSignal Horizon One-three years One-three years One-three years One-three years One-three months Six months-tw o yrs. Six months-tw o yrs.

Source: Morgan Stanley Wealth Management GIC. Text in a factor box denotes a color change.

Current Indicators

Page 20 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

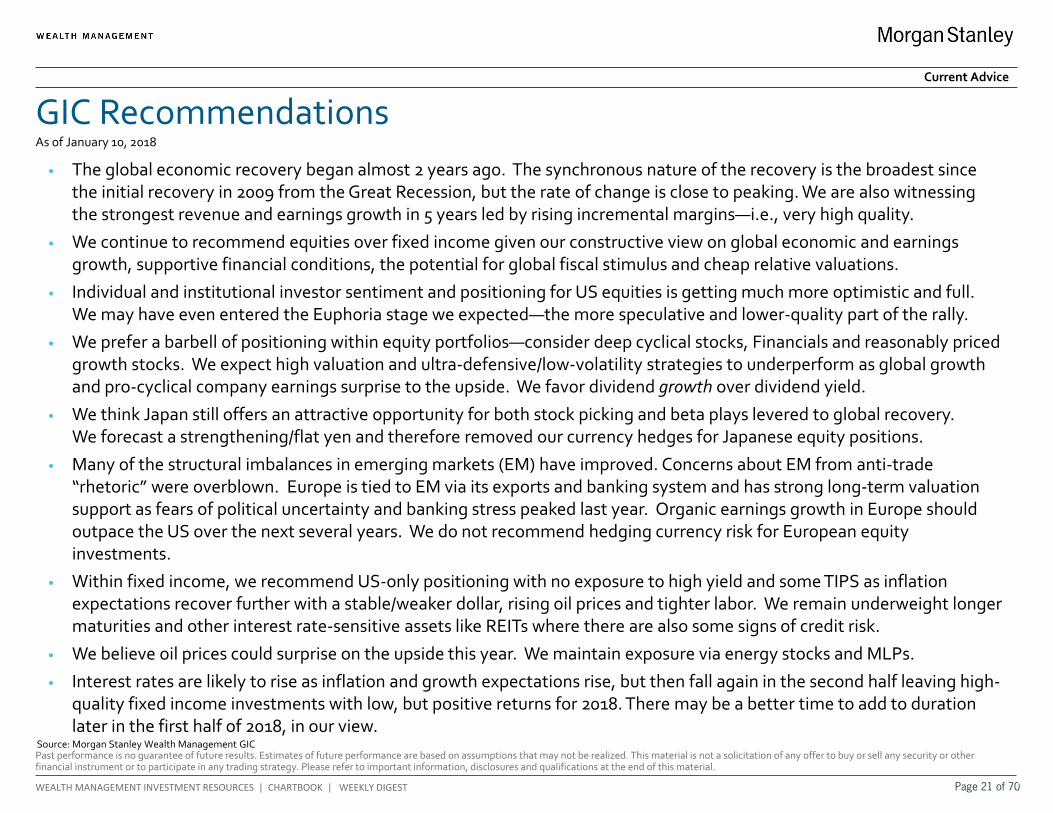

GIC Recommendations As of January 10, 2018

Source: Morgan Stanley Wealth Management GIC

Current Advice

• The global economic recovery began almost 2 years ago. The synchronous nature of the recovery is the broadest since the initial recovery in 2009 from the Great Recession, but the rate of change is close to peaking. We are also witnessing the strongest revenue and earnings growth in 5 years led by rising incremental margins—i.e., very high quality.

• We continue to recommend equities over fixed income given our constructive view on global economic and earnings growth, supportive financial conditions, the potential for global fiscal stimulus and cheap relative valuations.

• Individual and institutional investor sentiment and positioning for US equities is getting much more optimistic and full. We may have even entered the Euphoria stage we expected—the more speculative and lower-quality part of the rally.

• We prefer a barbell of positioning within equity portfolios—consider deep cyclical stocks, Financials and reasonably priced growth stocks. We expect high valuation and ultra-defensive/low-volatility strategies to underperform as global growth and pro-cyclical company earnings surprise to the upside. We favor dividend growth over dividend yield.

• We think Japan still offers an attractive opportunity for both stock picking and beta plays levered to global recovery. We forecast a strengthening/flat yen and therefore removed our currency hedges for Japanese equity positions.

• Many of the structural imbalances in emerging markets (EM) have improved. Concerns about EM from anti-trade “rhetoric” were overblown. Europe is tied to EM via its exports and banking system and has strong long-term valuation support as fears of political uncertainty and banking stress peaked last year. Organic earnings growth in Europe should outpace the US over the next several years. We do not recommend hedging currency risk for European equity investments.

• Within fixed income, we recommend US-only positioning with no exposure to high yield and some TIPS as inflation expectations recover further with a stable/weaker dollar, rising oil prices and tighter labor. We remain underweight longer maturities and other interest rate-sensitive assets like REITs where there are also some signs of credit risk.

• We believe oil prices could surprise on the upside this year. We maintain exposure via energy stocks and MLPs.

• Interest rates are likely to rise as inflation and growth expectations rise, but then fall again in the second half leaving high-quality fixed income investments with low, but positive returns for 2018. There may be a better time to add to duration later in the first half of 2018, in our view.

Page 21 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

Asset Class Strategic Weight Tactical Weight Difference Benchmark Weight

Ultra Short Term F.I. 4% 4% 0% 5%

Equities 48% 58% 10% 50%US Equities 20% 26% 6%

US Large-Cap Growth 6% 9% 3%US Large-Cap Value 6% 9% 3%US Mid-Cap Growth 2% 2% 0%US Mid-Cap Value 2% 2% 0%US Small-Cap Growth 2% 2% 0%US Small-Cap Value 2% 2% 0%

International Equities 22% 25% 3%European Equities 15% 17% 2%Japan Equities 6% 8% 2%Asia Pacific ex Japan Equities 1% 0% -1%

Emerging & Frontier Markets Equities 6% 7% 1%

Fixed Income 31% 23% -8% 45%Short-Term Fixed Income 10% 12% 2%US Fixed Income Taxable 15% 9% -6%International Fixed Income 1% 0% -1%Inflation-Protection Securities 0% 2% 2%High Yield Fixed Income 4% 0% -4%Emerging Markets Fixed Income 1% 0% -1%

Alternatives 17% 15% -2% 0%Real Assets 8% 7% -1%

REITs 3% 0% -3%Commodities 0% 0% 0%Master Limited Partnerships 5% 7% 2%

Absolute Return Assets 4% 4% 0%Equity Hedge Assets 5% 4% -1%Equity Return Assets 0% 0% 0%

GIC Balanced Growth (Model 3) Current Allocations

Source: Morgan Stanley Wealth Management GIC. Note: Model 3 Benchmark is represented by 50% MSCI ACWI, 45% Bloomberg Barclays US Aggregate Bond Index, and 5% Citi 3-Month T-Bill Index.

Current Advice

As of January 31, 2018

Page 22 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

++ + 0 + ++ Themes ++ + 0 + ++ Themes ++ + 0 + ++ Themes

US Global Japan and Europe Rates Credit Bank loans, preferredsLow Inflation

Protection

High Inflation

ProtectionMLPs, TIPs

Value Growth Financials, Energy, TechShort

DurationLong

DurationLadder 3 months to 3

yearsLow

VolatilityHigh

VolatilityGlobal macro, managed

futures

Small Large Neutral on Cap TaxableNon-

TaxableGeneral obligations

Low Leverage/

Alpha

High Leverage/

AlphaEquity L/S, event driven

Quality Junk IG HYRemoved High Yield

Exposure

Defensives Cyclicals Industrials, Energy US Int'l Non-sovereign

Active PassiveActive management outlook continue to

improveDeveloped

Emerging Markets

Hedged UnhedgedUnhedged in both Europe

and Japan

AlternativesEquities Fixed Income

Summary of Tactical Portfolio Construction Advice

Source: Morgan Stanley Wealth Management GIC. Note: ++ is most attractive, + is moderately attractive, 0 is neutral, - is moderately unattractive, -- is most unattractive.

Current Advice

-- - 0 + ++ Themes

Private EquitySmall and middle market buyout,

secondaries, co-investments, VC/growth equity

Private CreditDirect lending (senior secured),

structured credit, distressed

Private Real EstateSecondaries, core, demographic

trends, non-major markets

Private Alternatives

Cash Equities Fixed Income Alternatives

Underweight Overweight Underweight Equalweight

Asset Allocation

As of January 31, 2018

Page 23 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

Our US Active/Passive Model

Source: Morningstar, FactSet, Bloomberg, Morgan Stanley Wealth Management GIC. Signal trend is based on the trailing 3 months. Trending up = more active, tending down = more passive.

Current Advice

Factor Model Weights for Select Styles and Current Signals As of February 2, 2018

Active vs. Passive Tactical & Strategic Allocations As of December 31, 2017

Active (%) Passive (%) Active (%) Passive (%)

Large Core45% 55% 45% 55%

Large Growth45% 55% 45% 55%

Large Value75% 25% 45% 55%

Mid Core85% 15% 55% 45%

Mid Growth85% 15% 55% 45%

Mid Value85% 15% 55% 45%

Small Core40% 60% 70% 30%

Small Growth70% 30% 70% 30%

Small Value40% 60% 70% 30%

Tactical (1 Year Horizon) Strategic (7 Year Horizon)Factors

Large Core

Mid Core

Small Core

Current SignalLast 6M Signal Trend

Last 12M Signal Trend

Value Dispersion 20% 25% 15% Moderate Active Active Active

S&P Macro Sensitivity Trend 14% 22% 12% Strong Active Active Active

Trailing Return Breadth 11% 6% 9% Strong Active Active Active

Trailing Global vs. US Return 11% 4% 12% Moderate Passive Passive Passive

Return Correlation 7% 13% 19% Moderate Active Passive Passive

Return Correlation Trend 16% 8% 8% Strong Passive Passive Passive

Yield Slope 2% 11% 3% Moderate Passive Active Passive

Yield Slope Trend 8% 3% 1% Moderate Active Active Active

Modeled Return Breadth 7% 6% 11% Strong Passive Passive Passive

Earnings Estimate Dispersion 5% 2% 10% Moderate Active Neutral Neutral

Page 24 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

-$25

-$20

-$15

-$10

-$5

$0

$5

$10

$15

$0

$10

$20

$30

$40

$50

$60

Jan '16 May '16 Sep '16 Jan '17 May '17 Sep '17

Par

Val

ue (B

illio

ns)

Par

Val

ue (B

illio

ns)

2000-2016 Average Supply (left axis)Actual and Forecasted Redemptions (left axis)Net Supply Proxy (right axis)

US Municipal Market

Source: Thomson Reuters Municipal Market Data (MMD), Interactive Data, Morgan Stanley Wealth Management GIC

Municipal Bond Market Supply and Redemptions

10-Year Relative Value Ratio (Municipal Yield/Treasury Yield)

75%

80%

85%

90%

95%

100%

105%

110%

115%

120%

125%

130%

2010 2011 2012 2013 2014 2015 2016 2017 2018

% O

f Cor

resp

ondi

ng U

STs

10-Year RatioLong-Term Average (1990)Average Post JOBS Act (Sep 2011)

86%

As of December 2017 As of February 2, 2018

Munis Cheaper Relative to Treasuries

Munis Richer

Current Advice

Consistent with the dynamics discussed in our last review, municipals continued to underperform UST weakness this week (bear flattening during earlier trading sessions). Healthy bid lists and this week’s considerable decline in fund inflows, elicited by the household sector’s delayed response to rates, are harbingers for continued underperformance moving forward. Additionally, rich relative-value ratios suggest that tax-exempts hold a paltry buffer against future weakness. Consequently, municipals should follow any negative UST price trajectory downward (as has already occurred). Our objectives stand at: (1) exercise caution in the current period of low ratio / interest-rate weakness; (2) cautiously consider entry points once present UST weakness fully stabilizes/sustainably rallies; and (3) favor high-quality securities with short/low-to-neutral duration due to tight spreads and the flatter curve (6-12 year finals), but keep some dry powder as catalysts for further rate weakness remain.

Page 25 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

Duration Yield Breakeven

Ratio Duration Yield

Breakeven Ratio

2YR Treasury 1.95 1.88 0.96 1.96 2.14 1.095YR Treasury 4.69 2.21 0.47 4.73 2.59 0.5510YR Treasury 8.73 2.41 0.28 8.75 2.84 0.3230YR Treasury 19.99 2.74 0.14 20.02 3.09 0.15Barclays Aggregate 5.98 2.71 0.45 6.17 3.06 0.50Investment Grade Corporate 7.58 3.25 0.43 7.51 3.54 0.47

AA Corporate 6.43 2.71 0.42 6.33 3.03 0.48A Corporate 7.61 3.03 0.40 7.55 3.36 0.45BBB Corporate 7.60 3.54 0.47 7.55 3.80 0.50

High Yield Corporate 3.86 5.72 1.48 4.03 5.92 1.47BB Corporate 4.39 4.37 1.00 4.58 4.61 1.01B Corporate 3.55 5.70 1.61 3.72 5.86 1.58CCC Corporate 3.17 8.45 2.67 3.31 8.52 2.57

Fixed-Rate Preferreds 3.87 1.85 0.48 5.15 3.14 0.61Leveraged Loan1 0.50 5.11 10.22 0.50 5.11 10.22

BB Loan 0.50 4.15 8.30 0.50 4.15 8.30B Loan 0.50 5.37 10.74 0.50 5.37 10.74

MBS 4.43 2.91 0.66 5.27 3.31 0.63CMBS 5.47 3.19 0.58 5.43 3.50 0.64

Asset Class Dec 29, 2017 Feb 2, 2018

US Fixed Income Positioning: Trim Low-Quality Allocations

Source: Morgan Stanley Wealth Management Fixed Income Strategy, Bloomberg Barclays indices, Bloomberg, S&P/LSTA, Morgan Stanley & Co. Research and Bank of America Merrill Lynch Fixed Rate Preferred Index. (1) Latest leveraged loan data is as of 7/31/2017. High yield is represented by the Bloomberg Barclays US High Yield Index, Investment grade, MBS and CMBS are represented by the Investment grade, MBS and CMBS portions of the Bloomberg Barclays Aggregate; fixed rate preferreds represented by the BofA Merrill Lynch Fixed Rate Preferred Securities Index. The BofA Merrill Lynch Fixed Rate Preferred Securities Index is used with permission from BofA Merrill Lynch. BOFA MERRILL LYNCH IS LICENSING THE BOFA MERRILL LYNCH INDICES “AS IS,” MAKES NO WARRANTIES REGARDING SAME, DOES NOT GUARANTEE THE SUITABILITY, QUALITY, ACCURACY, TIMELINESS AND/OR COMPLETENESS OF THE BOFA MERRILL LYNCH INDICES OR ANY DATA INCLUDED IN, RELATED TO, OR DERIVED THEREFROM, ASSUMES NO LIABILITY IN CONNECTION WITH THEIR USE, AND DOES NOT SPONSOR, ENDORSE OR RECOMMEND MORGAN STANLEY SMITH BARNEY LLC, OR ANY OF ITS PRODUCTS OR SERVICES.

Current Advice

US Breakeven Ratios

From a breakeven perspective, lower-quality fixed income sectors, like triple-C corporate credits and leveraged loans, have become significantly less attractive over the last year

As of February 2, 2018

Page 26 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

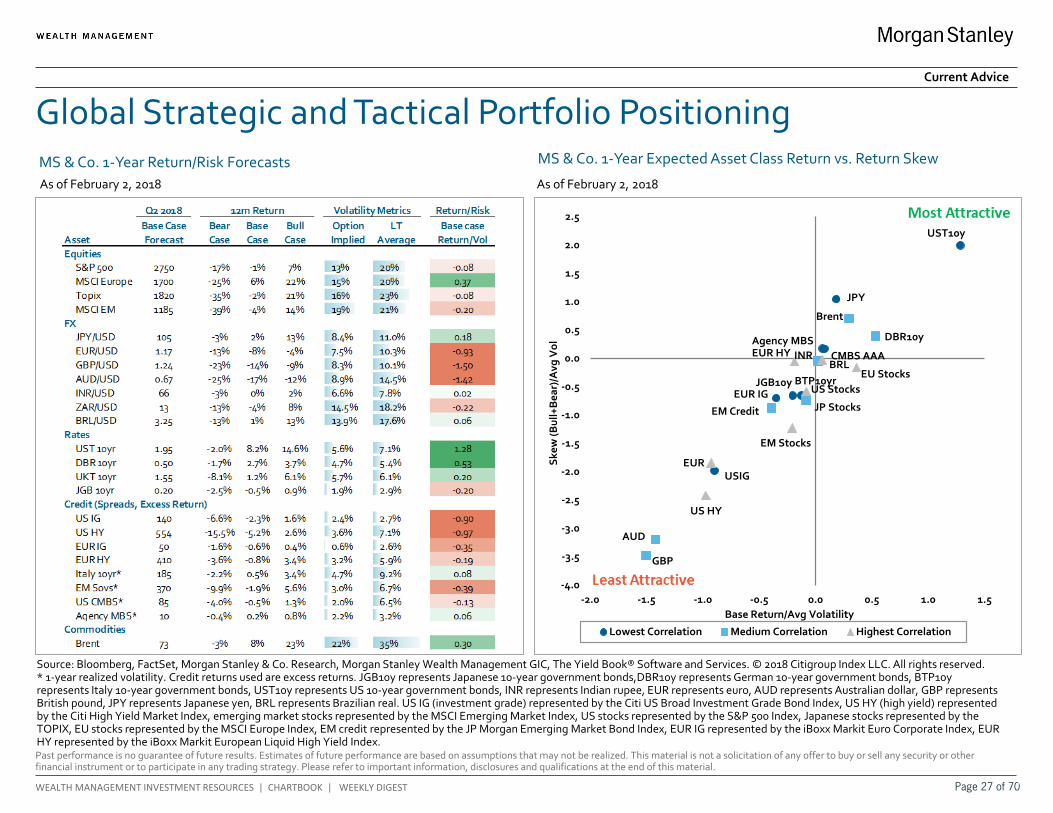

Global Strategic and Tactical Portfolio Positioning MS & Co. 1-Year Expected Asset Class Return vs. Return Skew

Source: Bloomberg, FactSet, Morgan Stanley & Co. Research, Morgan Stanley Wealth Management GIC, The Yield Book® Software and Services. © 2018 Citigroup Index LLC. All rights reserved. * 1-year realized volatility. Credit returns used are excess returns. JGB10y represents Japanese 10-year government bonds,DBR10y represents German 10-year government bonds, BTP10y represents Italy 10-year government bonds, UST10y represents US 10-year government bonds, INR represents Indian rupee, EUR represents euro, AUD represents Australian dollar, GBP represents British pound, JPY represents Japanese yen, BRL represents Brazilian real. US IG (investment grade) represented by the Citi US Broad Investment Grade Bond Index, US HY (high yield) represented by the Citi High Yield Market Index, emerging market stocks represented by the MSCI Emerging Market Index, US stocks represented by the S&P 500 Index, Japanese stocks represented by the TOPIX, EU stocks represented by the MSCI Europe Index, EM credit represented by the JP Morgan Emerging Market Bond Index, EUR IG represented by the iBoxx Markit Euro Corporate Index, EUR HY represented by the iBoxx Markit European Liquid High Yield Index.

Current Advice

MS & Co. 1-Year Return/Risk Forecasts As of February 2, 2018

UST10y

JPY

Agency MBS DBR10y

USIG

CMBS AAA

AUD

US StocksJGB10y

EUR

Brent

EUR IG

EM Credit

BTP10yrBRL

JP Stocks

GBP

EU Stocks

EM Stocks

INREUR HY

US HY

-4.0

-3.5

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

-2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5

Skew

(Bul

l+B

ear)

/Avg

Vol

Base Return/Avg Volatility

Lowest Correlation Medium Correlation Highest Correlation

As of February 2, 2018

Page 27 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

Source: FactSet, Morgan Stanley Wealth Management GIC. Other Developed Markets includes Canada, Australia, New Zealand, Hong Kong, and Singapore. Other Emerging Markets includes all MSCI Emerging Market countries except China and India. Developed Europe includes all MSCI Europe countries. Frontier Markets includes all MSCI Frontier Emerging Market countries. JPN represents Japan, GBR represents United Kingdom, USA represents United States, CNH (A) represents China A-Shares, CNH (H) represents China H-Shares, IND represents India. Information ratio is a ratio of portfolio returns above the returns of a benchmark (usually an index) to the volatility of those returns. For definitions of factors and universes, please reference our special report, Tactical Equity Allocation: Introducing a Systematic Framework for Short-Term Investment Views, dated December 2015. Note: ++ is most attractive, + is moderately attractive, 0 is neutral, - is moderately unattractive, -- is most unattractive.

Global Region/Sector Preferences

Global Top 10 Regions/Sectors Global Bottom 10 Regions/Sectors

USA Industrials Dev EUR Staples

GBR Discretionary IND Financials

USA Staples CNH (A) Healthcare

USA Discretionary Dev EUR REITs

JPN Discretionary Other Dev Mkt Util ities

Other Dev Mkt Discretionary IND Materials

Dev EUR Telecom CNH (A) Industrials

USA Tech CNH (A) Materials

USA Financials Dev EUR Tech

Other EM Energy CNH (A) Tech

GIC Tactical Equity Region/Sector Allocation Model Current Advice

Company Size & Style Tilt Preference by Region As of February 3, 2018

As of February 3, 2018

Small -- - 0 + ++ Large Growth -- - 0 + ++ Value

StyleMarket Cap

Emerging Markets

Reg

iona

l Pre

fere

nces

Other DM

Europe

United Kingdom

United States

Japan

As of February 3, 2018 Regional Factor Attractiveness Over NTM Relative to Global Equities

-- - 0 + ++Least Attractive Most Attractive

United States

Japan Europe UKOther

DMChina-A China-H India

Other EM

Deep Value - + 0 + + - ++ -- +

Near-Term Value - 0 + + + -- ++ -- +

Momentum + + - - - - ++ 0 +

Earnings Revisions ++ ++ - - 0 0 + -- -

Profitability + ++ 0 - - 0 -- + +

Earnings Quality ++ - - + + -- 0 - -

Total Yield + 0 + + + -- + -- 0

Capital Use + ++ 0 - 0 -- - -- 0

Total Score + + - 0 0 - ++ -- 0

NTM Forecasted IR 0.23 0.17 -0.05 0.10 0.08 -0.10 0.15 -0.22 0.05

Page 28 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

US

JapanTaiwan

Australia

China H

Russia

United Kingdom

Norway South Korea

Italy

Hong KongSingapore

Canada Spain DenmarkBrazil Saudi ArabiaThailand

France South Africa

Ireland

Germany

Netherlands

Sweden

MexicoIndonesia

China ASwitzerland

India

Malaysia

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5% 10% 15% 20% 25% 30% 35%

Fore

cast

ed R

etur

n

Forecasted Volatility

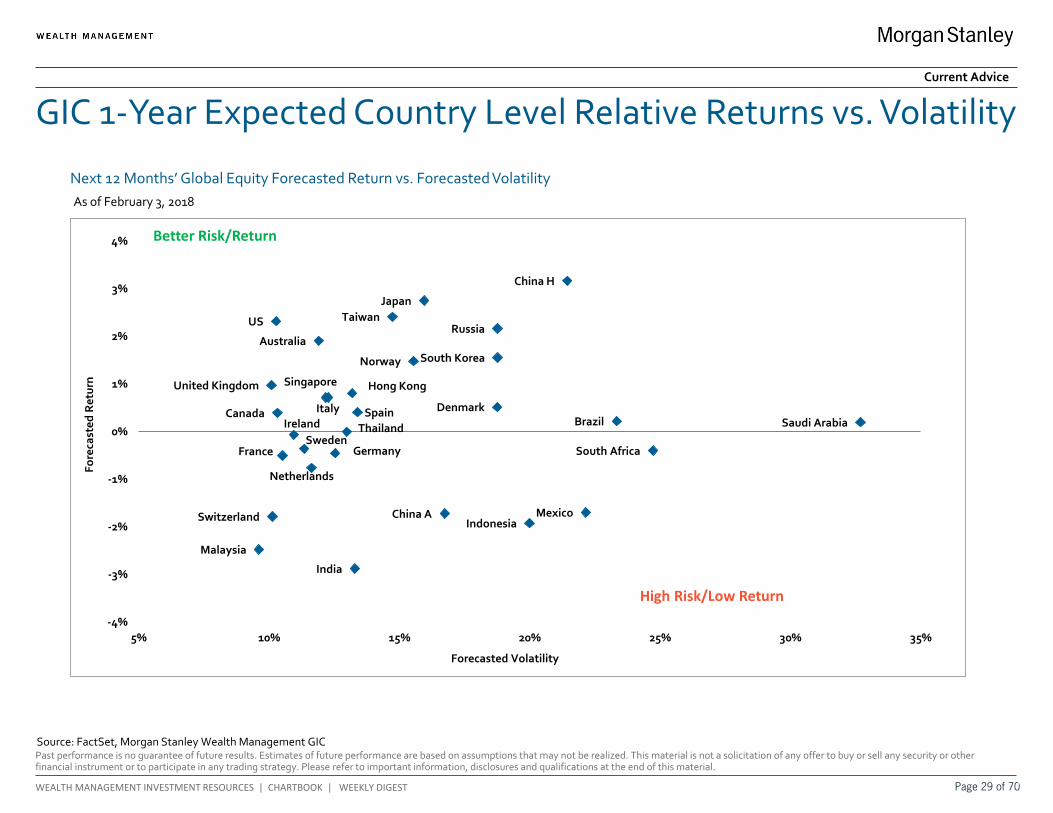

GIC 1-Year Expected Country Level Relative Returns vs. Volatility

Source: FactSet, Morgan Stanley Wealth Management GIC

Next 12 Months’ Global Equity Forecasted Return vs. Forecasted Volatility

Current Advice

Better Risk/Return

High Risk/Low Return

As of February 3, 2018

Page 29 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

00.10.20.30.40.50.60.70.80.91

60

70

80

90

100

110

120

130

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

USD Likely to StrengthenDXY Index

Dollar Appreciates

Historical Signals of the Dollar Strength Indicator

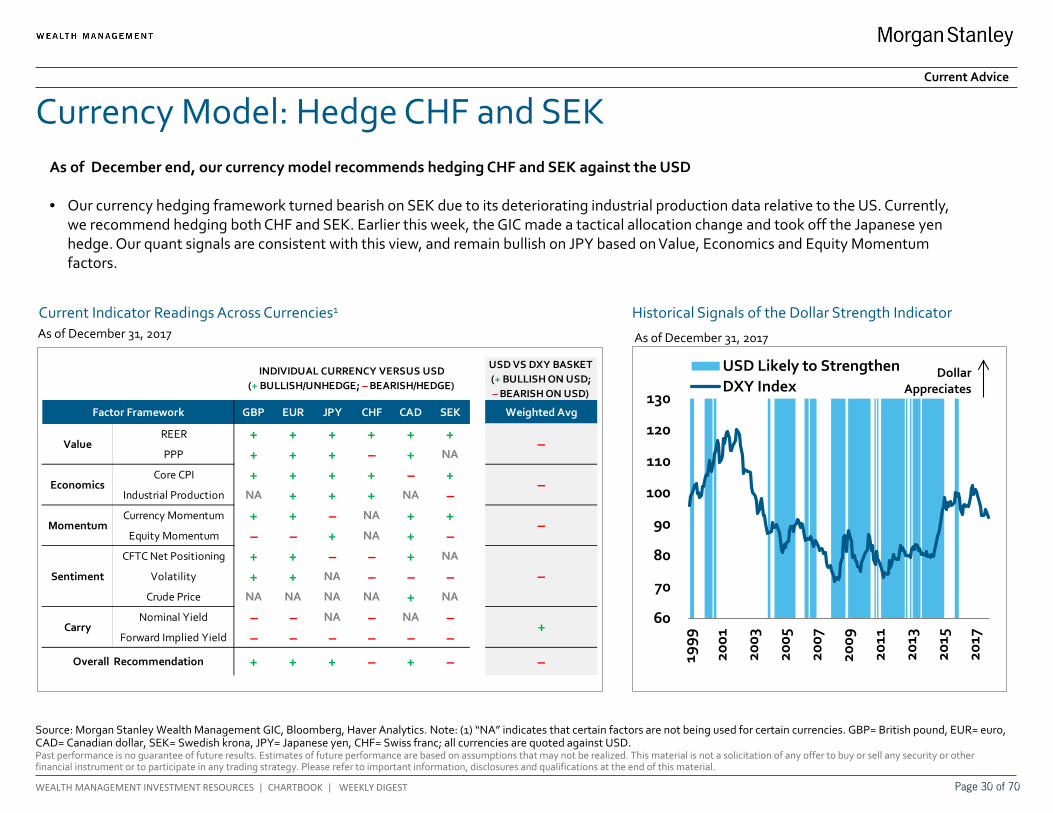

Currency Model: Hedge CHF and SEK

Source: Morgan Stanley Wealth Management GIC, Bloomberg, Haver Analytics. Note: (1) “NA” indicates that certain factors are not being used for certain currencies. GBP= British pound, EUR= euro, CAD= Canadian dollar, SEK= Swedish krona, JPY= Japanese yen, CHF= Swiss franc; all currencies are quoted against USD.

As of December 31, 2017

Current Advice

Current Indicator Readings Across Currencies1

As of December 31, 2017

USD VS DXY BASKET (+ BULLISH ON USD; – BEARISH ON USD)

GBP EUR JPY CHF CAD SEK Weighted Avg

REER + + + + + +PPP + + + – + NA

Core CPI + + + + – +Industrial Production NA + + + NA –Currency Momentum + + – NA + +

Equity Momentum – – + NA + –CFTC Net Positioning + + – – + NA

Volatility + + NA – – –Crude Price NA NA NA NA + NA

Nominal Yield – – NA – NA –Forward Implied Yield – – – – – –

+ + + – + – –

Carry

Factor Framework

Value

Economics

–

–

–

+

–

Momentum

Sentiment

INDIVIDUAL CURRENCY VERSUS USD (+ BULLISH/UNHEDGE; – BEARISH/HEDGE)

Overall Recommendation

As of December end, our currency model recommends hedging CHF and SEK against the USD • Our currency hedging framework turned bearish on SEK due to its deteriorating industrial production data relative to the US. Currently,

we recommend hedging both CHF and SEK. Earlier this week, the GIC made a tactical allocation change and took off the Japanese yen hedge. Our quant signals are consistent with this view, and remain bullish on JPY based on Value, Economics and Equity Momentum factors.

Page 30 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

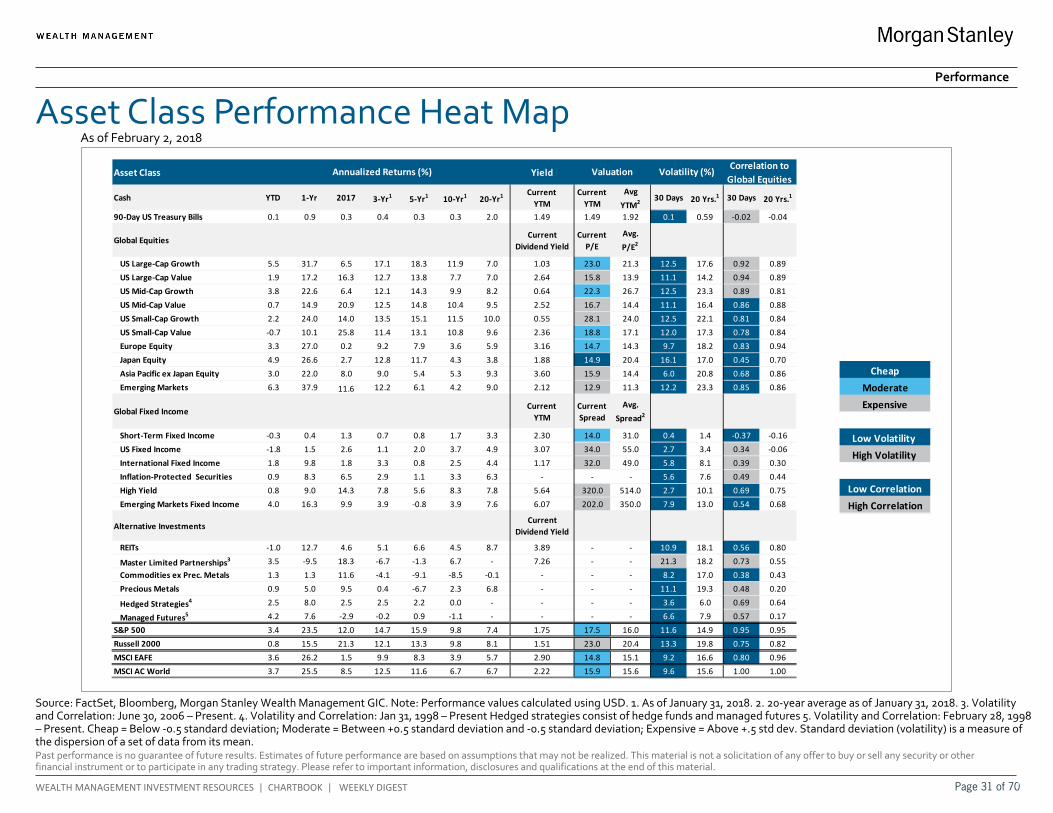

Asset Class Performance Heat Map

Source: FactSet, Bloomberg, Morgan Stanley Wealth Management GIC. Note: Performance values calculated using USD. 1. As of January 31, 2018. 2. 20-year average as of January 31, 2018. 3. Volatility and Correlation: June 30, 2006 – Present. 4. Volatility and Correlation: Jan 31, 1998 – Present Hedged strategies consist of hedge funds and managed futures 5. Volatility and Correlation: February 28, 1998 – Present. Cheap = Below -0.5 standard deviation; Moderate = Between +0.5 standard deviation and -0.5 standard deviation; Expensive = Above +.5 std dev. Standard deviation (volatility) is a measure of the dispersion of a set of data from its mean.

Performance

As of February 2, 2018

Moderate

High Volatility

High Correlation

Expensive

Cheap

Low Volatility

Low Correlation

Asset Class Yield

Cash YTD 1-Yr 2017 3-Yr1 5-Yr1 10-Yr1 20-Yr1 Current YTM

Current YTM

Avg YTM2 30 Days 20 Yrs.1 30 Days 20 Yrs.1

90-Day US Treasury Bills 0.1 0.9 0.3 0.4 0.3 0.3 2.0 1.49 1.49 1.92 0.1 0.59 -0.02 -0.04

Global Equities Current Dividend Yield

Current P/E

Avg. P/E2

US Large-Cap Growth 5.5 31.7 6.5 17.1 18.3 11.9 7.0 1.03 23.0 21.3 12.5 17.6 0.92 0.89 US Large-Cap Value 1.9 17.2 16.3 12.7 13.8 7.7 7.0 2.64 15.8 13.9 11.1 14.2 0.94 0.89 US Mid-Cap Growth 3.8 22.6 6.4 12.1 14.3 9.9 8.2 0.64 22.3 26.7 12.5 23.3 0.89 0.81 US Mid-Cap Value 0.7 14.9 20.9 12.5 14.8 10.4 9.5 2.52 16.7 14.4 11.1 16.4 0.86 0.88 US Small-Cap Growth 2.2 24.0 14.0 13.5 15.1 11.5 10.0 0.55 28.1 24.0 12.5 22.1 0.81 0.84 US Small-Cap Value -0.7 10.1 25.8 11.4 13.1 10.8 9.6 2.36 18.8 17.1 12.0 17.3 0.78 0.84 Europe Equity 3.3 27.0 0.2 9.2 7.9 3.6 5.9 3.16 14.7 14.3 9.7 18.2 0.83 0.94 Japan Equity 4.9 26.6 2.7 12.8 11.7 4.3 3.8 1.88 14.9 20.4 16.1 17.0 0.45 0.70 Asia Pacific ex Japan Equity 3.0 22.0 8.0 9.0 5.4 5.3 9.3 3.60 15.9 14.4 6.0 20.8 0.68 0.86 Emerging Markets 6.3 37.9 11.6 12.2 6.1 4.2 9.0 2.12 12.9 11.3 12.2 23.3 0.85 0.86

Global Fixed Income Current YTM

Current Spread

Avg. Spread2

Short-Term Fixed Income -0.3 0.4 1.3 0.7 0.8 1.7 3.3 2.30 14.0 31.0 0.4 1.4 -0.37 -0.16 US Fixed Income -1.8 1.5 2.6 1.1 2.0 3.7 4.9 3.07 34.0 55.0 2.7 3.4 0.34 -0.06 International Fixed Income 1.8 9.8 1.8 3.3 0.8 2.5 4.4 1.17 32.0 49.0 5.8 8.1 0.39 0.30 Inflation-Protected Securities 0.9 8.3 6.5 2.9 1.1 3.3 6.3 - - - 5.6 7.6 0.49 0.44 High Yield 0.8 9.0 14.3 7.8 5.6 8.3 7.8 5.64 320.0 514.0 2.7 10.1 0.69 0.75 Emerging Markets Fixed Income 4.0 16.3 9.9 3.9 -0.8 3.9 7.6 6.07 202.0 350.0 7.9 13.0 0.54 0.68

Alternative InvestmentsCurrent

Dividend Yield

REITs -1.0 12.7 4.6 5.1 6.6 4.5 8.7 3.89 - - 10.9 18.1 0.56 0.80

Master Limited Partnerships3 3.5 -9.5 18.3 -6.7 -1.3 6.7 - 7.26 - - 21.3 18.2 0.73 0.55 Commodities ex Prec. Metals 1.3 1.3 11.6 -4.1 -9.1 -8.5 -0.1 - - - 8.2 17.0 0.38 0.43 Precious Metals 0.9 5.0 9.5 0.4 -6.7 2.3 6.8 - - - 11.1 19.3 0.48 0.20

Hedged Strategies4 2.5 8.0 2.5 2.5 2.2 0.0 - - - - 3.6 6.0 0.69 0.64

Managed Futures5 4.2 7.6 -2.9 -0.2 0.9 -1.1 - - - - 6.6 7.9 0.57 0.17S&P 500 3.4 23.5 12.0 14.7 15.9 9.8 7.4 1.75 17.5 16.0 11.6 14.9 0.95 0.95Russell 2000 0.8 15.5 21.3 12.1 13.3 9.8 8.1 1.51 23.0 20.4 13.3 19.8 0.75 0.82MSCI EAFE 3.6 26.2 1.5 9.9 8.3 3.9 5.7 2.90 14.8 15.1 9.2 16.6 0.80 0.96MSCI AC World 3.7 25.5 8.5 12.5 11.6 6.7 6.7 2.22 15.9 15.6 9.6 15.6 1.00 1.00

Valuation Volatility (%) Correlation to Global Equities

Annualized Returns (%)

Page 31 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.

WEALTH MANAGEMENT INVESTMENT RESOURCES | CHARTBOOK | WEEKLY DIGEST

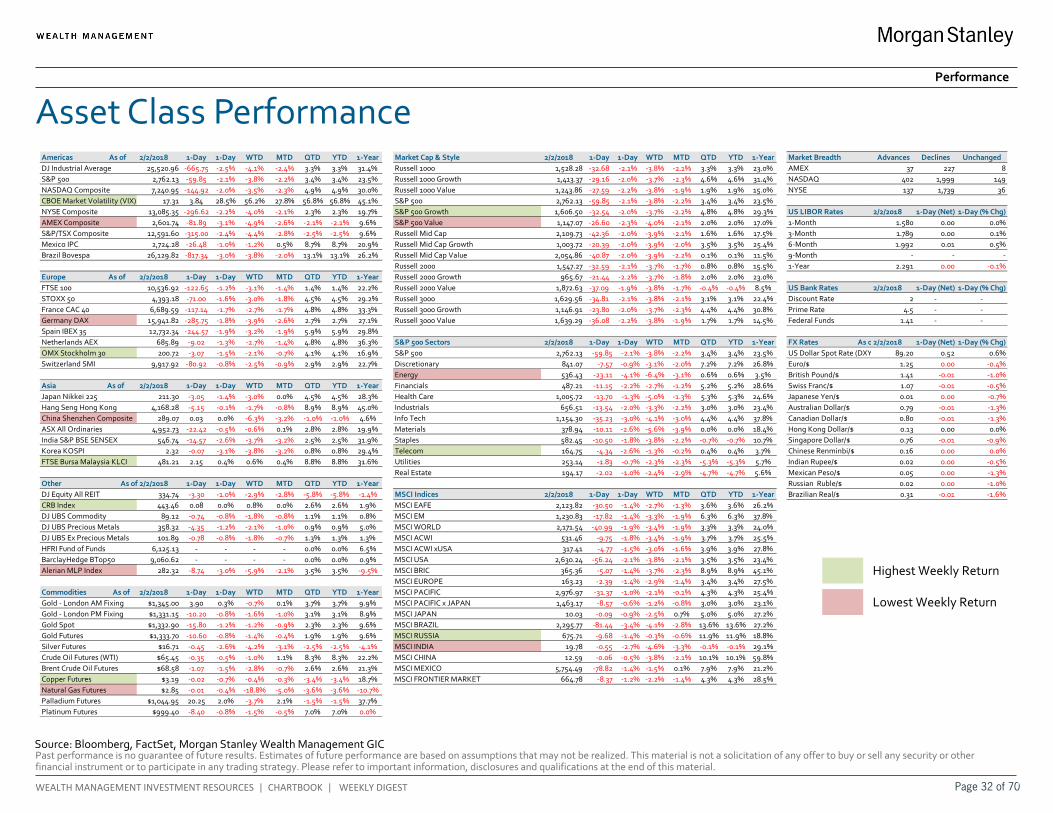

Americas As of 2/2/2018 1-Day 1-Day WTD MTD QTD YTD 1-Year Market Cap & Style 2/2/2018 1-Day 1-Day WTD MTD QTD YTD 1-Year Market Breadth Advances Declines UnchangedDJ Industrial Average 25,520.96 -665.75 -2.5% -4.1% -2.4% 3.3% 3.3% 31.4% Russell 1000 1,528.28 -32.68 -2.1% -3.8% -2.1% 3.3% 3.3% 23.0% AMEX 37 227 8S&P 500 2,762.13 -59.85 -2.1% -3.8% -2.2% 3.4% 3.4% 23.5% Russell 1000 Growth 1,413.37 -29.16 -2.0% -3.7% -2.3% 4.6% 4.6% 31.4% NASDAQ 402 1,999 149NASDAQ Composite 7,240.95 -144.92 -2.0% -3.5% -2.3% 4.9% 4.9% 30.0% Russell 1000 Value 1,243.86 -27.59 -2.2% -3.8% -1.9% 1.9% 1.9% 15.0% NYSE 137 1,739 36CBOE Market Volatility (VIX) 17.31 3.84 28.5% 56.2% 27.8% 56.8% 56.8% 45.1% S&P 500 2,762.13 -59.85 -2.1% -3.8% -2.2% 3.4% 3.4% 23.5%NYSE Composite 13,085.35 -296.62 -2.2% -4.0% -2.1% 2.3% 2.3% 19.7% S&P 500 Growth 1,606.50 -32.54 -2.0% -3.7% -2.2% 4.8% 4.8% 29.3% US LIBOR Rates 2/2/2018 1-Day (Net) 1-Day (% Chg)AMEX Composite 2,601.74 -81.89 -3.1% -4.9% -2.6% -2.1% -2.1% 9.6% S&P 500 Value 1,147.07 -26.60 -2.3% -4.0% -2.1% 2.0% 2.0% 17.0% 1-Month 1.580 0.00 0.0%S&P/TSX Composite 12,591.60 -315.00 -2.4% -4.4% -2.8% -2.5% -2.5% 9.6% Russell Mid Cap 2,109.73 -42.36 -2.0% -3.9% -2.1% 1.6% 1.6% 17.5% 3-Month 1.789 0.00 0.1%Mexico IPC 2,724.28 -26.48 -1.0% -1.2% 0.5% 8.7% 8.7% 20.9% Russell Mid Cap Growth 1,003.72 -20.39 -2.0% -3.9% -2.0% 3.5% 3.5% 25.4% 6-Month 1.992 0.01 0.5%Brazil Bovespa 26,129.82 -817.34 -3.0% -3.8% -2.0% 13.1% 13.1% 26.2% Russell Mid Cap Value 2,054.86 -40.87 -2.0% -3.9% -2.2% 0.1% 0.1% 11.5% 9-Month - - -

Russell 2000 1,547.27 -32.59 -2.1% -3.7% -1.7% 0.8% 0.8% 15.5% 1-Year 2.291 0.00 -0.1%Europe As of 2/2/2018 1-Day 1-Day WTD MTD QTD YTD 1-Year Russell 2000 Growth 965.67 -21.44 -2.2% -3.7% -1.8% 2.0% 2.0% 23.0%FTSE 100 10,536.92 -122.65 -1.2% -3.1% -1.4% 1.4% 1.4% 22.2% Russell 2000 Value 1,872.63 -37.09 -1.9% -3.8% -1.7% -0.4% -0.4% 8.5% US Bank Rates 2/2/2018 1-Day (Net) 1-Day (% Chg)STOXX 50 4,393.18 -71.00 -1.6% -3.0% -1.8% 4.5% 4.5% 29.2% Russell 3000 1,629.56 -34.81 -2.1% -3.8% -2.1% 3.1% 3.1% 22.4% Discount Rate 2 - -France CAC 40 6,689.59 -117.14 -1.7% -2.7% -1.7% 4.8% 4.8% 33.3% Russell 3000 Growth 1,146.91 -23.80 -2.0% -3.7% -2.3% 4.4% 4.4% 30.8% Prime Rate 4.5 - -Germany DAX 15,941.82 -285.75 -1.8% -3.9% -2.6% 2.7% 2.7% 27.1% Russell 3000 Value 1,639.29 -36.08 -2.2% -3.8% -1.9% 1.7% 1.7% 14.5% Federal Funds 1.41 - -Spain IBEX 35 12,732.34 -244.57 -1.9% -3.2% -1.9% 5.9% 5.9% 29.8%Netherlands AEX 685.89 -9.02 -1.3% -2.7% -1.4% 4.8% 4.8% 36.3% S&P 500 Sectors 2/2/2018 1-Day 1-Day WTD MTD QTD YTD 1-Year FX Rates As o 2/2/2018 1-Day (Net) 1-Day (% Chg)OMX Stockholm 30 200.72 -3.07 -1.5% -2.1% -0.7% 4.1% 4.1% 16.9% S&P 500 2,762.13 -59.85 -2.1% -3.8% -2.2% 3.4% 3.4% 23.5% US Dollar Spot Rate (DXY 89.20 0.52 0.6%Switzerland SMI 9,917.92 -80.92 -0.8% -2.5% -0.9% 2.9% 2.9% 22.7% Discretionary 841.07 -7.57 -0.9% -3.1% -2.0% 7.2% 7.2% 26.8% Euro/$ 1.25 0.00 -0.4%

Energy 536.43 -23.11 -4.1% -6.4% -3.1% 0.6% 0.6% 3.5% British Pound/$ 1.41 -0.01 -1.0%Asia As of 2/2/2018 1-Day 1-Day WTD MTD QTD YTD 1-Year Financials 487.21 -11.15 -2.2% -2.7% -1.2% 5.2% 5.2% 28.6% Swiss Franc/$ 1.07 -0.01 -0.5%Japan Nikkei 225 211.30 -3.05 -1.4% -3.0% 0.0% 4.5% 4.5% 28.3% Health Care 1,005.72 -13.70 -1.3% -5.0% -1.3% 5.3% 5.3% 24.6% Japanese Yen/$ 0.01 0.00 -0.7%Hang Seng Hong Kong 4,168.28 -5.15 -0.1% -1.7% -0.8% 8.9% 8.9% 45.0% Industrials 656.51 -13.54 -2.0% -3.3% -2.2% 3.0% 3.0% 23.4% Australian Dollar/$ 0.79 -0.01 -1.3%China Shenzhen Composite 289.07 0.03 0.0% -6.3% -3.2% -1.0% -1.0% 4.6% Info Tech 1,154.30 -35.23 -3.0% -4.1% -3.0% 4.4% 4.4% 37.8% Canadian Dollar/$ 0.80 -0.01 -1.3%ASX All Ordinaries 4,952.73 -22.42 -0.5% -0.6% 0.1% 2.8% 2.8% 19.9% Materials 378.94 -10.11 -2.6% -5.6% -3.9% 0.0% 0.0% 18.4% Hong Kong Dollar/$ 0.13 0.00 0.0%India S&P BSE SENSEX 546.74 -14.57 -2.6% -3.7% -3.2% 2.5% 2.5% 31.9% Staples 582.45 -10.50 -1.8% -3.8% -2.2% -0.7% -0.7% 10.7% Singapore Dollar/$ 0.76 -0.01 -0.9%Korea KOSPI 2.32 -0.07 -3.1% -3.8% -3.2% 0.8% 0.8% 29.4% Telecom 164.75 -4.34 -2.6% -1.3% -0.2% 0.4% 0.4% 3.7% Chinese Renminbi/$ 0.16 0.00 0.0%FTSE Bursa Malaysia KLCI 481.21 2.15 0.4% 0.6% 0.4% 8.8% 8.8% 31.6% Utilities 253.14 -1.83 -0.7% -2.3% -2.3% -5.3% -5.3% 5.7% Indian Rupee/$ 0.02 0.00 -0.5%

Real Estate 194.17 -2.02 -1.0% -2.4% -2.9% -4.7% -4.7% 5.6% Mexican Peso/$ 0.05 0.00 -1.3%Other As of 2/2/2018 1-Day 1-Day WTD MTD QTD YTD 1-Year Russian Ruble/$ 0.02 0.00 -1.0%DJ Equity All REIT 334.74 -3.30 -1.0% -2.9% -2.8% -5.8% -5.8% -1.4% MSCI Indices 2/2/2018 1-Day 1-Day WTD MTD QTD YTD 1-Year Brazilian Real/$ 0.31 -0.01 -1.6%CRB Index 443.46 0.08 0.0% 0.8% 0.0% 2.6% 2.6% 1.9% MSCI EAFE 2,123.82 -30.50 -1.4% -2.7% -1.3% 3.6% 3.6% 26.2%DJ UBS Commodity 89.12 -0.74 -0.8% -1.8% -0.8% 1.1% 1.1% 0.8% MSCI EM 1,230.83 -17.82 -1.4% -3.3% -1.9% 6.3% 6.3% 37.8%DJ UBS Precious Metals 358.32 -4.35 -1.2% -2.1% -1.0% 0.9% 0.9% 5.0% MSCI WORLD 2,171.54 -40.99 -1.9% -3.4% -1.9% 3.3% 3.3% 24.0%DJ UBS Ex Precious Metals 101.89 -0.78 -0.8% -1.8% -0.7% 1.3% 1.3% 1.3% MSCI ACWI 531.46 -9.75 -1.8% -3.4% -1.9% 3.7% 3.7% 25.5%HFRI Fund of Funds 6,125.13 - - - - 0.0% 0.0% 6.5% MSCI ACWI xUSA 317.41 -4.77 -1.5% -3.0% -1.6% 3.9% 3.9% 27.8%BarclayHedge BTop50 9,060.62 - - - - 0.0% 0.0% 0.9% MSCI USA 2,630.24 -56.24 -2.1% -3.8% -2.1% 3.5% 3.5% 23.4%Alerian MLP Index 282.32 -8.74 -3.0% -5.9% -2.1% 3.5% 3.5% -9.5% MSCI BRIC 365.36 -5.07 -1.4% -3.7% -2.3% 8.9% 8.9% 45.1%

MSCI EUROPE 163.23 -2.39 -1.4% -2.9% -1.4% 3.4% 3.4% 27.5%Commodities As of 2/2/2018 1-Day 1-Day WTD MTD QTD YTD 1-Year MSCI PACIFIC 2,976.97 -31.37 -1.0% -2.1% -0.1% 4.3% 4.3% 25.4%Gold - London AM Fixing $1,345.00 3.90 0.3% -0.7% 0.1% 3.7% 3.7% 9.9% MSCI PACIFIC x JAPAN 1,463.17 -8.57 -0.6% -1.2% -0.8% 3.0% 3.0% 23.1%Gold - London PM Fixing $1,331.15 -10.20 -0.8% -1.6% -1.0% 3.1% 3.1% 8.9% MSCI JAPAN 10.03 -0.09 -0.9% -2.5% 0.7% 5.0% 5.0% 27.2%Gold Spot $1,332.90 -15.80 -1.2% -1.2% -0.9% 2.3% 2.3% 9.6% MSCI BRAZIL 2,295.77 -81.44 -3.4% -4.1% -2.8% 13.6% 13.6% 27.2%Gold Futures $1,333.70 -10.60 -0.8% -1.4% -0.4% 1.9% 1.9% 9.6% MSCI RUSSIA 675.71 -9.68 -1.4% -0.3% -0.6% 11.9% 11.9% 18.8%Silver Futures $16.71 -0.45 -2.6% -4.2% -3.1% -2.5% -2.5% -4.1% MSCI INDIA 19.78 -0.55 -2.7% -4.6% -3.3% -0.1% -0.1% 29.1%Crude Oil Futures (WTI) $65.45 -0.35 -0.5% -1.0% 1.1% 8.3% 8.3% 22.2% MSCI CHINA 12.59 -0.06 -0.5% -3.8% -2.1% 10.1% 10.1% 59.8%Brent Crude Oil Futures $68.58 -1.07 -1.5% -2.8% -0.7% 2.6% 2.6% 21.3% MSCI MEXICO 5,754.49 -78.82 -1.4% -1.5% 0.1% 7.9% 7.9% 21.2%Copper Futures $3.19 -0.02 -0.7% -0.4% -0.3% -3.4% -3.4% 18.7% MSCI FRONTIER MARKET 664.78 -8.37 -1.2% -2.2% -1.4% 4.3% 4.3% 28.5%Natural Gas Futures $2.85 -0.01 -0.4% -18.8% -5.0% -3.6% -3.6% -10.7%Palladium Futures $1,044.95 20.25 2.0% -3.7% 2.1% -1.5% -1.5% 37.7%Platinum Futures $999.40 -8.40 -0.8% -1.5% -0.5% 7.0% 7.0% 0.0%

Asset Class Performance

Source: Bloomberg, FactSet, Morgan Stanley Wealth Management GIC

Performance

Highest Weekly Return

Lowest Weekly Return

Page 32 of 70

Past performance is no guarantee of future results. Estimates of future performance are based on assumptions that may not be realized. This material is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any trading strategy. Please refer to important information, disclosures and qualifications at the end of this material.