the hong kong institute of chartered ... diet...page 1 of 14 the hong kong institute of chartered...

TRANSCRIPT

Page 1 of 14

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES

THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS

International Qualifying Scheme Examination

CORPORATE FINANCIAL MANAGEMENT DECEMBER 2011

Time allowed – 3 hours

Section A – Compulsory case study

Section B – 5 long questions (attempt any 3)

DO NOT OPEN THIS PAPER UNTIL INSTRUCTED TO DO SO BY THE INVIGILATOR

Important Note: Candidates are allowed 15 minutes reading time to read through the question paper before the commencement of the examination between 9:15a.m.-9:30a.m. During the reading time, all candidates must be silent and must not write or mark anything on their question papers or answer books. Candidates must close all their reference books, notes or other unauthorised materials and put these under their chairs. If any candidates write or make any marks during the reading time, or if they speak or in any other way communicate with anyone either in or outside the examination hall during this period or read any unauthorised materials, they will be disqualified from continuing this examination paper. Once candidates have opened the question paper, they are not allowed to leave the examination hall until 10:00a.m.

Page 2 of 14

THIS IS A BLANK PAGE

Page 3 of 14

SUBJECT NO 16J

CORPORATE FINANCIAL MANAGEMENT DECEMBER 2011

The examination paper is divided into TWO sections. Section A is compulsory and carries 40 marks. Candidates should attempt THREE q uestions from Section B, all of which carry 20 marks each. You should allow yourself approximately 70 minutes in total to answer the question in Section A, and 35 minutes for each of the questions attempted in Section B. Unless otherwise stated, $ denotes Hong Kong dollars. All interest rates are annual rates. Round your numerical answers to two decimal places. Friday morning 2 December 2011 Time allowed: 3 hours

SECTION A (Compulsory – answer ALL questions in this section)

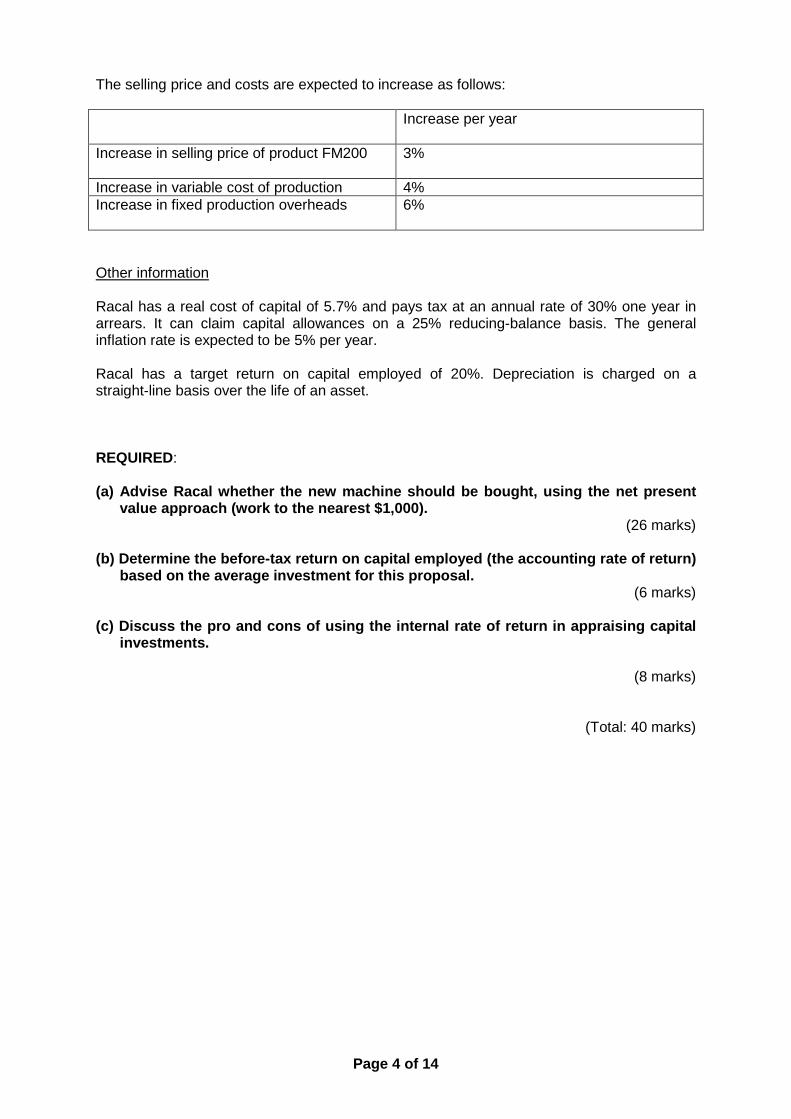

1. Racal Company (HK) Limited (Racal) is a manufacturer of fire extinguishing products.

Racal plans to buy a new machine to meet expected demand for a new product, Product FM 200. According to the company’s finance director, Joseph Cheung, there should be strong demand for the new product.

This new machine will cost $250,000 and last for four years, at the end of which time it will be sold for $5,000.

Racal anticipates demand for product FM200 to be as follows:

Year 1 2 3 4 Demand (units) 35,000 40,000 50,000 25,000

The selling price for product FM200 is expected to be $12 per unit and the variable cost of production is expected to be $7.80 per unit. Incremental annual fixed production overheads of $25,000 per year will be incurred. Selling price and costs are all in current price terms.

Page 4 of 14

The selling price and costs are expected to increase as follows: Increase per year

Increase in selling price of product FM200 3%

Increase in variable cost of production 4% Increase in fixed production overheads 6%

Other information Racal has a real cost of capital of 5.7% and pays tax at an annual rate of 30% one year in arrears. It can claim capital allowances on a 25% reducing-balance basis. The general inflation rate is expected to be 5% per year. Racal has a target return on capital employed of 20%. Depreciation is charged on a straight-line basis over the life of an asset.

REQUIRED: (a) Advise Racal whether the new machine should be bought, using the net present

value approach (work to the nearest $1,000). (26 marks)

(b) Determine the before-tax return on capital empl oyed (the accounting rate of return)

based on the average investment for this proposal. (6 marks)

(c) Discuss the pro and cons of using the internal rate of return in appraising capital

investments.

(8 marks)

(Total: 40 marks)

Page 5 of 14

SECTION B

(Answer THREE questions from this section)

2 (a) Explain the use of sensitivity analysis as an appraisal tool for a project.

(5 marks)

(b) A project requires an initial cost of $100,000 and has an expected rate of return of 10%.

Year Cash flows 1 $30,000 2 $30,000 3 $30,000 4 $30,000

REQUIRED:

Examine the sensitivity of the project under the fo llowing scenarios:

(i) Change in the initial cost of investment (8 marks)

(ii) Change in the length of the project.

(7 marks)

(Total: 20 marks)

Page 6 of 14

3. Mr. Wang is the asset manager of a $2 million portfolio. His portfolio has an expected return of 13.8% and standard deviation of 23.1%. Mr. Wang expects an additional $2 million to be put into the fund soon and plans to invest the whole amount in a mutual fund that best complements the current portfolio. He has narrowed his choice to four funds. His selection criteria are to:

(i) maintain or enhance the expected return, and

(ii) maintain or reduce the risks

of the existing portfolio.

Index fund Expected return Standard deviation Correlation of returns

with existing portfolio

A 15% 25% 0.80 B 11% 22% 0.60 C 16% 25% 0.90 D 14% 25% 0.65

REQUIRED: (a) Based on the information provided, recommend ONE of the four index funds to

Mr. Wang, assuming that Mr. Wang is a typical risk- averse investor. Explain why you have not selected the other three funds.

(10 marks) (b) If Fund A is added to Mr. Wang’s existing portfolio , calculate the portfolio risk,

in terms of standard deviation of the new portfolio . Comment on how Mr. Wang’s degree of risk aversion affects your recomme ndation in (a) above.

(10 marks)

(Total: 20 marks)

Page 7 of 14

4 (a) Distinguish between convertible bonds and loa n stocks with warrants

attached, and explain the benefits they can offer t o the issuer and to the investor.

(10 marks)

(b) Talent Cosmo Limited, a public-listed company, has issued 8% convertible loan stock which is quoted at $112 per $100 nominal. The first date for conversion is in four years’ time at the rate of 20 ordinary shares per $100 nominal loan stock. The existing share price is $5.10.

REQUIRED:

Calculate the conversion price and the conversion premium as a percentage of the existing share price of $5.10.

(5 marks)

(c ) Glory International Limited, a locally listed company, has issued loan stock with

warrants of $0.20 attached. The warrants provide the right to purchase one ordinary share at a price of $15 for every six warrants in 2013. The existing share price is $12.

REQUIRED:

Calculate the conversion premium as a percentage of the existing share price; and the value of a warrant during the conver sion period if the share price is then $20.

(5 marks)

(Total: 20 marks)

Page 8 of 14

5 Valiant Company PLC, a UK trading company, is anticipating paying €20 million

to a French supplier in three months’ time. It has decided to hedge its foreign exchange risk by using currency options. A €20 million call option was purchased at an exchange rate of €1.45: £1 at a premium of £106,040.

REQUIRED:

(a) If the spot exchange rate of sterling against the euro in three months’ time

is €1.4366-1.4389 to £1, compute the value of the o ption and the profit or loss that Valiant makes by buying and using the opt ion instead of buying euros at t he spot rate.

(8 marks)

(b) Using the purchasing power parity and interest rate parity formulae, calculate the theoretical forward spot rates for Cu rrency A in three months’ time, based upon the current middle spot rates.

Foreign exchange market Currency A/Currency B

Spot 13.4056 – 13.4093

1 month forward 0.0012 -0.0015 discount

3 months forward 0.0050 -0.0056 discount

Country A Country B

Inflation (projection) 0.8% p.a 1.6% p.a. Interest rates (projection) 2 % p.a. 4.8% p.a.

(12 marks)

(Total: 20 marks)

Page 9 of 14

6 Aaron Trading Company Limited (Aaron), with annual credit sales of $240 million,

grants on average two months’ credit to its customers. To improve its working capital management, the company is considering a change to its terms of trade to require quicker payment. It expects this to lead to customers paying on average in one month, but also to reduce its annual sales by 5%.

At the same time, it is planning to offer a discount of 1% for payment in 15 days and expects this offer to be taken up for 30% of its new, reduced turnover.

Aaron’s marginal profit on sales is 20% before discount for prompt payment, and this is not expected to change if the new credit policy is introduced.

REQUIRED:

Advise Aaron whether:

(a ) the planned change in credit allowed to its c ustomers is worthwhile, if the

company requires a return of 16% on its investments ; and (10 marks)

(b) the discount for prompt payment is worthwhile.

(10 marks)

(Total: 20 marks)

End of Examination Paper

Page 10 of 14

Page 11 of 14

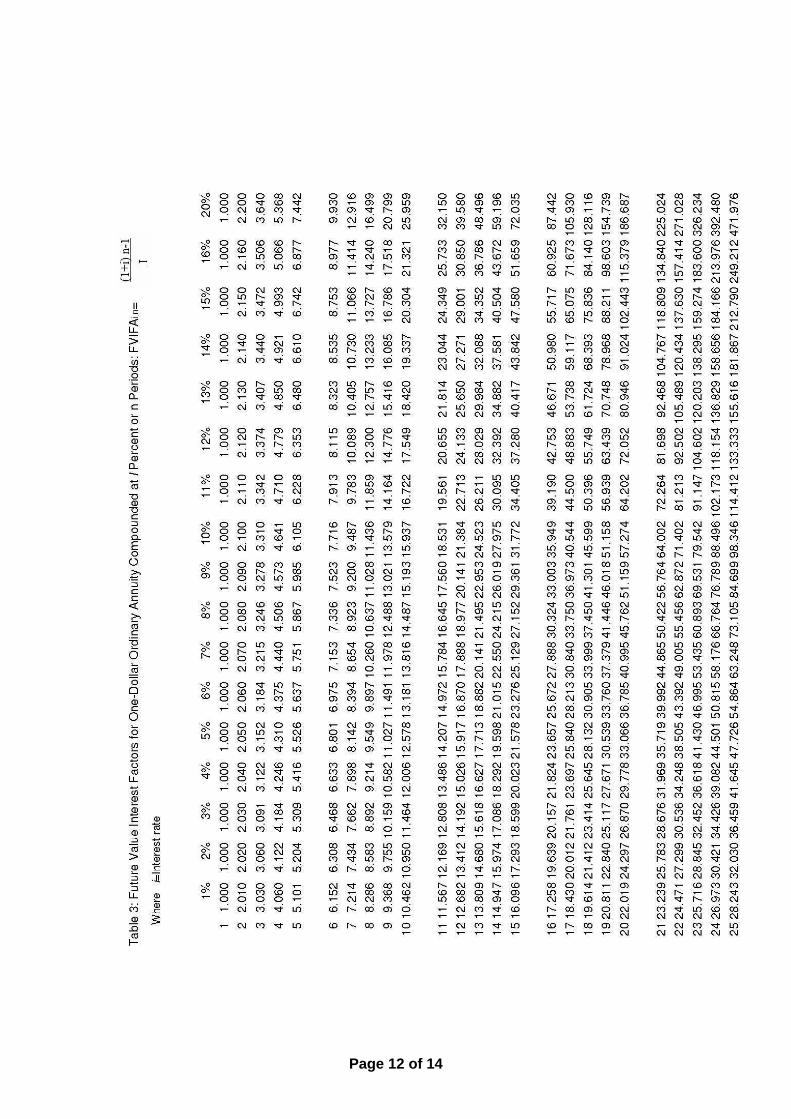

Page 12 of 14

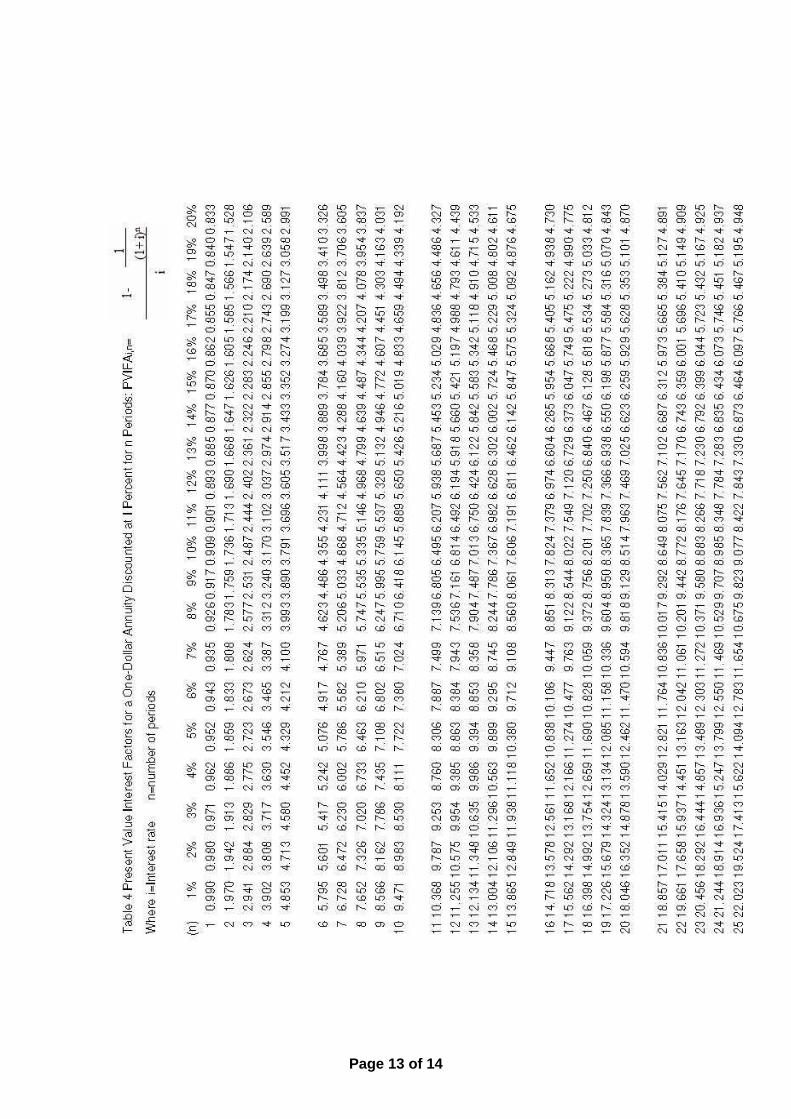

Page 13 of 14

Page 14 of 14

THIS IS A BLANK PAGE