the impact of ifrs adoption versus non-adoption on ... the impact of ifrs adoption versus...

TRANSCRIPT

1

The Impact of IFRS Adoption versus Non-Adoption on Corporate Disclosure

Levels in the Asian Region

Richard D. Morris*

Isabelle Susilowati*

and

Sidney J. Gray**

*University of New South Wales

** University of Sydney

July 2012

Our research was supported by the Australian Research Council‟s Discovery Projects

funding scheme (project number DP0346684).

2

The Impact of IFRS Adoption versus Non-Adoption on Corporate

Disclosure Levels in the Asian Region

Abstract

Using a unique hand-collected dataset of 262 companies from eight Asian region

countries in both 2002 and 2007, we examine whether the adoption of IFRS in four of

those countries between 2002 and 2007 improved their disclosure levels more relative

to the other four countries which did not adopt IFRS. A 441 item IFRS-based checklist

is used to measure disclosure. Disclosure levels not only differ across countries but also

on average improve over time. Countries which adopted IFRS between 2002 and 2007

improve disclosure levels more than countries that did not. The result holds after

controlling for country-level and firm-level variables known to influence disclosure

practices. While country-level and firm-level factors do influence disclosure levels,

IFRS adoption has also made a positive difference to disclosure levels in the region.

The paper contributes to the literature by showing that IFRS adoption improves

corporate disclosure in the Asian region over and above the generally upward trend in

disclosure across time.

3

The Impact of IFRS Adoption versus Non-Adoption on Corporate

Disclosure Levels in the Asian Region

Introduction

The adoption of International Financial Reporting Standards (IFRS) by many countries

in the past decade, for example by EU countries in 2005, has been an important event in

financial reporting. This paper examines whether there has been an increase in

corporate disclosure levels in Asian countries that adopted IFRS around 2005 compared

to Asian countries where domestic GAAP was still being used. We find that countries

which adopted IFRS improve corporate disclosure levels more than countries that did

not. The result holds after controlling for country-level and firm-level variables known

to influence disclosure practices and for the generally upward trend in disclosure across

time.

Poor corporate disclosure and transparency became an important issue in Asian

countries following the Financial Crisis of 1997/98. Despite subsequent regulatory

attempts to increase corporate disclosure in many Asian countries, concerns remain

about weak levels of disclosure in the region. For example, the Opacity Index study

2004 (Kurtzman, Yago, Phumiwasana, 2004) shows that to invest in the eight Asian

countries in our study would require at that time an average annual return 3.02% more

than comparable investments in the USA to compensate for additional risk created by

lack of disclosure in these countries.

IFRS are generally thought to be more comprehensive than domestic GAAP of most

countries (with the exception of US GAAP). Studies have investigated the impact of

IFRS adoption on earnings quality, on cost of capital, and on the value relevance of

profits and book value (for example, Barth, Landsman & Lang 2008; Daski, Hail, Leuz

& Verdi, 2008; Armstrong, Barth, Jagolinzer & Reidl, 2010; Horton & Serafim, 2010;

Clarkson, Hanna, Richardson & Thompson, 2011; Landsman, Maydew & Thornock,

forthcoming). However, little is known about whether IFRS adoption has led to an

increase in disclosure levels - in Asian countries or elsewhere. The likely reason is that

disclosure is not measured in computerised databases such as Compustat Global

Vantage or Worldscope, and so not readily accessible by researchers. Yet high

disclosure levels are an important component of quality financial reporting and help to

reduce information asymmetry between a firm and its stakeholders. We provide results

4

of a hand-collected 441 item IFRS-based disclosure checklist for matched samples of

256 companies from eight Asian countries in both 2002 and 2007. These countries are

Australia, China, Hong Kong, and the Philippines which adopted IFRS between those

years, and Japan, India, Singapore, and Malaysia which did not.

Ball (2006) points out that the adoption of IFRS, now in more than 100 countries,

although driven by global integration of markets, may not produce high quality

financial statements in practice because of political and legal barriers to successful

implementation at the country level. Studies show both country-level and firm-level

factors are important determinants of governance choices (including disclosures)

(Doidge, Karolyi & Stulz, 2007) and voluntary IFRS adoption (Francis, Khurana,

Martin, & Perera, 2008). Ball, Robin & Wu (2003) show that, in four Asian countries

(Hong Kong, Malaysia, Singapore & Thailand), firms report earnings which are less

timely in terms of loss recognition than earnings in some common law countries

(Australia, Canada, UK, USA) but about the same as in some code-law countries

(France, Germany, Japan). They argue that poor timeliness of earnings in the four

Asian countries is associated with factors/incentives such as the system for setting and

enforcing standards, the influence of inside stakeholders such as families and banks on

financial reporting decisions, political influences, tax incentives, and enforcement

mechanisms (Ball et al., 2003, pp241-246)1.

Our research is relevant to Ball‟s (2006) point because we examine the impact of IFRS

adoption on four Asian countries which differ in legal system and other regulatory

characteristics and we investigate whether IFRS adoption has been successful in all four

in terms of enhancing disclosure levels. We also compare disclosure levels in these

countries with a control group of four other Asian countries which, up to 2007, had not

adopted IFRS.

A separate stream of research commencing with Gray (1988) and building on the work

of Hofstede (1980) suggests that cultural factors influence corporate disclosures. In a

study covering 42 countries, Hope (2003) finds that corporate disclosures are

consistently associated with legal system type, but he also finds disclosures associated

1 Ball et al. (2003) is among a stream of papers, including Pope & Walker (1999), Ball, Kothari &

Robin (2000); Leuz, Nanda & Wysocki (2003) and Bushman, Piotroski & Smith (2004), which

investigate the influence of country-level factors, for example legal system, enforcement, and

accounting standards, on corporate accounting practices. However, only Ball et al. (2003) focuses on

Asian countries.

5

with cultural variables. He concludes that cultural differences may well be a valid

determinant of disclosures. We examine whether the cultural dimension of “secrecy”,

derived by Gray (1988) from Hofstede‟s cultural values and measured by Braun &

Rodriquez (2008), is associated with changes in disclosure in IFRS adopting Asian

countries.

Several studies have examined the determinants of disclosure in individual Asian

countries (for example, Hossain, Tan & Adams, 1994; Ho & Wong, 2001, 2002;

Hannifa & Cooke, 2002; Chau & Gray, 2002; Morris et al., 2004; Ali, 2005; Sutthachai

& Cooke, 2009; Wan-Hussin, 2009); however none examines the effect of IFRS

adoption on disclosures. Furthermore, these studies do not deal with the fact that some

firm-level determinants are influenced by country-level factors; for example, Japanese

companies tend to be larger than those from other countries in the region. These

differences in turn are driven by macro-level factors, such as, amongst many things,

economic development: as Japan‟s economy is among the largest in the Asian region, it

tends to have larger firms.

Our paper contributes to the literature in several ways. First, we provide evidence from

the Asian region about the impact of IFRS adoption on corporate disclosure levels.

Most studies of the impact of IFRS adoption focus on adoption in the EU and examine

IFRS-induced changes in earnings quality, cost of capital, value relevance of earnings,

as well as IFRS-induced changes in profitability and shareholders‟ equity. To our

knowledge, none investigates the impact of IFRS on disclosure levels.

Second, we find that, even after controlling for country-level and firm-level factors

known to impact disclosures, IFRS adoption still has a significant positive impact on

disclosures in the four Asian countries that adopted IFRS between 2002 and 2007. That

is, while consistent with Ball‟s (2006) conjecture that country-level differences matter

in explaining corporate disclosures, adoption of IFRS also has a significant positive

impact. A number of firm-level variables are also robustly associated with disclosure -

they are organisational, financing and monitoring variables which are market-driven

rather than regulation-driven.

6

Third, our disclosure measure is based on a checklist of 441 items from IFRSs in

2001/022, covering 265 companies from eight Asian countries for both 2002 and 2007.

The items contained therein cover most of the financial section of a typical company

annual report. Our data are finely detailed, hand-collected and taken from primary

sources (companies‟ annual reports) rather than from computerised databases. Other

studies of corporate disclosure across Asian countries use limited and/or more dated

measures of disclosure, and are thus noisy indicators of transparency. For example, the

CIFAR Disclosure Scores, now very outdated, cover only 85 disclosure items in 1991

and 1993, albeit for about 1000 companies from 42 countries (CIFAR, 1995; Hope,

2003, p.266); the Standard & Poor‟s Transparency and Disclosure Survey (2001)

covers 98 items of which only 35 are about financial transparency and disclosure in

annual reports; and the CLSA (2001) corporate governance survey, which covers 495

firms from 25 countries, includes only 10 items on financial disclosure. Most cross-

country studies3 of accounting practices utilise the availability of such computerised

databases. None of these databases allows a researcher to investigate the adoption of

IFRS.

Fourth, the CLSA (2001) and Standard & Poor‟s (2001) data examine large numbers of

companies across many countries but have relatively few firms per country. The CLSA

(2001) data has an average of 15 firms per country. The Standard & Poor‟s (2001) data

for Asian countries has an average of 26 firms per country, and is dominated by one

country, Japan, with 130 firms. While our study examines a smaller number of

countries (eight), we collect more disclosure items (441 per firm) from each firm from

more firms per country.

Fifth, our paper complements and extends studies, mentioned above, that have

examined the determinants of disclosure in individual Asian countries before IFRS

adoption.

2 2002 was the latest year available when we began this project. As far as we are aware, our data set is

the largest collection of finely detailed disclosure information on Asian countries. 3 They include papers which have examined: (a) the value relevance of financial statements in different

countries (Hung, 2001); (b) earnings management (Leuz et al., 2003); (c) conservatism of accounting

income (Ball et al., 2003); (d) the price of earnings opacity (Bhattacharya et al., 2003); (e) the impact of

disclosure levels on cost of capital (Francis et al., 2005), (f) determinants of the voluntary adoption of

IASs (Barth et al., 2005); (g) disclosure and emerging market companies‟ access to capital in global

equity markets (Frost, Gordon & Pownall, 2005).

7

Our paper is organised as follows. The next section provides the hypothesis

development, followed by a section on research methodology, sample selection and

measurement. Our results are presented next, followed by discussion and conclusions.

Hypothesis development

The Impact of IFRS Adoption on Disclosure

From humble beginnings in 1973, through a series of reforms including the

Comparability and Improvements Project (1989-1993) and the “core standards” project

(Schweikart, Gray & Salter, 1996, p.113), IFRSs and their predecessors International

Accounting Standards (IASs) have become since the early 2000s a serious challenge to

US GAAP. In 2005, over 100 countries had adopted IFRS including countries of the

EU. In Asia, IFRS was adopted for all companies by the Philippines, Australia and

Hong Kong in 2005 and by China and New Zealand4 in 2007.

Adoption of IFRS did not happen in the same way for each of these countries, but for

our purposes it was complete by 2007. In the Philippines, a gradual adoption of

IAS/IFRS had been underway from 2001, but was complete in 2005 (IASPlus,

Philippines, January and November 2005 updates). In Australia, despite a process of

convergence of domestic GAAP with IFRS, many differences still remained between

Australian GAAP and IFRS in 2005 when the final changeover occurred. IFRS were

fully converged with Hong Kong standards in 2005 (IASPlus, Hong Kong, January

2005 update). In China, adoption of IFRS in 2007 was for listed companies only and

contained “certain modifications that reflect China's unique circumstances and

environment” (IASPlus, China, April 2006 update).

By contrast, domestic GAAP in our other four countries still remains different to IFRS.

Singaporean GAAP will not be fully converged with IFRS until 2012 (IASPlus,

Singapore, May 2009 update). Japan in 2011 deferred mandatory IFRS adoption but

permitted some companies to adopt IFRS voluntarily (IASPlus Japan, June 2011

update). Malaysia finalised IFRS-compliant standards only in November 2011

(IASPlus, Malaysia, June and November 2011 updates). In 2011, India issued 35 new

4 We do not cover New Zealand in our study because of its close similarity to Australia. However, one

New Zealand company, NZ Telecom, is included in the Australian sample because it is listed on the

Australian Stock Exchange.

8

standards which were converged with IFRS but still contained significant differences

from IFRS (IASPlus, India, February 2011 update).

Our focus is on IFRS disclosure rules. These are very extensive, much more than

countries‟ domestic GAAP. In our eight countries, the proportion of our IFRS-based

disclosure checklist (discussed later) also contained in countries‟ domestic GAAP in

2002 ranges from .43 (China) to .88 (Singapore) with five countries in the range .68 to

.74 (Table 1, panel A). All else equal, we expect that the adoption of IFRS will lead to

an increase in disclosure levels. Our primary hypothesis therefore is:

H1: Countries in the Asian region adopting IFRS will improve their disclosure levels

more relative to countries not adopting IFRS.

Country-level controls

As mentioned, Ball (2006) conjectures that the success of IFRS adoption will be

dependent on the basic financial regulatory infrastructure of the adopting country.

Therefore, in testing H1, country-level regulatory factors must be controlled for. Many

regulatory infrastructure mechanisms could be chosen, but we select a small number

which have good empirical grounding in the recent accounting literature, and have some

plausible, proximal associations with corporate disclosure.

Country legal system. The works of LaPorta et al., (1998, 1999) have had an important

influence on empirical research into cross-country differences in accounting standards

and practices. They show that countries with English common law legal systems

tended to have better economic development, stronger capital markets, better

accounting standards and better enforcement than countries with code law legal

systems. The distinction between common-law and code law countries, and differences

in enforcement and economic development have been used as country-level

determinants in many recent accounting studies, using either the LaPorta et al. data or

more recent measures, for example Ball et al. (2003).

La Porta et al. (1998, tables 5 & 6) show that countries with English common law

systems have significantly better quality accounting standards than countries with

German-origin legal systems, these countries in turn having significantly better quality

accounting standards than countries with French-origin legal systems. For a series of

enforcement mechanisms, La Porta et al. also found that civil law countries are

9

significantly weaker than English common law countries. Since disclosure practices

(not examined by La Porta et al.) will be influenced by both the quality of accounting

standards and their enforcement, our first control proposition is that:

Control proposition 1: Disclosure levels in countries with common law legal systems

will be higher than those in countries that have code law legal systems

Country legal system has the advantage of likely being an exogenous factor, given that

legal systems have been in place for very long periods, often from countries‟ colonial

days – for instance, all English common law countries in our sample were once British

colonies. However, legal system by itself is unlikely to be a sufficient condition for

corporate disclosure. Therefore, related but more proximal influences must also be

explored.

Enforcement. Based on the aforementioned evidence of La Porta et al. (1998), the first

of these more proximal factors is enforcement of laws. Where enforcement is strong,

mandatory disclosure rules ensure better access to basic financial information. Where

enforcement is weak, the mere adoption of IFRS by a country is one vital step towards

improved transparency, but it is not a sufficient condition (Ball, 2006). Domestic

standards, in some cases identical to IFRSs, coupled with comparatively weak

enforcement mechanisms, are found in some Asian countries (Ball et al. 2003).

Accordingly our second control proposition is that:

Control proposition 2: Corporate disclosure levels will be higher in countries where

enforcement of rules is stronger.

Other studies use compilations of data from La Porta et al. (1998) to construct

enforcement indexes (such as Francis et. al. 2005; Bhat, Hope & Kang, 2006).

However, La Porta et al. did not cover China, so that approach is not available to us.

Instead we measure enforcement using the Rule of Law variable, averaged for 2002 and

2007, from Kaufman, Kraay & Mastruzzi (2003). Rule of Law measures the extent to

which citizens of a country have confidence in and abide by that country‟s laws

(Kaufman et al., 2003, p. 4).

Similarity of local standards to IFRS. Another proximal variable to control for is the

closeness of domestic GAAP to IFRS before the adoption of IFRS. Countries whose

10

domestic GAAP in 2002 was closer to IFRS should have disclosure levels closer to

IFRS and thus increase less after IFRS was adopted.

Control proposition 3: Corporate disclosure levels will be influenced by the closeness

of domestic GAAP to IFRS

National culture The cultural dimensions of uncertainty avoidance, power distance,

individualism and masculinity derived by Hofstede (1980) and Hofstede & Hofstede

(2005) were applied to accounting values and accounting practices by Gray (1988), and

have since produced a stream of analytical and empirical papers in international

accounting. Uncertainty avoidance measures the extent to which a society tolerates

ambiguity and uncertainty. Power distance measures how a society handles inequality

among its members. Individualism measures the importance of individuals versus

groups in society. Masculinity measures the extent to which masculine-type attitudes

are preferred over feminine-type attitudes in a society.

Using Hofstede‟s cultural dimensions, Gray (1988) developed the four accounting value

dimensions of statutory control versus professional regulation of accounting, uniformity

versus flexibility of accounting rules, conservatism versus optimism in accounting

measurement, and transparency versus secrecy in accounting disclosures. The last of

these dimensions – transparency versus secrecy - is of relevance to our disclosure study.

Gray (1988, p. 11) argued: “the higher a country ranks in terms of uncertainty

avoidance and power distance and the lower it ranks in terms of individualism and

masculinity, then the more likely it is to rank highly in terms of secrecy.” Therefore we

expect firms from such countries to have poorer financial reporting transparency. Put

another way, firms will likely have higher disclosure levels if they come from countries

with low uncertainty avoidance, low power distance, high individualism and/or high

masculinity cultural scores. Accordingly, we expect that:

Control proposition 4: Corporate disclosure levels will be higher in countries with a

lower secrecy orientation

We use the Secrecy measure provided by Braun & Rodriquez (2008), which is a

mathematical combination of Hofstede‟s four cultural dimensions of uncertainty

avoidance, power distance, individualism and masculinity. Broadly speaking, for each

Hofstede cultural dimension, Braun & Rodriquez (2008) calculate the difference

11

between each country‟s score and the mean score across 56 countries for that

dimension. Each country then has “difference” scores for uncertainty avoidance, power

distance, individualism and masculinity. The secrecy score for each country is the sum

of its “difference” scores for uncertainty avoidance and power distance minus its

“difference” scores for individualism and masculinity. The resultant secrecy score thus

makes use of all four Hofstede cultural dimensions and is influenced by the country‟s

relative position above or below the mean on each cultural dimension.

Firm-level controls

No single theory addresses all the incentives for firms‟ disclosures. Instead the problem

has been examined from several theoretical perspectives including agency theory

(Jensen & Meckling, 1976; Watts & Zimmerman, 1986); signalling theory (Spence,

1973) and related benefit-cost analyses (Verrecchia, 1983, 1990). However, these

perspectives are consistent conceptually5 so all may be used in hypothesis development.

At their core, our firm-level hypotheses are based on the relationship between those

who control the firm on the one hand, and its external suppliers of equity or debt

finance on the other.

The separation between outside owners and inside managers of companies creates

agency costs (Jensen & Meckling, 1976). In the USA, separation between management

and shareholders is common in listed companies (Berle & Means, 1932). However in

Asian countries, family/insider control of companies is common (La Porta et al., 1999,

Claessens, Djankov & Lang, 2000), so that the key agency problems are those between

inside shareholders and outside shareholders. These agency problems include the

transfer of wealth away from outside shareholders to insiders, a phenomenon known as

“tunnelling” (Johnson, La Porta, Lopez-de-Silanes & Shleifer, 2000). Nobes (1998)

characterises countries where insider ownership predominates as insider dominant

countries. The larger the holdings of inside shareholders, the less likely will public

disclosure of information occur because insiders have access to information internally

and may also wish to hide any tunnelling activities from outsiders. La Porta et al.‟s

(1998) study shows that there is a strong negative correlation between the extent and

effectiveness of investor protection laws and ownership concentration. They find that

5 Morris (1987) shows that agency and signalling theories are consistent conceptually, in the sense that

if one is correct, the other may also be correct. They may thus be used together in hypothesis

development.

12

emerging markets tend to have relatively poor investor protection laws (bad laws per se,

or good laws poorly enforced) and high ownership concentration, particularly among

East Asian firms. Thus inside control at the firm level could be associated with poor

rule enforcement at the country level.

Conversely, the larger the cumulative holdings of small outside shareholders, the

greater their demand for information and the more likely the company is to supply it, all

else equal. Nobes (1998) characterises countries where outside shareholders

predominate as outsider dominant countries.

Companies that have recently raised equity or debt finance, at home or abroad, are also

likely to face pressures for increased disclosure, as is shown by the empirical evidence

(for example, Firth, 1980; Meek, Roberts & Gray, 1995). Similarly, the

multinationality of companies (which we proxy by whether they have international

sales) will influence disclosure as a way for firms to provide information to current and

potential customers or investors without local domestic knowledge of such firms (Jaggi

& Low, 2000). Similarly, companies which rely extensively on debt financing from

external sources face an information asymmetry problem with their lenders. Therefore,

all else equal, there should be a positive association between disclosure and leverage.

Signalling theory (Spence, 1973), by which high quality firms take costly-to-copy

actions that signal their superior quality to the market, is a theory consistent with

reducing agency costs (Morris, 1987). Disclosures are one such costly signal.

Signalling costs include direct preparation costs, proprietary costs and, in some cases,

political costs, as well as the cost incurred if the signal is false. Quality can be equated

with profitability and larger firm size. More profitable firms will disclose more so that

investors can assess better the credibility of their reported earnings. For example,

Miller (2002) reports that US firms with increases in earnings also increase their

voluntary disclosures. Larger firms are expected to disclose more because they are

usually more successful and wish to convey that information to the market. Also, larger

firms, having more market power, might disclose more because, compared to smaller

firms, they are less likely to face competitive losses (Hossain, Perera & Rahman, 1995).

Larger firms may also disclose more because they have the accounting expertise to do

so. Of course, larger firms might simply have more to disclose than smaller firms. An

example is firm complexity: all else equal, a company which operates in many different

13

businesses has more to tell the market than one which operates in only one line of

business. Therefore we expect more diversified firms to be more transparent than less

diversified firms. Research has consistently found that larger firms disclose more than

smaller firms (Foster, 1986; Chow & Wong-Boren, 1987; Meek, Roberts, & Gray,

1995; Hossain, Perera & Rahman, 1995); but the evidence on the association between

disclosure and profitability and business complexity is mixed and inconclusive.

A company‟s choice of audit firm can also act as a signal of quality (Bar-Yosef &

Livnat, 1984). Larger audit firms, as typified by the now Big 4, are usually perceived to

be of higher quality than smaller audit firms (DeAngelo, 1981; Chow & Wong-Boren

1987; Hossain et al., 1995). Larger auditors have incentives to ensure that client

companies comply with accounting standards. Therefore the presence of a Big 4

auditor should be associated with better disclosure. Street & Gray (2001) show that

companies claiming to comply with IFRSs in 1999 did so more comprehensively if they

were audited by a large audit firm. In like fashion, the adoption of firm-level corporate

governance mechanisms can act as a signal of quality. Such mechanisms are aimed at

protecting outside shareholders. Therefore, we expect that internal corporate

governance mechanisms will be associated with more disclosures, all else equal.

In summary, our fifth control proposition is that:

Control Proposition 5 Companies will have higher disclosure levels if they:

(a) have more outside shareholders;

(b) have fewer inside controlling shareholdings;

(c) have recently raised equity or debt finance;

(d) have international sales

(e) are larger;

(f) have more business segments;

(g) are more profitable;

(h) employ a Big-4 auditor; and/or

(i) have more internal corporate governance mechanisms.

Research Methodology

Sample Selection

Selection of countries. We focus on eight major Asian countries - Australia, China,

Hong Kong, and the Philippines which adopted IFRS between 2002 and 2007, and

India, Japan, Malaysia, and Singapore which did not. These eight countries vary in

legal system, rule enforcement, and level of secrecy (exhibit 1, panel A and table 1,

14

panel A). In 2002, all were in the top half of 32 countries in the region as measured by

GDP per capita6 and arguably they are among the important countries in the region in

terms of international investor interest. These countries were also chosen for the

practical reason that we were able to obtain annual reports of listed public companies

residing therein from corporate websites or publicly available databases (exhibit 1,

panel B).

Australia, Hong Kong, India, Malaysia and Singapore have English common law legal

systems, reflecting their English colonial histories; the Philippines have a French civil

law system, while Japan and China have German civil law systems. For enforcement

we use the Rule of Law measure in Kaufman, Kraay & Mastruzzi (2008) averaged for

2002 and 2007.

The four non-IFRS adopting countries are included to control for general economic

changes across the region and to allow for the fact that disclosure levels might have a

tendency to increase across time, as companies grow bigger and have more to disclose,

even if IFRS were not adopted.

Selection of companies. Using Stock Exchange Fact Books, newspaper share lists and

stock exchange websites, those companies from the largest 50 listed public companies

by market capitalisation in 2002 that survived to 2007 were identified in each country,

after excluding banks, financial institutions and insurance companies (SIC codes 6000-

6999) due to their special regulatory requirements. Also excluded were companies

which, although listed on the Stock Exchange of one country, were incorporated and

headquartered in a different country7 The year 2007 was chosen because it covered the

adoption of IFRS in our four Asian countries, because it maximised the availability of

annual reports on Mergent Online during the data collection process, and because it has

the advantage of not being influenced by the impact of the Global Financial Crisis of

2008.

[INSERT TABLE 1 HERE]

6 GDP per capita in purchasing power parity dollars (IMF 2009:

http://www.imf.org/external/pubs/ft/weo/2009/01). 7 This exclusion rule applies particularly to Singapore where nine companies among the top 50 are

incorporated and headquartered in other countries and are thus subject to the accounting standards of

those other countries. Several Hong Kong companies incorporated in Bermuda have been retained in

the sample because they are headquartered in Hong Kong and adopt Hong Kong accounting standards.

As mentioned, an exception is that we retained New Zealand Telecom in our Australian sample even

though it is a New Zealand company. It adopted IFRS in 2007.

15

Companies‟ annual reports for 2002 and 2007 in English were obtained from sources

listed in exhibit 1, panel B. All data are hand-collected. Data validity and integrity

checks carried out are reported in the appendix.

The final sample size is 530 (265 x 2) companies but the number varies across countries

(table 2) due to non-availability of annual reports in English of some companies.

Country-and firm-level descriptive statistics appear in table 1, panel B. There are

significant differences in 2002 between IFRS adopting countries and non-IFRS

adopting countries for legal system, rule of law and secrecy, with IFRS adopting

countries being higher on legal system but lower on rule of law and secrecy. There are

also significant differences in 2002 across these country groups for SIZE, KREQUITY

AUDITOR, IDIR, and AC as well as SSH, FCTL3 and DISC. Changes from 2002 to

2007 in firm-level descriptive statistics appear in table 1 panel C. They show that SIZE,

ROR, IDIR, AC and TOPSH all significantly increased between 2002 and 2007 while

KRDEBT significantly decreased.

Disclosure Measure

Companies‟ annual reports were compared with an IFRS-based disclosure checklist.

Such a benchmark is suitable given the nature of the study. As mentioned, table 1 panel

A shows that the proportion of IFRS contained in domestic standards for our sample of

countries ranged in 2002 from 0.43 (China) and 0.62 (Philippines) to 0.88 (Singapore)

with the other five countries in the range .68 to .74. However, the difference between

IFRS adopting countries as a group versus non-adopters is insignificant (table 1, panel

B).

We began with a checklist developed by Deloitte Touche Tohmatsu (2001) divided into

twelve sections, namely General Principles of Presentation, Income Statement, Balance

Sheet, Statement of Changes in Equity, Cash Flow Statements, Accounting Policies,

Explanatory Notes, Disclosures by Banks & Financial Institutions, Disclosure of

Information Reflecting the Effects of Changing Prices, Disclosure for Enterprises

Reporting in the Currency of a Hyperinflationary Economy and Disclosures of

Agricultural Activities. We removed items that could not reasonably be found by

reading an annual report and items which would not be applicable to all companies in

16

our sample (see appendix). Our resulting checklist has 441 items.8. The checklist does

not cover any IFRS introduced after 2002, but the number of such standards is very

small relative to those that the checklist does cover. We also need a checklist that would

be relevant in both 2002 and 2007 to provide a constant benchmark. All annual reports

for 2007 are in English, even from countries like China, Japan and the Philippines

where English is not the main language, while those for 2002 are mainly but not

exclusively in English. That creates a bias as such companies likely are more

internationally oriented and may have better disclosure levels anyway. However, the

bias applies both to IFRS adopting countries (Philippines and China) and to non-IFRS

adopting countries (Japan). Also, the bias is counteracted by our coding conventions

which bias disclosure scores downwards. Jeanjean, Lesage and Stolowy (2010) show

that companies with English language annual reports from non-English speaking

countries are more likely to be larger, internationally oriented, US-listed and to need

external financing. We control for most of those possibilities in our regressions.

The Treatment of Non-Disclosures

In coding the checklist, a decision had to be made about the treatment of undisclosed

items. Non-disclosure can occur for several reasons. First, a company may deliberately

refuse to disclose an item. Second, it may disclose something but not everything about

the item9. Third, the item may actually not be applicable to the company. Fourth, the

item may be too small (not material) to warrant disclosure. With only annual reports to

go by, these possibilities are difficult to tease apart.

As well as choosing checklist items that arguably would be applicable to all or most

companies, two additional approaches could be adopted to deal with non-disclosures: (i)

remove undisclosed items deemed not-applicable to the firm; (ii) treat all undisclosed

items as “applicable” and leave them in the firm‟s disclosure score calculation. Each

approach has its own strengths and weaknesses. In the first approach, if a company has

320 of the 441 checklist-items applicable to it and discloses 180 of these 320 items, its

disclosure score will be 180/320 = 0.563. The number of “applicable” items will vary

8 Studies which used a disclosure checklist have items that range in number from 30 (Wallace and

Naser, 1995) to 224 (Cooke, 1989). 9 Selective disclosure can create distortions. For example, in the case of segment reporting, suppose

company A has one segment and discloses information about it; while company B has five segments but

only discloses information about three. B appears to disclose more than A, but, relative to their

respective disclosure opportunities, A has disclosed more (Botosan, 1997).

17

across firms. If coding were error-free, this is a good approach because firms are not

penalised for having non-applicable items. However, errors can be made in deciding if

undisclosed items are applicable or not, and the chance of judgement errors increases

with the number of coders. We rejected this approach because of the large number of

coders employed in the study (see appendix).

Treating all undisclosed items as “applicable” means that each company will be given a

score out of 441. Companies trying to hide information will be rightly penalised, but

good disclosers could be wrongly penalised. The disclosure scores of many firms are

thus biased downwards using this conservative approach. The downward bias helps to

counteract the above-mentioned upward bias caused by our sample comprising mainly

companies with English-language annual reports. Other advantages of the conservative

coding strategy are objectivity and reduced need for judgement, important matters for

us because many people contributed to coding our dataset; and all firms are measured

against a common benchmark of 441 items in both 2002 and 2007. Choosing larger

companies in each country makes it likely that more items in the IFRS checklist will be

applicable to sample members. Also, the difference-in-difference methodology,

covered later, which focuses on changes across time, reduces the impact of differing

disclosure opportunities. Other surveys of transparency such as Standard & Poor‟s

Transparency and Disclosure Study 2001/02 code conservatively (items either disclosed

or not) with a restricted number of checklist items. So we adopted this conservative

coding approach.

To sum up, the disclosure score (hereafter DISC) was calculated as follows:

TOTM

aijDISC

Where: aij is company i‟s score (0 or 1) on the jth

item in the checklist;

TOTM is the maximum possible score of 441 for DISC

All disclosure scores are unweighted. The reason is to eliminate any bias inherent in a

weighted score (Chow & Wong-Boren, 1987) which may reflect the importance of

items to a specific group of information users (Chau & Gray, 2002). We are not

focusing on any specific user group here. The unweighted method has been used in

many studies (Cooke, 1989; Chau & Gray, 2002; Morris, et al 2004).

Results

18

Descriptive statistics for DISC appear in table 2, as do country means. There are

significant differences in DISC across countries in both 2002 and 2007, as shown by the

one-way ANOVA F statistics, and all countries show significant increases between

2002 and 2007. Three IFRS-adopting countries (Australia, China and the Philippines)

have the largest of these increases.

Table 3 shows Pearson correlations between DISC and country-level variables. DISC is

significantly positively correlated with IFRS, legal system, rule of law and closeness of

local standards to IFRS in 2002, but is not significantly correlated with secrecy.

Correlations between DISC and firm level variables appear in table 4 panel A for 2002

and panel B for 2007. In both years, DISC is significantly positively correlated with

BSEG, ISALDum, KREQUITY, IDIR, and AC, with AUDITOR in 2002 only, and is

significantly negatively correlated with SSH in both years.

While some country level (table 3) and firm level (table 4) variables are themselves

significantly correlated, none is correlated high enough to raise concerns about

multicollinearity (Field, 2005, pp.174-175; Cohen et al., 2003, pp.424-425).

Multivariate results

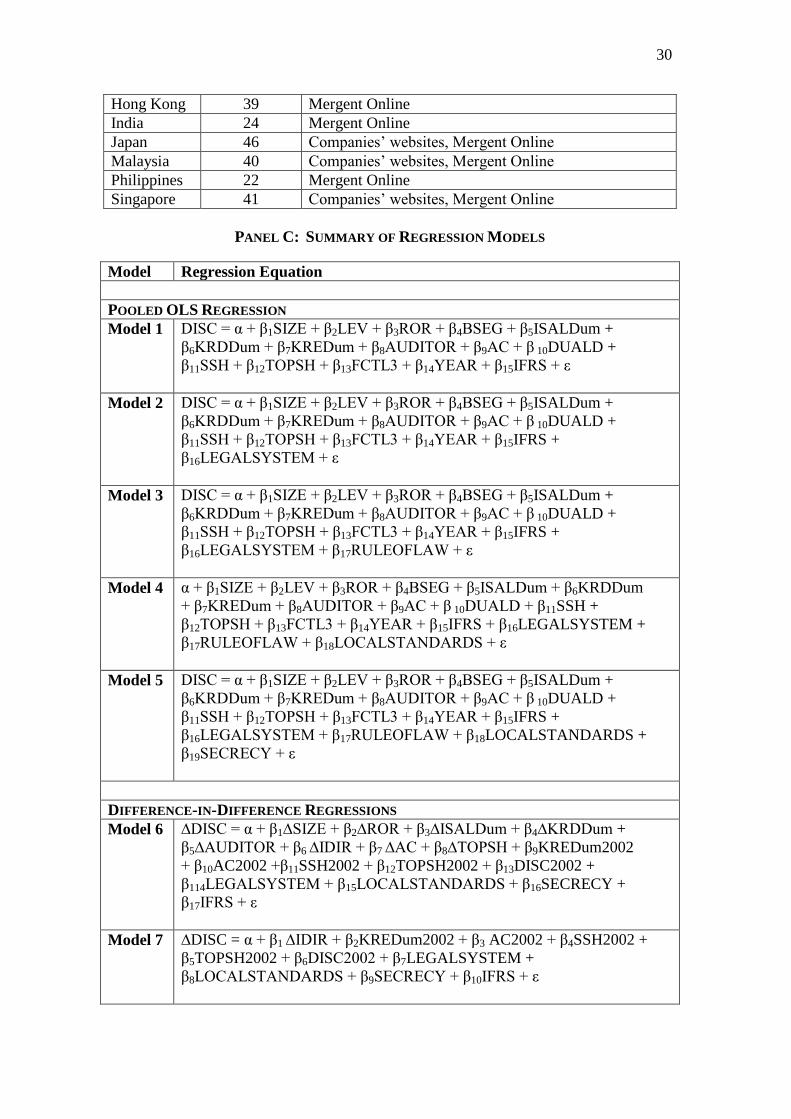

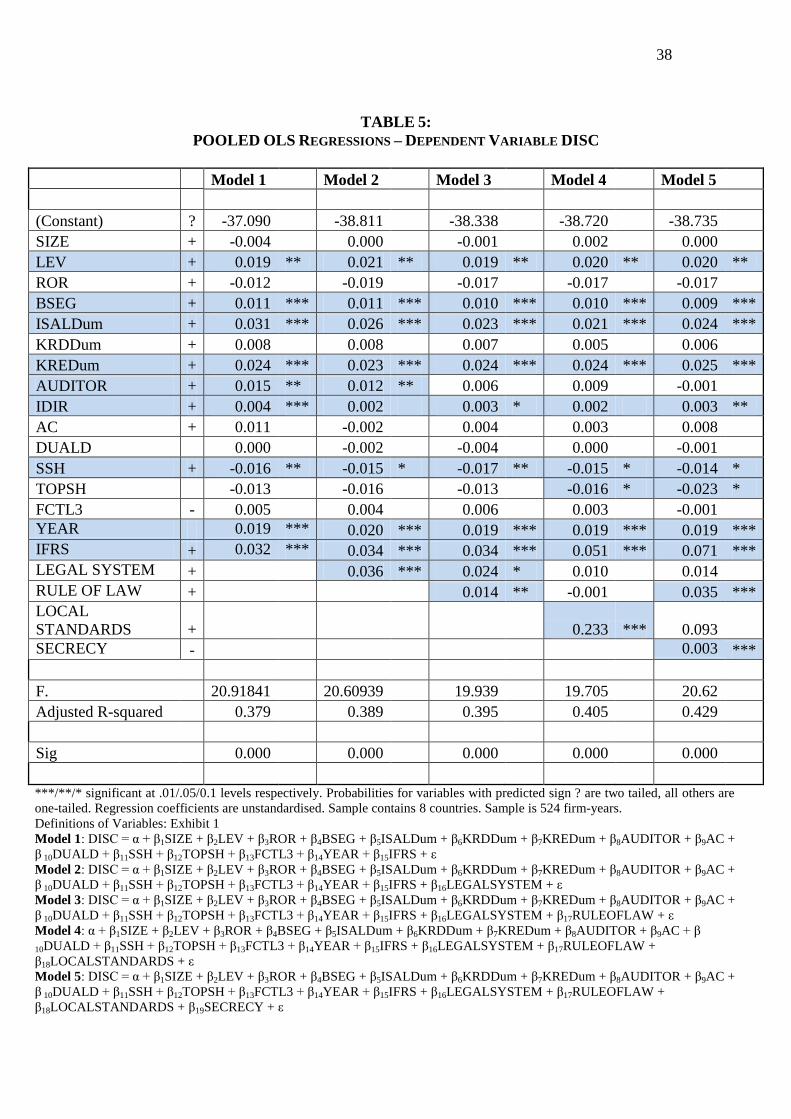

Pooled Cross-Sectional Regressions. Table 5 shows OLS pooled regressions of DISC

on company-level control variables; YEAR, a binary variable for 2002 & 2007; and

IFRS equal to 1 for countries that adopted IFRS between 2002 and 2007, zero otherwise

(model 1). YEAR controls for any upward time trend in disclosure due to increases in

firm and/or country size or profitability. Country-level control variables are then added

one-at-a-time in models 2-510

. Model 2 adds Legal System to model 1, model 3 adds

Rule of Law to model 2, model 4 adds Local Standards to model 3 and model 5 ads

Secrecy to model 4. A summary of the regression models and definitions of all

variables can be found in Exhibit 1 (panels A and C). The regression specifications are

also summarised at the foot of table 5. In all models, the Variance Inflation Factors

(VIFs) are less than 10.0, reducing concerns about multicollinearity (Field, 2005, p175).

10

Country fixed effects are not included in any model because of multicollinearity problems when they

are combined with IFRS.

19

In all five models, IFRS is positive and significant as predicted by Hypothesis 1. This

indicates that, even after controlling for a number of country-level and firm-level

variables known to influence disclosure, adoption of IFRS has a significant positive

impact on disclosure in the countries covered. The result appears to be robust, but is

probed further in the Difference-in-Difference regressions shortly.

Of the country-level control variables, legal system is positive in all models but

significant in models 2 and 3 only. This is understandable given that the top four

countries for DISC in 2002 and three of the top four for DISC in 2007 all have English

common law legal systems. Rule of Law is positive and significant in models 3 and 5

only, as are Local Standards in model 4 and Secrecy, contrary to expectation, in model

5.

Among the firm-level controls, leverage, BSEG, ISALDUM, KREQUITY, and IDIR

are positive and significant in all five models while, contrary to expectation, SSH is

negative and significant in all models.

The YEAR binary variable is significant and positive in all models, indicating an

upward trend in disclosure across 2002 and 2007, consistent with table 2.

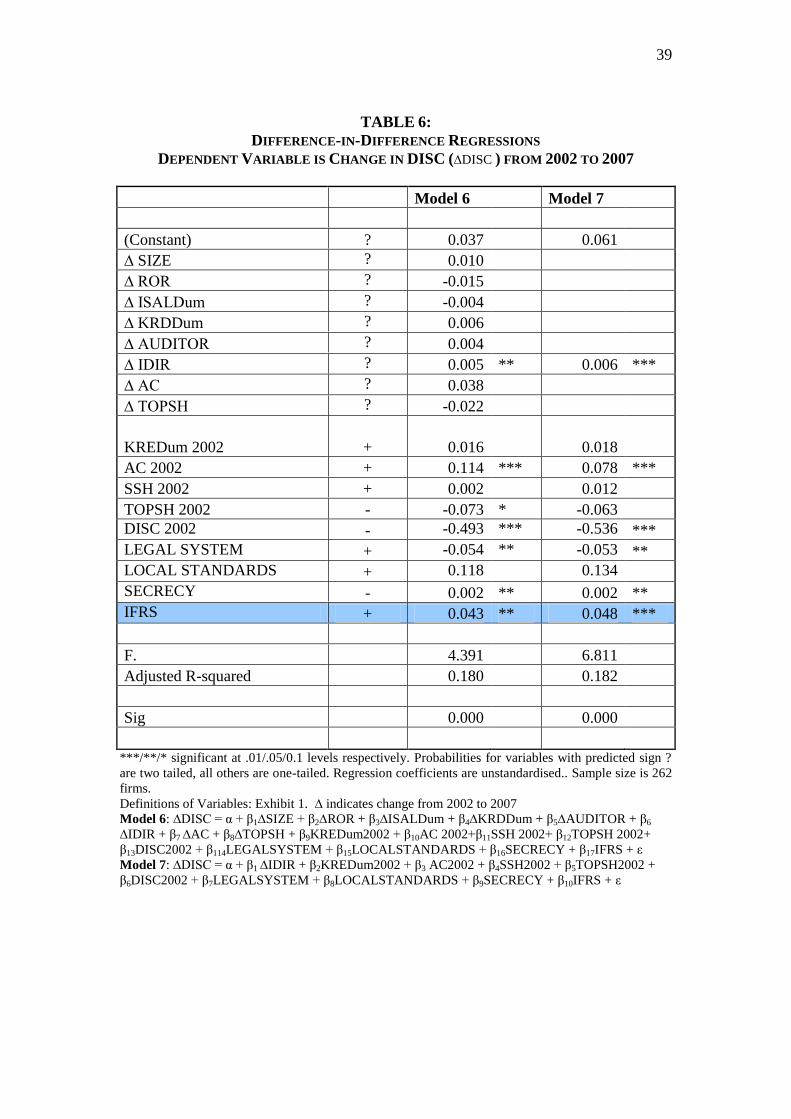

Difference-in-Difference Regressions. The pooled cross-sectional regressions in table

5 treat each firm-year as an independent observation and do not consider that each firm

in the sample appears in 2002 and 2007. Thus the possibility of using each firm as its

own control over time is ignored. Nor do the pooled regressions control for omitted

variables such as industry which are unchanged across time but vary across firms. To

more powerfully probe the impact of IFRS on disclosure, we ran a Difference-in-

Difference regression (table 6, model 6) which regresses Change in DISC 2002-2007

(∆DISC) on changes in those control variables that did significantly change from 2002 to

2007, as shown in table 1 panel B, and those control variables that significantly differed

in 2002 between IFRS adopting countries (as a group) and non-adopting countries (as a

group), as shown in table 1 panel C. Variables which changed significantly from 2002

to 2007 (table 1 panel B) are SIZE, ROR, ISALDum, KRDEBT, AUDITOR, IDIR, AC

and TOPSH. Variables which varied significantly in 2002 across IFRS vs non-IFRS

adopting countries are DISC, KREQUITY, SSH, TOPSH, Legal System, Local

Standards and Secrecy.

20

The DiD methodology treats each firm as its own control thus removing the effect of

firm level factors that do not change over time. However, control variables that

significantly vary across firms in 2002 or which significantly change from 2002 to 2007

are retained in the regression. That is necessary because the DiD methodology has a

parallel trend assumption, namely that the treatment group (IFRS adopting countries)

and the control group (IFRS non-adopting countries) should be reasonably similar

before the „treatment‟ event occurs. The parallel trend assumption also assumes that the

impact on disclosure of any other factors in the two groups in 2002 and between 2002

& 2007 should be reasonably similar. These conditions are not met in our case, and

require the control variables shown in table 6, model 6. Model 7 in table 6 repeats

model 6 but removes control change variables which are not statistically significant in

model 6. A summary of the regression models and definitions of all variables can be

found in Exhibit 1 (panels A and C). The regression specifications are also summarised

at the foot of table 6.

Models 6 and 7 show that IFRS is significant and positive, indicating support for

Hypothesis 1 using the more powerful DiD methodology. Change in DISC 2002- 2007

(∆DISC) is significantly greater in IFRS adopting Asian countries than in IFRS non-

adopting Asian countries.

Only one control change variable – ∆ IDIR – is significant. Of the control variables for

2002, DISC is significant and negative, indicating that firms with higher changes in

DISC tend to have lower DISCs in 2002. Firms with larger changes in DISC also tend

to come from code law countries as shown by the significant negative coefficient on

legal System and from countries with a higher Secrecy scores. That is consistent with

the descriptive statistics in table 2 which shows that the Philippines and China have the

highest changes in DISC 2002-2007, followed by Australia. Firms with larger changes

in DISC also tend in 2002 to have lower TOPSH values and to have an audit committee.

Discussion and Conclusions

We have examined the extent to which disclosure levels increased in four Asian

countries that adopted IFRS between 2002 and 2007, relative to disclosure levels in four

other Asian countries which did not adopt IFRS by 2007. Disclosure is measured by a

441 item checklist, conservatively coded, based on IFRS in 2001. Our central finding is

that firms in IFRS adopting countries significantly increased their disclosure levels as

21

hypothesised, even after controlling for country-level and firm-level variables known

from the literature to influence disclosure. The result is robust across several pooled

cross-sectional regression specifications as well as in Difference-in-Difference

regressions.

It might be thought that our main result occurs because our companies from the

Philippines and China (which have the highest average change scores for DISC in table

2) prepare their annual reports in English and thus have upwardly biased DISC scores.

However, the result holds even with the DiD regressions where any uncontrolled factors

driving the use of English language reports are cancelled out. Also, the coding

conventions we use tend to counteract any English-language-induced upward bias, and

we control for most factors identified by Jeanjean et al (2010) as being associated with

the publication of English language reports in non-English speaking countries..

Our central result has implications for Ball‟s (2006) conjecture that adoption of IFRS

may not succeed in producing high quality financial statements in practice because of

political and legal barriers to successful implementation at the country level. We find

that companies from China and the Philippines (both IFRS adopting countries) have the

largest changes in DISC from 2002 to 2007, even after controlling for these countries‟

code law legal systems, their relatively poor Rule of Law, their pre-existing domestic

GAAP and their level of secrecy.

Our results have implications for standard setters‟ attempts to achieve convergence of

financial reporting practices towards IFRSs across the region. While country-level

differences, be they differences in legal system, enforcement, or national culture are

important determinants of disclosure levels, IFRS adoption does seem to have led to an

increase in disclosure levels in our four Asian countries. That bodes well for the

success of IFRS adoption in other countries from the region.

22

References

Akerlof, G.A. 1970. “The Market for „Lemons‟: Quality Uncertainty and the Market

Mechanism” Quarterly Journal of Economics August, pp. 488-500.

Ali, M.J. 2005. “A Synthesis of Empirical Research on International Accounting

Harmonization and Compliance with International Financial Reporting

Standards” Journal of Accounting Literature 24, 2005, pp. 1-52

Armstrong, C., M. Barth, A. Jagolinzer & E. Reidl, 2010 “Market Reaction to the

Adoption of IFRS in Europe” The Accounting Review 85 (1) pp. 31-61

Ball, R. 2006. International Financial Reporting Standards (IFRS): Pros and Cons

for Investors” Accounting & Business Research 36 (4), pp. .

Ball, R., A.P. Kothari and A. Robin 2000. “The Effect of International Institutional

Factors on Properties of Accounting Earnings” Journal of Accounting &

Economics 29, pp. 1-51.

Ball, R., A. Robin and J.S. Wu 2003. “Incentives versus Standards: Properties of

Accounting Income in Four East Asian Countries” Journal of Accounting

and Economics 36, pp. 235-270.

Barth, M., W.R. Landsman and M. Lang 2008. “International Accounting Standards

and Accounting Quality” Journal of Accounting Research 46 (3) June pp.

467-498

Bar-Yosef S and J. Livnat, 1984 “Auditor Selection: An Incentive Signalling

Approach” Accounting & Business Research Autumn, pp. 301-309

Beck, T., A. Demirgüç-Kunt and R. Levine 2005. "A New Database on Financial

Development and Structure," Policy Research Working Paper No. 2146,

Washington DC: World Bank 1999, revised March 14, 2005.

Berle A. and G. Means 1932. The Modern Corporation and Private Property New

York: MacMillan

Bhat, G., O-K Hope and T. Kang 2006. “Does Corporate Governance Transparency

Affect the Accuracy of Analyst Forecasts?” Accounting & Finance 46 (5)

December, pp. 715-732.

Bhattacharya, U., H. Daouk and M. Welker 2003. “The World Price of Earnings

Opacity” The Accounting Review 78 (3) pp. 641-678.

Botosan, C. 1997. “Disclosure Level and the Cost of Equity Capital” The

Accounting Review 72 (3) July, pp323-349.

Braun, G. And R. Rodriquez 2008. “Earnings Management and Accounting Values:

A Test of Gray (1988)” Journal of International Accounting Research 7 (2)

pp. 1-24.

Bushman, R. and A.J. Smith 2001. “Financial Accounting Information and

Corporate Governance” Journal of Accounting and Economics 32, pp. 237-

333.

Bushman, R.M. and A.J. Smith (2003) “Transparency, Financial Accounting

Information and Corporate Governance” FRBNY Economic Policy Review

April, pp 65-87.

Bushman, R.M., J.D. Piotroski and A.J. Smith 2004. “What Determines Corporate

Transparency?” Journal of Accounting Research 42 (2) May pp. 207-251.

Byrne, I. 2003. “Surveying Transparency and Disclosure in Business” in H. Fletcher

“Corporate Transparency in the Fight against Corruption” Chapter 3 of

Global Corruption Report 2003, pp. 40-41. www.globalcorruptionreport.org/gcr2003.html.

Chau, G.K. and SJ Gray 2002. “Ownership structure and corporate voluntary

23

disclosure in Hong Kong and Singapore” The International Journal of

Accounting 37, pp. 247-265

Choi, F.D.S. and G.K. Meek 2005. International Accounting 5th

ed. Upper Saddle

River, New Jersey: Pearson Education.

Chow C. & A. Wong-Boren 1987 “Voluntary Disclosure by Mexican Companies”

Accounting Review July pp533-541.

Chow, C. W. and A. Wong-Boren 1987. “Voluntary Financial Disclosure by

Mexican Corporations”. The Accounting Review, 62(3), pp. 533 – 541.

CIFAR 1995. Center for International Financial Analysis and Research International

Accounting and Auditing Trends 4th

ed. Edited by V.B. Bavishi. Princeton,

New Jersey: CIFAR

Claessens, S., S. Djankov, and L.H.P. Lang, 2000. “The Separation of Ownership

and Control in East Asian Corporations” Journal of Financial Economics 58,

pp. 81-112.

Claessens, S., S. Djankov and T. Nenova 2000. “Corporate Risk Around the World”

World Bank Policy Research Working paper No. 2271.

http://ssrn.com/abstract=629121.

Clarkson, P., D. Hanna, G. Richardson & R. Thompson, 2011 “The impact of IFRS

adoption on the value relevance of book value and earnings” Journal of

Contemporary Accounting & Economics 7 pp. 1-17

CLSA 2001. “CG Watch: Corporate Governance in Emerging Markets – Saints and

Sinners Who‟s Got Religion?” www.clsa.com.

Cohen, J., P. Cohen, S.G. West and L.S. Aiken 2003. Applied Multiple Regression /

Correlation Analysis for the Behavioral Sciences 3rd

ed. Mahwah, New

Jersey: Lawrence Erlbaum Associates.

Cooke, TE 1989 “Voluntary Corporate Disclosure by Swedish Companies” Journal

of International Financial Management and Accounting Summer, pp. 171-

195

Daske, H., L. Hail, C. Leuz and R. Verdi 2008 “Mandatory IFRS Reporting around

the World: Early Evidence on the Economic Consequences” Journal of

Accounting Research 46 (5) December, pp1085-1142

DeAngelo L 1981. “Auditor Size and Audit Quality” Journal of Accounting &

Economics 3(2) pp. 183-9

Deloitte Touche Tohmatsu 2002. “International Accounting Standards Presentation

and Disclosure Checklist” http://www.iasplus.com/fs/iaschk01.pdf

Deloitte Touche Tohmatsu, 2002. “GAAP Differences in your Pocket: IAS and

GAAP in the Peoples‟ Republic of China”

Ding, Y., O-K Hope, T. Jeanjean and H. Stolowy 2007. “Differences between

domestic accounting standards and IAS: Measurement, determinants and

implications” Journal of Accounting and Public Policy 26, pp. 1-38.

Doidge, C., G.A. Karolyi and R.M. Stulz 2007. “Why do Countries Matter so Much

for Corporate Governance?” Journal of Financial Economics 86 (1) pp1-39

Doupnik, T. and G. Tsakumis 2004. “A Critical Review of Tests of Gray‟s Theory

of Cultural Relevance and Suggestions for Future Research” Journal of

Accounting Literature 23, pp. 1-48.

Durand, R.B. and A. Tarca, 2005. “The Impact of US GAAP Reconciliation

Requirements on Choice of Foreign Stock Exchange for Firms from

Common law and Code law Countries” European Accounting Review 14 (4)

pp. 789-813.

24

Durnev, A. and E.H. Kim 2005. “To Steal or Not to Steal: Firm Attributes, Legal

Environment, and Valuation” The Journal of Finance 60 (3) June, pp. 1461-

1493.

Field, A. 2005. Discovering Statistics Using SPSS 2nd

ed. London: Sage

Publications.

Fields, T., T. Lys and L. Vincent, 2001, “Empirical research on accounting choice”

Journal of Accounting and Economics 31: 255-307

Firth, M. 1980 “Raising Finance and Firms‟ Corporate Reporting Policies”, Abacus

16 (2) December, pp100-115.

Foster, G. 1986. Financial Statement Analysis 2nd

ed. Prentice-Hall.

Francis, J., I. Khurana, X. Martin & R. Pereira 2008: The Role of Firm-Specific

Incentives and Country Factors in Explaining Voluntary IAS Adoptions:

Evidence from Private Firms, European Accounting Review, 17:2, 331-360

Francis, J.R., I.K. Khurana, X. and R. Pereira 2005. “Disclosure Incentives and

Effects on Cost of Capital Around the World” The Accounting Review 80 (4)

October, forthcoming.

Frost, C.A., E.A. Gordon and G. Pownall 2005. “Financial Reporting Quality,

Disclosure, and Emerging Market Companies‟ Access to Capital in Global

Equity Markets”. 12 September. http://ssrn.com/abstract=802824.

Gray SJ, G.K. Meek, and C.B. Roberts 1995 “International Capital Market Pressures

and Voluntary Annual Report Disclosures by US and UK Multinationals”

Journal of International Financial Management and Accounting (USA) 6

(1) Spring, pp. 43-68.

Gray, S.J. 1988. “Towards a Theory of Cultural Influence on the Development of

Accounting Systems Internationally” Abacus 24 (1) March, 1-15.

Haniffa, R.M and T.E. Cooke 2002. “Culture, Corporate Governance and Disclosure

in Malaysian Corporations” Abacus, 38 (3), pp. 317-349

Hatfield, H.R. 1911. “Some Variations in Accounting Practice in England, France,

Germany and the United States” reprinted in Journal of Accounting Research 4 (2)

(Autumn, 1966): 169-182.

Healy, P.M. and K.G. Palepu, 2001. “Information asymmetry, corporate disclosure

and the capital markets: a review of the empirical disclosure on literature”,

Journal of Accounting and Economics 31:405-440

Ho, S. S., and Wong, K. S. 2001. “A Study of Corporate Disclosure Practice and

Effectiveness in Hong Kong”. Journal of International Financial

Management and Accounting, 12(1), pp. 75 – 102.

Ho, S.S. M. and K.S. Wong, 2002, “A study of the relationship between corporate

governance structures and the extent of voluntary disclosure”, Journal of

International Accounting, Auditing and Taxation 10: 139-156

Hofstede, G. 1980. Cultures Consequences: International Differences in Work

Related Values. Beverly Hills: Sage Publications.

Hofstede, G. and Hofstede G.J. 2005. Cultures and Organizations: Software of the

Mind 2nd

ed. New York: McGraw-Hill.

Holthausen, R.W. 2003. “Testing the Relative Power of Accounting Standards

Versus Incentives and Other Institutional Features to Influence the Outcome

of Financial Reporting in an International Setting” Journal of Accounting

and Economics 36, pp.271-283.

Hope, O-K. 2003. “Disclosure Practices, Enforcement of Accounting Standards,

and Analysts‟ Forecast Accuracy: An International Study” Journal of

25

Accounting Research 41 (2) May, pp. 235-272.

Horton, J and G. Serafim, 2010 “Market reaction to and valuation of IFRS

reconciliation adjustments: first evidence from the UK” Review of

Accounting Studies 15 pp. 725-751.

Hossain, M., L. M. Tan, and M. Adams. 1994. Voluntary Disclosure in an Emerging

Capital Market: Some Empirical Evidence from Companies Listed on the

Kuala Lumpur Stock Exchange. The International Journal of Accounting.

29: 334-351.

Hossain, M., Perera, M. H. B., and Rahman, A. R., 1995, “Voluntary Disclosure in

the Annual Reports of New Zealand Companies”, Journal of International

Financial Management and Accounting, 6(1), pp. 69–85.

Hung, M. 2001. “Accounting Standards and Value Relevance of Financial

Statements: An International Analysis” Journal of Accounting and

Economics 30, pp401-420.

IASPlus Accounting Standards Updates by Jurisdiction at

http://www.iasplus.com/country/country.htm (accessed 10 January 2012)

Jaggi, B. and P.Y. Low 2000. “Impact of Culture, Market Forces, and Legal System

on Financial Disclosures” International Journal of Accounting 35 (4) pp.

495-519.

Jeanjean, T., C. Lesage and H. Stolowy 2010. “Why do you speak English (in your

annual report)? International Journal of Accounting 45 pp200-223.

Jensen, M. and W. Meckling 1976. “Theory of the Firm: Managerial Behaviour,

Agency Costs and Ownership Structure” Journal of Financial Economics

October, pp305-360.

Johnson, S, R. La Porta, R. Lopez-de-Silanes & A. Shleifer, 2000. “Tunneling”

American Economic Review 90 (2), May, pp22-27.

Kaufman, Kraay and Mastruzzi 2003. Governance Matters III: Governance

Indicators for 1996-2002 World Bank Policy Research Working Paper 3106.

Kemp, S. and J. Knapp (eds) 2005. CA Financial Reporting Handbook 2005.

Milton, Qld John Wiley & Sons

Kimbro, M.B. 2002. “A Cross-Country Empirical Investigation of Corruption and

its Relationship to Economic, Cultural, and Monitoring Institutions: An

Examination of the Role of Accounting and Financial Statements Quality”

Journal of Accounting, Auditing & Finance pp. 325-349.

Kogut, B. and H. Singh 1988. “The Effect of National Culture on Choice of Entry

Mode” Journal of International Business Studies 19 (3) Autumn, 411-432

Kurtzman, J. G. Yago and T. Phumiwasana 2004. The Opacity Index: The Global

Costs of Opacity MIT Sloan Management Review 2004.

La Porta, R., F. Lopez-de-Silanes, A. Shleifer and R.W. Vishny 1998. “Law and

Finance” The Journal of Political Economy 106 (6) December, pp. 1113-

1155.

La Porta, R., F. Lopez-de-Silanes, and A. Shleifer 1999. “Corporate Ownership

Around the World” The Journal of Finance 54 (2) April pp. 471-517.

Landsman, W., E. Maydew and J. Thornock, “The information content of annual

earnings announcements and mandatory adoption of IFRS” Journal of

Accounting & Economics forthcoming

Leuz, C., D. Nanda and P. Wysocki 2003. “Earnings management and Institutional

Factors: An International Comparison” Journal of Financial Economics 69,

pp. 505-527

Levine, R. and S.J. Zervos 1993. “What We have learned About Policy and Growth

26

from Cross-Country Regressions?” The American Economic Review 83 (2)

May pp. 426-430.

Levitt, A. 1998. “The „Numbers Game‟” presentation at the New York University

Center for Law and Business, New York, September 28, 1998, as cited by

M.Z. Rahman “The Role of Accounting Disclosure in the East Asian

Financial Crisis: Lessons Learned?” Transnational Corporations, 7 (3), pp.

1-52. (1998).

Meek, G. K., Roberts, C. B., and Gray S. J., 1995, “Factors Influencing Voluntary

Annual Report Disclosures by U.S., U.K. and Continental European

Multinational Corporations”, Journal of International Business Studies,

26(3), pp. 555–572.

Miller, G.S. 2002. “Earnings Performance and Discretionary Disclosure” Journal of

Accounting Research 40 (1) March, pp. 173-203.

Morris, R.D. 1987 “Signalling, Agency Theory and Accounting Policy Choice”

Accounting and Business Research Winter pp.47-56.

Morris, R.D. B.U.S. Ho, T. Pham and S.J. Gray 2004. “Financial Reporting

Practices of Indonesian Companies Before and After the Asian Financial

Crisis” Asia-Pacific Journal of Accounting & Economics 11 (2) December

pp. 1-27.

Nobes, C. 2001 GAAP 2001 Survey www.iasplus.com

Nobes, C. and R. Parker 2000. Comparative International Accounting 6th

ed.

Harlow: Financial Times Prentice-Hall.

Patel, S.A., A. Balic, and L. Bwakira 2002. “Measuring Transparency and

Disclosure at Firm-Level in Emerging markets” Emerging Markets Review 2,

pp. 325-337.

Pope, P. and M. Walker 1999. “International Differences in the Timeliness,

Conservatism, and Classification of Earnings” Journal of Accounting

Research 37 (Supplement), pp. 53-87.

Radebaugh, L.H. and S.J. Gray 2002. International Accounting & Multinational

Enterprises 5th

ed. New York: John Wiley.

Schweikart, J.A., S.J. Gray and S.B. Salter 1996 „An Interview with Sir Bryan

Carsberg, Secretary-General of the International Accounting Standards

Committee‟, Accounting Horizons, 10 (1) March pp.110-117..

Spence, M 1973 “Job Market Signalling” Quarterly Journal of Economics 87

pp355-374

Standard & Poor‟s 2001. “Standard & Poor‟s Transparency and Disclosure Study

for International Investors” www.standardandpoors.com

Street DL and SJ Gray 2001. Observance of International Accounting Standards:

Factors Explaining Non-Compliance ACCA Research Report No. 74

Street, D. 2002. “GAAP Convergence 2002: A Survey of National Efforts to

promote and Achieve Convergence with International Financial Reporting

Standards” http://www.ifac.org.

Sutthachai, S. and T. Cooke 2009 “An Analysis of Thai Financial Reporting

Practices and the Impact of the 1997 Economic Crisis” Abacus 45 (4) pp.

493-517.

Taylor, S. 1987. “International Accounting Standards: An Alternative Rationale”

Abacus 23 (2) pp. 157-171.

Verrechia, R. 1983. “Discretionary Disclosure” Journal of Accounting and

Economics 5 (3) pp. 179-194.

Verrechia, R. 1990. “Information Quality and Discretionary Disclosure” Journal of

27

Accounting and Economics 12 March pp. 365-380.

Wallace, R. S. Olusegan and K. Naser. 1995. “Firm-specific determinants of the

comprehensiveness of mandatory disclosure in the corporate annual reports

of firms listed on the stock exchange of Hong Kong”, Journal of Accounting

and Public Policy, 14(4): 311-368.

Wan-Hussin, W.N. 2009. “The impact of family-firm structure and board

composition on corporate transparency: Evidence based on segment-

disclsoures in Malaysia” International Journal of Accounting 44 (4) pp. 313-

333.

Watts, R. and J. Zimmerman 1986. Positive Accounting Theory Prentice-Hall.

Willard Report, 1998. “Report of the Working Group on Transparency and

Accountability”, G22 Working Group, October.

28

EXHIBIT 1

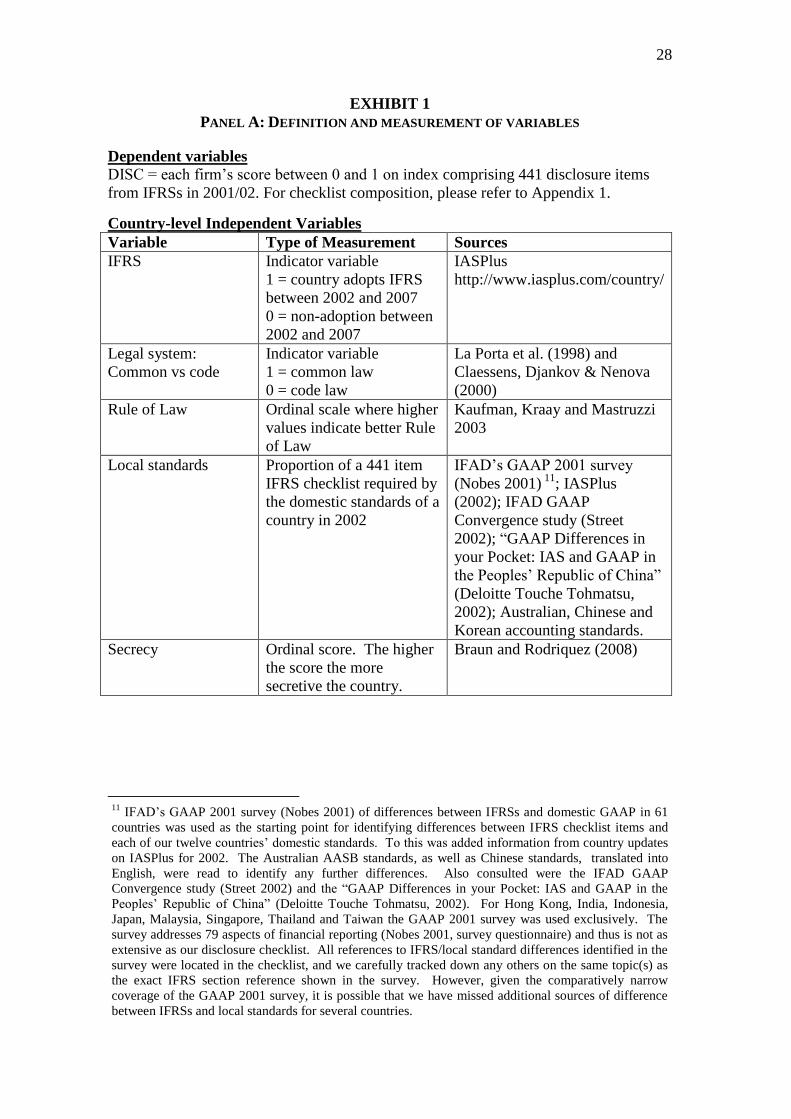

PANEL A: DEFINITION AND MEASUREMENT OF VARIABLES

Dependent variables

DISC = each firm‟s score between 0 and 1 on index comprising 441 disclosure items

from IFRSs in 2001/02. For checklist composition, please refer to Appendix 1.

Country-level Independent Variables

Variable Type of Measurement Sources

IFRS Indicator variable

1 = country adopts IFRS

between 2002 and 2007

0 = non-adoption between

2002 and 2007

IASPlus

http://www.iasplus.com/country/

Legal system:

Common vs code

Indicator variable

1 = common law

0 = code law

La Porta et al. (1998) and

Claessens, Djankov & Nenova

(2000)

Rule of Law Ordinal scale where higher

values indicate better Rule

of Law

Kaufman, Kraay and Mastruzzi

2003

Local standards Proportion of a 441 item

IFRS checklist required by

the domestic standards of a

country in 2002

IFAD‟s GAAP 2001 survey

(Nobes 2001) 11

; IASPlus

(2002); IFAD GAAP

Convergence study (Street

2002); “GAAP Differences in

your Pocket: IAS and GAAP in

the Peoples‟ Republic of China”

(Deloitte Touche Tohmatsu,

2002); Australian, Chinese and

Korean accounting standards.

Secrecy Ordinal score. The higher

the score the more

secretive the country.

Braun and Rodriquez (2008)

11

IFAD‟s GAAP 2001 survey (Nobes 2001) of differences between IFRSs and domestic GAAP in 61

countries was used as the starting point for identifying differences between IFRS checklist items and

each of our twelve countries‟ domestic standards. To this was added information from country updates

on IASPlus for 2002. The Australian AASB standards, as well as Chinese standards, translated into

English, were read to identify any further differences. Also consulted were the IFAD GAAP

Convergence study (Street 2002) and the “GAAP Differences in your Pocket: IAS and GAAP in the

Peoples‟ Republic of China” (Deloitte Touche Tohmatsu, 2002). For Hong Kong, India, Indonesia,

Japan, Malaysia, Singapore, Thailand and Taiwan the GAAP 2001 survey was used exclusively. The

survey addresses 79 aspects of financial reporting (Nobes 2001, survey questionnaire) and thus is not as

extensive as our disclosure checklist. All references to IFRS/local standard differences identified in the

survey were located in the checklist, and we carefully tracked down any others on the same topic(s) as

the exact IFRS section reference shown in the survey. However, given the comparatively narrow

coverage of the GAAP 2001 survey, it is possible that we have missed additional sources of difference

between IFRSs and local standards for several countries.

29

Firm Level Independent Variables

Variables Explanation

SIZE Natural log of firm total assets in US $m

LEV Total liabilities/Total assets

ROR NPAT/Total assets

BSEG Number of business segments

ISALDum Dummy variable

1=firm generated revenue in countries other than country of

incorporation

0=firm did not generate revenue in countries other than

country of incorporation

KRDDum Dummy variable

1= firm raised debt capital in the financial year

0= firm did not raise debt capital in the financial year

KREDum Dummy variable

1= firm raised equity capital in the financial year

0= firm did not raise equity capital in the financial year

AUDITOR Dummy variable

1=firm‟s financial statements were audited by Big 5 auditor

0=firm‟s financial statements were not audited by Big 5

auditor

IDIR Dummy variable

1 = firm has independent directors on board

0 = firm does not have independent directors on board

AC Dummy variable

1= firm has an audit committee

0= firm does not have an audit committee

DUALD Dummy variable

1 = Chairman and CEO are different persons

0 = Chairman and CEO are the same person

SSH Accumulated % of shareholding <5%.

Where the information is absent, the company is assumed to

be widely held, i.e. SSH =1; if the information for block

ownership is present, SSH is estimated to be 1 – highest

blockownership OR 1 – (sum of % of block ownership >5%)

TOPSH % holding of largest shareholder

FCTL3 Dummy variable for block ownership

2 = 30% or more of shares are held by individuals, private

firms or government body;

1 = 30% or more of shares are held by a public company;

0 = otherwise

PANEL B: SOURCES OF COMPANIES’ ANNUAL REPORTS

Country Sample size Data sources

Australia 41 Connect4, Aspect, and Mergent Online Databases

China 12 Mergent Online, Chinese Securities and Regulation

Commission‟s website

30

Hong Kong 39 Mergent Online

India 24 Mergent Online

Japan 46 Companies‟ websites, Mergent Online

Malaysia 40 Companies‟ websites, Mergent Online

Philippines 22 Mergent Online

Singapore 41 Companies‟ websites, Mergent Online

PANEL C: SUMMARY OF REGRESSION MODELS

Model Regression Equation

POOLED OLS REGRESSION

Model 1 DISC = α + β1SIZE + β2LEV + β3ROR + β4BSEG + β5ISALDum +

β6KRDDum + β7KREDum + β8AUDITOR + β9AC + β 10DUALD +

β11SSH + β12TOPSH + β13FCTL3 + β14YEAR + β15IFRS + ε

Model 2 DISC = α + β1SIZE + β2LEV + β3ROR + β4BSEG + β5ISALDum +

β6KRDDum + β7KREDum + β8AUDITOR + β9AC + β 10DUALD +

β11SSH + β12TOPSH + β13FCTL3 + β14YEAR + β15IFRS +

β16LEGALSYSTEM + ε

Model 3 DISC = α + β1SIZE + β2LEV + β3ROR + β4BSEG + β5ISALDum +

β6KRDDum + β7KREDum + β8AUDITOR + β9AC + β 10DUALD +

β11SSH + β12TOPSH + β13FCTL3 + β14YEAR + β15IFRS +

β16LEGALSYSTEM + β17RULEOFLAW + ε

Model 4 α + β1SIZE + β2LEV + β3ROR + β4BSEG + β5ISALDum + β6KRDDum

+ β7KREDum + β8AUDITOR + β9AC + β 10DUALD + β11SSH +

β12TOPSH + β13FCTL3 + β14YEAR + β15IFRS + β16LEGALSYSTEM +

β17RULEOFLAW + β18LOCALSTANDARDS + ε

Model 5 DISC = α + β1SIZE + β2LEV + β3ROR + β4BSEG + β5ISALDum +

β6KRDDum + β7KREDum + β8AUDITOR + β9AC + β 10DUALD +

β11SSH + β12TOPSH + β13FCTL3 + β14YEAR + β15IFRS +

β16LEGALSYSTEM + β17RULEOFLAW + β18LOCALSTANDARDS +

β19SECRECY + ε

DIFFERENCE-IN-DIFFERENCE REGRESSIONS

Model 6 ∆DISC = α + β1∆SIZE + β2∆ROR + β3∆ISALDum + β4∆KRDDum +

β5∆AUDITOR + β6 ∆IDIR + β7 ∆AC + β8∆TOPSH + β9KREDum2002

+ β10AC2002 +β11SSH2002 + β12TOPSH2002 + β13DISC2002 +

β114LEGALSYSTEM + β15LOCALSTANDARDS + β16SECRECY +

β17IFRS + ε

Model 7 ∆DISC = α + β1 ∆IDIR + β2KREDum2002 + β3 AC2002 + β4SSH2002 +

β5TOPSH2002 + β6DISC2002 + β7LEGALSYSTEM +

β8LOCALSTANDARDS + β9SECRECY + β10IFRS + ε

31

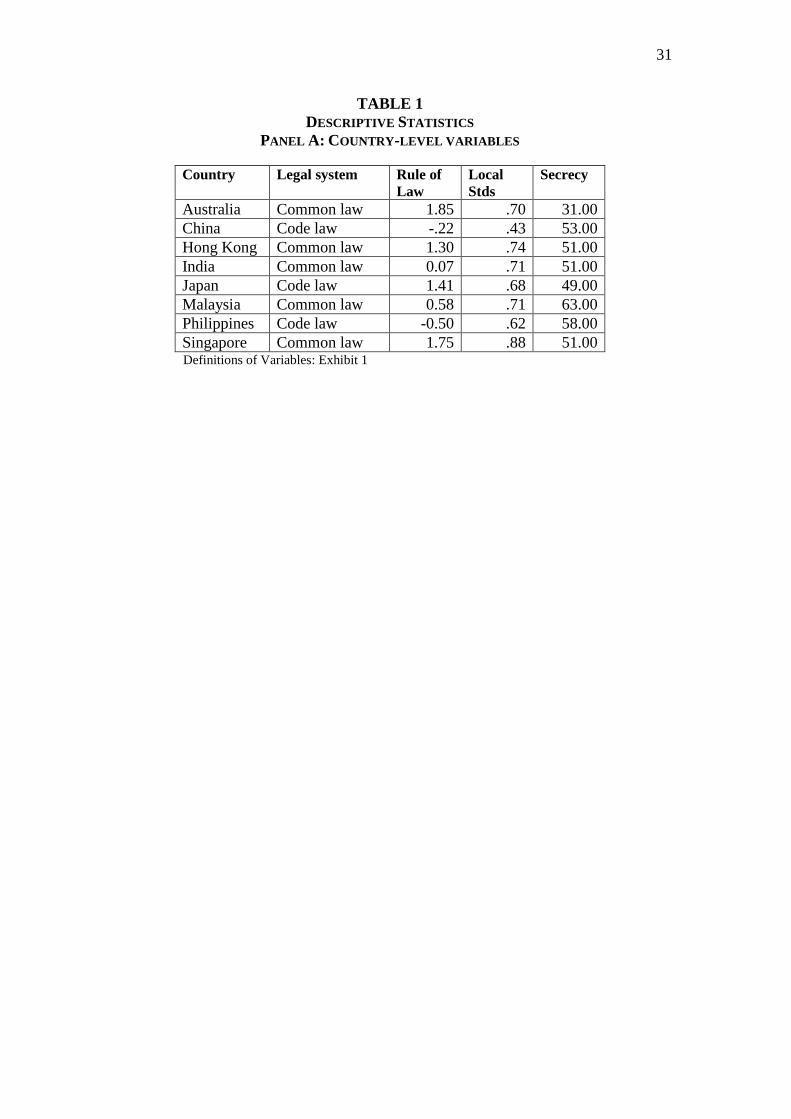

TABLE 1

DESCRIPTIVE STATISTICS

PANEL A: COUNTRY-LEVEL VARIABLES

Country Legal system Rule of

Law

Local

Stds

Secrecy

Australia Common law 1.85 .70 31.00

China Code law -.22 .43 53.00

Hong Kong Common law 1.30 .74 51.00

India Common law 0.07 .71 51.00

Japan Code law 1.41 .68 49.00

Malaysia Common law 0.58 .71 63.00

Philippines Code law -0.50 .62 58.00

Singapore Common law 1.75 .88 51.00 Definitions of Variables: Exhibit 1

32

PANEL B: DESCRIPTIVE STATISTICS OF VARIABLES FOR COUNTRIES ADOPTING IFRS

AND NOT ADOPTING IFRS

IFRS = 0 IFRS = 1

Variable Mean Std. Dev Mean Std. Dev t stat Prob.

COUNTRY-LEVEL VARIABLES

LEGAL SYSTEM .5198 .50023 .7018 .45849 75.289 .000

LOCAL

STANDARDS

.7470 .08230 .6698 .09265 .327 .567

RULE OF LAW 1.0695 .62015 .9904 .94091 74.366 .000

SECRECY 53.5695 5.73329 45.3684 11.07067 335.822 .000

FIRM-LEVEL VARIABLES

SIZE 2002 8.333 1.564 8.289 1.263 12.062 .001

LEV 2002 .545 .343 .531 .571 .458 .499

ROR 2002 .054 .084 .067 .095 .007 .934

BSEG 2002 3.523 1.989 3.667 1.990 .033 .855

ISALDum 2002 .702 .459 .675 .470 .833 .362

KRDDum 2002 .781 .415 .816 .389 1.915 .168

KREDum 2002 .450 .499 .675 .470 15.897 .000

AUDITOR 2002 .728 .824 .825 .382 7.661 .006

IDIR 2002 3.318 3.016 2.798 2.388 9.357 .002

AC 2002 .715 .453 .868 .340 42.774 .000

DUALD 2002 .718 .450 .702 .460 .408 .524

SSH 2002 .541 .309 .429 .261 13.164 .000

TOPSH 2002 .306 .234 .364 .227 .347 .556

FCTL3 2002 .927 .888 .982 .841 4.231 .041

DEPENDENT VARIABLE

DISC 2002 .353 .074 .353 .074 .692 .406

Definitions of Variables: Exhibit 1

33

PANEL C: INDEPENDENT VARIABLES DESCRIPTIVE STATISTICS FOR 2002 AND 2007

Year 2002 Year 2007

Variable Mean Std. Dev Mean Std. Dev t stat Prob.

SIZE 8.315 1.440 8.740 1.522 8.366 .000

LEV .539 .454 .499 .304 -1.318 .189

ROR .059 .089 .120 .242 3.911 .000

BSEG 3.585 1.987 3.619 2.036 .292 .771

ISALDum .691 .463 .785 .412 3.578 .000

KRDDum .796 .404 .732 .444 -2.029 .043

KREDum .547 .499 .517 .501 -.799 .425

AUDITOR .770 .671 .838 .369 1.772 .078

IDIR 3.094 2.771 4.449 2.875 8.076 .000

AC .781 .414 .947 .225 6.295 .000

DUALD .711 .453 .717 .451 .187 .852

SSH .493 .294 .458 .623 -.949 .343

TOPSH .331 .232 .376 .406 2.071 .039

FCTL3 .951 .867 1.042 .827 1.486 .138 Definitions of Variables: Exhibit 1

34

TABLE 2

DESCRIPTIVE STATISTICS

DEPENDENT VARIABLE

DISC

2002

DISC

2007 Difference

T (two-tailed

sig)

Full Sample Mean .365 .468 .103 .000

N = 265 Std Dev .075 .111

Australia Mean .388 .503 .115 .000

N = 41 Std Dev .028 .060

China Mean .315 .461 .146 .005

N = 12 Std Dev .037 .150

Hong Kong Mean .430 .499 .069 .001

N = 39 Std Dev .085 .104

India Mean .290 .383 .094 .000

N = 24 Std Dev .047 .112

Japan Mean .322 .414 .092 .000

N = 46 Std Dev .030 .125

Malaysia Mean .363 .469 .106 .000

N = 40 Std Dev .065 .097

Philippines Mean .316 .508 .192 .000

N = 22 Std Dev .054

Singapore Mean .416 .493 .077 .000

N = 41 Std Dev .082 .087

One way

ANOVA

comparing

countries

F 5.933 24.306

Prob. .000 .000

. Definitions of Variables: Exhibit 1

35

TABLE 3

PEARSON CORRELATIONS OF DISC WITH COUNTRY-LEVEL INDEPENDENT VARIABLES

DISC

LEGAL

SYSTEM SECRECY

RULE OF

LAW

LOCAL

STANDARD

DISC 1

LEGAL

SYSTEM

.197**

1

SECRECY -.080 -.138**

1

RULE OF

LAW

.192**

.348**

-.630**

1

LOCAL

STANDARD