the hunt reporthunt-partners.com/displays/uploaded/file/thehuntrepo… · · 2015-10-23the hunt...

TRANSCRIPT

the hunt report

Dear Reader,

It is a pleasure to bring to you the second issueof The Hunt Report, a half-yearly industryupdate from Hunt Partners.

The Hunt Report provides key business insightsacross a wide spectrum of industry practices,we are strongly represented in. It also gives aflavour of trends in executive hiring along witha compilation of key senior leadership moves inthese sectors.

We thank each one of you for your encouragingresponses and constructive critique to makethis endeavour more focused and relevant.

We are sure you will find this issue aninteresting and a meaningful read.

We welcome your comments [email protected]

Happy Reading!

Yogesh Chopra

Mumbai, India, May 2011

the hunt report

FOREWORD

CONTENTS I VOL II

pg.6 ASSETMANAGEMENTA mixed bag of results

pg.8 AUTOMOBILEOn the wheels of growth

pg.10 CAPITAL MARKETSBanking on debt, leveraging on equity

pg.12 ENGINEERINGSERVICESOUTSOURCINGTouching new shores

pg.14 HUMANRESOURCESExpanding thelearning curve

pg.16 INFRASTRUCTURE A concrete future

pg.18 INSURANCERestructuringinsurance

pg.20 INVESTMENTBANKINGThe highs andlows of investment banking

pg.22 LEGAL ANDSECRETARIALReforms sweepinglegal and secretarialfunctions

pg.24 LOGISTICSM&A season inlogistics

pg.26 PHARMACEUTICALSAND HEALTHCAREIn the pink of health

pg.28 PRIVATE EQUITYRetention,the key

The Hunt Report, a half-yearly update, evaluates the key

business trends in industry practices, ranging from Retail

to Insurance. This issue of The Hunt Report analyses the

impact of these significant business trends on the

executive hiring process and the leadership movements

in fifteen industry verticals.

IN THIS ISSUE

the hunt report

pg.30 REAL ESTATEOn a high rise

pg.32 RETAIL ANDCONSUMERCountering pricingpressures

pg.34 WHOLESALEBANKING AND TRADE FINANCEBanking beyondborders

ASSET MANAGEMENT

According to industry data, the totalAssets Under Management (AUM)over the there-month period endingDecember 2010 declined 5 percent.AUM fell from Rs 713,281 crore inSeptember 2010 to Rs 675,377 crorein December 2010.

Interestingly, a few fund-housesexperienced a decline more than theindustry average. JP Morgan MF AUMdropped 38 percent (the fund housesaw a leadership vacuum with theincumbent moving to IDBI MF).Baroda Pioneer MF AUM saw a dip of21 percent. Birla Sun Life MF AUMdropped 14 percent, which is nearlythree times the industry average. Thequantum of AUM decrease at BirlaSun Life (Rs 9,700 crore) would be ona stand-alone basis – the fifteenthlargest MF in terms of assets.

As the following chart demonstrates,there is a massive polarisation of assetsin the Indian MF industry. The top five

fund-houses now account for 56 percentof the total AUM (refer the pie-chart inthe corresponding page).

The press reported that Bank of India(BoI) is looking at the possibilities to re-enter the Indian MF industry. It may berecollected that BoI had exited theindustry through a part-redemption andpart sale of assets to Taurus MutualFund. It is reported that the bank hasalready finalised the selection of apartner. However, there was no suchofficial confirmation available at the timeof writing this report. Recent firms to jointhe list of asset managers in Indiainclude Edelweiss, IndiaInfoline,Indiabulls and Motilal Oswal, Edelweiss.

Domestic fund-houses seem to be keenon inducting international partnerswithin the asset management company.This seems to be driven by the need toleverage international distribution fordomestic equities. IDFC made asignificant move by divesting a 26

The Indian Mutual Funds industry has witnessed a sharppolarisation of assets with the top five fund-housesaccounting for 56 percent of the total AUM. With thechange of guard at SEBI, company heads are hopeful of areview of the stringent regulations in the industry.

A mixed bag of results

The quarter ending December 2010 has ensured some stability in the Mutual Funds(MF) industry. This is a welcome change, especially after the tumultuous period ofthe ban on entry-loads in 2009, the uncertainty surrounding the leadership regime

at Securities and Exchange Board of India (SEBI) and the public dispute on regulatory turfbetween SEBI and Insurance Regulatory and Development Authority (IRDA).

BY ARJUN ERRY

pg.7

the hunt reportPEOPLE MOVEMENT

percent equity stake to Natixis GAM ofFrance. LIC Mutual Fund, too, divested 35percent to Nomura Asset Management.Perhaps, the Board of UTI Mutual Fundhad already seen this opportunity whenit invited T Rowe Price to buy-out acombined 26 percent equity stake fromthe four existing shareholders.The needto have an international distribution isbound to accelerate, considering theUnion Budget allowing overseasindividuals to invest in domestic MFs.

An analysis of FY11 over FY10 providessome interesting statistics. Profitability ofthe industry (PBT basis) grew 247percent for March 2010 as compared toMarch 2009.This is in contrast to a PBTgrowth of barely 5 percent for March2009 over March 2008. Further, the topfive fund-houses in terms of AUM,control a greater share of total PBT at 69percent of the industry's PBT.The graphon this page shows the growth of fee-income and PBT over the three-yearperiod ending March 2010.

The early part of 2011 also witnessed achange of leadership in SEBI. UK Sinha,Chairman and Managing Director of UTIAsset Management overtook Chairman,SEBI from the outgoing Chairman, CBBhave. Association of Mutual Funds in

India also experienced a change ofguard with Milind Barve assuming theChairmanship after UK Sinha’s exit.Several MF Chief Executive Officers seemconfident that the new leadership atSEBI may be positive in rolling-back ordiluting some of the regulatorydecisions.While it looks highly unlikelythat the ban on the entry-load will berevoked, some MF Chief ExecutiveOfficers do expect a ‘halfway house’.

● Ajai Kaul, acting Chief ExecutiveOfficer of Asia ex Japan at AllianceBernstein has been confirmed asthe company’s Chief ExecutiveOfficer.

● Anand Shah, Head of Equities atCanara Robeco Mutual Fund hasjoined BNP Paribas Mutual Fund asChief Information Officer.

● Manish Sinhai and Kevin Talbothave been appointed by AvivaInvestors as inaugural ChiefInvestment Officers for Asia Pacific.

● Nikhil Srinivasan, ChiefInvestment Officer of Asia Pacific atAllianz Investment Managementwas named as Group ChiefInvestment Officer.

● Nilesh Shah, Deputy ManagingDirector at ICICI Prudential MutualFund joined AXIS Bank as Presidentof Corporate Banking.

● Piyush Surana was named theChief Executive Officer at DaiwaAsset Management, following thelatter's acquisition of Shinsei AssetManagement India.

● Prateek Agrawal, Head ofEquities at Bharti AXA IM moved toASK Mutual Fund.

● Puneet Chaddha, ManagingDirector of Commercial Banking,HSBC moved to HSBC Mutual Fundas Chief Executive Officer.

● Sanjay Sachdev has joined TataAsset Management as Presidentand Chief Executive Officer.

● Uday Suri, Head, Retail Sales,Fidelity Mutual Fund has joinedBNP Paribas MF as Head, Sales.

● Vikaas Sachdeva, Country Head,Sales and Business Development atBharti AXA Investment Managershas joined Edelweiss MF as ChiefExecutive Officer.

MF Assets: AUM Distribution byFund Houses

All Others

Top 5

44% 56%

PBTFee Income

FY10FY09FY08620 653

1615

27382963

4201

Income over PBT - 3 Year Trend(INR Crore)

AUTOMOBILE

In the light of upbeat market sentiment,increased hiring activity is more visibleamong some players. Companies likeTata Motors and Mahindra & Mahindra,that expect exponential growth, haveadopted a “more plus”hiring strategy toensure continued productivity. Originalequipment manufacturers (OEMs) arehiring 20 to 25 percent in excess of needto mitigate the risks associated withdelivery timelines due to the shortage oflabour.This process particularly workswhere the company is supplying to theWest – these customers focus on timelyend product; diametrically oppositefrom Japanese companies which focuson the process.Take the example ofEicher which would recruit 25 where 15were needed; thereby ensuring no delayin delivery to Volvo

Another company to look out for isHonda Motorcycles. Following thedissolution of the Hero Honda jointventure; the Japanese major hasannounced a plan to rejig the entire topmanagement of its Indian subsidiary.The

senior most position of President andChief Executive Officer will be retainedby a Japanese national (KeitaMuramatsu replaces Shinji Aoyama) andother functional heads might also beheld by Japanese expatriates. However,given the company’s plans to launchmass market bikes aimed at rural India,they might require strong local talentwith significant expertise inunderstanding the Indian rural mindset.

According to the Society of IndianAutomobile Manufacturers (SIAM), theIndian automobile market is the seventhlargest in the world.With sales projectedto reach 5 million by 2015, investmentby the auto and auto componentindustries is expected to cross $30 billionin the next four years.

In anticipation of these robust growthprojections, several auto componentmanufacturers have acquired land fornew plants in Manesar, Uttarakhand andin Thiruvallur and Sriperumbudur nearChennai. Hiring is likely to increase

The rising number of cars on the roads coupled with anincreasing geographical spread surely puts the Indianautomobile industry on the right path to success.

On the wheels of growth

TThe Indian automobile industry has witnessed a 33 percent rise in the number ofpassenger cars on the road from 2008-09 to 2009-10. A strong upswing continueswith 20 plus new hatchback and sedan models hitting the Indian roads this year.

BY SUNISHI GABHAWALA

pg.9

the hunt reportPEOPLE MOVEMENT

significantly in these regions. However,an estimated 30 percent gap exists inthe availability of technical engineers,especially in the 6 to 12 years experiencebracket.This may result inunprecedented salary hikes in the OEMand component space.

Attrition within the component space isat an all-time high with 35 percentmoving to auto OEMs, who can afford topay better salaries. An engineer with anannual salary of Rs 2.5 lakh can expectanything between Rs 7 to 8 lakh with anautomobile manufacturer. New player,Mahindra Navistar has absorbed a largenumber of professionals from thecomponent space

The auto component manufacturerscannot afford to tie their fortunes to theeconomies of the auto industry, havingexperienced a downturn in 2007-09.Traditional auto componentmanufacturers like Bharat Forge haveshifted to manufacturing non-auto partsto ensure sustained business. From an85:15 product offering mix; the companyplans to diversify into 55:45 mix, offeringnon-auto products including marineproducts, power generation equipmentand diesel engines.

Another important strategy adopted bymid to large players in the auto industryis to sponsor one or two IndustrialTraining Institutes (ITIs) in the country.The sponsoring company assists indesigning the course and providespractical training; thus assuringthemselves a broad array of traineeengineers for recruitment. Companies

also sponsor undergraduate workers topremier institutes like BITS Pilani for adiploma program.

Over the next three to five years,hiring high quality engineers will remaina challenge. Early movers havedeveloped these and other strategies toensure that talent does not become aconstraint to growth.

● Sunil Gandhi has moved to KPITCummins InfoSystems as VicePresident. He was earlier Director,Operations in Force Motors.

● PK Das has resigned from hisposition of Deputy GeneralManager, Engineering ServiceSales, Chicago at Larsen & Toubro,to join Sarralle Equipment India asDirector, Operations.

● Vijay Grover, who was earlierHead, Engineering at Bechtel, isnow President and Chief ExecutiveOfficer of SK E&C India.

● Rajan Madan is now Plant Head of Denso India. He was earlierAssistant Plant Head at General Motors.

● Sriram P has moved fromHindustan Motors as Head,Operations to Daimler IndiaCommercial Vehicles as GeneralManager, Operations.

● Kaushik Haldar has joined JohnDeere India as Head,Manufacturing Engineering andPlant Engineering. He was earlierHead, Manufacturing at ZAOCummins Kama, Russia.

● Nirmal Matharu has beenappointed as Vice President andPlant Head at Mahindra &Mahindra. He was earlier SeniorGeneral Manager, Manufacturing atHero Honda Motors.

CAPITAL MARKETS

Debt capital marketThe gradually strengthening debt marketseems to have entered an interesting erathat presents a wider universe ofinvestible options.Besides the debtproducts that mutual funds offer,the newdebt options like zero-coupon bonds,non-convertible debentures,corporatebonds and infrastructure bonds,havegained great potential to create plenty ofinterest among investors – domestic aswell as overseas.

Debt raised by Indian entities in foreignmarkets has registered almost a three-foldgrowth.The interest rates are hardening,liquidity is tight and there is a strongdemand for Indian debt.The prevailingmarket conditions should supportcorporates and banking institution’sdemand for G3 bond market.

It is also likely that more Indian companieswould look for acquisitions andinvestments in overseas operations acrosssectors.Since the interest on dollar loans is

expected to continue to be lower thanrupee loans,the preference will be to raisefunds overseas.At the same time,dollar-denominated bond sales from India willcontinue to generate plenty of interest.

The Union Budget has proposed to raisethe Foreign Institutional Investors (FII) limitfor investment in corporate bonds by $20billion to $40 billion.The increase in thelimit should foster an increase ininvestment of foreign funds in thecorporate debt market.The action thoughlate is a welcome step to deepen thecorporate debt market and we expectthat it will encourage companies tolaunch more such bonds.

We are further witnessing another interestgroup that is queuing up to invest inrupee-denominated debt issued by RBIand major companies.Malaysian CentralBank,Bank Negara has stepped in andregistered as an FII.

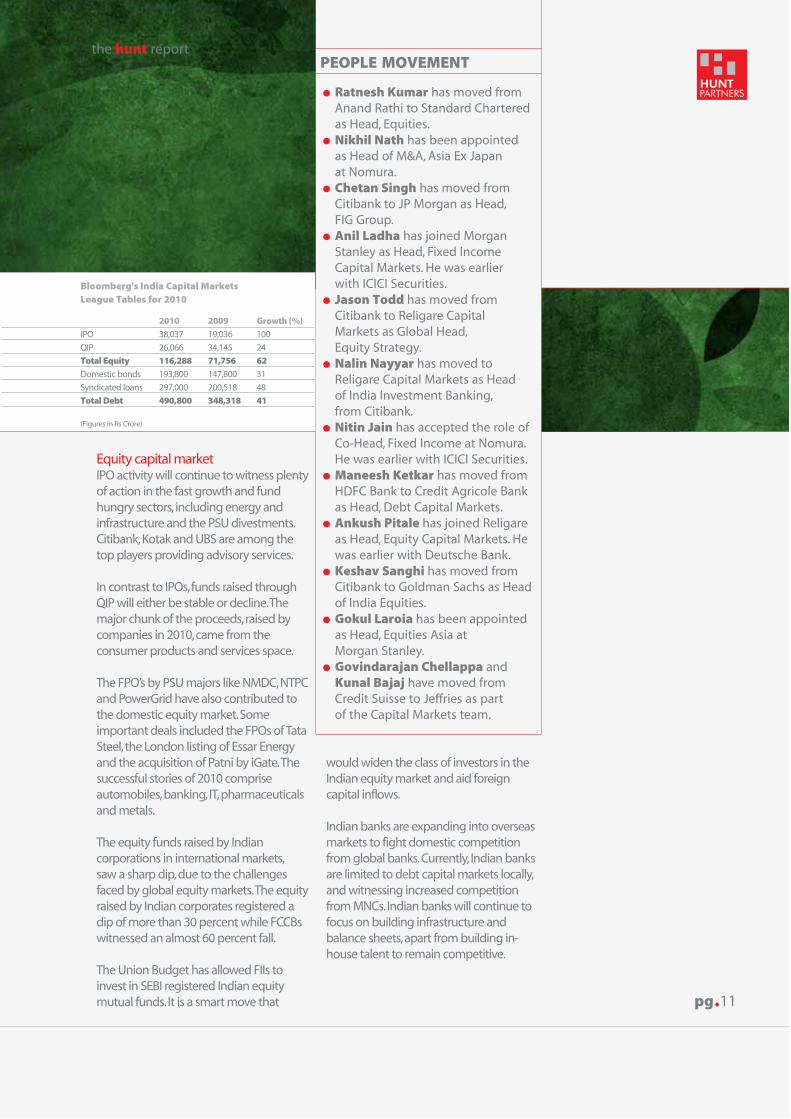

The capital market experienced an upswing in the debtmarket, which has attracted not only Indian investors,but also their global counterparts. The hike in ForeignInstitutional Investors limit may further boost the flow offoreign funds into the Indian debt market.

Banking on debt, leveragingon equity

2010 was one of the best years for the Indian capital market, recording a bumpergrowth of more than 31 percent for a volume of $29 billion in equities. The yearregistered more than 25 deals, each worth more than $1 billion. However, debt held

on to its pole position as the most preferred capital raising source

BY SURESH RAINA

pg.11

the hunt reportPEOPLE MOVEMENT

Equity capital marketIPO activity will continue to witness plentyof action in the fast growth and fundhungry sectors, including energy andinfrastructure and the PSU divestments.Citibank,Kotak and UBS are among thetop players providing advisory services.

In contrast to IPOs,funds raised throughQIP will either be stable or decline.Themajor chunk of the proceeds,raised bycompanies in 2010,came from theconsumer products and services space.

The FPO’s by PSU majors like NMDC,NTPCand PowerGrid have also contributed tothe domestic equity market.Someimportant deals included the FPOs of TataSteel,the London listing of Essar Energyand the acquisition of Patni by iGate.Thesuccessful stories of 2010 compriseautomobiles,banking,IT,pharmaceuticalsand metals.

The equity funds raised by Indiancorporations in international markets,saw a sharp dip,due to the challengesfaced by global equity markets.The equityraised by Indian corporates registered adip of more than 30 percent while FCCBswitnessed an almost 60 percent fall.

The Union Budget has allowed FIIs toinvest in SEBI registered Indian equitymutual funds.It is a smart move that

would widen the class of investors in theIndian equity market and aid foreigncapital inflows.

Indian banks are expanding into overseasmarkets to fight domestic competitionfrom global banks.Currently, Indian banksare limited to debt capital markets locally,and witnessing increased competitionfrom MNCs.Indian banks will continue tofocus on building infrastructure andbalance sheets,apart from building in-house talent to remain competitive.

● Ratnesh Kumar has moved fromAnand Rathi to Standard Charteredas Head, Equities.

● Nikhil Nath has been appointedas Head of M&A, Asia Ex Japan at Nomura.

● Chetan Singh has moved fromCitibank to JP Morgan as Head,FIG Group.

● Anil Ladha has joined MorganStanley as Head, Fixed IncomeCapital Markets. He was earlier with ICICI Securities.

● Jason Todd has moved fromCitibank to Religare CapitalMarkets as Global Head,Equity Strategy.

● Nalin Nayyar has moved toReligare Capital Markets as Head of India Investment Banking,from Citibank.

● Nitin Jain has accepted the role ofCo-Head, Fixed Income at Nomura.He was earlier with ICICI Securities.

● Maneesh Ketkar has moved fromHDFC Bank to Credit Agricole Bankas Head, Debt Capital Markets.

● Ankush Pitale has joined Religareas Head, Equity Capital Markets. Hewas earlier with Deutsche Bank.

● Keshav Sanghi has moved fromCitibank to Goldman Sachs as Headof India Equities.

● Gokul Laroia has been appointedas Head, Equities Asia at Morgan Stanley.

● Govindarajan Chellappa andKunal Bajaj have moved fromCredit Suisse to Jeffries as part of the Capital Markets team.

Bloomberg's India Capital Markets League Tables for 2010

2010 2009 Growth (%)IPO 38,037 19,036 100

QIP 26,066 34,145 24

Total Equity 116,288 71,756 62Domestic bonds 193,800 147,800 31

Syndicated loans 297,000 200,518 48

Total Debt 490,800 348,318 41

(Figures in Rs Crore)

ENGINEERING SERVICES OUTSOURCING

Engineering Services Outsourcing(ESO) started in the early 90s. Thetrend received a significant boost asglobal engineering organisationsbegan to look for ways to increaseproduct development while reducingper-unit labour costs. Over the years,global organisations have continuedto grow their offshore presence bysetting up or expanding existingcaptive facilities and augmentingspends through third party providers.Offshore ESO centres in India havegrown in capability as well asmaturity. Today, many of themdevelop full systems or products forOutsourced Engineering customers inthe western markets.

Trends-spottingEngineering services thatpredominantly focused on verticalslike automotive, aerospace and hightech are now witnessing theemergence of verticals such as

infrastructure, energy, constructionand heavy engineering. However, thetraditional sectors still continue togrow. For instance, India’s automotiveESO industry is expected to grow at aCAGR of 32 percent by 2012-13, withthe potential to generate revenuesworth $2.2 billion over the next twoyears (Source: Frost & Sullivan).

The automotive sector is expanding,especially with India becoming aninnovation hub for small carprograms. This, in turn, is fuelling theneed for domain experts at tier-2level to lead such programs. So is thecase with embedded software andelectronics (that are gaining steam)and the emerging sectors like energy.The demand for domain experts, whopossess a deep understanding of theecosystem and the ability to work on global contracts, is on the rise.This is primarily because there is aneed for working in an evolving

Engineering Services Outsourcing is touching new highs,given the stellar growth in recent years. While newverticals are coming under its ambit, there is also agrowing demand for tier-2 domain experts. And itsexpansion into emerging markets will place the industryon a sure-footed growth trajectory.

Touching new shores

Budgets for Global engineering Research & Development have almost tripled from amere $407 billion to $1,100 billion in 2009. It is expected to touch $1,350 billion in2020. The growth is fuelled by various trends such as green technology,

convergence technologies, electronics and an increased customer base in emergingmarkets (Source: Booz Innovation 1000 database 2020; Booz and Company Analysis).

BY ANNE PRABHU AND ARJUN ERRY

pg.13

the hunt reportPEOPLE MOVEMENT

ecosystem and providing design tomanufacturing services, especially inthe aerospace domain.

ESO, which supported mature marketsin the early and mid 2000, is nowgearing up for emerging markets aswell. This trend is a result of risingincomes in these nascent markets,which further leads to a demand formore products and services. Philipsand Nokia are examples of suchorganisations. To boost this trend thehighest demand for talent is in thehigh-end technical skills domain andthe ability to innovate and develop IP.

While semiconductors,pharmaceuticals and medical deviceshave been the fastest growingverticals, automotive, consumerelectronics and high tech haveemerged as the largest spenders.These trends are primarily fuelled bythe need for new product

development, convergence oftechnologies, et al.

Traditionally, industry thought leaders,academicians, domain experts andproduct specialists—both from publicsector organisations andmanufacturing industries—moved tothe ESO industry and helped inestablishing it. Today, the industry hasevolved. While such leaders are stillinducted into specialist roles, there isa great demand for leaders, who cantransform organisations, strategiseand create innovative models, driveoperational excellence. Such leadershave the potential to grow and addvalue to the organisation. Suchdemand is across both captive andthird party ESO providers at the ChiefExecutive Officers or at the CentreHead level.

● Rajesh Kumar Ojha joinedAccenture as Vice President andIndia Lead in its Aerospace andDefence and Embedded SoftwareServices vertical. He was earlier the Sales Leader, Aerospace,Defence and Industrial Products at IBM India.

● Sridhar Lakshminarayanan hasbeen appointed as the VicePresident in Satyam VentureEngineering Services. He waspreviously with IDS Infotech asBusiness Head and Senior VicePresident, Engineering and Design BU.

● Sudhakar Kolli joined Joy MiningMachinery as Vice President. Earlierhe was the Director, MachineDesign Centre at Caterpillar.

● Chetan Rangaiah has movedfrom TCS, where he was ClientPartner, Medical Devices to L&T IESas Director, Client Relations.

● Amit Majithia, who was the AreaVice President, E&PC at L&TInfotech, has moved as Senior ClientPartner to Wipro Technologies.

HUMAN RESOURCES

L&D professionals are challenged totransform the old-school command-and-control approach to a culture thatattracts and retains employees. Today,employees have access to a gamut oftraining programmes. This furtherchallenges L&D professionals toprovide the best training possible sothat it has a measurable impact onthe business and organisationalsuccess. The lecturer and classroomapproach is also being replaced by amore participative, collaborative andone-on-one coaching sessions thatallow for immediate feedback and learning.

After the rapid economical growthand the subsequent recession, L&D

professionals are back in focus toensure that productivity, retentionand engagement levels remain high.Organisations that are traditionallyknown for their L&D practices, such asthe Tatas, Hindustan Unilever, Infosysand the Aditya Birla Group have ledby example for their well-plannedstrategies that span several years.

Almost all organisations—from theservice sector to manufacturing, start-ups or steady-state—are increasingtheir investment in L&D, andspecifically, in leadershipdevelopment. In 2010, Infosys put anew premium on internal training togroom employees for leadership rolesin its myriad ventures. The company

In today’s fast-paced business world, companies havebegun to realise that corporate learning and developmentis mandatory for a successful business. While on one handorganisations, today, earmark separate training budgets,on the other, they have also ushered in a moreparticipative approach to employee engagement.

Expanding thelearning curve

Today’s dynamic business environment, heightened competition and rapid growthhave led Chief Executive Officers to focus on Learning and Development (L&D), sothat they obtain the much-needed competitive edge. Corporate L&D has evolved

into a key business function, transcending the traditional training and educationparadigm. The mandate for business leaders and learning professionals has been defined,and the scope is enormous. These individuals are responsible for strengtheningleadership traits, meeting demands, developing innovative cultures, catering to customerrequirements, constructing engagement levels and providing leadership to virtual anddiverse teams. Moreover, they also have to provide a faster on-boarding, gear up to handlenew responsibilities and functions in order to meet the aspirations of Generation Y andretain high potential talent, among others.

BY ANNE PRABHU

pg.15

the hunt reportPEOPLE MOVEMENT

increased its training budget by 24percent to $230 million and hikedtraining time by 10 weeks to 29weeks.“We want employees tounderstand the context of thecustomer and equip them with betterbusiness acumen so that they canoffer solutions and options to clientsand not just routine services,” said TanMoorthy, Vice President and Head(Education and Research), Infosys.

According to the Hay Group study(2010 edition), all the top 20companies reported that each andevery employee (at all the levels of theorganisation) has the opportunity todevelop and practise the capabilitiesneeded to lead others, compared toless than 70 percent of all othercompanies in the study. The studyranks the best companies forleadership around the globe, andexamines how they develop currentand future leaders.

There is an increase in demand forL&D professionals in services sectorslike IT, ITeS, banking and telecom thatallocate about 0.5 to 2 percent of theirrevenue on L&D. For professionals,with an in-depth knowledge of thebusiness and who can clearly alignL&D to business needs, havenumerous opportunities in the jobmarket. Today, companies haveawakened to the fact that neglectingL&D needs because of cost pressureswill only backfire through increasingconflicts, decreased productivity andreduced competitiveness.

● Vinita Tikoo joined ReligareEnterprises as Executive VicePresident, Talent Management andDevelopment. She was previouslywith Bharti Airtel as GeneralManager, Leadership Developmentand Capability Building.

● Sujatha Das moved from Oracle,where she was Head, Learning,Competency and KnowledgeExcellence to American Express as Director.

● Shachi Kaul has accepted the roleof Head, Learning andDevelopment, South Asia, atDeutsche Bank. She was formerlywith HSBC as Vice President,Learning and Development.

● Dipankar Khanna moved toMindTree as Associate LeadershipCoach from Meta CoachingFoundation, where he was Directorfor India.

● Abhishek Kumar joined Aircel asHead, Learning and Developmentfrom Vodafone, where he served inthe same capacity.

● Madhushree Ganguli, who wasearlier Head, Learning andDevelopment at Sapient, has joinedMercer India as Training Leader.

● Harlina Sodhi has beenappointed Senior Vice President,Learning and Development atReliance Industries. She wasformerly Vice President, Learningand Development at Genpact.

● Bhanu Chandran joined NorthernTrust as Regional Head of Learningand Development for Asia Pacific.She was earlier Vice President Indiaand Head of Learning, Developmentand Talent Management Services atGoldman Sachs.

● Gautam Bhushan joined Aircel asHead of Learning andDevelopment. He previously servedin the same capacity with WNSGlobal Services.

INFRASTRUCTURE

Infrastructure companies are on ahuge capital raising binge to cater tothe accelerated growth in theindustry. The current trend indicatesthat large infrastructure companiesare strengthening their internalfinance and advisory teams with acombination of investment bankingskill-sets – debt syndication, corporateadvisory and project finance. Privatesector partnership will be the key todevelopment, and about 50 percent ofthe capital required will be met byprivate sector schemes.

Private equity investments are flowinginto the sector too, but they cannotmake significant investments in coreinfrastructure because of their growthequity nature. Therefore, a lot of actionis being seen in the ancillaries or theinfrastructure enablers space.Equipment suppliers to the powersector, such as boiler, turbine andgenerator packages for coal-basedpower plants, are in demand by UMPPand large plants. Another trend is thatIndian companies are struggling toreduce expenses and boost thecapacity to retain their market share.On the other hand, Chinese players

With contractors donning the role of developers,the face of the infrastructure industry in India is set to undergo a change. While the overall industry is on a capital raising spree, heightened activity in the roads and ports sector is likely to usher in new infrastructure projects.

A concrete future

There is a significant change in the project value chain of the infrastructure industry.Numerous players are increasingly moving towards an asset ownership model, thusclimbing up the value chain. No longer content with being mere constructors, they

aspire to be owners, developers and operators where revenues are expected to amassover a period of 15-25 years, combined with higher risks. Operating at this level woulddemand higher degree of risk management and financial engineering skills. Thus,companies will need to acquire design skills and build balance sheets that are strongenough to support towering projects. They will increasingly looking at bringingexceptional talent on board for those roles that form the core of their business. There aretwo main reasons for such a trend: one being a general scarcity of talent, and secondly,companies are growing at a pace of 20-30 percent. Thus, these companies will soonengage in outsourcing non-core functions. The next fiscal is estimated to witnessheightened activity in the roads and ports sector, and the prospect of more projectscoming in, especially after the slowdown in the last six months, looks bright.

BY SURESH RAINA

pg.17

the hunt reportPEOPLE MOVEMENT

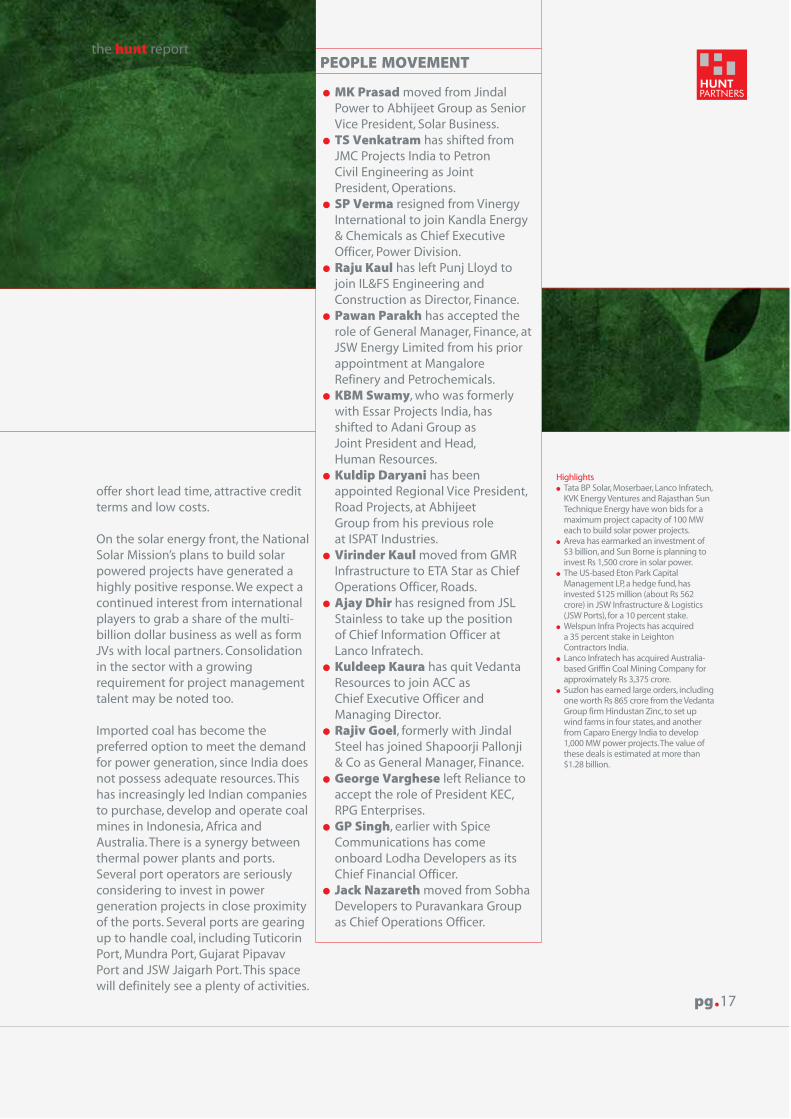

offer short lead time, attractive creditterms and low costs.

On the solar energy front, the NationalSolar Mission’s plans to build solarpowered projects have generated ahighly positive response. We expect acontinued interest from internationalplayers to grab a share of the multi-billion dollar business as well as formJVs with local partners. Consolidationin the sector with a growingrequirement for project managementtalent may be noted too.

Imported coal has become thepreferred option to meet the demandfor power generation, since India doesnot possess adequate resources. Thishas increasingly led Indian companiesto purchase, develop and operate coalmines in Indonesia, Africa andAustralia. There is a synergy betweenthermal power plants and ports.Several port operators are seriouslyconsidering to invest in powergeneration projects in close proximityof the ports. Several ports are gearingup to handle coal, including TuticorinPort, Mundra Port, Gujarat PipavavPort and JSW Jaigarh Port. This spacewill definitely see a plenty of activities.

● MK Prasad moved from JindalPower to Abhijeet Group as SeniorVice President, Solar Business.

● TS Venkatram has shifted fromJMC Projects India to Petron Civil Engineering as Joint President, Operations.

● SP Verma resigned from VinergyInternational to join Kandla Energy& Chemicals as Chief ExecutiveOfficer, Power Division.

● Raju Kaul has left Punj Lloyd tojoin IL&FS Engineering andConstruction as Director, Finance.

● Pawan Parakh has accepted therole of General Manager, Finance, atJSW Energy Limited from his priorappointment at MangaloreRefinery and Petrochemicals.

● KBM Swamy, who was formerlywith Essar Projects India, hasshifted to Adani Group as Joint President and Head,Human Resources.

● Kuldip Daryani has beenappointed Regional Vice President,Road Projects, at Abhijeet Group from his previous role at ISPAT Industries.

● Virinder Kaul moved from GMRInfrastructure to ETA Star as ChiefOperations Officer, Roads.

● Ajay Dhir has resigned from JSLStainless to take up the position of Chief Information Officer atLanco Infratech.

● Kuldeep Kaura has quit VedantaResources to join ACC as Chief Executive Officer andManaging Director.

● Rajiv Goel, formerly with JindalSteel has joined Shapoorji Pallonji& Co as General Manager, Finance.

● George Varghese left Reliance toaccept the role of President KEC,RPG Enterprises.

● GP Singh, earlier with SpiceCommunications has comeonboard Lodha Developers as itsChief Financial Officer.

● Jack Nazareth moved from SobhaDevelopers to Puravankara Groupas Chief Operations Officer.

Highlights● Tata BP Solar, Moserbaer, Lanco Infratech,

KVK Energy Ventures and Rajasthan SunTechnique Energy have won bids for amaximum project capacity of 100 MWeach to build solar power projects.

● Areva has earmarked an investment of $3 billion, and Sun Borne is planning toinvest Rs 1,500 crore in solar power.

● The US-based Eton Park CapitalManagement LP, a hedge fund, hasinvested $125 million (about Rs 562crore) in JSW Infrastructure & Logistics(JSW Ports), for a 10 percent stake.

● Welspun Infra Projects has acquired a 35 percent stake in LeightonContractors India.

● Lanco Infratech has acquired Australia-based Griffin Coal Mining Company forapproximately Rs 3,375 crore.

● Suzlon has earned large orders, includingone worth Rs 865 crore from the VedantaGroup firm Hindustan Zinc, to set upwind farms in four states, and anotherfrom Caparo Energy India to develop1,000 MW power projects.The value ofthese deals is estimated at more than$1.28 billion.

INSURANCE

The Insurance Regulatory andDevelopment Authority (IRDA) hasbeen highly active in issuing newregulations and guidelines for theindustry, especially in the lifeinsurance space. As per the recentguidelines, commissions are requiredto be evenly distributed in the firstfew years – a sharp deviation from theinternational practices.

Unfortunately, on the legislative front,the progress is almost nil. Theamendments to the Insurance Act arepiling up and now pending for years,severely impacting the overall healthof the industry. Simultaneously, theincreasing foreign equity is also heldup for several years now.

IRDA’s Chairman, J Harinarayanexpressed his views on the limitationsof tied agency and made a strongpitch for bancassurance as the betterchannel. He argued that the 80,000strong branch networks should be

leveraged in a better way. Assessingthe overall activities of the regulator,it appears that its regulations andguidelines have a direct impact on the day-to-day operations of manyplayers than merely acting as anoverseeing authority.

Several insurance companies arejoining hands to address some of thefundamental issues in the industrywith an objective to achieve a well-balanced legal, regulatory,competitive and compliant industrystructure to secure the customerinterests as well. Reliance LifeInsurance has set an importantbenchmark by striking a deal withNippon Life Insurance, the largest lifeinsurance company in Japan. Nipponwill acquire a 26 percent stake inReliance for a reported $680 million,valuing Reliance at $2.3 billion. HDFCStandard Life changed its brand toHDFC Life dropping the “StandardLife” from its branding. It was also one

Despite spiraling challenges like tightening of policiesand high attrition, the overall performance of theinsurance sector has been positive, driven largely byhealth insurance. The industry has been trying to changethe customer's perception of insurance as a wealthmanagement too.

Restructuringinsurance

The insurance industry grew at over 20 percent in the first 11 months of FY11.However, the sharp difference emerged as the private life insurers experienced a 15.1 percent decline in the new businesses, while the health insurance

continued its brisk growth over 40 percent.

BY YVO METZELAAR AND ARJUN ERRY

pg.19

the hunt reportPEOPLE MOVEMENT

of the only three private companiesregistering positive growth in thefiscal year till February 2011 –climbing to the third position,preceded by ICICI Prulife and SBI LifeInsurance in the second slot.

The health insurance space lookspromising with two of the fullydedicated players achieving a growthof 100 percent plus from a small base.Health insurance ought to be seen asa separate vertical given the nature ofits business, its social and politicalrelevance, and its impact onhealthcare financing. Healthcarefinancing, currently, accounts for notmore than a few percent of the totalhealthcare spend in the country.However, the regulatory environmentremains challenging.

Another very exciting news is that thelong-awaited guidelines for publiclisting are emerging and that somecompanies are preparing for an IPOwithin the next 12 to 24 months. Suchcompanies are SBI Life Insurance, ICICIPrulife, HDFC Life and several others.The insurance sector is definitelyhighly involved in the emerging needof regulating the advisory and salesprocess for financial products. Someaddress it as wealth management – aterm, though undefined, includessteps of the process followed toadvise clients on protecting,maintaining and enhancing theirwealth, including financial planningfor the future. The BFSI industry,regulators and the governmentappear to be investigating the proper

platform to develop such frameworkwhich, by itself, will take years todevelop and implement.

The senior management in theinsurance industry continues tomigrate to other industries. It is amatter of serious concern that maylead to a critical talent crunch,especially the top management.Meanwhile, the recognition of freshtalent is growing in the industry. Fiveof the 10 largest life insurancecompanies have appointed new ChiefExecutive Officers in the last 24months, which reflects the changingface of the industry.It is also important to mention thatthe terrible human cost and thefinancial impact of the devastatingearthquake and tsunami in Japan. Itappears that insurers' exposure will beto the tune of $50 billion.

● Kamesh Goyal has beenappointed as the Chief ExecutiveOfficer of Allianz Asia Pacificsucceeding Bruce Bowers, whohas moved to Europe for Allianz.Kamesh was the Country Head forBajaj Allianz Life Insurance.

● Following the appointment ofKamesh Goyal, V Philip has beenappointed as the new ChiefExecutive Officer of Bajaj AllianzLife Insurance. He was previouslythe Chief Operating Officer of the company.

● John Holden has taken over fromHarpal Karlkut as the ChiefExecutive Officer of Canara HSBCOBC Life Insurance. He comes fromHana HSBC Life Insurance in Korea,where he was Deputy Presidentand Chief Operating Officer.

● Milind Chalisgaonkar took overas the Chief Executive Officer ofBharti AXA Life Insurance fromGlenn Williams who moved backto AXA Hong Kong Life Insurance.

● DLF Pramerica Life Insurance has anew Managing Director and ChiefExecutive Officer in PavanDhamija, who joined the companya few months back as its Chief Operating Officer from HDB Financial Services.

INVESTMENT BANKING

From the global standpoint, the M&Aactivity has been pegged at $717 billion this quarter. This is a riseof 58 percent from the correspondingperiod in 2010 and the best start sincethe heydays of 2007. But a detailedanalysis of the last six months in Indiareveals that the first quarter of 2011witnessed a decline of more than 60 percent in the number of M&As,as compared to the fourth quarter of2010, as per the ISI Emerging Marketsdatabase. Experts attribute thisdecline to the macro-economicuncertainties emerging from theEuropean debt issues, the aftermathof the Japan tragedy and unrest in theMiddle East and North Africa. Mostcompanies are adopting a wait andwatch approach. According to GrantThornton, India witnessed 143 M&Adeals in the first quarter of 2011 as compared to the 188 in the

corresponding quarter of 2010, a dipof 24 percent. However, the deal valuein 2011 has registered higher figures,thanks to the $7.2 billion Reliance-BPdeal in February 2011. The year alsosaw some significant high value dealswith six transactions crossing the$600 million mark, the highestamongst the corresponding periodsin the last five years.

A sector-wise analysis of the last sixmonths shows that IT and ITeS hasseen 45 M&A deals, followed bypharma, healthcare andbiotechnology while the banking andfinancial services sector has registered29 and 23 deals, respectively. Some ofthe high value deals for this periodhave been the $726 million buyout ofParas Pharma by Reckitt Benckiser,International Paper picking upcontrolling stakes in Andhra Pradesh

Although the number of M&A deals in the globalinvestment banking space has been heading north, thelast quarter has witnessed a steep decline in India.However, even in a scenario marred by macro-economicuncertainties, a few high value deals have been struck.

The highs andlows of investmentbanking

When Goldman Sachs invested $500 million for a 1 percent stake in Facebook, itcreated a furore and a myth of sorts. The illusion of a $50 billion valuation forFacebook and for Goldman Sachs might augment its coffers with $60 million in

fees, 4 percent placement fee and 5 percent of any profits generated. The investmentbanking behemoth’s deal should have been just another illustration of how investmentbanking advisory is back in full force – both on the M&A and the IPO front. But the pictureis far from rosy and a frenetic M&A activity a myth.

BY SUNIT MEHRA AND AMANPREET SINGH

pg.21

the hunt reportPEOPLE MOVEMENT

Paper Mills for $257 million and Essar Oil acquiring Shell’s StanlowRefinery for $350 million. In factexperts point towards an increasedactivity in sectors such as mining,resources, energy and industrials.Aditya Birla is currently eying a $3.5billion deal for the Australian coalmine, Whitehaven Coal while TataSteel has already acquired stakes incoal mines in Mozambique andAustralia. In terms of volume, the ITand ITeS sector has witnessed themaximum number of transactions at 22. Meanwhile the iGate - ApaxPartners’ $1.21 billion acquisition of Patni was the largest deal in thissector in the past five years.

● Brooks Entwistle, Chief ExecutiveOfficer, Goldman Sachs India hasmoved out of the country to takeup the position of Chief ExecutiveOfficer of Goldman Sachs,Southeast Asia.

● Vijay Karnani, Managing Director,Goldman Sachs India has beenpromoted to the post of Co-ChiefExecutive Officer alongside Sonjoy Chatterjee.

● Nomura has elevated TarunJotwani from Chief ExecutiveOfficer, Europe, the Middle East andAfrica to Head, Global Markets andExecutive Vice President.

● Saurabh Sonthalia, Bank ofAmerica-Merrill Lynch’s Head,Global Capital Markets for India hasleft the organisation to join aprivate equity firm.

● Keshav Sanghi, Head, Equities atCitibank India has moved toGoldman Sachs’ secondary marketequities business

● ICICI Securities, Executive Director,Alagappan Murugappan is nowheading the private equity fund ofUTI AMC.

● Credit Suisse’s Vice Chairman andCo-Global Head of FinancialInstitutions Group, Vikram Gandhisteps down to pursue philanthropy.

● Anup Bagchi has been promotedas Head, ICICI Securities asMadhabi Puri Buch steppeddown.

● Boutique investment bank, EquirusCapital, roped in Vineet Toshniwalas Director to lead the I-bankingpractice areas of engineering,discrete manufacturing and services.

● Nomura has elevated Nikhil Nathfrom Head, M&A India to lead thebusiness across Asia, excludingJapan and Australia.

● BNP Paribas Securities India’sManaging Director of InstitutionalEquities Praveen Chakravarty isleaving the company to be a part ofNandan Nilekani’s UniqueIdentification Authority of India(UIDAI) project.

● Saurabh Mukerjea, who had setup the institutional equitiesbusiness for Execution Noble, hasjoined Ambit Capital as ManagingDirector and Head, Equities.

● KPMG’s Corporate Finance Head,Rohit Kapur has quit to join RajeshKhanna’s Private Equity fund Arka Capital.

● Mid-market Investment Bankingadvisory firm, Singhi Advisors,has recruited Actis Director,Girija Tripathy.

LEGAL AND SECRETARIAL

The role of the Indian CompanySecretary has become more complex.The Company Law Board isuncompromisingly stringent aboutthe accuracy of data and reportingtimelines; thus managing compliancedeadlines by “back dating” reports is athing of the past. After the InitialPublic Offer (IPO) drought of 2009,there was a relieved charge to list in2010, driven primarily by privateequity investors. Given the complexlisting regulations prescribed by SEBI,companies have been eager to hiremature company secretaries withcommercial acumen. This trend hasresulted in 30 to 50 percent increment

pressure on company secretarycompensations in the last 18 to 24 months.

More invaluable than an experiencedCS is the legal-cum-secretary head.Smaller companies, especially, find it a challenge to attract this talent yet uneconomical to keep thefunctions separate.

Large firms with an aggressiveorganic-cum-inorganic growthstrategy may benefit by hiring twodistinct experts – a legal head and acompany secretary. Usually, thereporting and compliance pressure on

As the legal and secretarial functions become morecomplex, Indian corporates are faced with an uphill taskof creating two distinct roles for company secretariesand legal experts.

Reforms sweepinglegal and secretarial functions

According to a report featured in The Times of India, there are currently 22,000qualified company secretaries (CS) in the country, and the numbers are expected torise to 50,000 by 2020 as projected by the Institute of Company Secretaries of India

(ICSI). Over the past decade, the legal and secretarial functions of corporate India haveundergone a paradigm shift. In the pre-liberalisation era, companies outsourcedsecretarial filing to a local Chartered Accountant (CA) firm or a practicing companysecretary. The growing impetus on economic reforms, establishment of SEBI in 1992 andthe leap in globalisation have resulted in a 360-degree change in the secretarial hiringneeds of Indian corporates. There is a definitive trend seen with public and private limitedcompanies (even as small as Rs 250 crore) to hire a CS than outsourcing the function. Inrecent years, especially in Rs 1,000 crore plus companies, the secretary’s team of graduateshas now been replaced with a three to four member team of qualified secretaries withtwo to three years experience.

BY SUNISHI GABHAWALA

pg.23

the hunt reportPEOPLE MOVEMENT

a CS, especially while managing agroup of companies, is high. Thecompany would be better served if it has a legal expert; keeping in viewthe complexity of work in new jointventures, pricing agreements and due diligence required in pre-global acquisitions.

The talent needs in the legal space areindustry-specific. Unlike finance orhuman resources, the legal function isless fungible. For example, a CS andlegal head from the banking industrymay be challenged to accept a lateralrole in a manufacturing organisation,which requires the knowledge ofexcise, industrial laws and factoryregulations. Certain industries,however, do find synergy in hiringfrom a dramatically different industry.For example, a patent andinfringement law expert in thepharmaceutical industry may find agood opportunity with a media or asoftware product company, where themost critical skill is IP protection.

Companies in the telecom andsoftware services domains have multi-year service level agreements whichare of high value. In such a scenario,the legal head is required to protectthe company through well structuredforex and penalty clauses, and at thesame time play the role of a businessenabler to ensure that the companyattracts and retains clients.

While there has been an upswing inthe students registering for the CScourse (the President of the ICSI has

noticed a 70 percent increase in newstudents), quality of talent will remaina challenge, given the low entry barfor the course. On the other hand,while the stringent selection processfollowed by India’s premier NationalLaw Schools ensures an excellentpipeline of good lawyers, the bestlegal minds aspire to work with theleading legal firms in the country.Corporate India will continue to face a challenge hiring good talent for this function.

● Raju Kaul has accepted the role ofDirector, Finance in Jindal Steel & Power. He was earlier Punj Lloyd’sPresident, Finance.

● Ashutosh Dhawan has joinedSTMicroelectronics as ChiefFinancial Officer. He was earlier Vice President, Finance at HCL Technologies.

● Ranjeev Lodha, General Manager,Finance at Mahindra & Mahindrahas moved to Tata Chemicals asVice President, Finance.

● Sekhar Bhattacharjee has beenappointed as Company Secretary ofTIL. Prior to this, he was CompanySecretary and Compliance Officer at Alstom India.

● Vikrant Gandhe, CompanySecretary and Compliance Officer at Tech Mahindra, has moved toSynechron Technologies asCompany Secretary and Head, Legal.

● Sanjay Dwivedi has beenappointed as Head, Finance ofNimbus Communications. He wasearlier Vice President, Finance atENIL, a Times Group company.

● Madhusudan K has quit fromPrestige Group as Group ChiefFinancial Officer, Retail to set up hisown financial advisory firm.

● Sunil Kakar was appointed asGroup Chief Financial Officer atIDFC. He was previously ChiefFinancial Officer at Max New YorkLife Insurance.

LOGISTICS

Some of the major M&A in the logisticsindustry include:● The acquisition of AFL and its affiliate

Unifreight India by FedEx.This wouldprovide AFL and UFL the access toFedEx's international network and alsoextend FedEx’s network across India.

● The acquisition of RR Enterprises byKuehne + Nagel to foray into the fastgrowing cold chain logistics.

The recent investments by private equityfirms and corporates in the logisticsindustry are indicative of the interest inthe sector and the growth of sub-sectorslike the cold chain. India Equity Partners(IEP) and Ashmore Alchemy InvestmentAdvisors invested $10 million, each, inSwastik Roadlines (a food cargo supplychain provider) and Siesta LogisticsCorporation (an integrated logisticsplayer), respectively.There are otherinstances of such investments too.Mayfield Fund and Sidbi Venture Capitalinvested $11 million in Fourcee

Infrastructure Equipments, with another$10 million coming from IEPsubsequently. Café Coffee Day hasacquired Sical Logistics to cater to itssupply chain requirements.

The growth in the energy and utilitiessectors has further bolstered the needfor specialised logistics solutions. Also, asevident from the investments, sub-sectors within the logistics industry—road transport, cold chain segments andrail transportation—have gatheredsteam.This is a result of the heightenedbusiness demand coupled with policychanges. For instance, Finance Minister,Pranab Mukherjee, in his Union Budget2011-12, announced the establishmentof 15 more mega food parks in thecountry. He has also been workingtowards encouraging states to reformlegislation pertaining to the agriculturalproduce marketing.This is a timelymeasure, considering that about 40percent of the fruit and vegetable

The logistics industry is progressing at a steady speed.With the revival of the economy and increase in spendson infrastructure projects, the sector is expected to gainfurther momentum. The growth of sub-sectors and therising number of M&As will lead to an increase in thedemand for tier-1 and tier-2 leadership talent.

M&A season in logistics

The logistics industry has witnessed a strong wave of M&As in recent times, followingan upward trend in the sector. This rise is fuelled by the revival of the economy,especially a burgeoning retail and manufacturing segment. Several factors that

fostered M&As in the sector include the need for integrated multi-modal transportnetwork and the requirement to collaborate and provide broader services.

BY ANNE PRABHU

pg.25

the hunt reportPEOPLE MOVEMENT

production in India is wasted due toinadequacies in the transportation, coldchain and storage facilities.The Budgethas even provided an ‘infrastructurestatus’to these facilities, besides themega parks.

The government has several initiativesthat have catalysed the growth of thelogistics industry in the country. Somesuch endeavours include the NationalHighways Development project,interconnecting the 12 major ports inIndia, enhancing the port handlingcapacities, developing the eastern andwestern rail freight corridor, bolsteringrail freight handling capacities andinvesting in the Delhi-MumbaiDedicated Freight Corridor.

From a talent perspective, the rise in thenumber of M&As in the industry havecreated a demand for leadership talentat the tier-2 level, who have the ability tointegrate and drive smooth businesses.

Moreover, the growth of sub-sectorswithin logistics and the fact that thesesectors are at a nascent stage havecreated the need to draw talent fromrelated sectors.

● S Ravi Kumar has joined BhartiAirtel as Chief Supply Chain Officer,South Asia Operations. He waspreviously the Vice President andBusiness Head, Southeast Asia atSamsonite Corporation.

● Vinay Kushwaha has moved toBritannia Industries as VicePresident, Supply Chain. His earlierrole was Executive Director,Operations at Dabur India.

● Avik Sanyal has joined NarangAccess (Danone Narang JV &Narang Group) as Vice President,Supply Chain and Industrial. Hewas earlier Head, SCM, NetworkDesign and Private Label at AdityaBirla Retail.

● Prasad Deshpande has relocatedfrom the US to join Biocon as Head,Supply Chain. He was previouslyworking as Director, GlobalLogistics and Supply at Pfizer,the US.

● Milind C Mandlik has beenappointed as Head of Supply Chainby Huntsman International India.Earlier, he worked as Head ofSupply Chain Centre at BayerMaterial Science.

● Juzar Mustan has started his own consulting services in supplychain for various organisations.Earlier he was Chief ExecutiveOfficer at AFL Logistics.

● Mansingh Jaswal has joinedGenEx Logistics as Director aftermoving from BLR Logistiks as Director.

● Dharmesh Dutta has moved from a subsidiary of AllCargoGlobal Logistics as Chief ExecutiveOfficer to Hanjin Logistics as Chief Executive Officer.

Source: Exim News Service, IBN Live

PHARMACEUTICALS AND HEALTHCARE

India's share in the global bulk drugmarket has grown from around 3.5 - 4 percent in 2003-04 to 6.5 - 7 percent in 2008-09. Last year,the bulk drug market in India wasestimated at $7.69 billion, growing ata CAGR of 18.5 percent during the lastfive years. It is estimated that themarket will grow to $16.91 billion by2014, at a CAGR of 21 percent. About30 percent of the bulk drugsmanufactured are for domesticconsumption and the remaining 70 percent is contributed by exports.

High growth of generics and patentexpiries, new drug development andcontract manufacturing opportunities(which is a result of cost efficiencies inmanufacturing) propels the growth ofthis industry. This trend has provided astupendous growth opportunity for

the leadership talent in thepharmaceutical manufacturing space.They can now evolve into techno-commercial profiles, and eventuallydrive independent business units.

The Indian pharmaceutical sector,with a size of $16 billion, is expectedto grow to $50 billion by 2015. Thedomestic market is expected to growto $30 billion by 2020, and willcontinue to grow at a CAGR of 14percent for the subsequent threeyears. In international markets,companies that have entered both thedeveloped and developing marketsare likely to be the prime beneficiariesof the US generics opportunity.Pharmaceutical companies havereported a sound growth in earningsin the first three quarters of FY11. Thiswas fuelled by stellar growth in

The pharmaceuticals and healthcare sector is on anunprecedented growth path, fuelled by big deals andexpansion strategy. As the sector continues to expand itsglobal market share, it will require professionals withtechno-commercial profiles eventually drivingindependent business units.

In the pink of health

The recent years have been buoyant for the pharmaceuticals and healthcare industry,in terms of performance and testimonies. This trend is reinforced by theunprecedented growth ushered in by big deals and an expansion strategy. As per

estimates, by the year end 2011, the Indian pharmaceuticals and healthcare industry willexpand its market share to over 3 percent, accounting for $25 billion of the $848 billionglobal market. The Indian market has over 650 companies, which includes about 250 bulkdrug and 450 formulation units. More than 60 percent of these companies are small andmedium enterprises.

BY YOGESH CHOPRA

pg.27

the hunt reportPEOPLE MOVEMENT

exports, expansion of market share ingeneric sales in US (Dr Reddy's) and afew M&As (Sun Pharma and Taro).

The relative cost attractiveness of theIndian pharmaceutical manufacturershas been recognised by largemultinational pharmaceuticalcompanies. However, the innumerableoutsourcing contracts gained by theIndian pharmaceutical industry areadversely impacted by the M&As inthe global pharmaceutical space. Thistrend is a result of the reduction inresearch work for Indian contractresearch and manufacturing servicesfirms. Global firms have merged theiroperations to compensate for animminent loss of revenues as theirpatents for top selling drugs expire.Thus, it unveils a huge opportunity forIndian generics. For example, Pfizer’s$60 billion buyout of Wyeth, Merck’sacquisition of Schering-Plough for $41billion and Sanofi Aventis’ $20 billionbid for Genzyme will lead to massivecost-cutting measures, especially inR&D spends.

The Indian healthcare system haswitnessed unprecedented growthover the last few years. However, it hasbeen unable to match the pace of thegrowing population in the country.The unavailability of hospital beds is a

clear indicator of this gap. Against aworld average of four beds per 1,000persons, India has only over 0.7 bedsper 1,000 people. Estimations haverevealed that about 400-500 hospitalprojects are under way in the country.Moreover, there are plans to build anequal or larger number of healthcaredelivery centres in the next few yearstoo. According to a KPMG report, thehealthcare infrastructure spend inIndia is expected to reach $14.2 billionin 2013. This reflects a 50 percentjump over the corresponding figure in2006. The steep rise in expenditure ispropelled by rising income levels,changing demographics and illnessprofiles, especially due to a shift fromchronic to lifestyle diseases.

Given such a scenario, the need forcompetent professionals to leadmultiple projects—from concept tocommissioning and validation, acrossgeographies—is on the rise. It is alsoexpected that these professionals may eventually be entrusted with the responsibility of driving the operations on completion of these projects.

● Shireesh Ambhaikar, DirectorManufacturing at UCB Pharma, hasmoved to Perrigo API as ChiefExecutive Officer.

● Anil Kamath, who was theManaging Director at WockhardtHospitals, has moved to set up hisown consulting practice.

● Dr Firdosh Gardin, GeneralManager Contracts atGlaxoSmithKline, has beenappointed as the Technical Director at Novartis.

● Chandrsekaran KN, ChiefOperating Officer at KhandelwalLaboratories, has joined Novartis asits Head, Commercial Operations.

● Anil Agarwal has accepted therole of Vice President, Operations atZydus Cadila. Earlier, he was VicePresident , Operations at Glenmark.

● Dr Vikram Raghuvanshi hasresigned from his current capacityof Chief Operating Officer atWockhardt Hospitals, to establishhis own consulting practice.

Growth rate of Pharmaceuticals Majors

Dr Reddy's Cipla Sun Lupin Cadila Auro Pharma Health Pharma

NET SALES*

Dec-09 5385.39 4255.33 2993.62 3537.78 2840.28 2650.63

Dec-10 5452.01 4648.78 4370.84 4278.45 3417.28 3227.07

% Chg 1.24 9.25 46.01 20.94 20.31 21.75

NET PROFIT*

Dec-09 -59.96 806.48 956.6 461.01 386.38 441.53

Dec-10 769.51 753.12 1418.12 635.35 532.03 438.45

% Chg -6.62 48.25 37.82 37.7 -0.7

* Trailing nine months ending December, 2010 Source: Business India

(Figures in Rs Crore)

PRIVATE EQUITY

The reality of the PE space is that ithas become a tight clique; thus everymove gets magnified. The industry’sopinion is divided on variousparameters for the ‘round robin’, butthe consensus is that, in largemeasures, it is due to the fact thatmost firms are personality-driven.Other issues include the lack ofprofessionalism at the top, seniorprofessionals driven by egotransparency over carry, lack ofimportance of the Indian office (in the case of MNC funds) and, of course,the old adage of ‘employees leave their bosses, not their jobs’always holds true.

Although such high level peoplemovement is a sign of a maturingmarket with star transactors receivingmore opportunities to exhibit theirskills, it is also a sign of caution forothers to keep the house in order.Limited Partners’ (LPs) confidence onteam stability is riding low, given thenumerous moves at the Partner andthe Managing Director level in the last18 months. With several personality-led funds present in the market andmore making their way, a keychallenge for the industry goingforward will be ‘retention’. Teams thatare able to stay together will beeventual winners.

The private equity space has witnessed an exceptionalchurn, especially at the top level. With several othersexpected to follow suit, the challenge of attracting andretaining employees is the key concern in the verticaleven as it continues to address the burgeoning issue offund raising.

Retention,the key

Welcome to the carousel! It’s where the biggies play in the private equity (PE)fairground. If PE professionals turned avant garde in 2010 with the likes of CXPartners and Multiples swinging into action, then 2011 definitely started with a

bang! The Sequoia split witnessed the quartet of founding partners—Sumir Chadha, KPBalaraj, Sandeep Singhal and SK Jain—returning to their original venture - Westbridge. Toadd to the encore, there was a significant movement at the Partner and the ManagingDirector level too. The poster boy of investment in India and founder of ChrysCapital,Ashish Dhawan announced that he will hang up his boots in 2012. Rajeev Gupta,Managing Director of Carlyle India has quit as did Jasmin Patel, Managing Director ofFidelity Growth Partners. Paddy Sinha, Managing Director of Temasek bid adieu to thecompany in order to join the newly formed Tata Opportunities Fund as did RajeshSinghal, Managing Partner of Milestone Religare. The list of such high-profile peoplemovement only gets longer.

BY SUNIT MEHRA AND AMANPREET SINGH

pg.29

the hunt reportPEOPLE MOVEMENT

Meanwhile the challenges of fundraising continue to exist. This iscompounded by the fact that thereare close to 1,600 funds in the frayseeking $660 billion worldwide. Thisrepresents a scenario of the highestnumber of managers ever present inthe market at any given point of time.The likes of Subbu Subramaniam’sMCap Fund Advisors, PR Srinivasan’sExponentia Capital, Rajesh Khanna’sArka, Nilesh Mehta’s Access IndiaAdvantage Fund and ex-ICICI trio’sPravi Capital are yet to announce thefirst close on their funds. On the flipside, Tata Opportunities Fund hasannounced its first close of $450million against a target of $1 billionwhile Everstone’s fund was over-subscribed and has managed to raise$550 million.

Exits were the theme in the fourthquarter of 2010 and November alonesaw 21 exits totalling $689 million.December witnessed the largest everexit, whereas Actis and Sequoiatogether made a $500 million profitthrough the sale of Paras Pharma.Theyear experienced 164 investment exitswith at least eight making losses.Thisrepresents an increase over five in 2009and three in 2008, but also points to anincrease in liquidity keeping the LPssatisfied. Several firms exited troubleddeals and non-performing assets. Onthe other hand, there were several big-ticket PE investments - the largestbeing $1 billion by Bain Capital andSingapore’s GIC into Hero Honda. Apaxinvested $375 million in iGate tofacilitate the Patni buyout.This is morethan double the $1.5 billion in thefourth quarter of 2010.

In the last decade, the industry hasseen dizzying heights and survivedabysmal lows; however, the PE firmshave continued to gain respect fromLPs and promoters, enabling thesector to become more than just aprovider of capital.

● Arun Prakash Korati has beenpromoted as Chief Executive Officerat Axis PE after Alok Gupta’s exit.

● Amitvikram Sharma, Partner,Milestone Religare has joined Aditya Birla PE as Investment Director.

● Andrey Purushottam, ChiefExecutive Officer, Mumbai Mantrahas moved to Helix Investments as its Executive Director.

● Cyrus Driver, Director and HeadInvestments at Helix Investmentsand Rohit Kapur, Head, CorporateFinance at KPMG have joined thenewly formed Arka Capital startedby ex-Managing Director ofWarburg, Rajesh Khanna.

● Everstone’s Executive DirectorSanjay Gujral has moved to LCapital as Managing Director.

● Girija Tripathy, Director at Actishas been appointed by SinghiAdvisors as a Director.

● Harish Gandhi, Executive Directorat Canaan Partners has joined AIF Capital.

● Rahul Khanna, Managing Directorof Clearstone Venture Partners hasmoved to Canaan Partners asManaging Director.

● Raj Chinai left SVB India CapitalPartners to join IndoUS VenturePartners as Principal.

● Ranjeet Nabha has quit from hisposition as Head India at WilburRoss to raise his own fund.

● Raul Rai, Managing Director atGeneral Atlantic Partners has joinedFidelity Growth Partners asManaging Director.

● Vibhav Parikh, Associate at TPGGrowth has moved to StanChart PEas Associate Director.

REAL ESTATE

According to Cushman & Wakefieldestimates, the hospitality domain isexpected to garner around $11 billionin investments in the near future, andthe demand for office space across thecountry is expected to peak at 240million sq ft by 2014.

The financing of property constructionhas steadily moved away from debtand towards equity. Private equityinvesting opened up in 2005, followingthe relaxation of FDI norms in theindustry by the Government of India.Domestic players like ICICI, HDFC, Kotakand IL&FS raised funds ranging from$350-700 million. Foreign names soonjoined the bandwagon. By 2006-07,Goldman Sachs, Lehman Brothers,Merrill Lynch and JP Morgan hadstarted deploying funds in India out of

their respective Asia Real Estate funds.Once the FDIs began to open up,almost every financial institution beganto flood the market with equity-based,structured finance products for retailinvestors – akin to mature markets.Now, investing in the real estate sectorspans the entire capital structure –mezzanine finance, structured finance,preferred private equity, project-basedfunding, and pure private equity withlisted and unlisted developers.

India’s high-growth real estate market became a playing field for retail investors once SEBI decided toallow the implementation of real estate mutual funds. Active asset management companies in the sector include ICICI Prudential and HDFC AMC.

Statistics indicate that the real estate sector has a brightand promising future in India. The demand for residentialand commercial spaces is on an upswing, and several bignames in the financial realm—domestic andinternational—are venturing into the housing marketwith a gamut of products and investments.

On a high rise

The real estate sector is one of India’s focal areas of development. While burgeoninghome sales have contributed significantly to the growth of the industry, thedevelopment and sale of commercial/non-residential complexes have also vastly

improved. Most property analysts predict a continuation of this trend with strongerdemands in the future. Statistics indicate that an estimated shortage of 26.53 millionhouses during the Eleventh Five Year Plan (2007-2012) combined with increasingdisposable incomes and expanding cities will ensure sustained growth in the domain forthe next decade. More availability and easier access to housing finance, and the perceivedstability in real estate as an asset class, will provide a further fillip to the sector.

BY SUNISHI GABHAWALA

pg.31

the hunt reportPEOPLE MOVEMENT

The collapse of Bear Stearns andLehman Brothers brought real estateinvesting, especially by foreign funds,to a grinding halt. Funds like CreditSuisse First Boston, Actis, UBS andGoldman Sachs have since closedshop. The year 2010 witnessed thereturn of investing in the sector; theaction is primarily with domesticfunds. Between January andSeptember 2010, 32 deals worth $1.28 billion were registered,including 13 deals in non-residentialprojects – a 50 percent increase invalue over 2009.

The last six months have seen apositive comeback as well. Red FortCapital has been visible with an Rs 200 crore equity plus convertibledebenture investment in AnsalProperties, to develop a 108 acreresidential township project inGurgaon, Haryana. The fund has alsocommitted Rs 809 core in a ParsvnathDelhi SPV.

On the divestment side, funds havefound commercial properties moresaleable. HDFC Property Ventures isselling its investment in ManyataBusiness Park—a technology exportzone—back to Embassy (thedeveloper) for Rs 490 crore. Thus, it isreturning 133 percent on a five-year-old investment. Nitesh Estates boughtback the 50 percent stake held byHDFC Property Ventures in itsBangalore mall project.

The selling side includes exits tosecondary investors as well. TataRealty acquired Peepul Tree Properties(IT/ITeS Park in Mumbai) from KotakReal Estate Fund for an enterprisevalue of Rs 525 crore. GodrejProperties bought realty firm UdhavGK-Realty from HDFC Realty for Rs 129 crore. HDFC Realty hadinvested Rs 51 crore in the companyfour years ago.

Given the rather cautious investorsentiment in the sector and depressedvaluations, funds are challenged touse the IPO route to exit. AlthoughOberoi Realty’s IPO was arguably oneof the most successful in 2010,Morgan Stanley, which invested in thedeveloper in 2007, consciouslyrefrained from diluting its investmentin the company.

● Ambar Burman, Vice President,Operations and Project at GlobalRealty Ventures, has joined RoyalPalms as General Manager.

● Madhusudhan K has steppeddown from the Chief FinancialOfficer position at Prestige Group to start his own financialadvisory firm.

● Charles Hayward has moved fromLifespace Hospitality Ventures toRE/MAX as Business Associate.

● Anandjit Sunderaj has joinedKARVY Realty as Chief ExecutiveOfficer from ICICI Ventures,where he headed Investments in Real Estate.

● Shahzad Madon has moved fromICICI Prudential AMC to RelianceADA Group to set up a fund.

● Rahul Rai has joined ICICIPrudential AMC as Head, Real Estate Investment, from SUN-ApolloReal Estate.

● Balaji Rao has left StarwoodCapital last year to set up his ownfund – India Capital Advisors.

● Ashutosh Pathare, Vice President,Corporate Strategy, has quit K Raheja Universal.

In the consumer goods industry, theraw material costs generally account forabout 40 to 50 percent of a company’sturnover.The price hike in the primaryraw materials such as sugar, wheat, milk,coffee, tea and copra is likely to make adent in the profitability of thesecompanies.The steady rise in crude oilprices has also added to the concernsover margins, as packaging costs mayshoot up.To combat this, mostcompanies have raised prices. However,due to the economies of scale the largeplayers are in a better position tocounter these challenges.

In the December quarter, the marketingand promotions spend has seen a steeprise. Apart from advertising throughmass media, the companies have alsobeen spending on ground level (below-the-line) marketing activities. It has

been estimated that the ad spends willbe in double-digit percentage of thecompanies’ net sales.

Rising inflation may cause a slowdownin consumer spending, due to whichsustaining volume growth can becomechallenging for companies.To addressthese challenges and successfullyachieve the balancing act, thecompanies may adopt strategiesfocused on efficient supply chainmanagement and vendor relationship,strong distribution network, innovativeproduct portfolio and provision ofproducts across various price points.These are some of the critical areas thatneed to be focused upon to achievesustainable success for the leadershiptalent in the consumer goods industry.However, due to the rising input costs,many local and regional players have

The FMCG industry has witnessed an upsurge in salesfuelled by increasing consumer demand. However, thesector's prime focus is on managing the price points ofproducts, which is challenged by heightened rawmaterial prices and ad spend.

Counteringpricing pressures

The FMCG sector has reported robust growth due to strong consumer demand.However, rising raw material prices and increased advertising expenditure are likelyto put pressure on margins. The sector witnessed an average of 20 percent increase

in revenue during the quarter ending December 2010, compared to the correspondingperiod a year ago. Festivals and a good winter have been the main factors strengtheningconsumer demand for the industry’s products. Since most of the companies haveselectively raised the prices of their products, the growth in revenue is likely to be drivenby a mix of volume and value.

RETAIL AND CONSUMER

BY YOGESH CHOPRA

pg.33

PEOPLE MOVEMENT

found it difficult to compete againstestablished players on the pricingplank. This has propelled severalconsumers to shift from unbrandedproducts to branded ones as the pricegap has watered down. Britanniareported a decline in profits whileHindustan Unilever recorded singledigit growth. The number for GodrejConsumer could be attributed largelyto recent acquisitions. As reported byBooz & Co, the FMCG industry isexpected to grow at a base rate of atleast 12 percent annually to become aRs 400,000 crore industry by 2020,from the current Rs 130,000 crore level. Consumer goods playersare actively pursuing inorganicgrowth opportunities to chart theirfuture path, more specifically inmarkets like India, China and Russia.Consolidation of smaller companies toimprove production and productpricing is the main factor driving therise in M&A deals. Large Indian playerssuch as Godrej, Dabur and Maricohave made multiple acquisitionsacross Asian and African markets. Andthe opportunity presented by theIndian consumer goods market hasgarnered significant interest frommost large international retailers suchas Wal-Mart, Tesco and, most recently,Carrefour. The BMI India Retail Reportfor the first quarter of 2011 forecasts

that total retail sales is expected togrow from $392.63 billion in 2011 to$674.37 billion by 2014. The keyfactors driving this estimated growthare the strong underlying economicgrowth, the population expansion, theincreasing wealth of individuals andthe rapid construction of theorganised retail infrastructure. Theexpanding middle and upper classconsumer base are expected topresent opportunities in India’s tier-2and tier-3 cities.

According to a report titled‘Expanding Opportunities for GlobalRetailers’, by AT Kearney, India's retailmarket is expected to be valued atabout $410 billion, with 5 percent ofsales coming from organised retail.Hence, the opportunity in Indiaremains vast. It also states that theretail market should continue to growrapidly to attain the $535 billion markby 2013, with 10 percent contributionfrom organised retail. The reportfurther predicts that this growth willbe reflected by the demands of a fast-growing middle class for higherquality shopping environments andstronger brands.

● Manu Anand has moved from ChiefExecutive Officer at SE Asia ofPepsiCo to Chairman and ChiefExecutive Officer, PepsiCo India.

● Rakshit Hargave has joined asManaging Director, Nivea India,moving from Chief Operating Officer,Lakme Lever.

● Sangeeta Pendurkar has moved toKellogg’s India as Managing Directorfrom Vice President, Strategy at Coca-Cola, India.

● Arvind Nair has accepted the role of Operating Partner at India EquityPartners. He was earlier Head of DLFRetail Business.

● Satendra Aggarwal has movedfrom his capacity as ExecutiveDirector, North at PepsiCo to ChiefExecutive Officer, Supermarkets atAditya Birla Retail.

● Kannan Sitaram has beenappointed as Operating Partner atIndia Equity Partners. He was ChiefOperating Officer at Dabur India.

Growth rate of FMCG Majors

ITC Hindustan Britannia Dabur GodrejUnilever Industries India Consumer

NET SALES*

Dec-09 13250.63 13345.09 2482.22 2555.75 1536.76

Dec-10 15508.26 14768.59 3096.19 2994.82 2595.81

% Chg 17.04 10.67 24.73 17.18 68.91

NET PROFIT*

Dec-09 3032.78 1620.83 135.54 367.78 247.8

Dec-10 3706.13 1736.84 102.04 421.59 366.26

% Chg 22.2 7.16 -24.72 14.63 47.8

Source: Business India

Source: Economic Times,Business India

(Figures in Rs Crore)

* Trailing nine months ending December, 2010

the hunt report

WHOLESALE BANKING AND TRADE FINANCE

We have made certain observations inthe wholesale banking sector:● Financial performance: HSBC has

registered an 82 percent rise in itspre-tax profits from Indianoperations at $679 million (Rs 3,046crore) with its prime focus on thewholesale trade finance and high-end individual banking. India hasemerged as the world's top profitcentre for StanChart Bank. Profitbefore tax of StanChart's Indianoperations touched $1.2 billion (Rs5,386 crore) in 2010 increasing by13 percent from the correspondingperiod in 2009.