the hidden cost of federal tax policy - mercatus … · the hidden cost of federal tax policy / by...

TRANSCRIPT

The Hidden Cost of

Federal Tax Policy

JASON J. FICHTNER & JACOB M. FELDMAN

Arlington, Virginia

ABOUT THE MERCATUS CENTER AT GEORGE MASON UNIVERSITYThe Mercatus Center at George Mason University is the world’s premier university source for market- oriented ideas— bridging the gap between academic ideas and real- world problems.

A university- based research center, Mercatus advances knowledge about how markets work to improve people’s lives by training graduate students, conducting research, and applying economics to offer solutions to society’s most pressing problems.

Our mission is to generate knowledge and understanding of the institu-tions that affect the freedom to prosper and to find sustainable solutions that overcome the barriers preventing individuals from living free, prosperous, and peaceful lives.

Founded in 1980, the Mercatus Center is located on George Mason University’s Arlington campus.

Mercatus Center at George Mason University3434 Washington Blvd., 4th FloorArlington, Virginia 22201www . mercatus . org

© 2015 Jason J. Fichtner, Jacob M. Feldman, and the Mercatus Center at George Mason University

All rights reserved.

Printed in the United States of America

Library of Congress Cataloging- in- Publication Data

Fichtner, Jason J. The hidden cost of federal tax policy / by Jason J. Fichtner and Jacob M. Feldman. — 1 Edition. pages cm Includes index. ISBN 978-1-942951-10-0 (pbk.) — ISBN 978-1-942951-11-7 (kindle ebook)

1. Fiscal policy— United States. 2. Taxation— United States. I. Feldman, Jacob M. II. Title. HJ257.3.F58 2015 336.200973— dc23

2015009193

CONTENTS

Introduction. What Are the Goals

of Tax Policy? 1

Chapter 1. What Are the Hidden

Costs of Tax Compliance? 7

Chapter 2. What Can Be Learned from

the Tax Reform Act of 1986? 33

Chapter 3. Why Should Congress Restructure

the Corporate Income Tax? 63

Chapter 4. Why Do Workers Bear a Significant

Share of the Corporate Income Tax? 81

Chapter 5. How Does the Corporate Tax Code

Distort Capital Investments? 101

Chapter 6. Why Should Congress Reform

the Mortgage Interest Deduction? 127

Chapter 7. How Do People Respond to

the Marriage Tax Penalty? 161

Conclusion. Key Principles for Successful,

Sustainable Tax Reform 179

Appendix. Effective Tax Rates by Industry 183

Notes 195

About the Authors 231

161

Politicians often stress that marriage is a key institution that promotes strong family values. However, some aspects of the federal tax code

do not promote marriage. Because of the structure of joint income tax filing, many couples face significant tax disincentives to marriage. The United States is one of only seven countries in the Organisation for Economic Co- operation and Development that uses joint taxation for married couples.1 This chapter uses the term marriage tax penalty to refer to the disad-vantageous tax treatment of a married couple’s joint income relative to two individuals earning an equiva-lent income but choosing cohabitation over marriage.2 Economists Daniel Feenberg and Harvey Rosen note that for some low- income couples in 1990, “The size of the marriage tax is now quite extraordinary, amount-ing to over 18 percent of total income.”3 Many of the issues surrounding the marriage tax penalty remain unchanged. Given the generally more elastic labor supply of married women, the marriage tax penalty may give married women in all income ranges incen-tive not to work outside the home.4 In 1942, feminist activist Florence Guy Seabury sent a letter to the New

CHAPTER 7

How Do People Respond to the Marriage

Tax Penalty?

162 T H E H I D D E N CO S T O F F E D E R A L TA X P O L I C Y

York Times regarding a proposal at that time for joint income taxation in which she wrote:

To those who know the long struggle of women in this country to own property, to control their earnings, to be guardians of their children, to move out of the subject class, this mea sure is a symbol. It represents the defeat of a major prin-ciple of our way of life.5

Certainly, in 1942, wide disparity existed between male and female labor force participation rates and wages. Today, with increasingly more equivalent wages between men and women and a record number of women working, reducing the marriage tax penalty makes more sense than ever.6

Not all joint filers incur a penalty in the federal tax code, however. Some receive a marriage bonus, which is the advantageous tax treatment of a married couple’s combined income relative to two individual filers earning an equivalent combined income. The mar-riage bonus most commonly occurs with single- earner house holds. The marriage tax penalty most commonly occurs with two- earner house holds. For the couples most burdened by the marriage tax penalty, it acts as a financial disincentive to marriage.7

The penalty is predominantly borne by two groups of two- earner couples: (a) low- income, two- earner house holds filing for the earned income tax credit (EITC) and (b) low- and middle- income, two- earner couples for which the two salaries are roughly equal. The effect of marriage tax penalty is greatest for low-

C H A P T E R 7 163

income house holds that use the EITC,8 the same house holds that would potentially benefit most from the acclaimed social benefits of marriage.9

Where the marriage bonus is present, it discour-ages labor force participation by secondary earners, who are predominantly women. A higher marginal tax rate for a single- earner house hold more strongly depresses the economic return of a potential second-ary earner. On their own and not married, secondary earners could experience an entry marginal tax rate of 10 percent rather than a rate of 25 percent or higher. As a result, economic growth and productivity are lost as a consequence of the filing status requirements applying to married couples. An ideal tax code would be neutral with respect to marriage.

EFFECT OF THE MARRIAGE TAX PENALTY ON EXISTING MARRIAGES

No marriage penalty or tax per se appears in the US tax code. The penalty phenomenon emerges as an economic effect of joint taxation on the combined incomes of two married earners. Williams College economist Sara LaLumia examines the historical effect of joint taxation:

Joint taxation equalizes the marginal tax rates of a husband and wife. Because husbands tended to earn more than wives, the introduction of joint taxation lowered husbands’ marginal tax rates and raised wives’ marginal tax rates, on average.10

164 T H E H I D D E N CO S T O F F E D E R A L TA X P O L I C Y

When most house holds contained only one working spouse, joint taxation did not result in a tax penalty for the majority of married couples. Traditionally, men were the breadwinners, and women raised chil-dren and managed the home. As the proportion of women in the labor force increased dramatically from 1960 to 2000 and as women’s wages rose, the marriage tax penalty became an increasingly common issue for two- earner marriages. Economists Michael Bar and Oksana Leukhina write about the rise in female labor force participation during the 40 years from 1960 to 2000: “The proportion of two- earner couples among married couples of working age in the U.S. rose from 34% to 77%.”11 With the increased number of two- earner married couples, the existing tax code plays a prominent role in discouraging earned income by a secondary earner because the secondary earner’s first dollar is often taxed at a higher rate. The marginal tax rates are then significantly distorted by factors such as the EITC, the tax code’s treatment of the earned income difference for a two- earner married couple, and family size.

Low- income couples in the joint income salary range of $30,000 to $50,000 face particularly strong tax disincentives to marriage.12 As a percentage of income, the marriage penalty is highest for couples in that income range because the EITC is phased out for both earners.13 A substantial package of transfer ben-efits for having dependent children can create strong financial incentives for divorce among married joint filers and continued cohabitation among single filers.14

C H A P T E R 7 165

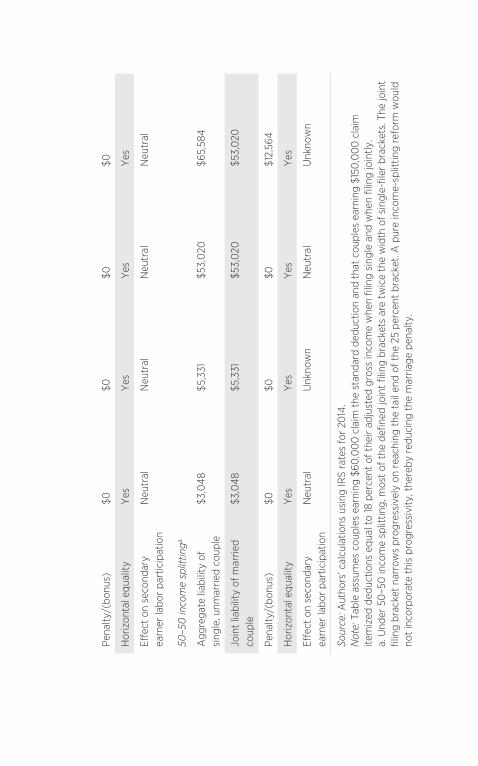

Tax law generates significant horizontal inequali-ties that are based on each earner’s income and how many dependent children a house hold has. Horizontal in e qual ity means identically sized families earning the same amount of income are taxed differently. Joint income filing penalizes marriage when both spouses earn a similar amount of income.15 For example, the tax code subsidizes single- worker house holds earning $60,000 but penalizes two- worker house holds earn-ing the same amount when the income earners are married (see table 7.1).

For those qualifying for the EITC, horizontal in e-qual ity has historically depended on family size, where having one or more dependent children actually penal-izes two- earner married couples. Examining the mar-riage tax penalty over 14 years, economists Nada Eissa and Hilary Hoynes find the following:

Penalized married taxpayers with less than $20,000 earned income face an average marriage penalty of 8 percent of income. . . . [M]arriage tax penalties increase with family size (number of children) among EITC- eligible couples. . . . [A] dual- earning couple with two children faces a sizeable marriage tax penalty of $2,733 (11.4 per-cent of income). A similar childless couple, on the other hand, faces a tax penalty of $210 (1 per-cent of income).16

Benefits can also arise. In a 1995 paper, Feenberg and Rosen find that 52 percent of American families

Table

7.1. E

ffects

of V

ariou

s Pro

posa

ls on

Tax L

iabilit

y of C

ouple

s

50–5

0 E

AR

NIN

GS:

$30

,00

0 A

ND

$30

,00

0

100

–0 E

AR

NIN

GS:

$60

,00

0 A

ND

$0

50-5

0 E

AR

NIN

GS:

$150

,00

0 A

ND

$150

,00

0

100

-0 E

AR

NIN

GS:

$30

0,0

00

AN

D $

0

Cur

rent

law

Agg

rega

te li

abili

ty o

f si

ngle

, unm

arrie

d co

uple

$2,5

24$6

,319

$50

,685

$61,6

49

Join

t lia

bilit

y of

mar

ried

coup

le$3

,048

$3,0

48$5

4,29

8$5

4,29

8

Pena

lty/(

bonu

s)$5

24($

3,24

1)$4

,243

($7,

351)

Hor

izon

tal e

qual

ityN

oN

oN

oN

o

Effec

t on

sec

onda

ry

earn

er la

bor

part

icip

atio

nN

eutr

alN

egat

ive

Neu

tral

Neg

ativ

e

Man

dato

ry s

ingl

e fil

ing

Agg

rega

te li

abili

ty o

f si

ngle

, unm

arrie

d co

uple

$3,0

48$5

,331

$53,

020

$65,

584

Join

t lia

bilit

y of

mar

ried

coup

le$3

,048

$5,3

31$5

3,0

20$6

5,58

4

Pena

lty/(

bonu

s)$0

$0$0

$0

Hor

izon

tal e

qual

ityY

esY

esY

esY

es

Effec

t on

sec

onda

ry

earn

er la

bor

part

icip

atio

nN

eutr

alN

eutr

alN

eutr

alN

eutr

al

50–5

0 in

com

e sp

littin

ga

Agg

rega

te li

abili

ty o

f si

ngle

, unm

arrie

d co

uple

$3,0

48$5

,331

$53,

020

$65,

584

Join

t lia

bilit

y of

mar

ried

coup

le$3

,048

$5,3

31$5

3,0

20$5

3,0

20

Pena

lty/(

bonu

s)$0

$0$0

$12,

564

Hor

izon

tal e

qual

ityY

esY

esY

esY

es

Effec

t on

sec

onda

ry

earn

er la

bor

part

icip

atio

nN

eutr

alU

nkno

wn

Neu

tral

Unk

now

n

Sour

ce: A

utho

rs’ c

alcu

latio

ns u

sing

IRS

rate

s fo

r 20

14.

Not

e: T

able

ass

umes

cou

ples

ear

ning

$60

,00

0 c

laim

the

sta

ndar

d de

duct

ion

and

that

cou

ples

ear

ning

$15

0,0

00

cla

im

item

ized

ded

uctio

ns e

qual

to

18 p

erce

nt o

f the

ir ad

just

ed g

ross

inco

me

whe

n fil

ing

sing

le a

nd w

hen

filin

g jo

intly

.a.

Und

er 5

0–5

0 in

com

e sp

littin

g, m

ost

of t

he d

efine

d jo

int

filin

g br

acke

ts a

re t

wic

e th

e w

idth

of s

ingl

e-fil

er b

rack

ets.

The

join

t fil

ing

brac

ket

narr

ows

prog

ress

ivel

y on

rea

chin

g th

e ta

il en

d of

the

25

perc

ent

brac

ket.

A p

ure

inco

me-

split

ting

refo

rm w

ould

no

t in

corp

orat

e th

is p

rogr

essi

vity

, the

reby

red

ucin

g th

e m

arria

ge p

enal

ty.

168 T H E H I D D E N CO S T O F F E D E R A L TA X P O L I C Y

paid a marriage tax penalty and 38 percent received a marriage tax bonus.17 Today, such inequities still exist and will continue as long as filing on the basis of mari-tal status is required.

MARRIAGE INCENTIVES

Expansions of the EITC under the Tax Reform Act of 1986, the Omnibus Bud get Reconciliation Act of 1990, and the Omnibus Bud get Reconciliation Act of 1993 reduced the marriage tax penalty for low- income cou-ples.18 Eissa and Hoynes find a steady decrease in the penalty from the 1980s into the late 1990s: “Each of three tax acts passed between 1984 and 1997 reduced the marriage tax cost for the poorest families, so that marriage cost was about $450 lower in 1997 compared to 1984.”19 These acts also expanded benefits to single filers. Although these reforms did reduce the federal income tax costs associated with marriage, they did not do so relative to the alternative of cohabitation. As a result, marriage is not a financially neutral choice for many couples. Economists Leslie Whittington and James Alm come to a similar conclusion: “A tax plan that gives larger reductions to single individuals can actually increase the marriage penalty. In short, reducing marriage penalties is not as simple as reduc-ing income taxes.”20

The 2001 and 2003 tax reforms passed under President George W. Bush are illustrative.21 These reforms were intended to reduce the tax penalty asso-ciated with marriage by reintroducing a two- earner deduction of 10 percent on the earnings of a lower-

C H A P T E R 7 169

income spouse, up to an annual income of $30,000.22 The deduction thus allowed a $3,000 maximum subtraction from income subject to federal taxation. In 2003, the White House justified the deduction as follows:

Couples frequently face a higher tax burden after they marry. High marginal tax rates act as a tollgate, limiting the access of low and moderate income earners to the middle class. The current tax code frequently taxes couples more after they get married. This marriage tax contradicts our values and any reasonable sense of fairness.23

Although these reforms decreased the negative tax consequences of marriage, they did not account for the effect on the alternative to marriage: cohabi-tation. Although the marriage tax penalty decreased, the tax benefits of cohabitation increased at a faster rate. Whittington and Alm examine a few scenarios for a couple with $60,000 in annual earnings and find that, “although the Bush tax plan lowers the liabilities of both singles and married couples, the plan lowers taxes more for singles than for married couples.”24 Hence, although they were intended to create income tax incentives that favor married- couple family struc-tures, the reforms actually may encourage greater cohabitation. Whittington and Alm call this “a result that seems counter to the family- oriented image favored by President Bush.”25

On a more positive note, a 2010 study by Hayley Fisher finds that individuals with the least education

170 T H E H I D D E N CO S T O F F E D E R A L TA X P O L I C Y

were four times more responsive to the financial incen-tives of marriage than individuals with the most edu-cation.26 These data suggest that public policies meant to increase the financial benefits of marriage without increasing a single filer’s tax liability might be more successful at promoting marriage than previously thought. Marriage neutrality in the tax code could be successful in promoting marriage among low- income taxpayers.

DIVORCE INCENTIVES

One of the consequences of the implicit marriage tax penalty is that it increases the probability of divorce for certain income ranges. Economist Stacy Dickert- Conlin finds that “most low- income couples are eli-gible for higher welfare benefits if they are separated rather than married.”27 Lower tax liability outside of marriage is positively correlated with the decision to divorce at statistically significant levels.28 Using 1990 data, Dickert- Conlin finds that the marriage tax pen-alty has the strongest effects at the tail ends of income distribution:

The family at the 10th percentile in the distribu-tion of the marriage tax penalty faces a $3,067 marriage tax subsidy. A 50 percent reduction in the subsidy is correlated with a 10.8 percent increase in the probability of separating. . . . At the 90th percentile in the distribution of the marriage tax penalty, the family faces a marriage tax penalty of $1,285.29

C H A P T E R 7 171

Lowering the marriage tax penalty for families in the 90th percentile in the distribution of the penalty by 50 percent would decrease the probability of separa-tion by 4 percent.30 Dickert- Conlin’s results are largely consistent with those of Feenberg and Rosen, who estimate that for a low- income couple the marriage tax penalty combined with the EITC for two depen-dent children would lead to a tax refund of $359 in 1994. If those same taxpayers divorced and each filed under head- of- household status with one child, their combined tax refund would be $4,076.31 In simple terms, the marriage tax penalty is set up such that low- income couples with dependent children have a finan-cial incentive to divorce. As the EITC is phased out with increasing income, a married couple faces higher tax rates, whereas the cohabiting couple does not. As Dickert- Conlin states, “Although marital status, per se, does not affect the EITC, the joint income of a two- earner family may exceed the maximum allowable income for EITC eligibility, but if the couple separates, at least one spouse with sufficiently low income may become eligible.”32

FEMALE LABOR FORCE PARTICIPATION

The tax cuts of 2001 and 2003, enacted during the George W. Bush administration, encouraged increased labor force participation by women by easing the mar-ginal tax rates for a secondary earner. Although the 10 percent deduction on the first $30,000 of income from the second earner is not necessarily the ideal reform to address the horizontal inequities in each

172 T H E H I D D E N CO S T O F F E D E R A L TA X P O L I C Y

tax bracket caused by joint income filing by married couples, the deduction did promote a shift toward more women working. Research by economists Bar and Leukhina confirms that labor force participation by a married woman is more responsive to tax pol-icy changes the higher her husband’s income is. Bar and Leukhina find that, as a result of Reagan- era tax reforms that reduced the marriage tax penalty, there was a 30 percent increase in labor force participation by women whose husbands earned over $84,000.33

By examining the aggregate effect of tax reforms that reduced the marriage tax penalty on two- earner employment, Barry Bosworth and Gary Burtless find that in the 1980s married women’s annual number of hours of paid work increased by 7.1 percent, most significantly among the bottom quintile of income.34 Controlling for demographic trends of higher female salary levels (and higher levels of education), econo-mists Nada Eissa and Hilary Hoynes find that “about 55–60 percent of the change in the marriage tax is due to changing the tax laws.”35

However, in some cases, particularly for low- income married women, the EITC actually decreased female labor force participation (by 2 to 4 percent in the 1970s when the EITC was introduced and by 10 to 12 percent when it was expanded in the 1990s).36 Bar and Leukhina find that, combined with the EITC, “Secondary income is heavily taxed, because it often disqualifies the [married] couple from the credit or reduces it substantially.”37

These data indicate that the filing of joint income tax returns seems to discourage labor force participa-

C H A P T E R 7 173

tion by women across all income levels. A shift in tax policy toward marriage neutrality may increase female labor force participation among low- and high- wage earners alike.

CONCLUSION

As Alm and Whittington state,

In par tic u lar, although the initial decision to cohabit versus marry is only somewhat affected by the tax consequences, the decision to make the transition from cohabitation to marriage is much more significantly affected by taxes. Put differently— and colloquially— the initial deci-sion seems determined more by “passion” than “economics,” but “cold reality” seems more likely to enter the calculus of the transition decision.38

If politicians desire to uphold the prominence of marriage, the federal government should not penal-ize the institution through the tax code. The alterna-tive of cohabitation is commonly chosen in the face of significant financial penalty. Even from a labor force perspective, more equal treatment of a higher- income, two- earner family could have significant implications for macroeconomic growth as labor force participation rates rise. In 1998, the Joint Economic Committee considered three different proposals to alleviate the marriage tax penalty: (a) empowering married couples to select individual filing rather than requiring joint filing, (b) income splitting, and (c) a

174 T H E H I D D E N CO S T O F F E D E R A L TA X P O L I C Y

second- earner deduction.39 The second- earner deduc-tion became law as part of the Economic Growth and Tax Relief Reconciliation Act of 2001. This deduction has reduced the tax penalty for married couples and encouraged female participation in the labor force, but it represents only a Band- Aid solution to tax reform.

Income splitting is a tax reform that maintains joint filing status but adjusts for differences in tax sched-ules between single and joint filers.40 The effect of such a reform would be that nearly all couples would see a reduced marriage penalty or an increased mar-riage bonus. Generally, under 50–50 income split-ting, the joint income deduction is twice the single deduction, and the width of the joint filing bracket is calculated by doubling single- filer tax brackets. For single- earner joint filers, the marriage bonus would generally increase, whereas any existing marriage penalty would be decreased (or bonus increased) for two- earner joint filers. Income splitting could either encourage or discourage women’s labor force partici-pation rates. To the extent that income splitting would result in a lower tax rate for secondary earners in a couple, it could encourage labor force participation. Although the marginal unit of additional income may be taxed at a lower rate for secondary earners, income splitting reduces the marginal rate for the primary earner. Therefore, this reform may encourage longer hours of work for one spouse rather than entry into the labor market by the other. Although income split-ting increases horizontal equality for single- earner couples and for two- earner couples with the same adjusted gross income, the reform does not treat mar-

C H A P T E R 7 175

riage in a tax- neutral manner. A number of countries have therefore moved from taxing the family as a unit to taxing the individual earner.41

The income tax reform that best promotes hori-zontal equality and treats marriage in a tax- neutral manner would require individual filing regardless of marital status. As a 1998 Joint Economic Committee publication states, “Marriage neutrality can only be achieved by reverting to a system of individual filing or through fundamental tax reform.”42 Po liti cally acceptable policy recommendations tend to define the unit of taxation as the individual rather than the family.43 Both the marriage tax bonus and the mar-riage tax penalty would be eliminated with the use of an individual schedule of taxation for all taxpayers.44 Eliminating the marriage tax penalty would enable couples deciding whether to marry to do so without worrying about their changing tax status. And if the marriage tax bonus were removed, national economic growth would benefit from the skills of secondary earners no longer financially discouraged from enter-ing the labor force. As noted earlier, the United States is one of only seven countries in the Organisation for Economic Co- operation and Development to require joint income tax filing by married couples.

The Joint Economic Committee study raises con-cerns that giving couples the option of filing jointly or as two single individuals would increase the complex-ity of the US tax code. Although such a reform could increase the cost of complying with the federal income tax system, greater horizontal equality among tax-payers regardless of marital status would be promoted

176 T H E H I D D E N CO S T O F F E D E R A L TA X P O L I C Y

at the same time as encouraging greater labor force participation. However, using a mandatory single- filer system would eliminate that complexity.

The potential effects on vertical equality are worth noting, and changes to the width of tax brackets may be necessary. If policymakers want to subsidize stay- at- home parents through the tax code, the value of their noneconomic labor could be recognized by an expansion of the child tax credit and dependent deduction rather than through mandatory filing based on marital status.

The joint income filing requirement for married couples creates horizontal inequalities among couples at nearly every level of income depending on marital status. It also penalizes women for participating in the labor force. Joint income filing made more sense in the 1940s, when men tended to be higher paid than women and fewer two- earner house holds existed. Today, both spouses often work, and women are often the top earner in a house hold.

Given that a move to a single- taxpayer filing system for single and married people alike might be difficult to achieve po liti cally, married couples should, at a minimum, be given the freedom to choose which filing status is best for them— filing a joint return as a mar-ried couple or filing separate individual tax returns as if they were unmarried taxpayers (as opposed to the current system, which penalizes married taxpayers who file separately by lowering the income thresholds at which marginal tax rates apply). Although allowing taxpayers to choose for themselves which filing sta-tus is best would still result in a marriage tax bonus

C H A P T E R 7 177

for some couples, it would remove the marriage tax penalty altogether. Fostering the economic contribu-tions of a married, educated workforce would be a major step toward creating a simpler, more equitable tax code.

226 N OT E S TO PAG E S 1 5 8 –1 6 1

of adhering to a neutral tax system but also as a means to increase saving, investment, and economic growth.

67. Ling and McGill, “Variation of Homeowner Tax Preferences.” 68. Follain and Melamed, “False Messiah of Tax Policy.” 69. Poterba and Sinai, “Revenue Costs and Incentive Effects.” 70. Anderson, Clemens, and Hanson, “Capping the Mortgage

Interest Deduction.” See also Rosen, “Housing Decisions and the U.S. Income Tax.”

71. To avoid potential gaming of the credit, it would only apply to primary residences with a mortgage. It would not be available for second homes or for home equity lines of credit.

72. Green and Reschovsky, “Design of a Mortgage Interest Tax Credit.”

73. Authors’ calculations. According to the US Census Bureau’s most recent 2009 data on mortgages, there are 76.4 mil-lion owner- occupied homes with mortgages in the United States. See US Census Bureau, The 2012 Statistical Abstract: The National Data Book (Washington, DC, 2012), table 998. In 2013, $69 billion was spent on the home mortgage interest deduction. See Office of Management and Bud get, Analytical Perspectives: Bud get of the United States Government, Fiscal Year 2015, 206.

74. Jason J. Fichtner and Jacob M. Feldman, “The Hidden Costs of Tax Compliance,” Mercatus Center at George Mason University, Arlington, VA, May 20, 2013. See also Jason J. Fichtner and Jacob M. Feldman, “When Are Tax Expenditures Really Spending? A Look at Tax Expenditures and Lessons from the Tax Reform Act of 1986,” Mercatus Working Paper 11-45, Mercatus Center at George Mason University, Arlington, VA, November 2011.

CHAPTER 7: HOW DO PEOPLE RESPOND TO THE MARRIAGE TAX PENALTY? 1. James R. Alm and Mikhail I. Melnik, “Taxing the ‘Family’ in

the Individual Income Tax,” Andrew Young School of Policy Studies, Georgia State University, Atlanta, July 2004, 19.

2. Married couples must choose to file either a joint return (“married filing jointly”) or a separate return (“married filing separately”). But using the “married filing separately” status is not the same as filing as an unmarried person. The “married filing separately” status is generally the least beneficial filing status because the two taxpayers are not allowed to claim all the deductions and credits that are allowed otherwise.

N OT E S TO PAG E S 1 6 1 – 1 6 4 227

Furthermore, the income level at which the 25 percent, 28 per-cent, 33 percent, 35 percent, and 39.6 percent marginal tax rates begin to apply are lower for “married filing separately” than when filing either as an unmarried person or as “married filing jointly,” an obvious tax penalty.

3. Daniel R. Feenberg and Harvey S. Rosen, “Recent Developments in the Marriage Tax,” NBER Working Paper 4705, National Bureau of Economic Research, Cambridge, MA, April 1994, 15.

4. Sara LaLumia, “The Effects of Joint Taxation of Married Couples on Labor Supply and Non- wage Income,” Journal of Public Economics 92, no. 7 (July 2008): 1698–1719, 1700.

5. Florence Guy Seabury, letter to the editor, New York Times, May 25, 1942.

6. The Economist, “We Did It!,” December 30, 2009. See also Jonathan House, “Women Reach a Milestone in Job Market,” Wall Street Journal, November 20, 2013.

7. Leslie A. Whittington and James Alm, “Tax Reductions, Tax Changes, and the Marriage Penalty,” National Tax Journal 54, no. 3 (September 2001): 455–72. See also James Alm and Leslie A. Whittington, “Shacking Up or Shelling Out: Income Taxes, Marriage, and Cohabitation,” Review of Economics of the House hold 1, no. 3 (2003): 169–86.

8. The EITC is a federal tax credit for low- to moderate- income individuals and married couples. The credit predominantly applies to filers with one or more dependent children and has three different phaseout schedules for one, two, and three or more children. Many two- earner couples would experience a diminished credit if married because the delay in schedule phaseout is not double the single- filer credit.

9. For example, see Laura Wheaton, “Low- Income Families and the Marriage Tax,” Policy Brief, Urban Institute, Washington, DC, September 1998; Robert I. Lerman, “How Do Marriage, Cohabitation, and Single Parenthood Affect the Material Hardships of Families with Children?,” US Department of Health and Human Ser vices, Washington, DC, July 2002; and Heather J. Bachman, Rebekah Levine Coley, and P. Lindsay Chase- Lansdale, “Is Maternal Marriage Beneficial for Low- Income Adolescents?,” Applied Developmental Science 13, no. 4 (2009): 153–71.

10. LaLumia, “Effects of Joint Taxation of Married Couples,” 1699.

11. Michael Bar and Oksana Leukhina, “To Work or Not to Work: Did Tax Reforms Affect Labor Force Participation of Married

228 N OT E S TO PAG E S 1 6 4 –170

Couples?,” B.E. Journal of Macroeconomics 9, no. 1 (2009): 1–23.

12. Nada Eissa and Hilary Williamson Hoynes, “Explaining the Fall and Rise in the Tax Cost of Marriage: The Effect of Tax Laws and Demographic Trends, 1984–1997,” National Tax Journal 53, no. 3, part 2 (September 2000): 683–711, 685.

13. Whittington and Alm, “Tax Reductions, Tax Changes, and the Marriage Penalty,” 469. See also Kyle Pomerleau, “Understanding the Marriage Penalty and Marriage Bonus,” Tax Foundation, Washington, DC, April 23, 2015.

14. Feenberg and Rosen, “Recent Developments in the Marriage Tax.”

15. Ibid., 10. 16. Eissa and Hoynes, “Explaining the Fall and Rise in the Tax Cost

of Marriage,” 686–88. 17. Feenberg and Rosen, “Recent Developments in the Marriage

Tax,” 15. 18. Eissa and Hoynes, “Explaining the Fall and Rise in the Tax Cost

of Marriage,” 684. 19. Ibid., 704. 20. Whittington and Alm, “Tax Reductions, Tax Changes, and the

Marriage Penalty,” 456. 21. These reforms were included in the Economic Growth and Tax

Relief Reconciliation Act of 2001 and the Jobs and Growth Tax Relief Reconciliation Act of 2003.

22. Whittington and Alm, “Tax Reductions, Tax Changes, and the Marriage Penalty,” 458.

23. Frederick J. Feucht, L. Murphy Smith, and Robert H. Strawser, “The Negative Effect of the Marriage Penalty Tax on American Society,” Academy of Accounting and Financial Studies Journal 13, no. 1 (2009): 103–25, 104–5, quoting remarks made by President Bush.

24. Whittington and Alm, “Tax Reductions, Tax Changes, and the Marriage Penalty,” 459.

25. Ibid., 470. 26. Hayley Fisher, “The Health Benefits of Marriage: Evidence

Using Variation in Marriage Tax Penalties,” Working Paper, Cambridge University, Cambridge, UK, November 2010, 19.

27. Stacy Dickert- Conlin, “Taxes and Transfers: Their Effects on the Decision to End a Marriage,” Journal of Public Economics 73, no. 2 (August 1999): 217–40.

28. Ibid., 234.

N OT E S TO PAG E S 170 –179 229

29. Ibid., 230. 30. Ibid. 31. Feenberg and Rosen, “Recent Developments in the Marriage

Tax,” 7. This example is specific to a couple in which each earner receives $10,000 per year in income with two depen-dent children after the 1993 tax reform act.

32. Dickert- Conlin, “Taxes and Transfers,” 221. 33. Bar and Leukhina, “To Work or Not to Work?,” 2. 34. Eissa and Hoynes, “Explaining the Fall and Rise in the Tax Cost

of Marriage,” 683. 35. Ibid., 685. 36. Bar and Leukhina, “To Work or Not to Work?,” 3. 37. Ibid., 14. 38. Alm and Whittington, “Shacking Up or Shelling Out,” 16. 39. Joint Economic Committee, “Reducing Marriage Taxes: Issues

and Proposals,” Washington, DC, May 1998. 40. A form of income splitting already exists in the United States.

However, it applies only to own ers of profitable small corpora-tions paying themselves under categorizations of employee salaries and bonuses. Some researchers argue that the expanded brackets for joint filers are a form of income split-ting. This chapter refers to potential income splitting in the context of direct proportionality to the “single” tax bracket.

41. Stephen Matthews, “Trends in Top Incomes and Their Tax Policy Implications,” OECD Taxation Working Paper 4, Organisation for Economic Co- operation and Development, Paris, November 3, 2011, 37.

42. Joint Economic Committee, “Reducing Marriage Taxes,” 8. 43. Whittington and Alm, “Tax Reductions, Tax Changes, and the

Marriage Penalty,” 472. 44. Eissa and Hoynes, “Explaining the Fall and Rise in the Tax Cost

of Marriage,” 685.

CONCLUSION: KEY PRINCIPLES FOR SUCCESSFUL, SUSTAINABLE TAX REFORM 1. As noted in the introduction to this book, meeting the govern-

ment’s spending requirements is not a mandate to raise taxes to higher levels to support even higher levels of government spending. Although good tax reform will increase economic growth and such growth will increase tax revenue to some extent, the United States spends more money than it collects