the greening of the federal tax code renewable energy tax credits

TRANSCRIPT

The Greening of the The Greening of the Federal Tax CodeFederal Tax CodeRenewable Energy Tax CreditsRenewable Energy Tax Credits

Presented By:Presented By:

Nate SmithsonNate SmithsonJackson Walker L.L.P.Jackson Walker L.L.P.

901 Main Street901 Main StreetSuite 6000Suite 6000

Dallas, Texas 75202Dallas, Texas 75202(214) 953-5641(214) 953-5641

[email protected]@jw.com

©© December 5, 2011 December 5, 2011

This presentation represents only a summary of the applicable This presentation represents only a summary of the applicable provisions with respect to renewable energy tax credits and related provisions with respect to renewable energy tax credits and related matters set forth in the Internal Revenue Code of 1986, as amended matters set forth in the Internal Revenue Code of 1986, as amended from time to time (the “from time to time (the “CodeCode”), revenue rulings and administrative ”), revenue rulings and administrative interpretations (all as currently in effect and all of which are subject to interpretations (all as currently in effect and all of which are subject to change, possibly with retroactive effect). change, possibly with retroactive effect).

This presentation does not constitute tax, legal or other advice from This presentation does not constitute tax, legal or other advice from Nathan Smithson or Jackson Walker L.L.P., and neither assumes any Nathan Smithson or Jackson Walker L.L.P., and neither assumes any responsibility with respect to assessing or advising the reader as to tax, responsibility with respect to assessing or advising the reader as to tax, legal or other consequences arising from the reader’s use of the legal or other consequences arising from the reader’s use of the information. information.

This presentation is not intended or written to be used, and may not be This presentation is not intended or written to be used, and may not be relied upon, by any person for the purpose of avoiding penalties that relied upon, by any person for the purpose of avoiding penalties that may be imposed under any federal tax law or otherwise. may be imposed under any federal tax law or otherwise.

The Push for RenewablesThe Push for Renewables

• Federal Government:– The Carrot: Tax Credits for investment and

production– The Stick: EPA limits on pollutants

• Local Governments:– Renewable Energy Standards across all

states that provide fungible, valuable energy credits.

Personal ChoicesPersonal Choices

• More people looking to reduce their carbon footprint (i.e., global warming fears)

• Reduce dependency on foreign resources.

Wind Farm ScenarioWind Farm Scenario

Why a Wind Farm?Why a Wind Farm?

• Many opportunities in west Texas and the panhandle.

• Can build and co-exist on land currently used for ranches, among other things– Benefit for the land owner

• Relatively quick to set up – purchase to generation within a few months

Wind Farm FactsWind Farm Facts

• Over 35,000 electricity producing wind turbines in the world

• 800 wind farms within the US for a total of 43,000 Megawatts of capacity (3.25% of US total energy capacity)

• Texas has the most wind farms of any state, with a total capacity of over 10,000 Megawatts -- Enough to power:– 100,000 100w light bulbs

Current Drawbacks to Wind PowerCurrent Drawbacks to Wind Power

• Efficiency: Wind has to be blowing over 20mph to cause a 2 MW wind turbine to generate 2MW of electricity– Efficiency of 30% is pretty good

• Timing: Wind is at its highest at night, and due to lack of storage for the wind, its peak comes when most homes do not need it.

Drawbacks cont’dDrawbacks cont’d

• Transmission: As wind farms are generally located in more remote areas, the ability to get the electricity to the hubs in hampered:– Dearth of transmission capacity currently;– Loss of strength in transmission.

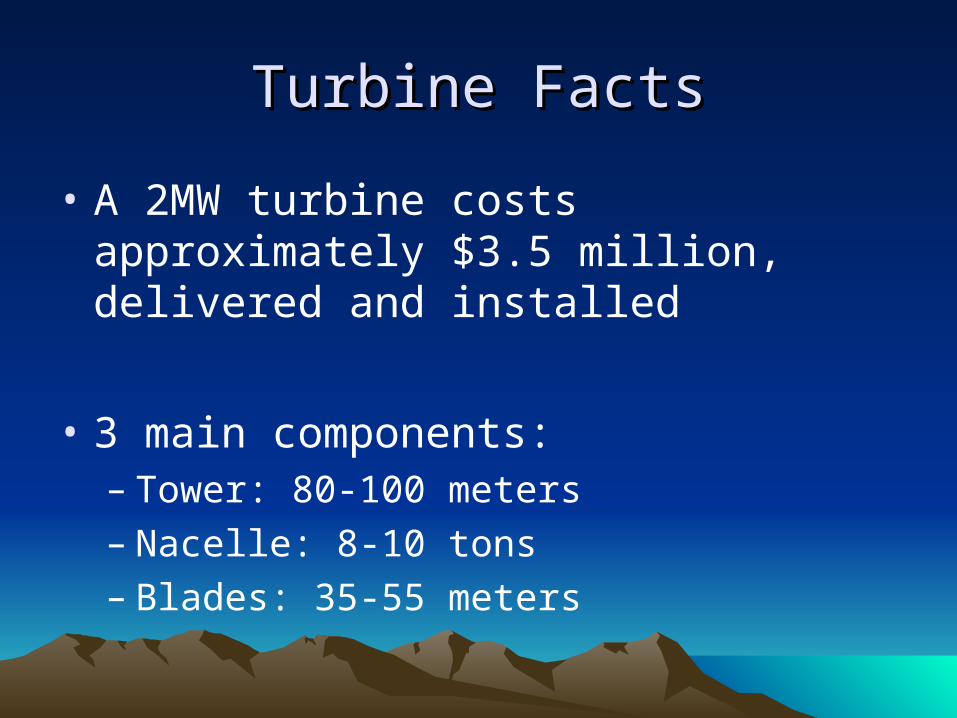

Turbine FactsTurbine Facts

• A 2MW turbine costs approximately $3.5 million, delivered and installed

• 3 main components:– Tower: 80-100 meters– Nacelle: 8-10 tons – Blades: 35-55 meters

Our Wind FarmOur Wind Farm

The “Dallas Bar Wind Farm”The “Dallas Bar Wind Farm”

Dallas Bar Wind FarmDallas Bar Wind Farm

• 10 2MW Wind Turbines located on a farm in west Texas.

Total cost: $35 million

Estimated start of construction: December 15, 2011

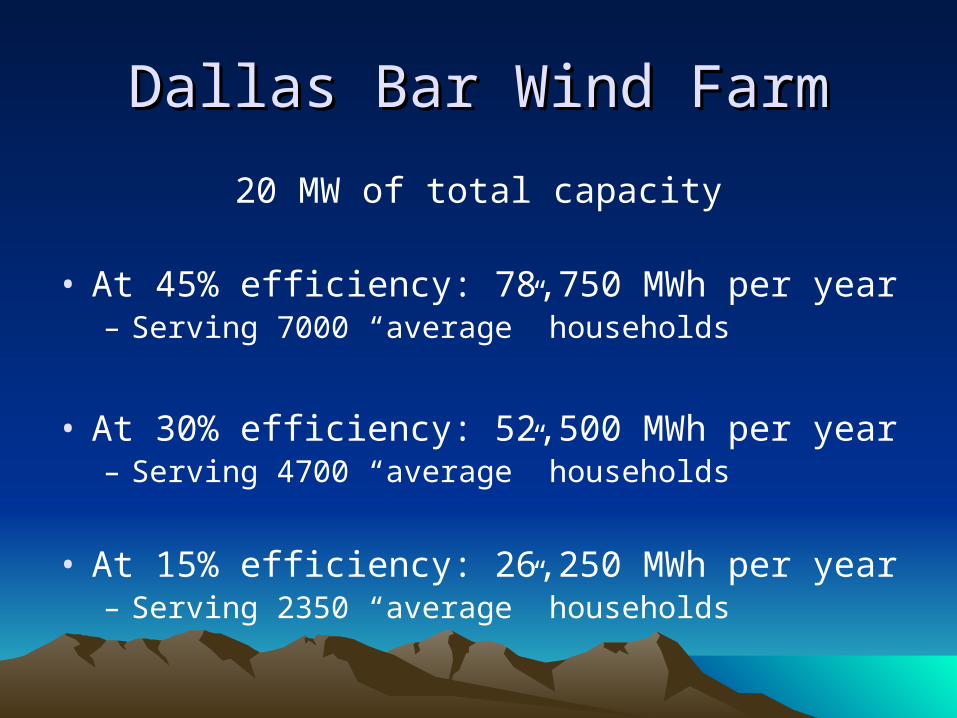

Dallas Bar Wind FarmDallas Bar Wind Farm

20 MW of total capacity

• At 45% efficiency: 78,750 MWh per year– Serving 7000 “average” households

• At 30% efficiency: 52,500 MWh per year– Serving 4700 “average” households

• At 15% efficiency: 26,250 MWh per year– Serving 2350 “average” households

Federal Tax OpportunitiesFederal Tax Opportunities

• Production Tax Credit

• Investment Tax Credit

• Section 1603 Cash Grant

• Accelerated Depreciation

Production Tax CreditProduction Tax Credit

PTCPTC = = 2.17¢ * kWh produced 2.17¢ * kWh produced from Qualified Energy from Qualified Energy

Resources at a Qualified Resources at a Qualified FacilityFacility

Production Tax CreditProduction Tax Credit

• Available over the 10 year period starting on the date the Qualified Facility was originally placed in service.

• Electricity must be sold to an unrelated person.

• Electricity must be produced in the US or a US possession.

““Sold to an Unrelated Person”Sold to an Unrelated Person”

• Where electricity is ultimately sold to an unrelated person, an intermediate sale of the electricity to a related person for resale will still qualify for the Production Tax Credit. – OK to sell to a partner in a partnership that

ultimately resells this on the market

Qualified Energy ResourcesQualified Energy Resources

• Wind, solar energy, geothermal energy, hydropower production, etc...

– See Appendix A to the outline for a description of the type of facilities associated with these resources.

Qualified FacilityQualified Facility

• Facilities producing electricity from qualified energy resources– more specifically set forth in Code section 45(d) (and Exhibit A)

• A wind facility placed in service after December 31, 1993 and before January 1, 2013 constitutes a qualified facility– Placed in service = placed in a condition or state of readiness

and available to produce electricity– Note – extended through 2012 by the American Recovery and

Reinvestment Act of 2009 (the “ARRA”)

DBA Wind FarmDBA Wind Farm

30% Efficiency = 52,500 MWh

• Results in a credit of:– $1.14 million annually, or – $11.4 million over the 10 year PTC period.

• Approximately 33% of the total cost is returned

• Estimated Present Value: $8.8 million– 25% return on investment

DBA Wind FarmDBA Wind Farm

45% Efficiency = 78,750 MWh– “Rock Star”– $1.7 million annual credit – Estimated Present Value: $13.2 million

15% Efficiency = 26,250 MWh– “Basement Band”– $570,400 annual credit– Estimated Present Value: $4.4 million

Investment Tax CreditInvestment Tax Credit

ITC = Energy Percentage * ITC = Energy Percentage * Basis of Energy Property Placed in Basis of Energy Property Placed in

ServiceService

Energy PercentageEnergy Percentage

Either:

– 30% for certain enumerated property; or

– 10% for all other property

30% Property30% Property

• Initially, this was certain limited scope property that was generally not included within the ambit of Code section 45.

• ARRA added the provision: “Qualified Property” that is part of a “Qualified Investment Credit Facility”

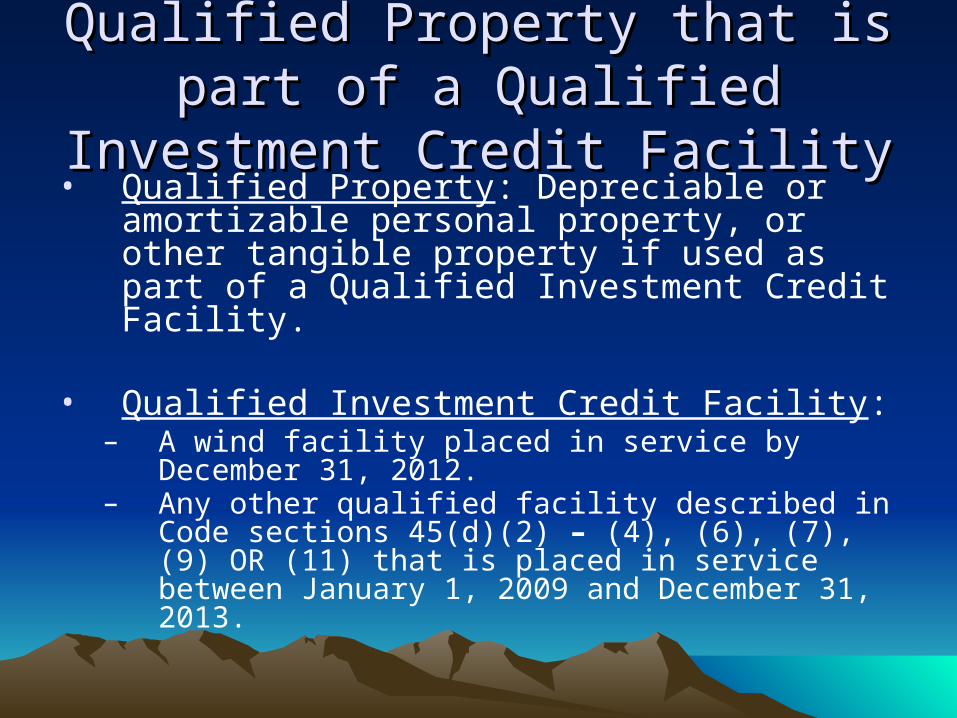

Qualified Property that is part of a Qualified Property that is part of a Qualified Investment Credit FacilityQualified Investment Credit Facility

• Qualified Property: Depreciable or amortizable personal property, or other tangible property if used as part of a Qualified Investment Credit Facility.

• Qualified Investment Credit Facility:– A wind facility placed in service by

December 31, 2012.– Any other qualified facility described in Code

sections 45(d)(2) – (4), (6), (7), (9) OR (11) that is placed in service between January 1, 2009 and December 31, 2013.

Energy PropertyEnergy Property

• Certain energy property described in Code section 48(a)(3); provided that such property:

– Was either constructed and completed by the taxpayer requesting the credit, or acquired by such taxpayer, if the original use of such property commences with such taxpayer;

– Is subject to deprecation or amortization; and– Meets certain performance and quality standards

set forth by the Department of the Treasury; and

• Qualified Property that is part of a Qualified Investment Credit Facility.

BasisBasis

• Only the cost of the property and installation.

• Basis does not include the cost of any property to which it is attached (e.g., cost of the solar panel placed on a building, but not the cost of the building itself).

• Basis of the Energy Property will be reduced by 50% of the Investment Tax Credit allowed.

RecaptureRecapture

• Applies to the ITC, but not the PTC

• The ITC will be recaptured if the Energy Property is sold or ceases to be eligible for the credit

• 100% of the credit is due if the disqualifying event happens within 1 year of placed in service.

– Reduced by 20% per each year thereafter.

– Thus, after the 5th year placed in service, the Recapture Percentage is 0%.

ITC for the DBA Wind FarmITC for the DBA Wind Farm

30% * cost basis of $35 million

=

$10.5 million

Section 1603 Cash GrantSection 1603 Cash GrantGrant = Applicable Percentage * Grant = Applicable Percentage *

Eligible Basis of Specified Energy Eligible Basis of Specified Energy Property Placed in ServiceProperty Placed in Service

Cash Grant HighlightsCash Grant Highlights

• Direct payment of cash to the taxpayer once property is placed in service (within 60 days)

• Not includable within the gross income of the taxpayer

Cash Grant FactsCash Grant Facts

• 22,747 projects funded to date

• $9.6 billion in grants made – At up to 30% of the eligible basis, this reflects $32.9 billion in

total federal and private investments– $1.6 billion in funding in Texas alone for 288 projects

• 14.3 GW of installed capacity resulting from grant funded projects

• 36.8 TWh of estimated electricity generation– 3.3 million “average” homes

Applicable PercentageApplicable Percentage

• Either 30% or 10%, as set forth in Program Guidance from the Department of the Treasury, revised as of April, 2011.

• Generally mirrors the ITC Energy Percentage

Specified Energy PropertySpecified Energy Property

• Certain Qualified Facility Property eligible for the Production Tax Credit; and

• Certain Energy Property eligible for the Investment Tax Credit

– Both are further set forth in Program Guidance from the Department of the Treasury, revised as of April, 2011.

Eligible BasisEligible Basis

• The cost of the Specified Energy Property

– Includes installation and shipping costs.– Also includes roads and parking areas to be

used for the transportation of material for processing or equipment for maintenance and operation of the facility

– Does not include roadways and parking that are provided for employees and visitors.

Non-Eligible BasisNon-Eligible Basis

• Costs that will be deducted in the year in which they are paid or incurred: – Code section 179 deduction. – Election to expense intangible drilling and

development costs.

BasisBasis

• As with the ITC, the basis of Specified Property will be reduced by 50% of the amount of the Cash Grant.

EligibilityEligibility

• Must:– Own and continue to own the eligible property; and– Originally place it in service

• A lessee of property can apply too, provided that: – A valid lease is included in application;– The owner/lessor waives its right to the payment;– Both lessor and lessee are otherwise eligible to receive the

credit; and – Lessee agrees to include ratably in gross income over the five

years an amount equal to 50% of the grant amount.

EligibilityEligibility

• Cannot be an exempt entity, a governmental entity, an energy co-op or a partnership with a such an entity as an owner, unless owned through a blocker.

• OK to have a foreign owner provided that 50% of the gross income of such foreign owner with respect to the project is subject to taxation at the federal level.

EligibilityEligibility

• Original use of the property must start with the applicant.– Less than 20% of the total cost of the facility

can be made up of used parts.– OK to use a sale-leaseback if within 3 months

of original placing in service.

EligibilityEligibility

• Property must be used predominantly in the US.

• Project must have started by 12/31/11

When to ApplyWhen to Apply

• Application Deadline: October 1, 2012– If not placed in service by the application

deadline, then additional information must be submitted within 90 days after being placed in service

– Credit terminates if not placed in service by the credit termination date – January 1, 2013 for wind.

Documentation RequirementsDocumentation Requirements

• Must show that:

– 1) the property is eligible;

– 2) it has been placed in service; and

– 3) the amount is accurate.

DocumentationDocumentation

• Eligibility of the property – design plans stamped by a licensed professional engineer

DocumentationDocumentation

• Placed in Service:– Commissioning report from an engineer,

vendor or qualified 3rd party that equipment works for its intended purpose; and

– an interconnection agreement for facilities interconnected with a utility.

DocumentationDocumentation

• Accuracy – Detailed breakdown of all costs, and an independent accountant’s certification if basis is over $500,000

DocumentationDocumentation

• If the property will be placed in service after December 31, 2011, must demonstrate that “physical work of a significant nature” has begun on or before December 31, 2011

– This is the beginning of construction

Physical Work of a Significant Physical Work of a Significant NatureNature

• Includes work both at the site as well as the prep work with respect to the facility.

• Does not include preliminary activities such as planning or designing, clearing a site, acquiring financing, changing the contour of land.

Physical Work of a Significant Physical Work of a Significant Nature – Wind TurbineNature – Wind Turbine

• Examples for a wind turbine: – On-site: excavation of foundation, setting

anchor bolts or pouring concrete pads.– Off-site: the beginning of the manufacturing of

the component parts of the turbine –

**The component being manufactured must be associated with the applicable facility being constructed.

Physical Work of a Significant Physical Work of a Significant Nature – Work Under ContractNature – Work Under Contract

• Contracted work qualifies if:– Entered into prior to the start of such work;– The contract is binding and enforceable under

state law against the applicant; and – Does not limit damages to a specified amount.

Physical Work of a Significant Physical Work of a Significant Nature – Safe HarborNature – Safe Harbor

• Safe Harbor: Physical work of a significant nature has begun when 5% of the total cost of the property has been paid or incurred.– When constructed by the applicant – when paid or

incurred by the applicant.– When constructed for the applicant under a contract –

the contractor must itself incur such costs to be effective.

• The above costs can be combined.• This requires substantiation.

Physical Work of a Significant Physical Work of a Significant Nature – Multiple UnitsNature – Multiple Units

• An applicant can elect to treat multiple independent units as a single unit for purposes of determining the beginning of construction (e.g., an applicant building a wind farm can treat all turbines as a single unit).

Physical Work of a Significant Physical Work of a Significant Nature – ContinuityNature – Continuity

• Work must be continuous – cannot start work in 2011 to meet the “beginning of work” requirement followed by a long hiatus.– OK to stop because of conditions relating to

the time of year.– Not OK to stop because of lack of

funds/supply.

RecaptureRecapture

• The Cash Grant will be recaptured if the Energy Property ceases to be eligible for the grant.– This differs from the ITC in that a sale of the property

will not necessarily cause a recapture event.

• Similar to the ITC, 100% of the grant amount is due if the disqualifying event happens within 1 year of placed in service, reduced by 20% per each year thereafter.

DBA Wind Farm Cash GrantDBA Wind Farm Cash Grant

30% * cost basis of $35 million

=

$10.5 million

Adjustments to BasisAdjustments to Basis

BasisBasis

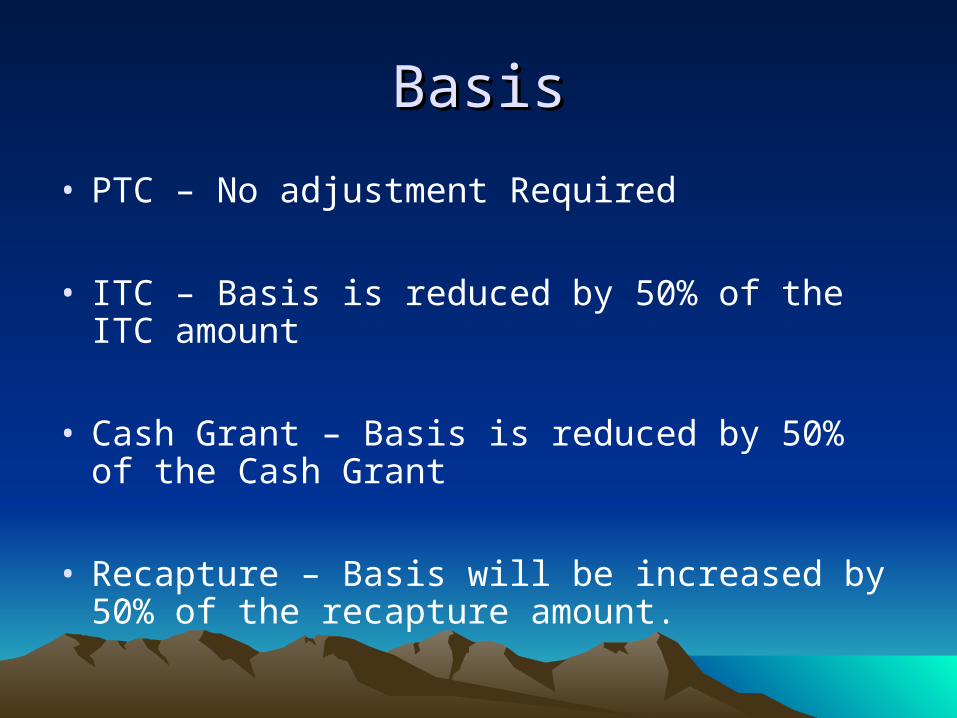

• PTC – No adjustment Required

• ITC – Basis is reduced by 50% of the ITC amount

• Cash Grant – Basis is reduced by 50% of the Cash Grant

• Recapture – Basis will be increased by 50% of the recapture amount.

Bonus DepreciationBonus Depreciation

Bonus DepreciationBonus Depreciation

• Code section 168(k) – deduction of 50% of the adjusted basis of property in the first year qualified property is placed in service after December 31, 2007 and before January 1, 2013.*** 100% if placed in service before January 1, 2012***– relates to the original use of property

• Qualified property includes property that has a recovery period of 20 years or less.– Both solar and wind energy property are treated as “5

year property” for purposes of Code section 168.

Bonus DepreciationBonus Depreciation

• The lessor of property may also use bonus depreciation if:– If all of the 168(k) requirements are otherwise

met; and – The property is sold and leased back within a

3 month period of being placed in service.

DBA Wind Farm Bonus DBA Wind Farm Bonus DepreciationDepreciation

(assume placed in service in 2012)

• If using the PTC:$35 million depreciable basis * 50% =

$17.5 million depreciable currently

• If using the ITC or Cash Grant:$29.75 million depreciable basis (reduced by $5.25

million required adjustment) * 50% =

$15 million depreciable currently

Summary of Federal Benefits Summary of Federal Benefits for DBA Wind Farmfor DBA Wind Farm

DBA Wind Farm SummaryDBA Wind Farm Summary

• If efficiency is 30% and the PTC is used:– Annual Credit of $1.14 million for 10 years (Present

Value: $8.8 million)– 2011 Accelerated Depreciation: $17.5 million * 35% =

$6,125,000– 2011 benefit = $7.2 million

• If efficiency is 45%, 2011 benefit = $7.8 million• If efficiency is 15%, 2011 benefit = $6.7 million

DBA Wind Farm SummaryDBA Wind Farm Summary

• If the ITC or Cash Grant is used:– Credit/Grant of $10.5 million– 2011 Accelerated Depreciation: $15 million *

35% = $5,250,000– 2011 benefit = $15.75 million

Financing OpportunitiesFinancing Opportunities

Solo FinancingSolo Financing

• The Cash Grant program provides direct funding to a developer

– Reduces the ultimate amount of financing necessary to develop a project.

DBA Wind Farm Solo FinancingDBA Wind Farm Solo Financing

• Our initial outlay of $35 million is really a $24.5 million outlay following the receipt of cash.

– The $5.25 million accelerated depreciation deduction doesn’t do much good:

• we don’t yet have the income to be offset by the deduction.

Flip PartnershipFlip Partnership

Flip PartnershipFlip Partnership

• By bringing in investor partners, the developer of a project has the opportunity to pass through to the investors certain of the currently recognizable benefits.

Flip PartnershipFlip Partnership

• General Structure:– Investor puts in money;– Developer puts in know-how and some capital;– Allocations:

• 99-1 between investor and developer so that investor receives the credits, along with income items;

– Distributions:• First to developer until it receives its return;• Then to investor until it receives the negotiated return –

taking in to consideration the allocation of credits;• Then flip to developer – possibly with purchase right

Flip Partnership – Safe HarborFlip Partnership – Safe Harbor

• Treasury has established, under Notice 2007-65, a safe harbor for “wind farm” partnerships, so that if the terms of the safe harbor are met, the IRS will respect the allocation of Production Tax Credits.

Safe Harbor RequirementsSafe Harbor Requirements

• 1) Partnership must own the applicable wind property;

• 2) Developer must have at least 1% interest in partnership income, gain, loss, deduction, and credit at all times;

• 3) Each investor must have minimum interest in each material item of income and gain equal to 5% of such investor’s percentage interest in partnership income.

Safe Harbor RequirementsSafe Harbor Requirements

• 4) Each investor must maintain a minimum investment in the partnership of 20% of its capital requirements. – Can be reduced by cash flow distributions.– Such amount must not be protected against loss.

• 5) Any purchase right with respect to the partnership property must:– Be either:

• The fair market value of the property determined at the time of exercise; or

• If the purchase price is determined prior to exercise, the estimated fair market value of the property at the time the right may be exercised.

– Not be exercisable by the developer earlier than 5 years after the facility is first placed in service.

Safe Harbor RequirementsSafe Harbor Requirements

• No investor may have a “put” right with respect to its partnership interest, and the partnership may not have a “put” right with respect to the partnership property.

• Each partner must fully bear the risk of the investment in the property (no guarantees)

Sale-LeasebackSale-Leaseback

Sale-LeasebackSale-Leaseback

• Typical Steps:– Developer builds and places the applicable

property in service;– Developer sells the property to an investor;– Investor leases the property back to

developer in a “true lease;”– Investor avails itself of a Credit or the Cash

Grant and the accelerated depreciation.

TimingTiming

• Investor must acquire the applicable property within 3 months of it being placed in service in order to receive the Credit or Cash Grant.

““True Lease”True Lease”

• Treasury guidance: Revenue Procedure 2001-28

• 1) The lessor must have made a minimum unconditional “at risk” investment in the property at the outset and such minimum investment must remain throughout the entire lease term until the end.

– Minimum investment -- at least 20% of the cost of the property

– Must be unconditional (i.e., lessor must not be entitled to a return of any portion of the minimum investment from lessee).

True LeaseTrue Lease

• 2) The lease term (including all renewals or extensions) must be at fair rental value (determined at the time of such renewal or extension).

• 3) Lessee cannot have a contractual right to purchase the property at a price less than its fair market value, determined at the time the right is exercised.

True LeaseTrue Lease

• 4) Lessor may not have a “put” right with respect to the property (when placed in service).

• 5) Lessee cannot make nonseverable improvements.

• 6) Lessee may not loan money to lessor with respect to the property, or guarantee any loans with respect thereto.

True LeaseTrue Lease

• 7) Lessor expects to make a profit on the ownership and lease of the property, which profit shall not take in to consideration any tax benefits.

• 8) The lease period must be less than the entire useful life of the property.

Flip Partnerships v. Sale-Flip Partnerships v. Sale-LeasebacksLeasebacks

• Sale-leaseback does not work for PTCs as they can only be claimed by an owner and operator of the facility;

• Lessor can receive 100% of the tax benefits, whereas in a partnership, the developer would be required to have at least a 1% interest therein;

• Sale-leasebacks with ITC and accelerated depreciation generate upfront tax benefits to an equity investor and do not directly depend on productivity of the facility or demand for the energy.

Flip Partnership v. Sale LeasebackFlip Partnership v. Sale Leaseback

• Easier for the developer to benefit in a flip partnerships following the full realization of the credits (can end up with a 95% interest post-flip);

• Fair market value of the property upon a developer buyout must be determined at the time of exercise in a sale-leasebacks, instead of pre-determined based on estimates in a flip partnership;

• Investor need not participate in the operations of the project in a sale-leasebacks.

• Investor doesn’t need a profit motive in a flip-partnership.

Inverted LeaseInverted Lease

Inverted LeaseInverted Lease

• Developer leases the applicable property to an investor, who sells the electricity generated therefrom.

• Developer may pass through the Investment Tax Credit or the Cash Grant, subject to a valid election, provided:– the investor is eligible to receive such benefit; and – in the case of the Cash Grant, the investor agrees to

return 50% of the amount of the grant over the recapture period.

Inverted LeaseInverted Lease

• Developer would receive rent and be able to take depreciation deductions.

• At the end of the lease term the developer owns the property.

Texas Specific ImpactTexas Specific Impact

Texas Specific ImpactTexas Specific Impact

• Texas’ grid:– Isolated – ERCOT relies almost entirely on internal

resources to serve its load and reserves. – A report from the North American Electric Reliability

Corporation suggests that Texas may not have the electrical reserves to meet peak demand by 2013.

• New environmental regulations will result in the mothballing of generating units, and added to the current drought, the power supply in the next year may soon fall short of ERCOT’s minimum target.

Texas Specific ImpactTexas Specific Impact

• Texas Renewable Portfolio Standard - enacted in 1999

– The program required electricity providers collectively generate 2,000 megawatts (MW) of additional renewable energy by 2009 (met in 6 years).

– The 2005 Texas Legislature increased the state's total renewable-energy mandate to 5,880 MW by 2015 (500 of which must not be from wind) (also surpassed) and a target of 10,000 MW in 2025.

Renewable Portfolio StandardRenewable Portfolio Standard

Each provider is required to obtain new renewable energy capacity based on their market share of energy sales times the renewable capacity goal.

Example: a retailer with 10 percent of the Texas retail electricity sales in 2011 would be required to obtain 200 megawatts of renewable energy capacity

Renewable Energy CreditsRenewable Energy Credits

• One REC represents one megawatt-hour of qualified renewable energy that is generated and metered in Texas.

– No requirement to actually take delivery – highlights the transmission problem out in west Texas

• The REC trading system created great flexibility in the development of renewable energy projects.

Competitive Renewable Energy Competitive Renewable Energy ZonesZones

• Public Utility Commission has been assigned almost $5 billion of CREZ transmission projects to be constructed by 7 transmission and distribution utilities (such as Oncor)

• Intended to transmit almost 18,500 MW of wind power from west Texas and the panhandle to the highly populated areas

• Currently working, but much is not expected to be completed until 2013