the great refesh

TRANSCRIPT

The Great REfresh Marti O’Mara PhD, CRE Minneapolis Minnesota

November 2015

Confidential – Colliers International 2014 2 The Place Strategy Process has been applied to ~ 2 billion SF of occupancy including 12 of the 100 largest office portfolios

Strategy and Innovation Consulting: Background

Much of what you have today may not be what you will need in the future. Corporate real estate and facility investments are the longest range commitments most organizations make and require a view towards the company’s future competitive demands that go well beyond the typical business forecasting horizon. The development of a Colliers Place Strategy focuses on aligning location, workplace, culture and technology with future business demand. Our solutions result in impactful real estate and workplace solutions that increase innovation, productivity and business returns.

Confidential – Colliers International 2014

What is the Great REfresh?

1. Aging assets: most office buildings today are more than 30 years old. Most interiors are 10 or more years older.

2. The connections between social, economic and technological change that are impacting

where, how and when people work in offices 3. New drivers of location strategy

4. What is a “future ready” building?

5. How can we respond?

3

Confidential – Colliers International 2014

1. Aging Assets While overall demand for office space is not increasing (actually decreasing) except in very few markets, the age and obsolescence of assets is a growing issue.

Deferred maintenance

High cost of renovation

Obsolete layout

Obsolete infrastructure

Wrong location

Fun facts! • SMR found, the average age of U.S. commercial buildings (all classes – 4.61 million

buildings) is 41.7 years.

• The weighted average office building age in Manhattan is 60.4 years.

4

Confidential – Colliers International 2014 5

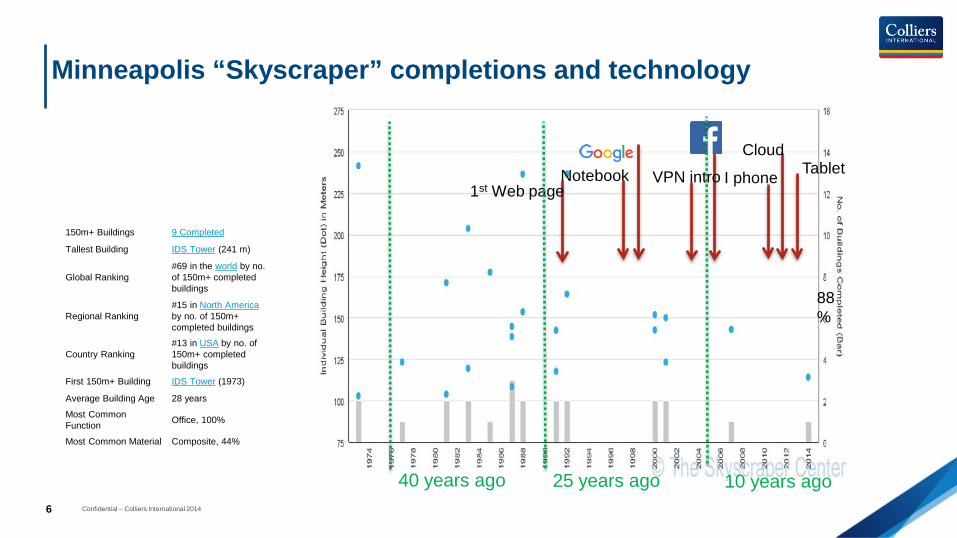

1st Web page I phone Notebook Tablet VPN intro

Cloud

US “Skyscraper” completions and office technology advancements

10 years ago 25 years ago

88%

40 years ago

Confidential – Colliers International 2014 6

1st Web page I phone Notebook Tablet VPN intro

Cloud

Minneapolis “Skyscraper” completions and technology

10 years ago 25 years ago

88%

40 years ago

150m+ Buildings 9 Completed

Tallest Building IDS Tower (241 m)

Global Ranking #69 in the world by no. of 150m+ completed buildings

Regional Ranking #15 in North America by no. of 150m+ completed buildings

Country Ranking #13 in USA by no. of 150m+ completed buildings

First 150m+ Building IDS Tower (1973)

Average Building Age 28 years

Most Common Function Office, 100%

Most Common Material Composite, 44%

Confidential – Colliers International 2014

Example: “older asset” – ca 1980’s - Rigid layout and poor utilization (20 year lease was up)

7

Bldg Address Lease

Rentable Area (SF)

Occupied/ assigned

Capacity (# workstations)

SF/per person

SF/per workstation

1 15 Hampshire St 107,000 294 474 364 226 2 9 & 11 Hampshire St 160,000 337 485 475 330 3 100 Hampshire Rd 124,803 384 531 325 235 4 5 Hampshire St 83,400 325 522 257 160 Total 475,203 1340 2012 355 236

Bldg.1 2nd flr.

Bldg.2 2nd flr.

No one wants to work in an ugly box….

YUCK!

“High utilization breeds collaboration, while high vacancy breeds more vacancy.”

8

2. The perfect storm leading to the changing workplace

Sustainability & Carbon reduction

Demographics: younger workers’

work-styles

Operating Cost Reduction

$$

Cost & Performance of Mobility Tools

Lag between our workplaces and the

work that we actually do

10

Boomers now 70-50

Gen X: 49-35 a lot fewer

Next gen/millennials “Arrested Development”

Where are our employees, managers and leaders of the future?

Changing workforce demographics

Underlying social trends impacting workplace Everything in life is getting spread out over more years

11

2. Longer periods of formal education. It takes longer to achieve a college degree (6yrs) and a larger proportion of college graduates pursue post-college studies - 40%.

1. Longer life expectancy: 50 years ago, average life expectancy in the US was 69.9 years. Today it is 78.1. Expansion of “middle years” rather than elderly years is key.

3. Marrying later – or not at all In the 70’s – average age of marriage for a college educated person was 23.By 2000, rose to age 28+. By married couples are less than half of American households, compared to nearly 80% in the 1950’s.

4. Having children later – or not at all Labor force participation for mothers with children under 18 is 70%, compared with 47% in the 1970’s. 20-25% of US women will not have children. It is already 25% in the UK.

Confidential – Colliers International 2014

How much space” is now a really hard question!

12

Three “P”s of High Performance Workplace Transformation

ToPography

People

Property Highest cost/FTE Ability to exit space Poorest quality space

Already mobile Work processes can support mobility Demographics – career stage

Long commutes Public transportation options Attractiveness of urban core, edge cities

When you don’t have to go to the office, what makes you want to go there?

Confidential – Colliers International 2014 13

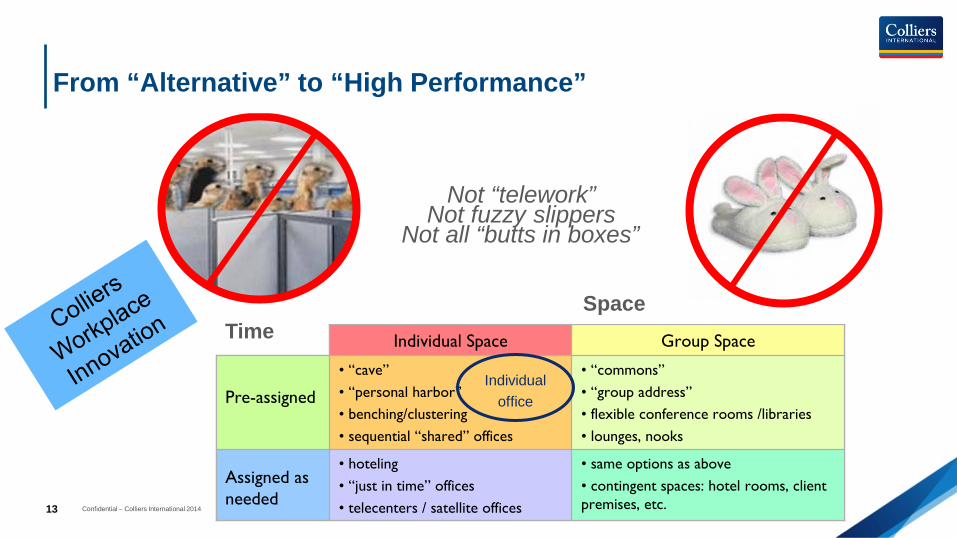

Not “telework” Not fuzzy slippers

Not all “butts in boxes”

Assigned as needed

Pre-assigned

Group SpaceIndividual Space

• same options as above• contingent spaces: hotel rooms, client premises, etc.

• hoteling• “just in time” offices• telecenters / satellite offices

• “commons”• “group address”• flexible conference rooms /libraries• lounges, nooks

• “cave”• “personal harbor”• benching/clustering• sequential “shared” offices

Assigned as needed

Pre-assigned

Group SpaceIndividual Space

• same options as above• contingent spaces: hotel rooms, client premises, etc.

• hoteling• “just in time” offices• telecenters / satellite offices

• “commons”• “group address”• flexible conference rooms /libraries• lounges, nooks

• “cave”• “personal harbor”• benching/clustering• sequential “shared” offices

Time Space

Individual office

From “Alternative” to “High Performance”

Confidential – Colliers International 2014

Space per FTE is shrinking ‘increased asset utilization’ = higher load

14 SF/PERSON VARIES BY REGION AND INDUSTRY

SF/PERSON PER IS TRENDING DOWNWARD DRAMATICALLY

0

100

200

300

400

500 U.S. Square Feet per Worker in 2010

180

10 years 5 years 3 years Today

227 SQ.FT

205 SQ.FT 180

SQ.FT 135 SQ.FT

Corenet Global, NY Times, Feb. 2, 2015

BOMA Experience Exchange Report

OFFICES VS. CUBES Based on CoStar data

In 3 Years

100? SQ.FT

0

100

200

300

400

500Office Space per Worker by U.S. Industry

Office 186 SF

Cube 90 SF

Confidential – Colliers International 2014

3. New drivers of location strategy

15

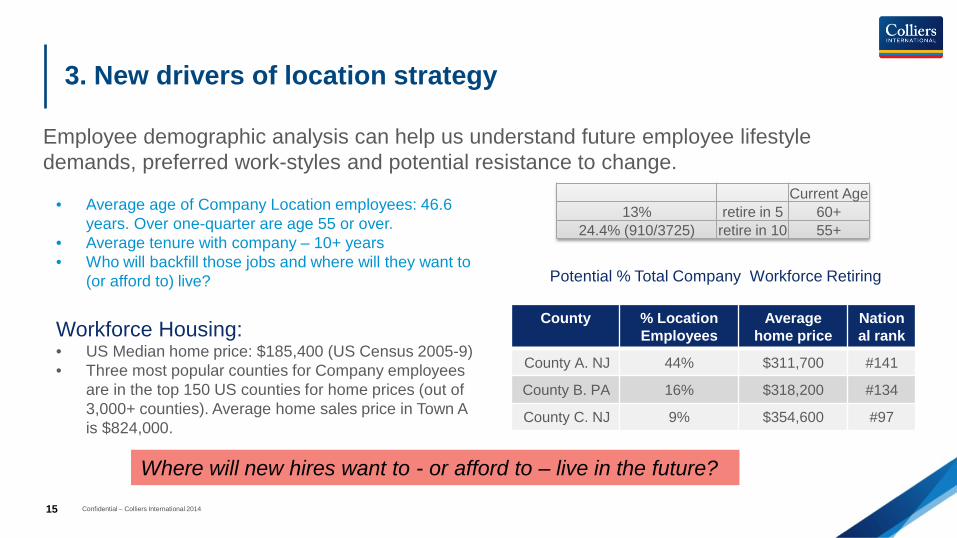

Employee demographic analysis can help us understand future employee lifestyle demands, preferred work-styles and potential resistance to change.

• Average age of Company Location employees: 46.6 years. Over one-quarter are age 55 or over.

• Average tenure with company – 10+ years • Who will backfill those jobs and where will they want to

(or afford to) live? Workforce Housing: • US Median home price: $185,400 (US Census 2005-9) • Three most popular counties for Company employees

are in the top 150 US counties for home prices (out of 3,000+ counties). Average home sales price in Town A is $824,000.

Current Age 13% retire in 5 60+

24.4% (910/3725) retire in 10 55+

County % Location Employees

Average home price

National rank

County A. NJ 44% $311,700 #141

County B. PA 16% $318,200 #134

County C. NJ 9% $354,600 #97

Where will new hires want to - or afford to – live in the future?

Potential % Total Company Workforce Retiring

Increased resistance to commute times

16

15

m i

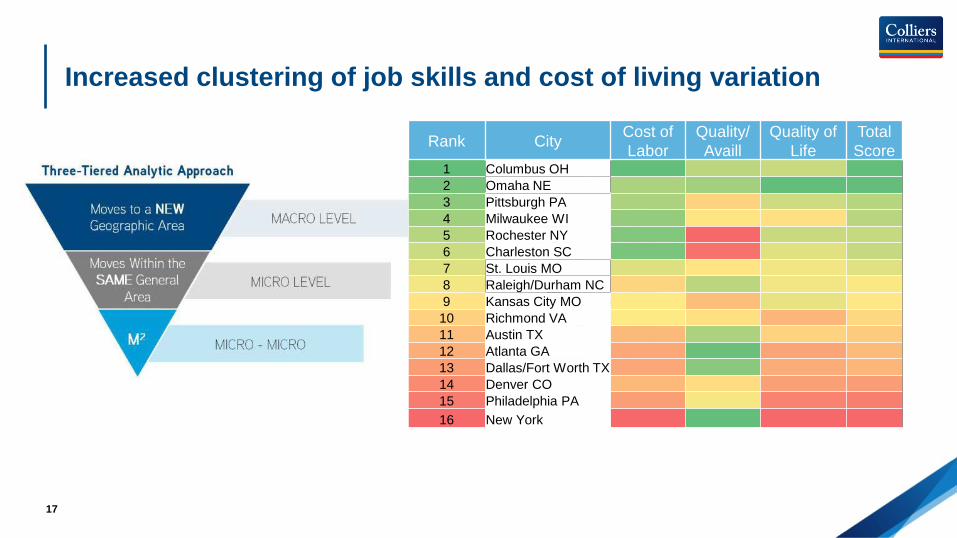

17

Rank City Cost of Labor

Quality/ Availl

Quality of Life

Total Score

1 Columbus OH 2 Omaha NE 3 Pittsburgh PA 4 Milwaukee WI 5 Rochester NY 6 Charleston SC 7 St. Louis MO 8 Raleigh/Durham NC 9 Kansas City MO 10 Richmond VA 11 Austin TX 12 Atlanta GA 13 Dallas/Fort Worth TX 14 Denver CO 15 Philadelphia PA 16 New York

Increased clustering of job skills and cost of living variation

18

“Percentage of total” compares each city’s salary per occupation to the most expensive salary for that occupation

Columbus OH Austin TX

Denver CO Rochester NY

Omaha NE Milwaukee WI Richmond VA St. Louis MO

Charleston SC Raleigh/Durham NC

Atlanta GA Dallas/Fort Worth TX

Pittsburgh PA Philadelphia PA Kansas City MO

New York

Securities…Avg Salary And % of Total

40% 45% 46% 49% 51% 52% 53% 55% 57% 59% 59% 60% 63% 71% 74%

100%

Financial Analysts Avg Salary and % of Total

75% 95% 85% 80% 75% 75% 78% 72% 70% 82% 87% 86% 77% 87% 80%

100%

Management Analysts Avg Salary and % of Total

63% 78% 83% 63% 61% 64% 72% 69% 50% 65% 65% 74% 60% 67% 62%

100%

Systems Software Avg Salary

And % of Total

74% 90% 98% 60% 83% 73% 81% 82% 75% 83%

100% 84% 71% 87% 74% 93%

Source: US BLS

Targeting desired employee skills/salary differentials

Confidential – Colliers International 2014

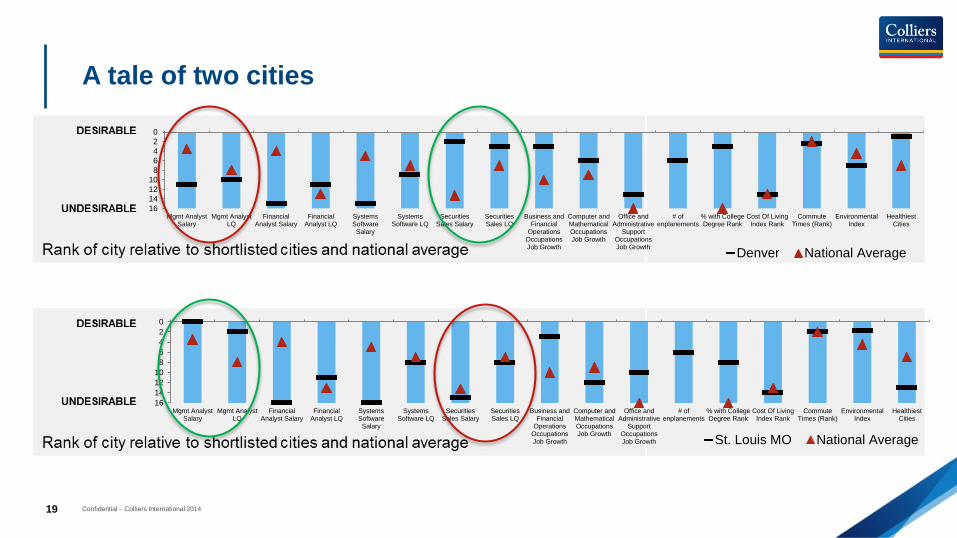

A tale of two cities

19

02468

10121416

Mgmt AnalystSalary

Mgmt AnalystLQ

FinancialAnalyst Salary

FinancialAnalyst LQ

SystemsSoftwareSalary

SystemsSoftware LQ

SecuritiesSales Salary

SecuritiesSales LQ

Business andFinancial

OperationsOccupationsJob Growth

Computer andMathematicalOccupationsJob Growth

Office andAdministrative

SupportOccupationsJob Growth

# ofenplanements

% with CollegeDegree Rank

Cost Of LivingIndex Rank

CommuteTimes (Rank)

EnvironmentalIndex

HealthiestCities

St. Louis MO National Average

02468

10121416

Mgmt AnalystSalary

Mgmt AnalystLQ

FinancialAnalyst Salary

FinancialAnalyst LQ

SystemsSoftwareSalary

SystemsSoftware LQ

SecuritiesSales Salary

SecuritiesSales LQ

Business andFinancial

OperationsOccupationsJob Growth

Computer andMathematicalOccupationsJob Growth

Office andAdministrative

SupportOccupationsJob Growth

# ofenplanements

% with CollegeDegree Rank

Cost Of LivingIndex Rank

CommuteTimes (Rank)

EnvironmentalIndex

HealthiestCities

Denver National Average

Confidential – Colliers International 2014

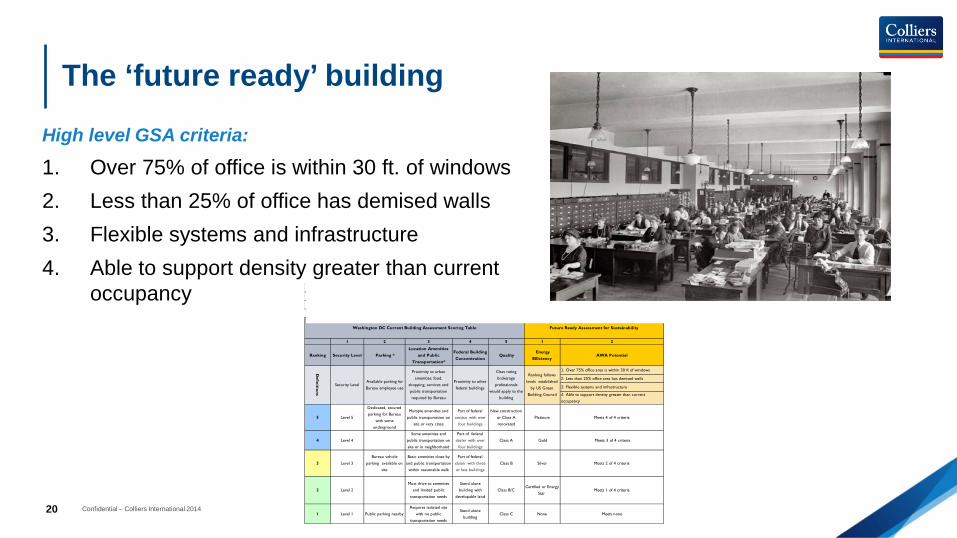

The ‘future ready’ building

20

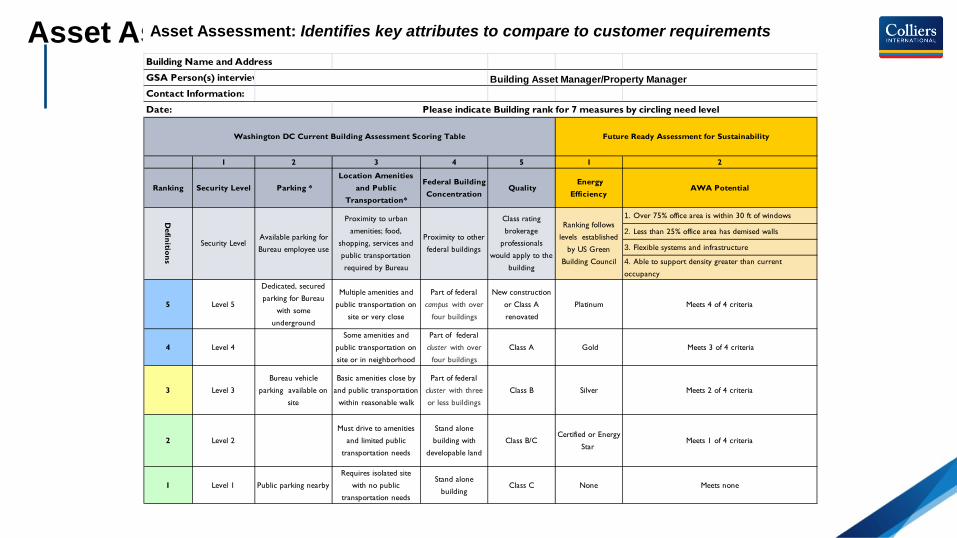

Building Name and Address

GSA Person(s) interview Building Asset Manager/Property ManagerContact Information:

Date: Please indicate Building rank for 7 measures by circling need level

1 2 3 4 5 1 2

Ranking Security Level Parking * Location Amenities

and Public Transportation*

Federal Building Concentration

Quality Energy

EfficiencyAWA Potential

1. Over 75% office area is within 30 ft of windows

2. Less than 25% office area has demised walls

3. Flexible systems and infrastructure

4. Able to support density greater than current

occupancy

5 Level 5

Dedicated, secured

parking for Bureau

with some

underground

Multiple amenities and

public transportation on

site or very close

Part of federal

campus with over

four buildings

New construction

or Class A

renovated

Platinum Meets 4 of 4 criteria

4 Level 4

Some amenities and

public transportation on

site or in neighborhood

Part of federal

cluster with over

four buildings

Class A Gold Meets 3 of 4 criteria

3 Level 3

Bureau vehicle

parking available on

site

Basic amenities close by

and public transportation

within reasonable walk

Part of federal

cluster with three

or less buildings

Class B Silver Meets 2 of 4 criteria

2 Level 2

Must drive to amenities

and limited public

transportation needs

Stand alone

building with

developable land

Class B/CCertified or Energy

Star Meets 1 of 4 criteria

1 Level 1 Public parking nearby

Requires isolated site

with no public

transportation needs

Stand alone

buildingClass C None Meets none

Definitions

Security LevelAvailable parking for

Bureau employee use

Proximity to urban

amenities; food,

shopping, services and

public transportation

required by Bureau

Proximity to other

federal buildings

Class rating

brokerage

professionals

would apply to the

building

Ranking follows

levels established

by US Green

Building Council

Washington DC Current Building Assessment Scoring Table Future Ready Assessment for Sustainability

High level GSA criteria:

1. Over 75% of office is within 30 ft. of windows 2. Less than 25% of office has demised walls 3. Flexible systems and infrastructure 4. Able to support density greater than current

occupancy

“All Roads Lead to Rome” – getting to 150 usf/fte

Lower Cost / Change Higher Cost / More Change

Workplace Design Change

Work Style Change

21

Increase utilization with current furnishings by “Sharing” 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 1 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2

1 1 1 1 1 1 1 1 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2

1 1 1 1 1 1 1 1 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2

1 1 1 1 1 1 1 1 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2

1 1 1 1 1 1 1 1 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2

1 1 1 1 1 1 1 2 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2

1 1 1 1 1 1 1 2 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2

1 1 1 1 1 1 1 2 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2

1 1 1 1 1 1 1 2 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2

1 1 1 1 1 1 1 2 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2

1 1 1 1 1 1 1 1 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 6 6 6 6 6 6 6 3

1 1 1 1 1 1 1 1 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 1 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 6 6 6 6 6 6 6 3

1 1 1 1 1 1 1 1 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 1 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 6 6 6 6 6 6 6 3

1 1 1 1 1 1 1 2 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 2 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 6 6 6 6 6 6 6 3

1 1 1 1 1 1 1 2 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 2 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 6 6 6 6 6 6 6 3

1 1 1 1 1 1 1 2 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 2 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2

1 1 1 1 1 1 1 2 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2

1 1 1 1 1 1 1 2 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2

1 1 1 1 1 1 1 2 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2

1 1 1 1 1 1 1 2 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2

1 1 1 1 1 1 1 1 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2

1 1 1 1 1 1 1 1 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2

1 1 1 1 1 1 1 1 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2

1 1 1 1 1 1 1 1 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2

1 1 1 1 1 1 1 1 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2

Existing: All Assigned

Seating

Offices Open Plan: Cubes or Benching

Future: 25% Additional

Capacity

All Individually Assigned

50% of Offices 25% of Open Plan

Individually Assigned

70% of Offices 50% of Open

Plan Individually Assigned

70% of Offices 70% of Open

Plan Individually Assigned

2:1

11:10

2:1 6:5

1.5:1

5:4

22

Illustrative purposes only

Ways to increase utilization without a major overhaul Existing Plan – could double capacity

(18-20 offices/wing ~360 sf/person)

Replace file and storage areas with benching

Double up some offices

Confirm staff assigned to every seat

Remove demountable walls where possible

Replace sections of modular cubes with benching

Maximum (70-80 seats/wing ~ 100 usf/person)

People – Some Should Be in the Office Everyday

24

Confidential – Colliers International 2014

Thank you!!

25

Confidential – Colliers International 2014

Workplace Innovation

26

Real Estate Factors Human Resource Factors

Strategic Redeploy capital to core business Greater geographical access to labor markets

Financial Operating cost reduction Cost savings to employees from commuting

Operational Locations based upon use, function

Access to a more diverse workforce through flexible schedules

Individual Work settings that support the way work is done

More personal choice regarding schedule, work-style

Stakeholder Impact Analysis

How will offering high performance workplace strategies help build and maintain competitive advantage? What is good for the business?

People: Parents, Professionals and Potentates

27 Office images courtesy of Margulies Perruzzi Architects

Mobility Metrics by Industy

IndustryPerson per Seat

Target

Seat Per Person

Target

Insurance Firm 0.71 1.4:1

Pharmaceutical Firm 0.83 1.2:1

Financial Firm (IT & Support) 0.83 1.2:1

Public Accounting 0.17 - 0.10 6:1 - 10:1

Source: Workplace Mobility’, Corporate Real Estate Journal, November 2010. Underlying research performed by Christine Barber and Andrew Garner-Wortzel of Gensler and Trex Morris of Ernst & Young.

Confidential – Colliers International 2014

1. No more “butts in boxes”. Ever. 2. Most everyone’s life runs better if they can work from home one day a week. 3. If you don’t have to go to the office, what is going to make you want to go to the office? 4. Organizational structures and managerial practices seriously lag the revolution in mobile work. From corporate real estate strategy to

PLACE STRATEGY™

“Organizing your company in space and time, utilizing human talent and technology to its highest potential.”

28

Confidential – Colliers International 2014 29

http://www.imdb.com/title/tt0151804/trailers

Building Name and Address

GSA Person(s) interview Building Asset Manager/Property ManagerContact Information:

Date: Please indicate Building rank for 7 measures by circling need level

1 2 3 4 5 1 2

Ranking Security Level Parking * Location Amenities

and Public Transportation*

Federal Building Concentration

Quality Energy

EfficiencyAWA Potential

1. Over 75% office area is within 30 ft of windows

2. Less than 25% office area has demised walls

3. Flexible systems and infrastructure

4. Able to support density greater than current

occupancy

5 Level 5

Dedicated, secured

parking for Bureau

with some

underground

Multiple amenities and

public transportation on

site or very close

Part of federal

campus with over

four buildings

New construction

or Class A

renovated

Platinum Meets 4 of 4 criteria

4 Level 4

Some amenities and

public transportation on

site or in neighborhood

Part of federal

cluster with over

four buildings

Class A Gold Meets 3 of 4 criteria

3 Level 3

Bureau vehicle

parking available on

site

Basic amenities close by

and public transportation

within reasonable walk

Part of federal

cluster with three

or less buildings

Class B Silver Meets 2 of 4 criteria

2 Level 2

Must drive to amenities

and limited public

transportation needs

Stand alone

building with

developable land

Class B/CCertified or Energy

Star Meets 1 of 4 criteria

1 Level 1 Public parking nearby

Requires isolated site

with no public

transportation needs

Stand alone

buildingClass C None Meets none

Definitions

Security LevelAvailable parking for

Bureau employee use

Proximity to urban

amenities; food,

shopping, services and

public transportation

required by Bureau

Proximity to other

federal buildings

Class rating

brokerage

professionals

would apply to the

building

Ranking follows

levels established

by US Green

Building Council

Washington DC Current Building Assessment Scoring Table Future Ready Assessment for Sustainability

Asset Assessment Worksheet Asset Assessment: Identifies key attributes to compare to customer requirements