the global market for u.s. lpg - platts€¢ in business since the mid-1980s • primary source...

TRANSCRIPT

©2014, ESAI Energy LLC, 401 Edgewater Place, Suite 640 | Wakefield MA 01880 | T: +1781.245.2036 | www.esai.com

The Global Market for U.S. LPG

Prepared for:

Platts 4th Annual NGLs Conference, Houston September 30, 2014

Presented by: Vivek S. Mathur

ESAI Energy, LLC

• In business since the mid-1980s

• Primary source bottom-up data collection and analysis.

• tracks ethane, propane & butane (LPG), naphtha, plant and lease

condensate supply, demand, inventories and trade data by country, globally.

• analyzes and forecasts petroleum and alternative fuels markets.

• Clients include producers, transformers and consumers of energy worldwide

• Headquarters outside of Boston

2

About ESAI Energy

Presentation Structure

U.S. LPG Supply/Demand Outlook to 2020 o Is there no choice but to export? o The exportable surplus

Global Markets for U.S. LPG

o Latin America o Europe o Asia

Impact on Trade Flows

3

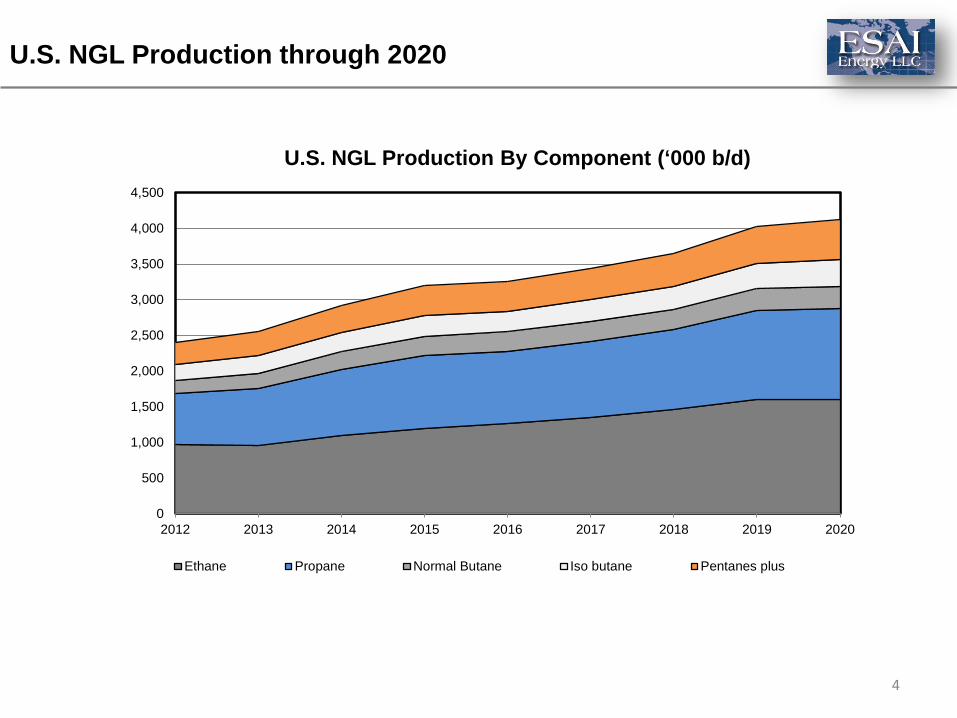

U.S. NGL Production through 2020

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2012 2013 2014 2015 2016 2017 2018 2019 2020

U.S. NGL Production By Component (‘000 b/d)

Ethane Propane Normal Butane Iso butane Pentanes plus

4

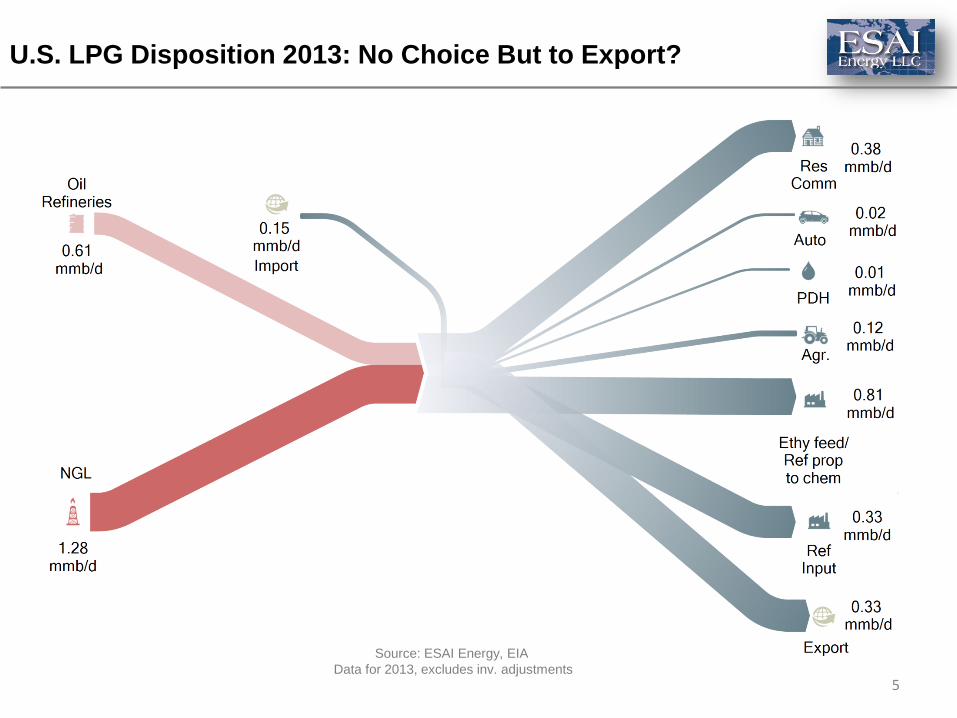

U.S. LPG Disposition 2013: No Choice But to Export?

5

Source: ESAI Energy, EIA Data for 2013, excludes inv. adjustments

0

500

1,000

1,500

2,000

2,500

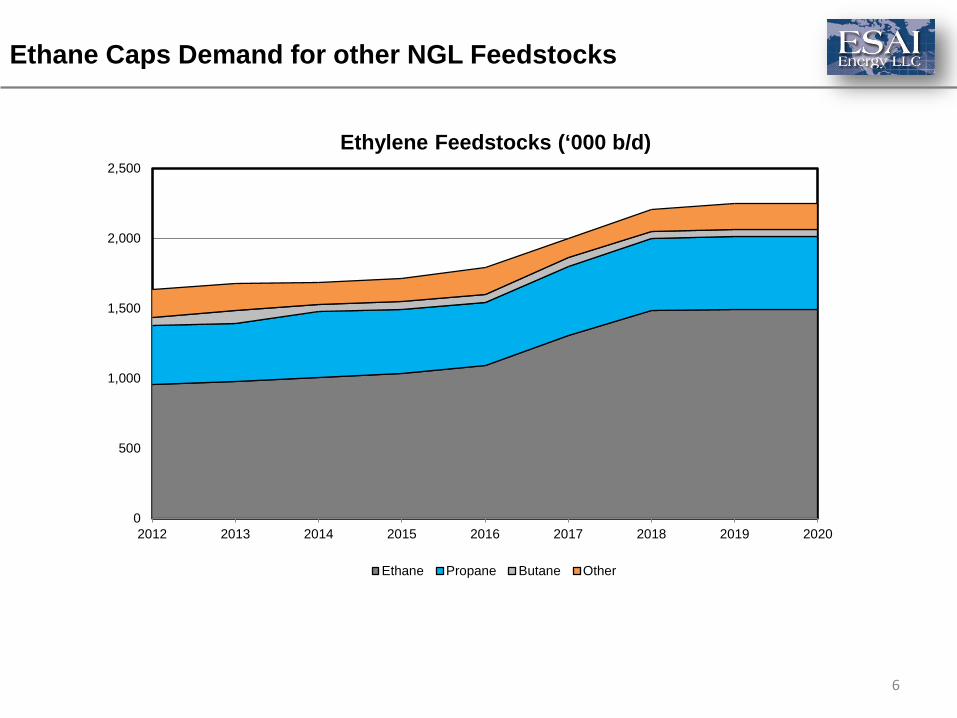

2012 2013 2014 2015 2016 2017 2018 2019 2020

Ethylene Feedstocks (‘000 b/d)

Ethane Propane Butane Other

6

Ethane Caps Demand for other NGL Feedstocks

7

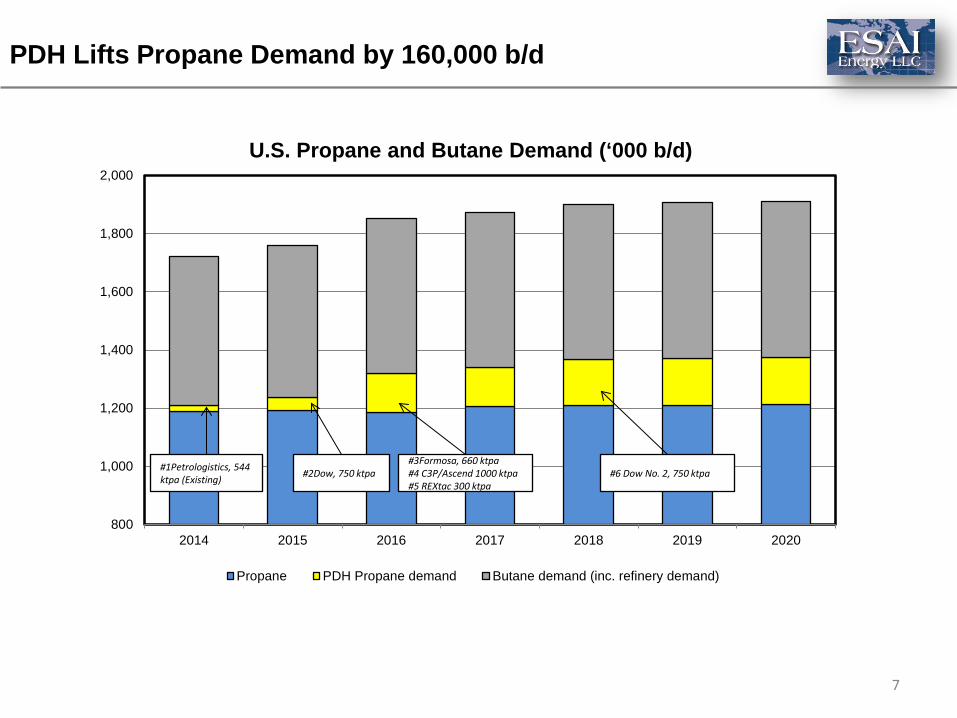

PDH Lifts Propane Demand by 160,000 b/d

800

1,000

1,200

1,400

1,600

1,800

2,000

2014 2015 2016 2017 2018 2019 2020

U.S. Propane and Butane Demand (‘000 b/d)

Propane PDH Propane demand Butane demand (inc. refinery demand)

#1Petrologistics, 544 ktpa (Existing)

#3Formosa, 660 ktpa #4 C3P/Ascend 1000 ktpa #5 REXtac 300 ktpa

#2Dow, 750 ktpa #6 Dow No. 2, 750 ktpa

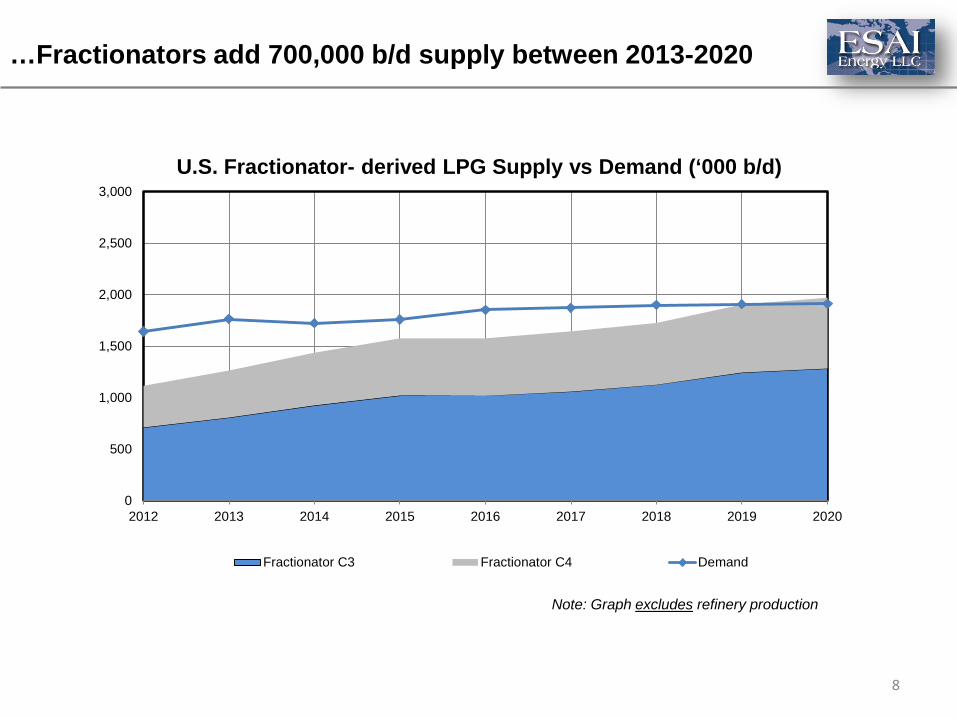

…Fractionators add 700,000 b/d supply between 2013-2020

8

0

500

1,000

1,500

2,000

2,500

3,000

2012 2013 2014 2015 2016 2017 2018 2019 2020

U.S. Fractionator- derived LPG Supply vs Demand (‘000 b/d)

Fractionator C3 Fractionator C4 Demand

Note: Graph excludes refinery production

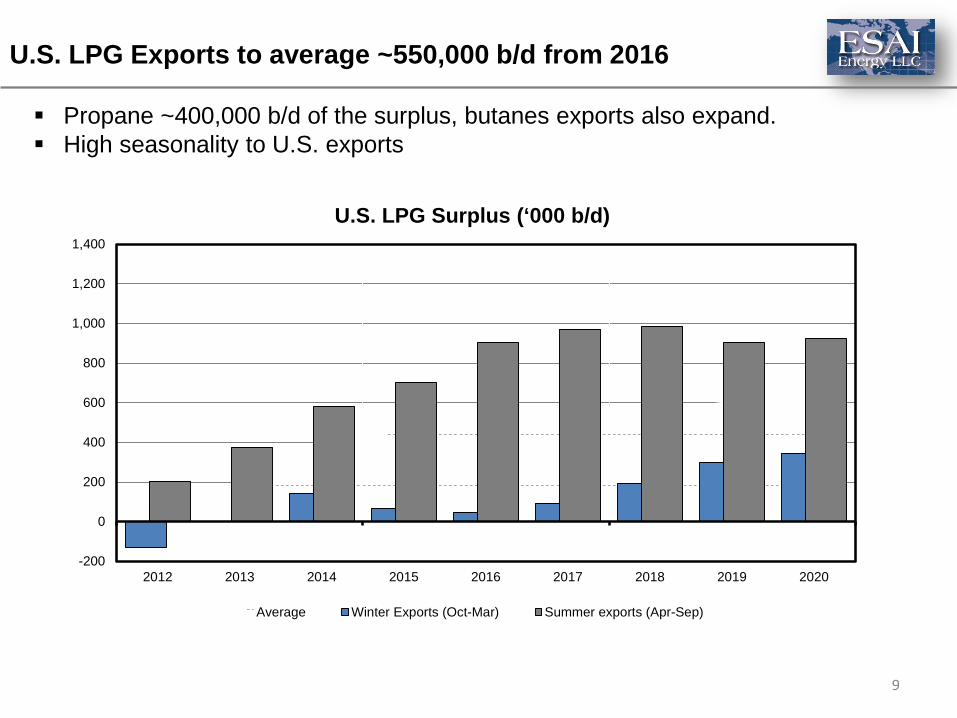

U.S. LPG Exports to average ~550,000 b/d from 2016

9

-200

0

200

400

600

800

1,000

1,200

1,400

2012 2013 2014 2015 2016 2017 2018 2019 2020

U.S. LPG Surplus (‘000 b/d)

Average Winter Exports (Oct-Mar) Summer exports (Apr-Sep)

Propane ~400,000 b/d of the surplus, butanes exports also expand. High seasonality to U.S. exports

U.S. & Canadian LPG Terminal Capacity* (‘000 b/d)

10

0

200

400

600

800

1,000

1,200

1,400

2013 2014 2015 2016 2017 2018 2019 2020

Pembina, BC (Potential)

Altagas/Idemitsu, BC Coast (Potential)

P66-Freeport

BWP/Williams-Lake Charles

Oxy-Ingleside

DCP-Chesapeake

Martin Gas-Pt Aransas

Sea 3-Newington NH

Sea 3 - Tampa

Trafigura-Corpus Christi

Sunoco-Marcus Hook PA

ETC (SXL/LS) Mariner South

Petrogas-Ferndale

Targa-Galena Park

Enterprise-Houston

An LPG Export Capacity Overbuild?

*Capacity announced & under evaluation

Who Will Absorb U.S. LPG? ELLESMERE ISLAND

Household 53%

Autofuel 9%

Petchem 26%

Other industry

12%

Global LPG Demand By Sector, 2013

Key Regional Deficits, 2013

(1,800)

(1,600)

(1,400)

(1,200)

(1,000)

(800)

(600)

(400)

(200)

0

Lat Am Asia Europe Other

11

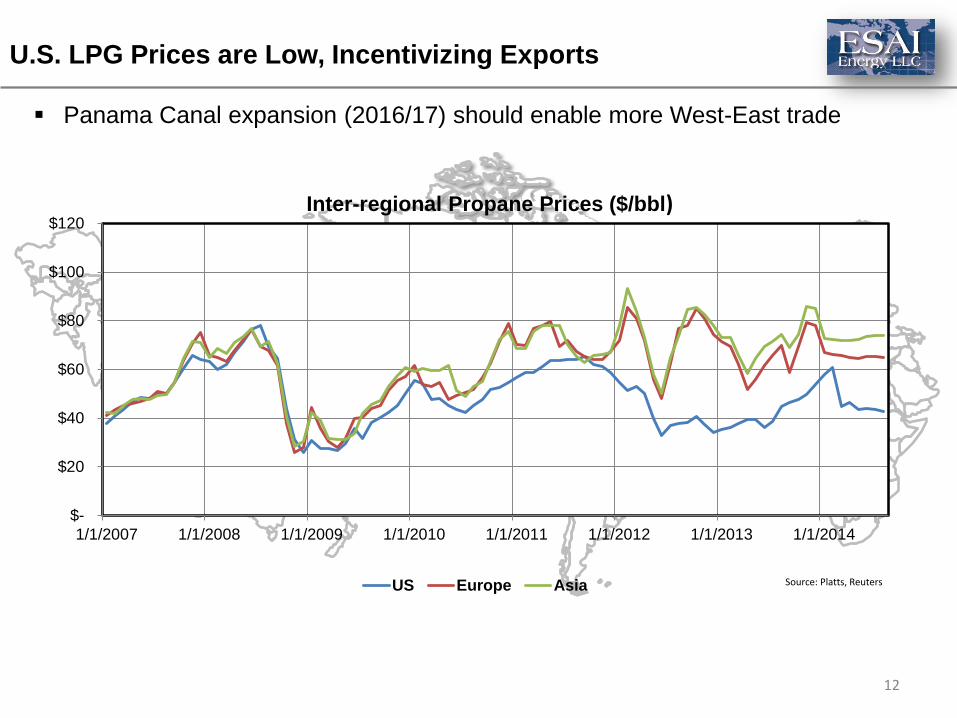

U.S. LPG Prices are Low, Incentivizing Exports ELLESMERE ISLAND

$-

$20

$40

$60

$80

$100

$120

1/1/2007 1/1/2008 1/1/2009 1/1/2010 1/1/2011 1/1/2012 1/1/2013 1/1/2014

Inter-regional Propane Prices ($/bbl)

US Europe Asia Source: Platts, Reuters

Panama Canal expansion (2016/17) should enable more West-East trade

12

13

U.S. Propane and Butane Exports by Destination

0

50

100

150

200

250

300

350

400

2012 2013 2014 YTD

Asia

Europe

Mexico

Canada

S. America

C.America

Caribbean0

50

100

150

200

250

300

350

400

2012 2013 2014 YTD

U.S. Propane Exports (‘000 b/d) U.S. Butane Exports (‘000 b/d)

H1 2014 H1 2014

14

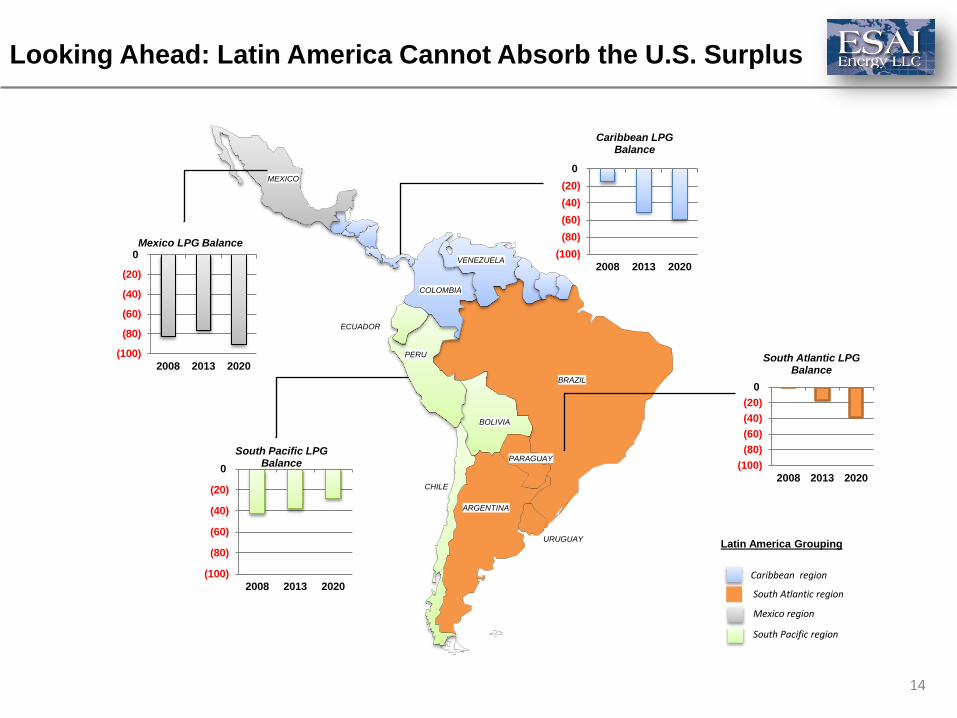

MEXICO

COLOMBIA

VENEZUELA

BRAZIL

PERU

ECUADOR

BOLIVIA

PARAGUAY

CHILE

ARGENTINA

URUGUAY

Caribbean region

South Atlantic region

Mexico region

South Pacific region

Latin America Grouping

Looking Ahead: Latin America Cannot Absorb the U.S. Surplus

(100)(80)(60)(40)(20)

0

2008 2013 2020

Caribbean LPG Balance

(100)

(80)

(60)

(40)

(20)

0

2008 2013 2020

Mexico LPG Balance

(100)

(80)

(60)

(40)

(20)

0

2008 2013 2020

South Pacific LPG Balance (100)

(80)(60)(40)(20)

0

2008 2013 2020

South Atlantic LPG Balance

15

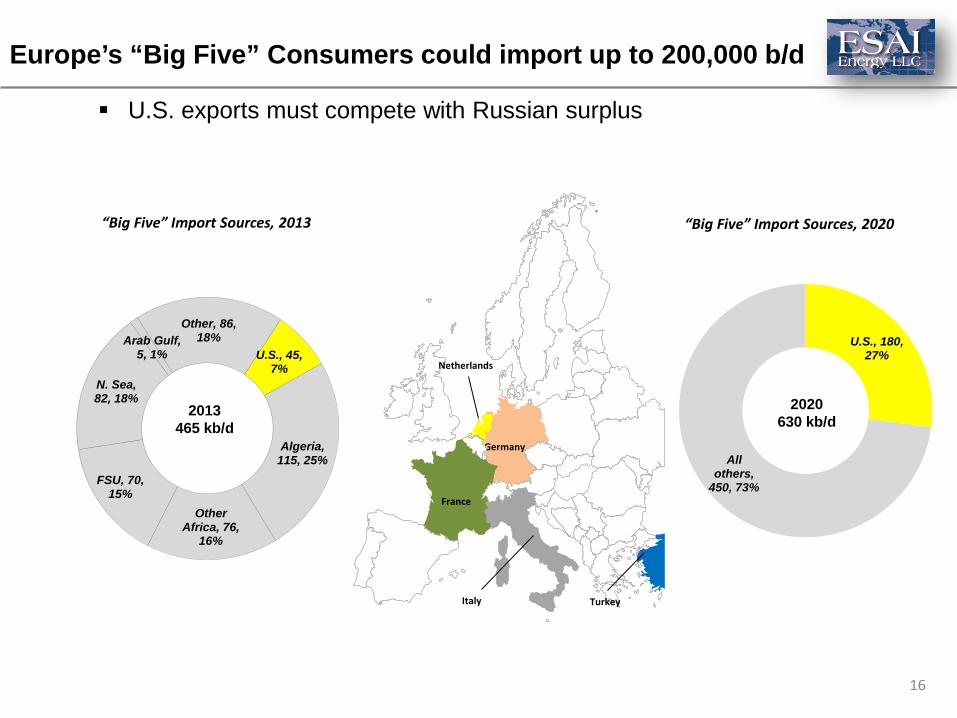

European petchems expand LPG, and shut down some naphtha-based capacity Turkey adds one PDH project

How Much Could Europe Absorb?

2013 2020

Ethane Naphtha Propane Butane Other

Ethylene Production By Feedstock (mil tpa)

18.5 19

16

Germany

France

U.S. exports must compete with Russian surplus

U.S., 45, 7%

Algeria, 115, 25%

Other Africa, 76,

16%

FSU, 70, 15%

N. Sea, 82, 18%

Arab Gulf, 5, 1%

Other, 86, 18%

2013 465 kb/d

U.S., 180, 27%

All others,

450, 73%

2020 630 kb/d

“Big Five” Import Sources, 2020 “Big Five” Import Sources, 2013

Italy Turkey

Netherlands

Europe’s “Big Five” Consumers could import up to 200,000 b/d

17

• Al- KARAANA (2017), 1300 ktpa P/E

• RUWAIS/TAKREER PDH (2014), 500 ktpa • Al- CHEMEYA PDH, 1300 ktpa (+2016) • ADBIC , 1450 ktpa, (+2017) P/B

KEY MIX FEED PETROCHEMICAL PROJECTS *

* Selected list of projects known, or expected to consume LPG

• SADARA (2016) 1500 ktpa, N/P

Note: E= Ethane, P=Propane, B= Butane, N= Naphtha

Petchem Demand in the Mideast Caps LPG Exports

Exports remain in the 1 million b/d range AG mix-feed project cancellations (eg. Al-Sejeel) poses risks

2013 2020

Ethane Naphtha Propane Butane Other

Ethylene Production By Feedstock (mil tpa)

23

29

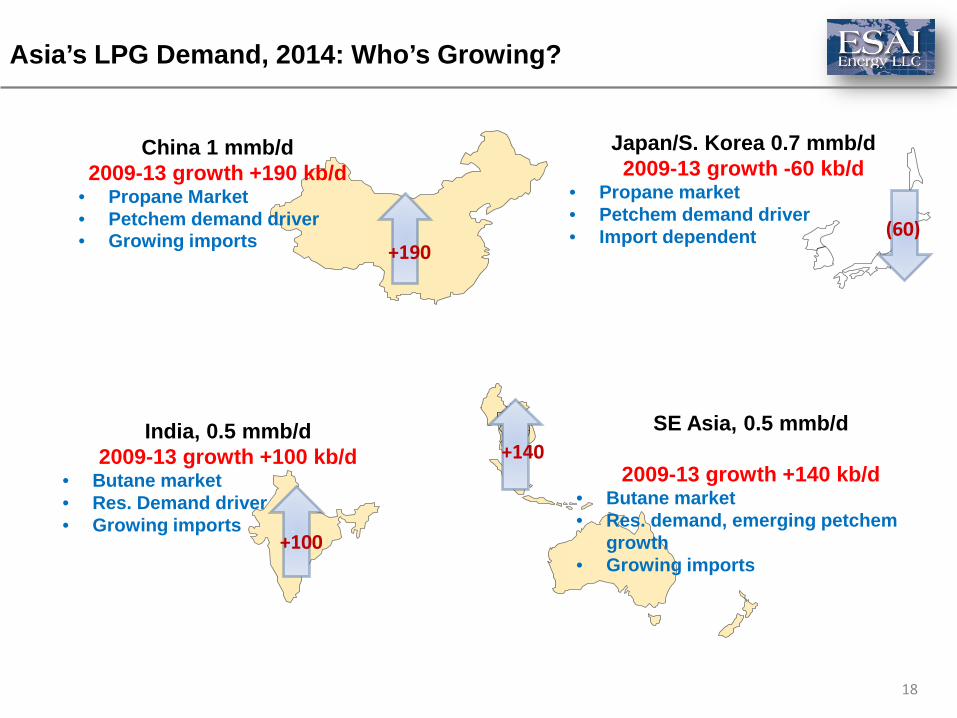

Asia’s LPG Demand, 2014: Who’s Growing?

Japan/S. Korea 0.7 mmb/d 2009-13 growth -60 kb/d

• Propane market • Petchem demand driver • Import dependent

SE Asia, 0.5 mmb/d

2009-13 growth +140 kb/d • Butane market • Res. demand, emerging petchem

growth • Growing imports

India, 0.5 mmb/d 2009-13 growth +100 kb/d

• Butane market • Res. Demand driver • Growing imports

China 1 mmb/d 2009-13 growth +190 kb/d

• Propane Market • Petchem demand driver • Growing imports +190

(60)

+100

+140

18

19

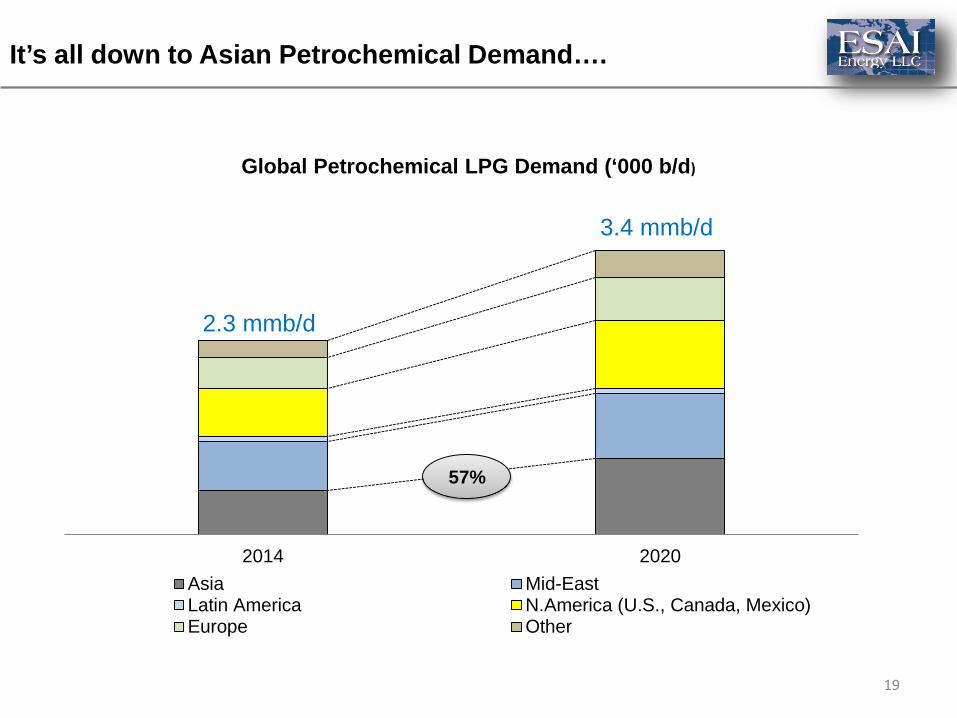

It’s all down to Asian Petrochemical Demand….

2014 2020

Global Petrochemical LPG Demand (‘000 b/d)

Asia Mid-EastLatin America N.America (U.S., Canada, Mexico)Europe Other

2.3 mmb/d

3.4 mmb/d

57%

..especially in China

China’s PDH Projects: Impact on Propane Demand (‘000 b/d)

PDH Propane demand 200,000 b/d by 2015, demand could reach 350,000 b/d 2016+

0

50

100

150

200

250

300

350

400

2013 2014 2015 2016+

Other

Jiangsu Haili

Changjiang Natural Gas Chem

Oriental Energy - 2

Oriental Energy - 1

Meide PC -2

Meide PC -1

Yantai Wanhua

Yanzijiang PC Phase 1

Shaoxing Sanyuan

Satellite

Ningbo Haiyue

Tianjin Bohai

20

21

…this drives up Asian Imports

2014 2020

Res/Comm Petchem Transport Supply

Asia LPG Supply/Demand (‘000 b/d)

3 mmb/d

3.5 mmb/d

Note: Other demand grouped in Res/Comm. demand in this chart

22

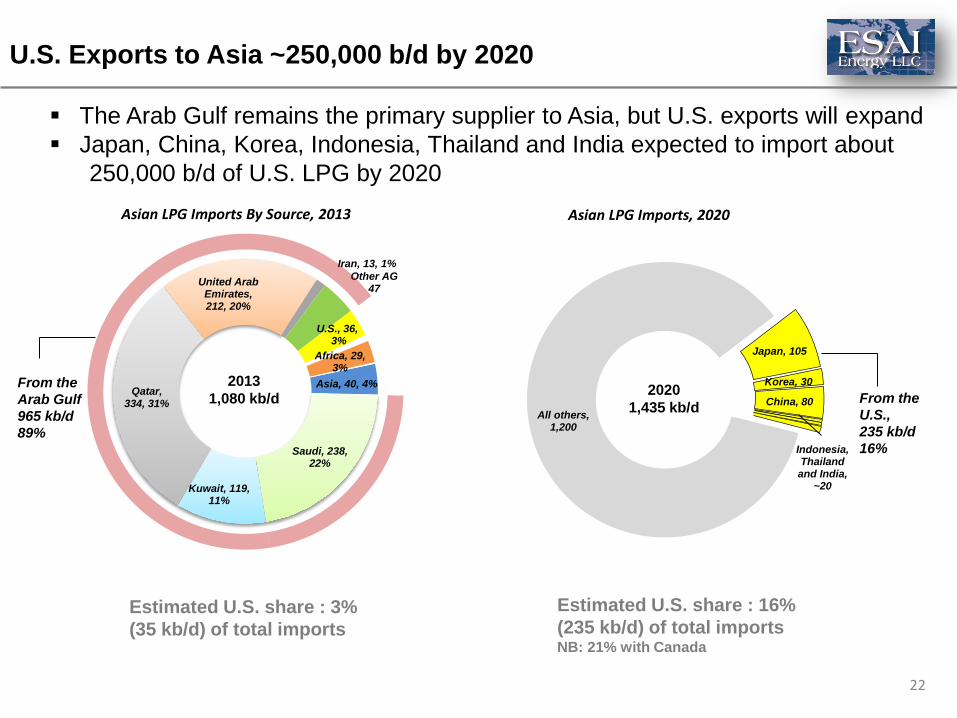

The Arab Gulf remains the primary supplier to Asia, but U.S. exports will expand Japan, China, Korea, Indonesia, Thailand and India expected to import about 250,000 b/d of U.S. LPG by 2020

Asia, 40, 4%

Saudi, 238, 22%

Kuwait, 119, 11%

Qatar,

334, 31%

United Arab Emirates, 212, 20%

Iran, 13, 1% Other AG

47

U.S., 36, 3%

Africa, 29, 3%

2013 1,080 kb/d

All others, 1,200

Japan, 105

Korea, 30

China, 80

Indonesia, Thailand and India,

~20

2020 1,435 kb/d

Asian LPG Imports By Source, 2013 Asian LPG Imports, 2020

From the U.S., 235 kb/d 16%

From the Arab Gulf 965 kb/d 89%

Estimated U.S. share : 3% (35 kb/d) of total imports

Estimated U.S. share : 16% (235 kb/d) of total imports NB: 21% with Canada

U.S. Exports to Asia ~250,000 b/d by 2020

23

200

60

Propane ($/bbl), MBV = $43 Saudi CP ($/bbl) =$73

970

(Figures in ‘000 b/d)

USGC/AG LPG Trade, 2013: West-East Trade

330

40

24

210

185

1000

230

(Figures in ‘000 b/d)

625

Hypothetical USGC/AG LPG Trade, 2020: West-East Trade

+80*

*Potential Canadian exports to Asia

Fundamentals: U.S. Exports Upend Global LPG Trade

• By 2020, U.S. exports will be in the 600,000 b/d range.

• Latin America’s inability to absorb more U.S. LPG will boost exports beyond the Americas.

• Petrochemical demand growth should drive up Asian imports Pricing: Mont Belvieu Pricing Will Impact Asia

• U.S. origin LPG will be 16 percent of Asian LPG imports in 2020.

North American imports into Asia including Canada could be in the 20 percent range.

• Middle Eastern LPG producers will defend market share and lower

prices in the coming years.

25

In Summary

©2014, ESAI Energy LLC, 401 Edgewater Place, Suite 640 | Wakefield MA 01880 | T: +1781.245.2036 | www.esai.com

Thank You!

Questions?

Vivek S. Mathur [email protected]

26